FEDERAL COURT OF AUSTRALIA

Sirtex Medical Limited, in the matter of Sirtex Medical Limited [2018] FCA 584

Table of Corrections | |

In paragraph 37, a closing bracket has been inserted after “forms”. | |

3 May 2018 | In paragraph 39, “cased” has been replaced with “cast”. |

ORDERS

SIRTEX MEDIAL LIMITED (ACN 078 166 122) Plaintiff | ||

AND: | ||

Other | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to subsection 411(1) of the Corporations Act 2001 (Cth) (“Act”):

(a) the Plaintiff, Sirtex Medical Limited (“Sirtex”), convene a meeting (“Scheme Meeting”) of the holders of ordinary shares issued in Sirtex (“Shareholders”) for the purpose of considering and, if thought fit, agreeing to (with or without modification) a scheme of arrangement proposed to be entered into between Sirtex and those shareholders (“Scheme”), the terms of which are contained in the Explanatory Statement, a copy of which is behind tab 10 of Exhibit DS1 (“Scheme Booklet”);

(b) the Scheme Meeting be held at 10:00 am (AEST) on 7 May 2018 at the Royal Automobile Club of Australia, 89 Macquarie Street, Sydney NSW 2000; and

(c) the Scheme Booklet be approved for distribution to shareholders (for the purposes only of subsection 411(1) of the Act).

2. Pursuant to section 1319 of the Act:

(a) Mr John Eady or, failing him, Mr Neville Mitchell, be authorised to act as Chairman of the Scheme Meeting;

(b) the Chairman of the Scheme Meeting has the power to adjourn the Scheme Meeting in his absolute discretion for such time and to such date as he considers appropriate;

(c) at the Scheme Meeting, the Shareholders present and entitled to vote in person or by proxy or by an attorney under power or by a corporate representative (if applicable) shall constitute a quorum;

(d) at the Scheme Meeting, each Shareholder, present and entitled to vote, will be entitled to one vote for each fully paid ordinary share in the capital of Sirtex that the Shareholder is registered as holding at 7:00pm (AEST) on 5 May 2018;

(e) at the Scheme Meeting, the resolution whether to approve the Scheme be decided by way of poll;

(f) on or before 5 April 2018, there be dispatched to:

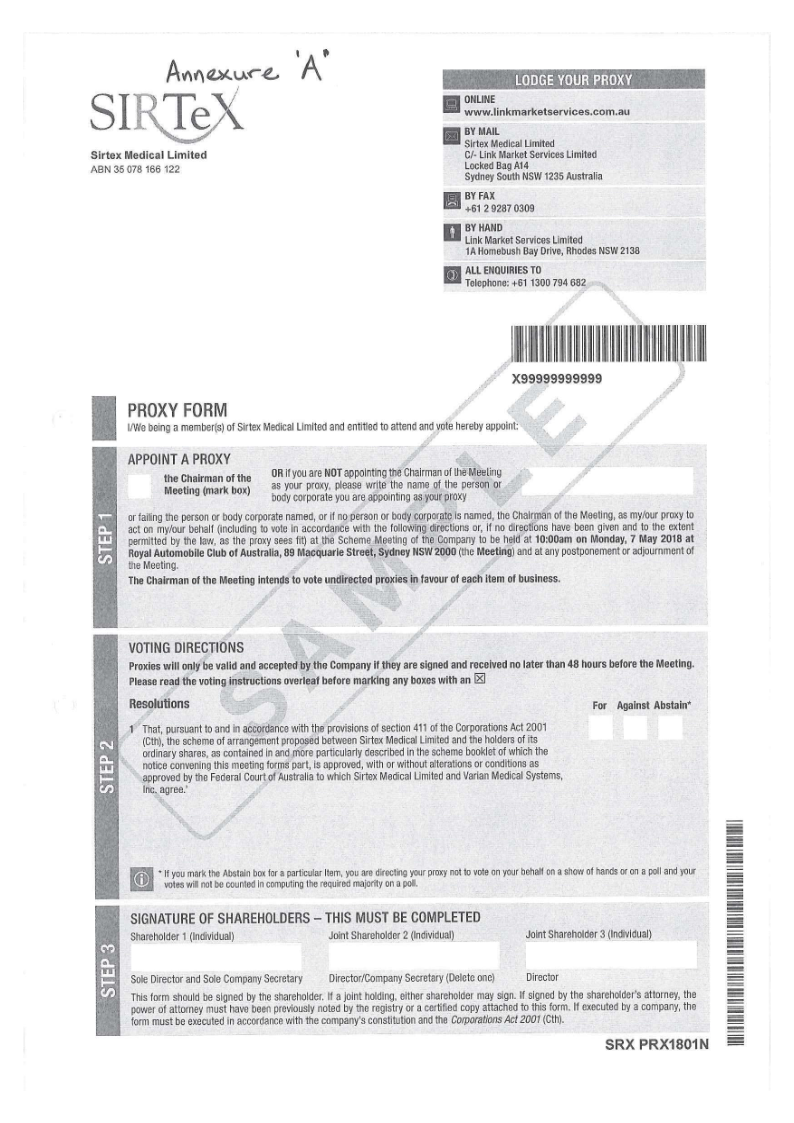

(i) each Shareholder who has nominated an electronic address for the purposes of receiving notices of meeting and proxy forms from Sirtex, at such address, an email substantially in the form of the document behind Tab 22 in Exhibit DS1, including URL links to documents substantially in the form of the Scheme Booklet and the proxy form in respect of the Scheme Meeting, a copy of which is Annexure A (“Proxy Form”); and

(ii) each other Shareholder, by hand or by pre-paid post or courier, to the address of that Shareholder as set out in the register of members of Sirtex, a document substantially in the form of the Scheme Booklet, a Proxy Form in respect of the Scheme Meeting, and a reply paid envelope addressed to Link Market Services Limited; and

(g) the time by which Proxy Forms for the Scheme Meeting must be lodged in accordance with the instructions given on the Proxy Form is 10:00am (AEST) on 5 May 2018.

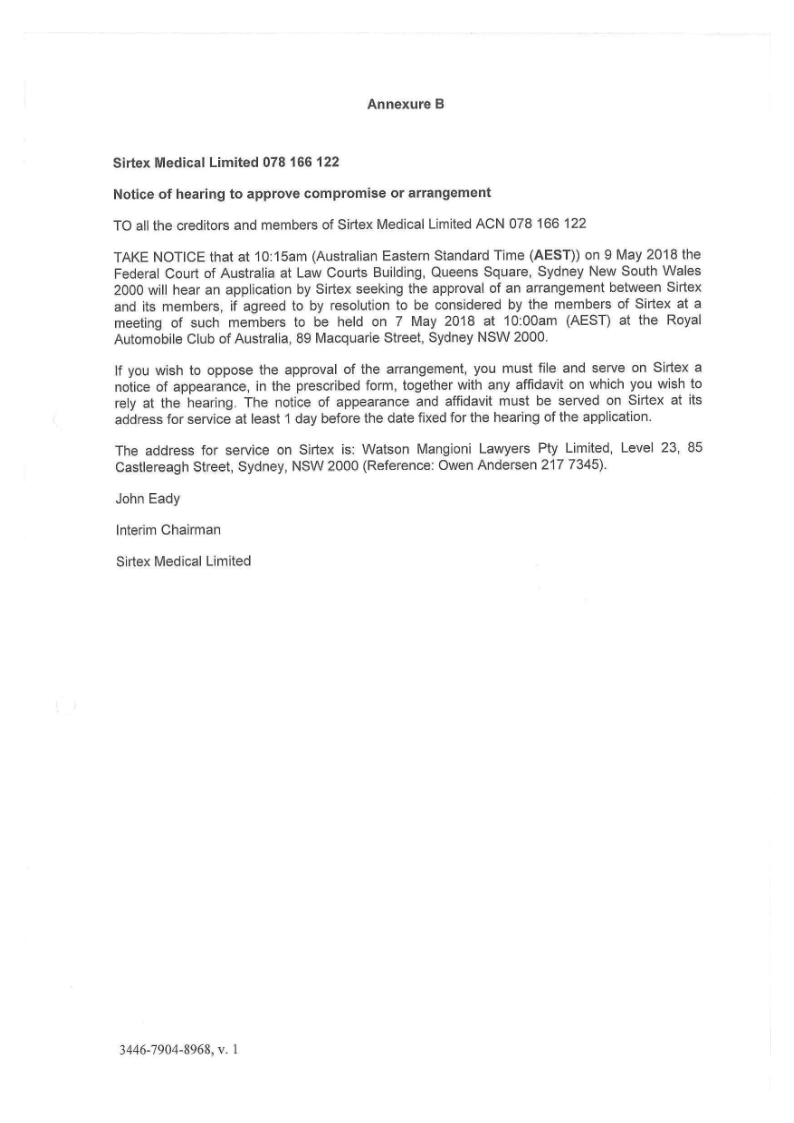

3. On or before 3 May 2018, Sirtex publish a Notice of Hearing substantially in the form of Annexure B hereto in The Australian newspaper and the Plaintiff be relieved of compliance with Rule 3.4 of the Federal Court (Corporations) Rules 2000 (Cth) to the extent necessary.

4. Rule 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) shall not apply to the Scheme Meeting, except insofar as that rule applies regulation 5.6.13 of the Corporations Regulations 2001 (Cth).

5. The proceeding be stood over to 10.15am on 9 May 2018 before Gleeson J for the hearing of any application to approve the Scheme.

6. Liberty to apply.

7. These Orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Annexure A

Annexure B

GLEESON J:

1 On 29 March 2018, I made orders pursuant to s 411(1) of the Corporations Act 2001 (Cth) (“Act”) after a first hearing in relation to a proposed scheme of arrangement including an order to convene the proposed scheme meeting and approving the scheme booklet, that is the explanatory statement required by s 412(1)(a) to accompany notices of the scheme meeting.

2 These are my reasons for making those orders.

BACKGROUND

3 Sirtex Medical Limited (“Sirtex”) is a public company limited by shares traded on the ASX. The company’s principal activities include development and delivery of oncology treatments that use small particle technology. Sirtex generates revenues through the sale of SIR-Spheres® Y-90 resin microspheres, a targeted radiation therapy for liver cancer.

4 As at close of trade on 26 March 2018, Sirtex had:

(1) 55,773,045 fully paid ordinary shares on issue and no other class of shares on issue; and

(2) 9,817 shareholders, of which 6,225 had elected to receive electronic notifications.

5 As at 23 March 2018 (being the “Last Practical Trading Date”), Sirtex had 787,539 performance rights on issue pursuant to the “Sirtex Executive Rights Plan”, approved by Sirtex shareholders at the 2015 annual general meeting held on 27 October 2015, and amended from time to time. By resolutions passed on 26 March 2018, the directors of Sirtex made determinations to the effect that, if the Court ordered the scheme meeting, all rights under the plan would vest with effect from 29 March 2018 subject to the scheme becoming effective. The board noted its intention that its determinations have consequence that, if the scheme becomes effective, shares issued to holders of the vested and exercised rights would be acquired by Varian Medical Systems, Inc (“Varian”) along with the other shares held by Sirtex shareholders and the holders of those shares would be entitled to receive the scheme consideration of $28 per share. Section 9.2 of the scheme booklet discusses the impact of the scheme on the Sirtex incentive plan.

Proposed scheme

6 On 30 January 2018, Sirtex entered into a Scheme Implementation Deed with Varian. Sirtex announced the proposal by Varian to acquire 100% of the issued share capital in Sirtex to the ASX the same day.

7 On 16 February 2018, the proposal was lodged with the Foreign Investment Review Board and on 26 March 2018, the Board issued a “no objections” letter.

8 A draft scheme booklet was first lodged with the Australian Securities and Investments Commission (“ASIC”) on 9 March 2018.

9 On 27 March 2018, Sirtex, Varian and Varian Medical Systems Australasia Holdings Pty Ltd (“Varian Bidco”) entered into a Variation and Restatement Deed to vary and restate the Scheme Implementation Deed. The Scheme Implementation Deed, as varied and restated, is included in the scheme booklet.

10 Under that deed, the proposal is that:

(1) shareholders will transfer their shares to Varian Bidco;

(2) the consideration for each share transferred is a total cash payment of $28 per share;

(3) payment of the scheme consideration is secured by a deed poll executed by Varian and Varian Bidco, who are not parties to the scheme; and

(4) the scheme will effect the acquisition of Sirtex by Varian Bidco and will result in Sirtex becoming a subsidiary of Varian Bidco and being delisted.

11 The proposed cash consideration represents a substantial premium over trading prices up to 29 January 2018, being the last trading day prior to the scheme announcement, as set out in the Chairman’s letter in the scheme booklet.

12 The independent expert appointed by the directors, Deloitte Corporate Finance Pty Ltd (“Deloitte”), concludes that the proposed scheme is fair and reasonable and therefore in the best interests of shareholders. Deloitte’s comparison of the market value of a share in Sirtex on a control basis with the cash consideration of $28 shows that the consideration is within Deloitte’s estimate of the market value of a Sirtex share. Deloitte values a Sirtex share between $23.41 and $29.42. The expert report notes that Deloitte’s valuation has not had explicit regard to any potential compensation payable by Sirtex as a result of two securities class actions presently on foot in this Court against Sirtex. The report states that attributing a value for such compensation would only result in the value of the shares decreasing and the proposed scheme being assessed as more fair.

13 The directors have unanimously recommended that, in the absence of a superior proposal, shareholders vote in favour of the scheme at the proposed scheme meeting.

14 It is proposed to hold a single scheme meeting on Monday 7 May 2018 at 10.00 am.

EVIDENCE and submissions

15 Sirtex relied on the following evidence in support of the application:

(1) an affidavit of Darren Smith, chief financial officer and company secretary of Sirtex, sworn 28 March 2018, together with two volumes marked exhibit “DS1”;

(2) an affidavit of John Eady, non-executive director of Sirtex, interim chairman of Sirtex and proposed chairperson for scheme meeting, sworn 26 March 2018;

(3) an affidavit of Neville John Mitchell, non-executive director of Sirtex and proposed alternative chairperson, sworn 21 March 2018;

(4) an affidavit of Tapan Parekh, authorised representative of Deloitte, affirmed 27 March 2018;

(5) two affidavits of Owen James Anderson, solicitor employed by Watson Mangioni Lawyers Pty Ltd, Sirtex’s solicitors, one sworn 26 March 2018 and the other 28 March 2018;

(6) an affidavit of Michael Brody Dunn, senior corporate counsel of Varian, affirmed 26 March 2018;

(7) an affidavit of John Mark Zeberkiewicz, Delaware attorney in the firm Richards, Layton & Finger, P.A., affirmed 22 March 2018; and

(8) a letter dated 28 March 2018 from ASIC confirming compliance with s 411(2)(a) and expressing the view that ASIC has had a reasonable opportunity to examine the terms of the scheme and the scheme booklet for the purposes of s 411(2)(b)(i).

16 The scheme booklet is behind tab 10 of exhibit “DS1” to the affidavit of Darren Smith.

17 Sirtex filed written submissions dated 28 March 2018. The written submissions set out the relevant legal principles and identified the evidence in support of the various matters about which the Court was required to be satisfied.

18 In addition to the written submissions, counsel for Sirtex made oral submissions and identified important aspects of the evidence.

19 Senior counsel for Varian did not make any submissions.

Issue for decision

20 At the first hearing, the Court’s task is to decide whether to approve both the convening of the proposed scheme meeting pursuant to s 411(1) and the scheme booklet, that is the explanatory statement required by s 412(1)(a) to accompany the notices convening the scheme meeting.

21 The relevant legal framework is set out in the submissions filed by Sirtex. It is also explained in Re Staging Connections Group Limited [2015] FCA 1012, particularly at [18] to [31].

22 I was satisfied that counsel for Sirtex sought conscientiously to discharge the duty of candour which applies in ex parte applications of this kind, bringing to the Court’s attention all matters that could be considered relevant to the Court’s decision: see Re Permanent Trustee Company Limited [2002] NSWSC 1177; (2002) 43 ACSR 601 at [7].

CONSIDERATION

Part 5.1 body

23 The term “Part 5.1 body” is defined in s 9 of the Act to mean, relevantly, a company. The evidence confirms that Sirtex is a Pt 5.1 body.

Proposed scheme is an “arrangement“

24 Generally, almost any arrangement otherwise legal which touches or concerns the rights and obligations of the company or its members, and which is properly proposed, is an “arrangement” within the meaning of s 411: see Re NRMA Insurance Limited (No 1) [2000] NSWSC 82; (2000) 156 FLR 349 at [20] per Santow J. The text of the scheme (annexed to the scheme booklet) provides prima facie evidence that the proposed scheme is such an “arrangement”. Sirtex committed itself to propounding the scheme by the Scheme Implementation Deed, as varied and restated by the Variation and Restatement Deed, and the directors have unanimously recommended the scheme. I accepted that these matters also provide prima facie evidence that the scheme is bona fide and has been properly proposed.

Scheme booklet will provide proper disclosure to members

25 On 9 March 2018, the directors resolved to approve the scheme booklet in its then current form, and approved it for lodgement with ASIC. On 26 March 2018, the directors resolved to approve a draft of the scheme booklet as at 23 March 2018 subject to certain matters listed in the board minutes including receipt of verification certificates from Varian and each director. This draft was marked up to show changes from the draft provided to the board in advance of the board meeting held on 9 March 2018 (other than changes to the tax considerations provided by PwC which were not marked up).

26 The directors also resolved that this version of the scheme booklet be approved for release to ASIC for registration and the ASX, once it had been approved by the Court for issue to Sirtex shareholders.

27 I accepted that the affidavits of Mr Smith (at paras 41 to 56) and Mr Dunn (at paras 7 to 16) demonstrate that reasonable steps have been taken to confirm that the statements in the scheme booklet are accurate, not misleading or deceptive and that no material information has been omitted in respect of those statements.

28 The written submissions included an annexure identifying how the scheme booklet complied with s 412(1)(a)(i) and s 412(1)(a)(ii) and the relevant provisions of Pt 3 of Sch 8 of the Corporations Regulations 2001 (Cth). I note that at section 5.4 of the scheme booklet, the directors give reasons why it is not possible for them to give a statement of their intentions in accordance with cl 8310 of Pt 3 of Sch 8.

29 On the basis of the evidence and submissions set out above, I was satisfied that there is prima facie evidence that the scheme booklet will provide proper disclosure to members.

Other procedural requirements have been met

30 Division 3 of the Federal Court (Corporations) Rules 2000 (Cth) (“Corporations Rules”) applies relevantly to an application for approval of an arrangement between a Pt 5.1 body and its members (r 3.1).

31 The affidavits of Mr Eady and Mr Neville met the requirements in r 3.2 of the Corporations Rules (concerning nomination of the chairperson for the scheme meeting).

32 The proposed orders were in a form that met the requirements of r 3.3 and provided for publication of the notice as required by r 3.4.

Proposed electronic notification of shareholders

33 Sirtex proposed to email those shareholders who have elected to receive notices by email with links to the scheme booklet.

34 Sections 249J(3)(c) and (ca) of the Act contemplate sending notices of meetings to members. Rule 3.3(2) of the Corporations Rules requires, in the absence of court orders to the contrary, that a meeting of members ordered under s 411 must be convened, held and conducted in accordance with the provisions of Pt 2G.2 of the Act (in which s 249J appears) and Sirtex’s constitution (to the extent that it is not inconsistent with Pt 2G.2).

35 Sirtex submitted that Articles 9.1(a)(iv) and 9.1(d) of its constitution deal with electronic mail-out in a manner not inconsistent with Pt 2G.2.

36 Electronic-mail out orders are now commonly made in relation to scheme meetings: see, for example, Re David Jones Limited [2014] FCA 530; Re Staging Connections at [49]-[52]; Re Signature Gold Limited [2017] FCA 1481 at [55]; and Re Intecq Limited [2016] NSWSC 1429 at [21].

37 The proposed form of notification conforms with the requirement that information concerning the scheme booklet precede any invitation for shareholders to act (for instance, by submission of proxy forms): Farrell J in David Jones at [37].

No reason apparent why the scheme should not receive the Court’s approval if the necessary number of votes are achieved

38 I was satisfied that there was no order sought which goes beyond current accepted practice.

39 I was also satisfied that the proposed scheme is of such a nature and is cast in such terms that, if it were to receive the requisite statutory majority, the Court would be likely to approve the scheme on the hearing of an unopposed application.

40 Counsel for Sirtex, Mr Wood, drew the following five matters to the Court’s attention, although his submission was that none of these matters should be of concern to the Court. I accepted that submission.

1. Classes

41 Sirtex proposes a single class for voting purposes.

42 As noted in Sirtex’s written submissions, the test for whether members are required to be divided into different classes is whether their rights are so dissimilar as to make it impossible for them to consult together with a view to their common interest: Sovereign Life Assurance Co v Dodd [1892] 2 QB 573 at 583; Re Nine Entertainment Group Limited (No 1) (2012) 211 FCR 439 at [53]. As Barrett J emphasised in Re Hills Motorway Limited (2002) 43 ACSR 101 at [12] (see also Re Nine Entertainment Group Limited at [56]), the test is not one of differentiation or identical treatment, but of community of interest. “It is only if the differentiation ‘destroys the ability’ or makes it impossible for the creditors [or members] to consult together that the creditors [or members] are to be divided into classes”: see also Re Staging Connections at [29].

43 As Santow J observed in Re NRMA Limited (2000) 33 ACSR 595 at [80]:

“The ‘shifting’ or ‘fracturing’ of classes into smaller groups can undermine the objective of obtaining decision by a large majority, by giving one group an effective veto over the wishes of the majority. That itself can be oppressive.”

44 Courts have previously accepted that performance rights do not result in the creation of a separate class in relevantly similar circumstances in Re Cashcard Australia Limited [2004] FCA 223; (2004) 48 ACSR 738 at [8]-[9]; Re Fosters Group Limited (No 2) [2011] VSC 547 at [38]-[43] and Re Aston Resources Limited [2012] FCA 229 at [39]. In Re Cashcard, Jacobson J noted that, if a scheme is passed only as a result of the vote of the parties who would receive additional benefits from the scheme, a court can take that matter into account in deciding whether to exercise its discretion to approve the scheme.

45 In accordance with the decisions identified in the previous paragraph, I was satisfied that the proposed single class was appropriate.

2. Deal protection clauses

46 The Scheme Implementation Deed, as varied and restated, includes exclusivity provisions which are referred to in the scheme booklet at sections 2.4(c) and 9.1(c). At section 9.1(c), the provisions are referred to as “customary exclusivity arrangements”.

47 The Scheme Implementation Deed also provides for a “Reimbursement fee” (colloquially a “break fee”) payable by either Sirtex or Varian if certain events occur. The “break fee” is 1% of the total scheme consideration. The break fee is consistent with the 1% referred to in the Takeovers Panel’s “Guidance Note 7 – Lock-up devices”.

48 In Re APN News & Media Limited [2007] FCA 770; (2007) 62 ACSR 400 at [55] (“APN News”), Lindgren J expressed the view that it would be desirable that applications under s 411(1) be supported by affidavit evidence directed to showing:

• that the no-shop and break fee provisions are the result of a normal commercial negotiation, and explaining, at least briefly and in general terms, the factual basis for that statement…;

• that the directors of the target company, or at least those directors of it who are not affiliated with the offeror, believe that the provisions do not operate against the interests of offeree shareholders, and that in fact it was in the interests of such shareholders that the directors agreed to the inclusion of the provisions in the merger implementation agreement (see …In re Paramount Communications Inc Shareholders’ Litigation 637 A2d 34 (Del Supr 1993) for a case in which a target company’s directors’ commitment to no-shop and break fee provisions was held, in all the circumstances, to constitute a breach of their fiduciary duty); and

• in the case of the break fee, explaining, by reference to calculations based on the evidence before the Court, the percentage that the break fee represents (a) of the “equity value” of the target company, calculated in accordance with para 7.18 of the Takeovers Panel’s Guidance Note 7, and (b) of the scheme consideration (the explanation might, instead, be conveyed in a submission, but still by reference to the evidence before the Court).

49 In oral submissions, Mr Wood identified the evidence addressing the matters suggested in Lindgren J in APN News, and set out above.

50 At cl 10.6 of the Scheme Implementation Deed, the parties recorded their agreement that the costs incurred in pursuing the scheme are of such a nature that they cannot be accurately quantified and that a genuine pre-estimate of the costs would equal or exceed the break fees.

51 There is a “fiduciary carve out” from the no talk and no due diligence exclusivity arrangements in cl 9.5 of the Scheme Implementation Deed.

52 I did not conclude that the exclusivity arrangements should cause me not to make the orders sought. In particular, I did not identify any reason to think that the break fee payable by Sirtex is excessive or will operate coercively in the circumstances: see Re Staging Connections at [37]-[42].

3. Deed poll

53 In Re Simavita Holdings Limited [2013] FCA 1274 at [43], Farrell J explained:

A deed poll operates under Australian law to allow those for whose benefit it is expressed to sue on the promises in the deed poll. This is a common mechanism, especially in acquisition schemes, for binding an “outsider” to a scheme to perform its obligations under the scheme …, especially the payment of scheme consideration. This is an important element of managing “performance risk“.

54 Following the approach in Simavita and Re Biosceptre International Limited [2013] FCA 1429 at [21], Varian adduced evidence from Mr Zeberkiewicz, a Delaware attorney in the firm Richards, Layton & Finger P.A., as to the proper execution of the deed poll by Varian. On the basis of Mr Zeberkiewicz’s evidence, I am satisfied that the deed poll in the present case has been duly executed by Varian and is prima facie enforceable.

4. Performance risk

55 Clause 5.2(a) of the scheme provides for the transfer of the scheme shares after provision of the scheme consideration under cl 6.1. Thus, the scheme consideration must be provided before the transfer of the scheme shares occurs, satisfying concerns that might otherwise exist about performance risk.

5. Conditions precedent

56 The scheme is subject to certain conditions precedent set out in cl 3.1. Subject to the usual court orders and such orders being lodged with ASIC, these conditions precedent need to be satisfied or waived by 8:00 am on the second court hearing date. As a result, the scheme will be self-executing upon the making of orders at the second court hearing and registration of those orders with ASIC.

Conclusion

57 Accordingly, I made the orders sought by Sirtex.

I certify that the preceding fifty-seven (57) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: