FEDERAL COURT OF AUSTRALIA

Knauf Plasterboard Pty Ltd v Plasterboard West Pty Ltd (In Liquidation) (Receivers and Managers Appointed) [2017] FCA 866

ORDERS

KNAUF PLASTERBOARD PTY LTD ACN 003 621 010 Applicant | ||

AND: | PLASTERBOARD WEST PTY LTD (IN LIQUIDATION) (RECEIVERS AND MANAGERS APPOINTED) ACN 150 949 803 Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. On or before 8 August 2017 the parties are to provide to the associate to Markovic J short minutes of order to give effect to these reasons.

2. On or before 15 August 2017 the parties are to file and serve submissions, not exceeding 5 pages in length, in relation to costs of the proceeding.

THE COURT NOTES THAT:

3. Unless the parties indicate otherwise, the issue of costs will be dealt with on the papers. If the parties require an oral hearing on the issue of costs they are to approach the associate to Markovic J for a date for the matter to be listed for argument on that issue.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 Knauf Plasterboard Pty Ltd (Knauf) is a manufacturer and supplier of plasterboard products. It had been in a trading relationship with Plasterboard West Pty Ltd trading as Retroflex Building Supplies (Retroflex) since about May 2012. The terms on which Knauf agreed to supply Retroflex were documented and are set out below but, relevantly, they included the provision of security by Retroflex over its assets to secure its indebtedness to Knauf from time to time.

2 It is common ground that the security interest provided by Retroflex was not registered on the Personal Property Securities Register (PPSR) at the time it was granted. The security interest was only registered several years later at a time proximate to Knauf taking steps to enforce its security by the appointment of receivers and managers. That appointment took place two days before the members of Retroflex purported to resolve to wind up Retroflex and appoint a liquidator to it.

3 Knauf now applies for declarations about the effectiveness of its security interest over Retroflex’s assets. Two issues arise for determination:

first, whether s 588FL of the Corporations Act 2001 (Cth) (Corporations Act) has any application. This issue arises in circumstances where Knauf alleges that a valid resolution for the voluntary winding up of Retroflex was not passed. If s 588FL does not apply then the security interest did not vest in Retroflex and it is valid and enforceable; and

secondly, whether the appointment of the receivers and managers to Retroflex had the effect of perfecting Knauf’s security interest in accordance with s 21 of the Personal Property Securities Act 2009 (Cth) (PPS Act) and, in particular, whether Knauf perfected its security interest by taking possession of the collateral other than by way of seizure or repossession. If it did not perfect its security interest then, pursuant to s 588FL of the Corporations Act or s 267 of the PPS Act, the security interest vested in Retroflex.

knauf’s application

4 In its originating process Knauf seeks the following declarations:

1. A declaration that the General Security Deed between the Applicant and the Respondent dated on or about June, 2014 ("GSD") is a valid and subsisting security interest for the purposes of the Corporations Act 2001 and the Personal Property Securities Act 2009.

2. A declaration that the GSD is a perfected security interest within the meaning of the Personal Property Securities Act 2009.

3. A declaration that the Applicant's security interest has not vested in the Respondent pursuant to section 588FL of the Corporations Act 2001.

4. A declaration that Ian Francis and John Park ("the Receivers") have been validly appointed by a Deed of Appointment executed by the Applicant on 10 February, 2016.

5 Retroflex is named as the respondent to the application. Retroflex and its liquidator, Gary Anderson, appeared on the application and, in effect, alleged that a valid resolution for the voluntary winding up of Retroflex was passed and that Knauf’s security interest has not been perfected.

BACKGROUND

The trading relationship

6 Retroflex was registered on 17 May 2011. Mark Hardy was appointed as a director of Retroflex on 1 September 2011 and, since the resignation of Andre Blignaut as a director on 2 February 2015, has been its sole director.

7 On or about 3 May 2012 Retroflex applied to Knauf for credit by completing an application for credit form. The terms of that application relevantly included:

(1) a retention of title clause; and

(2) a charging clause over land owned by Retroflex.

8 The application for credit form also included a deed of guarantee and indemnity in favour of Knauf by which two directors of Retroflex, Ross McGinn and Mark Hardy, agreed, in consideration of Knauf having agreed to sell goods or provide services to Retroflex, to guarantee all monies payable by Retroflex and to indemnify Knauf against any loss that it incurred as a consequence of Retroflex’s failure to pay any monies due.

9 On or about 4 February 2014 Retroflex entered into a further credit application form with Knauf (Second Credit Application). That form included a retention of title clause for goods supplied by Knauf to Retroflex and a clause granting Knauf a PPS Act security interest in those goods.

10 As part of the Second Credit Application, Messrs McGinn and Hardy entered into a personal guarantee and indemnity agreement in favour of Knauf. Pursuant to the terms of that agreement, in consideration for Knauf supplying Retroflex with goods on credit, they agreed to indemnify Knauf against any losses incurred by it as a result of any default by Retroflex and to guarantee to Knauf all monies due at that time or at any time in the future for goods supplied by it to Retroflex.

11 In or about June 2014 Knauf and Retroflex entered into a deed of acknowledgement, forbearance and repayment (June 2014 Deed). Pursuant to the June 2014 Deed, among other things, Retroflex acknowledged and agreed that it was liable to Knauf for $900,000 (Outstanding Amount), which amount was immediately due and payable, and that:

(1) interest would be payable on the Outstanding Amount;

(2) the Outstanding Amount would be repaid by 24 monthly Minimum Payments of at least $40,500;

(3) to secure the repayment obligation Retroflex would execute the Security Deed, which was defined as “the General Security Deed annexed to [the June 2014 Deed] as Schedule 3”;

(4) the Guarantors, Messrs Hardy, McGinn and Blignaut, would agree to execute the Guarantee, which was defined as “the Guarantee annexed to [the June 2014 Deed] as Schedule 4”, and return it to Knauf; and

(5) Retroflex and the Guarantors would do all things necessary to perfect the Securities, including executing any document necessary to have the Securities registered on the PPSR. The Securities were defined as the Security Deed and the Guarantee.

12 In or about June 2014 Knauf as the secured party and Retroflex as the grantor also entered into the General Security Deed (Security Deed).

13 Clause 3 of the Security Deed is titled “Creation of Security”. It provides at cl 3.1:

3.1 Security

The Grantor:-

(a) grants a PPSA Security Interest over all of the Personal Property; and

(b) charges all of the Other Property,

to the Secured Party as security for the due and punctual payment of all of the Secured Money. The Grantor does this as legal and beneficial owner of the Secured Property.

14 The relevant definitions for the purposes of cl 3.1 are set out in cl 1.1 of the Security Deed. They are:

“PPSA Security Interest” means “a ‘security interest’ as defined in the PPS Act”;

“Secured Property” means “all of the Grantor’s present and future:-

(a) property, undertaking and rights, including all of its real and personal property, cash, uncalled capital, capital which has been called but is unpaid, any choses in action and goodwill; and

(b) PPSA Retention of Title Property”;

“Personal Property” means “all of the Secured Property which is ‘personal property’ as defined in the PPS Act”;

“Other Property” means “the Secured Property, excluding the Personal Property”; and

“Secured Money” means “all present and future debts and monetary liabilities (whether actual or contingent and whether owed jointly or severally or in any other capacity) of the Grantor to the Secured Party (whether alone or not) for any reason including but not limited to the Grantor's liabilities under or in connection with the Relevant Agreement and irrespective of whether those debts or liabilities are:-

(a) owed as principal, interest, fees, charges, taxes, losses, damages, costs or expenses or on any other account;

(b) owed as a result of the assignment to the Secured Party of any debt or monetary liability of the Grantor or any other person, or as a result of any dealing with that debt or monetary liability by any person; or

(c) owed to the Secured Party before the date of this Deed or before the date of any assignment of this Deed to the Secured Party by any person”.

15 Clause 1.1 also provides that “Security” means “each Security Interest and PPSA Security Interest over the Secured Property created under this Deed”.

16 Pursuant to cl 8.1 of the Security Deed, Knauf may appoint any one or more persons to be a receiver or a receiver and manager of all or any part of the Secured Property if the Security has become enforceable or if Retroflex requests Knauf to do so in writing at any time.

17 Clause 9 sets out the powers of a receiver or receiver and manager appointed under the Security Deed. Relevantly, pursuant to cl 9.1(b)(ii), he or she may:

9.1 General

…

(b) A Receiver may:-

…

(ii) access any business premises of the Grantor and take immediate possession of, enter and collect and manage, any Secured Property;

18 Retroflex made payments to Knauf pursuant to the June 2014 Deed until October 2015 in a total amount of $532,777.66. Knauf continued to supply goods to Retroflex until about January 2016.

19 Due to an oversight the security interest created by the Security Deed in the Personal Property was not registered on the PPSR in the period immediately following its execution. On 3 February 2016 Damian Frost, the chief financial officer of Knauf, caused Knauf’s solicitors to register that security interest on the PPSR.

The appointment of receivers and managers to Retroflex

20 Retroflex defaulted under the June 2014 Deed, including by failing to pay the Minimum Payment for November 2015, December 2015 and January 2016.

21 On 10 February 2016 Knauf appointed Ian Francis and John Park of FTI Consulting as receivers and managers of Retroflex (Receivers) pursuant to the Security Deed. On that day Mr Francis, together with Jacquie Sinclair, one of his employees, attended Retroflex’s premises in order to notify the director, Mr Hardy, of his and Mr Park’s appointment as Receivers. They found that the premises were locked and no one was present.

22 On the evening of 10 February 2016 Mr Francis caused a letter to be sent by email to all of the major banks advising of his appointment and requesting that each bank advise him of the existence of any account in the name of Retroflex and freeze any such account. At 5.23 am on 11 February 2016 Selina Naylor of FTI Consulting received an email from the ANZ Bank (ANZ) setting out, among other things, accounts operated by Retroflex with ANZ and their balances.

23 On 10 and 11 February 2016 Mr Francis attempted to contact Mr Hardy on his mobile phone. On each occasion he left a voicemail message to the following effect:

on 10 February 2016:

My name is Ian Francis and I have been appointed receiver by Knauf. Can you please call me as a matter of urgency.

on 11 February 2016:

My name is Ian Francis and we are taking possession of the business. Can you please call so I can discuss our role.

24 Mr Francis also sent Mr Hardy a text message to the above effect. Mr Hardy responded by text message to the effect that he was in a meeting and would call later.

25 Mr Francis and Ms Sinclair returned to Retroflex’s premises on the morning of 11 February 2016 at approximately 7.30 am. Mr Hardy was not in the office. An employee of Retroflex informed Mr Francis that he would call Mr Hardy and shortly thereafter informed Mr Francis that he had spoken to Mr Hardy and that Mr Hardy was unavailable.

26 Mark Norris, an employee of Retroflex, then arrived at Retroflex’s premises and took Mr Francis and Ms Sinclair into an office. Mr Francis says that, to the best of his recollection, he had a conversation with Mr Norris at that time which commenced as follows:

Francis: I have been appointed as receiver and manager. I am here to take control of the business. So it is important that I speak with Mr Hardy as soon as possible. In the meantime, can we have a chat about the Company?

Norris: Ok. What will happen to the entitlements of employees of the Company?

Francis: They will be paid out of the assets of the Company to the extent assets are available for that purpose. What's your role at the Company?

Norris: I have been a consultant here for a year mostly collecting the Company's debts.

Francis: What is the Company’s financial position in respect of debtors and creditors?

27 Mr Norris then provided Mr Francis and Ms Sinclair with information about Retroflex’s debtors, employees, its accountant, recent trading results, computer arrangements and who held keys to Retroflex’s premises.

28 Cheryl-Lynn Hardy, Mr Hardy’s wife, also arrived at Retroflex’s premises. Mr Francis informed her of his and Mr Park’s appointment as Receivers and requested that she provide him with information in relation to Retroflex’s affairs. Mrs Hardy refused to provide the information to Mr Francis.

29 By letter dated 11 February 2016 sent by email the Receivers notified Mr Hardy of their appointment. A copy of the notice of appointment of the Receivers enclosed with that letter was also hand-delivered to Retroflex’s registered office address.

30 On 11 February 2016 at 12.46 pm Ashley Tiplady of Russells, the solicitors for Knauf and, at that time, the Receivers, sent an email to Calvin Ko of Trinix Lawyers, the solicitors for Retroflex, which included:

I understand that employees of the company are actively obstructing the receivers and managers; for example, refusing access to the books and records of the company and by locking themselves in rooms in the company's premises and refusing to deal with the receiver (sic) and managers or permit access to such rooms (and hence the books of the company).

31 On 11 February 2016 at 1.38 pm Mr Tiplady sent another email to Mr Ko in which, among other things, she said:

I look forward to confirmation that your client is willing to provide the requisite assistance to the receivers by return email. Should that not be forthcoming by 2.30 pm (your time), it can only be assumed that your client will continue to obstruct the receivers in the discharge of their obligations and duties.

32 Following the passing of the deadline referred to in Mr Tiplady’s second email sent on 11 February 2016, Mr Francis caused a locksmith to be engaged to attend Retroflex’s premises and change the locks.

33 Also on 11 February 2016 Mr Francis arranged for his firm’s national IT manager, Ritchie Cunningham, to attend Retroflex’s premises to back up Retroflex’s computer server. Mr Cunningham was unable to do so because of a lack of cooperation.

34 On 12 February 2016 at 9.40 am Lavan Legal, who then acted for the Receivers, wrote to Trinix Lawyers in their capacity as solicitors for Mr Hardy. That letter included:

2 We have been provided with correspondence passing between you and Mr Ashley Tiplady of Russells Lawyers, which firm acts on behalf of the secured creditor being our clients' appointor. It is apparent from that correspondence that your client is aware of our clients' appointment and their attempts to engage with him in relation to the conduct of the receivership.

3 By reason of our clients' appointment, Mr Hardy is no longer in control of the Company and his powers as a director of the Company are suspended without express written authorisation from our clients. No authorisation has been sought not (sic) provided and, for the avoidance of doubt, our clients do not grant any such authorisation to Mr Hardy or indeed, any other officers of the Company.

4 Please confirm that your client will co-operate with our clients by allowing them to access the Company's books, records and property by 10am this morning so that our clients may undertake such tasks as are required of our clients to discharge their duties, and exercise their powers, conferred by their appointment.

…

(original emphasis)

35 Also on 12 February 2016 Mr Francis instructed Ms Sinclair to attend Retroflex’s premises to unlock the doors, which she did. Ms Sinclair met with Mr Norris, who told her that Mr Hardy had instructed him to co-operate with FTI Consulting and who took her around the premises while Ms Sinclair took photographs.

36 Shortly after midday Mr Francis had a telephone conversation with Ms Sinclair during which she informed Mr Francis that, among other things, she had been requested to leave the premises by Mr Hardy and that Mr Hardy had informed her that a liquidator had been appointed to Retroflex. The liquidator changed the locks at Retroflex’s premises in the afternoon of 12 February 2016.

37 On 12 February 2016 at 2.29 pm Lavan Legal sent a further letter to Trinix Lawyers and the liquidator which included:

…

2 Our clients' representative, Ms Sinclair, attended the Company's premises this morning from 6.30am. Ms Sinclair was denied access to the Company's books, records and property by Mr Hardy, seemingly on the basis that he had appointed a liquidator to the Company at 9.30am today.

3. We understand that liquidator to be Mr Gary Anderson. Please provide us with the documents by which Mr Anderson was purportedly appointed. Even if that appointment is valid (which is neither accepted nor rejected), please explain the basis for Mr Hardy's refusal to allow Ms Sinclair (as a representative of the receivers and managers) access to the premises.

…

5 Our clients have serious concerns about Mr Hardy's conduct including his refusal to permit our clients to secure the Company's books, records and property. Please provide confirmation that Mr Hardy will preserve and maintain the books, records and property of the Company and that he will immediately desist from conducting any business of the Company.

6 For the avoidance of doubt, Ms Sinclair left the Company's premises on the basis that:

6.1 her right to be present at the premises was disputed at or obstructed;

6.2 Mr Hardy, and/or you on his behalf, have conveyed the suggestion that there is some doubt as to the basis of our clients' appointment That position has not been articulated in any correspondence; and

6.3 Mr Hardy's continued assertion that Ms Sinclair was not permitted to be at the premises be (sic) reason of the liquidator's appointment.

7 These matters were communicated by Ms Sinclair to Mr Hardy at the time of her departure.

8 Our clients do not accept the veracity of any of the matters in paragraphs 6.1-6.3 but, for the sake of preserving the status quo, and until any concerns as to their appointment are resolved, will not take any active steps in the receivership.

9 As you know, our clients have certain rights and duties which they must discharge once appointed. Mr Hardy is preventing that from occurring.

10 We therefore seek Mr Hardy's immediate undertaking that:

10.1 He will immediately cease conducting any business or any activity at the Company's premises.

10.2 He will permit the receivers and managers to secure the books, records and property of the Company until any concerns as to their appointment is resolved.

10.3 Alternatively to paragraph 10.2, he will permit Mr Anderson to secure the books, records and property of the Company until any concerns as to our clients' appointment is resolved.

…

The appointment of a liquidator to Retroflex

38 On or about 29 January 2016 Mr Hardy arranged to meet with Gary Anderson of HLB Mann Judd. He thereafter met with Mr Anderson on three occasions in early February 2016. By 12 February 2016 Mr Hardy had decided to put Retroflex into liquidation. By that time Mr Hardy’s negotiations with an interested party, the Watson Group, in relation to its potential acquisition of a part of Retroflex’s business had come to an end.

39 On 12 February 2016 Mr Hardy signed a Form 529 – Notice of Extraordinary Meeting of Members of Retroflex, which gave notice of an extraordinary general meeting to be held on 12 February 2016 at 10.15 am and which provided:

Agenda:

1. Special Resolution

"That the Company be wound up voluntarily".

Should the above be passed as a special resolution, ordinary resolutions will be submitted as follows:

2. Ordinary Resolution

"That Gary John Anderson be appointed liquidator for the purpose of winding up the affairs and distributing the assets of the Company";

Proxies to be used at the meeting must be lodged with the Chairman 24 hours before the meeting.

40 A document titled “Members Consent for Short Notice” also dated 12 February 2016 and signed on behalf of MAC Investments (WA) Pty Ltd (MAC Investments) and Mr Blignaut provided:

We, the undersigned, being a majority of members who together hold not less than 95 percent in nominal value of the shares of the above named Company, having the total voting rights and having the right to attend and vote at a meeting to be held at 661 Newcastle Street, Leederville WA on 12 February 2016 at 10:15 am, which a special resolution as detailed below may be proposed, hereby waive the right to receive 21-days' notice of that meeting pursuant to Section 249H(2)(b).

Proposed special resolution:

"That the Company be wound up voluntarily"

41 The minutes of an extraordinary meeting of members of Retroflex that took place on 12 February 2016 (February Meeting of Members) and was chaired by Mr Blignaut record that the members of Retroflex resolved by special resolution that Retroflex be wound up voluntarily and resolved to appoint Mr Anderson as liquidator for the purpose of winding up the affairs and distributing the assets of Retroflex. A list of persons present at the meeting records that present were MAC Investments, represented by its sole director, Mrs Hardy, and Mr Blignaut. Mr Hardy deposes that he also attended the meeting. The meeting commenced at 10.15 am and closed at 10.17 am.

42 According to a current and historical search of the Australian Securities and Investments Commission (ASIC) database carried out on 23 February 2016 (Retroflex Search), as at that date, Retroflex had 85 shares on issue, of which MAC Investments held 35 shares, Mr Blignaut held 20 shares and Sevenoaks Investment Pty Ltd (Sevenoaks) held 30 shares.

43 Mr Hardy said that Sevenoaks was not given formal written notice of the February Meeting of Members because he believed that it was no longer a shareholder of Retroflex. But because he still had a close working relationship with Mr Norris, who had been the sole director and secretary of Sevenoaks, Mr Hardy told Mr Norris about the meeting and that a liquidator was going to be appointed to Retroflex.

Sevenoaks and the share buy-back

44 Mr Norris was the former managing director and CEO of Knauf. He held the position of managing director of Knauf at the time it entered into the June 2014 Deed with Retroflex. Mr Norris commenced working with Retroflex in February 2015. He reported to Retroflex’s managing director, Mr Hardy, and to its finance manager, Mr Blignaut.

45 Mr Norris gave evidence that he is the sole director of Sevenoaks. However, that evidence is contrary to a search of the current and historical records maintained by ASIC of Sevenoaks carried out on 8 March 2017. That search shows that:

Sevenoaks was registered on 28 January 2015;

Mr Norris’ wife, Helen Norris, is the sole shareholder of Sevenoaks, holding 300 ordinary shares;

Mr Norris was Sevenoaks’ sole director and secretary from its registration date until 30 June 2015; and

on 30 June 2015 Mrs Norris became the sole director and secretary of Sevenoaks.

46 In cross-examination Mr Norris said that he thought he was the sole director of Sevenoaks after 30 June 2015, but conceded that he had signed the documentation for Mrs Norris to become the sole director and secretary.

47 According to Mr Norris, on or about 31 August 2015 he had a conversation with Mr Hardy to the following effect:

Mr Hardy: I’m worried that as Ross has killed himself that some Retroflex shares are sitting in escrow and the shares are not taken up and I’m thinking about options to try and restructure the business. I have just been diagnosed with a serious condition that I need to address. Can you caretake the shares as I’m concerned about my health and that the shares are still in escrow. I can offer you a credit line for the Shares to be sold to Sevenoaks.

Mr Norris: Ok I’ll agree for Sevenoaks to purchase the shares on a credit line.

Mr Hardy: I will arrange for the shares to be transferred to Sevenoaks.

48 Mr Norris’ evidence is that Sevenoaks acquired 30 shares in Retroflex on or about 31 August 2015 at a price of $3,400 per share for a total purchase price of $102,000. He said that at that time he agreed with Mr Hardy that Retroflex would extend a credit line to Sevenoaks to pay for the shares. Mr Norris believes that that arrangement was recorded in the books and records of Retroflex as a loan.

49 According to an ASIC Form 484 – Change to company details dated 31 October 2015, on 31 August 2015 Highlight Investments Pty Ltd (Highlight) decreased its shareholding in Retroflex by 30 shares so that it no longer held any shares and Sevenoaks became a shareholder in Retroflex, increasing its shareholding from nil to 30 shares with a total paid of $30. In cross-examination Mr Norris agreed that:

(1) the Form 484 recorded a transfer of shares in Retroflex from Highlight to Sevenoaks and that Highlight was selling its shares to Sevenoaks;

(2) his evidence recorded in his affidavit that on or about 31 August 2015 Sevenoaks purchased 30 shares in Retroflex at a price of $3,400 per share was not correct and that in August 2015 Sevenoaks purchased 30 shares in Retroflex for $30; and

(3) Highlight had acquired 30 shares in Retroflex on 28 April 2015 for $120,000, as recorded in an ASIC Form 484 – Change to company details dated 16 June 2015 and certified by Mr Hardy. Mr Norris said that when Highlight acquired those shares it did not pay $120,000 to Retroflex but that the acquisition was funded by Retroflex providing a loan to Highlight.

50 According to Mr Norris, he had a conversation with Mr Hardy in or about the first week of January 2016 to the following effect:

Mr Hardy: I have been talking to a number of potential investors and believe the Watson group is the best option for the business moving forward however the Watson group want an equal share or a controlling share of the Retroflex business.

Mr Norris: I don’t really have any interest in continuing with the business and have been looking at new opportunities overseas. My family and I are considering returning overseas to work. I’m happy to sell the shares for book value provided Sevenoaks’ line of credit is cleared.

Mr Hardy: Ok. I can have David Carson prepare the required documents and I will record the transaction in the accounts of the business.

Mr Norris: Ok.

51 Mr Hardy also gave evidence of a conversation that he had with Mr Norris in or about the first week of January 2016, which he said was to the following effect:

Mr Hardy: As you know I’ve been having informal conversations with a couple of investors to come into the business. I feel that the Watson group is the best option for the business moving forward as it gives both me and them access to each other’s specified products, Retroflex can reduce its logistic costs for country customers and gives Retroflex access to the Watson database of a non-active customers for Retroflex to pursue. The Watson group have told me they would want an equal share or even a controlling share of the Retroflex business.

Mr Norris: I have some industry related interviews overseas and me and my family are weighing up our options to return to work overseas. I’m happy to return the shares for the book value of $102,000.00 if you clear Sevenoak’s (sic) line of credit so I can explore further opportunities for me and my family.

Mr Hardy: Ok. I will inform Watsons. I will also record the transaction in the accounts.

Mr Norris: Ok.

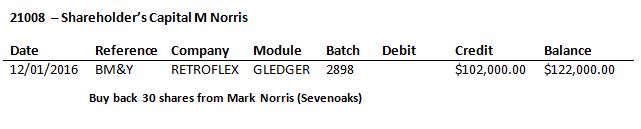

52 Mr Hardy’s evidence is that on 12 January 2016 he caused the proposed transaction to be recorded in the books and records of Retroflex. An extract from the general ledger report for Retroflex dated 10 February 2016 shows two entries made on 12 January 2016 as follows:

53 As of 12 January 2016 Mr Norris believed that Sevenoaks was no longer a shareholder of Retroflex. Accordingly, after that date he did not attend any meetings of Retroflex on behalf of Sevenoaks. Mr Norris’ evidence is that on or about 29 January 2016 Mr Hardy said words to him to the effect that he had arranged a meeting with Mr Anderson with a view to putting Retroflex into liquidation. Mr Norris said that he did not object to the proposed course of action by Mr Hardy and, because he believed that Sevenoaks was not a shareholder of Retroflex, that he did not attend the meeting.

54 As of 12 January 2016 Mr Hardy no longer considered Sevenoaks to be a shareholder of Retroflex. Mr Hardy said that following the share buy-back, in late January or early February 2016, he attended the offices of BM&Y, Retroflex’s accountant. Mr Hardy accepted in cross-examination that he met with David Carson of BM&Y on 29 January 2016. According to Mr Hardy, either at that meeting or on the telephone he had a conversation with Mr Carson to the following effect:

Mr Hardy: Mark Norris has sold his shares back to the company so that Watsons can buy in and in exchange I have cleared Sevenoak’s (sic) line of credit in the company’s ledgers.

Mr Carson: There are certain forms and timelines that need to be followed when a company buys back shares.

Mr Hardy: Prepare whatever forms are needed and I will sign them.

55 Mr Hardy said that he was then given ASIC Forms 280 and 281 by Mr Carson, already completed, which he signed in his capacity as director of Retroflex. Those forms are both signed by Mr Hardy and dated 3 February 2016. Mr Hardy said that he:

(1) was not aware at the time that those forms recorded the proposed date for the buy-back of the shares from Sevenoaks as 24 February 2016. He believed that this was incorrect as the buy-back was entered into on 12 January 2016 when he had his discussion with Mr Norris; and

(2) could not recall if he received the forms on 3 February 2016 and that he would have signed them and moved on.

56 A notice of a meeting of members of Retroflex signed by Mr Hardy and dated 12 January 2016 gives notice of a general meeting of Retroflex to be held on 3 February 2016 at 10.00 am at BM&Y, 47 Ord Street, West Perth. The purpose of the meeting was to consider the following resolution:

It was resolved to approve the following buy back:

SEVENOAKS INVESTMENT PTY LTD

ACN 603 912 223

No of Shares 30

ORDINARY FULLY PAID

Amount per Share $3,400.00

57 Mr Hardy cannot recall when he signed the notice of meeting. However, given that Mr Hardy accepted that he met with Mr Carson on 29 January 2016; that at that time, or during a telephone conversation at about that time, he informed Mr Carson of the acquisition of Sevenoaks’ shares; and that Mr Carson in turn informed Mr Hardy about the need to observe certain timelines and complete particular forms when effecting a share buy-back, it cannot be the case that Mr Hardy in fact signed the notice of meeting on 12 January 2016. He must have signed it between 29 January 2016 and 3 February 2016.

58 On 3 February 2016 at 10.00 am Mr Hardy attended a shareholders’ meeting of Retroflex at the offices of BM&Y with Mr Norris, Mr Blignaut and Mrs Hardy for MAC Investments. A memorandum of resolutions of the members of Retroflex signed by or on behalf of all the members of Retroflex, being Mr Blignaut, MAC Investments and Sevenoaks, records that it was resolved to approve a buy-back of 30 ordinary fully paid shares at $3,400 per share from Sevenoaks. Mr Hardy also signed a memorandum of resolutions of the sole director of Retroflex which was in the following terms:

Buy Back of Shares: It was resolved to approve the following buy back or reduction of shares:

SEVENOAKS INVESTMENT PTY LTD

ACN: 603 912 223

No of Shares: 30

ORDINARY FULLY PAID

Amount per Share: $3,400.00

59 An ASIC Form 484 – Change to company details for Retroflex certified by Mr Hardy on 24 February 2016 records the following:

(1) under the heading “C1 Cancellation of shares”, that 30 ordinary shares were cancelled with an amount paid of $102,000 and with the earliest date of cancellation recorded as 24 February 2016. The reason for the cancellation was recorded as “ss.257H(3) Share buyback – Other buy-back type”;

(2) under the heading “C3 Change to share structure”, that the updated details for the changed class of ordinary shares were 55 shares with a total amount paid on those shares of $77,682.65; and

(3) under the heading “C4 Changes to the register of members”, that Sevenoaks’ ordinary shares had decreased by 30 with a total paid of $0 and with the earliest date of change recorded as 24 February 2016.

60 The register of members for Retroflex at 24 February 2016 records that:

Mr Blignaut held 20 shares;

MAC Investments held 35 shares; and

a buy-back of 30 shares from Sevenoaks on 24 February 2016 reduced its shareholding to zero with an amount paid per share of $1,412.41.

61 Mr Hardy said that he did not arrange for the register of members to be amended to record the share buy-back from Sevenoaks, but that it was amended by BM&Y. He said that he thought that the buy-back occurred much earlier than 24 February 2016. However, a Form 509 – Presentation of summary of affairs of a company made up to 12 February 2016 and signed by Mr Hardy on 16 February 2016 includes a valuation of share capital, issued and paid up, at $120,055. Mr Hardy acknowledged that he had signed the Form 509 and that prior to doing so he would have gone through the numbers included in it to check that they were correct.

does Section 588FL of the corporations apply?

62 Section 588FL applies, relevantly, when an order is made or a resolution is passed for the winding up of a company and a PPS Act security interest granted by the company in collateral is covered by s 588FL(2). The balance of the section relevantly provides:

588FL Vesting of PPSA security interests if collateral not registered within time

…

(2) This subsection covers a PPSA security interest if:

(a) at the critical time, or, if the security interest arises after the critical time, when the security interest arises:

(i) the security interest is enforceable against third parties under the law of Australia; and

(ii) the security interest is perfected by registration, and by no other means; and

(b) the registration time for the collateral is after the latest of the following times:

(i) 6 months before the critical time;

(ii) the time that is the end of 20 business days after the security agreement that gave rise to the security interest came into force, or the time that is the critical time, whichever time is earlier;

(iii) if the security agreement giving rise to the security interest came into force under the law of a foreign jurisdiction, but the security interest first became enforceable against third parties under the law of Australia after the time that is 6 months before the critical time—the time that is the end of 56 days after the security interest became so enforceable, or the time that is the critical time, whichever time is earlier;

(iv) a later time ordered by the Court under section 588FM.

Vesting of security interest in company

(4) The PPSA security interest vests in the company at the following time, unless the security interest is unaffected by this section because of section 588FN:

(a) if the security interest first becomes enforceable against third parties at or before the critical time—immediately before the event mentioned in paragraph (1)(a);

(b) if the security interest first becomes enforceable against third parties after the critical time—at the time it first becomes so enforceable.

…

(7) In this section:

critical time, in relation to a company, means:

(a) if the company is being wound up—when, on a day, the event occurs by virtue of which the winding up is taken to have begun or commenced on that day under section 513A or 513B; or

(b) in any other case—when, on a day, the event occurs by virtue of which the day is the section 513C day for the company.

63 The resolution passed for the winding up of the company must be valid in order for the winding up to be effective. If it is not then the circumstances in which s 588FL is engaged will not arise.

64 Retroflex was wound up voluntarily. Section 491 of the Corporations Act provides that a company may be wound up voluntarily if it so resolves by special resolution. Section 9 of the Corporations Act defines “special resolution” to mean, relevantly:

(a) in relation to a company, a resolution:

(i) of which notice as set out in paragraph 249L(1)(c) has been given; and

(ii) that has been passed by at least 75% of the votes cast by members entitled to vote on the resolution; or

…

65 Part 2G.2 of the Corporations Act concerns meetings of members of companies. Division 3 of Pt 2G.2 is titled “How to call meetings of members”. Relevantly:

(1) s 249H(1) provides that, subject to s 249H(2), at least 21 days’ notice must be given of a meeting of a company’s members;

(2) s 249H(2)(b) provides that a company may call a general meeting other than an AGM on shorter notice if members with at least 95% of the votes that may be cast at the meeting agree beforehand;

(3) s 249J(1) provides that written notice of a meeting of a company’s members must be given individually to each member entitled to vote at the meeting and to each director;

(4) ss 249J(3) and (3A) set out the ways in which a company may give the notice of meeting to a member; and

(5) s 249L(1) sets out the contents of a notice of meeting. In particular, para (c) requires that if a special resolution is to be proposed at the meeting then the notice must set out an intention to propose the special resolution and state the resolution.

66 Knauf submitted that a special resolution had not been passed because the first requirement of the definition in s 9 had not been met. This was said to be so because, as at the date of the February Meeting of Members, 12 February 2016, there were three shareholders of Retroflex and no notice of the meeting was given to one of those shareholders, Sevenoaks. Having received no notice of the meeting whatsoever, Sevenoaks could not have received notice of the special resolution as set out in s 249L(1)(c).

67 I accept that submission. As is clear from the Retroflex Search and the register of members dated 24 February 2016, as at 12 February 2016, Sevenoaks was a member of Retroflex. Clause 13.3 of the Constitution of Retroflex provides that a transferor of shares remains the holder of shares transferred until the transfer is registered and the name of the transferee is entered in the register. Sevenoaks’ name remained in the register until 24 February 2016, when its name was removed.

68 On Mr Hardy’s own evidence, notice of the meeting was not given to Sevenoaks. As a result, Retroflex failed to comply with the requirement to put Sevenoaks on notice of the proposed special resolution as required by s 249L(1)(c): see Re Soul Outlet Pty Ltd (in liq); ex parte Jack James as liquidator of Soul Outlet Pty Ltd (in liq) [2015] WASC 307 (Re Soul Outlet) at [64] (per Pritchard J).

69 In addition:

(1) the members’ consent for shorter notice did not comply with s 249H(2)(b) of the Corporations Act. As at 12 February 2016 there were 85 shares on issue. Those members who agreed to shorter notice held a total of 55 shares, being approximately 64% of those shares, which was significantly less than the required 95%. It follows that the abridgement of the notice period for the meeting was not valid; and

(2) written notice of the meeting was not given to each member entitled to vote at the meeting individually as required by s 249J(1).

70 Despite the resolution to wind up Retroflex having been “passed by at least 75% of the votes cast by members entitled to vote on the resolution” (that is, by at least 75% of the votes actually cast: see Re Soul Outlet at [58]-[62]), there was a failure to comply with the first requirement for a special resolution in s 9 of the Corporations Act and with the notice requirements for a meeting of the company’s members. Thus the special resolution to voluntarily wind up Retroflex was not validly passed at the February Meeting of Members.

71 Retroflex relies on the conversation which took place between Messrs Hardy and Norris in the first week of January 2016 to contend that, by reason of that conversation, there was an agreement with Sevenoaks that it would sell its shares back to Retroflex on certain agreed terms and conditions. However, even accepting that the conversation occurred, there are a number of issues that arise. Those issues inevitably lead to the conclusion that no binding contract was created by reason of that conversation and that there was no effective share buy-back as at 12 January 2016, as at 3 February 2016 or as at the date of the February Meeting of Members, 12 February 2016.

72 Before explaining why that is the inevitable conclusion, it is necessary to set out the provisions of the Corporations Act governing a company’s ability to buy back its own shares. Chapter 2J of the Corporations Act is concerned with transactions affecting share capital. Part 2J.1 deals with share capital reductions and share buy-backs. Section 256A sets out the purpose of Pt 2J.1 as providing the rules to be followed by a company for reductions in share capital and share buy-backs. It states that the rules are designed to protect the interests of shareholders and creditors by addressing the risk of those transactions leading to the company’s insolvency; seeking to ensure fairness between the company’s shareholders; and requiring the company to disclose all material information.

73 Division 1 of Pt 2J.1 deals with reductions in share capital not otherwise authorised by law and Div 2 deals with share buy-backs. Section 257A provides that a company may buy back its own shares if:

(1) the buy-back does not materially prejudice the company’s ability to pay its creditors; and

(2) the company follows the procedures laid down in Div 2.

74 Section 257B sets out the steps to be followed for, and the sections that apply to, the five different types of buy-back. One of those types of buy-back is a “selective buy-back”. Section 9 defines a “selective buy-back” as a buy-back that is none of the following:

(a) a buy-back under an equal access scheme within the meaning of ss 257B(2) and (3);

(b) a minimum holding buy-back;

(c) an on-market buy-back; and

(d) an employee share scheme buy-back.

75 The buy-back of Sevenoaks’ shares was a selective buy-back. According to s 257B(1), the sections that apply to selective buy-backs are ss 257D, 257E, 257F, 257G, 257H and 254Y. Those sections relevantly provide that:

(1) the terms of the buy-back agreement must be approved before it is entered into either by a special resolution passed at a general meeting of the company, with no votes being cast in favour of the resolution by any person whose shares are proposed to be bought back, or by a resolution agreed to at a general meeting by all ordinary shareholders; or the agreement must be conditional on such an approval: s 257D(1);

(2) the company must include with the notice of the meeting a statement setting out all information known to the company that is material to the decision as to how to vote on the resolution: s 257D(2);

(3) before the notice of meeting is sent to shareholders the company must lodge with ASIC a copy of the notice of the meeting and any document relating to the buy-back that will accompany the notice of the meeting sent to shareholders: s 257D(3). The documents must be lodged at least 14 days prior to the resolution being passed: s 257F(1); and

(4) the company must lodge with ASIC before the buy-back agreement is entered into a copy of a document setting out the terms of the offer and any document that is to accompany the offer: s 257E.

76 I return then to the alleged agreement relied on by Retroflex, said to be constituted by the conversation between Messrs Hardy and Norris that took place in the first week of January 2016. For the following reasons that conversation did not constitute a binding agreement to buy back Sevenoaks’ shares

77 First, at the time of the conversation, Mr Norris was not a shareholder or director of Sevenoaks. He had no authority to bind Sevenoaks. Secondly, on Mr Norris’ own version of the conversation, Mr Hardy acknowledged that he would have Mr Carson “prepare the required documents” to give effect to the share buy-back. Thirdly, Mr Hardy had no authority to enter into such an agreement on behalf of Retroflex. To bind Retroflex the agreement required shareholder approval pursuant to s 257D of the Corporations Act. That had not occurred as at the time of the conversation.

78 Further support for the conclusion that there was no binding agreement can be gleaned from the objective evidence relating to the purported buy-back as follows:

(1) Mr Hardy first informed Mr Carson of the intention to buy back Sevenoaks’ shares on 29 January 2016. According to Mr Hardy’s own evidence he informed Mr Carson either at a meeting or during a telephone conversation at about that time that Mr Norris had sold his shares back to the company. Mr Hardy’s evidence is that during that conversation Mr Carson informed him that there were certain “forms and timelines” that needed to be followed when a company buys back its shares;

(2) a notice of general meeting signed by Mr Hardy and dated 12 January 2016 gave notice of a meeting of the members of Retroflex to be held on 3 February 2016 to approve a buy-back of Sevenoaks’ shares. Given the date on which Mr Hardy says he informed Mr Carson about the proposed buy-back and the other surrounding evidence, it cannot be the case that the notice was in fact signed on 12 January 2016;

(3) at the general meeting of Retroflex which took place on 3 February 2016 the buy-back of Sevenoaks’ shares was approved;

(4) Mr Hardy signed a memorandum of resolutions of the sole director of Retroflex that reflected the resolution to approve the buy-back of those shares which was also dated 3 February 2016;

(5) the ASIC Form 280 – Notification of share buy-back details signed by Mr Hardy and dated 3 February 2016 specifies a selective buy-back with the relevant date, that is, the date of the passing of a resolution, as 3 February 2016;

(6) the ASIC Form 281 – Notice of intention to carry out a share buy-back signed by Mr Hardy and dated 3 February 2016 specifies a selective buy-back with the “Proposed date for buy back agreement to be entered into” as 24 February 2016 and the “Proposed date for passing the resolution to approve the buy back” as 3 February 2016;

(7) the ASIC Form 484 – Change to company details signed by Mr Hardy on 24 February 2016 shows that the earliest date of the cancellation of Sevenoaks’ 30 shares in Retroflex pursuant to a share buy-back was 24 February 2016; that the earliest date of the change to share structure, such that there were only 55 ordinary shares in Retroflex, was 24 February 2016; and that the earliest date of the change to the register of members, decreasing Sevenoaks’ shareholding to zero, was 24 February 2016; and

(8) the register of members for Retroflex as at 24 February 2016 shows that on that date, pursuant to a buy-back, Sevenoaks ceased to hold its 30 ordinary shares in Retroflex.

79 Knauf also submitted that even if there was a contract it was void and ultra vires, but given the conclusion I have reached on the existence of the contract I do not need to address that submission.

80 Knauf further submitted that the buy-back was not effective. It contended that a company may only buy back its shares in the circumstances set out in s 257A of the Corporations Act. The first condition set out in s 257A places an onus on the company to ensure that the buy-back does not materially prejudice its ability to pay its creditors.

81 In Re Molopo Energy Ltd (2014) 294 FLR 13; [2014] NSWSC 1864 White J considered similar provisions concerning capital reductions. At [87]-[89] his Honour endorsed a submission to the effect that if a company were in a position where it “appeared that a reduction might materially prejudice its ability to pay its creditors, that is, if it could not affirmatively say that the reduction did not have that effect, then the reduction was prohibited” (original emphasis). His Honour held that the current regime was one where “the onus is on the company to ensure that the reduction does not prejudice its ability to pay creditors”.

82 In Re CSR Ltd (2010) 183 FCR 358 a Full Court of this Court (Keane CJ, Finkelstein and Jacobson JJ) considered the meaning of “material prejudice” in the context of s 256B of the Corporations Act, concerning reductions in capital. Keane CJ and Jacobson J, with whom Finkelstein J relevantly agreed, said at [45]:

In relation to the question of “material prejudice” to a company’s ability to pay its creditors, the text of the Act and the explanatory memorandum which accompanied the Bill which introduced s 256B into the Act are not particularly helpful. In cl 12.23 it said: “Whether prejudice is ‘material’ will be a question of judgment to be determined in light of all relevant circumstances”. One is, we think, on safe ground, however, in treating “material prejudice” to a company’s ability to pay its creditors as relating to the creation of a material as opposed to theoretical increase, in the likelihood that the reduction in capital will result in a reduced ability to pay creditors.

83 It is clear that as at January 2016 Retroflex was facing financial difficulties. Mr Hardy was having discussions with Watsons but those discussions did not eventuate into anything and, according to Mr Hardy, came to an end when Knauf appointed the Receivers. Retroflex had defaulted in its payment obligations to Knauf. By 29 January 2016 Mr Hardy had arranged to meet with Mr Anderson with a view to putting Retroflex into liquidation. In his declaration of independence, relevant relationships and indemnities for Retroflex dated 15 February 2016 Mr Anderson states that a Mr Thomason first contacted him on 29 January 2016 to arrange a meeting with his client, Mr Hardy. Mr Anderson met with Mr Hardy on 4, 11 and 12 February 2016. Mr Anderson states that the purpose of the meetings on 4 and 11 February 2016 “was to discuss the financial position and options available to [Retroflex] considering its financial position”. In addition, the Form 509 – Presentation of summary of affairs of a company, which provides a summary of assets and liabilities of Retroflex as at 12 February 2016 and which was signed by Mr Hardy on 16 February 2016, shows a deficiency of assets over liabilities of $264,124.

84 In those circumstances the forgiveness by Retroflex of a debt of $102,000 due to it from Sevenoaks would likely affect Retroflex’s ability to pay its creditors. In the absence of Retroflex proving the contrary, that is, that the buy-back did not have that effect, the buy-back would be contrary to, and thus prohibited by, s 257A. Retroflex has not discharged its onus of proof in this regard.

85 Further and in any event, Retroflex did not follow the procedures set out in the Corporations Act to affect the buy-back. The Forms 280 and 281 referred to above at [78(5)] and [78(6)] were not lodged with ASIC 14 days prior to the February Meeting of Members as required by s 257F(1). Those forms were lodged after the February Meeting of Members. As submitted by Knauf, the Form 280 nominated 3 February 2016 as the “relevant date”, from which it follows that any buy-back agreement must have been conditional on shareholder approval and could not have been entered into on 12 January 2016.

86 Retroflex seeks to rely on s 259F of the Corporations Act to remedy any default on its part in complying with the procedures relating to share buy-backs set out in Div 2 of Pt 2J.1. Section 259F provides:

Consequences of failing to comply with section 259A or 259B

(1) If a company contravenes section 259A or subsection 259B(1):

(a) the contravention does not affect the validity of the acquisition or security or of any contract or transaction connected with it; and

(b) the company is not guilty of an offence.

(2) Any person who is involved in a company’s contravention of section 259A or subsection 259B(1) contravenes this subsection.

(3) A person commits an offence if they are involved in a company’s contravention of section 259A of section 259B(1) and the involvement is dishonest.

87 Section 259A relevantly provides:

Directly acquiring own shares

A company must not acquire shares (or units of shares) in itself except:

(a) in buying back shares under section 257A; or

…

88 Retroflex submitted that, by reason of s 259F of the Corporations Act, the transaction pursuant to which Sevenoaks’ shares were sold back to it is not invalidated if it has not complied with the buy-back provisions. It further submitted that on or about 12 January 2016, or at the latest 3 February 2016, Sevenoaks ceased to be a shareholder of Retroflex.

89 Knauf contended that s 259F is of no assistance to Retroflex. That was said to be so for two reasons: first, Retroflex has failed to establish that the buy-back does not materially prejudice its ability to pay its creditors as required by s 257A(a). Thus, the power in s 257A was never enlivened. Secondly, for the reasons set out at [77] above, there was no acquisition or contract connected with any buy-back.

90 I accept Knauf’s contention that s 259F cannot assist Retroflex, but only for the second of the two reasons advanced by it. A buy-back is not authorised by the Corporations Act if either of the conditions in s 257A, namely, that the buy-back does not materially prejudice the company’s ability to pay its creditors and that the company follows the procedures contained in Div 2 of Pt 2J.1, is not met. If a buy-back is not authorised under s 257A, or covered by the other exceptions in s 259A that are not presently relevant, then it will contravene s 259A. A contravention of s 259A will not affect the validity of the acquisition or of the contract or transaction connected with it, nor will the company be guilty of an offence for that contravention: s 259F(1). But a person involved in the company’s contravention of s 259A will contravene s 259(2), which is a civil penalty provision.

91 The effect of s 259F(1) is that an acquisition of shares made contrary to s 259A, including a buy-back not authorised by s 257A, is valid despite the contravention. Accordingly, s 259F(1) would have preserved the validity of the buy-back of Sevenoaks’ shares notwithstanding that it materially prejudiced the ability of the company to pay its creditors and thus did not comply with s 257A(a). The persons involved in the contravention of s 259A may then have been liable for the consequences of contravening s 259F(2). However, nothing in the terms of s 259F(1) suggests that that subsection is able to cure defects in the contract or transaction underlying the acquisition, nor that it is able to overcome the absence of such a contract or transaction. Section 259F(1) cannot remedy the fact that the conversation between Messrs Hardy and Norris in early January 2016 did not constitute a binding agreement to buy-back Sevenoaks’ shares.

92 It follows from the matters set out above that:

(1) there was no agreement to buy back Sevenoaks’ shares in Retroflex as at 12 January 2016 or 3 February 2016;

(2) if there was an effective agreement of the buy-back of Sevenoaks’ shares then that agreement was only effective on and from 24 February 2016;

(3) s 259F of the Corporations Act cannot assist Retroflex in remedying the absence of an effective agreement for a share buy-back prior to 24 February 2016; and

(4) a valid resolution to wind up Retroflex was not passed at the February Meeting of Members.

93 As a result, s 588FL does not apply and the security interest did not vest in Retroflex immediately before the passing of the purported resolution to wind up Retroflex.

Did the appointment of the receivers perfect KNauf’s security interest?

94 Given the conclusion I have reached in relation to the operation of s 588FL it is not necessary for me to consider the second issue but, given the detailed argument by the parties in relation to it and for completeness, I do so below. The analysis that follows assumes that the resolution passed at the February Meeting of Members was effective.

95 The issue for determination is whether the appointment of the Receivers had the legal effect of perfecting Knauf’s security interest in the Personal Property under the Security Deed in accordance with s 21 of the PPS Act. That in turn raises the issue of whether Knauf perfected its security interest by possession, other than by way of seizure or repossession, such that the security interest did not vest in Retroflex under s 267 of the PPS Act or s 588FL of the Corporations Act.

Statutory regime

96 Section 21 of the PPS Act concerns perfection of a security interest. It relevantly provides:

21 Perfection—main rule

(1) A security interest in particular collateral is perfected if:

(a) the security interest is temporarily perfected, or otherwise perfected, by force of this Act; or

(b) all of the following apply:

(i) the security interest is attached to the collateral;

(ii) the security interest is enforceable against a third party;

(iii) subsection (2) applies.

(2) This subsection applies if:

(a) for any collateral, a registration is effective with respect to the collateral; or

(b) for any collateral, the secured party has possession of the collateral (other than possession as a result of seizure or repossession); or

…

97 Section 10 of the PPS Act relevantly defines “collateral” to mean “personal property to which a security interest is attached” and “personal property” to mean “property (including a licence) other than … land; [among other things]”.

98 Section 19 of the PPS Act deals with attachment. It provides that a security interest is enforceable against a grantor in respect of particular collateral only if the security interest has attached to the collateral: subs 19(1). The attachment rule, which provides for when security attaches to collateral, is set out in subs 19(2). That subsection provides:

19 Enforceability of security interests against grantors—attachment

…

Attachment rule

(2) A security interest attaches to collateral when:

(a) the grantor has rights in the collateral, or the power to transfer rights in the collateral to the secured party; and

(b) either:

(i) value is given for the security interest; or

(ii) the grantor does an act by which the security interest arises.

99 Section 20 of the PPS Act deals with enforceability of security interests against third parties. It relevantly provides:

20 Enforceability of security interests against third parties

General rule

(1) A security interest is enforceable against a third party in respect of particular collateral only if:

(a) the security interest is attached to the collateral; and

(b) one of the following applies:

(i) the secured party possesses the collateral;

(ii) the secured party has perfected the security interest by control;

(iii) a security agreement that provides for the security interest covers the collateral in accordance with subsection (2).

Written security agreements

(2) A security agreement covers collateral in accordance with this subsection if:

(a) the security agreement is evidenced by writing that is:

(i) signed by the grantor (see subsection (3)); or

(ii) adopted or accepted by the grantor by an act, or omission, that reasonably appears to be done with the intention of adopting or accepting the writing; and

(b) the writing evidencing the agreement contains:

(i) a description of the particular collateral, subject to subsections (4) and (5); or

(ii) a statement that a security interest is taken in all of the grantor’s present and after‑acquired property; or

(iii) a statement that a security interest is taken in all of the grantor’s present and after‑acquired property except specified items or classes of personal property.

…

100 Part 2.3 of the PPS Act concerns possession and control of personal property. Subsections 24(1) and (2) are mirror provisions. They respectively provide that a secured party cannot have possession of personal property if the property is in the actual or apparent possession of the grantor or debtor; and that a grantor or debtor cannot have possession of personal property if the property is in the actual or apparent possession of the secured party.

101 Sections 123 and 124 of the PPS Act concern seizing collateral. They provide:

123 Secured party may seize collateral

(1) A secured party may seize collateral, by any method permitted by law, if the debtor is in default under the security agreement.

Seizing intangible property

(2) For the purposes of this Act, unless subsection (3) applies, a secured party may seize intangible property only by giving a notice, stating that the giving of the notice constitutes seizure of the property, to the following persons:

(a) the grantor;

(b) if the intangible property is a licence—either:

(i) the licensor; or

(ii) the licensor’s successor.

(3) Intangible property may be seized by another method, if so agreed between:

(a) the parties to the security agreement; or

(b) if the intangible property is a licence—the parties to the security agreement together with the licensor or the licensor’s successor.

No perfection by seizure

(4) A secured party who seizes collateral under this section does not perfect the secured party’s security interest in the collateral.

124 Secured party who has perfected a security interest in collateral by possession or control

(1) This section applies if:

(a) a secured party has perfected a security interest in collateral by possession or control of the collateral; and

(b) the debtor is in default under the security agreement.

(2) A secured party may seize the collateral under section 123 by giving a notice to:

(a) the grantor; and

(b) if the collateral is a licence—either:

(i) the licensor; or

(ii) the licensor’s successor.

(3) To avoid doubt, this section applies whether the secured party has perfected the security interest only by possession or control, or by another method as well.

102 Section 267 deals with the vesting of unperfected security interests in the grantor upon, among other things, its winding up. It provides that, in the case of a winding up of a grantor, an unperfected security interest will vest in the grantor immediately before the winding up commenced.

103 Section 588FL of the Corporations Act (see [62] above) provides that if a security interest is registered after the latest of certain specified times then, if the security interest is perfected by registration and no other means, it will vest in the grantor, relevantly, immediately before the commencement of the winding up. The specified times are, relevantly, six months prior to the commencement of the winding up; or the earlier of 20 business days after the security agreement that gave rise to the security interest came into force or the time of the commencement of the winding up.

Consideration

104 Section 588FL is the relevant vesting provision. As at 3 February 2016, before the commencement of the winding up of Retroflex on 12 February 2016, Knauf perfected its security interest by registration. It follows that s 267 of the PPS Act, which deals with the vesting of unperfected security interests, does not apply. Rather, s 588FL, which deals with security interests perfected by registration and by no other means, may cause Knauf’s security interest to vest in Retroflex.

105 For the purposes of s 588FL, the latest of the specified times is six months prior to the commencement of the winding up of Retroflex, 12 August 2015. As Knauf’s security interest was not registered until after that date its effectiveness depends upon whether it has been perfected other than by registration alone. Relevantly, perfection will occur under the PPS Act if: the security interest is attached to the collateral: s 21(1)(b)(i); the security interest is enforceable against third parties: s 21(1)(b)(ii); and the secured party has possession of the collateral, provided that the possession is not as a result of seizure or possession: subss 21(1)(b)(iii) and 21(2)(b).

Attachment

106 A security interest attaches to collateral in the circumstances set out in s 19(2) of the PPS Act, namely, when the grantor has rights in the collateral or the power to transfer rights in the collateral to the secured party; and either value is given for the security interest or the grantor does an act by which the security interest arises.

107 Given the terms of the Security Deed, in particular cl 3.1, it is clear that a security interest has attached to collateral. Relevantly, pursuant to cl 3.1(a) of the Security Deed, that collateral comprises all of Retroflex’s then present and future property.

Enforceability against a third party

108 The circumstances in which a security interest is enforceable against a third party are set out in s 20 (see [99] above). The security interest must be attached to the collateral and, among other things, a security agreement may provide for the security interest to cover the collateral. That security agreement must be in writing, signed or accepted by the grantor, and the writing evidencing the agreement must contain one of the matters set out in subs 20(2)(b). Those matters relevantly include a statement that a security interest is taken in all of the grantor’s present and after-acquired property.

109 Again, in light of the terms of the Security Deed, in particular cl 3.1 and the relevant definitions set out in cl 1.1, it is clear that the security interest is enforceable against a third party.

Possession, other than as a result of seizure or repossession

110 The real issue between the parties is whether Knauf perfected its security interest by taking possession of the collateral other than by way of seizure or repossession.

111 In summary, Retroflex submitted that:

(1) the Receivers did not obtain actual or apparent possession of its assets and the mere act of appointing a receiver does not amount to possession;

(2) even if the Receivers had possession, because they are agents of Retroflex, possession remained with Retroflex;

(3) there is doubt about how Knauf could have taken possession of all of the property of Retroflex given its debtor finance facility with Scottish Pacific Business Finance Pty Ltd (Scottish Pacific) which, in turn, raises an issue about what assets the Receivers were entitled to possess; and

(4) if possession was obtained, it was by seizure.

112 I will consider each of those submissions below.

Did the Receivers obtain actual or apparent possession of Retroflex’s assets? If so was possession obtained by seizure?

113 Knauf’s position is that it was in possession of Retroflex’s assets within the meaning of the PPS Act either because of:

the existence of the right to appoint a receiver together with the exercise of that right, such that the receiver appointed may then give Knauf the power to deal exclusively with the collateral, namely, the assets of Retroflex; or

the existence of the right to appoint a receiver, the exercise of that right and the implementation of those rights by the Receivers in asserting control over the assets.

114 Retroflex submitted that the mere act of appointing a receiver does not amount to possession and that having a right to possess property is not the same as having possession of it. Retroflex noted that cl 9.1(b)(ii) of the Security Deed provides that a receiver may take immediate possession of any secured property and that s 420(2)(a) of the Corporations Act similarly provides that an appointed receiver has power to enter into possession and take control of property of the corporation. It submitted that neither the Security Deed nor the Corporations Act say that a receiver immediately takes possession. It submitted that the word “may” in cl 9.1(b)(ii) indicates that a receiver must actively take another step and seize the property from the company.

115 Retroflex contended that, accordingly, possession does not happen automatically on the mere appointment of a receiver. It further contended that this was consistent with the facts, which show that the Receivers demanded possession from it and the Liquidator. Retroflex submitted, relying on s 24(1) of the PPS Act, that it was apparent from the sequence of events and the actions of Knauf and the Receivers that it had actual and apparent possession so that Knauf and the Receivers could not have had possession.

116 Knauf maintains that it gained possession of the collateral within the meaning of s 21(2)(b) of the PPS Act and that its security was thereby perfected before the appointment of the liquidator. In order to determine whether that is so it is necessary to consider the meaning of the term “possession” as it is used in the PPS Act.

117 Knauf made extensive submissions concerning the common law meaning of possession. It referred me to the detailed treatise on possession of the learned authors Pollock F and Wright RS, An essay on possession in the common law (Clarendon Press, 1888). Knauf noted that the right to possess, though distinct from possession, is treated as equivalent to possession itself for certain purposes, relying on the following passage at page 13:

We have to add that the right to possess, though distinct from possession, is treated as equivalent to possession itself for certain purposes, more important with regard to procedure than to the substance of the law, and under the modern English practice of only historical importance, but still needful to be understood. It is then called constructive possession. Want of attention to the somewhat minute distinctions arising from this extension of the rights of a possessor to one who is not an actual possessor has led to much confusion.

118 Knauf submitted that the common law concept of possession may be equated with de facto possession, legal possession and/or the right to possess or to have legal possession. But, as is evident from the above passage, Pollock and Wright equate the right to possess with constructive possession.

119 Knauf also drew my attention to the multiple dictionary definitions of possession. It observed that in Stroud’s Judicial Dictionary (4th ed, Sweet & Maxwell, 1979) there are 57 different entries for possession and that in Black’s Law Dictionary (8th ed, West Group, 2004) there are 36 different types of possession listed. It suffices to say that most of those 36 types of possession are not relevant for present purposes. However, the current edition of Stroud’s Judicial Dictionary (9th ed, Sweet & Maxwell, 2016) has only seven entries for possession. The opening paragraph of the definition of possession draws an extract from J A Pye (Oxford) Ltd v Graham [2002] 3 WLR 221 at 233 and provides:

… there are two elements necessary for legal possession: (1) a sufficient degree of physical custody and control (‘factual possession’); (2) an intention to exercise such custody and control on one’s own behalf and for one’s own benefit (‘intention to possess’). What is crucial to understand is that, without the requisite intention, in law there can be no possession …

120 Knauf also relied on Gamer’s Motor Centre (Newcastle) Pty Limited v NatWest Wholesale Australia Pty Ltd (1987) 163 CLR 236 (Gamer’s), where the High Court considered the meaning of “delivery” for the purposes of s 28(2) of the Sale of Goods Act 1923 (NSW). It referred in particular to the judgment of Dawson J, where his Honour said at 262-263:

Delivery is sometimes said to be constructive where it is symbolic as, e.g., where the keys to goods kept under lock and key are handed over. Sir Frederick Pollock doubted that in such circumstances, at least where control of the goods went with the key, there was a mere symbolic transfer of possession:… He preferred the view that there was a transfer of control in fact which constituted a change in possession. For it is control which is central to the notion that possession in law may consist of something other than physical or actual possession.

121 Finally, as to actual possession, Knauf referred to Thomas v Metropolitan Housing Corporation Ltd [1936] 1 All E.R. 210 at 216 and submitted that possession of the key to the premises in which chattels are located gives actual possession of the premises and the chattels.

122 In my opinion, the resolution of the question before me does not turn on nuances in the meaning of possession at common law. It is sufficient for present purposes to recognise that the word possession connotes a legal meaning that is wider than the ordinary meaning of that term. For example, relevantly, the legal meaning of possession at common law embraces the concept of constructive possession. But it is not necessary to exhaustively state the meaning of possession at common law to understand how that meaning may be modified for the purposes of the PPS Act.

123 Section 10 of the PPS Act provides that “possession has a meaning affected by section 24”. The phrase “has a meaning affected by” is also used for the definitions of “Australia” and “jurisdiction” in s 10 of the PPS Act. It is a phrase that has been used in other Commonwealth statutes for definitional purposes.

124 In Vanstone v Clark (2005) 147 FCR 299 (Vanstone) a Full Court of this Court (Black CJ and Weinberg J) considered the meaning of that phrase in the context of the definition of the word “behaviour” in s 4A of the Aboriginal and Torres Strait Islander Commission Act 1989 (Cth). Weinberg J said at [132]-[133] and [135]:

132 The use of the term “has a meaning affected by” is a drafting device that is now found in a number of Commonwealth statutes. …

133 Despite the fact that there are now numerous examples of the use of this drafting device, counsel were not able to point to any authority bearing upon the question whether, as a matter of construction, this formula allows for an expanded meaning to be given to a word beyond the ordinary meaning that would otherwise be accorded to it.

…

135 If the words “affected by” are to be given any sensible interpretation, they must contemplate the expansion or contraction of the meaning that would otherwise be applicable. The word “affected”, in its ordinary and natural sense, means “influenced”, “altered”, or “shaped”. It is not merely a synonym for “touching”, “relating to” or “concerning”: Re Bluston (Deceased) [1967] Ch 615 at 633 per Winn LJ. It is plainly apt to include the power to modify, whether by widening or by narrowing, the ordinary meaning of any word that is “affected”.

(emphasis added)

125 The meaning of “possession” in s 21(2)(b) of the PPS Act thus is an expansion or contraction of the meaning that would otherwise be applicable.

126 The meaning that would otherwise be applicable to the word possession in s 21(2)(b) is, in my opinion, the meaning of that term at common law. In Gamer’s at 243, Mason CJ rejected a submission that the word “possession”, as used in the definition of “delivery” under the Sale of Goods Act 1923 (NSW), would be given its common or ordinary meaning of “actual physical custody”. His Honour noted that “‘possession’ is an established legal concept, particularly in its application to goods and chattels”. The same must be said of “possession” in its application to articles of personal property covered by the PPS Act.

127 Thus, the word possession in the PPS Act has its common law meaning, modified to the extent provided for in s 24 of the PPS Act. As set out at [100] above, subss 24(1) and (2) limit the meaning of “possession” by reference to the party who has the “actual or apparent possession” of the personal property. That is, as between a secured party and a grantor or debtor, a secured party cannot have “possession” if the grantor or debtor, or someone on their behalf, has actual or apparent possession: s 24(1). Similarly, a grantor or debtor cannot have “possession” of personal property if the secured party, or someone on their behalf, has actual or apparent possession: s 24(2).