FEDERAL COURT OF AUSTRALIA

Deputy Commissioner of Taxation v Citi Pty Ltd [2018] FCA 103

BROMWICH J | |

DATE OF ORDER: |

THE COURT NOTES THAT:

1. Leave was given to file in Court:

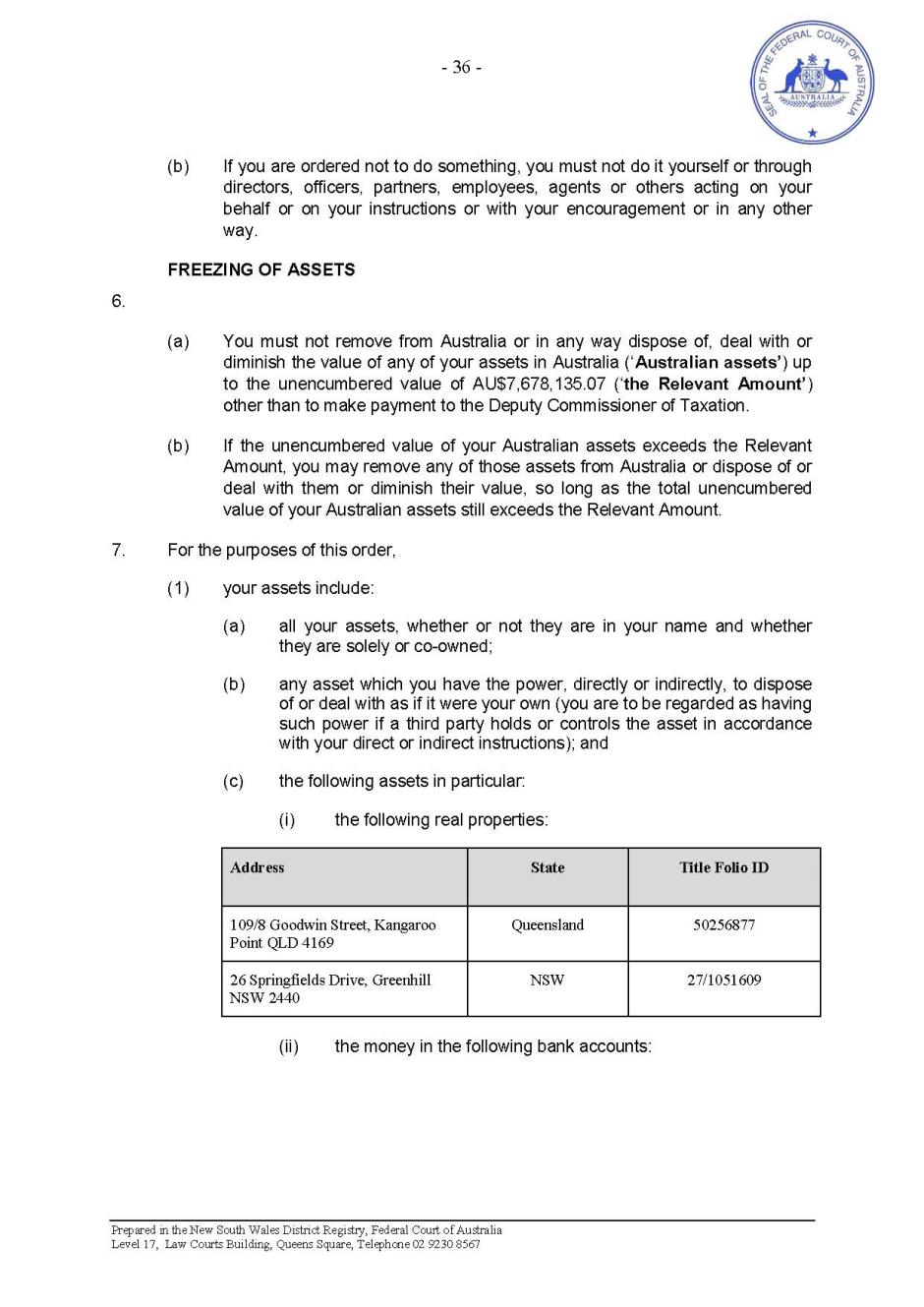

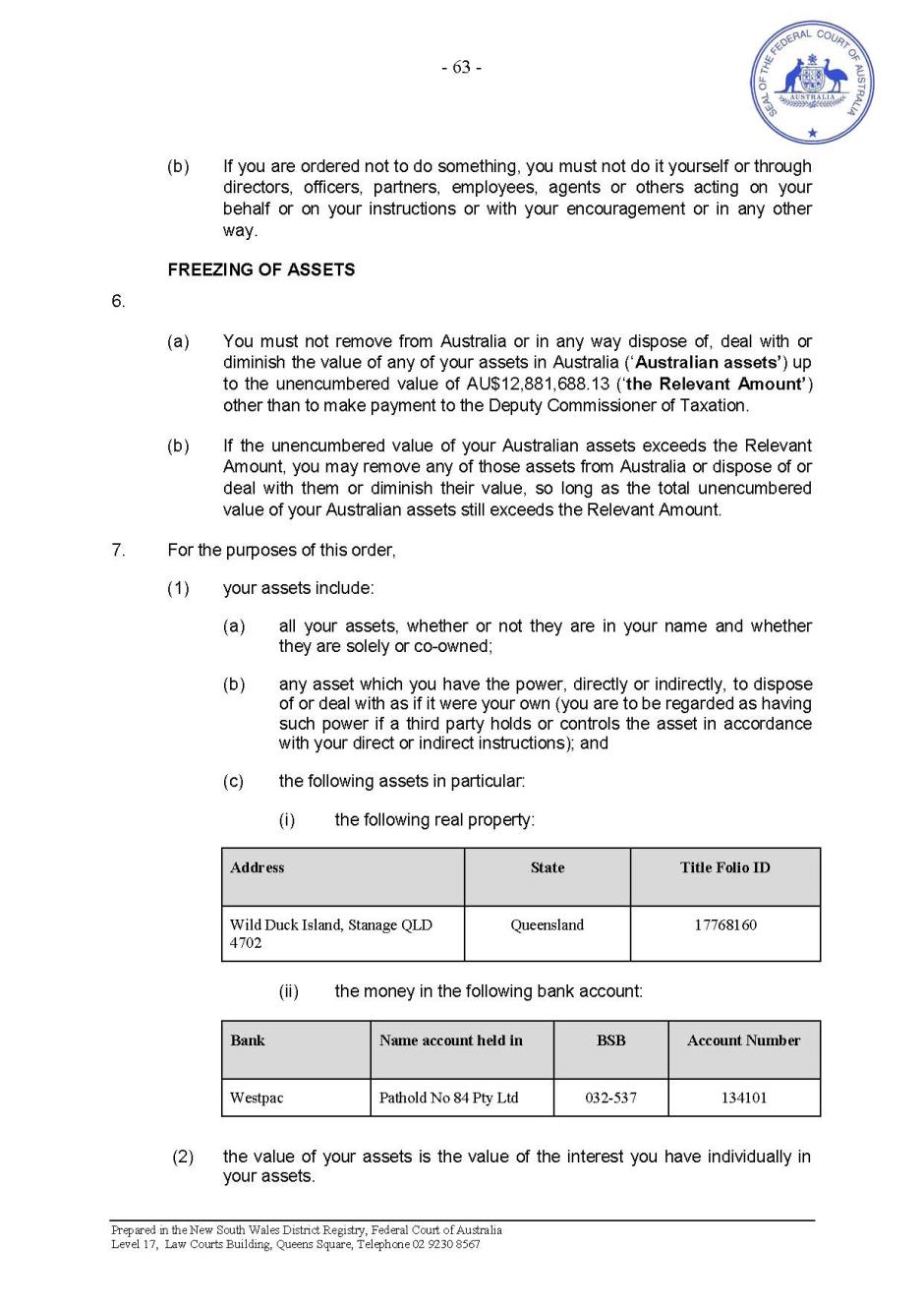

(a) Affidavit of Kathleen Chau, sworn 13 February 2018;

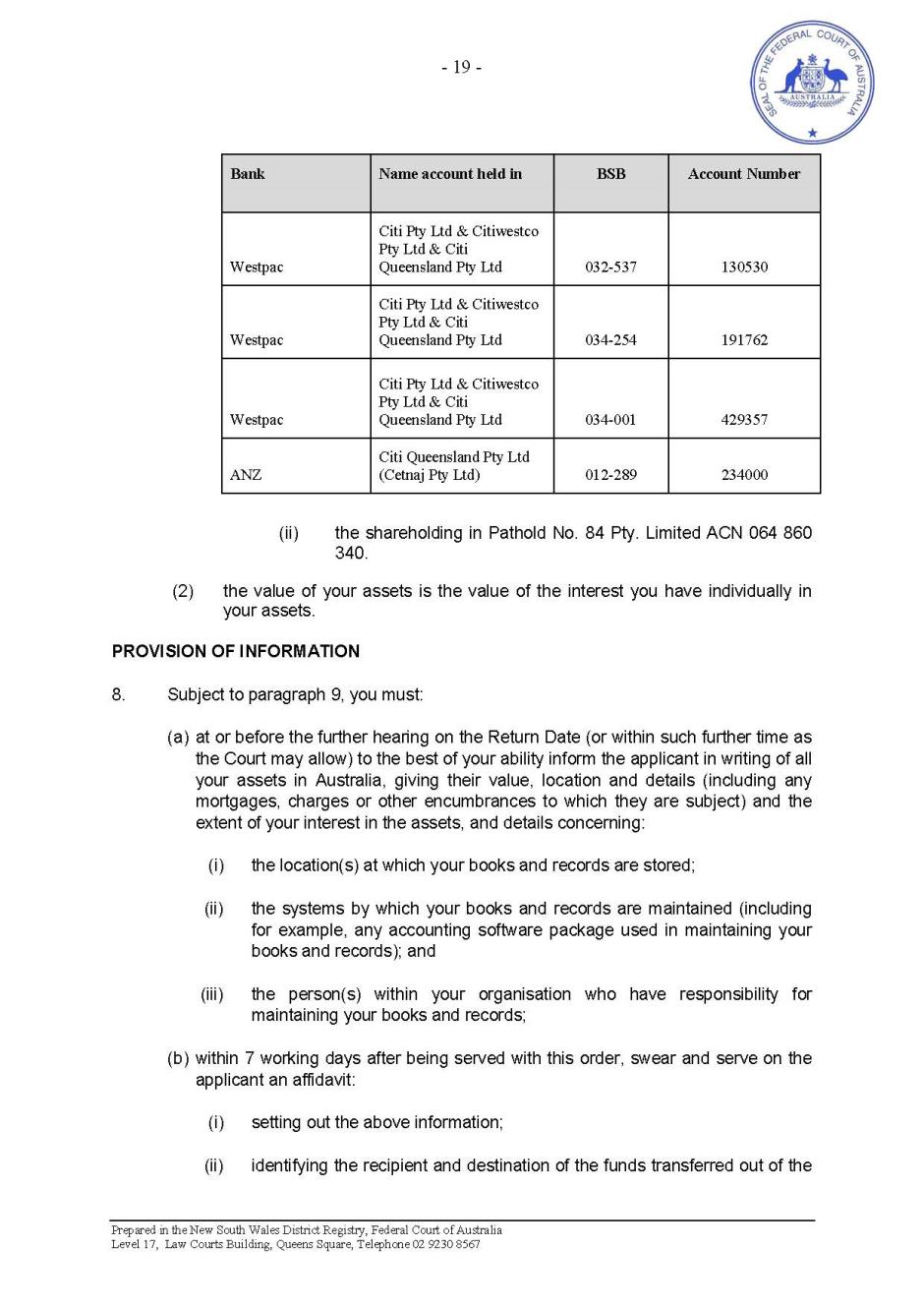

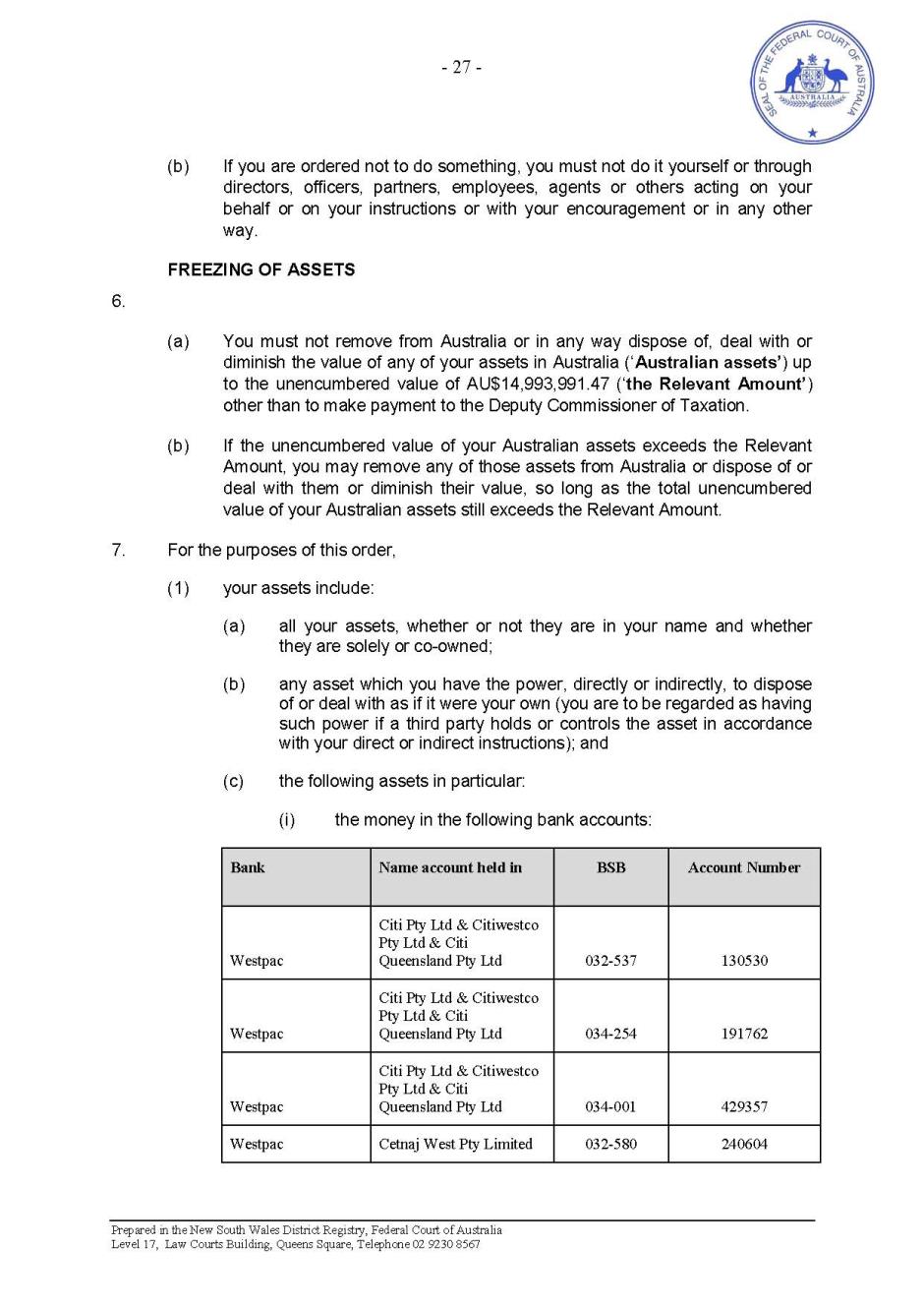

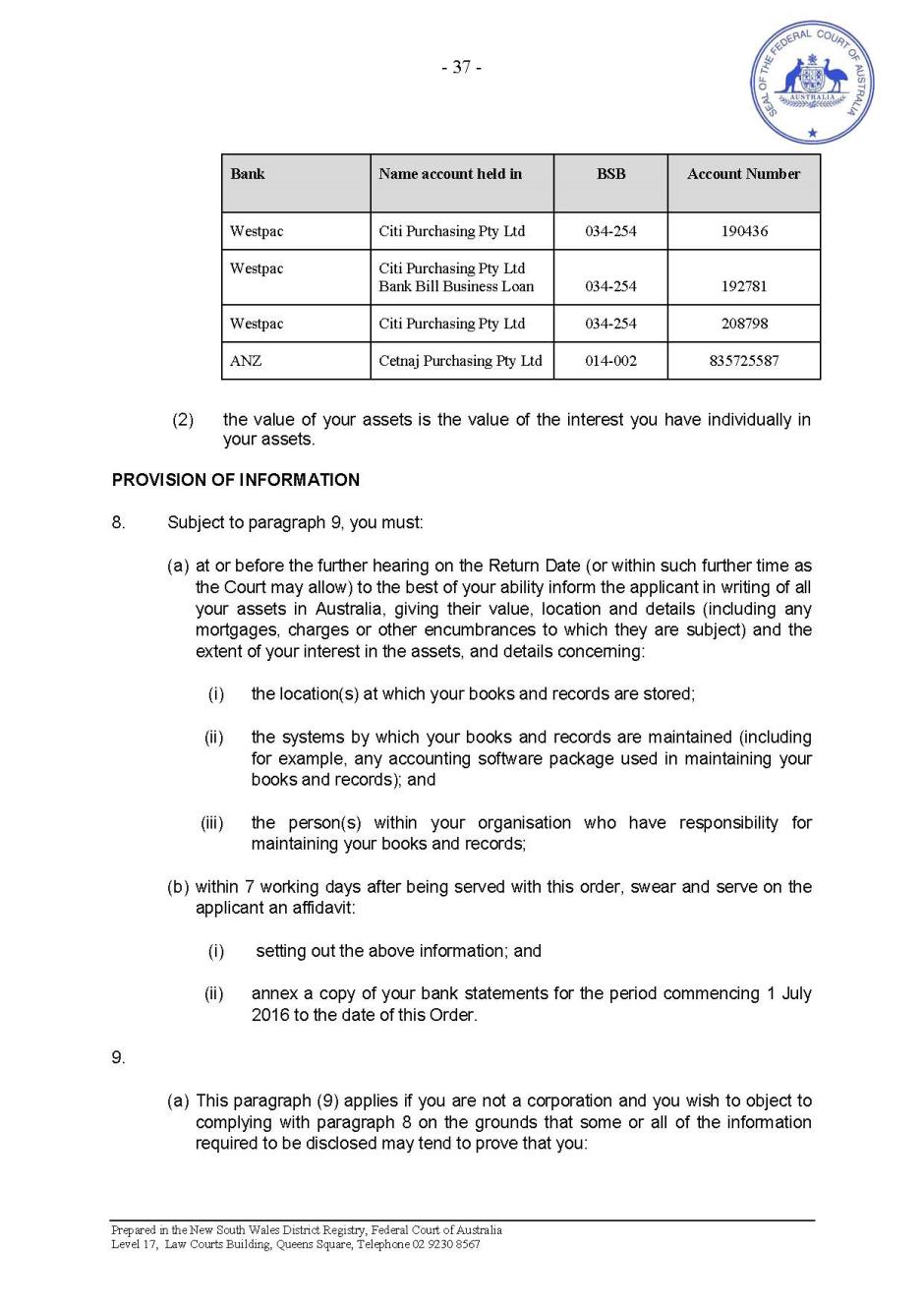

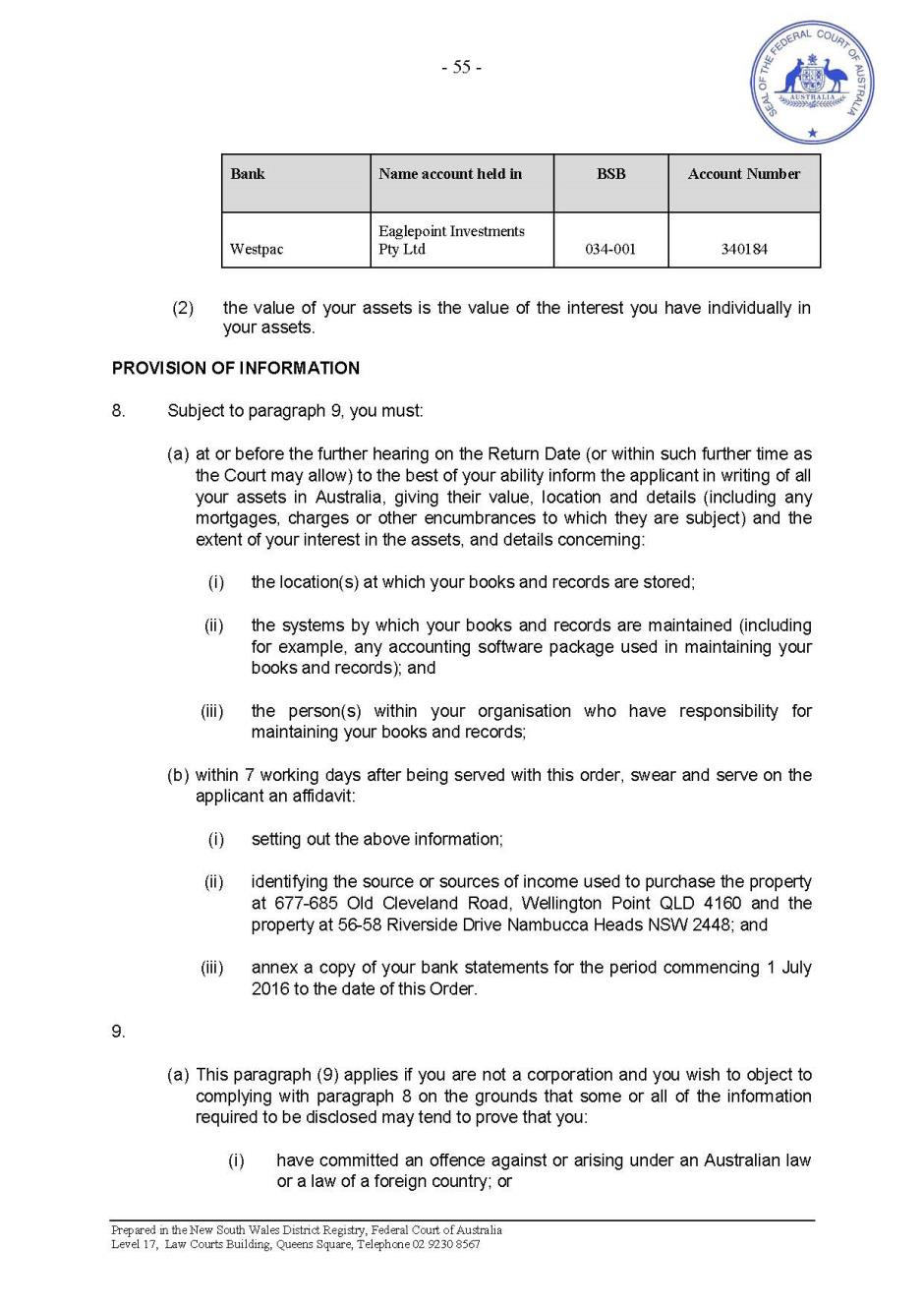

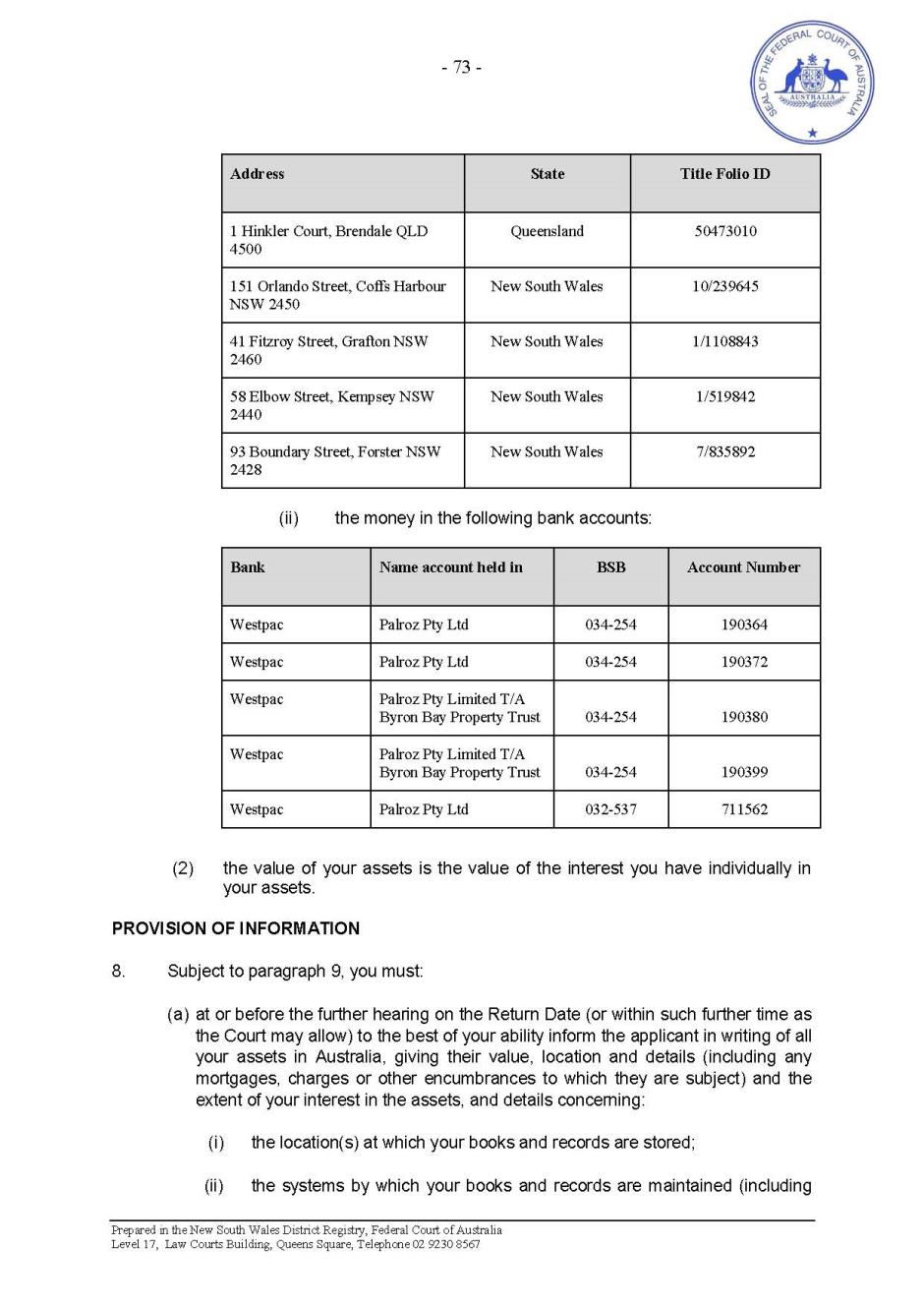

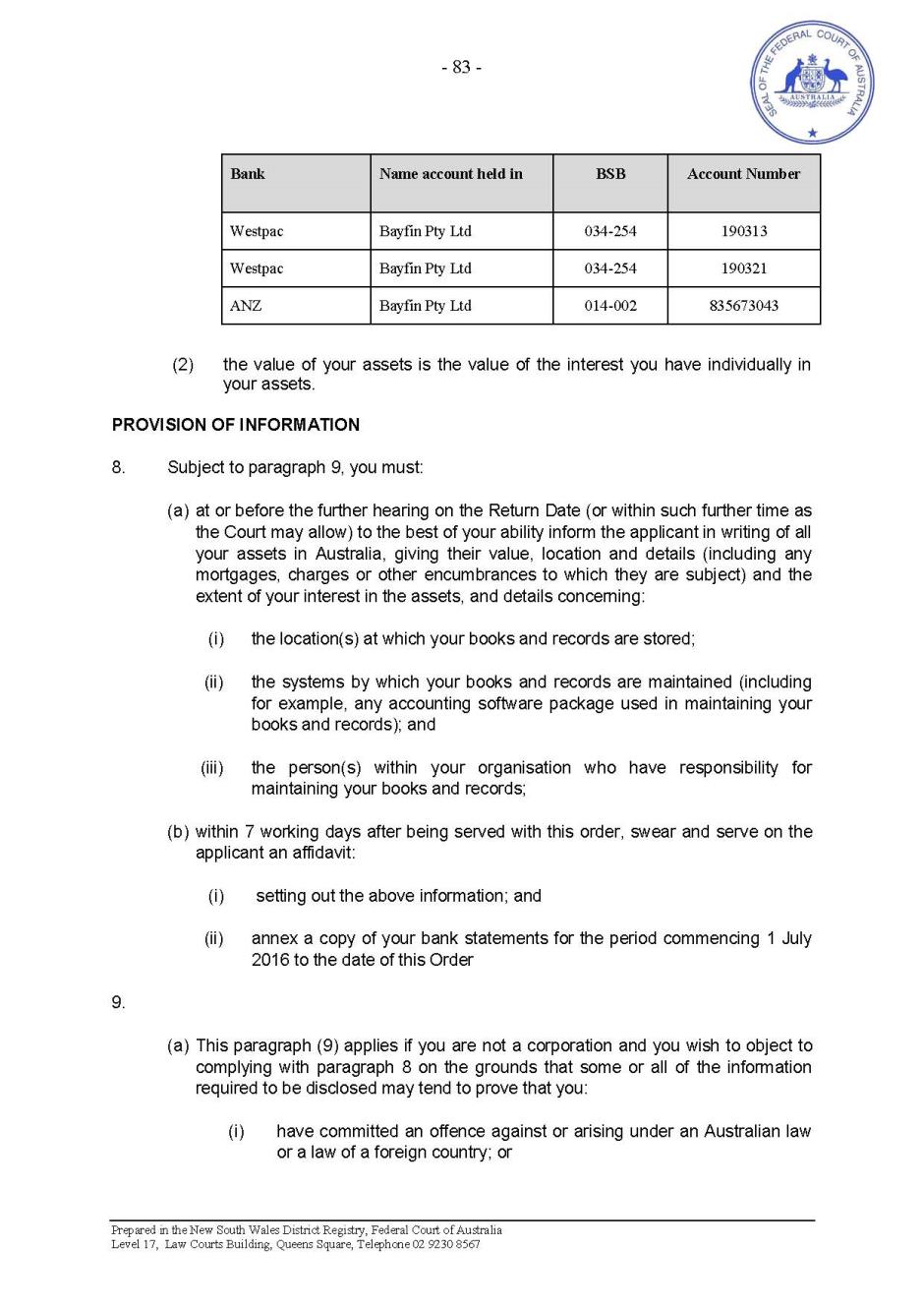

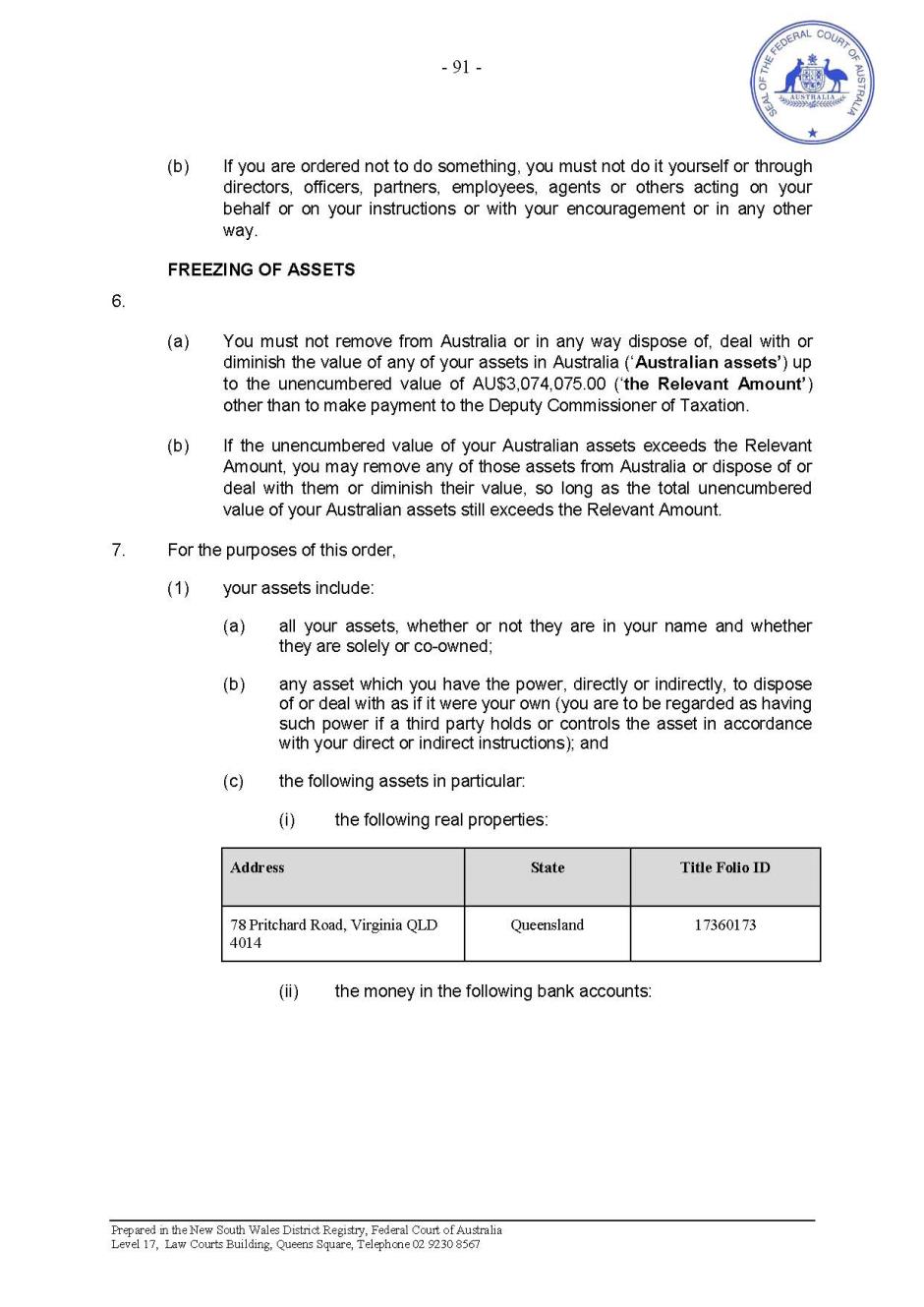

(b) Affidavit of Jared Davies, affirmed 13 February 2018;

(c) Affidavit of Sandra Kirisitina Aofia sworn 13 February 2018; and

(d) Affidavit of Khaled Metlej sworn 13 February 2018.

THE COURT:

2. DIRECTS, in respect of the application for interlocutory relief, that:

(a) it be made returnable instanter; and

(b) service of the Originating Application and supporting Affidavits on the Respondents be dispensed with.

3. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure A to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the First Respondent.

4. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure B to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Second Respondent.

5. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure C to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Third Respondent.

6. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure D to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Fourth Respondent.

7. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure E to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Fifth Respondent.

8. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure F to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Sixth Respondent.

9. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure G to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Seventh Respondent.

10. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure H to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Eight Respondent.

11. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure I to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Ninth Respondent.

12. Until further Order, and upon the Applicant by his Counsel giving the undertakings in Schedule A of the document entitled “Penal Notice” (a copy of which is Annexure J to these Orders), MAKES ORDERS in the terms of the Penal Notice directed to the Tenth Respondent.

13. NOTES that, in respect of each Respondent, the time and manner of service of the originating application, supporting affidavits and these Orders, is to be in accordance with Order 1 contained in the document titled “Penal Notice” pertaining to that Respondent.

14. DIRECTS that, upon the undertaking of the Applicant to provide a paper copy of Exhibit KC-1 to each of the Respondents upon their request within three business days:

(a) personal service of Exhibit KC-1 on the Respondents be dispensed with;

(b) in lieu of personal service, service of Exhibit KC-1 on all of the Respondents may be effected by delivering only a total of two (2) copies of Exhibit KC-1 to 7986 GRAFTON ROAD, EBOR NSW 2453 by 6.00PM on 14 February 2018.

15. DIRECTS that the proceedings be adjourned for further directions before the Duty Judge at 10.15 AM on 21 February 2018.

16. Liberty to apply on 24 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

Revised from transcript

BROMWICH J:

1 These are revised reasons, given ex tempore, for freezing and related orders that were made pursuant to rules 7.32 and 7.35 of the Federal Court of Australia Rules 2011 (Cth) on the evening of 13 February 2018. The orders were made upon the usual undertaking as to damages being given to the Court by senior counsel for the applicant.

2 The applicant in these proceedings, the Deputy Commissioner of Taxation, sought freezing and related orders in relation to the respondents, which comprise 10 companies. Five of those companies are described as “assessed respondents”. They are so described because notices of assessment have been issued and were served on 13 February 2018. In respect of those five respondents, each of those notices of assessment resulted from default assessments under s 167 of the Income Tax Assessment Act (1936) (Cth). Those respondents are part of a group of companies which have been referred to by the applicant by their historical name, the “Cetnaj Group”.

3 The Cetnaj Group operated a business in the electrical wholesaling and retail industry, and also later in the data industry. This information and some of the other information I refer to comes from an affidavit of Ms Kathleen Chau, sworn 12 February 2018, to which is annexed an index to an exhibit, KC1, and that exhibit.

4 The corporate entities comprising the Cetnaj Group are ultimately controlled by, and apparently operate for the benefit of, four natural persons, being Mr Martyn Richardson, Mr John Connors and their respective wives, Mrs Roslyn Richardson and Mrs Cathy Connors. The tax agent for that group of companies is Mr John Florent, a sole practitioner accountant who at one stage practiced from Taree, in northern New South Wales, under the name “J.G. Florent & Co”.

5 The assessed respondents, as they have been conveniently described, being these five companies, have not lodged income tax returns since the 2013 financial year. Default assessments have been raised in relation to the first respondent, Citi Pty Limited, for each of the completed financial years since then, being 2014, 2015, 2016 and 2017. Other companies have had either similar or, in a few cases, slightly shorter periods for which default assessments have been raised. Penalty assessments have also been raised.

6 The background and history to this matter is as follows. In January 2015, the Commissioner of Taxation commenced an audit into the taxation affairs of the companies in the Cetnaj Group. The evidence before me indicated that during the course of the audit, the Commissioner encountered considerable difficulties in obtaining information required to conduct the audit. Some information was provided, but a significant amount was not provided. One of the documents before me was a list of the various notices that have been issued, indicating where they have not been complied with.

7 Importantly for the purposes of this application, in February 2016, unbeknownst to the Australian Taxation Office (ATO), the Cetnaj Group entered into an agreement to sell its business to an entirely unrelated entity, who was a trade competitor. That sale was approved by the Australian Competition and Consumer Commission (ACCC), and it was only through the ACCC’s website that the ATO became aware of the sale having taken place. The sale price was $67,836,881.27. The material indicates that little or no tax was declared by companies in the Cetnaj Group in the period from 1997 up to when income tax returns were filed (that is, up to the 2013 financial year). Minimal amounts of income were declared, and yet an asset was created that achieved that sale price.

8 The sale was effected by an agreement, and subsequent agreement, entered into with the purchaser, Metal Manufactures Limited. There is no suggestion that that company had done anything untoward. They were simply the purchaser of the business, but not of the companies which owned the business.

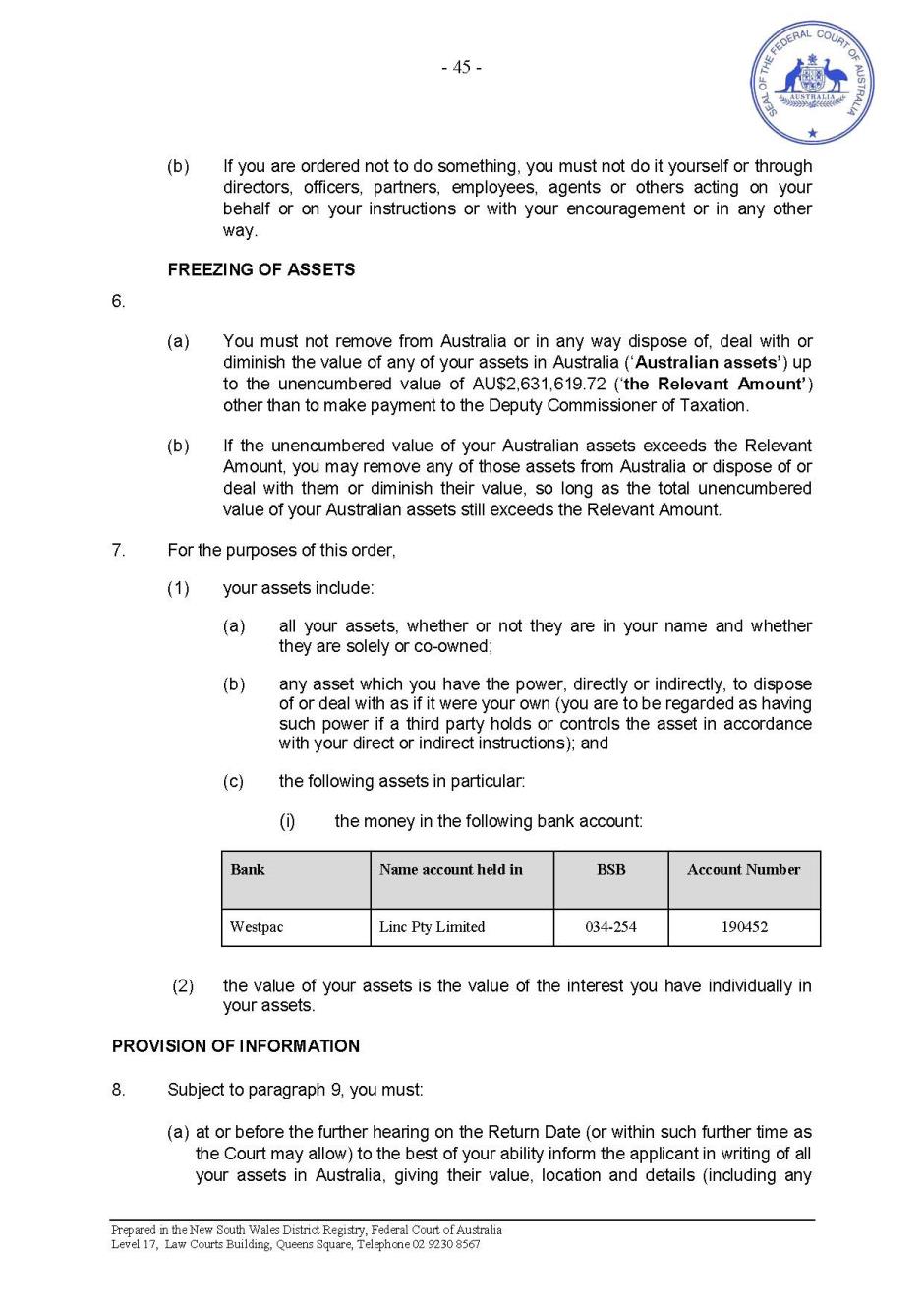

9 As I have already indicated, the notices of assessment have issued, and have now been served upon the assessed respondent companies. The Commissioner has also issued and had served a style of garnishee order allowed for under s 260-5 of schedule 1 to the Taxation Administration Act 1956 (Cth) to Westpac Banking Corporation and the five assessed respondents.

10 The freezing orders sought are against the respective judgment debtors, being the five assessed respondents, namely, the first to fifth respondents, and third parties related to those companies, being the sixth to tenth respondents. Those third party respondents were sought to be the subject of freezing orders by reason of the fact that they have either received assets from one or more of the assessed respondents, or owe or are accountable to one of those assessed respondents, and therefore are capable of satisfying debts owed to the applicant.

11 I need not go into the legal principles at this interlocutory stage, but it suffices to say that the requirements for making freezing orders under rule 7.32 of the Federal Court of Australia Rules 2011 (Cth), and rule 7.35 against third parties, have been made out. In particular, I am satisfied that the applicant has a reasonably arguable case on the law and the facts, that there is a danger that a prospective judgment will be wholly or partially unsatisfied because assets may be removed either from Australia or from a place inside or outside Australia, or that assets may be disposed of, dealt with or diminished in value. I am further satisfied that the balance of convenience favours the granting of interim freezing orders.

12 In particular, in terms of the danger that I have adverted to, Perram J, in Deputy Commissioner of Taxation v Chemical Trustee Limited (No 4) [2012] FCA 1064; 90 ATR 711, referred at [23]-[24] to the nature of the danger of dissipation. One of the matters that his Honour relied upon in those paragraphs was the substantial amount of tax and penalties, including interest in that case. His Honour also referred to large amounts of money being transferred into and out of Australia. In this case, relevantly similar amounts of money are involved – in fact, considerably larger amounts of money when it came to the default income tax assessments. In that case, the income tax assessment amounts were closer to the $5 million mark, as opposed to the $54 million mark in this case.

13 It is also worth noting that a freezing order may be granted even if there is no evidence of a positive intention to frustrate a judgment. What matters is that there is evidence from which inferences could be drawn of a real danger or risk. In this case, that is made out by the combination of little or no tax being returned over a lengthy period of time, no tax returns being filed since 2013, the resistance to the provision of information to the Commissioner of Taxation, and the apparent claiming of expenses which are not on their face claimable to reduce the tax liabilities of the companies concerned. It should also be observed, for completeness, that there is an accrued cause of action because of the service of the notices of assessment: see Commissioner of Taxation v Ornelas [2016] FCA 457 at [7].

14 In all the circumstances, that suffices as giving sufficient reason, ex parte and ex tempore, for making the orders. The form of the orders will be those provided, with suitable adjustments, as provided in draft to the Court.

15 I note, for completeness, that the draft orders sought went somewhat further in relation to the provision of information than the standard form of orders in the practice notes of the Court. In particular, freezing orders practice note GPN-FRZG, in the standard form attached to that practice note, refers only to “location at which books and records are stored”, whereas what is sought here is “the systems by which books and records are maintained, including, for example, any software package used in maintaining those books and records, and the persons within the organisation who have responsibility for maintaining those books and records”. The justification, which I accept, for extending the scope of the standard order is that the material that has been provided so far as evidence before me indicates a lack of reasonable information as to those matters. I considered that it was reasonable, in all the circumstances, that the additional information be ordered to be provided in order to facilitate the effectiveness of the freezing orders and any extension to those freezing orders that may be required.

16 Similarly, the affidavit that is required by the draft orders goes further than just setting out the information referred to above. It also specifically seeks both the recipient and destination of funds transferred out of an account in the name of the first respondent, second respondent and third respondent, being a joint account, in the sums of $500,000 and $14 million, on 20 January 2017 and 10 February 2017 respectively, it not being known where that money has gone. It similarly would require the annexure of a copy of bank statements for the period after that for which the applicant has already been able to obtain bank statements, that is, commencing from 1 July 2016 to the date of the orders. Again, that is justified, in all the circumstances, in support of the making of the freezing orders.

17 For the reasons given above, I made the orders in the form provided by the applicant.

I certify that the preceding seventeen (17) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Bromwich. |

Associate:

SCHEDULE OF PARTIES

NSD 160 of 2018 | |

CITI PURCHASING PTY LTD ACN 055 420 249 | |

Fifth Respondent | LINC PTY LTD ACN 007 239 661 |

Sixth Respondent | EAGLEPOINT INVESTMENTS PTY LTD ACN 603 602 615 |

Seventh Respondent | PATHOLD NO. 84 PTY. LIMITED ACN 064 860 340 |

Eighth Respondent | PALROZ PTY LTD ACN 002 333 173 |

Ninth Respondent | BAYFIN PTY. LIMITED ACN 003 941 740 |

Tenth Respondent | MARTJOHN INVESTMENTS PTY LTD ACN 112 244 087 |