FEDERAL COURT OF AUSTRALIA

Carr v Commissioner of Taxation [2017] FCA 1486

ORDERS

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: | 8 December 2017 |

THE COURT ORDERS THAT:

1. The further amended notice of appeal be dismissed.

2. The applicant pay the respondent’s costs as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BROMWICH J:

1 In April 2012, the respondent, the Commissioner of Taxation, made default assessments of the income tax liability of the applicant, Mr Leon Carr, pursuant to s 167 of the Income Tax Assessment Act 1936 (Cth) (ITAA 1936), in respect of the four income years ending on 30 June 2003, 2004, 2005 and 2006 (relevant years). In total, Mr Carr’s taxable income across those four income years was determined to be $2,168,375. His tax liability was assessed accordingly, together with penalties and interest.

2 The default assessments were made upon the basis that Mr Carr had not lodged tax returns for the relevant years. Mr Carr objected to the default assessments. His objections were disallowed by the Commissioner.

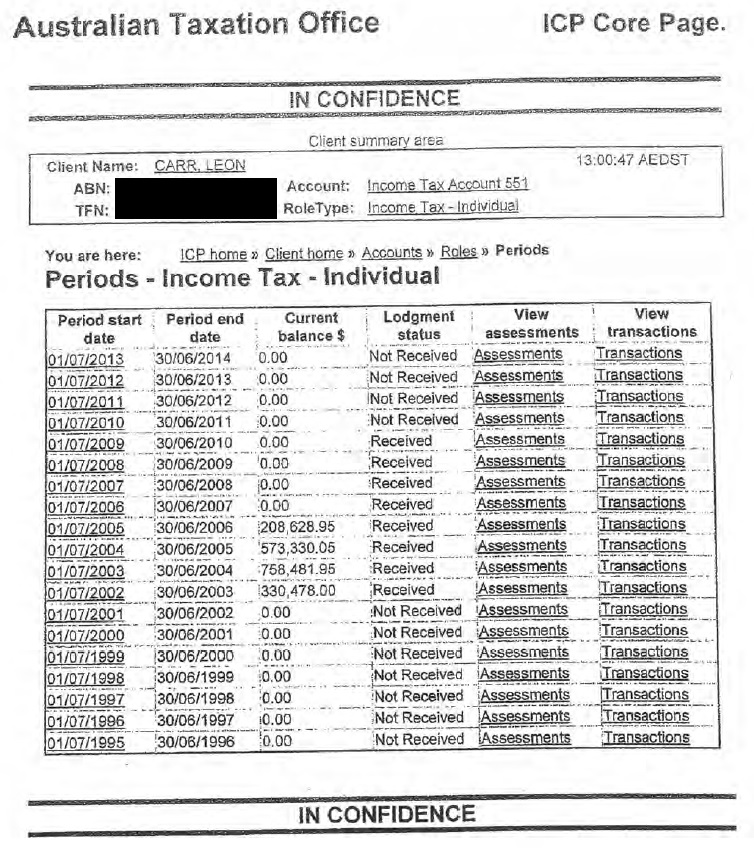

3 Mr Carr applied to the Administrative Appeals Tribunal for merits review of the Commissioner’s objection decisions, contending that he had, in fact, lodged tax returns for the relevant years, having done so even before the Commissioner started sending notices in 2011 requiring that to be done. Ultimately, the Tribunal did not accept Mr Carr’s claim to have lodged the tax returns and concluded that Mr Carr had not shown that any of the assessments were excessive. This was unsurprising, in circumstances where Mr Carr alleged error in the Commissioner’s objection decisions but did not advance a positive case to prove his actual income tax liability, as is required by s 14ZZK(b)(i) of the Taxation Administration Act 1953 (Cth) (TAA). In its decision dated 25 August 2016, the Tribunal therefore found that the Commissioner’s objection decisions were correct.

4 Mr Carr then appealed to this Court under s 44 of the Administrative Appeals Tribunal Act 1975 (Cth) (AAT Act), being an appeal confined to a question of law. Following the unanimous decision of a five-member bench of the Full Court in Haritos v Federal Commissioner of Taxation [2015] FCAFC 92; 233 FCR 315 at [62(1)], it is beyond doubt that the questions of law raised in such an appeal determine its ambit. Such a question of law does not have to be a pure question of law: Haritos at [62(8)].

