FEDERAL COURT OF AUSTRALIA

Pearce v Gulmohar Pty Ltd [2017] FCA 660

Table of Corrections | |

In the first sentence of paragraph 15, $832,031 has been replaced with $857,031. | |

6 July 2017 | In the second sentence of paragraph 497 the word “of” following the word “total” has been replaced with “claimed for”. |

TABLE OF CONTENTS

[6] | |

[15] | |

[24] | |

[94] | |

[117] | |

[131] | |

[144] | |

[144] | |

[158] | |

[165] | |

Analysis of contractual arrangements between GVF and Toxfree | [169] |

Contract for collection and removal of waste from GVF’s site | [169] |

[205] | |

[231] | |

[251] | |

[254] | |

[256] | |

[275] | |

[276] | |

[286] | |

[325] | |

[328] | |

[337] | |

[340] | |

[353] | |

[371] | |

[375] | |

[385] | |

[399] | |

[402] | |

[412] | |

[417] | |

[420] | |

[424] | |

[427] | |

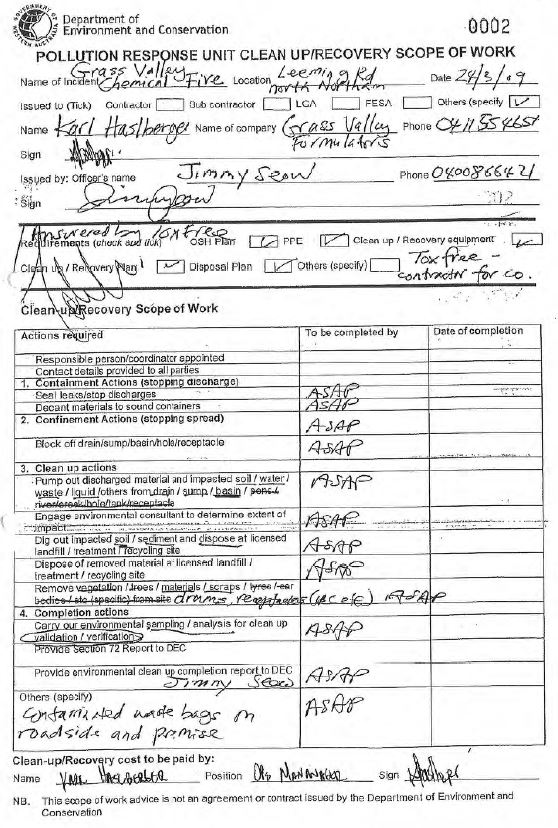

[436] | |

[441] | |

[444] | |

[447] | |

The claim against Peter Heyn as trustee of the Heyn Family Trust | [453] |

[458] | |

[459] | |

[465] | |

The Palacimo payments, the Vaudell payments, the Superway Garden payment and the Heyn payments | [469] |

[475] | |

[483] | |

[487] | |

[490] |

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The matter is listed for hearing on 6 July 2017 at 9.30 am as to the form of orders and as to costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

RANGIAH J:

1 Before going into liquidation, the first plaintiff, Grass Valley Formulators Pty Ltd (in liquidation) (GVF), engaged in a series of transactions with the first to fifth defendants. The plaintiffs allege that these transactions are “voidable transactions” within s 588FE of the Corporations Act 2001 (Cth). The plaintiffs also allege that the fifth and sixth defendants breached their duties as directors of GVF by causing the company to enter the transactions.

2 GVF’s problems began on 24 March 2009 when a fire broke out at its factory, resulting in chemical contamination of its site. GVF engaged Toxfree Solutions Ltd (Toxfree) to collect contaminated material from the site. Whether Toxfree was engaged to do any other work and its charges are matters in dispute. The maximum amount of GVF’s insurance cover was $1,549,000 after deduction of the excess. The insurer paid GVF that amount, but it was not enough to cover Toxfree’s invoices. GVF did not use the insurance proceeds to pay any part of Toxfree’s invoices, but instead made a series of payments to its undisputed creditors, including the first to fifth defendants.

3 Toxfree commenced proceedings against GVF in the Supreme Court of Western Australia. While those proceedings were pending, GVF made an application in the Supreme Court of Queensland for orders that it be wound up in insolvency. That application was granted on 17 November 2010.

4 The plaintiffs seek orders for the repayment of money paid by GVF to the first to fifth defendants. The plaintiffs’ case that the transactions are voidable transactions within s 588FE of the Corporations Act relies substantially on the allegation that GVF was insolvent when the transactions were entered.

5 I propose to describe the parties and the issues in the case before summarising the evidence. I will then address the question of GVF’s solvency. That depends principally upon the extent of the Toxfree debt, which was the area of greatest factual and legal debate in the case. I will then turn to the question of whether the transactions are voidable transactions and whether the fifth and sixth defendants breached their duties as directors.

6 The first plaintiff, Mark William Pearce, was appointed as liquidator of GVF under orders made by the Supreme Court of Queensland on 17 November 2010. Mr Pearce also gave expert accounting evidence at the trial.

7 The period of time relevant to the present proceedings is from March 2009 to November 2010. The positions of the defendants in that period were as follows.

8 The fifth defendant, Peter Karl Heyn, and the sixth defendant, Geoffrey Martin Vaughan, were directors of GVF. There also was a third director, Terrence Armstrong, who died in 2014. There was little evidence led about Mr Armstrong’s role in the management of the company.

9 Mr Heyn was the sole director and secretary of the first defendant, Gulmohar Pty Ltd (Gulmohar). Gulmohar provided stock to GVF on credit from time to time. GVF was indebted to Gulmohar throughout the relevant period.

10 Mr Heyn was also the director and secretary of, and a shareholder in, the second defendant, Palacimo Pty Ltd (Palacimo). Mr Heyn’s wife, Monique Heyn, was the other shareholder in Palacimo. Palacimo owned the shares in Gulmohar.

11 Mr Vaughan was a director and the secretary of the third defendant, Vaudell Pty Ltd (Vaudell).

12 Mr Vaughan was also a director and the secretary of the fourth defendant, Superway Garden AG & Pest Products Pty Ltd (Superway Garden).

13 The shares in GVF were owned by Palacimo, Vaudell and Mr Armstrong.

14 The defendants accept that each of them was a “related entity” of GVF within the meaning of that expression in s 9 of the Corporations Act.

15 In the period from 30 April 2009 to 17 November 2010, GVF paid the following amounts to the first to fifth defendants, totalling $857,031:

(a) $582,031 to Gulmohar (this was the net amount paid by GVF after deducting the value of stock supplied by Gulmohar);

(b) $100,000 to Palacimo;

(c) $90,000 to Vaudell;

(d) $42,500 to Superway Garden; and

(e) $42,500 to Mr Heyn as trustee of the Heyn Family Trust.

16 It is these payments, together with the granting to Gulmohar of a fixed and floating charge over GVF’s assets, which are said to be the voidable transactions. Those transactions also found the claim that Mr Heyn and Mr Vaughan breached their duties to GVF as its directors.

17 The plaintiffs allege that GVF was insolvent throughout the period from 30 April 2009 to 17 November 2010. The date 30 April 2009 seems to have been selected because the first payment among the impugned transactions was $50,000 to Gulmohar on 1 May 2009.

18 The allegation of insolvency requires consideration of three issues, namely:

(a) the extent of the debts due and payable by GVF in the period from 30 April 2009 to 17 November 2010;

(b) what funds GVF had available to pay such debts; and

(c) whether funding from related third parties was available to allow GVF to pay such debts.

19 The first issue, the extent of the debts due and payable, requires assessment of the debt owed by GVF to Toxfree. This requires examination of the terms of the contracts between GVF and Toxfree, the nature and extent of the work done by Toxfree and a determination as to what amounts were payable at what times.

20 The owner of the premises leased by GVF, Hamcor Pty Ltd (Hamcor), also claimed that it was owed a debt for unpaid rent. GVF disputed the debt and Hamcor was not paid. In the course of submissions the plaintiffs accepted that the Hamcor claim is not determinative of insolvency and can be left aside. I therefore do not propose to deal specifically with the Hamcor claim.

21 The second issue depends largely upon the evidence given by two expert accountants as to the funds GVF had available to it from its own assets and from an overdraft facility.

22 As to the third issue, Mr Heyn and Mr Vaughan gave evidence that they and companies they controlled were willing to provide financial support to GVF if required. Mrs Heyn also says she could have allowed her assets to be used to provide financial support. It is necessary to determine their capacity and willingness to provide such support as would allow GVF to pay its debts.

23 The remaining issues include whether the transactions are unfair preferences within s 588FA of the Corporations Act, uncommercial transactions within s 588FB, insolvent transactions within s 588FC, or unreasonable director-related transactions within s 588FDA, and whether the “good faith” defence in s 588FE is made out. It is also necessary to decide whether Mr Vaughan and Mr Heyn breached their fiduciary duties to GVF and their duties under ss 181, 182 and 183 of the Corporations Act.

EVIDENCE CONCERNING GVF’s ENGAGEMENT OF TOXFREE

24 GVF manufactured, or formulated, pesticides for sale to the agricultural industry. It operated from premises at Grass Valley, near Northam in Western Australia. The premises consisted of a factory and a separate administration building.

25 Karl Haslberger was GVF’s factory manager. At about 4 am (Western Australian time) on Tuesday, 24 March 2009, Mr Haslberger became aware that the factory was on fire. The fire brigade was called and the fire was extinguished.

26 The fire and the spraying of water by the fire brigade resulted in chemical contamination of the site. A pond on the site became filled with contaminated liquid. The soil at the site became contaminated. There was also contamination of containers and other equipment.

27 At about 7 or 8 am on the morning of the fire, Mr Haslberger was told by Ken Raine of the Western Australian Department of Environment and Conservation (DEC) that it would be a good idea to have someone on stand-by to carry out a clean up and removal of contaminated liquid. Mr Haslberger then telephoned Betty Carr, who was employed by Gulmohar as personal secretary to Mr Heyn, and gave her some names of companies that could assist to clean up the contaminated liquid, including Toxfree.

28 Toxfree provides waste management and industrial services, including providing emergency response services in relation to chemical spills. Toxfree is certified by the relevant government department in Western Australia as an emergency responder to dangerous goods incidents. Toxfree had previously been engaged by GVF to dispose of waste materials in 2007.

29 The witnesses have differing recollections of the precise sequence of relevant conversations and the content of those conversations. That is unsurprising, given the passage of time. Many of the differences are unimportant and need not be resolved. Other differences are more significant and I will deal specifically with these.

30 Errol Beere, a Business Development Manager employed by Toxfree, spoke to Mr Haslberger by telephone on the morning of 24 March 2009. Mr Haslberger said that storage tanks which contained chemicals were about to overflow and could spill into the Avon River. Mr Beere said that Toxfree could not commence providing its emergency response services until GVF raised a purchase order confirming that it accepted Toxfree’s terms. Mr Haslberger asked Mr Beere to liaise with Ms Carr to arrange a purchase order.

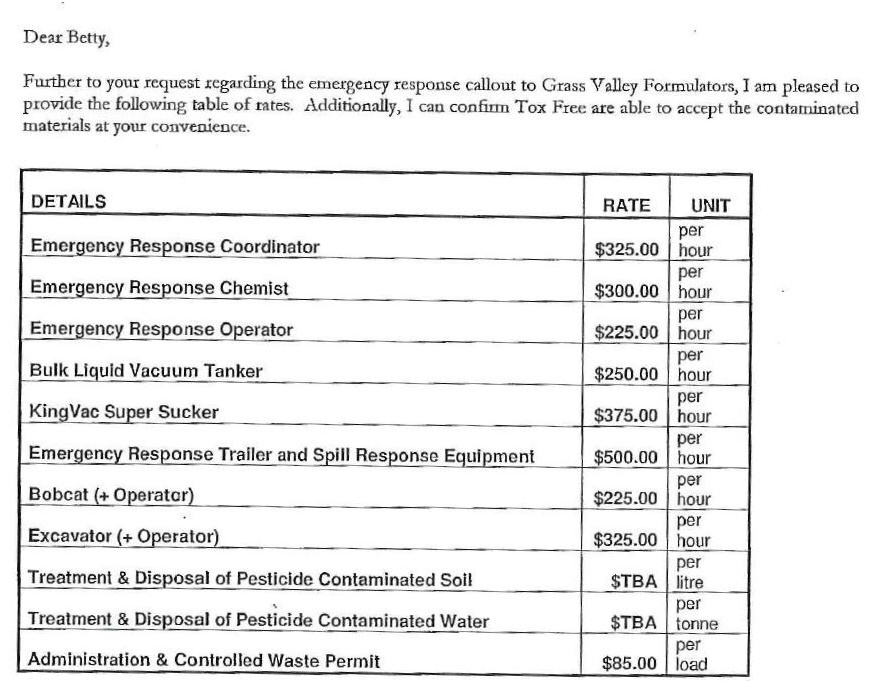

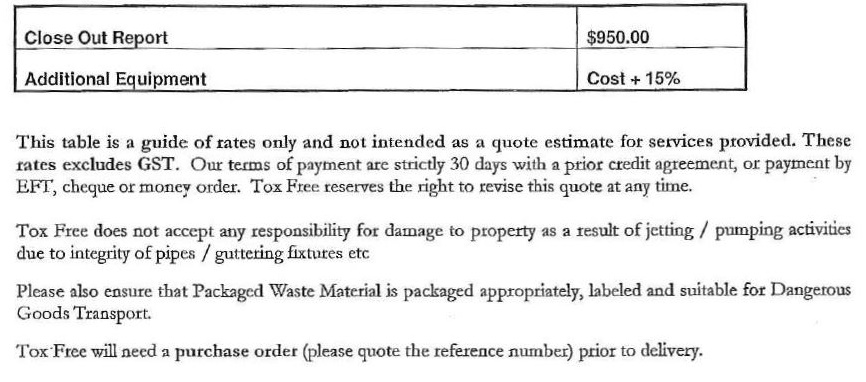

31 Mr Beere then spoke to Ms Carr by telephone. I accept Mr Beere’s version of the discussion. Mr Beere told Ms Carr that Toxfree would require a purchase order before it could start providing its emergency response services. Ms Carr asked Mr Beere for an estimate of costs. Mr Beere had already spoken to Mr Raine of the DEC, and had been told that approximately 500 tonnes of contaminated soil and approximately 300 kilolitres of liquid waste would need to be removed from the site. Mr Beere informed Ms Carr of the estimated quantities and said that it was extremely difficult to give an estimate of costs without seeing the site. Ms Carr informed Mr Beere that she required a figure solely for the purpose of preparing a purchase order. Mr Beere said that it would be not less than $160,000, exclusive of GST, for Toxfree’s emergency response services and he would provide her with a table of Toxfree’s rates along with his estimate.

32 Mr Beere told Ms Carr that he could not provide an estimate with respect to disposal costs until an analysis of the waste had been performed and the full extent of the chemicals involved was known. Ms Carr told Mr Beere that she understood that the estimate did not include Toxfree’s disposal rates and would confirm this on the purchase order.

33 Mr Beere then sent the following email to Ms Carr at 1.38 pm on 24 March 2009:

Hello Betty,

Please find attached our rates for Emergency Response callouts.

As discussed it is very difficult to pinpoint an estimated figure at this early stage. We will need to run sampling of both the contaminated water and contaminated soil before we can quote a rate for treatment and disposal.

The Department of Environment & Conservation representative onsite has said there could be up to 300 kilolitres of contaminated water and 500 tonnes of contaminated soil – he too has stressed that this is a rough estimation only.

Based on these figures though I can also give you a rough estimation of cost.

If we were to collect this amount of waste with the vehicles, equipment & personnel currently onsite then a rough estimation of this service/hire would be $160,000. Please note this does not include the treatment and disposal costs of the wastes mentioned.

As we progress on the job we will be able to provide a more accurate estimation of costs.

If you have any queries please either (sic) myself on 0419 870 077 or Toby Edmunds (Emergency Response Coordinator onsite) on 0428 927 827.

34 Mr Beere’s email attached a document addressed to Ms Carr with the heading “Emergency Response Rates – Grass Valley Formulators Fire”. The document said:

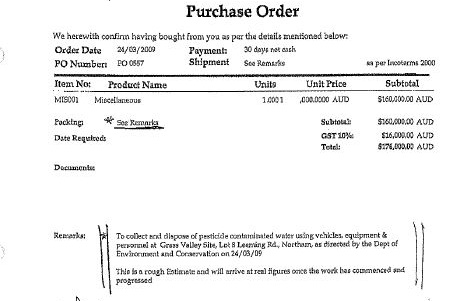

35 Ms Carr faxed a purchase order to Mr Beere. Ms Carr was in Victoria. The fax marking on the purchase order shows a time of “16:17”. I infer that the fax was sent at 4.17 pm Victorian time, or 2.17 pm Western Australian time. That timing seems to fit with Mr Beere’s earlier email which was sent to Ms Carr at 1.38 pm Western Australian time. The purchase order reads as follows:

36 Ms Carr says that she received the information for her wording of the “Remarks” section from the Toxfree representative she spoke to (Mr Beere) and obtained approval for the wording from Mr Haslberger.

37 Mr Beere says that the purchase order did not accurately reflect the conversation he had with Ms Carr because his estimate of $160,000 was exclusive of treatment or disposal costs. Despite this, he did not then draw that matter to Ms Carr’s attention. It may also be noted that the purchase order referred only to the removal of contaminated water, and not to the removal of contaminated soil or equipment.

38 Gerrard Styles was employed by Toxfree as its General Manager, Operations. On 24 March 2009, Mr Styles sent an email to Ms Carr at 3.37 pm Western Australian time:

Hi Betty

Thanks for forwarding your PO for the work to Errol and myself. Lynda has forwarded the credit application forms, so we look forward to their return.

I would like to confirm a few details for clarity, to avoid any confusion following the clean up operation.

• Toxfree will only deal direct with Grass Valley Formulators and their nominated holding companies/subsidiaries. Toxfree will not deal direct with Grass Valley Formulators Insurance company with regard to the Northam Incident. The order number is a contract between Grass Valley Formulators and Toxfree Solutions.

• Toxfree will determine the method of disposal for all arisings it collects from the Northam incident, and disposes of the material as quickly as possible to avoid hold up on its current operation.

• Toxfree has issued a quotation for estimated rates on quotation 8307-09 KW, issued to yourself today 24/03/09.

If you have any questions, please do not hesitate to contact me on the numbers below.

39 Mr Styles appears to have assumed that the contract encompassed disposal of the waste.

40 Tobias Edmunds was employed as an Emergency Response Manager by Toxfree. Mr Edmunds had received a phone call from Mr Raine of the DEC suggesting that Toxfree deploy staff and emergency response equipment to GVF’s site as he was concerned that waste could leak into the Avon River. Mr Edmunds says he arrived at the site at about 10 am on 24 March 2009 and liaised with Mr Haslberger. Mr Edmunds says that the purpose of his discussion with Mr Haslberger was to explain the emergency response services that Toxfree would be providing and the schedule of rates. They did not discuss disposal of the waste. Mr Edmunds says that Toxfree began providing its emergency response services immediately after that discussion, which suggests that the work started not long after 10 am. However, Mr Edmunds also says that Toxfree deployed its emergency response unit to GVF’s site upon receipt of the purchase order. Mr Edmunds seems to be mistaken as to the time the work was commenced. It appears that Toxfree had deployed its staff and equipment to the site in anticipation of the purchase order being provided, but the purchase order was not provided until 2.17 pm. The work must have commenced sometime after that.

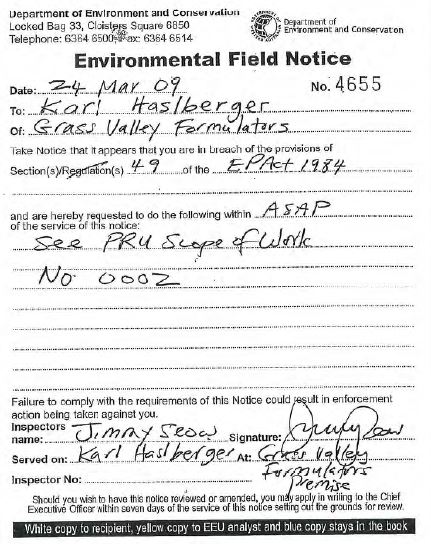

41 On the afternoon of 24 March, Mr Haslberger was handed documents headed “Environmental Field Notice” and “Pollution Response Unit Clean Up/Recovery Scope of Work” by Mr Raine of the DEC. Mr Edmunds was present when Mr Haslberger was given those documents. Earlier, Mr Raine had walked Mr Haslberger and Mr Edmunds through the site to point out what needed to be done in terms of the clean up and containment of waste. Mr Haslberger says that Toxfree “was left to continue with the clean up”, and “took over the clean up”, at about 4 pm. Mr Haslberger’s evidence suggests that the documents must have been handed to him shortly before that time.

42 The Environmental Field Notice stated:

43 The “Pollution Response Unit Clean Up/Recovery Scope of Work” document stated:

44 Mr Edmunds deposes that the job for GVF involved two defined stages: the emergency stage which commenced when the environmental field notice was issued and which finished once the site was cleared of all contaminated materials and the post-emergency stage, which covered the transport, storage and ultimate disposal of the contaminated material.

45 Mr Edmunds states that Toxfree’s emergency response services involved containing and collecting all of the contaminated material from the premises in accordance with the Environmental Field Notice from 24 March to 1 April 2009. It appears that the work on the first day consisted principally of securing leaking tanks and pumping the contaminated liquid from the pond into tanker trucks and transporting the liquid to Toxfree’s sites at Kwinana.

46 Mr Vaughan was in Queensland. He received a call on the morning of 24 March 2009 from Mr Haslberger telling him that GVF’s factory was on fire. Mr Vaughan arrived at the site that evening. He observed that by about 10.30 pm, about half the water had been removed from the pond and it appeared to him that there was no longer any risk of contaminated liquid flowing into the environment.

47 Mr Vaughan attended the GVF site each day until 31 March. He says that as a result of the fire there was no power to the site and no telephone or fax lines working. He says he had no access to any emails until he returned to Queensland on 1 April 2009.

48 Mr Styles says he telephoned Ms Carr on the day after the fire, Wednesday, 25 March 2009, to inform her that the value of the purchase order had almost been reached. He says he told Ms Carr that she should inform Mr Vaughan of this so that Mr Vaughan could advise Toxfree what he wanted Toxfree to do going forward. He says that Ms Carr responded with words to the effect that GVF would require Toxfree’s rates concerning the continuation of the services to determine the cost going forward. Mr Styles says Ms Carr also said that GVF would continue with the initial purchase order and she would consult Mr Vaughan. Mr Styles says that Ms Carr did not request that Toxfree cease providing the emergency response services.

49 Mr Styles states that Mr Vaughan had asked him if GVF could store the waste at Toxfree’s facility until GVF had determined if the liquid waste could be salvaged. He states that because of this request, he introduced a storage fee as Toxfree could not use its facilities for other clients while GVF’s wastes were stored. Mr Styles says that Toxfree stored the waste at its Kwinana and Port Headland facilities awaiting the results of analysis of the waste and further instructions from GVF. Mr Vaughan denies that he spoke to Mr Styles until 27 March 2009.

50 Mr Styles followed up his discussion with Ms Carr with an email to her, copied to Mr Vaughan, in the following terms:

Hi Betty

Further to our telephone conversation, I can confirm we are close to the original estimated PO of $ 160,000 + GST.

On your instruction we will continue to use the same PO (0557) and provide you with cost and operational updates.

We are currently freighting the liquid material to our Kwinana Operation, and will be charging storage at $0.0261 per litre, per day, until a decision is made of the fate of the material.

Additional charges to quote 8307-09KW will be made up as follows, please note this is purely an operational estimate at this stage.

• Additional PPE (Personal Protective Equipment) required for the ongoing operation EST only $ 300.00 per person (est. 8 personnel)per day

• Accomodation (sic), meals for all the team (est. 2 nights total) EST only $ 250 per person

• Lab analysis for disposal assessment – Est only $ 400.00

• Out of hours opening (including labour) for treatment plant opening, and transfer of existing products to make space. EST only $ 5480.00

• Decontamination of all plant and equipment post job, and disposal of all residues TBA

• Controlled Waste bulk liquid transfer of material transport (pocket road train configuration) to Kwinana ex. Northam EST $ 520.00 / hr

If you have any questions, please do not hesitate to contact myself on the numbers below. Please acknowledge your receipt of these charges.

51 GVF did not provide acknowledgement of the receipt of the new charges, despite the email seeking such acknowledgement.

52 It appears that Mr Styles had another conversation with Ms Carr later on 25 March 2009. He sent an email to various people within Toxfree referring to that conversation. That email reads:

Hi all

Just a brief update, spoke with Betty from Gulmohar (Grass Valley Formulators), they had received my email this morning detailing the extra charges for storage PPE etc. She had forwarded on to both directors and the Insurance Company. All parties want to proceed on the open PO (0557), and no comments have come back.

I will update you when more information becomes available.

53 Ms Carr disputes Mr Styles’ assertion that she said GVF would continue with the original purchase order. She says that Mr Styles said that Toxfree was close to the original estimate of $160,000 and would require a further purchase order for the additional work that was required. Ms Carr says she did not have the authority to authorise another purchase order, but said that Mr Styles should email her the details and she would forward the information to Mr Heyn and Mr Haslberger. She also denies that she agreed that the purchase order was to be an “open” purchase order. Ms Carr says that she understood the email to her of 25 March to mean that upon receiving GVF’s further instruction, Toxfree would use the same purchase order to provide any further work. She says her only role was to relay information between Toxfree and the directors of GVF. Mr Heyn was in Europe at that time, but she was in touch with him by email. Ms Carr forwarded Mr Styles’ email of 25 March to Mr Heyn shortly after she received it.

54 On 27 March 2009, Mr Styles and Mr Vaughan had a telephone conversation. Mr Styles says he told Mr Vaughan of the quantities of liquid and solid waste that had been removed from the site and the amounts that remained to be removed in the coming days. Mr Vaughan said that he would discuss this with Mr Heyn and they would review the figures. Mr Styles states that Mr Vaughan did not instruct him to not proceed with the work order or to cease doing work. He says that he explained to Mr Vaughan that the waste needed to go to Port Headland as this was where the liquid waste was to be disposed if it could not be salvaged. Toxfree’s Port Headland facility had the only industrial waste incinerator in Western Australia and was licensed for chemical incineration by the DEC. Mr Styles says Mr Vaughan told him that GVF would assess whether there were any other options available to it, but Mr Styles said there were no other options as there was no other licensed facility in Western Australia to store the waste.

55 Mr Styles sent Mr Vaughan a fax on 27 March. The fax states:

Further to our conversation today, I can confirm the following estimates of literage of pesticide contaminated material moved as of this evening;

• 250,000 litres (liquid, which will be transferred to Toxfree Solutions High Temperature facility in Port Hedland)

• Approx. 70 tonnes of pesticide contaminated soil which will be processed through TOxfree (sic) Solutions thermal desorption unit in Kwinana

After discussing with site there are an additional 60,000 litres to be transported from site tomorrow (liquid) and an additional 200 tonnes of contaminated soil.

Indications from site are that there is a certain amount of packaged waste in IBC’s to be pumped out and disposed of, and additional contaminated material for disposal.

As discussed, I will forward a copy of this email (faxed to Northam) to the DEC at your request.

After evaluation from both treatment plants, processing of the material will be at the following rates excluding GST and associated costs on the quote issued by Errol Beere

• Disposal only – Liquid (persicide(sic)/pesticide contaminated washwater (sic)- $ 3.14 per litre (Blending to Incineration specification and Incineration)

• Disposal only – pesticide contaminated soil - $ 1.62 per kg (thermal Desorption)

Work is being carried out against your original order (0557)

56 Mr Vaughan denies that Mr Styles had said during the conversation earlier that day that the waste would have to be disposed of by high temperature incineration or that the waste was being transported to Port Headland. Mr Vaughan says that Mr Styles said that the costs to date, including disposal, were in the vicinity of $1.6 million. Mr Vaughan says he requested an urgent meeting to discuss what Toxfree had done and how it had arrived at the figure. Mr Vaughan denies that he had agreed that Toxfree could carry out further work against GVF’s purchase order.

57 Mr Styles states that by 27 March 2009, the initial containment work had been completed in that Toxfree had averted the waste spilling in the Avon River and off-site, but there were still a number of issues listed in the DEC’s “Pollution Response Unit Clean Up/Recovery Scope of Work” document. He states that Toxfree had a skeleton staff on-site on 28 and 29 March 2009. Toxfree’s equipment was also on-site, and was charged to GVF.

58 Mr Edmunds recalls that on about 27 March 2009, Mr Vaughan asked him if Toxfree would store the following wastes at its storage facilities in Kwinana and Port Headland: 100,000 litres of liquids at Kwinana; 200,000 litres of liquids at Port Headland; and 200 tonnes of contaminated soil at Kwinana. Mr Edmunds understood that the split was based on Mr Styles’ fax of 27 March 2009. Mr Edmunds states that while he was on-site, Mr Vaughan instructed Toxfree to dispose of approximately 127 tonnes of contaminated soil removed from the GVF site. Mr Vaughan denies having such a discussion with Mr Edmunds. Mr Edmunds states that the solid waste that was held at Kwinana was disposed of within several months of Toxfree completing its services (ie by mid 2014).

59 On 30 March 2009, Mr Edmunds and Mr Styles met with Mr Vaughan and Mr Haslberger. Mr Styles said that the costs to date for the services were approximately $1.5 million for the emergency response services and the disposal costs. Mr Styles says that at the time of the meeting the most pressing issue still to be addressed was the disposal of the waste. He says that Mr Vaughan said he wanted Toxfree to provide him with the sequence of events for use by GVF’s insurer, QBE Insurance (Australia) Ltd (QBE). Mr Vaughan also said that Toxfree’s invoices would be covered by GVF’s insurance policy with QBE. Mr Vaughan discussed engaging an expert, Bruce Heath, and said that Mr Heath would analyse the waste to assess what options other than disposal of the waste might be available to GVF. Mr Styles said that was fine, but Toxfree was a waste disposal company and not a storage company and that storage rates would apply.

60 Mr Vaughan says that during that meeting Mr Styles said Toxfree would be issuing invoices which would detail how the costs were broken up. Mr Vaughan says he said he would not be able to receive the invoices because he had no email access. He said he could not understand how Toxfree could get to $1.6 million for the job. Mr Styles also said that now that the emergency was over, Toxfree would be going back to its regular rates.

61 On 31 March 2009, Mr Styles sent an email to Mr Vaughan, copied to Ms Carr, in the following terms:

Thanks for the courtesy extended to myself and Toby during our visit yesterday to discuss the progress with the clean up of the site following the fire last week. Please find a summary of the points raised, outcomes and actions going forward.

• The conditions of the Environmental Field Notice (EFN) issued by the Dept, of Environment and Conservation (DEC) will be completed by today (Tuesday) – conditions 2 & 3 are complete.

• The remainder of the contaminated soil will be removed by today to avoid any recontamination with rain filling up the containment dam. This will be verified by an Environmental Consultant (sampling today, results as soon as possible, by 3rd party laboratory), and further works (if any) will be identified.

• Copies of all non commercial documentation will be provided to DEC on Grass Valley Formulators request.

Insurances and financial liability

• Toxfree will provide a Sequence Of Events (SOE) to Grass Valley Formulators and DEC for Insurance and audit purposes

• Estimated total costs to date, attributable to Grass Valley Formulators are approximately $ 1,500,000 as of Monday 30th March. This includes labour, equipment and disposal costs.

• Samples of liquid will be made available to Grass Valley Formulators and their Insurance Company (QBE Insurance).

• The majority of the cost is the disposal of pesticide liquid residues currently approx. 100,000 L at Toxfree Solutions (Kwinana), the remainder approx. 200,000 L is at Toxfree Solutions Port Hedland Operation (OEC), where it was transferred due to capacity constraints at Toxfree (Kwinana). All liquid residues will be disposed of via High Temperature Incineration following blending.

• Contaminated Soil is currently stored at Toxfree (Kwinana) where it will be treated by thermal desorption.

• Total Invoice Value for the Emergency Response Component value for the work once complete will be in the region of $ 1,600,000

• Financial surety will be attained by submitting invoices as soon as possible, and detailing transport & labour components.

• Toxfree’s terms are standard 30 days

• In terms of cash flow, Toxfree will need prompt payment due to paying its labour up front for Emergency Response Work and disposal processing.

Other

• Toxfree to provide an up to date quote of all aspects top the cleanup aspect (non ER) of the operation

• All personnel included in the above email to be cc.d in all documentation

If you have any questions, please do not hesitate to contact myself or Toby

62 Mr Vaughan says that to the best of his recollection there was no discussion at the meeting on 30 March 2009 about transportation of waste to Port Hedland or Kwinana. He says he first became aware that waste had been transported to Port Hedland when he got email access on 2 April 2009. Ms Carr forwarded the email of 31 March 2009 to Mr Heyn.

63 On 31 March 2009, Toxfree provided invoice # 2318 to GVF. The invoice contained the heading “Description”. Under that heading, appeared the words:

Collection and disposal of pesticide contaminated water using Vehicles, equipment and Personnel at Grass Valley Site (Northam) as directed by the Department of Environment and Conservation on 24/03/09.

64 The invoice then set out a number of items of work for 24, 25, 26, 27, 28 and 29 March 2009. The invoice listed items of equipment or personnel, the number of hours charged for each item and the rate per hour. The rates were in accordance with Toxfree’s emergency response rates provided to Ms Carr on 24 March 2009. The invoice contained totals for each item for each day.

65 Although the invoice stated that it was for collection and disposal of pesticide contaminated water, this was wrong in two respects. Firstly, the invoice was in respect of the collection and removal of both solid waste and contaminated water. Second, the invoice was for collection and removal of waste, but not for its “disposal” (in the sense of its destruction).

66 The total amount of the invoice was $275,279.40 (incl GST). This exceeded the estimate of $160,000 (plus GST) by $99,279.40. Mr Beere states that the excess was accounted for by his underestimation of the time it would take for trucks to travel to and from Toxfree’s site at Kwinana. He says that additional time was required because GVF’s site only allowed one truck to enter or leave the site at a time, because a detour had to be taken to access a weighbridge which added an extra 30 minutes to each round trip and because it took longer to unload the waste at Toxfree’s Kwinana depot than it had estimated. There were also additional amounts for items which were first noted in Mr Styles’ email of 25 March 2009.

67 Toxfree sent a second invoice (# 2340) to GVF also dated 31 March 2009. Under the heading “Description”, the invoice referred to “Grass Valley Formulators Pesticide Spill. Disposal of”. The invoice included items for disposal of pesticide solutions and “wash waters” at $3.14 per litre, disposal of contaminated soil at $1,620 per tonne and transport costs from Kwinana to Port Headland by road train. The total of the invoice was $1,592,910.23.

68 Mr Edmunds states that by 1 April 2009, the emergency response services had been provided and emergency response rates no longer applied as the contaminated material had been removed and the premises no longer presented a pollution or combustion risk. He says that after 1 April 2009, Toxfree continued to provide services to GVF related to the DEC requirement that GVF provide a “section 72” closeout report. This was part of the work set out in the Pollution Response document. Preparation of that report required analysis of samples of liquid and soil removed from GVF’s site.

69 On 2 April 2009, Mr Edmunds provided a quotation for analysis of the material collected from the GVF site and a report. The amount quoted for analysis was $39,988 and the amount for the report was $950. Toxfree indicated that it would need a purchase order. On 9 April 2009, GVF provided a purchase order for these services.

70 On 2 April 2009, Mr Vaughan sent an email to Mr Edmunds stating:

Hi Toby, Sorry I have not been in touch since our meeting, I have had to return to Qld early yesterday to attend a family emergency. At this stage I will be remaining in Qld in the short term.

Thanks to both you and Ged on Monday for you (sic) time. As I mentioned to you both then, both Company Directors and our Insurers are seeking clarification on quite a number of issues. I am still awaiting your clarification of costs with our first and main issue being the vast difference between your original quote of $160,000 to remove the approx 300k Literage of contaminated water in question as well as 500 tonnes soil. The estimates of quantities to be removed that were given for you to quote on were surprisingly accurate (in particular the liquids) at the time. I do not believe the contaminated soil was anywhere near 500 tonnes, however we have not yet been advised final quantities. The second main issue as we discussed is the cost of disposal. I understand that you have been requested to supply a copy of analysis results by Bruce Heath of Chemical Consulting Services. I also understand to date he has not received analysis results. Can you please forward as soon as possible so that we can progress this matter forward.

71 In Mr Vaughan’s email, he disputed both invoices that Toxfree had sent. By then, GVF had retained Mr Heath of Chemical Consulting Services Pty Ltd to help and advise with regard to Toxfree’s fees and work.

72 On 4 April 2009, Mr Styles wrote to Mr Vaughan as follows:

Hi Geoff

Toby has forwarded me a copy of your request for clarification following our meeting last week, I hope your family emergency has been resolved.

Please find the following information for yourself and Insurance company;

• Costing, this has been provided out in the split quotes Toby has issued, as detailed as possible covering equipment, labour, tank rental and waste disposal.

• The PO issued (0557) on the 24th was a rough estimate (as detailed in the remarks section) primarily to cover Emergency Response, Equipment and labour, this PO was issued prior to determination of what disposal route the material had to be processed by.

• Liquid estimates are reasonably accurate (I think there is approx 350 k of washings/product etc.) and soils in the vicinity of 200 te(sic), final quantities will be advised.

• The majority of the bulk liquids are at our Port Hedland facility awaiting disposal via incineration. The contaminated soils and packaging remain at our Kwinana operation for thermal desorption.

• I have discussed with Bruce Heath of Chemical Consulting Services, and analysis is being provided as quickly as possible, I have advised Bruce verbally our storage tanks and transport are for waste products.

I hope this answers your queries to date, myself, Toby and Steve Gostlow (MD) are in Melbourne (Mt. Waverley) on Monday and Tuesday. If you require us to meet at your Ricketts Road office, we would be happy to do so.

Please do not hesitate to contact me if you have any questions

73 Mr Vaughan responded by email on 6 April 2009 saying:

In regards to disposal we have requested that liquid and solid waste be held for the time being until independent party (Chemical Consulting Services) can have a look at the analysis from which you determined your disposal costs. You have mentioned that you were arranging. I would have thought this was readily available as you have already determined what the disposal costs would be, based I assume upon this analysis.

74 On 7 April 2009, Mr Styles attended a meeting with Mr Heyn and Mr Vaughan to address GVF’s concerns with the invoices and explain how the costs in the invoices were calculated. Mr Heyn referred to the lower pricing for the job that Toxfree was involved in 2007. Mr Styles said that this was a different job with a different set of circumstances, that a price had been set and Toxfree was not going to move on the issue and that there would not be any further negotiation on the cost of disposal.

75 On 9 April, Mr Styles sent an email saying that GVF and Mr Heath would be provided with the basis for Toxfree’s costings for disposal and the chemical analysis, once received.

76 Mr Vaughan sent an email to Mr Styles on 15 April 2009. In that email Mr Vaughan said:

I have arranged to forward your invoices direct to our insurer, who will no doubt have numerous questions for you regarding your account. I am trying to organize a meeting possibly next week for both our assessor and ourselves to meet with you and work through some of these questions and discuss your accounts on a line by line basis. As soon as I hear back from our assessor, I will contact you to organize.

The matter regarding disposal costs has already been raised with you in a meeting with Peter Heyn last week. I note, we still have not seen any communication as to what basis you have arrived at your costing nor the analysis used to arrive at this figure. As we have indicated and have provided written evidence to you, there is a big difference in what we have paid you in the past (70c per Litre for incineration at Port Headland (your invoice 27956) and $3.14 per litre you now seek. The transport and disposal method is the same however the difference in the account would be in the vicinity of $886k approx. As you will appreciate, this huge difference is of extreme concern to GVF and its insurers.

In regard to your account for expenses (invoice 2318), again, there are a lot of questions being asked by GVF Directors and its insurers as to how the invoice amount has been arrived at. As we have mentioned before your estimate for removal was $160k (our purchase order based upon this) and yet we have an invoice tendered for $250k approx. How can this estimate be so far out?

77 Mr Vaughan’s email went on to question what he saw as excessive amounts in invoice # 2318, such as the cost of $27,250 plus GST for hire of a trailer and 4WD.

78 On 15 April 2009, Neil Armstrong of Toxfree responded by email, saying that Mr Styles was on annual leave, but that Mr Armstrong would look into Mr Vaughan’s queries and respond as soon as possible. Mr Armstrong also said that he would forward the analytical results once received. The results had in fact been received by Toxfree on 9 April 2009. The results were not provided to GVF until 24 April 2009.

79 There is in evidence an email sent by Mr Armstrong to Mr Styles and others within Toxfree on 23 April 2009 saying:

Please review attachment response to last weeks email and provide comment.

Note: I have not provided analysis results to the client as yet but shall send onwards tonight – results showed much lower contamination levels than expected.

Disposal rate suggested is based on revised contaminant levels and current incineration rates charged to Nufarm and others. Market rate unknown Geocyle tentative $1.80/1 and WRR? (No quote as yet)

Meeting scheduled 2pm tomorrow please confirm attendance.

80 The attachment provided a detailed response to Mr Vaughan’s email of 15 April. It is not entirely clear, but the attachment may have been sent to Mr Vaughan at some later stage.

81 On 24 April, Mr Vaughan attended a meeting with Mr Armstrong, Mr Edmunds, Mr Beere and Steve Gostlow of Toxfree. Mr Vaughan’s note of the meeting is as follows:

…

…

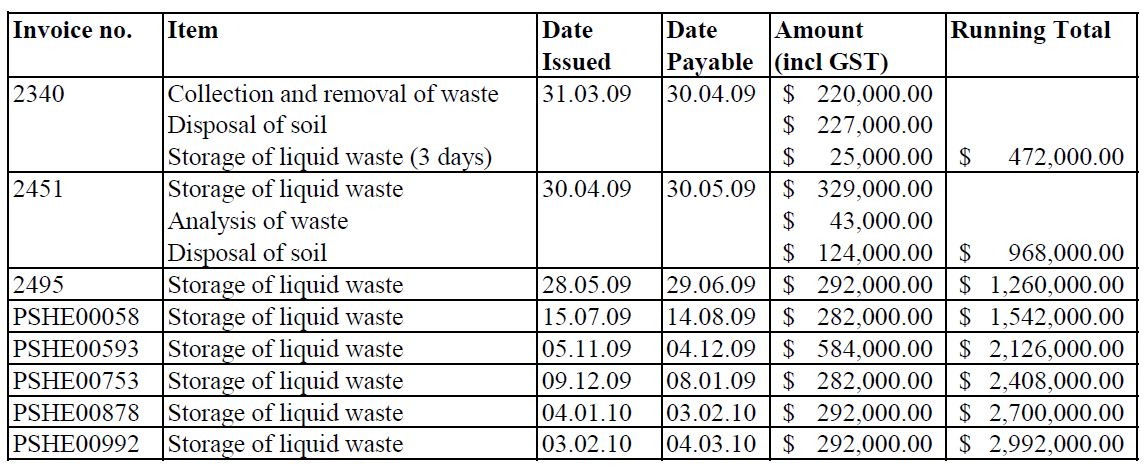

82 On 30 April 2009, Toxfree provided GVF with an invoice # 00002451 in the amount of $738,433.58 including GST. That consisted of $39,988 for the analysis of samples, $77,500 for the transport of waste to Port Headland, with almost all of the remainder consisting of storage costs for the solid and liquid waste material.

83 On 15 May, Mr Vaughan sent an email to Toxfree in the following terms:

I have just earlier this week received your invoice 2451 dated 30 April 2009 and must say GVF are very disappointed in the way Tox free is handling this storage/disposal of waste water. In particular we must question your invoice detailing $300k approx for storage of waste.

A point of contention from day one way has been getting an analysis of the waste water to determine what it consists of and sourcing the best/ cheapest method of disposal. Our reasoning, the less contaminated, the cheaper the disposal costs.

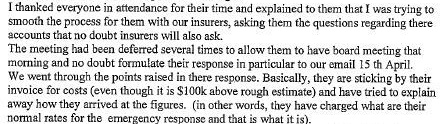

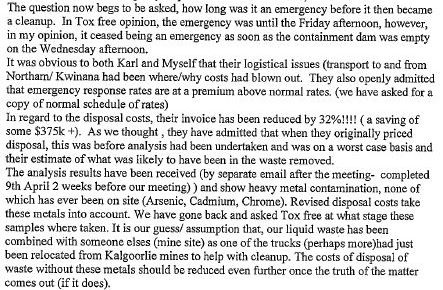

It was not until after our meeting.(sic) 24 April that we finally got a copy of the analysis report dated 9th April 2009 and that Toxfree kindly offered a reduction in the disposal costs by 32%. (Little did we realize at the time that the reduction in costs offered by Tox free had been quickly overtaken in storage costs).

84 On 22 May 2009, Toxfree issued an amended invoice # 2340A, which lowered the rate for disposal of liquid waste to $2.12 per litre, so that the total was $1,185,287.63.

85 On 28 May 2009, Toxfree issued invoice # 2495 to GVF for storage costs (described as “Tank and DG pad rental”) from 4 May 2009 to 1 June 2009 in an amount of $363,800.28 including GST.

86 In June 2009, Mr Vaughan set an email to Mr Armstrong of Toxfree saying:

As a result of the above, as soon as our insurer’s decision is known, Grass Valley management have some serious decisions which need to be taken, especially if there is a shortfall in what insurance are prepared to pay towards Toxfree claimed costs. Obviously, the ongoing viability of Grass Valley must also be taken into account if we are unable to replace equipment loss. We must also comply with current company law legislation.

87 On 11 June 2009, Mr Vaughan wrote to Mr Armstrong and Mr Styles saying:

Ged mentioned in an earlier meeting that storage costs had been applied in an effort to get us to decide on course of action a lot sooner. Whilst I can appreciate it is in everyone’s interest to get this matter finalized, you must understand that, from the very 1st days of cleanup, we have advised you that your costs will be a matter for our insurance company and our assessor could not enter into the discussions until fire investigation had been completed. I do not believe unrealistic invoicing (Storage in particular) is in anyones best interest in having this matter resolved quickly. The delay being encountered is outside GVF control whilst insurance claim progresses.

88 On 29 May 2009, GVF received a report from Bruce Heath. Mr Heath advised, inter alia, that the storage charges were unreasonable, that GVF had good cause to refuse to pay more than $0.70 per litre for disposal and that GVF should consider alternative methods of disposal.

89 On 15 July 2009, Toxfree issued a further invoice # PSHE00058 to GVF for storage of liquid waste in an amount of $352,064.79 for the period from 1 June 2009 to 30 June 2009.

90 On 15 January 2010, Toxfree commenced proceedings against GVF in the Supreme Court of Western Australia. The Statement of Claim alleged that GVF was indebted to Toxfree in the amount of $2,914,865.68. On 5 February 2010, GVF filed a Defence, Set-Off and Counterclaim. The counterclaim was based on the allegation that Toxfree had further contaminated the liquid waste with heavy metals, causing GVF unspecified loss and damage. It may be noted that in this proceeding, the plaintiffs do not dispute that the liquid waste was contaminated as a result of the presence of heavy metals in some of the tankers used by Toxfree. The tankers had not been cleaned before they were sent to the GVF job.

91 On 28 July 2010, Toxfree’s lawyers wrote to GVF’s lawyers, asking that GVF collect the waste stored at Toxfree’s facilities. It was not collected.

92 In the end, GVF provided no authorisation for Toxfree to proceed with the disposal of the liquid waste collected from the site and stored at Toxfree’s Port Headland facility. Neither did GVF provide any instructions for the return of the waste or its transfer elsewhere.

93 In late 2014, Toxfree transported the liquid waste from its Port Headland facility to Laverton in Victoria to allow it to make other use of its storage capacity. Approximately 363,000 litres of liquid was stored at Laverton. Between January and March 2015, the liquid waste was disposed of by high temperature incineration by Toxfree’s competitor, Geocycle. Mr Edmunds states that the costs incurred by Toxfree associated with the disposal of the liquid waste, not including any profit margin, were approximately $750,000. This consisted of $250,000 for transportation costs of the liquid waste from Port Headland to Laverton and $500,000 to incinerate the liquid waste.

EVIDENCE CONCERNING OTHER EVENTS

94 Mr Vaughan deposes that GVF was able to recommence trading within about a month after the fire occurred. It operated with one tank, whereas it would normally have six or seven tanks operating at the same time. GVF was able to progressively get other tanks operational over the following months, but its manufacturing capacity remained limited. There were delays in having the factory repaired because the owner of the property, Hamcor, delayed in paying its insurance excess. There were subsequent problems with defective work done by Hamcor’s builder. The factory was not fully reinstated until early 2010. Mr Heyn’s evidence is to similar effect.

95 GVF lost sales as a result of the fire because it was unable to meet orders. Mr Vaughan states that the company found itself with a huge inventory, but limited capacity to fill its orders. Mr Heyn also states that GVF had earlier stocked up in anticipation of a busy period, so the timing of the fire could not have been worse.

96 Mr Vaughan states that GVF paid all its debts, other than the disputed invoices from Toxfree and some of the rent claimed by Hamcor. He says that in order to ensure that it remained solvent, GVF scaled down its production levels and related expenses. Mr Heyn says that casual staff were laid off.

97 GVF received an initial payment of $199,000 from its insurer, QBE, on 27 July 2009. By that time QBE had accepted liability for the claim, but had not determined the quantum of the amount it was required to pay out. GVF received a second payment of $68,481.81 on 1 September 2009. On 27 November 2009, QBE and GVF signed a deed of release, settling the insurance claim. GVF received a final payment of $1,281,518.10 from the insurer on 2 December 2009. The amounts received from the insurer totalled approximately $1,549,000. These amounts were paid in respect of the Toxfree invoices and other costs resulting from the fire.

98 By July 2009, the invoices rendered by Toxfree had increased to approximately $2,900,000. Mr Vaughan says that GVF had delayed in posting those invoices into its MYOB accounting software because of the dispute and because it was hoped that the dispute could be settled. In July 2009, the full amount of Toxfree’s invoices was included in GVF’s accounts. This allowed GVF to claim a GST input credit based on the full amount. GVF received $264,988 for the GST input credit on 22 September 2009.

99 There were negotiations between GVF and the solicitors for Toxfree for settlement of the dispute. On 30 July 2009, GVF offered to settle by paying $850,000. Toxfree offered to settle for $1,600,000. GVF made a final offer on 25 August 2009 to pay $1,050,000 which was rejected. Mr Vaughan states that the offer was certainly not an admission that GVF owed Toxfree that amount of money. He says that the way Toxfree had conducted itself, including charging GVF about $300,000 per month for storage, was unconscionable. Mr Heyn states that he considered the Toxfree claim to be “unwinnable” (ie Toxfree could not win). Mr Heyn said the advice from GVF’s lawyers, Mason Siers Turnbull (MST Lawyers) was that GVF “had good prospects to defend the Tox Free Proceedings and also to pursue the counterclaim.”

100 Mr Vaughan says that in late 2009, following a discussion with Mr Heyn, he approached Graham Bendeich, whom he knew to be a insolvency practitioner, to obtain specialist advice. Mr Bendeich is a consultant to the firm Pearce & Heers. The first plaintiff, Mr Pearce, is a partner in that firm.

101 Mr Vaughan met with Mr Bendeich on 13 November 2009. They discussed a number of issues concerning Toxfree’s claims, GVF’s dispute with Hamcor and the proceeds of the insurance claim. Mr Vaughan asked whether the insurance proceeds had to be utilised for Toxfree’s claim, or whether the proceeds could be used to pay out GVF’s secured creditors and free up cash flow. He says that Mr Bendeich said that GVF could use the money for whatever business purposes were required and that payout of the loans would not be an issue. Mr Vaughan says that he asked about payment of Gulmohar’s loans or accounts. He says that Mr Bendeich told him that Gulmohar was entitled to be paid for its services or goods, being a major supplier to the company and a secured creditor, provided these had been supplied during the normal course of business.

102 Mr Bendeich gave evidence concerning his discussion with Mr Vaughan on 13 November 2009. He contemporaneously prepared a diary note of that discussion. Mr Vaughan vigorously contests a number of aspects of Mr Bendeich’s account of the discussion. Although there is inaccuracy in some aspects of Mr Bendeich’s diary note, where their recollections differ, I generally prefer the evidence of Mr Bendeich. That said, I do not think that there is any significant difference in their recollections of the important parts of the discussion.

103 I accept that Mr Vaughan told Mr Bendeich that GVF disputed Toxfree’s claim and that he considered the claims were excessive and unjustified. Mr Vaughan told Mr Bendeich he believed GVF was solvent and would be able to continue, but this was something that might change depending on how future matters panned out, including GVF’s dispute with Toxfree. Mr Vaughan requested advice from Mr Bendeich as to whether there were any difficulties or problems with paying the insurance proceeds to secured creditors. Mr Bendeich said that the directors of GVF had the ability to decide how to use the insurance proceeds, but if there was a liquidation further down the track, the payments were likely to come under the scrutiny of a liquidator if GVF was insolvent. Mr Bendeich also informed Mr Vaughan that in the event of an insolvency appointment, the charge in favour of Gulmohar was likely to be subject to scrutiny and might be vulnerable, given its recent creation.

104 GVF consulted MST Lawyers on 26 November 2009. In a file note, Mark Skermer of MST Lawyers, recorded that:

I met with Peter Heyn and Geoff Vaughan on Thursday 26 November and we proceeded to have a discussion with respect to the following matters:

1. QBE release;

2. Defending the Toxfree litigation; and

3. Corporate options and potential consequences.

I will address these in turn:

…

Corporate advice

I gave the client general corporate advice with respect to receiverships and liquidation without giving any advice as to whether they should engage either process at this point in time.

I advised the client that they needed to take extreme care in avoiding insolvent trading and preference payments. The client and I discussed this in detail and I supplied the client with an indepth knowledge of how the processes worked and what the client should do to avoid these sorts of claims.

I also advised the client that in the event that it wished to sell its plant and equipment, valuations should be obtained (minimum of 2 maximum of 3) before such items were sold and that a book valuation was not appropriate in this case.

I was instructed by the client to proceed and defend the Toxfree litigation.

…

105 Mr Vaughan states that he and Mr Heyn decided to clear GVF’s debts to its secured creditors and thereby free up the company’s cash flow. Their intention was to allow GVF to trade through the difficult period in anticipation of having a really good season in 2010. He says that GVF’s business was seasonal in nature and that the peak season was from March to July, August or September each year. After GVF received the insurance proceeds on 2 December 2010, it paid out its loan from Westpac Bank and an overdraft from ANZ and reduced some of its liability to Gulmohar. Mr Vaughan says that this improved GVF’s monthly cash flow by $15,155.

106 Mr Vaughan says he had seen a report in September 2009 which said that Australia’s wheat crop was expected to reach its highest levels in four years. It contributed to his belief that GVF would have a successful 2010 and to the decision to use the insurance proceeds to pay the secured creditors. However, a drought occurred in 2010, which affected GVF’s sales. The effects were felt from about February or March 2010. Orders slowed down and this had a detrimental impact on sales, which had become worse by the end of 2010, when the decision was made to liquidate the company. There is evidence supporting Mr Vaughan’s statement that the wheat-belt area of Western Australia was drought-affected in 2010.

107 On 15 January 2010, Mr Vaughan sent an email using his grassvalley.com.au email address, and describing himself as a director of GVF, to Darren Sommers of MST Lawyers. Mr Heyn was copied into the email. The email said:

At present time, GVF is trading minimally however with litigation that Mark is handling for us, in all probability the company will be liquidated as insurance settlement was insufficient to cover exorbitant and disputed clean up costs. As and when this happens is yet to be decided and open to advice.

GVF has been using the insurance funds received from QBE to replace damaged P & E destroyed in the fire as well as clearing majority of secured creditors/private loans.

With the company in its current form and unlikely to continue trading for the longer term, we have been having plant and equipment valued as well as the real estate which we currently rent.

…

Questions I have are as follows:

1. Directors Peter Heyn and myself are looking at buying (in some form of trading entity) P & E from GVF. The valuations are being done on market and forced (auction) value. With the transaction not being at arms’ length as such, can we purchase the P & E at auction value? The valuation advises that if goods are taken from site, the amount realised will be even further reduced. Concern is a challenge by liquidator, especially if we have Toxfree in the background getting most proceeds. My thought is that we are able to sell the assets, it is just the price paid which can be argued. Am I correct?

…

Intention was originally for Peter (secured creditor) to appoint a Receiver/Manager (all prior charges have been paid out) however if GVF can do the sale and renegotiate lease, we could probably just appoint administrator after the event to wind the company up and deal with the remaining creditor (Toxfree). Is this appropriate.

108 Mr Vaughan’s evidence is that he was not seeking advice on behalf of GVF, but was instead seeking advice for Mr Heyn and himself in their personal capacities.

109 On 26 July 2010, MST Lawyers provided a letter of advice in relation to GVF’s prospects of success in the proceeding in the Supreme Court of Western Australia. The letter of advice noted that Toxfree had claimed $2,914,865.68 for breach of contract plus interests and costs. MST Lawyers expressed the view that GVF was “in a strong position”. The letter said GVF’s argument that Toxfree was entitled to only $176,000 under the contract would probably fail, but that GVF was expected to have success “in reducing the quantum”, contingent upon obtaining experts’ reports. The letter said that one component of the counter-claim was based upon Toxfree depositing heavy metals on GVF’s property and advised that this aspect of the counter-claim was strong (although, it may be noted, such a case was never pleaded). The letter said that the second component of the counter-claim that Toxfree had made misleading representations concerning the cost and breadth of its services - would probably fail. MST Lawyers advised that GVF was expected to have “considerable success” in relation to reducing the quantum of Toxfree’s claim and that at least one component of the counter-claim was likely to have the effect of further reducing the amount payable to Toxfree. The letter also noted that the legal fees incurred by GVF to MST Lawyers to date were $65,427.68. MST Lawyers’ estimate of costs for the further conduct of the litigation, including a five to ten day trial, was in the order of $230,000.

110 Mr Heyn states that after receiving the advice from MST Lawyers, he and Mr Vaughan discussed the future of GVF. Mr Heyn states:

It was shortly after the time we received the MST Lawyer’s Advice that Geoff and me started to discuss whether we continue with the Tox Free Proceedings and with the Company. The MST Lawyer’s Advice pointed out the enormous cost of taking the Tox Free Proceedings all the way to a Court trial. Apart from the chances of winning or losing the shear (sic) amount of money involved in just getting the Company to a Court trial was more or less a main reason why the decision was made to liquidate the Company. The solvency of the Company didn’t even cross my mind because it continued to pay all its debts (excluding of course the disputed and unjustifiable Tox Free invoices), the decision to liquidate the Company was purely a commercial decision primarily based on the fact that the Company would have to raise the funds to litigate because it could not have raised sufficient funds just from its own trading.

111 Mr Vaughan and Mr Heyn say they made a decision to wind down the business, clear the debts (other than the disputed debts), pay all taxes that were due, pay all the staff entitlements, terminate the employment of its remaining staff and apply for an order to wind up the company.

112 On 27 October 2010, Mr Vaughan met with Mr Bendeich and Mr Pearce. Mr Vaughan told them that the directors had formed the view that it was no longer viable for GVF to continue and that they had decided to cease operating GVF’s business. They discussed the main issues involved in the likely liquidation of GVF. On 29 October 2010, Mr Vaughan sent an email to Mr Bendeich saying that he had spoken to his lawyers and that the directors had decided to make an application to wind up GVF.

113 On 15 November 2010, Gregg Lawyers, acting on behalf of GVF, filed an application seeking orders the company be wound up in insolvency. The application was accompanied by an affidavit of Mr Vaughan sworn on 15 November 2010 in which he deposed that GVF could not afford to continue with the litigation with Toxfree. He said that the directors had formed the view that it was not viable for the company to continue trading or to continue with the Toxfree litigation. He deposed that the company was “unable to meet its debts”.

114 Mr Vaughan’s affidavit of 15 November 2010 annexed a document in which he provided his assessment of the Toxfree debt:

My thoughts on whole matter and what Tox free are owed based on Tox free previous costing

Clean up cost (equipment) say $300k (this is without questioning account should be closed to $200k)

Liquid disposal $1.0 per liter) $375k. Nearly 50% than previously charged.

Solid disposal $1620 per tonne 319k without questioning cost.

Close to $1.0M or up. In my opinion this is more than generous.

We capped an offer to Tox at $1.050M in order to allow us to remedy the site allowing up to $200k to do so. With the $270k already paid by insurance this bought us to close to policy cap.

115 In this proceeding, Mr Vaughan deposes that the decision to liquidate GVF was not made on the basis that the company was insolvent. He says that GVF was “very solvent” in that it had paid all its debts except for the “unreasonable and unjustifiable claims” by Toxfree and, to a lesser extent, part of the rent claimed by Hamcor. Mr Vaughan says that he was concerned with how “we were going to continue the Company” and deal with the Toxfree proceedings. He understood MST Lawyers to have advised that GVF was going to be held liable for some amount, but it was a question of how much. He says he considered the Toxfree proceedings to be “vindictive” and he was concerned that the costs that would actually be incurred would be greater than the estimate. He says that if the drought were to persist through to 2011 and beyond, GVF was going to end up with bigger problems and most likely become insolvent. Mr Vaughan says that he and Mr Heyn had a discussion in early August 2010 with regard to how long GVF should continue to litigate with Toxfree and the utility of the company continuing to trade while the proceedings remain unresolved.

116 After GVF went into liquidation, Hamcor commenced proceedings against Mr Vaughan and Mr Heyn as guarantors of GVF’s lease. Those proceedings were settled out of court in 2011.

117 The plaintiffs called four current or former employees of Toxfree to give evidence. These were Mr Styles, Mr Beere, Mr Edmunds and Dr Morton. In assessing the reliability of those witnesses’ evidence, it is appropriate to consider them as a group. That is because all of them seemed anxious to justify Toxfree’s conduct and charges and, in addition, they were shown each other’s affidavits before they swore or affirmed their own affidavits. The fact that they were shown each other’s affidavits gives me cause for concern as to extent to which they were influenced by each other’s evidence.

118 Further, there is some evidence consistent with an overzealous desire amongst Toxfree’s employees to maximize its revenue from the GVF emergency. For example, Dr Morton sent an email to Mr Styles and Mr Edmunds on 26 March 2009 saying:

Men, I have just seen photos of the fire site from Rick…

Any chance we could make the argument to take the whole structure away?...burnt, pesticide affected steel…??????

119 In an email dated 24 March 2009 to Mr Beere and others, Mr Styles said:

Individual semi’s are fine, we’ll just charge more for transport, so good work, get all the gear out!

120 Further, despite Mr Beere saying that Toxfree could not provide a price for disposal of waste, until it had been analysed, Mr Styles proceeded to impose a price of $3.14 per litre for disposal of the liquid. At that stage, Toxfree provided no explanation to GVF as to how that rate was arrived at. Mr Armstrong of Toxfree prepared a document for internal use responding to questions raised by GVF, saying that the rate of $3.14 per litre “was to represent a worst case scenario in order to give GVF immediate estimates of disposal costs”. However, the rate of $3.14 per litre was never presented to GVF as an estimate or as a worst case scenario – it was the invoiced price. On 7 April 2009, Mr Styles said that Toxfree would not negotiate on the cost of disposal, but, on 24 April 2009, reduced the price to $2.12 per litre. In my view, GVF’s action in charging the “worst case” rate reflected an element of what Mr Vaughan described as “price gouging”. Toxfree’s inconsistent conduct contributed significantly to the ensuing dispute between the parties.

121 Having regard to these matters, I approach the evidence of the Toxfree witnesses with caution. That said, many aspects of their evidence were supported by emails or faxes sent shortly after relevant conversations.

122 It is understandable that Mr Vaughan and Mr Heyn were shocked by the invoices delivered on 31 March 2009, which totalled nearly $1,600,000. Their outrage and anger at Toxfree’s conduct is also understandable. That outrage and anger remained apparent when they were giving evidence. However, it is also clear that Toxfree was entitled to the payment of a substantial amount for work it did.

123 There are a number of aspects of the evidence of Mr Vaughan and Mr Heyn which I found to be inconsistent or implausible. I will give only a few examples for the moment.

124 In Mr Vaughan’s affidavit of 15 November 2010 in support of the application to wind up GVF, he swore that the company was “unable to meet its debts”. In contrast, in this proceeding, he swore that the decision to liquidate GVF was “not a decision, in my mind, that was made because the Company was insolvent” and that GVF was “very solvent”. Under cross-examination, Mr Vaughan initially appeared to blame the solicitor who prepared the affidavit filed in the Supreme Court of Queensland. He accepted that there was conflict between his affidavits. This conflict reflects what I consider was a tendency for Mr Vaughan to adapt his evidence to suit his present purpose.

125 Mr Vaughan and Mr Heyn defended proceedings brought against them by Hamcor in the District Court of Queensland for non-payment of rent on the basis that, following the fire, the premises “could not be occupied or used.” Mr Vaughan accepted the Hamcor defence was consistent with the instructions he had given. Inconsistently, he swore in this proceeding that within a month after the fire, GVF was able to produce pesticides, although in a limited capacity. It seemed to me that Mr Vaughan’s instructions in the Hamcor litigation were adapted to suit his extant purpose.

126 I thought that Mr Vaughan’s evidence in his affidavits and under cross-examination was evasive at times. For example, Mr Styles sent Mr Vaughan a fax on 27 March 2009 and, rather than acknowledging that it was received, Mr Vaughan merely deposed he had not seen it on that day. Under cross-examination, Mr Vaughan initially failed to accept that he had a Superway email account in 2009, before later acknowledging that he did. His answers under cross-examination were frequently unresponsive, leaving the impression that he was trying to avoid giving direct answers when confronted with difficult questions.

127 I also have substantial doubts about the reliability of Mr Heyn’s evidence. He was cross-examined about the defence in the Hamcor proceedings which alleged that GVF’s premises were unfit for occupation and use from the date of the fire until the termination of the lease on 17 November 2010. He said that the allegations in the defence were true and correct. In this proceeding, Mr Heyn’s evidence was that GVF was able to return to trading at full capacity at the start of 2010. Mr Heyn did not accept that there was an inconsistency, when there clearly was.

128 Mr Heyn was cross-examined about a consultation with Mr Skermer of MST Lawyers on 26 November 2009. Mr Heyn insisted that he could not recall discussing the issue of liquidation. He accepted the accuracy of Mr Skermer’s file note, but said that if receivership and liquidation was discussed “it must have been a sideline, otherwise I would recollect it”. He accepted that Mr Skermer would not have just volunteered advice. Mr Skermer’s file note shows that advice about receiverships and insolvency was not merely given as a “sideline”, but was a central part of the discussion. The file note shows that Mr Skermer gave advice with respect to receivership and liquidation, advised “in detail” that they needed to take care in avoiding insolvent trading and preference payments and gave advice as to the proposed sale of GVF’s plant and equipment in light of possible receivership and insolvency. It is implausible that Mr Heyn would have no recollection of discussing receivership and liquidation. Further, in this context, Mr Heyn’s statement in his affidavit of 23 October 2014 that the solvency of the company “didn’t even cross my mind” is implausible.

129 In his affidavit of 27 November 2015, Mr Heyn refers to his discussion with Mr Vaughan about getting advice from Mr Bendeich. He said that they wanted to ensure that they were acting appropriately as company directors and wanted to get advice from “someone who specialised in advising companies in difficult circumstances”. Under cross-examination, he denied that he was referring to companies experiencing financial difficulty. He said that he was instead referring to a company facing an exorbitant claim and being sued by Toxfree and difficulties with builders. But that is implausible since GVF was already receiving legal advice about the Toxfree debt and litigation, and Mr Bendeich is a liquidator. It is implausible that the “difficult circumstances” Mr Heyn was referring to were not financial difficulties.

130 My views as to the unreliability or implausibility of these aspects of Mr Vaughan’s and Mr Heyn’s evidence colour the approach I take to the remainder of their evidence.

131 Gulmohar supplied stock to GVF from time to time. Mr Heyn says he received advice from an accountant in 2008 to obtain a mortgage debenture to secure Gulmohar’s interest in the stock it was supplying, but which had not been paid for. Mr Heyn deposes that Mr Vaughan and Mr Armstrong agreed in 2008 that GVF would provide security by way of a mortgage debenture, but that it took some time for the documents to be prepared and signed.

132 On 4 May 2009, Mr Heyn wrote on behalf of Gulmohar to Mr Vaughan, in his capacity as a director of GVF, saying:

Please refer to the discussion we have had over the last week regarding the outstanding payments of Grass Valley to Gulmohar.

Gulmohar is owed approx. $800k by Grass Valley and for us to be able to provide ongoing support we require security towards the loans given to Grass Valley in the form of a mortgage debenture.

Could you please confirm this will be in order and I will arrange for necessary documentation to be forwarded.

133 The minutes of a meeting of Mr Vaughan and Mr Heyn, as GVF’s directors dated 22 May 2009 record the following:

Letter from Gulmohar Pty Ltd (“Gulmohar”) 4th May 2009 refers. Gulmohar has over the past few years provided financial support to the company in providing extended terms. They are owed in the vicinity of $800k and have requested that, for them to continue ongoing support in the same manner that we provide mortgage Debenture as security.

…

In order to secure Gulmohar’s ongoing support Directors have agreed to execute mortgage debenture documentation as requested by Gulmohar.

134 On 22 May 2009, GVF executed a Deed of Charge in favour of Gulmohar over GVF’s assets securing $800,000 plus interest plus any further advances.

135 Mr Vaughan says that GVF gave Gulmohar a mortgage debenture shortly after he and Mr Armstrong had agreed to it. He says that it was a mere coincidence that by the time the paperwork was in order, the fire had occurred in March 2009.

136 GVF’s financial statements and its MYOB accounting records record a number of debts owed to GVF’s related entities.

137 At the time of the fire on 24 March 2009, GVF owed Gulmohar $637,892.17 for the supply of stock on credit. After the fire, GVF’s accounts showed purchases from Gulmohar which totalled $957,546.39. GVF made payments to Gulmohar of $1,356,999.47. At the date of liquidation the amount owed to Gulmohar was $238,439.09. After the date of the fire the debt to Gulmohar was reduced by $399,453.08.

138 The payments made by GVF to Gulmohar were as follows:

Date | Amount |

1 May 2009 | $ 50,000.00 |

9 July 2009 | $ 100,000.00 |

16 July 2009 | $ 100,000.00 |

17 August 2009 | $ 30,000.00 |

14 October 2009 | $ 30,000.00 |

2 November 2009 | $ 30,000.00 |

12 November 2009 | $ 141,242.95 |

23 November 2009 | $ 21,000.00 |

8 December 2009 | $ 326,246.91 |

18 December 2009 | $ 14,240.66 |

20 January 2010 | $ 151,255.95 |

2 February 2010 | $ 53,000.00 |

9 April 2010 | $ 23,000.00 |

20 April 2010 | $ 10,000.00 |

11 May 2010 | $ 40,345.00 |

11 May 2010 | $ 141,488.00 |

7 July 2010 | $ 20,000.00 |

20 July 2010 | $ 10,000.00 |

13 September 2010 | $ 20,000.00 |

11 November 2010 | $ 45,000.00 |

139 At the date of the fire, GVF owed Superway Garden $42,500 under a loan agreement. The loan was not required to be repaid until 2016. GVF repaid Superway Garden $17,500 on 27 November 2009 and the remaining $25,000 on 9 December 2009.

140 At the date of the fire, GVF owed Mr Heyn, as trustee of the Heyn Family Trust, $42,500. GVF repaid $17,500 on 27 November 2009 and the remaining $25,000 on 16 December 2009.

141 Mr Vaughan states that he provided management services to GVF through Vaudell. GVF’s accounting records show that GVF had incurred a debt of $40,000 to Vaudell for management fees prior to the date of the fire. GVF paid $90,000 to Vaudell between May 2009 and February 2010 for management fees. The payments made to Vaudell were as follows:

Date | Amount |

28 May 2009 | $ 5,000 |

30 June 2009 | $ 2,500 |

30 June 2009 | $ 2,500 |

9 October 2009 | $ 10,000 |

9 October 2009 | $ 10,000 |

6 November 2009 | $ 10,000 |

18 November 2009 | $ 25,000 |

3 February 2010 | $ 12,500 |

3 February 2010 | $ 12,500 |

142 Mr Heyn deposes that he provided management services to GVF through Palacimo. According to Mr Pearce, Palacimo was owed $45,000 at the date of the fire. GVF paid $100,000 to Palacimo between May 2009 and February 2010. The payments made to Palacimo were:

Date | Amount |

28 May 2009 | $ 5,000 |

18 June 2009 | $ 5,000 |

9 October 2009 | $ 20,000 |

6 November 2009 | $ 15,000 |

10 December 2009 | $ 25,000 |

3 February 2010 | $ 25,000 |

4 February 2010 | $ 5,000 |

143 The only payments previously made to Vaudell and Palacimo were $10,000 each in December 2008.

Principles for assessment of solvency

144 Under s 95A(2) of the Corporations Act, a person who is not solvent is insolvent. Under s 95A(1), a person is solvent only if they are able to pay all their debts as and when they become due and payable.

145 The test for solvency requires application of a number of guiding principles recognised by the authorities. The principles include the following.

146 Insolvency is a question of fact to be ascertained from a consideration of the company’s financial position taken as a whole. The Court must have regard to the commercial realities. Commercial realities will be relevant in considering what resources are available to the company to meet its liabilities as they fall due, whether resources other than cash are realisable by sale or borrowing upon security and when such realisations are achievable: see Southern Cross Interiors Pty Ltd v Deputy Commissioner of Taxation (2001) 53 NSWLR 213 at [54]; Emanuel Management Pty Ltd (in liq) v Foster’s Brewing Group Ltd (2003) 178 FLR 1 at 26 [75] per Chesterman J; Hussain v CSR Building Products Limited, in the matter of FPJ Group Pty Ltd (in liq) (2016) 246 FCR 62 at [58].

147 The definition focuses on a “cash flow test” of insolvency, and not simply a “balance sheet test”: Hussain at [58]. That said, a company’s balance sheet remains relevant because the cash flow position must be assessed by reference to the company’s financial position as a whole: Hussain at [58]; Smith v Bone (2015) 104 ACSR 528 at [24].