FEDERAL COURT OF AUSTRALIA

Commonwealth of Australia v Essendon Airport Pty Ltd [2019] FCA 1411

ORDERS

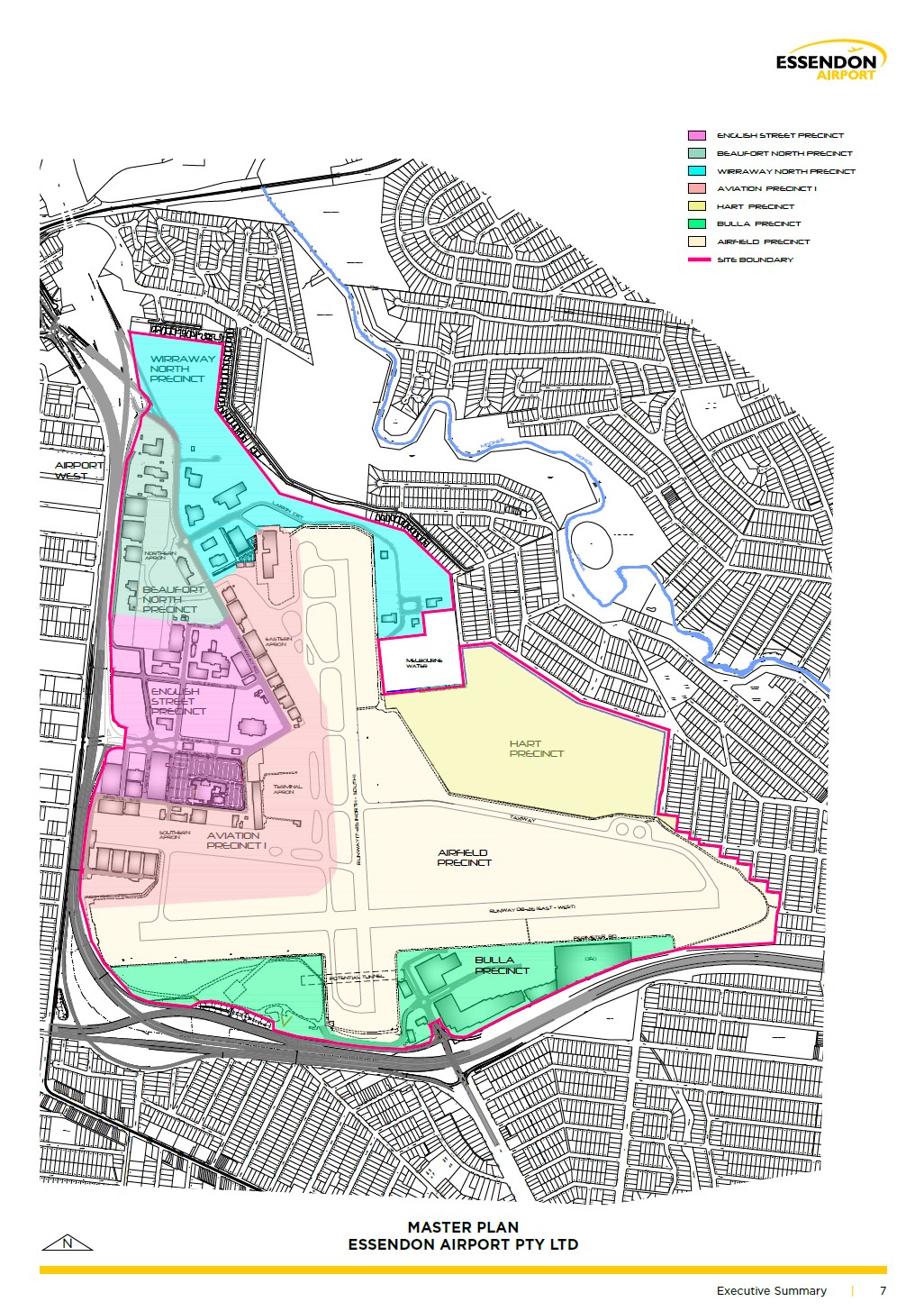

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties have 14 days to agree upon the form of final relief to give effect to the reasons for judgment or, failing that, to file submissions of no more than five pages concerning the orders the Court should make.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

STEWARD J:

1 In June 1998, the Commonwealth of Australia (the “Commonwealth”), as the owner of land, entered into a 50-year lease agreement (the “Lease”) with the respondent (“EAPL”), an entity then wholly owned by the Commonwealth. The land leased comprises the site of Essendon Airport (the “Airport Site”). It includes areas devoted to aviation, such as runways and aprons, and areas devoted to, or available to be used for, other commercial uses, such as shops. EAPL was effectively privatised in 2001. Before me the parties dispute the meaning and application of a clause in the Lease which obliges EAPL to make an annual payment to the Commonwealth “in lieu of land tax at the relevant State rate”. Each sought declaratory relief concerning how to calculate that payment.

Facts

2 There were no disputed facts. The parties, to their credit, prepared a statement of agreed facts which I adopt. It is Annexure “A” to these reasons.

3 There was no dispute about the identification of the land in issue, or that it was divided into different precincts. A diagram of the land was annexed to the submissions of the Commonwealth. It is Annexure “B” to these reasons. Most of the Airport Site is contained within a single certificate of title (302.30 hectares) (the “Main Airport Title”). The balance of 1.736 hectares is contained within 16 certificates of title. It was not disputed that parts of the Main Airport Title were divided into seven precincts and were used for two principal purposes, namely for aviation and for other commercial uses.

4 Because the land in issue is owned by the Commonwealth, land tax in respect of it was not payable when the Land Tax Act 1958 (Vic) (“1958 Land Tax Act”) was in force, and is still not payable under the present Land Tax Act 2005 (Vic) (“2005 Land Tax Act”).

The Grant of the Lease

Statutory Context

5 Before turning to the clause in dispute, I should set out some relevant contextual matters. The grant of the Lease was authorised by s 21 of the Airports (Transitional) Act 1996 (Cth) (the “Transition Act”). Section 3 of that Act describes relevantly the regulatory context in which the Lease was granted. It states as follows:

Simplified outline

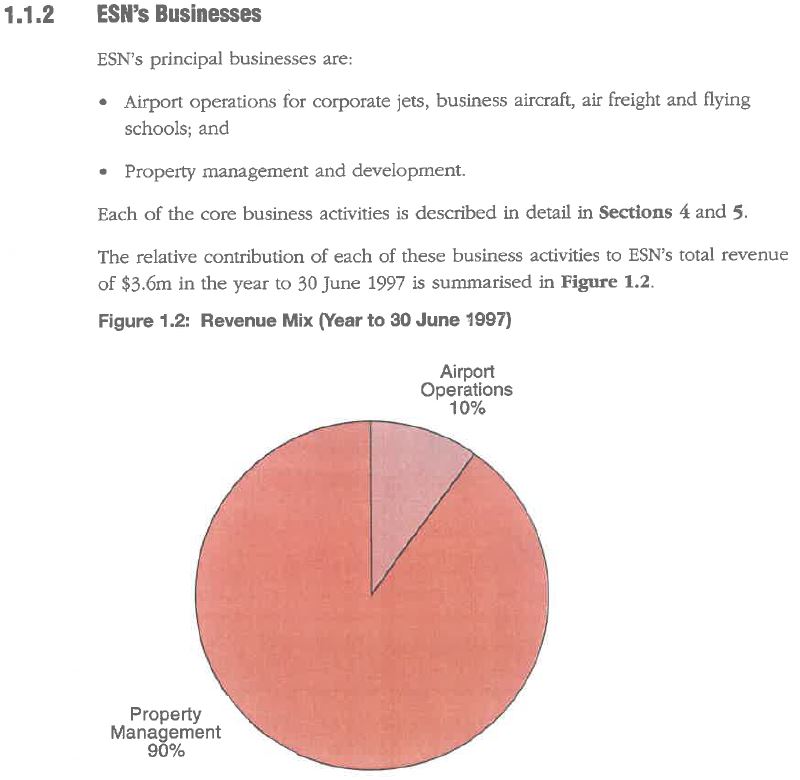

The following is a simplified outline of this Act:

• This Act provides for the leasing of certain airports.

• Airport land and other airport assets will be transferred from the Federal Airports Corporation (FAC) to the Commonwealth.

• The Commonwealth will grant an airport lease to a company. The company is called an airport-lessee company.

• Immediately after the grant of the airport lease, the Commonwealth may transfer or lease certain assets to the airport-lessee company.

• Certain employees, assets, contracts and liabilities of the FAC will be transferred to the airport-lessee company.

6 The Transition Act provided for the lease of airport sites to both Commonwealth-owned companies and privately owned companies. In the case of leases to Commonwealth-owned companies, provision was also made for the sale of shares in those companies to new owners. Section 21 of the Transition Act relevantly provides:

Commonwealth may grant airport lease to a Commonwealth‑owned company

(1) The Commonwealth may grant an airport lease under this section.

(2) The Commonwealth must not grant an airport lease under this section unless the lessee is a company all of whose shares are beneficially owned by the Commonwealth.

(3) If a purported lease contravenes subsection (2), it is of no effect.

Note: In addition to the requirements of subsection (2), a grant must comply with the rules in Part 2 of the Airports Act 1996.

7 The “rules in Part 2 of the Airports Act 1996” are described below. The term “airport lease” is defined by reference to its meaning in the Airports Act 1996 (Cth) (the “Airports Act”). Section 5(1) of that Act relevantly provides:

airport lease:

(a) means a lease of the whole or a part of an airport site, where the Commonwealth is the lessor; and

(b) when used in relation to an airport—means a lease of the whole or a part of the airport site of the airport, where the Commonwealth is the lessor.

The term “airport site” is also defined by the Airports Act as follows:

airport site means a place that is:

(a) declared by the regulations to be an airport site; and

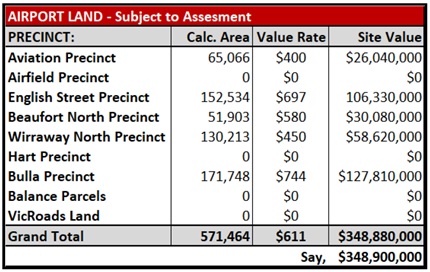

(b) a Commonwealth place; and

(c) used, or intended to be developed for use, as an airport (whether or not the place is used, or intended to be developed for use, for other purposes).

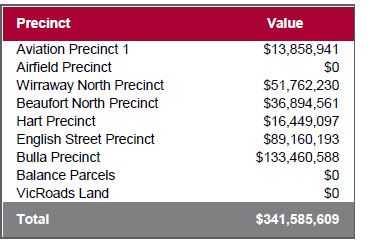

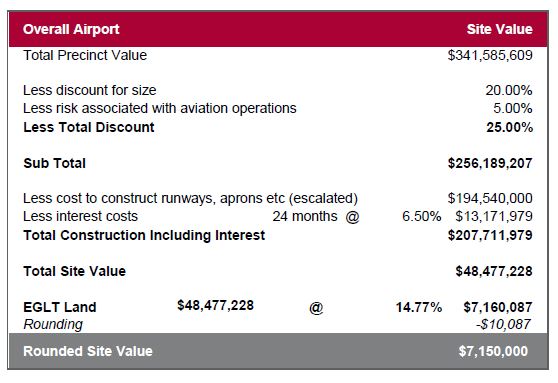

Note: The boundaries of an airport site are ascertained in accordance with the regulations.

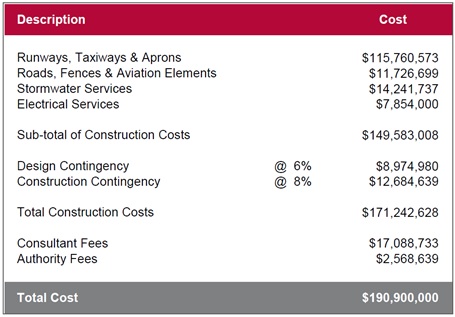

8 Section 22 of the Transition Act gives the Commonwealth the power to grant leases over airport sites to privately owned companies. It is in these terms:

Commonwealth may grant airport lease to a company that is not owned by the Commonwealth

(1) The Commonwealth may grant an airport lease under this section.

(2) The Commonwealth must not grant an airport lease under this section unless the lessee is a company none of whose shares are beneficially owned by the Commonwealth.

(3) If a purported lease contravenes subsection (2), it is of no effect.

Note: In addition to the requirements of subsection (2), a grant must comply with the rules in Part 2 of the Airports Act 1996.

9 Part 6 of the Transition Act contains rules for the sale of shares in an airport-lessee company owned by the Commonwealth. As already mentioned, the shares in EAPL were transferred by the Commonwealth in 2001 when the Airport Site was privatised.

10 Section 3 of the Airports Act records the objects of that Act as follows:

Objects

The objects of this Act are as follows:

(a) to promote the sound development of civil aviation in Australia;

(b) to establish a system for the regulation of airports that has due regard to the interests of airport users and the general community;

(c) to promote the efficient and economic development and operation of airports;

(d) to facilitate the comparison of airport performance in a transparent manner;

(e) to ensure majority Australian ownership of airports;

(f) to limit the ownership of certain airports by airlines;

(g) to ensure diversity of ownership and control of certain major airports;

(h) to implement international obligations relating to airports.

11 Section 4 of the Airports Act sets out a simplified outline for the leasing of airport sites which again provides useful regulatory context. Relevantly, at the time when the parties entered into the Lease, a Commonwealth-owned airport could only be leased to a company; there could be only one airport-lessee company for each airport; the “sole business” of the airport-lessee company had be the running of the airport; and each airport required an airport master plan and major development plans for significant developments.

12 Sections 13 and 14 are contained in Pt 2 of the Airports Act. Section 13 empowers the Commonwealth to grant an “airport lease”. Section 14 prescribes rules about airport leases, which apply to the Lease before me (because it is an “airport lease” as defined: see also the note to s 21 of the Transition Act). It is in the following terms:

Rules about airport leases

Grant

(1) The Commonwealth must not grant an airport lease unless the lease complies with subsection (5).

Variation

(2) An airport lease must not be varied unless the varied lease complies with subsection (5).

Transfer

(3) The Minister must not approve the transfer of an airport lease unless the transferred lease complies with subsection (5).

Contravention

(4) If a purported grant, variation or approval contravenes this section, it is of no effect.

Rules about airport leases

(5) An airport lease complies with this subsection if:

(a) there is a single lessee; and

(b) the lessee is a qualified company; and

(c) the term of the lease is not longer than 50 years (with or without an option to renew the lease for up to 49 years); and

(d) if the airport is neither a joint-user airport nor Sydney West Airport—the lease provides for the use of the site as an airport (whether or not the lease also provides for other uses); and

(e) if the airport is a joint-user airport—the lease provides for the use of the leased area for purposes in connection with the airport (whether or not the lease also provides for other uses); and

(f) if the airport is Sydney West Airport—the lease provides for the development of the site as an airport or the use of the site as an airport, or both (whether or not the lease also provides for other developments or other uses); and

(g) the lease provides for access to the airport by interstate air transport or international air transport, or both (whether or not the lease also provides for other access).

13 Division 3 of Pt 5 of the Airports Act sets out detailed rules for the preparation of a “final master plan” for each airport. Through the enactment of the Airports Amendment Act 2007 (Cth), Parliament clarified that such a plan must establish, amongst other things, the strategic direction of the relevant airport and “to provide for the development of additional uses of the airport site”.

14 Section 32 of the Airports Act prescribes the activities that may be undertaken by a lessee that is an airport-operator company (as EAPL is here). It provides in subs (1) as follows:

Airports other than joint-user airports

(1) An airport-operator company for an airport (other than a joint-user airport) must not carry on substantial trading or financial activities other than:

(a) activities relating to the operation and/or development of the airport; or

(b) activities incidental to the operation and/or development of the airport; or

(c) activities that, under the regulations, are treated as activities incidental to the operation and/or development of the airport; or

(d) activities that are consistent with the airport lease for the airport and the final master plan for the airport.

15 The foregoing review of the legislative scheme highlights the centrality of the operation and/or development of an airport on the land the subject of a lease granted under the Airports Act. That being said, the legislative scheme expressly made clear that the lease could make provision for other uses of the airport site such as carrying on trading or financial activities.

Contextual documents

16 A contextual document, principally relied upon by the Commonwealth, was the Competition Principles Agreement entered into by the Commonwealth and the States in 1995 (the “1995 Agreement”). Clause 3 of that Agreement was relevantly in the following form:

Competitive Neutrality Policy and Principles

3.(1) The objective of competitive neutrality policy is the elimination of resource allocation distortions arising out of the public ownership of entities engaged in significant business activities: Government businesses should not enjoy any net competitive advantage simply as a result of their public sector ownership. These principles only apply to the business activities of publicly owned entities, not to the non-business, non-profit activities of these entities.

…

(4) Subject to subclause (6), for significant government business enterprises which are classified as “Public Trading Enterprises” and “Public Financial Enterprises” under the Government Financial Statistics Classification:

(a) the Parties will, where appropriate, adopt a corporatisation model for these government business enterprises (noting that a possible approach to corporatisation is the model developed by the inter-governmental committee responsible for GTE National Performance Monitoring); and

(b) the Parties will impose on the Government business enterprise:

(i) full Commonwealth, State and Territory taxes or tax equivalent systems;

…

17 It was said that the clause in dispute here, which provides for the making of payments in lieu of land tax, was the product of the foregoing clause in the 1995 Agreement. It was submitted that the purpose of the clause in dispute was to ensure that a Commonwealth-owned entity (which EAPL was originally) did not enjoy the competitive advantage of not paying land tax because it operated on Commonwealth land when engaged in business activities. It therefore needed to make payments which were equivalent to land tax: Helicopters Pty Ltd v Bankstown Airport Ltd [2010] NSWCA 178 at [7] per Handley AJA. Of course, EAPL is no longer government owned. Whether this possible rationale for the clause in dispute has any bearing on the constructional issues the Court faces may be doubted. For one thing, I am satisfied that when the Lease was entered into, the privatisation of EAPL was planned and expected. Even if applicable, it does not resolve the particular dispute here between the parties.

18 I have found to be of more assistance two further contextual documents. The first is a document entitled “Phase 2 Federal Airports General Information Memorandum”. It was dated November 1997 and was issued by the Commonwealth. In this document the government announced its intention to sell Essendon Airport as a “non-core regulated airport”, together with a number of other airports, by either freehold sale or “on a leasehold basis under the Airports (Transitional) Act”.

19 The second was entitled “Phase 2 Federal Airports Essendon Airport Information Memorandum” (the “Essendon Airport Memorandum”). It was also issued by the Commonwealth in November 1997. It is specific to Essendon Airport. It described the principal business being undertaken at that airport in the following way:

20 The foregoing supports the finding, which I make, that there were two principal business operations being undertaken at Essendon Airport at the time the Lease was entered into: aviation and property management. As the diagram set out above demonstrates, 90% of the income was generated from property management. That property business was described in the Essendon Airport Memorandum in the following way:

1.2.3 Property Development and Management

Essendon airport has approximately 86 hectares of undeveloped land. Land is available for both aviation and non-aviation development for which ESN [(refers to the Federal Airports Corporation in the context of its commercial, legal and operational activities carried out in connection with Essendon airport)] has an indicative land use concept plan.

Previous uncertainty surrounding the future of the airport led to restrictions on airport management entering into medium to long term leases and developing the site. Therefore whilst the airport may not have been able to be developed to its full potential, these circumstances provide a greater degree of flexibility for a new owner to plan and develop the site as a whole.

A building “recycling” program has resulted in buildings which were previously vacant being improved and leased for commercial purposes. Potential exists to continue with this program by further upgrading buildings.

Essendon airport’s location and substantial amount of serviced and unserviced land makes it suitable for further commercial development.

21 The Essendon Airport Memorandum described the assets of the airport as including runways, taxiways, navigation aids, aprons, a main terminal building, hangars, refuelling facilities, a control tower, car parks and roads. It also had, at the time, 95 other general buildings and 86 hectares of undeveloped land. The non-aviation property was described in the Essendon Airport Memorandum as follows:

5.3.2 Non-aviation Related Property

Buildings range in size up to approximately 10,000 square metres and are up to two or three storeys in height, with a number having multiple tenancies. Many were constructed in the 1940s, 1950s and the 1960s. Following the staged relocation of the airlines to Melbourne airport, ESN has converted many of the buildings, or permitted tenants to convert them, for non-aviation uses. These activities include computer sales and service, gymnastics youth club, dentist, health food distribution, medical practice, equipment storage and maintenance, olive and pasta food preparation and distribution, plumbing and airconditioning maintenance, processing and export of live seafood, road transport and freight distribution and wine mail order import and sales business.

Land leased by non-aviation related tenants is situated in various areas of the airport. The more significant activities of these tenants include mobile telecommunications monopoles, storage of new motor vehicles, produce and stockfeed warehouse, import and sales of off-road, snow and water recreational vehicles, Sunday market, bus storage and nursery regeneration and growth area.

The airport also has two large outdoor advertising hoardings located along the western perimeter.

22 The Essendon Airport Memorandum also described the business potential to develop the non-aviation business in the following terms:

5.4.1 Location and Availability of Land

Essendon airport is located to the north-west of Melbourne and is surrounded by industrial, commercial and residential property. The airport has land available for both aviation and non-aviation development and, accordingly, ESN has developed an indicative land use concept plan. The Essendon Airport Chamber of Commerce has also produced its own Development Plan dated September 1996, which the Chamber is willing to make available to potential bidders.

…

5.4.3 Non-Aviation Related Property

Essendon airport’s location and substantial amount of serviced and unserviced land make it suitable for further commercial development.

A building “recycling”, program has resulted in buildings which were previously vacant being improved and leased for commercial purposes. Potential exists to continue with this program by further upgrading buildings.

Other activities such as leasing of sites for outdoor advertising are means by which the airport has obtained revenue.

23 Finally, I should note that the Essendon Airport Memorandum also disclosed “Proforma Profit and Loss Statements” for the 1993 to 1997 years, and other financial data. These disclosed that, in the 1997 year, revenue from the aeronautical part of the business was $366,000 and revenue from “property” was $3,250,000. Total operating expenses before maintenance and depreciation amounted to $1,671,000. These figures show how much more profitable the non-aviation business was when compared to the aviation business.

The Lease

24 I now turn to consider the terms of the Lease. The clause in dispute, which is cl 26.2(b), is in these terms:

26.2 Ex Gratia payment in lieu of Rates and Land Tax

…

(b) Where Land Tax is not payable under sub-clause 26.1 because the Airport Site is owned by the Commonwealth, payments in lieu of Land Tax must be made by the Lessee in respect of those parts of the Airport Site:

(i) which are sub-leased to tenants; or

(ii) on which trading or financial operations are undertaken including, but not limited to, retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes,

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from making payments by Commonwealth policy or law. Unless otherwise directed by the Lessor, the Lessee will make payments promptly in lieu of land tax at the relevant State rate to the Commonwealth addressed as provided for in sub-clause 24.1.

These payments in lieu of Land Tax will be levied on a financial year basis. The Lessee must submit an assessment of the payment in lieu of land tax to the Commonwealth on 31 August of the current financial year with this payment due 30 days later. Land value assessment for the purposes of making payments in lieu of land tax are required at least every three years.

25 What divides the parties before me is how to calculate the payment to be made “in lieu of Land Tax” in respect of “those parts” of the Airport Site identified by cl 26.2(b) (which I will refer to as “those parts” or the “exigible land”). The exact difference between the parties is explained in these reasons when I describe below the expert evidence. There is a subsidiary dispute about which car parks are included in “those parts” of the Airport Site.

26 Other clauses in the Lease relevant to the disposition of this matter are set out below.

27 Clause 2.1 contains the following definitions which are relevant:

‘Airport Site’ means the site (including the Structures thereon) which at Grant Time is named Essendon Airport and the boundaries of which are as specified in regulations made pursuant to the Airports Act, a copy of which regulations is attached to this Lease.

‘Governmental Authority’ means the Commonwealth government or any government of any State or Territory of Australia, administrative body, governmental body, department or agency of any such government or local government authority.

‘Land Tax’ means any tax levied or imposed by a Governmental Authority on land.

‘Master Plan’ means a final master plan as defined in the Airports Act.

I note that the definition of “Airport Site” describes that land by reference to a series of Victorian certificates of title.

28 Clause 2.2(i) is in these terms:

a reference to legislation includes statutes, regulations, ordinances, by-laws or other legislative instruments and all amendments, consolidations or replacements thereof;

29 Clause 3.1 imposes an obligation on the lessee to use the Airport Site as an airport. It is in these terms:

Lessee must give access

The Lessee:

(a) must at all times:

(i) subject to sub-clause 19.5, provide for the use of the Airport Site as an airport;

(ii) subject to sub-clause 19.5, provide for access to the airport by interstate air transport;

(iii) provide for access to the airport by intrastate air transport;

(iv) not use, or permit to be used, the Airport Site for any unlawful purpose or in breach of legislation; and

(v) not use any name other than Essendon Airport for the Airport Site without the prior written consent of the Lessor;

(b) may:

(i) permit the Airport Site to be used for other lawful purposes that are not inconsistent with its use as an airport; and

(ii) subject to sub-clause 5.10 and clause 14, construct, alter, remove, add to or demolish the Structures.

30 Clause 13.1 provides:

Development of airport site

Throughout the Term the Lessee must develop the Airport Site at its own cost and expense having regard to:

(a) the actual and anticipated future growth in, and pattern of, traffic demand for the Airport Site;

(b) the quality standards reasonably expected of such an airport in Australia; and

(c) Good Business Practice.

31 Clause 13.3 provides:

Provision of plan to Lessor

(a) Subject to sub-clause 13.8, within 120 Business Days of the receipt of a written notice under sub-clause 13.2 the Lessee must provide the Lessor with a plan required to bring the Airport Site up to a standard consistent with that required by sub-clause 13.1 within 5 years.

(b) The relevant plan must contain at least the equivalent detail to that required of a major development plan under section 91 of the Airports Act. For the avoidance of doubt any plan lodged by the Lessee with the Lessor under this clause 13 will not constitute a major development plan or master plan for the purposes of the Airports Act.

32 Clause 26.1 is in these terms:

Payment of Rates and Land Tax and Taxes

The Lessee must pay, on or before the due date, all Rates, Land Tax and Taxes without contribution from the Lessor.

33 A payment in lieu of land tax is not the only equivalent tax payment EAPL is obliged to make under the Lease. By cl 26.2(a) payments equivalent to an amount payable for rates must be paid to a relevant governmental authority. Clause 26.2(c) is another example of this type of obligation. It is in the following terms:

Where Taxes such as stamp duty, payroll tax, financial institutions duty and debits tax imposed by a Governmental Authority are not payable by the Lessee because they are Taxes on transactions, instruments or activities on or related to the Airport Site owned by the Commonwealth, the Lessee must pay to the relevant Governmental Authority such amount as is equivalent to the amount which would be payable for such Taxes if such Taxes were leviable or payable.

34 No “Airport Master Plan” of the kind referred to in the Essendon Airport Memorandum was before me which pre-dated the Lease, or was made at the same time as the Lease. Instead, the Commonwealth relied upon a Master Plan prepared in 2013 to describe the activities which take place at the Airport Site. I have placed no weight on the contents of this Master Plan for the purposes of construing the Lease as it post-dates by about 15 years the entry into of the Lease: Agricultural and Rural Finance Pty Ltd v Gardiner (2008) 238 CLR 570 at 582 [35] per Gummow, Hayne and Kiefel JJ; Brambles Holdings Ltd v Bathurst City Council (2001) 53 NSWLR 153 at 164 [26] per Heydon JA (as his Honour then was).

Expert Evidence

35 Each of the Commonwealth and EAPL relied upon expert valuations for the purpose of calculating the payment that must be made “in lieu of land tax” in respect of “those parts of the Airport Site” specified by cl 26.2(b) of the Lease. The Commonwealth relied upon an expert report of Mr Cations of Property Dynamics Independent Property Advisers Pty Ltd which concluded that “those parts” had a value of $348,900,000 (rounded). EAPL relied upon an expert report of Mr Brown of m3property (Vic) Pty Ltd which concluded that “those parts” had a value of $7,150,000. In my view, both experts were well qualified to give their respective opinions about the value of “those parts”.

36 A joint “statement of experts” was before me which had been prepared by each expert. It recorded that the experts agreed upon the following matters:

i) Land Description, Title Details, Planning Details

The valuers largely agree on the important facts surrounding the overall description of Essendon Fields including the land area, title description, lease particulars and planning controls. This includes the Essendon Airport Master Plan 2013 which is the key document relating to planning at the Airport. As a general principle, both valuers agree (largely) on the buildings which were erected on the land having regard to the date of valuation.

ii) The valuers agree on the date of valuation being 1 January 2016 with regard being had to all occupied (sub leased) land at 30 June 2016.

iii) The valuers agree the legislation requires the land to be considered as fee simple ignoring any leases (e.g. head lease and sub leases).

iv) The valuers agree that in the above consideration of freehold land the requirement to operate an airport would be a covenant on title as described in the lease.

v) The valuers agree the identified sub leased land as at 30 June 2016 should be the subject of valuation.

vi) The valuers note the area of EGLT [(ex-gratia payments in lieu of land tax)] land varies between the two reports. Applicant area 57.1464 hectares (571,464 square metres) and Respondent 44.8997 hectares (448,997 square metres). The valuers have identified the major area of difference is in the Bulla Precinct. There are other minor differences. It hasn’t been possible to resolve this matter in the time allocated for the preparation of this report …

The Commonwealth’s valuation

37 In essence, Mr Cations was instructed to determine the “site value” of “those parts” of the Airport Site without taking into account the value of the balance of the Airport Site. He was, for that purpose, to have regard to the Valuation of Land Act 1960 (Vic) (the “VLA”) and the 2005 Land Tax Act. He defined the term “site value” by reference to its meaning in s 2 of the VLA which provides as follows:

site value of land, means the sum which the land, if it were held for an estate in fee simple unencumbered by any lease, mortgage or other charge, might in ordinary circumstances be expected to realise at the time of the valuation if offered for sale on such reasonable terms and conditions as a genuine seller might be expected to require, and assuming that the improvements (if any) had not been made;

The requirement in this definition to assume that the improvements on the Airport Site have not been made, together with the obligation on EAPL to operate the airport, drove the dispute before me. The parties did not agree on which improvements to consider.

38 Mr Cations valued each individual precinct falling within “those parts” identified by cl 26.2(b) and then aggregated those values (the identification of these precincts was not disputed). His conclusion was summarised in the joint expert report in the following way:

39 Mr Cations made no adjustments to these values. Critically, he made no adjustment for any requirement to operate an airport because each “parcel” set out above was considered by him to be “stand-alone” and not part of the rest of the Airport Site for the purposes of valuation under cl 26.2(b).

EAPL’s valuation

40 Mr Brown took a different approach. He valued the entire Airport Site which had been leased, including the land on the Main Airport Title (302.30 hectares). This resulted in the following conclusion:

41 Mr Brown then made a series of adjustments. He applied a 20% discount “to reflect the bulk nature of the combined landholding”. No real criticism was made about this adjustment. Mr Brown applied another discount of 5% for the risk of operating the airport. That is because Mr Brown assumed that the owner of “those parts” was required to operate Essendon Airport (consistently with the terms of the Lease). He then made another adjustment which followed from the presence of that obligation and the necessity of ascertaining the unimproved value of the land. This is the adjustment that really divided the parties. Mr Brown determined that, assuming the site was vacant, any potential purchaser would need to reduce the value of the entire Airport Site as leased to EAPL by the cost of fulfilling the obligation to operate an airport: that is, for the cost of constructing the necessary airport infrastructure. His conclusion about that cost was as follows:

42 He then added to that cost, interest of $13,171,979 and arrived at a figure of $207,710,000 (rounded). He reduced his valuation by these adjustments and concluded that the site value of the leased land was $48,477,228. Because “those parts” of that leased land comprised 14.77% of the whole “Airport Site”, the value of “those parts” was $7,160,087. Mr Brown’s calculations are summarised in the following table:

43 In determining that site value, Mr Brown relied upon s 22 of the 2005 Land Tax Act, which is in the following terms:

Taxable value of parts of land not separately valued

(1) This section applies if—

(a) it is necessary to determine the taxable value of part of land (the part) for or in a tax year; and

(b) the part was not valued separately as at the relevant date (within the meaning of section 19) in relation to that year; and

(c) the whole land was valued separately as at the relevant date.

(2) The taxable value of the part is the same proportion of the taxable value of the whole land as the area of the part bears to the area of the whole land.

44 I should note that the Court was not asked to determine whether the precise values identified by each valuer was or was not correct. The values so identified merely served the purpose of illustrating the different approach for which each party contended. The Court makes no comment about their respective accuracy.

The Contentions of the Parties

45 The parties agree upon what “parts” of the Airport Site are to be valued (subject to the issue about car parks); they disagree about how to determine that value. Critically, EAPL says that the 2005 Land Tax Act requires a determination and valuation of land comprised in a certificate of title, and then an allocation of that value to the identified “parts” propositionally in accordance with s 22. In that respect, and practically, EAPL’s real focus was on the certificates of title comprising the overall landholding of the Airport Site (most importantly the land covered by the Main Airport Title and also the adjoining ancillary land covered by the very much smaller other certificates of title). The Commonwealth disagrees. It submits that the approach adopted by EAPL procures a “depressed site value” as it reduces the high value of “those parts” of the Airport Site by aggregating it with the low value land which is not exigible pursuant to cl 26.2(b). It says one does not start with the value of the land comprising the entire Airport Site, including the Main Airport Title, because the parties agreed that the payments in lieu of land tax were confined to land comprising “those parts” of the Airport Site prescribed by cl 26.2(b) and no more. Implicitly, but for the obligation to operate an airport and the need then to ascertain the unimproved value of land, the Commonwealth may not have objected to EAPL’s methodology.

Principles of construction

46 The parties agree upon the principles to be applied in construing the Lease. They were helpfully summarised in the Commonwealth’s written submissions as follows:

The rights and liabilities of parties under a provision of a contract are determined objectively, by reference to its text, context, including the entire text of the contract as well as any contract, document or statutory provision referred to in the text of the contract, and purpose.

In determining the meaning of the terms of a commercial contract, it is necessary to ask what a reasonable businessperson would have understood those terms to mean. That enquiry will require consideration of the language used by the parties in the contract, the circumstances addressed by the contract and the commercial purpose or objects to be secured by the contract.

Ordinarily, this process of construction is possible by reference to the contract alone. Indeed, if an expression in a contract is unambiguous or susceptible of only one meaning, evidence of surrounding circumstances (events, circumstances and things external to the contract) cannot be adduced to contradict its plain meaning.

Although the process of construction is ordinarily possible by reference to the contract alone, it may be necessary to have recourse to events, circumstances and things external to the contract in two situations:

(i) in identifying the commercial purpose or objects of the contract where that task is facilitated by an understanding “of the genesis of the transaction, the background, the context [and] the market in which the parties are operating”; and

(ii) in determining the proper construction where there is a constructional choice.

Each of the events, circumstances and things external to the contract to which recourse may be had is objective. Evidence of the parties’ statements and actions reflecting their actual intentions and expectations is inadmissible.

Finally, a commercial contract should be construed so as to avoid it “making commercial nonsense or working commercial inconvenience”.

(Footnotes omitted.)

Citing Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd (2015) 256 CLR 104 at 116-117 [46]-[51] per French CJ, Nettle and Gordon JJ; Electricity Generation Corporation v Woodside Energy Ltd (2014) 251 CLR 640 at 656-657 [35] per French CJ, Hayne, Crennan and Kiefel JJ; Codelfa Construction Pty Ltd v State Rail Authority (NSW) (1982) 149 CLR 337 at 350, 352 per Mason J (as his Honour then was); Reardon Smith Line Ltd v Hansen-Tangen [1976] 3 All ER 570 at 574 per Lord Wilberforce; Zhu v Treasurer (NSW) (2004) 218 CLR 530 at 559 [82] per Gleeson CJ, Gummow, Kirby, Callinan and Heydon JJ.

I note particularly that there was no dispute before me that I was entitled to consider the statutory context and the contextual documents (the 1995 Agreement and information memoranda) described above for the purposes of construing cl 26.2(b): see also Cherry v Steele-Park (2017) 96 NSWLR 548 at 566 [77]-[78] per Leeming JA.

47 Objectively imputing a contractual intention concerning the method of valuing “those parts” in a determination of the payment to be made “in lieu of land tax” is especially difficult in this case. That is because the Lease says nothing about that method, whether directly or indirectly. It may be that the language used in cl 26.2 was taken from other government contracts which assumed continuing government ownership of the lessee. Future issues about the method of valuation in such cases would matter less because they would be addressed through federal ownership of the lessee.

48 The parties agree that both the 1958 and 2005 Land Tax Acts were relevant to the determination of the correct valuation method. The 1958 Land Tax Act was in operation when the Lease was entered into. But the Lease provided for payment “at the relevant State rate” (cl 26.2(b)). It also provided that references to Acts and to law included replacement Acts (cl 2.2(i)). The 2005 Land Tax Act was thus also relevant. For the reasons given below, in my view, the 2005 Land Tax Act is applicable to the issue of construction which I must resolve.

The Commonwealth’s submissions

49 The parties disagree about the operation of both Acts. The Commonwealth submitted that EAPL wrongfully placed too much emphasis on the operation of the Land Tax Acts and paid insufficient attention to the words of the Lease. In particular, the Commonwealth case stressed the language in cl 26.2(b) of exclusion: “those parts” expressly excluded “runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes” (unless sub-leased to tenants). This language, it was said, manifested a clear contractual intention to exclude from the valuation parts of the Airport Site that are not expressly exigible land pursuant to cl 26.2(b). There is much to be said for that construction.

50 The Commonwealth submitted that its construction of cl 26.2(b) is supported by authority, relying upon Helicopters Pty Ltd. That case concerned an airport lease which contained a clause in the same terms as cl 26.2(b). The lessee had sub-leased part of the land. It was a term of that agreement that the sub-lessee pay the lessee those outgoings reasonably related to the subject premises; they included payments to be made in lieu of land tax by the lessee. It was said that the sub-lessee was liable to pay a sum of this kind. The sub-lessee submitted that in calculating the correct amount, the tax free threshold arising under the Land Tax Management Act 1956 (NSW) had to be re-applied for each area sublet. The lessee submitted that the threshold was only applicable once to the entire part of the land sub-leased. Handley AJA, with whom McColl and Basten JJA agreed, observed that cl 26.2(b) is silent as to the method of calculating the payments to be made. At [19] his Honour said:

Subclause (b) defines the assessable area and requires periodical revaluations but apart from requiring the sub-lessor to make payments in lieu of land tax “at the State rate” it does not spell out the method to be used for calculating those payments.

His Honour agreed with the lessee’s contention and said at [20]:

The Dictionary meanings of “in lieu of” are “in place of” or “instead of”. The payments in lieu under the head lease are “in respect of” the assessable area. In my judgment the subclause provides for one assessable area within the airport site formed by aggregating the areas sub-leased to tenants with other areas on which trading or financial operations are undertaken by the lessee excluding certain areas as defined and other areas occupied by the Commonwealth or a Commonwealth authority. The “or” at the end of cl 26.2(b)(i) is conjunctive, and the defined exclusions relate to the Airport as a whole and indicate that payments were to be made in respect of a single composite area. There would be no need to exclude runways etc and land occupied by the Commonwealth or an authority of the Commonwealth if each area subleased was to be the subject of a separate calculation.

The Commonwealth stressed that this case confirms the need to consider “those parts” as “one assessable area”. With respect, nothing submitted by EAPL contradicted that proposition. Accepting its accuracy does not determine the answer to the question before me: how is one to determine the value of that one assessable area?

51 Handley AJA went on at [21] to say the following:

The Management Act provides for a single annual assessment based on the taxable value of all land owned by the taxpayer at the end of the calendar year subject to a single tax threshold. Prima facie a payment in lieu of land tax should be calculated on the same basis.

If anything, the foregoing observation supports a close application of the terms of the applicable Land Tax Act in order to calculate the payment to be made in lieu of land tax. In support of that conclusion Handley AJA said at [23]-[24]:

Clause 26.2(b) of the head lease applies where Land Tax is not payable, ie by the sub-lessor under cl 26.1, because the airport is owned by the Commonwealth. Payments in lieu of land tax must therefore be calculated on a fictional basis, but the clause does not clearly identify the fiction.

Clause 26.1 dealt with land tax payable by the sub-lessor and, in this context, cl 26.2(b) should be construed as providing for payments in lieu of the land tax that would be payable by the sub-lessor if it was a taxable lessee.

(Emphasis added.)

EAPL’s submissions

52 In contrast to the Commonwealth, EAPL submitted that its method of valuing “those parts” should be preferred because it most closely followed what would have been required by the Land Tax Acts, had they applied. There is also much to be said for that construction. EAPL contended that the passages I have set out from the reasons of Handley AJA in Helicopters Pty Ltd supported its construction rather than that advanced by the Commonwealth. The essence of EAPL’s case was that the 2005 Land Tax Act (and the 1958 Land Tax Act) taxed land identified by a certificate of title owned by a taxpayer. It did not, save in limited cases, permit land tax to be payable on only part of land described in a certificate of title.

53 EAPL relied upon the decision of Croft J in Lotus Projects Pty Ltd v Commissioner of State Revenue [2017] VSC 63; (2017) 105 ATR 252. That case concerned a liability to pay land tax on land used in part for a golf course and clubhouse and in part for residential development. In each of the tax years in question, the land was the subject of a single certificate of title. The taxpayer contended that the part of the land used for the golf course and clubhouse was exempt pursuant to s 71(1) of the 2005 Land Tax Act. That provision was (and still is) in the following form:

(1) Land vested in a person or body is exempt land if the Commissioner determines that—

(a) it is leased for outdoor sporting, outdoor recreational, outdoor cultural or similar outdoor activities and is available for use for one or more of those activities by members of the public; and

(b) the proceeds from the leasing are applied exclusively by the person or body for charitable purposes.

The issue in the proceedings was the meaning of “[l]and vested in a person or body”. This was said to turn on whether “land” referred to all of the land described in the certificate of title on which the taxpayer was identified as the registered proprietor, or whether it was capable of referring only to that part of the land which was leased for use as a golf course and clubhouse. The Commissioner submitted that it referred to the land owned by the taxpayer as described in the relevant certificate of title. The taxpayer submitted that it referred to any identifiable piece or part of land. The Commissioner was successful.

54 After noting the broad definition of “land” in s 3(1) of the 2005 Land Tax Act, Croft J placed emphasis on s 10(1)(a) of that Act which is in the following terms:

(1) The following persons are owners of land for the purposes of this Act—

(a) a person entitled to land for a freehold estate in possession;

A similar definition existed in s 3 of the 1958 Land Tax Act.

55 His Honour then reasoned at [30]-[31] as follows:

… liability to land tax is imposed (subject to express statutory exceptions) on the “owner” of land within the meaning of s 10 of the Act, which relevantly includes “a person entitled to land for a freehold estate in possession”. The reference to the freehold estate naturally directs attention to the land described in a certificate of title, by which a person now obtains legal ownership of land in fee simple as the registered proprietor, or to the land described in a conveyance of general law land in fee simple.

…

Significantly, the term “land” is used in s 71(1) of the Act as part of a composite expression “[l]and vested in a person or body”. While the meaning of the word “vested” varies with the context, it is generally construed as meaning legal ownership of an estate in fee simple, such that land is “vested” in its registered proprietor notwithstanding that the land is subject to a lease. Again, this naturally directs attention to the land described in the certificate of title. It is, in my view, of no significance that the Act does not contain any express reference to “Torrens title”. The identification of the land which is “vested” in an owner is capable of application in the context of the system of land registration established by the Transfer of Land Act 1958. This approach to the meaning of the word “land” as used in s 71(1) of the Act does not involve reading any additional words into this sub-section but, rather, gives meaning to the words “[l]and vested in a person or body”. Nor does it involve any “qualification” or limit on the operation of s 71(1), and to suggest otherwise does beg the central question of construction.

(Footnotes omitted.)

56 At [34] his Honour concluded:

In summary, for the preceding reasons, I accept the position put by the Commissioner that neither the ordinary meaning of “land”, nor the extended meaning in s 3(1) of the Act are of direct assistance in this proceeding. The text and grammatical structure of s 71(1) strongly support the Commissioner’s construction that the exemption is applicable to the “land vested” in the Plaintiff, as opposed to the part of that land the subject of the Lease, which is leased to Black Bull. On the other hand, the Plaintiff’s position, though purporting to apply the principles of statutory construction that give primacy to the text and its surrounding context, essentially ignores or gives no operation to the word “vested” in s 71(1), and fails to address the broader context of the Act in which Parliament has given an express indication whenever it intends to refer to a “part of land” for the purposes of the imposition and assessment of land tax.

57 His Honour’s reasons focus, at least in part, on the phrase in s 71(1) “[l]and vested in a person or body”. However, his conclusion concerning the meaning of “land” was not confined to the meaning of that word in s 71(1). Croft J went on to consider the “broader context” and found that the word “land” more generally meant, for the purposes of the 2005 Land Tax Act, a reference to land identified in a certificate of title (or in a conveyance for general law land). Thus, at [37]-[38], his Honour said:

In the context of the Act, there are numerous examples of the use of the term “land” in contexts which are consistent with the Commissioner’s construction, and inconsistent with a construction that “land” can mean any identifiable part of the land described in a certificate of title (for example, the land identified in a lease).

(a) There are many provisions in the Act which refer to a “part of land” or an equivalent expression. Such provisions would arguably be otiose if the meaning of “land” was sufficiently ambulatory to encompass any discrete identifiable portion of the earth’s surface. The provisions are premised on there being a distinction between “land” (or “the whole land”) and a “part” of land, so that “land” cannot be treated as itself meaning any discrete or identifiable part thereof. The provisions also suggest that, in those cases where Parliament intended that the use of a “part” of land for a particular purpose was sufficient to attract an exemption, it made express provision to that effect. The exemption contained in s 71 does not do so.

(b) There are also several provisions of the Act that use the concept of a “parcel” of land – which is defined to mean any land owned by the same person that is contiguous or separated only by a road, railway or other similar area across or around which movement is reasonably possible. The concept of a “parcel” of land is consistent with the relevant components of that parcel being the land described in two or more certificates of title. If “land” was capable of meaning any discrete identifiable piece of land, the scope of the term “parcel of land” would become uncertain and potentially problematic as it could encompass any contiguous parts of land, even within a single certificate of title.

(c) The provisions of the Act which provide for partial exemptions in respect of a principal place of residence (see ss 62 and 62A) would be otiose if “land” could mean something other than the land described in a certificate of title. Similarly, in providing an ancillary exemption for land which is contiguous to and enhances principal place of residence land, s 54(3) does not suggest any differential treatment for land tax purposes of different parts of that contiguous land.

(d) In relation to “home units”, the special definition of “land” in s 12(3) of the Act would probably be otiose if “land” could encompass any discrete identifiable piece of land. If that were the case, it would be open to treat the “land” in question as the land on which the home unit is situated without the need for any special definition, because that land would be readily “identifiable” as a discrete physical area.

(e) Sections 96 and 97 of the Act provide for the registration of a charge in respect of unpaid land tax on the land on which the tax is payable. The charge is recorded on the certificate in the Register (s 97(2)). This further supports a construction of “land” as referring to the land which is described in a certificate of title.

(f) Both s 22 (taxable value of parts of land not separately valued) and s 46 (land tax on parts of land) draw a distinction between a “part of land” and “the whole land”. The latter can only mean the land described in a certificate of title. The distinction is difficult to reconcile with a construction of “land” which is capable of encompassing any identifiable piece or part of land.

The word “leased” also appears in several provisions of the Act, none of which use the word to qualify the meaning of “land” or to inform the manner in which land is to be identified. To the contrary, each of these provisions uses language that refers to “land or part” of land being leased. A reference to a “part” of land being leased is absent from s 71(1).

(Footnotes omitted.)

58 The presence in the 2005 Land Tax Act of provisions addressing the payment of land tax on “part” only of land in ss 22 and 46(1) made no difference to the foregoing conclusion. If anything, Croft J found that they supported his views. Section 46(1) is in these terms:

If it is necessary to assess land tax (other than vacant residential land tax) on a part of land, the land tax applicable to that part is the proportion of the land tax, assessed on the taxable value of the whole land, that the taxable value of the part bears to the total taxable value of the whole land.

His Honour reasoned at [39]:

Section 46 of the Act makes provision for the assessment of land tax on a part of land, namely by reference to the proportionate taxable value of the part relative to the whole land. Section 22 of the Act deals with the situation in which it is necessary to determine the taxable value of part of land where that part has not been separately valued. Both provisions only apply if “it is necessary” to assess land tax on a part of land or to determine the taxable value of part of land. The Commissioner submits that having regard to the provisions of the Act as a whole, it is plain that “it is necessary” to do so only when the Act makes express provision to that effect. For example, the Commissioner submits, the Act contains numerous provisions which expressly provide that land tax is assessable on a part of land, and that s 22 is to apply if necessary for that purpose. Thus, the Commissioner says that there is no occasion to resort to s 22 or s 46 unless there is express provision for the assessment of land tax on a part of land; referring to Dixon J in R v Wallis, where his Honour said: “an enactment in affirmative words appointing a course to be followed usually may be understood as importing a negative, namely, that the same matter is not to be done according to some other course”. Whilst I accept these submissions in general terms, I do not regard these provisions as impinging on the proper construction of s 71(1). Rather, the position is, in my view, that, were I to accept the Plaintiff’s construction of s 71(1), it would follow that the application of these provisions would become “necessary”.

(Footnotes omitted.)

59 Here, EAPL submitted that the “land” which would be taxed if EAPL had in fact been liable to pay land tax could only have been that described in the certificates of title that comprised the Airport Site. Relevantly, that required, as a starting point, valuing the land so identified and then apportioning value in accordance with s 22 or perhaps s 46(1) of the 2005 Land Tax Act to give effect to a payment “in lieu of” of land tax in respect of “those parts”.

60 EAPL supported its contention by emphasising that the concept of “land” in the 2005 Land Tax Act is closely tied to the concept of its ownership by an owner. It pointed out that the “owner of taxable land is liable to pay land tax”: s 8. A taxpayer is to be assessed for land tax by reference to the taxable value of all land held: s 36. “Taxable value” of land is an amount equal to its “site value” as at the relevant date: s 19. “Site value” is defined as having the same meaning given in the VLA (set out above): s 3(1). That meaning refers to the value of land “if it were held for an estate in fee simple”.

61 EAPL relied upon this definition as indicating that site value can only be ascertainable if land is capable of being sold as an estate in fee simple. Necessarily, it was submitted, that meant land expressed and identified in a “certificate of title” (or in a conveyance for general law land). One cannot sell a part of land so identified. In support of that contention, EAPL relied upon a decision of Wells J in Harry v Valuer-General (1975) 12 SASR 446. That authority concerned a similarly worded definition of “site value” in the Valuation of Land Act 1971 (SA). In that case, land held pursuant to one certificate of title was subject to 166 different leases. The Valuer-General issued 166 assessments of land tax. Wells J decided that this approach was misconceived. His Honour held that the statutory language contemplated a valuation of land “in a defined form capable of being sold”.

62 EAPL’s argument was said to be supported contextually by cl 26.2(a) of the Lease and the definition of “rates” in that agreement. That definition refers to rates imposed on land or on owners “or occupiers of land”. In context, the definition of “land tax” in the Lease refers to taxes levied “on land”. It was said that this reflected the legislative scheme whereby rates were calculated on an occupancy basis, whereas land tax was calculated by reference to the unimproved value of an estate in fee simple.

63 EAPL also relied upon the decision of Emerton J in Port of Melbourne Corp v Melbourne City Council & Valuer General Victoria [2015] VSC 714; (2015) 213 LGERA 152. That case concerned a dispute over the site value, for the purposes of the VLA, of certain land comprising a port. The dispute turned upon whether the land should be valued as a whole and then by carrying out an apportionment of that value in respect of individual occupancies or tenancies within the land, or whether each occupancy should be valued separately on a stand-alone basis. The Port of Melbourne (“PoMC”) contended that the starting point was to value the land as a whole. It principally relied upon s 2(3) of the VLA which expresses a rule for valuing land that “forms part of a larger property”. It is in the following terms:

If it is necessary to determine the capital improved value or site value of any rateable land in respect of which any person is liable to be rated, but which forms part of a larger property, the capital improved value and site value of each part are as nearly as practicable the sum which bears the same proportion to the capital improved value and site value of the whole property as the estimated annual value of the portion bears to the estimated annual value of the whole property.

In contrast, the Melbourne City Council said that the starting point was to undertake valuation on an occupancy basis which required each tenancy to be valued on a stand-alone basis. It relied upon s 13DC(1) of the VLA which relevantly provided at the time:

In every valuation for the purposes of the Local Government Act 1989, each separate occupancy on rateable land must be computed at its net annual value, its capital improved value and, if required by a rating authority, its site value ...

64 Emerton J undertook a thorough, and, if I may respectfully say, authoritative, analysis of the legislative history. Her Honour observed that historically in Victoria the concept of site value for land tax purposes had been based on ownership and not occupancy. In contrast, in determining council rates, value was historically based on occupancy. The VLA integrated both tests. Section 2(3), set out above, reflected this integration. But the starting point for valuation remained, not occupancy, but title. In that respect, her Honour rejected the Council’s reliance upon s 13DC(1). It did not address the method of apportionment to be used when valuing only part of land. This was the work of s 2(3). At [136]-[137], her Honour said:

[The precursor provision to s 2(3)] is a product of the need to adapt for rating purposes determinations made by the Commissioner for Taxes of the unimproved value of land on a single title. When used for rating purposes, the Commissioner’s determination had to cater for the existence of multiple occupancies on the title and the provision contained a formula to enable this to occur.

The “starting point” for the valuation exercise for “unimproved capital value” was therefore title rather than occupancy. Although what had to be given a value for rating purposes was the unimproved capital value of each separate occupancy, the valuer commenced by determining the unimproved capital value of the fee simple and proceeded from there to derive values for each occupancy by way of an apportionment.

Emerton J decided that each tenancy at the Port of Melbourne was part of a larger property for the purposes of s 2(3) which had first to be valued. Her Honour concluded at [148] in the following terms:

In summary, while rates in Victoria have been returned on an occupancy basis since the late nineteenth century, land tax has been calculated on the basis of the unimproved value of the unencumbered estate in fee simple. When, in 1914, councils were given the option of using unimproved capital value as the basis for the imposition of rates upon occupiers of land, the legislature devised a way to convert the unimproved capital value of the estate in fee simple into the unimproved capital value of any portion of the land under separate occupancy. The predecessor provisions to s 2(3) sought to reconcile the requirement to rate on a basis other than title or ownership with title or ownership-based valuations. The “starting point” was the valuation for site value purposes of land held under common ownership, now the “larger property”. The 1991 amending Act, which introduced the requirement to compute “each separate occupancy” for the values specified in s 13DC(1) did not change this. The extrinsic materials do not reveal any intention to effect substantive change to the approach to the valuation methodology for site value which preceded the 1991 amendment, namely, the valuation of the larger property, followed by the computation of the site value for each occupancy.

65 Emerton J decided that whether an area of land formed part of a “larger property” was a question of fact having regard to the highest and best use of the land. In the case before her Honour, that was using the land as a port. Emerton J decided that there was a “larger property” being used for that purpose. Her Honour said at [174]-[176]:

… In my view, because of its control over land use, roads, railways, services and waterways, PoMC’s management and development of the port was critical to the day to day operations of the port users and to the actual use that could be made by the tenants of the port of Melbourne land and waters.

I find, as a matter of fact, that the port of Melbourne land was planned, managed, operated and used as a “larger property” and that the occupancies formed part of this larger property.

The statutory and regulatory framework that governed the use and development of the port required it to be managed and developed strategically to serve the interests of the State as well as the tenants. Because of the capital expenditure required, the nature and scale of port development and the need for long term strategic planning, land use plans for the port were made and implemented over lengthy periods. Like its predecessors, PoMC was required to (and did) exercise stewardship over the port of Melbourne land to ensure that the necessary investment in channels and infrastructure, both land-side and water-side, occurred. PoMC was required to (and did) secure the land, waters and infrastructure necessary for the development of the port in order to ensure that the port could accommodate projected growth in trade along with changes in trade composition and ship size, and that the port was effectively integrated with other transport networks in the State. The use that could be made of the port of Melbourne land by the tenants depended on this strategic management and development.

66 EAPL also relied upon the decision in Lamanna v Commissioner of State Revenue [2005] VSC 436; (2005) 61 ATR 467. That case concerned a four-storey building. Each floor was separately leased but was not subdivided into separate titles. Hollingworth J held that land tax had to be assessed by valuing the entire land and then apportioning that value to each occupancy.

67 EAPL did not rely upon s 2(3) of the VLA for the purposes of this proceeding. It submitted that the provision could not be made to work. That is because it depended on the calculation of the “estimated annual value” of the whole property as well as each portion of that property. Section 2(1) of the VLA defines that term as follows:

estimated annual value of any land, means the rent at which the land might reasonably be expected to be let from year to year (free of all usual tenants’ rates and taxes) less—

(a) the probable annual average cost of insurance and other expenses (if any) necessary to maintain the land in a state to command that rent (but not including the cost of rates and charges under the Local Government Act 1989); and

(b) the land tax that would be payable if that land was the only land its owner owned

68 It was said that the definition could not be made to work because the amount of land tax payable formed part of the formula for determining “estimated annual value”. EAPL instead relied upon s 22 of the 2005 Land Tax Act, as set out above.

69 Finally, EAPL also submitted that the effect of the Commonwealth’s construction is that the “taxable value” attributed to “those parts” of the Airport Site of $348,900,000 (based on an area of between 14% and 18% of the Airport Site) is more than seven times the “taxable value” attributed to the Airport Site as a whole of $48,477,228 (using Mr Brown’s valuation). EAPL argued that if more of the Airport Site were to be developed (as envisaged in the 2013 Master Plan), what constitutes the exigible land under cl 26.2(b) would increase and, on the Commonwealth’s approach, the value of “those parts” would eventually exceed the site value of the Airport Site as a whole. To illustrate the purported flaw in the Commonwealth’s approach, EAPL produced a table based on Mr Cations’ valuation and then produced a table extrapolating the consequential increase in site value of “those parts” of the Airport Site – referred to as “EGLT Area” – as a result of increased development of the Airport Site:

Table constructed based on Mr Cations’ report

Precinct | Total area m2 | Value rate | Value |

English Street | 152,534 | $697 | $106,330,000 |

Beaufort North | 51,903 | $580 | $30,080,000 |

Wirraway North | 130,213 | $450 | $58,620,000 |

Airfield Precinct 1 | 65,066 | $400 | $26,040,000 |

Bulla Precinct | 171,748 | $744 | $127,810,000 |

Total | 571,464 m2 | $610.50 (average) | $348,880,000 |

EAPL’s table of extrapolated figures (using the average value per square metre in Mr Cations’ valuation and comparing the result with the site value of $393,400,000 attributed to the airport site as a whole)

EGLT Area m2 | % of Airport Site | Average rate ($ per m2) | Value | % of Site Value of $393,400,000 |

571,464 | 18.80 | 610.50 | $348,880,000 | 88.68 |

644,340 | 21.20 | 610.50 | $393,400,000 | 100 |

751,000 | 25.00 | 610.50 | $458,485,500 | 116.54 |

1,001,333 | 33.33 | 610.50 | $611,341,000 | 155.40 |

1,502,000 | 50 | 610.50 | $916,971,000 | 233.10 |

This, it was said, threw into sharp relief how the Commonwealth’s construction would result in “commercial nonsense” or work “commercial inconvenience” into the Lease.

The Commonwealth’s submissions in reply

70 The Commonwealth did not contend that Lotus Projects, Port of Melbourne, or Lamanna were wrongly decided. It submitted that Lotus Projects was distinguishable because it said nothing about how part of land was to be valued for land tax purposes. Port of Melbourne and Lamanna were cases concerning occupancies within a “larger property”. For that purpose it was wrong to confuse a “larger property” with a singular certificate of title; in Port of Melbourne the “larger property” comprised several titles. Moreover, it was said, there is no larger property here; rather the land is being used for two distinct and separate purposes: aviation and non-aviation.

71 Critically, the Commonwealth contended that both the 1958 and 2005 Land Tax Acts permitted the use of occupancy based valuations as a means of determining site value. In other words, those Acts permitted value to be ascertained by a consideration of each occupancy on land. Such an approach did not require one first to value the land as a whole. It relied upon s 16 of the 1958 Land Tax Act and s 21 of the 2005 Land Tax Act. Section 16, it was contended, was not considered by Emerton J in Port of Melbourne. It provided:

As to use of valuations by Commissioner

For the purpose of the assessment and levy of taxation the Commissioner may use—

(a) valuations made by a rating authority within the meaning of the Valuation of Land Act 1960;

(b) valuations made by the Valuer-General or a valuer nominated by the Valuer-General;

This provision was first inserted into the 1958 Land Tax Act in 1969. It facilitated the use of municipal valuations for land tax purposes. Section 21 of the 2005 Land Tax Act is similar and is in the following form:

Use of valuations

For the purposes of assessing land tax, the Commissioner may use—

(a) valuations made by a valuation authority; or

(b) valuations made for and on behalf of the Commissioner by the Valuer-General or a valuer nominated by the Valuer-General.

(2) Without limiting subsection (1), the Commissioner may–

(a) use a valuation made under the Valuation of Land Act 1960 that has determined the value of each separate occupancy on land; and

(b) include in a notice of assessment a description of the occupancy on land.

(3) A valuation of occupancy on land made under the Valuation of Land Act 1960 is deemed to be a valuation of land for the purposes of this Act.

It was said that the language of s 21(2)(a) put the use of occupancy based valuations for land tax purposes beyond doubt.

72 The Commonwealth submitted that the use of occupancy based valuations for assessing land tax is supported by the decision of the Victorian Court of Appeal in Melbourne City Council v Port of Melbourne Corporation [2005] VSCA 72; (2005) 139 LGERA 318. There, in the context of considering rights of objection, Nettle JA (as his Honour then was), with whom Buchanan and Eames JJA agreed, said at [31]-[32]:

… Under s 13DC of the Valuation of Land Act [in force in 1999] the rating authority is required to value each separate occupancy separately …

… Since the Commissioner is enabled by s 16 of the Land Tax Act to use for the purposes of one assessment of land tax a multiplicity of valuations made under the Valuation of Land Act, it is possible if indeed not probable that an assessment of land tax may be based on valuations of several different occupancies, possibly prepared by several different valuers (including one or more municipal councils and the Commissioner and the Valuer General) …

73 The Commonwealth also submitted that s 22 of the 2005 Land Tax Act was not applicable because it was a section of last resort which applied only if it was “necessary” to determine the value of part of land, the whole of which had been valued separately. Here it was not necessary to apply this provision because a separate valuation of “those parts” had been undertaken based on occupancy. For the purposes of cl 26.2(b), “those parts” did not form part of any larger property.

Disposition

74 I make the following observations and conclusions in respect of the construction of cl 26.2(b).

75 First, consistently with Helicopters Pty Ltd, in my view the parties to the Lease intended that the methodology for determining what payment should be made by EAPL to the Commonwealth should be based upon the fiction that EAPL was in fact liable to pay land tax on “those parts” identified in cl 26.2(b). In other words, the payment is to be ascertained on the “fictional basis” that EAPL is “a taxable” entity. That conclusion is supported by the language used in cl 26.2(c) which refers to the making of payments equivalent to those “which would be payable for such Taxes if such Taxes were leviable or payable”. As a result, the applicable Land Tax Act to be applied is that in force in the State of Victoria as that is where the Airport Site is located. The relevant version of the Land Tax Act, in the context of this dispute, is not that enacted in 1958 and in force when the Lease was entered into, but the 2005 Land Tax Act as amended from time to time. That is not only because of the reference to “at the relevant State rate” in cl 26.2(b) of the Lease; but also because cl 2.2(i), set out above, expresses the parties’ agreement that references to legislation should be to “all amendments, consolidations or replacements thereof”. In my view the 2005 Land Tax Act is a “replacement” of the 1958 Land Tax Act. That conclusion is supported by s 1 of the 2005 Land Tax Act which is in these terms:

Purposes

The purposes of this Act are—

(a) to re-enact and modernise the law relating to land tax;

…

76 Secondly, I accept that the better view is that “land” in the 2005 Land Tax Act refers to land identified in a certificate of title. I do so for the reasons given by Croft J in Lotus Projects, which I respectfully agree with and adopt. Even if I doubted their correctness, I would have in any event have followed Lotus Projects as a matter of comity. In my view, the law and justice of this case requires no different conclusion about the meaning of “land” in the 2005 Land Tax Act; the conclusion reached by Croft J was not “clearly wrong”: Sunchen Pty Ltd v Federal Commissioner of Taxation [2010] FCA 21; (2010) 75 ATR 13 at [20]-[21] per Perram J; R v Hookham (1993) 31 NSWLR 381 at 391 per Priestley JA; Undershaft (No 1) Limited v Federal Commissioner of Taxation (2009) 175 FCR 150 at 165-169 [68]-[88] per Lindgren J.

77 Thirdly, I accept that it is lawful to determine the site value of land on an occupancy basis. That is plain from the terms of s 21 of the 2005 Land Tax Act; the language of cl 26.2(a) of the Lease does not compel a contrary conclusion. But the acceptance of that methodology is no necessary answer to EAPL’s case. Occupancy, as a means of assessing value, says nothing about the identification of the land to be valued. It simply permits value to be determined by “each separate occupancy on land”, to use the language of s 21(2)(a) of the 2005 Land Tax Act. What is the “land” on which such occupancies may be located is another question.

78 Fourthly, for reasons set out below, it is unnecessary for me to determine whether “those parts” identified in cl 26.2(b) form part of a “larger property” for the purposes of s 2(3) of the VLA. If it matters, I would not have accepted the Commonwealth’s submission that “those parts” do not form part of a larger property because two distinct uses of land are carried on at the Airport Site. In my view, the Airport Site is primarily used for the purpose of an airport, and the non-aviation uses are subordinate to that purpose. That is the effect of both cl 3.1 of the Lease, and s 32(1) of the Airports Act. It is also unnecessary, for the reasons expressed below, for me to resolve the dispute concerning the application of s 22 of the 2005 Land Tax Act.

79 Fifthly, it is important that the calculation of the required payment be based upon a fiction prescribed by the Lease. The fiction is that EAPL is liable to pay land tax when, in fact, it is not. But in my view that is not an exhaustive statement of the fiction upon which the payment is to be determined. The parties to the Lease expressly identified the land in respect of which the payment in lieu of fictional land tax was to be made. It was not the entire Airport Site, but only “part” of it. They did so in an inclusionary and exclusionary way. The land included is that part of the Airport Site that is “sub-leased to tenants” or “on which trading or financial operations are undertaken including but not limited to retail outlets and concessions, car parks and valet car parks, golf courses and turf farms”. The land excluded is identified by the parties as “runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes” (to the extent such land is not sub-leased to tenants). In my view, in order to give effect to this expression of contractual intention, one must assume that not only is EAPL liable to pay land tax, but also that it is liable to pay that tax in respect of the land identified by the parties. For that purpose, the identified land is taken to be land which is exigible for land tax purposes; that is, land on a fictional certificate of title. In that respect, consistently with Helicopters Pty Ltd, and its reference to “one assessable area”, the land specified by the parties should be assumed to be on one certificate of title. For this reason, and with respect, EAPL’s valuer erred in commencing with a value of the land described in the actual certificates of title (comprising the entire Airport Site) and then apportioning value. That approach does not reflect the express intention of the parties to exclude the land used solely for aviation purposes. The valuer should only have valued the land identified by the parties on the fictional basis set out in this paragraph. For that purpose, there was accordingly no need to reduce the value so determined by reference to the cost of building airport infrastructure.