FEDERAL COURT OF AUSTRALIA

Queensland Bauxite Ltd, in the matter of Queensland Bauxite Ltd [2018] FCA 2113

ORDERS

QUEENSLAND BAUXITE LTD ACN 124 873 507 Plaintiff | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 1322(4)(a) of the Corporations Act 2001 (Cth) (Corporations Act), it is declared that any offer for sale or sale of the shares listed in Annexure A during the 12-month period commencing from the date of issue is not invalid by reason of:

(a) the seller’s failure to issue a notice under s 708A of the Corporations Act or a prospectus under s 708A(11) of the Corporations Act as the case may be before selling the shares;

(b) any consequent failure to comply with s 707(3) and 727(1) of the Corporations Act.

2. Any holder as at the date of these orders of shares listed in Annexure A who is still the holder at the time of application may apply at any time in the next 12 months for a different order.

3. Pursuant to s 1322(4)(c) of the Corporations Act any sellers of the shares listed in Annexure A are relieved from any civil liability arising out of any contravention of ss 707(3) and 727(1) of the Corporations Act.

4. A sealed copy of these orders is to be served on the Australian Securities and Investments Commission (ASIC) as soon as reasonably practicable and upon service of these orders on ASIC, ASIC is to include these orders on its database.

5. As soon as reasonably practicable a copy of these orders be sent to the last known email address of each person to whom the shares listed in Annexure A were issued.

6. As soon as reasonably practicable and prior to the reinstatement of the class of securities ‘QBL’ on the ASX the plaintiff is to publish an announcement on the ASX markets announcement platform in which a copy of these orders is included.

7. In addition to the liberty to apply under order 2, for a period of 28 days from the date of reinstatement on the ASX of the class of securities ‘QBL’ any person who claims to have suffered substantial injustice or is likely to suffer substantial injustice by the making of any or all of these orders has liberty to apply to vary or to discharge these orders.

8. There be no order as to costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MCKERRACHER J:

OVERVIEW

1 These are reasons for orders made pursuant to s 1322(4)(a) and s 1322(4)(c) of the Corporations Act 2001 (Cth) (CA) to:

(a) validate trading in the plaintiff’s shares that were issued pursuant to the issues set out in the table referred to in [24] below (Uncleansed Securities Issues);

(b) relieve on-selling shareholders from the civil consequences of any secondary trading in the shares issued under the Uncleansed Securities Issues (Uncleansed Securities).

2 The words ‘cleansing’ or ‘uncleansed’ are not used in the legislation but are used in industry documentation including ASIC’S Regulatory Guide 173 and the ASX Guidance Note 08.

3 The Uncleansed Securities Issues were not accompanied by cleansing notices issued under s 708A(5) of the CA or cleansing prospectuses issued under s 708A(11) of the CA.

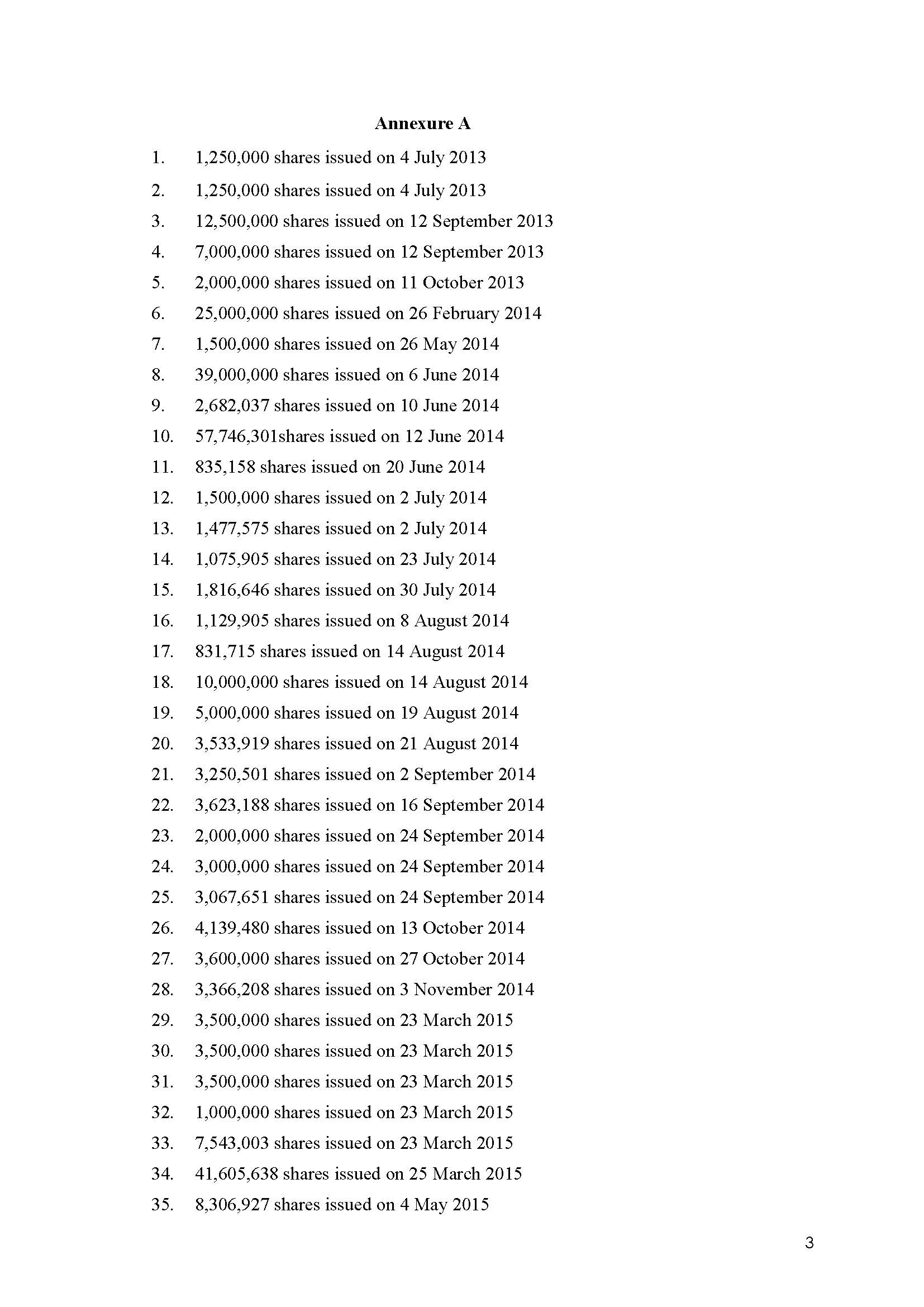

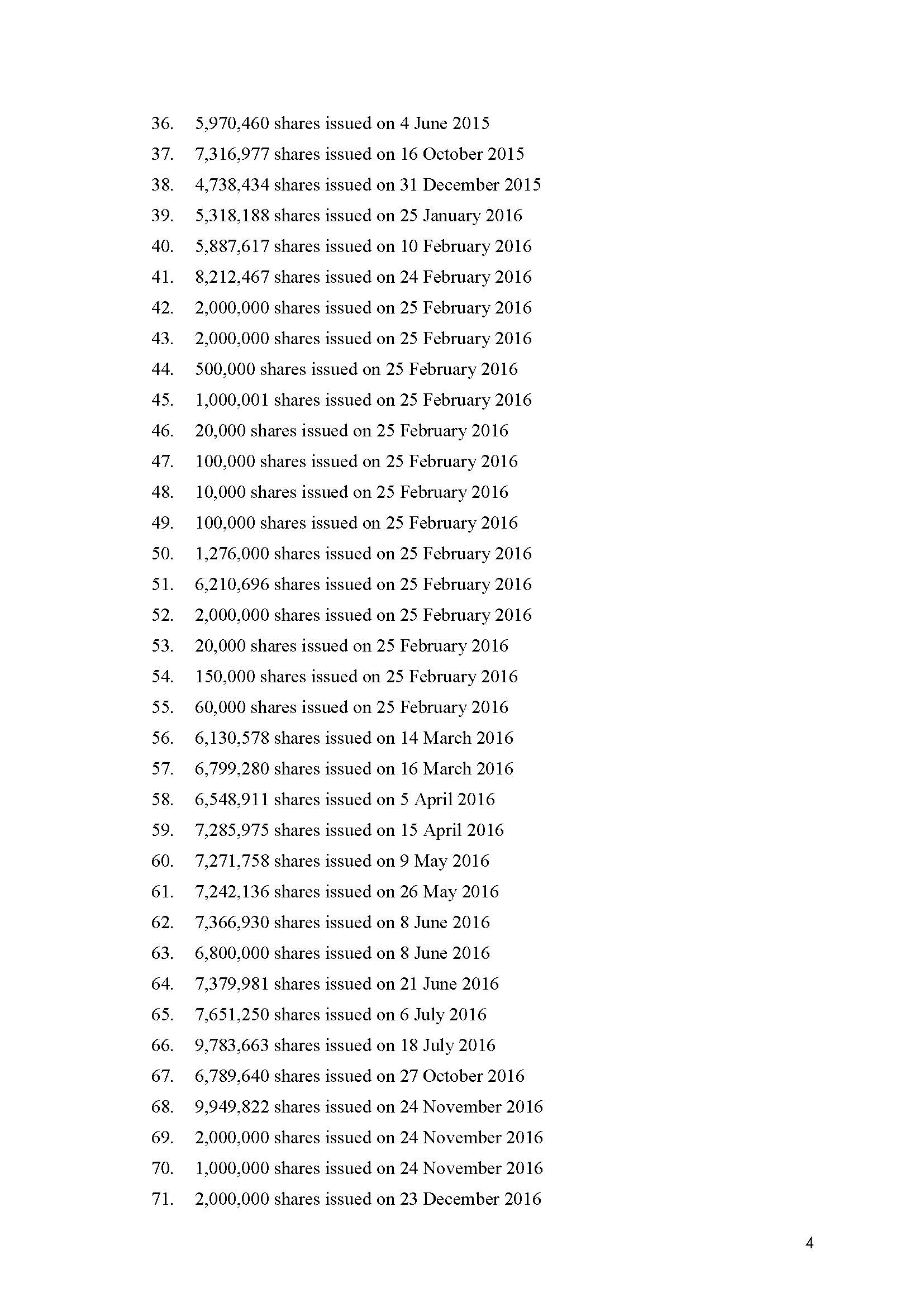

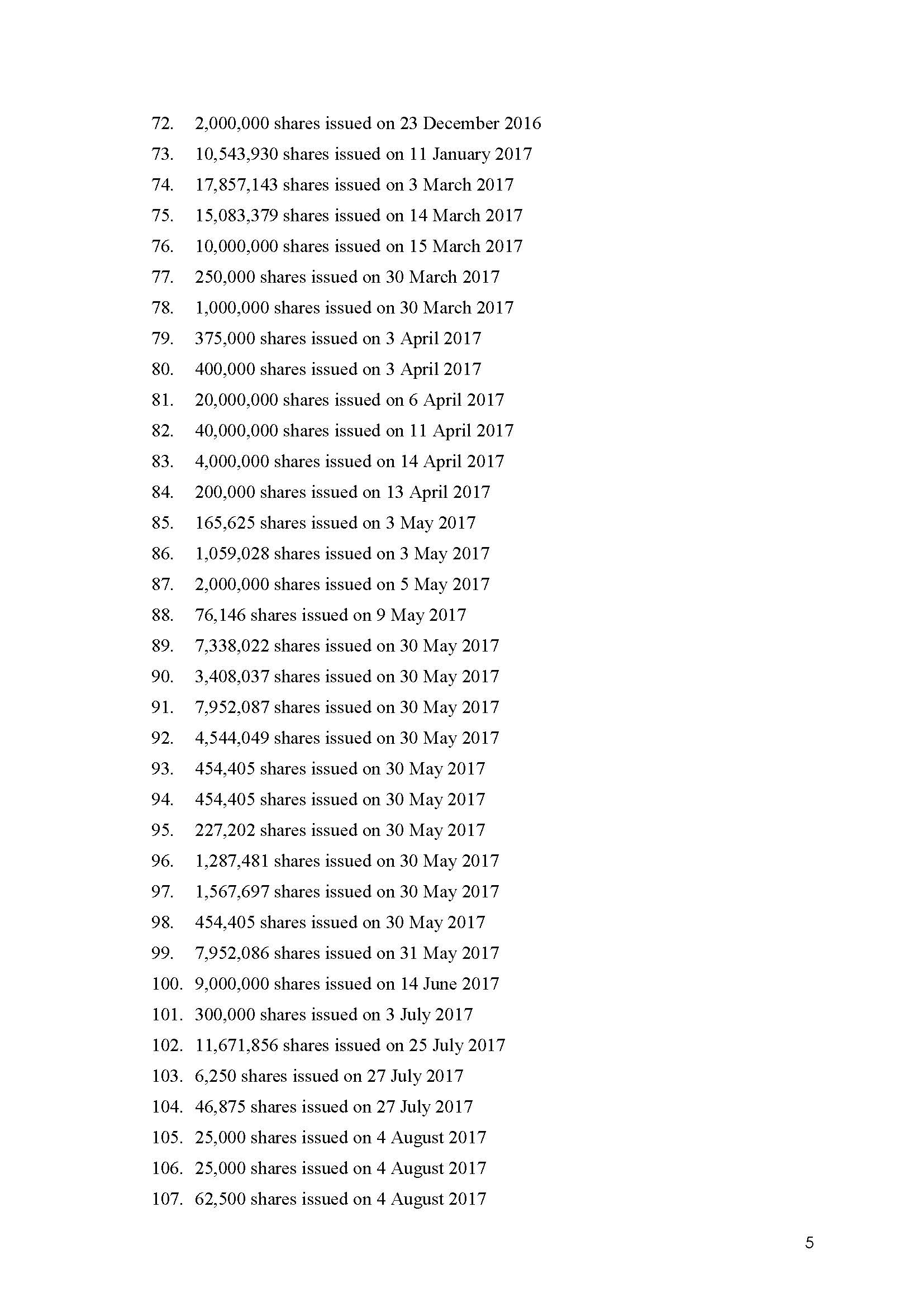

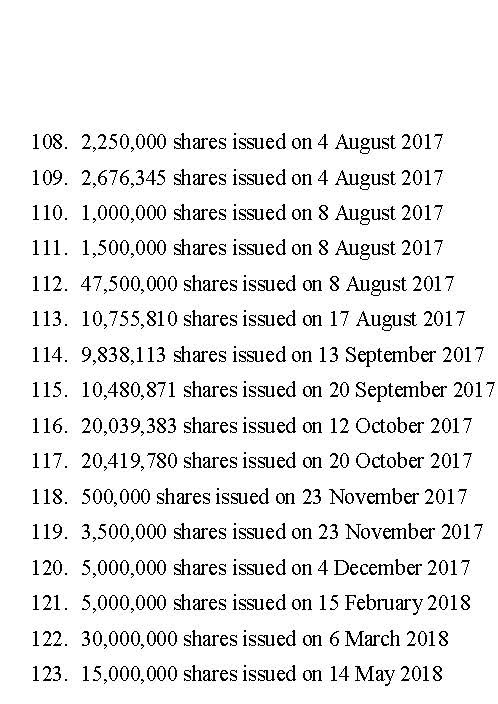

4 As a consequence, secondary trading in the Uncleansed Securities would involve breaches by sellers of s 707(3) and s 727(1) of the CA, unless the holders made prior disclosure under Ch 6D.2 of the CA.

5 The lodging by the plaintiff of a re-compliance prospectus on 27 September 2018 enabled subsequent trading in those Uncleansed Securities that were issued not more than 12 months prior to that date without disclosure.

6 Validating orders were sought from this Court in relation to secondary trading in Uncleansed Securities that occurred before 27 September 2018 (the Application).

7 The Application was supported by several affidavits, including affidavits deposed by the plaintiff’s director and company secretary, Mr Feldman.

LEGISLATION

8 Section 707 and s 708A of the CA provide:

707 Sale offers that need disclosure

Only some sales need disclosure

(1) An offer of securities for sale needs disclosure to investors under this Part only if disclosure is required by subsection (2), (3) or (5).

Off-market sale by controller

(2) An offer of a body’s securities for sale needs disclosure to investors under this Part if:

(a) the person making the offer controls the body; and

(b) either:

(i) the securities are not quoted; or

(ii) although the securities are quoted, they are not offered for sale in the ordinary course of trading on a relevant financial market;

and section 708 does not say otherwise.

Note: See section 50AA for when a person controls a body.

Sale amounting to indirect issue

(3) An offer of a body’s securities for sale within 12 months after their issue needs disclosure to investors under this Part if:

(a) the body issued the securities without disclosure to investors under this Part; and

(b) either:

(i) the body issued the securities with the purpose of the person to whom they were issued selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them; or

(ii) the person to whom the securities were issued acquired them with the purpose of selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them;

and section 708 or 708A does not say otherwise.

Note 1: Section 706 normally requires disclosure for the issue of securities. This subsection is intended to prevent avoidance of section 706. However, to establish a contravention of this subsection, the only purpose that needs to be shown is that referred to in paragraph (b).

Note 2 The issuer and the seller must both consent to the disclosure document (see section 720).

The purpose test in subsection (3)

(4) For the purposes of subsection (3):

(a) securities are taken to be:

(i) issued with the purpose referred to in subparagraph (3)(b)(i); or

(ii) acquired with the purpose referred to in subparagraph (3)(b)(ii);

if there are reasonable grounds for concluding that the securities were issued or acquired with that purpose (whether or not there may have been other purposes for the issue or acquisition); and

(b) without limiting paragraph (a), securities are taken to be:

(i) issued with the purpose referred to in subparagraph (3)(b)(i); or

(ii) acquired with the purpose referred to in subparagraph (3)(b)(ii);

if any of the securities are subsequently sold, or offered for sale, within 12 months after issue, unless it is proved that the circumstances of the issue and the subsequent sale or offer are not such as to give rise to reasonable grounds for concluding that the securities were issued or acquired with that purpose.

Sale amounting to indirect off-market sale by controller

(5) An offer of a body’s securities for sale within 12 months after their sale by a person who controlled the body at the time of the sale needs disclosure to investors under this Part if:

(a) at the time of the sale by the controller either:

(i) the securities were not quoted; or

(ii) although the securities were quoted, they were not offered for sale in the ordinary course of trading on a relevant financial market on which they were quoted; and

(b) the controller sold the securities without disclosure to investors under this Part; and

(c) either:

(i) the controller sold the securities with the purpose of the person to whom they were sold selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them; or

(ii) the person to whom the securities were sold acquired them with the purpose of selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them;

and section 708 does not say otherwise.

Note 1: Subsection (2) normally requires disclosure for a sale by a controller. This subsection is intended to prevent avoidance of subsection (2). However, to establish a contravention of this subsection, the only purpose that needs to be shown is that referred to in paragraph (c).

Note 2: See section 50AA for when a person controls a body.

Note 3: The controller and the seller must both consent to the disclosure document (see section 720).

The purpose test in subsection (5)

(6) For the purposes of subsection (5):

(a) securities are taken to be:

(i) sold with the purpose referred to in subparagraph (5)(c)(i); or

(ii) acquired with the purpose referred to in subparagraph (5)(c)(ii);

if there are reasonable grounds for concluding that the securities were sold or acquired with that purpose (whether or not there may have been other purposes for the sale or acquisition); and

(b) without limiting paragraph (a), securities are taken to be:

(i) sold with the purpose referred to in subparagraph (5)(c)(i); or

(ii) acquired with the purpose referred to in subparagraph (5)(c)(ii);

if any of the securities are subsequently sold, or offered for sale, within 12 months after their sale by the controller, unless it is proved that the circumstances of the initial sale and the subsequent sale or offer are not such as to give rise to reasonable grounds for concluding that the securities were sold or acquired (in the initial sale) with that purpose.

…

708A Sale offers that do not need disclosure

Sale offers to which this section applies

(1) This section applies to an offer (the sale offer) of a body’s securities (the relevant securities) for sale by a person if:

(a) but for subsection (5), (11) or (12), disclosure to investors under this Part would be required by subsection 707(3) for the sale offer; and

(b) the securities were not issued by the body with the purpose referred to in subparagraph 707(3)(b)(i); and

(c) a determination under subsection (2) was not in force in relation to the body at the time when the relevant securities were issued.

(1A) This section also applies to an offer (the sale offer) of a body’s securities (the relevant securities) for sale by a person if:

(a) but for subsection (5), disclosure to investors under this Part would be required by subsection 707(5) for the sale offer; and

(b) the securities were not sold by the controller with the purpose referred to in subparagraph 707(5)(c)(i); and

(c) a determination under subsection (2) was not in force in relation to the body at the time when the relevant securities were issued.

Determination by ASIC

(2) ASIC may make a determination under this subsection if ASIC is satisfied that in the previous 12 months the body contravened any of the following provisions:

(a) subsection 283AA(1), 283AB(1) or 283AC(1);

(b) the provisions of Chapter 2M as they apply to the body;

(c) section 674 or 675;

(d) section 724 or 728;

(e) subsection (9) of this section; or

(f) section 1308 as that section applies to a notice under subsection (5) of this section.

(3) The determination must be made in writing and a copy must be published in the Gazette as soon as practicable after the determination is made.

(4) A failure to publish a copy of the determination does not affect the validity of the determination.

Sale offer of quoted securities-case 1

(5) The sale offer does not need disclosure to investors under this Part if:

(a) the relevant securities are in a class of securities that were quoted securities at all times in the 3 months before the day on which the relevant securities were issued; and

(b) trading in that class of securities on a prescribed financial market on which they were quoted was not suspended for more than a total of 5 days during the shorter of the period during which the class of securities were quoted, and the period of 12 months before the day on which the relevant securities were issued; and

(c) no exemption under section 111AS or 111AT covered the body, or any person as director or auditor of the body, at any time during the relevant period referred to in paragraph (b); and

(d) no order under section 340 or 341 covered the body, or any person as director or auditor of the body, at any time during the relevant period referred to in paragraph (b); and

(e) either:

(i) if this section applies because of subsection (1)--the body gives the relevant market operator for the body a notice that complies with subsection (6) before the sale offer is made; or

(ii) if this section applies because of subsection (1A)--both the body, and the controller, give the relevant market operator for the body a notice that complies with subsection (6) before the sale offer is made.

(6) A notice complies with this subsection if the notice:

(a) is given within 5 business days after the day on which the relevant securities were issued by the body; and

(b) states that the body issued the relevant securities without disclosure to investors under this Part; and

(c) states that the notice is being given under paragraph (5)(e); and

(d) states that, as at the date of the notice, the body has complied with:

(i) the provisions of Chapter 2M as they apply to the body; and

(ii) section 674; and

(e) sets out any information that is excluded information as at the date of the notice (see subsections (7) and (8)).

Note 1: A person is taken not to contravene section 727 if a notice purports to comply with this subsection but does not actually comply with this subsection: see subsection 727(5).

Note 2: A notice must not be false or misleading in a material particular, or omit anything that would render it misleading in a material respect: see sections 1308 and 1309. The body has an obligation to correct a defective notice: see subsection (9) of this section.

(7) For the purposes of subsection (6), excluded information is information:

(a) that has been excluded from a continuous disclosure notice in accordance with the listing rules of the relevant market operator to whom that notice is required to be given; and

(b) that investors and their professional advisers would reasonably require for the purpose of making an informed assessment of:

(i) the assets and liabilities, financial position and performance, profits and losses and prospects of the body; or

(ii) the rights and liabilities attaching to the relevant securities.

(8) The notice given under subsection (5) must contain any excluded information only to the extent to which it is reasonable for investors and their professional advisers to expect to find the information in a disclosure document.

Obligation to correct defective notice

(9) The body contravenes this subsection if:

(a) the notice given under subsection (5) is defective; and

(b) the body becomes aware of the defect in the notice within 12 months after the relevant securities are issued; and

(c) the body does not, within a reasonable time after becoming aware of the defect, give the relevant market operator a notice that sets out the information necessary to correct the defect.

(10) For the purposes of subsection (9), the notice under subsection (5) is defective if the notice:

(a) does not comply with paragraph (6)(e); or

(b) is false or misleading in a material particular; or

(c) has omitted from it a matter or thing the omission of which renders the notice misleading in a material respect.

Sale offer of quoted securities-case 2

(11) The sale offer does not need disclosure to investors under this Part if:

(a) the relevant securities are in a class of securities that are quoted securities of the body; and

(b) either:

(i) a prospectus is lodged with ASIC on or after the day on which the relevant securities were issued but before the day on which the sale offer is made; or

(ii) a prospectus is lodged with ASIC before the day on which the relevant securities are issued and offers of securities that have been made under the prospectus are still open for acceptance on the day on which the relevant securities were issued; and

(c) the prospectus is for an offer of securities issued by the body that are in the same class of securities as the relevant securities.

Sale offer of quoted securities-case 3

(12) This subsection is satisfied if:

(a) the body offered to issue securities under a prospectus; and

(b) the body issued the relevant securities to:

(i) a person (the underwriter) named in that prospectus as an underwriter of the issue; or

(ii) a person nominated by the underwriter; and

(c) he relevant securities were issued to the underwriter, or the person nominated by the underwriter, at or about the time that persons who applied for securities under the prospectus were issued with those securities; and

(d) the relevant securities are in a class of securities that were quoted securities of the body.

DISCLOSURE IN OFFER OF SECURITIES

9 In Re Sprint Energy Limited, in the matter of Sprint Energy Limited [2012] FCA 1354 (at [17]-[20]), I discussed the legislative scheme for disclosure in relation to offers of securities and summarised the relevant principles as follows:

Chapter 6D

17 Chapter 6D CA is concerned with fundraising. As … stated in Re Golden Gate Petroleum Ltd (2010) 77 ACSR 17 (at [24]):

Chapter 6 is designed to ensure that investors are provided with all information that they and their professional advisers would reasonably require to make an informed assessment in connection with securities offered for issue or sale. This includes the rights and liabilities attaching to securities (and the underlying securities in the case of interests in or options over securities) and the assets, liabilities, financial position and performance, profits and losses and prospects of the body that is to issue or issued securities (or the underlying securities in the case of interest in or options over securities) that are offered for issue and, in certain cases, for sale to investors.

18 The starting point is that an offer of securities for issue requires disclosure to investors under Pt 6D.2 CA: s 706 CA. The manner of disclosure is provided for in s 709 CA. Section 708 and s 708AA contain a number of exceptions to that general rule: Golden Gate (at [26]). Sprint considered that the circumstances of the Relevant Share Issues fell within exceptions in s 708 CA.

19 Pursuant to s 707(1) CA an offer of securities for sale only requires disclosure to investors under Pt 6D.2 CA if required by any of s 707(2), (3) or (5) CA. Section 707 is an anti-avoidance provision to prevent the avoidance of disclosure requirements including those under s 706 CA. In Golden Gate (at [27]) I described the purposes of s 707 as being to:

... prevent the policy of Chapter 6D being circumvented by the issue of securities or offer of sale of securities to a party to whom disclosure is not required (under s 708 or s 708AA) and that party then offering those securities for sale to investors without disclosure.

20 As noted, s 707(3) CA provides that offers of sale or the sale of securities in a body needs disclosure to investors within 12 months in certain circumstances.

10 A person who sells securities in breach of s 707(3) or s 727(1) of the CA may be liable to having the sale set aside and to pay damages under s 1325(5) of the CA.

11 Section 708A sets out three exceptions to the requirement to give disclosure for offers for the sale of securities that would otherwise contravene s 707(3) CA in circumstances where comparable information to that which would be given in a disclosure document is publicly available before an offer for sale is made. Those exceptions include the circumstances where a notice under s 708A(5) and s 708A(6) is given to Australian Stock Exchange (ASX) within 5 business days of the date of issue of the securities and before any sale offers are made, or a prospectus is lodged with the Australian Securities and Investments Commission (ASIC) under s 708A(11) on or after the date of issue but before any sale offers are made.

12 A valid cleansing notice or cleansing prospectus will have a prospective operation, as is clear from s 708A(5)(e) and s 708A(11)(b) of the CA.

REMEDIAL ORDERS UNDER S 1322 OF THE CA

13 The Court has a broad discretion under s 1322(4) of the CA to make a remedial order. Such an order may be unconditional or subject to such conditions as the Court imposes. The Court is also empowered to make such consequential or ancillary orders as it thinks fit, subject to certain elements being satisfied. An order can be made under s 1322(4)(a) or s 1322(4)(c) notwithstanding that the contravention or failure resulted in the commission of an offence: s 1322(5) of the CA.

14 In Sprint Energy, I summarised the requirements for the making of orders under s 1322(4)(a) of the CA (at [31]). The plaintiff must satisfy the Court that:

(a) it is ‘an interested person’: s 1322(4)(a);

(b) there was an act, matter or thing purporting to have been done under the CA or in relation to a corporation that may be invalid by reason of a contravention of a provision of the CA: s 1322(4)(a);

(c) either:

(i) the act, matter or thing was essentially of a procedural nature: s 1322(6)(a)(i); or

(ii) the person or persons concerned in or party to the contravention acted honestly: s 1322(6)(a)(ii); or

(iii) it is just and equitable that the order be made: s 1322(6)(a)(iii); and

(d) no substantial injustice has been or is likely to be caused to any person: s 1322(6)(c).

15 Section 1322(6)(b) of the CA provides an additional requirement for the making of an order under s 1322(4)(c), namely that the person to be relieved from civil liability acted honestly.

16 Some key principles in relation to applications under s 1322 of the CA are:

(a) section 1322 is remedial in character and should be applied broadly: Sprint Energy (at [33] and the cases therein cited);

(b) limitations to the broadly expressed powers in s 1322 will not be readily implied: see Weinstock v Beck (2013) 251 CLR 396 per French CJ (at [43]), Hayne, Crennan and Kiefel JJ (at [55]-[56]) and Gageler J (at [64]);

(c) the prescriptive requirements of the wording in s 1322(4)(a) and s 1322(4)(c) and the pre-conditions in s 1322(6) need to be satisfied: Weinstock (at [53]); and

(d) the validation of a contravention may operate retrospectively: Sprint Energy (at [36]) and Re Golden Gate Petroleum Ltd (ABN 090 074 785) (2010) 77 ACSR 17 (at [37]).

17 In Sprint Energy (at [37]) it was noted that interested persons should be relieved of unnecessary liability or inconvenience or the consequences of invalid transactions where:

(a) a non-compliance with the CA is the product of honest error or inadvertence;

(b) to so relieve will not prejudice third parties; and

(c) to so relieve will not prejudice the public interest in compliance with the CA.

18 In Re Poseidon Nickel Ltd (2018) 129 ACSR 57, Colvin J observed (at [14]-[15] citing EHR Resources Ltd, in the matter of EHR Resources Ltd [2018] FCA 997) that it is appropriate to identify in any order the particular contravention that is the reason for the order and that care should be taken to confine the relief in a manner which is consistent with the justification for the application.

THE FACTS

19 In this instance, the plaintiff was incorporated in 2007 and until 2017 its main focus was on the development of bauxite deposits.

20 In 2017, the plaintiff began investing in the medical cannabis industry. This commenced with the acquisition of a controlling stake in Medical Cannabis Limited in late May 2017 and resulted in the plaintiff needing to re-comply with Chapters 1 and 2 of the ASX Listing Rules in light of the change in the nature or scale of the plaintiff’s activities.

21 The plaintiff lodged a re-compliance prospectus with ASIC on 27 September 2018. On 17 October 2018 the plaintiff lodged a supplementary prospectus with ASIC. This was followed by a second supplementary prospectus lodged with ASIC on 31 October 2018. A third supplementary prospectus was lodged with ASIC on 7 November 2018.

22 Trading in the plaintiff’s shares has been suspended since 1 August 2018 pending, relevantly, re-compliance with Chapters 1 and 2 of the ASX Listing Rules.

23 Mr Feldman first became aware of problems in relation to secondary trading in the plaintiff’s shares on reading an email from ASX, forwarded by the plaintiff’s solicitors on 5 October 2018.

24 Investigations revealed the extent of secondary trading, as set out in the table annexed to a supporting affidavit deposed to by Mr Feldman.

25 The failure to cleanse the Uncleansed Securities Issues arose from a misunderstanding on the part of Mr Feldman about the circumstances in which a cleansing notice or cleansing prospectus should be issued. He understood the general requirement for, and importance of, disclosure regarding securities issues and the exemptions to this requirement. He also understood the plaintiff’s continuous disclosure obligations. What was not appreciated was that where a securities issue is validly made without disclosure because an exemption applies, the recipients of shares will be treated as if they were the issuing entity; the recipients must themselves make disclosure if they are to avoid contraventions of s 707(3) and s 727(1) of the CA.

26 Mr Feldman’s understanding was that a cleansing notice could be issued to ASX to confirm to the market that there was no excluded information and that the continuous disclosure requirements would be met. He issued such notices only when requested to do so by recipients.

27 The plaintiff argued that Mr Feldman’s error was to some extent understandable. The CA does not stipulate that cleansing notices must be issued to ASX where securities issues are made without disclosure. There will not be any breach of s 707(3) and s 727(1) of the CA if there are no offers or on-sales by recipients within 12 months of the issue date and secondary trading within 12 months of issue will only be a contravention because of the deeming effect of these provisions.

28 Mr Feldman satisfied himself that those securities issues made without disclosure were exempt from disclosure. In some instances, disclosure was made by prospectus. Mr Feldman also satisfied himself that there was no excluded information when the Uncleansed Securities Issues were made.

DECLARATIONS IN RELATION TO THE UNCLEANSED SECURITIES ISSUES

29 The statutory requirements of s 1322(4)(a) are each met in relation to this order.

30 The plaintiff is an interested person who may seek relief as required by s 1322(4): see Golden Gate (at [44]).

31 The relevant ‘act, matter or thing’ is the sale or offering for sale of the securities and the specific contraventions are of s 707(3) and s 727(1) of the CA.

32 The next requirement is as to satisfaction of one of the matters set out ss 1322(6)(a)(i), (ii) and (iii) of the CA.

33 I am satisfied on the evidence, the second and third of these requirements are both met.

Section 1322(6)(a)(ii) – acting honestly

34 In Re iCandy Interactive Ltd (ACN 604 871 712) (2018) 125 ACSR 369 (at [101]), Banks-Smith J found that while it is clear that the honesty of the shareholders as the persons who offered or sold shares without disclosure is relevant under s 1322(6)(a)(ii), in cases where the applicant seeks to rely on s 1322(6)(a)(ii) as a pre-condition to the making of validating orders, the Court is entitled to take into account the role of the company and those involved in the securities issue.

35 Honesty can properly be inferred in circumstances where the explanation for the relevant conduct does not reveal any evidence of dishonesty: Re iCandy (at [54]).

36 It is appropriate to accept the honesty of the plaintiff in light of the evidence of its officer, Mr Feldman. The failure arose through Mr Feldman’s mistaken view about the circumstances in which cleansing notices should be issued.

Section 1322(6)(a)(iii) – just and equitable

37 In Re Chinese Cultural Club Ltd (2004) 183 FLR 33 (at [19]), Campbell J quoted with approval from a decision of Barrett J in Eddy Lau Constructions Pty Ltd v Transdevelopment Enterprise Pty Ltd [2004] NSWSC 273 where his Honour had considered the width of ‘just and equitable’:

The phrase “just and equitable” is commonly used in legislative drafting: see, for example, Corporations Act 2001 (Cth), s 461(1)(k), Family Law Act 1975 (Cth), s 75(2); Motor Accidents Act 1988 (NSW), s 74(3); Property (Relationships) Act 1984 (NSW), s 20(1); Conveyancing Act 1919 (NSW), s 66M. Numerous cases have considered the significance of the phrase. The conclusions drawn are reflected in the words borrowed by Lord Shaw of Dunfermline in Loch v John Blackwood Ltd [1924] AC 783 at 791 from Neville J in Re Bleriot Manufacturing Aircraft Co (1916) 32 TLR 253 at 255:

The words “just and equitable” are words of the widest significance and do not limit the jurisdiction of the Court to any case. It is a question of fact, and each case must depend on its own circumstances.

