FEDERAL COURT OF AUSTRALIA

Zurich Australian Insurance Limited, in the matter of Zurich Australian Insurance Limited [2018] FCA 1567

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 17C(5) of the Insurance Act 1973 (Cth) (Act), the need for the applicants to comply with s 17C(2)(c) of the Act be dispensed with, insofar as it requires an approved summary of the Scheme the subject of this proceeding to be given to holders of New South Wales motor vehicle compulsory third party (CTP) insurance policies issued by the first applicant as insurer under the NSW motor accidents CTP insurance regime governed by the Motor Accidents Act 1988 (NSW), the Motor Accidents Compensation Act 1999 (NSW) and the Motor Accidents (Lifetime Care and Support) Act 2006 (NSW) (Zurich NSW CTP Policies):

(a) in respect of which policy there is no notified claim that is unsettled or otherwise outstanding;

(b) for whom the first applicant has no record of a current mailing address; or

(c) who cease to maintain a current mailing address with the first applicant after despatch of the Scheme Summary to holders of Zurich NSW CTP Policies,

on condition that Orders 2 to 5 below are complied with.

Mail-out

2. The first applicant carry out the following steps:

(a) Prior to the publication of the Notice of Intention referred to in Order 3 below and the release of the Scheme for public inspection as referred to in Orders 4 and 5 below, the first applicant cause to sent, by pre-paid mail, a summary in a form approved by the Australian Prudential Regulation Authority (APRA) (Scheme Summary) to the following persons (collectively, the Policyholders/Claimants):

(i) the persons (or their representatives) to whom the Zurich NSW CTP Policies were issued by the first applicant and in respect of each such policy there is a notified claim that is unsettled or otherwise outstanding;

(ii) the claimants (or their representatives) who have a notified claim that is unsettled or otherwise outstanding in respect of a Zurich NSW CTP Policy; and

(iii) the claimants (or their representatives) who have a notified compulsory third party insurance claim with the first applicant under the Nominal Defendant Scheme,

for whom the first applicant has current mailing addresses.

(b) In the event the Scheme Summary sent by the first applicant is returned undelivered before the date of the confirmation hearing and to the extent reasonably practicable, follow its returned mail procedure to identify the new mailing address for that Policyholder/Claimant and, if identified, resend the Scheme Summary to that new mailing address by pre-paid mail.

(c) If a new claim is made in respect of a Zurich NSW CTP Policy after the date of the mail-out in Order 2(a) but prior to a date two weeks before the confirmation hearing, send the Scheme Summary by pre-paid mail to:

(i) the claimant (or their representative); and

(ii) if the claimant is not the policyholder, the policyholder of that Zurich NSW CTP Policy;

(d) If a new claim is made with the first applicant under the Nominal Defendant Scheme after the date of the mail-out in Order 2(a) but prior to a date two weeks before the confirmation hearing, send the Scheme Summary to the claimant (or their representative) by pre-paid mail.

(e) Prior to the publication of the Notice of Intention and the release of the Scheme for public inspection, send the Scheme Summary by courier to the following counterparties (other than the first applicant) to the following deeds:

(i) in respect of the "Insurance Industry Deed" contained in the Motor Accidents Compensation Act 1999 (NSW), to the Attorney General of the State of New South Wales for and on behalf of Her Majesty Queen Elizabeth the Second in right of the State of New South Wales, the Motor Accidents Authority of New South Wales (now SIRA), AAI Limited (trading as AAMI and GIO), Allianz Australia Insurance Limited, CIC Allianz Insurance Limited, Insurance Australia Limited (trading as NRMA Insurance), and QBE Insurance (Australia) Limited;

(ii) in respect of the "Deed Providing For The Sharing of Claims in the Australian Capital Territory and New South Wales" entered into in 1990 between certain licensed compulsory third party insurers to provide for and regulate the sharing of claims involving motor vehicles insured under the laws of the Australian Capital Territory or New South Wales to SIRA, Allianz Australia Insurance Limited, CIC Allianz Insurance Limited, Insurance Australia Limited (trading as NRMA Insurance), QBE Insurance (Australia) Limited, AAI Limited (trading as AAMI and GIO), and Australian Pensioners Insurance Agency Pty Ltd (Apia) as agent for AAI Limited; and

(iii) in respect of the "Deed Providing For The Sharing of Claims in Queensland and New South Wales" dated 27 November 1990 between certain licensed compulsory third party insurers licensed to provide for and regulate the sharing of claims involving motor vehicles insured under the laws of Queensland or New South Wales, to SIRA, AAI Limited (trading as Suncorp Insurance, GIO and AAMI), Allianz Australia Insurance Limited, CIC Allianz Insurance Limited, RACQ Insurance Limited (trading as RACQ Insurance), Insurance Australia Limited (trading as NRMA Insurance), and QBE Insurance (Australia) Limited.

Publication

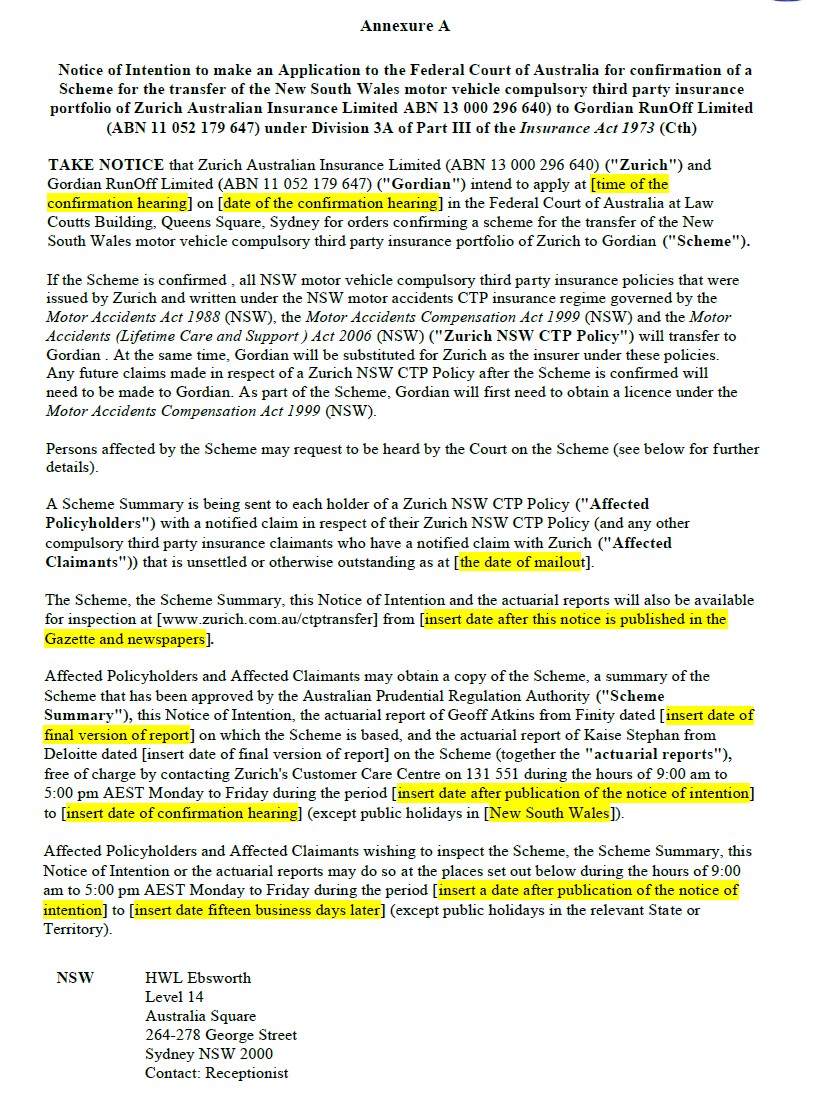

3. The first applicant publish a Notice of Intention substantially in the form of Annexure A to these orders in the following publications before the documents referred to in Order 4 below are made available for inspection, by 5 December 2018 or such later date as the Court permits:

(a) the Government Gazette;

(b) The Australian Financial Review;

(c) The Australian;

(d) The Sydney Morning Herald;

(e) The Courier Mail; and

(f) The Canberra Times.

Inspection

4. After the publication of the Notice of Intention until the date of the confirmation hearing, the first applicant maintain a link to a "www.zurich.com.au/ctptransfer" webpage on the first page of the first applicant's website, www.zurich.com.au, containing telephone numbers for the first applicant's Customer Care Centre and access to the following documents (Inspection Documents):

(a) Notice of Intention;

(b) the Scheme;

(c) the Scheme Summary;

(d) the actuarial report of Geoff Atkins from Finity in final form, on which the Scheme is based; and

(e) the actuarial report of Kaise Stephan from Deloitte in final form, on the Scheme.

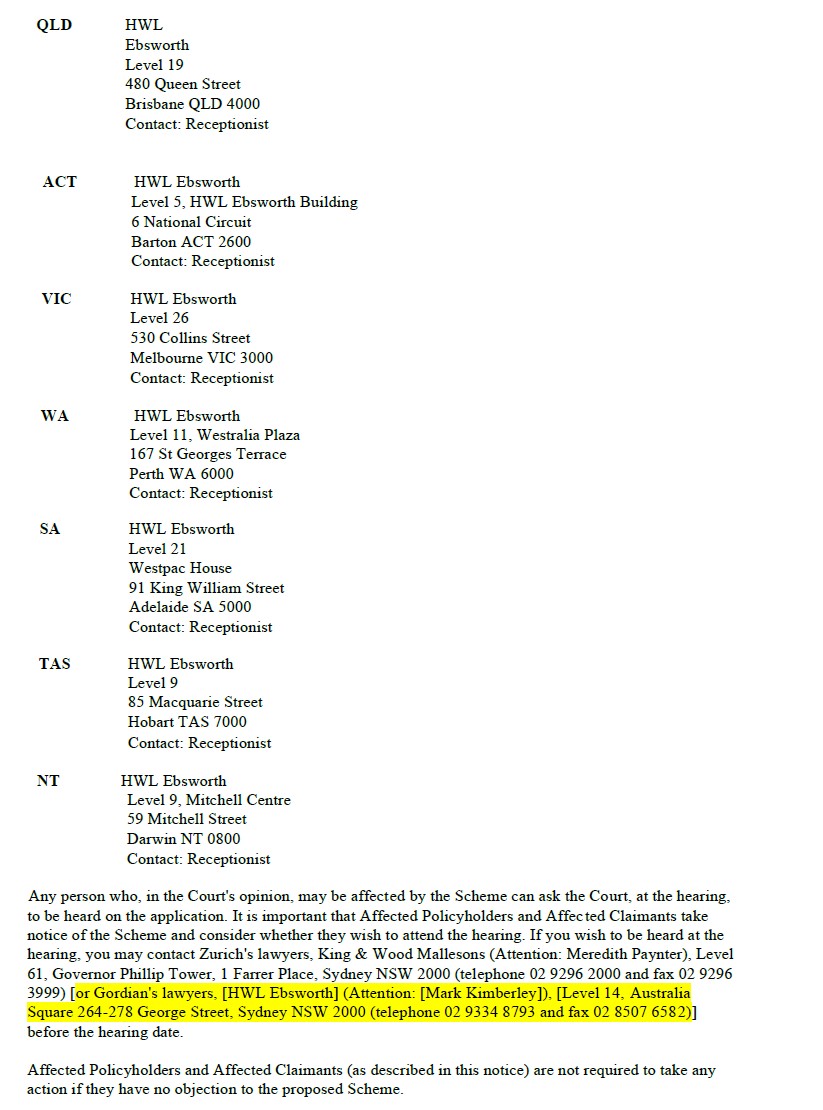

5. After publication of the Notice of Intention, make available for inspection the Inspection Documents between 9.00 am and 5.00 pm, Monday to Friday, for 15 business days at the following locations:

(a) HWL Ebsworth in Sydney (NSW);

(b) HWL Ebsworth in Brisbane (QLD);

(c) HWL Ebsworth in Canberra (ACT);

(d) HWL Ebsworth in Melbourne (VIC);

(e) HWL Ebsworth in Perth (WA);

(f) HWL Ebsworth in Adelaide (SA);

(g) HWL Ebsworth in Hobart (TAS); and

(h) HWL Ebsworth in Darwin (NT).

6. On request, provide a copy of the Inspection Documents to Policyholders/Claimants free of charge.

7. The applicants pay APRA's costs of the proceeding to date as agreed or assessed.

8. There be liberty to apply.

9. The parties have liberty to approach the Associate to Yates J for a date for the hearing to confirm the Scheme (the confirmation hearing).

10. These orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

YATES J:

Introduction

1 The applicants have commenced this proceeding to seek the Court’s confirmation under s 17F(1) of the Insurance Act 1973 (Cth) (the Act) of a proposed scheme in relation to the transfer of the New South Wales motor vehicle compulsory third-party (CTP) insurance portfolio of the first applicant, Zurich Australian Insurance Limited (Zurich), as insurer under the New South Wales motor accidents CTP insurance regime governed by the Motor Accidents Act 1988 (NSW) (MAA), the Motor Accidents Compensation Act 1999 (NSW) (MACA), and the Motor Accidents (Lifetime Care and Support) Act 2006 (NSW) (the CTP portfolio). The transfer will be to the second applicant, Gordian RunOff Limited (Gordian).

2 Section 17C(2)(c) of the Act requires an approved summary of the scheme to be given to “every affected policyholder” before an application for confirmation under s 17F(1) is made. The present application is to dispense with that requirement to the extent that it requires the approved summary to be given to policyholders:

(a) in respect of policies for which there are no unsettled or otherwise outstanding, notified claims;

(b) for whom Zurich has no record of a current mailing address; or

(c) who cease to maintain a current mailing address with Zurich after dispatch of the scheme summary.

3 The applicants seek orders providing for an alternative notification procedure, as a condition of the dispensation that is sought. Under this procedure, it is proposed that, where it has a current mailing address, Zurich will send the approved summary by pre-paid mail to:

(a) each policyholder in respect of whose policy there is a notified claim that is unsettled or remains outstanding;

(b) each claimant who has notified a claim that is unsettled or remains outstanding; and

(c) each claimant who has notified a CTP insurance claim with Zurich under the Nominal Defendant Scheme.

4 In the case of returned mail, Zurich will invoke its returned mail procedure with the aim of identifying a new mailing address to which the approved summary will be sent. In the case of new claims after the date of the mail-out, Zurich will send the approved summary to the claimant and the policyholder.

5 The proposed alternative notification procedure also provides that Zurich will:

(a) send the approved summary by courier to certain counterparties to deeds into which Zurich has entered (namely, the Insurance Industry Deed contained in the MACA, the Deed Providing For The Sharing of Claims in the Australian Capital Territory and New South Wales entered into by certain licensed compulsory third-party insurers to provide for and regulate the sharing of claims involving motor vehicles insured under the laws of the Australian Capital Territory or New South Wales, and the Deed Providing For The Sharing of Claims in Queensland and New South Wales, entered into by certain licenced compulsory third-party insurers to provide for and regulate the sharing of claims involving motor vehicles insured under the laws of Queensland or New South Wales);

(b) publish the notice of intention in the Government Gazette and certain identified newspapers circulating either nationally or locally in New South Wales, Queensland, and the Australian Capital Territory;

(c) maintain a website through which documents (the notice of intention, the scheme, the approved summary and two actuarial reports) (the Inspection Documents) can be accessed; and

(d) provide, in the capital city of each State, the Australian Capital Territory and the Northern Territory, an office in which the Inspection Documents will be made available for inspection on request.

Evidence

6 The following affidavits were read in support of the present application:

(a) Cathy Anne Manolios, sworn 3 October 2018;

(b) Sandra O’Sullivan, sworn 8 October 2018; and

(c) Hilary Janette Bates, affirmed 16 October 2018.

Background

7 Zurich is an Australian general insurance company authorised under s 12 of the Act. It also holds a licence granted under Div 1 of Pt 8 of the MAA, which is taken to be a licence granted under Pt 7.1 of the MACA. It is part of the Zurich Australia group of companies of which Zurich Financial Services Australia Limited is the holding company.

8 Zurich has issued a range of general insurance products, including the CTP policies the subject of this proceeding (the Zurich NSW CTP policies). Zurich has not sold new Zurich NSW CTP policies since 30 September 2016. Its compulsory third-party activities in New South Wales are now dedicated to managing claims relating to the CTP portfolio rather than issuing new policies. The CTP portfolio was transitioned into run-off in November 2015. This reflected Zurich’s decision to focus on general insurance business lines in which it considered it had a distinct market position. The last period of insurance in respect of the policies issued as part of the CTP portfolio expired on 31 March 2017.

9 Gordian is authorised under s 12 of the Act to carry on the business of general insurance run-off.

10 By a series of agreements entered into on 23 February 2018, Zurich and entities referred to in the evidence as the Enstar parties (including Gordian) agreed to transfer the CTP portfolio to Gordian by way of confirmation of a scheme. They entered into arrangements in relation to the reinsurance and administration of the CTP portfolio pending completion of the transfer.

The scheme

11 Under the scheme, Zurich will transfer all its right, title and interest in, and all the risk in relation to, certain assets referred to as Transferring Assets, to Gordian. The Transferring Assets consist of Transferring Policies and Transferring Contracts.

12 The Transferring Policies are all contracts of insurance issued, entered into or assumed by Zurich in the conduct of the CTP portfolio business.

13 The Transferring Contracts consist of a contract under which Zurich had agreed to issue CTP policies insuring the New South Wales State Transit Authority (STA) bus fleet (the STA contract); a reinsurance agreement between Zurich and Cavello Bay Reinsurance Ltd (Cavello Bay) (one of the Enstar parties); the deeds referred to at [5(a)] above; and a trust deed between Zurich, Cavello Bay and NAB Trustee Services Limited.

14 Under the scheme, Zurich will transfer to Gordian, and Gordian will assume, all of Zurich’s Transferring Liabilities. These consist of all Zurich’s claims, losses, liabilities and costs under the Transferring Policies; all Zurich’s claims, losses, liabilities and costs under the Transferring Contracts; and certain monetary obligations and liabilities referred to in the evidence as the SND Obligations.

15 On implementation of the scheme, each CTP policyholder will continue to have the same rights against Gordian as were available against Zurich prior to the Transfer Time (proposed as 10 December 2018), and each CTP policyholder who has a claim on or obligation under a CTP policy will have the same claim on or obligation to Gordian in substitution for any claim on or obligation to Zurich.

16 All costs and expenses incurred by Zurich and Gordian in connection with the scheme and the proposed transfer will be borne by the parties and not by the policyholders of Zurich or Gordian.

17 Cavello Bay has fully reinsured the CTP portfolio with effect from 1 January 2018. Therefore, 100% of the economic risk in respect of the portfolio has already been transferred. Zurich has ceased to have any net economic exposure to the portfolio, although it retains a gross exposure to, and remains ultimately responsible for, the portfolio as a matter of law, and in accordance with its regulatory obligations, until such time as the transfer is completed.

18 Further, on 15 June 2018, another Enstar party, Enstar Australia Limited, commenced providing claims handling and other administrative services in relation to the CTP portfolio. This was pursuant to an authorisation granted by SIRA on 1 June 2018.

The CTP portfolio

19 The CTP portfolio comprises CTP policies issued since 1989, primarily in respect of commercial vehicles and the STA’s bus fleet under the STA contract. Zurich has issued approximately two million CTP policies since that time. Approximately 16% of open claims in respect of the portfolio relate to the STA contract.

20 As I have noted, the CTP portfolio transitioned into run-off in November 2015 and Zurich ceased issuing new Zurich NSW CTP policies and renewals on 30 September 2016. The last period of insurance expired on 31 March 2017. The statutory time period for claims reporting is within six months after an accident. Therefore, the claim period for all policies in the CTP portfolio expired on 30 September 2017, although a late claim may be made if there is a full and satisfactory explanation for the delay. Zurich expects that it will only receive a small number of future claims notifications. The evidence of claims since 2007 suggests that the number of such claims is diminishing as time goes by. As at 5 October 2018, only 39 new claims that are late claims have been made.

21 As regards the Nominal Defendant Scheme, all CTP insurers in New South Wales are required to contribute to a fund maintained by the State Insurance Regulatory Authority (SIRA). The fund compensates those with a CTP claim for which the details of the at-fault driver are not available. Nominal Defendant claims are randomly allocated to licensed insurers in proportion to the market share, by earned exposure, of that insurer for the accident year of the claim.

22 As at 31 August 2018, there were 906 open claims in respect of the CTP portfolio. Of these claims, 717 are managed by Zurich; 121 are managed by another insurer under the CTP sharing arrangements referred to at [5(a)] above; and 68 claims are managed under the Nominal Defendant Scheme. As to the latter, prior to transitioning into run-off in November 2015, the CTP portfolio had a market share, by earned exposure, of 5%. With the run-off, this has been reduced to nil. The last claims under the Nominal Defendant Scheme were allocated to Zurich in 2016.

Policyholders

23 The Zurich NSW CTP policies have been predominantly sold by Zurich through brokers and green slip agents, although some policies were sold directly. Policyholder details were collected, recorded and used by the following process.

24 Zurich’s systems were used to input policyholder details. These details were then sent to Roads and Maritime Services (RMS), and batch-processed overnight. RMS reverted to Zurich with corresponding vehicle and registered owner details relating to the new policyholder information. RMS also provided Zurich with any change of vehicle ownership details, as these changes occurred. The information provided by Zurich’s systems and RMS was entered into Zurich’s “Polisy” mainframe system to facilitate the ongoing administration of the policies and any associated claims. This information was used by Zurich to communicate with vehicle owners about policy renewal; for reserving, pricing and portfolio analysis; and for reporting to large commercial clients details of their claims experience performance in accordance with client agreements in place from time to time. Claims officers would access policy details on receipt of a claim notification to identify the owner of the vehicle. A substantial portion of the CTP portfolio comprises CTP policies for commercial vehicles, rather than other vehicle classes. The majority of the insureds are corporate entities rather than individuals.

25 Because the claim period for all policies in the CTP portfolio expired on 30 September 2017, and because it expects that it will only receive a small number of future claims notifications, Zurich does not propose to provide a copy of the approved summary to policyholders with no notified claims that are unsettled or otherwise outstanding. Except to the extent that they may wish to make a late claim (and, therefore, are able to provide a full and satisfactory explanation for the delay), these policyholders no longer have any interest in their expired CTP policies. Further, as I have recorded, the applicants propose that Zurich will undertake the alternative notification procedure I have summarised.

Actuarial reports

26 Two draft actuarial reports have been obtained in relation to the scheme, one from Mr Atkin (Finity Consulting Pty Limited) (latest draft, 26 September 2018), and one from Mr Stephan (Deloitte Consulting Pty Ltd) (latest draft, 28 September 2018). Mr Atkin has expressed the provisional view that the affected policyholders will not be adversely affected in a material way as a consequence of the proposed scheme. Mr Stephan has expressed the provisional view that the interests of the transferring policyholders, the remaining post-transfer Zurich policyholders and the existing pre-transfer policyholders of Gordian, will not be materially adversely affected by the proposed transfer.

Proposed Notification

27 There are policyholders whose current addresses are unknown. Although policyholders’ addresses were recorded at the time of inception of the policies, the nature of CTP insurance is such that, once a policy has expired, Zurich’s ongoing contact (if a claim is notified) is with the claimant rather than the policyholder. Following notification of a claim, Zurich’s claims officers contact the relevant policyholder to validate the claim and seek further particulars. But, from this point on, the primary contact for Zurich is the claimant, not the policyholder. Details of the claimant, or the claimant’s nominated representative, is captured on file for periodic correspondence from Zurich’s claims department.

28 Zurich does not ordinarily update a policyholder’s address once that person’s policy has expired. Therefore, for the purpose of notifying policyholders, Zurich proposes to use the last known address when giving the approved summary to policyholders for which there is a notified claim that is unsettled or otherwise outstanding.

29 As I have noted, in the event that copies of the approved summary sent by Zurich are returned undelivered, Zurich will, to the extent reasonably practicable, follow its returned mail procedure to identify the new mailing address for the relevant policyholder/claimant and, if by that process the policyholder/claimant is identified, resend the approved summary to the new mailing address. Zurich’s returned mail procedure involves interrogating its records for updated details and searching through Australia Post’s National Change of Address database, which is built exclusively from data sourced from Australia Post’s mail redirection service.

30 Zurich will engage Computershare for the mail-out. Computershare managed and facilitated Zurich’s mail-out for the CTP portfolio run-off process in December 2015. Zurich will provide Computershare with a full mail-out brief and relevant data and assistance. A mail-out quality assurance review will be undertaken prior to approval for enveloping. Following successful completion of that review, the correspondence will be enveloped, batched and securely transported to Australia Post to be managed through standard Australia Post services.

31 As I have recorded, the notice of intention will be published in the Government Gazette as well as in a number of newspapers circulating either nationally or locally in New South Wales, Queensland and the Australian Capital Territory. Zurich will maintain a webpage containing links to the Inspection Documents. Further, office facilities will be made available for inspection of the Inspection Documents, as I have noted at [5(d)] above.

32 Zurich is making preparations for telephone response handling, and will engage the services of a domestic call centre to receive enquiries in relation to the proposed scheme and transfer. Enquiries not immediately answerable at the time of the call will be escalated to Zurich’s New South Wales CTP Claims Manager. Escalated enquiries will be managed within seven business days. Call centre staff will be trained to provide information about the proposed scheme and transfer using a “frequently asked questions” format. Zurich will regularly monitor the quality of the response handling being undertaken, and will record calls. The call log will be maintained. Zurich will collate and record any concerns raised or objections received by telephone. It will also collate and record any concerns raised and objections received by letter. There will be a formal escalation process put in place in respect of calls or letters that contain objections or raise concerns. All such letters and calls will be considered by a specialist team including, where appropriate, representatives from Zurich’s legal and actuarial functions. Enquiries from current claimants will be directed to Zurich’s New South Wales CTP Claims Manager.

33 It is a condition of Zurich’s licence under the MACA that it must not transfer any part of its CTP business to a person who is not a licensed insurer under that legislation. Gordian has sought such a licence. Its application is pending. It is currently proposed that notification, as proposed, will not commence until the week beginning 5 November 2018. As yet, no date has been appointed for the confirmation hearing.

APRA

34 The Australian Prudential Regulation Authority (APRA) has been consulted in relation to the promulgation of the proposed scheme. It has indicated that formal approval of the scheme summary, the notice of intention and other documents (see Prudential Standard GPS 410 Transfer and Amalgamation of Insurance Business for General Insurers), will only be given after the present application so as to ensure that dates inserted in the relevant documents are accurate having regard to the proposed commencement of communication in the week beginning 5 November 2018. Zurich has stated that it is not aware of any reason why such approval would not be forthcoming.

35 APRA was represented at the hearing of the present application. It supports the making of the orders that are presently sought. It has expressed the view that the proposed alternative notification procedure is appropriate and thorough. In forming this view, it has drawn a degree of comfort from the fact that SIRA has been involved in the process to date, including identifying relevant stakeholders to whom notice should be given.

Submissions

36 The applicants submit, firstly, that there is no utility in providing the scheme summary to the holders of Zurich NSW CTP policies for which no unsettled or otherwise outstanding claims have been made. The applicants submit that these policyholders have no continuing interest in their (now) expired policies, save for making a late claim (if the circumstances for making such a claim can be established). The applicants submit that the expense involved in sending the scheme summary would be for little, if any, benefit. Further, other steps (see [27]-[33] above) are proposed that will bring the proposed scheme to public attention, in any event.

37 The applicants submit, secondly, that, for those policyholders to whom it is proposed the scheme summary will be sent, it should be sufficient if the summary is sent to each policyholder’s currently known address. They submit that the concern of the Court should be whether all reasonable efforts have been made to identify the affected policyholders concerned. This submission is an appeal to the practical realities of the case: see Application of Gordian RunOff Limited under the Insurance Act 1973 (Cth) [2013] FCA 983 at [16].

Consideration

38 The granting of dispensation pursuant to s 17C(5) of the Act is a matter of considerable importance and should not be regarded as a matter of course: Challenger Life Limited [2004] FCA 618 at [2]-[3]; Munich Reinsurance Company of Australasia Limited [2004] FCA 1391 at [4]. The plain policy intention of s 17C(2)(c) is that every affected policyholder should be given a summary of the scheme and an opportunity to make submissions to the Court in respect of the scheme at a confirmation hearing: The Application of Commonwealth Life Ltd & Anor [2003] FCA 501 at [8]; see also Westport Insurance Corporation, in the matter of Westport Insurance Corporation [2009] FCA 1357 at [38]; HDI-Gerling Australia Insurance Company Pty Limited, in the matter of HDI-Gerling Australia Insurance Company Pty Limited (ABN 16 069 985 196) [2010] FCA 505 at [38]-[39]. Nevertheless, I am satisfied that it is appropriate in the present case to grant the dispensation that is sought.

39 I am satisfied that, because of the nature of the business concerned, it is not necessary that the approved summary be given to every affected policyholder as contemplated by s 17C(2)(c) of the Act. I accept that there is little utility in requiring the scheme summary to be given to the holders of policies in respect of which there are no unsettled or otherwise outstanding, notified claims. I also accept that, for those policyholders to whom it is proposed the approved summary will be sent, it is appropriate that currently known addresses be used, provided Zurich undertakes the follow-up procedures it has proposed in relation to returned mail. I also note that, in respect of claims made after the mail-out, Zurich will send the approved summary to both the claimant and the policyholder

40 I am satisfied that notification of this kind, taken with the other steps proposed to notify and publicise the proposed scheme, is likely to bring forth any potential, reasonably-based objection or opposition to the proposed scheme. In this connection, I take into account the fact that APRA has been consulted on this aspect of the proposed scheme and has raised no objection to dispensation or to the suitability or adequacy of the other notification steps proposed. Indeed, as I have noted, it supports the making of the orders presently sought.

41 Finally, I also take into account the fact that two expert views have been expressed, albeit provisionally at the present time, that the proposed scheme and transfer will not adversely affect, in a material way, the policyholders to whom s 17C(2)(c) otherwise requires the approved summary to be sent.

Disposition

42 For these reasons, orders, substantially as proposed, should be made.

I certify that the preceding forty-two (42) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Yates. |

Associate: