FEDERAL COURT OF AUSTRALIA

PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd) v Peter Vogel Instruments Pty Ltd [2018] FCA 1587

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. There be judgment for the first respondent/cross-claimant against the applicant/first cross-respondent in the amount of $383,956 (exclusive of interest).

2. The first respondent/cross-claimant pay to the applicant/first cross-respondent the amount of $9,808 (exclusive of interest).

3. The applicant/first cross-respondent is entitled to set-off the amount referred to in order 2 (and any interest thereon) against the judgment referred to in order 1.

4. Orders 1-2 are made without prejudice to the right of the parties to seek interest on the amounts referred to in those orders pursuant to s 51A of the Federal Court of Australia Act 1976 (Cth) ("s 51A interest").

5. The parties are to confer for the purpose of reaching agreement in relation to s 51A interest calculations.

6. Within 14 days the parties are to file and serve written submissions (limited to 3 pages in length) in relation to:

(a) the amount of any s 51A interest that should be awarded; and

(b) the costs of the proceeding generally including the costs of and incidental to the remittal hearing (but excluding the costs of the appeal from Edmonds J's orders of 17 December 2015).

7. Within 21 days the parties are to file and serve any written submissions in reply (limited to 2 pages in length).

8. The proceeding be listed before Nicholas J at 9.30am on 22 November 2018 for the purpose of making further orders relating to interest, costs and the final disposition of the proceeding.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NICHOLAS J:

Introduction

1 This proceeding was remitted by a Full Court for further hearing following the determination of an appeal and a cross-appeal against a judgment of another judge of the Court (Edmonds J): see Fairlight.AU Pty Ltd v Peter Vogel Instruments Pty Ltd (No 3) [2015] FCA 1422 and Peter Vogel Instruments Pty Ltd v Fairlight.Au Pty Ltd [2016] FCAFC 172.

2 Peter Vogel Instruments Pty Ltd ("PVI"), formerly known as Fairlight Investments Pty Ltd ("FI"), is the first respondent and cross-claimant in the proceeding, and Mr Peter Vogel is the second respondent. Fairlight.Au Pty Ltd ("Fairlight.Au"), which is now called PKT Technologies Pty Ltd, is the applicant and cross-claimant in the proceeding. Fairlight.Au was the respondent to PVI's appeal and the cross-appellant in the Full Court.

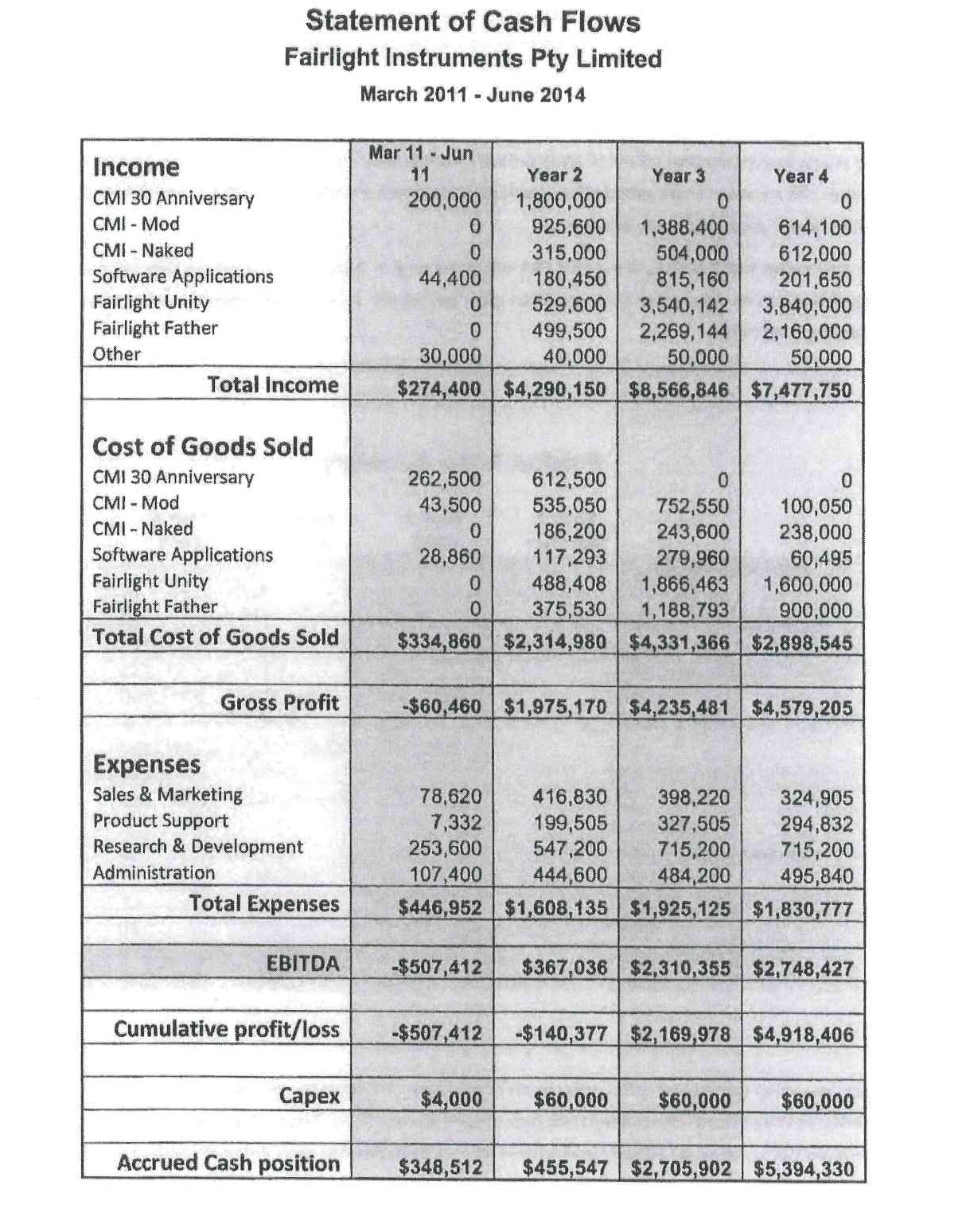

3 The orders of the Full Court require:

(a) the determination on the evidence adduced at the trial held in December 2014, and subject only to any order allowing further evidence to be adduced, any damages to which PVI is entitled:

(i) for repudiation of a written agreement dated 15 August 2010 ("the agreement") by the cross-respondent; and

(ii) for infringement of PVI's copyright in a computer program known as Dream II;

(b) the taking of an account of profits to which the applicant may be entitled for infringement of Fairlight.Au's trade mark;

(c) the determination of the entitlement of the parties to costs on the claim and cross-claim; and

(d) the determination of the disposition of the proceedings.

4 At the hearing of the remittal, Mr Vogel was granted leave to appear for PVI. Mr Sirtes SC and Mr Kaufmann appeared before me for Fairlight.Au, as they had done before Edmonds J and before the Full Court. PVI was also represented by Mr Vogel at the hearing before Edmonds J and by counsel before the Full Court.

Factual background

5 The background to the agreement was the subject of findings by the primary judge that were not disturbed by the Full Court.

6 In 1975 Mr Vogel, who is an electronics engineer, co-founded a company called Fairlight Instruments, which developed the world's first music synthesiser capable of sampling natural or instrumental sounds. It was known as the Fairlight Computer Musical Instrument or the Fairlight CMI. Mr Vogel enjoys a long-standing reputation as a co-founder of Fairlight Instruments and as the designer of the Fairlight CMI.

7 Mr Vogel worked at Fairlight Instruments for approximately 14 years. He ended his association with Fairlight Instruments in 1989.

8 In 2009 Mr Vogel decided to build a 30th anniversary commemorative version of the Fairlight CMI. He entered into negotiations with Fairlight.Au aimed at facilitating the production of the commemorative version which he called the Fairlight CMI-30A. As a result of these negotiations PVI, a new company established by Mr Vogel in October 2009 (which he called Fairlight Instruments Pty Ltd) entered into a written agreement dated 15 August 2010. Fairlight.Au was by this time controlled by KFT Investments Pty Ltd ("KFT").

The Written Agreement

9 The Full Court set out the terms of the written agreement entered into between PVI and Fairlight.Au at [10]:

This Agreement is made on 15th August 2010 between:

Fairlight Instruments Pty Ltd (ACN 140 173 397) of 10 Whitney Street, Mona Vale, New South Wales, 2103, Australia ("FI"); and

Fairlight.au Pty Ltd (ACN 104 307 888) of Unit 3/15 Rodborough Road, Frenchs Forest, New South Wales, 2086, Australia ("F.au").

Background

1. FI is a corporation established by Peter Vogel to develop and commercialise electronic musical instruments and related products.

2. F.au is a developer of technology for the audio and film industry.

3. FI wish to produce:

(1) a 30 Year anniversary model of the Fairlight CMI referred to as the "CMI-30A" and

(2) a PC compatible version known as the "Series IV", referred to collectively as the "CMI Products".

4. F.au will provide FI with:

(1) certain hardware and technologies including customised software development for the CMI Products

(2) a license for the use of the name "Fairlight" for the CMI Products during the term of this agreement; and

(3) supply of core components including sound library, on the terms contained in this agreement.

5. FI will raise the required development funds, manufacture, market and distribute the CMI Products internationally. FI warrants that it has sufficient capital to commit to contract F.au to carry out the development contemplated herein.

Operative provisions

Obligations of FI

6. FI will pay F.au a total of $200,000 (plus GST) for:

(1) the development of the Fairlight CMI Software; and

(2) worldwide use of the "Fairlight" name and brand for marketing purposes for the CMI Products developed and/or marketed by FI pursuant to and during the term of this agreement.

(3) Use of Fairlight name and brand cannot be sold or transferred to any other party without written agreement by F.au.

(4) F.au reserves the right to withdraw the right for FI to use the Fairlight name and brand, should the name and brand be used in any way which F.au deem to be damaging to the Fairlight Brand reputation.

7. FI will make the payment to F.au required by clause 6 by way of four payments, each of $50,000 (plus GST) (total of $200,000) against F.au's demonstrated meeting of milestones as agreed between the parties before commencement of the development project.

8. Based around the hardware and software provided to FI by F.au as described herein, FI will package, develop, manufacture and market Fairlight branded musical instruments.

9. FI will package, develop, manufacture and market Fairlight branded musical instruments at its own cost, pay F.AU a one-off fee for development of the software as specified below, and purchase F.au custom components including Crystal Core and SX-x devices.

10. FI will develop the necessary components of the CMI Products including the retro keyboard and CMI box ready to accept the F.au boards and software. FI will also undertake all aspects of the marketing of the CMI Products, including but not limited to:

(1) direct sales;

(2) sales channel management; and

(3) promotional activities.

11. FI will market and sell the CMI Series IV in a "sound-module" form, ie without a keyboard, but as CC-1 and Fairlight CMI software only.

12. FI will assist in the specification and testing process, and in gathering market feedback.

Obligations of F.au

13. F.au agrees to produce a software application emulating the sounds and user interface of the Fairlight CMI running on a PC using a CC-1 card.

14. In addition to hardware and software provided by F.au to FI, F.au will include a licensed version of the Fairlight CMI sound libraries.

15. F.au will supply the following products and technology to FI for the CMI Products:

(1) "Fairlight CMI Software" application;

(2) CC-1 card; and

(3) SX-8 or similar input/output device.

16. A detailed specification for the final CMI-30A product will be produced by the parties prior to commencement of development.

17. F.au agrees to complete the necessary CMI Hardware and Software within four months from order. 'Order' being defined as: signed agreement, signed specification of product, signed list of monthly milestones, signed definition of transferred IP, and receipt of first $50K.

18. F.au reserves the right to extend the 4 month delivery period should FI not make its stage payment in a timely manner.

19. F.au agrees that in the event that it is unable to supply hardware or software as contracted within a commercially reasonable time, or if an administrator or receiver is appointed to F.au, FI is automatically granted an immediate perpetual, royalty-free licence to use anything belonging to or controlled by F.au necessary for FI to complete the development or manufacturing contemplated by this agreement. This is provided that full payment for any work completed up to that point has been provided by FI to F.au.

Intellectual property rights

20. Upon receipt of the final payment-from FI, F.au agrees that the software and its source components developed by F.au pursuant to this agreement will transfer to FI. The exact definition of IP to be transferred will be defined in a separate document.

21. F.au does not own any of the FI business that commercialises the CMI Products and related products and technology.

22. FI will own the Fairlight CMI Software application and all its specific source code including elements of the Crystal Core source code. There are no other IP implications.

Sale of CMI Products

23. By default, a CC-1 card sold for use in a CMI system cannot run Dream II software without additional licensing. Likewise, a CC-1 card sold for use in a Dream II system cannot run CMI software without additional licensing.

24. All licensing will be handled through F.au, with appropriate and timely reporting to FI.

25. F.au will have the opportunity to purchase Fairlight CMI Software licenses to sell with existing and future F.au products at a price to be negotiated in the order of AUD $1,500.00 per license.

26. The Parties agree the following cost of components for the CMI-IV, subject to negotiation and based on exchange rates and discount for product volumes:

(1) Package 1 (CC-1, SX-8) AUD $2,542.00

(2) Package 2 (CC-1, SX-20) AUD $3,977.00

27. FI is licensed to offer CMI-30A customers an upgrade path to full Dream II capability, through purchasing a license from F.au at a price to be negotiated, in line with the prevailing list price.

28. F.au will also be able to market the CMI Products through its distribution channel.

General.

29. This agreement is governed by the laws of New South Wales, Australia.

30. All references to "$" are to Australian dollars.

31. This agreement binds the parties and their successors.

Term

32. After one year from signing, this agreement can be terminated on three months written notice by F.au if FI fails to purchase from F.au products to a minimum value of $50,000 per annum (calculated annually in arrears, commencing from the date of completion of the development contract contemplated herein).

33. This agreement can be terminated by FI by giving three months written notice.

34. Otherwise the agreement is ongoing unless terminated by agreement between the parties.

10 The primary judge found:

by virtue of clauses 3, 4 and 6 of the agreement, PVI was granted a licence to use the FAIRLIGHT trade mark worldwide, but only in relation to two products being the "CMI-30A" and the "Series IV;

during the term of the agreement, PVI had developed Apps for the iPhone and iPad ("the Fairlight Apps") which were promoted and sold by PVI under the FAIRLIGHT trade mark. The Fairlight Apps were found to be products that replicated the essential functions of the CMI-30A;

the licence conferred by the agreement to use the trade mark did not extend to its use in relation to the Fairlight Apps; and

by using the mark for the Apps from 22 March 2011, PVI infringed the trade mark.

11 The relief granted by the Full Court included the following declarations:

(1) Fairlight.Au validly withdrew the right for PVI to use the FAIRLIGHT name and brand pursuant to clause 6(4) of the agreement by notice given to PVI and Mr Vogel by letter dated 30 May 2012.

(2) From 1 June 2012, by reason of the withdrawal of the right for PVI to use the FAIRLIGHT name and brand, PVI did not have and does not have any right, licence or authority to use the FAIRLIGHT name and brand with respect to "CMI Products" as defined in the agreement (except for those already supplied under the agreement) or any other products or services or otherwise in the course of business.

(3) PVI contravened s 120 of the Trade Marks Act 1995 (Cth) by using the FAIRLIGHT trade mark in the course of trade without the licence or authority of Fairlight.Au from about March 2011, with respect to applications for use with or in respect of the iPad and iPhone or similar products and in marketing and selling such applications.

12 The Full Court did not grant any declaratory relief in respect of Fairlight.Au's repudiation of the agreement but it is clear from a reading of the Full Court's reasons for judgment that it concluded that the sending of the letter dated 30 May 2012 to PVI amounted to a repudiation of the agreement by Fairlight.Au. The Full Court observed at [70] that PVI seems to have accepted Fairlight.Au's repudiation but it did not make any more specific findings as to when or how PVI did so.

The Information Memorandum

13 In March 2011 PVI issued an information memorandum in which PVI sought to raise A$500,000 through a share placement. In this document Mr Vogel is described as a co-founder of Fairlight Instruments who performed ground breaking work in music technology. Mr Ross is described as Business Development Manager. At all material times Mr Vogel and Mr Duncan Ross were directors and shareholders of PVI.

14 The information memorandum, dated 11 March 2011 ("the Memorandum") included an Executive Summary. The Executive Summary stated:

• Thirty years ago Peter Vogel co-founded Fairlight Instruments, the company which developed the first keyboard instruments to use sound sampling technology.

• Fairlight.au Pty Ltd today is a recognised leader in the global audio post-production industry but is no longer active in the musical instrument market.

• Peter Vogel has now established a new company, Fairlight Instruments Pty Ltd, which seeks to capitalise on his reputation as an innovative product developer and - new technological advances by producing a new line of musical instruments.

• Fairlight Instruments has obtained a licence to use the Fairlight trademark from Fairlight.au Pty Ltd in the musical instruments market.

• Fairlight Instruments' first product, the CMI-30A, is a commemorative replica of the original Computer Musical Instrument (CMI), with the look and feel of the original but using modern technology to achieve dramatic cost reduction.

• After a first round of capital raising in 2010, a prototype CMI-30A was developed and showcased at the 2011 NAMM (National Association of Music Merchants) show in the USA in January. This launch generated tremendous interest around the world from both musical instrument distributors and end users.

• The CMI-30A will be a flagship product that will lead to a range of prestige musical instruments in various formats.

• A second round of capital is now being raised to fund production and continue product development. The current business plan suggest the following financials are achievable:

Part Year 1 March-June | Year 2 | Year 3 | Year 4 | |

Revenue (est) | $247,400 | $4,290,150 | $8,566,846 | $7,477,750 |

EBITDA | -$507,412 | $367,036 | $2,310,355 | $2,748,427 |

Investment | 500,000 |

• Fairlight Instruments is seeking to raise AU$500,000 with a minimum parcel of size of AU$100,000 for a total of 14% of the business.

15 The Memorandum contains a section headed "The Fairlight Story" which provides an account of the history of the Fairlight brand, the Fairlight CMI and the sound sampling technology developed by Mr Vogel. It explains that Fairlight.Au, the successor to the original Fairlight company, later moved out of the musical instrument market and into professional sound and video post-production equipment. In 2006 Fairlight.Au developed a new digital sample processor ("DSP") system known as "Crystal Core" incorporating a new technology delivering improved performance at a fraction of the cost of the old DSPs. Crystal Core technology is installed into computers using a Crystal Core media processor (a "CC-1 card" or a "CC-1"). The CC-1/SX12 was the CC-1 card developed by Fairlight.Au for use in the CMI-30A.

16 The Memorandum includes a section entitled "Fairlight Instruments in 21st century" which describes the business strategy which the proposed capital raising will be used to pursue. The following appears at pp 4-6:

Fairlight Instruments in the 21st century

Since the original Fairlight CMIs (Computer Musical Instruments) of the eighties, there have been many advances in the creation and production of electronic music. Although synthesised sounds today approach technical perfection, many musicians lament that current equipment and techniques produce sounds which lack the warmth and unique characteristics that defined music of the eighties and nineties.

Peter Vogel, who had not been involved in Fairlight.au for many years, was excited by the prospect of applying Crystal Core technology in the musical instrument market. As a result of discussions with Fairlight.au, in 2009 he established Fairlight Instruments with the intention of releasing a new breed of musical instruments based on the Crystal Core. Fairlight Instruments has now licensed the mature Crystal Core technology from Fairlight.au for use in a range of musical instruments Peter is now designing.

Strategy

Fairlight Instruments' broad strategy is to exploit the Fairlight brand and Peter Vogel's reputation as an innovator in music technology, both of which are held in great esteem by the global musical instrument market.

An underlying philosophy is to maximise return on investment in R&D by repurposing hardware and software to address multiple market opportunities.

Products will be targeted at a range of markets. These markets will include the vintage instrument market, professional musicians, prosumer and high end retail markets.

All products and software will be priced at the high end of the market reflecting both the brand values and high cost of product development and customised manufacturing.

The company will work proactively to more broadly re-establish the brand profile in high value markets. This will be done by association with thought leaders in the music industry including composers and performers in addition to engaging enthusiasts through a range of social networking media. Fairlight will also drive the brand into specific musical groups that may not have traditionally had extensive exposure to the brand - such as the hip hop movement.

Strategic joint venture opportunities will be pursued to provide brand lift and secure broad distribution.

High end, specialised products will be sold directly from Australia to end users, whereas products with mass appeal will be sold through conventional musical instrument distribution/retail channels.

Wherever possible, Fairlight will maintain a high industry profile including attendance at trade shows and industry forums.

Products

To commemorate the 30th anniversary of the sale of the first CMI systems, Fairlight Instruments' first product is a limited edition 30th Anniversary model, the Fairlight CMI-30A. This includes a 76 note keyboard, screen with "lightpen" and computer.

…

The 30A software combines the very best of the early CMIs, with a number of significant new features.

…

Some celebrities who put Fairlight on the map in the eighties have offered to assist with the re-launch of the CMI, including permission to include sounds which they used on their hits in the sound library to be supplied with the CMI-30A.

In the seventies, the CMI was by necessity complex and bulky, with a correspondingly huge price tag. Thanks to the extraordinary price/performance of the Crystal Core media processor (CC-1), the CMI-30A will not only faithfully reproduce the authentic CMI sound but go well beyond the original capabilities at dramatically lower cost and size.

Once the initial demand for the classic CMI has been met, the software developed for the CMI-30A will also be packaged with a CC-1 card and sold as a smaller and lower cost option for musicians who want the CMI sound but are not interested in the "retro" packaging and keyboard. This will be sold as the CMI-series 4 or "Naked 30A" and comprise a standard PC package with CC-1 and audio interface. No new hardware or software will be required for this product.

This product lineup maximises return on the company's investment in software, which is the major development cost.

17 There follows some discussion of the Fairlight App which is said to be due for release in March 2011. This appears at page 6:

Apple iOS Application

Fairlight Instruments has now completed development a Fairlight app for iPhone and iPad. Due for release in March 2011, this app was previewed at the 2011 NAMM show, where it generated enormous excitement. The app is intended to introduce a new generation of musicians to the famous and mythical Fairlight, while potentially generating significant revenue in its own right.

…

An Android version will be developed, subject to the commercial results of the iOS release. Software applications for Macintosh and PC platforms are also planned.

…

It is anticipated that the Fairlight App, CMl-30A and Naked-30A will sustain the business for at least the first year. During this time, feedback from the marketplace and the company's board of directors will drive development of significant new concepts in synthesis and sequencing. These will essentially be software upgrades and will breathe new life into the market from year 2 onwards.

18 There is then a description of other keyboard products referred to as the "Fairlight Father", the "Fairlight Unity" and the "CMI Module". The CMI Module was a small rack unit with network, USB and audio interfaces which, when connected to a computer running the CMI application, would provide the same functionality as the CMI-30A.

19 It is also said (at p 8) that it is an object of the company to market "software only derivatives of its product line" which "is potentially a much more profitable and lower risk activity than manufacturing hardware".

20 The Memorandum states that first production units of the CMI-30A were expected to be delivered in June 2011. It is said that a business plan had been prepared based on initial sales forecasts of ten units per month. Also included was a Product Sales Summary and a Statement of Costs Plan for the period March 2011-June 2014 and a Statement of Cash Flows for the same period. A copy of the latter is reproduced in Schedule A to these reasons.

21 The Memorandum includes the following description of investment risk at page 13:

As with any start-up company, investment in Fairlight Instruments Pty Ltd carries risk. However the risk is mitigated by the following factors:

• The Fairlight brand is already established and extremely well respected in the musical instrument and technology markets.

• Technical risk is low since prototypes have been constructed and demonstrated.

• Commercial risk is low because the market has been tested with positive results.

• The first software-only product, the Fairlight iOS App, is complete and ready to launch.

• The company's founder and major shareholder, Peter Vogel, is internationally recognised as a pioneer of music technology.

• The company has already sold the first CMI-30A and full production will commence in June 2011.

22 It is said that the proceeds of the capital raising would be used to fund "manufacture and marketing".

23 It is common ground that the capital raised by PVI as a result of the Memorandum was $100,000, which is well short of the $500,000 PVI sought.

24 It is important to note that the agreement between PVI and Fairlight.Au authorised PVI to sell only two particular products under the Fairlight name, viz. the CMI-30A and the Series IV, which was also referred to in the Memorandum as the "Naked CMI-30A". It is the CMI-30A and the Series IV that are referred to in the agreement as "the CMI Products". Edmonds J held at [34] that the agreement granted PVI a licence to use the FAIRLIGHT mark only in relation to these products.

25 It is common ground that the only CMI Product (as defined in the agreement) produced by PVI was the Fairlight CMI-30A. In total, there were 14 of these sold, about 10 of which were ordered in or about March 2011.

26 Leaving aside the Fairlight Apps, none of what Mr Vogel described as "follow on" products (ie. the Fairlight Father, the Fairlight Unity or the CMI-55 Module) referred to in the Memorandum were ever produced.

Damages for Repudiation

Background

27 PVI contended that the repudiation of the agreement resulted in a loss of sales of products that were waiting to be dispatched at the time of the repudiation for which PVI should be compensated, as well as the loss of the chance to profit from further performance of the agreement. The total amount claimed by PVI on this basis is approximately $9.5 million (exclusive of interest).

28 PVI contended that if the Court was not satisfied that the agreement would have proved profitable, then it was entitled to recover reliance damages which it calculated at approximately $1.28 million (exclusive of interest).

29 I was referred by Mr Sirtes SC to the written submissions that were relied on by PVI in the Full Court. As mentioned, PVI was represented by counsel before the Full Court by whom those submissions were prepared. In PVI's outline of submissions in chief to the Full Court the claim for damages for breach of contract was put as follows:

46. The appellant claims $1,196,929 in damages for breach of contract, summarised as: (a) $977,210 in reliance damages; (b) $219,719 in costs of mitigation.

47. The reliance damages component is comprised of: (a) $504,635 in general reliance damage; (b) $472,575 in research and development costs thrown away.

48. The $219,719 costs of mitigation are simply the value of refunds to customers who purchased a CMI-30A, as calculated by the respondents' expert.

(footnotes omitted)

30 Fairlight.Au argued in its written submissions to the Full Court that the claim for reliance damages was not sustainable for a number of reasons including, at para 7(b) of its written submissions, that PVI sought expectation damages on the basis that it was possible to predict what position PVI would have been in had the contract been performed and that PVI had no basis to also claim reliance damages.

31 The response to this submission in PVI's written submissions in reply was unequivocal. PVI said (at para 32) that it "… no longer pursues any claim for expectation damages … [a]ccordingly, there is nothing to preclude it from seeking reliance damages."

32 A real question arises as to whether PVI should now be permitted to maintain a claim for expectation loss given its submissions to the Full Court. Although the Full Court did not decide the damages issues, it is apparent that the appeal was conducted on the basis that PVI did not make any claim for expectation damages.

33 In any event, it is extremely unlikely that PVI would have ever made a profit from the agreement. This is because most of the projected revenue referred to in the Memorandum is attributable to sales of other products that were not the subject of the licence referred to in clause 4 of the agreement. Sales of these additional projects were included in the revenue projections apparently on the assumption that permission would be obtained from Fairlight.Au to use the Fairlight name in relation to those products at some time in the future. However, there was no evidence to suggest that there was any prospect of PVI obtaining that permission. By 30 May 2012, Fairlight.Au was not even prepared to allow PVI to use the Fairlight name on the CMI products.

The Relevant Principles

34 In Commonwealth of Australia v Amann Aviation Pty Limited (1991) 174 CLR 64 Mason CJ and Dawson J said at pp 80-81:

The general rule at common law, as stated by Parke B. in Robinson v. Harman [(1848) 1 Ex 850, at p 855 [154 ER 363, at p 365]], is "that where a party sustains a loss by reason of a breach of contract, he is, so far as money can do it, to be placed in the same situation, with respect to damages, as if the contract had been performed". This statement of principle has been accepted and applied in Australia [See Wenham v. Ella (1972) 127 CLR 454, at p 471, per Gibbs J].

The award of damages for breach of contract protects a plaintiff's expectation of receiving the defendant's performance. That expectation arises out of or is created by the contract. Hence, damages for breach of contract are often described as "expectation damages". The onus of proving damages sustained lies on a plaintiff and the amount of damages awarded will be commensurate with the plaintiff's expectation, objectively determined, rather than subjectively ascertained. That is to say, a plaintiff must prove, on the balance of probabilities, that his or her expectation of a certain outcome, as a result of performance of the contract, had a likelihood of attainment rather than being mere expectation.

In the ordinary course of commercial dealings, a party supplying goods or rendering services will enter into a contract with a view to securing a profit, that is to say, that party will expect a certain margin of gain to be achieved in addition to the recouping of any expenses reasonably incurred by it in the discharge of its contractual obligations. It is for this reason that expectation damages are often described as damages for loss of profits. Damages recoverable as lost profits are constituted by the combination of expenses justifiably incurred by a plaintiff in the discharge of contractual obligations and any amount by which gross receipts would have exceeded those expenses. This second amount is the net profit.

The expression "damages for loss of profits" should not be understood as carrying with it the implication that no damages are recoverable either in the case of a contract in which no net profit would have been generated or in the case of a contract in which the amount of profit cannot be demonstrated. It would be an invitation to the repudiation of contractual obligations if the law were to deny to an innocent plaintiff the right to recoupment by an award of damages of expenditure justifiably incurred for the purpose of discharging contractual obligations simply on the ground that the contract breached would not have been or could not be shown to have been profitable. If the performance of a contract would have resulted in a plaintiff, while not making a profit, nevertheless recovering costs incurred in the course of performing contractual obligations, then that plaintiff is entitled to recover damages in an amount equal to those costs in accordance with Robinson v. Harman, as those costs would have been recovered had the contract been fully performed. Similarly, where it is not possible for a plaintiff to demonstrate whether or to what extent the performance of a contract would have resulted in a profit for the plaintiff, it will be open to a plaintiff to seek to recoup expenses incurred, damages in such a case being described as reliance damages or damages for wasted expenditure.

35 Mason CJ and Dawson J continued at pp 85-86:

An award of damages for expenditure reasonably incurred under a contract in which no net profit would have been realized, while placing the plaintiff in the position he or she would have been in had the contract been fully performed, also restores the plaintiff to the position he or she would have been in had the contract not been entered into. In this particular situation it will be noted that there is a coincidence, but no more than a coincidence, between the measure of damages recoverable both in contract and in tort.

It should be observed that, in a case where it is not possible to predict what position a plaintiff would have been in had the contract been fully performed, as was the case in both McRae and Anglia Television, it is not possible as a matter of strict logic to assess damages in accordance with the principle in Robinson v. Harman. But the law considers the just result in such a case is to allow a plaintiff to recover such expenditure as is reasonably incurred in reliance on the defendant's promise. In this case, the law assumes that a plaintiff would at least have recovered his or her expenditure had the contract been fully performed. It will still be open to a defendant, however, to argue that, notwithstanding the fact that it is impossible to assess what profits, if any, the plaintiff would have made had the contract been fully performed, the expenditure claimed by a plaintiff would nevertheless not have been recovered even if, to use the examples of McRae and Anglia Television, the tanker had existed or the defendant actor, Oliver Reed, had participated in the production of the film. In essence, such an argument is to the effect that, far from being impossible to predict what the result of the contract would have been, if fully performed, it is possible to demonstrate that performance of the contract would not even have resulted in the recovery by the plaintiff of reasonable expenses incurred.

36 Their Honours said at p 89:

[A] plaintiff has a prima facie case for recovery of wasted expenditure once it is established that the expense was incurred in reliance on the promise of the party in breach, there being a failure of performance by that party.

37 Brennan J said at pp 104-108:

Where a contract has been rescinded for breach, the amount which a plaintiff has reasonably expended in reliance on the defendant's promise and which is wasted by reason of the defendant's breach of his promise is a proper subject of damages for breach of contract [McRae v Commonwealth Disposals Commission (1951) 84 CLR at pp 412, 414]. Damages assessed for wasted expenditure incurred in reliance on the defendant's promise may be described as reliance damages to distinguish them from damages assessed for loss of the benefits which the plaintiff expected from performance of the contract (expectation damages). A plaintiff who seeks to recover reliance damages must ordinarily prove that the net value of the benefits to which he would have been entitled if the contract had been performed ($B - $y) would have exceeded the wasted expenditure incurred in reliance on the defendant's promise ($x) and, to the extent that he fails to do so, his claim will fail. To discharge the onus of proof, however, the plaintiff may be able to raise and rely on an inference that a party would not incur expenditure in reliance on the other party's promise without a reasonable expectation that, on performance of the contract, the expenditure would be recouped. That is an inference of varying strength according to the circumstances. Sometimes, the inference would be of sufficient strength to enable the plaintiff to discharge the onus; sometimes, the inference would be too weak.

However, when a contract is rescinded for breach and that breach, by preventing the performance of the contract, has made it impossible for the plaintiff to prove that the net value of his contractual benefits ($B - $y) exceeds the wasted expenditure incurred in reliance on the defendant's promise prior to rescission ($x), it is just to shift to the defendant the ultimate onus of proving that, had the contract been performed, the net value of the plaintiff's benefits would not have covered the expenditure he had incurred before rescission.

…

The sufficient and necessary justification for shifting the onus to the party in breach in the assessment of damages for wasted expenditure incurred in reliance on the defendant's promise before rescission for breach is that the breach of the contract itself makes it impossible to undertake an assessment on the ordinary basis.

…

A plaintiff's inability to quantify his lost benefits is no justification by itself for casting on the defendant an onus to prove that the plaintiff would not have recouped reliance damages had the contract been performed. What justifies the reversal of the onus is the defendant's repudiation or breach which denies, prevents or precludes the existence of circumstances which would have determined the value of the plaintiff's contractual benefits.

…

Where justification for reversing the onus exists, reliance damages may be recovered; absent that justification, the plaintiff must recover expectation damages, if any, by proof of the value of benefits and the cost of performance; that is, by proof that $B - $y is greater than $x. These are alternative methods of assessing damages, but the plaintiff does not have an election as to the method. The plaintiff who seeks recovery of reliance damages must show that justification for reversing the onus of proof exists. Otherwise, he must endeavour to prove his damages on the ordinary basis.

38 Gaudron J said at pp 155-156:

It is also clear … that damages which are assessed by reference to wasted expenditure are awarded to compensate for loss of contractual rights or loss of profits and, despite any coincidence in effect, not to put the contracting party in the position in which he or she would have been if the contract had not been made. It follows that any loss which would have been involved in performing the contract must be brought to account. Were it otherwise, the plaintiff would be put in a better position than if the contract had been performed. It also follows that it is not correct to characterize damages assessed by reference to wasted expenditure as damages to be claimed by election or in the alternative to damages for loss of profits. However, as damages are assessed on that basis because the contract would not have produced a profit or it is impossible to prove what the profit would have been, it may be expected that a claim for wasted expenditure will ordinarily be framed as an independent claim or in the alternative to a claim for damages for loss of profits.

Once it is appreciated that damages assessed by reference to wasted expenditure are awarded to compensate for the loss of contractual rights or for loss of profits, it is apparent that what is involved is an assumption that the loss is no less than that which has been outlaid and wasted by reason of repudiation or breach. An assumption to that effect is no more than the recognition of the ordinary expectations of the world of commerce that the value of a contract will be no less than the cost of its performance. That assumption necessarily contemplates that damages will include preliminary expenses, as was held in Anglia Television.

The assumption which underlies the award of damages by reference to wasted expenditure, like all assumptions, is one which, once made, will ordinarily be maintained unless displaced by evidence pointing to the contrary. In a practical sense that may mean that the assumption will often be made and maintained unless the defendant proves otherwise. However, save in that limited and practical sense, I do not think it right to say, as was held in C.C.C. Films Ltd. [[1985] QB, at p 40] that the onus is on a defendant "to prove that the expenditure ... is irrecoverable because [the plaintiff] would not have recouped [his] expenditure".

39 Deane J said at p 118:

The frequent inability of curial procedures to determine with certainty what has happened in the past, let alone what would have been or what will be, necessarily gives rise to a need for a number of subsidiary rules governing the determination of the loss or injury which a plaintiff has actually sustained by reason of a wrongful act. One such subsidiary rule is that, even in an action for repudiation or breach of contract where damage is not an element of the cause of action, a plaintiff bears the onus of establishing the extent of his loss or injury on the balance of probabilities. To satisfy the requirements of that rule, a plaintiff must, if he is to recover more than a nominal amount in such an action, affirmatively establish assessable damage, that is to say, loss or injury which is capable of being measured in monetary terms. In many cases, proof of the full extent of the loss or injury sustained will involve establishing an evidentiary foundation for positive and detailed ultimate findings by the court upon the balance of probabilities. There are, however, cases where considerations of justice or the limitations of curial method render ultimate findings, about what would have been or will be, impracticable or inappropriate. In such cases, damages must be assessed on some basis other than findings about what would have ultimately happened if the repudiation or breach had not occurred or about the precise ultimate implications of the situation which exists after the repudiation or breach. In particular, it may be appropriate that damages be assessed by reference to the probabilities or the possibilities of what would have happened or will happen rather than on the basis of speculation that probabilities would have or will come to pass and that possibilities would not have or will not.

(citations omitted)

40 The High Court's decision in Amann was considered in Sellars v Adelaide Petroleum NL (1994) 179 CLR 332. The plurality said at p 349:

[W]here there has been an actual loss of some sort, the common law does not permit difficulties of estimating the loss in money to defeat an award of damages. The damages will then be ascertained by reference to the degree of probabilities, or possibilities, inherent in the plaintiffs succeeding had the plaintiff been given the chance which the contract promised.

This approach is not confined to contracts relating to games of chance, sporting contests or other competitions. Fink v. Fink concerned a contract to provide an opportunity for a reconciliation, breach of which was held to entitle the wife to damages. And there can be no doubt that a contract to provide a commercial advantage or opportunity, if breached, enables the innocent party to bring an action for damages for the loss of that advantage or opportunity. So, in The Commonwealth v Amann Aviation Pty Ltd, Mason CJ. and Dawson J. [at p 92], Brennan J. [at pp 102-104] and Deane J. [pp 118-119) concluded that a lost commercial advantage or opportunity was a compensable loss, even though there was a less than 50 per cent likelihood that the commercial advantage would be realized. Damages for breach of contract were assessed by reference to the probabilities or possibilities of what would have happened.

41 Their Honours also referred to the High Court's earlier decision in Malec v JC Hutton Pty Ltd (1990) 169 CLR 638. Their Honours said at pp 350:

In Malec v J C Hutton Pty Ltd ([(1990) 169 CLR 638], this Court drew a distinction between, on the one hand, proof of historical facts what has happened - and, on the other hand, proof of future possibilities and past hypothetical situations. The civil standard of proof applies to the first category but not to the second, particularly when it is necessary to determine future possibilities and past hypothetical situations for the purpose of assessing damages [pp 639-640, per Brennan and Dawson JJ; pp 642-643, per Deane, Gaudron and McHugh JJ].

In Malec, Deane, Gaudron and McHugh JJ. explained the way in which the matter is to be approached in these terms [at p 643]:

"If the law is to take account of future or hypothetical events in assessing damages, it can only do so in terms of the degree of probability of those events occurring .... But unless the chance is so low as to be regarded as speculative - say less than 1 per cent - or so high as to be practically certain - say over 99 per cent - the court will take that chance into account in assessing the damages. Where proof is necessarily unattainable, it would be unfair to treat as certain a prediction which has a 51 per cent probability of occurring, but to ignore altogether a prediction which has a 49 per cent probability of occurring. Thus, the court assesses the degree of probability that an event would have occurred, or might occur, and adjusts its award of damages to reflect the degree of probability."

…

Neither in logic nor in the nature of things is there any reason for confining the approach taken in Malec concerning the proof of future possibilities and past hypothetical situations to the assessment of damages for personal injuries. The reasons which commended the adoption of that approach in assessments of that kind apply with equal force to the assessment of damages for loss of a commercial opportunity, as the judgments in Amann acknowledge.

Damages for loss of profits – PVI's submissions

42 PVI submitted that the repudiation of the agreement by Fairlight.Au resulted in a loss of profit from sales of products waiting to be despatched at the time for which PVI must be compensated as well as the loss of the chance to profit from execution of its ongoing business plan. It argued that the loss of chance is compensable even if, on the balance of probabilities, it is more likely than not that the chance would not have come to fruition. It also argued that damages for deprivation of a commercial opportunity should be ascertained by reference to the Court's assessment of the prospects of success of that opportunity had it been pursued.

43 PVI further submitted that the most reliable measure of the likely profitability of its business was the Memorandum which provided an appropriate basis for estimating the profit lost as a result of Fairlight.Au's repudiation. The amount that PVI claimed as compensation for this loss was $5,077,918 which, it was said, would restore PVI to the position it would have been in two years after the repudiation if Fairlight.Au had performed its obligations under the agreement.

44 Mr Hood, the expert witness who gave evidence for Fairlight.Au, concluded that "there was no quantifiable loss of profits" which PVI could claim. This conclusion was primarily based on the actual sales of the CMI-30A made which, he said, cast doubt on the reliability of the sales projections contained in the Memorandum. In its submissions, PVI described this conclusion as "fatally flawed" because it did not take into account the reason for the poor sales of the CMI-30A which, it was submitted, was attributable to Fairlight.Au's failure to perform its obligations under the agreement.

45 As is clear from PVI's submissions, the primary evidence on which it relies to support its claim to having lost a valuable business opportunity as a result of Fairlight.Au's repudiation of the agreement was the Memorandum which, according to PVI, represented a credible business plan that was prepared well before the dispute the subject of this litigation first arose.

46 There are two main reasons why I do not think the Memorandum provides a credible basis for inferring that PVI's contract with Fairlight.Au may have proven profitable had it not been repudiated.

47 First, the reliability of the projections contained in the Memorandum is greatly diminished by the actual sales achieved compared to what was projected in the Memorandum. As previously mentioned, PVI's total CMI-30A sales numbered 14, about 10 of which were ordered in about March 2011, with very few sales being made after that time. There were no sales of the Series IV (or Naked CMI-30A).

48 Secondly, the projections in the Memorandum and, in particular, the statement of cash flows, was predicated on the ability of PVI to manufacture and sell a number of products under the Fairlight name that were not within the scope of the trade mark licence granted to PVI under the agreement.

49 As to the first of these points, PVI submitted that it could not meet its own sales projections due to Fairlight.Au's breaches of the agreement. The difficulty with this submission is that it was also made to Edmond J's who rejected it unequivocally. His Honour's finding that the evidence did not establish that Fairlight.Au was in breach of the agreement due to any delays that occurred in the delivery of computer software to PVI was not disturbed on appeal. This provides a complete answer to PVI's submission that the disparity between projected sales and actual sales of the CMI-30A should be disregarded on the basis that it was Fairlight.Au's breach of agreement that prevented PVI from selling more CMI Products than it actually did.

50 As to the second point, even if I was to accept that the projections in the Memorandum provided a reliable basis from which conclusions might be drawn as to potential profitability of PVI, it cannot be concluded that the loss claimed by PVI on the basis of such projections was attributable to Fairlight.Au's repudiation. This is because the cash flow forecasts in the Memorandum include the projected sales of the additional products not covered by the licence.

51 The cash flow projections for the period March 2011 to June 2014 included in the Memorandum project revenue attributable to the CMI-30A of $200,000 for the period March-June 2011 and $1,800,00 for the period June 2011-June 2012. They contemplate sales of 10 units in the initial March-June 2011 period followed by sales of another 90 units in the financial year ending June 2012. The projected cost of goods sold for the CMI-30A in the period March 2011-June 2012 totals $875,000 which equates to a gross profit from sales of $1,125,000.

52 The projected revenue included in the statement of cash flows includes nothing for sales of the Series IV in the initial period and sales of 104 such units, generating $315,000 of revenue, in the financial year ending June 2012. The cost of goods sold for the Series IV in the period June 2011-June 2012 totals $186,200 which equates to a gross profit of $128,800.

53 Hence, the projected gross profit from sales of the CMI Products during the period March 2011-June 2012 totalled $1,253,800. Expenses for the same period are shown in the statement of cash flows as slightly over $2,000,000. Even if these are assumed to be half what was projected, the earnings before interest, tax, depreciation and amortisation ("EBITDA") would be approximately $250,000 for the period March 2011 to June 2012. This may suggest that if the business had managed to manufacture and sell the CMI Products as projected in the Memorandum, the business may have been modestly profitable. But there are many assumptions underlying that conjecture. In particular, it assumes that the actual sales of the CMI Products were as projected, that the costs of goods sold was as projected, and that the indirect expenses would be approximately half what was projected.

54 In the result, I am not satisfied that PVI would have made a profit from the agreement. But it does not follow that PVI is not entitled to recover any damages in respect of Fairlight.Au's repudiation of the agreement. As I will explain, this is a case in which I am satisfied that PVI was likely to have recouped some additional portion of the expenditure incurred by it in the course of its performance of the agreement had the agreement not been repudiated by Fairlight.Au.

Reliance Damages – Fairlight.Au's submissions

55 Fairlight.Au made an overarching submission in respect of PVI's claim for reliance damages. It submitted that, having sought to prove and recover expectation or loss of profit damages, PVI was precluded from making any claim for reliance damages.

56 I confess to having had some difficulty following this submission. When pressed as to whether it was open to PVI to maintain claims for expectation damages or reliance damages in the alternative, Mr Sirtes SC submitted that it was not, apparently on the basis that PVI was precluded from doing so because it had elected to seek expectation damages.

57 It is true that a party cannot obtain an award of damages for both loss of profits and reliance damages. But this does not mean that a party cannot advance claims for expectation damages and reliance damages in the alternative. Gaudron J made this point very clearly in Amann at p 155. Although Brennan J said at p 108 that the plaintiff does not have an election to make as to the method of assessment, I do not take this to mean that a party cannot make alternative claims for damages for loss of profits and reliance damages. What his Honour was saying at p 108 was that the plaintiff must justify recovery of any reliance damages by showing that the defendant's repudiation "denies, prevents or precludes the existence of circumstances which would have determined the value of the plaintiff's contractual benefits." This is because the justification for allowing the plaintiff to recover reliance damages (or, more particularly, the reversing of the onus referred to by Brennan J) is that the defendant's repudiation of the agreement prevents the court from determining with certainty what position the plaintiff would have been in had the defendant fulfilled its contractual obligations.

58 Fairlight.Au also challenged PVI's reliance damages claim on other grounds raised in Mr Hood's expert reports. I deal with the various components of PVI's reliance damages claim and Mr Hood's responses to them in the next section of these reasons.

What is the proper measure of PVI's reliance damages?

Breakdown of PVI's reliance damages

59 PVI's written submissions included the following breakdown of its claim for reliance damages:

Mr Hood's reliance damages: | $508,724 |

Mr Hood's mitigation costs: | $209,860 |

Additional mitigation costs: | $66,484 |

R&D costs: | $472,575 |

Total reliance damages: | $1,257,643 |

60 In his first report Mr Hood calculated PVI's reliance damages (on various assumptions) at $508,724. This amount reflected what he referred to as "residual non-R&D costs". In a later report Mr Hood revised this figure to $504,635. The amount of $504,635 is slightly less than the figure referred to in PVI's breakdown, but in circumstances where PKT did not dispute any of the arithmetic underlying Mr Hood's revised calculation I propose to accept it.

61 As a matter of principle, and subject to some qualifications that I will return to, it is apparent that Mr Hood accepted that what he called "residual non R&D expenses" were properly recoverable as damages suffered by PVI as a result of Fairlight.Au's repudiation of the agreement.

62 The principal difference between the parties in relation to reliance damages relates to R&D costs. Mr Hood has excluded from his figure of $504,635 any amount expended by PVI on R&D. He calculated such expenditure to be $472,575, a figure which PVI accepted as correct in its submissions.

63 One reason why Mr Hood excluded the $472,575 from his reliance damages figure was that he could not be satisfied that the R&D expenses were solely related to the development of the CMI Products. However, he did accept, subject to his next point (which I will come to) that R&D expenses would be recoverable to the extent they related to the development of the CMI Products, assuming that Fairlight.Au's repudiation of the agreement rendered any resulting asset worthless.

64 The other point made by Mr Hood in relation to R&D expenditure was that it is by definition uncertain and, at the time the relevant expenditure was incurred, PVI could not know whether it would create anything of value. It was in this sense that he described it as a "black hole expense" or a "sunk cost".

65 I will first deal with Mr Hood's second point.

66 The R&D expenditure would not be recoverable if incurred by PVI irrespective of whether PVI had entered into the agreement. But in that situation the R&D expenditure would not be recoverable for the reason that it was not incurred for the purpose of performing the agreement, and therefore was not money lost as a result of Fairlight.Au's repudiation of the agreement. In essence, the question that arises is one of causation. If an innocent party is entitled to have damages for breach of contract assessed on a reliance basis, then it may be entitled to recover expenses incurred and wasted in reliance on the defaulting party's contractual promises under one or other limb of the rule in Hadley v Baxendale (1854) 9 Ex 341: see Amann at p 88 per Mason CJ and Dawson J. Hence, if the R&D expenditure was reasonably incurred by PVI for the purpose of performing the agreement, then I do not see why, as a matter of principle, it is not prima facie recoverable.

67 The first question in the present case is whether it can be said that the R&D expenditure was incurred in reliance on the Fairlight.Au's contractual promises. I think it should be inferred that PVI would not have incurred the R&D expenditure had it not entered into the agreement with Fairlight.Au. As I have explained, the use of the Fairlight brand was important to PVI's business plan. I do not think PVI would have incurred expenses developing the CMI Products without having obtained the right to market and sell those products under the Fairlight brand. Accordingly, I am satisfied that the R&D expenditure would not have been incurred in the absence of the agreement.

68 The second question is whether the reliance damages claimed are within the rule in Hadley v Baxendale. I am prepared to accept, as I think Mr Hood was, that R&D expenditure that related solely to the products the subject of the agreement would be recoverable under either the first or the second limb of the rule in Hadley v Baxendale. No submission to the contrary was made by Fairlight.Au.

69 Mr Hood made clear in his reports that he could not separate out the R&D costs that would enable him to say which of these may have been incurred in connection with the development of the CMI Products as opposed to any of the other products that were included in PVI's business plan and cash flow projects as set out in the Memorandum or other business activities in which Mr Vogel was involved. However, Mr Hood was able to determine from PVI's financial records that $31,088 of the R&D expenditure incurred by PVI related to the development of the Apps. PVI accepts that this amount should be excluded on the basis that it represents R&D expenditure on products not covered by the agreement.

70 In his affidavit of 28 October 2014, Mr Vogel said that the nett R&D expenditure relating solely to the CMI-30A was $478,053 In a later affidavit dated 17 November 2014 Mr Vogel referred again to the R&D expenditure of $478,053 relating to the CMI-30A which he said had been "thrown away". One of the difficulties I face in assessing this evidence is that the paragraphs in question were apparently the subject of an objection by Fairlight.Au, which, at its suggestion, Edmonds J was not required to rule upon.

71 Mr Vogel's evidence with regard to the R&D expenditure does not appear to have been challenged in his cross-examination. Nor did Mr Hood suggest that the R&D expenditure of $478,053 was excessive or unreasonable for the CMI Products. His point was that he could not be satisfied that the expenditure was solely related to the CMI Products. This point is in my view answered by Mr Vogel's unchallenged evidence.

72 As of March 2011 PVI was projecting that it would generate revenue of $2 million for sales of the CMI-30A period March 2011-June 2011 for a gross profit of $1.2 million, which equates to a gross profit margin of about 56%. With the benefit of hindsight, these sales forecasts were excessively optimistic. However, in the absence of evidence pointing to a different conclusion, it is not possible to characterise the R&D expenditure of $478,053 as unreasonable for products that were forecast to generate sales revenue of $2 million over a 15 month period.

73 It was submitted by Fairlight.Au that I could not be satisfied that the R&D expenditure did not produce anything of value that should be brought to account in determining whether the R&D expenditure was wholly or partly wasted.

74 Under the agreement PVI acquired rights to computer software developed by Fairlight.Au. However, the software was developed specifically for the CMI Products to be sold under the Fairlight name. In circumstances where the evidence indicates that there was only a very limited market (much smaller than projected) for the CMI Products I would not attribute anything more than a nominal value to the software. Moreover, Mr Vogel gave evidence that does not appear to have been challenged that the computer software was of no value to PVI because it was not supplied with all of the relevant source code. Further, he said that the software requires Fairlight.Au's Crystal Core hardware to function, which Fairlight.Au has not been willing to supply to PVI since May 2012. This evidence, which was not challenged in cross-examination, should be accepted. In my view it provides a complete answer to Fairlight.Au's submission.

Mitigation costs

75 To understand this aspect of PVI's claim it is necessary to refer to the particulars of loss and damage that were included in PVI's cross-claim. These particulars referred to "[m]itigation costs (to service existing customers)" of $780,000 made up as follows:

"Cost of developing alternative to CC-1/SX12 (conservative est)" $500,000

"Cost of developing alternative software (conservative est)" $200,000

"Retrofit alternative to CC-1/SX12 to 20 existing systems $4,000 each" $80,000

76 Mr Hood dealt with this aspect of PVI's claim in Section 6.3 of his report dated 24 June 2014 as follows:

6.3 Mitigation Costs

6.3.1 In assessing the cost to service existing customers, I note from the sales ledger [PVI 13.012] that total sales for the CMI-30A and related components in the period of 2011 and 2012 was $209,875, with subsequent sales of $61,900 (a combined total of $271,775).

6.3.2 One would hypothesize that, rather than pursue the cost of developing alternative software and retrofitting systems (at an unsubstantiated theoretical cost of $780,000) it would be prudent in mitigating losses to simply provide a full refund to customers minimizing costs to $219,719.

6.5.5 If one was to assume that the result of R&D expenditure was knowledge capable of being leveraged in future, incurring development costs for an alternative to the CC-1/SX12 and software may be rational (subject to a market for the products existing in the future). Should that be the case, then the market value of the software/firmware required could be the $200,000 that Fairlight was willing to provide software for in the original agreement, plus nominal licensing costs.

6.3.4 The evidence and history of sales (prior to any problems materializing) is overwhelmingly lower than anticipated in the IM (document PVl.12.012), being:

Anticipated | Actual | % of anticipated | |

Sales in the period Mar 11 to Jun 11 | $274,400 | $150,270 | 55% |

Sales in the period Jul 11 to Jan 12 | Approx. $2,145,075 | $30,284 | 1.4% |

6.3.5 Rational management may chose to discontinue the enterprise rather than continue to invest in, and create, a product which, the sales data suggests, the market may not have embraced.

77 It can be seen that Mr Hood describes the claim for mitigation costs in para 6.3.2 as (inter alia) "unsubstantiated". Mr Vogel responded to Mr Hood's report in an affidavit of 28 October 2014. In that affidavit Mr Vogel said (at para 84):

In relation to mitigation costs, I agree with Mr Hood (6.3.2) the most rational mitigation strategy would be to refund customers. 14 sales have been made and cost of refunds would be $308,000 including costs such as duties and freight, averaging about $5,000 per sale.

78 There is no suggestion that PVI has ever refunded any money to customers, that it has ever been asked to do so, or that it is liable to do so. Mr Hood addressed refund costs from a theoretical perspective when observing that it would have been more prudent for PVI to have provided refunds to a relatively small number of customers who purchased the CMI-30A rather than developing new software. Mr Hood's observation did not relieve PVI of the need to prove what costs is incurred in mitigating its loss, though it may have provided some basis for declining to award anything more than $219,719 in respect of PVI's reasonable mitigation costs.

79 Mr Hood was correct to say that the claims for mitigation costs were unsubstantiated. I was not referred to any evidence that could support a finding that PVI spent $780,000 or any other amount on mitigation costs at least not in addition to the residual non-R&D costs and the R&D costs also claimed by PVI. Even if I was to assume that PVI incurred costs developing an alternative to the CC-1/SX12 or some alternative software, there is no evidence to indicate that these costs did not form part of the expenditure that formed part of the R&D expenditure to which I have already referred. Similarly, there is no evidence to indicate that the costs of retrofitting the CC-1/SX12 to 20 existing systems (even though the evidences shows only 14 CMI-30A's were sold) was not accounted for in the $504,635 residual non-R&D expenses already allowed.

80 The final point to make in relation to this aspect of PVI's claim is that the lack of particularity (not to mention evidence) to support it makes it impossible to know precisely when those costs are alleged to have been incurred. But if it is assumed that they were largely incurred to enable the CMI-30A to be shown at the 2011 NAMM show that took place in California in January 2011, then it is difficult to see how this expenditure could be recoverable on the basis that it was reasonably incurred to mitigate loss inflicted by Fairlight.Au's breach of contract. I say this because there was no breach of contract proven against Fairlight.Au and the repudiation entitling PVI to terminate the agreement and sue for damages for breach of contract did not occur until May 2012.

Additional mitigation costs

81 In its written submission PVI claimed a further amount of $66,484. According to PVI, Mr Hood's calculation omitted additional mitigation costs "expended in a failed attempt to modify the software to work without the components Fairlight.Au refused to supply."

82 This aspect of PVI's claim was dealt with in Mr Vogel's affidavit of 5 September 2013. In that affidavit he says that R&D expenditure on CMI-30A during the 2012-2013 financial year was approximately $63,000 but that PVI's amount was still to be verified by PVI's accountant. He returned to this topic in his affidavit of 27 November 2017, producing a spreadsheet and invoices said to total $66,484. Mr Vogel says that these invoices relate to expenses incurred by PVI in developing an alternative to the Fairlight.Au software and hardware. He also said in his affidavit that PVI ran out of money before it could complete this development.

83 I am satisfied that some award should be made in respect of these additional mitigation costs. However, as with R&D expenditure for 2011 and 2012, it is necessary to make an allowance for R&D tax incentives received during the relevant years. The evidence shows that for the 2013 financial year this amounted to $29,918. Accordingly, I am satisfied that I should allow $36,566 in respect of the additional mitigation costs.

Loss of Opportunity Analysis

84 I am satisfied that PVI incurred further expenditure of $981,299 that might qualify for recovery as wasted expenditure. However, to award damages for the whole of this amount would be unjust. This is because it is highly unlikely that PVI would have recouped all of this expenditure if Fairlight.Au had not repudiated the agreement.

85 As I have explained, the licence to use the Fairlight name on CMI Products supplied, or to be supplied, by PVI was validly terminated in May 2012 with the consequence that PVI could no longer lawfully sell any CMI Products under or by reference to the Fairlight name. Moreover, the actual sales of CMI Products made by PVI in the period March 2011 to May 2012 were much less than projected in the Memorandum. Only 14 CMI-30A units were sold. At $20,000 per unit, that amounts to total sales of only $280,000 compared to projected sales of $2,000,000 for the period March 2011 to June 2012. The market for the CMI Products, or at least the CMI-30A, did not prove to be anywhere near as large as PVI expected.

86 PVI submitted that it would have been open to PVI to supply the CMI Products under a different name but still capitalise on Mr Vogel's reputation as the designer of the original Fairlight CMI. In its submissions Fairlight.Au sought to dismiss this possibility on the basis that it was contrary to the Memorandum which emphasised (at least implicitly) the importance of the Fairlight name to the business plan.

87 I do not accept that there would have been no market for the CMI Products if sold by PVI under a different name. The evidence of Mr Vogel's reputation as the designer of the original Fairlight CMI indicates that his name and reputation were closely associated with the Fairlight musical instruments by persons likely to be interested in acquiring the CMI-30A. Even so, I consider it highly unlikely that PVI would have sold enough CMI Products under a different name to fully recoup all of its expenditure.

88 I am satisfied that there would have been some market for the CMI Products that it was open to PVI to exploit after May 2012 using a different product name. It is not possible to say how substantial that market was likely to be. What is clear, however, is that it would have been much smaller than anticipated by the Memorandum.

89 What PVI's actual sales of CMI Products would have been if Fairlight.Au had not repudiated the agreement is impossible to say. But if, for example, it was assumed that PVI sold additional CMI Products (both the CMI-30A and the Naked CMI-30A) to the value of $750,000 at a gross profit margin of 40% (ie. less than was projected), that may well have allowed PVI to recoup expenditure in the amount of $300,000 depending on how those sales affected the overheads (ie. indirect expenses) of the business.

90 The present case is one in which the observations of Deane J in Amann at p 118 should be applied. To require proof on the balance of probabilities of what further sales of CMI Products would have been made by PVI were it not for Fairlight.Au's repudiation of the agreement would be impractical and unjust. Rather, it is appropriate in this case to assess damages by reference to the value that should be attributed to PVI's loss of the opportunity to recover at least some significant portion of PVI's expenditure. In the circumstances of this case, where I am required to assess damages based on a largely hypothetical state of affairs, I think this is the most appropriate approach to take. I regard it as consistent with the decisions in Malec, Amann and Sellars.

91 I accept that my assessment of PVI's loss involves a degree of speculation and guesswork, but this is unavoidable: see Sellars per Brennan J at p 364 citing Enzed Holdings Ltd v Wynthea Pty Ltd (1984) 57 ALR 167 at p 183.

92 I will allow a percentage of the wasted expenditure claimed (excluding mitigation costs) which reflects my assessment of the value of the lost opportunity. In my view an appropriate percentage figure is 30% which yields a figure of $294,390 (ie. 30% of $981,299). This figure reflects my view that, while the prospects of PVI recovering all of its expenditure were extremely low, the opportunity to recover at least some of that expenditure that was lost was not insignificant and of considerable value to PVI given Mr Vogel's reputation, and the time, effort and money that had been already spent on research and development for the CMI Products as of May 2012.

93 The total damages to be awarded to PVI in respect of Fairlight.Au's repudiation of the agreement are therefore $330,956.

Damages for Copyright Infringement

Background

94 The Full Court considered PVI's appeal against Edmonds J's rejection of PVI's copyright case at [71]-[84]. In those paragraphs the Full Court said:

[71] The primary judge's reasons at [125]–[137] included the following findings relevant to this ground:

(a) that the Agreement in clauses 20 and 22 did not operate to convey copyright in the software developed by Fairlight pursuant to the Agreement;

(b) that no other evidence adduced at trial established PVI's entitlement to ownership of the software;

(c) that there was no evidence that Fairlight had, without the licence of PVI, reproduced a substantial part of any copyright work owned by PVI; and

(d) that PVI had failed to supply any evidence of sales or copying by Fairlight such that it would allow the Court to award damages as a consequence of the alleged infringement.

[72] PVI contests each of these findings. A further relevant finding, which PVI does not contest, is that by April 2012, PVI had made all of the payments totalling $200,000 which were required by clauses 6 and 7 of the Agreement.

[73] PVI submits that the Agreement sufficiently operated as an assignment of Fairlight's future copyright, which is permissible pursuant to s 197 of the Copyright Act 1968 (Cth). It submits that evidence of ownership beyond the terms of the Agreement was present in the form of admissions made by the respondent, particularly when read in context with the evidence of the Chief Technical Officer of Fairlight, Mr Fibaek, to the effect first, that the software had been assigned to PVI, and secondly, that this software had been reproduced by Fairlight.

[74] Fairlight contended that clauses 20 and 22 of the Agreement were insufficient to convey title to PVI given the second sentence of clause 20 which said "[t]he exact definition of IP to be transferred will be defined in a separate document". It submitted that the purpose of the "exact definition" was to make clear that generic or third party proprietary software, not written by Fairlight, was to be identified as not included within the assignment. For this purpose a further document was required to complete the terms of the copyright assignment. Fairlight further submitted that the admissions made in the defence to the cross-claim were inadequate to discharge the onus upon PVI to prove either ownership or substantiality of reproduction necessary to establish copyright infringement.

Consideration

[75] In our view, this ground of appeal should be upheld.

[76] First, as a matter of construction, as we have noted above, there is no doubt that the parties had a clear intention that such software as Fairlight developed for the project was assigned to PVI upon receipt of the final payment of $200,000. That payment was made in April 2012. On a factual level, the need for exact definition arose because certain third party or generic software may have been necessary to complete the project. There is no doubt, as a matter of fact, that whatever third party or generic software was to be excluded from the software assigned was an insignificant aspect of the bargain being struck by the parties. They agreed that all software created by Fairlight for PVI was assigned to it, and the terms of clauses 23–25 indicated that the parties were content to nominate a fee for the licence-back ("about $1,500 per license"). In our view the mechanical step of identifying that software did not preclude the completion of the assignment of the software which originally lay in the hands of Fairlight.

[77] Secondly, in its cross claim, PVI alleged that Fairlight had sold the software known as the "Sound Design Sampler (SDS)" which included software, the copyright in which had been transferred to PVI pursuant to the Agreement.

[78] In [24(c)] of its defence to the cross-claim, Fairlight admitted that:

(i) Fairlight's SDS included source code written for the CMI-30A;

(ii) Fairlight has provided a small number of SDS units and/or licences to third parties.

(iii) By letter dated 1 June 2012 from... [PVI, it said]:

"We would like [Fairlight] to continue to use our CMI code in their SDS products. This is also mutually beneficial."

(iv) In the circumstances set out in the preceding subparagraph, at all relevant times [PVI] knew of and authorised Fairlight's use and reproduction of CMI source code written for the CMI-30A project in Fairlight's SDS products;

...

[79] The pleading went on to assert that in the circumstances PVI was "estopped and precluded" from saying that its copyright had been infringed, because PVI had authorised that reproduction.

[80] Further, the evidence of Mr Fibaek served to clarify that the "small number" of SDS units or licences provided to third parties (referred to in (ii) above) included two licences supplied by Fairlight after April 2012 (being the date upon which the copyright assignment took effect). His evidence confirmed that the Dream II product included the SDS software.

[81] Mr Fibaek went on at [12]: