FEDERAL COURT OF AUSTRALIA

Popeye Holdco Pty Limited v Intermediate Capital Asia Pacific 2008 GP Limited [2017] FCA 369

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The applicants’ application for an interlocutory injunction is refused.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

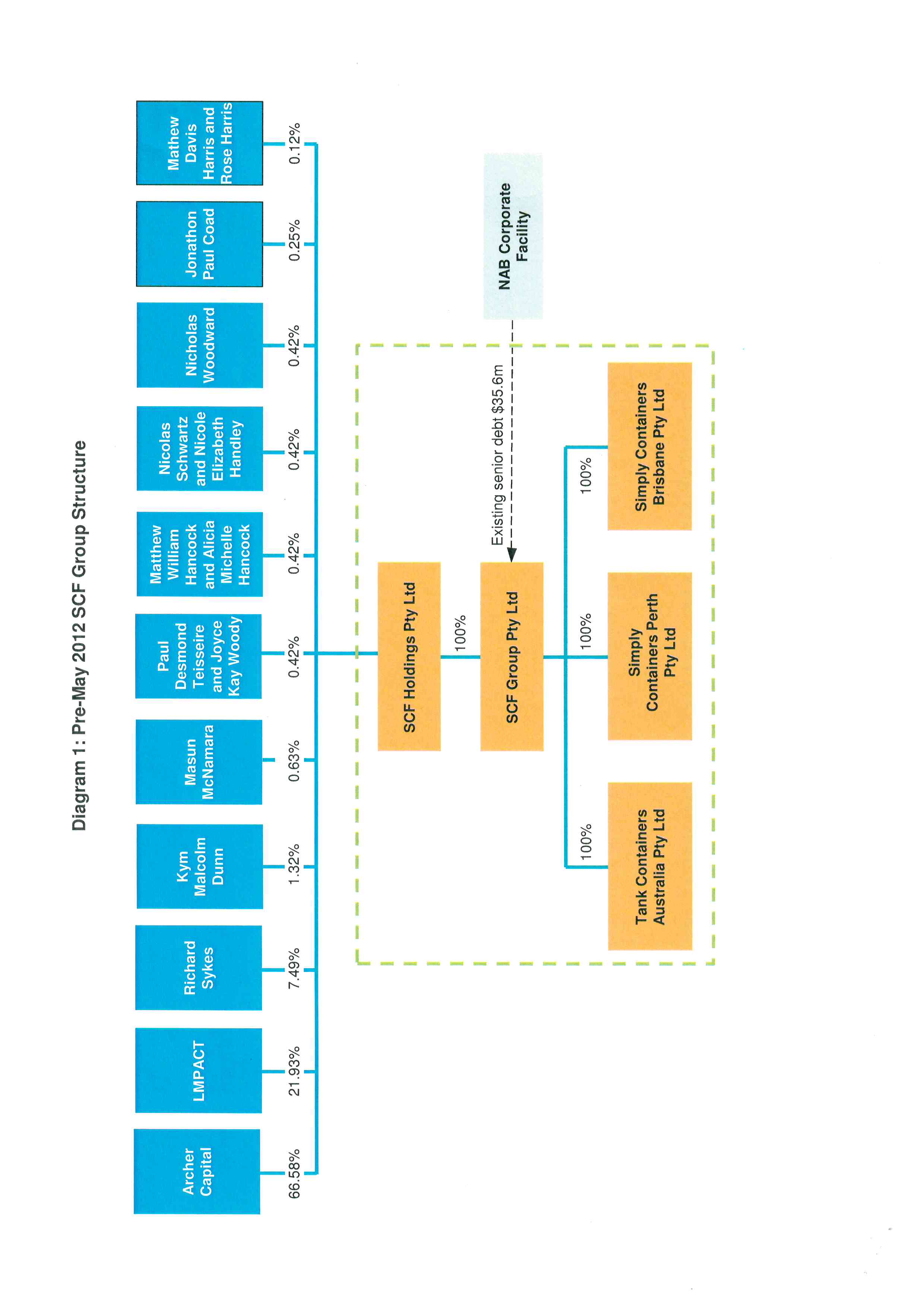

BESANKO J:

Introduction

1 The applicants in this proceeding are Popeye Holdco Pty Limited (Holdco), Popeye Bidco Pty Limited (Bidco), SCF Holdings Pty Limited (SCF Holdings) and SCF Group Pty Limited and they seek an interlocutory injunction against Intermediate Capital Asia Pacific 2008 GP Limited, Intermediate Capital Asia Pacific Fund 2008 LP, Intermediate Capital Asia Pacific Limited, Intermediate Capital Group Plc, AET Structured Finance Services Pty Limited, Intermediate Capital Australia Pty Limited, Hartland Investments Pte. Limited and Mr Ryan Shelswell. Those parties are the respondents to the proceeding. AET Structured Finance Services Pty Limited is the agent under certain agreements. It is separately represented and has taken no part in the hearing to this point. Hartland Investments Pte. Limited appears not to have been involved in the initial events which are the subject of this proceeding. The other respondents are part of or associated with the Intermediate Capital Group of Companies (ICG). There is an interim injunction in place and the applicants now seek an interlocutory injunction in the following terms:

1. Upon the applicants giving the undertaking set out in Annexure A to these orders, the respondents and each of them be restrained, whether by their servants, agents, or otherwise, until further order from taking any steps under, or purporting to invoke or exercise any rights set out in any of the written agreements, deeds or other instruments between any one or more of the respondents and any one or more of the applicants, including, without limitation:

1.1 the Share Sale/Purchase Agreement dated 25 May 2012 between Archer Capital Growth Funds Pty Limited as Custodian for Archer Capital GF1A Pty Limited as Trustee for the Archer Capital GF Trust 1A, Archer Capital Growth Funds Pty Limited as Custodian for Archer Capital GF1B Pty Limited as Trustee for the Archer Capital GF Trust 1B, LMPACT Pty Limited as Trustees for the LMPAC Family Trust, Richard Sykes as Trustee for the Richard Sykes Family Trust, Richard Sykes, LMPACA Pty Limited ACN 125 011 636 as Trustee for the LMPAC1 Super Fund; Kym Malcolm Dunn, Masnun McNamara, Paul Desmond Teisseire and Joyce Kay Woody as Trustees for the Teisseire/Woody Superannuation Fund; Matthew William Hancock and Alicia Michelle Hancock, Nicholas Schwartz and Nicole Elizabeth Handley, Nicholas Woodward as Trustee for the Woodward Family Trust, Jonathan Paul Coad, Matthew Davis Harris and Rose Harris, Popeye Bidco Pty Limited ACN 158 359 285, Popeye Holdco Pty Limited ACN 158 356 471;

1.2 the Preferred Loan Notes Subscription Agreement dated 25 May 2012 between Popeye Bidco Pty Limited ACN 158 359 285, Popeye Holdco Pty Limited ACN 158 356 471, Intermediate Capital Australia Pacific Limited, Intermediate Capital Group plc, and AET Structured Finance Services Pty Limited ACN 106 424 088; and

1.3 the General Security Interest dated 25 May 2012 between Popeye Holdco Pty Limited ACN 158 356 471 and Popeye Bidco Pty Limited ACN 158 359 285, and AET Structured Finance Services Pty Limited,

but excluding the Subscription and Shareholders Deed dated 25 May 2012 between Richard Sykes, Nicholas Woodward, Kym Malcolm Dunn, Jonathan Paul Coad, Matthew William Hancock, Nicholas Schwartz, Matthew Davis Harris and Brett Carthew, Richard Sykes as Trustee for the Richard Sykes Family Trust, Nicholas Woodward as Trustee for the Woodward Family Trust, Alicia Michelle Hancock, Nicole Elizabeth Handley, Rose Harris and LMPACT Pty Limited as Trustee for the LMPAC Family Trust, Intermediate Capital Group Plc, Popeye HoldCo Pty Limited ACN 158 356 471, Intermediate Capital Group plc.

2 The relevant principles for the purposes of determining whether to grant an interlocutory injunction are not in dispute. In Ottoway Engineering Pty Ltd v Westpac Banking Corporation [2016] FCA 635 at [2], I said the following:

The test to be applied in determining whether an interlocutory injunction should be granted is well-established. The applicant must establish a prima facie case in that it must show a sufficient likelihood of success to justify, in the circumstances, the preservation of the status quo pending the trial. For convenience, I will refer to this as a prima facie case. The Court must consider the balance of convenience, including whether damages will be an adequate remedy (Australian Broadcasting Commission v O’Neill (2006) 227 CLR 57 at 68-69 [19] per Gleeson CJ and Crennan J, and at 81-84 [65]-[72] per Gummow and Hayne JJ). As the Full Court of this Court made clear in Samsung Electronics Company Ltd v Apple Inc and Another (2011) 217 FCR 238 at 261 [67], the strength of the applicant’s case is not considered in isolation from the balance of convenience. The strength of the parties’ substantive cases will often be an important consideration to be weighed in the balance.

3 In these reasons, I will use the expression, prima facie case, in the sense described in the above passage.

4 As will be seen from the interlocutory injunction sought by the applicants, the dispute relates to agreements entered into in May 2012. Four agreements are referred to in the interlocutory injunction, being a Share Sale/Purchase Agreement, a Preferred Loan Notes Subscription Agreement (PLNSA), a General Security Interest and, in the exclusion, a Subscription and Shareholders’ Deed (Shareholders’ Deed). The catalyst for the applicants’ application for an interlocutory injunction was action taken by the ICG which might lead to a substantial sum of money ($173 million or $350 million) becoming due and payable under the PLNSA. I will explain the reason that there are two different figures later in these reasons.

5 The financial transactions which took place in May 2012 are complex and involved large sums of money. It will be necessary to outline them in some detail. Before doing that, I will briefly outline the causes of action upon which the applicants rely. First, the applicants rely on the proper construction of the agreements or an estoppel to claim the ICG cannot take the action they propose to take under the PLNSA. Secondly, they claim that the ICG has been guilty of misleading and deceptive conduct under s 18 of the Australian Consumer Law in connection with the agreements. Thirdly, they allege that members of the ICG have breached directors’ duties under the general law and under the Corporations Act 2001 (Cth) in connection with the agreements. Fourthly, they allege that members of the ICG have been guilty of unconscionable conduct within ss 20 and 21 of the Australian Consumer Law in connection with the agreements. Finally, they allege that, insofar as the ICG seeks to recover the sum of approximately $350 million under the PLNSA, recovery of that sum is a penalty and is unenforceable.

The SCF Group of Companies Prior to May 2012

6 Prior to May 2012, there was a group of companies which may be described as the SCF Group. The Group conducted a business of selling and hiring out new and used shipping containers, including and in particular, hiring out container-based transportable units for mining camps. The Group had a substantial turnover and offices in most of the capital cities in Australia. It was profitable. SCF Group Pty Ltd was the company which engaged in trade with the public. Mr Richard Sykes was the founder of the business of the SCF Group and he was the Chief Executive Officer of the Group and responsible for the day-to-day operations of the Group.

7 The structure of the SCF Group prior to May 2012 is shown in Diagram 1 of Annexure A to these reasons.

8 Mr Sykes, who swore three affidavits in support of this application, set out his own history in business and the history of the SCF Group in his second affidavit. For the purposes of this application, it is not necessary for me to set out those histories. Mr Sykes describes the circumstances in which the private equity firm, Archer Capital Growth Funds Pty Limited (Archer Capital) became involved in the SCF Group of Companies in 2007 and, in particular, the establishment of SCF Holdings. Again, for the purposes of the present application, it is not necessary for me to set out those circumstances.

9 Archer Capital became the majority shareholder in the SCF Group and the other shareholders were Mr Sykes, another founding member, and other members of the SCF Group’s management team.

10 In 2010, Archer Capital was looking to sell its shares in the SCF Group. The potential purchasers included the ICG. Mr Sykes describes the advisers who were engaged by the SCF Group for the purposes of the transaction, but again, it is not necessary for me to set out the details. Mr Sykes states that Allen & Overy were engaged to act for the ICG and he contends that Allen & Overy also acted for Holdco and Bidco after the incorporation of those companies. According to Mr Sykes, a Mr John Levy advised him personally in relation to some aspects of the sale.

The Negotiations in early 2012 and the Agreements entered into in May 2012

11 On 30 March 2012, Intermediate Capital Asia Pacific Limited, on behalf of Intermediate Capital Group Plc and its funds, made an indicative non-binding offer to acquire 100% of the shares in SCF Holdings. In the offer, the ICG described the group in the following terms:

ICG is one of the largest independent mezzanine and minority equity investors in the world, and also the largest non-bank funder of senior debt in Europe, with over €12 Billion assets under management. ICG was founded in 1989, is a FTSE250 listed company, and is regulated by the FSA. We have invested over €10 Billion in 340 mezzanine and equity transactions and have exited 249 deals. We currently manage over 200 senior debt positions.

ICG has had a permanent presence in Asia Pacific since 2001 and manages US$1.5 Billion in funds dedicated to the region. We are currently investing our second dedicated Asia Pacific fund, which is a lender to, and investor in, several businesses with significant Australian operations. Our most recent deal in Australia was the minority equity and mezzanine investment in Ventura Motors in partnership with the owner-managers of Ventura, in order to fund their acquisition of Grenda Transit Management, which competed in February 2012.

12 Relevant aspects of the offer included the following:

Intermediate Capital Asia Pacific Limited (“ICAP”) on behalf of Intermediate Capital Group plc (“ICG”) and its funds are pleased to offer to acquire 100% of the shares (the “Transaction”) of SCF Holdings Pty Limited (“SCF”), a portfolio company of funds managed and advised by Archer Capital (“Archer”) on terms described in this letter (the “Offer”).

…

Partnership Bid with SCF Management Team

As you are aware, we are not a control buyout sponsor and so our bid structure will deliver control of the business and over 50% of equity to the SCF management team.

Under our bid structure, the day to day management of the business will be in the hands of the SCF management team and our interaction will be at the board level. Before finalising our bid we will agree a business plan with the SCF management team which will be fully funded from the outset. ICAP has also made allowance for a management incentive package to reward the team for driving the business forward.

However, as agreed with you, we make this Offer prior to detailed discussion of the bid structure with the SCF management team and continuing shareholders. If the Vendors conclude that our Offer is attractive relative to other options for the business, we would seek to promptly meet with SCF management and minority shareholders to discuss the Offer and the bid structure under which ICAP would partner with them going forward in order to ensure we have their full support.

13 The Enterprise Value under the offer was said to be A$131 million.

14 Mr Sykes said that he understood the offer to be “essentially like-for-like with the investment structure that had been employed by Archer Capital, save that the ‘SCF management team’ would have control of over 50% of the voting equity”. He said that if that had not been the case, then he would not have been interested in continuing negotiations.

15 Mr Sykes states that he met Mr Shelswell (the eighth respondent) for the first time between 30 March 2012 and 8 April 2012. He outlines the negotiations that took place between 30 March 2012 and 4 May 2012. It is not necessary for me to set out the details. Mr Sykes states that on 4 May 2012, it first came to his attention that it might be preferable for all parties if the ICG was to undertake any purchase of the SCF Group by way of debt rather than equity. He received a copy of an email that had been sent by Mr Shelswell to Mr Nicholas Woodward, who was (and is) another of the management shareholders. The email was in the following terms:

Per our call just now - if I have understood the Deloitte’s advice they think we could get an extra c$9m tax deduction per year by making the preferred equity into “debt for tax purposes”.

This is something we have seen before and I guess our approach in general is, if it doesn’t change the commercial deal, then getting a better tax position is a win-win.

What it will do is help our investment return modelling and obviously help us get our heads around where we need to be on value to win the sale process.

Have a think about it and then let’s chat when you have some time

16 A draft report from Deloitte which considered the differences between the ICG “Junior Equity” being tax debt or tax equity was attached to the email. The draft report set out the assumptions made for the purposes of its preparation as follows:

• A new Australian tax resident holding company (HoldCo) and acquisition company (BidCo) will be incorporated to undertake the acquisition

• The enterprise value of the shares in SCF is $141m

• SCF has existing senior debt of $35m (which may increase due to any pre-completion dividends paid, but in any event will be repaid in full on acquisition)

• The acquisition (and estimated transaction costs of $6.4m) will be funded via:

1) New acquisition senior debt of $60m

2) Management equity in the form of ordinary shares of $6.6m (which will be issued by HoldCo in satisfaction of existing shares held in SCF)

3) ICG equity in the form of ordinary and non-voting shares totalling $17.1m

4) ICG ‘Junior Capital’ of $63.7m.

• SCF is unlikley [sic] to have franking credits at the time of acquisition (due to pre-completion dividends)

• SCF is subject to the Taxation of Financial Arrangement (TOFA) provisions

The draft report set out what it called the indicative terms of the ICG Junior Capital as follows:

• The indicative terms of the ICG Junior Capital are as follows (the specific terms of which are subject to agreement by the parties):

- Redeemable preference shares with a face value of $1.00

- Minimum buy-out price of $2.00 (being $127.4m based on an initial investment of $63.7m) plus additional upside participation of 80% in total per share equity value created above $2.00

- Full participation rights on a pro-rata basis (i.e. to annual distributions, etc) as if the Junior Capital was ordinary equity

- Target Exit Date of 30 June 2017, but mandatorily repayable within 5 years

• The ‘public offer’ test for the purposes of the section 128F withholding tax (WHT) exemption may be satisfied by SCF

• If any of the above indicative terms change, the outcomes of our analysis may also change.

17 Mr Sykes set out his understanding as a result of reviewing Mr Shelswell’s email. It was as follows:

80. I understood the effect of Mr Shelswell’s words ‘making the preferred equity into “debt for tax purposes”’ to mean that the only material change to the ICG’s indicative terms would be in respect of the tax effect.

81. Further, I understood from the words in the email ‘if it doesn’t change the commercial deal’ to mean that the change to ‘debt for tax purposes’ did not affect the ‘commercial deal’. I understood the words ‘commercial deal’ as referring to the rights, risks and obligations of the parties to the proposed ‘deal’.

82. Further, I understood the words ‘win-win’ to mean that the change would be to the advantage of all parties to the ‘commercial deal’.

83. If at the time of the email of 4 March [sic] 2012 I had been aware that a change from equity to debt did not effect only ‘for tax purposes’ and, or that a change from redeemable preference shares to debt has significant consequences for the risk to the solvency of the company incurring the debt and, or that a change from redeemable preference shares to debt did not provide a material advantage to all parties, I would not have continued negotiations.

18 On or about 7 May 2012, Mr Sykes received a copy of an email from Mr Shelswell to Mr Woodward which was in the following terms:

Given timing constraints we need to make a call on this - hopefully you had some time to read over the weekend amongst all the other commitments.

I’m happy to have a call to discuss live, but from my side, I can tell you it would be a positive for getting the deal approved internally, for two reasons - it will produce some more cash funding post acquisition (i.e. the cash that would otherwise go to the govt) which helps to defray the high entry valuation, and secondly, given that we may want to access more funding from growth, having a debt form will enable us to syndicate growth funding to a wider class of investors (because there are more investors who are able to invest in ‘debt’ than in ‘equity’, even if the commercial terms of the paper are exactly the same. I know that makes very little sense but it’s how the finance markets are...)

Hopefully this works but let’s discuss live on a separate session not with Archer or EY.

19 Mr Sykes set out his understanding of the transaction as a result of reviewing this email. It was as follows:

92. I understood the reference to ‘debt’ in this email to be the same as ‘debt for tax purposes’ referred to in Mr Shelswell’s email dated 4 May 2012, and that, consequently, the only material change to ICG’s proposal would be in respect of the tax effect.

93. I further understood the words ‘even if the commercial terms of the paper are exactly the same’ to mean that there would no material difference for the parties between a ‘debt’ investment and an ‘equity’ investment, other than tax benefit and access to a wider class of investors for ‘growth funding’.

94. I noted Mr Shelswell’s statement ‘I know that makes very little sense but it’s how the finance markets are’ as an assurance that I should not be concerned about a change from equity to debt.

95. If at the time of the email of 7 May 2012 I had been aware that a change from equity to debt did not have effect only ‘for tax purposes’ and, or that a change from equity to debt has significant consequences for the risk to the solvency of the company incurring the debt, I would not have continued negotiations. Further, I was comforted by Mr Shelswell’s assurance and accepted his statements as true.

20 Over the following days, there was discussion about a document prepared by Allen & Overy on behalf of the ICG which purported to set out the key terms of a proposed Shareholders’ Deed. This document with some changes was eventually executed by the parties on 15 or 16 May 2012. I will refer to it as the Terms Sheet for the Shareholders’ Deed. Three matters in the document are significant. First, it refers to the Preferred Notes to be issued to the ICG. Secondly, it describes a “Formal Exit Process” as involving the Board (of Holdco) determining the exit timing and method and it being a full or partial share sale, asset sale or IPO and that the Board may initiate an exit event at any time, providing Holdco has obtained the prior written consent of holders of a majority of the Preferred Loan Notes (by face value). Thirdly, the Terms Sheet for the Shareholders’ Deed provides that until (among other things) the Preferred Loan Notes are repaid, Holdco is not able to take a number of steps, including borrowing monies, other than under current credit arrangements, or to trade creditors in the ordinary course of business.

21 There was a meeting of the management shareholders on 10 May 2012 and Mr Shelswell gave a presentation to the meeting. Mr Levy also attended the meeting and he gave a short presentation to the management shareholders.

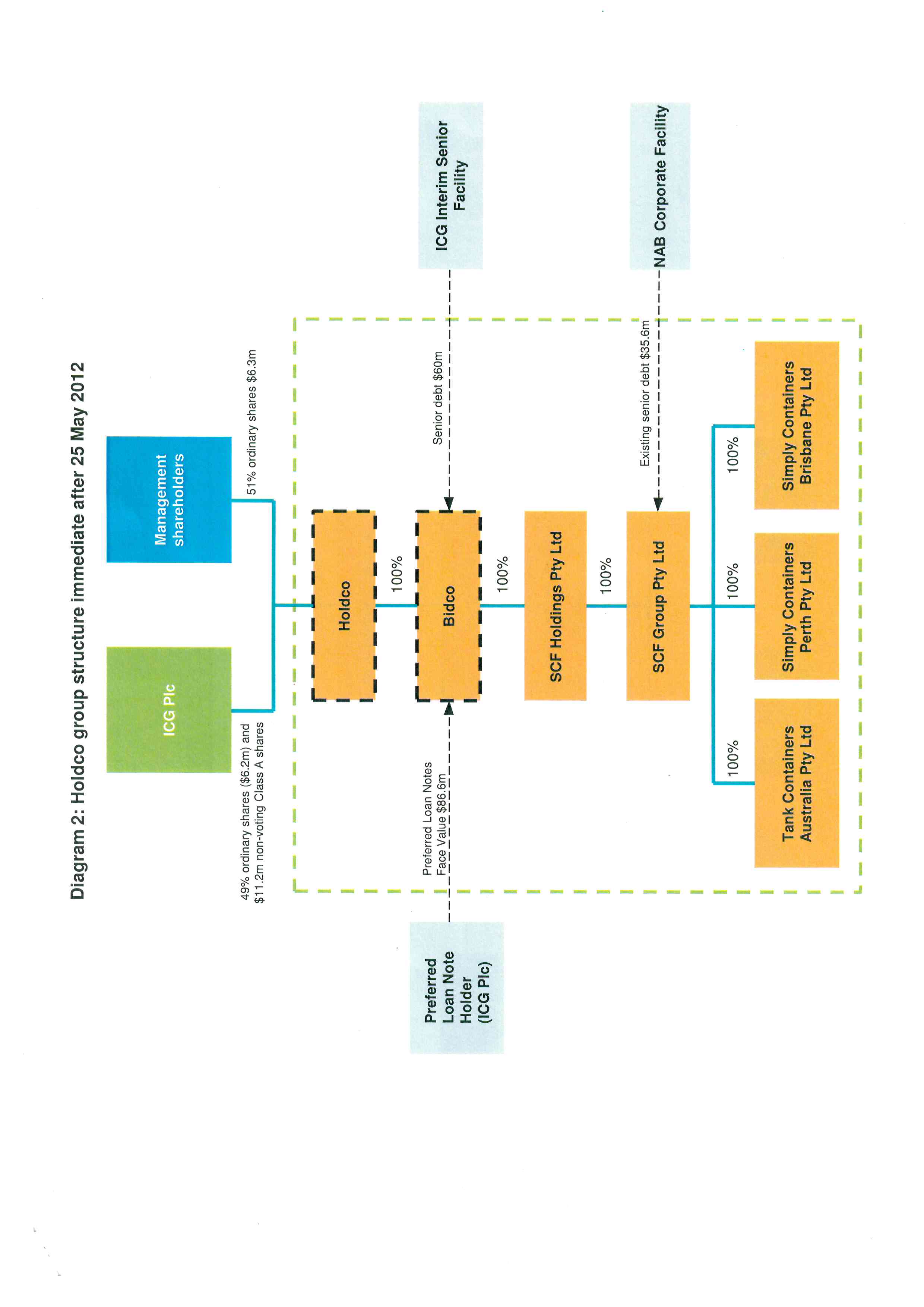

22 Holdco was incorporated on 15 May 2012 and Mr Sykes and Mr Shelswell were appointed as the initial directors. Mr Woodward and Mr Thomas Anning became directors on 22 May 2012 and Dr Heine replaced Mr Anning on 20 November 2012. The same position obtained with respect to Holdco’s wholly owned subsidiary Bidco except that Mr Woodward and Mr Anning became directors on 25 May 2012. In late May 2012, the directors of SCF Holdings were Mr Sykes, Mr Woodward, Mr Shelswell and Mr Anning. The same position obtained with respect to SCF Holdings’ wholly owned subsidiary, SCF Group Pty Limited.

23 As I have said, the Terms Sheet for the Shareholders’ Deed was executed on 15 or 16 May 2012. The Terms Sheet states that it is legally binding on the parties. Mr Levy gave Mr Sykes advice about that document.

24 Mr Sykes and Mr Shelswell, as the directors of Holdco and Bidco, executed a Share Sale Agreement on 17 May 2012. Mr Sykes states that he would not have executed this document had he known the following matters:

117.1 the change in the proposed funding arrangements, from ICG subscribing for redeemable preference shares to funding by debt, was a substantial change in the commercial effect of the Sale and the Transaction, and, or

117.2 the change in the proposed funding arrangements, from ICG subscribing for redeemable preference shares to funding by debt, was not a ‘win-win’ where each party to the Sale and the Transaction (including ICG, SCF Group and SCF Holdings) would be better placed commercially than if the change did not occur; and, or

117.3 the legal and practical consequences of funding by debt rather than redeemable preference shares operated to the advantage of ICG and other Lenders under the Transaction, and to the disadvantage of Popeye Holdco and Popeye Bidco because they are exposed to a substantially greater risk under the preferred loan note arrangement than would have been the case if the change did not occur, and, or

117.4 the change in the proposed funding arrangements, from ICG subscribing for redeemable preference shares to funding by debt, created a real commercial disadvantage to Popeye Holdco, Popeye Bidco, SCF Holdings and SCF Group when compared to the terms of the original proposed funding arrangements and was not a positive change; and, or,

117.5 the execution of the share sale agreement would bind Popeye Holdco and Popeye Bidco to enter into subsequent agreements (so as to obtain funding to meet the obligations they assumed) which would expose them to a severe risk of significant detriment and insolvency, but with no corresponding commercial benefit to them,

25 On 22 May 2012, a number of emails passed between Mr Sykes, Mr Woodward and Mr Shelswell. Mr Woodward wrote to Mr Sykes in the following terms:

I’ll update the balance sheet in the morning and we can discuss.

Are you comfortable with releasing the full consolidated group position from Holdco down and would we consider the Pref Notes as equity or debt?

Mr Sykes responded to Mr Woodward with a copy to Mr Shelswell and others as follows:

I think it is form of debt for tax purposes but leave that one to you Ryan.

We should work out what they need in morning as they may as well wait until we have constructed the balance sheet.

Mr Shelswell responded to Mr Sykes and Mr Woodward in the following terms:

I would prefer not to release the full position if we don’t have to. Maybe try to satisfy them with SCF?

If you do need to disclose, then in regard to the PLN, you should give them the colour that it is economically/commercially pref equity, but it is tax debt

26 An Indicative Terms Sheet for the PLNSA appears to have been sent to Mr Levy by Allen & Overy on 23 May 2012 together with a draft copy of the PLNSA. It refers to a Termination Date of the first to occur of 30 June 2017 (or such later date as might be agreed by the Agent acting for the Lenders) or an Exit Event.

27 Mr Sykes deposes to events which occurred on the settlement date of 25 May 2012. He said that there were a large number of documents to sign in the offices of Minter Ellison in Adelaide and no time to read the documents. Mr Sykes said that he has since tried to read the PLNSA, but he found it extremely complex and he is unable to understand it.

28 I turn now to describe briefly the provisions of the relevant agreements. The PLNSA dated 25 May 2012 is between Bidco as borrower, Holdco as original guarantor, Intermediate Capital Asia Pacific Limited as arranger, Intermediate Capital Group Plc as original lender and AET Structured Finance Services Pty Limited as the agent. The lender subscribes for Loan Notes to be issued by the borrower in the amount of $86,626,499. The guarantor guarantees the borrower’s obligations under the agreement, including its obligation to repay the amount owing. The minimum amount repayable is the Loan Amount multiplied by two. As I understand it, this is the means whereby interest (which is capitalised) is recovered. There is provision for the recovery of a larger amount by way of a variable return to note if the venture is successful. The Holdco group did not achieve its expected returns and the variable return to note is not relevant in the circumstances. There is provision for the payment of an Early Redemption Amount (calculated to be in the order of $350 million) if the Loan becomes payable on demand before 30 June 2017. Pursuant to clause 6, the Termination Date of the PLNSA is 30 June 2017 unless the Agent on instructions from the Lenders agrees to a later date no later than a date 10 years after the Loan is made. As I understand it, unless the date is extended, in the circumstances of this case $173 million will become due and payable by Holdco and Bidco on 30 June 2017. There is provision for an Exit which is a concept I will describe in summarising the Shareholders’ Deed, and on an Exit, an Exit Redemption Amount is payable pursuant to clause 7.2. I understand the calculation of that amount to be different from the calculation of the Termination Date Redemption Amount in accordance with clause 6.

29 The borrower has a number of other obligations under the PLNSA, including the provision of audited consolidated financial statements of the Group within 120 days of the end of each of the Group’s financial years. Failure to do so can lead to an event of default under clause 18, which in turn, can lead to the Loan becoming payable on demand.

30 The Shareholders’ Deed dated 25 May 2012 is between the management shareholders, Intermediate Capital Group Plc, Holdco and Intermediate Capital Asia Pacific Limited. An Exit Event is defined as a change in control of Holdco, a Listing, a disposal of all or substantially all of the business and assets of the Group or a combination of a change of control and a disposal. The Shareholders’ Deed may come to an end if the Board of Holdco determines it is reasonably required in connection with an Exit. The parties to the Deed acknowledge that they intend to achieve an Exit prior to 25 May 2017. The Board of Holdco is able to propose an Exit at any time providing a majority of the Preferred Loan Note Holders agree. The initial Investors may initiate an Exit in certain circumstances, including the occurrence of an Event of Default or at any time after 25 May 2012 where any of the Preferred Loan Notes remain outstanding. The Exit process in terms of the precise timing and method is controlled by the Board of Holdco, although if no Exit occurs before 25 May 2017, the Exit process must be completed as soon as reasonably practicable following that date.

31 The General Security Interest is a Deed dated 25 May 2012 between Holdco and Bidco which are the providers of security, and AET Structured Finance Services Pty Limited which is the Security Trustee. The secured property is all of the property of Holdco and Bidco and it is security for the performance of the obligations and the payment of the secured money as defined.

32 There were other agreements, but it is not necessary for me to summarise their effect.

33 The structure of the Holdco group after the transactions in May 2012 is shown in Diagram 2 of Annexure A.

Events in 2013 – 2016 inclusive

34 The PLNSA was amended in one respect by Deed of Amendment dated 9 August 2013. The nature of the amendment is not presently relevant. The respondents submit that the following clause in the Deed of Amendment is significant:

2.2 Entry into this deed does not affect the validity or enforceability of the Principal Agreement or any accrued rights or liabilities of any party under the Principal Agreement and each party is bound by the Principal Agreement as amended by this deed.

35 The Holdco group was required to complete consolidated annual financial statements. The statements for the financial years ended 30 June 2012, 2013, 2014 and 2015 were put before the Court. In each case, the statements show the Preferred Loan Notes as a non-current liability and not as equity. In each case, there is a reference in the notes to the accounts to a target exit date of 30 June 2017 or within 10 years. In each case, the financial statements are signed by Mr Sykes and, in the case of the financial statements for the year ended 30 June 2012, he signed the statements on 15 April 2013. That was before the Deed of Amendment was executed on 9 August 2013. The financial statements for the financial year ended 30 June 2015 contain the following statement:

At the balance date, the Group has a deficiency of equity of $9,812,458, current assets exceed current liabilities by $7,215661 [sic] and non-current liabilities of $187,121,406. The non-current liability mainly relate to preferred loan notes of $129,103,734 and an embedded derivative of $887,127 within the preferred loan notes (see Notes 14 and 17 for further details), and secured borrowings of $57,000,000 (see notes 14 and 20 for further details). As the preferred loan notes have a maturity date of 30 June 2017 and the secured borrowings have a maturity date of September 2017, the directors do not believe the amount will become due and payable for a period of at least 12 months from the date of signing the financial report.

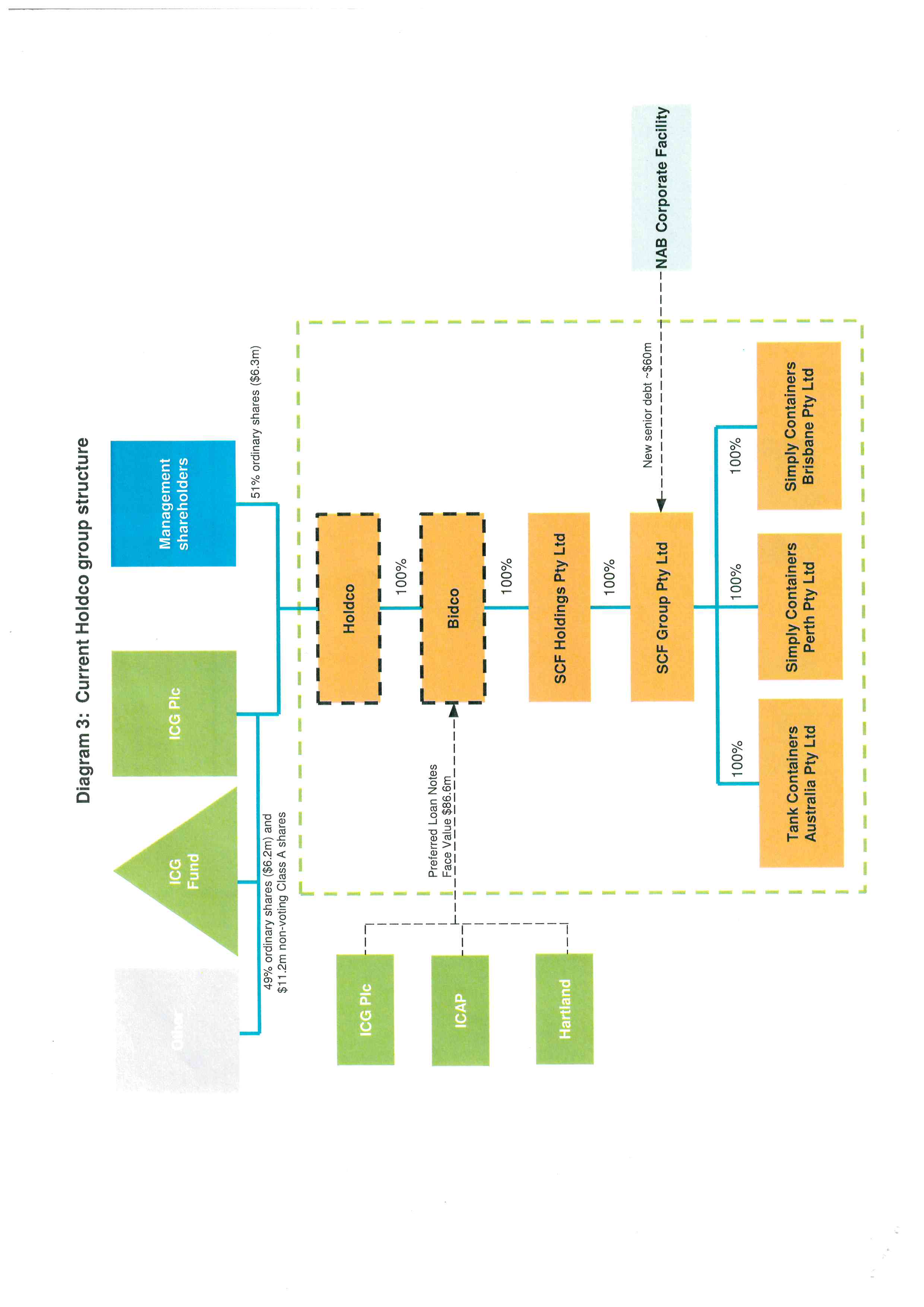

36 The business of the Holdco group did not grow as anticipated and rather than five years of growth before another sale process and the realisation of the investment in equity envisaged for June 2017, those with an interest in the Holdco group were, towards the end of 2016, considering the refinancing and restructuring of the Holdco group with a view to what was called delivery of a new plan to June 2019. The proposal for refinancing and restructuring involved converting the Preferred Loan Notes to equity and, as the paper which sets out the proposal states, setting all current equity to zero. The senior debt (i.e., the NAB debt) is said to be approximately $40 million and the estimated value of the enterprise is said to be $132 million. The parties with an interest in the Holdco group have not been able to reach an agreement as to the refinancing and restructuring of the group.

Events in 2017

37 The present structure of the Holdco group is shown in Diagram 3 of Annexure A.

38 Bidco has not delivered to the Agent the audited consolidated financial statements for the Holdco group for the financial year ended 30 June 2016 as required by clause 16.1 of the PLNSA. That led to a letter from the ICG to Holdco and Bidco dated 20 February 2017, but not delivered until 21 February 2017. The next step, assuming the interlocutory injunction is not granted, will be a formal demand under clause 18.2(b), and if that is not met, the ICG could (among other things) declare all or part of the Loan payable on demand under clause 18.9. There is also power under the General Security Interest to appoint a receiver.

39 A meeting of the board of directors of each of the four applicants was held on 22 February 2017. Dr Heine and Mr Shelswell resigned from the board of each of Holdco and Bidco before a resolution authorising the appointment of lawyers on behalf of the companies was passed. In the case of SCF Holdings and SCF Group, the resolution authorising the appointment of lawyers was passed on the casting vote of Mr Sykes.

Analysis

A prima facie case

40 At the heart of the applicants’ case is the difference between redeemable preference shares and preferred loan notes of the type issued in this case. At a general level it may be said that the former is equity and the latter is debt. Under the Corporations Act, redeemable preference shares may only be redeemed out of the company’s profits or from a share issue organised for that purpose. The terms of the issue of redeemable preference shares may include a date for repayment and the type of terms that one sees in the PLNSA, such as an obligation on the issuing company to provide audited financial statements. The difference arises where the date for redemption arrives and there are insufficient profits and no possibility of a new issue of shares. In those circumstances, the holders of the redeemable preference shares may petition to have the company wound up (Austin RP, Ford’s Principles of Corporations Law (16th ed, LexisNexis Butterworths, 2015) at [24.610]-[24.650]). The circumstances in which redeemable preference shares may be redeemed on the one hand, and an Exit Event under the PLNSA and the Shareholders’ Deed on the other, do not correspond precisely.

41 The difficulties with a case that the Preferred Loan Notes are to be treated as debt for tax purposes, but are redeemable preference shares for all other purposes and subject to s 254K of the Corporations Act, are as follows. First, Mr Sykes did not give any evidence about s 254K of the Corporations Act or that he had any understanding of its provisions. Secondly, other than redeemable preference shares being equity, Mr Sykes did not give evidence of his understanding of the terms and conditions of the “redeemable preferences shares”. Thirdly, if the Preferred Loan Notes are to be treated as redeemable preference shares, it is not at all clear what terms and conditions apply to them. Finally, the applicants’ case as reflected in the interlocutory injunction it seeks acknowledges that the ICG may initiate an Exit Event after 25 May 2017.

42 It seems to me to follow from the above that the applicants’ case is that as a result of the agreements or the ICG’s conduct or both, the only way the ICG can realise their investment represented by the Preferred Loan Notes is by an Exit Event.

43 The applicants’ first submission is that the agreements when read together provide that the only way in which the ICG can realise their investment is through an Exit Event. That submission cannot be sustained if the PLNSA dated 25 May 2012 and the Shareholders’ Deed dated the same date are read together. The PLNSA contemplates at least two methods of bringing the agreement to an end and that is by the Termination Date with a Termination Date Redemption Amount calculated in a particular way, and an Exit Event with an Exit Event Redemption Amount calculated in a different way. There is nothing in the Shareholders’ Deed which suggests that it qualifies the PLNSA by providing that only an Exit Event brings the ICG’s investment to an end.

44 The applicants sought to overcome this difficulty by the following argument. They submitted that the Terms Sheet for the Shareholders’ Deed was executed some 10 days before the PLNSA and the Shareholders’ Deed. It was expressed to be legally binding on the parties. It provided the sole method of exit being, in effect, an Exit Event. The later agreement, being the PLNSA, is to be read subject to what the parties had already agreed. That can be done (so it was submitted) because the Lenders have the power under the PLNSA to extend the Termination Date so that it coincided with an Exit Event. I reject this submission. It is clear from the documentation in early May that the parties contemplated a five year arrangement and a target exit date of 30 June 2017 and in that respect, I refer to the draft Deloitte report and the business plan adopted by Holdco on or about 23 May 2012. More importantly, the parties contemplated a suite of agreements and there is no reason to think they gave priority to the Terms Sheet for the Shareholders’ Deed. Furthermore, it remains difficult to construe the terms of the Lenders’ power to extend the Termination Date as imposing an obligation on them to do so in order that it coincide with an Exit Event. I do not think the applicants’ alternative submission that an estoppel arose adds anything to their position for the same reasons.

45 The applicants’ second submission is that there is a prima facie case that the ICG were guilty of misleading and deceptive conduct in connection with their “investment” of approximately $86 million in Holdco and Bidco. Broadly speaking, that conduct was a representation that, but for taxation consequences, the investment was equivalent to equity and, more particularly, redeemable preference shares. For reasons I have given, the highest the applicants can put their case is that the only way the ICG can seek to recover their investment is through an Exit Event. I have earlier identified some of the conduct the applicants rely on as misleading and deceptive conduct. The conduct was mainly that of Mr Shelswell who was a director of Intermediate Capital Australia Pty Limited. That company was said to be the agent of the other ICG companies. The applicants identified other conduct in the course of their submissions, such as the fact that the Preferred Loan Notes carry the right to receive distributions equal in amount to dividends.

46 The applicants relied on s 18 of the Australian Consumer Law and in terms of the orders which might be made, ss 237 and 243 of the Australian Consumer Law. The respondents suggested that the transaction involved financial services and the relevant sections are the equivalent sections in Australian Securities and Investments Commission Act 2001 (Cth). It is not suggested that there is any material difference between the two and, for the purposes of this application, I will proceed by reference to the provisions of the Australian Consumer Law.

47 The orders the applicants may obtain if successful raise a number of complex considerations. They seek an order setting aside the PLNSA, but if that was to occur without more, I do not think that it could be seriously argued that setting aside the PLNSA would not be on terms that Holdco and Bidco repay the ICG the sum of approximately $173 million, an obligation they plainly could not discharge. The order that would reflect the applicants’ case would be a variation of the Termination Date and Exit Event, but the other terms and conditions which would apply is far from clear.

48 I need not pause on the recent High Court authorities dealing with misleading and deceptive conduct as the principles are well known: Butcher and Another v Lachlan Elder Realty Pty Limited (2004) 218 CLR 592; Campbell and Another v Backoffice Investments Pty Ltd and Another (2009) 238 CLR 304; Miller & Associates Insurance Broking Pty Ltd v BMW Australia Finance Limited (2010) 241 CLR 357. It is sufficient to say that in Butcher and Another v Lachlan Elder Realty Pty Limited at [109] and [111], McHugh J made the point that whether conduct is misleading or deceptive, or likely to mislead or deceive, is a question of fact and the Court is required to consider the conduct as a whole and in light of the relevant surrounding facts and circumstances. His Honour also said that conduct is misleading or deceptive if it induces or is capable of inducing error.

49 The applicants’ misleading and deceptive conduct case faces a number of significant difficulties. The first is a matter of some complexity. The applicants’ case depends on attributing Mr Sykes’ state of mind and not Mr Shelswell’s, or not including Mr Shelswell’s state of mind to Holdco and Bidco. It is not obvious that that would be done. The second difficulty with the applicants’ case is the obvious point that Mr Sykes signed the PLNSA as a director of Holdco and Bidco and the PLNSA included clause 6. The third difficulty is that the applicants “affirmed” the PLNSA by the Deed of Amendment in August 2013. Aside from the legal effect of that act, it does bear on the applicants’ case as a matter of fact. Mr Sykes would have been aware in April 2013 when he signed the Holdco group accounts that the investment was treated as a non-current liability and not equity, and did not raise any query which might be taken to suggest that he did not have the state of mind in May 2012 which he alleges. In the alternative, it might be argued that the applicants are guilty of unexplained delay.

50 There is another matter which I mention, but which in the end I think is neutral because it involves a disputed question of fact. Mr John Levy was a legal practitioner who was advising Mr Sykes as well as other management shareholders. He advised Mr Sykes on the Terms Sheet for the Shareholders’ Deed and the Intercreditor Deed. The respondents’ case is that Mr Levy was sent a copy of a draft of the PLNSA. He appears to have been sent a copy of a draft of the PLNSA on 23 May 2012. The applicants, through Mr Sykes, deny that he received it.

51 The applicants’ third submission is that Mr Shelswell and members of the ICG acted in breach of fiduciary and statutory duties they owed as directors of Holdco and Bidco in connection with that company’s entry into the PLNSA. It was not in Holdco and Bidco’s best interests to incur such a large liability. This claim is framed in various ways. Mr Shelswell was a director of Holdco and Bidco and the ICG’s liability is said to flow from its knowing involvement in equity or under s 79 of the Corporations Act. In the alternative, the companies in the ICG were themselves de facto or shadow directors within s 9 of the Corporations Act. The duties said to have been breached were the fiduciary duties of directors and those set out in ss 180 and 181 of the Corporations Act. It is also said that Mr Shelswell failed to declare a conflict as required by s 191 of the Corporations Act.

52 It is not obvious to me that causing Holdco and Bidco to enter into the PLNSA in the circumstances was a breach of a director’s duty. The two companies were established in order to give effect to a broader transaction. The companies borrowed money in order to purchase very substantial assets. There is no reason to think that those assets were not competently valued at the time of the transaction. The debt was not due for repayment for at least five years. The companies supported a business plan which showed very lucrative returns to management and the holder of the Preferred Notes in the financial year ended 30 June 2017. As it happens, an Exit Event under the Shareholders’ Deed is likely to lead to the sale of the companies’ assets as would an insolvency for the failure to repay a debt.

53 The applicants’ fourth submission is that the respondents’ conduct was unconscionable. The applicants’ Originating Application refers to s 20 of the Australian Consumer Law (i.e., unconscionable conduct within the unwritten law), whereas the applicants’ Amended Statement of Claim also refers to unconscionable conduct with the Statute. Either way, the applicants’ case faces substantial difficulties. In addition to the matters to which I have already referred, the following matters raise difficulties for the applicants. This was a large commercial transaction between sophisticated parties. Mr Sykes was the Chief Executive Officer of a group which had an enterprise value of over $100 million. Furthermore, whether Mr Sykes received advice about the PLNSA from Mr Levy or not, the fact is that the respondents appear to have acted in an open manner and without predatory or overbearing characteristics. The conduct does not seem to have any of the required features for unconscionable conduct under the general law (Kakavas v Crown Melbourne Limited and Others (2013) 250 CLR 392; Australian Competition and Consumer Commission v Samton Holdings Pty Ltd and Others (2002) 117 FCR 301) and it is not immediately obvious that many of the non-exhaustive statutory factors would be engaged.

54 Finally, the applicants claim that enforcement of the PLNSA before 30 June 2017 would involve the enforcement of a penalty because of the early redemption amount of approximately $350 million. The respondents accept that there is a prima facie case that such an amount would be a penalty. However, they seek to deal with the problem by proffering the following undertaking:

The Majority Lenders undertake to the Court and to the Applicants that the Majority Lenders will direct the Agent not to issue a notice to Popeye Holdco Pty Ltd (the Original Guarantor) pursuant to clause 18.9(a) of the Preferred Loan Note Subscription Agreement and will not agree [sic], vary or countermand that undertaking prior to 30 June 2017 without providing five business days prior written notice to the Applicants.

55 The significance of the date 30 June 2017, is that if there is a declaration that the loans are payable on demand, then the amount payable on and after 30 June 2017 is not the early redemption amount, but is the termination date redemption amount, namely, an amount of approximately $173 million. That latter amount is not alleged to be a penalty. There may be an issue about the question of a penalty, but in light of the undertaking, it does not arise at this stage. The undertaking should be noted in the order dealing with this application.

56 In conclusion, in my opinion, the applicants do not have a strong prima facie case.

The balance of convenience

57 Absent an injunction, the ICG could serve a notice under clause 18.2(b) of the PLNSA. Failure to comply with the notice would be an Event of Default which could lead to a declaration that the Loan is payable on demand and the appointment of a receiver. The steps which the respondents could take would be subject to the undertaking, but leaving aside the penalty issue, Holdco and Bidco would be required to repay approximately $173 million. They could not do that. They could not do that even if all of their assets are sold. On present indications, there would be a shortfall in repayment to the ICG of approximately $81 million (Enterprise value $132 million – Senior debt of $40 million – Respondents’ debt of $173 million).

58 The applicants refer to the restructure proposal put forward by the ICG in December 2016. Under this proposal, Holdco would remain the ultimate holding company of the SCF Group and the investors, being Intermediate Capital Group Plc, Intermediate Capital Asia Pacific (2008) GP Limited and Hartland Investment Pte. Limited, would hold 100% of the share capital of the company. The applicants contend that the respondents have not resiled from this plan and that absent an injunction, irreparable injury will be occasioned to Holdco which would have, without having received any benefit, lost the whole of the business undertaking, the prospects of future growth of that business undertaking, and its only asset.

59 The applicants contend that it is unclear whether the respondents would suffer any loss or damage should an interlocutory injunction be granted. They submit that the respondents have provided no indication of what they might do as a result of the alleged non-monetary default. They have provided no indication of whether they are actively considering the exercise of any rights under the PLNA and the General Security Interest. They have provided no indication of valuations of the entities or of time frames. The applicants submit that the respondents have produced no evidence of what they intend to do. They submit that it is difficult to see any prejudice in those circumstances.

60 On the other hand, the respondents point to the fact that an Exit Event may be activated on or after 25 May 2017 and that that may well lead to the sale of the Holdco group’s business. Furthermore, they are the party carrying the loss at the present with a substantial shortfall in the repayment of their investment. The only parties likely to recover anything are the senior debt-holder (i.e., the NAB) and the respondents.

61 In a letter from their solicitors, the respondents pointed to likely ongoing loss if there is an interlocutory injunction. The applicants countered by pointing out that the solicitors’ assertions of ongoing loss were just that, and were not supported by any evidence.

62 The first category of alleged ongoing loss is the inability to realise value from the secured property for a period beyond the term of the initially envisaged financing term and, as a consequence, lost time value of money during that extended period. The respondents put forward a figure of $3,795,000 assuming they succeed in defending the proceeding, but that enforcement is delayed for six months. They have calculated that figure on the basis of an enterprise value of $132 million and an interest rate of 5.75%. The respondents contend that such an interest rate is very conservative for the type of investor involved.

63 The second category of alleged ongoing loss is the loss of revenue, opportunity and customer confidence by reason of the uncertainty and inability which SCF Holdings and SCF Group will suffer as a consequence of being embroiled in these proceedings, rather than focusing on growing its core business. The ICG submit that that will lead to a deterioration in the value of the enterprise when it comes to the realisation of the security. The applicants submit that this alleged loss is “rank speculation”.

64 The third category of alleged ongoing loss is the reputational prejudice to the ICG, having regard to the nature of their business and their investors’ reliance upon its ability to make sound investment decisions and to deliver returns and the inability of the ICG to repay its investors (which include several pension funds) in full and in the time frame forecasted or at all. The applicants submit that there is no evidence relating to the nature of the business conducted by the ICG and there is no evidence of the nature or reliance of any investors. The applicants submit that the matters put forward by the ICG are “matters of mere assertion which require speculation, without any admissible foundation, asserted prospective events”.

65 The fourth category of alleged ongoing loss is that there will be an immediate and irreversible depletion in the value of the secured property in circumstances where the first and second applicants have no funds to meet legal costs meaning that the third and fourth applicants will bear the disproportionate and unreasonable burden of paying the entirety of the applicants’ legal costs. The applicants submit that there is no evidence that the continuation of the injunction will lead to any depletion in value of the secured property far less any irreversible depletion in the value of the secured property.

66 The ICG seek security for the undertaking as to damages in the sum of at least $5 million.

67 The respondents submit that the operative obligations in respect of the PLNSA are the obligations created afresh by the 2013 Amending Deed. Secondly, they submit that the Court would not set aside one agreement in a suite of interdependent agreements reached as part of a single transaction. Thirdly, they submit that if the PLNSA is set aside, that would necessarily be on terms that Bidco repay the monies advanced. In those circumstances, any injunction granted would be on terms that the applicants pay into Court at least the amount advanced plus interest. There is no suggestion that they could do that.

68 The respondents also submit that ICG is currently prevented from taking any steps to protect its interests arising from the breach of the obligation in the PLNSA to provide audited accounts. Mr Sykes’ complaint relates only to the repayment obligations. The respondents submit that however the transaction was funded, it is inevitable that there would have been obligations to provide accounts to enable the majority investor to monitor the financial performance of the company. Such obligations are described by the respondents as “common and fundamental”. The respondents submit that even though the relevant undertaking to provide audited accounts is contained in the PLNSA, it is not connected in any way to the conditions for repayment, and it would have been included even if the PLNSA was instead a redeemable preference share subscription agreement. The respondents submit that even if an external administrator took steps to realise the assets, there is no prejudice because the ICG has the right to require that to be done on and from 25 May 2017 in any event. The respondents submit that the undertaking as to damages is inadequate because the only property the applicants have is property to which the respondents claim an entitlement. Finally, the respondents submit that the applicants have delayed and are not now entitled to an injunction.

69 My conclusions on the balance of convenience are as follows.

70 The Court must consider the hardship to the respondents if an injunction is granted and the hardship to the applicants if an injunction is not granted. The Court will ordinarily require an undertaking as to damages. In an appropriate case, the Court will require security for the undertaking as to damages.

71 The applicants do not contend that from 25 May 2017 the respondents will not be able to initiate an Exit Event and that the respondents will not be entitled to the repayment of an amount of approximately $173 million. If the respondents’ case is correct, then absent the respondents granting an extension of time, the applicants will be liable to repay the respondents approximately $173 million on 30 June 2017. On the evidence before me, there is no prospect the applicants will be able to do that without a major injection of cash. On the evidence before me absent a major injection of cash, the applicants will recover something in the order of $92 million.

72 The hardship to the applicants if an injunction is not granted is that the respondents may well take action under the PLNSA and General Security Interest which would result in the sale of the Bidco shares held by Holdco and effectively the business. That is something that could happen in any event after 25 May 2017 if the respondents initiated an Exit Event, although in the latter case, Holdco would be in control of the process. It is possible that such a process might take longer than sale by a receiver and might result in a better price, but it is really not possible to say that with any certainty. The reality is that Holdco does not have the right to continue to carry on business with the assets after 25 May 2017. The applicants seemed to recognise that this creates a difficulty for them and, as I have said, they argued that, as a matter of fact, it is unlikely the respondents will initiate an Exit Event. I can infer that (so it was argued) from the fact that the respondents had not resiled from the December 2016 proposal which envisaged trading until 2019 and from the fact that the respondents had not put on any evidence as to what their intentions were. It is true that the respondents have not put on any evidence as to what they intend to do. However, I am not prepared to draw any inference as to what the respondents will do. What does seem plain is that the Holdco group is not able to repay the “debt” in full and that the shortfall is significant. It is highly likely that some form of action will need to be taken in the near future. The short point is that an injunction may not avoid a similar, although I acknowledge not identical, form of “hardship” to that which is said to justify the injunction.

73 As far as the respondents are concerned, they will soon be able to extricate themselves from the investment by initiating an Exit Event. They will have to wait until 25 May 2017 and they may not wish to initiate a process which will be under the control of Holdco. Otherwise, the respondents will have to await the determination of this proceeding. That process can be facilitated by an order for an early trial, but from what I have seen, the trial could be a substantial one involving a number of complex issues. In the circumstances, I am prepared to proceed on the basis that there will be, or may well be, a loss of use of money, in other words, the first category of alleged ongoing loss identified by the respondents. As to the other categories of alleged ongoing loss, while the events identified might well eventuate, it seems to me almost impossible to identify a specific financial loss as a result.

74 I do not think that the balance of convenience obviously favours one party or the other. As I have said, the applicants’ prima facie case is not a strong one and, in those circumstances, the application for an interlocutory injunction should be refused.

75 I add this. I have reached the above conclusion without questioning the adequacy of the undertaking as to damages. Had I been otherwise disposed to grant the injunction, I would have found that the undertaking as to damages needed to be secured because the applicants have no assets other than those to which the NAB and the respondents are or will be entitled. The appropriate security would be an amount in the order of $4 million or $5 million. I do not need to consider whether I would have given the applicants the opportunity to provide that security, or the respondents having raised this from the time of their first involvement, the application for an interlocutory injunction should be refused because of the failure of the applicants to offer security in support of their undertaking as to damages.

76 In view of my conclusions, I do not need to reach a final view on the respondents’ submission that Holdco and Bidco have not authorised the institution of these proceedings. That argument was based not on the constitution of each of Holdco and Bidco, but on the Shareholders’ Deed which provides that a quorum for a directors’ meeting of those companies is at least one management director (i.e., Mr Sykes or Mr Woodward) and one investment director (i.e., Dr Heine or Mr Shelswell). The applicants seemed to acknowledge the force of this contention in their Originating Application because they sought an order that Mr Sykes and Mr Woodward have leave under s 237 of the Corporations Act to bring this proceeding in the name of those companies. The application for that order did not appear in the Amended Originating Application. My tentative view is that, absent action by the respondents based on the Shareholders’ Agreement resulting in orders, the resolutions carried in accordance with the constitution of each company are sufficient.

Conclusion

77 For these reasons, the application for an interlocutory injunction is refused.

I certify that the preceding seventy-seven (77) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Besanko. |

Associate:

Annexure A

SAD 54 of 2017 | |

S.C.F. GROUP PTY LIMITED ACN 065 732 078 | |

INTERMEDIATE CAPITAL GROUP PLC | |

Fifth Respondent: | AET STRUCTURED FINANCE SERVICES PTY LIMITED ACN 106 424 088 |

Sixth Respondent: | INTERMEDIATE CAPITAL AUSTRALIA PTY LIMITED |

Seventh Respondent: | HARTLAND INVESTMENTS PTE. LIMITED |

Eighth Respondent: | RYAN SHELSWELL |