Quinlan, in the matter of Halifax Investment Services Pty Ltd (Administrators Appointed) (No 3) [2019] FCA 124

Table of Corrections | |

The MNC “Quinlan (liquidator) of Halifax Investment Services Pty Ltd (Administrators Appointed), in the matter of Halifax Investment Services Pty Ltd (Administrators Appointed) (No 2) [2019] FCA 124” has been replace with “ Quinlan, in the matter of Halifax Investment Services Pty Ltd (Administrators Appointed) (No 3) [2019] FCA 124”. | |

30 April 2019 | In the Catchwords, the word “liquidator” has been replaced with “administrators”. |

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Interlocutory Process be returnable instanter.

2. Subject to Order 3 below, pursuant to s 90-15(1) of the Insolvency Practice Schedule (Corporations), being Schedule 2 to the Corporations Act 2001 (Cth) and/or sections 63 and 81 of the Trustee Act 1925 (NSW), the Administrators were and will continue to be justified in using and applying the funds held in NAB Account Nos. 946205445, 308580742, the sum of $100,000 that was paid into the Johnson Winter & Slattery Trust Account on 2 August 2018, and the term deposit with Bankwest Account No. 4646460 to pay:

(a) the trading expenses of Halifax Investment Services Pty Ltd (Administrators Appointed) (Company) of the nature set out in the schedule of costs, which is attached to these Orders and marked “A”, up to the amounts specified therein;

(b) the administration expenses of the Company in respect of meeting costs and Link Market Services of the nature set out in the schedule of costs, which is attached to these Orders and marked “A”, up to the amounts specified therein; and

(c) any further reasonable and necessary trading expenses incurred by the Company.

3. Liberty to apply be granted to any person, including any creditor of the Company or the Australian Securities and Investments Commission, who can demonstrate sufficient interest to vary Order 2 above on the giving of three (3) business days’ notice to the Plaintiffs, and to the Court, such liberty to be exercised within 7 days of the Plaintiffs complying with Order 4 below.

4. The Plaintiffs, within seven (7) business days of the making of these orders are to take all reasonable steps to give notice of the Orders to the Company’s creditors (including the persons claiming to be creditors) by means of a circular:

(a) to be published on the website maintained by the Plaintiffs at https://www.ferrierhodgson.com/au/creditors/halifax-investment-services-pty-ltd;

(b) to be published on the Company’s website at www.halifax.com.au (Company Website);

(c) to be published via a message on the electronic trading platforms provided by the Company “Halifax Plus”, “Halifax Pro” and “Trader Workstation” on the company website;

(d) to be sent by email to the landlord of the premises occupied by the Company at Level 49, Governor Phillip Tower, 1 Farrer Place, Sydney;

(e) to be sent by email to the members of the Committee of Inspection as listed in paragraph 8 of the Affidavit of Philip Alexander Quinlan affirmed 11 December 2018 (Mr Quinlan’s affidavit);

(f) to be sent by email to the trade creditors of the Company as listed at page 43 of Exhibit “PAQ-1” of Mr Quinlan’s affidavit;

(g) to be sent by email to the employees of the company.

