FEDERAL COURT OF AUSTRALIA

Weston (Trustee) v Sanna [2019] FCA 32

ORDERS

NSD 276 of 2016 | ||

PAUL GERARD WESTON AS TRUSTEE OF THE BANKRUPT ESTATE OF LEPA SANNA Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. On or before 14 February 2019, the parties are to provide to the Associate to Markovic J draft short minutes of order giving effect to these reasons and, if required, a proposed timetable for the second stage of the proceeding.

2. If the parties are unable to agree on a form of draft short minutes as contemplated by Order 1, on or before 14 February 2019 the applicant and respondent should each provide the Associate to Markovic J with a form of draft orders and submissions, not exceeding 3 pages in length, explaining why their form of order is proposed and the basis of any disagreement.

3. The matter be listed for case management hearing on 21 February 2019.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

background

1 This proceeding concerns two properties: one situated at 33-35 Circulo Drive, Copacabana (Copacabana Property) and the second situated at 83B Lindeman Crescent, Green Valley (Green Valley Property).

2 By transfer registered no AH755747 dated 8 May 2013 for consideration of $1.00 (Copacabana Transfer), Lepa Sanna transferred the Copacabana Property to her estranged husband, Corrado Sanna, the respondent. By unregistered transfer signed by Mrs Sanna in favour of Mr Sanna as transferee, Mrs Sanna transferred her half share interest in the Green Valley Property to Mr Sanna for consideration of $1.00 (Green Valley Transfer). After making those transfers, on 10 December 2013 Mrs Sanna became a bankrupt. The applicant, Paul Gerard Weston, is the trustee of her bankrupt estate (Trustee).

3 Pursuant to orders made by Katzmann J in NSD619/2016 on 6 July 2016, proceedings NSD619/2016 and NSD276/2016 were heard together. Due to the related and overlapping nature of the relief sought my reasons deal with the applications together.

4 In NSD276/2016 the Trustee seeks declarations pursuant to s 120 or, in the alternative, s 121 of the Bankruptcy Act 1966 (Cth) (Act) that the Copacabana Transfer and the Green Valley Transfer are void as against him and relief consequent upon the making of those declarations. In the case of the Copacabana Property, which has subsequently been subdivided as explained at [94]-[96] below, the Trustee seeks an order that Mr Sanna execute all necessary instruments to effect a transfer of one of the subdivided parts of that property to him. In the case of the Green Valley Property, the Trustee seeks a declaration pursuant to s 58 of the Act that Mrs Sanna’s share in that property vests in him and another trustee and seeks orders for the appointment of both of them as trustees for sale pursuant to s 66G of the Conveyancing Act 1919 (NSW) (Conveyancing Act) and s 79 of the Judiciary Act 1903 (Cth) (Judiciary Act).

5 In NSD619/2016 the Trustee relevantly also seeks a declaration that the Green Valley Property vests in him pursuant to s 58 of the Act as well as an order that Mr Sanna execute all such instruments and do all such acts and things as are necessary to transfer that property to the Trustee.

6 During the course of the hearing it became apparent that, in the event that the Trustee was successful in setting aside the Copacabana and Green Valley Transfers, the parties were not in a position to deal with the consequences that flowed from findings to that effect. In particular, late in the hearing, and after Mr Sanna had been cross-examined, counsel for Mr Sanna attempted to tender further evidence to establish that he had discharged certain liabilities which he said were secured over the Green Valley Property. In those circumstances, the parties agreed that the matter should proceed in two stages: the first being the determination of whether the Copacabana Transfer and the Green Valley Transfer are void against the Trustee pursuant to s 120 or s 121 of the Act; and the second being the consequences of such findings, assuming that the parties could not resolve that issue by consent between themselves.

7 These reasons deal with the first issue.

THE TRUSTEE’S CLAIMS AND MR SANNA’S DEFENCE

8 Before proceeding further it is necessary to set out a summary of the claims made by the Trustee and Mr Sanna’s defence.

9 In his further amended statement of claim filed in NSD276/2016, the Trustee alleges that, contrary to what is recorded in the Copacabana Transfer and the Green Valley Transfer, at the date of these transfers there was no financial agreement between Mr and Mrs Sanna entered into pursuant to s 90C of the Family Law Act 1975 (Cth) (Family Law Act).

10 In relation to the Copacabana Transfer, the Trustee further alleges that:

(1) either Mr Sanna gave no consideration for the Copacabana Transfer or gave consideration of less than the Copacabana Property’s market value such that it is void against him pursuant to s 120 of the Act; or

(2) in the alternative, Mrs Sanna’s main purpose in making the Copacabana Transfer was to prevent the Copacabana Property from becoming divisible among her creditors or to hinder or delay that process and that the property would probably have been part of her estate or be available to creditors if it had not been transferred.

11 In relation to the Green Valley Transfer, the Trustee further alleges that:

(1) Mr Sanna gave no consideration for the Green Valley Transfer or provided consideration of less than the Green Valley Property’s market value such that it is void against him pursuant to s 120 of the Act; or

(2) in the alternative, Mrs Sanna’s main purpose in making the Green Valley Transfer was to prevent the Green Valley Property from becoming divisible among her creditors or to hinder or delay that process and, where the Green Valley Transfer remains unregistered, the Green Valley Property would probably have become part of her estate or be available to creditors.

12 In his defence to the further amended statement of claim (Defence), Mr Sanna denies that upon Mrs Sanna becoming a bankrupt, all of her property vested in the Trustee and relies on s 58(2) of the Act. Mr Sanna also denies that the Copacabana Transfer is void against the Trustee pursuant to s 120 or s 121 of the Act. He denies that the Green Valley Transfer is void against the Trustee pursuant to s 121 of the Act but does not include any pleading in the Defence in response to [37] of the further amended statement of claim where the Trustee alleges that the Green Valley Transfer is void against him pursuant to s 120 of the Act.

13 Relevantly, in relation to the Copacabana Property, Mr Sanna denies that:

(1) the Copacabana Transfer recorded consideration of $1.00 and that the transfer was made pursuant to s 90C of the Family Law Act;

(2) as at the date of the Copacabana Transfer, there was no financial agreement pursuant to s 90C of the Family Law Act between him and Mrs Sanna; and

(3) he gave no consideration for the Copacabana Transfer or that he gave consideration that was less than market value for the Copacabana Property or that, in making the Copacabana Transfer, Mrs Sanna’s main purpose was to prevent the Copacabana Property from becoming divisible among her creditors or to hinder or delay that process.

14 Mr Sanna says further that:

(1) on 25 July 2012 the Copacabana Property was transferred in equity to Arcadia Property Holdings Pty Ltd (Arcadia) pursuant to a contract for sale of that property entered into by Mrs Sanna with Arcadia and with the consent of the then mortgagee, Australian Executor Trustees Limited (AETL), for a sale price of $995,946;

(2) at settlement Arcadia gave two bank cheques to AETL, one for $10,016.62 made payable to Gadens Lawyers (Gadens) and one for $913,473.65 made payable to AETL, AETL gave Arcadia a discharge of its mortgage and the certificate of title for the Copacabana Property and Mrs Sanna gave Arcadia a transfer of land in registrable form;

(3) the discharge of the AETL mortgage was lodged by George Dimitriou who, in order to do so, had to have the certificate of title for the Copacabana Property in his possession;

(4) from 25 July 2012 Mrs Sanna held the legal title and interest in the Copacabana Property on a bare trust for Arcadia. It follows that the Trustee has no interest in the Copacabana Property and no entitlement to require the legal title to it to vest in him pursuant to s 90 of the Real Property Act 1900 (NSW) (Real Property Act) or otherwise;

(5) Mrs Sanna was not entitled to any consideration for the transfer or, to the extent she was, she was only entitled to that consideration in her capacity as bare trustee for Arcadia which is a complete answer to the Trustee’s case under s 120 of the Act;

(6) on 3 August 2012 Defined Properties Investment Pty Limited (DPI) registered a mortgage on the title of the Copacabana Property. That mortgage did not evidence an actual transaction, agreement or loan; did not secure repayment of any money; was not in fact signed by Mrs Sanna; and was registered by Mr Dimitriou, the controlling mind of Arcadia and DPI, as he did not wish to register a transfer from Mrs Sanna to Arcadia because he intended to transfer the Copacabana Property to Mr Sanna without paying any stamp duty. In the meantime, in order to protect the interest of Arcadia, Mr Dimitriou had DPI register a mortgage;

(7) in April 2013 Arcadia offered to sell the Copacabana Property to him;

(8) he then obtained finance from Westpac Banking Corporation (Westpac) and on 25 May 2013, upon obtaining finance, Arcadia, in exchange for $818,000, gave Mr Sanna the transfer for the Copacabana Property in registrable form. Mr Sanna says he does not know why the Copacabana Transfer is stamped for payment of $1.00 and is said to be pursuant to the Family Law Act other than that it was arranged by Mr Dimitriou, his accountant at the time, with whom he is now involved in litigation in the Supreme Court of New South Wales (Supreme Court); and

(9) on 25 May 2013 the discharge of the mortgage to DPI, the Copacabana Transfer and the mortgage to Westpac were recorded on title.

15 In relation to the Green Valley Property, Mr Sanna admits that:

(1) in about May 2013 Mrs Sanna purported to transfer her interest in that property to him pursuant to the Green Valley Transfer;

(2) the Green Valley Transfer recorded consideration of $1.00 and that it was made pursuant to s 90C of the Family Law Act;

(3) contrary to what was recorded in the Green Valley Transfer, there was, as at May 2013, no financial agreement between him and Mrs Sanna pursuant to s 90C of the Family Law Act;

(4) in about May 2013 Westpac made loan facilities available to him which were to be secured, among other things, by a mortgage over the Green Valley Property. Westpac also obtained a mortgage executed by him over the Green Valley Property and refinanced Permanent Mortgages Pty Limited (Permanent Mortgages); and

(5) caveats prevent the registration of Westpac’s mortgage on the title of the Green Valley Property and Permanent Mortgages’ mortgage remains registered on the title of the Green Valley Property.

16 Mr Sanna denies that he gave no consideration for the Green Valley Transfer or that he gave consideration of less than the market value of the Green Valley Property, the subject of that transfer, and says that:

(1) in 2012 he and Mrs Sanna separated;

(2) it was agreed between them that Mrs Sanna would transfer her half share in the Green Valley Property to him in consideration for him paying out all of the encumbrances on the property, including the registered mortgage, the sum of $100,000 plus costs and interest they jointly owed to Boral Limited (Boral) and a debt of $77,000 owing by Mrs Sanna to Barrie Horne; and

(3) pursuant to that agreement he refinanced the mortgage over the Green Valley Property held by Permanent Mortgages with Westpac, went to register a transfer of the Green Valley Property to himself and negotiated a settlement with Boral.

17 Mr Sanna also denies that Mrs Sanna’s main purpose in making the Green Valley Transfer was to prevent the Green Valley Property from becoming divisible among her creditors or to hinder or delay that process.

18 At this point it is relevant to observe an inconsistency in the Defence. That is, Mr Sanna denies that, as at the date of the Copacabana Transfer, there was no financial agreement pursuant to s 90C of the Family Law Act between him and Mrs Sanna but admits that there was no such agreement between them as at the date of the Green Valley Transfer.

facts

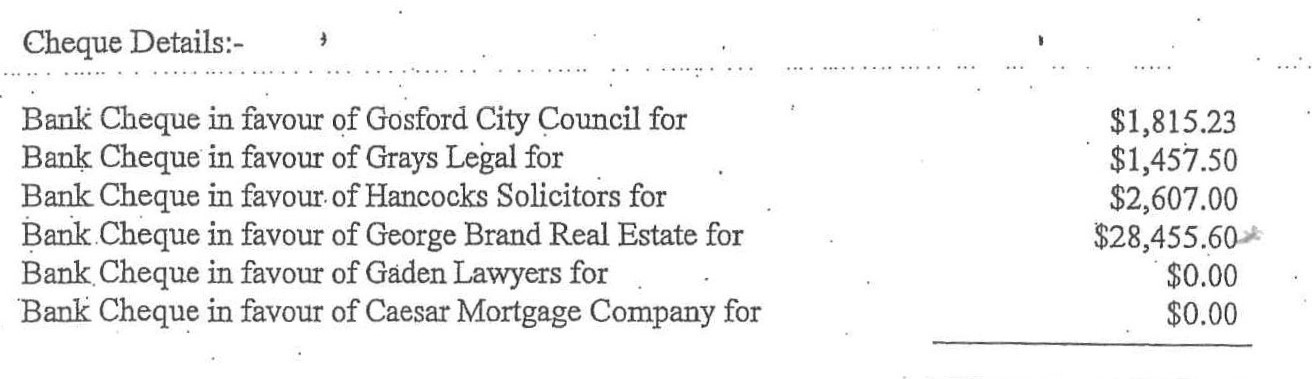

19 Much of the evidence relied on by the parties was documentary. Only Mr Sanna gave evidence to attempt to make good the matters raised by him in defence of the Trustee’s claim. Mr Sanna provided an explanation of the transactions which occurred and was cross-examined. Mrs Sanna did not give evidence. Before proceeding to the detail of the evidence and the inferences that the parties invited me to draw from the evidence, I make some general observations about Mr Sanna as a witness and his evidence.

20 Mr Sanna is a company director and has been involved in the construction industry for some time. He is a director of DCL Constructions Pty Limited (DCL) which has operated since about 2010 or 2011 and was involved in the management, but was not a director, of DCL Constructions (NSW) Pty Limited (DCL (NSW)) which is now in liquidation. DCL is a building subcontractor involved in concrete, steel and formwork. DCL (NSW) undertook the same type of activity now undertaken by DCL.

21 Mr Sanna has also been involved in property development, namely two joint ventures between Castle Property Group and Danic Holdings Pty Ltd (Danic), a company which was run by Mrs Sanna and of which she was a director. The first joint venture involved the construction of 36 industrial units at Wisemans Ferry Road, Somersby and the second involved the construction of 22 industrial units and a coffee shop at Kangoo Road, Somersby. Danic and Castle Property Group purchased the land, obtained the development approvals and were the developers. Mr Sanna was involved with the architects and the council at the time of obtaining the development approvals and the concrete, steel and formwork on the developments was subcontracted to DCL.

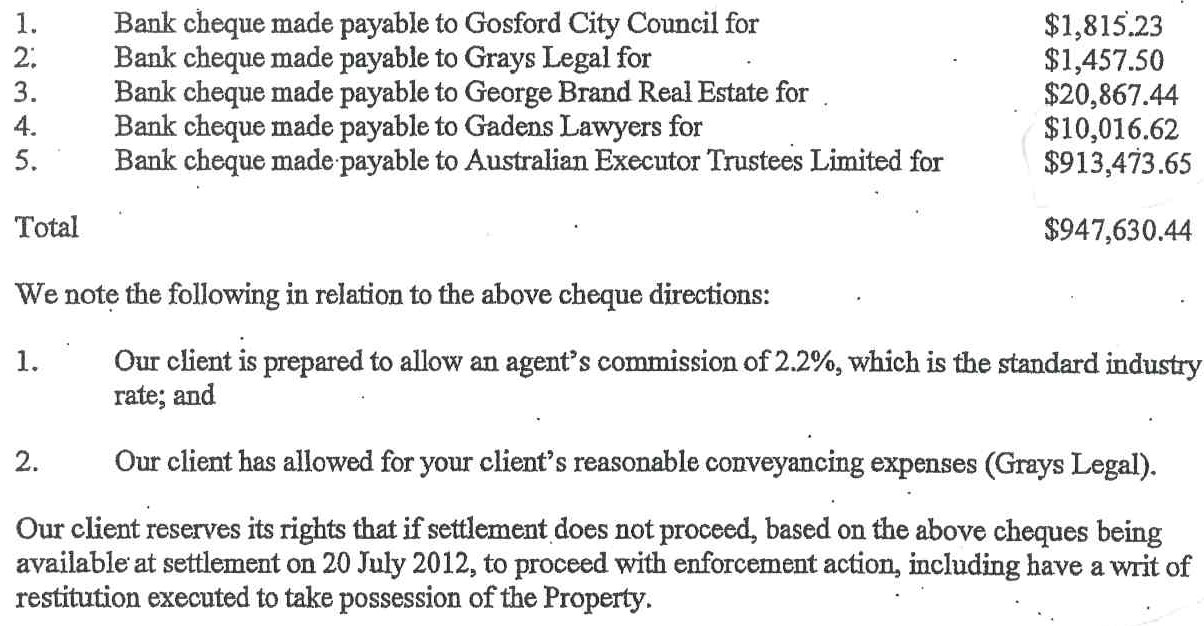

22 Notwithstanding Mr Sanna’s experience and years in business, he was prepared to outsource the preparation of important documents, including applications for loans, to others, in particular, Mr Dimitriou who he engaged on the terms set out at [31]-[33] below. Mr Sanna was also prepared to sign documents without considering or reading their content or checking their accuracy. He gave the impression that he did not care about the detail or veracity of the information he provided in documents of some significance. An example of this was his tax return for the financial year ended 30 June 2012. He left its preparation to his accountants and did not check its contents because, according to Mr Sanna, you did not do so with Mr Dimitriou. Mr Sanna was unconcerned with the document’s accuracy and simply signed the documents sent to him. Similarly, Mr Sanna signed a loan application to Westpac, in circumstances described at [78]-[79] below, without reading it.

23 I did not find Mr Sanna to be a reliable witness. He was often evasive, failing to answer the questions that were asked and I formed the impression that he sought to avoid answering those questions that went to the heart of the issues in dispute. In addition, as explained below, aspects of his evidence were not supported by the objective facts disclosed by the documents.

24 I turn now to deal with the relevant facts.

Acquisition of the Copacabana Property and the Green Valley Property

25 In about 1995 and 1999 respectively Mr and Mrs Sanna purchased the Green Valley Property as joint tenants and Mrs Sanna acquired the Copacabana Property for $700,000.

26 On 6 November 2006 Mrs Sanna entered into a loan agreement with AETL for an amount of $1.65m to “refinance owner occupied residence from Colonial/CBA” (AETL Loan). The AETL Loan was to be secured by a first registered mortgage over the Copacabana Property and guarantees from DCL and Danic.

27 By August 2009 Mrs Sanna was having difficulty servicing the AETL Loan. According to a statement of account for the period 1 August 2009 to 15 January 2010, in that period there were three “repayment dishonour” entries and six “default interest” charges. According to Mr Sanna, Mrs Sanna’s financial difficulties commenced in 2009 when the global financial crisis hit resulting in a market downturn and a drop in asset values of nearly 40 to 50%. Mrs Sanna could not sell assets for the amount she owed on them and could not earn sufficient income to service the debts on those assets.

28 On 1 September 2011 AETL issued Mrs Sanna with a notice of default pursuant to s 88 of the National Credit Code and s 57(2)((b) of the Real Property Act (AETL Demand) demanding payment of $56,020.21 to rectify the default under the AETL Loan agreement and the mortgage. Mr Sanna did not recall seeing the AETL Demand but said that he would have been aware of it at the time and that Mrs Sanna did not have the funds to repay it.

29 Mr Sanna submitted that from about the time of service of the AETL Demand it was clear that Mrs Sanna’s financial circumstances were not good and it was likely that she would become bankrupt. While I accept that Mrs Sanna found herself in financial difficulty from at least 2009, there was no evidence that it was likely that from September 2011 she would become a bankrupt. That did not occur until several years thereafter.

Wyse & Young

30 Mr Sanna was introduced to Mr Dimitriou in about 2010 by a mutual friend. Mr Dimitriou was the director of Wyse & Young International (Wyse & Young) which describes itself as Litigation, Property, Business and Tax Accountants.

31 On 21 October 2011 Mr and Mrs Sanna, DCL, DCL (NSW) and Danic, among others, (Sanna Parties) accepted the terms of an appointment letter and costs agreement (Wyse & Young Agreement) with Wyse & Young signed by Mr Dimitriou pursuant to which the Sanna Parties appointed Wyse & Young to act for them on a range of accounting work, including the preparation of individual tax returns for Mr and Mrs Sanna. The nominated partner responsible for the work to be undertaken was Gerard Quin.

32 Pursuant to the terms of the Wyse &Young Agreement, the Sanna Parties also authorised Wyse & Young to:

…negotiate the discharge from the current 1st Registered Mortgagee and the Second registered Mortgagee or Caveator, all charges over any companies, and any other security over any other goods or chattels to make way for Finance to a new incoming Mortgagee. In doing this we agree to pay a fee payable no less than 20% plus GST of the amount negotiated off the current balance of debt payable and the negotiated amount paid (“the saved debt”)…

In relation to the obtaining of finance, the Sanna Parties agreed to pay a fee:

… of (3%) of the total loan amount unconditionally approved, plus G.S.T, being the fee payable for obtaining the unconditional loan approval and discharge of any current liability the subject of the loan application and we irrevocably agree and authorise such amount together with the fee for the saved debt, if any, shall be paid from any proceeds of any approved loan paid to our credit and/or to discharge any liability on our behalf.

33 Wyse & Young was also authorised by the Sanna Parties to “lodge a Caveat over any property any of [those parties] own either solely or jointly to secure, charge and encumber any property for such of [their] fees and disbursements which remain unpaid”.

34 Mr Sanna said that he first saw the Wyse & Young Agreement “a couple of years ago” in connection with proceedings between him and Mr Dimitriou at a time when Mr Dimitriou filed his evidence in that proceeding. He denied that he ever signed or that he was provided with a copy of the Wyse & Young Agreement.

35 Despite Mr Sanna denying that he signed the Wyse & Young Agreement, there was no issue made about the fact that Mr Dimitriou undertook work for him and Mrs Sanna. Mr Sanna said that he put all his trust in Mr Dimitriou; whenever Mr Dimitriou provided documents to him “it was always on the fly”; Mr Dimitriou would tell them to “sign here” and that he would “sort the rest”; Mr Dimitriou might just provide the last page of a document to sign; when he signed documents with Mr Dimitriou he did not read them in full; everything signed at Mr Dimitriou’s request was left at the accountant’s office; and Mr Dimitriou never provided copies of those documents to him.

Family law deed

36 On 16 December 2011 Mr and Mrs Sanna entered into a deed described at recital A thereof as “a financial agreement under Section 90c of the Family Law Act 1975 (Cth)” (Family Law Deed) and relevantly provided:

(1) under the heading “Background”:

2.2 Corrado and Lepa separated on or about 1 March 2011.

(2) under the heading “Property, liabilities and financial resources”:

5.1 As at the date of this Agreement and subject to compliance with the terms of this Agreement, the assets and liabilities to be retained by Corrado are as set out in Annexure A, and Corrado shall be solely entitled to retain to the exclusion of Lepa all assets set out in Annexure A.

5.2 As at the date of this Agreement and subject to compliance with the terms of this Agreement, the assets and liabilities to be retained by Lepa are as set out in Annexure B, and Lepa shall be solely entitled to retain to the exclusion of Corrado all assets set out in Annexure B.

…

(3) under the heading “Transfer of assets and liabilities”:

6.1 In relation to the former Matrimonial Home the parties agree as follows:

(a) that within 28 Days of the making & executing of this agreement, Lepa do all such acts and things sign all necessary documents so as to transfer to Corrado all his right title and interest in the former Matrimonial Home and further shall vacate the home and give vacant possession thereof to Corrado within 28 Days of making this agreement.

…

(c) In the event that Corrado does not obtain finance in accordance with clause 6.1 (b) within 28 days of the date hereof and Lepa does not allow any extension to the 28 date time frame then the parties agree that clauses 6.1(a) and (b) will not apply and the parties will do all things necessary to effect the sale of the Matrimonial Homes in the following manner:

(i) list the Property for sale by private treaty with the Agent, the costs of and incidental to such appointment to be borne equally by the parties as and when they fall due;

…

6.2 The parties agree Lepa shall be entitled the right title and interest of the parties in the company 100% of DCL Constructions (NSW) Pty Ltd ABN 71 085 544 627 (the “Company” including but not limited to the business and assets of the Company to the exclusion of Corrado.

6.3 The parties agree Lepa shall be entitled the right title and interest of the parties in the company 100% of DLD (NSW) Pty Ltd ABN 33 100 196 076 ATF the Danic Unit Trust, Danic Holdings Pty Ltd ABN 93 100 187 862 (under External Administration) and DCL Constructions Pty Ltd ABN 35 072 499 426 (under External Administration) (the “Companies” including but not limited to the business and assets of the Companies, to the exclusion of Corrado.

37 Annexures A and B to the Family Law Deed, which Mr Sanna agreed were accurate as at their date, respectively set out Mr and Mrs Sanna’s assets and liabilities:

(1) in relation to Mr Sanna Annexure A included the following assets:

DCL Constructions (NSW) Pty Ltd to be transferred to – Lepa Sanna rights to be transferred $660,000 | $660,000 |

Property 33 Circulo Dr Copacabana NSW (Folio 33/718953 – Lepa Sanna rights to be transferred $1,900,000 | |

Property 83B Lindeman Crescent, Green Valley NSW (Folio 41/875272) – Lepa Sanna rights to be transferred $225,000 | Half share value $225,000 |

Mr Sanna’s interest in DCL (NSW) was a loan he made to the company which was never repaid as the company subsequently went into liquidation; and

(2) in relation to Mrs Sanna Annexure B included the following assets:

Property 33 Circulo Dr, Copacabana NSW (Folio 33/718953 – to be transferred to Corrado Sanna $1,900,000 | $1,900,000 |

Property 83B Lindeman Crescent, Green Valley NSW (Folio 41/875272) rights to be transferred to Corrado Sanna $450,000 | Half share value $225,000 |

Danic Holdings Pty Ltd (previous) DLD (NSW) Pty Ltd ATF Danic Unit Trust (Including Gold Coast property and 3 Factory Units) | $1,550,000 |

DLD (NSW) Pty Ltd ATF Danic Unit 1 vehicle | $6,000 |

Mr Sanna explained that Mrs Sanna’s interest in Danic was comprised of three factory units at Kangoo Road, Somersby and a unit in Queensland which were sold because Danic could not meet the repayments on them. Mr Sanna also said that by 12 January 2012 Danic was in receivership and Mrs Sanna never recovered anything from those assets.

38 Annexures A and B to the Family Law Deed also provided that the transfer of the Copacabana Property and Mrs Sanna’s half share in the Green Valley Property to Mr Sanna were to be accompanied by a transfer of the mortgage to AETL over the Copacabana Property and the “Mortgage Latrobe” over the Green Valley Property to Mr Sanna.

39 As to the date of their separation recorded in the Family Law Deed, in cross-examination, Mr Sanna gave evidence that 1 March 2011 was the first date on which Mrs Sanna moved out but that she “was coming and going”. The following exchange took place between counsel for the Trustee and Mr Sanna:

Q: But this was a document that was being dealt with in December of 2011?

A: Mmm.

Q: So – and you signed it, so it rather suggests that she hadn’t come back by the end of December?

A: Well, I don’t know.

Q: By 16 December, didn’t it – doesn’t it?

A: Well, that date just looks a bit dodgy to me. Everything George does is dodgy, but, anyway.

Enforcement of the AETL Loan

40 On 12 January 2012 AETL obtained judgment in the Supreme Court for possession of the Copacabana Property and for the payment of $1,840,309.83 against Mrs Sanna as first defendant and Danic, then in receivership, as second defendant.

41 On about 31 January 2012 Mr Sanna applied to Westpac for a loan for the purposes of refinancing an external loan.

42 On 17 February 2012 the Supreme Court issued a writ of possession for the Copacabana Property (Copacabana Writ).

43 Mr Sanna submitted that, after AETL obtained judgment against Mrs Sanna, it was clear she had no prospect of refinancing the Copacabana Property given her financial difficulties and so she contemplated selling the property. As Mrs Sanna did not give evidence, what she contemplated at this point is unknown. But it is clear that, based on her entry into the agency agreement described at [48] below, by April 2012 she was considering selling the Copacabana Property.

44 On 23 February 2012 the New South Wales Sheriff issued an amended notice to vacate to the occupier of the Copacabana Property requiring those premises to be vacated prior to 11.30 am on Monday, 2 April 2012.

45 On 15 March 2012 Elders Real Estate Copacabana provided Mrs Sanna with a valuation of the current market value of the Copacabana Property, being between $940,000 and $990,000.

46 In early April 2012 Mrs Sanna and Danic filed an application in the Supreme Court seeking to stay the execution of the Copacabana Writ. The documents filed in the Supreme Court by Mrs Sanna and Danic name Mr Dimitriou as their contact and authorised representative.

47 According to Mr Sanna, on 2 April 2012 he and Mrs Sanna vacated the Copacabana Property and rented a property at Daleys Point.

48 On 14 April 2012, with AETL’s consent, Mrs Sanna entered into an exclusive agency agreement with George Brand Real Estate for the period 14 April 2012 to 14 August 2012 for the sale of the Copacabana Property.

49 On 14 May 2012 Gadens, solicitors for AETL, wrote to Wyse & Young in relation to the Copacabana Property informing them, among other things, that:

We are instructed by our client to proceed with the current enforcement action, including the scheduled eviction which is to occur on Wednesday, 13 June 2012 at 11:30am.

We note if you provide our office with an exchanged unconditional contract for sale for Property, we will seek our client’s instructions in relation to same.

…

(emphasis added)

50 On 12 June 2012 a Gadens file note records the following telephone conversation with Mr Dimitriou:

…

have we received anything from George Brand real estate? no we havnt (sic)

he thinks contracts have been exchanged. told him our clients (sic) consent is required for any sale of the property.

told him as we have received no documents, eviction is proceeding tomorrow.

51 On 13 June 2012 Mr Dimitriou sent an email to Pip Nagam of Gadens which included (as written):

We request your consideration and acceptance for a further stay as to the eviction that you had obtained.

We request generally a stay to the eviction scheduled for 11:30am 13th June.

…as this will assist the finalisation and completion of sale that was exchanged unconditionally. We now urgently request your clients acceptance for the sale to proceed and provide urgent instructions for the discharge of mortgage on the security property.

With relation to the contract of sale, reliant on the valuation of John Virtue Valuers and also that of the marketing agent, we say our client has certainly achieved reasonably the property’s value in this current market.

We were advised by the purchasers solicitors that they are preparing a settlement direction sheet and we would like to assure Ms Sanna’s intention to provide to the bank net balance in full of the contract sale price, that amount to be $ 948,520.

…

The attachments to Mr Dimitriou’s email included an “exchanged contract of sale” for the Copacabana Property for AETL’s acceptance. The attached contract of sale was dated 9 June 2012 and named the “vendor” as Russo & Partners, evidently a firm of solicitors which was also named as the purchaser’s solicitor. The nominated purchaser was Arcadia. From 9 January 2012 when Arcadia was registered to 5 June 2016, Arcadia’s sole director, secretary and shareholder was Danny Kalischer.

52 On 13 June 2012 an order was made staying the execution of the Copacabana Writ until 21 July 2012.

53 On 18 June 2012 Mr Dimitriou sent an email to Ms Nagam attaching the “[s]ales contract as sent again for your clients (sic) consideration”. A further copy of the contract for sale of the Copacabana Property also dated 9 June 2012 named Mrs Sanna as vendor, Grays Legal as her solicitor, Arcadia as purchaser and Russo & Partners as its solicitors.

54 On 25 June 2012 Ms Nagam sent an email to John Hancock of Hancocks, who until late June 2012 or early July 2012 acted for Mrs Sanna in the Supreme Court proceeding commenced by AETL, which included:

It was agreed that the sale proceed for this matter provided that settlement takes place by 21 July 2012 and conditions were satisfied being:

1. A statutory declaration from both Mrs Sanna and the purchaser in relation to the sale, being at arm’s length and the parties are in no way related. We note we have received the executed statutory declaration from Mrs Sanna. As at the time of writing, we have not received the purchaser’s statutory declaration; and

2. An acknowledge from Mrs Sanna that she is liable for the shortfall debt. Please see attached our client’s shortfall agreement form which is to be executed by Mrs Sanna and returned to the writer prior to settlement occurring:

Would you kindly have the documents provided to the writer as a matter of urgency.

55 On 28 June 2012 Mrs Sanna signed a letter from Pepper Australia Pty Limited (Pepper) written on behalf of AETL in relation to the AETL Loan by which she acknowledged, among other things, that:

(1) the Copacabana Property would be sold and the proceeds paid to AETL as a partial repayment of the AETL Loan; and

(2) as the proceeds of sale of the Copacabana Property would not be sufficient to repay the full amount of the debt:

(a) she was liable for the shortfall in accordance with the terms of the loan agreement;

(b) interest would continue to accrue on the outstanding amount;

(c) she would continue to make repayments after completion of the sale in order to repay the amount of any shortfall; and

(d) Pepper may take any action permitted by law and in accordance with the terms of the AETL Loan in order to recover the balance outstanding.

56 The statutory declaration contemplated by Ms Nagam in her email dated 25 June 2012 (set out at [54] above) was provided by Mr Kalischer in his capacity as the director of Arcadia who declared, among other things, that the transaction was at arm’s length and that the purchaser was “not in any way related to the vendor”.

57 On 28 June 2012 a Gadens file note records a telephone conversation with Mr Dimitriou as follows:

…

Hancock Lawyers no longer act for Lepa Sanna, they told him they’ve advised us of that

He has sent me an email w attachments.

Wants to know who the cheque get (sic) directed to

I will need to ask instructions

58 Settlement of the sale of the Copacabana Property was scheduled to take place on 20 July 2012. Between about 3 July 2012 and 20 July 2012 correspondence was exchanged between Gadens, Hancocks and Mr Dimitriou. An issue arose between AETL and Mrs Sanna about her proposed deductions from the sale proceeds on settlement. The settlement adjustment sheet proposed by Mrs Sanna showed an amount due on settlement after deduction of the deposit and adjustments as at 20 July 2012 of $900,204.44. It then provided for the following cheque details:

That is, Mrs Sanna’s settlement adjustment sheet provided that the amount available to AETL, putting aside the fees payable to its lawyers, was approximately $865,000. The deposit paid for the property was not to be made available to AETL.

59 On 19 July 2012 Gadens wrote to Wyse & Young informing them that their client was ready, willing and able to proceed with settlement on 20 July 2012. The letter then listed the following bank cheques that AETL required in order for it to provide the certificate of title and a discharge of its mortgage over the Copacabana Property:

60 Mr Dimitriou responded to Gaden’s letter by email dated 19 July 2012 sent at 11.25 pm in which he indicated that he thought that the best outcome was to permit settlement to proceed on the basis of the “settlement sheet provided”, which I infer was the settlement sheet provided on behalf of Mrs Sanna (as described at [58] above).

61 In their letter dated 20 July 2012 addressed to Wyse & Young, Gadens informed Mr Dimitriou that:

We refer to your email dated 19 July 2012 and our letter dated 19 July 2012.

Our client has always been, and remains to consent to the sale, provided that any deductions from the sale proceeds are reasonable and genuinely connected with the sale.

The deductions our client objects to do not meet those requirements.

Our client remains ready, willing and able to proceed with settlement at 2:00pm today on the basis of the cheque directions set out in our letter dated 19 July 2012.

In exchange for our client’s original certificate of title for the Property and discharge of mortgage, we are to receive at settlement the following:

1. Bank cheque made payable to Gadens Lawyers $10,016.62; and

2. Bank cheque made payable to Australian Executor Trustees Limited $913,473.65.

The Bank cheque to Australian Executor Trustees Limited is made up of the net proceeds from settlement plus the deposit.

Our client reserves its rights that if settlement does not proceed, based on the above bank cheques being available at settlement at 2:00pm, Friday 20 July 2012, to proceed with enforcement action, including have a writ of restitution executed to take possession of the Property.

…

62 Later on the same date Mr Dimitriou informed Ms Nagam that he would seek the purchaser’s approval to reschedule settlement to the following Monday to enable Mrs Sanna “to raise the difference in monies” and to “have the court set a time suitable to entertain a motion if required”. In other words, it was evident that Mrs Sanna had to raise additional funds in order to be able to settle with AETL, obtain a discharge of mortgage from it and avoid execution of the Copacabana Writ.

63 On 24 July 2012:

(1) at 10.15 am Ms Nagam and Mr Dimitriou had a telephone conversation. Ms Nagam’s file note records:

… He is on his way – he has been waiting for the purchasers sol

Pls call me when you are here & my agent will come down.

…

(2) at 11.45 am Ms Nagam left a detailed message for Mr Dimitriou “asking when he will be here? Matter must settle today”;

(3) at 1.12 pm Mr Dimitriou sent an email to Ms Nagam in which he informed her that “he was just about to head into town to see Lisa of your office” and requested the total amount owing to AETL as that date, 24 July 2012; and

(4) at 2.30 pm Lisa Banner of Gadens sent an email to Mr Dimitriou in which she wrote:

Our client has advised that the balance of the loan as at today’s date is $1,981,353.62. We note that this is an indicative balance only and does not include fees and charges, interest fees and charges will continue to accrue until the loan is repaid in full.

Please advise when you will be arriving in our office for settlement?

64 On 25 July 2012 Mr Dimitriou sent two emails to Ms Nagam:

(1) the first was sent at 10.36 am in which he wrote:

Just received the okay for Settlement from Incoming Purchasers (sic) solicitor.

Booked for 3pm in your office, please confirm that suits you both.

Unfortunately the delay beyond my control.

Need to get this finalized today for the “Sake of Everyones (sic) Sanity”;

(3) the second was sent at 4.21 pm in which he wrote:

Please find copy of Gadens (sic) bank Cheque the second will be emailed in the next email.

Unfortunately, settlement will now need to be tomorrow.

Again I was let down, out of my control.

Please advise a suitable time tomorrow. I am at court in a matter in town and can get to you in between if possible- right to go now

65 On 26 July 2012:

(1) Mrs Sanna executed a mortgage over the Copacabana Property in favour of DPI (Copacabana DPI Mortgage);

(2) Mr and Mrs Sanna executed:

(a) a mortgage over the Green Valley Property in favour of DPI;

(b) a deed of loan between DPI as lender, Arcadia, DCL, DCL (NSW) and DLD (NSW) Pty Limited (DLD) as borrowers and Mr and Mrs Sanna as guarantors (DPI Deed of Loan);

(c) a general security agreement between Arcadia, DCL, DCL (NSW) and DLD as grantors, DPI as the secured party and Mr and Mrs Sanna as guarantors;

(d) a document titled “Acknowledgement of borrower pursuant to section 12CC of the Australian Securities and Investments Commission Act, 2001” from DPI to Arcadia, DCL, DCL (NSW) and DLD as borrowers and Mr and Mrs Sanna as guarantors;

(e) a document titled “independent advice acknowledgement and undertaking” from DPI to Arcadia, DCL, DCL (NSW) and DLD as borrowers and Mr and Mrs Sanna as guarantors;

(f) a statutory declaration in connection with a loan of $1.2m from DPI; and

(4) Mrs Sanna on behalf of herself and Mr Sanna, DCL, DCL (NSW) and DLD signed a letter (26 July 2012 Letter) addressed to DPI directing it to pay the mortgage advance of $1.2m on behalf of themselves, DCL, DCL (NSW) and DLD as follows:

(a) $10,0016.62 to Gadens Lawyers – fees for acting for the Mortgagor

(b) $18,000.00 to Defined Properties Investment Pty Ltd – establishment fee

(c) $20,000.00 to Defined Properties Investment Pty Ltd – interest for one month

(d) $89,286.28 to Wyse & Young International Pty Ltd (part payment)

(e) $149,223.39 to Wolgan Consulting Pty Ltd – saving fee; and

(f) $913,473.65 to Australian Executor Trustees Ltd – Mortgage discharge

…

I assume that the sum listed at (a) above was intended to be $10,016.62 which was the amount of Gadens’ fees for acting for AETL. I also note that the copy of the 26 July 2012 Letter in evidence before me had not been signed by Mr Kalischer on behalf of Arcadia.

66 The DPI Deed of Loan included:

(1) at recital B:

The Borrower and the Guarantor have requested the Lender to lend the Borrower the Principal Sum.

(2) at cl 1.1 and cl 1.2:

1.1 The Borrower hereby acknowledges receipt of the Principal Sum, namely the sum of One Million Two Hundred Thousand Dollars ($1,200,000.00).

1.2 The Principal Sum will be advanced upon the last to occur of the following:

(a) ARCADIA PROPERTY HOLDINGS PTY LTD (ACN 155 050 285) as one of the Borrower, granting to the Lender a first registered mortgage over its property being the whole of the land comprised in Folio 33/718953 (“the Property”) in such form as the Lender may reasonably require;

(b) Lepa Sanna as a Guarantor granting to the Lender a first registered mortgage over her property being the whole of the land comprised in Folios 33/718953 (“the Property”) in such form as the Lender may reasonably require;

(c) Lepa Sanna and Corrado Sanna as a Guarantor granting to the Lender a first registered mortgage over their property being the whole of the land comprised in Folios 41/875272 in such form as the Lender may reasonably require;

…

(original emphasis)

67 The Copacabana DPI Mortgage, in which Mrs Sanna was referred to as the Mortgagor, relevantly provided:

This Mortgage is being granted by LEPA SANNA on the basis that it secures any and all monies owed by the Mortgagor and or ARCADIA PROPERTY HOLDINGS PTY LTD (ACN 155 050 285) and or DCL CONSTRUCTION GROUP PTY LTD (ACN 158 381 821) and or DCL CONSTRUCTIONS (NSW) PTY LTD (ACN 085 544 627) and or DLD (NSW) (ACN 100 196 076) and or CORRADO SANNA to the Mortgagee and further all references to “the Mortgagor” and “the Mortgagee” in this document are to be construed accordingly.

The Mortgagor hereby acknowledges receipt of the principal sum of One Million Two Hundred Thousand Dollars ($l,200,000.00) and:

…

(B) Covenants and agrees with the Mortgagee as follows:-

Firstly, the Mortgagor will pay to the Mortgagee the principal sum of One Million Two Hundred Thousand Dollars ($1,200,000.00) or so much thereof that shall remain unpaid within 30 days from the date hereof.

Secondly, the Mortgagor will pay a Facility Establishment Fee of Eighteen Thousand dollars ($18,000.00) on the date of this mortgage and the Mortgagor will also pay interest on the principal sum or on so much thereof as for the time being shall remain unpaid and upon any judgment or order in which this or the preceding covenant may become merged at the rate of TWENTY dollars ($20.00) per centum per annum by one payment computed from the commencement of this Mortgage and payable on or before thirty (30) days from the date hereof (“the repayment date”). …

(original emphasis)

68 Wolgan Consulting Pty Ltd (Wolgan) also prepared a caveat on 26 July 2012 over the Copacabana Property claiming an equitable interest by virtue of a saving fee agreement dated 15 December 2011 between, relevantly, Mrs Sanna and Wolgan. Mr Dimitriou signed the statutory declaration in the caveat declaring that Wolgan had “a good and valid claim to the interest” set out in the schedule to the caveat.

69 Foleys Attorneys and Solicitors (Foleys) acted for DPI in preparing some of the documents set out at [65] above, including the DPI Deed of Loan and Copacabana DPI Mortgage. Their tax invoice dated 30 July 2012 describes the work undertaken as including “receiving instructions on 24th July 2012 to proceed in this matter as a matter of urgency and to our various attendances with Mr Dimitriou discussing the best way to proceed in this matter”.

70 On 2 August 2012 Ms Nagam sent an email to Mr Dimitriou in which she noted that settlement could take place at 2.00 pm that day on the condition that two bank cheques were made available, one payable to Gadens and the other to AETL for $10,016.62 and $913,473.65 respectively. Settlement in fact took place as foreshadowed and a discharge of mortgage and the certificate of title for the Copacabana Property were handed to Mr Dimitriou in exchange for the two cheques specified.

71 Mr Sanna submitted that the Court would infer that the two cheques dated 25 July 2012 provided to Gadens on settlement were drawn on behalf of Arcadia because of the contractual arrangements between the parties and because of Mr Dimitriou’s communications made after 25 July 2012 in which he said that the contract would settle and the purchase would complete. Mr Sanna also submitted that there was no indication that the contract for sale with Arcadia did not settle and that the DPI Deed of Loan was evidence of its completion. He said that, although it was a peculiar arrangement, Mrs Sanna being one of the guarantors of the DPI Deed of Loan and also executing the Copacabana DPI Mortgage, the main inference to be drawn from the DPI Deed of Loan was that a sale to Arcadia was contemplated. He contended that it was clear that Mrs Sanna was going to become a bankrupt and, in those circumstances, the arrangement intended to put the Copacabana Property out of her hands by selling it at value to a third party.

72 Having regard to the totality of the evidence, I do not accept the inferences urged by Mr Sanna. There is no basis on which to infer that the two cheques handed to Gadens on 2 August 2012 were provided on behalf of Arcadia. Those cheques, copies of which were in evidence before me, were bank cheques drawn by the National Australia Bank. There was no direct evidence of the source of the funds or on whose behalf they were paid. No one gave evidence on behalf of Arcadia that the payments were made on its behalf. Mr Sanna was not involved in the sale of the Copacabana Property or in making the decision to accept Arcadia’s offer and did not participate in the receipt of payment from Arcadia. Thus no weight can be given to Mr Sanna’s evidence that Arcadia purchased the Copacabana Property for approximately $950,000 and that he was aware from Mr Dimitriou that on or about 25 July 2012 Arcadia provided AETL with two cheques totalling $923,490.27.

73 Nor was there any evidence which would lead me to infer that the contract for sale with Arcadia settled. That Mr Dimitriou referred to the “purchaser’s solicitor” and “settlement” during telephone conversations with Ms Nagam on 24 July 2012 (as evidenced by file notes taken of these conversations) and in his emails dated 24 and 25 July 2012 to Ms Nagam does not lead to the inevitable conclusion as contended for by Mr Sanna that the contract with Arcadia was carried into effect. An alternate available inference is that Mr Sanna was trying to hold AETL at bay to ensure that the arrangement that had been reached to prevent AETL executing the Copacabana Writ and to pay it the amount agreed could be carried into effect.

74 In my opinion, the inference to be drawn from the evidence is that on 2 August 2012 there was a partial refinance of the AETL Loan, not a sale of the Copacabana Property to Arcadia. The following facts support that conclusion:

(1) first, AETL obtained judgment for possession and took out the Copacabana Writ which, I infer, caused Mrs Sanna to take a number of steps including putting the Copacabana Property on the market for sale;

(2) secondly, the execution of the Copacabana Writ was scheduled to take place on 13 June 2012. On 14 May 2012 Gadens informed Mr Dimitriou that if they received an unconditional contract for sale of the Copacabana Property they would seek their client’s instructions. On the morning of 13 June 2012, a hastily drawn contract for sale of the Copacabana Property naming Arcadia as purchaser was provided to Gadens. The execution of the Copacabana Writ was accordingly stayed to 21 July 2012;

(3) thirdly, settlement did not take place on 20 July 2012 as contemplated. An issue arose about the proposed deductions from the proceeds of sale and the amount that Mrs Sanna proposed to pay to AETL. Upon AETL making its requirements clear as to the amount it expected to receive in exchange for a discharge of mortgage and the provision of the certificate of title, Mrs Sanna was required to raise further funds;

(4) fourthly, as set out at [63]-[64] above, that Mr Dimitriou first told Gadens that settlement would take place on 24 July 2012 and then said 25 July 2012, does not make Mr Sanna’s position any stronger. Settlement did not occur on either of those dates. The involvement of DPI, a company in the control of Mr Dimitriou, from 24 July 2012 and the documents which were executed on 26 July 2012 involving DPI (as set out at [65] above) would suggest that settlement could not occur on those dates;

(5) fifthly, on 24 July 2012 DPI retained Foleys to draft the suite of loan documents referred to at [65] above on an urgent basis. While some of those documents named four companies, including Arcadia, as borrowers, Mr and Mrs Sanna were guarantors and Mrs Sanna provided the Copacabana DPI Mortgage and Mr and Mrs Sanna provided a mortgage over the Green Valley Property as security for the monies advanced under the DPI Deed of Loan. In particular, under the Copacabana DPI Mortgage, Mrs Sanna was liable for repayment of the monies advanced by DPI and the 26 July 2012 Letter relevantly directed DPI to pay a portion of the loan monies to AETL in order to obtain a discharge of the AETL Mortgage and the balance of those monies to discharge other obligations of Mr and Mrs Sanna and companies associated with them. In other words, I would infer that, despite the inclusion of Arcadia as a borrower, the monies owed were advanced by DPI for the benefit of Mrs Sanna and parties associated with her to provide them with funding to meet a number of their obligations; and

(6) sixthly, a search of the Copacabana Property dated 3 August 2012 shows that, as at that date, Mrs Sanna remained the registered proprietor, the mortgage to AETL was no longer registered and a mortgage to DPI had been registered on the title of the property. There was simply no evidence that Mrs Sanna held the Copacabana Property as bare trustee or otherwise for Arcadia.

75 Mr Sanna submitted that it was not necessary to have a transfer to effect a sale of property and that a transfer is only required to effect a registration of a transfer of title. He said that the only explanation for Arcadia not becoming registered on title was so that it did not have to pay stamp duty which was a prerequisite to registration. That may well be a reason, albeit illegitimate, why a purchaser would not register a transfer of property following a sale but, given that I am not satisfied that the contract with Arcadia was carried into effect and that the property was sold to it, it is not necessary for me to consider that submission. In any event, there was no evidence of that intention on the part of Arcadia and it is difficult to accept that a third party purchaser for valuable consideration would be prepared to proceed without a transfer and registration in its name of the asset purportedly acquired. That is particularly so in circumstances where Mr Sanna submitted that it was highly likely that Mrs Sanna would become a bankrupt.

Transfer of the Copacabana Property to Mr Sanna

76 According to Mr Sanna, in late November 2012 he had a conversation with Mr Dimitriou to the following effect:

Mr Dimitriou: Corrado, I am prepared to sell Copacabana to you for whatever Arcadia paid for it. I really need the funds right now.

Mr Sanna: George, if I can raise the funds I will buy it.

Mr Dimitriou: I know a manager by the name of Anne Barton who works at Westpac. She can get the loan for you. Also, I have not transferred the property into Arcadia’s name as yet. I will arrange all the paperwork so you don’t have to pay stamp duty.

Mr Sanna: Okay, that sounds great.

77 In cross-examination Mr Sanna said that he learnt what Arcadia had paid for the Copacabana Property, which he recalls was approximately $948,000, prior to the time that he had the conversation referred to in the preceding paragraph. Mr Sanna said that he was at Daleys Point when Mr Dimitriou called him and told him he had done a deal and bought the property. Mr Sanna said the Mr Dimitriou had asked him whether he was interested in buying it from him and during that conversation also told him that he had purchased it for $948,000.

78 On 21 December 2012 Mr Sanna applied to Westpac for a loan of $1.48m for “residential facilities”. In the loan application (Westpac Loan Application) Mr Sanna’s real estate property assets were listed as the Green Valley Property owned jointly with Mrs Sanna and rented for $1,800 per week and the Copacabana Property to be transferred to him. In cross-examination Mr Sanna said that the Green Valley Property had never been rented out but that his mother had lived in the property since it was built in the mid-1990s until she passed away in July 2013 and that the property had since remained vacant. Mr Sanna’s liabilities in the Westpac Loan Application included a loan from DPI for $1.25m secured over the Copacabana Property and a loan from La Trobe for $190,000 secured over the Green Valley Property.

79 Mr Sanna said that the Westpac Loan Application was prepared on instructions from Mr Dimitriou and that he was asked to attend the Westpac branch to sign it, which he did without reading it. Mr Sanna said that the inclusion in the Westpac Loan Application of a loan of $1.25m to DPI secured over the Copacabana Property was not correct although he acknowledged that the total amount applied for by way of finance equated to the approximate combined amounts owing to DPI and La Trobe.

80 On 3 January 2013 Elders Real Estate wrote to Mrs Sanna providing its opinion of the current rental market value of the Copacabana Property, being around $1,500 per week on the basis that the property was fully furnished, maintained and all gardening was included.

81 By letter dated 15 January 2013 DPI referred to the first registered mortgages it held over the Copacabana Property and the Green Valley Property, informed Mr Sanna that it was holding documentation in preparation of “the proposed settlement” and provided an indicative discharge figure of $1,210,837.88 if the settlement took place before 31 January 2013.

82 On 17 April 2013 Mr Sanna accepted a loan offer for two loans from Westpac for a total amount of $1,008,000 for the purpose of refinancing existing home loans made up of a loan of $818,000 to be secured by a mortgage over the Copacabana Property and a loan of $190,000 to be secured by a mortgage over the Green Valley Property. In cross-examination, Mr Sanna said that Westpac was only willing to lend $818,000 on the Copacabana Property because that was its value at the time. He said that because the finance was less than the amount for which Mr Dimitriou had offered to sell the Copacabana Property to him, he paid Mr Dimitriou an additional $166,000 in cash.

83 On 17 April 2013 Mr Sanna also executed mortgages over the Copacabana Property and the Green Valley Property in favour of Westpac. At the time, Mrs Sanna was still the registered proprietor of the Copacabana Property.

84 On or about 8 May 2013 Mr Sanna signed the Copacabana Transfer which provided that Mrs Sanna transferred the Copacabana Property to him for consideration of $1.00 pursuant to s 90C of the Family Law Act. Mr Sanna said that he knew that at the time he signed the Copacabana Transfer he was intending to pay $948,000 for the Copacabana Property, not $1.00 and that he was buying the property from Arcadia, not Mrs Sanna. Mr Sanna explained the content of the Copacabana Transfer by saying that they signed whatever Mr Dimitriou put in front of them and that “it’s all Mr Dimitriou’s doing”.

85 Mr Sanna said that on or about 9 May 2013 he settled the purchase of the Copacabana Property from Arcadia for approximately $950,000 and, at the same time, arranged for the refinance of the Green Valley Property. He said that upon settlement of the Copacabana Property, Mr Dimitriou, on behalf of Arcadia, gave him the Copacabana Transfer signed by Mrs Sanna.

86 As at 25 May 2013 Mr Sanna was the registered proprietor of the Copacabana Property and a mortgage to Westpac was registered on title.

87 I do not accept Mr Sanna’s evidence that he purchased the Copacabana Property from Arcadia. Rather, in my opinion, on 9 May 2013 there was a refinance of the Copacabana Property by Westpac; DPI, as outgoing mortgagee, was paid out; and Mr Sanna became the registered proprietor of that property upon registration of the Copacabana Transfer. My reasons for forming that opinion follow.

88 First, I have already found that there was no sale of the Copacabana Property to Arcadia but that what took place on 2 August 2012 was a refinance with DPI. Thus there could be no subsequent sale by Arcadia to Mr Sanna.

89 Secondly, Mr Sanna’s evidence on the issue was unsatisfactory and should be rejected. In his evidence in chief Mr Sanna recounted a conversation with Mr Dimitriou in which Mr Dimitriou offered the Copacabana Property to Mr Sanna on behalf of Arcadia. In cross-examination Mr Sanna gave evidence of an earlier conversation in which Mr Dimitriou said that he had done a deal and brought the property and offered it to him for $948,000. But Mr Dimitriou was not an officer of Arcadia; it was unclear how he could offer the property for sale on behalf of Arcadia; and there was no evidence that Arcadia or Mr Dimitriou had purchased the Copacabana Property.

90 Thirdly, Mr Sanna said that he had signed the Copacabana Transfer knowing it was wrong but did so, in effect, because Mr Dimitriou told him to do so. I do not accept that explanation. Mr Sanna was an experienced developer who had run his own construction business and was able to make his own decisions. I do not accept that he slavishly did what Mr Dimitriou told him to do without understanding why that was so.

91 Fourthly, in cross-examination Mr Sanna accepted that he was not in fact present at the settlement but that someone from Westpac attended on his behalf and received the Copacabana Transfer as incoming mortgagee. In other words, contrary to his evidence, Mr Dimitriou did not provide the Copacabana Transfer to him on Arcadia’s behalf.

92 Fifthly, the objective evidence discloses that Westpac subsequently reported to Mr Sanna that it had opened his loan accounts on 9 May 2013 and that, as directed, had made payments on that date to, among others, La Trobe Financial for amounts of $184,423.43 and $451.72 and DPI for $820,662.26. No payments were made to the purported vendor, Arcadia, and there was no evidence that Arcadia directed Mr Sanna to make a payment to DPI on its behalf.

93 Sixthly, no written contract for sale of the Copacabana Property between Arcadia as vendor and Mr Sanna as purchaser was produced by Mr Sanna. Counsel for Mr Sanna submitted that the contract of sale was oral but the only evidence of such a contract was Mr Sanna’s conversation with Mr Dimitriou which I have rejected (see [89] above).

Subdivision of the Copacabana Property

94 The Copacabana Property was subsequently subdivided into two lots comprised in folio identifiers 331/1218658 (First Copacabana Lot) and 332/1218658 (Second Copacabana Lot). On about 4 May 2016 the First Copacabana Lot was sold to a third party for $535,000. There was no dispute that the purchasers were independent and that this was an arm’s length transaction.

95 Mr Sanna said that upon the sale of the First Copacabana Lot Westpac’s mortgage over the Green Valley Property of approximately $190,000 was paid out as were debts owing to E & B Pastoral Pty Limited (E & B Pastoral) and Boral. But a direction to pay from Dobell Conveyancing, who acted for Mr Sanna on the sale, shows that the proceeds of sale, net of the deposit, were paid at Mr Sanna’s direction as follows:

(1) Scott Ashwood $55.00;

(2) Dobell Conveyancing $2,094.10; and

(3) Westpac $479,326.56.

The balance of the deposit, after payment of the agent’s commission, was paid to Mr Sanna.

96 Mr Sanna remains the registered proprietor of the Second Copacabana Lot.

Transfer of the Green Valley Property to Mr Sanna

97 As at 30 December 2012 La Trobe Financial was owed $182,820.61 secured over the Green Valley Property.

98 Mr Sanna said that in May 2013 Mrs Sanna transferred her interest in the Green Valley Property to him and that thereafter he solely attended to making the mortgage repayments to Westpac. The Green Valley Transfer was also expressed to be in consideration of $1.00 and made pursuant to s 90C of the Family Law Act.

99 On 9 May 2013 Westpac paid La Trobe Financial the amounts referred to at [92] above as directed by Mr Sanna. A mortgage dated 17 April 2013 executed by Mr Sanna in favour of Westpac over the Green Valley Property was in evidence before me. However, a historical search of that property undertaken on 23 April 2015 discloses that the Westpac mortgage was not registered on title as at May 2013 or in the period following.

100 A search of the Green Valley Property dated 15 April 2015 shows that Mr and Mrs Sanna remained as registered proprietors as joint tenants.

101 Mr Sanna said that after a squatter was removed from the Green Valley Property he undertook repairs at a total cost of approximately $32,000.

Creditor claims

102 On 15 July 2011 Mr Sanna completed and signed a Boral confidential credit application form for DCL (NSW). At the time he was a director of DCL (NSW). On 15 and 25 July 2011 respectively Mr and Mrs Sanna signed a confidential personal guarantee and indemnity agreement guaranteeing the payment of the price charged by Boral for any goods supplied to DCL (NSW) and any other monies owing by DCL (NSW) to Boral (Boral Guarantee).

103 On about 10 May 2013 Boral registered caveat AH724887 on the title of the Green Valley Property claiming an equitable interest pursuant to the Boral Guarantee to secure the amount of $169,002.35 (Boral Caveat).

104 On 29 May 2013:

(1) Boral commenced proceedings in the District Court of New South Wales (District Court) against DCL (NSW) and Mr and Mrs Sanna claiming a total amount of $180,469.77 (Boral Proceeding); and

(2) Perpetual Trustee Company Limited (Perpetual) obtained judgment against Mrs Sanna for $478,583.54 in the District Court.

105 On 10 July 2013 Mrs Sanna committed an act of bankruptcy. On 23 July 2013 Perpetual filed a creditor’s petition against Mrs Sanna in the Federal Circuit Court of Australia and on 10 December 2013 that court made a sequestration order against Mrs Sanna’s estate and appointed Jason Lloyd Porter and the Trustee jointly and severally as trustees in bankruptcy of her estate. On 31 July 2015 this Court made an order for the joint appointment of the trustees to be transferred to the Trustee as sole trustee.

106 On 29 April 2015 orders were made by consent in the Boral Proceeding for judgment in favour of Boral against Mr Sanna in the sum of $100,000, staying the enforcement and execution of that judgment until 15 May 2015 and vacating the trial scheduled to commence on 4 May 2015. The District Court also noted an agreement between Boral and Mr Sanna which included that, at the time of payment of the judgment sum, Boral would provide Mr Sanna with an executed withdrawal of caveat in registrable form for the Boral Caveat. Notwithstanding the orders made by the District Court, Mr Sanna did not pay the judgment sum by 15 May 2015.

107 On 18 September 2015 Boral Construction Materials Group Limited registered caveat AJ819350D on the title of the Green Valley Property, relying on the Boral Guarantee to claim an equitable charge over all monies owing or becoming owing by Mr and Mrs Sanna to it, which at that date, was $200,000.

108 In May 2016 Boral commenced bankruptcy proceedings against Mr Sanna in relation to the monies owing by him to it. Mr Sanna accepted that it was not until after the commencement of that proceeding that he paid Boral.

109 In 2009 E & B Pastoral as lender, Danic as borrower and Mr and Mrs Sanna as guarantors entered into a deed pursuant to which E & B Pastoral made advances to Danic and DCL (NSW). There were three loans which were the subject of the deed made in 2008 and 2009 amounting to $140,000. Mr Sanna said that there were also some current loans from E & B Pastoral made to him which are the subject of caveats by that company over the Copacabana Property and the Green Valley Property.

110 On or about 30 September 2015 E & B Pastoral and Mr Horne registered caveat AJ884104B on the title of the Copacabana Property and the Green Valley Property, claiming an interest by way of equitable charge pursuant to an unregistered mortgage. It relied on a mortgage and deed of loan in respect of a debt of $77,895.97 dated 30 September 2015 between E & B Pastoral, Mr Horne and Mr Sanna.

statutory FRAMEWORK

111 Section 120 of the Act relevantly provides:

Transfers that are void against trustee

(1) A transfer of property by a person who later becomes a bankrupt (the transferor) to another person (the transferee) is void against the trustee in the transferor’s bankruptcy if:

(a) the transfer took place in the period beginning 5 years before the commencement of the bankruptcy and ending on the date of the bankruptcy; and

(b) the transferee gave no consideration for the transfer or gave consideration of less value than the market value of the property.

…

Exemptions

…

(3) Despite subsection (1), a transfer is not void against the trustee if:

(a) in the case of a transfer to a related entity of the transferor:

(i) the transfer took place more than 4 years before the commencement of the bankruptcy; and

(ii) the transferee proves that, at the time of the transfer, the transferor was solvent; or

(b) in any other case:

(i) the transfer took place more than 2 years before the commencement of the bankruptcy; and

(ii) the transferee proves that, at the time of the transfer, the transferor was solvent.

…

Refund of consideration

(4) The trustee must pay to the transferee an amount equal to the value of any consideration that the transferee gave for a transfer that is void against the trustee.

112 Section 121 of the Act relevantly provides:

Transfers that are void

(1) A transfer of property by a person who later becomes a bankrupt (the transferor) to another person (the transferee) is void against the trustee in the transferor’s bankruptcy if:

(a) the property would probably have become part of the transferor’s estate or would probably have been available to creditors if the property had not been transferred; and

(b) the transferor’s main purpose in making the transfer was:

(i) to prevent the transferred property from becoming divisible among the transferor’s creditors; or

(ii) to hinder or delay the process of making property available for division among the transferor’s creditors.

…

Showing the transferor’s main purpose in making a transfer

(2) The transferor’s main purpose in making the transfer is taken to be the purpose described in paragraph (1)(b) if it can reasonably be inferred from all the circumstances that, at the time of the transfer, the transferor was, or was about to become, insolvent.

…

Transfer not void if transferee acted in good faith

(4) Despite subsection (1), a transfer of property is not void against the trustee if:

(a) the consideration that the transferee gave for the transfer was at least as valuable as the market value of the property; and

(b) the transferee did not know, and could not reasonably have inferred, that the transferor’s main purpose in making the transfer was the purpose described in paragraph (1)(b); and

(c) the transferee could not reasonably have inferred that, at the time of the transfer, the transferor was, or was about to become, insolvent.

…

Refund of consideration

(5) The trustee must pay to the transferee an amount equal to the value of any consideration that the transferee gave for a transfer that is void against the trustee.

…

113 For the purposes of s 120 and s 121 of the Act the “market value” of property transferred is defined as its market value at the time of transfer: see s 120(7)(c) and s 121(9)(c) of the Act.

consideration

The Copacabana Property

Is the Copacabana Transfer void against the Trustee?

114 I turn first to consider the Trustee’s claim pursuant to s 121 of the Act which was the primary basis on which the Trustee sought to impugn the Copacabana Transfer.

115 It is clearly the case, as required by s 121(1)(a) of the Act that, but for the Copacabana Transfer, the Copacabana Property would probably have become part of Mrs Sanna’s estate or been available to creditors.

116 The next matter which the Trustee must establish is Mrs Sanna’s main purpose in making the Copacabana Transfer and, in particular, whether it was to prevent the Copacabana Property from becoming divisible among her creditors or to hinder or delay that process as required by s 121(1)(b) of the Act. In that regard, the Trustee relies on s 121(2) of the Act which facilitates proving a transferor’s main purpose. That is, Mrs Sanna’s main purpose will be taken to be a purpose listed in s 121(1)(b) of the Act if it can reasonably be inferred from all of the circumstances that, at the time of the Copacabana Transfer, she was or was about to become insolvent.

117 At the hearing counsel for Mr Sanna conceded that Mrs Sanna was insolvent as at 8 May 2013, the date of the Copacabana Transfer (at T144). That being so, s 121(2) of the Act operates to establish that Mrs Sanna’s main purpose in making the Copacabana Transfer was as set out in s 121(1)(b). Even absent that concession, I would readily find that Mrs Sanna’s main purpose in entering into the Copacabana Transfer was as set out in s 121(1)(b) for the following reasons.

118 First, the evidence established that, at the time she made the Copacabana Transfer, Mrs Sanna was in financial difficulty and had been for some time. She had been unable to meet her recurring financial commitments to AETL since 2009 and, despite the refinance on the Copacabana Property, had remained indebted to AETL for the balance of the AETL Loan, which she could not pay. Her financial difficulties were exacerbated by the fact that for a period, due to illness, she had been unable to work. Further, shortly after the date of the Copacabana Transfer, Perpetual obtained judgment for the balance of the AETL Loan against her of $478,583.54. The Boral Proceeding, in which Boral claimed $180,469.77 from Mrs Sanna, among others, was also commenced on that date. In those circumstances it could be reasonably inferred that, at the time of the Copacabana Transfer, Mrs Sanna was, or was about to become, insolvent.

119 Secondly, as the Trustee submitted, the Court would be obliged to draw such an inference about Mrs Sanna’s intention. In Official Trustee v Marchiori (1983) 69 FLR 291 at 294, in considering an application by the applicant trustee challenging the disposition of a motor vehicle by the bankrupt to the respondent under a former version of s 121 of the Act, Fisher J noted that it was settled law that the onus of establishing that the disposition was made with the intent to defraud creditors lay upon the applicant. At 296, after finding that the bankrupt made the disposition in question with the necessary intent, his Honour said:

… In this case the words of Brennan J. in delivering the judgment of the Full Court of the Federal Court in Noakes v. Harvy Holmes & Son (1979) 26 A.L.R. 297 are very much in point. He said at page 303:

The case falls squarely within the line of authorities of which Freeman v. Pope (1870) 5 Ch. App. 538 is the leading example, where Lord Hatherley L.C. said (at 541): ‘But it is established by the authorities in the absence of any such direct proof of intention, if a person owing debts makes a settlement which subtracts from the property which is the proper fund for the payment of those debts, an amount without which the debts cannot be paid, then, since it is the necessary consequence of the settlement (supposing it effectual) that some creditors must remain unpaid, it would be the duty of the judge to direct the jury that they must infer the intent of the settlor to have been to defeat or delay his creditors, and that the case is within the statute’.

That proposition does not trespass upon the rule as to onus of proof; it is a particular illustration of the discharge of the onus by inference from the known facts (cf. Re Holland; Gregg v. Holland [1902] 2 Ch. 360 at 381).

…

120 Here the only explanation, in the face of the evidence of Mrs Sanna’s financial circumstances, is that she made the Copacabana Transfer with the intent to prevent that property from becoming divisible among her creditors.

121 I turn then to consider whether Mr Sanna has made out his Defence as pleaded in relation to the Copacabana Property. In my opinion, he has not. In particular:

(1) there was no evidence that an auction of the Copacabana Property was held on 14 May 2012. Indeed in cross-examination Mr Sanna said that he did not believe the auction had been held despite what he deposed to in his affidavit (Defence at [5(i)]);

(2) there was no evidence that Mr Dimitriou told Mr Sanna that he could negotiate with AETL to purchase the Copacabana Property; that the purchaser would be a company controlled by Mr Dimitriou; that at a later point in time when Mr Sanna could get finance Mr Dimitriou would get that company to sell the Copacabana Property to Mr Sanna; and that Mr Sanna made no promise to act in any particular manner (Defence at [5(k)]);

(3) the evidence did not establish that on 25 July 2012 the contract for sale between Mrs Sanna and Arcadia settled and an agent of Russo and Partners attended the settlement on behalf of Arcadia and gave AETL two bank cheques in return for which AETL gave Arcadia a discharge of its mortgage and the certificate of title to the Copacabana Property (Defence at [5(l), (m) and (n)]). As set out at [71]-[73] above, the inference to be drawn from the evidence is that there was a refinance with DPI and on 2 August 2012 two cheques dated 25 July 2012 were provided by Mr Dimitriou, a director of DPI, to AETL in exchange for a discharge of its mortgage and the certificate of title for the Copacabana Property;

(4) the evidence did not establish that Mrs Sanna was at settlement and that she gave Arcadia a transfer of land in registrable form (Defence at [5(p)]);

(5) it has not been established that from 25 July 2012, Mrs Sanna held the legal title and interest in the Copacabana Property on a bare trust for Arcadia. Nor is it the case that, as a result, Mrs Sanna was entitled to no consideration for the Copacabana Transfer or, to the extent that she was, only entitled to that consideration in her capacity as bare trustee for Arcadia (Defence at [5(u) and (w)]);

(6) it has not been established that the Copacabana DPI Mortgage did not evidence an actual transaction or secure repayment of money; that it was not in fact signed by Mrs Sanna; or that Mr Dimitriou, as the controlling mind of Arcadia and DPI, did not wish to register a transfer from Mrs Sanna to Arcadia as he intended to have the Copacabana Property transferred to Mr Sanna without any stamp duty being paid and registered the Copacabana DPI Mortgage in the meantime to protect Arcadia’s interest (Defence at [6]); and

(7) given the finding that what occurred was a refinance and not a sale of the Copacabana Property to Arcadia, the matters pleaded in [7], [8] and [9] of the Defence are not made out. That is, it has not been established that Mr Sanna purchased the Copacabana Property from Arcadia. Rather, Mr Sanna obtained finance from Westpac, both in relation to the Copacabana Property and the Green Valley Property, which allowed him to pay out the Copacabana DPI Mortgage.

122 It follows that Mr Sanna has failed to establish that Arcadia acquired the Copacabana Property from Mrs Sanna such that from that time Mrs Sanna held the legal title on a bare trust for Arcadia and that he acquired the Copacabana Property from Arcadia with the legal title to the property being transferred pursuant to the Copacabana Transfer.

123 Mr Sanna has also failed to bring himself within the exemption set out at s 121(4) of the Act. To the extent he wished to do so, the onus fell on Mr Sanna, as the transferee of the property, to establish that he could have the benefit of that subsection: see Re Jury; Ashton v Prentice (1999) 92 FCR 68 at [67].

124 Mr Sanna’s defence does not seek to establish that he acted in good faith so as to bring him within s 121(4) of the Act but relies on establishing that the Copacabana Property was acquired from Arcadia and not Mrs Sanna and thus was not a transaction that could come within s 121 (or s 120) of the Act. Even if that were not so, I accept the Trustee’s submission that Mr Sanna has not led any evidence to establish that the consideration given for the Copacabana Transfer was at least as valuable as the market value of the Copacabana Property or that he did not know, and could not reasonably have inferred, that Mrs Sanna’s main purpose in making the Copacabana Transfer was to prevent the Copacabana Property from becoming divisible among her creditors or to delay or hinder that purpose. An additional matter preventing Mr Sanna from taking advantage of s 121(4) was his evidence of Mrs Sanna’s financial position which was clearly contrary to subs (4)(c).