FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Avestra Asset Management Limited (In Liquidation) [2017] FCA 497

ORDERS

DATE OF ORDER: |

THE COURT DECLARES THAT:

Declarations of contravention by Avestra

(a) Direct use of scheme property of the Advantage Fund to acquire shares in AG Financial

1. Between 20 and 21 March 2013, by making an off-market purchase of 230,000 shares in Excela Ltd (referred to in these declarations as “AG Financial”) on behalf of the Advantage Fund, Avestra Asset Management Limited (in liquidation) (Avestra), as the responsible entity of the Advantage Fund, gave a financial benefit out of the scheme property of the Advantage Fund to itself without obtaining approval of the members of the Advantage Fund in accordance with ss 217-227 of the Corporations Act 2001 (Cth) (the Act), and thereby contravened s 208(1) (as modified by s 601LC) of the Act.

(a) 4.2 million newly-issued shares in AG Financial on behalf of the Advantage Fund on or around 30 May 2013; and

(b) 16.7 million newly-issued shares in AG Financial on behalf of the Advantage Fund on or around 12 July 2013,

Avestra, as the responsible entity of the Advantage Fund, gave financial benefits out of the scheme property of the Advantage Fund to itself, and to AG Financial, being a related party of Avestra, without obtaining approval of the members of the Advantage Fund in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

3. In making each of the purchases of shares in AG Financial on behalf of the Advantage Fund referred to in paragraphs 1 and 2, Avestra was in a position of conflict between:

(a) Avestra’s own interests in furthering its commercial objective of achieving a merger of the Avestra and AG Financial businesses; and

(b) the interests of the members of the Advantage Fund in the sound and professional selection of investments appropriate for the fund, made solely with a view to realising the investment objectives disclosed to members of the fund,

and failed to give priority to the members’ interests, and thereby contravened s 601FC(1)(c) of the Act between 20 March 2013 and 12 July 2013.

(b) Indirect use of scheme property of the Advantage Fund to acquire shares in AG Financial

4. Between 20 and 21 March 2013, by making an off-market purchase of 2.0 million shares in AG Financial on behalf of the Worberg Global Fund, at a time when the Advantage Fund held substantial unitholdings in the Worberg Global Fund, Avestra, as the responsible entity of the Advantage Fund, gave a financial benefit indirectly out of the scheme property of the Advantage Fund to itself without obtaining approval of the members of the Advantage Fund in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act.

(a) 8.5 million newly-issued shares in AG Financial on behalf of the Worberg Global Fund on or around 12 July 2013; and

(b) 9 million newly-issued shares in AG Financial on behalf of the Worberg Global Fund on or around 19 July 2013,

when the Advantage Fund held substantial unitholdings in the Worberg Global Fund, Avestra, as the responsible entity of the Advantage Fund, gave financial benefits indirectly out of the scheme property of the Advantage Fund to itself, and to AG Financial, being a related party of Avestra, without obtaining approval of the members of the Advantage Fund in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

(c) Use of scheme and trust property of the Canton and Safecrest Funds to acquire shares in AG Financial

(a) 4.4 million shares in AG Financial between 20 and 21 March 2013;

(b) 17.76 million newly-issued shares in AG Financial on or around 12 July 2013; and

(c) 21 million newly-issued shares in AG Financial on or around 19 July 2013,

on behalf of the Canton Fund, when Avestra:

(d) was in a position of conflict between:

(i) Avestra’s own interests in furthering its commercial objective of achieving a merger of the Avestra and AG Financial businesses; and

(ii) the interests of the members of the Canton Fund in the sound and professional selection of investments appropriate for the fund, made solely with a view to realising the investment objectives disclosed to members of the fund; and

(e) failed to disclose that conflict of interest to, or obtain informed consent to that conflict of interest from, members of the Canton Fund,

and thereby failed to do all things necessary to ensure that it provided the financial services covered by its AFS licence efficiently, honestly and fairly, and thereby contravened s 912A(1)(a) of the Act on each occasion.

7. Avestra acquired:

(a) 500,000 shares in AG Financial on 3 July 2013;

(b) 500,000 shares in AG Financial on 4 July 2013;

(c) 7.5 million shares in AG Financial on or around 19 July 2013; and

(d) 500,000 shares in AG Financial on 1 August 2013,

on behalf of the Safecrest Fund, in furtherance of Avestra’s own commercial objective of achieving a merger of the Avestra and AG Financial businesses, and by doing so through the Safecrest Fund, concealed the use of scheme property of the Generator Fund to purchase shares in AG Financial from the books and records of the Generator Fund. Avestra thereby failed to do all things necessary to ensure that it provided the financial services covered by its AFS licence efficiently, honestly and fairly, and thereby contravened s 912A(1)(a) of the Act on each occasion.

(d) The Avestra loans

8. By advancing unsecured loans to itself from the Avestra Credit Fund:

(a) of $100,000 on 27 February 2014; and

(b) of $645,000 on 4 March 2014,

when scheme property of the Advantage, Emergent and Maximiser Funds was invested in the Avestra Credit Fund, Avestra, being the responsible entity of those funds, gave financial benefits indirectly out of the scheme property of those funds to itself, without obtaining approval of the members of those funds in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

(e) The AG Financial loans

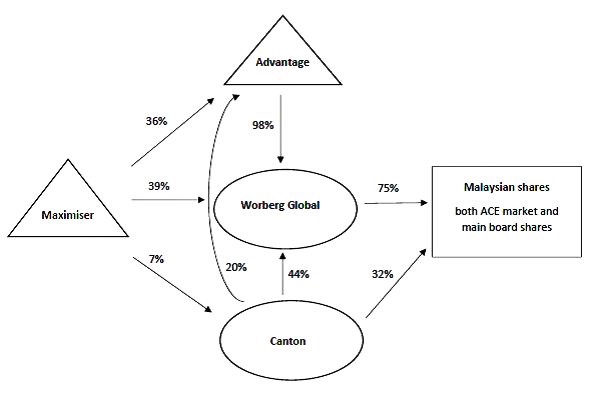

9. By advancing unsecured loans to AG Financial from the Avestra Credit Fund:

(a) of $250,000 between 20 and 25 February 2014;

(b) of $85,000 on 28 March 2014;

(c) of $90,000 on 24 April 2014;

when scheme property of the Advantage, Emergent and Maximiser Funds was invested in the Avestra Credit Fund, Avestra, being the responsible entity of those funds, gave financial benefits indirectly out of the scheme property of those funds to AG Financial, being a related party of Avestra, without obtaining approval of the members of those funds in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

10. By advancing an unsecured loan of $100,000 to AG Financial from the Avestra Credit Fund on 26 June 2014, at a time when scheme property of the Advantage, Accelerator, Emergent and Maximiser Funds was invested in the Avestra Credit Fund, Avestra, being the responsible entity of those funds, gave a financial benefit indirectly out of the scheme property of those funds to AG Financial, being a related party of Avestra, without obtaining approval of the members of those funds in accordance with ss 217-227 of the Act, in contravention of s 208(1) (as modified by s 601LC) of the Act.

(f) Investments of scheme property of the Accelerator Fund into the Avestra Credit Fund

11. By making cash investments from the Accelerator Fund into the Avestra Credit Fund:

(a) of $801,000 on or around 2 June 2014; and

(b) of $240,000 on 1 July 2014,

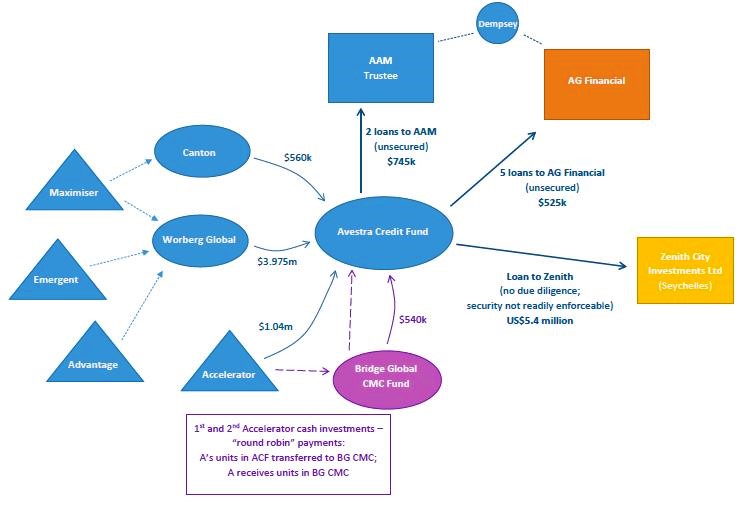

Avestra, being the responsible entity of the Accelerator Fund, gave financial benefits out of the scheme property of the Accelerator Fund to itself, in its capacity as trustee of the Avestra Credit Fund, without obtaining approval of the members of the Accelerator Fund in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

12. Between 2 June 2014 and 1 July 2014, by making the cash investments referred to in paragraph 11 from the Accelerator Fund into the Avestra Credit Fund, Avestra failed to act in the best interests of the members of the Accelerator Fund, and thereby contravened s 601FC(1)(c) of the Act.

(g) Failure to provide monthly reports for the AG Schemes

13. After becoming appointed as responsible entity of each of the Accelerator, Emergent, Generator and Maximiser Funds from 30 January 2014, Avestra failed to provide regular investment reports to members, as had been the practice prior to Bridge Global Securities’ appointment as fund manager of those schemes in April 2013, and thereby Avestra failed to do all things necessary to ensure that it provided financial services covered by its AFS licence efficiently, honestly and fairly, in contravention of s 912A(1)(a) of the Act.

(h) Non-disclosure, or inadequate disclosure, of change of investment mandate of the AG Schemes

14. Avestra failed to notify members of the Maximiser, Accelerator and Generator Funds of the material change to the investment risk, and to provide them with the information reasonably necessary to understand the nature and effect of that change in risk, as a consequence of those funds having become substantially exposed to Malaysian shares and equity derivatives, and thereby contravened s 1017B(1) of the Act on or around 7 February 2014 in respect of the Maximiser Fund, and from no later than 2 September 2014 in respect of each of the Accelerator and Generator Funds.

(i) Offshoring of the Canton Fund as the Bridge Global CMC Fund and cross-investments into the Canton Fund

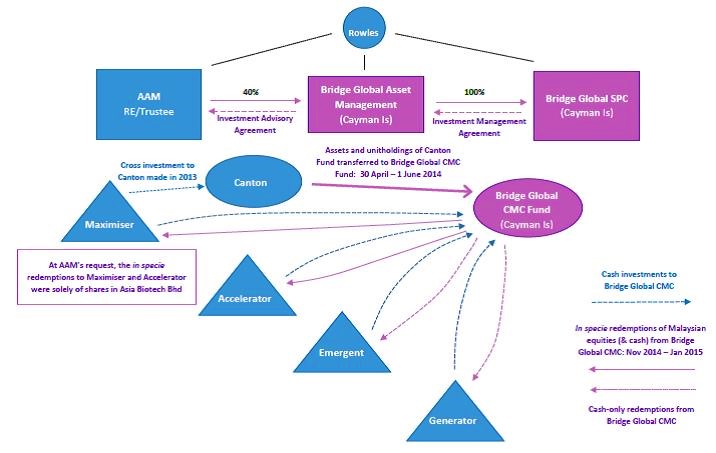

15. Between 30 April and 1 June 2014, by transferring investments held by the Canton Fund directly to the Bridge Global CMC Fund, and redeeming units held by investors (including by Avestra on behalf of the Maximiser Fund) in the Canton Fund in exchange for units in the Bridge Global CMC Fund, Avestra, being the responsible entity of the Maximiser Fund, gave a financial benefit out of the scheme property of the Maximiser Fund, to Bridge Global SPC (as operator of the Bridge Global CMC Fund), being a related party of Avestra, without obtaining approval of the members of the Maximiser Fund in accordance with ss 217-227 of the Act in contravention of s 208(1) (as modified by s 601LC) of the Act.

16. By making investments into the Bridge Global CMC Fund:

(a) of US$745,879.50 on behalf of the Accelerator Fund on 2 June 2014;

(b) of US$207,527.59 on behalf of the Generator Fund on 2 June 2014;

(c) of US$227,816.66 on behalf of the Accelerator Fund on 1 July 2014;

(d) of US$73,477.99 on behalf of the Emergent Fund on 1 October 2014; and

(e) of US$317,529.89 on behalf of the Maximiser Fund on 1 October 2014,

Avestra, being the responsible entity of the Accelerator, Generator, Emergent and Maximiser Funds, gave financial benefits out of the scheme property of those funds to Bridge Global SPC (as operator of the Bridge Global CMC Fund), being a related party of Avestra, without obtaining approval of the members of those funds in accordance with ss 217-227 of the Act, and thereby contravened s 208(1) (as modified by s 601LC) of the Act on each occasion.

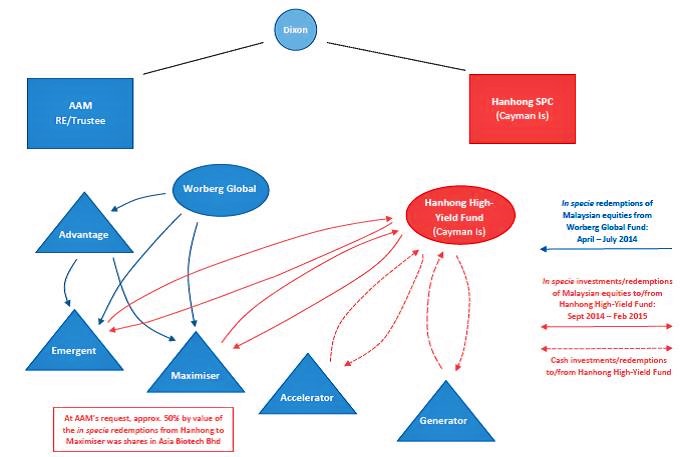

(j) In specie redemptions from the Worberg Global Fund and reinvestment of scheme property of the Emergent and Maximiser Funds into the Hanhong High-Yield Fund

17. Between 1 April 2014 and 1 February 2015, by making in specie redemptions of investments held by the Emergent and Maximiser Funds in the Worberg Global Fund, and substantially reinvesting the Malaysian shares and equity derivatives received by those redemptions into the Hanhong High-Yield Fund and then making in specie redemptions from the Hanhong High-Yield Fund to the Emergent and Maximiser Funds, with the result that the Emergent and Maximiser Funds were left holding extremely high weightings of shares and equity derivatives in a limited number of Malaysian-listed companies, Avestra failed to exercise the degree of care and diligence that a reasonable person would exercise if they were in Avestra’s position as responsible entity of those funds, in contravention of s 601FC(1)(b) of the Act.

(k) Management of conflicts of interest

18. At all times from 20 March 2013 until 1 February 2015, Avestra did not have in place adequate arrangements for the management of conflicts of interest arising wholly, or partially, in the provision of financial services by Avestra as part of its financial services business, in contravention of s 912A(1)(aa) of the Act.

Declarations of contravention by Rowles

(a) Direct use of scheme property of the Advantage Fund to acquire shares in AG Financial

19. Paul John Rowles (Rowles) authorised each of the acquisitions of shares referred to in paragraphs 1 and 2, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

20. Rowles authorised the acquisitions of shares referred to in paragraph 3, and was thereby involved in Avestra’s contravention of s 601FC(1)(c) of the Act, in contravention of s 601FC(5) of the Act.

(b) Indirect use of scheme property of the Advantage Fund to acquire shares in AG Financial

21. Rowles authorised each of the acquisitions of shares referred to in paragraphs 4 and 5, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(c) Use of scheme and trust property of the Canton and Safecrest Funds to acquire shares in AG Financial

22. Rowles authorised each of the transactions on behalf of the Canton and Safecrest Funds referred to in paragraphs 6 and 7, and in so doing failed to exercise his powers and discharge his duties with the degree of care and diligence that a reasonable person would exercise if they were a director or officer of a corporation in Avestra’s circumstances and occupied the office held by Rowles, and had the same responsibilities within the corporation as Rowles, in contravention of s 180(1) of the Act.

(d) Investment of scheme property of the Emergent, Generator and Maximiser Funds into the Advantage, Canton, Worberg Global and Safecrest Funds

23. Rowles authorised Bridge Global Securities, as an agent of the responsible entity of the Emergent and Maximiser Funds, to give financial benefits, namely cash investments:

(a) of $600,000, out of the scheme property of the Emergent Fund into the Advantage Fund on 1 May 2013;

(b) of $1.6 million, out of the scheme property of the Maximiser Fund into the Advantage Fund on 1 May 2013; and

(c) of $400,000, out of the scheme property of the Maximiser Fund into the Advantage Fund between 1 and 2 July 2013,

to Avestra in its capacity as responsible entity of the Advantage Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Emergent and Maximiser Funds in accordance with ss 217-227 of the Act. Rowles was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

24. Rowles authorised Bridge Global Securities, as an agent of the responsible entity of the Maximiser Fund, to give a financial benefit, namely a cash investment of $380,000, out of the scheme property of the Maximiser Fund into the Canton Fund on 1 August 2013, to Avestra in its capacity as trustee of the Canton Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Maximiser Fund in accordance with ss 217-227 of the Act. Rowles was thereby involved in Bridge Global Securities’ contravention of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act.

25. Rowles authorised Bridge Global Securities, as an agent of the responsible entity of the Emergent and Maximiser Funds to give financial benefits, namely cash investments:

(a) of $616,560, out of the scheme property of the Emergent Fund into the Worberg Global Fund on 1 May 2013;

(b) of $1.64 million, out of the scheme property of the Maximiser Fund into the Worberg Global Fund on 1 May 2013; and

(c) of $383,520, out of the scheme property of the Maximiser Fund into the Worberg Global Fund between 1 and 2 July 2013,

to Avestra in its capacity as trustee of the Worberg Global Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Emergent and Maximiser Funds in accordance with ss 217-227 of the Act. Rowles was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

26. Rowles authorised Bridge Global Securities, as an agent of the responsible entity of the Generator Fund, to give financial benefits, namely cash investments:

(a) of $300,000, out of the scheme property of the Generator Fund into the Safecrest Fund between 1 and 2 July 2013; and

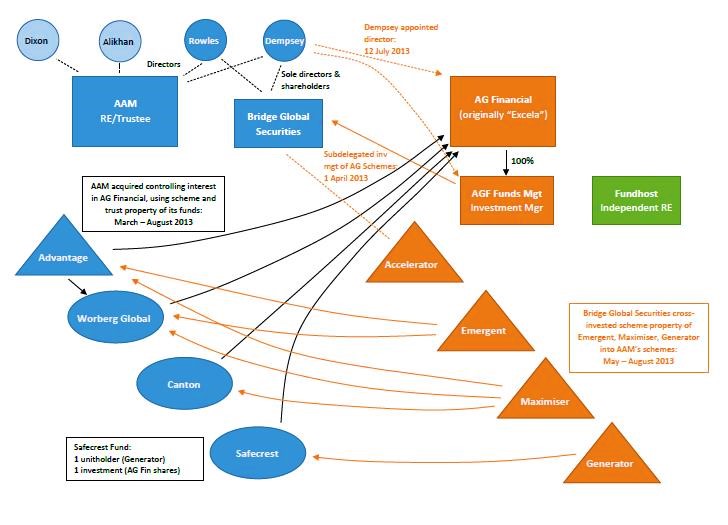

(b) of $125,000, out of the scheme property of the Generator Fund into the Safecrest Fund on 2 August 2013,

to Avestra in its capacity as trustee of the Safecrest Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Generator Fund in accordance with ss 217-227 of the Act. Rowles was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(e) Substantial shareholder notice contraventions

27. Rowles made, or authorised the making of, statements contained in substantial shareholder notices that Avestra gave to the ASX Limited on 5 April 2013, that were to Rowles’s knowledge misleading in a material respect, in that the notices disclosed only the voting power obtained by the Canton Fund and the Worberg Global Fund in AG Financial, and omitted to disclose the voting power in AG Financial that Avestra had obtained through the share purchases it made on 20 and 21 March 2013, in contravention of s 1308(2) of the Act.

28. Rowles failed to take all steps that a reasonable person would take, if they were in Rowles’s position, to ensure that Avestra did not acquire relevant interests in AG Financial in contravention of s 606(1) of the Act:

(a) between 20 and 21 March 2013;

(b) on 30 May 2013; and

(c) between 24 June 2013 and 2 August 2013;

and Rowles thereby contravened s 601FD(1)(f)(i) of the Act on each occasion.

29. Rowles failed to take all steps that a reasonable person would take, if they were in Rowles’s position, to ensure that Avestra did not fail:

(a) to give the required information about a substantial holding in AG Financial between 26 March 2013 and 5 April 2013;

(b) to lodge a substantial shareholding notice in respect of AG Financial on or around 3 June 2013; and

(c) to give the required information about a substantial holding in AG Financial between 6 July 2013 and 6 August 2013,

in contravention of s 671B(1) of the Act, and Rowles thereby contravened s 601FD(1)(f)(i) of the Act on each occasion.

(f) The Avestra loans

30. Rowles authorised the advancement of each of the loans by Avestra from the Avestra Credit Fund to itself referred to in paragraph 8, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(g) The AG Financial loans

31. Rowles authorised the advancement of each of the loans by Avestra from the Avestra Credit Fund to AG Financial referred to in paragraphs 9 and 10, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(h) Investments of scheme property of the Accelerator Fund into the Avestra Credit Fund

32. Rowles authorised the making of each of the investments by Avestra from the Accelerator Fund to the Avestra Credit Fund referred to in paragraph 11, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

33. Rowles authorised the cash investments from the Accelerator Fund into the Avestra Credit Fund referred to in paragraph 12, and was thereby involved in Avestra’s contravention of s 601FC(1)(c) of the Act, in contravention of s 601FC(5) of the Act.

(i) The Zenith loan agreement

34. Rowles authorised Avestra’s entry into a loan agreement with, and advancing US$6.0 million to, Zenith City Investments Ltd out of the Avestra Credit Fund on or around 6 May 2014, without having taken reasonable steps to ensure that Avestra had carried out adequate due diligence and obtained adequate security in respect of the loan, and in so doing failed to exercise his powers and discharge his duties with the degree of care and diligence that a reasonable person would exercise if they were a director or officer of a corporation in Avestra’s circumstances and occupied the office held by Rowles, and had the same responsibilities within the corporation as Rowles, in contravention of s 180(1) of the Act.

(j) Failure to provide monthly reports for the AG Schemes

35. Rowles failed to take all steps that a reasonable person would take, if they were in Rowles’s position, to ensure that Avestra complied with s 912A(1)(a) of the Act by providing regular investor reports to members of the Accelerator, Emergent, Generator and Maximiser Funds, and thereby contravened s 601FD(1)(f)(i) of the Act from 30 January 2014.

(k) Non-disclosure, or inadequate disclosure, of change of investment mandate of the AG Schemes

36. Rowles failed to take all steps that a reasonable person would take, if they were in Rowles’s position, to ensure that Avestra complied with s 1017B(1) of the Act with regard to the changed investment risk of the Maximiser, Accelerator and Generator Funds, and thereby contravened s 601FD(1)(f)(i) of the Act from 30 January 2014 in respect of the Maximiser Fund, and from no later than 2 September 2014 in respect of each of the Accelerator and Generator Funds.

(l) Offshoring of the Canton Fund as the Bridge Global CMC Fund and cross-investments into the Canton Fund

37. Rowles authorised the making of the transfers and redemptions referred to in paragraph 15, and was thereby involved in Avestra’s contravention of s 208(1) (as modified by s 601LC) of the Act, in contravention of s 209(2) (as modified by s 601LA) of the Act.

38. Rowles authorised the making of each of the investments referred to in paragraph 16, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(m) In specie redemptions from the Worberg Global Fund and reinvestment of scheme property of the Emergent and Maximiser Funds into the Hanhong High-Yield Fund

39. Rowles authorised the redemptions and investments referred to in paragraph 17, and was thereby involved in Avestra’s contravention of s 601FC(1)(b), in contravention of s 601FC(5) of the Act.

(n) Management of conflicts of interest

40. Rowles failed to take all steps that a reasonable person in Rowles’s position would have taken to ensure that Avestra did not contravene s 912A(1)(aa) of the Act, and thereby contravened s 601FD(1)(f)(i) of the Act between 20 March 2013 and 6 January 2015.

Declarations of contravention by Dempsey

(a) Direct use of scheme property of the Advantage Fund to acquire shares in AG Financial

41. Clayton Dempsey (Dempsey) was knowingly concerned in each of the acquisitions of shares referred to in paragraphs 1 and 2, and was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

42. Dempsey was knowingly concerned in the acquisitions of shares referred to in paragraph 3, and was thereby involved in Avestra’s contravention of s 601FC(1)(c) of the Act, in contravention of s 601FC(5) of the Act.

(b) Indirect use of scheme property of the Advantage Fund to acquire shares in AG Financial

43. Dempsey was knowingly concerned in each of the acquisitions of shares referred to in paragraphs 4 and 5, and was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(c) Use of scheme and trust property of the Canton and Safecrest Funds to acquire shares in AG Financial

44. Dempsey was knowingly concerned in each of the transactions on behalf of the Canton and Safecrest Funds referred to in paragraphs 6 and 7, and in so doing failed to exercise his powers and discharge his duties with the degree of care and diligence that a reasonable person would exercise if they were a director or officer of a corporation in Avestra’s circumstances and occupied the office held by Dempsey, and had the same responsibilities within the corporation as Dempsey, in contravention of s 180(1) of the Act.