5. The costs of the Interlocutory Process be costs and expenses in the administration of the Company.

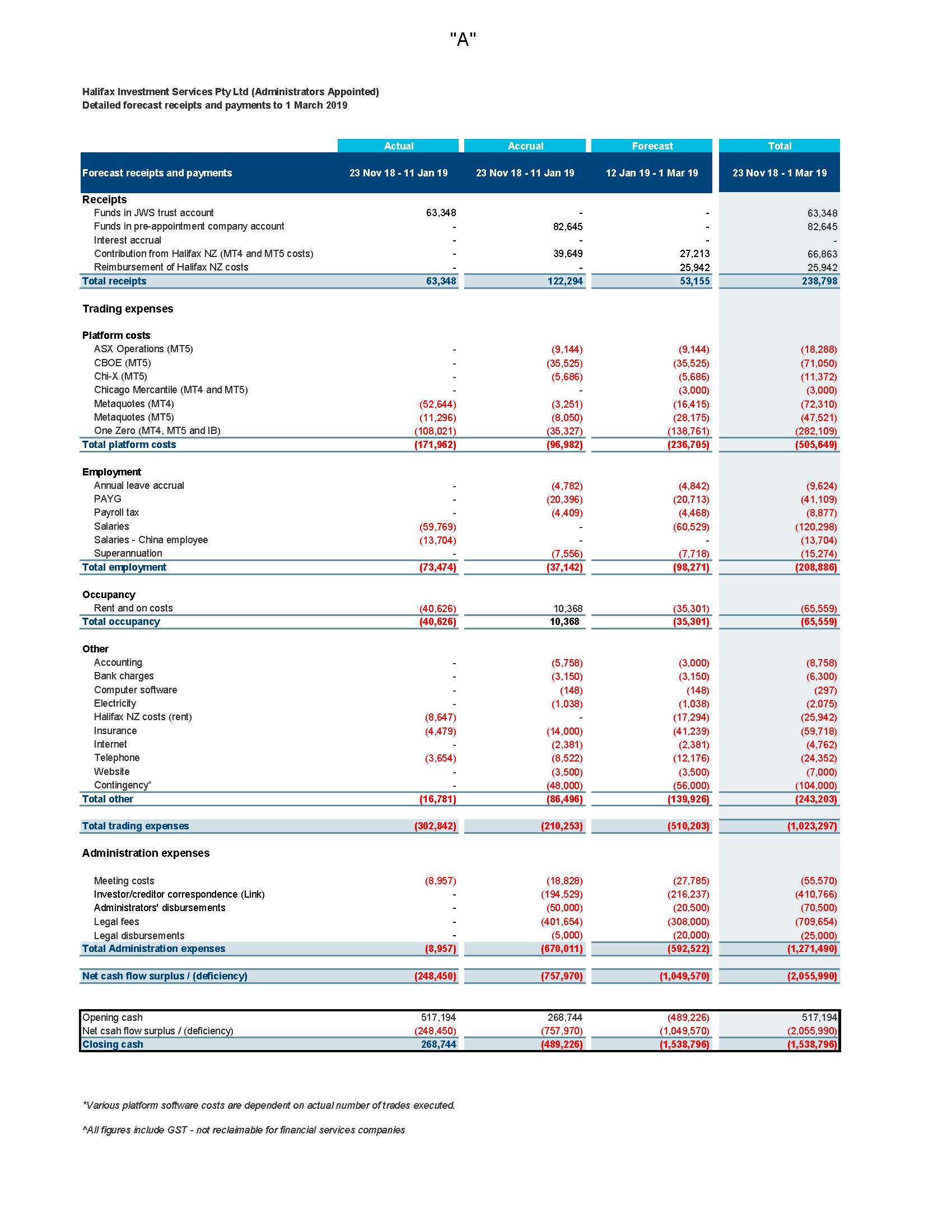

6. These orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE “A”

GLEESON J:

1 On 25 January 2019, on the ex parte application of the plaintiffs (“administrators”), I made orders intended to enable and facilitate the complex administration of Halifax Investment Services Pty Ltd (Administrators Appointed) (“company”) until the second creditors meeting, which the administrators presently anticipate will be held on about 1 March 2019.

2 The application was supported by affidavits made by Philip Alexander Quinlan, one of the administrators, sworn on 26 November 2018, 11 December 2018, 22 January 2019 and 24 January 2019 (two affidavits), as well as written and oral submissions made by Doran Cook SC.

3 Importantly, Mr Quinlan gave evidence of his belief that order 2, which is the substantive order justifying the administrators’ access to particular funds, is in the best interests of the creditors of the company including investor creditors. In particular, based on Mr Quinlan’s detailed evidence and in the absence of evidence to the contrary, I was satisfied that:

(1) without access to the funds, the operating expenses of the company cannot be met, specifically the services of essential suppliers, employees and other incidental operating costs;

(2) information available only from the trading platforms is required to close out investor positions, accurately adjudicate upon investor creditor claims and transfer funds and stock in a liquidation or deed of company arrangement (“DOCA”) scenario; and

(3) without access to the funds, the administrators’ access to the trading platforms is likely to cease to the detriment of investor creditors and any future liquidation or DOCA.

4 Mr Quinlan’s opinion, the basis for which was explained and is apparently reasonably held, is that it was necessary for the expenses incurred in the course of the administration to date (the bulk of which has been for access to the trading platforms) to be incurred, in order for the administrators to fulfil their statutory duty to investigate the affairs of the company and preserve and have visibility of the positions of investor creditors on the trading platforms.

5 Apart from the funds that are identified in the orders, there are no assets of the company that appear to be able to be realised in an immediate way to satisfy the expenses of the company and the administration expenses.

6 I was satisfied that orders should be made urgently in order to provide funds to permit the continued trading of the business and for payment of necessary administration expenses.

7 It is also significant that the administrators are in the process of formulating a DOCA proposal that is intended to provide a more expedient return to creditors than a liquidation. Mr Quinlan’s view is that a DOCA is likely to produce such a return, based on his knowledge of other comparable liquidations. That process would come to an end if the administration is required to cease for lack of funds.

8 The orders made do not permit access to funds for the purposes of paying the administrators’ substantial legal fees incurred in connection with the administration, or the administrators’ remuneration.

Background facts

9 In Quinlan (liquidator) of Halifax Investment Services Pty Ltd (Administrators Appointed), in the matter of Halifax Investment Services Pty Ltd (Administrators Appointed) [2018] FCA 2115, I set out facts concerning the administration up to about 12 December 2018 and various matters concerning the administrators’ application for an extension of time to convene the second meeting of creditors pursuant to s 439A(6) of the Corporations Act 2001 (Cth) (“Act”).

10 Briefly, the company was incorporated on 30 May 2001 and conducted the business of a licenced financial services provider that dealt in financial products, including listed shares and bonds and over-the-counter derivatives. It conducted this business through various electronic trading platforms that were supplied by third parties. The financial products involved were complex and involved transactions that occurred across different trading platforms, on behalf of investors within and outside of Australia, and through different related entities.

11 Both under the terms of its agreements with its investor clients and as a consequence of the Act (s 981H), the funds paid to it by its investor clients were held on trust. The administrators’ solicitors have undertaken a review of the various investor client agreements and concluded that the expenses that are the subject of this application are not capable of being paid out of the investor clients’ funds pursuant to those agreements.

12 On 7 January 2019, the Australian Securities & Investments Commission (“ASIC”) confirmed that it would suspend the company’s Australian Financial Services Licence (“AFSL”) for a period of 12 months.

Updated creditor position

13 Mr Quinlan provided the following current information about the company’s creditor position:

(1) Trade creditors total an estimated $631,375.

(2) Broker creditors owed commissions on opening and closing of trade total an estimated $294,031.61.

(3) Employee creditors total an estimated $177,817.26. This amount is less than the estimate contained in Mr Quinlan’s 11 December 2018 affidavit, because the administrators agreed to pay the annual leave of employees in exchange for a reduction in their pre-appointment balances.

(4) An amount of $263,221.15 is owing to the director, Jeffrey Worboys, and the previous director, Matthew Barnett, for pay in lieu of notice following their redundancies as at appointment.

(5) The lease of the premises from which the company operates its headquarters is continuing and the administrators have paid and continue to pay the rent.

(6) The administrators have identified possible security interests over computer equipment and security interests in three motor vehicles. They are continuing to investigate these interests and have disclaimed their interest in one of the vehicles.

Extent of deficiency of funds

14 In my previous judgment, I noted that the company was said to have 12,559 individual active client accounts held across the trading platforms.

15 As at the date of the administrators appointment (23 November 2018), the amounts owing to the company’s investor creditors is approximately $167,343,272 comprising:

(1) $110,044,790 to investors on the Trader Workstation trading platform;

(2) $24,346,969 to investors on the Halifax Pro trading platform; and

(3) $32,951,513 to investors on the Halifax Plus trading platform.

16 Further, an amount of at least $44,367,721 is owing to investor creditors of Halifax New Zealand Limited (In Administration) (“Halifax NZ”), to which the administrators are also appointed, on the Trader Workstation trading platform.

17 Investor creditors of Halifax NZ on the Halifax Pro and Halifax Plus trading platforms are incorporated in the figures at [15(2)] and [15(3)] above.

18 Mr Quinlan’s evidence was that, as at 22 January 2019, the equity position of the company and Halifax (excluding the funds that are the subject of the orders made on 25 January 2019) viewed together is:

(1) assets available to investors of approximately $192,000,000;

(2) amounts owing to investors of approximately $211,700,000; and

(3) deficiency of assets of approximately $19,700,000.

19 The extent of the deficiency is still being investigated by the administrators. It appears that $12.8 million of the deficiency has been applied by the company as revenue. The administrators are investigating the company’s entitlement to treat the funds as revenue. If not revenue, then the deficiency of assets will be commensurately less, that is, approximately, $6.9 million.

20 Mr Quinlan estimated that the equity position of the investor creditors as equivalent to a dividend of 90.71 cents per dollar. Although the evidence was not entirely clear, this figure appears to assume that the funds the subject of order 2 are ultimately established or accepted as company funds. By way of illustration, if the term deposit was determined to be entirely investor funds and was not defrayed on the expenses of the administration, the dividend would increase to 91.47 cents per dollar.

Trading expenses and expenses incurred in trustee capacity

21 Mr Quinlan’s evidence was to the effect that, since the start of the administration, the company has incurred and continues to incur expenses in its own capacity (operating expenses) and in its capacity as trustee of the funds of investor clients (expenses related to the investment of those funds in financial products and commodities on the trading platforms).

22 Mr Quinlan’s evidence was that, as at 11 January 2019, the net expenses that the company has incurred and paid in its own capacity total $302,842. These comprised:

(1) platform costs of $171,962;

(2) employment costs of $73,474;

(3) occupancy costs of $40,626; and

(4) other costs of $16,781.

23 Mr Quinlan stated that, as at 11 January 2019, the net expenses that the company has incurred but not yet paid total $210,253.

24 Further, the administrators estimate that the company will incur approximately net $510,203 in expenses if it maintains the limited operations of the company required to maintain the status quo up until 1 March 2019, being the date by which the administrators anticipate that the second meeting of creditors will have concluded.

25 On these figures, the total operating costs of the company during the administration are an estimated $1,023,297.

26 Mr Quinlan also gave evidence as to expenses incurred by the company in its trustee capacity for:

(1) commissions payable to introducing brokers of Halifax Pro and Halifax Plus; and

(2) fees payable on transactions on the Trader Workstation Platform to Interactive Brokers LLC.

27 These expenses are generally automatically satisfied and are not outstanding and payable by the company in its trustee capacity.

Administration expenses

28 As at 11 January 2019, the net administration expenses incurred total $670,011 including substantial legal fees and disbursements. Mr Quinlan forecast total administration expenses to be $1,271,490 by 1 March 2019.

29 In particular, the administrators have incurred significant liabilities to Link Market Services (“Link”) as a consequence of the administration, primarily arising out of dealings with investor clients. As at 11 January 2019, the amount owing to Link was $194,529.

30 Link has provided the following services to the administrators:

(1) processing and adjudicating proof of debt forms and proxy forms (approximately 1,580 proxy forms received at the first meeting of creditors and approximately 4,601 proofs of debt) in preparation for the first creditors’ meeting;

(2) responding to investor queries in accordance with a standard template prepared by the administrators. As at 17 January 2019, Link dealt with 1,418 telephone calls and 5,877 emails from creditors and investors; and

(3) processing registrations and running the voting at the first creditors’ meeting.

31 By reference to the costs of the first creditors meeting, the number of queries received from investors to date and the number of investor creditors (12,559), it is estimated that the administrators will incur a further liability of $216,237 to Link including in relation to the conduct of the second creditors meeting. Mr Cook SC informed the Court that Link had told the administrators that it will not assist with the second meeting unless the administrators pay their costs of the first meeting.

32 In oral submissions, Mr Cook SC noted that the decision to outsource the task of dealing with investor queries was made because Link’s rates to perform the services were lower than the administrators’ rates.

33 In addition, the administrators incurred costs of $27,785 in holding the first meeting of creditors, which included room hire, voice recording, video and transcription. Similar costs are expected to be incurred in holding the second meeting of creditors.

34 Mr Quinlan’s evidence was that the administration expenses incurred to date and anticipated to be incurred are substantially incurred for the benefit of the investor creditors who total 12,599 compared to only 25 trade creditors. Mr Quinlan expressed the view that “almost every aspect of the administration has linked back to the investor creditors whereas comparatively minimal work in relation to the trade creditors has been required”.

Funds the subject of the orders

35 The relevant funds are:

(1) NAB Account no. 946205445;

(2) NAB Account no. 308580742;

(3) funds paid into the Johnson Winter & Slattery (“JWS”) Trust Account; and

(4) a term deposit of $1.6 million in Bankwest Account No. 4646460.

NAB Account no. 946205445

36 At the start of the administration, there was $517,193.94 available in this account. The administrators were informed by Mr Worboys and employees of the company that this account contained only company funds.

37 Trading expenses of $248,450 have been paid from this account to date.

NAB Account no. 308580742

38 At the start of the administration, this account held $82,645.47. As at 25 January 2018, no funds had been withdrawn from the account.

39 On the basis that the amount was transferred from NAB Account no. 946205445, the administrators considered that these were apparently company funds.

JWS Trust account

40 On 2 August 2018 (that is, shortly before the start of the administration), the company paid $100,000 into the JWS trust account. Also before the administration, legal fees totalling $21,596.76 were paid from this amount. On 21 December 2018, Mr Quinlan and Mr Worboys instructed JWS to pay $52,051.83 to the administrators’ bank account and to pay $11,295.56 to Metaquotes in satisfaction of its outstanding invoices. This has left a balance of $14,045.85.

Term deposit

41 The company held $1.6 million in a term deposit with Bankwest (“term deposit”). The term deposit expired on 21 January 2019 and the administrators gave instructions to Bankwest not to roll it over.

42 A balance sheet of the company prepared by the company’s accountants, Moore Stephens, as at 29 November 2018 shows the term deposit as an asset of the company.

43 It is a requirement of holding the company’s AFSL that the company be solvent. Mr Quinlan was told the following by Mr Worboys concerning the source of the term deposit:

(1) The term deposit originated from $5.5 million in company funds held in an old bank account known as the Saxo Allocated Account (account No. 845127). Those funds were proceeds received by the company on 10 December 2010 following the issuance of preference shares to Australian Mutual Holdings Limited (“AMH”) in its capacity as responsible entity of Trident Global Growth Fund.

(2) Since that time, the funds have been placed in a series of term deposits. At the expiry of a term deposit, the funds would typically be paid back into a general Halifax account until a new term deposit is arranged.

(3) There have been two reductions in those funds over time:

(d) in June 2015, the company advanced NZ$1,200,000 to Halifax NZ as a subordinated secured loan; and

(e) in August 2015, the company paid $2,750,000 to buy-back half the preference shares on issues to AMH.

(4) The funds were placed on term deposit at the insistence of Moore Stephens to better demonstrate that the funds were company funds and not investor funds and, therefore, available to support the company’s adjusted surplus liquid funds requirements under the AFSL. Moore Stephens has been responsible for calculating the company’s adjusted liquid surplus funds since 2011.

44 The administrators have undertaken a trace of the term deposit. As at 22 January 2019, Mr Quinlan’s evidence was that he was not aware of any evidence to suggest that the term deposit is not the beneficial property of the company. However, since the funds constituted by the term deposit have gone through other accounts, there could be a suggestion that the term deposit funds have been co-mingled with investor funds.

45 By affidavit affirmed 24 January 2019, Mr Quinlan referred to a review of bank statements which indicated that, between September 2014 and August 2016, the balance in the account in which the term deposit funds were then held “dipped below the amounts that one would expect the term deposit to be at various points in time during that period”.

46 As Mr Cook put it, the administrator is of the view that the term deposit is property of the company but does not suggest that the Court could make a finding to that effect on the currently available evidence.

Difficulty in tracing funds

47 In my previous judgment, I noted that the company held 38 bank accounts. There were 41 bank accounts when the administrators were appointed.

48 Mr Quinlan gave evidence that the administrators are in the process of tracing the various funds held in the company’s bank accounts for the purpose of determining, to the extent possible, what funds are company funds and what funds are investor funds.

49 However, it is his view that the funds of the company are irreversibly deficient and mixed and it is not reasonable or economically practical to trace all of the funds held by the company, for reasons detailed in his 22 January 2019 affidavit.

50 In circumstances that are not explained in the evidence, and while the administrators maintain that the funds referred to in NAB Account no. 946205445, NAB Account no. 308580742 and the JWS trust account “appear to be company funds”, they have become aware that those accounts may also contain co-mingled funds.

Relief sought

51 The relief was sought because of the uncertainty that has arisen as to the beneficial ownership of the four funds identified above.

52 The administrators were concerned that, in using the funds to defray what they consider to be necessary expenses incurred, and to be incurred, by the company, they may be found at some later point to have dealt with trust funds, thereby exposing them to personal liability for those funds.

53 If, or to the extent that, the funds are the company’s funds, the administrators do not need the relief sought. However, the administrators consider that the present incomplete knowledge as to ownership of the funds mandates that they treat the funds as if they might be trust funds.

54 The administrators noted that, ordinarily, the costs of running the trading platforms and associated expenses, as well as the administration of the company, should be borne by the company from its own funds. However, they argued that, in the circumstances of this case, those costs can be seen as the costs of protecting the funds of investors and should be treated as costs incidental to the realisation of those funds: cf. In re Universal Distributing Co. Ltd (in liquidation) [1933] HCA 2; (1933) 48 CLR 171 at 174.

55 The administrators identified the following propositions relevant to whether the Court should give directions:

a. The Court’s power under s 90-15 to determine a question arising in the external administration of a company is at least sufficient to support an application by an administrator for direction of the kind that could formally have been made under s 447D of the Act, now repealed: In the matter of Australian Institute of Professional Education Pty Ltd (in liq) [2018] NSWSC 1028 at [2] per Black J.

b. An administrator’s power to approach the Court for directions under the Act is designed to facilitate the administrator’s functions and should be interpreted widely to give effect to that intention: Re One.Tel Networks Holdings Pty Ltd [2001] NSWSC 1065; (2001) 40 ACSR 83 (referring to s 447D, now repealed).

c. The Court may give directions to provide guidance on matters of law or to protect the administrator against accusations that they have acted unreasonably: In the matter of Bevillesta Pty Limited (In Voluntary Administration) Application under Corporations Act: Martin John Green and Peter Paul Krejci as Voluntary Administrators of Bevillesta Pty Limited (ACN 008 428 162) [2011] NSWSC 417; (2011) 254 FLR 324; 84 ACSR 215 at [10].

d. A direction under this section protects the administrator from liability for breach of duty or unreasonable behaviour if full disclosure was made to the Court: Re Ansett Australia Ltd [2001] FCA 1439; (2001) 39 ACSR 355 at [59]-[62].

e. Section 63(1) of the Trustee Act 1925 (Cth) (“Trustee Act”) permits a trustee to apply to the Court for an opinion, advice or direction on any question respecting the management or administration of the trust property and the proper purpose for seeking judicial advice includes relief aimed at resolving legitimate doubts held by the trustee as to the proper course of action and protecting the trust and those entitled to it: In the matter of International Art Holdings Pty Ltd (Admin Apptd); International Art Holdings Pty Ltd (admin apptd) & Ors v Adams & Ors [2011] NSWSC 164; 85 ACSR 1 at [36]-[37].

f. Section 81 of the Trustee Act permits a trustee to apply to Court for the power to incur expenditure which is in the opinion of the Court expedient but where the trustee does not have the power to do so under the instrument creating the trust, if any, or by law.

g. Since the Court has jurisdiction to hear this application in respect of the relief sought under the Act, and since the facts underlying the relief sought both under the Act and the Trustee Act are the same, this Court has accrued jurisdiction to grant relief under the Trustee Act: Hodges v Waters (No 7) [2015] FCA 264; 232 FCR 97 per Perram J at [40]-[53].

56 Next, the administrators identified the following principles relevant to whether they should be allowed to defray expenditure from trust assets:

(1) As the maintenance of the trading platforms was a function that Halifax was required to perform before it went into administration, it is within the statutory functions of the administrators to continue to perform the obligation of maintaining the trading platforms: White, in the matter of Mossgreen Pty Ltd (Administrators Appointed) v Robertson [2018] FCAFC 63 at [21]. In Mossgreen, which concerned an auction house, the Full Court concluded, relevantly, at [21], that:

It was “within the statutory functions of the administrators to continue to perform the function of holding … consigned items and, as part of doing so, to take steps in respect of the systems for the management and return of the consigned items. These are functions which Mossgreen and its officers would be expected to perform if the company was not under administration and were therefore activities that formed part of the administration: s 437A(1)(d)”.

(2) If costs are incurred by an administrator in performing statutory responsibilities necessary to identify, preserve and facilitate the return to the owners of their property (in this case, the return of investor funds) then a lien may arise over the trust property in respect of those costs. Thus, in Mossgreen at [22]-[23], the Full Court continued:

[22] Further, if costs have truly been incurred by an administrator in performing statutory responsibilities necessary to identify, preserve and facilitate the return to the owners of their property then a lien (whether statutory under s 443F or in equity) may arise over the company’s property or the property owned by the consignors in respect of those costs. What was claimed here was an equitable lien over the property of the consignors.

[23] There is no general principle which covers the diversity of cases in which an equitable lien has been held to be created: Stewart v Atco Controls Pty Ltd (in liq) [2014] HCA 15; 252 CLR 307 at 318 [14] approving Gibbs CJ in Hewett v Court [1983] HCA 7; 149 CLR 639 at 645. In our view, there can be such a lien in favour of administrators in respect of costs incurred in dealing with claims for the return of items even where there is no claim to ownership by the company under administration, including costs in holding them and keeping them secure in the meantime. This is but a small step from the circumstances in which a lien has been recognised in other cases.

(3) In relation to the use of trust funds to pay the expenses in winding up (which it is submitted apply analogously to a voluntary administration), Brereton J (as his Honour then was) set out the relevant principles in AAA Financial Intelligence Ltd (in liq) [2014] NSWSC 1004 at [13]:

(1) Where the company is trustee of a trading trust and has no other activities, the liquidators are entitled to be paid their costs and expenses, whether for administering the trust assets or for “general liquidation work”, out of the trust assets: Re Suco Gold Pty Ltd (1993) 33 SASR 99; 7 ACLR 873; Grime Carter & Co Pty Ltd v Whytes Furniture (Dubbo) Pty Ltd [1983] 1 NSWLR 158; Re French Caledonia Travel Service Pty Ltd (in liq) [2003] NSWSC 1008; (2003) 59 NSWLR 361; Bastion v Gideon Investments Pty Ltd (in liq) (2000) 35 ACSR 466 at 480 [70]; In the matter of North Food Catering Pty Ltd [2014] NSWSC 77.

(2) Where the company does not act solely as trustee, costs and expenses referable to work done in relation to trust assets which may nonetheless be considered as having been done for the purpose of winding up the company ought ordinarily be borne primarily by the (non-trust) property of the company, to the extent that the assets permit: Re GB Nathan & Co Pty Ltd (in liq) (1991) 24 NSWLR 674 at 685-689; Re Greater West Insurance Brokers Pty Ltd [2001] NSWSC 825; (2001) 39 ACSR 301; French Caledonia at [209].

(3) At least where the non-trust assets do not permit that course, and perhaps even when they do, a liquidator is entitled to be indemnified out of trust assets for his costs and expenses, but only to the extent that they are referable to administering the trust assets: 13 Coromandel Place Pty Ltd v CL Custodians Pty Ltd (in liq) (1999) 30 ACSR 377 at 385; French Caledonia at [211], [213]. This is pursuant to the court’s equitable jurisdiction to allow a trustee remuneration costs and expenses out of trust assets, which extends to a person such as a liquidator who is, for practical purposes, controlling a trustee: Berkeley Applegate (Investment Consultants) Ltd; Harris v Conway [1989] Ch 32 at 50–51; Re Application of Sutherland [2004] NSWSC 798; (2004) 50 ACSR 297; Trio Capital Ltd (Admin App) v ACT Superannuation Management Pty Ltd [2010] NSWSC 941; (2010) 79 ACSR 425; In re MF Global Australia Ltd (in liq) (No 2) [2012] NSWSC 1426, [55]; Alphena Pty Ltd (in liq) v PS Securities Pty Ltd atf Joseph Family Trust [2013] NSWSC 447; (2013) 94 ACSR 160.iv.

(4) In principle, where the liquidator does work which would entitle him both to remuneration as liquidator by the company, and recovery from the trust assets, there are two funds liable and there should be contribution between them. However, where there are no assets of the company available, it is unnecessary to consider the question of contribution. If a liquidator has done work which is attributable equally to the winding up of the company and the administration of trust assets, and there are no assets of the company at all to meet his expenses in doing so, the expenses are payable solely from the trust assets: French Caledonia at [212].

(5) Where the liquidator is administering, through the company of which he/she is liquidator, more than one trust, the liquidator is not entitled to charge the beneficiaries of one trust with the costs and expenses incurred in relation to the other, although where allocation is not possible a pari passu allocation may be permitted: Re Suco Gold at 882–3; 13 Coromandel at 386.

(4) Where a liquidator wishes to dispose of trust property to meet their right of indemnity, the liquidator should approach the Court for authority: Jones v Matrix Partners Pty Ltd, Re Killarnee Civil & Concrete Contractors Pty Ltd (in liq) [2018] FCAFC 40 at [44] and [91] per Allsop CJ, [139] per Siopis J.

Why administrators are justified in using the relevant funds

57 Applying the principles set out above, I accepted that the administrators should be given a direction in the terms they sought, covering the NAB Account no. 946205445, NAB Account no. 308580742, the JWS trust account and the term deposit, for the reasons identified by the administrators. In essence, to the extent that the funds are investors’ funds, the administrators are justified in using the funds to pay the trading expenses and the relevant administration expenses because those expenses have been incurred entirely or substantially for the purpose of protecting investor funds. In particular:

(1) The uncertainty as to the ownership of the funds justifies the administrators refraining from any further expenditure of those funds without applying to the Court for directions and judicial advice. The administrators’ expectation, based on their dealings with the trading platform providers, is that their access to the platforms will be terminated if they continue to refrain from paying expenses incurred.

(2) The maintenance of the trading platforms and associated expenses incurred as a result of the maintenance of those trading platforms will benefit the beneficiaries of the trust money held by the company, namely investors, as it will allow an orderly exit from their investments and preserve the ability of the administrators (and any liquidator) to ascertain the extent of their funds and outcomes of trades. Conversely, if the platforms are not maintained, the investors are likely to be adversely affected by the increased costs and delays in dealing with their future claims.

(3) The maintenance of the trading platforms, as an incident of the business conducted by the company and to allow the administrators to determine the liability of the company to the investor clients, is required to permit the administrators to discharge their statutory duty as administrators and, in due course, may be required to permit a liquidator to perform their functions.

(4) The costs of maintaining the platforms appear to be proportional to the benefits that the investors will receive in that, on the assumption that the funds are investor funds, they will have a limited impact on the expected dividend that investors may receive (if all the term deposit funds are used, the expected dividend will decrease from 91.47 cents per dollar to 90.71 cents per dollar): cf AAA Financial; Mossgreen.

(5) In the event that the funds are found to be intermingled with trust money, the administrators would be entitled to an equitable lien (if not a statutory lien) over the funds to recover expenses incurred in maintaining and returning the trust funds.

(6) It is appropriate that the Court gives a direction, in all the circumstances, that the administrators were justified in using the funds they have to defray these expenses and will be justified in using the balance of the funds likewise.

(7) To the extent that the administrators propose using the funds to pay administration expenses (rather than costs relating directly to the maintenance of the trading platforms), given that there are no other funds available to the administrators to meet these expenses, it is appropriate that, to the extent that the funds are found to be trust funds or intermingled funds, such funds are made available to the administrators to perform their statutory functions, the exercise of which will benefit the investor clients through the orderly determination of their claims and the repayment of their investments as part of the administration (or a possible winding up). As noted above, the evidence of Mr Quinlan was that almost every aspect of the administration has linked back to the investor creditors and comparatively minimal work has been done in relation to the trade creditors.

58 Mr Cook SC submitted that the orders sought would not prejudice the interests of non-investor creditors because, if the term deposit turns out to be the company’s money (as expected), then the right of indemnity for recoupment of those moneys will be property available to the company which will be recoverable for the substantial trust assets.

59 I considered whether the direction should be limited to future expenditure but, once satisfied that it was appropriate to give the direction to that extent, there did not appear to be any principled basis on which to decline to give a direction in the wider terms sought.

60 Further, I considered whether the direction should be limited to the identified trading expenses but was satisfied that there was no principled basis for that limitation either.

Ancillary orders permitting application to vary orders made

61 I accepted that it was appropriate to make the orders sought for the giving of notice of the orders made in electronic form. I accepted that the form of orders struck the appropriate balance between the need to take appropriate steps to give notice to creditors, on the one hand, and, on the other hand, the need to avoid costs in giving such notice that otherwise operate to the detriment of creditors generally: In the matter of Renovation Boys Pty Ltd (admins apptd) [2014] NSWSC 340 at [38]-[40] per Black J.

62 I also accepted that the proposed orders provided interested parties with a reasonable opportunity to seek a variation of the orders. As Mr Cook SC noted, the effect of the orders is that the administrators are at risk that they will not continue to have the benefit of the Court’s direction and judicial advice in the event that a variation to that effect is successfully sought.

Other matters

63 ASIC and the committee of inspection appointed at the company’s first meeting of creditors were given notice of the ex parte application. Neither ASIC nor any member of the committee of inspection sought to appear on the hearing of the application.

64 ASIC did not oppose the administrators accessing the term deposit covered by the orders but stated that any DOCA which contemplated the lifting of the suspension of the AFSL would require reinstatement of the term deposit. Otherwise, ASIC’s position was the administrators should take their own advice in relation to the application.

65 The committee of inspection was notified of the proposed application at a meeting on 11 January 2019. However, at that stage, it seems that the funds were believed to be company funds. Accordingly, the position of the committee of inspection on the basis of the most recent facts is not known.

I certify that the preceding sixty-five (65) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: