FEDERAL COURT OF AUSTRALIA

Zappia v Commissioner of Taxation [2017] FCA 390

ORDERS

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The application be dismissed.

2. The Applicant pay the Respondent’s costs as taxed or agreed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Perram J:

1. Introduction

1 On 30 June 2010, Mrs Rose Zappia received $2 million into a bank account maintained in her name with the National Australia Bank (‘NAB’). She did not include this sum as income in her income tax return for the 2010 year. During the 2011 year, interest was earned on the same funds but Mrs Zappia did not include that interest in her income tax return for the 2011 year either. The Commissioner is of the view that the $2 million was on revenue account and should have been returned by her as income in the 2010 year together with the interest on it in the 2011 year. He issued default assessments to her to that effect and, at least on this issue, has rejected her objection that the $2 million was not income (although he did accept that she was entitled to certain deductions in relation to that amount).

2 Mrs Zappia now appeals to this Court under the provisions of Part IVC of the Taxation Administration Act 1953 (Cth) (‘the TAA’). The effect of s 14ZZO(b)(i) of the TAA is that Mrs Zappia needs to demonstrate for the purposes of the appeal that the two assessments issued to her are excessive or otherwise incorrect. Consequently, Mrs Zappia must prove what her assessable income was in each of the 2010 and 2011 years and must also demonstrate that each was less than the amounts which the Commissioner assessed: see Mulherin v Commissioner of Taxation [2013] FCAFC 115; (2013) 96 ATR 835 at 846 [42] .

3 There are many ways such a forensic task might be undertaken, but in this case Mrs Zappia, or at least her advisers, has decided that she should go through the front door and prove that the $2 million was not income. I emphasise this because it identifies an important feature of the forensic tussle which this Court was called upon to resolve. The issue is not whether the Commissioner made an error nor, perhaps a little surprisingly, even whether the $2 million is assessable income. Rather, it is whether Mrs Zappia has proven that the $2 million is not assessable income. It is implicit in that statement, which is about who bears the burden of proof, that the Commissioner is under no obligation to prove that the $2 million was income. The onus lies, rather, on Mrs Zappia to prove that it was not.

4 The principal issue in the appeal therefore concerns the status of this $2 million and what Mrs Zappia has proved about it. There is a second set of minor procedural issues relating to the objections process itself. It is best to start with the facts.

2. The Facts

5 Mrs Zappia is the wife of Mr John Zappia. Mr Zappia is a property developer. Since 2007, he has been attempting to develop a property at Shingley Drive, Airlie Beach, in Queensland. Airlie Beach is a popular tourist destination. There are two parcels of land involved: Lot 95 on HR 1223 (‘Lot 95’) and Lot 268 on HR 1060 (‘Lot 268’); both in the Parish of Conway. The development was to be known as the ONE Whitsundays Project or the ONE Whitsundays Resort and Spa. A planning approval issued in relation to the project suggested that several buildings were contemplated and that some might have been as high as 8 stories. All up there were to be 75 multiple dwelling units together with some shops, refreshment premises, a function room and a health club.

6 It appears that Mr Zappia pursued the development of the project through an entity named after Shingley Drive (where the property is situated) called Shingley Projects Pty Ltd (‘Shingley’). Mr Zappia is the sole director of Shingley. On 20 April 2007, there was settled the Shingley Unit Trust (‘the Trust’), the trustee of which was Shingley. The Trust had only one unitholder, Mr Zappia. It seems that the development was to be effected through the Trust.

7 To pursue development of the project it was necessary for Mr Zappia to arrange finance. The initial financier was Capital Finance. Although the evidence about this is not totally clear it appears likely that this was to be an interest only facility. Apart from a loan balance document, none of the transactional material involving Capital Finance was placed before the Court. There was an initial drawdown from the facility on 12 October 2007 of $8,931,339.49 (excluding GST) which I infer was used, in part, to purchase Lots 95 and 268. Mr Zappia says that the project encountered immediate difficulties because of the Global Financial Crisis (‘GFC’) in 2007-2008. According to Mr Zappia, this was because the crisis reduced the public’s appetite for apartments of the kind he was seeking to develop. The situation was also exacerbated by a slow approval process for the development which had been attended by community opposition. Additionally, Mr Zappia thought that the value of the Shingley Drive land dropped once it had been purchased.

8 These stresses contributed, according to Mr Zappia, to the Trust defaulting on its facility with Capital Finance. The Respondent was in no position to challenge this assertion and it was never submitted that I should not accept it. I am bound to observe, however, that the evidence concerning it puzzles me. Presumably, the Trust’s business model involved borrowing the money to buy the land and develop it. Mr Zappia anticipated that the full construction cost would be around $55 million, $45 million of which he was proposing to borrow from the NAB. No doubt the apartments would be sold off the plan but these transactions would not settle until the building work was complete and, in the meantime, the Trust would not, in the ordinary course, have access to any deposits that were paid. It seems quite unlikely that the Trust’s ability to service its interest-only cash advance from Capital Finance was ever going to come from the development whilst it was under construction. It is not clear to me how, therefore, a steep decline in the number of intending purchasers would, by itself, have led to an inability to service the facility. In saying that I do not doubt that such a decline imperilled the project from a broader perspective but it is difficult to see that it was the cause of the direct stress on the facility. This raises another related mystery. The $45 million NAB facility never occurred but, if it had, it is quite unclear how the Trust could have serviced the interest on that facility unless it was capitalised.

9 Regardless of these puzzles, Mr Zappia says that because of the Global Financial Crisis the Trust did not have ‘the resources and financial capacity…to pay the Capital Finance Loan’. From 2008, Mr Zappia says he was on the lookout for ‘financial partners so as to pay out and get rid of Capital Finance’. Because it will be presently relevant when a different perspective emerges, it is worth noting that this sought after arrangement was not project finance in the strict sense but a refinancing (by debt or equity) of a pre-existing facility which had been used, at least in part, to purchase land. It is inherent in that arrangement that what would be sought would not involve payment in tranches.

