FEDERAL COURT OF AUSTRALIA

Ample Source International Limited v Bonython Metals Group Pty Limited (in liquidation), in the matter of Bonython Metals Group Pty Limited (in liquidation) (No 8) [2018] FCA 1614

ORDERS

DAVID JOHN LEIGH AND MICHAEL ANDREW OWEN IN THEIR CAPACITIES AS LIQUIDATORS OF BONYTHON METALS GROUP PTY LIMITED (ACN 141 257 294) (IN LIQUIDATION) Applicant | |

AND: | JOHN HILLAM First Respondent SARABOL TEERANUKUL Second Respondent BRIAN RAYMENT (and others named in the Schedule) Third Respondent |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Michael Andrew Owen (“liquidator”) as liquidator of the first defendant (“BMG”) is justified in proceeding with the liquidation on the basis that Pure Metals Pty Ltd (“Pure Metals”) indemnified Michael Andrew Owen and David Leigh as liquidators of BMG for their legal expenses incurred in the defence of Federal Court of Australia proceeding NSD363/2013 (“Hawsons proceeding”) pursuant to cl 9(a) of the deed of assignment between Pure Metals, BMG, the liquidators and Silvergate Capital Pty Ltd dated 24 May 2013.

2. The liquidator is justified in paying Pure Metals the amount of $15,806.57 from the assets of BMG, being the amount still owing to Pure Metals in connection with the indemnity referred to in order 1.

3. The liquidator is justified in proceeding on the basis that the rule in Cherry v Boultbee [1839] Eng R 1099; (1839) 41 ER 171 may be applied to the calculation of the amounts for distribution to the contributories in accordance with the reasons for judgment published on the date of these orders.

4. Within 14 days of the date of these orders, the liquidator file and serve short minutes of orders for the further conduct of this proceeding.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GLEESON J:

1 This is an application for judicial advice, originally made by David Leigh and Michael Owen as joint and several liquidators of the first defendant (“BMG”). Relief is sought by a further amended interlocutory process (“FAIP”) filed 30 January 2018 under ss 90-15(1), 90-15(3)(a) and 90-20(d) of the Insolvency Practice Schedule (Corporations) (“Insolvency Practice Schedule”), which is Schedule 2 to the Corporations Act 2001 (Cth) (“Act”) (given force by s 600K of the Act). On 26 February 2018, Mr Leigh resigned as liquidator of BMG. Mr Owen continues to be appointed as BMG’s sole liquidator and seeks judicial advice in that capacity.

2 The judicial advice application raises the following three principal issues:

(1) Whether BMG owes any amount to Pure Metals Pty Ltd (“Pure Metals”), which funded the defence of the liquidators and BMG to a proceeding (NSD363/2013) referred to as the “Hawsons proceeding”?

(2) Whether the liquidator should apply the rule in Cherry v Boultbee [1839] Eng R 1099; (1839) 41 ER 171, by taking into account monies owed by the first respondent to the application (“Mr Hillam”) and the second respondent to the application (“Ms Teeranukul”) to BMG in calculating the amounts to be distributed to contributories from surplus funds?

(3) Whether special orders should be made in connection with a costs order made against Mr Hillam and Ms Teeranukul on 18 December 2017?

3 Apart from Mr Hillam and Ms Teeranukul, who together own 67.4% of the total issued shares in BMG, the respondents to the FAIP are:

(1) Ample Source International Limited (“Ample Source”), James Richard Vereker, Giralia Resources Pty Ltd (formerly Giralia Resources NL) (“Giralia”) and Red Gold Australia Pty Ltd (“Red Gold”), who are the contributories of BMG; and

(2) Brian Rayment QC, Matthew Gollan, and Pure Metals, who are creditors of BMG.

4 Red Gold filed a submitting notice on 14 August 2017. Matthew Gollan filed a submitting notice on 14 December 2017. By letter dated 10 July 2018, Mr Rayment QC confirmed that he submits to the order of the Court and proposes only to seek to enforce a charge over money paid to Mr Hillam and Ms Teeranukul in due course.

5 Mr Hillam appeared at the hearing and opposed the application. Ms Teeranukul did not appear in person although Mr Hillam purported to represent Ms Teeranukul, as well as Wentworth Metals Group Pty Ltd (“Wentworth”).

6 In August 2017, lawyers acting for Ample Source and Pure Metals, McCullough Robertson, informed the then liquidators’ lawyers, HWL Ebsworth, that Pure Metals did not intend to take an active role in the proceeding. In November 2017, Pure Metals’ lawyers consented to the filing of the then proposed amended interlocutory process. On 29 January 2018, HWL Ebsworth copied McCullough Robertson into an email to the Court which attached, among other things, a copy of the then proposed FAIP. By letter dated 3 July 2018, HWL Ebsworth sought confirmation of the various respondents’ position in relation to the FAIP. By 19 July 2018, HWL Ebsworth had not received a response from McCullough Robertson. Mr Whatley, the liquidator’s solicitor, swore an affidavit dated 19 July 2018, deposing to these matters.

7 The positions of Mr Vereker and Giralia in relation to the FAIP is not known.

Evidence

8 The liquidator’s evidence comprised the following:

(1) An affidavit of David John Leigh sworn 19 July 2017, and the accompanying exhibit, marked exhibit “DJL-1”.

(2) An affidavit of David John Leigh sworn 25 January 2018.

(3) An affidavit of Stephen Richard Lord 25 January 2018.

(4) An affidavit of Matthew Youssef sworn 14 August 2017.

(5) An affidavit of Matthew Youssef sworn 27 November 2017.

(6) An affidavit of Holly Ho-Yi Lam sworn 15 December 2017.

(7) An affidavit of Grant Bradley Whatley sworn 19 July 2018.

9 At the hearing, Mr Hillam objected to Mr Leigh’s affidavits on the basis that they contained inaccurate information. He submitted that generally he had not had an opportunity to go through the liquidator’s evidence and raise objections. I rejected that submission, having concluded that Mr Hillam had been given reasonable time to prepare for the hearing.

10 Mr Hillam did not adduce evidence in answer to the liquidator’s application but made oral submissions, which may be summarised as follows:

(1) The “Hawsons asset” (being BMG’s interest in the Hawsons Iron Project, described below) was sold by the liquidators at a gross undervalue. If a damages claim was made against the liquidator for sale of the asset at an undervalue, the liquidators would have access to the Pure Metals’ indemnity to recover those damages. The current application for judicial advice concerning the indemnity is a “Trojan horse”, which seeks to remove any further liability that the liquidator may have in connection with the indemnity. If the Court makes a ruling on the liquidator’s submission about the indemnity, the indemnity will disappear.

(2) Substantial assets that Mr Hillam accumulated in BMG were lost.

(3) The Court should determine that Wentworth Metals Group Pty Ltd (“Wentworth”) is still a creditor of BMG and consequently has the right to call a meeting of BMG.

(4) Mr Hillam requests that the Court call a shareholders meeting, or directs the liquidator to convene such a meeting. The purpose of the meeting would be to put a proposal which would have the effect of removing BMG from liquidation.

(5) There is no basis for the date chosen by the liquidator for offsetting amounts.

11 As will appear below, Mr Hillam has previously sought to litigate his complaint concerning the sale of the Hawsons asset but has not pursued that claim since an interlocutory application to restrain the sale was dismissed in April 2013. In those circumstances, the suggestion that the Court should not determine the liquidator’s application concerning the scope of the Pure Metals’ indemnity, because it may in some way affect a possible claim in relation to the sale, is fanciful. Wentworth is not a party to the proceeding and it is not appropriate to consider whether it is entitled to call a meeting of BMG in its absence. It is also not appropriate to consider Mr Hillam’s request to call a shareholders’ meeting where BMG has been ordered to be wound up as a result of oppression by Mr Hillam and in the absence of any serious reason to believe that there is a proposal that might have the effect of ending BMG’s liquidation.

Background

12 On 27 February 2012, a judge of this Court made an order that BMG be wound up pursuant to s 233 of the Act (that is, following a finding that the conduct of the company’s affairs was oppressive to a member, namely, Ample Source) and consequential orders including for the appointment of the liquidators as joint and several liquidators of BMG, for reasons explained in Ample Source International Ltd v Bonython Metals Group Pty Ltd (No 6) [2011] FCA 1484; (2011) 285 ALR 488.

13 An appeal from that judgment was dismissed on 3 May 2012: Hillam v Ample Source International Ltd (No 2) [2012] FCAFC 73; (2012) 202 FCR 336 (“Full Court judgment”).

14 BMG was, and still is, a solvent company. The liquidation process is now coming to an end.

15 Mr Leigh gave evidence that, as at 21 December 2017, a total of $881,479.84 (“surplus funds”) were available to members of BMG calculated as follows:

Cash held by BMG $1,009,642.71

LESS unpaid fees and disbursements $32,356.30

LESS estimated future fees $30,000.00

LESS estimated future disbursements $50,000.00

LESS amount payable for Pure Metals $15,806.57

TOTAL SURPLUS FUNDS $881,479.84

Contributories

16 A list of contributories has been drawn up pursuant to s 478 of the Act. The list comprises the following fully paid shareholders who hold the following numbers of shares:

(1) Mr Hillam 32,000 shares

(2) Ms Teeranukul 32,000 shares

(3) Ample Source 25,010 shares

(4) Giralia 2,940 shares

(5) Red Gold 3,060 shares

17 In addition, Mr Vereker holds 5,000 unpaid shares. He has previously refused demands for payment.

18 On 22 December 2011, BMG (and Mr Hillam and Ms Teeranukul) were ordered to do all things necessary to cause BMG to issue a further 10 fully paid ordinary shares in BMG to Ample Source. To give effect to this order, the liquidator intends to issue 10 additional shares to Ample Source prior to distribution of the surplus.

19 After the additional shares are issued to Ample Source and provided that Mr Vereker does not pay a call on his unpaid shares, the share register will comprise 95,010 fully paid shares held in the following proportions:

(1) Mr Hillam 33.7%

(2) Ms Teeranukul 33.7%

(3) Ample Source 26.3%

(4) Red Gold 3.2%

(5) Giralia 3.1%

20 Upon the resolution of the issues the subject of the FAIP, the liquidator is poised to make the final distribution of the surplus funds to BMG’s contributories.

21 Mr Leigh calculated that, based on the proportions in [18] above and the surplus funds of $881,479.84 referred to at [14] above, the surplus would be distributed as follows:

Contributory | Amount |

Mr Hillam | 33.7% x $881,479.84 = $297,058.71 |

Ms Teeranukul | 33.7% x $881,479.84 = $297,058.71 |

Ample Source | 26.3% x $881,479.84 = $231,829.20 |

Red Gold | 3.2% x $881,479.84 = $28,207.35 |

Giralia | 3.1% x $881,479.84 = $27,325.88 |

22 Mr Vereker does not appear on the table as his shares are unpaid and as he has previously refused demands for payment.

23 As explained below, the liquidator is proposing to distribute the surplus in a different manner, by the application of the rule in Cherry v Boultbee.

Circumstances leading to BMG’s liquidation

24 The Full Court judgment sets out the following background facts concerning BMG at [11] and [12]:

[11] BMG was incorporated on 23 December 2009. The majority shareholders were … Mr John Hillam and his domestic partner Ms Sarobol Teeranukul…. At the time of the trial Mr Hillam and Ms Teeranukul held 64 per cent of the shares of BMG (32 per cent each). Mr Hillam was the driving force behind BMG. He was at all times a director and the CEO of BMG. Mr Hillam had interests in other companies. One such company was Wentworth Metal Group Pty Limited (“Wentworth”). Mr Hillam and Ms Teeranukul were the only two shareholders of Wentworth. The directors of Wentworth at the relevant time were Mr Hillam and Mr Dennis Brennan. Another company in which Mr Hillam had an interest was CFM Media Holdings Pty Ltd, (“CFM Media”). CFM Media was registered on 4 May 2010. Its only two shareholders were Mr Hillam and Ms Teeranukul. Its sole director was Mr Hillam. Before the registration of CFM Media, Mr Hillam on occasion used the business name “CFM Media Holdings” when doing business in his own right.

[12] Mr Hillam is a geologist. A principal business activity of BMG was to raise capital to undertake exploration and development of mineral resources, usually in joint venture arrangements with companies which held permits to explore and exploit mineral resources.

Hawsons Iron Project

25 The Hawsons Iron Project involved the exploration for mineral deposits of an area in the vicinity of Broken Hill, New South Wales, on mining tenements owned by Carpentaria Exploration Limited (“Carpentaria”).

26 The Full Court judgment sets out the following relevant background facts (at [19] to [22]):

[19] In early 2010 Mr Hillam, on behalf of BMG, was also in negotiations with Carpentaria Exploration Limited (“CAP”) concerning arrangements to explore and develop mineral resources on mining tenements held by CAP. In addition, BMG had arrangements with respect to other tenements.

[20] On 3 April 2010 Mr Hillam met with Ms Linda Lau, a representative of Ample Source. The sole shareholder in Ample Source was Mr Wilson Cheung. Mr Cheung lives in Hong Kong. Ms Lau resides in the People’s Republic of China. The trial judge found that Ms Lau recommended to Mr Cheung that Ample Source take a 25 per cent equity stake in BMG owing principally to the possibility of acquiring an interest in the “Hawsons Knob” venture being pursued by CAP, and on the basis that an opportunity would exist to increase Ample Source’s holding in BMG upon contribution of further funds. The initial contribution was to be $16.5m. The arrangements were negotiated urgently owing to short time frames in which BMG might conclude a binding arrangement with CAP. On 23 February 2010 BMG had been granted “exclusivity” with respect to the possibility of an investment in the Hawsons Knob project. On 8 April 2010 the exclusivity period was extended until close of business on 13 April 2010. The trial judge recorded (at [18]):

Between 3 April and 9 April 2010 Mr Hillam and Ms Lau negotiated proposed terms of the investment by Ample Source in Bonython Metals as the funds for Bonython Metals to commit to the Hawsons Knob project were required immediately. During that period Mr Cheung decided to invest $16.5 million in Bonython Metals on behalf of Ample Source.

[21] On 12 April 2010 a “Terms Sheet” was executed. The parties were BMG, Mr Hillam and Ms Teeranukul on one side and Ample Source on the other side…

[22] [After execution of a share allotment and shareholders agreement on 20 April 2010] [a]lmost immediately conflict arose between the representatives of Ample Source and Mr Hillam. There were various sources of conflict. … the parties came to regard each other with considerable suspicion.

27 On 15 April 2010, BMG and Carpentaria entered into a joint venture agreement in relation to the project (“BMG/Carpentaria JVA”). The agreement was varied by a variation deed dated 12 July 2011 (“2011 variation”).

28 The Hawsons asset was an asset of BMG at the commencement of the liquidation.

Liquidators sale of the Hawsons asset

29 After the dismissal of the appeal in May 2012, the liquidators sought to realise the Hawsons asset for the benefit of creditors and members of BMG.

30 On 8 February 2013, BMG, the liquidators, Pure Metals and Silvergate Pty Ltd (“Silvergate”) entered into an agreement in respect of the sale of the Hawsons asset. The agreement was recorded in a letter entitled “Letter of Offer”, accompanied by a draft document entitled “Draft Deed of Assignment and Assumption Exploration Joint Venture and Farm-In Agreement (Hawsons Iron Project)” (“draft deed”).

31 On 24 May 2013, the parties to the 8 February 2013 agreement entered into an agreement entitled “Deed of Assignment – Exploration Joint Venture and Farm In Agreement (Hawsons Iron Project)”.

32 Clause 9 of the deed of assignment provides:

9. As consideration for [BMG] and the Liquidators entering into this deed, on and from 8 February 2013 [Pure Metals] irrevocably and unconditionally agrees to:

(a) Indemnify [BMG], the Liquidators and each of their Representatives (the indemnified parties) and to keep them indemnified on demand against all Claims and Liabilities suffered or incurred by any of the indemnified parties arising out of or in connection with:

(i) this deed, including the assignment contemplated under clause 3 of this deed … but this clause 9(a)(i) does not apply to any Claims or Liabilities arising out of or in connection with any breach of duty by the Liquidators or breach of this deed by the Assignor or the Liquidators;

…

irrespective of whether the Claim or Liability relates to a period or events, acts or omissions occurring before or after Completion and irrespective of any waiver of Conditions under clause 2.2.

33 By cl 1.1 of the deed, “Claim” is defined to mean:

Any claim, notice, demand, action, proceeding, litigation, investigation or judgment, however arising, whether present, unascertained, immediate, future or contingent, whether based on contract, tort (including negligence), statute or otherwise and whether involving a third party or a party to this deed.

And “Liabilities” is defined to include:

[A]ll liabilities (whether actual, contingent or prospective), losses, damages, costs (including legal costs on a solicitor-client basis) and expenses of whatever description.

34 Clause 3 of the deed provides:

3. [BMG] agrees to assign the Assigned Interest to [Pure Metals] and [Pure Metals] agreed to accept that assignment:

(a) for the Purchase Price;

(b) with effect on and from Completion; and

(c) subject to the terms of this deed.

35 The “Assigned Interest” is defined to mean:

[A]ll of the Assignor’s rights and interests under the JVA, including the Assignor’s Stage IC Percentage Share.

36 The “JVA” is defined to mean the BMG/Carpentaria JVA as amended by the 2011 variation.

37 The “Purchase Price” is defined to mean the cash and other consideration set out in cl 4.1 of the deed of assignment. Clause 4.1 provides:

(1) The Purchase Price shall be comprised of the following consideration:

(a) $3,250,000; plus

(b) the benefit of the indemnities given by [Pure Metals] in clauses 9(a)(i), 9(a)(ii) and 9(a)(iii), and the benefit of the releases given by [Pure Metals] in clause 9(b).

Hawsons proceeding

38 On 4 March 2013, Wentworth, Mr Hillam and Ms Teeranukul (“Wentworth parties”) commenced Federal Court proceeding NSD363/2013 against BMG, the liquidators and Pure Metals. The originating application sought a declaration that the liquidators were in breach of their duties under s 420A of the Act or otherwise in making an offer to sell to Carpentaria the Hawsons asset for the consideration of a cash component of $3,250,000 together with a non-cash component.

39 By letter dated 5 March 2013, MinterEllison, on behalf of BMG and the liquidators, wrote to Pure Metals as follows:

We consider that the proceeding brought by [the Wentworth parties] is a “Claim” against which Pure Metals…has agreed to indemnify the Liquidators and … BMG … pursuant to clause 9(a) of the Deed of Assignment, which forms part of the agreement dated 8 February 2013 between Pure Metals …, BMG and the Liquidators.

We give notice that BMG and the Liquidators call upon that indemnity for the purposes of the Claim.

40 The draft deed, referred to at [30] above, does not contain a cl 9(a), although the deed executed on 24 May 2013 does contain such a provision. However, the existence of a deed containing a cl 9(a) around this time is further supported by a letter dated 13 March 2013 from MinterEllison to McCullough Robertson, whom MinterEllison understood to be acting for Pure Metals, again referring to “the operation of the indemnity provided by Pure Metals … and, in particular, whether the claims made in the Proceeding are within the exclusionary provisions of cl 9(a)(i)”. On this basis, I accept that Pure Metals had agreed to give an indemnity in the terms set out at [32] above by about March 2013.

41 By email dated 14 March 2013, Pure Metals declined to pay any amount to MinterEllison’s clients or otherwise to confirm the application of the indemnity, at that stage. By another email that day, Pure Metals’ director Edward McCormack wrote to MinterEllison:

David Leigh and I have just spoken.

We have agreed, in substance, that Pure Metals will loan money to PPB in order to fund the litigation against Hillam’s claim.

Funding is separate from any indemnity that may or may not be associated with Hillam’s claim.

The funding will be a loan secured against funds the liquidator knows it will receive from the soonest of the settlement of the Hawsons Iron transaction, or another transaction that David Leigh just mentioned on the phone to me.

42 By an amended originating process filed on 28 March 2013, the Wentworth parties sought an interlocutory injunction restraining the liquidators and BMG, until further order, from relevantly proceeding with or carrying into effect the “Pure Metals Offer”, described as an offer from Pure Metals to acquire the Hawsons asset on terms contained in a letter of offer dated 8 February 2013 as varied by letter dated 15 February 2013.

43 On 9 April 2013, Pure Metals, BMG and the liquidators entered into a deed of funding (“funding deed”). The deed contains the following background:

A. The parties have entered into the Assignment Agreement.

B. A claim has been made by the Hillam Parties, including in the Wentworth Proceeding, against BMG and the Liquidators.

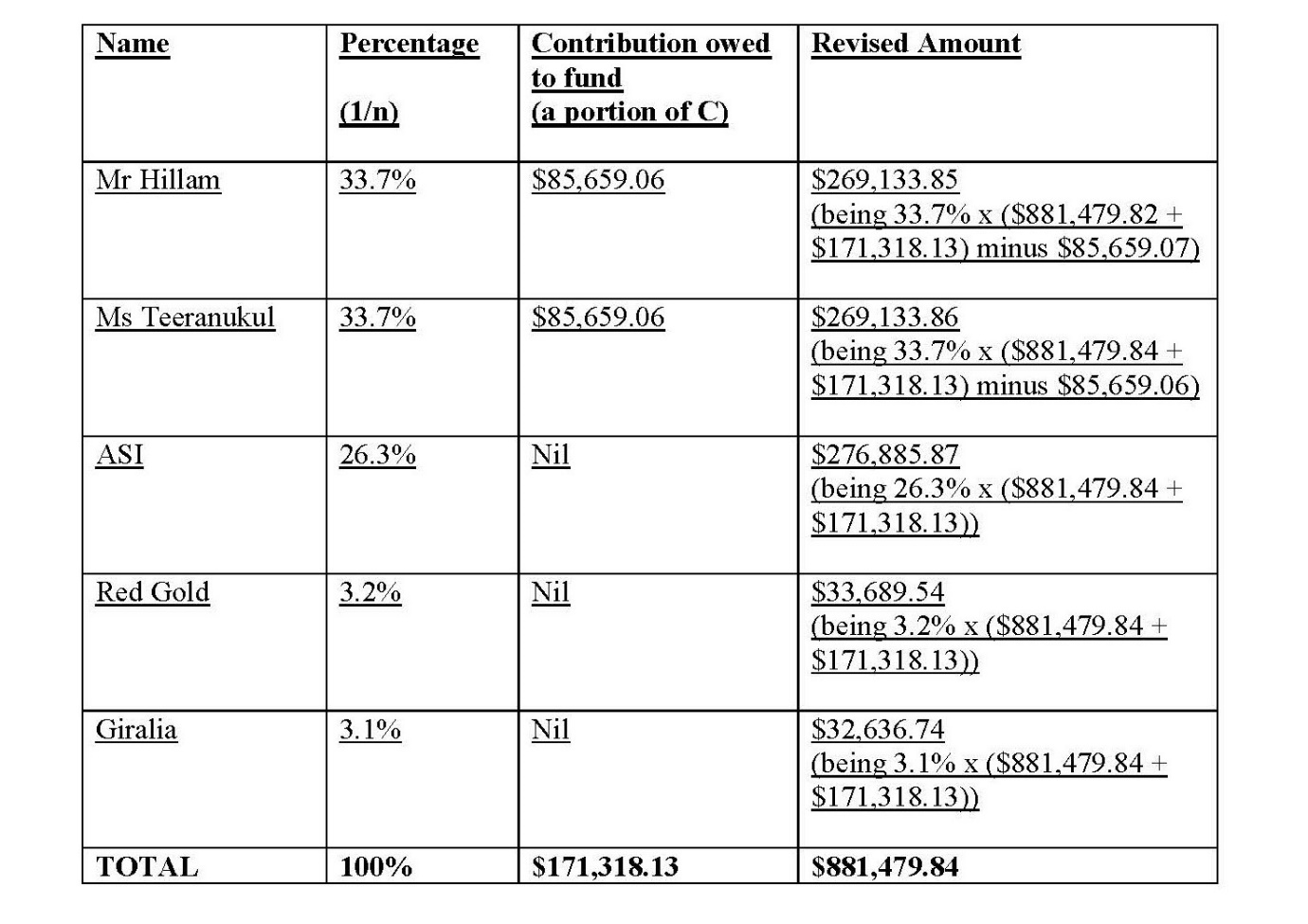

C. BMG and the Liquidators assert that they are entitled to be indemnified by Pure Metals against the claim pursuant to the terms of the Assignment Agreement.

D. Pure Metals does not accept liability to provide indemnity for the claim.

E. In any event, BMG and the Liquidators have sought funding from Pure Metals for the costs of the conduct of the Wentworth Proceeding.

F. Pure Metals has agreed to provide funding on the terms set out in this deed.

44 Under the funding deed:

(1) The “Funding Amount” was defined to mean $150,000 plus any sum advanced pursuant to cl 5(c).

(2) By cll 2(a) and (b), Pure Metals agreed to pay tax invoices to a total amount of $150,000 issued to the liquidators by their lawyers, MinterEllison, in respect of the legal costs of the Hawsons proceeding.

(3) By cl 5(c), the parties agreed that the funding amount of $150,000 could be increased to cover the costs of court approval of the funding agreement.

(4) By cl 2(c), the liquidators agreed, subject to cl 2(d), to “forthwith pay to Pure Metals, by way of reimbursement, the Funding Amount”.

45 Clause 2(d) of the funding deed provides:

The Liquidators will have no obligations under clause 2(c) except to the extent that there are funds available to the Liquidators or BMG as a result of the realisation of:

(i) the Hawsons JV Interest…; or

(ii) any other assets of BMG (which may include legal claims BMG may have against third parties) but only to the extent of any funds available after payment of any remuneration, costs and expenses of the liquidators.

46 Clause 3, entitled “Indemnity”, provides:

(a) In entering into this deed, and performing the obligations under this deed:

(i) no admission is made by any party; and

(ii) it is agreed that there is no prejudice to the rights and obligations of the parties,

in relation to the Assignment Agreement, including in relation to the Indemnity Provisions.

(b) Notwithstanding clause 3(a), the Funding Amount less any payment made to Pure Metals pursuant to clause 2, shall be deducted from the amount of any Liabilities of Pure Metals pursuant to the Indemnity Provisions.

47 The defined terms in the funding deed include:

(1) “Assignment Agreement”, which is defined to mean “the agreement entered into on or about 8 February 2013 between BMG, the liquidators, Pure Metals and Silvergate in respect of the sale of the Hawsons JV Interest as varied by the agreement entered into on or about 15 February 2013”;

(2) “Indemnity Provisions”, which is defined to mean “the provisions of the Assignment Agreement pursuant to which Pure Metals indemnifies BMG and the Liquidators”; and

(3) “Liabilities”, which is defined to “include all liabilities (whether actual, contingent or prospective), losses, damages, costs (including costs on a solicitor-client basis) and expenses of whatever description”.

48 On 18 April 2013, Griffiths J dismissed the application for interlocutory relief with costs: Wentworth Metals Group Pty Ltd v Leigh and Owen (as liquidators of Bonython Metals Group Pty Ltd), Re Bonython Metals Group Pty Ltd (in liq) [2013] FCA 349; (2013) 93 ACSR 626. The Australian Corporations & Securities Reports headnote to the judgment relevantly summarises the facts as follows:

On 3 September 2012, the liquidators commenced the process of selling BMG’s interest in [the Hawsons Iron Project]. As part of this process, offers were received from four parties … [Wentworth] offered approximately $13 million (with between $6 million and $7 million offered as a cash component). The liquidators did not accept this offer and did not inform [Wentworth] of its decision. On 8 February 2013, Pure Metals … lodged a final offer for $3.25 million, which was accepted by the liquidators. [Wentworth] became aware of this decision as a result of announcements to the Australian Stock Exchange.

On 3 April 2013, a creditors meeting of BMG was held and a resolution passed under s 477(2B) of the … Act … approving BMG’s entry into an agreement with Pure Metals for the sale of its interest in [the Hawsons Iron Project].

49 At [11] of his Honour’s reasons, Griffiths J recorded that the Wentworth parties’ fundamental criticism of the liquidators’ decision to accept Pure Metals’ offer was “that it was made in circumstances where the liquidators could not have reasonably been satisfied that the offer from Pure Metals represented the best price reasonably obtainable for the asset being sold”.

50 At [15], his Honour recorded that Mr Leigh had sworn an affidavit in which he set out his reasons for rejecting Wentworth’s offer and accepting the offer made by Pure Metals. At [17], Griffiths J recorded that the Wentworth parties challenged the correctness of many aspects of Mr Leigh’s reasoning but, at [34], found that the Wentworth parties had failed to establish a serious issue to be tried. In particular, his Honour concluded that, where the liquidators were using their commercial judgment and business acumen in exercising their broad powers relating to the sale, the Wentworth parties had not established a prima facie case that the liquidators’ conduct was unreasonable. His Honour said (at [36]):

… When proper allowance is made for the business judgment rule, I am not satisfied that the plaintiffs have established that it was unreasonable of the liquidators to prefer the Pure Metals offer over that of [Wentworth]. On the contrary, it was plainly open to the liquidators to hold that preference in circumstances where the Pure Metals offer provided a higher and certain amount of cash immediately and was made in circumstances where Pure Metals accepted [Carpentaria’s] version of the assumption deed and also provided indemnities. Further, the Pure Metals bid was based on credible offers of security and did not rely on share issues of uncertain value.

51 On 19 March 2014, a Registrar of the Court issued a certificate of taxation in the Hawsons proceeding pursuant to r 40.20 of the Federal Court Rules 2011 that the costs of BMG and the liquidators were deemed to be $167,144.00 (“Hawsons proceeding taxed costs”).

Costs of Hawsons proceeding

52 MinterEllison issued two tax invoices for fees and expenses (mainly counsels’ fees) incurred by the liquidators in the Hawsons proceeding, namely invoice 1451889 dated 28 March 2013 for $129,056.21 and invoice 1460866 dated 30 April 2013 for $108,353.60.

53 The invoices are addressed to PPB Advisory, Attention: David Leigh. The total of the invoices is $237,409.81. Pure Metals paid the amount of the first invoice into the BMG liquidation bank account on 18 April 2013 and the amount of the second invoice into the BMG liquidation bank account on 27 May 2013. The liquidators used the monies received from Pure Metals to pay MinterEllison’s invoices from the BMG liquidation bank account.

54 The total amount paid by Pure Metals exceeded the “Funding Amount” by $87,409.81. Under cl 2(c) of the funding deed, the liquidators were immediately liable to reimburse Pure Metals the amount of $150,000.

55 By letter dated 18 June 2013, MinterEllison wrote to McCullough Robertson as follows:

Funds are now available to the Liquidators as a result of a realisation of the Hawsons JV Interest (as that term is defined in the Deed of Funding). Accordingly, the Liquidators are in a position to repay to Pure Metals Pty Ltd the amount of $150,000 pursuant to clause 2(c) of the Deed of Funding.

We consider it is now beyond doubt that the indemnity in the Deed of Assignment responds to the Liquidators and BMG’s costs of the proceeding. Accordingly, simultaneously with repayment, the Liquidators and BMG seek payment from Pure Metals Pty Ltd in the amount of $150,000 pursuant to the indemnity.

It seems that the sensible way forward in this respect is that your client agree that the Liquidators and BMG may apply the amount of $150,000 due to be repaid to Pure Metals Pty Ltd to the same amount due to our clients pursuant to the indemnity. Please tell us if your client agrees.

In any event, we confirm that to the extent that any amount for costs [is] recovered from the plaintiffs which relate to costs your clients have met pursuant to the indemnity, our clients will repay those amounts to Pure Metals Pty Ltd.

56 MinterEllison sent a similar letter to McCullough Robertson dated 21 August 2013, but did not receive a response.

57 By New South Wales Supreme Court proceeding No. 2013/127662, the Wentworth parties sought a review of a decision of the liquidators to admit a certain proof of debt for voting purposes at a meeting of creditors on 3 April 2013.

58 The proceeding was settled and, on 23 October 2014, the parties signed a consent order which provides for the Wentworth parties to pay the liquidators’ costs of the proceeding in the amount of $75,000 (“$75,000 costs liability”).

59 At the hearing, I understood Mr Hillam to say that he did not dispute the $75,000 costs liability.

2014 proceedings in this Court

60 On 24 September 2014, the liquidators filed an interlocutory process in the present proceeding seeking judicial advice concerning proofs of debt submitted by Wentworth and CFM Media Holdings Pty Ltd (“CFM”).

61 On 3 October 2014, CFM commenced Federal Court proceeding NSD1007/2014 (“CFM proceeding”) in respect of the liquidators’ 19 September 2014 decision to reject the CFM proof of debt.

62 On 11 February 2015, the liquidators filed an amended interlocutory process in the present proceeding.

Wentworth proof of debt

63 Wentworth lodged a proof of debt in BMG’s liquidation, dated 20 November 2014, in the sum of $1,853,906.78.

February 2015 costs orders

64 By orders made by consent in the present proceeding on 25 February 2015:

(1) The Wentworth parties and CFM were ordered to pay the liquidators’ costs of the February 2015 amended interlocutory process in this proceeding.

(2) The originating process in the CFM proceeding was dismissed and CFM was ordered to pay the liquidators’ costs.

65 On 27 March 2015, parties including, relevantly, Wentworth, agreed during a telephone conference that the total amount to be paid in respect of the two February 2015 costs orders was $90,000 plus interest (“$90,000 plus interest costs liability”).

