Australian Competition and Consumer Commission v Ashley & Martin Pty Ltd [2019] FCA 1436

ORDERS

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION Applicant | ||

AND: | ASHLEY & MARTIN PTY LTD (ACN 090 141 021) Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Within 14 days the parties are to file a minute of proposed orders to program a further hearing to address relief.

2. The parties be heard as to costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[7] | |

[10] | |

[11] | |

[15] | |

[20] | |

[22] | |

[32] | |

[33] | |

[43] | |

[43] | |

[45] | |

Section 24 - Reasonably necessary to protect legitimate interest | [48] |

[60] | |

[65] | |

[69] | |

Ashley & Martin's overarching 'no obligation' and 'supply term' submissions | [87] |

[93] | |

[94] | |

[97] | |

[98] | |

[104] | |

[107] | |

[110] | |

[118] | |

Are the terms of the First Contract unfair (s 24 definition) | [128] |

[129] | |

[137] | |

[138] | |

[161] | |

[173] | |

[183] | |

[195] | |

[197] | |

[203] | |

[214] | |

[216] | |

REASONS FOR JUDGMENT

BANKS-SMITH J:

1 Ashley & Martin carries on the business of supplying to its customers a hair regrowth medical treatment program called 'Personal RealGROWTH Program' (Medical Treatment Program). Customers (referred to as patients) sign a contract that governs the terms upon which the Medical Treatment Program is provided.

2 The Medical Treatment Program offered by Ashley & Martin includes prescribed pharmaceuticals and is by name and nature a medical treatment.

3 The proceedings relate to three iterations of a standard form contract used during the period June 2014 to June 2017. The particular contracts in question are no longer in use.

4 The Australian Competition and Consumer Commission (ACCC) seeks declarations that certain clauses within the contracts are void on the basis that they are unfair terms within the meaning of s 23 and s 24 of the Australian Consumer Law (ACL) and seeks orders as to consumer redress under s 239.

5 The overarching theme of the ACCC's contention is that the terms operate together in a manner that commits patients to undertake and pay for a Medical Treatment Program that includes prescription-only medicines before patients have had an opportunity to obtain and consider medical advice as to risk and suitability, and in circumstances where patients remain liable to make payments regardless of the nature of the advice. It is only after an appointment with a doctor that a patient is able to give informed consent. By that time, the patient has already committed to a contract from which they cannot withdraw without cost.

6 Ashley & Martin contends that any attack on the contracts is circumscribed by s 26 of the ACL, which quarantines core terms of a contract from an assessment of whether they are unfair. In any event, Ashley & Martin contends that the impugned terms are not unfair and are reasonably necessary to protect its interests.

7 The parties filed concise statements/responses and there was no oral evidence. A tender bundle was largely agreed. The parties filed a statement of agreed facts (and a supplementary statement) as provided for by s 191 of the Evidence Act 1995 (Cth).

8 Importantly, the number of contracts entered into in the relevant period exceeded some 25,000. During the interlocutory stage the parties agreed that Ashley & Martin would produce to the ACCC a representative sample of 240 contracts across 12 categories. The parties then agreed the contents of a data schedule that collated pertinent information from the sample contracts. The data schedule formed part of the statement of agreed facts.

9 After the hearing Ashley & Martin provided an 'aide memoire' that compiled information as to the sums that might be paid by patients upon termination of the contracts in various scenarios based on the retail ('standard') cost of products to be supplied under the contracts. The information was checked and agreed by the parties. I have accepted the aide memoire as a submission.

10 The following is based primarily on the statement of agreed facts.

11 When a patient first approaches Ashley & Martin for treatment, the patient will speak to a receptionist by telephone and/or email a request for a consultation. That contact results in an appointment for the patient to see a 'hair loss consultant' for 60 minutes. Ashley & Martin then sends the patient an email to confirm the appointment. This appointment is known as the 'initial consultation'. The confirmatory email informs patients of the option to enrol on the day of the initial consultation and advises them to come to the initial consultation 'financially prepared'. It also appears from the annexures to the statement of agreed facts that an initial email is sent when an appointment is requested that states in two places that the first consultation is free.

12 Hair loss consultants are not medical doctors or otherwise healthcare professionals. They are trained by Ashley & Martin's medical director on how Ashley & Martin wishes them to conduct the initial consultation.

13 At the initial consultation the patient fills out a questionnaire and a checklist. The questionnaire includes questions about the reason for seeking treatment and the patient's medical history. The checklist requires a yes/no answer to a number of questions, including 'Do you understand what is involved with your program?', 'Have you been informed about our Maintenance program and the associated costs?' and 'Have you read, signed and received the Terms & Conditions?'. If the patient wishes to proceed with a Medical Treatment Program, the Ashley & Martin consultant completes the first page of the contract in front of the patient and the patient and the consultant sign the contract.

14 Most patients who signed a contract did so at the initial consultation. These patients were usually provided with non-prescription goods - such as shampoos, conditioners, herbal supplements and multivitamins - at the initial consultation. They were provided with the quantity of the non-prescription goods that Ashley & Martin estimated they would require for the whole term of their Medical Treatment Program.

The consultation with an Ashley & Martin doctor

15 Generally at the initial consultation an appointment is made for the patient to see a medical doctor engaged by the respondent as an independent contractor. These doctors are referred to generally in communications as Ashley & Martin doctors. At the medical appointment an Ashley & Martin doctor meets with the patient for the first time. Ashley & Martin provides a protocol letter to the Ashley & Martin doctor that sets out its requirements and procedures for the contracted doctors. The information that the doctor must discuss under the protocol letter includes the risks to the patients of undertaking the Medical Treatment Program. Sample protocol letters were included in the tender bundle.

16 Some of the risks identified in the information include:

(1) For female users, Ashley & Martin's sample protocol letters provide that the RealGROWTH lotion has possible side effects including scalp irritation, redness, itchiness, flakiness and facial hair growth, and a component (retinoic acid) may cause birth defects. Pregnancy and breastfeeding are to be avoided whilst using the lotion. The antiandrogen tablets prescribed for women of reproductive age had possible side effects including breast enlargement, weight gain, fluid retention, high blood pressure and headaches with a rare side effect of blood clots in leg veins, whilst that prescribed to postmenopausal or sterilised women had possible side effects including breast enlargement, period irregularities, headaches and lethargy.

(2) For male users, the protocol letters provide that the RealGROWTH lotion has the uncommon (<1%) side effect of irritation, redness or scaling of the scalp, along with rare side effects including allergic reactions, palpitations, dizziness and swelling of the hands and feet. The Finasteride tablets have possible uncommon (<1%) side effects of decreased sex dive, impotence, decreased semen volume, ejaculation disorder and orgasm disorder, and have rare possible side effects including breast enlargement and tenderness, rashes, allergic reactions, testicular pain, depression and lethargy. They rarely may have an effect on fertility and decrease prostate specific antigen levels.

(3) As to the non-pharmaceutical goods, the protocol letters provide that the LaserCap can have rare adverse reactions including headaches, dizziness or vertigo, and that patients may experience a drop in blood pressure when using it, and that the Saw Palmetto capsules can have a rare side effect of stomach upsets.

17 At the first appointment, male patients under 55 years old are usually prescribed Finasteride and Minoxidil. Finasteride is usually supplied by the doctor to the patient at the appointment. According to the 'doctor information pack 2015' tendered in the proceedings, it appears that Finasteride is supplied direct to Ashley & Martin for distribution to patients, but is only handled by an in-house doctor. Minodoxil is usually supplied shortly after the appointment with the doctor, as it is compounded by a third party pharmacy and so subject to compounding and postage times.

18 Male patients over 55 years old are generally prescribed Minoxidil and see their own general practitioner for a prescription for Finasteride.

19 Female patients are usually prescribed anti-androgen tablets known as Brenda 35 or Spironolacone and Minoxidil at their first appointment, and those products are supplied to them by Ashley & Martin after blood test results are returned (usually about two weeks after the initial consultation with an Ashley & Martin doctor).

The products used in the Medical Treatment Program

20 The range of goods and services provided by Ashley & Martin varies from patient to patient, but typically includes a combination of shampoos, conditioners, herbal supplements, prescription medicines and, in some cases, a laser cap device called LaserCap.

21 The goods are as follows:

(1) Finasteride - a prescription only medication registered on the Australian Register of Therapeutic Goods (ARTG), used for male pattern baldness and presented in tablet form as 'Fintab'. The Therapeutic Goods Administration (TGA) has approved both product information and consumer medical information for use in relation to Finasteride. Ashley & Martin refers to Finasteride in the contracts as 'RealGROWTH tablets';

(2) Minoxidil - a prescription only medication in liquid form for topical application used to treat baldness. Minoxidil is also registered on the ARTG and the TGA has approved product information and consumer medical information in relation to it. Ashley & Martin refers to Minoxidil in the contracts as 'RealGROWTH topical solution';

(3) anti-androgen tablets (Brenda 35) - prescription only for female patients;

(4) anti-androgen tablets (Spironolactone) - prescription only for female patients;

(5) Saw Palmetto - a herbal supplement made from plant extract, used to treat male pattern baldness. The ARTG has provided a public summary for Saw Palmetto;

(6) Presol (its nature was not explained);

(7) shampoo;

(8) conditioner;

(9) LaserCap - low level light therapy via laser diodes contained in a laser cap; and

(10) Hair Nutrient Complex - a multivitamin used by Ashley & Martin to treat female hair loss.

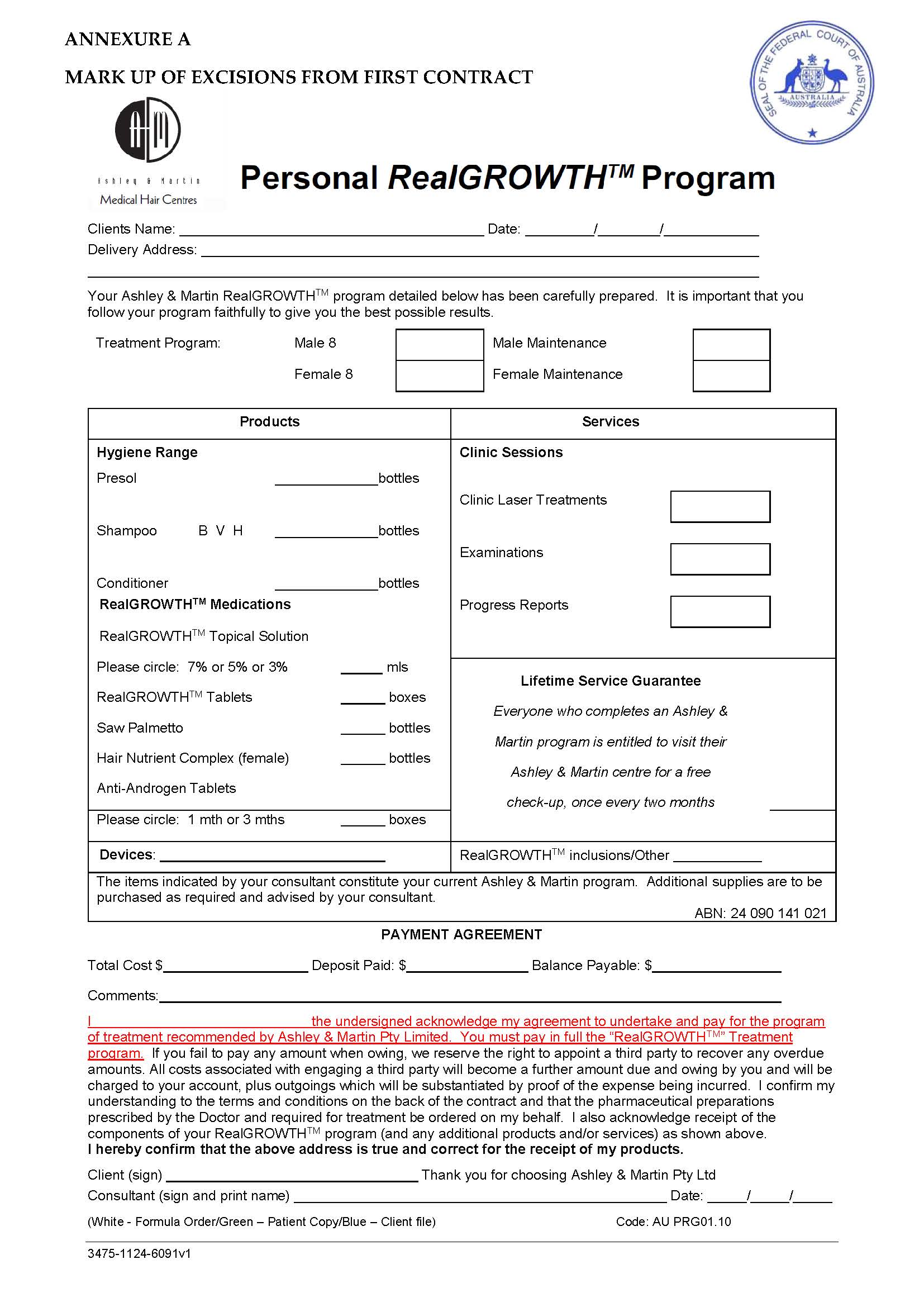

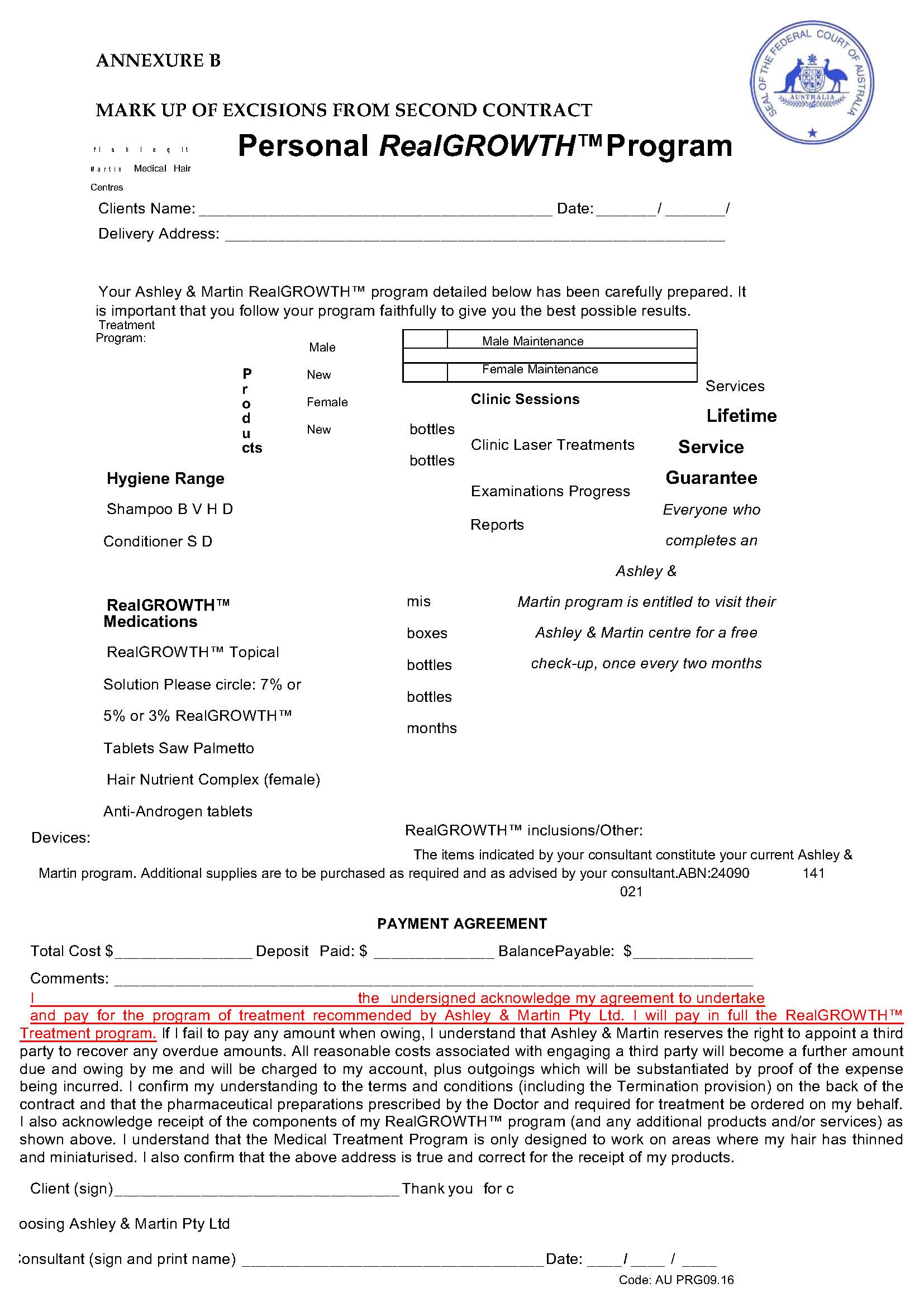

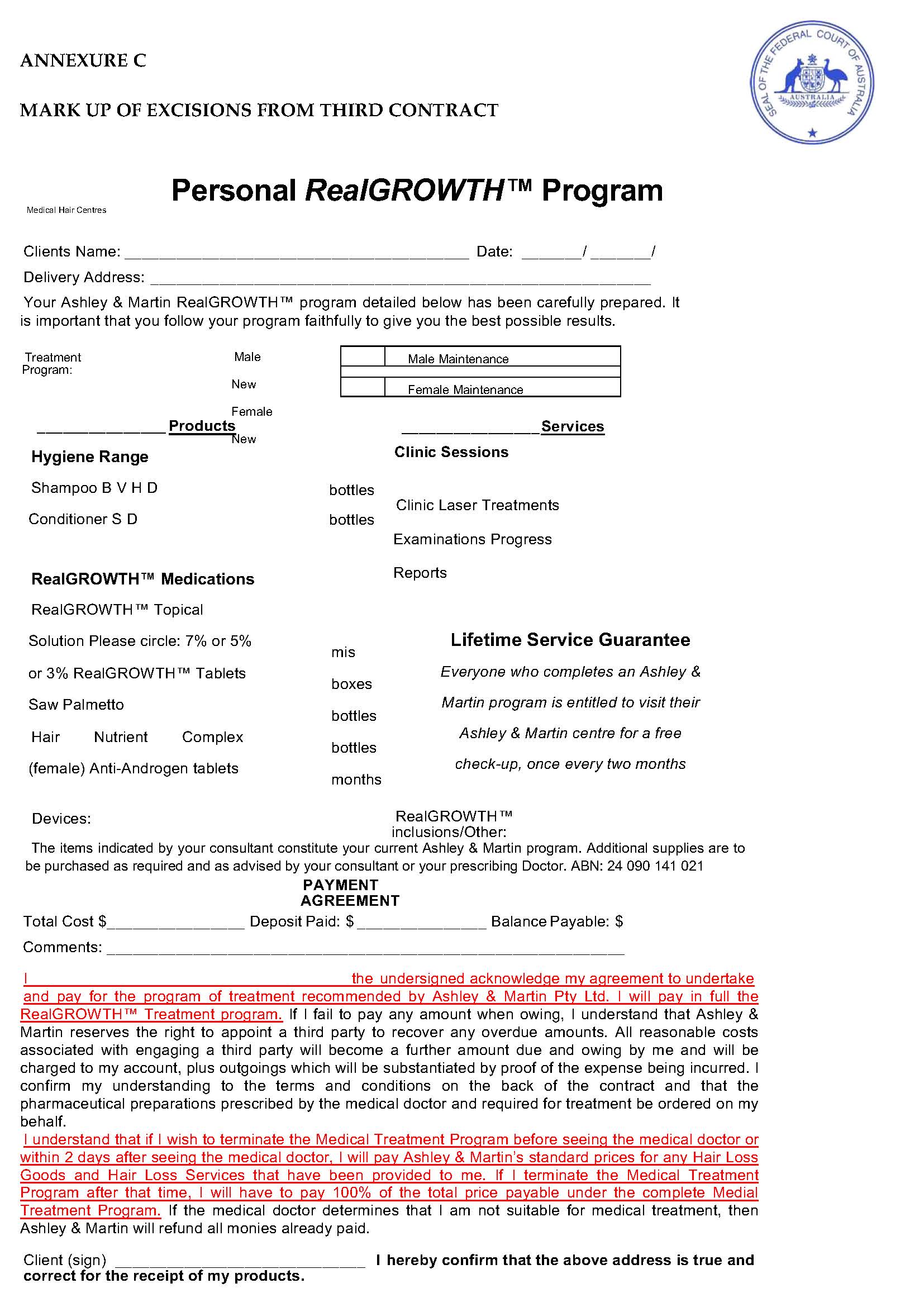

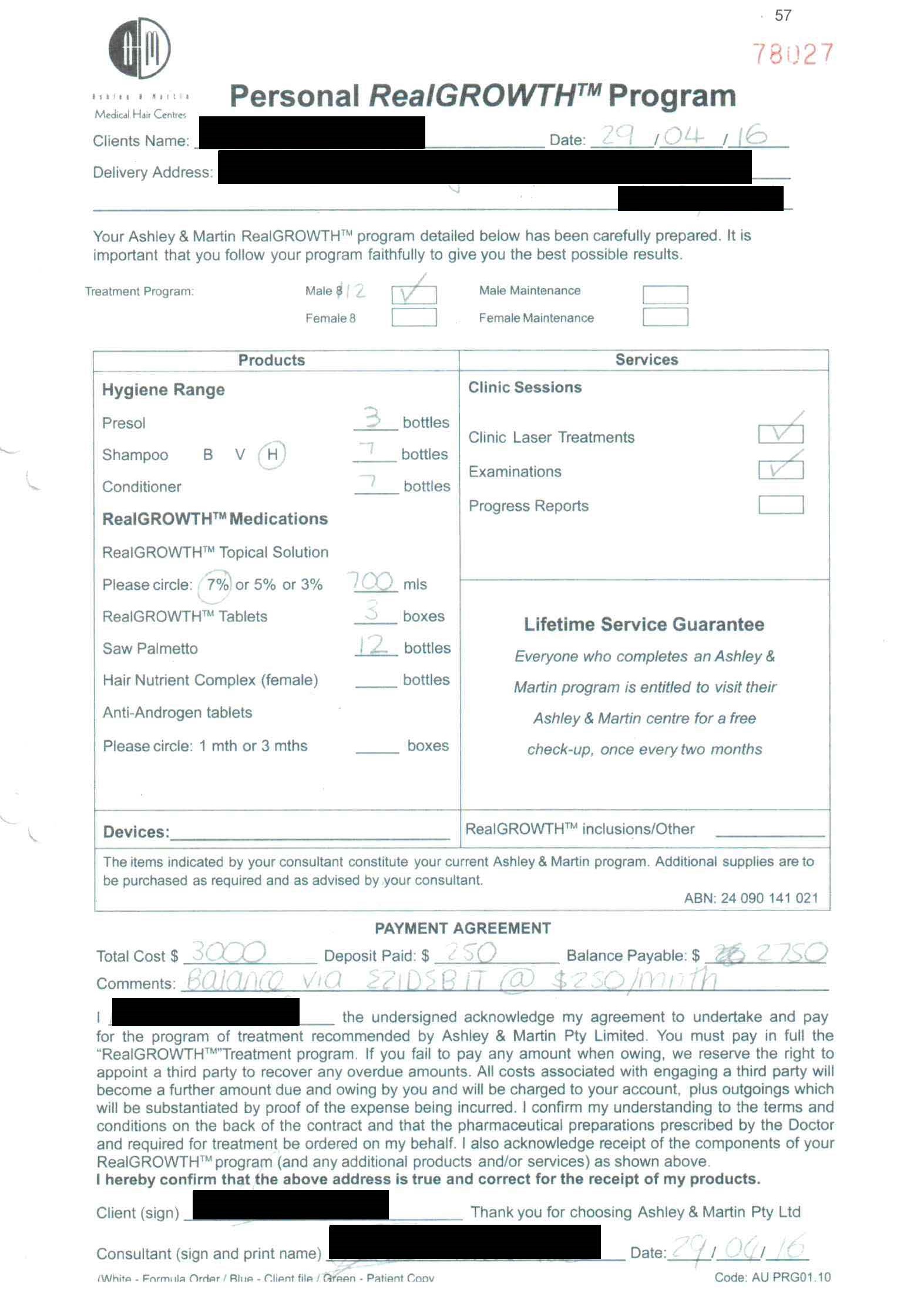

22 The parties referred to the three iterations of the contracts as the First Contract, Second Contract and Third Contract respectively, and referred to them collectively or generally as the Contracts. I will adopt the same convention in the balance of these reasons. The First Contract was used during the period June 2014 to September 2016. The Second Contract was used during the period September 2016 to January 2017. The Third Contract was used during the period February 2017 to June 2017. A copy of each is attached to these reasons as Annexure A, Annexure B and Annexure C respectively.

23 The impugned terms of the Contracts are marked up in the attachments and will be addressed in detail below.

24 During the relevant three year period, Ashley & Martin entered into the First Contract with 18,981 patients; the Second Contract with 3,402 patients; and the Third Contract with 3,571 patients. Of those patients, approximately 93% were male. Only a small proportion of patients signed up for a LaserCap (2.42%, 2.08% and 1.12% respectively of patients who entered into the First, Second and Third Contracts).

25 Upon execution of the Contract, the patient is obliged to pay for all or part of the cost of the Medical Treatment Program, subject to the terms of the Contract. Based on the sample Contracts reflected in the data schedule, those payments ranged from $1,820 to $6,600.

26 The patient typically makes the first payment for the Medical Treatment Program by payment of a deposit specified in the Contract at the initial consultation when the Contract is signed.

27 Ashley & Martin prepares the form of the Contract before it participates in any discussions with a potential patient.

28 The Contracts that were signed by patients did not specify prices for specific goods or services to be supplied under each Contract but stated a single price.

29 Contracts were for a term of eight or 12 months, and provided for the supply of a quantity of goods estimated by Ashley & Martin to be sufficient for the patient's requirements during the term.

30 The following examples from the data schedule (with identifying data deleted) indicate the manner in which supply and pricing of the goods component of a Medical Treatment Program might differ between patients:

Patient No | Term | Patient Age | Goods supplied | Quantity of each product | Price |

