FEDERAL COURT OF AUSTRALIA

Changshu Longte Grinding Ball Co., Ltd v Parliamentary Secretary to the Minister for Industry, Innovation and Science (No 2) [2018] FCA 1135

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The originating application dated 15 June 2017 be dismissed.

2. The applicant pay the respondents’ costs, as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

1 This is an application for judicial review of a decision to impose dumping duties on the export to Australia from the People’s Republic of China (PRC) of ferrous grinding balls, whether or not containing alloys, cast or forged, with diameters in the range 22 mm to 170 mm inclusively (grinding balls).

2 Ferrous grinding balls are steel balls used to break up material such as lumps of ore into smaller lumps of ore. The applicant (Longte) is incorporated and registered under the laws of the PRC. It produces steel grinding ball products and sells them into domestic and export markets.

3 It is convenient to say something briefly about the history of the decision under review. On 9 September 2016, the first respondent (the Minister) published a notice dated 1 September 2016 that s 8 of the Customs Tariff (Anti-Dumping) Act 1975 (Cth) (Dumping Duty Act) applied to the export of grinding balls from the PRC such that dumping duty was payable. That decision was based in part on a report dated 6 June 2016 by the second respondent (the Commissioner) (Report 316). Several persons, including Longte, sought a review of the Minister’s decision dated 1 September 2016. As part of that review, a further report was published by the third respondent (the Review Panel). The Review Panel’s report is dated 18 April 2017 (Report 47). In Report 47, the Review Panel affirmed the Commissioner’s approach in Report 316 to the calculation of normal value of goods pursuant to s 269TAC(2) of the Customs Act 1901 (Cth) (Customs Act). The Review Panel recommended to the Minister that he affirm his original decision dated 1 September 2016 to impose dumping duties. In a notice dated 18 May 2017, the Minister accepted that recommendation and affirmed his original decision. The Minister’s decision dated 18 May 2017, which is at the heart of the judicial review challenge, resulted in the export of grinding balls to Australia by various Chinese companies, including Longte, being subject to payment of dumping duties pursuant to s 8 of the Dumping Duty Act.

4 Longte challenges the Minister’s decision to impose dumping duties on it on 7 grounds, which may be summarised as follows:

(a) The Minister determined the cost of production or manufacture of grinding balls in the PRC by applying s 43(2) of the Customs (International Obligations) Regulation 2015 (Cth) (the Regulation) in circumstances where a condition of that regulation (i.e. that the exporter’s records reasonably reflect competitive market costs associated with the production and manufacture of like goods), was not satisfied in the view of either the Commissioner or the Review Panel (ground 1).

(b) The Minister relied for his determination on the cost of production of steel billet data from Latin America, rather than the steel billet cost of production in the PRC as required by s 269TAC(2)(c)(i) of the Customs Act (grounds 2 and 3).

(c) If, contrary to grounds 2 and 3, the Minister was entitled to use third country data, the decision was invalid because the Minister:

(i) failed to adapt that data so that it could be, or could constitute, part of the cost of production or manufacture of goods in the country of export for the purposes of s 269TAC(2)(c)(i) of the Customs Act (ground 4);

(ii) wrongly failed to use that same data in the determination of the sales in the ordinary course of trade for the purposes of ss 269TAAD(1), (2), (3), (4)(a) and (5) of the Customs Act, and instead used Longte’s records for that purpose (ground 5); and

(iii) failed to use that third country data consistently in ascertaining the amount of profit for the purposes of s 269TAC(2)(c)(ii) of the Customs Act (ground 6).

(d) The calculation of profit, by applying a percentage worked out on the basis of Longte’s actual cost base, which percentage was then applied without adjustment to the substituted cost base, was irrational, illogical and unreasonable (ground 7).

5 Longte seeks orders quashing both the final decision of the Minister dated 18 May 2017 and Report 47, as well as costs.

6 During the period 19 September 2011 to 12 June 2012, the Australian Customs and Border Protection Service conducted an investigation into alleged dumping and subsidisation of hollow structural sections from the PRC, which resulted in its report dated 7 June 2012 (Report 177).

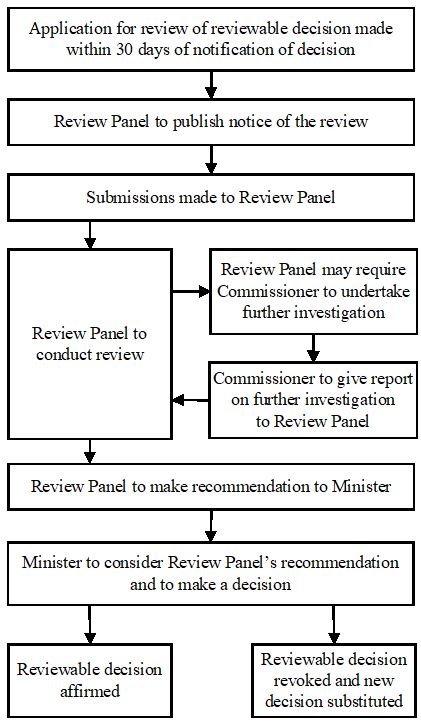

7 On 17 November 2015, the Commissioner published a notice under s 269TC(4) of the Customs Act which announced the initiation of an investigation into alleged dumping and subsidisation in relation to the export of grinding balls from the PRC.

8 On 21 April 2016, the Commissioner published a statement of essential facts (SEF) upon which he proposed to base his recommendation to the Minister concerning the investigation. The Commissioner invited and received submissions on the SEF from various persons, including Longte who made a submission dated 11 May 2016.

9 On 6 June 2016, the Commissioner provided to the Minister Report 316, which set out his findings and recommendations to the Minister on his investigation into the export of grinding balls from the PRC and recommended that dumping duties be imposed on Longte.

10 On 9 September 2016, the Minister published a notice dated 1 September 2016 pursuant to ss 269TG(1) and (2) of the Customs Act. The notice accepted the findings and recommendations in Report 316 and imposed dumping duties on several companies, including Longte (Anti-Dumping Notice No. 2016/90).

11 In October 2016, Longte and three other Chinese companies applied to the Review Panel for a review of the Minister’s decision. The Review Panel subsequently initiated such a review.

12 On 22 December 2016, the Review Panel asked the Commissioner pursuant to s 269ZZL of the Customs Act to reinvestigate various findings made in Report 316. On 15 March 2017, the Commissioner provided the Review Panel with a report of his findings in response to that request for reinvestigation (Reinvestigation Report 388).

13 On 18 April 2017, the Review Panel provided Report 47 to the Minister, which contained its findings and recommendations arising from its review. It recommended to the Minister that the decision to impose dumping duties be affirmed.

14 On 18 May 2017, the Minister, acting pursuant to s 269ZZM(4) of the Customs Act, published a notice accepting the findings and recommendations in Report 47 and affirming the earlier decision to impose dumping duties on Longte and others. This is the decision which is the subject of the present judicial review proceeding, which was commenced by Longte on 15 June 2017.

Outline of the legislative regime

15 It is necessary to describe the somewhat complex relevant legislative regime.

16 Division 2 of Pt XVB of the Customs Act describes, among other things, the requirements for making an application for the publication of a dumping duty notice and the procedures to be followed, and the matters to be considered, by the Commissioner in conducting investigations into goods covered by such an application, for the purpose of making a report to the Minister (s 269TBA).

17 The process begins with s 269TB of the Customs Act, which deals with the making of an application for dumping duty notices to be published. Section 269TB(1) provides:

(1) Where:

(a) a consignment of goods:

(i) has been imported into Australia;

(ii) is likely to be imported into Australia; or

(iii) may be imported into Australia, being like goods to goods to which subparagraph (i) or (ii) applies;

(b) there is, or may be established, an Australian industry producing like goods; and

(c) a person believes that there are, or may be, reasonable grounds for the publication of a dumping duty notice or a countervailing duty notice in respect of the goods in the consignment;

that person may, by application in writing lodged with the Commissioner, request that the Minister publish that notice in respect of the goods in the consignment.