66 The 25 February 2015 order contains a notation that Wentworth undertook to limit its proof of debt to an amount of $190,000.00, defined as “POD Amount”, and the following notation:

The parties agree that the POD Amount shall be set-off against monies owing pursuant to costs orders in the following proceedings:

(a) Federal Court of Australia NSD363 of 2013 (Certificate of Taxation issued 19 March 2014); and

(b) Supreme Court of New South Wales (2013/127662), order taken out 27 October 2014.

67 The “parties” included BMG, the liquidators, Wentworth and others.

68 The 19 March 2014 certificate of taxation is referred to at [51] above, and concerns the Hawsons taxed costs of $167,144.00.

69 The 27 October 2014 Supreme Court order gave rise to the $75,000 costs liability referred to at [57] above.

70 On the judicial advice application, the liquidator submitted that the use of the word “set-off” in the notation was inapposite, and that it would be more accurate to characterise the agreement as a “mutual releases”, that is, a promise by each party to release the other from debts owed by each party to the other. The liquidator submitted that nothing turns whether it was correct to use the term “set-off” as the liquidators acted within their powers to effect the settlement. The liquidator noted:

(1) the statutory right of set-off pursuant to s 553C of the Act was not available as BMG was not insolvent;

(2) set-off under the rules of court was also not available, as the asserted set-off did not occur by way of a pleaded defence: cf Civil Procedure Act 2005 (NSW) s 21 and Federal Court Rules 2011 r 16.10;

(3) there could be no set-off between judgments as the liquidators’ acceptance of the Wentworth proof of debt was not a “judgment” in the requisite sense; and

(4) there is doubt whether the requirements of an equitable set-off were satisfied.

71 I am uncertain about the “mutual releases” characterisation: it is not obvious that the relevant debts are reciprocal. The POD Amount is a debt owed by BMG to Wentworth; the Hawsons taxed costs was a debt owed (jointly and severally) by the Wentworth parties to the liquidators and BMG jointly; the Supreme Court costs debt was owed by the Wentworth parties (jointly and severally) to the liquidators. I accept that there is mutuality between the POD Amount debt and Wentworth’s several liability to BMG for payment of the Hawsons taxed costs. To the extent that those costs were in fact incurred by the liquidators, the liquidators were entitled to be indemnified by BMG. As a matter of fact, the costs were paid by BMG from funds provided by Pure Metals (see [53] above).

72 After the hearing, the liquidator contended that the “set-off agreement”, contained in the notation recorded at [66] above, consisted of a set-off by which the amount of $190,000 was set-off against:

(a) Firstly, the amount of $180,300.29 (being the costs orders (Hawsons Costs) in our clients’ favour of $167,144 plus interest in the amount of $13,156.29 in respect of the [Hawsons proceeding] and the Certificate of Taxation issued on 19 March 2014; and

(b) Secondly, the remainder amount of $9,699.71 (resulting in a partial set-off of the amount of $75,000.

73 This contention is not consistent with the “mutual releases” characterisation that had earlier been proposed. In my view, the better construction of the “set-off agreement” is that it does not involve a release of the $75,000 costs liability: the ordinary meaning of the words of the agreement do not indicate any such release and nor does the context of the agreement: cf Pacific Carriers Ltd v BNP Paribas [2004] HCA 35; (2004) 218 CLR 451 at [22].

74 In my view, the “set-off agreement” included, relevantly:

(1) an agreement that the POD Amount ($190,000) would be admitted as a debt in the BMG liquidation;

(2) that debt would be reduced by the amount of the costs debt in the Hawsons proceeding (being the Hawsons taxed costs of $167,144.00 plus any interest that formed part of that debt), to the benefit of Wentworth and the other parties who were severally liable for that debt; and

(3) the debt would be further reduced to nil by the amount of the $75,000 costs liability.

75 Once the set-off agreement is performed, there will remain a liability owed by the Wentworth parties to the liquidator, being the balance of the $75,000 costs liability.

Liquidator’s calculation of costs “recoveries” pursuant to “mutual releases”

76 On 11 March 2015, the liquidators admitted the Wentworth proof of debt in the amount of $190,000.

77 The liquidator calculated that, as at 11 March 2015:

(1) BMG owed Wentworth $233,434, being the sum of $190,000 plus interest of $43,434.52 calculated on $190,000 for the period 3 May 2012 to 11 March 2015.

(2) The Wentworth parties owed BMG $255,300.29 comprising:

(a) the Hawsons taxed costs amount of $167,144.00 plus interest of $13,156.29 (totalling $180,300.29); and

(b) the $75,000 costs liability.

78 The liquidator submitted that the price of this compromise for BMG was the foregoing of the possibility of enforcing a debt for $21,866.29 (being the difference between $233,434 and $255,300.29). The liquidator says that he considered the price was justified by the limitation of the risk of a non-recovery of a judgment debt and the reduction of litigation costs.

79 As noted above, the costs of the Hawsons proceeding were incurred by the liquidators but paid by BMG. I accept that BMG was owed the Hawsons taxed costs amount pursuant to the Hawsons costs order. It is not accurate to say that the Wentworth parties owed BMG any amount in respect of the $75,000 costs liability because BMG was not a party to the proceeding in which the relevant costs order was made.

80 On the liquidator’s analysis, the effect of the “mutual releases” appears to be that BMG’s liability to Wentworth is reduced to nil because the POD Amount is less than the total of the amounts owing pursuant to the identified costs orders. I accept that this is a reasonable interpretation of the agreement recorded in the consent orders.

2015 payments to Pure Metals

81 On 27 March 2015, the liquidators paid Pure Metals the sum of $105,000.

82 On 18 September 2015, the liquidators paid Pure Metals the sum of $59,493.72.

83 In his first affidavit, Mr Leigh stated that these payments were made “once the liquidators had recovered” the Hawsons tax costs and the $75,000 costs liability. However, the evidence does not show that the liquidators “recovered” those amounts. In particular, the facts that Mr Leigh points to in his affidavit as evidence that the liquidators had recovered the amounts do not demonstrate any such recovery.

84 Based on the payments to Pure Metals, Mr Leigh calculated that the liquidators are indebted to Pure Metals in the sum of $15,806.57 being the amount of $180,300.29 “received” in respect of the Hawsons taxed costs less the amount of $164,493.72 paid to Pure Metals, as set out at [76] and [77] above.

85 The figure of $180,300.29 does not reflect an actual receipt in respect of the Hawsons tax costs. Rather it comprises the amount of the Hawsons taxed costs ($167,144) plus interest calculated from the date of the certificate of taxation to the date of the “mutual releases” (that is, 25 March 2014 to 25 February 2015). Mr Leigh explained that he had notionally credited the POD Amount against the sum of $180,300.29, with the result that the Hawsons taxed costs had been recorded as having been paid in full as at 25 February 2015.

86 Mr Leigh’s affidavit stated what these payments were once the liquidators had “recovered” the costs. The payments were made from the BMG liquidation bank account. The bank statements do not indicate that the payments were made following the receipt of any particular amount on account of costs and there is no other suggestion that the liquidators received any payments in respect of any costs order they obtained.

Legal framework

87 The liquidator seeks orders of the kind referred to in s 90-15(3)(a) of the Insolvency Practice Schedule. Section 90-15 relevantly provides:

Court may make orders

(1) The Court may make such orders as it thinks fit in relation to the external administration of a company.

Orders on own initiative or on application

(2) The Court may exercise the power under subsection (1):

(a) on its own initiative, during proceedings before the Court; or

(b) on application under section 90-20.

Examples of orders that may be made

(3) Without limiting subsection (1), those orders may include any one or more of the following:

(a) an order determining any question arising in the external administration of the company;

….

Matters that may be taken into account

(4) Without limiting the matters which the Court may take into account when making orders, the Court may take into account:

(a) whether the liquidator has faithfully performed, or is faithfully performing, the liquidator's duties; and

(b) whether an action or failure to act by the liquidator is in compliance with this Act and the Insolvency Practice Rules; and

(c) whether an action or failure to act by the liquidator is in compliance with an order of the Court; and

(d) whether the company or any other person has suffered, or is likely to suffer, loss or damage because of an action or failure to act by the liquidator; and

(e) the seriousness of the consequences of any action or failure to act by the liquidator, including the effect of that action or failure to act on public confidence in registered liquidators as a group.

Costs orders

(5) Without limiting subsection (1), an order mentioned in paragraph (3)(d) in relation to the costs of an action may include an order that:

(a) the external administrator or another person is personally liable for some or all of those costs; and

(b) the external administrator or another person is not entitled to be reimbursed by the company or its creditors in relation to some or all of those costs.

…

Section does not limit Court’s powers

(7) This section does not limit the Court's powers under any other provision of this Act, or under any other law.

88 By s 90-20(1)(d) of the Insolvency Practice Schedule and the definition of “officer” in s 9 of the Act, a liquidator is a person who may apply for an order under s 90-15.

89 The Court’s supervisory powers under s 90-15 of the Insolvency Practice Schedule are arguably as broad, or broader than, its powers under the previous provision, being the former s 479(3) of the Act.

90 Section 479(3) allowed a court-appointed liquidator to apply to the Court for directions in relation to a matter arising under a winding up. The function of a liquidator’s application for directions under s 479(3) was to give the liquidator advice as to the proper course of action for him or her to take in the liquidation: Re MF Global Australia Ltd (in liq) [2012] NSWSC 994; (2012) 267 FLR 27 at [7].

91 In Re Ansett Australia Ltd and Korda [2002] FCA 90; (2002) 115 FCR 409, Goldberg J explained at [44]:

When liquidators and administrators seek directions from the Court in relation to any decision they have made, or propose to make, or in relation to any conduct they have undertaken, or propose to undertake, they are not seeking to determine rights and liabilities arising out of particular transactions, but are rather seeking protection against claims that they have acted unreasonably or inappropriately or in breach of their duty in making the decision or undertaking the conduct. They can obtain that protection if they make full and fair disclosure of all relevant facts and circumstances to the Court. In Re G B Nathan & Co Pty Ltd (1991) 24 NSWLR 674, McLelland J said at 679–680:

“The historical antecedents of s 479(3) …, the terms of that subsection and the provisions of s 479 as a whole combine to lead to the conclusion that the only proper subject of a liquidator’s application for directions is the manner in which the liquidator should act in carrying out his functions as such, and that the only binding effect of, or arising from, a direction given in pursuance of such an application (other than rendering the liquidator liable to appropriate sanctions if a direction in mandatory or prohibitrary form is disobeyed) is that the liquidator, if he has made full and fair disclosure to the court of the material facts, will be protected from liability for any alleged breach of duty as liquidator to a creditor or contributory or to the company in respect of anything done by him in accordance with the direction.

…

Modern Australian authority confirms the view that s 479(3) ‘does not enable the court to make binding orders in the nature of judgments’ and that the function of a liquidator’s application for directions ‘is to give him advice as to his proper course of action in the liquidation; it is not to determine the rights and liabilities arising from the company’s transactions before the liquidation’: [cases cited omitted].”

(Emphasis added)

92 At [65], Goldberg J concluded:

[T]he prevailing principle adopted by the courts, when asked by liquidators and administrators to give directions, is to refrain from doing so where the direction sought relates to the making and implementation of a business or commercial decision, either committed specifically to the liquidator or administrator or well within his or her discretion, in circumstances where there is no particular legal issue raised for consideration or attack on the propriety or reasonableness of the decision in respect of which the directions are sought. There must be something more than the making of a business or commercial decision before a court will give directions in relation to, or approving of, the decision. It may be a legal issue of substance or procedure, it may be an issue of power, propriety or reasonableness, but some issue of this nature is required to be raised. It is insufficient to attract an order giving directions that the liquidator or administrator has a feeling of apprehension or unease about the business decision made and wants reassurance. There must be some issue which arises in relation to the decision. A court should not give its imprimatur to a business decision simply to alleviate a liquidator’s or administrator’s unease. There must be an issue calling for the exercise of legal judgment.

(Emphasis added)

93 I am satisfied that the Court has power to make orders of the kind sought pursuant to s 90-15 of the Insolvency Practice Schedule, and that the question of whether to exercise that power is to be answered by reference to the principles that applied to the exercise of the discretions previously contained in s 479(3) of the Act.

94 I am also satisfied that the issues raised by the liquidator arise in the external administration of BMG; call for the exercise of legal judgment; and arise in the context of significant disputation during the course of the liquidation, including in the context of the criticisms made by Mr Hillam of the conduct of the liquidation and the threat of litigation against the liquidator in connection with their conduct thereof. In these circumstances, it is appropriate to make directions in connection with the issues raised by the liquidator.

Pure Metal’s liability to indemnify liquidators and liquidator’s liability to reimburse Pure Metals

95 The first question is whether the liquidator is justified in proceeding on the basis that Pure Metals is liable to indemnify him for the legal expenses incurred in the defence of the Hawsons proceeding pursuant to cl 9(a) of the deed of assignment.

96 The second question is whether the liquidator is liable to reimburse Pure Metals for its indemnity from “recoveries” made by the liquidator as a result of the Hawsons taxed costs order and the subsequent notional credit made against the POD Amount.

97 The liquidator identified as the central issue for resolution of these questions as “the obligation of the [liquidator] to provide the benefit of costs orders obtained by the liquidators from proceedings to a litigation funder. The [liquidator] consider[s] that the funding party is subrogated to the [liquidator’s] rights under the costs orders”. As I understand the position, there is only one relevant costs order which is the order that gave rise to the Hawsons taxed costs.

98 The relevant factual propositions identified by the liquidator are:

(1) Pursuant to the deed of assignment, Pure Metals indemnified BMG and the liquidators in respect of claims arising out of, or in connection with, the transfer of the Hawsons asset to Pure Metals (“Pure Metals indemnity”).

(2) The Wentworth parties brought proceedings against BMG and the liquidators to challenge the liquidators’ sale of BMG’s Hawsons asset (“Hawsons proceeding”).

(3) Pure Metals paid the liquidators’ legal bills in the Hawsons proceeding. Some funds were provided by Pure Metals pursuant to the Pure Metals funding deed. At the time, Pure Metals denied that the Pure Metals indemnity covered the liquidator’s costs of the Hawsons proceeding.

(4) Subsequently, the liquidators and BMG received the benefit of costs orders made against Wentworth in the Hawsons proceeding, and other proceedings in which Wentworth challenged other actions by the liquidators.

(5) The liquidators settled other proceedings between Wentworth and BMG through a “mutual release”. One of the debts identified in this settlement was the debt owed by Wentworth to BMG in the amount of the Hawsons taxed costs.

(6) The liquidator considers that he is under an obligation to return to Pure Metals the benefit of the costs order relating to the proceedings to which the Pure Metals indemnity extends. To this end, the liquidator has made certain interim payments to Pure Metals. The liquidator seeks judicial directions in relation to the balance of his obligations.

99 Each of these propositions is considered below.

100 Proposition (1): On the proper reading of cl 9(a), on and from 8 February 2013, Pure Metals agreed to indemnify, relevantly, BMG and the liquidator on demand against all “Liabilities”, including legal costs on a solicitor-client basis, incurred by any of them arising out of or in connection with the assignment contemplated by cl 3 of the deed of assignment. The assignment contemplated by cl 3 is the transfer of the Hawsons asset to Pure Metals. Accordingly, proposition (1) is correct.

101 Proposition (2) is also correct. The Hawsons proceeding is a proceeding brought by the Wentworth parties to challenge the liquidators’ sale of BMG’s Hawsons asset.

102 Proposition (3) is also correct. The facts set out above show that Pure Metals paid the liquidators’ legal bills in the Hawsons proceeding. Funds of $150,000 were provided pursuant to the Pure Metals funding deed. As appears from the funding deed, at the time that it entered into that deed, Pure Metals did not accept that it was liable to indemnify the liquidators under the terms of the February 2013 assignment agreement. However, Pure Metals provided the liquidators with funds of $87.409.81 in excess of the amount that it was obliged to provide under the funding deed. Having found that Pure Metals was obliged to indemnify the liquidators in respect of their legal costs on a solicitor-client basis, incurred in connection with the transfer of the Hawsons asset to Pure Metals, I accept that the additional funds were paid in discharge of Pure Metal’s obligation under cl 9 of the deed of assignment.

103 The liquidator submitted that:

(a) The Pure Metals funding deed operated as a form of interest-free loan or debt facility in favour of the liquidators with an obligation to repay only in the event that the liquidator obtained funds from the realisation of BMG’s assets.

(b) The liability of Pure Metals for the costs of the Hawsons proceeding was otherwise undiminished by the existence of the deed of funding.

(c) The benefit of any costs order obtained by the liquidators in relation to the Hawsons proceeding would be transferred back to Pure Metals.

104 Based on the provisions of the deed of assignment and the funding deed set out above, I accept propositions (a) and (b). Proposition (c) arises from Pure Metals’ asserted right of subrogation explained below.

105 Proposition (4) is correct. The liquidators and BMG variously obtained the costs orders against Wentworth referred to at [51], [57] and [64] above.

106 Proposition (5): In February 2015, the liquidators, Wentworth and others settled an interlocutory dispute in this proceeding on terms that included the set-off agreement, referred to at [65] to [71] above. As appears from [47] and [48], one of the debts identified in this settlement was the debt owed by Wentworth to BMG for the costs of the Hawsons proceeding.

107 Proposition (6): As appears from the correspondence from MinterEllison to McCullough Robertson in June and August 2013, the liquidators (and now the sole liquidator) consider that they are under an obligation to return to Pure Metals the benefit of recoveries pursuant to the costs order made in the Hawsons proceeding. To this end, the liquidators made the payments to Pure Metals referred to at [81] and [82] above.

Obligation to return benefit of costs order to surety

108 Based on the facts set out above, I accept the following propositions:

(1) Pure Metals became a surety under cl 9 of the deed of assignment in respect of claims and liabilities incurred in relation to the assignment of BMG’s Hawsons asset.

(2) Clause 9 responded to the legal expenses incurred by the liquidators in the Hawsons proceeding and therefore Pure Metals became principally liable for the amount of the legal expenses: see Bofinger v Kingsway Group Ltd [2009] HCA 44; (2009) 239 CLR 269 at [7].

(3) The liquidators presented Pure Metals as surety with the tax invoices of the third party creditor Minter Ellison.

(4) The surety paid BMG so that the liquidators could satisfy their creditor, Minter Ellison, in full by the payment of amounts totalling $237,409.81 from the BMG liquidation bank account. The debt between the liquidators and Minter Ellison was thereby extinguished.

(5) BMG obtained the benefit of the POD Amount by the “set-off” agreement, as payment for monies owing by Wentworth pursuant to the costs orders referred to in that agreement. The amounts owing under those costs orders exceeded the POD Amount.

109 In Re Dalma No 1 Pty Ltd [2013] NSWSC 1335; (2013) 95 ACSR 641 at [24], Brereton J explained when subrogation will be permitted in the following terms:

[T]here is no all-embracing theory that explains when subrogation will be permitted; the equity arises from the conduct of the parties on well-settled principles and in defined circumstances which make it unconscionable for the defendant to deny the plaintiff's right [Boscawen v Bajwa [1995] EWCA Civ 15; [1995] 4 All ER 769, 777 (Millett LJ); Bofinger v Kingsway Group Ltd [2009] HCA 44; 239 CLR 269, 300-1]. Pomeroy identified those circumstances as follows [Pomeroy (1941) Vol 4 p 1074, [1419], citing Louisville Joint Stock Land Bank v Bank of Pembroke 9 SW (2d) 113, 115 (Ky CA)(1928); cited with approval in Re Trivan Pty Ltd (1996) 134 FLR 368, 371 (NSWSC, Young J)]:

The doctrine is in general applied in favour of all persons who are required to pay the debt of another for the protection of their own interests. [Without attempting a comprehensive classification of cases in which the doctrine of subrogation may be applied, it is generally held that the right of subrogation will arise where the party claiming it has advanced money to pay a debt, which, in the event of default by the debtor, he would be bound to pay; or where the one making the payment has some interest to protect; or where the money advanced to pay the debt was under an agreement with the debtor, or the creditor, express or implied, that he should be subrogated to the rights and remedies of the creditor.]

(Emphasis in original)

110 The liquidator submitted, and I accept, that the relationships in this case are analogous to those considered in Stewart v Atco Controls Pty Ltd (in Liq) [2014] HCA 15; (2014) 252 CLR 307. The liquidator noted the following relevant facts in that case:

(1) Seeley International Pty Ltd (“Seeley”), an unsecured creditor of Newtronics Pty Ltd (“Newtronics”), provided the liquidators of Newtronics with funding under a series of agreements by which Seeley undertook to indemnify the liquidators for “costs and expenses” incurred in certain work for the liquidation.

(2) The indemnity provided by Seeley was found to respond to the costs and expenses of the liquidators incurred in legal proceedings brought against receivers that were appointed to Newtronics by its parent company, Atco Controls Pty Ltd (“Atco”).

(3) The receivers settled the proceeding with the liquidators, and the liquidators brought the settlement sum into Newtronics’ funds.

(4) The liquidators then paid the settlement sum to Seeley by way of reimbursement of the costs and expenses that Seeley had paid under the indemnity agreement respecting the actions against the receivers.

(5) Atco, which was a secured creditor of Newtronics, then demanded payment from the settlement sum and commenced an action against the liquidators.

111 At [49] and [50], the High Court explained the legal basis for the liquidator’s reimbursement payment to Seeley from the settlement sum as follows:

On this appeal, Atco continued to pursue a submission … that, at the time the settlement sum was received, there was no indebtedness that could give rise to an equitable lien, for the reason that Seeley had paid the liquidator’s costs and expenses respecting the litigation under the indemnity agreement. The argument ignores Seeley’s right to reimbursement and the liquidator’s obligation to provide such reimbursement out of the settlement sum.

It has never been disputed in these proceedings that the agreement between Seeley and the liquidator took effect as an indemnity. It is an incident of such an agreement that an indemnifier has a right to reimbursement of all monies paid under the indemnity. The indemnifier has a right of subrogation to all the rights and remedies of the party indemnified and any monies recovered by that party: Burnand v Rodocanachi Sons & Co (1882) 7 App Cas 333 at 335; Castellain v Preston (1883) 11 QBD 380 at 386, 393, 403-404; Morris v Ford Motor Co [1973] QB 792]. It follows that the liquidator was obliged to reimburse Seeley and that the equitable lien attached to the settlement sum as a charge to permit that indebtedness to be met.

112 Applying this reasoning, on the making of the “set-off” agreement, the liquidators of BMG were obliged to reimburse Pure Metals from the benefit obtained by BMG, namely, the agreement that the POD Amount would be reduced by the amount of the costs liability in the Hawsons proceeding. In this case, the position is stronger because the indemnity given by Pure Metals was in favour of BMG as well as the liquidators.

113 Accordingly, I am satisfied that Pure Metals’ right to subrogation arose on the making of the “set-off” agreement.

Conclusion

114 It follows from propositions (1) and (2) that Pure Metals was liable to indemnify the liquidators and BMG for liabilities, including relevantly, to indemnify the liquidators for the legal expenses incurred by them in the defence of the Hawsons proceeding pursuant to cl 9(a) of the deed of assignment. It discharged this obligation: proposition (3).

115 Either the liquidator or BMG is liable to reimburse Pure Metals out of the benefit obtained by BMG under the “set-off” agreement on account of the legal expenses paid by Pure Metals for the defence of the Hawsons proceeding. It would be unconscionable for BMG to retain that benefit.

116 Accordingly, I am satisfied that the liquidator is justified in paying to Pure Metals the further sum of $15,806.57 referred to in [84] above.

Proposed reduction of the distribution to Mr Hillam and Ms Teeranukul

117 The liquidator submitted that Mr Hillam and Ms Teeranukul’s distribution from the liquidation should be reduced by the amount to which they are indebted to BMG in accordance with the rule in Cherry v Boultbee.

118 The most common expression of the rule in Cherry v Boultbee is found in Re Peruvian Railway Construction Company Ltd [1915] 2 Ch 144 at 150 per Sargent J:

[W]here a person entitled to participate in a fund is also bound to make a contribution in aid of that fund, he cannot be allowed so to participate unless and until he has fulfilled his duty to contribute.

119 In Re Anglican Development Fund Diocese of Bathurst [2015] NSWSC 440, Brereton J reviewed the history of the rule, concluding at [30] that although Cherry v Boultbee “might have been capable of a narrower explanation, the later authorities establish an equitable principle, founded in conscience, that a contributor to a fund will not be permitted to participate until the contribution has been completed”.

120 In Derham on the Law of Set-Off (4th ed., Oxford University Press, 2013) at [14.08], the author said that:

Cherry v Boultbee may be invoked to prevent a shareholder of a company which is in liquidation, but which has a surplus available for distribution amongst the shareholders, from receiving a rateable proportion of the surplus without satisfying a debt that he or she owes to the company, citing Re Peruvian Railway Construction Company Ltd [1915] 2 Ch 144, 151; RE 3 Ernest Street Pty Ltd (1980) CLC 40–619 at p 34,146; Re Kowloon Container Warehouse Co Ltd [1981] HKLR 210; and Otis Elevator Co Pty Ltd v Guide Rails Pty Ltd [2004] NSWSC 383; (2004) 49 ACSR 531.

121 The underlying principle is that it would be inequitable to allow the claimant to compete against the other persons entitled to share in the fund until the whole fund has been constituted, by getting in the asset which the claimant’s debt represents: Re SSSL Realisations (2002) Ltd [2006] EWCA Civ 7; [2006] Ch 610 (“SSSL Realisations”) at [103]-[104] and Ansett v Travel Software Solutions [2007] VSC 326; (2007) 214 FLR 203 at [105].

122 The liquidator submitted that the following preconditions for the application of the rule in Cherry v Boultbee will be met at the time that the liquidator distributes the surplus:

(1) Mr Hillam and Ms Teeranukul are both persons entitled to and also liable to contribute to the liquidation fund. Thus, the requirements of mutuality are met.

(2) Upon the grant of leave to distribute the surplus pursuant to s 488(2) of the Act, the liquidator will distribute the surplus to the contributories. This decision will make the debts to Mr Hillam and Ms Teeranukul for their shares of the surplus due and payable.

(3) The proposed distribution of BMG’s surplus assets will be in the form of money.

123 I accept that it is reasonable to assume that (1) to (3) will apply at the time that the liquidator seeks to distribute the surplus.

124 In Public Trustee v Gittoes aka Caldar [2005] NSWSC 373 at [138], White J explained that the equity illustrated by Cherry v Boultbee would be satisfied:

… either by the defendant making the contribution which he is required to make before the estate is distributed, in other words by paying the amount due under the costs order, or by the administrator treating the amount as if it had notionally been paid, dividing the fund for distribution between the [persons entitled to the surplus] on that basis, and then deducting from the amount to be paid to the defendant, the amount of his unpaid liability.

125 In Cumming v Sands [2001] NSWSC 706 at [9], Hamilton J similarly concluded that “the deduction of the amount at the time of payment to the plaintiff will satisfy the dictates of equity”.

126 I therefore accept that, provided the pre-conditions set out above apply, it would be appropriate to make a deduction of any debt due by Ms Hillam and Ms Teeranukul from the amount to be distributed to each of them from the surplus.

Liquidator’s calculations

Principles

127 The calculations are intended to reflect the proposition that Mr Hillam and Ms Teeranukul will be entitled to a percentage of the available surplus. Derham on the Law of Set-Off explains the proper calculation in these terms at [14.93]:

[T]he administrator invoking the principle calculates the claimant’s share on the basis that the fund has been increased by the value of the claimant’s indebtedness, and the claimant becomes entitled to the requisite percentage of the total fund, which includes the debt. The administrator then directs the claimant to appropriate the debt as pro tanto payment of his or her share, and so the net sum (if any) payable to the claimant is the difference between the share calculated in this manner and the indebtedness to the fund.

128 In SSSL Realisations at [79], Chadwick LJ suggested an equation to determine the amount that the debtor/contributor claimants are to receive.

Effect is given to the general rule, as a matter of accounting, by treating the fund as notionally increased by the amount of the contribution; determining the amount of the share by applying the appropriate proportion to the notionally increased fund; and distributing to the claimant the amount of the share (so determined) less the amount of the contribution. The rule can be expressed in the form: D=1/n of (A+C)−C, where 1/n where 1/n is the proportion which the aliquot share bears to the whole, A is the amount of the assets to be distributed before taking account of the contribution due to the fund from the claimant, C is the amount of the contribution, and D is the amount which the claimant is entitled to receive in the distribution. It can be seen that the claimant will receive nothing by way of distribution if C > 1/n of (A + C).

129 The proposed contribution by Mr Hillam and Ms Teeranukul of $171,318.13 is calculated as follows:

(d) “CM costs” $65,300.29

(e) “Joint JD and CFM costs” $106,017.84

TOTAL $171,318.13

130 The “CM costs” comprise the $75,000 costs liability less the amount of $9,699.71 being the difference between the POD Amount and the amount of the Hawsons proceeding costs liability.

131 Having regard to my conclusion above, that there was no release of the $75,000 costs liability was compromised by the “set-off” agreement, I accept that this amount should be included in the proposed contribution.

132 The “Joint JD and CFM costs” is the $90,000 plus interest costs liability, referred to at [64] above. Mr Leigh’s first affidavit includes a calculation of interest on the sum of $90,000 from 28 March 2015 to 28 June 2017 in accordance with interest rates set by this Court. Although it is a liability to the liquidators, it is sufficient for the application of the rule in Cherry v Boultbee that the relevant debt is a contribution “in aid of the fund”: Re Saltergate Insurance Co Ltd (No 2) [1984] 3 NSWLR 389 at 393-394.

Direction concerning proposed distribution of assets

133 The liquidators proposed the following distributions, following the application of the rule in Cherry v Boultbee:

134 The allocation of the surplus must be in the proportions indicated by the respective shareholding, subject to any provisions of the constitution fixing or affecting proportions: Re Yanollee Pty Ltd [2006] NSWSC 705 at [12]. The liquidator’s written submission stated that there is nothing in the constitution of BMG that would alter the distribution of the surplus to the contributories rateably, according to the numbers of shares held by each contributory. Mr Hillam did not say anything to the contrary.

135 The amount of the contribution by Mr Hillam and Ms Teeranukul will include the interest which accumulates on the debt until the share becomes payable Gray v Gray & Anor [2004] NSWCA 408 at [94] and [100].

136 The proposal involves an acceptance of the liquidator’s calculation of surplus funds. I would require further evidence to accept that calculation. However, I will make an order that the liquidator is justified in proceeding on the basis that the rule in Cherry v Boultbee may be applied to the calculation of the amounts for distribution to the contributories.

Costs

137 On 18 December 2017, I made an order that the hearing listed to take place that day be vacated on the basis that the 1st and 2nd applicants on the interlocutory process of 18 December 2017 (Mr Hillam and Ms Teeranukul) pay the liquidator’s costs thrown away by reason of the hearing being vacated, including the costs of the hearing on 15 December 2018.

138 The liquidator now seeks orders that:

(1) The liquidator’s costs as agreed or assessed be owed by Mr Hillam as a debt to BMG.

(2) The costs amount be deducted (for the benefit of BMG) from Mr Hillam’s distribution through an application of the rule in Cherry v Boultbee.

(3) The liquidator recovers from BMG the amount of the costs order prior to the distribution of the surplus funds.

139 I will hear an application for a lump sum costs order in relation to the liquidator’s costs, provided it is filed promptly.

140 Applying the principles set out earlier in these reasons, it would be appropriate to add these costs to the amount to be contributed to the fund by Mr Hillam and Ms Teeranukul. However, I do not accept that the first and the third proposed orders are either appropriate or necessary.

Conclusion

141 I will make orders pursuant to s 90-15(3)(a) of the Insolvency Practice Schedule that the liquidator is justified:

(1) in proceeding with the liquidation on the basis that Pure Metals indemnified the liquidators for their legal expenses incurred in the defence of the Hawsons proceeding pursuant to cl 9(a) of the deed of assignment;

(2) in paying Pure Metals the amount of $15,806.57 from the assets of BMG, being the amount still owing to Pure Metals in connection with the indemnity; and

(3) in proceeding on the basis that the rule in Cherry v Boultbee may be applied to the calculation of the amounts for distribution to the contributories in accordance with the reasons set out above.

142 I will also make an order requiring the liquidator to take steps for the further conduct of this proceeding, with a view to its finalisation as soon as practicable.

I certify that the preceding one hundred and forty-two (142) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate:

NSD 1784 of 2010 | |

SARABOL TEERANUKUL | |

Fifth Defendant: | WENTWORTH METAL GROUP PTY LIMITED (ACN 139 532 719) |

Respondents to the Amended Interlocutory Process | |

Fourth Respondent: | MATTHEW GOLLAN |

Fifth Respondent: | AMPLE SOURCE INTERNATIONAL LIMITED (BVICN 157 5638) |

Sixth Respondent: | JAMES RICHARD VEREKER |

Seventh Respondent: | GIRALIA RESOURCES PTY LTD (FORMERLY GIRALIA RESOURCES N.L.) (ACN 009 218 204) |

Eighth Respondent: | RED GOLD AUSTRALIA PTY LTD (ACN 147 204 457) |

Ninth Respondent: | PURE METALS PTY LTD (ACN 151 066 321) |