5 By a further amended notice of appeal, Mr Carr advances what are said to be four questions of law with accompanying grounds of appeal. The Commissioner does not accept that this is the correct characterisation of those questions, but it is not necessary to determine that aspect of the dispute. Mr Carr asserts that:

(1) either there was no evidence, or it was not open on the evidence before the Tribunal, for the Tribunal to conclude that the Commissioner had no record of Mr Carr having lodged the tax returns (ground 1);

(2) the Tribunal overlooked evidence tendered by Mr Carr that he had lodged the tax returns, and thereby constructively failed to exercise its jurisdiction (ground 2);

(3) the Tribunal denied Mr Carr procedural fairness by not informing him, as a self-represented litigant, of his right to an adjournment upon him discovering the legal requirements for discharging the onus he faced in his application for review, and giving him an opportunity to seek such an adjournment in order to rectify the defects in his case (grounds 3 and 4); and

(4) in the alternative to grounds 3 and 4, the Tribunal failed to comply with s 39(1) of the AAT Act by denying Mr Carr a reasonable opportunity to present his case (ground 5).

6 Mr Carr seeks to have this matter remitted to the Tribunal, differently constituted, to enable a rehearing of his application, with the opportunity for further evidence to be adduced.

7 The Commissioner contends that the appeal is without any principled foundation and should be dismissed.

8 For the reasons that follow, the Commissioner’s contentions must be accepted, the arguments advanced on behalf of Mr Carr must be rejected and the further amended notice of appeal must be dismissed.

Before the Tribunal

9 There are several features of Mr Carr’s case before the Tribunal that should be emphasised to provide context for his appeal:

(1) Mr Carr was self-represented.

(2) Mr Carr contended that he had lodged his returns for the relevant years and that they were not outstanding at all. However, he was unable to produce copies of the purported returns or any notices of assessment to support that claim. In this regard, Mr Carr asserted to the Tribunal that those documents had been destroyed as a result of an incident with his storage company. Relevantly, the Tribunal found at [4] of its reasons that the Commissioner had no record of Mr Carr having lodged the returns in question. Ultimately, the Tribunal did not accept Mr Carr’s claim to have lodged returns for the relevant years.

(3) As pointed out by the Commissioner, Mr Carr’s case before the Tribunal was fundamentally misconceived in that he sought to discharge the onus imposed on him by s 14ZZK(b)(i) of the TAA to prove that the assessments were excessive by showing error in the Commissioner’s reasoning, when this was not enough to meet the requirements of that provision, citing Agius v Commissioner of Taxation [2015] FCA 707 at [55]; Commissioner of Taxation v Rigoli [2013] FCA 784; 95 ATR 94 at [9]-[10] and George v Federal Commissioner of Taxation (1952) 86 CLR 183 more generally. The Tribunal’s reasons at [29] accorded with that authority; see also Zappia v Commissioner of Taxation [2017] FCAFC 185 at [3], citing Federal Commissioner of Taxation v Australia and New Zealand Savings Bank Limited (1994) 181 CLR 466 at 479.

(4) As pointed out by the Commissioner, it was for Mr Carr to prove before the Tribunal what the correct assessment should have been, and for that purpose to show that his assessable income was less than that in the assessments: Federal Commissioner of Taxation v Dalco (1990) 168 CLR 614 at 621, 631. The Tribunal at [7]-[11] correctly identified this ultimate question, the principles by which it was required to be addressed and the onus that fell upon Mr Carr to address it. At no point did Mr Carr show, or attempt to show, what his actual assessable income was for the relevant years.

(5) It appears, and is deposed to by Mr Carr for the purposes of this appeal, that he was not, in fact, aware, until the Tribunal hearing, that he needed to file evidence as to his income and expenses for the relevant years. Similarly, it is deposed to by Mr Carr that he was not aware until the Tribunal hearing that he could contend that the assessments were excessive if he could show that previous assessments had been issued and the amended assessments that were the subject of the application were therefore issued out of time.

(6) Mr Carr did not seek an adjournment of the Tribunal hearing to enable him to put further evidence before the Tribunal. As described by the Tribunal, his evidence as to his actual taxable income during the relevant years was “meagre” and did not enable that amount to be determined.

Evidence before the Tribunal as to the lodgment of Mr Carr’s tax returns

10 For the purposes of considering the first and second grounds of appeal, it is necessary to canvass the evidence before the Tribunal relevant to the question of lodgment or non-lodgment of Mr Carr’s tax returns for the relevant years.

11 The material before the Tribunal encompassed certain affidavit evidence, oral evidence of the applicant and five witnesses, and a large number of documents that were tendered to the Tribunal as exhibits. Most of that evidence did not require consideration in this appeal.

12 In relation to the issue of whether the Commissioner had records of Mr Carr having lodged tax returns for the income years ending in 2003, 2004, 2005 and 2006, the material before the Tribunal relevantly included the following:

(1) An oral representation by Mr Carr at the hearing as follows:

DEPUTY PRESIDENT: Let me put it as simply as I can. The Tax Office has no records of your previous returns and neither do you. Is that right?

MR CARR: Correct.

(2) Evidence given by Mr Carr in cross-examination by counsel for the Commissioner as follows:

--Do you recall in the course of opening this morning making other assertions to the Deputy President along the lines of you having lodged the tax returns for the tax years in issue?

MR CARR: To the best of my knowledge my tax returns had been lodged.

(3) Evidence given by Mr Carr that the relevant tax returns he purported to have lodged could not be produced because there had been an incident with his storage company that had resulted in the destruction of those documents.

(4) Letters dated 5 August 2009 and 4 September 2009 from the Commissioner to Mr Carr, consisting of a request and final notice for lodgment of tax returns for the 2005 to 2008 income years.

(5) A letter issued in February 2011 giving final notice requiring Mr Carr to lodge tax returns for the 1996 to 2006 income years.

(6) The default assessments issued under s 167 of the ITAA 1936 in April 2012 for the 2003 to 2006 income years.

(7) A “Notice of intention to commence prosecution action” issued by the Australian Taxation Office (ATO) dated 6 July 2012, which included the sentence “Despite the issue of a final notice on 7 May 2012, our records show that the returns have not been received.”

(8) Reasons given on 21 January 2013 on behalf of the Commissioner for the disallowance of Mr Carr’s objections, which relevantly included as background information the statement that “ATO records indicate that you did not lodge tax returns for the income years ending 30 June 1996 to 2006 inclusive.”

13 The material before the Tribunal also included documents that had been prepared for the purposes of an unsuccessful prosecution of Mr Carr by the Commissioner on charges under s 8C(1)(a) of the TAA that he had failed to comply with notices to furnish tax returns for the seven income years prior to the relevant years. Those documents were tendered to the Tribunal and admitted into evidence as annexures to a statement prepared by Mr Carr. In the present appeal, reliance is placed by Mr Carr on one of those documents and its annexures as constituting evidence that the Commissioner had received his tax returns for the relevant years. The document in question is a statement prepared by Ms Julie Kang, a prosecutor for the ATO, which records Ms Kang’s view, based on a review of the ATO’s information systems, that she had found “no record of lodgment or refund for the tax periods ending 30 June 1996 to 30 June 2002 under [Mr Carr’s] two [Tax File Numbers]”. Relevantly, that statement refers to and annexes four printouts from one of the ATO’s information systems, which is identified as the “Integrated Core Processing (ICP) system” and is said to provide “an integrated view of client information and interactions concerning processing of income tax, accounts, forms, payments, debts and lodgments”. In respect of those four printouts (the ATO electronic records), Mr Carr places particular reliance on the display of the word “Received” in the “Lodgment status” columns for the four income years in question before the Tribunal. An image of one of those records has been reproduced further below as part of the consideration of Mr Carr’s first ground of appeal.

Ground 1 – no evidence or finding not reasonably open

14 By ground 1, Mr Carr asserted that there was “no probative evidence to support the Tribunal’s finding that the [Commissioner] had no record of [Mr Carr] having lodged returns for the relevant years”. The relevant finding was set out within [4] of the Tribunal’s reasons as follows (emphasis added):

Mr Carr claims that he had in fact lodged his returns for the relevant years and that they were not outstanding at all. He claims that his returns had been lodged even before the Commissioner started sending notices to him in 2011. Mr Carr was not able to produce file copies of any such tax returns, nor any notices of assessment to support his claim that he had previously lodged returns for the relevant years. The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years. I do not accept Mr Carr’s claim that he had lodged returns for those years.

15 According to Mr Carr, the emphasised sentence in the above passage that “The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years” was either:

(1) a finding for which there was no evidence for the negative proposition stated; or

(2) a finding that was not reasonably open on the whole of the evidence.

16 Each point has been considered in turn.

The first point: there was no evidence for the Tribunal’s negative proposition

17 Mr Carr’s assertion that there was no evidence for the negative proposition stated by the Tribunal – namely, that the Commissioner had no record of Mr Carr having lodged tax returns for the relevant years – relied upon establishing that that there was in fact some evidence before the Tribunal to the contrary. In this regard, Mr Carr relied on the printouts of the ATO electronic records that were annexed to the statement of Ms Julie Kang, canvassed at [13] above. Those printouts were said to constitute evidence that was inconsistent with the Tribunal’s finding, to the extent that, in recording details about income tax periods in respect of Mr Carr, certain of those records display the word “Received” in a column headed “Lodgement status” for each of the four relevant years. Mr Carr contended that this Court should make a finding in this appeal that the only proper reading of those entries is to give them the meaning suggested on their face – namely, that the ATO had a record of having “received” Mr Carr’s lodged tax returns for the relevant years – and that this was overlooked by the Tribunal.

18 It is easier to understand the point being made by reproducing an image of one of the records in question (noting that Mr Carr’s Australian Business Number and Tax File Number have been redacted):

19 The first issue to be determined is the proper meaning to be attributed to the impugned sentence in the Tribunal’s reasons, namely, that “The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years.” I accept, as contended by Mr Carr, that the sentence should be read as being a negative statement that there was no ATO record at all in existence that indicated that the tax returns in question had been lodged. That construction seems to be the only proper way to read the sentence both grammatically and in context.

20 The next issue to be resolved is whether the Tribunal’s finding was, in fact, contradicted by the printouts of the ATO electronic records that displayed the word “Received” in the “Lodgement status” column for each of the relevant years. A number of collateral questions arise.

21 The first collateral question is whether the meaning of the word “Received” in the printouts from the ATO electronic records can be determined by this Court in a s 44 appeal confined to a question of law. Having regard to what was said by the Full Court in Haritos at [62(8)], the answer to that question seems to be “yes”, insofar as a mixed question of fact and law may be raised as to whether the only correct way to view the evidence is that it was incapable at law of supporting the conclusion reached by the Tribunal as to the state of the evidence before it: see also Rawson Finances Pty Ltd v Commissioner of Taxation [2013] FCAFC 26; 133 ALD 39; 296 ALR 307 at [83]-[86], [103]. If it were only a question of interpretation of the evidence about which reasonable minds could differ, no question of law arises.

22 With some hesitation, I am prepared to accept that the argument advanced on behalf of Mr Carr does raise a question of law. That question of law is whether the meaning of “Received” in the ATO electronic records did not permit the Tribunal to conclude that the Commissioner had no record of Mr Carr lodging the income tax returns for the relevant years. The correctness of the consequential conclusion reached by the Tribunal that Mr Carr had not filed income tax returns so as to give rise to default assessments, however, would not be for this Court to determine but, rather, a matter for the Tribunal if remittal were otherwise appropriate.

23 The next question that arises is whether the only proper interpretation of the word “Received” in the ATO’s electronic records is to accord it its ordinary meaning in the context of the heading in which that word appears. Although, superficially, that construction might seem compelling and obvious as a matter of English language, further consideration reveals that it is unsafe to proceed upon that abstract linguistic basis.

24 The only evidentiary explanation before the Tribunal for the ATO electronic records was that given by Ms Kang, whose statement for the prosecution proceedings described the source of the records, the “Integrated Core Processing (ICP) system”, as providing an “an integrated view of client information and interactions concerning processing of income tax, accounts, forms, payments, debts and lodgements”. It is clear, however, on the face of the four printouts, that they are too sparse to provide the entirety of that wide array of information, and are necessarily referred to by Ms Kang and annexed to her statement as reflecting only a partial record of the information in the “ICP” system.

25 The conclusion that the ATO’s “ICP” system must encompass more information than is disclosed on the face of the printouts is also supported by having regard to what are clearly hyperlinks in the columns for each taxation period headed “View assessments” and “View transactions”, which doubtless must direct the viewer to further information about any such assessments or transactions that have been recorded. That further information may in turn expand on and inform the meaning of the information in the other columns, including, potentially, the meaning of “Received”. For example, the word “Received” might indicate that something purporting to be a lodgment has been uploaded to the system, notwithstanding that the file might contain no information, or otherwise be invalid as a tax return. The true position might only be ascertained upon inspection of the information available elsewhere, via the links to assessments and transactions. It follows that, while tempting, it is contextually unsafe to insist on the ordinary meaning of the word “Received”. Critically, insistence on that meaning would be to ignore the word’s use as part of records within a digital information system, which may use such commonplace words in a way at odds with their ordinary textual meaning. It would also be to ignore the balance of the evidence which the Tribunal did have regard to that strongly indicated that no tax returns had been lodged, in which case it is most unlikely that there would exist any record to the contrary.

26 If the word “Received” meant that the relevant tax returns had, in fact, been lodged, it is difficult to comprehend how and why that would be ignored. That is especially so given the ATO information system’s evident use to manage the process of lodgement and assessment of tax returns, and therefore to inform ATO officers of what has happened and what action might need to be taken. To conclude that the word “Received” can only mean that the relevant tax returns had been lodged, but overlooked, is also inconsistent with the steps taken by the ATO of requesting that the tax returns be lodged, of issuing a notice requiring that to take place and of raising default assessments upon the basis that lodgement had not occurred. The taking of those steps sounds an alarm bell that the word “Received” does not necessarily have the limited meaning attributed to it by Mr Carr and urged upon this Court. There is a distinct possibility that while the words “Not Received” might, or might not, have an unambiguous meaning in accordance with Ms Kang’s statement, the word “Received” as used in a computer system may signify a variety of things.

27 I therefore decline to make the indispensable finding urged upon me by Mr Carr that “Received” in the printouts of the ATO electronic records had to be regarded by the Tribunal as some kind of record that the relevant tax returns had been lodged by Mr Carr, and that the Tribunal was therefore required to take that record into account in deciding whether or not such returns had in fact been lodged by him.

28 The first point in ground 1 must therefore fail because the evidence relied upon by Mr Carr does not rise to the asserted level of showing that the conclusion reached by the Tribunal was not available, so as to be an error of law.

29 For more abundant caution, in case I am wrong on the basis for the foregoing to refuse to attribute to the word “Received” the unambiguous meaning that Mr Carr contends for, I turn to the evidence that the Commissioner sought to rely upon to prove the true meaning of that word as used in the ATO electronic records.

30 It is apparent that the meaning of “Received” in the printouts of the ATO’s electronic records was not an issue that was raised at any time before the Tribunal. Quite to the contrary; early on the first day of the three-day hearing, recorded on page 8 of the transcript (out of a total of some 280 pages), the following exchange took place between the Deputy President and Mr Carr:

DEPUTY PRESIDENT: Let me put it as simply as I can. The Tax Office has no records of you[r] previous returns and neither do you. Is that right?

MR CARR: Correct.

31 In the above exchange, I do not read the use of the word “Correct” by Mr Carr as being confined to the issue of his own records, but, rather, as reflecting both an acceptance of the overall position summarised by the Deputy President, and Mr Carr’s stance as to the status of the Commissioner’s records insofar as they were known to him (and indeed tendered by him). That necessarily included the printouts of the ATO electronic records put into evidence before the Tribunal by Mr Carr. The response of “Correct” by Mr Carr to the question asked by the Deputy President therefore amounted to a concession, or at least a position taken, by Mr Carr that he was not contending that there was such a record held by the ATO, but rather that the ATO records were wrong or incomplete in failing to record the lodgements that he said had in fact taken place. This view is supported by Mr Carr’s statement filed with his application for review by the Tribunal dated 20 February 2014, in which he said in relation to the ATO not having a record of him having lodged the tax returns, “I would suggest there is a lost file and I am paying for a computer glitch”.

32 In light of Mr Carr’s concession, or stated position, and his failure to rely on the use of the word “Received” to advance the position he took before the Tribunal that he had, in fact, lodged the relevant tax returns, the point raised in this appeal as to the proper meaning of that evidence appears to be something that has been devised after the adverse result. It does not reflect any issue that was live before the Tribunal at the hearing about the meaning of that part of the evidence. Had such an issue been raised at the time, the Commissioner would have had an opportunity to address it then, rather than endeavouring to do so now in this appeal. In those circumstances, there was no systems evidence put before the Tribunal as to what the word “Received” meant in the printouts of the ATO electronic records. There is no indication that the word “Received” in those printouts was therefore given any consideration by the Tribunal that was contrary to the concession by, or stated position of, Mr Carr.

33 There is little reason to doubt that, had the issue been raised before the Tribunal, it would have been resolved by way of evidence in the Tribunal, rather than sought to be addressed in this Court by way of a superficially attractive inference or conclusion that does not bear closer examination or resolve doubt in the context of all of the evidence. There is no reason to doubt that the Commissioner would have sought to adduce evidence on the correct meaning to be given to the word “Received” in the ATO electronic records. There is equally no reason to doubt that adducing such evidence would most likely have been permitted in order that the Tribunal be properly informed to make findings about the meaning of the electronic records. This was meant to be a serious determination of a merits appeal by the Tribunal in accordance with its statutory objectives and obligations, not some kind of forensic word game.

34 This leads to consideration of evidence sought to be relied upon by the Commissioner in the form of an affidavit of a Mr Lever, an officer of the ATO. This evidence is sought to be relied upon by the Commissioner under s 44 of the AAT Act in order to assist in determining the meaning of “Received” in the ATO electronic records. The conduct of the case before the Tribunal, and, in particular, the comment made by Mr Carr on this very issue, are compelling reasons to allow the Commissioner to do now what he would almost certainly have done before the Tribunal by way of evidence to explain what was meant by the word “Received” in the ATO’s electronic records. That is a preferable course to the alternative of not giving Mr Carr leave to depart from his case before the Tribunal for the purposes of his appeal. To the extent that such leave is required, it is therefore granted.

35 As already noted at [33] above, there is no reason to doubt that evidence of this kind or to this effect would have been led had this been an issue before the Tribunal. Equally, there is no reason to doubt that such evidence would be led at any remittal. That evidence is effectively beyond practical challenge. Mr Lever was not sought for cross-examination, presumably in recognition of that reality.

36 I am satisfied that the additional evidence should be permitted to be relied upon by the Commissioner, in accordance with ss 44(7) and (8)(b) of the AAT Act, by reason of:

(1) the foregoing history of the proceedings before the Tribunal;

(2) the narrowness of the issue raised;

(3) the convenience and desirability of having the most reliable evidence of what the word “Received” as used in the ATO’s electronic records in fact meant for the purposes of resolving this issue now; and

(4) avoiding what might otherwise be a time-wasting, if not futile, remittal back to the Tribunal.

37 Mr Lever’s affidavit relevantly states:

5. Pages T1-46, T1-47, T1-49 and T1-50 of the T-Documents are extracts from the [Integrated Core Processing system] records held by the Respondent in relation to the Applicant (the “Extracts”). The extract shown at T1-50 relates to a duplicate tax file number (“TFN”) of the Applicant, that TFN being [number omitted] (the other being [number omitted]). The Extracts show the Applicant’s income tax return lodgement status for the income years ended 30 June 1996 to 30 June 2014.

6. The ‘Lodgement Status’ column on the Extracts (as is the case with the Respondent’s ICP records generally) uses one of three descriptions in relation to a tax return: ‘Received’; ‘Not Received’; or ‘Return not Necessary’. If a default assessment pursuant to s 167 of the Income Tax Assessment Act 1936 (Cth) is raised by the Commissioner because a taxpayer has not lodged an income tax return, the ‘Lodgement Status’ for that year will change from ‘Not Received’ to ‘Received’.

7. On 28 July 2017, I went into the ICP records kept by the Respondent in relation to the Applicant, and viewed the ‘Transactions’ pages pertaining to the Applicant’s income tax returns for the income years ended 30 June 2003, 30 June 2004, 30 June 2005 and 30 June 2006 (see paragraphs 8 to 11 below for the relevant annexures). In none of those four years, for either of the Applicant’s two TFNs is ‘Client form’ recorded in the ‘Transaction type’ column. This indicates that the Applicant did not lodge a return for any of those four years. In each of those four years ‘Cmsr default assessment’ is recorded in the ‘Transaction type’ column, with the exception of the extract for the duplicate TFN, where no transactions are recorded. This indicates that the Commissioner issued a default assessment to the Respondent for each of those four years.

38 In context, the meaning of “Received” that is applicable to Mr Carr is that default assessments had issued against him for the four income years in question. It did not mean that tax returns had been received from him, or on his behalf, for those years. Had the records accessible via the link reading “Transactions” for each income year been reviewed, as doubtless would have happened had this issue been raised before the Tribunal, the results would have been shown, as per Mr Lever’s evidence, to depict “Cmsr default assessment”, indicating not that a tax return had been filed, but, rather, that a default assessment had been made by the Commissioner. In all probability, that page would have been printed out and put in evidence, putting this issue entirely to rest. Those pages were annexed to Mr Lever’s affidavit, but do not warrant further reproduction.

39 On any view, correctly understood, the word “Received” in the printouts before the Tribunal were not any evidence that income tax returns had been received for any of the relevant years, and certainly not evidence that any prior assessments had issued. The only conclusion that this Court needs to reach is that the use of the word “Received” in the ATO’s electronic records did not require the Tribunal to find other than that “The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years”. This reinforces the conclusion reached above, without recourse to the additional evidence from Mr Lever, that no error of law has been established. That additional evidence shows that no error of law could have been established.

40 In any event, it is doubtful that there could be any error of law based on a point not taken in the Tribunal, irrespective of the need for leave to take it on appeal. As the Full Court pointed out in Commissioner of Taxation v Glennan [1999] FCA 297; 90 FCR 538 at [82], as a general rule, there can be no error of law if the AAT fails to address an issue of fact or law that was not the subject of argument by the taxpayer.

41 The Tribunal on any remittal would have little choice but to receive Mr Lever’s evidence and, upon that basis, would be entitled, if not obliged, to adhere to the finding already made that “The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years”. Remittal upon this ground would therefore be futile. However, that does not arise for determination by reason of the other reasons for rejecting ground 1. This conclusion is therefore only recorded for completeness.

The second point: the Tribunal’s finding was not open to it on the whole of the evidence

42 The second point, that the relevant finding was not reasonably open to the Tribunal on the whole of the evidence, is more easily disposed of than the first. That is because the Tribunal had before it logically probative material which indicated that the Commissioner had no record that tax returns had been lodged, including material outlining steps taken that were inconsistent with any such record having existed. That material included the following, adverted to in [2], [3] and the earlier portion of [4] of the Tribunal’s reasons:

(1) unsuccessful attempts by the Commissioner to secure lodgement of outstanding tax returns for 2005 to 2008 years of income, thus covering the last two years in issue, 2005 and 2006;

(2) the issuing in February 2011 of a final notice, requiring Mr Carr to lodge tax returns for the 1996 to 2006 income years, covering all four years in issue;

(3) the issuing of default assessments under s 167 of the ITAA 1936 in April 2012 for the four income years ending 30 June 2003 to 2006 based upon tax returns not being lodged for those years;

(4) “Notice of intention to commence prosecution action” issued by the ATO dated 6 July 2012, including the sentence, “Despite the issue of a final notice on 7 May 2012, our records show that the returns have not been received”; and

(5) reasons given on 21 January 2013 on behalf of the Commissioner for the disallowance of Mr Carr’s objections, which relevantly included as background information the statement that “ATO records indicate that you did not lodge tax returns for the income years ending 30 June 1996 to 2006 inclusive.”

43 It was open to the Tribunal to accept the evidence that was expressly referred to, in the context of like evidence that was not expressly referred to, and to conclude that the Commissioner had no record that tax returns had in fact been lodged by the applicant. It cannot be said that such a finding was not reasonably open, merely because an alternative conclusion might have been reached to the effect that some record or entry was capable of being interpreted differently. This is a question of weight on the whole of the evidence, being fact finding that was a matter for the Tribunal provided the evidence was legally capable of supporting the conclusion reached. The Tribunal was entitled to conclude that “The Commissioner had no record of Mr Carr’s having lodged returns for the relevant years.”

Ground 2 – failure to consider evidence

44 Ground 2 asserted a constructive failure by the Tribunal to exercise jurisdiction, on the basis that it had overlooked parts of Mr Carr’s evidence, being the ATO’s electronic records, and thereby failed to consider Mr Carr’s claim that the default assessments had been issued out of time.

45 The conclusion reached in relation to ground 1 necessarily dictates the outcome of this ground. Having regard to the inability of this Court to find that the reference to “Received” in the ATO electronic records constituted evidence that the Commissioner had a record of Mr Carr having lodged his tax returns, it cannot be concluded that this evidence was overlooked in relation to Mr Carr’s claim that the default assessments had been issued out of time. This is particularly so in circumstances where Mr Carr had effectively conceded to the Tribunal that the Commissioner had no record of him having lodged an income tax return, and Mr Carr did not place any express reliance on the electronic records for the purpose of proving otherwise.

46 Therefore the asserted issue concerning the default assessments being out of time could not have arisen and there could be no constructive failure to exercise jurisdiction on such an issue.

Ground 3 – denial of a reasonable opportunity for Mr Carr to present further evidence

47 Under ground 3, Mr Carr asserted that he had been denied a fair opportunity to present his case before the Tribunal. In particular, he contended that the Tribunal ought to have informed him, with sufficient clarity, that it had the power to adjourn the hearing to enable him to obtain the further evidence that he needed, and that it was a matter for him to make such an application and set out the reasons for the adjournment being granted. This obligation was said to have arisen in circumstances where Mr Carr was self-represented, had not prepared any evidence as to his income and expenses for the relevant years, and had only become aware for the first time during the hearing that he was required to discharge the onus of proof under s 14ZZK of the TAA by proving his income and expenses for those years. To demonstrate those circumstances, Mr Carr relied upon affidavit evidence that was admitted without objection and the transcript of his comments at the Tribunal hearing.

48 Any requirement for the Tribunal to advise overtly of the right to apply for an adjournment cannot be a standing obligation, but rather one that is triggered in the particular circumstances of the case at hand. It would necessarily arise as an aspect of the general obligation to afford an applicant a reasonable opportunity to present his or her case: cf Sullivan v Department of Transport (1978) 20 ALR 323. It follows that the existence of such an obligation must be considered having regard to the applicant’s position as assessed objectively.

49 In the present case, it cannot be concluded that Mr Carr was denied a reasonable opportunity to present his case. While it might be shown that Mr Carr was in fact apparently not aware of the nature of the case he was required to make, he cannot show that this lack of awareness was reasonable in the circumstances, let alone that the Tribunal was subject to an obligation to advise him of his capacity to apply for an adjournment in those circumstances. Critically, Mr Carr had been provided with clear information to the effect that to discharge the relevant onus of proof, he was required to prove his income and expenses for the years in question.

50 The information furnished to him was as follows:

(1) the Commissioner’s reasons for the decision to disallow Mr Carr’s objections dated 21 January 2013, more than three years before the Tribunal hearing, included numerous clear and express references to the onus on Mr Carr;

(2) the Commissioner’s submissions before the Tribunal stated at length the hurdle Mr Carr was facing – while those submissions were dated 19 February 2016, which was the Friday before the first hearing day on Monday, 22 February 2016, they fall to be considered in the context of the Commissioner’s reasons for the decision to disallow Mr Carr’s objections dated 21 January 2013, which amply put Mr Carr on notice of the problems with the case he sought to advance, had he troubled to read those reasons, which were expressed in reasonably clear and blunt terms; and

(3) the Tribunal spelt out the position at several points on the first hearing day.

51 Moreover, it was not the role of the Tribunal to make Mr Carr’s case for him, nor even to help him to do so: see Glennan at [82]. The obligation to ensure that a party to proceedings before the Tribunal has a reasonable opportunity to present their case does not extend to ensuring that a party takes the best advantage of such opportunities: Sullivan at 343. To hold that the Tribunal was subject to an obligation to advise Mr Carr of a right to seek an adjournment, no matter how lacking in merit such an application might be, and no matter what information had already been provided, crosses the line and would oblige the Tribunal to go further than necessary or desirable for the proper discharge of its functions in this or any other like case.

52 There was no “practical injustice” in the Tribunal not advising or otherwise suggesting that Mr Carr could apply for an adjournment: see Re Minister for Immigration and Multicultural Affairs; Ex parte Lam [2003] HCA 6; 214 CLR 1 at [37]. Nor is there anything to indicate that such an adjournment would have been a reasonable or proper course for the Tribunal to adopt, let alone one compelled by the circumstances. There was no clear indication of what an adjournment could possibly have achieved. There was no evidence that it could possibly have made any difference to the outcome.

53 Accordingly, there was no denial of procedural fairness by the Tribunal. Ground 3 must fail.

Ground 4 – denial of a reasonable opportunity for Mr Carr to present a “new argument”

54 This ground is based on the proposition that, because Mr Carr was expressly made aware at the Tribunal hearing that he could prove that the assessments were excessive by proving that they were issued out of time, he should have been given an opportunity to advance this “new argument”. The problem with this asserted new argument is that it turns entirely on Mr Carr being able to prove that he had lodged his tax returns for the four income years in question, so as to render the default assessments out of time. He was given ample opportunity over many years to prove that position, but failed to avail himself of that opportunity. For the reasons given in relation to ground 1, there was no error of law on the part of the Tribunal in reaching that conclusion and, in any event, no different result would be tenable on remittal. Ground 4 must therefore fail.

Ground 5 – failure to comply with the procedural fairness requirement in s 39(1) of the AAT Act

55 Ground 5, which was in the alternative to grounds 3 and 4, asserted a failure to comply with the statutory duty in s 39(1) of the AAT Act to provide Mr Carr with a reasonable opportunity to present his case. This ground was not argued on any different basis to that advanced for grounds 3 and 4, save only that a different legal framework was referred to as giving rise to the requirement of procedural fairness. As those grounds have failed, so too must this ground of appeal.

Conclusion

56 The appeal must be dismissed with costs.

I certify that the preceding fifty-six (56) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Bromwich. |

Associate: