FEDERAL COURT OF AUSTRALIA

Australian Securities & Investments Commission, in the matter of MG Responsible Entity Limited v MG Responsible Entity Limited [2017] FCA 1531

File number(s): | VID 1244 of 2017 |

Judge(s): | DAVIES J |

Date of judgment: | |

Catchwords: | CORPORATIONS – Contravention of s 674(2) of the Corporations Act 2001 (Cth); Facts agreed between the parties including agreement that the contravention was serious for the purpose of section 1317G(1A) of the Corporations Act; pecuniary penalty pursuant to subsection 1317G(1A) of the Corporations Act |

Legislation: | Corporations Act 2001 (Cth) |

Registry: | Victoria |

Division: | General Division |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Category: | Catchwords |

Number of paragraphs: | |

Solicitor for the Plaintiff: | Australian Securities and Investments Commission |

Counsel for the Defendant: | Mr MC Garner |

Solicitor for the Defendant: | Herbert Smith Freehills |

ORDERS

AUSTRALIAN SECURITIES & INVESTMENTS COMMISSION Plaintiff | ||

AND: | Defendant | |

DATE OF ORDER: |

THE COURT DECLARES THAT:

1. The defendant contravened section 674(2) of the Corporations Act 2001 (Cth) (“the Act”) on and from 22 March 2016 continuing until 8:48 am on 27 April 2016 by failing to notify the Australian Securities Exchange (“the ASX”) that circumstances had arisen a consequence of which was that Murray Goulburn Co-operate Co. Limited was unlikely to achieve the forecast Available Weighted Average Southern Region Farmgate Milk Price for the financial year ending 30 June 2016 (“FY16”) of $5.60 per kilogram of milk solids and full-year net profit after tax for FY16 of appropriately $63 million as stated by MG and MGRE in their ASX announcements dated 29 February 2016 titled “Murray Goulburn – Half Year Financial Results News Release” and “Murray Goulburn – Half Year Financial Results Presentation”.

2. The contravention particularised at paragraph 1 of these orders was serious within the meaning of section 1317G(1A)(c)(iii) of the Act.

THE COURT ORDERS THAT:

3. The defendant pay the Commonwealth a pecuniary penalty pursuant to subsection 1317G(1A) of the Act in respect of the declared contravention in the amount of $650,000.

4. The defendant pay the plaintiff’s party and party costs of the proceeding in the sum of $25,000.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

DAVIES J:

Introduction

1 The defendant (“MGRE”) is a listed disclosing entity within the meaning of s 111AL(1) of the Corporations Act 2001 (Cth) (“the Act”) and is subject to the continuous disclosure requirements of s 674 of the Act. MGRE has admitted that it contravened s 674(2) of the Act in failing to notify the Australian Securities Exchange (“ASX”) of material information. MGRE has consented to a declaration being made that it contravened s 674(2) of the Act and to a declaration that the contravention was serious within the meaning of s 1317G(1A)(c)(iii) of the Act. Under s 1317G(1A)(c) of the Act, MGRE is liable to pay a pecuniary penalty of up to $1 million and MGRE has agreed with ASIC that a penalty of $650,000 is appropriate. MGRE has also agreed to pay $50,000 towards ASIC’s investigation costs and $25,000 towards ASIC’s legal costs.

The admission of contravention

2 The admission of contravention is that MGRE contravened s 674(2) of the Act on and from 22 March 2016 continuing until 8:48 am on 27 April 2016 by failing to notify the ASX that circumstances had arisen, a consequence of which was that Murray Goulburn Cooperative Co Limited (“MG”) was unlikely to achieve the forecast Available Weighted Average Southern Milk Region Farmgate Milk Price (“FMP”) for the financial year ending 30 June 2016 (“FY16”) of $5.60 per kilogram of milk solids (“Kgms”) and full-year net profit after tax for FY16 of approximately $63 million, as stated by MG and MGRE in their ASX announcements dated 29 February 2016 titled “Murray Goulburn – Half Year Financial Results News Release” and “Murray Goulburn – Half Year Financial Results Presentation”.

continuous discloure provisions

3 Section 674 of the Act provides:

(1) Subsection (2) applies to a listed disclosing entity if provisions of the listing rules of a listed market in relation to that entity require the entity to notify the market operator of information about specified events or matters as they arise for the purpose of the operator making that information available to participants in the market.

(2) If:

(a) this subsection applies to a listed disclosing entity; and

(b) the entity has information that those provisions require the entity to notify to the market operator; and

(c) that information:

(i) is not generally available; and

(ii) is information that a reasonable person would expect, if it were generally available, to have a material effect on the price of value of ED securities of the entity;

the entity must notify the market operator of that information in accordance with those provisions.

4 The determination of whether or not information is generally available is governed by s 676 of the Act, which relevantly provides that:

(2) Information is generally available if:

(a) it consists of readily observable matter; or

(b) without limiting the generality of paragraph (a), both of the following subparagraphs apply:

(i) it has been made known in a manner that would, or would be likely to, bring it to the attention of persons who commonly invest in securities of a kind whose price or value might be affected by the information; and

(ii) since it was so made known, a reasonable period for it to be disseminated among such persons has elapsed.

(3) Information is also generally available if it consists of deductions, conclusions or inferences made or drawn from either or both of the following:

(a) information referred to in paragraph (2)(a);

(b) information made known as mentioned in subparagraph (2)(b)(i).

5 Section 677 of the Act provides that:

For the purposes of sections 674 and 675, a reasonable person would be taken to expect that information to have a material effect on the price or value of ED securities of a disclosing entity if the information would, or would be likely to, influence persons who commonly invest in securities in deciding whether to acquire or dispose of the ED securities.

6 There is no contravention of s 674 unless the relevant Listing Rules require disclosure of the information. The relevant listing rules are the ASX Listing Rules, and Listing Rule 3.1 provides that:

Once an entity becomes aware of any information concerning it that a reasonable person would expect to have a material effect on the price or value of the entity’s securities, the entity must immediately tell ASX that information.

7 The term “aware” is defined in Listing Rule 19.12 as follows:

an entity becomes aware of information if, and as soon as an officer of the entity … has, or ought reasonably to have, come into possession of the information in the course of the performance of their duties as an officer of that entity.

8 The continuous disclosure obligation in Listing Rule 3.1 is subject to certain exceptions set out in Listing Rule 3.1A. Listing Rule 3.1 does not apply to particular information while:

(a) one or more of the five situations set out in Listing Rule 3.1A.1 applies, namely:

(i) it would be a breach of a law to disclose the information;

(ii) the information concerns an incomplete proposal or negotiation;

(iii) the information comprises matters of supposition or is insufficiently definite to warrant disclosure;

(iv) the information is generated for the internal management purposes of the entity;

(v) the information is a trade secret; and

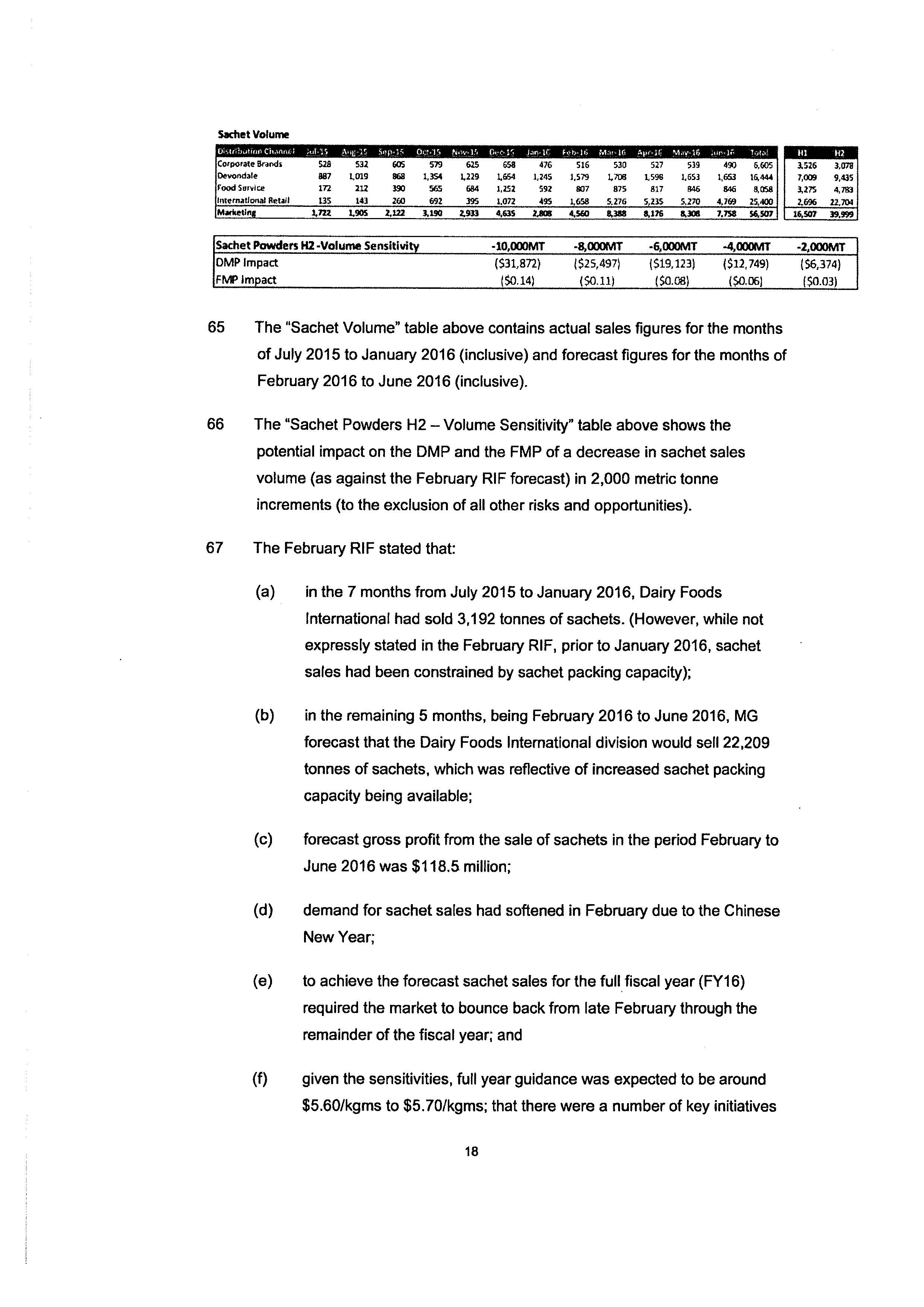

(b) the information is confidential and the ASX has not formed the view that the information has ceased to be confidential; and

(c) a reasonable person would not expect the information to be disclosed.

9 None of the exceptions referred to in Listing Rule 3.1A apply in this case.

civil Penalty provisions

10 Section 674(2) of the Act is a civil penalty provision, contravention of which requires that the Court make a declaration of contravention: s 1317(E)(1) of the Act. Section 674(2) is also a “financial services civil penalty provision” (s 1317DA of the Act), permitting the Court to impose a pecuniary penalty of up to $1 million (s 1317G(1B)(b) of the Act) if the contravention (s 1317G(1A)(c) of the Act):

(a) materially prejudices the interests of acquirers or disposers of the relevant financial products; or

(b) materially prejudices the issuer of the relevant financial products or, if the issuer is a corporation or scheme, the members of that corporation or scheme; or

(c) is serious.

11 ASIC has alleged, and MGRE has accepted, that the contravention was “serious” for the purposes of s 1317G(1A)(c).

agreed statement of facts

12 The parties have filed an agreed statement of agreed facts (“the Agreed Facts”) for the purposes of this proceeding, which is annexure 1 to these reasons for decision. In summary form, the key facts that are material to the contravention of s 674(2) of the Act are as follows.

13 MGRE is a wholly owned subsidiary of MG, a large dairy foods company, and one of the largest milk processors in Australia receiving approximately 20% of milk produced in Australia. During the relevant period MGRE had the same directors as MG, the same managing director (Mr Helou) and the same chief financial officer (Mr Hingle).

14 On 1 May 2015 the MG Unit Trust was established and MGRE was appointed the trustee and the responsible entity for the purposes of Part 5C.2 of the Act. On 29 May 2015, MGRE issued a product disclosure statement (“PDS”) by which it offered fully paid units in the MG Unit Trust. The issue of the units was intended to raise capital for MG and give unitholders an economic exposure to MG and its business. This was via a profit-sharing mechanism (described at paragraph [9] of the Agreed Facts). Return on the units therefore depended on MG’s financial performance.

15 The PDS presented forecast financial information for MG for FY16 which included the following pro forma forecast results:

(a) net profit after tax (“NPAT”) attributable to MG shareholders and unitholders of $86 million; and

(b) FMP of $6.05 per kilogram of milk solids (kgms).

16 Between 1 July 2015 and 27 April 2016, MGRE made three further public statements in relation to the forecast NPAT and FMP for FY16:

(a) on 31 August 2015, as part of its Full Year Financial Results, MGRE made statements regarding the forecast NPAT and FMP, including that they “can be achieved, provided dairy commodity prices strengthen during the balance of FY16”;

(b) on 26 October 2015, MGRE released the Managing Director’s AGM Address to the ASX which stated that “we believe the FY16 PDS forecast of a $6.05 per Kgms Available Southern Milk Region FMP can be achieved, provided dairy commodity prices continue to materially strengthen during the balance of FY16…[I]f MG’s expectations do not materialise, it is likely that:

(i) the FY16 FMP would be in the range of $5.60 to $5.90 per Kgms;

(ii) the FY16 NPAT attributable to shareholders and unitholders would be in the range of $66 million to $79 million”; and

(c) on 29 February 2016, MGRE provided to the ASX MG’s Interim Financial Report for the half year ended 31 December 2015, a Half Year Financial Results Presentation and a Half Year Financial Results News Release (“February Announcement”), which stated that:

MG expects to maintain its opening Available Weighted Average Southern Milk Region FMP of $5.60 per kgms in FY16…

However, this is subject to there being no further material deterioration in dairy commodity prices or unfavourable changes to the current AUD:USD exchange rate. This is at the bottom end of the previous guidance provided and reflects the lack of improvement in global dairy commodity prices and the continued weak outlook for those prices…

Under the Profit Sharing Mechanism, a $5.60 per kgms milk price would be expected to generate for the full year FY16 NPAT attributable to shareholders and unitholders of approximately $64 million.

17 From November 2015, MGRE’s sachet sales of its adult milk powder and revenues forecast were to make a significant contribution to the financial performance of MG in FY16 and to MG meeting the forecast FMP and NPAT for FY16.

18 Throughout the period 1 July 2015 to 30 April 2016, MG prepared monthly “revised income forecasts”, which were internal management documents which provided a monthly update of the company's forecast FMP and NPAT for FY16.

19 The revised income forecasts were usually presented to the Board at each monthly Board Meeting. However, the monthly revised income forecast was not presented to the Board in January 2016 because there was no scheduled Board Meeting (due to the Christmas break). A monthly revised income forecast was also not presented to the Board in March 2016, due to the Board holding a Strategy Day instead. Draft revised income forecasts for March 2016 were prepared and provided to Mr Hingle (as detailed in paragraphs [93]-[95] and [98] of the Agreed Facts), but these drafts were not presented to the Board and not finalised.

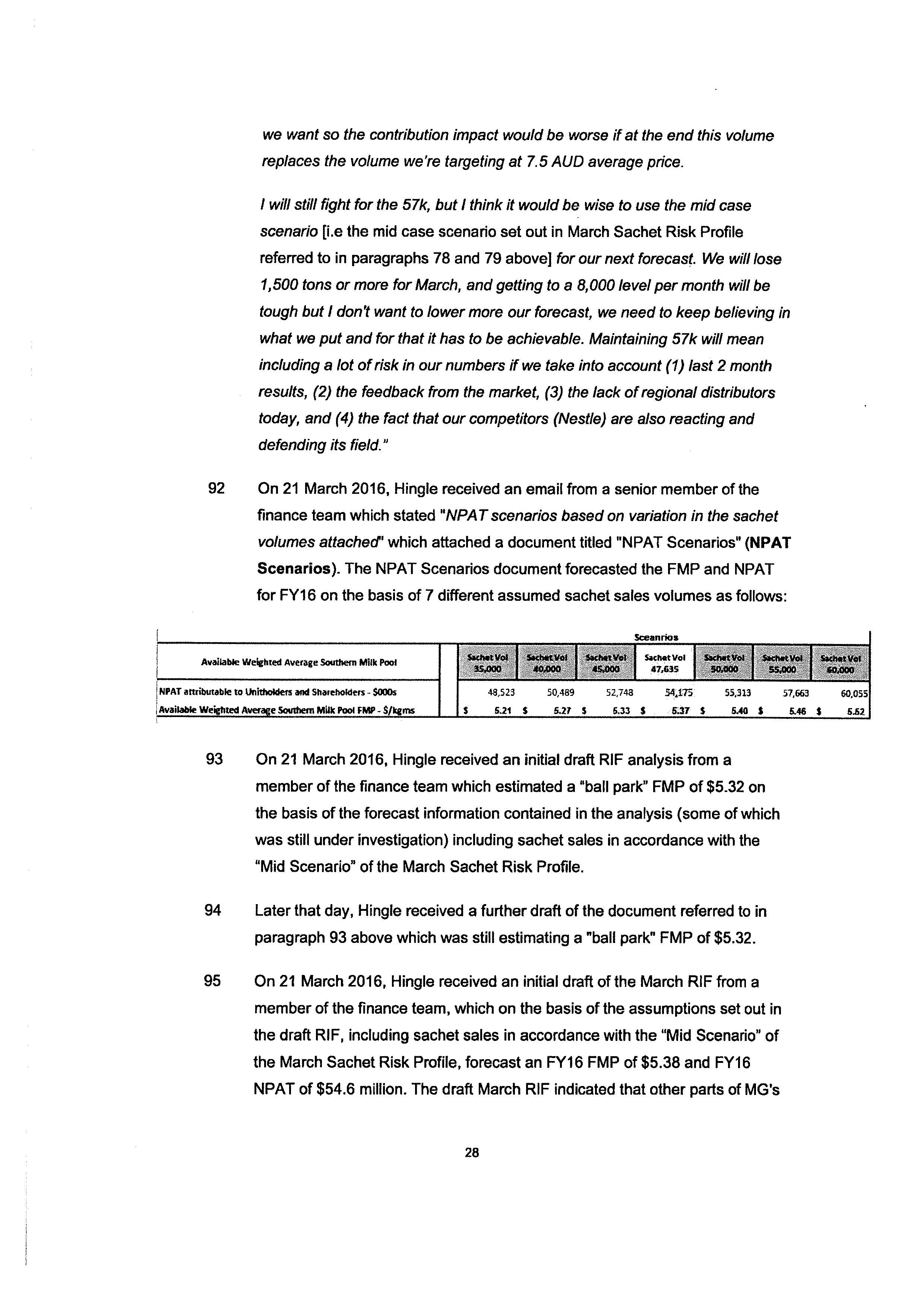

20 During March 2016, Messrs Hingle and Helou became aware of a number of facts relevant to the performance of the sachet sales and the forecast FMP and NPAT for FY16. Those facts are set out at paragraphs [74]-[99] of the Agreed Facts.

21 As at 22 March 2016, MGRE was aware (by reason of the knowledge of Messrs Hingle and Helou of those facts) that:

(a) sachet sales for the month of March to date were tracking significantly below forecast sales for the month of March;

(b) the planned and expected rebound in sachet sales in the month of March 2016, following below forecast sales in each of January and February 2016, had not occurred;

(c) sales of the forecast sachet volumes of 56,507 tonnes for FY16 was considered to be an important contributor to MG achieving the forecast FY16 FMP of $5.60;

(d) sachet sales for FY16 were tracking significantly below forecast sales volumes of 56,507 tonnes;

(e) sachet sales gross sales revenue for FY16 was tracking significantly below forecast sachet sales gross revenue for FY16;

(f) achieving 56,507 tonnes of sachet sales in FY16 was substantially dependent upon MG concluding new distribution arrangements under which sachets would be sold and shipped to China before the end of FY16; and

(g) notwithstanding MG's attempts to do so, new distribution arrangements under which sufficient sachets would be sold and shipped to China before the end of FY16 to meet forecast sachet sales for FY16 had not yet been concluded by MG,

(the “March 22 Facts”).

22 On 19 April 2016, an April Revised Income Forecast (the “19 April RIF”) was provided to the Board. The 19 April RIF stated in relation to sachet sales that:

• Previously forecast 57kt sachets. Slower offtake in Feb and March has impacted full year projection.

• In process of finalising China distribution for Apr to June with 23kt of the 27kt forecast for balance of year supply to China;

• Management require further analysis over the next 2 weeks to better understand:

o Performance of April month, in particular final sachet shipments;

o Agreement of terms and contracts for Sachet sales for May/June with agreed pricing.

• Propose to revert to Board on 6 May, following performance of April, with a definitive range for FY16 outlook.

23 At the Board meeting on 19 April 2016:

(a) the Managing Director provided an update on forecast sachet sales including progress being made on a 24,000 tonne distribution contract to China (being a reference to the proposed arrangements with Asipac); and

(b) the Board requested management to undertake urgent further analysis to better understand final sachet shipments in April, expected contract sales for May and June, infant formula sales into both domestic and Chinese markets and the impact of an increase in promotional activities for domestic consumer markets for May and June in order to assess the impact, if any, on the current forecast.

24 On 22 April 2016, MGRE entered into a trading halt. On 27 April 2016, MGRE released an announcement to the ASX in which it informed the market that MG expected the FY16 FMP to be between $4.75 to $5.00 per Kgms and that MG expected to achieve an NPAT for FY16 of $39 million to $42 million.

25 At 8:48 am on 27 April 2016, MG released the April Announcement to the ASX and at about the same time published the April Announcement on its website. The April Announcement disclosed MG's expected FY16 FMP and NPAT of $4.75 to $5.00 and $39 million to $42 million respectively. The primary driver of MG's revised FY16 FMP was stated to be lower than expected adult milk powder sales in China.

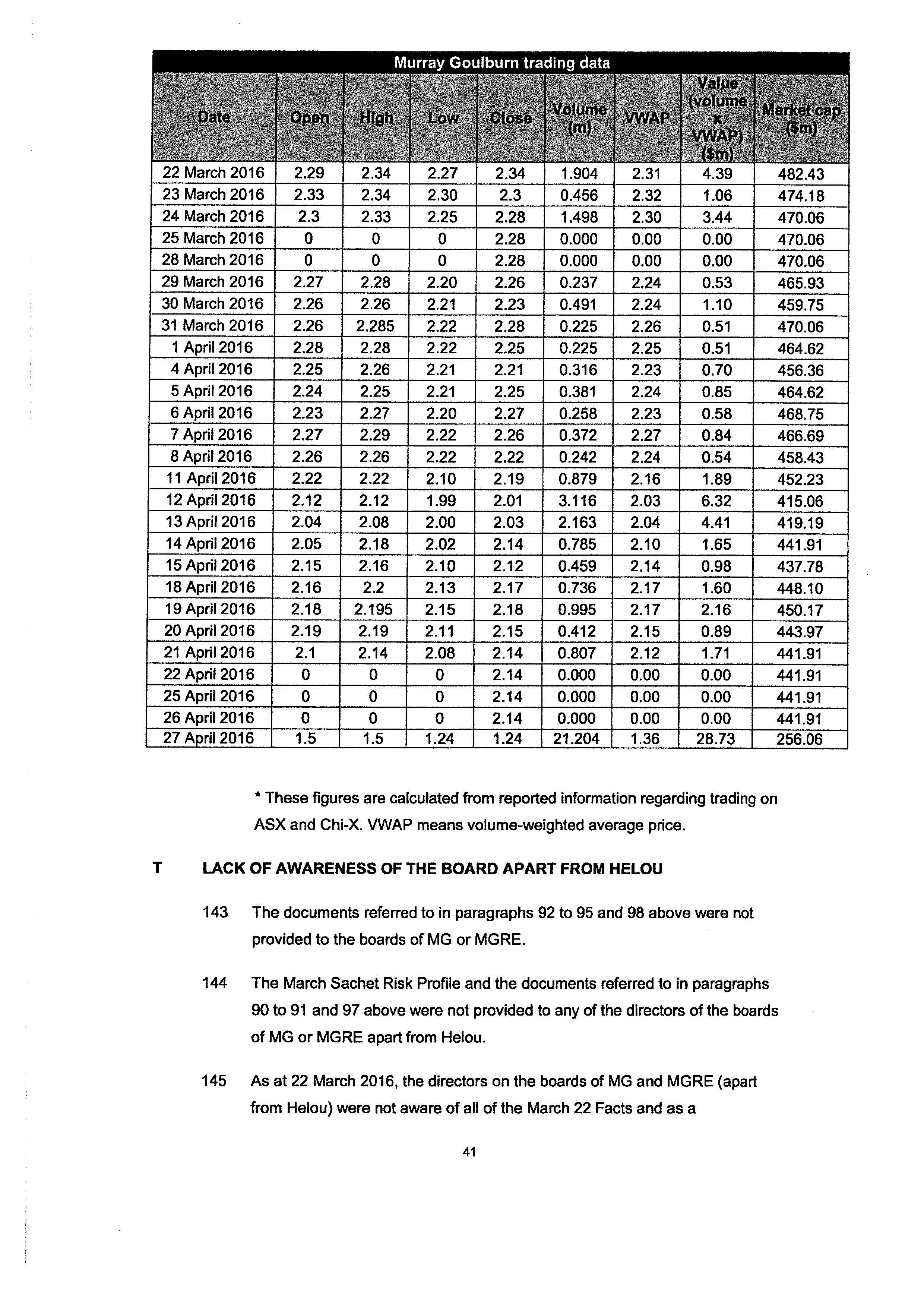

26 The closing price of Units of the MG Unit Trust on 21 April 2016 prior to the trading halt on 22 April was $2.14. Following the April Announcement on 27 April 2016, the price opened at $1.50 (29.9% lower than the closing price prior to the trading halt) and closed that day at $1.24 (42.06% lower than the closing price prior to the trading halt). The volume of Units reported as traded on ASX and Chi-X on 27 April 2016 was approximately 21,203,529 significantly above the 30 day moving average of 818,500 Units.

27 During the period from 22 March to 26 April 2016 (inclusive), approximately 17 million Units in the MG Unit Trust were reported as traded on ASX and Chi-X with a value of $36.7 million (calculated on the basis of volume multiplied by the volumed-weighted average price).

28 The Agreed Facts included that:

(a) it was an objective consequence of the March 22 Facts, when taken collectively and in combination, that MG was unlikely to achieve the forecast FY16 FMP of $5.60 per Kgms and full year FY16 NPAT attributable to shareholders and unitholders of approximately $63 million, as stated in the February Announcement) (“the Material information”);

(b) the Material Information was information that was required to be notified to the ASX by MGRE under ASX Listing Rule 3.1 and s 674(2)(b) of the Act;

(c) as at 22 March 2016, the Material Information was not generally available;

(d) the Material Information was information which a reasonable person would have expected, if it had been generally available, to have had a material effect on the price of the Units, within the meaning of s 674(2) and s 677 of the Act.

declaration of contravention

29 I am satisfied on the basis of the Agreed Facts that the contravention occurred and that the contravention was “serious” for the purposes of s 1317G(1A)(c) of the Act. Accordingly, a declaration of contravention must be made: s 1317E(1) of the Act.

penalty

30 MGRE and ASIC have jointly submitted that the proposed penalty of $650,000 is appropriate for the contravention and in written submissions put the following matters in support:

Market impact and prejudice

86 During the period from 22 March 2016 to 26 April 2016 (inclusive):

(a) the volume of units of the MG Unit Trust traded on market was 16.9 million units; and

(b) the value of units of the MG Unit Trust traded on market was $36.7 million (being the daily VWAP [volume-weighted average price] multiplied by the volume of units traded).

87 The closing price of units of the MG Unit Trust on 21 April 2016 prior to the trading halt on 22 April was $2.14. Following the April Announcement on 27 April 2016, the price opened at $1.50 (29.9% lower than the closing price prior to the trading halt) and closed that day at $1.24 (42.06% lower than the closing price prior to the trading halt).

88 While the Material Information relates only to the fact that MG's forecast FMP and NPAT for FY16 given in the February Announcement were unlikely to be achieved, if that information had been disclosed on 22 March 2016, it would have required MGRE to downgrade those forecasts.

89 It is likely that the announcement by MGRE of a reduced forecast FMP and NPAT for FY16 would have resulted in a fall in the unit price in any event. However, the contravention delayed a likely fall in unit price. It may therefore be inferred that some persons may have acquired units in the period between 22 March 2016 and 21 April 2016 (the day before the trading halt) at a price that was higher than the price the units would have traded at had the Material Information (and the accompanying reduced forecast FMP and NPAT) been disclosed on 22 March 2016.

Circumstances of the contravention

90 The fact that circumstances had arisen as at 22 March 2016 which would lead to a downgrade of the forecast FY16 FMP and NPAT for MG was significant information, particularly in light of the fact that market expectations had been set by the February Announcement:

The seniority of officers responsible for the non-disclosure and whether they included directors of the company

91 As was the case in Sino, the contravention by MGRE occurred at a very senior level of management, namely as a result of the conduct of both Chief Financial Officer and Managing Director. A summary of the key elements of their conduct is set out in paragraph 60 above. Apart from being aware of the March 22 Facts, the objective consequence of which should have been disclosed to the ASX, as in Sino, neither Hingle nor Helou disclosed the March 22 Facts to the Board.

Duration of contravention

92 The period of time over which the contravention by MGRE occurred was 36 days. That period is greater than in Newcrest (10 days) and Southcorp (24 hours).

Compliance policies

93 Although MGRE had written continuous disclosure policies, those policies were not effective in achieving compliance. Significantly, both Helou and Hingle were members of the disclosure committee, but the disclosure committee did not meet during 1 January 2016 and 27 April 2016. Further, neither of them made any relevant disclosures to the disclosure committee, to the Board or to the ASX.

Mitigating circumstances

94 The following circumstances represent mitigating factors.

95 First, the contravening conduct was not deliberate. This is in contrast, for example, to the conduct in Macdonald, where JHINV's conduct was flagrant and grossly negligent, involving a deliberate decision not to disclose in the face of legal advice to the contrary. As the ASOF makes clear, the directors of the Boards of MG and MGRE (except for Helou) were not aware of all of the March 22 Facts, and as a consequence MG and MGRE did not believe or hold the opinion that the forecast FY16 FMP of $5.60 per kgms and full year FY16 NPAT attributable to shareholders and unitholders of approximately $63 million were unlikely to be achieved.

96 Second, MGRE and MG have co-operated with ASIC throughout its investigation and MGRE has made appropriate admissions of fact and contravention.

97 Third, MGRE and MG have reviewed and made changes to their policies and procedures in relation to the company's disclosure practices.

31 I accept that the proposed penalty of $650,000 is appropriate for the contravention. The penalty is towards the higher end of the statutory maximum but a penalty towards the higher end is warranted, reflecting the gravity of the contravention, the market impact and prejudice caused by the contravention, the involvement of the senior level of management in the contravention and failure of governance, and the inadequacy of MGRE’s compliance policies at the time and the duration of the contravention. General deterrence is an important factor in this case and I accept that a penalty of $650,000 gives appropriate weight to general deterrence but allows for the mitigating factors submitted by the parties, including that the contravening conduct was not deliberate. Specific deterrence is less relevant in fixing the penalty in this manner, given that the composition of the board and executive leadership team of MGRE has changed, MGRE has already reviewed and made changes to its policies and procedures in relation to the company’s disclosure practices, and has suffered significant adverse publicity as a result of the events giving rise to the contraventions.

32 I will make the declarations and orders sought.

I certify that the preceding thirty-two (32) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Davies. |

Associate:

ANNEXURE 1