FEDERAL COURT OF AUSTRALIA

Mentha, in the matter of Arrium Finance Limited v National Australia Bank Limited [2017] FCA 818

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to section 588FM of the Corporations Act 2001 (Cth), 24 May 2017 be fixed as the later time for the purposes of section 588FL(2)(b)(iv) of the Act in respect of security interests granted by the Second Plaintiffs (Arrium Grantor Companies) in favour of the Defendant in connection with the:

(a) Syndicated Facility Agreement dated 22 May 2017;

(b) Vesper Standby Facility Security Trust Deed dated 22 May 2017; and

(c) Vesper (Standby Facility) General Security Agreement dated 22 May 2017,

as limited and amended by the:

(d) Deed of Partial Release of Security executed by the Defendant on 26 May 2017 in respect of released property the subject of security interests in favour of Alleasing Pty Ltd; and

(e) Deed of Partial Release of Security dated 21 June 2017 executed by the Defendant in respect of released property the subject of security interests in favour of Export Finance and Insurance Corporation,

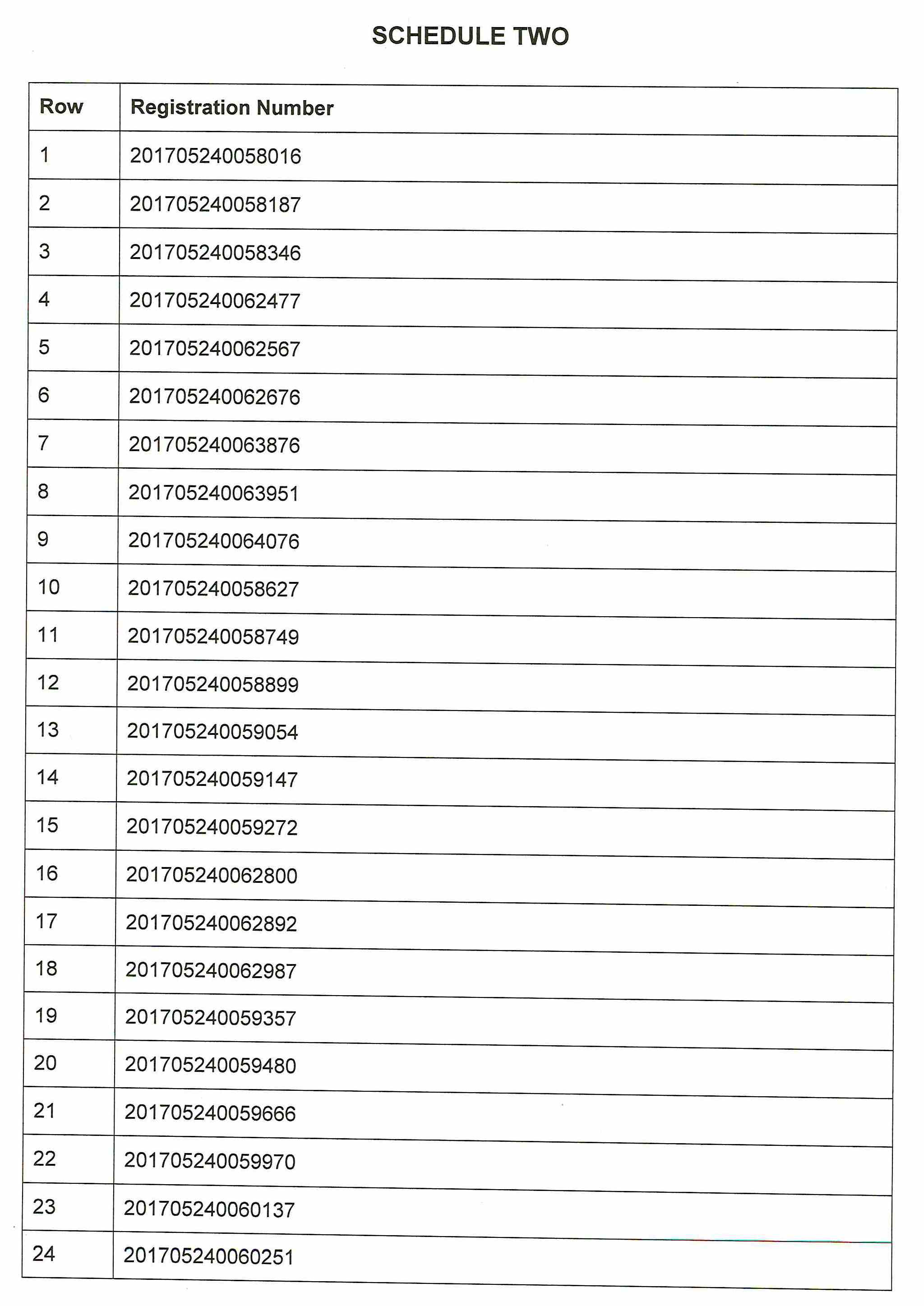

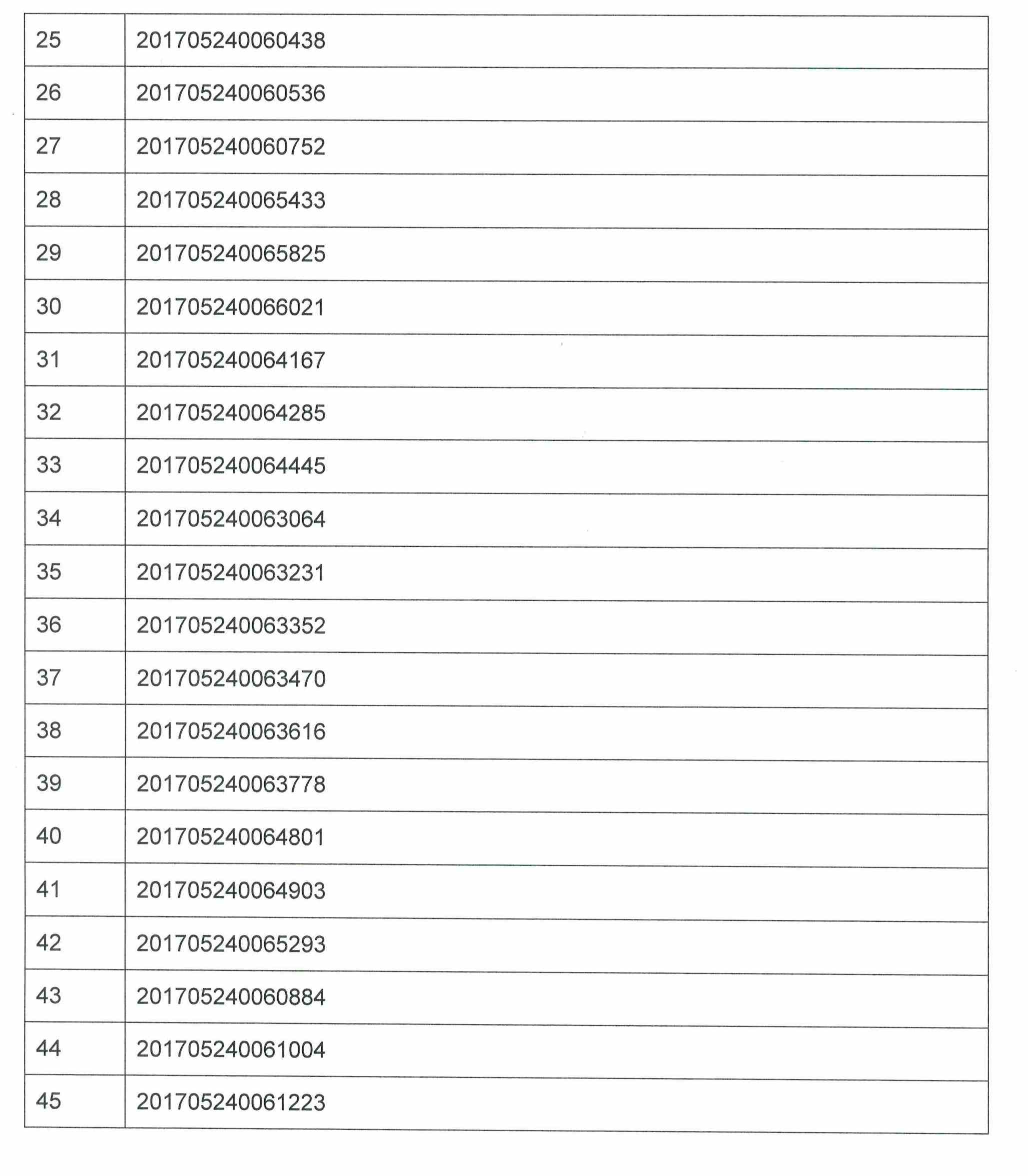

such security interests corresponding to the registration numbers listed in “Schedule Two” in the register established under the Personal Properties Securities Act 2009 (Cth).

2. Pursuant to section 37AF of the Federal Court of Australia Act 1976 (Cth), Tab 2 to exhibit MM-1 of the affidavit of Martin Madden sworn 5 June 2017 be kept “confidential”, placed in a sealed envelope on the Court file and is not to be published or accessed except pursuant to an order of the Court.

3. The Plaintiffs’ costs of this application be costs in the administration of the Arrium Grantor Companies.

4. The Plaintiffs and any creditor of the Arrium Grantor Companies affected by these orders have liberty to apply upon two business days’ written notice to the parties.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BESANKO J:

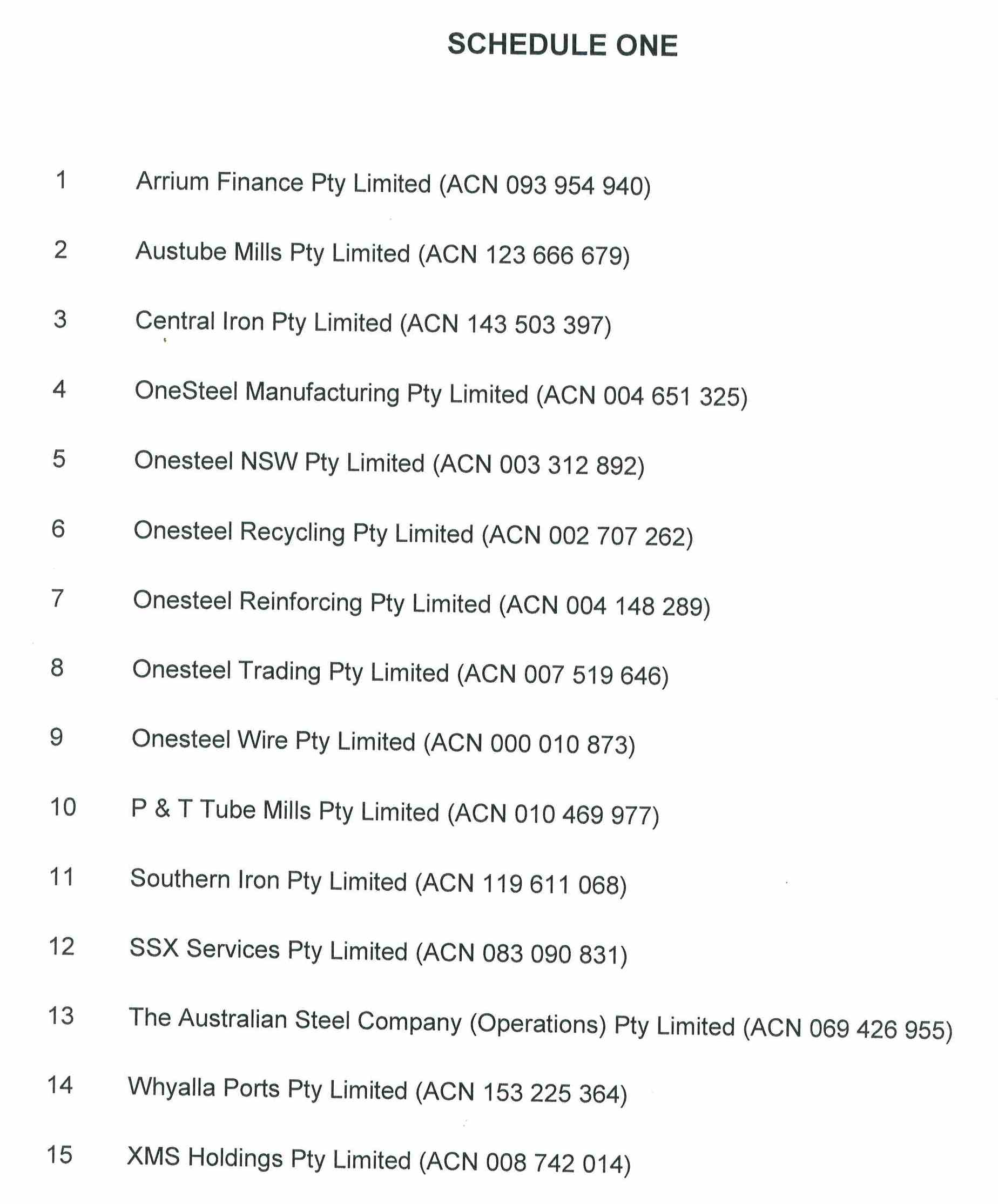

1 This is an application in the matter of Arrium Finance Limited (subject to Deed of Company Arrangement) ACN 093 954 940 and 14 other companies. Those companies are identified in Schedule One of the Originating Process. I will refer to Arrium Finance Limited and the 14 companies as “the Arrium Grantor Companies”.

2 The plaintiffs to the application sought an order pursuant to section 588FM of the Corporations Act 2001 (Cth) (the Act) that 24 May 2017 be fixed as the later time for the purposes of section 588FL(2)(b)(iv) of the Act in respect of certain security interests granted by the Arrium Grantor Companies in favour of the defendant. On 6 July 2017, I made the orders sought by the plaintiffs. These are my reasons for making those orders.

3 The first plaintiffs to the proceeding are Mr Mark Mentha, Ms Cassandra Mathews, Mr Martin Madden and Mr Bryan Webster in their capacities as Deed Administrators of the Arrium Grantor Companies. The second plaintiffs are the Arrium Grantor Companies. The defendant is the National Australia Bank Limited (NAB).

4 On 7 April 2016, members of the firm, Grant Thornton, were appointed administrators of Arrium Limited (subject to Deed of Company Arrangement) and 93 of its direct or indirect subsidiaries. I will refer to Arrium Limited and its direct or indirect subsidiaries as “the Arrium Administration Group” or “Group”. The Arrium Grantor Companies are members of the Arrium Administration Group. On 12 April 2016, the first plaintiffs replaced the previous administrators of the Arrium Administration Group.

5 On 4 November 2016, the second meeting of creditors of the Arrium Administration Group was held and at the meeting, it was resolved as follows:

(a) each of the Arrium Administration Group entities accept SSX Pty Limited (subject to Deed of Company Arrangement) (SSX) and their creditors would each enter into identical deeds of company arrangement which would facilitate sale or realisation transactions and maximise returns (Transaction Support DOCAs);

(b) SSX would enter into a distribution deed of company arrangement in which the proceeds of sale of all the sales/realisations would be aggregated into a fund and distributed to creditors of the Arrium Administration Group (Distribution DOCA).

6 Since 4 November 2016 and pursuant to the Transaction Support DOCAs, the first plaintiffs have been pursuing a sale of the businesses undertaken by the Arrium Administration Group.

7 Mr Madden has sworn two affidavits in this proceeding. In his first affidavit, he describes the Arrium Administration Group. The Group carries on a very large and complex integrated mining, iron ore export, steel manufacturing, steel recycling and steel distribution business under separate business divisions. Although the Arrium Administration Group consists of 94 separate entities, only some of these companies carry on the Arrium businesses. Mr Madden refers to these entities as the Arrium Sales Entities. Mr Madden describes the businesses carried on by the entities in Australia, including business operations in Whyalla and business operations in Victoria and New South Wales. The OneSteel business operates in all States and Territories in Australia. Mr Madden states that the operations of the Group’s business divisions are highly integrated and intermingled as between various corporate entities. The business divisions are as follows:

(a) Mining and Port;

(b) Whyalla Steel Works;

(c) Manufacturing;

(d) Distribution;

(e) Recycling; and

(f) Head office/shared services.

8 Mr Madden states that in view of the size, complexity and intermingling of the Arrium Administration Group businesses, the Arrium Administration Group entities entered into the Transaction Support DOCAs and the Distribution DOCA so as to allow flexibility in selling the Arrium business and assets through a share sale or restructure that maximises the chances of the Arrium Administration Group businesses, or as much of them as possible, continuing in existence.

9 Mr Madden describes the key terms of the Transaction Support DOCAs. They include the power to borrow or raise money and grant security (cl 7.6(b)(xliv)).

10 The first plaintiffs are continuing to operate and trade the Arrium Sales Entities and the Arrium Administration Group businesses on a “going concern” basis to maximise the chances of the Arrium Administration Group businesses, or as much of them as possible, continuing in existence so as to maximise the return to creditors.

11 As I have said, the first plaintiffs have been engaged in the sale campaign in relation to the Arrium Sale Entities since November 2016. On 31 May 2017, final bids in the sale process were received.

12 Shortly before 31 May 2017, the first plaintiffs formed the view that it would be in the best interests of the Arrium Administration Group if they entered into standby facility agreements with NAB, Australia and New Zealand Banking Group Limited, the Commonwealth Bank of Australia and Westpac Banking Corporation. The Standby Facility Agreements comprise a Syndicated Facility Agreement, a Trust Deed and a General Security Agreement.

13 Mr Madden states that the Arrium Administration Group currently has approximately $166.4 million cash available for operations as at 1 June 2017. The first plaintiffs are reviewing cashflow on a weekly basis and have been doing so throughout the voluntary administration and the administration of the Transaction Support DOCAs. In his first affidavit sworn on 5 June 2017, Mr Madden said that the Arrium Administration Group made payments of $156.5 million and received $137 million in the last week. The plaintiffs entered into the Standby Facility Agreements on 22 May 2017 because whilst they were of the view that the Arrium Administration Group was currently generating positive earnings, they considered that there was some risk that the Group would have insufficient working capital during the period it would take to conclude negotiations and the sale process.

14 Mr Madden summarised the key provisions of the Syndicated Facility Agreement in the following way:

(a) the Syndicate will make available to Arrium Finance a loan facility up to a total amount of $50 million (Facility) (clause 2);

(b) Arrium Finance must use funds drawn from the Facility to fund the net trading cash requirements of the Arrium Administration Group with the purpose and object of giving effect to the DOCAs (clause 5(a));

(c) the Facility is secured by the security set out in the Trust Deed (Security) (clause 5(b));

(d) Arrium Finance must repay any outstanding amount (being any drawdowns, plus interest and any costs payable) by the termination date being 30 September 2017 or on completion of a sale of the Arrium Sales Entities, (whichever is the sooner) (clause 13.1);

(e) each of the Arrium Grantor Entities agree to do anything which NAB as security trustee asks and considers necessary to (acting reasonably) including, amongst other things, ensure that the Security is enforceable, perfected and otherwise effective (clause 13.3(b));

(f) events of default are set out in clause 20.1 and include, amongst other things, the failure to pay any amount when due and remains unremedied after three business days following notice to pay, breaches of other provisions which remain unremedied after fifteen business days following notice to remedy and termination of the DOCAs and/or we cease to be the Deed Administrators; and

(g) in the event of a default, NAB, as security trustee and agent for the Syndicate, may take certain steps including requiring immediate payment of amounts due, cancelling the Facility and enforcing rights under the other transaction documents (clause 20.3).

15 Mr Madden summarised the key provisions of the Trust Deed and General Security Agreement in the following way:

(a) the Security is defined to include, amongst other things, all present and after-acquired property of the Arrium Grantor Entities (clause 1.1 of the Trust Deed and clause 1.2 of the General Security Agreement);

(b) NAB, as security trustee, may register the Security on the Personal Properties Securities Register (clause 13.2 of the General Security Agreement); and

(c) if an event of default continues, NAB as security trustee may, amongst other things, appoint a receiver (clause 15.4 of the General Security Agreement).

16 On 24 May 2017, NAB registered the security on the Personal Property Securities Register. On 26 May 2017, NAB as security trustee, clarified that certain crushing and parts equipment used at Iron Knob, the subject of a dispute (now resolved) with Alleasing Pty Ltd, was not captured by the security and provided the first plaintiffs with a Deed of Partial Release of security as confirmation. Alleasing Pty Ltd leased certain equipment and vehicles to OneSteel Manufacturing Pty Ltd (subject to Deed of Company Arrangement) (OneSteel) which is one of the Arrium Grantor Companies. OneSteel also leases equipment and vehicles from KJ Renfrey Nominees Pty Ltd, but that company indicated that it did not object to the orders sought.

17 Prior to entering into the Standby Facility Agreements, the first plaintiffs formed the following views. First, they considered that a sale or recapitalisation of the Arrium Sales Entities through the Transaction Support DOCAs will maximise returns for creditors. Secondly, they formed the view that continuing to operate and trade the Arrium Sales Entities and the Arrium Administration Group businesses on a “going concern” basis until completion, would maximise the prospects of a successful sale or recapitalisation and maximise the price achievable. Thirdly, they formed the view that there is some risk that the Arrium Administration Group will have insufficient working capital during the period between the period it takes to conclude negotiations and the sale process. They also formed the view that entering into the Standby Facility Agreements would be in the best interests of creditors.

18 On 5 July 2017, the first plaintiffs signed a binding agreement for the sale of the Arrium Administration Group’s Manufacturing, Distribution, Recycling, Whyalla Steel Works and Mining divisions to GFG Alliance. The sale agreement is subject to approval by the Arrium Committee of Creditors and the Foreign Investment Review Board. Completion of the sale is expected to occur in late August 2017. Under the sale agreement, the first plaintiffs are required to operate and trade the Arrium Administration Group businesses until completion. Mr Madden swore a second affidavit on 5 July 2017. In his second affidavit, Mr Madden stated that the first plaintiffs continue to hold the view that there is a risk that the Arrium Administration Group will have insufficient working capital to continue to trade until completion of the Arrium sale and they remain of the view that the Standby Facility Agreements are necessary and in the best interests of creditors so as to maximise the chances of the Arrium sale completing as a “going concern”.

19 On 8 June 2017, the Creditors’ Committee under the Arrium Administration Group Deeds of Company Arrangement was advised by the first plaintiffs that they had entered into the Standby Facility Agreements and of the terms of those agreements. The Committee consists of representatives of a wide range of groups, including members who are representatives of the different creditor groups and interests who have claims against the various Arrium Administration Group companies, including union and non-union employees, the Australian bank lenders, the US Noteholders, trade creditors, other lenders and South Australian State Government and Federal Government representatives. The Committee was also advised that the first plaintiffs had applied to the Court for an extension of time under s 588FM of the Act in respect of registration under the Personal Properties Securities Act 2009 (Cth) of the Standby Facility Agreements. Mr Madden asked the Creditors’ Committee whether there were any questions. There were no questions and no one on the Creditors’ Committee voiced any opposition to the application.

20 An entity known as Export Finance and Insurance Corporation (EFIC) also holds security over assets within the Arrium Administration Group. NAB as security trustee for the Standby Lenders has executed a Deed of Partial Release of Security by which the Standby Lenders excluded from the Standby Security any property of the Arrium Grantor Companies that is the subject of the EFIC security.

21 In this case, the security interest arises and was registered after the Arrium companies were placed into administration on 7 April 2016. Section 588FL of the Act applies in those circumstances and the security interest would vest in the company on creation, even if registered within 20 days after the security agreement came into force, unless an order was made under s 588FM extending the time for registration: K.J. Renfrey Nominees Pty Ltd (Trustee), in the matter of OneSteel Manufacturing Pty Ltd v OneSteel Manufacturing Pty Ltd [2017] FCA 325 (Re Renfrey) at [23]-[26] per Davies J.

22 Section 588FM(2) provides that the Court may make an order under s 588FM(1) if it is satisfied that:

(a) the failure to register the collateral earlier:

(i) was accidental or due to inadvertence or some other sufficient cause; or

(ii) is not of such a nature as to prejudice the position of creditors or shareholders; or

(b) on other grounds, it is just and equitable to grant relief.

The plaintiffs rely on the just and equitable ground.

23 In determining an application based on that ground, the Court will consider carefully the particular circumstances of the case. As the effect of an order is to preserve the secured creditor’s security, it is necessary to consider the interests of the unsecured creditors. However, mere evidence that the dividend to unsecured creditors may be less may not be enough to establish prejudice. The type of prejudice which may be particularly relevant is that suffered where there is delay in registration and a creditor deals with the company unaware of the security interest. Where the security interests is to be entered into by administrators or deed administrators, their opinion that entering into the security interests is in the best interests of creditors, having regard to the objects of Part 5.3A of the Act, is relevant (Re Appleyard Capital Pty Ltd; 123 Sweden AB v Appleyard Capital Pty Ltd [2014] NSWSC 782; (2014) 101 ACSR 629 (Re Appleyard) at [29]-[30]; Re Renfrey at [28]; Alleasing Pty Ltd, in the matter of OneSteel Manufacturing Pty Ltd v OneSteel Manufacturing Pty Ltd [2017] FCA 656 (Re Alleasing) at [17]).

24 In Re Appleyard, Brereton J put the matter in this way in a context where, through inadvertence, there had been a failure to register the collateral earlier (at [29]-[30]):

29. The purpose of giving the court a discretion to fix a later time is to relieve a secured creditor from the consequences of accident or inadvertence. In the event of insolvency this necessarily involves detriment to unsecured creditors who would otherwise benefit from the vesting of the security in the company. It would be contrary to the purpose of the section to treat the risk that unsecured creditors could be adversely affected by making an order as a dominant consideration. The fact that absence of prejudice to creditors is an alternative ground for relief [s 588FM(2)(a)(ii)] indicates that it was not intended that relief from accident or inadvertence be granted only where there is no prejudice to creditors, as Bray CJ observed in Re Flinders Trading Co (at 220). The cases to which I have referred show that, despite the majority view in Re Flinders Trading Co, courts have not infrequently been prepared to grant extensions of time, even in a context where liquidation or administration is in contemplation, though reserving leave to any liquidator or administrator to apply to set the order aside.

30. Thus, although I accept, as the authorities make clear, that the presence or absence of prejudice to unsecured creditors is a relevant discretionary consideration, relevant prejudice is not necessarily established merely by showing that the dividend to unsecured creditors will be less if the security interest does not vest in the company; the unsecured creditors may well have been in no different a position had the security interest been timely registered. The type of prejudice that is of particular relevance is prejudice attributable to the delay in registration, rather than prejudice from making the order (which is inevitable). This is the type of prejudice contemplated the legislation (see s 588FM(2)(a)(ii), which refers to prejudice from the failure to register earlier, not from making the order), and referred to by Buckley J in In re Cardiff Workmen’s Cottage Co Ltd; by Long Innes J in Re a Ltd Co (see also Re Flinders Trading Co, 225 (Bray CJ); 234 (Mitchell J)); and by McLelland J in Re Guardian Securities (at 98). The period of delay in effecting registration is relevant, because the shorter the delay the less likely that the failure to register within time will have had any impact. The significance of the passage of time is mainly related to the possibility of competing interests having arisen, in particular through others having dealt with the company on the footing that the collateral was unencumbered.

25 In Re Renfrey, Davies J made similar observations in a context of a security interest granted in settlement of a dispute by the administrators over assets of entities within the Arrium Administration Group. Her Honour said (at [28]):

28. To make an order under s 588FM(2)(b), the Court must be satisfied that it is just and equitable to grant relief. The circumstances that would justify an order extending the time for registration on the just and equitable ground to avoid the operation of s 588FL(4) will depend upon the circumstances of each particular case. Some general observations can be made though. As the purpose and effect of an order under s 588FM is to avoid the vesting of the security interest in the company and preserve the secured creditor’s security, it is relevant in determining whether it is just and equitable to fix a later time to consider the interests of the creditors: Re Appleyard Capital Pty Ltd [2014] NSWSC 782; (2014) 101 ACSR 629 at [29]-[30]. As Brereton J observed in Re Appleyard Capital Pty Ltd at [30] whilst “the presence or absence of prejudice to unsecured creditors is a relevant discretionary consideration, relevant prejudice is not necessarily established merely by showing that the dividend to unsecured creditors will be less if the security interest does not vest in the company; the unsecured creditors may well have been in no different a position if the security interest been timely registered”. His Honour stated that the type of prejudice that is of particular relevance is prejudice attributable to the failure to effect registration earlier where the delay in the registration of the security interest causes prejudice to creditors who have transacted with the company to their detriment, being unaware of the creation of a security interest. In the present case, there was no delay in registration.

26 The administrators have the power to enter into the Standby Facility Agreements (see cl 7.6(b)(xliv) of the Transaction Support DOCAs). The administrators are of the opinion that the entry into the Standby Facility Agreements is in furtherance of the objects of Part 5.3A of the Act (section 435A) and is in the best interests of the creditors. There is no reason to doubt the soundness of those opinions. The security interests were registered in a timely fashion. The Creditors’ Committee, which, as I have said, represents a wide range of interests, has no opposition to the proposal. The secured creditors who might otherwise have reason to object to the Standby Facility Agreements are protected by the proposed orders. In those circumstances, it was appropriate to make the orders sought.

27 The Standby Facility Agreements were plainly commercially confidential documents and, in those circumstances, it was appropriate to make a confidentiality order with respect to those documents.

28 It was for these reasons that I made the orders I did on 6 July 2017.

I certify that the preceding twenty-eight (28) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Besanko. |

Associate: