FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2017] FCA 459

ORDERS

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | ||

AND: | AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

Pleadings and originating process

1. The Plaintiff have leave to file a further amended statement of claim in the form submitted to the Court on 28 April 2017.

2. The Plaintiff file and serve the Further Amended Statement of Claim by 4pm on 28 April 2017.

3. The Plaintiff file and serve any amended Particulars Schedules to the Further Amended Statement of Claim by 4pm on 5 May 2017.

4. The Defendant file and serve a defence to the Further Amended Statement of Claim by 26 May 2017.

5. The Plaintiff have leave to file a second further amended originating process in the form submitted to the Court on 28 April 2017.

6. The Plaintiff file and serve the Second Further Amended Originating Process by 4pm on 28 April 2017.

7. The Plaintiff pay the Defendant’s costs thrown away by reason of the amendments to the Amended Statement of Claim and the Further Amended Originating Process.

8. The Plaintiff have leave to withdraw its agreement to the matters stated in paragraphs 17, 32, 95d and 96d of the Statement of Agreed Facts filed on 8 December 2016 and to file an amended Statement of Agreed Facts with these paragraphs struck-through (and with any further agreed facts) by 4pm on 2 June 2017.

9. The Plaintiff and Defendant file any amended Statement of Facts Not Agreed by 4.00pm on 9 June 2017.

Evidence

10. The time for compliance with order 4 of the Orders made on 9 December 2016 be extended to 14 August 2017.

11. The parties to the proceedings (and in consultation with the parties in proceedings numbered VID282/2016 (ASIC v Westpac Banking Corporation) and VID604/2016 (ASIC v National Australia Bank Limited) to the extent expert evidence is common to the BBSW proceedings (as defined in order 1 of the Orders made on 9 December 2016)) and experts on the same topic prepare a list of issues for expert conferral by 28 August 2017.

12. A conference of experts be held by 4 September 2017.

13. The experts provide a joint report or conference report on the outcomes of conferral to the parties and the Court by 11 September 2017.

Mediation

14. The parties confer as to an appropriate form of mediation of the proceeding and the identity of the mediator by 11 September 2017.

15. A mediation be held by 25 September 2017 and the mediator report to the Court on the outcome by 28 September 2017.

Trial

16. Order 2 of the Orders made on 9 December 2016 be vacated.

17. The BBSW proceedings be listed for trial on liability only commencing at 10.15am on 23 October 2017.

Case management hearing

18. A further case management hearing be listed for 9.30am on 21 August 2017.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

VID 282 of 2016 | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | WESTPAC BANKING CORPORATION Defendant | |

JUDGE: | BEACH J |

DATE OF ORDER: | 28 APRIL 2017 |

THE COURT ORDERS THAT:

Pleadings and originating process

1. The Plaintiff have leave to file a further amended statement of claim in the form submitted to the Court on 28 April 2017.

2. The Plaintiff file and serve the Further Amended Statement of Claim by 4pm on 28 April 2017.

3. The Plaintiff file and serve any amended Particulars Schedules to the Further Amended Statement of Claim by 4pm on 5 May 2017.

4. The Defendant file and serve a defence to the Further Amended Statement of Claim by 26 May 2017.

5. The Plaintiff have leave to file a further amended originating process in the form submitted to the Court on 28 April 2017.

6. The Plaintiff file and serve the Further Amended Originating Process by 4pm on 28 April 2017.

7. The Plaintiff pay the Defendant’s costs thrown away by reason of the amendments to the Amended Statement of Claim and the Amended Originating Process.

8. The time for compliance with Orders made on 22 August 2016 (and amended by consent orders on 10 November 2016, and further amended by orders on 7 April 2017) be extended as follows:

(a) Order 5 be extended to 2 June 2017; and

(b) Order 6 be extended to 9 June 2017.

Evidence

9. The time for compliance with order 4 of the Orders made on 9 December 2016 be extended to 14 August 2017.

10. The parties to the proceedings (and in consultation with the parties in proceedings numbered VID197/2016 (ASIC v Australia and New Zealand Banking Group Ltd) and VID604/2016 (ASIC v National Australia Bank Limited) to the extent expert evidence is common to the BBSW proceedings (as defined in order 1 of the Orders made on 9 December 2016)) and experts on the same topic prepare a list of issues for expert conferral by 28 August 2017.

11. A conference of experts be held by 4 September 2017.

12. The experts provide a joint report or conference report on the outcomes of conferral to the parties and the Court by 11 September 2017.

Mediation

13. The parties confer as to an appropriate form of mediation of the proceeding and the identity of the mediator by 11 September 2017.

14. A mediation be held by 25 September 2017 and the mediator report to the Court on the outcome by 28 September 2017.

Trial

15. Order 2 of the Orders made on 9 December 2016 be vacated.

16. The BBSW proceedings be listed for trial on liability only commencing at 10.15am on 23 October 2017.

Case management hearing

17. A further case management hearing be listed for 9.30am on 21 August 2017.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

VID 604 of 2016 | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | NATIONAL AUSTRALIA BANK LIMITED Defendant | |

JUDGE: | BEACH J |

DATE OF ORDER: | 28 aPRIL 2017 |

THE COURT ORDERS THAT:

Pleadings and originating process

1. The Plaintiff have leave to file a further amended statement of claim in the form submitted to the Court on 28 April 2017.

2. The Plaintiff file and serve the Further Amended Statement of Claim by 4pm on 28 April 2017.

3. The Plaintiff file and serve any amended Particulars Schedules to the Further Amended Statement of Claim by 4pm on 5 May 2017.

4. The Defendant file and serve a defence to the Further Amended Statement of Claim by 26 May 2017.

5. The Plaintiff have leave to file a second further amended originating process in the form submitted to the Court on 28 April 2017.

6. The Plaintiff file and serve the Second Further Amended Originating Process by 4pm on 28 April 2017.

7. The Plaintiff pay the Defendant’s costs thrown away by reason of the amendments to the Amended Statement of Claim and the Amended Originating Process.

Evidence

8. The time for compliance with order 4 of the Orders made on 9 December 2016 be extended to 14 August 2017.

9. The parties to the proceedings (and in consultation with the parties in proceedings numbered VID197/2016 (ASIC v Australia and New Zealand Banking Group Limited) and VID282/2016 (ASIC v Westpac Banking Corporation) to the extent expert evidence is common to the BBSW proceedings (as defined in order 1 of the Orders made on 9 December 2016)) and experts on the same topic prepare a list of issues for expert conferral by 28 August 2017.

10. A conference of experts be held by 4 September 2017.

11. The experts provide a joint report or conference report on the outcomes of conferral to the parties and the Court by 11 September 2017.

Mediation

12. The parties confer as to an appropriate form of mediation of the proceeding and the identity of the mediator by 11 September 2017.

13. A mediation be held by 25 September 2017 and the mediator report to the Court on the outcome by 28 September 2017.

Trial

14. Order 2 of the Orders made on 9 December 2016 be vacated.

15. The BBSW proceedings be listed for trial on liability only commencing at 10.15am on 23 October 2017.

Case management hearing

16. A further case management hearing be listed for 9.30am on 21 August 2017.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BEACH J:

1 On 28 April 2017, I dealt with the following three main issues that the parties had raised with me:

(a) First, whether I should grant leave to the Australian Securities and Investments Commission (ASIC) to file and serve further amendments to its originating process and statement of claim in each proceeding against Australia and New Zealand Banking Group Ltd (ANZ), Westpac Banking Corporation (Westpac) and National Australia Bank Ltd (NAB).

(b) Second, whether I should extend the time for the filing and service of evidence by the Banks until 31 August 2017.

(c) Third, whether I should vacate the trial date of 25 September 2017, and refix that date no earlier than, on one estimate given by Westpac’s senior counsel, May 2018.

2 In summary, I decided to grant leave to ASIC to make the amendments sought, to extend the time for the Banks to file their evidence until 14 August 2017, and to postpone the trial date until 23 October 2017. These are my reasons for doing so.