A court directed by statute to proceed according to what is “just and equitable” is given a wide discretion. There is, as Owen J observed in Thomas v MacKay Investments Pty Ltd (1996) 22 ACSR 294 at p.302, “no necessary limit on the generality of the words”. They are “to be applied in their ordinary meaning as calling for the exercise of judgment in the conventional way.”

38 The making of the order would be consistent with the public policy of Chapter 6D of the CA, which is to ensure disclosure to shareholders.

39 It is relevant that recipients of the Uncleansed Securities most likely proceeded on the basis that their shares were tradable without having to make disclosure under s 707(3) of the CA: see Sprint Energy (at [47]), TV2U International Limited, in the matter of TV2U International Limited [2016] FCA 1556 and Golden Gate Petroleum (at [51]).

40 The granting of relief will permit the plaintiff to have the suspension in trading of its shares removed by the ASX (subject to re-compliance) and this will allow shareholders the ability to freely trade their shares. No prejudice will flow to shareholders if relief is granted.

Section 1322(6)(c) of the CA – whether any substantial injustice has been or is likely to be caused to any person

41 The final requirement for the making of an order under s 1322(4)(a) that was identified in Sprint Energy is that no substantial injustice has been or is likely to be caused.

42 In Elderslie Finance Corporation Ltd v Australian Securities Commission (1993) 11 ACSR 157, Owen J said (at 160):

The word “injustice” requires the court to consider real, and not merely in substantial or theoretical prejudice. A degree of prejudice to a person or persons may be outweighed if the overwhelming weight of justice is in favour of making the order[.]

(Citations omitted.)

43 In Super John Pty Ltd v Futuris Rural Pty Ltd (1999) 32 ACSR 398, Santow J said (at [14]):

[D]etriment per se is not the same as substantial injustice; that must depend upon whether the remedial order in giving rise to that detriment is unjust in the sense of causing such prejudice overall as to be unfair or inequitable, taking into account the interests of all of those directly affected by such dispensation.

44 It is very unlikely that on-sellers suffered any substantial injustice and there is no evidence that any person has, or will be likely to, suffer any injustice if the orders are made. It follows from this that there would not be any injustice to sellers if the orders were made because their trades, made in good faith, would be validated.

45 If the orders are not made then there may be substantial injustice to sellers of such securities given that any sales may be void or voidable. Also the general body of shareholders would be prejudiced by reason of the continuing suspension from official quotation.

RELIEF FROM CIVIL LIABILITY PURSUANT TO S 1322(4)(c) OF THE CA

46 An order under s 1322(4)(c) will relieve sellers from any liability under s 707(3) and s 727(1) of the CA for offers and sales of securities affected by the contraventions. These orders are similar to those made in Sprint Energy, Golden Gate, TV2U International and Poseidon Nickel.

47 There is no evidence that any of the sellers acted dishonestly in any way and the Court can readily infer that the sellers were likely to be acting honestly and would not have on-sold shares if they had known that disclosure was required.

48 Consistent with this approach, Siopis J in Re Silver Lake Resources Ltd (ACN 108 779 782) (2012) 87 ACSR 436 (at [19]) said that ‘the making of the orders will serve to give legal effect to the expectations no doubt held by the persons concerned’.

49 As to the requirement in s 1322(6)(c) of the CA, it is unlikely that the proposed orders will cause any substantial injustice to sellers. The shareholders would have protection under paragraphs 2 and 8 of the orders.

THE GENERAL DISCRETION UNDER S 1322(4) OF THE CA

50 The plaintiff acted promptly to rectify the secondary trading problems. This is a relevant consideration: Azure Minerals Limited, in the matter of Azure Minerals Limited [2013] FCA 63 per Barker J (at [12]).

51 There is no evidence of any substantial misconduct, serious wrongdoing or flagrant disregard of the corporate law or the company’s constitution so as to warrant refusal of the relief sought on discretionary grounds: see Re Wave Capital Ltd (ACN 006 031 161) (2003) 47 ACSR 418 per French J (at [29]).

52 Importantly, the plaintiff has not sought relief from civil liability for itself or its officers under s 1322(4)(c) of the CA, so that there is no bar to proceedings being brought against the plaintiff for damages, imposition of a civil penalty or prosecution for breaches of the CA.

53 Sellers who consider that they have suffered detriment as a result of the making of the orders are protected by the para 2 and para 8 of the orders.

54 The public policy of the CA would not be undermined if the sale transactions were validated: Sprint Energy (at [56]).

55 There are no discretionary reasons for refusing relief.

COSTS

56 Costs orders have not generally been made in similar applications. An exception to this general approach arose in Wave Capital Ltd, where French J considered that it was appropriate that those behind the restructuring should bear the costs of the proceedings due to their responsibility for the error.

57 In Poseidon Nickel, Colvin J declined to make costs orders. His Honour noted that the applicant company was in a position to consider the appropriate course in relation to costs. I consider, with respect, that approach is appropriate.

I certify that the preceding fifty-seven (57) numbered paragraph are a true copy of the Reasons for Judgment herein of the Honourable Justice McKerracher. |

Associate: