FEDERAL COURT OF AUSTRALIA

Sole Luna Pty Ltd as Trustee for the PA Wade No 2 Settlement Trust v Commissioner of Taxation (No 2) [2019] FCA 1387

ORDERS

SOLE LUNA PTY LTD AS TRUSTEE FOR THE PA WADE NO 2 SETTLEMENT TRUST Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Respondent’s objection decision with respect to penalty by assessment dated 21 June 2017 for the income year ended 30 June 2013 is set aside and the Applicant’s objection against the penalty assessment is allowed.

2. The Applicant pay 75% of the Respondent’s costs of the proceeding, including costs reserved on 18 May 2018 and 3 August 2018, as agreed or assessed.

3. The proceeding otherwise be dismissed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VID 310 of 2018 | ||

| ||

BETWEEN: | PETER ANTHONY WADE Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

ORDERS

JUDGE: | STEWARD J |

DATE OF ORDER: | 30 august 2019 |

THE COURT ORDERS THAT:

1. The Respondent’s objection decision with respect to penalty by assessment dated 22 June 2017 for the income year ended 30 June 2015 is set aside and the Applicant’s objection against the penalty assessment is allowed.

2. The Applicant pay 75% of the Respondent’s costs of the proceeding, including costs reserved on 18 May 2018 and 3 August 2018, as agreed or assessed.

3. The proceeding otherwise be dismissed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VID 311 of 2018 | ||

| ||

BETWEEN: | PETER ANTHONY WADE Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

ORDERS

JUDGE: | STEWARD J |

DATE OF ORDER: | 30 august 2019 |

THE COURT ORDERS THAT:

1. The proceeding be dismissed.

2. The Applicant pay the Respondent’s costs of the proceeding, including costs reserved on 18 May 2018 and 3 August 2018, as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

STEWARD J:

1 On 2 August 2019, I published my reasons in Sole Luna Pty Ltd as Trustee for the PA Wade No 2 Settlement Trust v Commissioner of Taxation [2019] FCA 1195 and gave the parties time to agree upon the form of final relief or, failing that, to file submissions about that issue. The parties were unable to reach full agreement. In what follows I adopt the terminology from my earlier reasons.

2 In essence:

(1) I found for the Commissioner in relation to the issues of primary tax for the 2013, 2015 and 2016 years of income. The 2013 assessment had been issued to Sole Luna. The 2015 and 2016 assessments had been issued to Mr Wade;

(2) notwithstanding that success, the Commissioner did not win every argument. In particular, the taxpayers persuaded me, in the face of stiff opposition, that the foreign currency loans had been made; and

(3) I decided that no penalty was payable either by Sole Luna or Mr Wade.

3 The parties were in dispute about the cost orders that I should make. In summary:

(1) the taxpayers contend that there should be no order as to costs in all proceedings; and

(2) the Commissioner contends that the taxpayers should pay 80% of his costs in proceedings VID309/2018 and VID310/2018 (which related to the 2013 and 2015 income years respectively); and 100% of his costs in proceeding VID311/2018 (which related to the 2016 income year and involved no dispute as to penalty).

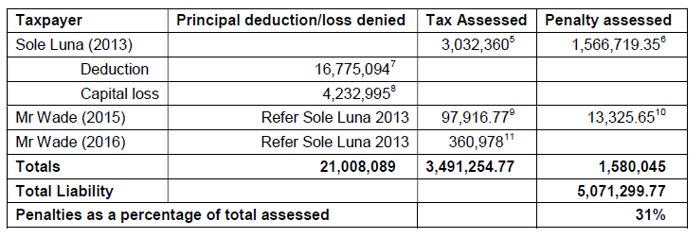

4 The relative success of each side may be illustrated by the following table, which I have extracted from the submissions of the taxpayers (omitting footnotes):

As can be seen, the taxpayers were successful in reducing their overall liability to the Commissioner by 31%. The penalties represented about 45% of the primary tax in dispute.

5 There was no real dispute about the principles which inform how I should exercise my discretion to award costs. It is thus unnecessary to repeat them in these reasons.

6 The taxpayers submit that the Commissioner should pay their costs of proving the existence of the foreign currency loans. They observe that the Commissioner only denied the reality of these loans late in the piece. They went to considerable trouble to recover records and assemble witnesses. Much cross-examination was devoted to this issue. They also submit that the Commissioner should pay the taxpayers’ costs on the issue of penalties. They contend that the Commissioner should have exercised greater discrimination in assessing penalties. They say that rather than making complex orders about the costs payable for each issue, and given the high cost (to them but not to the Commissioner) of dealing with the loan issue, the fairest outcome is that I should make no order as to costs in all proceedings.

7 The Commissioner acknowledges that the taxpayers have succeeded in proving the fact of the foreign currency loans. However, the taxpayers have nonetheless failed to show that the assessments of primary tax were excessive. That was the dispositive issue and the taxpayers have failed. He otherwise, properly, concedes that the issues of primary tax and penalties “were discrete issues” and that the taxpayers were entitled to their costs in relation to penalties. He submits that it is appropriate to make one “net order for costs” in favour of the Commissioner. He proposes a reduction by 20% of the costs otherwise payable in proceedings VID309/2018 and VID310/2018. In that respect, the Commissioner said the following in his written submissions:

It is submitted that a fair estimate of the proportion of costs incurred with respect to penalties is 10%. The Commissioner reaches that figure by noting that approximately 13% of the written submissions and the affidavit material concerned penalties and approximately 3% of the hearing time concerned penalties.

(Footnotes omitted.)

8 I respectfully agree with the Commissioner that he is entitled to an ordinary award of costs in his favour subject to a discount to reflect his loss on the issue of penalties in proceedings VID309/2018 and VID310/2018. As the issue of penalty did not arise in VID311/2018, he is entitled to all of his costs.

9 It is not uncommon for a taxpayer to win many issues or integers in a tax appeal, but nonetheless fail to show that an assessment is excessive. In the ordinary case, unless excessiveness is demonstrated, the Commissioner should have his costs. In my view, this matter came close to not being an ordinary case given the history of the many reviews and audits the Commissioner made of the Wade group of companies. Nonetheless, and on balance, he was entitled to issue the assessments in dispute on the basis that he did and on his then understanding of the available material and the rules of evidence.

10 In my view, however, the discount suggested by the Commissioner is too modest. The ascertainment of the correct discount here cannot be determined by only a quantitative assessment of the time spent on the issue of penalties in written submissions and oral argument. Qualitative evaluations should also be considered. That includes the materiality of the issue to the parties and the difficulty of the point concerning penalties that was determined. In my view, a discount of 25% rather than 20% more appropriately reflects the importance of that issue to the parties, as well as the time spent on it.

11 I shall make orders to reflect these reasons.

I certify that the preceding eleven (11) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Steward. |