Background

3 ASIC has essentially made three categories of claims against each Bank.

(a) The s 1041A case

4 First, ASIC has alleged that each Bank contravened s 1041A of the Corporations Act 2001 (Cth) (the Act), which provides:

Market manipulation

A person must not take part in, or carry out (whether directly or indirectly and whether in this jurisdiction or elsewhere):

(a) a transaction that has or is likely to have; or

(b) 2 or more transactions that have or are likely to have;

the effect of:

(c) creating an artificial price for trading in financial products on a financial market operated in this jurisdiction; or

(d) maintaining at a level that is artificial (whether or not it was previously artificial) a price for trading in financial products on a financial market operated in this jurisdiction.

5 In order to appreciate how such an allegation is made, it is useful to set out some relevant context as alleged by ASIC. What is set out below is a concise summary of ASIC’s case against each Bank relating to the relevant period(s) covered by its pleadings. I have only set out so much of what ASIC has alleged as is necessary to appreciate the further amendments sought to be made by ASIC to its pleadings in each case.

Background

6 A negotiable certificate of deposit (NCD) is a certificate issued by a bank evidencing an interest bearing deposit with the issuing bank for a fixed term, which NCD entitles its holder to payment of a specified sum (face value) by that bank on the date that the NCD matures. A bank accepted bill (BAB) is a bill of exchange as defined in s 8 of the Bills of Exchange Act 1909 (Cth), which has been accepted by a bank and bears the name of the accepting bank as acceptor, and which obliges the bank to pay the face value of the bill to the holder of the bill on the date that it matures. NCDs and BABs are instruments by which a bank, including a Prime Bank (defined in [21] below) may borrow funds for a short term, usually for a period of no longer than 12 months.

7 NCDs issued and BABs accepted by Prime Banks (Prime Bank Bills) were able to be traded on a fungible basis, and were recognised by participants in the short dated securities market (Bank Bill Market) as being of the highest quality with regard to liquidity, credit and consistency of relative yield. Prime Bank Bills were issued for tenors or “terms” of one, two, three, four, five and six months.

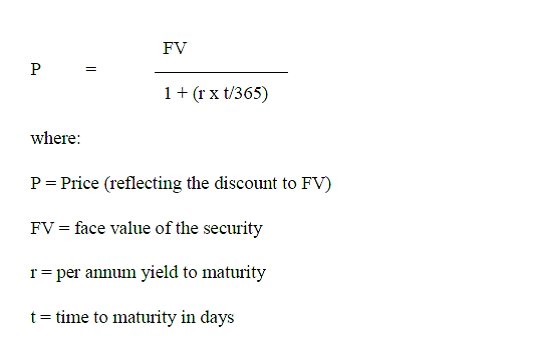

8 Prime Bank Bills were traded in one of two ways in the Bank Bill Market: (a) through what has been described as dealer markets, in which interdealer brokers acted as intermediaries by quoting prices at which their respective clients would buy (bid) and sell (offer) Prime Bank Bills as counterparties to and from other participants; or (b) in direct trades between counterparties. ICAP Brokers Pty Ltd (ICAP) and Tullett Prebon (Australia) Pty Ltd (Tullett) were the two interdealer brokers who were operative in the Bank Bill Market. For the moment, dimension (b) can be put to one side.

9 Participants trading Prime Bank Bills in the Bank Bill Market did not use electronic platforms to execute trades, but rather executed trades by “voice broking”, that is, by participants giving verbal instructions to brokers. Participants usually communicated and gave instructions to brokers via telephone lines which connected each participant to his or her individual broker(s). The telephone lines were often connected to speaker boxes, known as “squawkboxes”, at both the participant’s and the broker’s end.

10 For the purposes of trading Prime Bank Bills in the Bank Bill Market, each Bank had a broker at Tullett and/or ICAP.

11 At or shortly after the time of participants making bids and offers for Prime Bank Bills through ICAP and Tullett, ICAP and Tullett posted the best and most recent bid/offer for Prime Bank Bills of all tenors on separate electronic systems (that is, one system showing bids and offers through ICAP and one system showing bids and offers through Tullett). This information, once posted, became accessible by and visible to participants in the Bank Bill Market with access to such electronic systems.

12 The participants in the Bank Bill Market included banks which were not Prime Banks.

13 Prime Bank Bills traded at a discount to their face value, to reflect the fact that their holder would only receive the face value on the maturity date. The discount to face value was calculated on the basis of simple interest (or simple discounting) according to the following pricing discount formula identified in the Negotiable & Transferable Instruments (NTI) Conventions published by the Australian Financial Markets Association (AFMA) through the NTI Committee (discussed in [20] below):

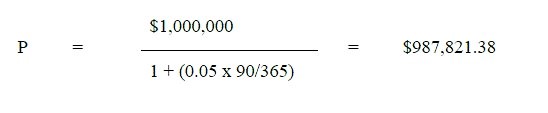

Accordingly, if a 90-day Prime Bank Bill with a face value of $1 million traded at a yield of 5%, then the pricing discount (ie the price paid by the party purchasing the Prime Bank Bill) was calculated as follows:

14 Consequently, yield (the rate of interest) moved inversely to the trading price of the Prime Bank Bills.

15 Trades in the Bank Bill Market were conducted by reference to yield, tenor and volume of the Prime Bank Bills the subject of the transaction.

16 At this point, it is appropriate to record that the Bank Bill Swap Reference Rate (BBSW) was the trimmed, average mid-rate of the observed best bid / best offer for Prime Bank Bills for certain tenors on each Sydney business day published by AFMA. As I will explain in a moment, it is said that the BBSW was set on the basis of observations submitted by BBSW panellists, including ANZ, Westpac and NAB as to the yield at which Prime Bank Bills in each tenor were trading at a particular time (approximately 10.00am) on each trading day.

17 It is said that the BBSW was a key reference rate and benchmark rate in the financial markets in Australia and was widely used as the benchmark (or reference) interest rate in financial products in Australia, including certain short term interest rate products, floating rate derivative products, commercial loans and other financial products.

18 At this point, it is necessary to say something further concerning what ASIC has said about AFMA and the BBSW rate setting mechanism.

Australian Financial Markets Association Limited

19 AFMA, a public company limited by guarantee, was a financial markets industry association and had members which included ANZ, Westpac and NAB. AFMA’s objectives included encouraging self-regulation by establishing efficient market practices and conventions and preparing and maintaining standard documentation. AFMA established and maintained codes, conventions, standards and procedures for the purposes of encouraging self-regulation by AFMA members. AFMA had a Market Governance Committee (MGC) that developed and maintained market protocols designed to facilitate and promote the efficient and orderly running of over the counter markets in Australia, and various market committees overseen by the MGC that met regularly with the objective of developing consensus in the market on technical matters such as transaction documentation, standards, trading conventions and market data.

20 The AFMA market committees included the NTI Committee, which was responsible for maintaining the conventions for trading in the Bank Bill Market in money market instruments (including Bank Bills) and the implementation of the rules governing the list of Prime Banks. It had as members, representatives of ANZ, Westpac and NAB. One of the other committees was the BBSW Committee, which was responsible for the overall management of the BBSW, the rates directly related to the BBSW, the procedure for setting and publishing the BBSW, and the resolution of any disputes among AFMA members involving the BBSW and the rate set mechanism. It also had as members, representatives from ANZ, Westpac and NAB.

21 AFMA specified and administered the process for the election and recognition of banks that were then to be designated by AFMA as “Prime Banks”. Each of ANZ, Westpac and NAB was recognised by AFMA and acted as a Prime Bank. Other Prime Banks were Commonwealth Bank of Australia, JP Morgan Chase Bank NA, Australia Branch (to 30 November 2011) and BNP Paribas, Australia Branch (to 24 February 2012).

The BBSW Rate Setting Mechanism

22 AFMA in consultation with the BBSW Committee:

(a) determined the BBSW rate setting mechanism;

(b) administered the calculation of the BBSW; and

(c) administered the publication of the BBSW.

23 The BBSW was calculated and published by AFMA for the one, two, three, four, five and six month tenors of Prime Bank Bills.

24 During the entirety of the relevant period(s) the following banks were BBSW panellists:

(a) each of ANZ, Westpac and NAB;

(b) Bank of Scotland plc, Australia Branch (trading under the name Lloyds TSB Bank plc Australia Branch from 15 November 2010);

(c) BNP Paribas, Australia Branch;

(d) Citibank NA, Australia Branch

(e) Commonwealth Bank of Australia;

(f) Deutsche Bank AG, Australia Branch;

(g) HSBC Bank Australia Limited;

(h) J.P. Morgan Chase Bank NA, Australia Branch;

(i) Macquarie Bank Limited; and

(j) UBS AG, Australia Branch.

25 The calculation of the BBSW by AFMA was prescribed in the BBSW procedures which were broadly to the following effect:

(a) AFMA received submissions from the BBSW panellists. It required each BBSW panellist to make a submission to AFMA by 10.05am Sydney time on each Sydney business day identifying that BBSW panellist’s view of the mid-rate of the yield for Prime Bank Bills at approximately 10.00am, expressed to two decimal places, on that Sydney business day for each tenor.

(b) A BBSW panellist’s submissions on any particular day would not be considered by AFMA unless the BBSW panellist provided a submission for each tenor by 10.05am Sydney time.

(c) Following the receipt of submissions from the BBSW panellists, the highest and lowest mid-rates submitted for each tenor were eliminated until a maximum of eight submissions remained.

(d) The BBSW for that day was calculated or set by AFMA by ascertaining, to four decimal places, the average of the eight remaining mid-rates for each tenor.

26 Each Bank’s usual practice was to make a submission to AFMA by 10.05am Sydney time on each Sydney business day to reflect their respective view of the mid-rates (mid of bid/offer rates for each tenor) for Prime Bank Bills at approximately 10.00am.

27 AFMA published the BBSW from approximately 10.10am on each Sydney business day and it was made available to subscribers to the BBSW service by information vendors such as Bloomberg or Reuters shortly after approximately 10.10am on the day of calculation, and to the general public on the following day. AFMA also published on each Sydney business day the average “bid” and “offer” values for each tenor, which were calculated on the same basis as BBSW using a spread of five basis points on either side of the BBSW.

BBSW referenced products

28 ASIC has alleged that financial products were issued under which the rights or obligations of the parties were calculated by reference to the BBSW for a relevant tenor on a particular day or days. These financial products included:

(a) interest rate swaps;

(b) 90-day Bank accepted bill futures (BAB Futures);

(c) forward rate agreements;

(d) cross-currency swaps;

(e) asset swaps;

(f) interest rate options;

(g) inflation swaps;

(h) floating rate notes;

(i) commercial loans; and

(j) Bank Bills.

Effect of sale or purchase of Prime Bank Bills

29 ASIC has alleged that on any business day in the relevant period(s), the sale by a Bank Bill Market participant, in sufficient volumes, of Prime Bank Bills in a particular tenor during the BBSW Rate Set Window (defined by ASIC to be the period between 9.55am and 10.00am (now changed to 10.05am)) was likely to:

(a) increase the volume of Prime Bank Bills in that tenor for sale in the Bank Bill Market during the BBSW Rate Set Window;

(b) as a result of subparagraph (a), cause Prime Bank Bills in that tenor to trade at an increased yield (lower price for the Bills / increased discount to face value) during the BBSW Rate Set Window;

(c) as a result of subparagraph (b), cause the BBSW panellists’ respective views of the mid-rate of the yield for Prime Bank Bills in that tenor at approximately 10.00am to be higher than they otherwise would have been;

(d) as a result of subparagraph (c), cause each BBSW panellist’s respective submission to AFMA to be higher than it otherwise would have been; and

(e) as a result of subparagraph (d), cause the BBSW for that tenor to be set by AFMA at a yield higher than it would otherwise have been.

30 Contrastingly, ASIC has alleged that on any business day in the relevant period(s), the purchase by a Bank Bill Market participant, in sufficient volumes, of Prime Bank Bills in a particular tenor during the BBSW Rate Set Window was likely to:

(a) deplete the supply of Prime Bank Bills in that tenor for sale in the Bank Bill Market during the BBSW Rate Set Window;

(b) as a result of subparagraph (a), cause Prime Bank Bills in that tenor to trade at a lower yield (higher price for the Bills / decreased discount to face value) during the BBSW Rate Set Window;

(c) as a result of subparagraph (b), cause the BBSW panellists’ respective views of the mid-rate of the yield for Prime Bank Bills in that tenor at 10.00am to be lower than they otherwise would have been;

(d) as a result of subparagraph (c), cause each BBSW panellist’s respective submission to AFMA to be lower than it otherwise would have been; and

(e) as a result of subparagraph (d), cause the BBSW for that tenor to be set by AFMA at a yield lower than it would otherwise have been.

31 Generally, ASIC has said that the sale or purchase of Prime Bank Bills on any business day in the relevant period, in sufficient volumes during the BBSW Rate Set Window, was likely to affect the setting of the BBSW for the relevant tenor on the relevant day.

Alleged conduct intended to influence the BBSW

32 ASIC alleges against each relevant Bank with respect to a relevant day(s) that before entering sale transactions of Prime Bank Bills, the relevant Bank took one or more of the following steps to accumulate a sufficient volume of Prime Bank Bills to sell into the BBSW Rate Set Window on the relevant day:

(a) It determined to issue and issued NCDs in the relevant tenor;

(b) It acquired BAB Futures shortly before expiry, held such futures to expiry and took delivery of Prime Bank Bills upon expiry;

(c) It acquired Prime Bank Bills in the relevant tenor shortly before the relevant day; and/or

(d) It allocated existing holdings of Prime Bank Bills in the relevant tenor for sale.

33 ASIC alleges that the relevant sale transactions undertaken by each relevant Bank:

(a) were undertaken by the relevant Bank for the sole or dominant purpose, alternatively a purpose, of raising or maintaining:

(i) the yield at which Prime Bank Bills were trading at approximately 10.00am on the relevant day; and

(ii) the level at which the BBSW was set by AFMA on the relevant day;

(b) accordingly resulted in yields which did not reflect the forces of genuine supply and demand in the Bank Bill Market on the relevant day; and

(c) had or were likely to have the effect of creating on the relevant day an artificial price for trading in traded BBSW referenced products, which I will define in a moment but a subset of the products described in [28] above.

34 ASIC alleges that the relevant purchase transactions undertaken by each relevant Bank:

(a) were undertaken by the relevant Bank for the sole or dominant purpose, alternatively a purpose, of lowering or maintaining:

(i) the yield at which Prime Bank Bills were trading at approximately 10.00am on the relevant day; and

(ii) the level at which the BBSW was set by AFMA on the relevant day;

(b) accordingly were entered into at yields which did not reflect the forces of genuine supply and demand in the Bank Bill Market on the relevant day; and

(c) had or were likely to have the effect of creating an artificial price for trading in traded BBSW referenced products on the relevant day.

35 The traded BBSW referenced products, as pleaded prior to ASIC’s recent amendments, were:

(a) BAB Futures; and

(b) interest rate swaps.

36 These traded BBSW referenced products have been described by ASIC in the following terms.

37 Under a BAB Futures contract, one party agrees to buy a 90-day Prime Bank Bill at an agreed yield (and thus price) on the expiry date of the contract and the other party agrees to sell a 90-day Prime Bank Bill at an agreed yield (and thus price) on the expiry date of the contract. BAB Futures contracts are standardised contracts with the following terms:

(a) The contracts relate to the delivery of 90-day Prime Bank Bill(s) with a face value of AUD$1,000,000.

(b) The contracts expire on one of four dates per year; the Thursday before the second Friday in each of March, June, September and December.

(c) The contracts are deliverable, meaning that if the BAB Futures contract is held to expiry then one party must actually deliver the 90-day Prime Bank Bill(s) to the other party, who must buy the Prime Bank Bill(s).

(d) The contracts expire at 12 noon on the expiry day and the delivery occurs the following day (so delivery occurs on the second Friday in each of March, June, September and December).

38 BAB Futures contracts are traded on the ASX Trade24. A party can enter into BAB Futures contracts with a term (time left to the expiry date) of up to five years.

39 The BAB Futures contract price reflects:

(a) the market’s view of what the price of 90-day Prime Bank Bills will be at the date of expiry of the BAB Futures contract; and

(b) the current interest rate that applies to the period until the BAB Futures contract expiry date (which determines the cost of holding the BAB Futures contract).

40 ASIC has said that a change in the price of Prime Bank Bills or a change in the BBSW (which are inversely related metrics) on any day during the term of a BAB Futures contract is likely to affect both of the matters referred to in [39(a)] and [39(b)] and therefore the BAB Futures contract price.

41 Let me describe (in the terms put by ASIC) the other traded BBSW referenced product. An interest rate swap is an agreement between two parties to exchange streams of cash flow based on a notional amount for a set period. The most common type of interest rate swap is a fixed rate for floating rate swap. A fixed rate for floating rate swap has the following legs:

(a) One leg of the swap has payment obligations calculated with reference to a floating interest rate (commonly the BBSW). The swap party taking this leg of the swap has obligations to pay to the other swap party cash flows equal to the agreed notional (principal) amount multiplied by the agreed floating interest rate.

(b) The other leg of the swap has payment obligations calculated with reference to an agreed fixed interest rate known as the “swap rate”. The swap party taking this leg of the swap has obligations to pay to the other party cash flows equal to the agreed notional (principal) amount multiplied by the swap rate.

42 Under an interest rate swap, rather than both parties making payments to each other, one party makes a cash payment to the other party based on the net difference between the two cash flows. Moreover, payments only reflect net interest payments. No “principal” payments are made by the parties. The net interest payments are made at regular intervals (the payment days are referred to as “reset dates”). The intervals may be set monthly, quarterly, annually or at another time period agreed between the parties. There is a formula for calculating the cash flow obligations of both swap counterparties to a fixed rate for floating rate swap on a reset date. But the detail is not important for present purposes.

43 Let me return to the principal allegations. ASIC alleges that the relevant sale transactions and the relevant purchase transactions of Prime Bank Bills had, or were likely to have, the effect of creating an artificial price, or maintaining, at a level that was artificial, a price for trading in traded BBSW referenced products on the relevant days. It is said that the traded BBSW referenced products:

(a) were financial products for the purpose of s 1041A of the Act; and

(b) were traded on a financial market for the purpose of s 1041A, namely one or more of the financial markets for traded BBSW referenced products.

44 It is said that by reason of the foregoing, the Banks contravened s 1041A on the various dates pleaded in each of the proceedings in relation to the relevant sale transactions (the sale contraventions) and the relevant purchase transactions (the purchase contraventions). It will be apparent from what I have said that the s 1041A case relates to a subset of BBSW referenced products, as compared with the other claims made by ASIC which I will now describe.

(b) Alleged unconscionable conduct

45 ASIC alleges that each of the Banks were a party to a number of BBSW referenced products, including one or more BBSW referenced products in relation to which:

(a) a payment was required to be made (whether on that day or some future day), either by the relevant Bank to the counterparty to the relevant BBSW referenced product or by the counterparty to the Bank;

(b) the amount of the said payment was determined by, or by reference to, or was derived from, the rate at which the BBSW for the tenor referenced in the particular product was set on the date of the particular sale contravention or purchase contravention;

(c) where a sale contravention occurred on that date, the counterparty may have had a “short exposure” (being opposite to the relevant Bank’s net long BBSW rate set exposure) to the BBSW for the relevant tenor, meaning that the payment under the relevant BBSW referenced product:

(i) if required to be made by the Bank to the counterparty, would be decreased if the BBSW for the relevant tenor was set higher on that day, and increased if the BBSW for the relevant tenor was set lower on that day; or

(ii) if required to be made by the counterparty to the Bank, would be increased if the BBSW for the relevant tenor was set higher on that day, and decreased if the BBSW for the relevant tenor was set lower on that day; and

(d) where a purchase contravention occurred on that date, the counterparty may have had a “long exposure” (being opposite to the relevant Bank’s net short BBSW rate set exposure) to the BBSW for the relevant tenor, meaning that the payment under the relevant BBSW referenced product:

(i) if required to be made by the Bank to the counterparty, would be decreased if the BBSW for the relevant tenor was set lower on that day, and increased if the BBSW for the relevant tenor was set higher on that day; or

(ii) if required to be made by the counterparty to the Bank, would be increased if the BBSW for the relevant tenor was set lower on that day, and decreased if the BBSW for the relevant tenor was set higher on that day.

46 I have referred to the relevant Bank’s net long BBSW rate set exposure and net short BBSW rate set exposure. This is explained in the following terms:

(a) A Bank might have portfolios or “books” across a number of sections or departments consisting of holdings of BBSW referenced products where for a particular day an obligation under each instrument from one party to the other party to pay an amount of money would be quantified when the BBSW was set on that day. Such an amount, whether it was payable by the Bank to the counterparty or vice versa, depended upon the rate at which the BBSW was set on that day.

(b) A “long exposure” refers to the position where the net value (or profit) of the portfolios or “books”:

(i) would be increased in the event that the BBSW (for the relevant tenor) was set by AFMA at a higher rate on the relevant day; and

(ii) would be decreased in the event that the BBSW (for the relevant tenor) was set by AFMA at a lower rate on that day.

(c) A “short exposure” refers to the position where the net value (or profit) of the portfolios or books:

(i) would be increased if the BBSW was set at a lower rate on the relevant day; and

(ii) would be decreased if the BBSW was set at a higher rate on the relevant day.

47 It is said that the transactions concerning or constituting the BBSW referenced products were:

(a) financial services within the meaning of s 12CA(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act);

(b) the provision of a financial service by the relevant Bank within the meaning of s 12BAB(1) of the ASIC Act; and

(c) either:

(i) the supply of a financial service by the relevant Bank to the affected counterparty for the purposes of:

(A) s 12CB of the ASIC Act in so far as the transactions occurred on or after 1 January 2012; and

(B) the former s 12CC of the ASIC Act (as it stood prior to 1 January 2012) in so far as the transactions occurred in the period 9 March 2010 to 31 December 2011; or

(ii) the acquisition of a financial service by the relevant Bank from the affected counterparty for the purposes of:

(A) s 12CB of the ASIC Act in so far as the transactions occurred on or after 1 January 2012; and

(B) the former s 12CC of the ASIC Act (as it stood prior to 1 January 2012) in so far as the transactions occurred in the period 9 March 2010 to 31 December 2011.

48 It is said that the sale contraventions and the purchase contraventions (described earlier in relation to the s 1041A case) had the actual or likely effect of influencing the calculation of the payments referred to above to the disadvantage or detriment of the affected counterparties.

49 ASIC has alleged that each of the affected counterparties was not aware that the relevant Bank had engaged, would engage or might engage in:

(a) the impugned conduct including the conduct giving rise to the s 1041A contravention(s); or

(b) any other trading in the Bank Bill Market with a purpose, or the sole or dominant purpose, of influencing the BBSW rate set to that Bank’s advantage and to the detriment of the affected counterparties.

50 It is said that the relevant Bank knew or ought reasonably to have expected or known that the affected counterparties were not aware of the Bank’s impugned conduct and the effect it would have or was likely to have on the interests of the affected counterparties. It is said that the relevant Bank did not, prior to or at any time in the relevant period, disclose to any of the affected counterparties:

(a) that the Bank had, would or might engage in:

(i) the impugned conduct; or

(ii) any other trading in the Bank Bill Market with a purpose, or the sole or dominant purpose, of influencing the BBSW rate set to the Bank’s advantage or to the disadvantage of the affected counterparties; or

(b) the risk that such conduct had, or might have, the effect of causing loss to one or more of the affected counterparties.

51 It is said that at the time of engaging in the impugned conduct, the relevant Bank knew or ought reasonably to have expected or known that each of the affected counterparties expected or was likely to expect that the BBSW was a key financial market reference or benchmark rate which was genuinely, independently and transparently determined.

52 It is said that at the time of engaging in the impugned conduct, the relevant Bank knew, or ought reasonably to have expected or known, that its conduct in seeking to influence the BBSW rate set for a particular tenor on a particular date to the Bank’s advantage may or would have the actual or likely effect of causing loss to persons (such as affected counterparties) who had an exposure to the BBSW rate set for the relevant tenor on the relevant date that was the opposite of that Bank’s BBSW rate set exposure.

53 Generally and by reason of the foregoing, it is said that the impugned conduct:

(a) constituted an unconscionable taking of advantage by the relevant Bank of its position in the Bank Bill Market to the disadvantage of the affected counterparties; and

(b) was otherwise unconscionable in all the circumstances.

54 The unconscionable conduct case has also been broadened out as against each Bank insofar as it has not been confined to the particular Bank’s direct counterparties, but also other counterparties to other instruments, products or contracts even though the particular Bank was not a party thereto. I do not need to elaborate further on these broader allegations for present purposes.

55 ASIC has also put a separate case for misleading or deceptive conduct against the Banks. ASIC says that each or all of the relevant counterparties were entitled to be informed or had a reasonable expectation of being informed of the impugned conduct, the rate set trading practice or the risk exposure conduct by reason of the circumstances pleaded, including:

(a) that each of the relevant counterparties was not aware that the relevant Bank had engaged, would engage, or might engage in the impugned conduct, the rate set trading practice, or the risk exposure conduct;

(b) that the relevant Bank knew or ought reasonably to have known or expected the matters in subparagraph (a), but did not disclose to the relevant counterparties that it had engaged, would engage or might engage in the impugned conduct, the rate set trading practice, or the risk exposure conduct;

(c) that the relevant Bank knew or ought reasonably to have known or expected that each of the relevant counterparties understood or was likely to understand that the BBSW was a key financial market reference or benchmark rate which was genuinely, independently and transparently determined; and

(d) the effect or potential effect of the impugned conduct, the rate set trading practice, or the risk exposure conduct on the interests of the relevant counterparties and the knowledge of the relevant Bank of such effect or potential effect.

56 It is said that in the circumstances, the failure of the relevant Bank to inform each or all of the relevant counterparties of the impugned conduct, the rate set trading practice, or the risk exposure conduct constituted conduct in relation to financial services or to financial products that was misleading or deceptive or likely to mislead or deceive because:

(a) the conduct led the relevant counterparties to the erroneous conception or belief that the BBSW, to which their transactions referred, was a genuinely, independently and transparently determined reference or benchmark rate and was or would be unaffected by conduct such as the impugned conduct, the rate set trading practice, or the risk exposure conduct; and

(b) it was reasonable for each or all of the relevant counterparties to infer from the relevant Bank’s silence that no such detriment to them existed or might exist when such detriment did or might exist.

57 In the premises, it is said that the relevant Bank contravened s 1041H of the Act or s 12DA of the ASIC Act by its conduct.

(c) Alleged contraventions of s 912A and other matters

58 ASIC also alleges breaches by the Banks of s 912A of the Act in relation to their Australian Financial Services licences, the detail of which I do not need to set out for present purposes.

asic’s application to amend

59 I have granted leave to ASIC to make the relevant amendments. In my view, they do not greatly change the forensic landscape that the Banks are already required to address on the current pleadings. Moreover, I propose to give the Banks an additional six weeks for the filing of their evidence in any event. Accordingly, they should have sufficient time to address the amended case, particularly given that I have also postponed the trial date for an additional month.

60 There are essentially five types of amendments that ASIC has sought leave to make, and it is convenient to deal with each in turn.

61 First, modifications have been sought concerning the mechanism for how the BBSW was set and the identification of the BBSW Rate Set Window. Such amendments have been brought about as a result of the further review by ASIC of data provided by brokers in the Bank Bill Market, further interviews of persons associated with the BBSW panellists and AFMA, and listening to recordings of trading conducted in that market. Essentially, the amendments are to reflect ASIC’s present position that the Bank Bill Market also traded shortly after 10.00am and that BBSW panellists took such post 10.00am trading into account as to their views of the mid-rate yield for Prime Bank Bills and in relation to their submissions thereon. In my view, ASIC has given an appropriate explanation for the delay in making these amendments, the amendments are sought to accord with the filed evidence of ASIC and the amendments do not substantially add to the forensic landscape.

62 Second, ASIC has sought to add cross-currency swaps as an additional traded BBSW referenced product, being a “financial product” traded on a “financial market” for the purposes of its present s 1041A case and for the new s 1041B case, which I will discuss in a moment.

63 A cross-currency swap is a variation on an interest rate swap. It is an agreement between two parties to exchange:

(a) a principal amount and associated interest payments denominated in one currency; for

(b) a principal amount and associated interest payments denominated in another currency.

64 The parties pay their respective interest payments on dates referred to as “reset dates” and typically exchange the principal amount at the swap creation and maturity date (either in the two currencies or in one currency based on an agreed exchange rate).

65 There are various types of cross-currency swaps. A simple example is a cross-currency swap where the parties agree to swap:

(a) an Australian dollar (AUD) principal amount plus interest payments determined by an AUD interest rate (such as BBSW); with

(b) a principal amount in another currency (currency X) plus interest payments determined by the currency X interest rate (either fixed or floating as agreed between the parties).

66 According to ASIC, cross-currency swaps involving AUD commonly use the BBSW as the AUD interest rate.

67 There is a formula for calculating the cash flow obligations of both swap counterparties on a reset date (other than the creation or maturity date). The detail of this is not relevant for present purposes.

68 It would appear that the need for these amendments arose from ASIC’s more recent enquiries. Now it is apparent that ASIC has always pleaded that cross-currency swaps were BBSW referenced products. The new dimension to its case involving s 1041A is that cross-currency swaps are also “financial products” traded on a “financial market operated in this jurisdiction” and therefore traded BBSW referenced products. I accept that this new dimension adds a new legal complexion to these products. I also accept that there may be additional issues of fact concerning whether such products are traded in a financial market operated in Australia. Nevertheless, on the material before me it does not appear that any new contestable facts will require additional voluminous new evidence. Moreover, ASIC’s evidence is now in. And in any event, the Banks now have until mid-August to respond.

69 Third, ASIC has sought to amend to add various new contraventions concerning:

(a) s 1041B;

(b) s 912A(1)(aa); and

(c) ss 12DB and 12DF of the ASIC Act (in relation to the proceeding against ANZ only).

70 As to the alleged new contraventions concerning s 1041B, ASIC has not sought to put any new or additional factual foundation to that on which its s 1041A case is based. Its case is that such contraventions are established on the material facts currently pleaded. It is convenient to set out s 1041B which provides:

False trading and market rigging – creating a false or misleading appearance of active trading etc.

(1) A person must not do, or omit to do, an act (whether in this jurisdiction or elsewhere) if that act or omission has or is likely to have the effect of creating, or causing the creation of, a false or misleading appearance:

(a) of active trading in financial products on a financial market operated in this jurisdiction; or

(b) with respect to the market for, or the price for trading in, financial products on a financial market operated in this jurisdiction.

(1A) For the purposes of the application of the Criminal Code in relation to an offence based on subsection (1):

(a) intention is the fault element for the physical element consisting of doing or omitting to do an act as mentioned in that subsection; and

(b) recklessness is the fault element for the physical element consisting of having, or being likely to have, the effect of creating, or causing the creation of, a false or misleading appearance as mentioned in that subsection.

(2) For the purposes of subsection (1), a person is taken to have created a false or misleading appearance of active trading in particular financial products on a financial market if the person:

(a) enters into, or carries out, either directly or indirectly, any transaction of acquisition or disposal of any of those financial products that does not involve any change in the beneficial ownership of the products; or

(b) makes an offer (the regulated offer) to acquire or to dispose of any of those financial products in the following circumstances:

(i) the offer is to acquire or to dispose of at a specified price; and

(ii) the person has made or proposes to make, or knows that an associate of the person has made or proposes to make:

(A) if the regulated offer is an offer to acquire—an offer to dispose of; or

(B) if the regulated offer is an offer to dispose of—an offer to acquire;

the same number, or substantially the same number, of those financial products at a price that is substantially the same as the price referred to in subparagraph (i).

Note: The circumstances in which a person creates a false or misleading appearance of active trading in particular financial products on a financial market are not limited to the circumstances set out in this subsection.

(3) For the purposes of paragraph (2)(a), an acquisition or disposal of financial products does not involve a change in the beneficial ownership if:

(a) a person who had an interest in the financial products before the acquisition or disposal; or

(b) an associate of such a person;

has an interest in the financial products after the acquisition or disposal.

(4) The reference in paragraph (2)(a) to a transaction of acquisition or disposal of financial products includes:

(a) a reference to the making of an offer to acquire or dispose of financial products; and

(b) a reference to the making of an invitation, however expressed, that expressly or impliedly invites a person to offer to acquire or dispose of financial products.

71 Contrastingly, the Banks make the point, correctly in my view, that howsoever ASIC wishes to put and substantiate its new case, substantial work will be required to analyse this new case and that new legal and forensic questions and defences are likely to arise. It is to be noted that s 1041B(1)(b) has two aspects being either “a false or misleading appearance … with respect to the market for …” or “a false or misleading appearance … with respect to … the price for trading in …”. This second aspect has some resonance with the themes in s 1041A, although I accept that it is different. For example, it may be said that s 1041A looks at effect or likely effect. Contrastingly, it may be said that s 1041B looks at appearance. Arguably, effect or likely effect on price may affect appearance. But arguably appearance may not require effect or likely effect on price to be demonstrated. Further, “price” in s 1041B(1)(b) arguably differs from the concept of “artificial price” in s 1041A. In other words, one could say that ASIC’s new case under s 1041B(1)(b) might succeed even if it failed on its case under s 1041A seeking to establish an “artificial price”. An act or omission, in this case the alleged manipulation by the Banks, arguably could have the effect of creating or causing the creation of a false or misleading appearance even if the price for trading in the relevant financial products was not an “artificial price”. Further and in any event, the first aspect of s 1041B(1)(b), namely “false or misleading appearance … with respect to the market for …” is arguably a different and broader concept than s 1041A. Now these questions are all matters for trial. But for present purposes, I have little doubt that the Banks in meeting the new s 1041B case will be raising new legal and forensic questions and defences, whatever the narrower factual foundation that ASIC is basing its case on. Nevertheless, I am not satisfied that the Banks will not be able to address such matters by mid-August.

72 As to ASIC’s additional case concerning s 912A(1)(aa) dealing with an allegation that each Bank did not have in place adequate arrangements for the management of any conflict of interest between:

(a) that Bank’s interest in managing its BBSW rate set exposure and incentives relevant thereto; and

(b) the interests of affected counterparties in respect of financial services provided by that Bank,

again it may be accepted that the Banks will need to make additional enquiries and require time for the preparation of evidence. But no detailed and probative evidence put to me suggested that this could not be done by mid-August, together with the other evidence preparation.

73 As to ASIC’s additional case concerning the ANZ proceeding dealing with ss 12DB and 12DF of the ASIC Act, these claims seem to me to give rise to different legal consequences and characterisations, but to facts already pleaded. Now I accept that the ANZ in defence thereof may raise other legal or forensic responses, but like the other amendments discussed above, I have been given no detail of what they might be, let alone any detail which might suggest that mid-August is not an achievable date for the filing of evidence to deal with such matters.

74 Fourth, ASIC has sought to make proposed amendments to Pleading Schedule 1 in each proceeding and Pleading Schedule 2 in each of the ANZ and Westpac proceedings to make what I would describe as arithmetic changes to exposure and trading figures. This is to ensure greater accuracy. It was not seriously suggested that the Banks could not readily deal with and assimilate such changes in their case preparation to meet a mid-August evidentiary filing date.

75 Fifth and finally, ASIC has sought to make changes in the NAB proceeding concerning the NAB’s organisational structure and internal conduct policies. I accept ASIC’s evidence to the effect that these changes were brought about as a consequence of reviewing NAB’s defence, the provision of further documents by NAB and information arising from a conferral process between ASIC and NAB. In my view, NAB is unlikely to be caught by surprise with these amendments and it is likely that it is already preparing its evidence on such a basis in any event. Moreover, I am confident that it will be able to address these matters by mid-August.

76 In summary:

(a) ASIC has given a proper explanation for the late amendments.

(b) The amendments raise claims that in substance are based on substantially the same or similar facts as those already pleaded.

(c) The amendments (as I have allowed) will ensure that so far as possible, all matters in controversy between the parties will be dealt with completely and finally.

(d) If there is any prejudice to the Banks, it can be adequately dealt with by the usual orders for costs and an extension of time for the filing of their evidence until mid-August.

77 My views are also fortified by the following further matters. First, neither the ANZ nor Westpac filed any evidence deposing to prejudice flowing from the amendments. Their real concern related to the volume of ASIC’s evidence and its late service relating to the case already pleaded, although their concern was said to be exacerbated by the proposed amendments. I will deal with their concern in the next section of my reasons. Second, in relation to the NAB, it did file evidence in the form of an affidavit sworn by Mr Alexander Morris, partner of the firm King & Wood Mallesons, which was supplemented by some oral evidence. Much of his affidavit was a chronological sequence of what ASIC had filed and when. I will deal with this in a moment. Only [10(e)] of his affidavit, which was in a conclusionary form, dealt with the amendments, and then with no detail in terms of their consequences. Other paragraphs (see at [52] and [54]) did not deal with the amendments in terms.

78 As a consequence of the foregoing and in the context of postponing the Banks filing and service of evidence until mid-August, I granted ASIC leave to make the requested amendments in each proceeding.

extension of time for banks’ evidence

79 The Banks each applied to vary my orders to extend the time until 31 August 2017 for filing their evidence.

80 They raised the following common themes to justify such an extension:

(a) First, ASIC had been late in filing its evidence.

(b) Second, ASIC’s evidence in volume and scope was significantly greater than what had been contemplated at the time I made the 9 December 2016 orders.

(c) Third, justice required that I give them the time that they asked for to complete their evidence. I would note that ANZ and Westpac asserted such an entitlement without putting any evidentiary foundation justifying why they needed until 31 August 2017.

81 Let me begin with some context. The ANZ proceeding was commenced on 4 March 2016. The Westpac proceeding was commenced on 5 April 2016. The NAB proceeding was commenced on 7 June 2016. The ANZ proceeding was followed on 6 May 2016 by a very detailed pleading by ASIC with voluminous schedules of particulars. This also occurred in the Westpac proceeding on 13 May 2016 and the NAB proceeding on 8 July 2016. At these times, ASIC gave full details of the identity and intention of the relevant traders on each alleged contravention date. It also gave comprehensive details of the knowledge and implementation of the rate set trading practices alleged in relation to each Bank. Moreover, the various proceedings had been commenced after substantial ASIC investigations which had involved the Banks, no doubt putting them on notice to some extent and provoking their own inquiries to some extent before the commencement of proceedings. On 9 December 2016, I fixed the proceedings for trial on 25 September 2017. I made the following order concerning the sequencing of the trial stages:

1. Subject to further order, the trial of VID 604/2016 (ASIC v National Australia Bank Ltd) (the NAB proceeding) and proceedings numbered VID 197/2016 (ASIC v Australia and New Zealand Banking Group Limited) (the ANZ proceeding) and VID 282/2016 (ASIC v Westpac Banking Corporation Ltd) (the Westpac proceeding) (together, the BBSW proceedings) will be heard as follows:

(a) the common issues of fact and law will be heard together (common issues hearing);

(b) the remaining issues, namely those that are specific to each proceeding will be heard immediately after the common issues hearing in the following sequence:

(i) the ANZ proceeding;

(ii) the Westpac proceeding; and

(iii) the NAB proceeding.

82 As part of my 9 December 2016 orders, in each proceeding ASIC’s evidence was ordered to be filed and served by 31 March 2017, with each Bank’s evidence to be filed and served by 30 June 2017 (ie three months later). It can be accepted that much of ASIC’s evidence was served late and I ultimately agreed on 7 April 2017 that it should have until 27 April 2017 to serve all material. The Banks’ present position is that they have sought a date of 31 August 2017 for their evidence. So, the three months relative difference (31 March to 30 June 2017) has been sought to be increased to four months (27 April 2017 to 31 August 2017). Moreover, a substantial amount of material was served by ASIC on and prior to 31 March 2017 pursuant to the previous direction. So for this ASIC evidence, the Banks now effectively want five months (31 March 2017 to 31 August 2017) to respond. This is all in the context where ASIC’s detailed case in each proceeding has been advanced through substantial particulars provided many months ago and where it is reasonable to assume that the Banks ought to have commenced their evidence preparation before waiting to receive ASIC’s evidence.

The nature of the evidence served by ASIC

83 The Banks have made much about the volume of material and the cross-served evidence, that is, evidence served by ASIC in one proceeding being served and relied upon in the other proceedings. Their arithmetic and volumetric approach had a superficial attraction. But their submissions failed to give context. I accept the evidence of ASIC which gave the following description and context to the material that it has served.

84 In the ANZ proceeding, ASIC relies upon 116 affidavits and expert reports consisting of the following:

(a) 83 counterparty affidavits, of which 35 relate to the ANZ proceeding and the remaining 48 affidavits relate to the NAB and Westpac proceedings. The counterparty evidence goes predominantly to two issues:

(i) the counterparties’ lack of knowledge of the impugned conduct; and

(ii) their reaction to the impugned conduct (if established) and the corresponding failure of the relevant Bank to disclose that conduct.

(b) 16 affidavits filed in all three proceedings being the following:

(i) Seven affidavits and outlines from employees of BBSW panellists responsible for making submissions to AFMA as part of the BBSW setting process. These affidavits and outlines provide evidence of the practice of the submitters during the relevant period.

(ii) An affidavit from the ASX directed to authenticating BAB Futures data.

(iii) Two affidavits from AFMA. The AFMA affidavits describe the role of AFMA in relation to BBSW, the codes, conventions and standards produced by AFMA in relation to BBSW, the BBSW calculation and publication process and authenticating various documents and BBSW submissions data produced to ASIC.

(iv) An affidavit from the operator of the financial market, BGC Trader. The BGC Trader affidavit describes the operations of BGC Trader, the process for trading interest rate swaps and cross-currency swaps through BGC Trader, and details of the trades in interest rate swaps and cross-currency swaps through BGC Trader during the relevant period.

(v) Two affidavits from brokers in the Bank Bill Market. The broker affidavits describe operations of brokers, the communications systems through which traders at the Banks interacted with brokers, the systems which resulted in the real time publishing of bids and offers for Prime Bank Bills by external information vendors Bloomberg and Reuters, and the details of trades in Prime Bank Bills in the relevant period.

(vi) Three ASIC affidavits analysing and summarising the BBSW submissions data provided to ASIC by AFMA and the trading data provided by BGC Trader.

(c) Five ASIC affidavits directed at authenticating documents produced by ANZ to ASIC or transcripts of ANZ telephone calls, and summarising broker data produced to ASIC.

(d) Two expert reports.

(e) Two ASIC affidavits directed at authenticating documents produced by Westpac to ASIC or transcripts of Westpac telephone calls.

(f) Two ASIC affidavits directed at authenticating documents produced by NAB to ASIC or transcripts of NAB telephone calls.

(g) Six affidavits/outlines of evidence from NAB employees.

85 In the Westpac proceeding, ASIC relies upon 115 affidavits and expert reports consisting of the following:

(a) The 83 counterparty affidavits referred to above, of which 12 relate to Westpac and the remaining 71 affidavits relate to the ANZ and NAB proceedings.

(b) The 16 affidavits filed in all three BBSW proceedings referred to above.

(c) Two ASIC affidavits directed at authenticating documents produced by Westpac to ASIC or transcripts of Westpac telephone calls (as referred to above).

(d) Two expert reports.

(e) Four ASIC affidavits directed at authenticating documents produced by ANZ to ASIC or transcripts of ANZ telephone calls (see above).

(f) Two ASIC affidavits directed at authenticating documents produced by NAB to ASIC or transcripts of NAB telephone calls (see above).

(g) Six affidavits/outlines from NAB employees (see above).

86 In the NAB proceeding, ASIC relies upon 115 affidavits and expert reports consisting of the following:

(a) The 83 counterparty affidavits referred to above, of which 36 relate to NAB and the remaining 47 affidavits were filed in the ANZ and Westpac proceedings.

(b) The 16 affidavits filed in all three proceedings referred to above.

(c) Six affidavits/outlines from NAB employees (see above).

(d) Two ASIC affidavits directed at authenticating documents produced by NAB to ASIC or transcripts of NAB telephone calls (see above).

(e) Two expert reports.

(f) Four ASIC affidavits directed at authenticating documents produced by ANZ to ASIC or transcripts of ANZ telephone calls (see above).

(g) Two ASIC affidavits directed at authenticating documents produced by Westpac to ASIC or transcripts of Westpac telephone calls (see above).

87 In the NAB proceeding, ASIC also relies on extracts from the transcripts of examinations of 15 NAB employees conducted pursuant to s 19 of the ASIC Act for the purpose of establishing admissions made by those NAB employees (and the correlative parts of relevant tape recordings).

88 ASIC also intends to rely in all three proceedings on the following:

(a) An outline of evidence from the operator of the Bloomberg Professional Service and the BETSY financial market. The Bloomberg evidence describes the operations of BETSY, the process for trading interest rate swaps through BETSY, and details of the trades in interest rate swaps through BETSY during the relevant period.

(b) An affidavit of a further NAB counterparty.

(c) The supplementary affidavits of two ASIC employees.

(d) An affidavit of an employee of ICAP.

89 With the exception of the documents annexed to the counterparty affidavits, the substantial majority of the documents exhibited or annexed to the affidavits filed in each of the proceedings were previously served on the Banks in tranches as follows:

(a) on ANZ on 31 January 2017, 10 February 2017, 24 February 2017, 16 March 2017 and 3 April 2017;

(b) on Westpac on 31 January 2017, 10 February 2017, 24 February 2017, 15 March 2017, 3 April 2017; and

(c) on NAB on 31 January 2017, 17 February 2017, 8 March 2017, 20 March 2017, 3 April 2017, 6 April 2017 and 19 April 2017.

90 But this does not include the documents that were filed in one of the proceedings and subsequently served in the other two proceedings.

Counterparty and cross-served evidence

91 The evidence filed and served in each of the proceedings has been (with the exception of one affidavit filed and served in the ANZ proceeding) served in the other two proceedings as follows:

(a) ANZ proceeding – evidence filed in the Westpac and NAB proceedings was served on 21 April 2017;

(b) Westpac proceeding – evidence filed in the ANZ and NAB proceedings was served on 21 April 2017;

(c) NAB proceeding – evidence filed in the ANZ and Westpac proceedings was served on 20 April 2017.

92 In relation to the cross-served material and counterparty evidence more generally, I would note the following:

(a) First, ten of the affidavits cross-served are of ASIC personnel for the purposes of authenticating documents produced by a Bank to ASIC or transcripts of telephone calls of that Bank’s personnel. ASIC has submitted that the records of internal communications within each Bank are relevant in the proceedings against the other Banks as it is said that they demonstrate a persistent belief amongst persons regularly trading in and observing the Bank Bill Market that the market was susceptible to manipulation through trading with a or the purpose of influencing the price of Prime Bank Bills.

(b) Second, the other affidavits cross-served (other than counterparty affidavits) consist of six affidavits/outlines of NAB staff who worked in roles related to the trading of Prime Bank Bills during the relevant period. ASIC has submitted that this evidence is relevant to: (i) the objective features of the Bank Bill Market, such as the precise timing of the concentrated trading during the BBSW Rate Set Window; (ii) that Market’s susceptibility to manipulation through trading with a or the purpose of influencing the price of Prime Bank Bills; and (iii) the conduct of other participants in that Market.

(c) Third, as to the numerous counterparty affidavits, ASIC has submitted that this evidence is relevant in all the proceedings as evidence of the lack of knowledge of counterparties to BBSW referenced products as a broad class and what each Bank ought reasonably to have expected counterparties to be aware of. ASIC has said that although the counterparty affidavits represent only a sample of all counterparties to BBSW referenced products, it is its case that it will seek to rely on the evidence of particular counterparties as indicative of the characteristics of counterparties more broadly.

93 I accept that the Banks have been surprised about the extent of the cross-served material, and that in relation to each Bank cross-served with material from the other proceedings this was served outside the period previously ordered in relation to ASIC’s evidence.

94 Nevertheless, it seems to me that each Bank ought to be able to assimilate and deal with this material by mid-August. I say this for the following reasons. First, although each Bank will need to analyse all cross-served material, nevertheless it may be accepted that the particular Bank, on which the material was served principally in the first instance dealing with that Bank’s own documents, traders, other employees, practices and counterparties (the “principal” Bank), will prepare the necessary response. But if that assumption is not made good, I will give time to the other Banks to supplement their evidentiary response after they have seen what the “principal” Bank files by way of evidence dealing with its own documents, traders, other employees, practices and counterparties. There will be adequate time after mid-August to permit this to occur (if necessary) before a late-October trial commencement, and particularly given the staging for tranches of evidence that I have foreshadowed. Second and more generally, the scope of the counterparty affidavit evidence (whether or not cross-served) should not be exaggerated; this material goes principally to the unconscionability case. Although there are a great number of these affidavits, they are short and in fairly common form, ie dealing with their lack of knowledge of the Banks’ alleged practices. Indeed, on one view of the Banks’ defences, and given that the Banks deny the alleged practices, this lack of knowledge may not ultimately be contestable. I accept though that the issue of detriment will loom large. Is the detriment to be characterised as exposure of the counterparty to the downside risk? Or is the detriment the counterparty’s actual financial loss? And if the latter, does a counterparty’s aggregate or net exposure need to be looked at across its total position? In the first instance, I accept that the answer to that question may require some detailed analysis (and evidence preparation) by the particular Bank that is a party to the transaction with the counterparty. But allowing to mid-August ought to be sufficient for that to occur by each Bank in relation to their direct counterparties. But if it is not, I may allow further time and postpone the tranche of evidence dealing with counterparties until later in the trial. I would rather neither speculate nor act on theoretical possibilities at this stage.

Expert evidence

95 Let me add some further context concerning the expert evidence.

96 There has been limited expert evidence filed by ASIC, which is now complete so far as each proceeding is concerned, being a report filed for Dr Tiago Duarte-Silva concerning the question of whether yields on Prime Bank Bills and changes thereto affected BAB Futures and a report filed for Professor Talis Putnins discussing microeconomic analysis, particularly market microstructure theory, going to the question of the extent to which sales and purchases of Prime Bank Bills on the Bank Bill Market by a participant therein had a causal effect on the BBSW.

97 This limited expert evidence was served on or prior to 31 March 2017 and in accordance with my previous orders, albeit that some data and modelling was not provided by ASIC to the Banks until more recently. I originally provided for the Banks to respond within three months, but I will now allow until mid-August for their response. It was not suggested that this was not achievable to both respond to ASIC’s expert evidence and for the Banks to file any other expert evidence beyond the scope of ASIC’s expert evidence. Nothing Mr Morris for the NAB said in his oral evidence of probative value demonstrated that a mid-August date for expert evidence was definitely unachievable.

98 Further, in terms of the length of time now allowed between the Bank’s mid-August filing date and the new trial date (some two months), I would also note the following matters concerning the expert evidence.

99 First, at this stage I do not propose to permit ASIC to file reply expert evidence. I have made orders for an expert conclave and a joint report that should act as a substitute for reply evidence. ASIC’s experts should be able to make any necessary reply points in a joint report. But if new areas of expert evidence are opened up by the Banks outside the subject matter and expertise of ASIC’s current experts, I may revisit this question.

100 Second, the expert conclave and joint report will take place with limited, if any, involvement of the parties’ lawyers other than administrative support services (ie coordinating dates, arranging the venue, provision of a typist and the like). Accordingly, the parties and their advisors will be able to use the two months window for other case preparation including a mediation.

101 Third, if there are any unexpected delays in the expert evidence timetable, such delays are unlikely to affect the trial date. I may push back my hearing of the tranche of expert evidence in the case to accommodate such an eventuality.

102 Finally, there may be other s 79 opinion evidence from industry participants in terms of how the relevant market(s) operated or how various products were priced or traded. But this will be dealt with in the running as part of the sequencing of the trial issues. Such evidence will not be part of the expert conclave / joint report protocols.

trial date

103 As a consequence of the late service of ASIC’s evidence and the extension of time I have given to the Banks to file their evidence, I postponed the trial date for one month until 23 October 2017. Essentially the Banks sought to postpone it to a later time than this; indeed Westpac suggested a start date around May 2018.

104 In my view, there is more than adequate time between mid-August and 23 October 2017 for other necessary trial steps and preparation to occur. I say this for a number of reasons including the following.

105 First, in relation to reply evidence from ASIC, I do not propose to have expert reply evidence for the reasons that I have given. As to reply lay evidence from ASIC, it is unclear at the moment what the subject matter and volume of this will be and whether that will be of such a magnitude as to warrant any further postponement of the trial. No doubt ASIC has an incentive to efficiently confine any reply lay evidence to that which is necessary. I would also note that ASIC’s need for reply evidence will be a function of the Banks’ evidence. Currently, the Banks have not stated in any detail what evidence they propose to file and the likely magnitude thereof. There is a spectrum of possibilities. Indeed, that is a further reason for not assuming at the moment that a 23 October 2017 trial date is not readily achievable.

106 Second, steps can take place concurrently (if necessary) concerning expert conclaves (not involving legal practitioners), mediation and trial preparation. To extol the virtues of a perfectly linear sequence of steps may conform to a Platonic idealisation of litigation, but otherwise lacks allure.

107 Third, given the manner in which ASIC has cross-served its material and the justification for that course in terms of how it says that such evidence in one case is relevant and admissible in the other two cases, it may not be feasible to have a voir dire / s 192A preliminary hearing prior to trial, but to deal with such questions after opening addresses. Moreover, if ASIC’s position is ultimately sustainable on this aspect, there may be less utility in having bright line divisions between the issues as I directed on 9 December 2016, but rather to hear tranches of evidence by reference to broad categories of subject matter substantially conforming to the spirit of the sequencing set out in the 9 December 2016 directions. I will keep this matter under review and will discuss it with the parties at the next case management hearing after the Banks’ evidence has been filed. But if it is necessary to have a preliminary hearing and rule upon the identification of common issues, cross-admissibility questions and the like, there is likely to be more than adequate time to do this well before a 23 October 2017 start date. Indeed I may deal with some of these matters on the papers in the interests of efficiency.

108 Fourth, a number of the Banks’ submissions seemed to raise multiple contingent hypothetical problems which they suggested justified postponing the trial date until 2018. I would rather deal with known problems as and when they arise rather than hypotheticals, unless the chance of the hypothetical scenario eventuating is high and the potential detriment arising therefrom is of such a magnitude and cannot be ameliorated by later appropriate procedural steps, such that it must now be anticipated and addressed.

109 Fifth, in relation to the evidence given by Mr Morris, after considering his oral evidence (including ASIC’s cross-examination), which added detail to the generalised assertions in his affidavit at [10], [52] and [54], I determined that the appropriate balance was to allow a mid-August filing date for NAB and the other Banks’ evidence. And as to his evidence concerning the appropriate procedural steps thereafter (see [55] and [56] of his affidavit), this was in the nature of submissions the substance of which I have addressed earlier.

110 Sixth, I accept that the NAB proceeding was filed and served several months after the other proceedings. But going forward, I do not now consider that this is a sufficiently distinguishing feature such that future directions now necessarily require specific tailoring to accommodate that historical narrative.

111 Finally, much criticism has been made of ASIC in terms of its late service of evidence. But what is, is. The issue that has concerned me is to solve the problem going forward. What I have ordered is an appropriate and adequate solution.

Conclusion

112 For the reasons set out above, I made the 28 April 2017 orders in each proceeding.

I certify that the preceding one hundred and twelve (112) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Beach. |

Associate:

Dated: 5 May 2017