10 In his search for equity partners, Mr Zappia says that he had a conversation in early 2010 with one Pierre Moio, whose family ran a restaurant in Darling Harbour. He told Mr Moio that he was looking for a partner ‘who will come on board and be a participant in the project and share the risks with me’.

11 Mr Zappia recalls that Mr Moio thought that he could help; and help he did, by introducing Mr Zappia to Mr Gino Cassaniti, who was an accountant at Banq Accountants. Mr Zappia then had a conversation with Mr Cassaniti in early March 2010. Mr Zappia opened the conversation by telling Mr Cassaniti that he was looking for people willing to share the risk and that he would offer them completed apartments. Mr Zappia says that he told Mr Cassaniti that he needed $12 million over stages. This makes little sense in light of his own evidence that he wanted the money ‘to pay out and get rid of Capital Finance’. Since Mr Zappia has not explained what the initial $8.9 million was spent on, it is difficult to understand the existence of any ongoing obligation which required these sums.

12 Mr Cassaniti then told Mr Zappia that this would be fine and that the Zeitouni brothers (of whom more later) – Leonard, Malik and Habib - would be interested in the deal. They would want a 50% return which would be paid by way of apartments. The deal would need to be documented and he, Mr Cassaniti, would set up a meeting with the Zeitounis’ solicitors, Leonard Legal, in Phillip Street. Mr Cassaniti’s fee for arranging this would be $300,000 which would take the form of an apartment. Mr Cassaniti would also organise for a draft agreement to be prepared.

13 There are a number of aspects of Mr Zappia’s evidence of this conversation which are surprising. First, on Mr Zappia’s evidence he conveyed no information about the equity investment in the project beyond the fact that it was a project in the Whitsundays and that the equity offering would take the form of apartments. Secondly, Mr Cassaniti was sufficiently informed by this vanishingly sparse information that he was immediately able to say that the Zeitouni brothers ‘may be able to help’. Thirdly, Mr Zappia’s evidence that he needed $12 million makes some sense given that this appears to have been a little more than the size of the Capital Finance loan plus interest incurred to that date, but his statement that he wished to have it in stages makes no sense at all in light of his earlier evidence that he wished to get rid of Capital Finance entirely. Fourthly, it is odd that Mr Cassaniti was sure enough that the transaction would proceed from the Zeitounis’ end to justify the drawing of transactional documents. Fifthly, Mr Zappia did not blink at Mr Cassaniti’s proposal that his fee be $300,000 or that it would be taken in the form of an apartment in lieu.

14 It was then on 22 March 2010 that Mr Zappia says that Mr Cassaniti sent through a proposed first draft of an investment deed between Shingley, as trustee for the Trust, and an entity called Jianxi Trade and Commerce Inc (‘Jianxi’). Mr Zappia did not know or care about the identity of Jianxi.

15 This draft is, at least in some ways, instructive. It came under cover of an email chain which commenced on 22 March 2010. It included Mr Cassaniti and one of Banq Accountants’ employees, Mr Fred Khalil. Another recipient involved in the email chain was Mr Niko Aquilina. Mr Zappia says that Mr Aquilina was his development manager.

16 Mr Zappia says he received the draft from Mr Cassaniti but this is not what the email shows. It seems it was Mr Aquilina who sent through the draft agreement to Banq Accountants on 22 March 2010. His email to Mr Cassaniti reads:

‘Hi Gino,

Attached is the updated WORD document with your changes, there are also some changes which were made just prior to our meeting last week, I had not sent this to you as I had hard copies on the day.

Just minor changes, take a look and let me know if its ok.

Thanks,

Niko’

(errors in original)

17 Mr Zappia says that it was Mr Cassaniti who sent through the deed and this is, it is true, one possible way of reading the email chain which does have at its end an email from Mr Cassaniti to Messrs Zappia and Aquilina. Unfortunately, one cannot tell whether this email had an attachment; further, it has no text from which its purpose might be inferred.

18 Mr Zappia does not refer in his evidence to the changes that Mr Aquilina sent through.

19 Mr Zappia’s evidence is that the terms and conditions were discussed at a meeting held on 30 March 2010 at Banq Accountants. This overlooks Mr Aquilina’s email which clearly shows negotiations over the terms had happened in the week preceding 22 March 2010.

20 The draft deed of 22 March 2010 contains a number of riddles which are not readily answered. The first concerns its origins. Mr Zappia says he received the deed from Mr Cassaniti but the draft deed is in mark-up mode and a number of the edits are curious. These curiosities include:

the recitals originally included the statement ‘Lavy, Selz, Anusaitia and Albatross are hereinafter referred to in this Agreement as (‘the Investor’)’. This rather suggests, although it does not prove, that the agreement did not first emerge in draft form from Jianxi (or the Zeitouni brothers) whose role seems to have been antedated by ‘Lavy, Selz, Anusaitia and Albatross’;

at some point the draft deed contained at least two clauses requiring some step to be taken by 7 June 2007. This is three years before Mr Zappia says these negotiations occurred. It is difficult to know what this might mean; and

the earlier 2007 version of the deed contained references to Shingley so this is not an example of a current draft template.

21 Also relevant are the terms of the draft deed itself. The principal obligation of Jianxi was set out in 2.1(a):

‘2.1 …

(a) the Investor will provide $12,204,000 in a series of tranches beginning at the execution of this agreement until the full amount is drawn down or funds provided as required.

…’

22 This was surprising given, as I have already mentioned, that Mr Zappia wished to receive the money to refinance its facility with Capital Finance and get it out of the picture. Indeed, the whole thrust of his earlier evidence was the need to relieve the stress caused by the GFC and to remove Capital Finance from Mr Zappia’s affairs. At this point Mr Zappia’s purpose seems to have changed. Proposed cl 2.1(b) now made clear that the funds were to be used for project costs:

‘‘2.1 …

…

(b) the funds will be used by the Developer for project related costs.

…’

23 The machinery of the investment was that Shingley, as trustee for the Trust, would receive $12,204,000 in return for 15 contracts for the sale of specified apartments in the development at specified prices. For example, apartment 74 was to be sold at a value of $3,250,000. The purchaser was to be Jianxi or one or more of its nominees.

24 Whatever the status of the earlier meeting or this draft may have been, Mr Zappia’s evidence was that he attended another meeting on 30 March 2010 at the premises of Banq Accountants about the transaction. Present were Mr Cassaniti, Mr Zappia and Mr Tino Di Bello, a solicitor from Leonard Legal.

25 At this point, another source of evidence becomes available about the transaction: Mr Di Bello, the solicitor for the Zeitouni brothers, kept a file for it. The file is detailed and contains a number of reasonably comprehensive file notes.

26 The earliest document on the file is the email of 23 March 2010 enclosing the then version of the draft deed. Between 23 March 2010 and 9 June 2010, a number of meetings took place between Mr Di Bello, the Zeitounis and their accountants. There were also meetings with Mr Zappia and his advisers. As I foreshadowed above at [24], the first meeting on the file occurred on 30 March 2010. It was a meeting between Mr Di Bello, Mr Zappia and Mr Cassaniti. The proposed terms of the agreement were discussed in detail.

27 The file note reveals that Mr Zappia was planning to borrow $45 million from NAB and that the construction costs including the land would be around $55 million. Mr Zappia said he needed about $10 million from Leonard Zeitouni. Building work had not yet commenced but a start was anticipated in 2 to 3 months. The land would first be cleared and levelled.

28 One mystery which the file note gives rise to is what the $10 million from Leonard Zeitouni was to be used for. Mr Zappia’s affidavit evidence very much identified this proposed facility as a means to refinance the initial Capital Finance facility, but the transaction described in this file note seems to assume that the $10 million would be used as project finance. This is an assumption also made in the draft agreement which had been circulated. I am not able to reconcile Mr Zappia’s evidence about the urgent need to refinance the Capital Finance facility because of the GFC and the subsequent negotiation of what appears only to be project finance. The discrepancy between the $12,204,000 contemplated by the draft agreement and the $10 million offered by Mr Zeitouni was likewise never really addressed.

29 On 6 April 2010, Mr Di Bello met with two of the Zeitouni brothers and Mr Cassaniti. Terms were discussed. At some point during the meeting someone said something which was recorded in the file note as:

‘-when Capital Finance is discharged will release mortgage on Zentrix – s/station at Woodpack.’

30 There is a continuing obscurity as to what was being borrowed. On 5 May 2010, there was a meeting between Mr Di Bello, two of the Zeitouni brothers, Mr Cassaniti and Mr Zappia. It is evident from Mr Di Bello’s detailed file note that there was a thorough discussion of the proposed transaction. These discussions at one point caused Mr Di Bello to record that Mr Zappia needed the next payment to be $12 million. It records:

31 Later in the file note it was recorded that:

32 It is quite difficult to understand entirely what this transaction was going to be. Was it to be a refinancing of the approximately $12 million owed to Capital Finance in capital plus interest at that date? Or was it project finance? And what was the reference to $3 million? The draft agreement suggested that such a sum may already have been advanced. No attempt was made by Mr Zappia to explain what any of this meant.

33 It is apparent from Mr Di Bello’s file that various steps consistent with the preparation of an equity investment by the Zeitouni brothers through Jianxi then took place: a quantity surveyor was engaged to estimate the construction costs and statements of the amounts already spent, and to be spent, on the project were obtained from Mr Zappia. At the same time, the draft deed underwent various changes.

34 All of this, which I accept is consistent with some kind of real transaction being documented, may be passed over until the next key event which was a meeting held on 3 June 2010 between Mr Zappia, Mr Cassaniti and Mr Di Bello.

35 The date of 3 June 2010 is, as it happens, a significant one in this case. It is the day before a series of payments were made into Shingley’s bank account. These started on 4 June 2010 and were as follows:

4 June 2010 | $375,000 |

7 June 2010 | $500,000 |

8 June 2010 | $425,000 |

9 June 2010 | $400,000 |

10 June 2010 | $300,000 |

36 These totalled, in all, $2 million. According to Shingley’s bank statements, these sums were each received from an account with Westpac in the name of ‘A and S Business SOL’. On 30 June 2010, these funds were transferred to Mrs Zappia’s personal account. It is those funds which are the subject of the present dispute.

37 It is Mrs Zappia’s contention that the funds in her account were the proceeds of the equity investment made by the Zeitounis through Jianxi. It is its nature as an alleged equity investment which grounds her contention that it was not assessable income. That it seemed to find its way into her own bank account was to be explained by her ability to get a superior interest rate to Shingley, for whom she was to be seen as minding it. I return to this aspect of the matter later in these reasons in more detail.

38 With that in mind, it is useful then to return to the meeting held on 3 June 2010. Mr Di Bello’s note is quite fulsome. Some minor amendments were made to the draft deed. The note contains this statement:

‘– apparently Len agreed to release another $2 million to Shingley once Agmt signed.’

39 The word ‘another’ suggests that there may have been an earlier advance. Perhaps this was a reference to the $3 million mentioned above. Perhaps it is not. Who knows? The taxpayer made no attempt to explain minor details such as this. Later in the file note it is recorded that Mr Zappia had signed the agreement:

‘ John signed Agt x 2 for Shingley’.

40 It then goes on to say:

‘Len in W.A. – will sign when returns.’

41 Obviously, one available view is that the $2 million which begins to arrive in Shingley’s account the next day is the $2 million referred to (Mr Zappia having signed the agreement). A copy of the version signed by Mr Zappia was in evidence.

42 By 7 June 2010, however, it is clear that ‘Len’ Zeitouni had not signed the agreement. As much is clear because an email sent that day by Mr Di Bello to the accountants asks who is going to sign the agreement on behalf of Jianxi.

43 A meeting then took place on 9 June 2010 between Mr Di Bello, two of the Zeitouni brothers and Mr Khalil. Of course, by the time that day came to its end, an amount of $1.7 million had already been paid into Shingley’s NAB account. The circumstances of the meeting therefore include the apparent fact that by the time it was held, no agreement had been executed by Jianxi but, notwithstanding that, a large amount had already been advanced. Despite that, this sum of $1.7 million was very different to the $2 million which Mr Zeitouni might have already advanced.

44 Surprisingly, neither of these notable matters is mentioned in Mr Di Bello’s file note of 9 June 2010. From the file note, it appears that Mr Di Bello gave advice about the transaction. Importantly for present purposes, Mr Di Bello advised the Zeitounis that the security offered by Mr Zappia was inadequate. The note records:

‘SECURITY - not adequate

- only 2nd unreg’d mtges on Airlie Beach + service station – both encumbered

- no personal guarantee from J/Z – wouldn’t give

- used all $12-5M + JB didn’t finish bldg. eg, couldn’t get refinances [sic], unlikely pty would sell enough to cover its 1st mtge Capital Finance + Len/Jianxi money’

45 Despite this it appears that the Zeitounis wished to proceed. The note records:

‘- still wants to proceed’

46 The discussion then moved to the question of the execution of the agreement. This is consistent with the fact that the agreement had not yet been executed by Jianxi (although Mr Zappia had already signed it). The note says:

‘- I asked what auth LZ had to sign Agmt – w/h – none – rang Gino – said “will sort out”

- I didn’t ask LZ to sign – till resolve [sic] who is authorised to sign’

47 It seems somewhat surprising, given these discussions on 9 June 2010, that Mr Zeitouni had already advanced $1.7 million to Shingley by 9 June 2010 (particularly, when it was said that he had already advanced $2 million, or at least some other substantial amount if I cannot surmise from the limited evidence before me that the previous amount was $2 million).

48 At this point, Mr Di Bello’s file takes an interesting turn. The last bill contained on the file was issued the following day, 10 June 2010. Its narrative form includes an entry for the meeting held on 9 June 2010 which appears to have taken half an hour. Unexceptionally for this kind of arrangement, the bill was sent to Shingley.

49 Apart from chasing Shingley through Mr Zappia to pay the bill, nothing further is disclosed by the file. There is no trace of any further advice to Jianxi on how the agreement might be executed nor any sign of the receipt of a signed version of the agreement. Although the draft signed by Mr Zappia called for the giving of various forms of security, there is no indication that any of this security was ever sought by the Zeitounis, or given by Shingley.

50 Further funds were deposited into Shingley’s NAB account on 10 June 2010 bringing the total advanced over that week to $2 million. As I have already noted, this is the same sum as Leonard Zeitouni is said to have agreed to advance on 3 June 2010 once the agreement was signed.

51 Consistently with that view, Mr Zappia says that it was his understanding that the deposited funds were monies from Jianxi made available under the agreement he had signed on 3 June 2010.

52 If matters rested there, Mr Zappia would have two difficulties. The first is that the funds were advanced without the agreement having been executed by the financier and without that financier having received any of the securities contemplated by it. The second difficulty is that the advances to Shingley were not made by Jainxi but instead, according to Shingley’s bank statements, by ‘A & S Business SOL’ from an account with Westpac.

53 The ATO consulted the Australian Transaction Report and Analysis Centre about these deposits, as a result of which records were produced which showed that:

the Westpac account was held at Westpac’s George St branch in Sydney

the account holder was A & S Business Solutions Pty Ltd which had an address in Pyrmont; and

each of the deposits by A & S Business Solutions Pty Ltd into Shingley’s NAB account was preceded by a cash deposit at the George St Branch.

54 The ultimate source of this large quantity of cash is therefore unknown. To those two difficulties there may be some available retorts. For example, the file note suggested that Mr Zeitouni might indeed advance the $2 million once Mr Zappia signed the agreement and the $2 million, therefore, may be able to be seen in that light. Further, it does not follow that just because Jianxi was the financier that the funds had literally to come from it. Where those funds came from was really not Mr Zappia’s problem and a financier might well arrange the payment of the funds from any source it deemed appropriate.

55 Those answers, if this was all there were, might leave the matter somewhat equivocal. However, what happened after 10 June 2010 makes things more complex.

56 The first complexity arises from the execution on 25 June 2010 of a record of a resolution of the Trust, by which the Trust appeared to resolve to distribute the net income of the Trust to Mrs Zappia. The second is the transfer of $2 million by Shingley as trustee to Mrs Zappia, a few days later on 30 June 2010.

57 Issues of some difficulty arise from both. As to the distribution from the Trust, the following are relevant matters. First, the relevant portion of the memorandum of the resolution is as follows:

MONIES RECEIVED: | It was resolved that the monies received from Jianxi Trading & Commerce Inc during the 2010 year be invested with Rose Zappia on the basis that the interest rate received was greater than the rate Shingley Projects Pty Ltd ATF can received [sic]. |

ALLOCATION OF NET INCOME: | It was resolved that the net income of the trust be paid to Rose Zappia. |

58 These two statements may be contradictory in that they tend to undermine the evidence which was given by Mr Zappia. An ‘investment’ with Mrs Zappia is consistent with the evidence that Mr Zappia has sought to give in his evidence. But a distribution of the net income of the Trust to her is not. The trust deed for the Trust was in evidence. Clause 5 required the trustee to determine the income of the Trust for each ‘Accounting Period’ which was defined as a financial year in cl 1.1. The trustee was not limited by the terms of the deed to appointing as income under the Trust only income for income tax purposes. For example, cl 5(b)(i) permitted capital profits to be included as income under the trust fund.

59 There may be some subtle questions as to how the distribution of income for trust purposes to a presently entitled beneficiary might be taxed for income tax purposes (see, eg, Commissioner of Taxation v Bamford [2010] HCA 10; 240 CLR 481). However, this thicket can be avoided by the observation that Mrs Zappia was not a beneficiary of the trust who was presently entitled or indeed a beneficiary at all. Cl 5 permitted distribution of the income of the Trust to unit holders, but this Mrs Zappia was not. What this resolution did is, therefore, less clear and potentially contrary to the express terms of the Trust deed.

60 That leaves the other part of the resolution intact and that is the resolution to invest the Jianxi funds with Mrs Zappia. This may have been authorised in principle under cl 6.1(b) of the deed which permitted the trustee to invest funds of the Trust. This is consistent with Mr Zappia’s explanation. However, I am not inclined to put much weight on this matter as Mr Zappia’s evidence was that his accountant had been responsible for this resolution. Where precisely this document fitted into Mr Zappia’s case beyond the proposition that it did not really matter was never satisfactorily explained.

61 The second complexity is that the deposits which had been made into Shingley’s NAB account between 4-10 June 2010 were transferred from that account to Mrs Zappia’s account in a single electronic transfer on 30 June 2010. Mr Zappia’s explanation for this in his affidavit was contained at paragraph 34:

‘I wanted Shingley Projects Pty Limited to receive a greater return on the funds it had received from Jianxi Trade and Commerce Inc. than it could obtain by investing the funds directly while awaiting approval for a property development. In addition, I did not want Capital Finance to know about the receipt of funds on account that they would demand repayment of Shingley’s indebtedness to them.’

62 There are a number of difficulties with this as an explanation. As I have endeavoured to show above, Mr Zappia’s original motive for obtaining the facility was so that he could refinance the Capital Finance facility. However, as the transaction with the Zeitounis was progressed it began to take on the shape of project finance. On neither view of the transaction, however, was it ever in contemplation that Shingley would seek to invest the funds which were to be provided to it in cash investments. Given the rate then payable on cash deposits with banks and the 50% return the Zeitounis were hoping to make if the apartments proceeded, what Mr Zappia suggests makes little sense.

63 Also difficult to accept is the suggestion that Mr Zappia put the money in Mrs Zappia’s name because that was the best rate he could find. Mr Zappia was taxed about this under cross-examination. Regardless of his denials, I do not accept either that the ‘best’ rate could be obtained only through personal rather than corporate bank accounts or that this can really have been Mr Zappia’s motive.

64 Mr Zappia’s parallel suggestion that he put the money in Mrs Zappia’s account so that Capital Finance would not see it is also implausible. There are two difficulties with this as a credible explanation:

his evidence at paragraphs 12-14 of his affidavit was that the point of the Jianxi arrangement was to refinance the Capital Finance transaction, a proposition entirely inconsistent with hiding the proceeds from Capital Finance; and

there was no evidence that Capital Finance had any access to Shingley’s NAB account so as to become aware of the existence of the $2 million in any event.

65 Accordingly, I do not accept Mr Zappia’s evidence about this. Undoubtedly, the $2 million was transferred into Mrs Zappia’s account on 30 June 2010 but I do not accept that it was for the reasons Mr Zappia gave during the hearing or in his affidavit. I do not doubt that Mr Zappia had his reasons for the transfer but it has not been proven to me what those reasons were, although they seem to have been compelling. In that regard, it was submitted to me that Mr Zappia was a witness of truth. I do not accept this submission. This was not because by his demeanour he seemed to be lying, but rather simply because I did not believe the version of events he proffered.

66 There then followed transactions on Mrs Zappia’s account which only increase the air of mystery surrounding the case. On 13 September 2010, Mr Zappia asked Mrs Zappia to transfer $210,000 to Capital Finance on behalf of the Trust. This would appear to be an example of the funds not being used to refinance the Capital Finance facility or, on the other hand, as project finance. Indeed, it seems to be an example of one facility being used to service another. Mr Zappia gave no evidence of such an arrangement. It appears that Capital Finance was also paid $230,000 on 23 June 2010 and $200,000 on 2 December 2010 but this was not from the Funds being held by Mrs Zappia so far as I can see. What is clear from the Capital Finance records is that its facility was partly repaid on 29 June 2012 by a single payment of $2,161,399.90. This can have had nothing to do with the funds allegedly advanced by the Zeitounis. In short, none of this makes any sense.

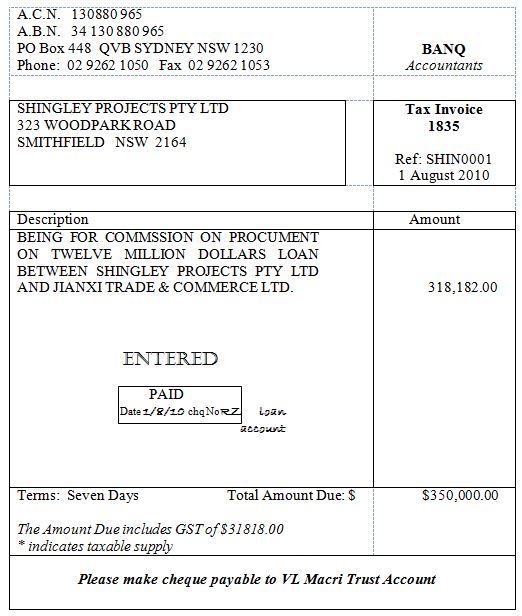

67 On 21 September 2010, Mr Zappia requested his wife to pay $350,000 to VL Macri Lawyers as an introduction fee for Banq Accountants. I note in passing that the draft agreement between Jianxi and Shingley rather suggested that the amount paid to Banq Accountants as a commission would be the lesser figure of $310,000. This notwithstanding, Banq Accountants had indeed issued a tax invoice for this sum. This invoice was issued on the letterhead of Banq Accountants and was dated 1 August 2010. It appeared in the form below:

68 There are some unusual features of this invoice. First, it bears a ‘paid’ stamp with the date 1 August 2010, six weeks before Mrs Zappia’s apparent payment. Secondly, pursuant to the agreement under which Mr Zappia says he was acting, Banq Accountants was to take its fee in the form of an apartment and yet this invoice calls for a cash payment. Thirdly, the paid stamp bears an annotation ‘RZ loan account’ which might suggest that the invoice was paid by debiting a loan account held by Banq Accountants for Shingley.

69 On the other hand, it is possible to read the description contained in the invoice of the transaction to which it related as corroborating Mr Zappia’s contention: ‘Being for commission for procurement on (sic) twelve million dollars loan between Shingley Projects Pty Ltd and Jianxi Trade & Commerce Ltd’. Added to that may be the idea that the fact that the commission was payable and paid tends to suggest that the transaction proceeded.

70 There are, so it seems to me, two difficulties with this view. The first is that Mr Zappia has led no evidence that the $12 million facility did proceed. The only material relating to that is the $2 million the subject of these proceedings. There has been no explanation forthcoming from Mr Zappia as to what happened to the other $10 million. Nor does Mr Zappia explain what happened to the project itself. This is a large gap in the evidence.

71 The second difficulty is, as I have already mentioned, that the payment to Banq Accountants was contemplated by the agreement to take the form of an apartment in the completed development and not a cash payment.

72 There is no evidence as to the terms of Banq Accountants’ retainer with Shingley. Hence, I do not know under what circumstances Banq Accountants’ commission might have become payable. It is possible that it became payable merely because of the introduction to the financier (as is not uncommon) even if the transaction did not proceed.

73 As a result of these matters, I do not think that the payment of $350,000 helps Mr Zappia very much, at least not without a good deal more explanation than Mr Zappia has thus far proffered. As evidence of the agreement being effected it is thin.

74 On 8 December 2010, Mr Zappia requested his wife to transfer the balance of her account to an account held jointly in both their names. This appears to have involved the sum of $1,227,221.95. The bank statements show that this occurred the day before Mr Zappia allegedly made the request. In the scheme of the case, this is a minor anomaly. In his affidavit, Mr Zappia did not explain why he made the request. Mrs Zappia’s account had been an NAB iSaver account and this request, it will be recalled, was apparently made because Mr Zappia wished to be able to take advantage of the higher interest rate which could be earned on that kind of account. The joint account to which the monies were now transferred was not an ‘iSaver’ account but instead an account called ‘NAB Gold Banking - Choice’. It is not clear to me what rate this attracted. It is not clear to me why this happened.

75 Both Mr and Mrs Zappia were cross-examined about the joint account but the evidence did not throw any light on why this transfer occurred. Mrs Zappia really knew nothing about it as this exchange during the hearing shows:

‘And from that bank account – well, can we assume that you were a cosignatory to that bank account? --- Yes. I was.

And are you able to point to any documents before the court evidencing any link between the funds in that joint bank account of you and your husband and the actual trust, Shingley Trust? --- I have not seen any. No.

Are you able to point to any documents before the court indicating that the moneys that joint bank account of you and your husband were held to the benefit of Shingley Trust? --- I have not seen anything. No.’

76 And Mr Zappia seemed to be in no better position as this exchange during the hearing shows:

‘Mr Zappia, you’ve given evidence in your affidavit that you received – well, before we get there, actually, we know that the money flowed from your wife’s personal bank account to a joint account of you and your wife. Can you point to any document before the tribunal – before the court, even – that links the amount held in the joint account to the trust?--- No.

Can you point to any document explaining any arrangement vis-à-vis that joint account and the trust?--- No. That’s a decision I made.’

77 As I will shortly explain, funds then flowed out of the joint account via other accounts to certain persons, some of whom were located outside Australia. Mr Zappia’s evidence was that this was in repayment of the facility advanced by the Zeitounis. For present purposes, the point to be made is that even if I were to accept that matter, it leaves unexplained why a detour through the joint account was necessary.

78 The funds in the joint account were then disbursed in the following fashion. First, on 19 January 2011, Mr Zappia caused $100,000 to be transferred to ‘Villa Villa PL’. Mr Zappia’s evidence was that this was a reference to the development’s architects, Mr Eduardo Villa and Mrs Maria Villa. Mr Zappia’s evidence in chief in his affidavit was that the payment was to an entity called ‘Villa Villa PL’, a view supported by the bank statements. No party made any point about this minor discrepancy.

79 Mr Zappia gave evidence in his affidavit that on 24 March 2011 he transferred $1,000,000 from the joint account to an entity called Chesy Nominees Pty Ltd. The bank statements do, in fact, reflect this. Mr Zappia is the sole director of Chesy Nominees Pty Ltd. Mr Zappia explained the transfer very briefly as being on the basis that he had decided that the funds for Shingley from Jianxi would now be held by Chesy instead.

80 No explanation was proffered by Mr Zappia in his affidavit or in his oral testimony as to why this was necessary or even what it achieved. I do not know why it occurred.

81 Mr Zappia then says that on 25 March 2011 he transferred $176,000 to an entity called Isico Pty Ltd. In his affidavit he did not explain what this payment was or why it was made. Under cross-examination, Mr Zappia said this about Isico:

‘There’s an entity that a payment was made to ISICO, I-S-I-C-O. That was a payment out of the joint account? --- Yes.

Can you point to any document before the court that would shed any light on what that entity is or how it relates to the agreement or the project? --- No.

Another payment was made to an entity called Villa Villa out of the joint account? --- Yes.

Can you point to any document today that shed any light on the relationship between that entity and the agreement in question? --- There should be documents in it, because they were part of the development expenses, which was the architect, and I think there was something here for ISICO as well. I can’t remember now.’

82 Under re-examination he gave evidence that ISICO was not connected with the Whitsundays project. Given Mr Zappia’s evidence, this payment is obscure.

83 Mr Zappia then says that in around May 2011 he received a letter of direction for Jianxi directing him to repay $1,200,000. I will set the letter out shortly but it may be immediately observed that it is very difficult to accommodate the concept of an equity investment with the right to demand immediate repayment of the money invested. Of course, this will depend on the terms upon which the investment was made. On Mr Zappia’s case, the relevant agreement was the one which he himself signed. But that agreement contains no provision allowing Jianxi to ask for its money back. Also, the amount originally advanced was $2 million and the amount demanded in the letter seems to be $800,000 short. Maybe this can be partially explained by an amount of $400,100 which, it was said during the hearing by counsel for Mrs Zappia, was allegedly paid on 24 August 2011 to one Malcolm B Stead. However, the bank statements for Chesy for the month of August 2011 were not in evidence, and in any event, that still leaves approximately $400,000 unaccounted.

84 Assuming everything else in Mr Zappia’s favour, this direction contradicts the case he (or his wife) seeks to advance.

85 However, that is only the beginning of the difficulties which this ‘direction’ generates. It is useful to set it out in full:

‘ JIANXI TRADE &

COMMERCE INC.

3908 Two Exchange Square

8 Connaught Place Central

Hong Kong

Shingley Projects Pty Ltd

327 Woodpark Rd

Smithfield NSW 2164

To the Directors:

As we are considering our position going forward in relation to the moneys invested in Shingley Projects Pty Ltd, we would like you to refund AU$1,200,000.00 (one million and two hundred thousand dollars) of the money you still hold in trust.

Please make preparations to transfer the money, all relevant banking details will be supplied to you soon.

The stages of transfer are to be as follows:

Week 1: $396,350.00 AUD

Week 2: $400,000.00 AUD

Week 3: $403,650.00 AUD

TOTAL: $1,200,000.00 AUD

Yours sincerely,

‘Signature’

LEONARD ZEITOUNI’

86 There are five problems. First, the letter refers to the $1.2 million being held ‘in trust’. But Mr Zappia’s version of events is that the money was advanced under the agreement he signed. On no view, did that agreement appoint Shingly as trustee of a bare trust which Jianxi might be entitled to revoke at will. Perhaps if the development did not proceed it might be possible for Jianxi to call for the funds. But by 2011 this certainly could not be said to be the case.

87 Secondly, as will be seen, the sums actually disbursed did not match the amounts set out in this letter.

88 Thirdly, the letter is undated.

89 Fourthly, there is no evidence of Mr Zappia’s complaining about this demand which must have been very negative in its impact on his development.

90 Fifthly, there is reason to believe that the signature on the letter may not be Mr Zeitouni’s (I discuss this further below).

91 How much was transferred and where was it transferred to? Mr Zappia says that on 24 May 2011 he caused to be transferred $396,350 from the Chesy account with the Bank of Queensland. The bank statement shows that this was a telegraphic transfer to Mexico to one Jose Eduardo Salado. The bank records show that the sum involved was $391,330.61 although a US dollar sum was transferred. Mr Zappia says that he received the bank account details for this from Mr Khalil at Banq Accountants. Mr Zappia’s evidence as to the $396,350 matches the first entry in the letter of demand. What happened in the bank account does not.

92 Mr Zappia says that on 22 June 2011 he caused a further transfer of $393,913.76 from the Chesy account. The transfer confirmation was in evidence and shows that this amount was transferred to an account in the name of Juan Diego Ramirez Aguilera with a New York branch of the Bank of America. It may be observed that this does not match any of the figures in the letter.

93 There is no evidence that Mr Zappia made a third payment as contemplated by the letter. The payments thus do not match the letter even approximately. The letter does not match the original facility. The transaction described in the letter does not resemble the one Mr Zappia advances by reference to the agreement which he signed. Nor is there any coherent explanation of why Mr Zappia would return an equity investment whose purpose according to him was to get another financier, namely Capital Finance, ‘off his back’.

94 It was submitted by the Commissioner that I should conclude that this letter had been concocted. It was said that the signature on it did not match Mr Zeitouni’s signature as recorded on an immigration departure card and passport application. I consider there may be considerable force in this. However, I do not need to express a concluded view on it. Even if the letter were authentic it fails to match, even roughly, the events which occurred in the real world.

3. The Taxpayer’s Contentions

95 Mrs Zappia advances two propositions. First, the money which ended up in her account was the proceeds of an equity investment received by Shingley under the agreement of 3 June 2010 (I take this date to be the date of the agreement even though, as I have already mentioned, only Mr Zappia executed the agreement on that date). Secondly, Mrs Zappia says that, whatever else all of this means, she was holding the funds in her account on trust for Shingley as trustee for the Trust and therefore that the funds were not taxable in her hands.

96 It is for the taxpayer affirmatively to prove what her taxable income should have been in the 2010 and 2011 years and that the Commissioner’s assessments are excessive: TAA, s 14ZZO(b). This entails that the ‘onus rests upon the taxpayer of establishing the facts upon which he relies and if it is necessary for him to establish a particular fact in order to displace the assessment he must satisfy the Court with respect to that fact’: Danmark Pty Ltd v Federal Commissioner of Taxation (1944) 2 AITR 517; 7 ATD 333 at 337 per Latham CJ.

97 Thus, to make good the taxpayer’s first contention it will be necessary for her to prove on the balance of probabilities that the $2 million advanced to Shingley between 4 June 2010 and 10 June 2010 was the proceeds of an equity investment by Mr Zeitouni under an agreement dated 3 June 2010.

98 I do not think that the taxpayer comes close to proving this. I have set out above the available evidence about this advance of $2 million and flagged, in the course of doing so, some of the potential difficulties I saw with this evidence.

99 In light of those observations, I do not accept Mr Zappia’s account for the following reasons.

100 Firstly, Mr Zappia’s explanation of the circumstances in which the alleged facility with Mr Zeitouni came into existence makes no sense. The purpose of the facility was, according to Mr Zappia, to refinance the Capital Finance facility in order to remove it from the picture. But there is no evidence that the funds allegedly raised from Mr Zeitouni were ever so used. Instead, the $2 million which was obtained went from Shingley to Mrs Zappia and then to Mr and Mrs Zappia. Although some of it did apparently go to Capital Finance, those amounts did not constitute a refinancing. After the transfer to Mrs Zappia, some of the funds went to Mr Zappia’s company, Chesy, some of it to the architect, and some of it to Banq Accountants. The money in Chesy, in turn, was telegraphically transferred to Juan Diego Ramirez Aguilera’s account in New York with the Bank of America and Jose Eduardo Salado’s account with a bank in Mezzanine in Mexico. There was also an alleged transfer to Malcolm B Stead, whom it was suggested was a business associate of Mr Zappia’s. It was not suggested, nor could it be, that any of these people or entities had anything to do with Capital Finance. This evidence suggests that the purpose for which Mr Zappia alleges he sought funding from Mr Zeitouni cannot be correct. It is possible, I do not doubt, that the circumstances with Capital Finance might have changed; that, for example, its demands that Mr Zappia repay its debt ceased for some reason or that it was otherwise satisfied. But there is no evidence to suggest any of this away from the realm of conjecture. Any doubt that the purpose of the alleged Zeitouni facility could not have been to refinance the Capital Finance Facility is dispelled when one brings to account that the former was drawn down only as to $2 million whereas the latter was in excess of $8 million.

101 Secondly, it has not been proven that the investment agreement executed by Mr Zappia was executed by Mr Zeitouni on behalf of Jianxi. I accept that Mr Di Bello’s file suggests that, as at 9 June 2010, Mr Zeitouni was keen to proceed, but the file is more eloquent by reference to what is not in it. What is not in it is any documentation relating to any attempt to obtain the security contemplated by the agreement or to work out how the agreement was to be executed on behalf of Jianxi. And this is notwithstanding that the explicit question of the agreement’s execution had been recognised by Mr Di Bello as an issue requiring resolution. Instead, what appears to have happened is that the transaction stopped dead in its tracks. The absence of a copy of the agreement signed by Mr Zeitouni suggests, in this circumstance, not that it has been lost or is otherwise not available, but that it does not exist.

102 Thirdly, I am not satisfied that the $2 million which was advanced to Shingley between 4 June 2010 and 10 June 2010 was advanced by Mr Zeitouni or Jianxi. This is because the source of those funds appears to have been cash deposits in the name of ‘A and S Business SOL’ at the St George branch of Westpac and not in the name of Mr Zeitouni or Jianxi. It is true that Mr Di Bello’s file note of 3 June 2010 refers to Mr Zeitouni having agreed to advance $2 million once the agreement was signed, that Mr Zappia did sign the agreement and that $2 million did turn up in Shingley’s account between 4 June 2010 and 10 June 2010. But Mr Di Bello’s note says that this would be ‘another $2 million’ and there is no evidence to which I was taken of any such earlier advance. I accept, as I have indicated above, that it is possible that the $2 million received by Shingley really did ultimately derive from Mr Zeitouni via the cash deposits at Westpac who, on that view, must have had his own reasons for garnering the loan funds in this curious way and who was willing to advance substantial sums of money without security. Many things are possible. However, I am not satisfied on the balance of possibilities that this is what occurred.

103 Fourthly, what Mr Zappia did with the $2 million simply makes no sense. I have already explained why it makes no sense in relation to the supposed refinancing of the Capital Finance facility. It also makes no sense in relation to the evidence which suggests that Mr Zeitouni was making an equity investment in the development. One might expect that if, as the version of the agreement signed by Mr Zappia rather suggests, the equity investment was to be used as project finance then some project works might have taken place. Instead, the $2 million seems to have ended up in Mrs Zappia’s account to earn a better rate of interest (on Mr Zappia’s account). It is difficult to see that as having much to do with the development of the project at Airlie Beach. Further, regardless of what one thinks of the validity of the trustee’s resolution of 25 June 2010, it does not seem to have anything to do with building a residential complex.

104 For those reasons, I do not accept Mr Zappia’s evidence about this. I am not satisfied that the $2 million that was advanced by Jianxi was part of an equity investment in Shingley.

105 There remains then the taxpayer’s second contention that Mrs Zappia held the funds advanced to her on trust for Shingley. Two trusts seemed to be in play on the Applicant’s submissions: a bare trust under which Mrs Zappia was to be seen as a mere nominee for Shingley and a trust of a more developed kind in favour of Shingley, with Mrs Zappia interposed as trustee for the unit trust. At earlier times in the litigation, other trusts, and perhaps even at one time a loan agreement, were advanced by the taxpayer but they were not pursued by the end of the case. Indeed, under cross-examination Mr Zappia conceded that he ‘didn’t lend the money’ to his wife.

106 One starts, I think, with the proposition that $2 million is a lot of money, and that $2 million was received by Shingley. This much at least is clear. Also clear is that only limited books and records of the Trust have been put before the Court. One record is the trust resolution I have referred to above. Another is the Trust’s 2010 accounts which singularly fail to refer to this $2 million at all, an omission which contradicts the argument that the Trust held the beneficial interest in the funds under a bare trust arrangement. In short, there is therefore no evidence in the documents before the Court to support the idea that the $2 million held by Mrs Zappia was a trust asset. Indeed the resolution suggests to the contrary that the $2 million was not held by Mrs Zappia other than beneficially.

107 It may readily be accepted that it is possible that the resolution is invalid and that Mrs Zappia’s holding of the $2 million is impressed with a resulting trust in favour of the Trust. But so much of the picture is missing that I do not think it would be safe, on the balance of probabilities, to go down that path. Mr Zappia could not explain the resolution and put responsibility for it in the hands of his accountant. The accountant was not called to give evidence.

108 The position I arrive at, therefore, is that on the sparse materials available, I can see only a preliminary sketch, perhaps a suggestion, of an argument that Mrs Zappia held the funds as a bare trustee (or for that matter, that it was a loan). I could infer from the material which is available that such a trust existed but I do not think that such an inference is the only available one. For example, the resolution is certainly capable of supporting the inference that what was being sought to be done was to put income in Mrs Zappia’s hands; even if the resolution was ineffective to do so. Further, given the unexplained nature of the $2 million in the first place, another view could be that a significantly different explanation of what took place is available; that is to say, what is before the Court are the remnants of some other transaction which Mr Zappia is not explaining.

109 I do not propose to draw the inference that Mrs Zappia received the $2 million as a bare trustee or as any sort of trustee or, even if it is open, that it was a loan. It follows that the taxpayer fails to prove the alleged trust.

Other

110 There were two minor issues not developed in argument. These were:

(1) whether the Commissioner was entitled to issue default assessments against Mrs Zappia in circumstances where he was of the opinion that there had been fraud or evasion; and

(2) whether Mrs Zappia is out of time in relation to the interest amounts of $37,257 to object to the notice of amended assessment for the income tax year ended 30 June 2011 and issued to her on 5 March 2013.

111 No argument was addressed to me on either point and I disregard them.

Conclusion

112 The taxpayer’s appeal fails. The application will be dismissed with costs.

I certify that the preceding one hundred and twelve (112) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Perram. |