No 1 Perth Clinic 1st Contract | 8 months | 33 | Shampoo | 4 bottles | $5,700 |

Conditioner | 4 bottles | ||||

RealGROWTH Topical Solution | 500 mls | ||||

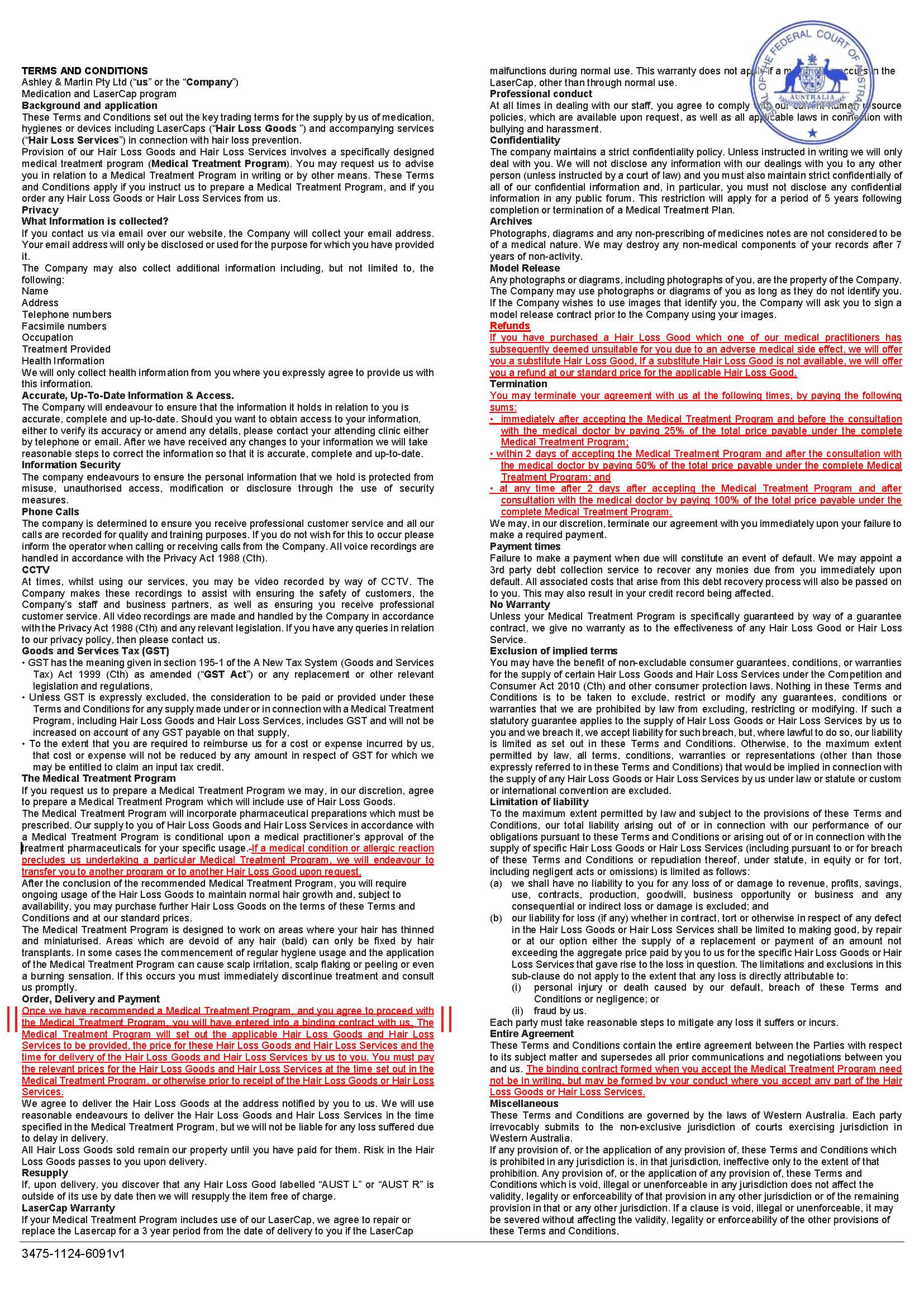

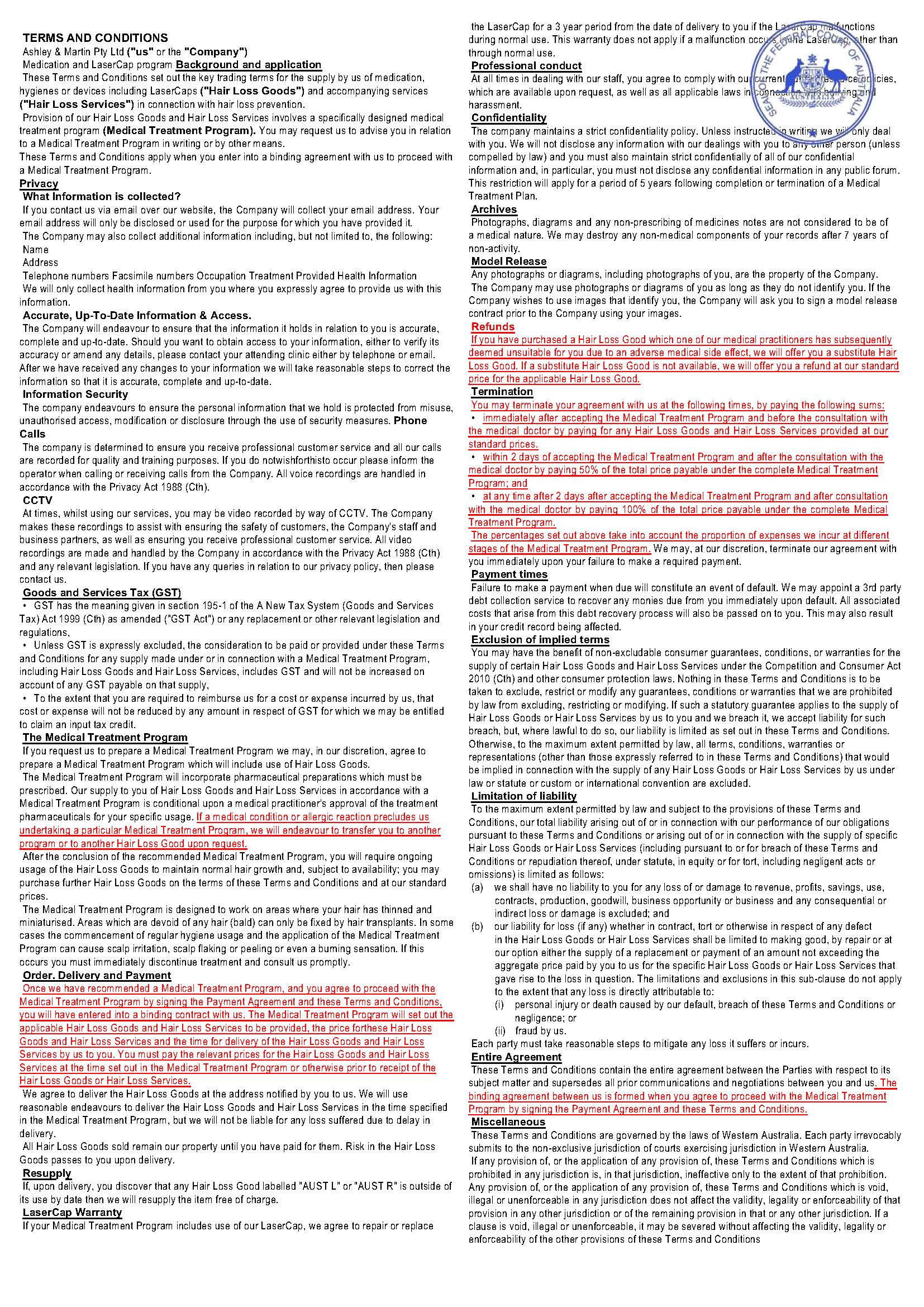

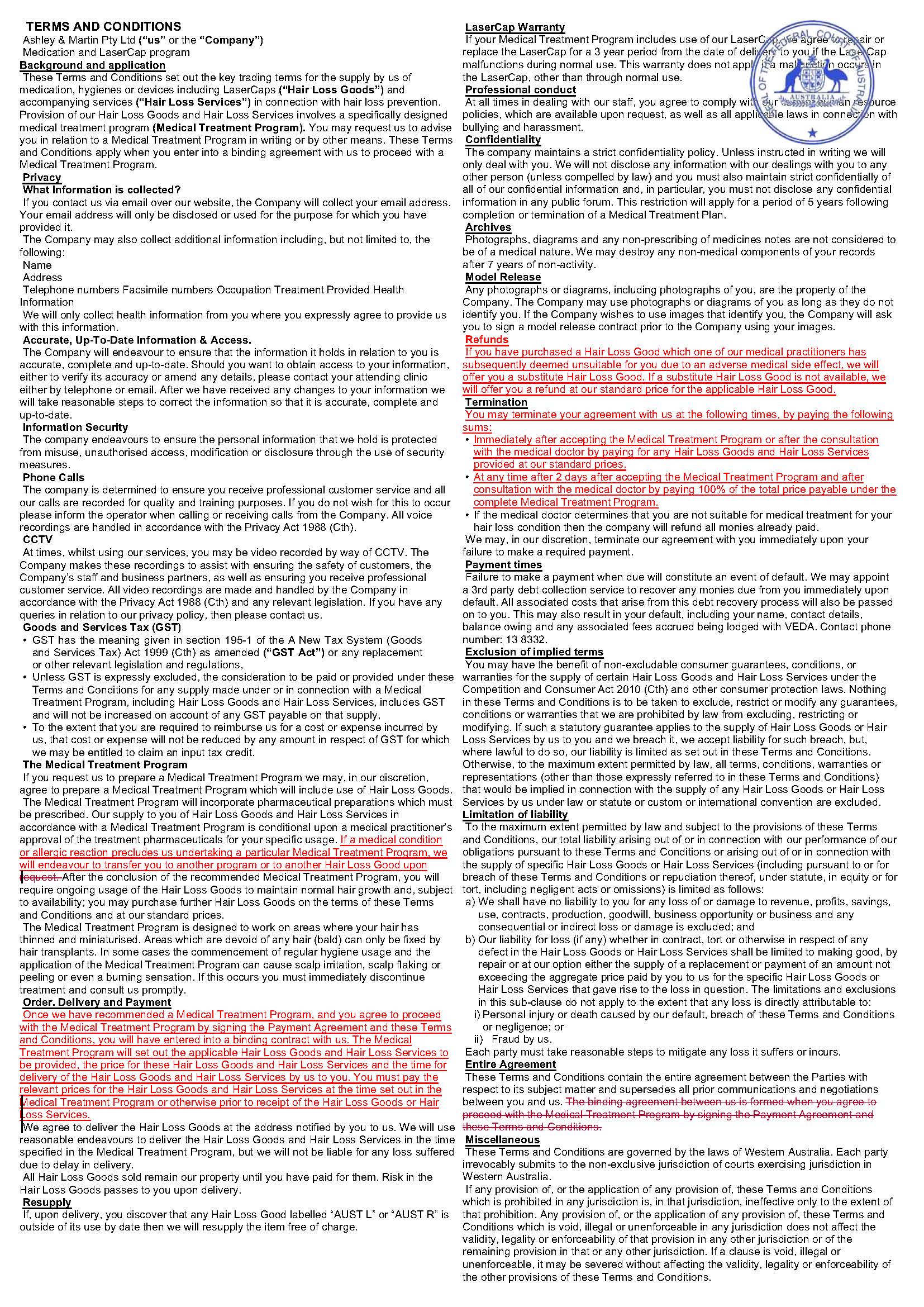

RealGROWTH tablets | 2 boxes | ||||

Saw Palmetto | 8 bottles | ||||

LaserCap | 1 | ||||

No 2 Sydney Clinic 1st Contract | 12 months | 29 | Presol | 3 bottles | $3,000 |

Shampoo 'H' | 7 bottles | ||||

Conditioner | 7 bottles | ||||

RealGROWTH Topical Solution 7% | 700 mls | ||||

RealGROWTH tablets | 3 boxes | ||||

Saw Palmetto | 12 bottles | ||||

No 3 Gladstone Park Clinic 2nd Contract | 8 months | 30 | Shampoo 'V' | 5 bottles | $4,000 |

Conditioner 'S' | 5 bottles | ||||

RealGROWTH Topical Solution 7% | 500 mls | ||||

RealGROWTH tablets | 2 boxes | ||||

Saw Palmetto | 2 bottles | ||||

No 4 Dandenong Clinic 3rd Contract | 8 months | 30 | Shampoo | 2 / 5 bottles | $4,500 |

Conditioner | 2 / 5 bottles | ||||

RealGROWTH Topical Solution 7% | 500 mls | ||||

RealGROWTH tablets | 2 boxes | ||||

Saw Palmetto | 2 bottles |

31 Annexure D is a random sample of a completed First Contract (minus the Terms and Conditions), with redactions for privacy.

32 During the relevant period, the 'standard' prices for the prescription and non-prescription goods supplied under the Contracts as determined by Ashley & Martin were as set out in the following table. These standard prices were the prices as referenced in the 'Refunds' clause in the First Contract and as referenced in both the 'Refunds' and 'Termination' clauses in the Second Contract and Third Contract, which are addressed below. The standard prices were incorporated in the aide memoire provided to the Court. There was no evidence as to the manner in which the difference between the cost price incurred by Ashley & Martin and the standard price was calculated.

Good | Standard price (for each unit) | Cost to Ashley & Martin (for each unit) |

Fintab (Finasteride) (For 5mg: 30 tablet pack; For 1mg: 126 tablet pack) | Between $93 and $140 | Between $38.50 and $60.64 |

Minoxidil (100 ml bottle) | $190 | Between $25.30 and $55.00 |

Saw Palmetto | $33 (30 capsule bottle before May 2016) $132 (120 capsule bottle after May 2016) | $3.52 (30 capsule bottle prior to May 2016) $18.15 (120 capsule bottle after May 2016) |

Presol (250 ml bottle) | $18 | $2.70 |

Shampoo (250 ml bottle) | $15 | Between $1.98 and $2.45 |

Conditioner (250 ml bottle) | $15 | $1.23 |

Laser cap | $2,800 | $1,136.34 |

Hair Nutrient Complex (60 tablet pack) | $60 | $3.94 |

Anti-Androgen tablets (Brenda 35) | $35 (1 month) $93 (3 months) | $40.85 (3 months) |

Anti-Androgen tablets (Spironolactone) | $35 (25 mg) $93 (100 mg) | $6.06 (25 mg) $23.77 (100 mg) |

33 The ACL appears as Schedule 2 to the Competition and Consumer Act 2010 (Cth). Chapter 2 of the ACL is headed 'General Protections' and includes statutory provisions addressing misleading or deceptive conduct (Part 2-1), unconscionable conduct (Part 2-2) and unfair contract terms (Part 2-3). This matter concerns s 23, s 24, s 25 and s 26, which fall within Part 2-3.

34 It can be accepted that unjustness and unfairness are of a lower moral or ethical standard than unconscionability, but the characterisation of unjustness or unfairness is, of course, evaluative and a task to be carried out with a close attendance to the statutory provisions: Paciocco v Australia and New Zealand Banking Group Ltd [2015] FCAFC 50 at [356], [363]-[364] (Allsop CJ); see also Australian Securities and Investments Commission v Kobelt [2019] HCA 18 at [118]-[119] (Keane J).

35 Section 23 provides, relevantly:

Unfair terms of consumer contracts and small business contracts

(1) A term of a consumer contract is void if:

(a) the term is unfair; and

(b) the contract is a standard form contract.

(2) The contract continues to bind the parties if it is capable of operating without the unfair term.

(3) A consumer contract is a contract for:

(a) a supply of goods or services; or

(b) a sale or grant of an interest in land;

to an individual whose acquisition of the goods, services or interest is wholly or predominantly for personal, domestic or household use or consumption.

…

36 It is common ground that the Medical Treatment Program involves the supply of goods and services for wholly or predominantly personal use or consumption and accordingly the Contracts comprise 'consumer contracts' within the meaning of s 23 of the ACL. Section 23 of the ACL provides that a term of a consumer contract is void if the term is 'unfair' and it is a 'standard form contract'. It is also common ground that the Contracts are standard form contracts.

37 Section 24 of the ACL provides:

Meaning of unfair

(1) A term of a consumer contract is unfair if:

(a) it would cause a significant imbalance in the parties' rights and obligations arising under the contract; and

(b) it is not reasonably necessary in order to protect the legitimate interests of the party who would be advantaged by the term; and

(c) it would cause detriment (whether financial or otherwise) to a party if it were to be applied or relied on.

(2) In determining whether a term of a consumer contract is unfair under subsection (1), a court may take into account such matters as it thinks relevant, but must take into account the following:

(a) the extent to which the term is transparent;

(b) the contract as a whole.

(3) A term is transparent if the term is:

(a) expressed in reasonably plain language; and

(b) legible; and

(c) presented clearly; and

(d) readily available to any party affected by the term.

(4) For the purposes of subsection (1)(b), a term of a consumer contract is presumed not to be reasonably necessary in order to protect the legitimate interests of the party who would be advantaged by the term, unless that party proves otherwise.

38 Therefore s 24(1) of the ACL requires the three elements in (a) to (c) to be satisfied before a term of a consumer contract is unfair.

39 Section 25 then sets out a list of potentially unfair terms:

Examples of unfair terms

(1) Without limiting section 24, the following are examples of the kinds of terms of a consumer contract that may be unfair:

(a) a term that permits, or has the effect of permitting, one party (but not another party) to avoid or limit performance of the contract;

(b) a term that permits, or has the effect of permitting, one party (but not another party) to terminate the contract;

(c) a term that penalises, or has the effect of penalising, one party (but not another party) for a breach or termination of the contract;

(d) a term that permits, or has the effect of permitting, one party (but not another party) to vary the terms of the contract;

(e) a term that permits, or has the effect of permitting, one party (but not another party) to renew or not renew the contract;

(f) a term that permits, or has the effect of permitting, one party to vary the upfront price payable under the contract without the right of another party to terminate the contract;

(g) a term that permits, or has the effect of permitting, one party unilaterally to vary the characteristics of the goods or services to be supplied, or the interest in land to be sold or granted, under the contract;

(h) a term that permits, or has the effect of permitting, one party unilaterally to determine whether the contract has been breached or to interpret its meaning;

(i) a term that limits, or has the effect of limiting, one party's vicarious liability for its agents;

(j) a term that permits, or has the effect of permitting, one party to assign the contract to the detriment of another party without that other party's consent;

(k) a term that limits, or has the effect of limiting, one party's right to sue another party;

(l) a term that limits, or has the effect of limiting, the evidence one party can adduce in proceedings relating to the contract;

(m) a term that imposes, or has the effect of imposing, the evidential burden on one party in proceedings relating to the contract;

(n) a term of a kind, or a term that has an effect of a kind, prescribed by the regulations.

40 Some explanation as to the listed examples is provided by the Explanatory Memorandum to the Trade Practices Amendment (Australian Consumer Law) Bill (No 2) 2010 (Cth). At [5.49]-[5.57], it is explained that:

(a) paragraphs 25(1)(a), (b), (d), (e), (f), (g), and (h) are examples of types of terms that allow a party to make changes to key elements of a contract, including terminating it, on a unilateral basis;

(b) paragraphs 25(1)(i), (k), (l), and (m) are examples of types of terms that have the effect of limiting the rights of the party to whom the consumer contract is presented;

(c) paragraph 25(1)(c) refers to terms that penalise, or have the effect of penalising, one party for a breach or termination of the contract (reflecting the common law concept of penalties); and

(d) paragraph 25(1)(j) refers to terms that allow for a party to assign the contract to the detriment of the other party, without that party's consent.

41 The list comprises illustrations and does not establish a presumption that a particular term is unfair. Any impugned term must still be considered in its context and an assessment made as to whether in the circumstances it is unfair.

42 Finally (for present purposes), s 26 is relevant. Section 26 exempts certain terms from the operation of s 23. It provides:

Terms that define main subject matter of consumer contracts or small business contracts are unaffected

(1) Section 23 does not apply to a term of a consumer contract to the extent, but only to the extent, that the term:

(a) defines the main subject matter of the contract; or

(b) sets the upfront price payable under the contract; or

(c) is a term required, or expressly permitted, by a law of the Commonwealth, a State or a Territory.

(2) The upfront price payable under a consumer contract is the consideration that:

(a) is provided, or is to be provided, for the supply, sale or grant under the contract; and

(b) is disclosed at or before the time the contract is entered into;

but does not include any other consideration that is contingent on the occurrence or non-occurrence of a particular event.

43 There was no dispute between the parties as to the appropriate principles with respect to s 24. In Australian Competition and Consumer Commission v CLA Trading Pty Ltd [2016] FCA 377; (2016) ATPR 42-517 at [54], Gilmour J summarised them as follows:

(a) The underlying policy of unfair contract terms legislation respects true freedom of contract and seeks to prevent the abuse of standard form consumer contracts which, by definition, will not have been individually negotiated: Jetstar Airways Pty Ltd v Free (2008) 30 VAR 295; [2008] VSC 539 at [112].

(b) The requirement of a 'significant imbalance' directs attention to the substantive unfairness of the contract: Director General of Fair Trading v First National Bank plc [2002] 1 AC 481; [2001] UKHL 52 at [37].

(c) It is useful to assess the impact of an impugned term on the parties' rights and obligations by comparing the effect of the contract with the term and the effect it would have without it: Director General of Fair Trading v First National Bank plc at [54].

(d) The 'significant imbalance' requirement is met if a term is so weighted in favour of the supplier as to tilt the parties' rights and obligations under the contract significantly in its favour. This may be by the granting to the supplier of a beneficial option or discretion or power, or by the imposing on the consumer of a disadvantageous burden or risk or duty: Director General of Fair Trading v First National Bank plc at [17] per Lord Bingham, applied in Australian Competition and Consumer Commission v ACN 117 372 915 Pty Limited (in liq) (formerly Advanced Medical Institute Pty Limited) [2015] FCA 368 at [950].

(e) Significant in this context means 'significant in magnitude', or 'sufficiently large to be important', 'being a meaning not too distant from substantial': Jetstar Airways Pty Ltd v Free at [104]-[105] per Cavanough J; cf Director of Consumer Affairs Victoria v AAPT Limited [2006] VCAT 1493 at [32]-[33].

(f) The legislation proceeds on the assumption that some terms in consumer contracts, especially in standard form consumer contracts, may be inherently unfair, regardless of how comprehensively they might be drawn to the consumer's attention: Jetstar Airways Pty Ltd v Free at [115].

(g) In considering 'the contract as a whole', not each and every term of the contract is equally relevant, or necessarily relevant at all. The main requirement is to consider terms that might reasonably be seen as tending to counterbalance the term in question: Jetstar Airways Pty Ltd v Free at [128].

44 In Australian Competition and Consumer Commission v Chrisco Hampers Australia Limited [2015] FCA 1204; (2015) 239 FCR 33 Edelman J noted that s 24 is an example of a legislative technique which creates broad evaluative criteria to be developed incrementally and that it is not possible to state a precise or universal test for its application (at [39]). His Honour approved the following approach concerning the construction of s 24 (at [43]):

(a) for a term to be unfair it must satisfy the requirements of all of s 24(1)(a) to (c);

(b) the onus is upon the applicant to prove the matters in s 24(1)(a) and s 24(1)(c) but it is upon the respondent in relation to s 24(1)(b);

(c) s 24(2)(a) only requires the Court to consider transparency in relation to the particular term that is said to be unfair and only in relation to the matters concerning that term in s 24(1)(a) to (c);

(d) similarly, the assessment of the contract as a whole in s 24(1)(c) only requires the Court to consider the contract as a whole in relation to the particular term that is said to be unfair and only in relation to the matters concerning that term in s 24(1)(a) to (c);

(e) as the Explanatory Memorandum provided at [5.39], 'if a term is not transparent it does not mean that it is unfair and if a term is transparent it does not mean that it is not unfair'; and

(f) guidance can be had to s 25 which provides examples of unfair terms.

Section 24 - significant imbalance

45 As is seen from the above extract, CLA Trading provides some guidance as to the meaning of significant imbalance. Further guidance is gained from Chrisco. Edelman J noted in Chrisco that the focus remains on the terms of the section (at [49]). The fact that there is a lack of individual negotiation of the contract between an entity and its customers is not relevant to whether a term causes a significant imbalance in the parties' rights and obligations under the contract. Rather, the assessment of whether the relevant term causes a significant imbalance in the rights and obligations arising under the contract requires consideration of the relevant term together with the parties' other rights and obligations arising under the contract (at [50]-[51]).

46 Other relevant matters under s 24(2) may include whether a party can 'opt-out' of an unfair term and whether the contract gives one party a right without imposing a corresponding duty or without giving any substantial corresponding right to the counterparty (Edelman J at [52]-[53], [70]).

47 In Australian Competition and Consumer Commission v JJ Richards & Sons Pty Ltd [2017] FCA 1224 at [31] Moshinsky J observed that:

A term is less likely to give rise to a significant imbalance if there is a meaningful relationship between the term and the protection of a party, and that relationship is reasonably foreseeable at the time of contracting. The fact that a party might profit from breaches of contract by a customer, without the customer in breach acquiring something in return, would not alone be sufficient to allow it to be concluded that the term caused a significant imbalance in the parties' rights and obligations arising under the contract: Paciocco v Australia & New Zealand Banking Group Ltd (2016) 258 CLR 525 at [201] per Gageler J.

Section 24 - Reasonably necessary to protect legitimate interest

48 It is not appropriate to attempt to define 'legitimate interest'. It will depend upon the nature of the particular business of the relevant supplier and the context of the contract as a whole. However, there is guidance in the authorities, even having regard to the fact that in those authorities the courts have considered different statutory provisions.

49 For example, a legitimate interest may not be purely monetary. A party's 'legitimate interests' are not confined to the reimbursement of expenses directly occasioned by the customer's default. A party may have interests in contractual performance which are intangible and unquantifiable: Paciocco v Australia and New Zealand Banking Group Ltd [2016] HCA 28; (2016) 258 CLR 525 at [26] (Kiefel J), [161] (Gageler J), [216], [266], [298] (Keane J). It may be of a business or financial nature: Paciocco (HCA) at [29] (Kiefel J).

50 The question of legitimate interest was discussed in Australian Competition and Consumer Commission v ACN 117 372 915 Pty Ltd (in liq) (formerly Advanced Medical Institute Pty Ltd) [2015] FCA 368 (ACCC v AMI). The respondent company sold expensive erectile dysfunction treatment programs using high-pressure sales practices. There was no proper scientific evidence to support long-term treatment programs with the relevant medications. The result was that patients were committed to a period of treatment which had no proper medical justification, but which entailed considerable cost to the patient. The reason the respondent required doctors to recommend long-term treatment programs was that such contracts produced more revenue than short-term programs. Whilst in the context of unconscionable conduct, North J held (upheld on appeal):

[925] For AMI and NRM to require doctors to recommend long-term treatment programs without a proper medical reason for so doing was to exploit the patients for the commercial benefit of AMI and NRM. That conduct was unconscionable because AMI and NRM had no legitimate interest in having patients agree to long-term contracts. They were not providing a treatment for a period which had a verified medical reason. That was not legitimate business. The inclusion in such circumstances of terms which are not reasonably necessary to protect the legitimate interests of a supplier is akin to the possible marker of unconscionable conduct referred to in s 51AB(2)(b) of the TPA, s 21(2)(b) of the ACL operating between 1 January 2011 and 1 January 2012, and s 22(1)(b) of the ACL in operation after 1 January 2012.

51 The question of what is 'reasonably necessary' will also involve consideration of the particular circumstances of the business.

52 The decision in JJ Richards provides some useful examples. In that case the respondent did not seek to rebut the presumption created by s 24(4) of the ACL and agreed that the impugned terms were not reasonably necessary to protect its legitimate interests. Nevertheless it was necessary for the Court to be satisfied as to those matters. Relevantly, Moshinsky J stated:

[57] …

(a) The automatic renewal clause: Contracts with JJR Customers are usually low value, with a low marginal cost to JJ Richards for each additional customer. Consequently, the automatic renewal clause is not reasonably necessary to protect JJ Richards' legitimate interests.

(b) The price variation clause: Although JJ Richards' costs may increase for reasons beyond its control, the price variation clause goes beyond what is reasonably necessary in order to protect JJ Richards' legitimate interests. For example, on one view, the price variation clause would allow JJ Richards to increase its prices simply because it wished to increase its revenue or profitability. While increasing prices in order to increase its revenue or profitability would be in JJ Richards' interests, those are not legitimate interests in this context.

(c) The agreed times clause: The agreed times clause goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests by absolving JJ Richards of its performance obligations and requiring JJR Customers to assume the risk of non-performance under circumstances that they do not control.

(d) The no credit without notification clause: The right to render charges when JJ Richards is unable to perform the service for any reason goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests.

(e) The exclusivity clause: The exclusivity clause goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests. JJ Richards does not need to have exclusivity in relation to waste management in order to conduct its business.

(f) The credit terms clause: The short credit term of seven days and the obligation on the JJR Customer to pay 'normal charges' during suspension without any limitations, irrespective of whether JJ Richards had in fact incurred any expenses, goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests.

(g) The indemnity clause: The unlimited indemnity in favour of JJ Richards, even where the loss incurred by JJ Richards is not the fault of the JJR Customer, goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests.

(h) The termination clause: Where monies remain outstanding from a JJR Customer, JJ Richards could recover those funds through ordinary legal recovery processes. JJ Richards could also charge interest for outstanding fees. By enabling JJ Richards to continue to charge JJR Customers for equipment they no longer require or enjoy, in circumstances where JJ Richards could recoup outstanding fees through other means, this clause goes beyond what is reasonably necessary to protect JJ Richards' legitimate interests in recovering outstanding monies.

53 It is clear (from [57(h)], for example) that Moshinsky J took into account other options that might be available to the respondent in terms of protecting its business interests in assessing the question of what is reasonably necessary.

54 This approach is supported by comments in Kobelt in which the High Court addressed the question of unconscionability. It was not a case that featured discussion of unfair terms provisions. However, in assessing whether conduct is unconscionable under s 12CB of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), s 12CC(1)(b) of the ASIC Act provides that the Court may have regard to whether the service recipient was required to comply with provisions that were not reasonably necessary for the protection of the legitimate interest of the supplier. In that context Gageler, Nettle and Gordon JJ commented on the question of protection of legitimate interests. Gageler J noted that there were other means by which the respondent might have protected his legitimate interests which had a less restrictive effect on the relevant customers (at [98]). Nettle and Gordon JJ took into account when assessing whether the relevant system was reasonably necessary to protect the respondent's legitimate interests that 'there were alternatives' (at [264]) (that Nettle and Gordon JJ were in the minority in Kobelt does not in its context diminish the value of the particular comment).

55 What is 'reasonably necessary' might also involve an analysis of the proportionality of the term against the potential loss sufferable.

56 In Paciocco (HCA), Gageler J found that it could not be said that a late payment fee was not reasonably necessary for the protection of ANZ's legitimate interests by express reference to the average costs incurred by ANZ in connection to the event giving rise to the entitlement to charge the late payment fee: at [195].

57 In Australian Competition and Consumer Commission v Get Qualified Australia Pty Ltd (in liq) (No 2) [2017] FCA 709 Beach J stated:

[344] Further, the terms of the refund policy were not reasonably necessary to protect GQA's legitimate interests because the policy could be relied upon to refuse a refund in circumstances where GQA had not incurred any significant costs in relation to a particular consumer or GQA would not be out of pocket if a refund were provided and s 24(4) applied.

58 In Re Elsmore Resources Ltd [2016] NSWSC 856, the plaintiff brought an action under a handwritten settlement agreement under which the defendant agreed to a guarantee. By the guarantee, the defendant agreed to pay an amount to the creditor that was substantially more than what was lost. The creditor claimed that the terms of the settlement could not be said to be unreasonably difficult to comply with or not reasonably necessary for the protection of its legitimate interests. Black J dealt with the question by contrasting the potential loss to the contract-maker with the amount they could recover from enforcing the contract term, as follows:

[81] … For the purposes of s 9(1) of the Contracts Review Act, it seems to me that the public interest would not be served, and that injustice would arise, where Elsmore seeks to rely on the Handwritten Terms to recover more than double the amount of its actual loss. It also seems to me that the Handwritten Terms imposed conditions that were not reasonably necessary for the protection of Elsmore's legitimate interests, where it sought to secure by a guarantee the recovery of more than double the loss that it had suffered.

59 Therefore, without limiting the matters relevant to the assessment, it is appropriate to have regard to matters such as available alternatives and proportionality.

60 The requirement that detriment 'would' exist requires that the detriment be more than a mere possibility. In the Explanatory Memorandum it is noted:

5.31 By requiring evidence of whether detriment has existed or would exist in the future, the provision requires more than a hypothetical case to be made out by the claimant. In this context, a claimant does not need to have proof of having suffered actual detriment, but that detriment would exist in the future as a result of the application of or reliance on the term.

5.32 In this regard, a term does not need to be enforced in order to be unfair, although the possibility of such enforcement may impact on the decisions made by the party that would be disadvantaged by the term's practical effect, to that party's detriment.

61 The question of detriment may be considered together with the question of whether the term would cause a significant imbalance in the parties' rights and obligations arising under the contract: ACCC v AMI at [950], affirmed on appeal in NRM Corporation Pty Ltd v Australian Competition and Consumer Commission [2016] FCAFC 98 at [200].

62 In Director General of Fair Trading v First National Bank plc [2002] 1 AC 481 at 499, Lord Steyn noted that an equivalent provision under the UK legislation does little other than clarify that it is primarily 'aimed at significant imbalance against the consumer, rather than the seller or supplier'.

63 Detriment may include the imposition of liability in circumstances where the consumer would otherwise not be liable, or allowing the company to charge the consumer for damage for breach of contract where that breach did not cause or contribute to the damage: CLA Trading at [80]. It may include the imposition of a termination fee which is imposed regardless of the reason for termination: ACCC v AMI at [951].

64 As the definition makes express, detriment may also be non-financial.

Section 24(2) - consideration of the contract as a whole

65 Section 24(2) expressly provides that in assessing whether a term is unfair under s 24(1) the Court may take into account such matters as it considers relevant, but it must take into account the extent to which the terms are transparent and the contract as a whole. The meaning of 'transparent' is defined and self-explanatory.

66 As to having regard to the contract as a whole, it is in any event clear that an impugned term cannot be assessed in a vacuum which ignores the practical considerations which attach to the carrying out of contractual obligations: Turner v MyBudget Pty Limited [2018] FCA 1407 at [69]. It is appropriate to consider how impugned terms interact or how non-impugned terms might ameliorate the impact of the impugned terms: JJ Richards at [61], [63].

67 If terms were considered in isolation, then the purpose of s 23 might be defeated by the careful drafting of individual terms that might not be unfair alone but are unfair when read together.

68 This provision has practical importance in this case where a number of different terms are impugned.

69 As to s 26, it appears the court has not yet had occasion to rule on its scope. An analogous provision in s 12BI(2) of the ASIC Act also has not been the subject of determination.

70 As to 'the main subject matter of the contract', the Explanatory Memorandum states:

[5.59] The exclusion of terms that define the main subject matter of a consumer contract ensures that a party cannot challenge a term concerning the basis for the existence of the contract.

[5.60] Where a party has decided to purchase the goods, services, land, financial services or financial products that are the subject of the contract, that party cannot then challenge the fairness of a term relating to the main subject matter of the contract at a later stage, given that the party had a choice of whether or not to make the purchase on the basis of what was offered.

[5.61] The main subject matter of the contract may include the decision to purchase a particular type of good, service, financial service or financial product, or a particular piece of land. It may also encompass a term that is necessary to give effect to the supply or grant, or without which, the supply or grant could not occur.

71 Therefore, s 26(1)(a) implies that a distinction can be drawn between terms that define the main subject matter of the contract and other terms.

72 As to 'the upfront price', the Explanatory Memorandum states:

5.63 Consideration includes any amount or thing provided as consideration for the supply of a good, service, financial service, financial product or a grant of land. It would also include any interest payable under a consumer contract.

5.64 The exclusion of upfront price means that a term concerning the upfront price cannot be challenged on the basis that it is unfair. Having agreed to provide a particular amount of consideration when the contract was made, which was disclosed at or before the time the contract was entered into, a person cannot then argue that that consideration is unfair at a later time. The upfront price is a matter about which the person has a choice and, in many cases, may negotiate.

5.65 The upfront price covers the cash price payable for a good, service, financial service, financial product or land at the time the contract is made. It also covers a future payment or a series of future payments.

…

5.67 A key consideration for a court in considering whether a future payment, or a series of future payments, forms the upfront price may be the transparency of the disclosure of such a payment, or the basis on which such payments may be determined, at or before the time the contract is made.

…

5.69 Other consideration (that is, further forms of consideration which are not part of the upfront price) under the consumer contract that is contingent on the occurrence or non‑occurrence of a particular event, is excluded from the determination of the upfront price.

5.70 Terms that require further payments levied as a consequence of something happening or not happening at some point in the duration of the contract are covered by the unfair contract terms provisions. Such payments are additional to the upfront price, and are not necessary for the provision of the basic supply, sale or grant under the contract.

73 Similar provisions in the UK Unfair Terms in Consumer Contracts Regulations have been the subject of decisions of the House of Lords in First National Bank (referred to in CLA Trading) and the Supreme Court in Office of Fair Trading v Abbey National plc [2010] 1 AC 696.

74 The UK Regulations were made under s 2(2) of the European Communities Act 1972 and their purpose was to give effect to a 1993 ECC Directive on unfair terms in consumer contracts. The regulations were thus interpreted taking into account the construction and purpose of the Directive. The provisions are not the same as s 26 and in fact have some important distinguishing features. Nevertheless, the detailed reasons in Abbey National provide some insight into the issues that arise in construing exclusion provisions such as s 26 of the ACL.

75 First National Bank concerned the construction of reg 3(2) of the 1994 Regulations. That regulation provided that:

In so far as it is in plain, intelligible language, no assessment shall be made of the fairness of any term which - (a) defines the main subject matter of the contract, or (b) concerns the adequacy of the price or remuneration, as against the goods or services sold or supplied.

76 In First National Bank, it was held that a provision in a contract between banker and customer for the payment of post-judgment interest was not excluded from review, as it applied only in the event of default and so could not be characterised as a provision concerning the adequacy of price or remuneration as against the goods sold or supplied within the meaning of the UK Regulation. Rather, it was concerned to ensure that a right to interest did not come to an end upon entry of judgment.

77 Abbey National concerned reg 6(2) of the 1999 Regulations. It provided that:

In so far as it is in plain intelligible language, the assessment of fairness of a term shall not relate - (a) to the definition of the main subject matter of the contract, or (b) to the adequacy of the price or remuneration, as against the goods or services supplied in exchange.

78 It was held that a provision in a contract between banker and customer for the imposition of fees in the event that the customer were to overdraw on a personal current account was excluded from review because such fees related to the adequacy of price. It was part of the package of costs that made up the price. It was irrelevant that the charges were contingent. The provision excluded an assessment of unfairness insofar as it related to the adequacy of the fees viewed against the services supplied.

79 The reference in Abbey National to the irrelevancy of the contingent nature of a payment highlights one of the significant differences between reg 6(2) there considered and s 26 of the ACL. The express carve out under s 26(2) of the ACL of consideration that is contingent does not appear in reg 6(2) of the UK provision. It can be seen immediately that for certain consumer or small business contracts in Australia, questions will remain under s 26 of the ACL as to whether particular charges or fees might fall within a package that comprises an upfront price or alternatively may be open to assessment because of their contingent nature.

80 Regardless, useful aspects of the reasons in Abbey National include:

(a) it is important to recall that the provision excludes an attack on fairness only insofar as the relevant charges comprise the price or remuneration and only insofar as the attack relates to the adequacy or appropriateness in amount of the price or remuneration: it does not exclude an attack on the terms on other grounds (Lord Walker at [57], Lord Phillips at [95], [101]);

(b) not every provision for payment is rendered immune from scrutiny. There can be monetary consideration that does not constitute either price or remuneration of goods or services provided in exchange, an example being the charges considered in First National Bank (Lord Walker at [43], Lord Phillips at [101]);

(c) care should be taken not to exclude price or remuneration from the application of reg 6(2) on the basis that it is 'ancillary', 'incidental' , 'subordinate' or the like. Such descriptions may be of some assistance but 'it is important, in considering provisions which apply across an extraordinarily wide range of consumer contracts, to treat them with caution' (Lord Walker at [46]); and

(d) nor do the expressions 'core term' or 'essential term' substitute for considering the content of paragraphs (a) and (b) of reg 6(2) (Lord Walker at [38]-[39]). A supply of services may be simple or composite. There may be no principled basis upon which to assess that some components are more 'essential' than others, and it may be that the main subject matter must be described in general terms. Similarly, it may be difficult to ascertain which price components are 'essential'. The regulation is not concerned with the 'essential price' but any consideration that falls within its language (Lord Walker at [40]-[42]).

81 It goes without saying that what might define the main subject matter and set the upfront price payable for the purpose of s 26 of the ACL will always depend upon the particular contract being construed. Delineation of terms by taxonomy or hierarchy will not necessarily assist with the application of s 26. Instead, it is important to steadily bear in mind the terms of the provision itself and its object, being to protect the 'basis for the existence of the contract' (Explanatory Memorandum [5.60]) whilst otherwise leaving open to challenge the terms of a contract that might be unfair.

82 Section 26 is drafted to protect from assessment a term 'but only to the extent' that it defines the main subject matter or sets the upfront price. The inclusion of the words 'but only to the extent' indicates that there is no generalised protection of any term that happens to touch upon obligations to supply goods or services.

83 Further, the provision is drafted with precision. It does not utilise general drafting expressions that are often used to denote a connection. That is, it does not refer to terms that 'relate to' or 'concern' supply or price. It is more specific. It addresses terms that 'define' the main subject matter or 'set' the upfront price.

84 Such level of precision does not lead to a task that is necessarily complicated. One would expect that in many cases identifying the main subject matter and the upfront price (with the assistance of the definition) will often be possible with little more than the application of common sense. Indeed, one would hope that is generally the case with consumer contracts. However, there is no doubt there will be cases where more complex questions may arise, for example as to whether particular charges or payments are contingencies or part of a package that comprises an upfront payment.

85 However, it is clear that the correct approach to the application of s 26 is to have careful regard to its particular terms and definitions when testing whether terms or parts of terms might fall within its ambit. Too broad an approach may tend to deny the object of the regime by extending protection from attack for unfairness beyond the scope of that anticipated by the Explanatory Memorandum and, more importantly, that reflected in the drafting.

86 I will return to the construction of s 26 in the context of the particular impugned clauses of the Contracts in due course.

Ashley & Martin's overarching 'no obligation' and 'supply term' submissions

87 Before embarking on an analysis of the terms of the First Contract, two overarching submissions made by Ashley & Martin should be noted.

88 First, Ashley & Martin denies that there is any obligation on the part of a patient to sign the Contract prior to seeing a doctor. It submitted that it is always open to a patient at a first consultation to ask to take the Contract away and see a doctor prior to signing. I will refer to this as the 'no obligation' submission.

89 There was no evidence about whether that ever occurred.

90 The ACCC points to the fact that the Contract anticipates that (consistent with practice) the Contract is signed at or shortly after the initial consultation and before the consultation with a medical practitioner. That a particular patient may ask to take the Contract away and obtain medical advice before signing does not deny the unfairness of the Contract when signed in the ordinary course. The ACCC says that Ashley & Martin's argument does not address the circumstances in which the impugned Contracts are in fact signed and relied upon.

91 Second, Ashley & Martin argues that despite the limited express rights on the part of a patient to terminate the contract in accordance with terms included under the heading 'Termination', it is also open to the patient to terminate the Contract if a doctor advises that a program is unsuitable. It says this follows because Ashley & Martin is not then compelled to supply the goods and services and that in such a scenario Ashley & Martin would not require payment and the contract is at an end. Ashley & Martin refers to this as the 'supply term' submission.

92 These overarching submissions influenced the manner in which Ashley & Martin addressed some of the particular impugned clauses. It will be necessary to return to them.

93 The terms of the First Contract which the ACCC submits are unfair are marked up in Annexure A. As terms are not numbered, for ease of reference I will collect them under subheadings. In doing so, I have not disregarded the obligation under s 24(2) to consider the terms as a whole.

94 On the first page of the Contract, under a heading 'payment agreement' is the following acknowledgment:

I [insert name] the undersigned acknowledge my agreement to undertake and pay for the program of treatment recommended by Ashley & Martin Pty Ltd. You must pay in full the RealGROWTH Treatment program.

95 At the time of signing (on the ACCC's case) the recommendation has been made by the hair loss consultant. The patient expressly agrees to pay for the Medical Treatment Program in full. The content of the program as determined by the consultant at the initial consultation is reflected on the first page, as can be seen in the example attached as Annexure D.

96 The first page also includes the indorsement:

Your Ashley & Martin RealGROWTH program detailed below has been carefully prepared. It is important that you follow your program faithfully to give you the best possible results.

97 Under the heading 'Background and application', the Terms and Conditions include definitions of 'Hair Loss Goods' (medication, hygienes [sic] or devices including LaserCaps) and 'Hair Loss Services' (accompanying services). The provision of these Hair Loss Goods and Hair Loss Services is said to involve a specifically designed medical treatment program, defined as a 'Medical Treatment Program'. It is clear from these definitions that what is provided is a medical treatment (not merely herbal or supplements based).

98 Under the heading 'Medical Treatment Program', it is provided that:

If you request us to prepare a Medical Treatment Program we may, in our discretion, agree to prepare a Medical Treatment Program which will include use of Hair Loss Goods.

99 The Contract then states:

[t]he Medical Treatment Program will incorporate pharmaceutical preparations which must be prescribed. Our supply to you of Hair Loss Goods and Hair Loss Services in accordance with a Medical Treatment Program is conditional on a medical practitioner's approval of the treatment pharmaceuticals for your specific usage. If a medical condition or allergic reaction precludes us undertaking a particular Medical Treatment Program, we will endeavour to transfer you to another program or Hair Loss Good upon request.

100 Again, it is clear from this clause that any Medical Treatment Program will include prescription medicines.

101 The ACCC observes that it is only Ashley & Martin's obligation to supply that is expressed to be conditional, and not the patient's obligation to pay. The term also has the effect that the patient cannot insist on the precise Hair Loss Goods and Hair Loss Services that were specified on the front page of the contract if the doctor advises that they are unsuitable, but that Ashley & Martin's obligation, in those circumstances, is to endeavour to transfer the patient to another program or Hair Loss Good on request.

102 Ashley & Martin relies on the term as an overarching defence to the ACCC's claims of unfairness. It relies on the following sentence as the basis for its supply term submission:

Our supply to you of Hair Loss Goods and Hair Loss Services in accordance with a Medical Treatment Program is conditional on a medical practitioner's approval of the treatment pharmaceuticals for your specific usage.

103 It submits that the clause, properly construed, means that if a doctor advises that the prescription goods are unsuitable for the patient, then Ashley & Martin has no obligation to provide the products, the patient has no obligation to pay any money and the contract is at an end.

104 The provisions under the heading 'Order, Delivery and Payment' include:

Once we have recommended a Medical Treatment Program, and you agree to proceed with the Medical Treatment Program, you have entered into a binding contract with us. The Medical Treatment Program will set out the applicable Hair Loss Goods and Hair Loss Services and the time for delivery of the Hair Loss Goods and Hair Loss Services by us to you. You must pay the relevant prices for the Hair Loss Goods and Hair Loss Services at the time set out in the Medical Treatment Program, or otherwise prior to receipt of the Hair Loss Goods and Hair Loss Services.

105 Those sentences are impugned.

106 The binding nature of the patient's obligation is further emphasised under the heading 'Entire Agreement' as follows:

The binding contract formed when you accept the Medical Treatment Program need not be in writing, but may be formed by your conduct where you accept any part of the Hair Loss Goods or Hair Loss Services.

107 The refund clause that is impugned is limited in scope and effect. It provides that:

If you have purchased a Hair Loss Good which one of our medical practitioners has subsequently deemed unsuitable for you due to an adverse medical side effect, we will offer you a refund at our standard price for the applicable Hair Loss Good.

108 The limitation is twofold. First, it does not apply where due to concern about risk and side effects the patient no longer wishes to continue the program. It applies only where there is an adverse medical side effect (or arguably where the adverse medical side effect is anticipated by the doctor) and a doctor has deemed the product unsuitable. Second, the refund concerns only a component of a tailored Medical Treatment Program. Without that component the Medical Treatment Program is incomplete. The patient is also left with other products for which no refund is provided.

109 Under one of the Medical Treatment Program terms (column 1 of the Terms and Conditions), Ashley & Martin must also endeavour in the case of a medical condition or allergic reaction to offer a substitute Hair Loss Good or transfer the patient to another program. That obligation may in some cases address the concern, but where neither outcome occurs then the patient is left to terminate and incur costs.

110 Leaving aside Ashley & Martin's supply term submission, the patient's rights to terminate after having entered into the agreement are set out expressly under the heading 'Termination':

You may terminate your agreement with us at the following times by paying the following sums:

• immediately after accepting the Medical Treatment Program and before the consultation with the medical doctor by paying 25% of the total price payable under the complete Medical Treatment Program;

• within 2 days of accepting the Medical Treatment Program and after the consultation with the medical doctor by paying 50% of the total price payable under the complete Medical Treatment Program, and

• at any time after 2 days after accepting the Medical Treatment Program and after consultation with the medical doctor by paying 100% of the total price payable under the complete Medical Treatment Program.

111 This clause, including the three limbs, is impugned.

112 The first limb contemplates that the patient enters into the Contract before seeing a doctor and thus before obtaining any medical advice about the medical treatments provided for in the Contract. It is clear from the reference to 'the consultation with the medical doctor' that it anticipates the consultation that Ashley & Martin organises with its doctor at the initial consultation with the hair loss consultant. Immediately upon signing the Contract, the patient is obliged to pay a minimum of 25% of the contract price. To put it in perspective, based on the aide memoire that 25% sum can range between $600 and $1,650, depending on the Contract.

113 The meaning of the second and third limbs is somewhat obscure, to adopt the ACCC's apt description. However, it appears that by the second limb if the patient sees the doctor within two days of signing the Contract then, after that consultation but before the expiry of two days, the patient may terminate, but must pay 50% of the contract price, that is, between $1,200 and $3,300.

114 By the third limb, after the lapse of the two days and after seeing the doctor, the patient effectively has no real right to terminate, being obliged to pay 100% of the contract price, that is, between $2,400 and $6,600.

115 The obscurity arises when one attempts to apply these terms to a situation where the two days have elapsed, but the patient has not yet seen the doctor. The second limb will not apply, because the time will not be 'within 2 days of accepting the Medical Treatment Program'. But the third limb also will not apply, because the time will not be 'after consultation with the medical doctor'.

116 However, Ashley & Martin relies upon its supply term submission. It contends that regardless of their construction, those terms that appear under the heading 'Termination' are not the sole means of termination. Those terms are simply permissive and coexist with the supply term and any common law and statutory rights of termination.

117 Ashley & Martin accepts that the second limb is unclear. However, it says that the objective intention of the parties is that the three limbs cover the period beginning with the acceptance of the Medical Treatment Program and accordingly, objectively construed, the second limb means that a patient may terminate on payment of 50% of the total price payable under the Medical Treatment Program within two days of seeing the doctor.

Are the terms in any event excluded from review

118 If Ashley & Martin is correct that certain terms are excluded from review under s 26(1), then there is no value in undertaking a fairness assessment of them. Logically, the question of exclusion should be considered first.

119 Ashley & Martin argues that part of the front page acknowledgment is excluded from review, that is, the clause:

I [insert name] the undersigned acknowledge my agreement to undertake and pay for the program of treatment recommended by Ashley & Martin Pty Ltd. You must pay in full the RealGROWTH Treatment program.

120 Ashley & Martin also argues that the following sentence from under the heading 'Order, Delivery and Payment' is excluded from review:

The Medical Treatment Program will set out the applicable Hair Loss Goods and Hair Loss Services and the time for delivery of the Hair Loss Goods and Hair Loss Services by us to you.

121 Ashley & Martin submits that the ACCC's complaint as to unfairness centres on the point at which the patient is contractually bound and when a patient will see a doctor; that the point of being contractually bound is when the subject matter is defined and the upfront price is set; that it follows that the ACCC challenges the core of the bargain and the way that it must be performed; and that s 26 prevents that challenge.

122 In my view, and having regard to the manner in which I consider s 26 operates, those terms to which Ashley & Martin refers do not fall within the ambit of s 26. It is important to remember that s 26 only protects terms 'to the extent, but only to the extent' that the term defines the subject matter of the contract or sets the upfront payment. An assessment of terms that considers only whether they relate to the price or subject matter will necessarily be incomplete. The terms or parts of the relevant terms are to be more precisely identified: they must define the subject matter or set the upfront price.

123 In this case, the main subject matter of the Contract is defined by the description of the Medical Treatment Program set out on the first page. The products and services are listed with a note immediately beneath them that states 'The items indicated by your consultant constitute your current Ashley & Martin program'. What is being purchased is the 'program of treatment recommended by Ashley & Martin'. There can be no complaint as to the content of those goods and services on the basis of unfairness. But nor does the ACCC make that complaint.

124 To the extent Ashley & Martin asserts protection of the second sentence referred to above, it refers to the 'applicable' goods and services. They are defined on the first page. The sentence of itself does not define or add to the definition of the main subject matter. It directs attention to the Medical Treatment Program itself. Nor do I consider the inclusion of a reference to the time of delivery comprises part of the main subject matter of the contract. There may well be cases where delivery comprises the main subject matter, but in these Contracts there is not the emphasis on a delivery timetable that one might expect to see if it was integral to the subject matter.

125 The first of the two sentences Ashley & Martin asserts are protected comprises an operable term confirming an obligation to pay, but the price to be paid is set by the upfront disclosure of the relevant total cost. By s 26, there is no capacity to argue the price as set is unfair within the meaning of s 23.

126 Ashley & Martin does not argue that any of the other costs or payments, for example the obligation to make termination payments, fall within the upfront price. This is not an occasion to consider the potentially difficult questions as to the scope of an upfront price that I touched upon above, such as whether certain fees or charges might form part of a package that comprises an upfront price or whether charges are by their nature contingent within the meaning of the relevant definition.

127 In this case the ACCC makes no complaint that the prices set out on the first page of the Contracts or the description of the goods and services to be provided are unfair. The ACCC's position is that objectively the Contracts are clearly contracts to supply identified medications and other products and services in return for a specified amount of money. The parts of the terms that define what is to be supplied and set how much it will cost on the first page of the Contract are unchallenged.

Are the terms of the First Contract unfair (s 24 definition)

128 It is then necessary to assess whether the impugned terms are unfair. It is appropriate at this point to determine the question of whether Ashley & Martin's overarching 'no obligation' submission can be sustained.

129 Ashley & Martin submits that the Contracts, properly construed, create no obligation on the patients to sign before seeking advice from a doctor. It submits that the patient may choose to first see the doctor if they wish to do so. No evidence as to such a practice nor any examples were referred to.

130 I accept that there is nothing on the face of the Contract that goes so far as to expressly require the patient to execute the Contract before seeing the Ashley & Martin doctor. But the unfairness of the terms of the Contract is to be construed having regard to both construction and context: MyBudget at [69].

131 The following are relevant:

(a) nothing on the first page of the Contract informs the question of the timing of medical advice. There is no suggestion that the obligation to undertake and pay for the Medical Treatment Program is conditional upon or takes effect only upon confirmation from a doctor as to the suitability of the program;

(b) there are various terms in the second page fine print Terms and Conditions that are consistent with a chronology that involves execution prior to medical advice. For example, under the heading 'Background and application' it is provided that 'You [the patient] may request us to advise you in relation to a Medical Treatment program in writing or by other means'. That anticipates advice post execution;

(c) it is said that the Medical Treatment Program will include pharmaceutical products, but that supply is conditional upon medical advice: implicit in those terms is an assumption that no advice has been received prior to execution of the contract as to whether or not such products should be included. If adverse advice had been received about a product prior to execution, it is unlikely the consultant would include it in any Medical Treatment Program to start with;

(d) the refund clause anticipates that the purchase of the program components precedes receipt of 'subsequent' medical advice and makes little sense if medical advice is received in advance; and

(e) the termination clauses quite clearly refer to acceptance of the Medical Treatment Program preceding the consultation with the medical doctor, as discussed at [112] above.

132 Therefore, it can be seen that the terms of the Contract anticipate and assume in various places that execution precedes the provision of medical advice.

133 As to context, the patients are encouraged to attend the first consultation with finances in place. The checklist provided at the initial consultation addresses medical history. The consultant identifies the components of the Medical Treatment Program including the pharmaceutical components at the first consultation: apparently it is not necessary from the consultant's perspective that there be medical advice provided by a doctor before the consultant is in a position to select the appropriate components (taking into account the checklist information, one assumes). The consultant is able to proceed regardless.

134 Moreover, it is agreed by Ashley & Martin that the Contract is generally executed by patients at their first consultation and that an appointment with a doctor post-dates that consultation. Furthermore, the circumstances of the first consultation as described are consistent with an assumption that medical advice has not been received. So that is the relevant context in which the Contract is executed, even allowing for the fact that sometimes the circumstances may be different.

135 Therefore, I do not accept Ashley & Martin's submission to the effect that the unfairness assessment should proceed on the basis that patients are not obliged to take on the obligations provided by the Contract without first seeking medical advice. That submission does not reflect the tenor of the contractual terms and it does not reflect the agreed predominant circumstance in which a patient in fact incurs such liability (the initial consultation that precedes a doctor's appointment).

136 I also note that whilst for the purpose of this submission Ashley & Martin seeks to downplay the relevance of the course of conduct by which the Contract is signed at the initial consultation and products are supplied, it in fact relies on such conduct for other purposes. In the context of seeking to establish that the termination payments are reasonably necessary to protect its legitimate interests, Ashley & Martin relies on the fact that it supplies products and services at the initial consultation (addressed in detail below).

137 Having rejected the 'no obligation' submission as to construction of the Contracts, the consideration of the impugned terms proceeds on the basis that a patient signs a Contract before receiving and considering medical advice. I also note that whilst I will deal with the significant imbalance and detriment limbs separately, there is inevitably some overlap in the matters that might inform those matters.

138 In my view the regime provided under the First Contract imposes on the patient a disadvantageous burden or risk, that being a requirement that the patient enter into a Contract in circumstances where they do not have the opportunity to make an informed or real choice.

139 A person should not commit to medical treatment without informed consent, and such consent will not be informed until they have spoken to a doctor and received advice as to risks and suitability. Whilst that would seem hardly controversial, the significance of informed consent is reflected in the authorities.

140 In Rogers v Whitaker (1992) 175 CLR 479, the Court held at 489:

There is a fundamental difference between, on the one hand, diagnosis and treatment and, on the other hand, the provision of advice or information to a patient. In diagnosis and treatment, the patient's contribution is limited to the narration of symptoms and relevant history; the medical practitioner provides diagnosis and treatment according to his or her level of skill. However, except in cases of emergency or necessity, all medical treatment is preceded by the patient's choice to undergo it. In legal terms, the patient's consent to the treatment may be valid once he or she is informed in broad terms of the nature of the procedure which is intended. But the choice is, in reality, meaningless unless it is made on the basis of relevant information and advice.

(citations omitted)

141 In Chappel v Hart [1998] HCA 55; (1998) 195 CLR 232, the Court held at [65]:

The nature and purpose of a duty with the content established in Rogers v Whitaker concern the right of the patient to know of material risks which are involved in undergoing or forgoing certain treatment. This, in turn, arises from the patient's right to decide for himself or herself whether or not to submit to the treatment in question. That choice 'is, in reality, meaningless unless it is made on the basis of relevant information and advice'.

(citations omitted)

142 The execution of a contract prior to receipt of medical advice is not necessarily of itself unfair. For example, the terms of the contract may include a cooling off period. The patient's obligations under the contract may be conditional upon the receipt and nature of medical advice. There are mechanisms whereby the interests of the patient might still be fully protected.

143 That is not so in this case.

144 In this case, the contractual regime between patients and Ashley & Martin is such that the patients commit to the program and to payment before seeing a doctor. They receive a long-term supply of non-prescription goods prior to meeting with the doctor. Once they see a doctor and have the opportunity to consider the risks they may not wish to proceed. The doctor may decline to prescribe integral components of the program, being the relevant prescription products, on the basis that they are not suitable for the patient. The patient is left with products that they may never use, as they no longer form part of a Medical Treatment Program designed for the patient. Absent the prescription drugs, the Medical Treatment Program is incomplete. They have been informed by the Contract that they should follow the Medical Treatment Program faithfully: and in any event there was no suggestion a program absent key components would be a program of value to patients.

145 Whether the Contract is unfair will depend on how it responds in such scenarios.