FEDERAL COURT OF AUSTRALIA

Lynch v Cash Converters Personal Finance Pty Ltd (No 4) [2018] FCA 988

ORDERS

NSD 900 of 2015 | ||

Applicant | ||

AND: | CASH CONVERTERS PERSONAL FINANCE PTY LTD ACN 110 275 762 First Respondent SAFROCK FINANCE CORPORATION (Qld) Pty Ltd ACN 098 566 520 Second Respondent | |

GLEESON J | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The respondents provide written answers to interrogatories 1(f), (g), (i), (j), 2-4 and 9-12 in the amended draft notice of interrogatories filed 25 June 2018.

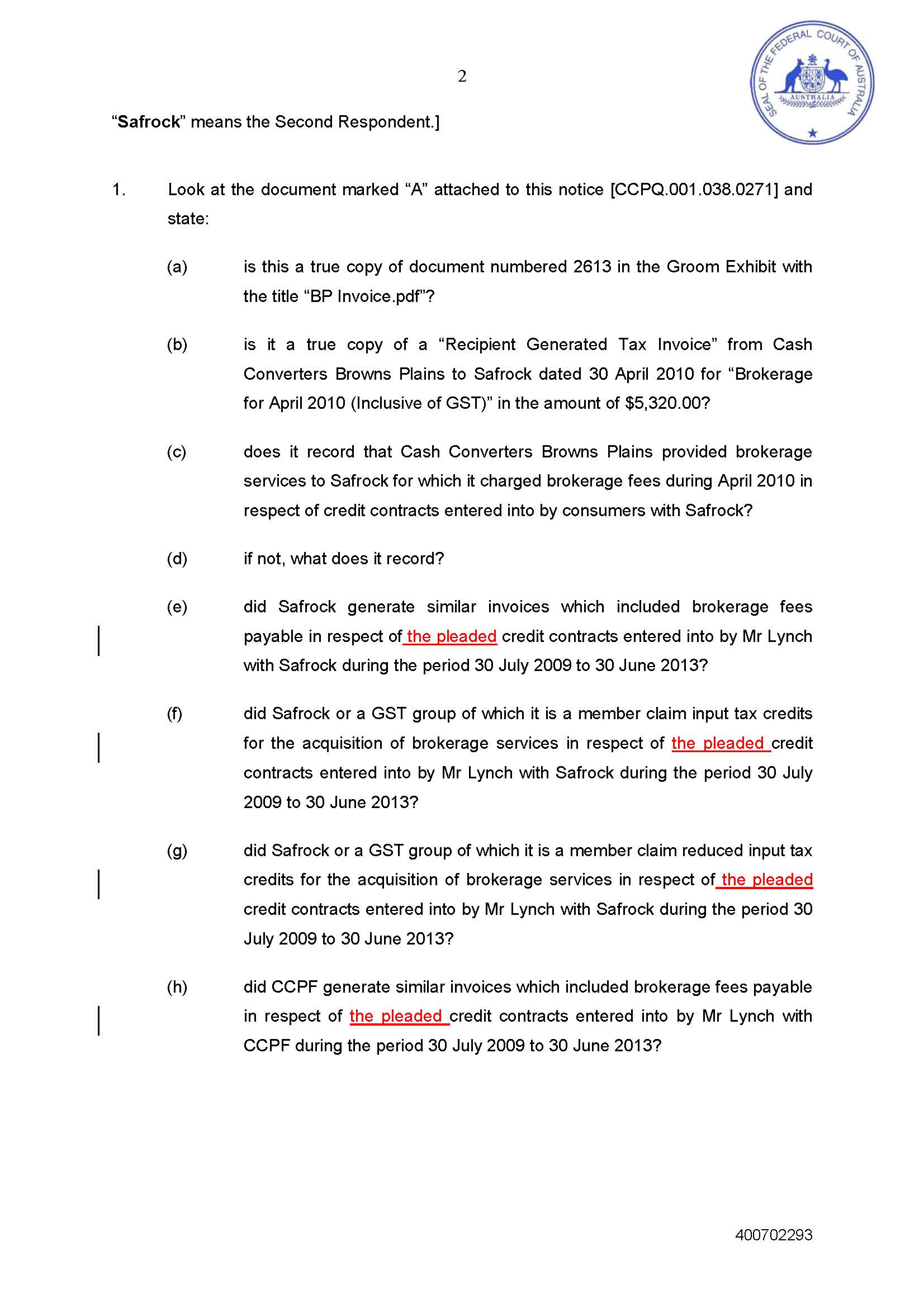

2. The respondents pay the applicant’s costs of the application for order 1 above.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

NSD 601 of 2016 | ||

BETWEEN: | KIM McKENZIE Applicant | |

AND: | CASH CONVERTERS INTERNATIONAL LIMITED (ACN 069 141 546) First Respondent CASH CONVERTERS (CASH ADVANCE) PTY LTD (ACN 127 866 308) Second Respondent CASH CONVERTERS (STORES) PTY LTD (ACN 127 343 293) Third Respondent BAK PROPERTY PTY LTD (ACN 103 054 824) Fourth Respondent | |

JUDGE: | gleeson j |

DATE OF ORDER: | 29 june 2018 |

THE COURT ORDERS THAT:

1. The respondents provide written answers to interrogatories 2-7 and 9-11 in the amended draft notice of interrogatories filed 25 June 2018.

2. The respondents pay the applicant’s costs of the application for order 1 above.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GLEESON J:

1 In each proceeding, the applicant has sought leave to administer interrogatories in connection with the issue of whether a “brokerage fee” was for services supplied to the respondents (“Cash Converters”), and not to the relevant applicant.

2 Cash Converters opposed the grant of leave on grounds explained below.

3 After the hearing on 22 June 2018, the applicants amended several of the proposed interrogatories to limit them by reference to the contracts that are identified in the statements of claim in each matter: in the Lynch proceeding (NSD900/2015), there are three relevant credit contracts; in the McKenzie proceeding (NSD601/2016), there are three tranches of cash advances. The amended draft interrogatories in the Lynch proceeding (not including annexures) are set out in annexure A to these reasons for judgment, while the amended draft interrogatories in the McKenzie proceeding (also not including their annexure) appear in annexure B.

4 It is convenient to consider the applications primarily by reference to the Lynch proceeding in the first instance. The outcome of the application in the McKenzie proceeding follows the outcome of the application in the Lynch proceeding.

Outline of Lynch proceeding

5 The Lynch proceeding concerns three loans obtained by Mr Lynch in Queensland. These loans are described in the affidavit of Mr Peter Butler, the respondents’ solicitor, sworn 21 June 2018 as follows:

(1) The first loan was obtained on 26 August 2010 through the Goodna store. At this time, the Goodna store was a franchised store that was shortly thereafter acquired by Cash Converters on 1 September 2010.

(2) The second loan was obtained on 1 June 2012 through the Inala store. The Inala store was at this time and continues to be a franchised store owned by an entity which is and always has been independently owned and operated from the Cash Converters group of companies.

(3) The third loan was obtained on 27 October 2012 through the Goodna store. The Goodna store was at this time and continues to be a part of the Cash Converters corporate group.

6 Mr Lynch contends that Cash Converters engaged in unconscionable conduct in contravention of s 12CB(1) of the Australian Securities and Investments Commission Act 2001 (Cth) by their entry into the relevant loan arrangements. He contends that brokerage fees paid by him in connection with the loans were a mechanism designed to ensure that the lender received a return greater than the statutory cap provided for under the Credit (Commonwealth Powers) Act 2010 (Qld). Mr Lynch also pleads that the services for which the brokerage fees were paid were illusory. The case includes allegations to the effect that Mr Lynch did not receive any benefit for the brokerage fee and that it was not a necessary part of organising the loan contracts. Mr Lynch’s case has recently been amended to include further allegations explained below, which have given rise to his application to administer interrogatories.

New issue concerning recipient of brokerage services

7 The interrogatories are sought following the applicants’ identification of six documents discovered by Cash Converters. As Ms Miranda Nagy, the applicants’ solicitor, put it in her affidavit affirmed 21 May 2018, these documents may indicate that Cash Converters’ tax treatment of the pleaded brokerage fees was reflective of a transaction whereby brokerage fees on each credit contract were payable by the lender to the broker for services provided by the broker to the lender (and the consumer reimbursed the lender that amount).

8 In chronological order, the first document is an email chain comprising two emails between Guy Noakes, Principal of Deloitte Touche Tomatsu Ltd (“Deloitte”), and Ralph Groom, Company Secretary and Group financial Controller of Cash Converters International, dated 14 October 2008. In the first email, Mr Groom relevantly writes:

GST issue for you.

We are proposing a broker arrangement in Queensland through which we will transact cash advance loans. This structure is being proposed to avoid the capped interest rates the government recently introduced. Basically the structure will consist of a company (the lender) who lends money to a cash advance client via another company (the Broker).

The lender charges, say 2% on the loan to the client and the broker charges a 33% brokerage fee (this then equates to the 35% currently charged under cash advance loans).

Is GST applicable to the brokerage fee? If GST is applicable then is it possible to claim a portion of the GST as an input credit or is it totally exempt as a financial service?

In response, Mr Noakes provides certain advice on alternate assumptions concerning the recipient of the brokerage services. Mr Noakes concludes:

The specific GST application to this proposal will depend on the details of the arrangements entered into by the parties and the nature of the services etc that are being supplied by each particular party to the other. We would be pleased to consider the drafts of agreements that are being proposed in order to provide specific GST advice on this matter for you.

9 The second document is an email dated 10 November 2008 from Bob Hoffman to qldsupportcentre@au.cashconverters.com. The email refers to discussion of “the rollout of the Cash Advance Brokerage Model”. The proposed structure is relevantly described in an attachment to the email as follows:

The broker will invoice the lender for the brokerage fee which will include GST.

The lender (because of being classified as a financial service) will be allowed to claim 75% of the GST on the brokers invoice.

However, for GST purposes if the two entities (broker & lender) are GST grouped there is no requirement to charge GST on transactions between the two entities. The advantage of grouping is that no GST at all will be lost to the ATO.

10 The third document is a document, apparently on the letterhead of the second respondent (“Safrock”), entitled “Recipient Generated Tax Invoice” dated 30 April 2010 (“Recipient Generated Tax Invoice”). The invoice is expressed as an invoice from Cash Converters Browns Plains for brokerage for April 2010 in the sum of $5,320 (inclusive of GST). On its face, the document appears to be a document created by Safrock to demonstrate payment of brokerage for the month of April 2010.

11 The fourth document is a spreadsheet entitled “Cash Converters Group Summary of intercompany transactions”. According to Ms Nagy’s evidence, the document was provided by Janic Kwok, then Cash Converters’ financial controller, to Mr Groom on 29 August 2011. One of the items refers to CC Cash Advance Pty Ltd and Safrock. The details are:

Brokerage fees (Queensland and ACT States only) paid to CC Stores on processing personal loans

Brokerage fees and license fees= 35% of original loan amount

In a column headed “Account”, the spreadsheet records:

Revenue – Safrock brokerage fees

Expense – Commission paid

Senior counsel for the applicants, Mr G Kennett SC, submitted that the spreadsheet appears to indicate transactions by which brokers provides services to the lender, and are paid by the lender.

12 The fifth document is a document dated August 2012 entitled “CCPF Personal Loan Invoices”. The document appears to describe how to access the first respondent’s “Recipient Generated Tax Invoices”, including a “Broker Fees Invoice”.

13 The final document is an advice from Grant Donaldson SC to Cash Converters Pty Ltd dated 14 May 2012. The advice concerns the meaning and effect of s 17(3) of the National Credit Code (Sch 1 to the National Consumer Credit Protection Act 2009 (Cth)) and the application of this provision to an arrangement between Cash Converters Pty Ltd, CGWM Pty Ltd (“CGWM”) and Safrock. The advice records that CGWM is a franchisee of Cash Converters Pty Ltd, trading as Cash Converters Toowoomba, and that, under the relevant agreement, it is to act as a finance broker for Safrock. The advice also records that for each loan Safrock pays CGWM a brokerage fee as specified in the relevant loan agreement. Mr Donaldson SC expresses the view that, in the event that Safrock did not, or refused to, pay to CGWM this brokerage fee in respect of a loan procured by it, CGWM could recover this fee in an action against Safrock.

14 By consent, on 29 May 2018, I granted Mr Lynch leave to file a second further amended statements of claim (“2FASOC”) which introduces an allegation to the effect that brokerage services, for which Mr Lynch paid a fee, were in fact provided to Cash Converters. At para 35(b) of the 2FASOC, Mr Lynch added the following additional allegation in support of the allegation in connection with the first loan that the services purported to be provided by Bak Property Pty Ltd (“Bak”) to Mr Lynch in acting as a ‘broker”‘ were illusory:

The brokerage services provided by Bak in respect of [the first loan] were provided to, and paid for, by Safrock.

The allegation is “particularised” by references to the first, third, fourth and sixth documents identified above.

15 At para 35(f), the same allegation is added in support of the allegation that Safrock used unfair tactics in its dealings with Mr Lynch in that “Safrock knew or ought to have known that the ‘brokerage’ services the subject of the First Lynch Appointment of Broker were of no or negligible value to Mr Lynch”.

16 At para 35(g), it is alleged that Safrock used unfair tactics in its dealings with Mr Lynch in that Safrock knew or ought to have known that the amount of the “First Lynch Brokerage Fee”, being approximately 35% of the amount advanced, was not reasonably related to the value of the service allegedly being provided by the “broker” to Mr Lynch. In the 2FASOC, the first, third, fourth and sixth documents identified above have been added as “particulars” to this allegation.

17 Similar amendments have been made to the claims based on the second and third loans.

18 Thus, as Mr Kennett SC summarised the position, as part of how the applicants seek to sustain the points already made in the pleading in connection with the brokers’ fees, the applicants seek to say that the fees which were ostensibly charged to each applicant were treated by Cash Converters as something by and paid by the lender for services rendered to it.

Cash Converters’ response to new issue

19 At the hearing on 22 June 2018, I granted leave to Cash Converters to file evidence relating to issues first raised by the 2FASOC by 20 July 2018.

20 In opposition to the proposed interrogatories, by his 21 June 2018 affidavit, Mr Butler gave evidence on information and belief concerning the results of a preliminary review of a one month sample period of Safrock’s accounts. From this review, it appears that brokerage fees were not treated as either income or expenses of Safrock in its accounts. Mr Butler’s 21 June 2018 affidavit also referred to a draft advice from Deloitte to Mr Groom dated 27 November 2008, that is, shortly after the first two documents of the six documents identified above. The draft advice refers to recent discussions with Mr Noakes concerning changes to Queensland credit legislation, placing a cap or limit on interest rates and fees and charges for small loans. The draft advice refers to changes to the processes for pay day loans services that would involve the lender engaging a loan broker to offer its loans to the customers. The draft advice sets out GST consequences of the new arrangement. Mr Butler’s affidavit noted that:

(1) the new arrangement was that the “broker will charge the customer a fee for the services it provides, and the customer agrees to pay the broker fee”;

(2) the brokerage fee charged to the customer by the broker was inclusive of applicable GST; and

(3) Deloitte understood that the Cash Advance outlet would not be acquiring services from the broker but for the sake of completeness Deloitte outlined the services provided by the broker that may be Reduced Input Tax Credit acquisitions, should the Cash Advance Outlet acquire and pay for such services.

21 It is possible to interpret the draft advice differently from Mr Butler in relation to point (3) above. However, it is not presently necessary to address this issue. Rather, it is sufficient to note that the draft advice indicates that the correct GST treatment of a proposed brokerage fee, including who would receive the services provided by the broker, was under discussion in late November 2008.

Legal framework

22 Rule 21.01 of the Federal Court Rules 2011 permits a party to apply to the Court for an order that another party provide written answers to interrogatories.

23 In Alliance Craton Explorer Pty Ltd v Quasar Resources Pty Ltd [2012] FCA 290 (“Alliance Craton”) at [25], Mansfield J stated:

The ultimate aim of the process of discovery of information by interrogatories is to shorten the trial and save costs. They are to enable a party to litigation to obtain discovery of material facts in order either to support or establish proof of his or her own case, or to find out what case (but not the evidence) the party has to meet; or to destroy or damage the case brought by his or her opposition: Adams v Dickeson [1974] VicRp 10; [1974] VR 77, as cited with approval in Australian Competition and Consumer Commission v Australia and New Zealand Banking Group Ltd [2010] FCA 230… (at [95]).

24 Ms E Collins SC, senior counsel for the respondents, noted that interrogatories are rarely administered, citing Granitgard Pty Ltd ACN 007 427 590 v Termicide Pest Control Pty Ltd ACN 093 837 337 (No 2) [2008] FCA 1451 at [32] and Alliance Craton at [27]. In the latter case, Mansfield J noted that interrogatories “are often seen as expensive and unnecessary to secure a proper disclosure of information” and that modern case management has explored more efficient and effective avenues to achieve the proper disclosure of information.

25 In Coal Cliff Collieries Pty Ltd v CE Heath Insurance Broking (Australia) Pty Ltd (1986) 5 NSWLR 703, Clarke J said at 707:

As a general rule it will be necessary…for the applicant to show that the provision of the answers will, or may, provide relevant information (such as admissions of facts and other material such [as] would facilitate the just and expeditious disposal of the proceedings) which the interrogating party has been unable to extract from his opponent. Because, however, of the pre-trial procedures in the court and its requirement that the parties make all admissions or concessions necessary to focus attention on the nature of the real dispute I envisage that an order will be unnecessary in many cases.

26 Generally speaking, interrogatories will not be permitted as to the contents of documents. In Becker v Smith’s Newspaper Ltd (No 1) (1931) SASR 1 at 8-9, Murray CJ said relevantly:

The interpretation of a document is a matter of law, as to which interrogation is not permissible, but, before interpretation begins, it is necessary to know the meanings of any foreign words that occur in the document, or any words or symbols which are insensible in the collocation in which they stand. Such meanings, however, are a matter of fact, as to which extrinsic evidence is admissible.

27 In Sharpe v Smail (1975) 49 ALJR 130 at 133, Gibbs J stated:

Although, speaking generally, interrogatories as to the contents of a document are not allowable, it is, in my opinion, permissible to interrogate as to the meaning of symbols, ciphers and abbreviations. I agree with the view taken on this matter by Murray CJ in Becker.

28 In Norton v Hoare (No 2) [1913] HCA 58; (1913) 17 CLR 348, the High Court refused leave to appeal where the Supreme Court of Victoria had refused to order a party to answer an interrogatory as to the contents of a document. One of the relevant interrogatories asked whether the words in an identified document differed “in any and what respect from the words which were or are on the original manuscript or document”. Based on the then-current Halsbury’s Laws of England (vol XI, para 169, p 102), the rule stated and applied by the Court at 354 was that “Interrogatories as to the contents of a lost document are permissible but not, as a rule, of those of an existing document”.

29 In Chan v Minister for Immigration & Ethnic Affairs (1983) 49 ALR 593, Dawson J refused an application for leave to administer, relevantly, an interrogatory which asked what was meant by the criteria of health and local character referred to in a specified document. His Honour said at 596:

That is an inquiry as to the meaning of a document which must speak for itself. The defendants’ interpretation of the document is not relevant, even if the document itself is relevant.

30 In CTC Resources NL v Australian Stock Exchange Ltd [2001] WASC 40, Master Sanderson refused leave to administer interrogatories which sought the substance of documents which had been concealed wholly or in part. At [8], the Master stated:

It is not the case that interrogatories which relate to discovered documents are never permitted. For instance, it is permissible to administer an interrogatory seeking an admission that a letter was sent by a party answering the interrogatory: See Drew v Drew (1917) SALR 286. But general interrogatories as to the contents of particular documents are not permitted. The rationale for this rule is not difficult to understand. An interrogatory which seeks evidence about the contents of a document offends the best evidence rule. What is relevant is what the document says, not what the person answering the interrogatory says that it says: See Winterbottom v Varden & Sons Ltd (1921) SASR 364 at 366; Chan v Minister for Immigration & Ethnic Affairs (1983) 49 ALR 593.

31 An interrogatory may be objected to when it is too wide, fishing or immaterial, or if it is unfair or unreasonable in the sense that the burden of answering it far outweighs the likely benefit which may be adduced from the answer: Austal Ships Pty Ltd v Incat Australia Pty Ltd (No 3) [2010] FCA 795; (2010) 272 ALR 177 (“Austal Ships”) at [6], 180-181. In Aspar Autobarn Co-Operative Society v Dovala Pty Ltd (1987) 16 FCR 284 at 285, Woodward J stated:

If the use of interrogatories is to be effective, the task must be approached responsibly on both sides. It should not be seen as a battle of wits, or indeed as any form of contest. It is an opportunity to assist the parties and the court to have the matter prepared for trial as quickly and as cheaply as possible. The chief obligations on the interrogator are to ask questions as clearly and concisely as possible, and to ask only those questions which really require an answer in the particular case – by way of providing information not already known or making a relevant and required admission - in order to advance the interrogator’s case or help to meet the opposition’s case.

32 In Alliance Craton at [36], Mansfield J explained:

In ascertaining whether interrogatories taken as a whole are oppressive, one must consider the number sought to be administered, the extent to which providing an answer imposes an unreasonable and onerous burden on the interrogated party, whether the interrogatory requires the interrogated party to form opinions, to exercise judgment or to draw conclusions, and whether the questions are repetitive: ACCC v ANZ (at [101]). If the energy, effort, time and cost required to address the interrogatories is not reasonably proportionate to the end sought to be achieved, then the interrogatories should not be administered. In making a decision, a balancing exercise must be undertaken: the benefits of narrowing and clarification of issues against the costs and the burden placed over the respondents inherent in the task of answering the written questions fully and accurately.

33 By r 21.02 of the Rules, the ordinary position is that a party would not be ordered to answer interrogatories until after discovery. However, the rules should not be applied inflexibly: see Central Practice Note: National Court Framework and Case Management (CPN-1) at para 7.3.

Cash Converters’ objections to proposed interrogatories

34 In their written submissions, Cash Converters objected to the proposed interrogatories on the following grounds:

(1) They are sought at a late stage, and would cast a significant burden upon Cash Converters to search for and produce material to make good the applicants’ new case.

(2) Many of the interrogatories impermissibly seek answers as to the content or meaning of documents.

(3) Several of the proposed interrogatories are impermissibly ambiguous, vague, uncertain or require Cash Converters to draw conclusions or make judgments.

(4) The proposed interrogatories are oppressive where they would require an unreasonable amount of time and resources to answer, without any guarantee of a concomitant benefit.

(5) Cash Converters will be prejudiced by being required to answer the interrogatories because they will be diverted from their trial preparation.

(6) Some of the proposed interrogatories require Cash Converters to search for records and then to provide supplementary discovery.

35 Orally, Ms Collins SC made the following additional submissions:

(1) Whether GST was paid by the brokers for the first two loans is not a matter about which Cash Converters should be required to answer interrogatories because they were not part of the Cash Converters group of companies at the time of the relevant loans (or in the case of Cash Converters Inala, at any time).

(2) The relevant transactions are difficult to identify because payment of brokerage fees was accompanied by set offs for license fees, because of the large number of franchise stores and the large number of loans, and because of the time that has passed since the relevant transactions.

(3) The records for the relevant transactions are affected by data losses and manual input processes that affect the integrity of the records and the ease of interrogating them.

(4) No brokerage fees have been charged since 1 July 2013 and therefore it cannot be assumed that current staff understand the relevant transactions, adding to the burden of responding to the interrogatories. Mr Noakes and Mr Groom are not within the control of Cash Converters. In particular, Mr Groom is no longer employed by Cash Converters.

(5) It would be unfair to require Cash Converters to give further discovery after the significant resources spent on discovery to date.

(6) The applicants should not be permitted to administer interrogatories because of the delay since Cash Converters’ discovery of the documents upon which they now rely.

(7) The applicants should not be permitted to administer interrogatories before Cash Converters has adduced evidence on the new issue.

Evidence concerning burden of answering interrogatories (both proceedings)

36 Voluminous discovery has been provided by Cash Converters from late 2016 onwards, in the order of some 25,000 documents. In his 21 June 2018 affidavit, Mr Butler estimated Cash Converters’ costs of conducting discovery and addressing discovery related queries as amounting to approximately $2.5 million.

37 Cash Converters noted that the proposed interrogatories involve the tax treatment of particular payments allegedly made by various corporate entities within the large corporate group; Cash Converters’ general business practices, including how invoices were generated; and the accounting policies of Cash Converters. Cash Converters submitted that they include interrogating Cash Converters about the business practices of entities of which Cash Converters have no knowledge. They contended that the time period that the proposed interrogatories cover is very broad and will encompass Cash Converters’ business operations over a four-year period.

38 Cash Converters relied on the evidence that:

(1) To date, the respondents’ solicitors and counsel have spent 100 hours and Cash Converters have spent approximately 30 hours responding to the issues raised by the interrogatories.

(2) In order to answer the interrogatories, Cash Converters would be put to the task of looking for information that may not even be present in the accounts. This would involve a review and interrogation of thousands of lines and journal entries for various of its entities “for over a four-year period commencing about 10 years ago”. In light of the thousands of journal entries that would need to be reviewed for each of the transactions at issue (three for Mr Lynch, and 15 for Ms McKenzie), it would take substantial time and resources to perform this task.

(3) To be able to evidence the actual GST paid in relation to a specific loan and tie all the transactions back to the payments made to the ATO (assuming full access to the relevant accounting and loan systems and archives), Cash Converters’ chief financial officer, Mr Jenkins, estimates that it would take a week for each month/BAS (assuming that the required information is available and free of errors).

(4) Working from the estimates in (3) above, it could take 90 days of labour to answer the proposed interrogatories. This would require the dedication of resources that Cash Converters do not presently have.

(5) It is possible for Cash Converters to engage an external accounting firm to assist with the exercise, however, internal resources from Cash Converters would still need to be dedicated to assist external accountants to operate the relevant systems. Assuming that 90 days of work is required, at $200 per hour, a cost of approximately $150,000 would be incurred if the respondents were to engage an external firm to assist.

Evidence concerning discovery of documents giving rise to application to administer interrogatories

39 In his affidavit sworn 22 June 2018, Mr Butler gave evidence that the two documents referred to in the proposed interrogatories in the Lynch proceeding were discovered on 17 March 2016 and 8 July 2016, respectively. The other documents referred to by the applicants in support of their application to administer interrogatories were discovered on 4 March 2016 (three documents) and 4 July 2017 (one document).

Consideration: Lynch application

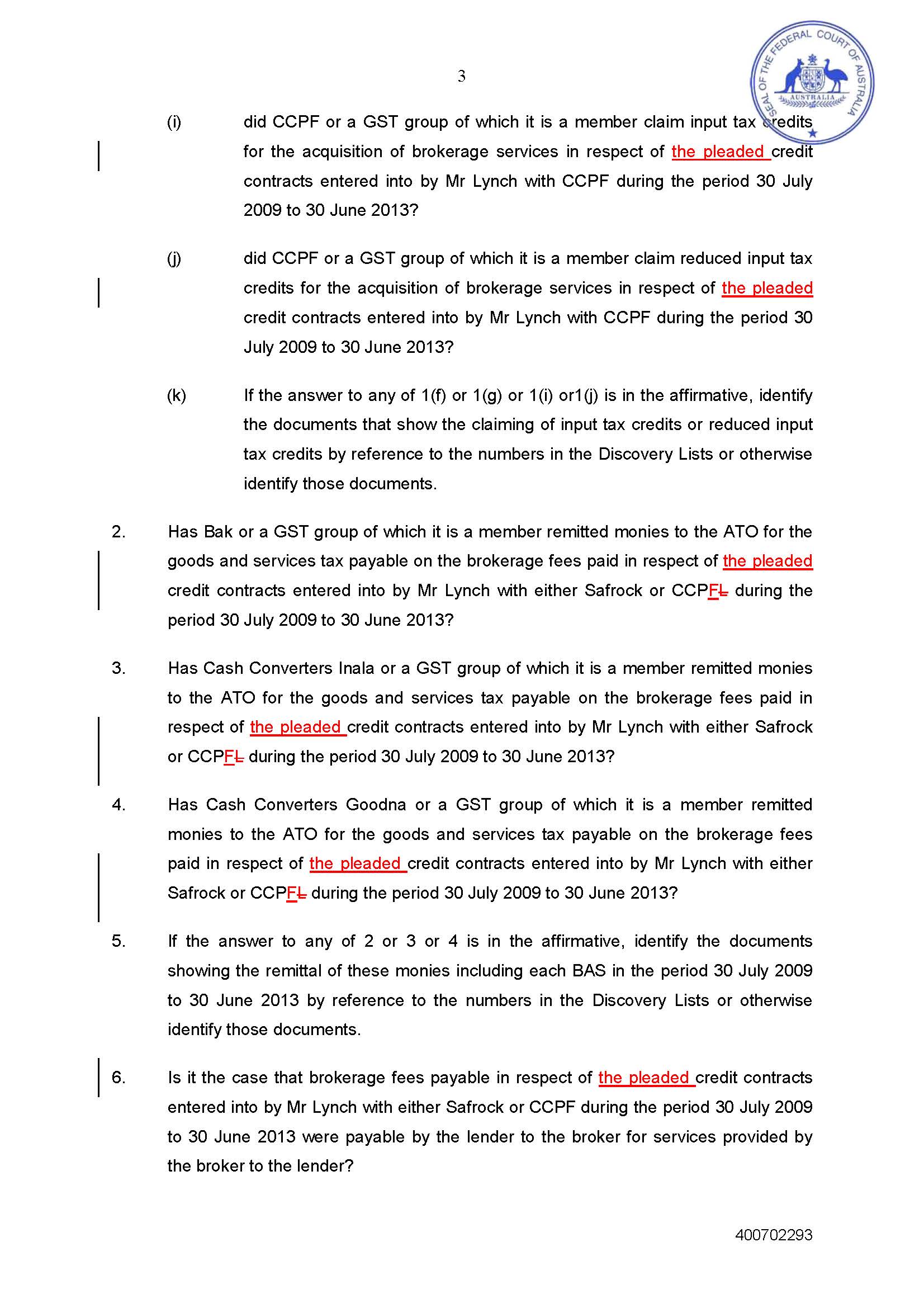

40 I accept that the interrogatories 1(a) to (d) and 8(a) to (k) should not be administered because they seek impermissibly to interrogate as to the contents of the relevant documents.

41 Interrogatories 1(e) and (h) ask whether Safrock and Cash Converters Personal Finance Pty Ltd respectively generated invoices “similar” to the Recipient Generated Tax Invoice “which included brokerage fees payable in respect of” the three loans. In order to answer this question, Cash Converters would be required to give an answer about the contents of documents and accordingly, this interrogatory is also impermissible. However, in my view, subject to any submission to the contrary by Cash Converters, Mr Lynch could issue a notice to produce calling for production of these documents and may be able to administer interrogatories to the extent that it can be demonstrated that such documents were created but are lost.

42 I accept that the interrogatories 6 and 7 should not be administered because they require the exercise of judgment about a legal question.

43 However, I accept that the interrogatories 1(f), (g), (i), (j), 2-4 and 9-12 are relevant and not impermissible for the reasons identified by Cash Converters.

44 Having regard to the franchise relationships between Cash Converters and the brokers, I do not accept that Mr Lynch is in as good a position as Cash Converters to obtain information from the brokers. Accordingly, I do not accept that interrogatories 2 and 3 should be refused on that basis. In particular, I do not accept that the independence of Bak (to 31 August 2010) provides a sufficient basis to refuse leave to administer interrogatory 3 where there is evidence that Bak’s BAS statement for the September 2010 quarter was prepared with the involvement or knowledge of Mr Noakes and Mr Groom.

45 Having regard to the six documents which gave rise to the recent amendments to the statement of claim, I accept that the provision of answers to these interrogatories may provide relevant information which Mr Lynch is otherwise unlikely to extract from Cash Converters.

46 I recognise that addressing the interrogatories will impose a considerable burden on Cash Converters and that the applicants could have made their applications earlier. However, the new issue is integral to the central issue of whether Cash Converters contravened the law by the imposition of the brokerage fee.

47 Having considered the evidence of Mr Butler as to the likely burden of answering the interrogatories, and assuming in Cash Converters’ favour that the burden is not greatly reduced by the restriction of the interrogatories to 11 in total, I do not accept that the burden of answering the remaining interrogatories is not reasonably proportionate to the end sought to be achieved.

48 I accept that interrogatories 1(k), 5 and 13 are not appropriate interrogatories because they do not seek the discovery of material facts. However, I acknowledge that Mr Lynch will almost inevitably require production of the documents by reference to which the permitted interrogatories are answered. This will be a further burden arising from the grant of leave to administer the interrogatories.

49 Accordingly, I will grant leave to Mr Lynch to administer interrogatories 1(f), (g), (i), (j), 2-4 and 9-12 in the amended draft notice of interrogatories filed 25 June 2018 (annexure A to these reasons for judgment).

McKenzie application

50 Applying the reasoning above, I will grant leave to Ms McKenzie to administer interrogatories 2-7 and 9-11 in the amended draft notice of interrogatories filed 25 June 2018 (annexure B to these reasons for judgment).

51 I reject proposed interrogatories 13 to 15 on the basis that they require answers which draw conclusions as to the legal relationships between the lender and the relevant broker.

I certify that the preceding fifty-one (51) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate:

Annexure A – Lynch

Annexure B – McKenziE