FEDERAL COURT OF AUSTRALIA

The Owners – Units Plan No. 3115 v The Trustees of the Master Builders Fidelity Fund Scheme [2019] FCA 115

ORDERS

THE OWNERS - UNITS PLAN NO. 3115 Applicant | ||

AND: | THE TRUSTEES OF THE MASTER BUILDERS FIDELITY FUND SCHEME Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The amended originating application dated 15 April 2018 be dismissed.

2. The applicant must pay the respondent’s costs, as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

1 This proceeding raises important issues regarding the operation of a fidelity fund scheme in the Australian Capital Territory (ACT). The scheme provides some consumer protection to residential property owners in respect of residential building work carried out by fidelity fund approved licensed builders in the ACT. The central issue is the nature and extent of that protection in the particular circumstances here.

2 The applicant is the owners corporation for Units Plan No. 3115. The plan relates to a building at 10 Thynne Street, Bruce, which comprises 120 residential units and four commercial units, which building was certified fit for occupation on 25 May 2007. The building is known as the Elara Apartments (Elara). The respondent is the trustee of a fidelity fund scheme (Fidelity Fund Scheme) established under the Master Builders Fidelity Fund Trust Deed (Deed).

3 B & T Developments (ACT) Pty Ltd was the developer of Elara (the developer). The respondent (the trustees) issued multiple fidelity certificates to the developer for residential building work to be carried out at Elara. B & T Constructions (ACT) Pty Ltd was nominated as the builder of the development (the builder).

4 The applicant claims that upon completion of the Elara development, it became the holder of a leasehold estate of the common property of the premises, which it is liable to maintain. It alleges that the building work carried out by the builder was not carried out in accordance with the Building Act 2004 (ACT) (the 2004 Act), with the plans approved for the work, in a proper and skilful way and with good and proper materials. It further alleges that, consequently, defects exist in the common property, load bearing walls, balconies and utility services. The cost of rectifying the defects is estimated at more than $19m, which is only slightly less than the cost of the initial project. The applicant alleges that the builder has breached the statutory warranties applicable to the development. It further claims that it lodged claims on the Fidelity Fund pursuant to the fidelity certificates, but the claims were rejected by the trustees on the basis inter alia that the claims were not submitted in the proper form and/or did not arise within the time periods specified in the relevant legislation or during the currency of any of the fidelity certificates. As will shortly emerge, two separate claims were made on the Fidelity Fund.

5 The applicant seeks declaratory relief to the effect that the trustees were not entitled under the Deed and the fidelity certificates to reject the claims on the Fidelity Fund.

6 It is appropriate to note at the outset that many of the issues which require determination in this proceeding have been made more difficult by anomalies in the drafting of various written instruments, including the Deed and the fidelity certificates, as well as some of the surrounding legislative instruments. The complexity of the Fidelity Fund Scheme was noted in the recent decision of the Court of Appeal of the Supreme Court of the Australian Capital Territory in Koundouris v The Owners – Units Plan No 1917 [2017] ACTCA 36; 323 FLR 375 at [11] and [12], a decision which raised different issues to those in this proceeding. The complexity is compounded by the multiple changes which have been made in the legislative regime since 2002, not all of which have been reflected in the administrative documents.

Summary of other relevant background facts

7 Construction of Elara commenced in June 2005. Under s 37(3) of the 2004 Act (as at June 2005), the builder was required to provide a residential insurance policy, a certificate of insurance, or a fidelity certificate for the residential building work at the time the builder applied for a commencement notice in respect of the proposed residential building work. On 18 May 2005, the builder applied to the Fidelity Fund for fidelity fund coverage for the Elara Apartments. On the same day, the Fidelity Fund issued an invoice in the amount of approximately $105,000. This sum was subsequently paid by the builder on 16 September 2005. On 18 May 2005, 120 fidelity certificates were issued in respect of each of the residential units to be constructed at Elara.

8 On 25 May 2007, a certificate of occupancy was issued for Elara.

9 On 7 July 2007, Units Plan 3115 for Elara was registered. This resulted in the cancellation of the previous Crown lease for the relevant land and the grant of 125 new Crown leases, comprising 120 Crown leases for the residential units, 4 Crown leases for the commercial units and 1 Crown lease to the owners corporation for the common property.

10 On one view, on 26 May 2012, the 120 fidelity certificates for each of the residential units expired because five years had lapsed after the certificate of occupancy was issued (see s 90(1)(c) of the 2004 Act and reg 26 of the Building Regulations 2004 (ACT) (the 2004 Regulations)). This is a significant issue and date for the purpose of the proceeding.

11 From 26 May 2012 to date, eleven units in Elara have been sold to new owners. There is an issue whether those successors in title have any rights to make a request under the fidelity certificates if the cover provided by the Fidelity Fund Scheme had expired before the eleven units were transferred to the new owners.

12 On 17 May 2013, the applicant commenced proceedings in the ACT Supreme Court against the builder for breach of statutory warranties. On 18 May 2017, external administrators were appointed to the builder. On 20 July 2017, liquidators were appointed to the builder. The Supreme Court proceedings were then stayed. The liquidators advised that unsecured creditors were unlikely to recover anything in the liquidation.

13 On 18 August 2017, the applicant lodged a claim with the trustees. The trustees noted that:

(a) the claim was not executed;

(b) an amount of $10.2m was claimed in compensation (in circumstances where there is a maximum of $85,000 for each fidelity certificate); and

(c) the claim stated that it was a claim under the statutory warranty.

14 The 18 August 2017 claim (the first claim) was rejected by the trustees on 23 November 2017 on the stated basis that the claim “was not submitted, nor did the basis of the claim arise, within the time period set out within the relevant legislation, or during the currency of any of the Fidelity Certificates issued for these units”.

15 Shortly thereafter, on 18 December 2017, the present proceedings were commenced in this Court.

16 Between May and June 2018, 66 unit owners purported to assign to the owners corporation their rights to claim under the fidelity certificates for their respective units. There is an issue whether such assignments are valid in the case of the eleven owners who acquired their units after 26 May 2012, that being the date which the trustees say was when the fidelity certificates expired.

17 On 5 July 2018, the applicant lodged a further claim as assignee of the rights of 66 unit owners (the second claim). This claim was rejected by the trustees on 3 August 2018 for several reasons, including that the applicant had not lodged an executed claim in proper form and the claim was out of time because the fidelity certificates had expired several years before any claimable event. Moreover, the trustees stated that the claim had been made more than 90 days after the builder went into liquidation, contrary to the requirement in s 90(1)(i) of the 2004 Act, and there was no assignment of any of the rights under various of the fidelity certificates.

18 On 3 August 2018, the applicant emailed a copy of an executed claim form with the aim of regularising the claim made on 5 July 2018 (and presumably in response to the trustees’ claim that the earlier claim was not in proper form). The executed claim form was said to be made under all 120 fidelity certificates for Elara and not just the certificates for the 66 units whose owners had purported to assign rights to the owners corporation. It claimed $10.2m from the Fidelity Fund, which represents almost twice the maximum amount available to the 66 unit owners who had assigned their rights to the owners corporation.

The Fidelity Fund Scheme

19 Prior to amendments which were made in May 2002 to the Building Act 1972 (ACT) (1972 Act), which amendments introduced the fidelity fund scheme which is the subject of these proceedings, Pt 5A of the legislation contained provisions dealing with statutory warranties (s 58C) and residential building works insurance (s 58E). The need for reform was highlighted by the withdrawal of a home warranty insurer from the ACT market in early 2002. The Building Amendment Act 2002 (ACT) introduced into Pt 5A the framework for a fidelity fund scheme (Div 5A). The amendments provided for the approval of a building industry fidelity fund scheme governed by a trust deed. It was stated that the scheme was intended to provide a similar level of consumer protection as home warranty insurance (see page 2 of the Explanatory Memorandum to the Building Amendment Bill 2002).

20 In the Presentation Speech to the 2002 amendments, the then Minister for Planning, Mr Corbell, explained that the amendments were in response to what he described as “a potential crisis in the ACT building industry caused by the withdrawal of [an] insurance broker… from the market for residential building work insurance”. The Minister noted that the 1972 Act required builders to have insurance before they could begin work and that insurance protected consumers if the builder went bankrupt, died, or for some other reason failed to complete construction and could not be located. He added that, once construction is complete, homebuyers receive a further five year warranty against construction faults. The Minister explained that the ACT Government’s objective was to provide choices in the market place, by establishing a fidelity fund scheme. The Minister stated that the Government was not underwriting the scheme. He further explained, however, that since the amendments introduced a new approach to building warranty, and because “it is not an insurance scheme”, a range of safeguards had to be put in place because safeguards under an insurance-based scheme, including the protection provided by Insurance Act 1973 (Cth), would not apply. Finally, the Minister noted that, under the scheme, consumers “will be afforded protection through the issue of fidelity certificates”.

21 It is common ground that, following enactment of the Building Amendment Act 2002 (ACT), Pt 5A of the 1972 Act was restructured so as to accommodate the new fidelity fund scheme (which was the subject of Div 5A.4). Various provisions of the legislation were also renumbered. Those changes were then shown in Republication No 7 of the 1972 Act. Under Republication No 7, Pt 5A was renumbered Pt 6 and Divs 5A.12 and 5A.6 were renumbered as Divs 6.12 and 6.6 respectively. The subject of statutory warranties was dealt with in s 62. Section 64 dealt with residential building work insurance (which had previously been dealt with in s 58E). Division 6.4 dealt with approved fidelity fund schemes.

22 Under s 58H, the Minister was empowered to approve a fidelity fund scheme, but this could occur only if the scheme complied with the approval criteria (s 58H(3)).

23 Under s 58K of the 1972 Act (as inserted by the 2002 amendments) the Minister was empowered to determine requirements (described as “approval criteria”) with which a fidelity fund scheme had to comply to be an approved scheme. Section 58K (which subsequently became s 70 in Div 6.4 of the 1972 Act) provided:

58K Approval criteria for fidelity fund schemes

(1) The Minister may, in writing, determine requirements (the approval criteria) for this Act with which a fidelity fund scheme must comply to be an approved scheme.

(2) The approval criteria must include requirements in relation to—

(a) the management of the fidelity fund scheme in accordance with the trust deed; and

(b) qualifications or suitability for appointment as a trustee of the scheme; and

(c) the powers and duties of the trustees; and

(d) the financial management of the scheme; and

(e) the building work for which a fidelity certificate may be issued or must not be issued under the scheme; and

(f) the people who can or cannot make claims under a fidelity certificate; and

(g) applications for claims under fidelity certificates issued under the scheme; and

(h) dealing with claims under the scheme; and

(i) compliance with the prudential standards.

(3) The approval criteria may apply, adopt or incorporate a law or instrument, or a provision of a law or instrument, as in force from time to time.

Note 1 The text of an applied, adopted or incorporated law or instrument, whether applied as in force from time to time or as at a particular time, is taken to be a notifiable instrument if the operation of the Legislation Act 2001, s 47 (5) or (6) is not disapplied (see s 47 (7)).

Note 2 A notifiable instrument must be notified under the Legislation Act 2001.

(4) A determination is a disallowable instrument.

Note A disallowable instrument must be notified, and presented to the Legislative Assembly, under the Legislation Act 2001.

24 The Minister was empowered under s 58O to determine prudential standards that must be complied with by an approved scheme. It was made an offence for the trustees to fail to ensure that a scheme complied with such standards (s 58P). Under s 58S, the Minister was empowered to suspend or cancel the approval of an approved scheme on specified grounds.

25 Pursuant to s 58K of the 1972 Act, the approval criteria for a fidelity fund scheme were established by the Building (Approval criteria) Determination 2002 DI 2002-49 (Approval Criteria), which remains current. The Explanatory Statement to this Determination stated that the effect of cll 4 to 8 of the Approval Criteria was to “impose on fidelity funds the same standard of protection for consumers as is currently required of an insurer” (Explanatory Statement, p 2). The relevant features of the Approval Criteria are summarised at [46]-[48] below.

26 The Master Builders Fidelity Fund Scheme was approved by the Minister on 21 June 2002 under what by then had become Pt 6 of the 1972 Act. It commenced to operate immediately under the provisions of an unexecuted draft fidelity trust fund deed, which was eventually executed on 10 September 2002.

27 The key relevant features of the Deed are summarised at [49]-[60] below.

28 The prudential standards applying to the management of the fidelity fund scheme were set out in the Building (Prudential Standards) Determination 2002 – Disallowable Instrument DI 2002-48 (the 2002 Determination). The 2002 Determination was revoked and replaced in 2005 by the Building (Prudential Standards) Determination 2005 – Disallowable Instrument DI 2005-250 (2005 Prudential Standards).

29 The 2005 Prudential Standards were made by the Minister under s 103 of the 2004 Act. They set out matters relating to the sound financial management of the scheme. Clause 32 requires the trustees to ensure that the scheme is maintained solely for the following purposes (emphasis added):

(a) the provision of a fidelity certificate to an owner in accordance with the Act and the trust deed;

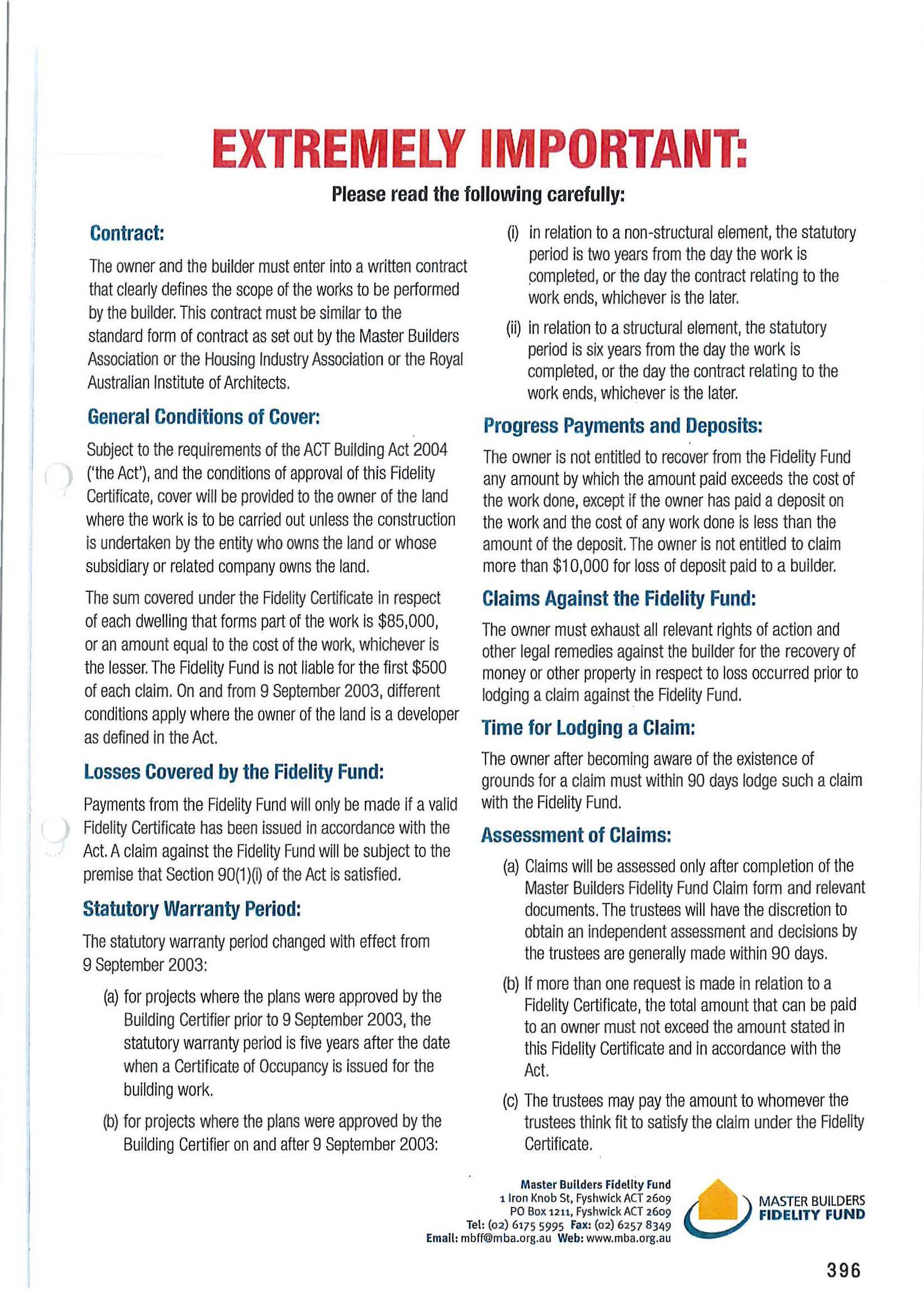

(b) the payment of an amount to an owner pursuant to a fidelity certificate in accordance with the Act and the trust deed;

(c) any other purpose that the Minister may in writing determine.

Key provisions of the Fidelity Fund scheme summarised

30 The key relevant documents appear to be various provisions of the 1972 Act, the 2004 Act, the Approval Criteria, the Deed and the fidelity fund certificates. It is appropriate to outline each of them in turn.

(a) 1972 Act

31 The 1972 Act initially provided only for insurance for residential building work.

32 Section 64(1) (which previously was numbered s 58E(1)) set out the requirements for residential building work insurance policies. It relevantly provided:

An insurance policy issued in relation to residential building work complies with this section if-

…

(c) if the builder is not the owner of the land where the work is to be carried out - it insures the owner and the owner's successors in title for the period beginning on the date when the certifier in relation to the work receives a notification under s 37A(l) or (2) in relation to the builder and ending the prescribed period after the date when a certificate of occupancy is issued for the work; and

(d) if the builder is the owner of the land where the work is to be carried out - insures the builder's successors in title for the period beginning on the date when the title in the land is transferred to another person and ending the prescribed period after the date when a certificate of occupancy is issued for the work; and

…

(f) it insures the owner (if the builder is not the owner) and the owner's successors in title against the risk of being unable to enforce or recover under the contract under which the work has been, is being or is to be carried out because of the insolvency, disappearance or death of the builder; and

(g) it insures the owner (if the builder is not the owner) and the owner's successors in title against the risk of loss resulting from a breach of a statutory warrant; and

(h) it insures the owner (if the owner is not the builder) and the owner's successors in title against the risk of loss resulting, by virtue of the builder's negligence from the subsidence of the land; and

(i) it provides that a claim under it may only be made within the prescribed period (or some specified longer period) after the claimant becomes aware of the existence of grounds for the claim; and

(j) the form of the policy has been approved in writing by the building controller.

33 The prescribed period as referred to in s 64(1)(c) and (d) (previously s 58E(1)(c) and (d), and now s 90(1)(c) and (d) was five years after a certificate of occupancy is issued for the work (see reg 20 of the Building Regulations 1972 (ACT) (now repealed). As noted in [38] and [41] below, for approximately one year between 9 September 2003 and 1 September 2004, the prescribed period of cover operated from the “completion day” as defined, but that has no significance in this proceeding.

34 It is common ground that the prescribed period as referred to in s 64(1)(i) (which relates to the period within which a claim must be made) was at all material times 90 days after the claimant became aware of the existence of grounds for the claim.

35 Following the restructuring of the 1972 Act in 2003, consumer protection provisions relating to residential buildings were set out in Pt 6. The key relevant elements were:

(a) residential building warranties created by Div 6.2 (particularly s 62);

(b) residential building insurance in Div 6.3 (particularly s 64); and

(c) approved fidelity fund schemes as dealt with in Div 6.4.

36 Section 62(1) of the Act set out statutory warranties which were incorporated into residential building contracts. Section 62(2) stated that each of the owner's successors succeeded to the rights of the owner in relation to the statutory warranties.

37 Sub-section 62(3) provided that the warranties ended at the end of the "prescribed period" after the date when a certificate of occupancy was issued for the building or the building work. Under reg 19 of the Building Regulations 1972 (ACT) the prescribed period was originally five years from that date.

38 It may be noted that the prescribed period of cover was altered on 9 September 2003 by virtue of the commencement of the Building (Residential Building Warranty) Amendment Act 2003 (ACT) (the 2003 Amendment Act). The 2003 Amendment Act amended both the 1972 Act and the Building Regulations 1972 (ACT). Section 62(3) of the 1972 Act was amended so that the prescribed period for calculating the length of the statutory warranties commenced after the ‘completion day’. ‘Completion day’ was a defined term introduced by the 2003 Amendment Act. It was defined in s 59A to be the

day the work is completed, or the day the contract for the work ends (whichever is later),

or if both of those days are after a certificate occupancy is issued, the completion date is deemed to be the date the certificate of occupancy is issued.

39 The Building Regulations 1972 (ACT) were amended by the 2003 Amendment Act so that the prescribed period in reg 19 for the purpose of the operation of the statutory warranties was 6 years after the ‘completion day’ in relation to structural elements, and 2 years after the ‘completion day’ in relation to non-structural elements, instead of 5 years as was the case previously. These changes effected by the 2003 Amendment Act were translated into the subsequent iterations of the regulations: the Building Regulation 2004 (ACT) and the Building (General) Regulation 2008 (ACT).

40 Thus, post the 2003 Amendment Act, the period of cover and the period within which the statutory warranties operated were no longer in alignment. Previously, the period for both was five years. Post the 2003 Amendment Act the period of cover remained at 5 years, but the statutory warranty period changed to 6 and 2 years, as explained in [39] above. The extrinsic materials cast no light on this apparent anomaly and it is difficult to discern any rational explanation for it. The Explanatory Statement to the Bill which became the 2003 Amendment Act states that the change in the period for which warranty protection applies to completed residential buildings was changed to 6 and 2 years for structural and non-structural defects respectively so as to bring this aspect of the ACT legislative regime into line with recent changes in NSW and Victoria and so as more closely to align with the periods in which faults in these categories can be expected to become apparent. Nothing was said about the non-alignment with the period of cover.

41 A further curiosity is that when the 1972 Act was repealed and replaced by the 2004 Act on 1 September 2004, the date for calculating the prescribed period of residential building insurance cover had returned to the date the certificate of occupancy was issued, rather than the ‘completion day’ which, however, remained the applicable statutory criterion for calculating the period of the statutory warranties. Again, the extrinsic materials provide no light on these matters.

(b) 2004 Act

42 On 1 September 2004, the 1972 Act was repealed and was replaced by the 2004 Act. It is common ground that ss 62 and 64 of the 1972 Act, which dealt respectively with statutory warranties and residential building works insurance, were replaced by ss 88 and 90 respectively of the 2004 Act. Those provisions are as follows:

88 Statutory warranties

(1) By force of this section, every contract for the sale of a residential building, and every contract to carry out residential building work to which the builder is a party, is taken to contain a warranty under this section.

(2) The builder warrants the following in relation to residential building work:

(a) that the work has been or will be carried out in accordance with this Act;

(b) that the work has been or will be carried out in a proper and skilful way and—

(i) in accordance with the approved plans; or

(ii) if the work involves or involved handling asbestos or disturbing friable asbestos—in accordance with approved plans that comply with this Act in relation to the asbestos;

(c) that good and proper materials for the work have been or will be used in carrying out the work;

(d) if the work has not been completed, and the contract does not state a date by which, or a period within which, the work is to be completed—that the work will be carried out with reasonable promptness;

(e) if the owner of the land where the work is being or is to be carried out is not the builder, and the owner expressly makes known to the builder, or an employee or agent of the builder, the particular purpose for which the work is required, or the result that the owner desires to be achieved by the work, so as to show that the owner is relying on the builder's skill and judgment—that the work and any material used in carrying out the work is or will be reasonably fit for the purpose or of such a nature and quality that they might reasonably be expected to achieve the result.

(3) Each of the owner's successors in title succeeds to the rights of the owner in relation to the statutory warranties.

(4) The warranties end at the end of the period prescribed under the regulations after the completion day for the work.

(5) In subsection (2):

owner means—

(a) for a contract mentioned in subsection (1) for the sale of a residential building—the person to whom title in the land where the building was built is transferred under the contract; or

(b) for a contract mentioned in subsection (1) to carry out residential building work—the owner of the land where the work is to be carried out under the contract.

90 Complying residential building work insurance

(1) An insurance policy issued for insurable residential building work complies with this section if—

(a) it is issued by an authorised insurer; and

(b) it provides for a total amount of insurance cover of at least the amount prescribed under the regulations, or the cost of the work, whichever is less, for each dwelling that forms part of the work; and

(c) if the builder is not the owner of the land where the work is to be carried out—it insures the owner and the owner's successors in title for the period beginning on the day the certifier for the work issues a building commencement notice under section 37 for the work and ending at the end of the period prescribed under the regulations after the day a certificate of occupancy is issued for the work; and

(d) if the builder is the owner of the land where the work is to be carried out—it insures the builder's successors in title for the period beginning on the day the title in the land is transferred to someone else and ending at the end of the period prescribed under the regulations after the day a certificate of occupancy is issued for the work; and

(e) the whole of the premium payable for the period has been paid; and

(f) it insures the owner (if the builder is not the owner) and the owner's successors in title against the risk of being unable to enforce or recover under the contract under which the work has been, is being or is to be carried out because of the insolvency, disappearance or death of the builder; and

(g) it insures the owner (if the builder is not the owner) and the owner's successors in title against the risk of loss resulting from a breach of a statutory warranty; and

(h) it insures the owner (if the owner is not the builder) and the owner's successors in title against the risk of loss resulting, because of the builder's negligence, from subsidence of the land; and

(i) it provides that a claim under it may only be made within the period prescribed under the regulations, or a stated longer period after the claimant becomes aware of the existence of grounds for the claim; and

(j) the form of the policy has been approved in writing by the construction occupations registrar.

(2) However, if the owner is a developer, the insurance is taken to comply with subsection (1) (c), (f), (g) or (h) if it insures the owner's successors in title, even though it does not insure the owner.

(3) To remove any doubt, an insurance policy issued in relation to insurable residential building work may exclude claims other than those in circumstances in which the builder is insolvent, dead or has disappeared.

(4) In this section:

developer, for insurable residential building work, means a person for whom the work is done in a building or residential development where 4 or more of the existing or proposed dwellings are or will be owned by the person.

43 The provisions relating to approved fidelity fund schemes were set out in Div 6.4 (ss 96 to 110) of the 2004 Act. Section 99 specified the approval criteria for schemes and it was worded in substantially similar terms to s 58K (which subsequently became s 70) of the 1972 Act (see [23] above).

44 Under s 37(3) of the 2004 Act, an application for a building commencement notice in respect of residential building work had to be accompanied by one of the following three documents:

(i) a residential insurance policy for the work;

(ii) a certificate issued by an approved insurer stating that the insurer has insured the work and residential building insurance policy; or

(iii) a fidelity certificate for the work issued by the trustees of a scheme approved under Div 6.4 (the terms “approved insurer” and “residential building work” were defined in s 37(6)).

45 It is also relevant to note that, under s 166 of the 2004 Act, an approved scheme under the 1972 Act, “is taken to be an approved scheme for this Act”. It is common ground that, because of the operation of ss 82 and 88 of the Legislation Act (ACT), s 166 continued to operate even though it no longer appeared in republications of the 2004 Act.

(c) Approval Criteria

46 As noted above, the Approval Criteria were established by a disallowable instrument dated 23 May 2002 (see [25] above). Clause 4 set out matters which must be included in a trust deed in order for it to be approved. Relevantly, cl 4 provided (without alteration):

Fidelity fund trust deed

4. The trust deed must:

(a) require the trustees to assess each application for a fidelity certificate;

(b) allow the trustees to require that, in certain circumstances, a contribution be made to the fidelity fund scheme including for the issue of fidelity certificate;

(c) set out the terms and form of the fidelity certificate to be issued by the trustees;

(d) provide for the issue of a fidelity certificate by the trustees, including a requirement that each fidelity certificate that the trustees issue:

(1) is only issued for residential building work in the ACT that is undertaken by a licensee or a holder of an owner-builder's licence;

(2) is only issued after the full contribution that the trustees require to be paid to the fidelity fund scheme for the issue of the fidelity certificate has been paid;

(3) must state the amount that the owner can request from the trustees under clause 4(f), being at least the amount that is the minimum amount of insurance cover that is required to provided by an insurance policy under section 58E(l)(b) of the Act; and

(4) must state that each of the following matters is at the discretion of the trustees when a request is made by an owner:

(i) whether any payment is to be paid to the owner from the assets of the fidelity fund scheme;

(ii) the amount of any such payment to be paid to the owner; and

(iii) the terms and conditions on which any payment to the owner is to be paid by the trustees from the assets of the fidelity fund scheme;

…

(f) only allow the person (owner) described in column 2 of the table set out below to make a request (request):

(1) in the circumstances set out in column I of the table set out below; and

(2) for the period set out in column 3 of the table set out below,

that the trustees pay to the owner an amount, up to the amount stated on the owner's fidelity certificate, out of the assets of the fidelity fund scheme for a part or the whole of any loss stated in clause 4(i) that the owner has incurred:

Column 1 Circumstance | Column 2 Person covered by the fidelity certificate | Column 3 Period for which the owner is covered |

The owner* is not the builder | The owner* and the owner’s* successors in title of the land on which the residential building work is to be, is being or has been carried out | The period that: • begins on the date on which the certifier in relation to the residential building work receives a notification under section 37A(1) or (2) of the Act in relation to the builder who will carry out the residential building work on the land; and • ends at the expiration of the specified period |

The owner* is the builder | The owner’s* successors in title of the land on which the residential building work is to be, is being or has been carried out | The period that: • begins on the date on which the residential building work is to be, is being or has been carried out is transferred to another person; and • ends at the expiration of the specified period. |

*Note: the word "owner" where used in this table has the same meaning as in the Act.

(g) require that only the amount stated on a fidelity certificate under clause 4(d)(3) can be requested by the owner;

(h) require that, if more than one request is made in relation to a fidelity certificate, the total amount that can be paid to an owner must not exceed the amount that is stated on the fidelity certificate;

(i) state that the types of losses in relation to which a request may be made are only those losses which would be recoverable under an insurance policy under sections 58E(l)(f), (g) and (h) of the Act;

(j) require that a request be made within the period that is the prescribed period for the purpose of section 58E(l)(j) of the Act after the owner becomes aware of the existence of the grounds for making the request;

(k) state how an owner can make a request under a fidelity certificate;

(l) subject to clause 4(m), state how a request will be handled by the trustees;

(m) subject to clause 4(t), require the trustees to consider a request from an owner and determine, in their discretion:

(1) whether the trustees will make a payment from the assets of the fidelity fund scheme in respect of the request;

(2) the amount of any such payment; and

(3) the terms and conditions on which the trustees will make the payment, such terms and conditions to include a right for the trustees to take whatever action they consider appropriate in the name of the owner against the builder to recover from the builder any amount paid by the trustees to the owner;

…

(t) prohibit the trustees from refusing to pay an owner under the fidelity certificate on the grounds that the fidelity certificate was obtained by misrepresentation or non-disclosure by the builder;

…

47 The several references in the Approval Criteria to s 58E are references to provisions in the 1972 Act relating to residential building work insurance prior to the renumbering of the provisions in Republication No 7, as explained above. Relevantly, at that time, s 58E(1)(b), (c), (d) (f), (g), (h) and (j) provided:

58E Residential building work insurance

(1) An insurance policy issued in respect of residential building work complies with this section if—

…

(b) it provides for a total amount of insurance cover of at least the prescribed amount, or an amount equal to the cost of the work, whichever is less, in respect of each dwelling that forms part of the work; and

…

(f) it insures the owner (if the builder is not the owner) and the owner’s successors in title against the risk of being unable to enforce or recover under the contract pursuant to which the work has been, is being or is to be carried out because of the insolvency, disappearance or death of the builder; and

(g) it insures the owner (if the builder is not the owner) and the owner’s successors in title against the risk of loss resulting from a breach of a statutory warranty; and

(h) it insures the owner (if the owner is not the builder) and the owner’s successors in title against the risk of loss resulting, by virtue of the builder’s negligence, from subsidence of the land; and

…

(j) it provides that a claim under it may only be made within the prescribed period (or some specified longer period) after the claimant becomes aware of the existence of grounds for the claim; and

48 The prescribed period is 90 days after the owner became aware of the existence of the grounds for making the request (see cl 4(j) of the Approval Criteria) and [34] above). Importantly, the “specified period” (which is relevant to the period of cover under cl 4(f), is defined in cl 1 of the Approval Criteria, as meaning, in relation to residential building work, “the period prescribed for the purposes of sections 58E(1)(c) and (d) of that Act commencing on the date on which a certificate of occupancy is issued for the building work”. As noted in [33] above, that period is 5 years.

(d) The Deed

49 The Deed commenced on or about 21 June 2002 (even though it was not executed until 10 September 2002). It was stated in cl D of the Preamble to the Deed that the Deed was made “with the intent that the benefits and obligations thereof shall ensure to those builders and members of the public who fall subject to the terms of the trust”.

50 The objects of the Fidelity Fund are set out in cl 2 of the Deed:

2. Objects

The trustees of the approved scheme must ensure that the approved scheme is maintained solely for the following purposes:

(a) the provision of a fidelity certificate to an owner in accordance with the Act and the trust deed;

(b) the making of a discretionary payment of an amount to an owner pursuant to a fidelity certificate in accordance with the Act and the trust deed;

(c) any other purpose that the Minister may in writing determine from time to time.

51 Clauses 4 and 8 are important. The former provides that the Fidelity Fund scheme is established pursuant to the 1972 Act and shall be administered pursuant to the disallowable instruments under Pt 6 of the Act. The reference to “disallowable instruments” includes the Approval Criteria and the 2005 Prudential Standards.

52 Clause 8 of the Deed provides that the trustees “shall at all times administer the fund in accordance with the disallowable instruments created pursuant to Pt 6 of the Act”. Again, this includes the Approval Criteria and the 2005 Prudential Standards.

53 Under cl 9, which deals with payments out of the Fund, it is provided that there “must be paid out of the Fidelity Fund in such order as the board of trustees deems proper” various matters, including “the amount of all claims, Including costs (sic), allowed by the board or established against the Fidelity Fund”.

54 Clause 11 of the Deed provides that a person may not commence proceedings under the Deed against the Fund without leave of the Board unless the Board has disallowed the person's claim and:

the certificate holder has exhausted all relevant rights of action and other legal remedies for the recovery of money or other property in respect of which a pecuniary loss has occurred, being rights and remedies that are available against the builder in relation to whom the claim arose and all other persons who are liable in respect of the loss suffered by the certificate holder, other than any rights or remedies that the claimant may have under other sections of this deed.

It is notable that this provision, which requires other remedies to be exhausted relates not to the making of a claim or request against the Fidelity Fund, but rather to a person bringing proceedings under the Deed against the Fidelity Fund without leave of the Board. There is nothing in the 2004 Act, the related disallowable instruments (including the Approval Criteria), nor the Deed which expressly requires an owner to exhaust other legal remedies for recovering money prior to lodging a claim against the Fidelity Fund. The fidelity certificates each contained a statement to the effect that an owner must exhaust all relevant rights of action and other legal remedies against the builder for the recovery of money or other property in respect to loss occurred prior to lodging a claim against the Fidelity Fund (see [63] below).

55 If the Board refuses leave to a person to bring proceedings under the Deed against the Fidelity Fund, the person may ask the Supreme Court for leave to bring such an action against (cl 12).

56 Under cl 13 of the Deed, the trustees are required to serve notice and reasons if they disallow, either wholly or in part, a claim for compensation under the Fund.

57 Clause 58 deals with the terms and form of fidelity certificates. Fidelity certificates are the certificates issued by the trustees for the building work. Clause 58(a) provides that such certificates “may be issued” on the condition that each fidelity certificate must comply with various specified matters, including that such a certificate only be issued for residential work in the ACT that is undertaken by a Fidelity Fund approved licensed builder, the contribution required to be paid to the Fund for the issue of a fidelity certificate and the amount that the owner can request from the trustees (being at least the amount that is the minimum amount of cover that is required to be provided by an insurance policy under the 1972 Act).

58 Because of its central significance in the proceeding, it is desirable to set out the entirety of cl 58(4), as well as the chapeau in cl 58(a) to which cl 58(4) relates:

TERMS AND FORM OF FIDELITY CERTIFICATES

58 (a) The issue of a fidelity certificate by the trustees may be issued on the condition that each fidelity certificate:

…

(4) must state that each of the following matters is at the discretion of the trustees when a request is made by an owner:

(i) whether any payment is to be paid to the owner from the assets of the Fidelity Fund scheme;

(ii) the amount of any such payment to be paid to the owner; and

(iii) the terms and conditions on which any payment to the owner is to be paid by the trustees from the assets of the Fidelity Fund;

(iv) a claim properly submitted in accordance with Clause 64 may be subject to an assessment by a properly qualified expert appointed by the trustees,

(v) the excess payable by the owner before any payment Is made from the assets of the Fidelity Fund.

…

59 The heading to cl 60 is “WARANTEE (sic) AND LOSSES COVERED BY THE FIDELITY FUND. In fact, however, it deals primarily with payments out of the Fund. Clauses 60-64 are all relevant (without alteration, while noting, however, that, as the applicant pointed out, the reference in cl 61(d) to s 64(1)(j) of the 1972 Act must be a typographical error because the correct provision in that legislation which deals with the prescribed period for making a clam is s 64(1)(i), as is made clear in [32] above):

WARRANTEE (sic) AND LOSSES COVERED BY THE FIDELITY FUND

60. (a) Payments out of the Fidelity Fund will only be made pursuant to a validly issued fidelity certificate and in accordance with sections 62 and 64 of the Act:

(b) For the purposes of assessment of a claim made under a validly issued fidelity certificate, a claim made pursuant to 62 of the Act will be made subject to the premise that section 64(1)(i) of the Act is satisfied.

61. The trustees may pay to the owner an amount, up to the maximum amount stated on the owner's fidelity certificate, out of the assets of the Fidelity Fund scheme for a part or the whole or any loss that the owner has incurred and;

(a) requires that only the amount stated on the fidelity certificate can be requested by the owner;

(b) requires that, if more than one request is made in relation to a fidelity certificate, the total amount that can be paid to an owner must not exceed the amount that is stated on the fidelity certificate;

(c) state that the types of losses in relation to which a request may be made are only those losses which would be recoverable under an insurance policy under sections 64 (1) (f),(g) and (h) of the Act;

(d) require that a request be made within the period that is the prescribed period for the purpose of section 64(1)(i) of the Act after the owner becomes aware of the existence of the grounds for making the request.

62. The trustees may pay the amount to whomever the trustees think fit to satisfy the claim under this fidelity certificate.

63. The trustees are prohibited from refusing to pay an owner under the fidelity certificate on the grounds that the fidelity certificate was obtained by a misrepresentation or non disclosure by the builder.

CLAIMS

64 A claim by a Fidelity Certificate Holder must be;

(a) made in writing within 90 days of becoming aware of a possible event that may cause a payment from the Fidelity Fund.

(b) In accordance with a Fidelity Fund claim form.

60 The trustees submit that cl 60 incorporates ss 62 and 64 of the 1972 Act into the Deed. They contend that those sections carry their meaning from the 1972 Act into the Deed subject to a contrary intention within the Deed itself. This is because the Approval Criteria require the Deed to comply with specific sections of the 1972 Act. The Deed does this by effecting exact incorporation. This, they contend, is further supported by cl 4 which provides that the fund "is established pursuant to the Building Act 1972 (ACT)" and that it shall be administered "pursuant to the disallowable instruments under Pt 6 of the Act." (See also cl 8 which is to similar effect).

(e) Fidelity Certificates

61 The fidelity certificates in the present case were issued on the express basis, as stated on the front page, that each was issued “subject to the requirements of the ACT Building Act 2004 and section 64, and in accordance with the terms and conditions set out in the Master Builders Fidelity Fund Trust Deed”. Although all the 120 certificates here are dated 18 May 2005 (i.e. post the commencement of the 2004 Act on 1 September 2004), it is common ground that the reference to “Section 64” is an erroneous reference to the 1972 Act and should be read as referring to s 90 of the 2004 Act (which is set out in [42] above).

62 Each certificate expressly stated that it applied to “one dwelling only”. It is desirable to set out relevant extracts from the front page of the certificate relating to unit 120 of the Elara Apartments (which is typical):

Builder's Name: B & T Constructions (ACT) Pty Ltd

Builder's Licence No: 7535

Name of Owners/Beneficiaries: B & T Developments

Address of Project:

Block: 4 Section: 34 Unit: 120 Suburb: Bruce

Type of project, ie speculative, contract or project management: speculative

For the construction of: project unit, standard specifications plus car space

Special conditions: n/a

63 At the bottom of the front page of each certificate, there is an instruction to read “the important information overleaf regarding this Certificate”. That information should be set out in full as the applicant places heavy reliance upon it for its contention that the certificate itself is an independent source of relevant legal rights and obligations:

The applicant’s submissions summarised

64 The following three issues were identified by the applicant as being the main issues for determination:

(a) Was the owners corporation entitled to lodge a claim for compensation in August 2017 under all or any of the fidelity certificates for Elara, in respect to the cost to repair defects in the common property and other parts of the buildings that the owners corporation was liable to maintain at all relevant times?

(b) Was the owners corporation entitled to lodge a separate claim for compensation in July 2018, as the assignee of the rights in relation to fidelity certificates of all or any of the owners listed in the Schedule of Eligible Elara Unit Owners, in respect to each unit’s proportional share of the cost to repair defects in the common property and other parts of the buildings that the owners corporation was liable to maintain at all relevant times?

(c) Were the trustees entitled to reject either or both of the claims on the grounds stated, or otherwise?

(a) Was the first claim a valid claim?

65 The applicant submitted that the owners corporation was entitled to lodge the first claim at that time on the grounds they were successor in title to the developer. The factual basis of the claim is not relevantly in dispute.

66 The applicant also submitted that the 90 day period for lodging a claim only commenced to run once an owner had exhausted all avenues of recovery against the builder. Thus, the applicant submitted that time only began to run on 20 July 2017, when the builder went into liquidation.

67 By letter dated 23 November 2017, the trustees’ solicitors acknowledged receipt of the documentation dated 18 August 2017 and stated that the documentation was not submitted, nor did the basis of the claim arise, within the time periods set out in the relevant legislation or during the currency of any of the certificates issued for Elara. Thus the claim was rejected.

(b) Was the second claim a valid claim?

68 It is common ground that the period of cover expired on 26 May 2012. Accordingly, only loss resulting from a breach of statutory warranty that accrued on or before that date can be the subject of a claim. The owners corporation’s entitlement to lodge the further claim depends on whether the unit owners who assigned their rights to the owners corporation were entitled to claim under a fidelity certificate in respect to such loss. The ‘Schedule of Eligible Elara Unit Owners” appended to the further amended statement of claim identified which owners had such rights and on what grounds – i.e. whether the right arose under either ss 88(1) or (3).

69 The claim was lodged outside the period provided for in the fidelity certificates and the Deed. The question is whether that is sufficient, of itself, to invalidate the claim. The applicant submitted that it is not for the following reasons.

70 First, neither the Deed nor the fidelity certificates state in terms that an otherwise apparently valid claim may or must be rejected if it is submitted late.

71 Secondly, neither does s 90(1)(i) of the 2004 Act (which relates to residential building work insurance but is nevertheless referred to expressly on the back page of the fidelity certificates: see [63] above)). The phrase “a claim…may only be made” refers only to one of the matters for which an insurance policy must provide to comply with s 90, but it does not provide that a claim made outside that period may or must be refused. The applicant relied upon the terms and effect of both ss 64(1)(f)-(h) of the 1972 Act and s 90(1)(f)-(h) of the 2004 Act (see [42] above). They provide for the risks that must be insured during the period of cover. A claim can only arise if an insured event occurs during the period of cover. The period within which a claim may be made under either provision depends on when “the claimant becomes aware of the existence of the grounds for the claim”. The applicant submitted that it is not a requirement of either of these statutory provisions that a claim be made during the period of cover. Both the first and second claim here concerned loss resulting from breach of statutory warranty in the period prior to 26 May 2012.

72 As to the trustees’ claim that because the builder’s insolvency occurred after 26 May 2012 this meant that there never was any entitlement to make a claim, the applicant submitted that this reasoning was inconsistent with the proper construction of ss 64(1)(f)-(h) of the 1972 Act and ss 90(1)(f)-(h) of the 2004 Act. The applicant submitted that the right to indemnity provided by, for example, s 90(1)(g) or (h), does not depend on the risk to which s 90(1)(f) applies manifesting itself during the period of cover. In addition, the applicant submitted that the Deed did not exclude claims other than those in circumstances in which the builder is insolvent, dead or has disappeared. The applicant submitted that the trustees could issue a fidelity certificate that excluded liability except in those circumstances, but there was no obligation on them to do so.

73 Significantly, the applicant submitted that the owner’s entitlement to claim is governed by the fidelity certificate and not the Deed. It submitted that the Deed, of itself, conferred no rights on anybody and that no one is a beneficiary of anything under the Deed “unless and until a fidelity certificate is issued, and, in that respect, a fidelity certificate is no different than a certificate of insurance”. The applicant submitted that, while the Deed establishes and regulates and governs what the trustees may or must do, “the work that is covered, the amount that is covered, who is covered, is to be found only by reference to the fidelity certificate, and the rights arise only by virtue of the fidelity certificate”. It submitted that once a certificate is validly issued, it must operate according to its terms and cl 60 provides that a payment is made pursuant to “a validly issued fidelity certificate” and in accordance with the specified statutory provisions.

74 The applicant relied upon what it described as the representation of present fact on the front page of each fidelity certificate that it “is issued… in accordance with the terms and conditions set out in the… Trust Deed”. The applicant submitted that this did not incorporate into the certificate the provisions of the Deed so as to make cover under the fidelity certificate subject to the terms and conditions in the Deed.

75 In short, the applicant contended that the grounds for a claim in this case did not exist until a liquidator was appointed on 20 July 2017, at the earliest. The first claim was then submitted within the 90 day period commencing on 20 July 2017. Further, it was not until 4 May 2018 that the liquidator reported that there were insufficient assets to enable a dividend to be paid to any class of creditors and the second claim was then submitted on 3 August 2018, which was within 90 days of 4 May 2018. In his oral submissions, counsel for the applicant contended that the fidelity certificates altered the 90 day period referred to s 90(1)(i) of the 2004 Act “by, in effect, defining what are the grounds for the claim” and that the entitlement of an owner to make a claim against the fund did not arise until a loss had been suffered.

76 As to the owners of the eleven units which were sold after 26 May 2012, which is outside the five year period, the applicant submitted that it was not until the liquidator was appointed that it could be said that the owners had exhausted any other remedy which they had against the builder.

77 Thirdly, an insurer would be prevented by s 54(1) of the Insurance Contracts Act 1984 (Cth) (IC Act) from refusing a claim made under an insurance policy that complied with s 90 by reason only of the fact that the claim was made outside the period provided for in the policy, unless the delay “could reasonably be regarded as being capable of contributing to a loss in respect of which insurance cover is provided by the contract”. As the evident intention of the Deed is to provide the same level of protection for consumers as would be provided by home warranty insurance under the Act, the applicant contended that neither the Deed nor a fidelity certificate should be construed to permit the trustees to reject an otherwise apparently valid claim by reason only of the fact that it was submitted late. The discretions vested in the trustees are sufficient to protect the Fund against any additional loss covered by a fidelity certificate caused by such a delay.

78 Fourthly, the applicant submitted that a fidelity certificate is a “contract of insurance” within the meaning of s 10 of the IC Act. As such, the trustees are prevented by s 54 from refusing the claim only on the basis that it was submitted late. The applicant submitted that the reference in the definition in s 10 to “a contract that would ordinarily be regarded as a contract of insurance” invokes the common law concept of an insurance contract. Here the trustees issued the fidelity certificates at the request of the builder in consideration of payment of a total amount of $105,315 for the purpose of providing a benefit to the developer’s successors in title – namely, protection against the risk of loss resulting from the risks mentioned in ss 90(1)(c), (f) and (g) during the period of cover – in accordance with the provisions of the Deed and ss 88 and 90 of the 2004 Act.

79 The applicant contended that this arrangement, viewed in the context of the prudential standards that apply to the management of the fidelity fund scheme, has all of the hallmarks of insurance provided under a contract as described by Channell J in Prudential Insurance Co v Commissioners for Inland Revenue [1904] 2 KB 658 (Prudential Insurance) at 663 and explained more recently in Todd v Alterra at Lloyds Ltd [2016] FCAFC 15; 239 FCR 12 (Todd) at [35]–[44] per Allsop CJ and Gleeson J).

(c) Were the trustees entitled to reject the claims?

80 The applicant submitted that in determining who was covered, for what loss and for what period were matters primarily determined by the fidelity certificates. Having regard to relevant statements in those certificates, cover was provided to the owner (i.e. the developer) and the owner’s successors in title. This meant that the developer’s successors in title in respect to the land on which the residential building work covered by the fidelity certificates was carried out were entitled to make a claim under each fidelity certificate. The applicant emphasised that, in contrast with the trustees’ position, it is the residential building work involved in the construction of a dwelling and not the dwelling itself, which is covered by the certificates.

The trustees’ submissions summarised

81 The trustees’ submissions may be summarised as follows.

82 An owner's right to make a request for payment arises out of the Deed, particularly cl 60. That right does not arise from the 1972 Act, the Regulations or the Approval Criteria. These documents regulate the content, and influence the interpretation, of the Deed. They do not provide any right or entitlement.

83 Subsections 64(1)(f), (g) and (h) of the 1972 Act (see [32] above) are relevant to the application of cl 60 of the Deed (see [59] above). Paragraphs (g) and (h) are to be read together with paragraph (f) of s 64(1). The trustees submitted that paragraph (f) sets out a temporal limit on the risk that the policy is to cover. It is to operate when there is an inability to enforce or recover under the contract. Paragraphs (g) and (h) set out what is covered, namely loss due to breach of statutory warranties and land subsidence through negligence of the builder respectively. It is only when both (f) and (g) or (f) and (h) are satisfied that a request is payable.

84 The trustees contended that this construction is fortified by cl 11 of the Deed. Ordinarily, a person is obliged to exhaust all rights against a builder or any other person before commencing legal proceedings against the trustees; this is a textual indication within the Deed itself that the inability to recover from a builder is a precondition on making a valid claim on the Fund.

85 The trustees submitted that neither the first nor second claims conformed with the Deed for the following reasons.

(a) Neither claim was made within the period specified in cl 4(f) of the Approval Criteria, which was incorporated as a term of the Deed by cll 4 and 8. Compliance with that requirement was and is a precondition to the approval of the Fund. Sections 64(1)(c) and (d) as incorporated by reference must be read in conformity with this requirement, as those sections become clauses of a Deed which must satisfy the Approval Criteria before it can be approved.

(b) In the alternative, if all that was required to comply with s 64(1)(c) and (d) in light of cl 4(f) of the Approval Criteria was for the grounds for a claim to arise:

(i) the grounds for such a claim did not arise as the builder did not become insolvent until over 5 years after the expiry of the fidelity certificates; and/or

(ii) if the grounds for a claim did arise within the five-year period, then both claims were lodged far beyond the 90-day period permitted by s 64(1)(i) and cl 64 of the Deed and must be rejected for that reason.

(c) Additionally, each claim was tainted by misrepresentation as each purported to claim under certificates which were inutile, being certificates for units which were owned by the developer at all relevant times. Each claim sought a payment of $10.2m in circumstances where such a payout would have necessarily involved payment for fidelity certificates which never came into force.

86 The first claim (and to the extent that the second claim is brought by the applicant in its own name) was also non-conforming because the applicant did not and does not have a right to claim under any of the 120 fidelity certificates. The rights attaching to a fidelity certificate accrue to the owner, from time to time, of the property identified on the front of the certificate. The legal owner of each unit was the leaseholder of each of the 120 units at the relevant time, while the applicant was the legal owner of the common property only. The applicant had no capacity to exercise rights which accrued to unit owners – those rights were the property of the unit owners, not of the applicant.

87 The trustees contended that the second claim was non-conforming for the following reasons.

(a) On the assumption that the grounds for a claim arose when the builder went into liquidation on 20 July 2017 (which is not accepted), the second claim was over nine months in breach of the 90-day rule when it was lodged on 3 August 2018. The fidelity certificates are not contracts of insurance and s 54 of the IC Act does not assist the applicant (see further below).

(b) In its solicitor's letter dated 5 July 2018, the applicant purported to lodge a claim as assignee of only some unit owners, yet the claim form executed on 3 August 2018 stated that it was for all fidelity certificates and sought $10.2m. Fidelity fund claim forms are statutory declarations. The second claim could not have been true and correct in all material particulars at the time it was made as the applicant was the assignee of only some, and not all, of the unit owners. The trustees were entitled to refuse that claim became of the applicant’s misrepresentations.

88 As to the applicant’s claim that the fidelity certificates are "contracts of insurance" within the meaning of s 10 of the IC Act, with the effect that s 54 of that Act prevents the trustees from refusing the second claim for failure to comply with the requirement that any claim be made within 90 days, the trustees made the following submissions.

89 The fidelity certificates are not contracts of insurance. The core of a contract of insurance is a promise to pay a sum of money or provide some benefit upon the happening of a specified event. The owner of a unit for which a fidelity certificate has been granted does not have an entitlement to indemnity upon the happening of a claim event. There is no promise.

90 Rather, all that such an owner has is a right to have their claim considered. In Medical Defence Union Ltd v Department of Trade [1980] Ch 82 (Medical Defence Union), Megarry VC considered whether a contract between the Medical Defence Union Ltd and its members which gave the Council of the Union a discretionary power to conduct a member's defence of proceedings and indemnify a member in relation to any such proceeding was a contract of insurance. His Lordship held at 90 that it was not a contract of insurance as all a member had was:

… the right to have his request for the union's help under these heads properly considered by the council or by one of its committees ... all that the member has by way of right is that his request should be properly considered and, of course, if it is granted, that the union should conduct the proceedings or indemnify him, or both.

91 Megarry VC rejected the contention that a member's right, while not a right to money or money's worth, was nonetheless of value and thus a benefit for the purposes of the definition of an insurance contract. It was held that while the right to make a request and have it properly considered was a benefit, such benefit did not amount to a contract of insurance as it was the obligation to pay on the happening of a specified event which was essential to the existence of a contract of insurance.

92 Megarry VC's reasoning has been applied in Australia. On each occasion, the hallmark of the determination that the agreement in question was not a contract of insurance was the fact that the party to whom a claim was made retained a discretion as to whether amounts would be paid out in response to a claim.

93 The trustees have such a discretion, which is explicit in the terms of the Deed, namely cll 2(b), 58(a)(4), 61 and 62. The discretion was a requirement of the approval of the Fund, pursuant to clause 4(m) of the Approval Criteria. In light of the breadth of the discretion, the fidelity certificates are not contracts, as there is no exchange of promises; a promise to consider whether to exercise a discretion in favour of a unit owner is not sufficient to be insurance.

94 In the alternative, s 54 of the IC Act has no work to do in these circumstances as it only applies to claims which are refused, "by reason only" of an act or omission of an insured. Here, the second claim was refused for a variety of reasons, including breach of the 90-day requirement. Thus section 54 has no effect in the present circumstances.

The applicant’s submissions in reply

95 At the commencement of the applicant’s oral reply, counsel handed up a document dated 18 December 2018 entitled “Applicant’s Additional Submissions In Reply”. Counsel explained that the document did not replace the applicant’s written reply (which is summarised above) but responded to various matters which had arisen during the course of the hearing. Because of the prominence given by the applicant to the document, it is desirable to set it out in full:

1. What were the builder’s obligations with respect to insurance or fidelity cover?

(a) Section 37(3) of the 2004 Act required the builder to provide a residential insurance policy, a certificate of insurance, or a fidelity certificate for the work with the application for a commencement notice for the residential building work.

(b) Section 90 specified the insurance requirements for the work.

(i) The total amount of cover required by s 90(1)(b) was $10.2M ($85,000 “for each dwelling that forms part of the work”).

(ii) The builder was not the owner of the land where the work was to be carried out. Section 90(1)(c) required the owner and the owner’s successors in title to be insured for the period ending 5 years (the prescribed period at all material times) after the day a certificate of occupancy is issued for the work.

(iii) Section 90(1)(f) to (h) specified the risks against which insurance must be provided.

(iv) The owner of the land was a developer. Section 90(2) provided that insurance would comply with the section if it insures the owner’s successors in title, even though it does not insure the owner.

2. How did the builder comply with his obligations?

(a) The builder purchased Fidelity Cover for a 120-unit complex with a total expected project cost of $21.5M in consideration of payment of an amount of $105,315 (Ex 1 pp 58, 74).

(b) The Fidelity Fund issued 120 fidelity certificates providing fidelity cover for the work to third party beneficiaries (Ex 1 p 75 et. seq.).

3. For what work was each fidelity certificate issued?

(a) Fidelity Certificate (front page - Ex 1 p 75)

(i) “applies to one dwelling only”;

(ii) “issued subject to the requirements of the ACT Building Act 2004 and section 64 and in accordance with the terms and conditions of the…Trust Deed” (Section 64 is an erroneous reference to s 64 of the 1972 Act. Section 64 of the 2004 Act refers to completely unrelated matters - namely compliance with stop and demolition notices issued under Part 4 of the Act);

(iii) Each certificate referred to a unit numbered from 1 to 120.

(iv) “For the construction of: project unit, standard specification plus car space”

(b) “subject to the requirements of the ACT Building Act and section 64” refers to the insurance requirements for residential building work in the 2004 Act;

(c) Trust Deed, clause 58(a)(1) - residential building work in the ACT that is undertaken by a Fidelity Fund approved licensed builder;

(d) Clause 4(d)(1) of the approval criteria (Ex 1 p 3) - residential building work in the ACT that is undertaken by a licensee or a holder of an owner-builder’ licence.

4. Whom did each fidelity certificate cover, in respect of what loss and for what period?

(a) Fidelity Certificate (front page - Ex 1 p 75):

(i) “Name of Owners/Beneficiaries: B & T Developments” (which was the developer);

(ii) “subject to the requirements of the ACT Building Act and section 64” - where the owner is a developer, s 90(2) provides that cover will comply with s 90(1)(c), (f), (g) or (h) if it insures the owner’s successors in title, event (sic) though it does not insure the owner.

(b) Fidelity Certificate (back page - Ex 1 p 396):

(i) “Subject to the requirements of the ACT Building Act 2004 (“the Act”) and the conditions of approval of this Fidelity Certificate, cover will be provided to the owner of the land where the work is to be carried out unless the construction is undertaken by the entity who owns the land or whose subsidiary or related company owns the land”.

(ii) “On and from 9 September 2003, different conditions apply where the owner of the land is a developer as defined in the Act”. (Building (Residential Buildings Warranty) Amendment Act 2003 (ACT) (A2003-38) commenced on 9 September 2003 and replaced s 64(1)(c) and inserted new ss 64(1A) and (1B), later replaced by ss 90(1)(c), 90(2) and 90(3) of the 2004 Act).

(c) The “Owner/Beneficiaries” entitled to make a claim under each fidelity certificate were the developer’s successors in title with respect to the land on which the residential building work covered by the fidelity certificate was to be carried out - vis. “construction of a project unit, standard specification (sic), plus car space” identified as a unit numbered from 1 to 120. They were, respectively:

(i) the unit owner with respect to the part of the work, so described, that was carried out on what became, after registration of the units plan, the parcel shown on the units plan, including the unit subsidiaries shown on the units plan as annexed to the unit (Ex 1 Tab 30; ss 9, 10, 12, 12A, 14, 15 and 32 of the Unit Titles Act 2001 (ACT));

(ii) the owners corporation with respect to the part of the work, so described, that was carried out on what became, after registration of the units plan, all parts of the parcel identified as common property on the units plan (Ex 1 Tab 30 ss 13 to 15 and 33 of the Unit Titles Act 2001 (ACT)).

(d) Trust Deed, clause 60(a) - payments will only be made pursuant to a validly issued fidelity certificate and in accordance with ss 62 and 64 of the 1972 Act (replaced by ss 88 and 90 of the 2004 Act).

(e) Trust Deed, clause 61(c) - the types of losses in relation to which a request may be made are only those losses which would be recoverable under an insurance policy under section 64(1)(f), (g) and (h) of the 1972 Act (replaced by s 90(1)(f), (g) and (h) of the 2004 Act).

(f) Clause 4(f) of the approval criteria (Ex 1 pp 3-4) - where the owner is not the builder, the owner and the owner’s successors in title of the land on which the residential building work is to be, is being or has been carried out, are covered by the fidelity certificate (“owner” has the same meaning as in the Act) for the period ending at the “expiration of the specified period” in respect of loss stated in clause 4(i) - being losses that would be recoverable under an insurance policy under ss 58E(1)(f), (g) and (h) of the 1972 Act (renumbered s 64(1)(f), (g) and (h) and replaced by s 90(1)(f), (g) and (h) of the 2004 Act).

5. What amount was an owner entitled to claim?

(a) Fidelity Certificate (back page - Ex 1 p 396) -

(i) “The sum covered under the Fidelity Certificate in respect of each dwelling that forms part of the work is $85,000 or an amount equal to the cost of the work, whichever is the lesser. The Fidelity Fund is not liable for the first $500 of each claim”.

(ii) “If more than one request is made in relation to a Fidelity Certificate, the total amount that can be paid to an owner must not exceed the amount stated in this Fidelity Certificate and in accordance with the Act”.

(b) Trust Deed, clause 61 - Trustees may pay an amount up to the maximum amount stated on the owner’s fidelity certificate for a part or the whole or any loss that the owner has incurred.

(c) Trust Deed clause 61(a) and (b) - only the amount stated on the fidelity certificate can be requested by the Owner and, if there is more than one request, the total amount paid to an owner must not exceed the amount stated on the fidelity certificate.

(d) Clause 4(d)(3) of the approval criteria - at least the minimum amount of insurance cover that is required to be provided by an insurance policy under s 58E(1)(b) of the 1972 Act (renumbered s 64(1)(b) and replaced by s 90(1)(b) of the 2004 Act) - vis. “the total amount of insurance cover of at least the amount prescribed under the regulations, or the cost of the work, whichever is less, for each dwelling that forms part of the work” (the prescribed amount being $85,000 at all material times).

6. Within what period must a claim be made?

(a) Fidelity Certificate (back page, Ex 1 p 396)

(i) “A claim against the Fidelity Fund will be subject to the premise that section 90(1)(i) of the 2004 Act is satisfied.

(ii) “The owner must exhaust all relevant rights of action and other legal remedies against the builder…prior to lodging a claim against the Fidelity Fund”;

(iii) “The owner after becoming aware of the existence of grounds for a claim must within 90 days lodge such a claim with the Fidelity Fund”

(b) Section 90(1)(i) - an insurance policy issued for residential building work complies with s 90 if it provides that a claim under it may only be made within the period prescribed under the regulations, or a stated longer period after the claimant becomes aware of the existence of grounds for the claim (prescribed period was 90 days at all material times).

(c) Trust Deed clause 60(b) - for the purpose of assessment of a claim made under a validly issued fidelity certificate, a claim made pursuant to s 62 of the 1972 Act (replaced by s 88 of the 2004 Act) “will be made subject to the premise that s64(1)(i) (sic) of the 1972 Act (replaced by s 90(1)(i) of the 2004 Act) is satisfied.

(d) Trust Deed clause 61(d) - “require that a request be made within the period that is the prescribed period for the purposes of s 64(1)(j) of the 1972 Act after the owner becomes aware of the existence of the grounds for making a request” (Section 64(1)(j) refers to an approved form of policy. This is an incorrect reference to s 64(1)(i), later replaced by s 90(1)(i) of the 2004 Act).

(e) Trust Deed clause 64(a) and (b) - claim by a fidelity certificate holder must be made in writing within 90 days of becoming aware of a possible event that may cause a payment from the Fidelity Fund in accordance with the Fidelity Fund claim form.

(f) Fidelity Fund Claim Form, “Notes for Claimant” (1) - “For any claims against the Fidelity Fund, the owner must exhaust all relevant rights of action and other legal remedies …prior to lodging a claim against the Fidelity Fund”. “Additional Information” (9) - “In reference to ‘Notes for Claimant’ (1), provide details evidence (sic) that you have undertaken to resolve the situation prior to preparing this claim” (Ex 1 p 394).

(g) Clause 4(j) of the approval criteria (Ex 1 p 4) - request must be made within the period that is the prescribed period for the purposes of s 58E(1)(j) of the 1972 ACT (renumbered s 64(1)(i) and replaced by s 90(1)(i) of the 2004 Act) after the owner becomes aware of the existence of the grounds from (sic) making the request (the prescribed period being 90 days at all material times).

96 During the course of his closing oral submissions in reply, counsel for the applicant raised for the first time a contention that there was a contract between the builder and the fidelity fund involving the issue of the 120 fidelity certificates and that the contract conferred a benefit on third parties, namely the unit owners. He said that there was “a contract under which the fidelity certificates were to be issued to provide cover for work to third party beneficiaries on the terms and conditions stated in, and incorporated by referencing, the fidelity certificates”. The contention was left largely undeveloped.

Consideration and determination

(a) Are the fidelity certificates an independent and standalone source of legal rights and obligations?