18 Section 269TC deals with matters to be considered by the Commissioner in conducting an investigation in relation to goods covered by an application under s 269TB(1), for the purpose of making a report to the Minister. If the application is not rejected, then pursuant to s 269TC(4), the Commissioner must give public notice of various matters, including the identity of the applicant, particulars of goods the subject of the application and the countries of export. The notice must also specify the date of initiation of the investigation (which should be the date or estimated date of publication of the notice: s 269TC(4)(bc)), and an indication that a report will be made to the Minister on the basis of the examination of exports to Australia of goods the subject of the application during a period specified in the notice, referred to as the “investigation period” (s 269TC(4)(bf)). Interested persons can make submissions to the Commissioner (s 269TC(4)(f)-(g)). Export prices and normal values of goods are typically determined during the investigation period to consider whether dumping has occurred.

19 The next salient step is s 269TDAA, which requires the Commissioner to place on the public record a statement of essential facts (SEF) within a certain time after the date of initiation of the investigation. The SEF contains the facts on which the Commissioner proposes to base a recommendation to the Minister in respect of an application for a dumping duty notice to be published. The Commissioner must have regard to validly made submissions from interested persons in formulating the SEF (s 269TDAA(2)(a)(ii)).

20 Section 269TDA describes the circumstances in which the Commissioner must terminate an investigation. If an investigation is not terminated pursuant to s 269TDA, the Commissioner must give the Minister a report following the investigation in accordance with s 269TEA. That report must, among other things, contain a recommendation to the Minister as to whether any dumping duty notice should be published, and the extent of any duties payable under the Dumping Duty Act.

21 Section 269TLA requires the Minister to decide whether to publish a dumping duty notice within a certain time after receiving a report from the Commissioner. The Minister may publish a dumping notice under s 269TG if certain condition are satisfied. Section 269TG(1) deals with past exports, and subsection (2) deals with further goods which may be exported to Australia. The central issue for determination by the Minister under ss 269TG(1) and (2) is whether the “export price” of goods was less than the “normal value” of goods, such that it caused material injury to an Australian industry. The terms of ss 269TG(1) and (2) are as follows:

269TG Dumping duties

(1) Subject to section 269TN, where the Minister is satisfied, as to any goods that have been exported to Australia, that:

(a) the amount of the export price of the goods is less than the amount of the normal value of those goods; and

(b) because of that:

(i) material injury to an Australian industry producing like goods has been or is being caused or is threatened, or the establishment of an Australian industry producing like goods has been or may be materially hindered; or

(ii) in a case where security has been taken under section 42 in respect of any interim duty that may become payable on the goods under section 8 of the Dumping Duty Act—material injury to an Australian industry producing like goods would or might have been caused if the security had not been taken;

the Minister may, by public notice, declare that section 8 of that Act applies:

(c) to the goods in respect of which the Minister is so satisfied; and

(d) to like goods that were exported to Australia after the Commissioner made a preliminary affirmative determination under section 269TD in respect of the goods referred to in paragraph (c) but before the publication of that notice.

(2) Where the Minister is satisfied, as to goods of any kind, that:

(a) the amount of the export price of like goods that have already been exported to Australia is less than the amount of the normal value of those goods, and the amount of the export price of like goods that may be exported to Australia in the future may be less than the normal value of the goods; and

(b) because of that, material injury to an Australian industry producing like goods has been or is being caused or is threatened, or the establishment of an Australian industry producing like goods has been or may be materially hindered;

the Minister may, by public notice (whether or not he or she has made, or proposes to make, a declaration under subsection (1) in respect of like goods that have been exported to Australia), declare that section 8 of the Dumping Duty Act applies to like goods that are exported to Australia after the date of publication of the notice or such later date as is specified in the notice.

22 The Review Panel is established by Div 8 of Pt XVB of the Customs Act (see s 269ZK). Division 9 of Pt XVB sets out the process by which the Review Panel can review certain decisions made by the Minister or Commissioner (see s 269ZW). Division 9, Subdiv B deals with review of Ministerial decisions. Section 269ZZA(1)(a) provides that a decision by the Minister to publish a dumping duty notice under s 269TG(1) or (2) is a decision that is reviewable by the Review Panel. Interested persons are entitled to make submissions to the Review Panel in relation to a reviewable decision in accordance with s 269ZZJ and the Review Panel is obliged to have regard to validly made submissions subject to the qualifications in s 269ZZK(4)(b).

23 Section 269ZZB includes the following flow chart which describes how the review process works:

24 As is apparent from the flow chart, the Review Panel has to make a recommendation to the Minister. Section 269ZZK provides that the Review Panel is to make its recommendation in the form of a report as to whether the Minister should affirm or revoke the reviewable decision. In the present proceedings, the applicant seeks to quash or set aside the report made by the Review Panel under s 269ZZK, namely, Report 47.

25 After receiving the Review Panel’s report, the Minister is to make a decision as to whether to affirm or revoke the reviewable decision pursuant to s 269ZZM. As mentioned above, in the present proceedings, the Minister’s decision dated 18 May 2017 made under s 269ZZM is the subject of the judicial review proceeding.

Key concepts in these proceedings

26 The legislative regime in the Customs Act which imposes dumping duties has, as one of its central features, the concept of the “normal value of goods”, which is defined in s 269TAC. Section 8(2)(b) of the Dumping Duty Act allows a dumping duty to be imposed if the “export price” of goods brought into Australia is less than their “normal value”.

27 Pursuant to s 269TACB, the Minister must determine whether dumping has occurred by comparing, in the investigation period, the export price (determined under s 269TAB) and the normal value of the goods (determined under s 269TAC).

28 A central focus of the present dispute is the applicant’s contention that the “normal value” of grinding balls was incorrectly calculated under s 269TAC.

29 The primary method for calculating the normal value of goods is to use the sale price of “like goods” sold in the ordinary course of trade in the country of export, in sales that are arm’s length transactions (s 269TAC(1)). “Like goods” is defined in s 269T to mean “goods that are identical in all respects to the goods under consideration or that, although not alike in all respects…have characteristics closely resembling those of the goods under consideration”. The legislation recognises, however, that the primary method for calculating the normal value of goods may not be suitable in a particular case. Accordingly, it provides for alternative methods of calculation in, inter alia, s 269TAC(2) (which provision is itself affected by other subsections in s 269TAC).

30 The relevant provisions in s 269TAC are as follows:

269TAC Normal value of goods

(1) Subject to this section, for the purposes of this Part, the normal value of any goods exported to Australia is the price paid or payable for like goods sold in the ordinary course of trade for home consumption in the country of export in sales that are arms length transactions by the exporter or, if like goods are not so sold by the exporter, by other sellers of like goods.

(1A) For the purposes of subsection (1), the reference in that subsection to the price paid or payable for like goods is a reference to that price after deducting any amount that is determined by the Minister to be a reimbursement of the kind referred to in subsection 269TAA(1A) in respect of the sales.

(2) Subject to this section, where the Minister:

(a) is satisfied that:

(i) because of the absence, or low volume, of sales of like goods in the market of the country of export that would be relevant for the purpose of determining a price under subsection (1); or

(ii) because the situation in the market of the country of export is such that sales in that market are not suitable for use in determining a price under subsection (1);

the normal value of goods exported to Australia cannot be ascertained under subsection (1); or

(b) is satisfied, in a case where like goods are not sold in the ordinary course of trade for home consumption in the country of export in sales that are arms length transactions by the exporter, that it is not practicable to obtain, within a reasonable time, information in relation to sales by other sellers of like goods that would be relevant for the purpose of determining a price under subsection (1);

the normal value of the goods for the purposes of this Part is:

(c) except where paragraph (d) applies, the sum of:

(i) such amount as the Minister determines to be the cost of production or manufacture of the goods in the country of export; and

(ii) on the assumption that the goods, instead of being exported, had been sold for home consumption in the ordinary course of trade in the country of export—such amounts as the Minister determines would be the administrative, selling and general costs associated with the sale and the profit on that sale; or

(d) if the Minister directs that this paragraph applies—the price determined by the Minister to be the price paid or payable for like goods sold in the ordinary course of trade in arms length transactions for exportation from the country of export to a third country determined by the Minister to be an appropriate third country, other than any amount determined by the Minister to be a reimbursement of the kind referred to in subsection 269TAA(1A) in respect of any such transactions.

…

(5A) Amounts determined:

(a) to be the cost of production or manufacture of goods under subparagraph (2)(c)(i) or (4)(e)(i); and

(b) to be the administrative, selling and general costs in relation to goods under subparagraph (2)(c)(ii) or (4)(e)(ii);

must be worked out in such manner, and taking account of such factors, as the regulations provide for the respective purposes of paragraphs 269TAAD(4)(a) and (b).

(5B) The amount determined to be the profit on the sale of goods under subparagraph (2)(c)(ii) or (4)(e)(ii), must be worked out in such manner, and taking account of such factors, as the regulations provide for that purpose.

…

(6) Where the Minister is satisfied that sufficient information has not been furnished or is not available to enable the normal value of goods to be ascertained under the preceding subsections (other than subsection (5D)), the normal value of those goods is such amount as is determined by the Minister having regard to all relevant information.

31 In these proceedings, the Commissioner determined the normal value of goods pursuant to the method in s 269TAC(2)(c) (Report 316, pp 29, 38). This method of calculation refers, inter alia, to an assumption being made that the goods, instead of being exported, had been sold for home consumption in “the ordinary course of trade in the country of export” (s 269TAC(2)(c)(ii)).

32 Section 269TAAD makes provision for determining whether goods have been sold in “the ordinary course of trade”:

269TAAD Ordinary course of trade

(1) If the Minister is satisfied, in relation to goods exported to Australia:

(a) that like goods are sold in the country of export in sales that are arms length transactions in substantial quantities during an extended period:

(i) for home consumption in the country of export; or

(ii) for exportation to a third country;

at a price that is less than the cost of such goods; and

(b) that it is unlikely that the seller of the goods will be able to recover the cost of such goods within a reasonable period;

the price paid for the goods referred to in paragraph (a) is taken not to have been paid in the ordinary course of trade.

(2) For the purposes of this section, sales of goods at a price that is less than the cost of such goods are taken to have occurred in substantial quantities during an extended period if the volume of sales of such goods at a price below the cost of such goods over that period is not less than 20% of the total volume of sales over that period.

(3) Costs of goods are taken to be recoverable within a reasonable period of time if, although the selling price of those goods at the time of their sale is below their cost at that time, the selling price is above the weighted average cost of such goods over the investigation period.

(4) The cost of goods is worked out by adding:

(a) the amount determined by the Minister to be the cost of production or manufacture of those goods in the country of export; and

(b) the amount determined by the Minister to be the administrative, selling and general costs associated with the sale of those goods.

(5) Amounts determined by the Minister for the purposes of paragraphs (4)(a) and (b) must be worked out in such manner, and taking account of such factors, as the regulations provide in respect of those purposes.

33 In short, s 279TAAD(1) provides that if goods are sold in the country of export at a cheaper price than the cost of such goods, and other various conditions are satisfied, the cheaper price at which the goods are sold is deemed not to have been paid in “the ordinary course of trade”. This requires the Minister to calculate the “cost of goods”, which is worked out by adding the amount determined by the Minister to be the cost of production or manufacture of those goods in the country of export, and the amount determined to be the administrative, selling and general costs associated with the sale of those goods (s 269TAAD(4)). Both of those amounts must be determined in accordance with relevant regulations (s 269TAAD(5)).

34 Section 43(2) of the Regulation sets out a methodology for working out the cost of production or manufacture, referred to in s 269TAC(2)(c)(i):

43 Determination of cost of production or manufacture

…

(2) If:

(a) an exporter or producer of like goods keeps records relating to the like goods; and

(b) the records:

(i) are in accordance with generally accepted accounting principles in the country of export; and

(ii) reasonably reflect competitive market costs associated with the production or manufacture of like goods;

the Minister must work out the amount by using the information set out in the records.

…

35 Section 44 of the Regulation sets out a methodology for determining the administrative, selling and general costs, referred to in 269TAC(2)(c)(ii). In ordinary cases where like goods are sold into the domestic market, s 44(2) requires the use of the relevant business records of the producer (if they exist). Where the relevant business records do not permit this process, s 44(3) sets up an inquiry instead into various amounts incurred in relation to goods “of the same general category”. Section 44(2) and (3) provide:

44 Determination of administrative, selling and general costs

…

(2) If:

(a) an exporter or producer of like goods keeps records relating to the like goods; and

(b) the records:

(i) are in accordance with generally accepted accounting principles in the country of export; and

(ii) reasonably reflect the administrative, general and selling costs associated with the sale of the like goods;

the Minister must work out the amount by using the information set out in the records.

(3) If the Minister is unable to work out the amount by using the information mentioned in subsection (2), the Minister must work out the amount by:

(a) identifying the actual amounts of administrative, selling and general costs incurred by the exporter or producer in the production and sale of the same general category of goods in the domestic market of the country of export; or

(b) identifying the weighted average of the actual amounts of administrative, selling and general costs incurred by other exporters or producers in the production and sale of like goods in the domestic market of the country of export; or

(c) using any other reasonable method and having regard to all relevant information.

…

36 Section 45 of the Regulation sets out the manner in which the Minister must work out what would be the amount of profit on the assumed sale of goods for home consumption for the purposes of inter alia s 269TAC(2)(c)(ii). The method used here is that in s 45(2), but it is desirable to set out all of s 45:

45 Determination of profit

(1) For subsection 269TAC(5B) of the Act, this section sets out:

(a) the manner in which the Minister must, for subparagraph 269TAC(2)(c)(ii) or (4)(e)(ii) of the Act, work out an amount (the amount) to be the profit on the sale of goods; and

(b) factors that the Minister must take account of for that purpose.

(2) The Minister must, if reasonably practicable, work out the amount by using data relating to the production and sale of like goods by the exporter or producer of the goods in the ordinary course of trade.

(3) If the Minister is unable to work out the amount by using the data mentioned in subsection (2), the Minister must work out the amount by:

(a) identifying the actual amounts realised by the exporter or producer from the sale of the same general category of goods in the domestic market of the country of export; or

(b) identifying the weighted average of the actual amounts realised by other exporters or producers from the sale of like goods in the domestic market of the country of export; or

(c) using any other reasonable method and having regard to all relevant information.

(4) However, if:

(a) the Minister uses a method of calculation under paragraph (3)(c) to work out an amount representing the profit of the exporter or producer of the goods; and

(b) the amount worked out exceeds the amount of profit normally realised by other exporters or producers on sales of goods of the same general category in the domestic market of the country of export;

the Minister must disregard the amount by which the amount worked out exceeds the amount of profit normally realised by the other exporters or producers.

(5) For this section, the Minister may disregard any information that he or she considers to be unreliable.

(6) For paragraph (3)(b), subsection 269T(5A) of the Act sets out how to work out the weighted average.

Summary of relevant parts of Report 316 and Report 47

37 It is desirable to outline the reasoning of the Commissioner and the Review Panel in Reports 316 and 47 respectively which are at the heart of Longte’s judicial review challenge.

38 Both the Commissioner (Report 316, p 24) and the Review Panel (Report 47 at [34]) proceeded on the basis that determination of the cost of production under s 269TAC(2)(c)(i) and the administrative, selling and general costs under s 269TAC(2)(c)(ii) had to be worked out in such manner, and taking into account of such factors, as were prescribed in the Regulation. Section 43 of Regulation potentially applies to the determination under subparagraph (i). Section 44 of the Regulation potentially applies to the determination of administrative, selling and general costs for the purposes of subparagraph (ii) and s 45 of the Regulation potentially applies to the determination of profit for the purposes of that same subparagraph.

39 The Commissioner concluded that s 43(2) did not apply in the circumstances here. The Commissioner found that various plans, policies and taxation regimes of the PRC Government contributed to the distorted prices of production inputs including, but not limited to, raw materials used to make grinding balls in China. He concluded that this distortion rendered those costs unsuitable for the purposes of making a cost to make and sell calculation. He added that these distortions affected Chinese manufacturers’ costs to produce grinding bars which in turn are used to produce grinding balls (Report 316, p 23). Accordingly, the Commissioner concluded that, as a result of these distortions, the records of exporters in China, including Longte’s, did not reasonably reflect competitive market costs associated with production or manufacture (Report 316, pp 23-24 and 28).

40 Having found that there was a market situation for grinding balls in China, the Commissioner stated at p 24 that normal values may be determined on the basis of a cost construction or third country sales. Because the Commissioner was unable to rely on PRC Government data to quantify the impacts of distortion on exporters’ cost inputs, he proceeded to quantify the effects of that influence by comparing each exporter’s costs of production with an “external benchmark”, which comprised:

(a) a monthly Latin American export billet price in FOB terms;

(b) an uplift in the billet price using independently sourced ferroalloy prices, to provide a matrix of billet grades reasonably reflecting the chemical composition of each exported grinding ball grade; and

(c) a further uplift using the exporters’ actual cost of converting steel billet to grinding bar or, where those costs were not available, an uplift using a conversion factor based on an average of the conversion costs of the cooperating exporters (Report 316, p 25).

41 Having established what the Commissioner described as “a competitive grinding bar benchmark” using the above methodology, he then compared the competitive grinding bar benchmark to the costs reported in the Chinese exporters’ records. He found that this comparison indicated that the costs reported in the exporters’ records were significantly influenced by the market situation in the PRC and that they did not reasonably reflect competitive market costs (p 26). After noting that s 43(2) of the Regulation did not provide for how a cost of production should be determined where such records do not reasonably reflect competitive market costs, the Commissioner stated that the grinding bar costs in the exporters’ records should be adjusted. This involved adjusting the grinding bar costs in the exporters’ records to align them with the competitive grinding bar benchmark and to then implement the following steps to arrive at normal values for each exporter (see Report 316, p 26):

(a) the competitive grinding bar benchmark was uplifted by each cooperating exporter’s actual cost to convert grinding bar to grinding balls to determine the cost to make of each grade of each exporter’s grinding balls;

(b) the cost to make was uplifted by each exporter’s actual selling, general and administrative expenses to determine a cost to make and sell for each grade of each exporter’s grinding balls; and

(c) the cost to make and sell was uplifted based on each exporter’s profit on those domestic sales which met the original ordinary course of trade test (based on the exporter’s unadjusted records).

42 At p 28 of Report 316, the Commissioner explained the methodology in the following terms:

The Commission compared each of the cooperating exporters’ actual cost to manufacture or purchase grinding bar with the competitive market cost benchmark. This comparison at the grinding bar level supports the Commission’s view that direct and indirect influences of the [Government of China] affect Chinese manufacturers’ costs of grinding bar. The Commission is also mindful that grinding bar comprises a significant proportion of the total [cost to make and sell] for grinding balls and an adjustment to the costs at grinding bar level enables the Commission to account for the influences from the [Government of China] on the predominant input costs (apart from the cost of conversion of grinding bar to grinding balls and cost of selling) that would otherwise not be accounted for.

43 At p 28 of Report 316, the Commissioner summarised submissions he had received from Chinese exporters other than Longte. One exporter contended that an adjustment had to be made for profit and transport while two others submitted that adjustments should be made for profit and export costs. It is clear that the Commissioner considered those submissions and he explained at some length at p 29 why they were rejected. For example, in declining to adjust the Latin American billet price to take into account a profit component, the Commissioner explained that, unlike other cases, he did not have average verified level of profit information from Chinese exporters in relation to the sales of billet used in grinding balls. He reasoned that, absent such information and also noting the weakness in global steel markets, it was unreasonable to assume that a profit was necessary. Similarly, the Commissioner explained that he did not have information concerning the inland transport costs required to transport steel billet from the factory to the port of shipment for Latin American billet. Thus he made no adjustment for inland transportation, while also noting that no upward adjustment had been made to reflect the fact that the Chinese manufacturers of grinding balls would incur inland transportation costs.

44 At pp 29 and 30 of Report 316, the Commissioner specifically addressed submissions which he had received from Longte in response to the SEF which preceded the making of Report 316. After considering Longte’s submissions, the Commissioner revised the construction of normal values for all exporters. Longte had submitted that by uplifting steel billet cost used in the grinding bar competitive benchmark by percentages derived from Longte’s actual records, the Commissioner had unnecessarily inflated conversion costs as well as selling, general and administrative expenses. The Commissioner declined, however, to accept Longte’s similar submission in relation to the calculation of profit for the purposes of s 269TAC(2)(c)(ii). On that matter, the Commissioner added a profit component, which was calculated on the basis of Longte’s unadjusted records, to the cost of production which had been ascertained using the “substituted” benchmark costs (Report 316, p 33). The Commissioner stated at p 30 that he considered that this approach was consistent with s 45(2) of the Regulation.

Longte’s submissions summarised

45 Longte’s judicial review challenge focused primarily on how the normal value of the goods had been determined in Report 316 and Report 47, upon which the Minister relied in affirming the decision to impose dumping duties. Longte challenged the validity of the Commissioner’s calculation of the normal value using s 269TAC(2)(c) of the Customs Act on the following seven grounds.

Grounds 1 to 4 : Determination of cost of production or manufacture in the country of export

46 Longte initially contended that s 43(2) of the Regulation prescribes the only source of information by which the amount of the cost of production is to be determined. It claimed that both the Commissioner and the Review Panel applied an erroneous construction of s 43(2) of the Regulation in using the cost of production or manufacture of steel billet in Latin America (as adjusted) to determine the cost of production or manufacture for exporters of steel billet from the PRC.

47 Longte contended that this misconstruction of s 43(2) led to the calculation of the normal value applicable to Longte’s exports on the basis of cost of production or manufacture of the goods which were not the costs in the country of export, namely the PRC, contrary to s 269TAC(2)(c)(i). Longte noted that the Review Panel had rejected its submissions on this issue. In doing so, the Review Panel relied on Robertson J’s decision in Steelforce Trading Pty Ltd v Parliamentary Secretary to the Minister for Industry, Innovation and Science [2016] FCA 1309 (Steelforce) at [110]-[111]. His Honour held there that the use of third country information was available on the terms of s 269TAC(2)(c).

48 Longte contended that Robertson J’s decision on this issue was plainly wrong and should not be followed. At the time of the hearing of the present proceeding the Full Court had reserved its decision in an appeal from Robertson J’s decision in Steelforce. Accordingly, by consent, the hearing of grounds 1 to 4 of Longte’s judicial review application was deferred until after the Full Court published its judgment. The Full Court’s decision in Steelforce Trading Pty Ltd v Parliamentary Secretary to the Minister for Industry, Innovation and Science [2018] FCAFC 20 (Steelforce Full Court) was published on 19 February 2018.

49 The parties made supplementary written submissions in respect of grounds 1 to 4 having regard to the Full Court’s decision.

50 Longte conceded that ground 1 in these proceedings must be dismissed following Steelforce Full Court. As noted above, the central argument which underpinned Longte’s submissions on ground 1 is that, for the purposes of s 269TAC(2)(c)(i) of the Customs Act, s 43(2) of the Regulation prescribes the only source of information by which the amount of the cost of production is to be determined. This argument was rejected by the Full Court in Steelforce Full Court. Justice Perram considered that the methodology in s 43 was “not an exhaustive statement on the topic of how production costs are to be determined” and that, outside of the situation referred to in s 43, s 269TAC(2)(c)(i) remained applicable “on its own terms” (at [108]; Pagone and Bromwich JJ agreeing at [128] and [137] respectively). Although Longte formally submitted that it did not accept the correctness of Perram J’s reasoning, it recognised that the Court was bound to follow that reasoning and to dismiss ground 1.

51 Longte contended that Perram J’s reasoning did not prevent the Court from upholding grounds 2, 3 and 4 in the present proceedings. Both Longte and the applicant in Steelforce Full Court argued that s 269TAC(2)(c)(i) required the determination of the cost of production in the country of export, which did not permit the use of prices paid in other countries (see [4(b)] above and Steelforce Full Court at [113(a)]). Although Perram J rejected this argument in concluding that s 269TAC(2)(c)(i) is not offended “as long as the exercise being embarked upon was in substance the calculation of the cost of production in China” (Steelforce Full Court at [116]), Longte emphasised that Perram J added that, where foreign pricing information is used, it will be necessary to consider any comparative advantages or disadvantages that producers in the country of export have over the producers from whose activities the foreign pricing information has been collected, and this is a mandatory relevant consideration (at [118]). Justice Perram concluded that the Commissioner in Steelforce Full Court had in fact considered the issue of comparative advantage and thus there was no failure on the Commissioner’s part to take account of a mandatory relevant consideration. The Commissioner concluded that it was not possible to adjust the benchmark for the comparative advantages of the Chinese producers compared with other producers in that case (at [119]).

52 In the present proceedings, Longte submitted that, unlike the situation in Steelforce Full Court, there was no consideration given to the advantages and disadvantages that producers in China enjoyed as compared to producers whose goods underpinned the Latin-American benchmark, nor was any consideration given to whether adjustments were reasonably possible. For these reasons, Longte submitted that the Minister’s decision is invalid.

53 Longte also formally advanced an argument which it acknowledged was not consistent with the reasoning in Steelforce Full Court, namely, that adjustments must be made to foreign pricing information to reflect the advantage/disadvantage of producers in the country of export, and the resulting figure must be capable of being considered to be the cost of production in the country of export. If the benchmark does not represent the cost of production in the country of export and no adjustments are feasible to rectify this, then there is insufficient information to use s 269TAC(2)(c), with the result that the Minister would need to use the method in s 269TAC(2)(d) or the method in s 269TAC(6), so Longte submitted.

Grounds 5 to 7 : Determination of profit

54 Longte submitted that the effect of s 269TAC(5B) of the Customs Act is to require s 45 of the Regulation to be used in determining the amount of profit under s 269TAC(2)(c)(ii).

55 As noted in [44] above, after considering Longte’s submissions on the SEF, the Commissioner revised the construction of normal values for all exporters after accepting Longte’s submission that, by uplifting steel billet cost used in the grinding bar competitive benchmark by percentages derived in the Chinese exporters’ actual records, the Commissioner had unnecessarily inflated conversion costs and selling, general and administrative expenses. The Commissioner declined, however, to revise his calculation of an amount of profit. Longte contended that this was contrary to s 45(2) of the Regulation. Longte specifically referred to [78] of Report 47, in which the Review Panel stated:

The Commission did determine an amount of profit. However, the process by which it determined an amount of profit involved ascertaining a profit ratio as a preliminary step, then applying that ratio to the substituted cost of production to arrive at an amount of profit.

56 Longte contended that there is an inconsistency in the approach of both the Commissioner and the Review Panel. It said that this involved a “hybrid application of the costs in Longte’s actual records, in the preliminary step of obtaining a profit margin, and the substituted costs relied on for the purposes of s 269TAC(2)(c)(i)”. Longte contended that using a percentage figure for profit was insufficient and wrong; rather, an amount or figure representing profit had to be used. It contended that using a percentage figure had a disproportionate impact on the determination of the amount of profit. Longte also submitted that the use of a profit margin was in error because this did not involve an “amount”, as required by s 45(2) of the Regulation.

57 Longte contended that if the Commissioner had adopted the correct approach in determining the cost of production or manufacture for the purposes of s 269TAC(2)(c)(i), those same costs should have been used to determine profit for the purposes of s 269TAC(2)(c)(ii).

58 Mr Lloyd SC (who appeared together with Ms Mitchelmore for Longte) relied upon the following aide memoire to illustrate the alleged flaws in the Commissioner’s calculation of profit, which was adopted by the Review Panel. Hypothetical monetary amounts were used to illustrate the various steps adopted by the Minister in arriving at his final decision:

1. The numbers can be conceived as applicable to a manufacturer of widgets in China, which exports to Australia (numbers are per widget):

a) Export price: $55.

b) Sale price in China: $55

c) Actual cost of production in China: $40

d) Administrative, general and selling costs in China: $10

e) Total costs: $50

2. If s 269TAC(1) applies, normal value is domestic sale price: $55. No dumping (as export price equals normal value).

3. If s 269TAC(2)(c) applied and the exporters [sic] records could be used, the constructed normal value would be amount for cost of production ($40) + amount for selling, general and admin costs ($10) + amount of profit ($5) = $55. Given export price, no dumping.

4. If contrary to applicant’s case, Latin American costs can be substituted for domestic Chinese costs of production, assume they are $80 (instead of $40):

a) Then total costs would be $80 + $10 = $90

5. If one determines profit by domestic sales at $55 and costs of $90: profit is zero (no negative amount allowed). (Or rather, there are no sales in the ordinary course of trade and so s 45(2) of the Regulations is unavailable.)

6. If one ignores ordinary course of trade test under s 45(2) and just uses actual Chinese data, then profit amount per widget is $5 (profit equals sales price minus total costs).

7. Minister expressed profit not as $5 but as 10% profit margin (return above cost base).

8. Minister then calculates normal value as $80 + $10 + 10% of total costs = $90 + 10% == $99.

9. Minister identified amount of profit ($9) as one greater than that enjoyed on goods that were actually sold in domestic sales ($5).

59 In relation to ground 7 of its judicial review application, Longte contended that the manner in which the Review Panel sought to justify its approach to calculating profit in [76] of Report 47 highlighted the illogicality of which Longte complained. The Review Panel said there:

In its submission, the Commission justified its approach to determining the amount of profit by referring to a discussion at pages 51 to 52 of the Australian Customs and Border Service Report 177. The approach described in that Report involves calculating a profit margin based on the non-substituted costs of the producer. It proceeds on the assumption that, if the market situation did not exist, exporters would achieve the same return on investment in percentage terms that they achieved under the market situation and that this profit margin should be applied to the (substituted) costs determined by the Commission. The assumption that the same profit margin would be achieved is a reasonable one and is consistent with the objective of determining a normal value which reflects arms length transactions in a competitive market. In determining the profit margin, or return on investment, which the producers achieved in reality, the Commission looked at whether goods were sold below the cost of production and applied the OCOT approach to arriving at that profit ratio. This approach reflects the process that would have been followed had the Commission not concluded that it was necessary to use the Benchmark to determine the costs of production or manufacture. I consider that this approach to determining the profit component of the normal value was reasonable.

60 Longte contended that this passage revealed that the Review Panel used two economic concepts interchangeably (i.e. return on investment and profit margin), whereas by reference to economic principle the two concepts cannot be equated. Longte relied on an expert report by Mr Greg Houston in support of this claim.

61 With reference to [76] of Report 47, Longte acknowledged that Report 177 was an appropriate starting point and was accurately referred to by Review Panel in [76], but it contended that the Review Panel then erred in what it said later in [76] by equating return on investment (which was considered in Report 177 at pp 50-51) with profit margin. Longte submitted that it was the “conflation” of these two separate concepts which lay at the heart of the error.

62 Longte criticised Dr Fahrer’s opinion on this matter in [113] of his report dated 6 November 2017, which was put into evidence in relation to ground 7 by the respondents following my earlier decision in Changshu Longte Grinding Ball Co., Ltd v Parliamentary Secretary to the Minister for Industry, Innovation and Science (No 1) [2017] FCA 1114. It is convenient to set out that part of Dr Fahrer’s evidence which relates specifically to [76] of Report 47 and to respond immediately to Longte’s criticisms of Dr Fahrer’s evidence:

(a) Is the assumption ascribed to Australian Customs and Border Service Report 177 (pp 51-52) feasible as a matter of economic theory?

113 My reading of “the same return on investment in percentage terms” is that this means the same profit margin, where profit margin is expressed as a percentage of revenue. On this reading, the assumption referred to in the question is feasible. The return on an investment i.e. profit, sought and able to be achieved by producers will reflect demand and supply conditions in the market. A market situation could change the price in the market, but it need not necessarily change the profit made by the producer, and even if it does, it need not change the return on investment.”

63 Dr Fahrer was closely cross-examined on this passage and the correctness of his reading of the phrase “the same return on investment in percentage terms”. He contrasted the use of that phrase with the phrase “rate of return on investment”. Dr Fahrer accepted that the concepts of return on investment and profit margin expressed as a percentage of sale price were different measures of a firm’s rate of profitability. He said, however, that he read the phrase “return on investment” in [76] of Report 47 as referring to profit margin. Dr Fahrer acknowledged that it would have been more accurate if [113] of his Report referred not to “necessarily change the profit”, but to “necessarily change the profit margin”. This did not derogate, however, from the way he understood the meaning of [76] of Report 47.

64 Longte submitted that no weight should be given to Dr Fahrer’s opinion relying upon the answers he gave under cross-examination. I reject that submission. I accept Dr Fahrer’s opinion and comments relating to [76] of Report 47 and to the evidence which I have summarised immediately above. Dr Fahrer’s reading of the relevant phrases accords with my own. It is important to bear in mind the well settled principle that such reasons need to be read fairly and not with an eye keenly attuned to detecting error. In addition, I prefer Dr Fahrer’s view and his reasons for rejecting Mr Houston’s absolute and unqualified view that there are no circumstances under which it may be assumed that, as costs of production increase, profits likewise increase at the same rate so as to maintain the same profit margin. Dr Fahrer made clear that he was not suggesting that it will always be the case that profits will be able to be maintained after a cost increase. Dr Fahrer acknowledged that, in some circumstances, a firm will be unable to increase its profits and maintain its profit margin after a cost increase but he was firmly of the view that this will not always be the case (see, in particular, the Joint Expert Report dated 30 November 2017 at [54]-[56] and [79]-[87] for a summary of Dr Fahrer’s views and his comments on Mr Houston’s contrary opinion). I accept Dr Fahrer’s evidence.

65 Longte confirmed in oral address that ground 7 was directed to both outcome and the methodology used in arriving at that outcome. It submitted that because the Minister had rejected the data concerning actual cost of production in China (which it substituted with a Latin-American benchmark), it should also have determined that s 45(2) was not practically available on the basis that the data was inadequate or unreliable to calculate profit. Nevertheless, the Minister inappropriately used that data to determine a profit margin based on the actual cost base pursuant to s 45(2), when he should have used the methodology in s 45(3), so Longte submitted.

66 Longte submitted that this was unreasonable, illogical and irrational citing Minister for Immigration and Citizenship v Li [2013] HCA 18; 249 CLR 332 (Li) and Minister for Primary Industries and Energy v Austral Fisheries Pty Ltd [1993] FCA 46; 40 FCR 381 per Lockhart, Beaumont and Hill JJ (Austral Fisheries). In the latter case, it was held that the use of a formula which contained a serious statistical fallacy produced an irrational or absurd result in allocating fishing quotas under a plan of management made under the Fisheries Act 1992 (Cth).

The respondents’ submissions summarised

67 It is convenient to summarise the respondents’ submissions by reference to grounds 1 to 4 and 5 to 7 inclusively.

Grounds 1 to 4 : Determination of cost of production or manufacture in the country of export

68 The respondents’ central submission was that the Court should not accept Longte’s contention that, where s 269TAC(1) does not apply by reason of a market situation, s 269TAC(2) may apply. Rather, they submitted that where the Minister is satisfied that the normal value of goods exported to Australia cannot be ascertained under s 269TAC(1) because sales in the market of the country of export are not suitable for use in determining a price under s 269TAC(1) then, unless s 269TAC(2)(d) applies, s 269TAC(2) stipulates that the normal value of the goods is the sum of the amounts referred to in s 269TAC(2)(c). This means that, absent that single exception (which is inapplicable here), where a particular market situation has been found to exist, the normal value of the goods must be determined in accordance with s 269TAC(2)(c), and this is what the Commissioner and Review Panel did.

69 As to Steelforce Full Court, the respondents’ supplementary submissions may be summarised as follows. The Full Court supported the primary judge’s conclusion that there is no prohibition in s 269TAC(2)(c)(i) on the use of foreign pricing information (Steelforce Full Court at [116], [128], [135] and [137]). Insofar as grounds 2 and 3 are predicated on such a prohibition, the respondents submitted that those grounds must fail, as also must ground 1.

70 As to ground 4, it was submitted that this ground is concerned with the treatment of foreign pricing information and Steelforce Full Court supports the conclusion that this ground should fail. With respect to Longte’s submission that Steelforce Full Court stands for the proposition that it is a mandatory relevant consideration for the decision-maker to consider any comparative advantage/disadvantage which producers in the country of export have over foreign producers whose pricing information have been used, the respondents submitted that this is not the principle which should be drawn from the Full Court’s decision. Justice Perram’s reference to “comparative advantage” should be understood as reflecting the circumstances of that case, where an adjustment described in those terms had been urged upon and considered by the decision-maker. Section 269TAC(2) does not support the implication of a mandatory relevant consideration framed with that level of particularity, so it was submitted.

71 The respondents contended that in the present case, as in Steelforce Full Court, the Commissioner established a competitive grinding bar benchmark and then considered whether adjustments were possible and appropriate. The Commissioner made some adjustments, notably in relation to conversion costs and grades of grinding bar, and rejected others proposed by the exporters (Report 316 at pp 25 and 33). The respondents also emphasised that it should be inferred from the Commissioner’s rejection of the other proposed adjustments that he was pursuing the statutory objective of determining costs in the country of export, as required by s 269TAC(2)(c)(i). They referred to pp 27-28 of Report 316 (see also p 29) and the Commissioner’s explanation there for rejecting adjustments concerning:

(a) inland transport costs;

(b) adjusting the external benchmark to reflect a level of profit contained therein; and

(c) the use of cost data extending six months beyond the investigation period to reflect the lag in Latin American steel billet prices to Chinese billet prices.

72 In response to Longte’s submission summarised at [53] above, which was acknowledged to be inconsistent with the reasoning in Steelforce Full Court, the respondents submitted that for the purpose of the present proceeding and the fate of grounds 2 and 4, it was sufficient to note that Longte has not demonstrated that the benchmark did not represent the cost of production in the country of export, either as a matter of the choice of a benchmark per se (which argument would fall foul of Steelforce Full Court at [116]), or as a matter of the process or method of adjustment. It was submitted that to the extent Longte’s argument canvassed the appropriateness of the adjustments, it strayed impermissibly into the merits of the decision.

Grounds 5 to 7 : Determination of profit

73 The respondents urged the Court to reject Longte’s claim that the Commissioner’s calculation of profit was not done in accordance with s 45(2) of the Regulation. In particular, the respondents submitted that Longte’s complaint of a “hybrid application” of actual costs and substituted costs should not be accepted.

74 The respondents handed up the following document headed “Respondents’ aide memoire on determining profit”, which responded to Longte’s aide memoire:

1. Assume the following costs and prices, per widget.

Export price: $55

Sale price in China: $55

Actual cost of production: $40

SGA costs in China: $10

So for domestic sales, total costs are $50 and profit is $5 (10% of costs)

2. If s 269TAC(1) applies, normal value is $55. No dumping.

3. Now assume a “market situation” under s 269TAC(2)(a) in which costs of production are distorted.

The undistorted production cost is found to be $42 and this figure is determined under s 269TAC(2)(c)(i) (“substituted cost”).

SGA costs are not affected by the market situation and are determined as $10, using the exporter’s records.

4. If profit is calculated using the substituted cost:

Production cost (determined under (c)(i)) = $42

SGA = $10

Profit = ($55 - $52) = $3 (Noting that the domestic sales at $55 remain profitable on this assumption and qualify as sales in the ordinary course of trade, for purposes of reg 45(2))

Normal value = $55 (same as the actual domestic selling price)

5. If profit is calculated using the exporter’s actual cost, in dollars:

Production cost (determined under (c)(i)) = $42

SGA - $10

Profit = ($55 - $50) = $5 (as in para 1)

Normal value = $57

There is then a $2 dumping margin.

6. Or if profit is calculated using the same date but as a percentage:

Production cost (determined under (c)(i)) = $42

SGA - $10

Profit = 10% of the total costs = $5.20

Normal value = $57.20

Dumping margin = $2.20

75 Mr Kennett SC (who appeared for the respondents with Ms Younan) clarified that the reference to “undistorted production costs” in [3] of the aide memoire is a reference to substituted costs rather than the exporter’s actual costs. He also clarified that [4] was intended to reflect Longte’s case as to the appropriate manner for calculating profit, that is, using the substituted cost base in the profit calculation. He emphasised that if that case is accepted it produces the same normal value (i.e. $55) as the actual domestic selling price which, in itself, discloses the problem with that approach. He submitted that Longte’s approach (reflected in [4]) undermines the purpose of s 269TAC(2) which is intended to be applied where there is a market situation and the methodology in s 269TAC(1) cannot be applied. In other words, if the amount of profit is calculated using substituted costs, the same normal value is arrived at in [4] as under [1], which Mr Kennett SC contended defeated the purpose under s 269TAC(2).

76 Mr Kennett SC explained that [5] and [6] of the respondents’ aide memoire were intended to reflect the outcome of calculations which are based on a dollar figure for profit as opposed to a percentage. He acknowledged that the choice between those approaches resulted in different dumping margins ($2 in the case of using dollar figures and $2.20 when using a percentage). He submitted that it was a matter for judgment by the decision-maker as to whether the calculation should be made by reference to actual dollars or a percentage figure in order to achieve a sensible outcome.

77 In reply, Mr Lloyd SC criticised this submission, primarily on the basis that it did not give effect to the significance of the use of the word “amount”. A dollar figure is an “amount”, but a percentage figure is not, so he submitted. Mr Lloyd SC drew attention to the fact that the word “amount” appears in both ss 44 and 45 of the Regulation.

Longte’s supplementary submissions in reply on Steelforce Full Court

78 It is expedient to summarise here Longte’s supplementary written submissions in reply, which were filed with the Court’s leave and the respondents’ consent. Longte submitted that its construction of the scope of the mandatory relevant consideration was clearly correct having regard to Perram J’s formulation of the consideration as arising “by implication drawn from s 269TAC(2)(c)(i) itself” (Steelforce Full Court at [118]). The submission was repeated that the decision-maker in the present case failed to consider the costs of production in China and the associated advantages/disadvantages that producers had with respect to those costs as compared with producers whose goods made up the Latin American Benchmark. In Steelforce Full Court, it was held that the Commissioner was “alive to this issue” but was unable to assess the comparative differences (at [111]). Longte claimed that the reports here did not demonstrate any corresponding awareness.

79 Longte submitted that the respondents adopted too narrow a reading of Perram J’s reasons. What his Honour said there was that use of foreign pricing information was not objectionable “[s]o long as the task being performed… remains in fact the determination of the cost of production in the country of origin”, and this task was not fulfilled in the absence of considering the mandatory relevant consideration.

Consideration and disposition of the judicial review application

80 It is convenient to consider judicial review grounds 1 to 4 before grounds 5 to 7.

Grounds 1 to 4 : Determination of cost of production or manufacture in the country of export

81 As noted above, Longte acknowledged that ground 1 had to be rejected because the Court was bound to follow Steelforce Full Court which, it conceded, is inconsistent with its position that third country information cannot be used at all in determining the cost of production or manufacture in the country of export.

82 Longte contended that grounds 2, 3 and 4 were supported by Steelforce Full Court. In particular, Longte contended that where foreign pricing information is used, as is the case here, any comparative advantages or disadvantages that the producers in the country of export have over producers from which the foreign pricing information has been obtained is a mandatory relevant consideration. It contended that this mandatory relevant consideration was not addressed by either the Commissioner or the Review Panel.

83 Longte’s submission relies heavily on what Perram J said in Steelforce Full Court at [118] (emphasis added):

118. The words ‘cost of production…in the country of export’ in s 269TAC(2)(c)(i) direct attention to the determination of an amount. The amount must have two qualities. It must be for production of the goods and it must be assessed on the basis that the goods have been produced in the country of export. Where a decision is made to seek to determine this amount using foreign pricing information it is necessary for the Commissioner to take into consideration any comparative advantages or disadvantages that the producers in the country of export have over the producers from whose activities the foreign pricing information has been collected. This is an implication from s 269TAC(2)(c)(i) itself and it means that when foreign pricing information is used to determine a normal price under s 269TAC(2)(c)(i) then the comparative advantages (and disadvantages) enjoyed by domestic producers are mandatory relevant considerations in the sense that expression is used in Minister for Aboriginal Affairs v Peko-Wallsend Ltd [1986] HCA 40; (1986) 162 CLR 24 at 39-41.

84 There are several points to make regarding Perram J’s statements in [118], which were directed to ground 5 in that appeal. The first is that it is not clear that the statements which are emphasised in the passage above form part of the ratio of the Full Court’s decision. Justice Pagone stated in [128] of Steelforce Full Court that he agreed with all but one of Perram J’s “conclusions”, leaving it unclear whether or not his Honour agreed with all of Perram J’s reasoning on the other grounds of appeal (i.e. grounds 1 to 3 and 5), all of which failed. Justice Pagone explained why he disagreed with Perram J’s conclusion that appeal ground 4 should succeed. Justice Bromwich agreed with Perram J that appeal ground 4 was established. In respect of appeal ground 5 in Steelforce Full Court, which was the ground which was the subject of Perram J’s statements in [118], Bromwich J gave his own brief reasons in [137(5)] of his Honour’s reasons for judgment for upholding that particular ground. His Honour was silent as to whether he agreed with all of Perram J’s reasoning on this ground. In those circumstances, I have strong doubts that Perram J’s views as set out in [118] are binding on me as appellate authority.

85 Secondly, in any event, it is important that Perram J’s statements in [118] not be divorced from the way in which the appeal was conducted in Steelforce Full Court. It is equally important that the statements be read and understood having regard to the balance of his Honour’s reasons for judgment. Those matters are now elaborated upon.

86 It is evident that the appeal in Steelforce Full Court was conducted on the basis that there was material before the administrative decision-makers there which indicated that Chinese producers had both comparative advantages and disadvantages over the foreign producers whose pricing information was used to calculate the cost of production in China. This is confirmed by parts of the written and oral submissions of the appellants in that appeal, copies of which were put in evidence before me (see [39] of the appellants’ outline of submissions dated 4 April 2017 in that appeal and the transcript of the hearing at pages 44 and 65). Although the precise nature of those advantages and disadvantages are not made clear in that material, it may be observed that at [110] of Steelforce Full Court, Perram J referred to “any advantages Chinese producers of HRC had by way of lower labour costs or lower costs of capital” in giving an example of how adjustments might need to be made. I accept the respondents’ submission that Perram J’s reference to “comparative advantages and disadvantages” have to be understood as reflecting the circumstances of that particular case and where the appellants had contended that adjustments had to be made because of identified comparative advantages and disadvantages. In highlighting these features of Steelforce Full Court, I do not overlook that the task of determining what is a mandatory relevant consideration normally falls to be determined by reference to the relevant statutory context and not particular factual matters (see the tentative observations in Abebe v The Commonwealth of Australia [1999] HCA 14; 197 CLR 510 at [195] per Gummow and Hayne JJ). An important feature of the statutory scheme here is the opportunity afforded to interested parties to make submissions and the obligation of the Commissioner to have regard to those submissions. I consider that Perram J’s view as expressed in [118] has to be read in the context of the particular facts and circumstances in which the issue arose in that appeal.

87 It is relevant to also have regard to other aspects of Perram J’s reasoning, particularly what his Honour subsequently said in [124] concerning the issue whether it was mandatory in determining the cost of production in the country of export in cases involving foreign pricing information to make actual adjustments for comparative advantages or disadvantages. Such a contention appears to have been made by the appellants in Steelforce Full Court, who cited a decision of the Appellate Body of the World Trade Organization in Appellate Body Report, European Union – Anti-Dumping Measures on Biodiesel from Argentina, WTO Doc WT/DS473/AB/R (6 October 2016), the relevant passage from which is set out in his Honour’s reasons for judgment at [123]. That passage from that decision (at [6.73]) includes a statement that, whatever information is used by an investigating authority in determining the cost of production in the country of origin, this “may” require the investigating authority to adapt the information that it collects. In response to that submission, Perram J said at [124]:

124. I do not read the Appellate Body as saying that adaption of the foreign pricing information is mandatory. The word it used was ‘may’. This connotes to my mind that in some cases adaption may not be necessary. I would accept that the passage at 6.73 requires an investigating body to consider the topic of adjustment and this accords with my own view that adjustment in cases involving foreign price information is a mandatory relevant consideration. But further than this I do not think it goes.

88 This may suggest that his Honour put a gloss on the view he expressed earlier in [118] in the sense that he appears to state in [124] that adjustment in cases involving foreign price information is itself a mandatory relevant consideration. There is considerable force in the respondents’ submission that the terms of s 269TAC(2) do not support the implication of a mandatory relevant consideration expressed at that level of particularity (see Foster v Minister for Justice and Customs [2000] HCA 38; 200 CLR 442 at [23] per Gleeson CJ and McHugh J). With respect, it is not easy to reconcile what his Honour said in [118] with what he subsequently said in [124].

89 Thirdly, and in any event, I reject Longte’s submission that the Commissioner here did not consider and determine whether comparative advantages or disadvantages existed and warranted the making of adjustments. As noted above, some adjustments were made to the benchmark, while others were rejected (see [43]-[44] above). Moreover, although the Commissioner’s consideration of whether or not to make adjustments focused primarily on adjustments to the benchmark, it is also evident that he turned his mind to the need to make adjustments vis à vis the Chinese exporters, including in respect of their inland transportation costs (see [43] above).

90 For these reasons, I reject Longte’s claims in grounds 2, 3 and 4. For completeness, I also reject its formal contention that where no adjustments are feasible there is insufficient information to use s 269TAC(2)(c). As Longte appreciated, that submission is inconsistent with Steelforce Full Court at [108], [128] and [137].

Grounds 5 to 7 : Determination of profit

91 I reject Longte’s claims that it was a reviewable error to have a “hybrid application” of actual costs and substituted costs. Where a market situation exists, normal value is constructed under s 269TAC(2)(c) by adding together the following two elements:

(a) the amount determined to be the cost of production of the goods exported to Australia in the country of export (which amount is determined in accordance with any relevant method prescribed in the Regulation as required by s 269TAC(5A)) or, alternatively, from data from other countries where s 43 of the Regulation does not apply, as approved in Steelforce Full Court; and

(b) the amounts determined to be the administrative, selling and general costs as well as profit, on the assumption that the goods, instead of being exported, had been sold for home consumption in the ordinary course of trade in the country of export.

92 Both these elements are arrived at by independent processes and there is no illogicality in using different bodies of data for the two processes. The calculation of profit for the purposes of s 269TAC(2)(c)(ii) is a separate exercise from a calculation of the cost of production for the purposes of s 269TAC(2)(c)(i). Having regard to that distinction, it is not unlawful to use substituted costs for the purposes of one calculation but not the other. I see nothing in the legislative regime which prevents that approach. I also accept the respondents’ submission that adoption of the approach urged by Longte would defeat the purpose of s 269TAC(2) which is intended to be applied where there is a market situation and the methodology in s 269TAC(1) cannot be applied, as the respondents’ aide memoire revealed (see [75] above). Longte’s approach does not make sense when it is applied against the background of a finding that a market situation exists.

93 Although it can make a difference whether the calculation of an amount of profit is made using dollar amounts or a percentage figure (see [76] above), I accept the respondents’ submission that the choice is a matter for judgment by the decision-maker in arriving at a sensible outcome which is not inconsistent with the legislative regime. It was not irrational or unreasonable for the Commissioner and the Review Panel to adopt the methodology they used, where there was a finding of a market situation. Section 269TAC(2)(c)(ii) permits a method of calculation to be used which overcomes the market situation and produces a price which is unaffected by that market situation.

94 As the respondents acknowledged, there may be a “lack of symmetry” in a case where costs of production have been determined in a different way for the purpose of s 269TAC(2)(c)(i) when s 45(2) of the Regulation requires the profit on hypothetical sales to be worked out by using data relating to production and sale of like goods by the exporter in the country of export. This, however, is a direct consequence of the terms of the Regulation. There is nothing in the legislative regime to prevent Longte’s actual cost of production data being used for the purposes of calculating profit under s 45, notwithstanding that that data had not been used in the different process of calculating cost of production.

95 Nor is there any reviewable error in the Commissioner’s use of unadjusted records of production costs to work out, in the course of applying s 45, which of Longte’s domestic sales of like goods were sales in the ordinary course of trade. This approach is consistent with the language and purpose of s 269TAAD and s 43 of the Regulation does not prevent that approach.

96 I do not accept Longte’s submission that the use of a profit margin expressed as a percentage was contrary to s 45(2) of the Regulation because it said that this did not involve working out “an amount” as being the profit on the sale of goods, as required by s 45(1). According to the Macquarie Dictionary, the primary meaning of the word “amount” is “quantity or extent”. Viewed in context, I see no legal reason why a percentage figure cannot be used as part of the methodology in arriving at an amount of profit. As the Review Panel correctly observed in Report 47, “the process by which [the Commissioner] determined an amount of profit involved ascertaining a profit ratio as a preliminary step, then applying that ratio to the substituted cost of production to arrive at an amount of profit”. No reviewable error has been established with this methodology.

97 As noted in [65] above, Longte’s contention that the Minister’s final decision is unreasonable or illogical, is directed to both the outcome of that decision and the methodology used in reaching it. In closing address, Longte confirmed that there were two aspects to ground 7. The first was that [76] of the Review Panel Report reveals a misunderstanding as to key economic concepts, namely “return on investment” and “profit margin”. The second aspect is that the assumption made in that paragraph, that it is reasonable to assume that as costs of production rise profits can increase at the same rate, was unreasonable, irrational or illogical.

98 For the following reasons, I do not consider that the language used in [76] of the Report 47 reveals reviewable error. Fairly read, I consider that, while there is some looseness in the language, neither the Review Panel nor the Commissioner equated profit margin with return on investment. As I have said, it is well established that the reasons of an administrative decision-maker are not to be read with an eye keenly attuned to detecting error. The experts were agreed that the concept of “profit margin” and “return on investment” are different economic concepts. I agree, however, with Dr Fahrer’s reading of [76], which is that the phrase “return on investment”, when read in context, refers to profit margin (see [63] and [64] above). Thus the reference in [76] to “the same return on investment in percentage terms” is best understood as meaning the same profit margin, where profit margin is expressed as a percentage of revenue.