(d) Investment of scheme property of the Emergent, Generator and Maximiser Funds into the Advantage, Canton, Worberg Global and Safecrest Funds

45. Dempsey was knowingly concerned in Bridge Global Securities, as an agent of the responsible entity of the Emergent and Maximiser Funds, giving financial benefits, namely cash investments:

(a) of $600,000 cash, out of the scheme property of the Emergent Fund into the Advantage Fund on 1 May 2013;

(b) of $1.6 million, out of the scheme property of the Maximiser Fund into the Advantage Fund on 1 May 2013; and

(c) of $400,000, out of the scheme property of the Maximiser Fund into the Advantage Fund between 1 and 2 July 2013,

to Avestra in its capacity as responsible entity of the Advantage Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Emergent and Maximiser Funds in accordance with ss 217-227 of the Act. Dempsey was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

46. Dempsey was knowingly concerned in Bridge Global Securities, as an agent of the responsible entity of the Maximiser Fund, giving a financial benefit, namely a cash investment of $380,000, out of the scheme property of the Maximiser Fund into the Canton Fund on 1 August 2013, to Avestra, in its capacity as trustee of the Canton Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Maximiser Fund in accordance with ss 217-227 of the Act. Dempsey was thereby involved in Bridge Global Securities’ contravention of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act.

47. Dempsey was knowingly concerned in Bridge Global Securities, as an agent of the responsible entity of the Emergent and Maximiser Funds, giving financial benefits, namely cash investments:

(a) of $616,560, out of the scheme property of the Emergent Fund into the Worberg Global Fund on 1 May 2013;

(b) of $1.64 million, out of the scheme property of the Maximiser Fund into the Worberg Global Fund on 1 May 2013; and

(c) of $383,520, out of the scheme property of the Maximiser Fund into the Worberg Global Fund between 1 and 2 July 2013,

to Avestra, in its capacity as trustee of the Worberg Global Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Emergent and Maximiser Funds in accordance with ss 217-227 of the Act. Dempsey was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

48. Dempsey was knowingly concerned in Bridge Global Securities, as an agent of the responsible entity of the Generator Fund, giving financial benefits, namely cash investments:

(a) of $300,000, out of the scheme property of the Generator Fund into the Safecrest Fund between 1 and 2 July 2013; and

(b) of $125,000, out of the scheme property of the Generator Fund into the Safecrest Fund on 2 August 2013,

to Avestra, in its capacity as trustee of the Safecrest Fund, a related party of Bridge Global Securities, without obtaining approval of the members of the Generator Fund in accordance with ss 217-227 of the Act. Dempsey was thereby involved in contraventions by Bridge Global Securities of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(e) Substantial shareholder notice contraventions

49. Dempsey failed to take all steps that a reasonable person would take, if they were in Dempsey’s position, to ensure that Avestra did not acquire relevant interests in AG Financial in contravention of s 606(1) of the Act:

(a) between 20 and 21 March 2013;

(b) on 30 May 2013; and

(c) between 24 June 2013 and 2 August 2013,

and thereby contravened s 601FD(1)(f)(i) of the Act on each occasion.

50. Dempsey failed to take all steps that a reasonable person would take, if they were in Dempsey’s position, to ensure that Avestra did not fail:

(a) to give the required information about a substantial holding in AG Financial between 26 March 2013 and 5 April 2013;

(b) to lodge a substantial shareholding notice in respect of AG Financial on or around 3 June 2013; and

(c) to give the required information about a substantial holding in AG Financial between 6 July 2013 and 6 August 2013,

in contravention of s 671B(1) of the Act, and thereby contravened s 601FD(1)(f)(i) of the Act on each occasion.

(f) The Avestra loans

51. Dempsey authorised the advancement of each of the loans by Avestra from the Avestra Credit Fund to itself referred to in paragraph 8, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(g) The AG Financial loans

52. Dempsey authorised the advancement of each of the loans by Avestra from the Avestra Credit Fund to AG Financial referred to in paragraphs 9 and 10, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(h) Investments of scheme property of the Accelerator Fund into the Avestra Credit Fund

53. Dempsey authorised the making of each of the investments by Avestra from the Accelerator Fund to the Avestra Credit Fund referred to in paragraph 11, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

54. Dempsey authorised the cash investments from the Accelerator Fund into the Avestra Credit Fund referred to in paragraph 12, and was thereby involved in Avestra’s contravention of s 601FC(1)(c) of the Act, in contravention of s 601FC(5) of the Act.

(i) The Zenith loan agreement

55. Dempsey authorised Avestra’s entry into a loan agreement with, and advancing US$6.0 million to, Zenith City Investments Ltd out of the Avestra Credit Fund on or around 6 May 2014, without having taken reasonable steps to ensure that Avestra had carried out adequate due diligence and obtained adequate security in respect of the loan, and in so doing failed to exercise his powers and discharge his duties with the degree of care and diligence that a reasonable person would exercise if they were a director or officer of a corporation in Avestra’s circumstances and occupied the office held by Dempsey, and had the same responsibilities within the corporation as Dempsey, in contravention of s 180(1) of the Act.

(j) Failure to provide monthly reports for the AG Schemes

56. Dempsey failed to take all steps that a reasonable person would take, if they were in Dempsey’s position, to ensure that Avestra complied with s 912A(1)(a) of the Act by providing regular investor reports to members of the Accelerator, Emergent, Generator and Maximiser Funds, and thereby contravened s 601FD(1)(f)(i) of the Act from 30 January 2014.

(k) Non-disclosure, or inadequate disclosure, of change of investment mandate of the AG Schemes

57. Dempsey failed to take all steps that a reasonable person would take, if they were in Dempsey’s position, to ensure that Avestra complied with s 1017B(1) of the Act with regard to the changed investment risk of the Maximiser, Accelerator and Generator Funds, and thereby contravened s 601FD(1)(f)(i) of the Act from 7 February 2014 in respect of the Maximiser Fund, and from no later than 2 September 2014 in respect of each of the Accelerator and Generator Funds.

(l) Offshoring of the Canton Fund as the Bridge Global CMC Fund and cross-investments into the Canton Fund

58. Dempsey authorised the making of the transfers and redemptions referred to in paragraph 15, and was thereby involved in Avestra’s contravention of s 208(1) (as modified by s 601LC) of the Act, in contravention of s 209(2) (as modified by s 601LA) of the Act.

59. Dempsey was knowingly concerned in the making of each of the investments referred to in paragraph 16, was thereby involved in Avestra’s contraventions of s 208(1) (as modified by s 601LC) of the Act, and thereby contravened s 209(2) (as modified by s 601LA) of the Act on each occasion.

(m) In specie redemptions from the Worberg Global Fund and reinvestment of scheme property of the Emergent and Maximiser Funds into the Hanhong High-Yield Fund

60. Dempsey authorised the redemptions and investments referred to in paragraph 17, and was thereby involved in Avestra’s contravention of s 601FC(1)(b), in contravention of s 601FC(5) of the Act.

(n) Management of conflicts of interest and Dempsey’s conduct as a member of the compliance committee

61. In his role as the sole executive member of Avestra’s compliance committee for the Advantage Fund and for the AG Schemes (from 30 January 2014), Dempsey failed to inform the compliance committee of numerous conflicts of interest and potential contraventions of the Act arising in connection with Avestra’s operation of the Advantage Fund and the AG Schemes, and thereby failed to exercise the degree of care and diligence that a reasonable person would exercise if they were in Dempsey’s position, in contravention of s 601JD(1)(b) of the Act between 20 March 2013 and 1 February 2015.

AND THE COURT ORDERS THAT:

62. Pursuant to s 1324(1) of the Act, Rowles be restrained, whether by himself, his servants, agents and employees or otherwise, from:

(a) carrying on a business related to, concerning or directed to financial products or financial services within the meaning of s 761A of the Act;

(b) providing financial product advice within the meaning of s 761A of the Act; or

(c) dealing in financial products within the meaning of s 761A of the Act,

for ten years from the date of this order.

63. Pursuant to ss 206C(1) and/or 206E(1) of the Act, Rowles be disqualified from managing corporations for ten years from the date of this order.

64. Pursuant to s 1324(1) of the Act, Dempsey be restrained, whether by himself, his servants, agents and employees or otherwise, from:

(a) carrying on a business related to, concerning or directed to financial products or financial services within the meaning of s 761A of the Act;

(b) providing financial product advice within the meaning of s 761A of the Act; or

(c) dealing in financial products within the meaning of s 761A of the Act,

for ten years from the date of this order.

65. Pursuant to ss 206C(1) and/or 206E(1) of the Act, Dempsey be disqualified from managing corporations for ten years from the date of this order.

66. There be no order for costs as between ASIC and Avestra and Rowles.

67. Dempsey pay ASIC’s costs of the proceeding fixed in the sum of $25,000.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BEACH J:

1 ASIC has brought the present proceedings against the corporate defendant and some of its former directors seeking declarations, injunctions and disqualification orders for, inter alia, contraventions of ss 180, 208(1) (modified by s 601LC), 209(2) (modified by s 601LA), 601FC, 601FD, 606, 671B, 912A, 1017B and 1308 of the Corporations Act 2001 (Cth) (the Act). Let me explain the context.

2 In March 2013, the first defendant, Avestra Asset Management Ltd (in liquidation) (Avestra) sought to obtain a majority interest in the shares of Excela Ltd, now known as Ennox Group Ltd, but between 29 November 2013 and 13 April 2016 known as AG Financial Ltd (AG Financial). AG Financial was an ASX-listed company whose subsidiaries were engaged in funds management and stockbroking. Avestra’s intention was to achieve a merger of the businesses of the Avestra group and the AG Financial group and in essence to achieve a back door listing for Avestra.

3 Avestra acquired an initial interest of 22% in AG Financial through off-market transactions with Peter Spann, the CEO of AG Financial. Several directors of Avestra, being the second defendant, Paul Rowles (Rowles), and the third defendant, Clayton Dempsey (Dempsey), also purchased smaller shareholdings in AG Financial for their respective superannuation funds, as did other entities associated with Avestra and its other directors.

4 In initiating and completing this strategy, Avestra did not use its own financial resources. Rather, it used funds that it held on trust as property of its sole registered managed investment scheme at the time and various unregistered wholesale managed investment schemes of which it was the responsible entity or trustee. Those transactions involved a conflict of interest between:

(a) Avestra’s own interest, being the pursuit of its objective of seeking to grow and benefit the business it conducted in its own right through acquiring and merging with AG Financial; and

(b) the interests of the members of its registered and wholesale schemes; their interests were to have scheme property invested in the best interests of scheme members, consistently with the investment objectives and risks that had been disclosed in relevant product disclosure statements and information memoranda.

5 Avestra purchased shares in AG Financial with such members’ funds in disregard of that conflict and without disclosing the proposed purchase to, or obtaining approval from, members of those schemes whose property Avestra had used to carry out its acquisition. Avestra also contravened the s 606 prohibition on acquiring more than 20% of voting shares in a listed company (s 606(1)(a)(i)) without making a takeover offer. That consequence was also facilitated by Avestra’s failure to disclose the extent of its own relevant interest(s) (as opposed to each scheme’s separate interests) in the voting shares of AG Financial.

6 And so began an extensive sequence of conflicts of interest and contraventions of the Act that followed throughout 2013 and 2014 by Avestra, Rowles and Dempsey.

7 Avestra’s conduct and that of Rowles and Dempsey throughout the relevant period demonstrated a systematic disregard of the conflicts of interest inherent in the transactions that Avestra carried out through its registered and wholesale investment schemes. In essence, Avestra repeatedly failed to:

(a) obtain member approval for related party transactions carried out directly or indirectly using scheme property;

(b) act in the best interests of members of the schemes and in particular to give priority to members’ interests in the event of a conflict with Avestra’s own interests; and

(c) ensure that Avestra did all things necessary to provide financial services efficiently, honestly and fairly.

8 A related failure of Avestra was that it failed to make appropriate or required disclosure to members of the schemes, particularly members of its registered managed investment scheme(s) pre and post its AG Financial acquisition strategy. In fact, Avestra took steps that had the effect of concealing matters from those investors. In particular:

(a) Avestra did not disclose or seek member approval of related party transactions; and

(b) Avestra carried out certain transactions in a manner that made the true use of scheme property invisible to any enquiring fund member.

9 Another feature of Avestra’s conduct was that the scheme property of a group of registered schemes known as the “AG Schemes” (I will elaborate on the detail of the AG Schemes later) became heavily invested in Malaysian shares and equity derivatives, including securities in a number of companies listed on the second-board “ACE market” of Bursa Malaysia. But except in the case of the Emergent Fund (one of the AG Schemes), the product disclosure statements for the AG Schemes had not disclosed that those funds would invest heavily in emerging-markets securities. Avestra did not give meaningful or adequate notification of the material changes in investment risk to members of those schemes. Moreover, after a sequence of in specie investments and redemptions between the AG Schemes and two Cayman Islands funds established in 2014 (the Bridge Global CMC Fund and the Hanhong High-Yield Fund), three of the four AG Schemes were left in early 2015 with very substantial and concentrated direct holdings of Malaysian shares and equity derivatives in a limited number of companies, including ACE market-listed companies.

10 Further, Avestra’s repeated engagement in undisclosed related party transactions, and its failure to act appropriately in the best interests of scheme members, resulted in the investment portfolios of the Accelerator and Maximiser Funds (two of the AG Schemes) becoming heavily exposed to high-risk investments that were at odds with the investment strategy and risks that had been presented to the retail investors in those schemes.

11 Generally, the conduct of Avestra was not in the best interests of scheme members, and appears to have been undertaken for the purpose of avoiding its statutory obligations and regulatory oversight. Regardless, objectively assessed, it was undertaken in contravention of the statutory protections for related party transactions and the behavioural standards of responsible entities.

12 A further dimension to Avestra’s conduct and the problems that occurred arose from its ability and predilection to invest the property from its registered scheme(s) in unregistered schemes. It is notable that prior to 2007 a registered managed investment scheme was prohibited from investing scheme property in any managed investment scheme that was not itself registered under s 601EB: former s 601FC(4). That prohibition was originally imposed to prevent a responsible entity from avoiding the scheme property protections that applied to registered schemes by investing the scheme property of a registered scheme into an unregistered managed investment scheme. For reasons that attracted itself to others, that prohibition was lifted in 2007 by the Corporations Legislation Amendment (Simpler Regulatory System) Act 2007 (Cth), Sch 1, cl 66 in the context of the following optimistic sentiment:

Increasingly registered managed investment schemes seek to diversify their investments among a range of foreign collective investment structures or focus on overseas investments. Generally such investment is not for the purpose of avoiding regulation and is directed to the best interests of members. (Explanatory memorandum to the Corporations Legislation Amendment (Simpler Regulatory System) Bill 2007 (Cth) at [1.38])

13 Further, as to the relevant individuals that ASIC has pursued, by reason of their involvement in Avestra’s conduct, both Rowles and Dempsey fell significantly short of the standards expected of directors of a responsible entity and of a financial services licensee.

the present proceedings

14 Before delving further into the detail of this matter, it is convenient to set out the background of the litigation.

(a) Provisional liquidation and liquidation of Avestra

15 On 9 September 2015, ASIC filed its originating process seeking orders that Avestra be wound up and that an official liquidator be appointed for the purposes of that winding up on the s 461(1)(k) ground of the Act that it was just and equitable to do so. The originating process also sought interim orders for the appointment of a provisional liquidator to Avestra pursuant to s 472(2).

16 ASIC alleged that Avestra was unfit to continue to act as a responsible entity or as a trustee of any managed investment schemes. ASIC sought a provisional liquidator to assume control over Avestra and its managed investment schemes, and to report to the Court and ASIC on matters including Avestra’s assets and liabilities, scheme assets controlled by it, and whether each of the schemes should be wound up or should continue to operate.

17 ASIC alleged that Avestra’s unfitness was demonstrated by the following matters:

(a) First, there had been persistent failures to recognise, and to appropriately resolve, conflicts between the interests of Avestra and its associates, and the interests of scheme members.

(b) Second, there were reasonable grounds to suspect that Avestra had committed multiple contraventions of the Act which related in essence to prohibitions on, and the obligation to manage or prevent conflicts of interests.

(c) Third, there had been repeated investments of scheme property of retail schemes into wholesale funds operated by Avestra or its associates, both in Australia and in the Cayman Islands.

(d) Fourth, one of the two central individuals responsible for Avestra’s conduct accepted that Avestra lacked expertise to operate the schemes.

(e) Fifth, there had been grossly inadequate supervision of key investment decisions.

(f) Sixth, there were considerably deficient conflict management procedures at Avestra and its related fund manager entities.

(g) Seventh, there had been a lack of disclosure to scheme members, both as to the conflicts of interest associated with the transactions involving Avestra and its schemes, and as to the composition of the schemes’ investment portfolios.

(h) Eighth, there had been multiple instances of failure to supply information formally requested by ASIC under various statutory notices.

18 On 27 October 2015, I made an order pursuant to s 472(2) of the Act appointing Simon Alexander Wallace-Smith of Deloitte Touche Tohmatsu and Richard Hughes of Deloitte Touche Tohmatsu as joint and several provisional liquidators of Avestra. My orders also directed the provisional liquidators to provide to the Court and to ASIC within 42 days of their appointment a report as to the provisional liquidation of Avestra. That report was to address matters including the assets and liabilities of Avestra and any suspected contraventions of the Act by Avestra or any of its current or former directors or any other person, whether in relation to any of Avestra’s schemes or otherwise. I adjourned the further hearing of ASIC’s originating process and its interlocutory application to 11 December 2015.

19 On 7 December 2015, the provisional liquidators issued their report on the provisional liquidation of Avestra. That report recommended, inter alia, the winding up of the Advantage Fund, the Accelerator Fund, the Emergent Fund, the Generator Fund and the Maximiser Fund. In light of that report, on 11 December 2015 ASIC filed an interlocutory application seeking an order pursuant to s 601ND(1)(a) of the Act that Avestra wind up each of the aforementioned registered schemes on the basis that it would be just and equitable to do so. On 11 December 2015, I made the order sought for the winding up of those registered schemes and also ordered under s 601NF(1) of the Act that the provisional liquidators be appointed to take responsibility for ensuring that each scheme be wound up in accordance with its constitution and for any orders that may be made under s 601NF(2). I adjourned the originating process to 19 February 2016.

20 On 17 February 2016, the provisional liquidators issued a further report which provided an update on the progress of the provisional liquidation of Avestra and the windings up of the Advantage Fund, the Accelerator Fund, the Emergent Fund, the Generator Fund and the Maximiser Fund. The provisional liquidators recommended that Avestra be placed into liquidation.

21 On 19 February 2016, I made orders for the winding up of Avestra on the basis that it was just and equitable to do so. The provisional liquidators were appointed as joint and several liquidators of Avestra. I also granted leave to ASIC to amend the originating process and to proceed against Avestra in liquidation.

(b) Enforcement proceedings against the parties

22 On 21 April 2016, ASIC filed an interlocutory application seeking orders to join Rowles and Dempsey as the second and third defendants respectively. ASIC’s application also sought, in essence, to amend the originating application to seek relief in the form of declarations of contraventions against Avestra, Rowles and Dempsey, and disqualification orders and injunctions against Rowles and Dempsey.

23 On 29 April 2016, I granted the orders sought by ASIC in its interlocutory application. ASIC subsequently filed an amended originating process together with a concise statement which set out the basis for the relief sought against the defendants. Subsequently, the matter then proceeded on pleadings.

24 On 25 November 2016, I set the matter down for trial on 24 April 2017 on an estimate of five days.

25 On or around 6 March 2017, ASIC and Rowles reached a settlement between them on the question of liability. On or around 20 April 2017, ASIC and Dempsey also reached a settlement on the question of liability. The parties agreed on proposed orders and declarations of contravention. Given that ASIC had resolved its claims on liability against Rowles and Dempsey, the trial date was vacated and the parties sought a hearing on the question of relief. That hearing was held on 26 April 2017.

26 Before me, a consolidated statement of agreed facts between ASIC, Rowles and Dempsey was tendered and relied upon pursuant to s 191 of the Evidence Act 1995 (Cth). Its content is too lengthy to reproduce in these reasons. I have summarised various aspects of the consolidated statement in the following sections of my reasons.

27 Before proceeding further, I should also note that I have had the benefit of detailed written submissions from Mr Jonathon Moore QC, with Mr Tom Clarke, counsel for ASIC. Their submissions display notable thoroughness and sophistication.

the relevant entities, individuals and schemes

(a) Avestra

28 Avestra was a licensed provider of financial services and the responsible entity and/or trustee of several investment funds.

29 During the period between 20 March 2013 and 1 February 2015, Avestra’s directors were Rowles who resigned on 6 January 2015, Dempsey, Rizwan Alikhan (Alikhan) and Jason Dixon (Dixon).

30 Under its Australian Financial Services Licence (AFSL), Avestra was licensed to provide general financial product advice for certain classes of financial products, deal in certain classes of financial products and operate specified registered managed investment schemes.

(b) Rowles and Dempsey

31 Avestra’s business and operations were primarily overseen by Rowles and Dempsey. Rowles was principally responsible for making investment decisions for Avestra’s various funds. Dempsey was principally responsible for compliance and administration matters.

32 The offices held by Rowles included director of Avestra at all relevant times until 6 January 2015, responsible manager under Avestra’s AFSL, director of Bridge Global Securities Pty Ltd (Bridge Global Securities) from 31 August 2011 to 9 July 2014 and then again from 20 August 2014 until 23 February 2015, director of Bridge Global Asset Management Ltd from 10 March 2014 and director of Bridge Global Absolute Return Fund SPC from 26 February 2014.

33 The offices held by Dempsey included director of Avestra, responsible manager under Avestra’s AFSL, member of Avestra’s compliance committee, director of Bridge Global Securities until 9 July 2014, director of AG Financial Ltd from 12 July 2013 until 24 September 2015 and director of AGF Funds Management Pty Ltd from 12 July 2013 until 28 September 2015.

(c) Avestra’s registered and wholesale funds

34 These proceedings concerns the following managed investment schemes of which Avestra was responsible entity or trustee:

Avestra-established registered scheme | Avestra’s wholesale schemes | The AG Schemes (Avestra took over as responsible entity of the AG Schemes on 30 January 2014) (registered schemes) |

Advantage Fund | Worberg Global Fund Canton Fund Safecrest Fund Avestra Credit Fund | Accelerator Fund Emergent Fund Generator Fund Maximiser Fund |

The Advantage Fund

35 The Avestra Advantage Fund (the Advantage Fund) was registered with ASIC on 16 April 2009. Avestra has been responsible entity of the Advantage Fund since its inception.

36 The replacement product disclosure statement (PDS) for the Advantage Fund, issued on 19 December 2012, indicated that the fund had a broad investment mandate:

The Fund will invest in listed Australian and international shares, Australian and International Exchange Traded Funds, hybrid securities, and option, Derivatives including Futures, CFDs and Margin Foreign Exchange including Exchange Traded and Over The Counter Products, either directly or by investing in other approved funds.

37 The Constitution of the Advantage Fund includes the following provisions, regarding the responsible entity’s ability to be interested in any transactions of or with the fund:

11.3 Investment powers

… [T]he Manager may in its capacity as trustee or responsible entity of the Trust invest in, dispose of or otherwise deal with property and rights in its absolute discretion. This includes the power to invest the whole or part of the Assets in related or like trusts or such other investments as the Manager determines.

16.3 Other capacities

Subject to the Corporations Act, if the Corporations Act applies, the Manager (or its associates) may:

(a) deal with itself (as trustee or responsible entity of the Trust or in another capacity), or with any of its associates or with any Member;

(b) be interested in any contract or transaction with itself (as trustee or responsible entity of the Trust or in another capacity) or with any Member or retain for its own benefit any profits or benefits derived from any such contract or transaction; or

(c) act in the same or a similar capacity in relation to any other managed investment scheme.

(footnotes omitted)

38 Apart from sizeable cross-investments from the Canton, Emergent and Maximiser Funds, the unitholders in the Advantage Fund were otherwise made up primarily of individuals and self-managed superannuation funds.

39 The Advantage Fund’s unit price decreased from $0.75 as at 31 October 2014 to $0.43 as at 30 June 2015.

The Canton Fund

40 The Canton Mackenzie Fund (the Canton Fund) was a wholesale scheme. It had previously been a registered scheme until December 2012. Avestra became the responsible entity and trustee of the Canton Fund in October 2012.

41 The PDS for the Canton Fund issued on 22 May 2013 stated that the Canton Fund would invest across a broad range of assets, including Malaysian, Australian and Hong Kong equities:

The Canton Mackenzie Fund invests across a range of assets including Malaysian IPO’s, Australian listed securities (including shares and Exchange Traded Funds), Hong Kong equities, fixed interest securities, managed investment schemes, hybrid securities, derivatives and cash. Derivatives will also be actively utilised in the risk management process and as an alternate to buying and selling a physical security.

42 The Canton Fund invested a substantial part of its net assets directly or indirectly in Malaysian shares and equity derivatives. As at 28 February 2014, approximately 32% of its net assets were invested directly in Malaysian shares, 44% were invested in the Worberg Global Fund and 20% were invested in the Advantage Fund (which was almost entirely invested in the Worberg Global Fund).

43 On around 1 May 2014, the Canton Fund was closed down, and unitholdings in, and the investments of, the Canton Fund, were transferred offshore to the Bridge Global CMC Fund.

The Worberg Global Fund

44 Avestra was the trustee of the Worberg Global Fund from at least March 2012. Bridge Global Securities was its fund manager.

45 In the information memorandum issued on 23 March 2012, the Worberg Global Fund was described as having a broad investment mandate:

The Fund may trade, variously, in listed Australian shares, Australian exchange traded funds, hybrid securities, fixed income securities, real property and derivatives products including, but not limited to, margin foreign exchange products, over the counter equity derivatives in global markets and exchange traded futures and options and/or managed investment schemes and unlisted companies.

46 At all relevant times, the unitholders in the Worberg Global Fund were wholly comprised of the Advantage and Canton Funds, the Emergent and Maximiser Schemes, Bridge Global Securities, AG Financial and the Bridge Global CMC Fund.

47 The Worberg Global Fund invested a substantial part of its net assets directly or indirectly in Malaysian shares and equity derivatives. As at 17 March 2014, approximately 75% of its net assets were invested directly in Malaysian shares and equity derivatives.

48 Between 1 April and 1 September 2014, the Worberg Global Fund was wound down by a sequence of in specie distributions to unitholders.

The Safecrest Fund

49 The Safecrest Capital Fund (the Safecrest Fund) was established as a trust by Avestra on or around 11 April 2013. On 2 July 2013, it received its first investment out of the scheme property of the Generator Fund.

50 At all times between July and December 2013, the Safecrest Fund had only one unitholder, namely the Generator Fund, and held only one investment, being shares in AG Financial.

51 The Safecrest Fund was terminated on around 30 June 2014.

The Avestra Credit Fund

52 The Avestra Credit Fund was established as a trust by Avestra on or around 31 January 2014.

53 Between February and July 2014:

(a) cash investments of approximately $6 million were made into the Avestra Credit Fund, primarily by the Worberg, Canton, Accelerator and Bridge Global CMC Funds; and

(b) Avestra granted loans out of the Avestra Credit Fund in the total sum of approximately $7.3 million, including unsecured loans to itself and to AG Financial.

54 From 1 July 2014, all of the units in the Avestra Credit Fund were held by the Bridge Global CMC Fund.

55 Bridge Global Securities is an Australian proprietary company, which successively had the following names:

15 September 2008 – 25 March 2013 | Avestra Funds Management Pty Ltd |

26 March 2013 – 8 July 2014 | AFM Global Pty Ltd |

9 July 2014 – | Bridge Global Securities Pty Ltd |

56 Between 1 October 2012 and 14 July 2014, Bridge Global Securities was owned, as to 50% each, by CCSM Holdings Pty Ltd and PRHL Capital Pty Ltd, being companies of which Dempsey’s and Rowles’s wives were, respectively, the sole shareholder and director.

57 During the relevant period, the directors of Bridge Global Securities were:

9 March 2012 – 12 August 2013 | Rowles, Dempsey |

13 August 2013 – 8 July 2014 | Rowles, Dempsey, Dixon |

58 Bridge Global Securities was appointed by Avestra as fund manager for the Advantage, Worberg Global and Avestra Credit Funds.

59 On 1 April 2013, shortly after Avestra’s initial purchases of shares in AG Financial, Bridge Global Securities was appointed as investment sub-manager of each of the AG Schemes.

60 In this proceeding, ASIC alleged that, in its capacity as investment sub-manager for the Emergent and Maximiser Funds, Bridge Global Securities committed a number of contraventions of s 208(1) in which Rowles and Dempsey were involved. The fact of Bridge Global Securities having committed those contraventions was also relevant in that ASIC sought disqualification orders against Rowles and Dempsey under s 206E(1)(a)(i), among other provisions. ASIC has not sought declarations of contravention against Bridge Global Securities in respect of those contraventions as it is not a party to the proceeding.

(e) AG Financial and its associated companies

61 AG Financial is an ASX-listed public company, which successively has had the following names:

12 January 2010 – 28 November 2013 | Excela Ltd |

29 November 2013 – 13 April 2016 | AG Financial Ltd |

14 April 2016 – | Ennox Group Ltd |

62 AG Financial’s business was in stockbroking and funds management.

63 Prior to 20 March 2013, AG Financial was controlled by Peter Spann, its chief executive officer. Spann sold his entire shareholding in AG Financial on around 20 March 2013, which was when Avestra first began purchasing shares in AG Financial through its registered and wholesale funds.

64 On 20 March 2013, the incumbent directors of AG Financial (including Spann) resigned, and were replaced as directors by Yosse Goldberg, Delan Pagliaccio, John Margerison and Craig Burbury.

65 On 12 July 2013, Dempsey was appointed as a director of AG Financial, in place of Burbury.

66 AGF Funds Management Pty Ltd (AGF Funds Management) was a wholly-owned subsidiary of AG Financial. It was formerly named Excela Funds Management Pty Ltd, until 24 February 2014. It operated the funds management business within the AG Financial group. Most significantly, it was the fund manager of each of the AG Schemes appointed by Fundhost (the responsible entity of the AG Schemes), but subdelegated that role to Bridge Global Securities from 1 April 2013.

67 Yosse Goldberg, Delan Pagliaccio, Craig Burbury and John Margerison were appointed directors of AGF Funds Management on 20 March 2013, on the same date as their appointment as directors of AG Financial. Dempsey was appointed as a director of AGF Funds Management (alongside Goldberg and Pagliaccio) on 12 July 2013, on the same date that he was appointed as a director of AG Financial.

68 As noted above, the AG Schemes were the Accelerator Fund, the Emergent Fund, the Generator Fund and the Maximiser Fund.

69 Each of the AG Schemes was originally registered by Fundhost Ltd, which was the independent responsible entity of those funds until it was replaced by Avestra on 30 January 2014.

70 AGF Funds Management was the investment manager for each of the AG Schemes, but sub-delegated that role to Bridge Global Securities on 1 April 2013.

71 The Constitution of each of the AG Schemes contains the following provisions regarding the responsible entity’s ability to be interested in any transactions of or with the fund:

8.1 The manager may invest in any asset it chooses, subject to what it tells investors from time to time (for example, in the trust’s product disclosure statement or telling investors of any material change in investment policy in accordance with the Corporations Act).

17.7 Subject to the Corporations Act, the manager may:

(a) deal with itself (as trustee of the trust or in any other capacity), or any associate or any investor

(b) be interested in any contract or transaction with itself (as trustee of the trust or in another capacity), any associate or investor and

(c) act in the same or a similar capacity in relation to any other trust or managed investment scheme,

and retain any benefit or benefits from doing so.

The Accelerator Fund

72 The PDS issued by Fundhost for the Accelerator Fund in June 2012 described the fund’s investment mandate as follows:

The Fund primarily invests in shares within the S&P/ASX Top 50, however the Fund may at times also hold S&P/ASX Top 200 shares (or an equivalent index tracking fund) on an index weighted basis.

73 The Accelerator Fund’s unit price declined from $0.33 on 31 October 2014 to $0.17 on 30 June 2015.

74 As at 31 October 2015, there were approximately 128 unitholders in the Accelerator Fund, overwhelmingly comprised of individuals and self-managed superannuation funds.

75 As noted below, by 31 January 2015, approximately 76% of the assets of the Accelerator Fund were invested in Malaysian equities, of which 72% was invested in the shares of a single company, Asia Biotech Bhd.

The Emergent Fund

76 Unlike the Accelerator, Generator and Maximiser Funds, the Emergent Fund was established and promoted as an emerging markets fund. The PDS issued by Fundhost for the Emergent Fund in June 2012 described the fund’s investment mandate as follows:

Emergent invests in a portfolio of managed funds, direct equities, cash, fixed interest securities and possibly derivatives in order to gain exposure to emerging markets which are expected to grow more quickly and produce higher returns than the Australian market over the medium to long term,

77 The PDS also included specific disclosures of the investment risks associated with that investment mandate, including emerging markets risk, sovereign risk and foreign exchange risk.

78 The Emergent Fund’s unit price declined from $1.17 as at 31 October 2014 to $0.81 as at 30 June 2015.

79 As at 31 October 2015, there were approximately 85 unitholders in the Emergent Fund, overwhelmingly comprised of individuals and self-managed superannuation funds.

The Generator Fund

80 The PDS issued by Fundhost for the Generator Fund in November 2008 described the fund’s investment mandate as follows:

GENERATORTM will invest in a combination of Managed Funds, Listed Investment Companies and cash or fixed interest in accordance with its Portfolio Construction Guidelines.

81 The Generator Fund’s unit price declined from $0.45 on 31 October 2014 to $0.23 on 30 June 2015.

82 As at 31 October 2015, there were approximately 61 unitholders in the Generator Fund, overwhelmingly comprised of individuals and self-managed superannuation funds.

The Maximiser Fund

83 The PDS issued by Fundhost for the Maximiser Fund in June 2012 described the fund’s investment mandate as follows:

Maximiser will invest in a portfolio of managed funds, direct equities, and cash or fixed interest securities that the Investment Manager believes will provide a high level of growth return over the medium to long term.

84 The Maximiser Fund’s unit price declined from $0.95 on 31 October 2014 to $0.60 on 30 June 2015.

85 As at 31 October 2015, there were 123 unitholders in the Maximiser Fund, overwhelmingly comprised of individuals and self-managed superannuation funds.

86 By 31 January 2015, approximately 83% of the assets of the Maximiser Fund were invested indirectly in Malaysian equities, of which 43% was invested in the shares of Asia Biotech Bhd.

(g) The Cayman funds: Bridge Global CMC Fund and the Hanhong High-Yield Fund

The Bridge Global CMC Fund

87 The Bridge Global Absolute Return Fund Segregated Portfolio (the Bridge Global CMC Fund) was one of a number of segregated portfolio investment funds operated in the Cayman Islands by Bridge Global Absolute Return Fund SPC (Bridge Global SPC), a Cayman Islands company. The Bridge Global CMC Fund was established in April 2014.

88 Bridge Global SPC was wholly owned by Bridge Global Asset Management Ltd (BGAM), a Cayman Islands company which, from 7 March 2014, was owned as to 40% by Avestra. Around the time that the Bridge Global CMC Fund was established, BGAM went through a succession of name changes:

Prior to 20 February 2014 | Bridge Partners Investment Management (Cayman) Ltd |

20 February – 3 March 2014 | Connect Capital Asset Management Ltd |

3 March – 1 June 2014 | Avestra Global Asset Management Ltd |

1 June – 11 August 2014 | AG Global Asset Management Ltd |

11 August 2014 – | Bridge Global Asset Management Ltd |

89 From 26 February 2014 and 10 March 2014 respectively, the directors of Bridge Global SPC and BGAM were Rowles and Sze-Wei Samuel Goh (Goh).

The Hanhong High-Yield Fund

90 The Hanhong High-Yield Fund Segregated Portfolio (the Hanhong High-Yield Fund) was one of a number of segregated portfolio investment funds operated in the Cayman Islands by Hanhong (Cayman) SPC Ltd (Hanhong SPC), a Cayman Islands company. The Hanhong High-Yield Fund was established in around August 2014.

91 On 28 July 2014, Jason Dixon, Nicholas McDonald and Neil Sheather were appointed directors of Hanhong SPC, in addition to two other incumbent directors. At the time, Dixon was also a director of Avestra, and each of Dixon, McDonald and Sheather were also directors of Bridge Global Securities.

factual background

(a) The AG Financial takeover and cross-investments from the AG Schemes

92 AG Financial operated a listed funds management business. AG Financial’s subsidiary, AGF Funds Management, was the investment manager of the AG Schemes. Until 30 January 2014, the AG Schemes had an independent responsible entity, Fundhost.

93 During the period from March to August 2013, there were two groups of transactions that ASIC now contends gave rise to contraventions by Avestra, namely:

(a) Avestra’s acquisition of a controlling interest in the shares of AG Financial, using scheme and trust property of its registered and wholesale funds; and

(b) cross-investments, by Bridge Global Securities, of the scheme property of the Emergent, Maximiser and Generator Funds into Avestra’s wholesale schemes.

94 Those two groups of transactions are illustrated in the following diagram:

Avestra’s acquisitions of shares in AG Financial

95 In around March 2013, Avestra and its associates, including Rowles and Dempsey, embarked on obtaining a controlling stake in AG Financial, in order to effect a merger or consolidation of the Avestra and Excela businesses, and to realise a “back-door listing” of Avestra.

96 In a succession of purchases between 20 March 2013 and 2 August 2013, Avestra used funds that it held on trust for unitholders in registered and wholesale managed investment schemes, rather than Avestra’s own funds, to acquire a controlling stake in AG Financial and to realise that commercial objective for the benefit of Avestra and its shareholders. The most significant purchases were:

Date | Type of purchase | Advantage Fund | Worberg Global Fund | Canton Fund | Safecrest Fund | Avestra’s % interest (aggregate) |

20-21 March 2013 | Off-market from Spann | 230,000 | 2,000,000 | 4,400,000 | 22.2% | |

30 May | Placement | 4,200,000 | 31.8% | |||

3 July | On market | 500,000 | 33.5% | |||

4 July | On market | 500,000 | 35.0% | |||

12 July | Rights issue | 16,700,000 | 8,500,000 | 17,760,000 | 46.3% | |

19 July | Shortfall allocation | 9,000,000 | 21,000,000 | 7,500,000 | 56.0% | |

1 August | Off market | 500,000 | 56.2% |

97 Rowles and Dempsey now accept the following:

(a) First, each of those purchases of shares in AG Financial by the Advantage Fund involved the giving of a financial benefit out of the scheme property of the Advantage Fund to Avestra and/or AG Financial, without having obtained the approval of members of the Advantage Fund, in contravention of s 208(1) (as modified by s 601LC). Further, in making those purchases, Avestra was in a position of conflict of interest and failed to give priority to the interests of the members of the Advantage Fund, in contravention of s 601FC(1)(c).

(b) Second, each of those purchases of shares in AG Financial by the Worberg Global Fund involved the giving of a financial benefit indirectly out of the scheme property of the Advantage Fund (scheme property of which was invested in the Worberg Global Fund) to Avestra and/or AG Financial, without having obtained the approval of members of the Advantage Fund, in contravention of s 208(1) (as modified by s 601LC).

(c) Third, they were each involved in the making of each of those purchases, and so they personally contravened s 209(2) (as modified by s 601LA) in relation to each purchase, and contravened s 601FC(5) in relation to the purchases by the Advantage Fund.

(d) Fourth, in making each of those purchases of shares in AG Financial by the Canton and Safecrest Funds, Avestra failed to provide financial services efficiently, fairly and honestly, in contravention of s 912A(1)(a).

(e) Fifth, they failed to take reasonable steps to prevent Avestra committing those contraventions of s 912A(1)(a), and so personally contravened s 601FD(1)(f)(i).

98 When making those acquisitions of shares in AG Financial through its registered and wholesale schemes, Avestra committed contraventions of the substantial shareholder notice obligation (s 671B) and takeover prohibition (s 606(1)). Avestra was convicted of those offences on 16 December 2014. Accordingly, no declarations of contravention were sought against Avestra for the contraventions of which it already had been convicted. Each of Rowles and Dempsey does not dispute having contravened s 1308(2) by filing substantial shareholder notices that did not reflect the extent of Avestra’s (as opposed to the schemes’) relevant interest in AG Financial, and thereby omitted information without which they knew the notices to be false or misleading. Further, Rowles and Dempsey do not dispute that they failed to take reasonable steps to prevent Avestra committing those contraventions, and so contravened s 601FD(1)(f)(i) on each occasion.

99 As a consequence of Avestra acquiring a controlling interest in AG Financial through its registered and wholesale funds, Dempsey was appointed as a director of AG Financial and AGF Funds Management on 12 July 2013, AG Financial moved its principal place of business to the same premises as Avestra’s principal place of business, and Excela Ltd was renamed AG Financial Ltd and adopted a logo closely resembling Avestra.

Cross-investments from the AG Schemes into Avestra’s registered and wholesale funds

100 On 1 April 2013, less than two weeks after Avestra made its first acquisition of 22% of the voting shares in AG Financial, AG Financial’s subsidiary, AGF Funds Management, sub-delegated investment management of the AG Schemes to Bridge Global Securities, a company of which both Rowles and Dempsey were then the sole directors.

101 Thereafter, Bridge Global Securities began to invest scheme property of the Emergent, Maximiser and Generator Funds into Avestra’s registered and wholesale funds and, in so doing, supplied additional capital for Avestra’s funds to make further purchases of shares in AG Financial, and thereby to increase the extent of Avestra’s control over AG Financial.

Date | From AG Scheme | To Avestra fund | Amount invested |

1 May 2013 | Emergent | Advantage | $600,000 |

Emergent | Worberg Global | $616,560 | |

Maximiser | Advantage | $1,600,000 | |

Maximiser | Worberg Global | $1,640,000 | |

1-2 July 2013 | Generator | Safecrest | $300,000 |

Maximiser | Advantage | $400,000 | |

Maximiser | Worberg Global | $383,520 | |

1 August 2013 | Maximiser | Canton | $380,000 |

2 August 2013 | Generator | Safecrest | $125,000 |

102 On 1 May 2013, when the first of those cross-investments were made, Fundhost, which was then the responsible entity of the AG Schemes, objected to the scheme property of the AG Schemes being invested into related party funds, without disclosure having been given to members of the AG Schemes. Avestra’s response was not merely to abruptly dismiss those concerns; but together with AG Stockbroking (another subsidiary of AG Financial), it set about removing Fundhost, and having itself appointed, as the responsible entity of the AG Schemes.

103 The Safecrest Fund was established as a wholesale fund in April 2013. Throughout the second half of 2013, the only investments into the Safecrest Fund were made out of the scheme property of the Generator Fund, and the only investment held by the Safecrest Fund was shares in AG Financial. In substance, the Safecrest Fund operated solely as a conduit for the undisclosed investment of scheme property of the Generator Fund in shares in AG Financial.

104 Another significant aspect of the cross-investments out of the Maximiser Fund was that, by its investments into the Worberg Global and Canton Funds, it became exposed to the substantial investments in Malaysian shares and equity derivatives held by those wholesale funds, which was not contemplated in the investment mandate described in the Maximiser Fund’s PDS.

105 Rowles and Dempsey do not dispute the following:

(a) First, each of those cross-investments out of the scheme property of the Emergent, Maximiser and Generator Funds involved Bridge Global Securities (as an agent of the responsible entity) giving a financial benefit to Avestra (a related party of Bridge Global Securities), in contravention of s 208(1) (as modified by s 601LC).

(b) Second, they were involved in the making of each of those cross-investments, and so they personally contravened s 209(2) (as modified by s 601LA) in relation to each cross-investment.