FEDERAL COURT OF AUSTRALIA

Ramsay Health Care Australia Pty Ltd v Compton (No 2) [2017] FCA 629

Table of Corrections | |

8 June 2017 | The date of judgment on the cover page has been amended to “2 June 2017”. |

8 June 2017 | The date of hearing on the second page of the cover page has been amended to “1 June 2017”. |

8 June 2017 | The date of order on the Orders page has been amended to “2 June 2017”. |

8 June 2017 | The certification date has been amended to “7 June 2017”. |

ORDERS

RAMSAY HEALTH CARE AUSTRALIA PTY LTD (ACN 003 184 889) Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 136 of the Evidence Act 1995 (Cth), the use of the affidavit of Anna Stevis sworn 4 September 2015 (Exhibit 5), the affidavit of Graham Baker sworn 31 May 2017 (Exhibit 6) and the spreadsheet marked Exhibit 7 be confined to evidence of the claims made, but not evidence of the supporting factual basis of the claims.

2. The estate of Adrian John Compton be sequestrated under the Bankruptcy Act 1966 (Cth).

3. The Applicant Creditor’s costs be taxed and paid from the estate of the Respondent Debtor in accordance with the Bankruptcy Act 1966 (Cth).

4. Order 2 is stayed until 4:00pm on 2 June 2017.

AND THE COURT NOTES THAT:

1. The date of the act of bankruptcy is 21 May 2015.

2. A Consent to Act as Trustee signed by Barry Anthony Taylor has been filed under section 156A of the Bankruptcy Act 1966.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

1 The facts giving rise to the present application have previously been set forth and need not be repeated: Ramsay Health Care Australia Pty Ltd v Compton [2017] FCA 612.

2 An application first made on 26 May 2017 and stood over part heard to 30 May 2017 to adjourn the present hearing has been refused: Ramsay Health Care Australia Pty Ltd v Compton [2017] FCA 612. The hearing went ahead on 1 June 2017.

3 The task now to be undertaken, following the orders previously made by the Full Court of this Court and the High Court, is to “go behind” the judgment of the Supreme Court and to determine whether a sequestration order should now be made: Compton v Ramsay Health Care Australia Pty Ltd [2016] FCAFC 106; Ramsay Health Care Australia Pty Ltd v Compton [2017] HCATrans 95. Ramsay Health Care, on the one hand, maintains that Mr Compton is indebted to it for a sum in excess of $9,810,312.33; Mr Compton, on the other hand, has long maintained that he owes Ramsay Health Care nothing and that Ramsay Health Care is instead indebted to MediChoice, the business in respect to which Mr Compton gave a personal guarantee.

4 Having now undertaken that task, it is concluded that a state of satisfaction can comfortably be reached that Mr Compton owes Ramsay Health Care a sum in excess of $5,000 and that the discretion to make a sequestration order should be exercised in favour of the Petitioning Creditor. It is further concluded that Mr Compton has not satisfied the Court that there is “other sufficient cause” for not making a sequestration order.

5 These states of satisfaction, it should be noted, have been reached notwithstanding the accepted difficulties confronting Mr Compton given the decision to refuse him an adjournment of the present hearing.

6 It should also be noted that such reasons and findings as are now made may be less fulsome than may otherwise have been desirable. But, given the time constraints now compelling both brevity upon the part of Ramsay Health Care in advancing its case and the need for the Court to make a decision (if at all possible) prior to Monday 5 June 2017, the best has been made of a bad situation.

7 A preliminary obstacle to the Court entertaining the Creditor’s Petition should, however, be addressed at the outset. That obstacle was said to arise by reason of s 189AAA of the Bankruptcy Act 1966 (Cth) (the “Bankruptcy Act”).

8 A further obstacle potentially arose because the solicitor who instructed when the application was made for Mrs Compton to be appointed as the litigation representative for Mr Compton again sought an adjournment of the present hearing and also sought to withdraw Mrs Compton’s consent to act as a litigation representative. That solicitor declined to otherwise participate in the hearing.

9 Neither of these obstacles, it is concluded, preclude the Court from now entertaining the petition presented by Ramsay Health Care.

A statutory stay – s 189AAA

10 At the outset of the hearing of the Creditor’s Petition seeking the making of a sequestration order pursuant to s 52(1) of the Bankruptcy Act, the Court was informed that Mr Compton had signed an authority pursuant to s 188 of that Act. It was thereafter contended that s 189AAA operated as a stay upon the hearing of the Creditor’s Petition.

11 Section 189AAA provides as follows:

Stay of proceedings relating to creditor’s petition until meeting of debtor’s creditors

(1) If:

(a) an authority signed by a debtor under section 188 has become effective; and

(b) either:

(i) a creditor’s petition was presented against the debtor before the authority became effective; or

(ii) a creditor’s petition is presented against the debtor after the authority became effective but before the first or only meeting of the debtor’s creditors called under the authority;

proceedings relating to that petition are, by force of this subsection, stayed until:

(c) the conclusion of the meeting; or

(d) the adjournment of the meeting;

whichever is the earlier.

(2) This section does not limit subsection 206(1).

Section 188 in relevant part provides as follows:

Debtor may authorise trustee or solicitor to be controlling trustee

(1) A debtor who desires that his or her affairs be dealt with under this Part without his or her estate being sequestrated and:

(a) is personally present or ordinarily resident in Australia;

(b) has a dwelling-house or place of business in Australia;

(c) is carrying on business in Australia, either personally or by means of an agent or manager; or

(d) is a member of a firm or partnership carrying on business in Australia by means of a partner or partners or of an agent or manager;

may sign an authority in accordance with the approved form naming and authorising a registered trustee, a solicitor or the Official Trustee to call a meeting of the debtor’s creditors and to take control of the debtor’s property.

…

(2C) If the person authorised is a registered trustee or solicitor, the authority signed by the debtor under this section is not effective for the purposes of this Part unless, before the person authorised consents to exercise the powers given by the authority, the debtor gives to the person authorised:

(a) a statement of the debtor’s affairs; and

(b) a proposal for dealing with them under this Part.

…

(2E) A proposal for dealing with the debtor’s affairs under this Part must include a draft personal insolvency agreement.

12 The potential impact of s 189AAA was raised at the outset of the hearing on 1 June 2017 by Counsel on behalf of the registered trustee, Mr Paul Gerard Weston. It was then submitted that Mr Compton had signed an “authority” in accordance with s 188. Given the existing location of Mr Compton in Virginia in the United States, it was not self-evident on the materials then available that Mr Compton met the requirements of s 188(1)(a). Nor was there any evidence available that he otherwise fell within s 188(1)(b), (c) or (d). Nor was there any evidence that the requirements imposed by s 188(2C) or s 188(2E) had been satisfied.

13 The potential deficiencies in the matters necessary to be satisfied before s 189AAA operated were drawn to his attention on 1 June 2017. Liberty was reserved to him to re-agitate the matter at any time during the course of the day should he wish to put before the Court evidence of relevance to the requirements imposed by s 188(1), (2C) and (2E). That invitation was not accepted. Such further materials as were provided to the solicitors for Ramsay Health Care, and which was in turn made available to the Court late on the evening of 1 June 2017 did not progress the matter much further.

14 When the matter was called on for delivery of judgment this morning on 2 June 2017, however, Counsel on behalf of Mr Weston sought to then adduce additional evidence to satisfy the requirements of s 188 and in support of the submission that s 189AAA operated by its own force to halt any further step being taken in the present hearing. Material was tendered in support of that application. Included within those materials is an affidavit of Mr Compton, sworn yesterday, in which (without alteration) he states, inter alia:

12. I have no intention of leaving Australia permanently and consider Australia to be my home. It is my intention to return to Australia with my wife and children as soon as we have dealt with health issues concerning myself and my father in law.

13. My wife is the registered proprietor of our family home at [address omitted]. Upon my return to Australia it is my intention to reside in that property.

14. I have bank account with National Australia Bank in Australia.

15. I have superannuation in Australia.

16. I am providing financial consultancy services to each of James McConvill & Associates who have 9 offices throughout Australia dealing with Australian clients and dealing with Australian issues which I undertake electronically and by telephone.

17. I have filed all tax returns in Australia as an Australian taxation resident, the last of which was for the financial year ended 30 June 2016.

18. I understand that in this 2017 income tax year I consider myself to be a resident of Australia and will be filing a taxation return. I anticipate that will continue for the 2018 income tax year.

15 For the purposes of s 188(1)(a) of the Bankruptcy Act, no conclusion can be reached that Mr Compton is a person personally present or ordinarily resident in Australia. The expression “ordinarily resident” was explored by Lockhart J in Re Taylor; Ex parte Natwest Australia Bank Ltd (1992) 37 FCR 194 at 198:

To say that a person is ordinarily resident in Australia must mean something more than that he is resident in Australia. The word “ordinarily” connotes a comparison, a measure of degree. A person may have more than one residence, but he is not necessarily ordinarily resident in each of them. The question must be determined for the purposes of s 43 of the Act at a particular time. One must ask the question whether at that time the person was ordinarily resident in Australia. The concept of “ordinary residence” for the purposes of the Act, in my opinion, connotes a place where in the ordinary course of a person’s life he regularly or customarily lives. There must be some element of permanence, to be contrasted with a place where he stays only casually or intermittently. The expression “ordinarily resident in” connotes some habit of life, and is to be contrasted with temporary or occasional residence: see [Levene v Commissioners of Inland Revenue [1928] AC 217] and [Commissioners of Inland Revenue v Lysaght [1928] AC 234]. As Lord Warrington said in Levene (at 232): “‘Ordinarily resident’ means according to the way a man’s life is actually ordered.” The concept of ordinarily resident cannot be stated in definite terms; each case must be determined on its facts and after taking into account all relevant matters: see the Canadian case of Thomson v Minister of National Revenue [1946] SCR 209 per Estey J at 231.

It depends on the facts of each case whether the debtor is ordinarily resident in Australia at the time of the commission of the relevant act of bankruptcy. At first blush it may seem strange to say that a person can be ordinarily resident in more than one country at the same time; but on closer analysis it is not. Plainly you cannot be physically present in more than one place at the same time. But the lifestyles of people vary greatly. Some people in the ordinary pursuit of their lives regularly or customarily live in more than one place, each of which has an element of permanence about it and is not merely a place of casual or intermittent resort.

On the limited materials available to the Court no conclusion can be reached that Mr Compton is “ordinarily resident in Australia”. His intention to return at some future date, and the fact that his wife may be the registered proprietor of a property in Mosman in Sydney, nor the fact that he holds a bank account and superannuation account in Australia, satisfy the requirements as formulated by Lockhart J, albeit not exhaustively.

16 In support of the contention that Mr Compton was ordinarily resident in Australia, counsel for Mr Weston relied upon the form of the authority submitted by Mr Compton to the controlling trustee which states that his residential address is at the wife’s premises in Sydney. To bolster that submission, reliance was placed upon reg 13.07(1)(a) of the Bankruptcy Regulations 1996 (Cth) which provides as follows

Extract, etc of the Index to be admissible in evidence

(1) In any proceedings, a document or copy of a document that qualifies under subregulation (2):

(a) is proof, in the absence of evidence to the contrary, of information on the Index that is stated in it; and

(b) may be tendered in evidence without further proof.

(2) A document or copy qualifies if it:

(a) purports (irrespective of the form of wording used) to be an extract of information on the Index; and

(b) does not appear to the Court to have been revised or tampered with in a way that affects, or is likely to affect, the information.

17 For the purposes of that regulation, “evidence to the contrary” is, it is considered, provided by the very terms of Mr Compton’s affidavit. Moreover, the connections which Mr Compton has with the United States lend some support to a conclusion that he is not ordinarily resident in Australia. That material included details as to his present employment with the United States Postal Service where he apparently has regular employment and is in receipt of regular income in Virginia.

18 Although reliance on s 188(1)(c) was initially disclaimed by counsel on behalf of Mr Weston, it was belatedly relied upon. Again, however, no conclusion can be reached that Mr Compton is “carrying on business in Australia”. His affidavit merely states that he is “providing financial consultancy services” with no details provided as to the frequency or regularity with which any services have been provided in the past or even details as to the last occasion on which any such service was provided. The materials made available by the trustee also indicate that whatever services may be being rendered by Mr Compton, those services were being rendered “remotely” and “from Virginia”. Reliance upon s 188(1)(c) is rejected.

19 It is accordingly concluded that any “authority” signed by Mr Compton has not “become effective” (s 189AAA(1)) and that there is no stay operative such that Ramsay Health Care cannot further pursue the hearing of its Creditor’s Petition.

The adjournment & withdrawal of Mrs Compton as the legal representative

20 The further application this morning for an adjournment was based upon:

the same facts as had previously been addressed in the earlier adjournment application: Ramsay Health Care Australia Pty Ltd v Compton [2017] FCA 612; and

the signing by Mr Compton of the authority under s 188 of the Bankruptcy Act.

Neither argument prevailed. The adjournment was refused. The circumstances have not materially changed since the previous adjournment application was decided. The “authority” signed by Mr Compton, being an “authority” which has not “become effective” may indicate an opposition on the part of Mr Compton to the hearing of the Creditor’s Petition but it does not alter the assessment previously made that he has been given sufficient notice and time within which to prepare for today’s hearing.

21 Mrs Compton, by her solicitor, separately sought to withdraw her consent to act as the litigation representative of her husband. That application was perhaps curious. Having previously indicated her willingness to consent to so act only a matter of days previously, the unexplained change of position only invited speculation as to the reason for the change of attitude. No explanation was forthcoming.

22 On any view of the matter, however, and the Court itself having accepted only a matter of days earlier that Mr Compton was a person suffering a “legal incapacity”, the position inevitably confronted was the fate of a proceeding in which the continuing “legal incapacity” of Mr Compton was a matter at least open to question.

23 If leave was required for Mrs Compton to withdraw her consent, she was told that such leave was not forthcoming; if leave was not required, her legal representative was told that the final hearing of the Creditor’s Petition would continue in her absence. The legal representative was invited to remain in Court to provide such assistance as she was able to provide. The legal representative declined the invitation and withdrew.

24 The proceeding thereafter proceeded, primarily upon the basis that it was an ex parte application, although as Senior Counsel for Ramsay Health Care pointed out, it was more properly characterised as a hearing at which Mr Compton decided not to participate.

25 Having apparently signed an authority under s 188 of the Bankruptcy Act on 30 May 2017, and having again signed a revised form of the authority on 1 June 2017, there was at least some basis upon which a conclusion could be reached that Mr Compton by at least that date had made an informed and considered decision as to the manner in which he would seek to resist the application being made by Ramsay Health Care. That inference is only more certainly drawn if reference is made to the more detailed communications made over the day leading up to this judgment being delivered between Mr Compton and Mr Weston. Any asserted lack of mental capacity, it is concluded, is not a reason for declining to proceed with the hearing of the Creditor’s Petition. The only available inference is that Mr Compton was able as at today’s date to manage his own affairs and to give instructions to those he retained to represent his interests. Indeed, if he were not competent to do so, there would only be further reason to question whether the “authority” that he had signed satisfied the requirements of s 189AAA.

The making of a sequestration order – the discretion conferred

26 Section 41 of the Bankruptcy Act provides for the issue of a bankruptcy notice in circumstances where (inter alia) there has been a final judgment or order for an amount “of at least $5,000”.

27 Section 43 of the Act thereafter provides for the jurisdiction of the Court to make a sequestration order.

28 Section 44(1)(a) provides in relevant part that a creditor’s petition is not to be presented against a debtor unless “there is owing by the debtor to the petitioning creditor a debt that amounts to $5,000”.

29 Section 52 thereafter provides for the making of a sequestration order. That section provides, in relevant part, as follows:

Proceedings and order on creditor’s petition

(1) At the hearing of a creditor’s petition, the Court shall require proof of:

(a) the matters stated in the petition (for which purpose the Court may accept the affidavit verifying the petition as sufficient);

(b) service of the petition; and

(c) the fact that the debt or debts on which the petitioning creditor relies is or are still owing;

and, if it is satisfied with the proof of those matters, may make a sequestration order against the estate of the debtor.

…

(2) If the Court is not satisfied with the proof of any of those matters, or is satisfied by the debtor:

(a) that he or she is able to pay his or her debts; or

(b) that for other sufficient cause a sequestration order ought not to be made;

it may dismiss the petition.

30 At least three things need to be noted in respect to s 52, namely:

section 52(1) sets forth those matters in respect to which proof is required for the making of a sequestration order;

sections 52(1) and (2) confer a discretion; and

the onus to satisfy the Court that a debtor is able to pay his debts or that there is “other sufficient cause” for not making a sequestration order rests upon the debtor.

31 “On proof of the matters in s 52(1) of the Act”, it has been said, “the Court will generally proceed to make an order for sequestration”: Totev v Sfar [2006] FCA 470 at [37], (2006) 230 ALR 236 at 243. Allsop J (as his honour then was) went on to observe (at 243):

[37] …It is for the debtor to persuade the court that the public interest in the dealing with the insolvent debtor and the rights of the individual creditors are outweighed by other considerations…

When exercising the discretion in the context of s 52(2)(b) it is thus the debtor who carries the onus of proof of establishing “that for other sufficient cause a sequestration order ought not to be made”: Ling v Enrobook Pty Ltd (1997) 74 FCR 19 at 24 per Davies, Wilcox and Branson JJ.

32 The countervailing factors must be of “significant weight”: Klinger v Nicholl [2005] FCAFC 153, (2005) 4 ABC(NS) 16. Emmett J (with whom Moore and Tamberlin JJ agreed) there observed (at 32):

[32] The exercise of discretion under s 52(2) entails a balancing exercise. While the fact of an instalment order may be a relevant consideration for a bankruptcy court to take into account (see Cain v Whyte (1933) 48 CLR 639), it is but one of the considerations that might be taken into account. For a matter to constitute sufficient cause to decline to make a sequestration order, when the prerequisites of ss 52, 43 and 44 of the Act have otherwise been satisfied, the matter must be one of significant weight to displace the interest of the community in avoiding insolvent trading.

33 Similarly, Sundberg J in St George Bank Ltd v Helfenbaum [1999] FCA 1337 had previously observed:

[13] … The existence of a cross-claim may be a “sufficient cause” within s 52(2)(b) for declining to make a sequestration order: Ling v Enrobook Pty Ltd (1997) 74 FCR 19 at 25. It is for the debtor to establish the existence of “sufficient cause”: Cain v Whyte (1933) 48 CLR 639 at 645-646; Ling at 24. He must establish that he has a real claim against the creditor that is likely to succeed. If the Court is satisfied that there is such a claim, and that its quantum is likely to equal or exceed the creditor’s claim, it will not make a sequestration order. If the claim is likely to be less than the creditor’s claim, the Court will require the debtor, if he is to avoid a sequestration order, to pay the difference between the judgment debt and the amount he is likely to recover on his claim. See Re Player (1962) 19 ABC 277 at 282; Re Schmidt; Ex parte Anglewood Pty Ltd (1968) 13 FLR 111 at 115-116; Ling at 25-26; Commonwealth Bank v McDonald [1999] FCA 984. A debtor does not establish a real claim that is likely to succeed merely by producing a statement of claim in an action against the creditor: Re Rivett; Ex parte Edward Fay Ltd (1932) 5 ABC 182; Player at 282, or by pointing to the existence of current litigation against the creditor: cf Re Douglas Griggs Engineering Ltd [1963] 1 Ch 19 at 23. While the Court does not try the cross-claim in advance, the debtor must adduce sufficient evidence to show that it is a real claim which is likely to succeed: cf Vogwell v Vogwell (1939) 11 ABC 83 at 88; Player at 282.

34 The phrase “other sufficient cause” is not confined to those circumstances in which a creditor is putting forward a petition “solely for some collateral illegitimate end, and not for the purpose of securing the equal distribution of the available assets amongst the creditors”: Cain v Whyte (1933) 48 CLR 639 at 645. “Other sufficient cause”, it was there held, “might arise in connection with any particular case” and “it is the duty of the Bankruptcy judge to examine in each case, if the question is raised, whether there is other sufficient cause than the fact that the debtor is able to pay his debts in full, for refusing to make an order”.

35 But one instance of “other sufficient cause” may be found in the fact that there is an appeal pending against the judgment debt relied upon: cf. Rigg v Baker [2006] FCAFC 179, (2006) 155 FCR 531. French J (as his Honour then was) there summarised the circumstances in which the discretion could be exercised as follows (at 545):

[67] When the creditor’s petition is based upon a judgment debt, the existence of a pending appeal against that judgment may also be a ground for adjourning the petition. In Ahern v Deputy Commissioner of Taxation (Qld) (1987) 76 ALR 137 the Full Court said that:

It is also well established that in general a court exercising jurisdiction in bankruptcy should not proceed to sequestrate the estate of a debtor where an appeal is pending against the judgment relied on as the foundation of the bankruptcy proceedings provided that the appeal is based on genuine and arguable grounds.

That observation arose in the context of an appeal against a sequestration order made after the primary judge had refused to adjourn a petition based on a default judgment then subject to appeal.

36 “Other sufficient cause” may also be found in, for example, a cross-claim a debtor may have against a creditor: Ling v Enrobook (1997) 74 FCR 19 at 25. The Court there observed:

A review of the authorities discloses that in certain circumstances, but not in all circumstances, the fact that the debtor has pending before a court a legitimate claim to funds sufficient to satisfy the petitioning creditor’s debt will amount to “other sufficient cause” not to make a sequestration order …

The Court thereafter went on to further observe (at 26):

The above authorities do not, in our view, support the appellant’s contention that the courts recognise a public interest in allowing a debtor to prosecute litigation commenced by the debtor…

The authorities also show that satisfaction that the debtor is well advanced with litigation likely to result in the debtor being in a position to pay his or her debts may well provide a basis for a finding that there is a “sufficient cause” for a sequestration order not to be made (see, for example, Maddestra v Penfolds Wines Pty Ltd [(1993) 44 FCR 303]). But the authorities do not suggest that it is in the public interest to allow insolvent debtors to prosecute litigation generally. They only recognise that it is not in the public interest for a debtor to be forced into bankruptcy by reason of a state of insolvency likely to be of only short duration.

See also: Commonwealth Bank of Australia v Jeans (No 3) [2006] FCA 693 at [11], (2006) 4 ABC(NS) 288 at 291 per Rares J.

37 A further basis upon which a debtor may establish “other sufficient cause” could also potentially be found where there is reason to question the judgment debt upon which a creditor’s petition otherwise proceeds. Even in the absence of an appeal from the judgment, a debtor may be able to make out a case that the judgment was procured in circumstances which give rise to questions as to whether a sequestration order ought to be made. Even cases falling short of fraud in procuring a judgment or abuse of process may suffice.

The indebtedness of Compton to Ramsay Health Care

38 For the purposes of satisfying the Court of those matters set forth in s 52(1) of the Bankruptcy Act and that Ramsay Health Care is indeed owed a significant amount of money, reliance was placed by Ramsay Health Care upon:

the Certificate of Debt pursuant to cl 12 of the Guarantee and Indemnity dated 18 February 2015 for an amount of $9,810,312.33;

the judgment of Hammerschlag J given on 6 March 2015 and entered on 10 March 2015 in favour of Ramsay Health Care against Mr Compton in the amount of $9,810,312.33;

a scheduled calculating interest on the judgment amount from 6 March 2015 up to 12 May 2017 totalling $1,701,518.22;

the Distribution and Group Purchasing Agreement entered into between Ramsay Health Care, MediChoice and Mr Compton dated 11 September 2012;

the Guarantee and Indemnity given by Adrian John Compton as guarantor in favour of Ramsay Health Care dated 28 November 2012;

the Summons and Commercial List statement dated 2 June 2014;

the Commercial List Response dated 24 July 2014;

the Bankruptcy Notice addressed to Mr Compton dated 27 April 2015; and

the Creditor’s Petition dated 4 June 2015 and accompanying affidavits verifying the Petition.

Such materials, it is concluded, establish “the matters stated in the petition”.

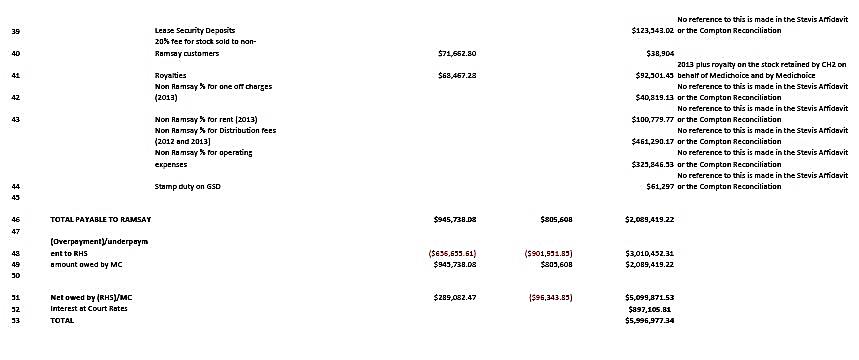

39 Separate from such matters as were previously before the Court, of importance is a more recent affidavit of Mr Paul Fitzmaurice sworn 26 May 2017. Mr Fitzmaurice is the Group Chief Commercial Officer of Ramsay Health Care. In that affidavit, Mr Fitzmaurice takes into account the challenges made by (inter alia) Ms Stevis to the quantification of the indebtedness previously relied upon in the Supreme Court proceeding. The conclusion reached by Mr Fitzmaurice, making a number of assumptions in favour of the challenges sought to be advanced, is that the indebtedness is reduced to an amount no less than $5,099,870.89. Mr Fitzmaurice also separately calculates the interest payable on the judgment debt as being $897,105.81, bringing the total figure to $5,996,976.70.

40 As of 2 June 2017, a state of satisfaction is reached that Mr Compton remains indebted to Ramsay Health Care for a considerable sum of money and a sum certainly more than $5,000. At the very least, the Court is satisfied that a sizeable portion of “the debt … on which the petitioning creditor relies is … still owing”.

A question of onus

41 The onus in the present proceeding lay on Mr Compton to “satisfy” the Court of the claims he sought to advance as to Ramsay Health Care in fact owing MediChoice money and that he was accordingly not liable to Ramsay Health Care under the personal guarantee.

42 That onus, it should be noted, arose either by reason of:

section 52(2) of the Bankruptcy Act (Totev v Sfar [2006] FCA 470, (2006) 230 ALR 236; St George Bank Ltd v Helfenbaum [1999] FCA 1337); or

the effect to be given to cl 12 of the Guarantee and Indemnity entered into between Mr Compton and Ramsay Health Care.

Clause 12, it should briefly be noted, provided as follows:

Certification by Ramsay

A certificate from Ramsay stating that an amount is owing or an event has occurred is taken to be correct unless the contrary is proved.

Such clauses, it should further be briefly noted, are to be given effect according to their terms: Permanent Trustee Co Ltd v Gulf Import and Export Co [2008] VSC 162 at [86] to [87] per Hansen J. And once a certificate has been issued, the onus thereafter shifts to the debtor to establish that the amount claimed in the certificate is incorrect: Beefeater Sales International Pty Ltd v MIS Funding No 1 Pty Ltd [2016] NSWCA 217. Bathurst CJ there observed:

[99] In the present case, the certificate under cl 14 is not conclusive evidence of the indebtedness. Rather, it casts on the borrower the onus of proving that the certificate is incorrect. There is nothing in the text to indicate that the right to give the certificate, along with the other rights conferred on the lender in the loan agreement, is incapable of assignment.

Gleeson and Payne JJA agreed with the Chief Justice.

The challenges sought to be advanced

43 If any question as to onus of proof is presently left to one side, there have been several attempts on the part of Mr Compton to quantify the amounts said to be owing from Ramsay Health Care to MediChoice and, accordingly, the amount for which Mr Compton assumes liability pursuant to his personal guarantee.

44 But the exposition of these attempts on the part of Mr Compton to quantify his indebtedness placed Senior Counsel for Ramsay Health Care in a dilemma – on the one hand, in the absence of Mr Compton participating in the present hearing and no evidence being tendered on his behalf, one choice for Ramsay Health Care was to accept that there was a need to “go behind” the Supreme Court judgment and simply rely upon (inter alia) the certificate of indebtedness as sufficient proof of the indebtedness; on the other hand, a choice could be made to tender in the present hearing the affidavit of Ms Stevis affirmed 4 September 2015 and the affidavit of Mr Graham Baker sworn 31 May 2017 annexing his Reports and to seek to satisfy the Court that even had such evidence been led the Court should nevertheless proceed to exercise the discretion to make a sequestration order.

45 A short adjournment was granted to permit Senior Counsel for Ramsay Health Care to obtain instructions as to the choice to be made. He opted for the latter course. The Court is grateful to Counsel and those instructing for the choice exercised and the exposition provided as to how the competing quantifications of indebtedness could be resolved. The evidence of Ms Stevis and Mr Baker was ultimately admitted – not as evidence of the factual assertions sought to be advanced in their evidence, but rather as evidence as to the competing quantifications to which the Court should give attention.

46 In very summary form:

Ms Stevis, the former General Manager and a Director MediChoice, had calculated that Ramsay Health Care owes MediChoice “at least AUD$2.449 million”; and

Mr Baker, a registered taxation practitioner and a registered company auditor, maintained that Ramsay Health Care is indebted to MediChoice in an amount variously calculated in the range of $1,293,620.68 through to $2,060,743.53.

Each of these calculations needs to be separately addressed.

47 The course taken in the present proceeding whereby evidence had been filed by Mr Compton but not adduced at the final hearing, it may be noted, follows a course previously pursued by Mr Compton in the Supreme Court proceedings where evidence had been filed but not read. But whatever may be the reason for the course now pursued by Mr Compton in the present proceeding, the Court nevertheless attempted as best as it was able to take into account the evidence (or at least some of the evidence) upon which Mr Compton may well have wished to rely upon had his legal representative not withdrawn from the hearing.

48 Mr Fitzmaurice, having undertaken his task, concludes that MediChoice is indebted to Ramsay Health Care in a sum no less than $5,099,870.89.

The competing calculations

49 The attempt made by Ms Stevis in her affidavit sworn on 4 September 2015 concludes that Ramsay Health Care owes MediChoice “at least AUD$2.449 million”.

50 Following the account provided by Ms Stevis, and her attempt to reconcile the position sought to be advanced by MediChoice and the competing claims of Ramsay Health Care, a further attempt was made by those previously representing Mr Compton to attempt a reconciliation of the claims founded upon the evidence of Ms Stevis and those being pressed by Ramsay Health Care. This further attempt resulted in a calculation that exposed – so it was claimed – an indebtedness on the part of Ramsay Health Care in a sum variously expressed as $96,338 or $96,343.85. The precise sum matters not. What was of importance to those representing Mr Compton was to establish that on their account it was Ramsay Health Care which owed at least some sum of money to MediChoice rather than any indebtedness to Ramsay Health Care.

51 Mr Fitzmaurice in his affidavit went through in some considerable detail the approach advanced by Ms Stevis. Mr Fitzmaurice provided his own Schedule setting forth an attempted reconciliation of the approach that had emerged to date, being the account of Ms Stevis and the latter reconciliation carried out on Mr Compton’s behalf. Mr Baker’s affidavit was not available to Mr Fitzmaurice at the time he undertook the task of attempting a reconciliation.

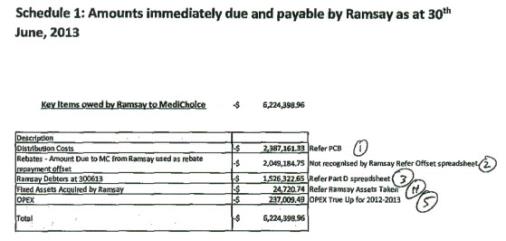

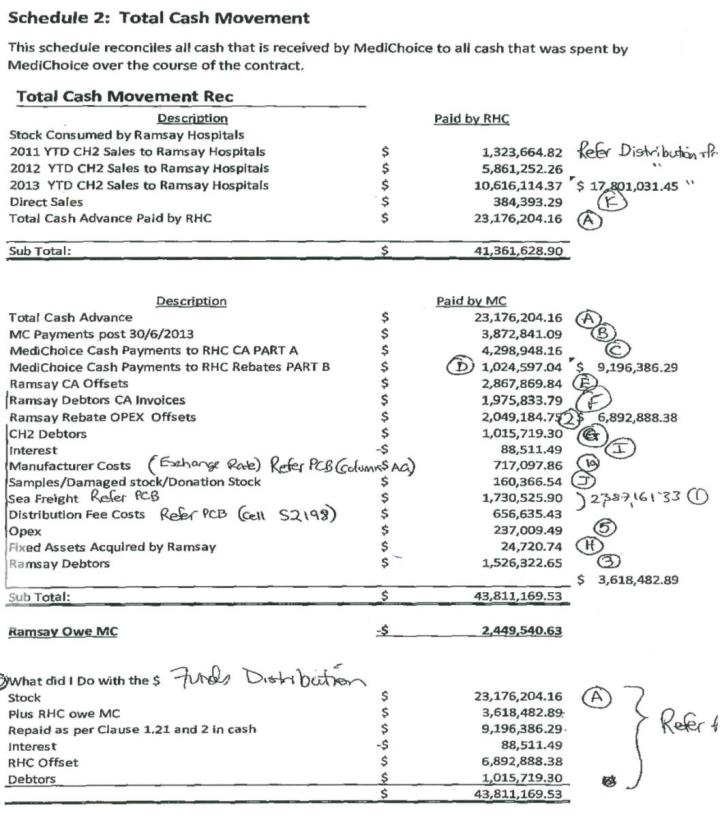

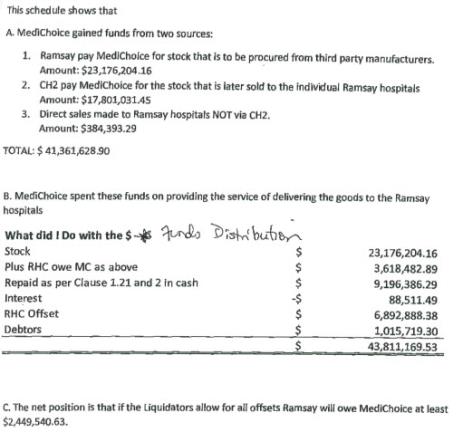

52 The calculation undertaken by Ms Stevis that resulted in her conclusion that Ramsay Health Care owes MediChoice “at least AUD$2.449 million” was the product of calculating the total amount of monies received by MediChoice ($41,361,628.90) and comparing it with the total amount of monies paid by MediChoice ($43,811,169.53). The calculations performed by Ms Stevis are set forth in two Schedules to her affidavit. The first Schedule provides as follows:

The second Schedule provides as follows:

This second Schedule goes on to summarise what the above calculation shows as follows:

The hand-written annotations to both Schedules are understood to be those of Ms Stevis.

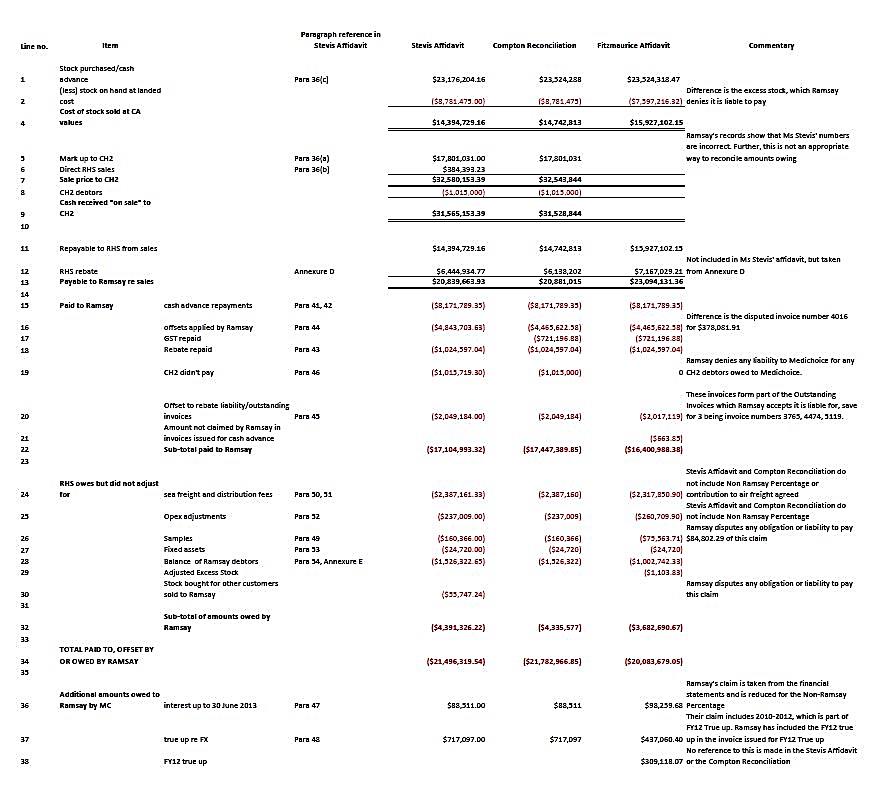

53 The Schedule of the reconciliation attempted by Mr Fitzmaurice was (in part) as follows:

Reservations expressed in respect to the Stevis and Compton calculations

54 If reference is made to the Schedules provided by Ms Stevis and that provided by Mr Fitzmaurice, and the explanations for the discrepancies exposed by Mr Fitzmaurice, it is concluded that the calculations of Ms Stevis do not expose any reliable basis upon which the Court could conclude that Ramsay Health Care owes MediChoice monies. Given this conclusion, there is no basis upon which the Court could conclude that Mr Compton has discharged the onus of satisfying the Court that “for other sufficient cause a sequestration order ought not to be made”.

55 There are several reasons for reaching these conclusions.

56 First, if reference is made to Ms Stevis’ calculation that Ramsay Health Care has paid a sum of $41,361,628.90 the competing calculation of Mr Fitzmaurice is $43,977,725.57. This discrepancy is exposed by the following comparison:

Payments made | The Stevis calculation | The Fitzmaurice calculation |

Cash advances | $23,176,204.16 | $23,524,318.56 |

Sales by Medichoice | $17,801,031.45 | $19,907,854.69 |

Direct sales | $384,393.29 | $545,552.32 |

$41,361,628.90 | $43,977,725.57 |

The significant difference between these calculations is obviously the discrepancy between $17,801,031.45 and $19,907,854.69. The former figure is that set forth by Ms Stevis and reflects the three payments for “CH2 Sales to Ramsay Hospitals” for 2011 to 2013. Mr Fitzmaurice, upon his review of “Ramsay’s books and records”, calculates the higher sum.

57 The calculation by Ms Stevis is carried forward in the schedule prepared by Mr Fitzmaurice (at Line Item 5). The explanation provided by Mr Fitzmaurice in both his affidavit and in his Schedule includes (inter alia) the simple assertion that Ramsay’s records show that Ms Stevis’ numbers are incorrect. If any question as to the manner in which Ms Stevis has taken into account “CH2 Sales” is presently left to one side, without the Court either itself reviewing the financial records or further evidence from Ms Stevis or her attendance in Court to give evidence and to be questioned in respect to her calculations, it is difficult to accept her calculations without some considerable reservation. Left at that point, the evidence would simply have exposed disagreement as to the facts, but Mr Fitzmaurice did attend and was available for cross-examination had Mr Compton participated in the hearing. There is every reason to accept the evidence he gives.

58 Second, if reference is made to the further exposition as to the calculation of $43,811,169.53 (being the amount claimed by Ms Stevis to have been “paid by MC”), Mr Fitzmaurice maintains that this sum is overstated by $2,976,267.52. A series of calculations have been undertaken by Mr Fitzmaurice, but principal among those calculations include:

a claim that the amount of $1,015,719.30 for “CH2 Debtors”, being a debt for which Mr Fitzmaurice claims Ramsay Health Care assumes no liability under the terms of the Agreement; and

a claim of “Ramsay Debtors” in the sum of $1,526,322.65, being a sum which is disputed, with Mr Fitzmaurice maintaining that this amount is “overstated by $514,114.76”.

Although there is a process of adjustment set forth by Mr Fitzmaurice, he asserts that invoices annexed to the affidavit of Ms Stevis totalling $536,821.98 include invoices which “have never been received by Ramsay and any liability to pay them is disputed by Ramsay”. Other than the claim made for these monies, there is no evidence that MediChoice ever sent these invoices to Ramsay Health Care. Again, indeed, there is every reason to accept the evidence of Mr Fitzmaurice that the invoices were not sent.

59 Ms Stevis in her affidavit seeks to verify the amount of $1,015,719.30 by reference to internal accounting records which she annexes. Mr Fitzmaurice refers to this amount in Line Item 19 of his Schedule. It has been assumed that these records total the amount claimed. But left unexplained by Ms Stevis was the entitlement of MediChoice to be paid the amounts claimed. The reference to “CH2” is a reference to Clifford Hallam Healthcare Pty Ltd, a preferred logistics supplier separate and distinct from Ramsay Health Care. Whatever may be the liability as between MediChoice and the arrangements it entered into with CH2, on Mr Fitzmaurice’s account any liability as between MediChoice and CH2 is a matter between them and stands separate and apart from any liability assumed by Ramsay Health Care. The claims of Mr Fitzmaurice seem to be independently supported by a Report to Creditors of Compton Fellers Pty Limited pursuant to s 439A of the Corporations Act 2001 (Cth). That Report, dated 5 August 2014, states in part as follows:

60 Third, the first of Ms Stevis’ Schedules incorporates a sum of $2,049,184.75 in respect to “Rebates” being an “Amount Due to MC from Ramsay used as rebate repayment offset”. The annotations states that this is “Not recognised by Ramsay Refer Offset spreadsheet”. That sum, in turn, is further addressed in Annexure D to Ms Stevis’ affidavit where her calculation proceeds from the statement that the sum for “Total Hospital Rebate Repayment Due” is $6,444,934.77. Annexure D provided as follows:

Summary of All terms Relating to the Finalisation of the MediChoice Supply Agreement

PART B – Hospital Rebate: To be confirmed by COB 6th February 2014

MediChoice Position | Ramsay Position | Variance | MediChoice Comments | |

INC GST | INC GST | INC GST | ||

Hospital Rebate Repayment (Inc GST) | ||||

FY11 Rebate Payable | 271,683.85 | 378,007.96 | (106,324.11) | Refer Ramsay Price Rebate July 2010 to June 2011 Worksheet |

FY12 Rebate Payable | 1,738,232.26 | 1,749,546.40 | (11,314.14) | Refer Ramsay Price Rebate July 2011 to June 2012 Worksheet |

FY13 Rebate Payable | 3,774.100.97 | 3,935.993.81 | (161,892,84) | Refer Ramsay Price Rebate July 2012 to June 2013 Worksheet |

Hospital rebate repayment due 12/06/2013 | 5,784.017.08 | 6,063,548.17 | (279,531.09) | |

13 June 2013-30June 2013 rebate on split stock | 657,188.88 | 825,527.80 | (168,338.92) | Refer Ramsay Price Rebate Stock Split 12 June 2013-30th June 2013 worksheet |

Rebated on 2% Shortfall under 1.125% arrangement | 52,191.63 | (52,191.63) | ||

Rebate Due on Hartmans Sales | 225,761.60 | (225,761.60) | ||

Rebate Due on Direct Sales | 3,728.81 | 11,000.00 | (7,271.19) | Refer Ramsay Price Rebate Direct Sales Worksheet |

Total Hospital Rebate Repayment Due | 6,444,934.77 | 7,178.029.20 | (733,094.43) | |

Hospital Rebate Repayments | ||||

3/02/2012 | (378,008.96) | (378.00796) | 0.00 | Refer Offsets Cell “E133” |

26/04/2012 | (587,808.25) | (587,808.25) | 0.00 | Refer Offsets Cell “E135” |

31/05/2012 | (58,780.83) | (58,780.83) | 0.00 | Refer Offsets Cell “E136” |

Total Rebate Repayments | (1,024.597.04) | (1,024.597.04) | 0.00 | |

Amounts due to MediChoice from Ramsay used as rebate repayment offset as per worksheet | (2,049,184.75) | (2,049,184.75) | 0.00 | Refer Offsets Cell “E140” |

Net Hospital Rebate Repayment Position as at 30 June 2013 | 3,371.152.98 | 4,104,247.41 | (733,094.43) |

61 The sum of $2,049,184.75 is carried forward into the Schedule prepared by Mr Fitzmaurice at Line Item 20. But the sum of $6,444,934.77 as set forth in Annexure D of Ms Stevis’ affidavit is disputed by Mr Fitzmaurice. He claims in his affidavit that “Ramsay has issued to Medichoice invoices totalling $7,167,029.21”. This is the sum set forth in Line Item 12 to his reconciliation. By reference to the figure claimed in respect to the Compton calculation, namely $6,138,202, Mr Fitzmaurice in his affidavit asserts that “there is no explanation provided for the disparity of $1,028,827.21”. There is no explanation provided by Ms Stevis in the body of her affidavit or in either Schedule 1 to her Affidavit or in Annexure D, other than the notation. But that notation, with respect, provides no explanation as to why she claims the sum that she does and what it is that is “not recognised”.

62 Fourth, is the failure on the part of Ms Stevis to account for the payments made pursuant to the Deed of Agreement and Settlement dated 9 April 2013 but signed on 15 April 2013. This Deed recites a dispute between Ramsay Health Care and MediChoice in respect to the liability of:

Ramsay Health Care to pay the costs of air freight totalling $65,035.54;

MediChoice to pass on interest to Ramsay Health Care earned from the trading activities of MediChoice in the name of Ramsay Health Care; and

liability of Ramsay Health Care to pay detention fees totalling approximately $305,000.

Without admission as to liability, the Deed records a retention by MediChoice from Ramsay Health Care of a sum of $100,000 towards the disputed air freight and an agreement on the part of Ramsay Health Care to pay MediChoice a sum of $305,000. What is in effect a payment by Ramsay Health Care of the sum of $100,000 is taken into account in the reconciliation effected by Mr Fitzmaurice; but there is an apparent failure on the part of Ms Stevis to record in her second Schedule any payment made by Ramsay Health Care to MediChoice of $305,000. Nor is there any apparent attempt on the part of Ms Stevis to bring to account either this sum of $305,000 or any such reduced sum as may otherwise have become payable by reason of cl 2.1(b) of the Deed.

63 Fifth, Line Item 24 of the Fitzmaurice Schedule sets forth a claim by Ms Stevis that Ramsay Health Care owes MediChoice a sum of $2,387,161.33. This calculation seems to have been arrived at, based on the figures in the Stevis Schedule, by adding the “Sea freight” ($1,730,525.90) and “Distribution Fee Costs” ($656,635.43). Mr Fitzmaurice calculates this amount at $1,856,560.73. Even given reference to her Schedule, the basis upon which Ms Stevis has performed her calculation is not self-evident. One explanation provided by Mr Fitzmaurice is that Ms Stevis has calculated the amount said to be payable by reference to gross sales and not calculated the amount payable by reference to Schedule 3 of the Distribution and Group Purchasing Agreement, being a calculation by reference to the “Non-Ramsey Percentage Contribution”.

64 Sixth, a similar challenge is mounted by Mr Fitzmaurice to Ms Stevis’ calculation in her Schedule of $237,009.49 being payable by Ramsay Health Care for “Opex”, namely “operating expenses”. Mr Fitzmaurice calculates the comparable sum as being $65,135.99.

65 If the analysis is confined to these amounts, being some but not all of the larger sums of money claimed, one conclusion is that there is simply a dispute as to the facts and that Mr Compton has not discharged any onus of establishing any liability on the part of Ramsay Health Care. But the analysis, with respect, goes beyond that to the extent (for example) that:

some of the matters claimed by Ms Stevis do not seem to be sums for which Ramsay Health Care assumes liability and in respect to which a basis for making a claim has not been substantiated by Ms Stevis by reference to any of the terms of the Agreement between Ramsay Health Care and MediChoice; and

some of the claims seem to be denied by independent Reports, such as the s 439A Report.

Mr Fitzmaurice’s evidence, it is concluded, provides a very certain foundation for a conclusion that Ms Stevis’ evidence was sufficiently unreliable that the Court should not be satisfied that Ramsay Health Care owes MediChoice the monies she claims. Had she attended at the hearing and been available for cross-examination, she may have provided greater insight as to the basis upon which her calculations proceeded. But she did not attend. Without her assistance, and confined to such guidance as may be gleaned from her affidavit and the calculations undertaken, her account is sufficiently unreliable that no conclusion could be reached that Ramsay Health Care is indebted to MediChoice.

The Baker Reports

66 Prior to the final hearing yesterday on 1 June 2017, there had been filed on behalf of Mr Compton’s then legal representative an affidavit sworn by Mr Baker on 31 May 2017. That affidavit annexed two Reports, including his initial Report dated 21 April 2016.

67 Mr Baker in this Report expresses the opinion that “Ramsay is a debtor of Medichoice”. Mr Baker sets forth three different scenarios, ranging from an indebtedness on the part of Ramsay Health Care to MediChoice of $1,293,620.68 through to $2,060,743.53. On any approach, however, it is the opinion of Mr Baker that Ramsay Health Care is indebted to MediChoice.

68 But this Report suffers from at least two difficulties, namely:

the fact that Mr Baker’s first Report does not self-evidently set forth the factual basis from which he proceeds; nor does that Report set forth his reasoning.

But one instance of this lack of any self-evident factual support for his conclusions starts with the very assumption at the outset of each of his calculations as to the indebtedness of Ramsay Health Care. The starting figure is set forth in each of the three calculations as being $23,801,940.47. A spreadsheet which had been produced with Mr Baker’s Report and which was apparently relied upon by Mr Baker (Exhibit A7) sets forth this sum as being the difference between “[t]otal payments received from Ramsay” ($23,932,151.86) “[l]ess amounts refunded per invoices” ($130,211.39). But there was no further exposition as to the source from which these sums had been derived. Ms Stevis (it would appear) calculates the comparable figure as an amount of $23,176,204.16 – but there is no explanation for the discrepancy; and

the fact that Mr Baker’s Report is more characterised as an attempt to make foreshadowed legal submissions rather than to objectively set forth a factual basis and a reasoning process which can be taken into account by this Court.

It is sufficient for present purposes to make reference to the following extract from his Report:

In that Ramsay has claimed this entire amount as excess stock, it appears that Ramsay is abrogating any responsibility to act on information it had in relation to excess stock, while demanding that all responsibility for excess stock rests with Medichoice. Given that the contract is silent regarding the over-ordering of stock, and the responsibility therefor, that it is not clear as to what forecast information Medichoice should rely on and that Ramsay had the information to act and chose not to, there is a question as to whether the liability for excess stock belongs to Medichoice alone or is shared by both Medichoice and Ramsay. I recommend that legal advice be sought in order to clarify this issue.

69 Any potential objection to the evidence proposed to be called from Mr Baker may presently be left to one side. It is the absence of explanation for the conclusions reached which leads to the present assessment that reliance cannot be placed independently upon his Reports as providing a factual foundation for being satisfied that Ramsay Health Care is the entity that owes money to MediChoice.

70 Also left to one side is the fact that Mr Baker would seem in his Report to accept some of the claims advanced on behalf of Ramsay Health Care; being matters which would not appear to be accepted by Ms Stevis. Mr Baker thus states that he agrees “with Ramsay on a number of items under review, including the … Rebates amounts [and] Lease securities”. But, just as the absence of explanation does not assist the case sought to be advanced by Mr Compton, the apparent acceptance of these amounts by Mr Baker without explanation does not assist Ramsay Health Care.

The reliability of the Fitzmaurice calculation

71 Although it may be sufficient to conclude that:

Ramsay Health Care has sufficiently set forth the indebtedness of MediChoice and Mr Compton to it by reason of the Certificate of Indebtedness issued under the Agreement and the other documents relied upon;

and that:

Mr Compton has not established either by reference to the evidence of Ms Stevis or Mr Baker that there is “other sufficient reason” to question that indebtedness and certainly has not established that Ramsay Health Care is indebted to MediChoice;

it is further concluded that on the evidence available at the hearing:

the calculations undertaken by Mr Fitzmaurice and his evidence provide a sufficiently certain factual foundation for a finding to be made that Mr Compton is indebted to Ramsay Health Care for a sum no less than $5,000 and (most probably) in excess of $5,099,870.89.

72 That conclusion and findings are based upon (inter alia):

the preparedness of Mr Fitzmaurice to make a significant number of assumptions in favour of the claims advanced on behalf of Mr Compton. Thus, for example, and confined to the purposes of the present hearing, Mr Fitzmaurice was prepared to accept that there could be reduced from the net amount owing to Ramsay Health Care by Mr Compton an amount of $3,019,861.01 in respect to what he characterised as the “Outstanding Invoices”.

The conclusions and findings are also based upon:

the explanation provided by Mr Fitzmaurice in respect to the more significant areas of factual difference between Ramsay Health Care and Mr Compton, being those areas presently addressed.

In making that finding, considerable care has been taken as far as possible to ensure that the factual detail provided by Mr Fitzmaurice has not operated to the prejudice of Mr Compton. Although it has been separately concluded that Mr Comtpon has been extended more than an adequate opportunity to advance his claims, the fact remains that the time within which he had to prepare his case for hearing has been less than he desired – albeit a time constraint, it has also been concluded, which was a matter of his own “procrastination, or … delay”: [2017] FCA 612 at [25].

CONCLUSIONS

73 There is no evidence before the Court as to any ability of Mr Compton to pay either the amount of the judgment debt of $9,810,312.33 or his ability to pay any lesser amount. There is no evidence as to his ability, for example, to pay the sum of $5,099,870.89, being the minimum amount said by Mr Fitzmaurice to be payable. Indeed, the further materials produced by Mr Weston on the day that judgment was delivered would appear to support the conclusion that Mr Compton is not in the position to pay these amounts.

74 If any consideration given to the onus borne by Mr Compton is presently left to one side, it is concluded that Ramsay Health Care has in fact established that it is owed a sum far in excess of $5,000.

75 Even if consideration is given to the fact that the two applications for the adjournment sought by Mr Compton have been refused and the fact that he was thereby placed in a position where he has had less time than may otherwise have been desirable in which to prepare, he has not been denied an opportunity to address (at the very least) the fundamental claims made in Mr Fitzmaurice’s affidavit and an opportunity to test those fundamental claims. There was, of course, less of an impediment placed in the path of Mr Compton in challenging the reliability of Mr Fitzmaurice’s affidavit to the extent that Mr Fitzmaurice maintained that certain amounts were not payable pursuant to the Agreement or that Ramsay Health Care assumed no liability under the Agreement for other amounts. Although it has been concluded after a more detailed analysis of the evidence and the manner in which it unfolded during the course of the final hearing that the reservations previously expressed and founded upon a professed inability to master the factual detail were not as great as claimed during the interlocutory hearing, there was ultimately little need to master the factual detail in order to challenge the reliability of the more prominent claims made by Mr Fitzmaurice as to the manner in which the Agreement operated according to its terms. But even that more limited challenge was not advanced during the final hearing by Mr Compton.

76 It is concluded that the affidavit of Mr Fitzmaurice provides more than adequate support for a finding that the indebtedness of Mr Compton to Ramsay Health Care is for a sum greater than $5,000. The reason for expressing this finding in that manner is to leave it to those administering the bankrupt estate of Mr Compton to finally determine what is the true state of indebtedness.

77 If any consideration is separately given to the onus placed upon Mr Compton to establish that he owes a sum less than $5,000, he has failed to discharge that onus. The calculations performed by Ms Stevis, with respect, have proved unreliable. Even if attention is confined to the greater sums of monies said to be in question, her calculations of those sums has proved to be unreliable.

78 The discretion conferred by s 52(1) of the Bankruptcy Act to make a sequestration order is exercised in favour of Ramsay Health Care.

THE ORDERS OF THE COURT ARE

1. Pursuant to s 136 of the Evidence Act 1995 (Cth), the use of the affidavit of Anna Stevis sworn 4 September 2015 (Exhibit 5), the affidavit of Graham Baker sworn 31 May 2017 (Exhibit 6) and the spreadsheet marked Exhibit 7 be confined to evidence of the claims made, but not evidence of the supporting factual basis of the claims.

2. The estate of Adrian John Compton be sequestrated under the Bankruptcy Act 1966 (Cth).

3. The Applicant Creditor’s costs be taxed and paid from the estate of the Respondent Debtor in accordance with the Bankruptcy Act 1966 (Cth).

4. Order 2 is stayed until 4:00pm on 2 June 2017.

AND THE COURT NOTES THAT:

1. The date of the act of bankruptcy is 21 May 2015.

2. A Consent to Act as Trustee signed by Barry Anthony Taylor has been filed under section 156A of the Bankruptcy Act 1966.

I certify that the preceding seventy-eight (78) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Flick. |

Associate: