FEDERAL COURT OF AUSTRALIA

Australian Competition and Consumer Commission v Harrison [2016] FCA 1543

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By 4.00 pm on 10 February 2017, each party file and serve a written submission (not exceeding 10 pages) on relief, the form of orders and costs.

2. By 4.00 pm on 17 February 2017, each party file and serve any written submission (not exceeding 2 pages) in response.

3. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MOSHINSKY J:

Introduction

1 The second to eleventh respondents (the Harrison Companies) were incorporated progressively between 2010 and 2015. The first respondent (Mr Harrison) was the controller of each of those companies. The companies provided telecommunications services to customers (individuals and small businesses) in Australia. In the first part of the relevant period, the services were provided under the name “Sure Telecom”. Subsequently, the services were provided under the name “SoleNet”.

2 The applicant (the ACCC) alleges that, between 2013 and 2015, following customer complaints, a number of the Harrison Companies faced regulatory action by or incurred significant debts to regulatory authorities, namely the Australian Communications and Media Authority (ACMA) and the Telecommunications Industry Ombudsman (TIO). It is alleged that Mr Harrison’s modus operandi has been to cease trading through those companies subject to regulatory action and to create new companies under his control which then carried on the business of the previous companies, often with the same business name.

3 The ACCC alleges that a consequence of this system of conduct or pattern of behaviour was that Mr Harrison transferred or purported to transfer the customers’ contracts (that is, both rights and obligations) from one Harrison Company to another, without the customer’s knowledge or consent. It is alleged that the following transfers or purported transfers (transfers) of customer contracts occurred:

(a) in December 2013, from the third respondent (trading as Sure Telecom) to the fourth respondent (also trading as Sure Telecom);

(b) in September 2014, from the fourth respondent (trading as Sure Telecom) to the fifth respondent (trading as SoleNet);

(c) in June 2015, from the fifth respondent to the sixth respondent (both trading as SoleNet);

(d) in July 2015, from the sixth respondent to four State-based retailing companies, the eighth, ninth, tenth and eleventh respondents (each trading as SoleNet).

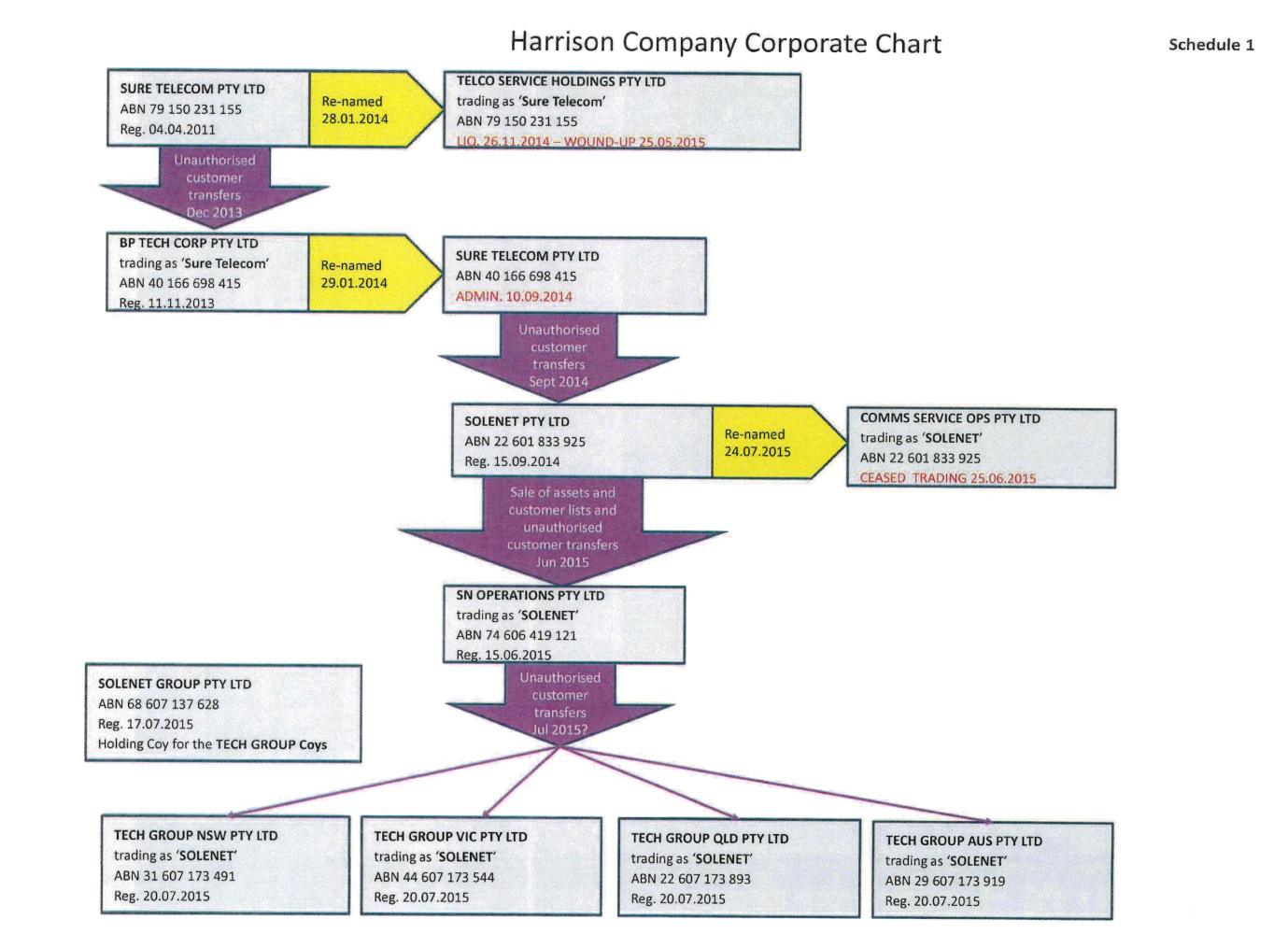

4 The series of transfers is depicted in the following corporate chart prepared by the ACCC and attached to its Concise Statement. The first, second and fifth to eleventh respondents admit the correctness of the diagram, save for the word “unauthorised”.

5 The ACCC contends that the terms of the contracts with the customers did not permit the transfer or assignment of the contracts without the consent of the customer, which was not obtained. It is contended that customers were unlikely to be or become aware that their contract had been transferred as (in many cases) the successor company used the same trading name, letterhead, address and logo as the previous company.

6 The ACCC alleges, in summary, that:

(a) the transferee companies made unjustified demands of customers who were not in any contractual relationship with the transferee company; for example, in some cases, the transferee company sought to enforce contractual terms that provided for the payment of early termination fees and cancellation fees when the customers sought to cancel the contracts; there was no basis for making such demands; on the contrary, the cessation of trade by the transferor company (with which the customer had a contractual relationship) meant that the customers were entitled to terminate the contracts;

(b) when customers whose contracts had purportedly been transferred refused demands for payment, they were subjected to persistent threats of legal action or threats of referral to debt collection agencies or law firms for debt recovery; the threats were calculated to intimidate in circumstances where there was no legitimate basis for the making of the demands.

7 The ACCC contends that, by engaging in the alleged conduct, the Harrison Companies engaged in unconscionable conduct in contravention of s 21 of the Australian Consumer Law (being Sch 2 to the Competition and Consumer Act 2010 (Cth)) (Australian Consumer Law) and conduct amounting to undue harassment and coercion in connection with the supply or possible supply of goods or services and/or the payment for goods or services in contravention of s 50 of the Australian Consumer Law.

8 The ACCC also contends that, at all material times, Mr Harrison was involved (within the meaning of s 2(1) of the Australian Consumer Law) in the alleged contraventions in circumstances where: Mr Harrison was or is the sole director of the Harrison Companies; Mr Harrison personally managed and controlled the day-to-day operations of the Harrison Companies; and Mr Harrison was often the author of, or had direct knowledge of, correspondence with customers and the regulators including, but not limited to, payment demands.

9 The hearing was in relation to both liability and relief. The respondents requested that I publish reasons on liability and then provide an opportunity for the parties to put on further written submissions on relief. The ACCC did not oppose this course. Accordingly, these reasons deal only with issues of liability.

10 My conclusions and reasons can be summarised as follows:

(a) In my view, the Harrison Companies engaged in a system of conduct or pattern of behaviour which was unconscionable in all the circumstances, in contravention of s 21 of the Australian Consumer Law. The key elements of the system or pattern were: the transfer of customer contracts from one Harrison Company to another without the customer’s consent; the failure to notify the customer of the transfer; save in relation to the second transfer, the adoption of the same trading name before and after the transfer; at least in the case of the third and fourth transfers, the sending of invoice documentation in substantially the same form before and after the transfer; and the ‘transferee’ company demanding payment of an early termination fee (or threatening to impose such a fee) if the customer wished to end a contract early. Additional elements in some cases were: the ‘transferee’ company threatening to refer the customer to a debt collection agency or lawyers if the customer did not pay the early termination fee; referral of the customer to a debt collection agency or lawyers if the fee was not paid; and the debt collection agency or lawyers threatening legal proceedings if the customer did not pay the early termination fee and additional charges. The conduct of the Harrison Companies was unconscionable in all the circumstances for the following main reasons. First, in general there was an imbalance in the strength of the bargaining positions of the Harrison Companies and the customer. Secondly, in the absence of a contractual term permitting the transfer, and in the absence of the customer’s consent, the transfers were invalid and ineffective. Consequently, there was no legitimate basis for the ‘transferee’ company to demand an early termination fee (or to threaten to impose such a fee). Thirdly, the process by which the Harrison Companies transferred the customer contracts from one company to another, at best, lacked transparency and, at worst, involved trickery and deception. Fourthly, the Harrison Companies placed undue pressure on the customer to pay the early termination fee or to ‘remain’ with the ‘transferee’ company.

(b) The system of conduct or pattern of behaviour described above was applicable in relation to each of the six customers who gave evidence in the proceeding. On this basis, the conduct of the relevant Harrison Companies in relation to these customers was unconscionable in contravention of s 21 of the Australian Consumer Law. There are also additional facts and matters which support the conclusion that the conduct of the relevant Harrison Companies in relation to the six customers was unconscionable in all the circumstances.

(c) In my view, in the cases of four of the six customers who gave evidence in the proceeding, the Harrison Companies used “undue harassment” in connection with the supply of services and the payment for services in contravention of s 50 of the Australian Consumer Law. The conduct amounted to persistent disturbance or torment; it was “undue” because the amounts were not owing.

(d) Mr Harrison was well aware of each of the elements of the system of conduct or pattern of behaviour. I am satisfied that he had knowledge of the aspects which lead to the conclusion that the conduct was unconscionable. It follows that I am satisfied that he was a person “involved” in the contraventions of s 21 of the Australian Consumer Law based on the system of conduct or pattern of behaviour of the Harrison Companies. However, I do not think the evidence establishes that he was aware of the particular conduct in relation to the six customers who gave evidence in the proceeding. As my conclusion in relation to s 50 of the Australian Consumer Law is based on particular conduct in relation to four of the customers, it follows that I am not satisfied that he was “involved” in the contraventions of s 50.

Procedural matters

11 Before the commencement of this proceeding, the ACCC sought and obtained freezing orders against the Harrison Companies in proceeding VID 220/2016.

12 The present proceeding was commenced by originating application. At the same time, the ACCC filed a Concise Statement setting out its case. The ACCC seeks the following relief in the originating application:

(a) a declaration that each of the Harrison Companies, in trade or commerce, engaged in conduct that was, in all the circumstances, unconscionable, in contravention of s 21 of the Australian Consumer Law;

(b) a declaration that each of the Harrison Companies used undue harassment or coercion, in connection with the supply or possible supply of goods or services and/or the payment for goods or services, in contravention of s 50 of the Australian Consumer Law;

(c) a declaration that Mr Harrison was directly or indirectly knowingly concerned in, and a party to, or aided and abetted, counselled or procured, the contraventions by the Harrison Companies of ss 21 and 50 of the Australian Consumer Law;

(d) injunctions restraining the Harrison Companies and Mr Harrison from engaging in certain kinds of conduct;

(e) pecuniary penalties against the Harrison Companies and Mr Harrison;

(f) an order disqualifying Mr Harrison from managing corporations for a period of time;

(g) orders for the payment of refunds to consumers and requiring the Harrison Companies to discontinue debt collection procedures against certain consumers;

(h) orders for Mr Harrison to undertake training in relation to ss 21 and 50 of the Australian Consumer Law;

(i) leave to proceed against the third and fourth respondents under s 471B of the Corporations Act 2001 (Cth);

(j) an order that a copy of the reasons for judgment, with the Court’s seal thereon, be retained in the Court for the purposes of s 137H of the Competition and Consumer Act; and

(k) costs.

13 The Concise Statement is summarised in [2]-[8] above. In the Concise Statement, the ACCC also contends that:

(a) the nature and intent of Mr Harrison’s system or pattern of behaviour is exposed in an email dated 17 December 2012 (the December 2012 Email), in which he responded to a demand by the TIO for debts owed by the third respondent by stating that he would seek to counter-claim against the TIO to delay any court process and that, by the time the hearing took place, the third respondent would have become a shell company and a different company would have taken over the customers;

(b) the Harrison Companies referred approximately 2,400 purportedly transferred customers to a debt collection agency or law firm acting for Mr Harrison or a Harrison Company seeking to recover approximately $2.4 million in purported debts;

(c) the debt collection agency, e-Collect.com.au Pty Ltd (eCollect), and the associated law firm, EC Legal Litigation Lawyers (EC Legal), recovered “debts” from at least 540 Harrison Company customers, with a value of at least $380,000;

(d) in at least one case, a Harrison Company commenced proceedings in the Magistrates’ Court of Victoria for unpaid debts allegedly owed by a customer whose contract had been transferred to that Harrison Company without that customer’s consent or knowledge;

(e) in some cases where a transferred customer resisted subsequent payment demands made by the debt collection agency or law firm, successor Harrison Companies, either directly or via the debt collection agency, offered to settle the disputed debt for a reduced, but still substantial, amount; customers often accepted this reduced offer in order to avoid the stress and time cost of being involved in the threatened legal action.

14 A Concise Response was filed. Although the document purports to be filed on behalf of all the respondents, I assume it was filed on behalf of the first, second and fifth to eleventh respondents (who were and are jointly represented by the firm of solicitors whose name appears on the document). The heading on this document refers to proceeding VID 220/2016 but, at the hearing before me, counsel for the first, second and fifth to eleventh respondents confirmed that the document should be treated as filed in this proceeding. In the document:

(a) the respondents deny that there was a pattern of behaviour to cease trading and to leave wholesalers and other creditors unpaid; they say that the transfers of customers took place due to difficulties with wholesalers, including the risk of litigation by the wholesaler against the relevant Harrison Company;

(b) Mr Harrison acknowledges sending the December 2012 Email and acknowledges that it was intemperate;

(c) in relation to the transfer from the third respondent to the fourth respondent, the respondents deny that the customers were not advised of the transfer of the contract and deny that there was a deliberate plan of establishing shell companies;

(d) the respondents admit the alleged transfers of customer contracts from the fourth respondent to the fifth respondent in September 2014 and say that all customers were given notice of the transfer; this was by way of an SMS referring the customer to the notice on the website and a written notice;

(e) the respondents admit the transfer of customer contracts from the fifth respondent to the sixth respondent in June 2015, and the transfer of customer contracts from the sixth respondent to the eighth, ninth, tenth and eleventh respondents in July 2015;

(f) the respondents admit the contents of paragraph 8 of the Concise Statement, which states that a series of transfers took place as depicted in the corporate chart in Schedule 1 to the Concise Statement (set out in [4] above); (it is convenient to note at this point that, in the course of the hearing, the respondents objected to an exhibit to Ms Snell’s affidavit which comprised a corporate chart to substantially the same effect; the respondents indicated that their objection was to the use of the word “unauthorised”; they were otherwise content with the chart);

(g) the respondents admit there was no provision in the customer contracts to transfer customers to another entity but state that the customers were advised of the proposed transfer at the time of the transfer and in all cases clients were sent an advice of transfer in compliance with Part 7 of the Telecommunications Consumer Protections Code (the TCP Code);

(h) in relation to the unjustified demands allegations, the respondents do not admit that there was a pattern of behaviour of attempting to recover fees from customers by an entity which was not entitled to the payment; the respondents admit that their collection agent “may have on some occasions attempted to recover from a customer under no legal obligation to make the payment” but say that this was done without the respondents’ knowledge at the time;

(i) the respondents deny that there was a systematic process of harassing customers, but admit that “there may have been some matters where payments which were not legally justified have been collected”;

(j) the respondents state that the value $380,000 in the Concise Statement would be for all collections made by eCollect for the five years, being the total of all customers since the beginning of the business, and would only partially relate to the matters alleged;

(k) the respondents admit paragraphs 16 and 17 of the Concise Statement (set out in [13](d) and (e) above);

(l) the respondents deny that the conduct referred to in the Concise Statement is a pattern of behaviour in breach of s 21 or 50 of the Australian Consumer Law;

(m) Mr Harrison “acknowledges”, which I take to mean admits, sub-paragraphs (a) and (b) of paragraph 21 of the Concise Statement, which are to the effect that at all material times Mr Harrison was the sole director of the Harrison Companies and personally managed and controlled the day-to-day operations of those companies;

(n) Mr Harrison denies that he had direct involvement in the collection process carried out by eCollect.

15 The ACCC filed a Concise Reply. In this document:

(a) the ACCC states that, irrespective of whether an SMS message or written notice was given to the customers (which is not admitted), the ACCC denies that all customers transferred from the fourth respondent to the fifth respondent were transferred in compliance with the TCP Code;

(b) the ACCC states that: eCollect was engaged by the various Harrison Companies as an agent and, as such, those Harrison Companies were responsible for the acts and omissions of eCollect regardless of whether the Harrison Companies knew about them; further, extensive email and telephone communications took place between eCollect and Mr Harrison or various Harrison Companies evidencing a detailed knowledge of Mr Harrison and the various Harrison Companies of the proposed and executed debt collection activities of eCollect, including activities directed at collecting debts from customers after they had been transferred without their consent; further, the various Harrison Companies and Mr Harrison were provided with direct access to the eCollect database by eCollect, so that those Harrison Companies and Mr Harrison could directly input into the eCollect system debts purportedly owed and customer details, with the intention that there would be follow-up debt collection activities by eCollect as agent for the various Harrison Companies.

The hearing

16 At the outset of the hearing, a representative of the third and fourth respondents (which are in liquidation) appeared as a matter of courtesy and indicated that the third and fourth respondents did not propose to participate in the proceeding, but sought to be heard in due course if any orders were proposed to be made against the third and fourth respondents. On the basis that such opportunity would be afforded to them, the third and fourth respondents did not participate in the hearing.

17 The first, second and fifth to eleventh respondents were jointly represented by counsel and solicitors at the hearing.

18 The ACCC led evidence from the following witnesses:

(a) Mr Clements (a customer);

(b) Heidi Snell (the Director of the Victorian and Tasmanian branch of the ACCC’s Enforcement Division);

(c) Ms Bomford (a customer);

(d) Mr Phillips (a customer);

(e) Mr O’Neill (a customer);

(f) Ms Krepak (a customer);

(g) Ms Adams (a customer).

19 Each of the above witnesses prepared an affidavit. Ms Adams was not required to attend for cross-examination. The other witnesses were cross-examined by the respondents. Mr Clements, Mr O’Neill and Ms Krepak gave evidence by video-link.

20 During the course of the cross-examination of the customer witnesses, audio files were played which were recordings of conversations between staff working for a telemarketing company in India on behalf of the Harrison Companies and the customer. Generally speaking, the Harrison Company representatives spoke quickly and with an accent. The audio files were admitted into evidence. The parties prepared transcripts of the audio files, which were treated as forming part of the exhibits for the audio files.

21 The affidavit of Ms Snell annexed, among other things, a copy of the transcript of an examination of Mr Harrison pursuant to s 155 of the Competition and Consumer Act.

22 Mr Harrison reserved his position as to whether or not he would go into evidence until after the ACCC had closed its case. After the ACCC closed its case (on day two of the hearing), Mr Harrison indicated that he would go into evidence. The matter was adjourned for several days, during which Mr Harrison filed and served an affidavit. He was then cross-examined on day three of the hearing. The case proceeded on the basis that his evidence was also relied on by the second and fifth to eleventh respondents. No other witnesses were called by the respondents.

23 During the cross-examination of Mr Harrison, I gave him a certificate under s 128 of the Evidence Act 1995 (Cth) in relation to questions that he was asked and answers that he gave on the topics of customer transfers between different respondents and the reasons for those transfers. It was common ground that the evidence he gave could be used against him in this proceeding: see Cornell v The Queen (2007) 231 CLR 260 at [88] per Gleeson CJ, Gummow, Heydon and Crennan JJ.

24 I found all of the customer witnesses to be credible witnesses and generally accept their affidavit and oral evidence. In some cases, these witnesses accepted during cross-examination that their affidavit evidence needed to be modified, for example, after the audio file of a conversation was played. In such cases, the witness did not have the benefit of listening to the audio file when preparing the affidavit.

25 In relation to Mr Harrison’s evidence, I make the following general observations. I have doubts about the reliability of much of Mr Harrison’s evidence. The corporate behaviour of his companies (for example, in repeatedly not paying debts due to the TIO), which companies he closely controlled, does not instil confidence as to the reliability of his evidence. The evidence as a whole establishes that he adopted a cavalier attitude to legal and regulatory requirements. He made self-serving statements in his evidence which were unsupported by objective evidence such as contemporaneous documents. I am not inclined to accept such statements.

Factual findings

26 The following factual findings are based on the admissions in the Concise Response, the affidavit evidence and the oral evidence during the hearing.

General matters

27 Mr Harrison was born in Australia. He spent some time living in the United Kingdom. He returned to Australia in 2009 and has resided here since then. In 2010, Mr Harrison established a telecommunications business. In 2011, he established the third respondent.

28 At all material times, Mr Harrison was the sole director of each of the Harrison Companies. He was the Chief Executive Officer (CEO) of the companies which traded as Sure Telecom, and was (and is) the CEO of the companies which traded, or are now trading, as SoleNet. At all material times, he oversaw the operations of each of the Harrison Companies and supervised the staff of each of these companies. Mr Harrison was in charge of compliance for each of the Harrison Companies. Mr Harrison also carries on business as a sole trader under the name “HSS Consulting”. On the website for this business he offers one-on-one business training and describes himself as a seasoned professional in sales, systems, operations, investing and asset protection.

29 The Harrison Companies and relevant details are as follows:

Company name | Date registered | Date of winding up | |

Second Respondent | TELCOLLECT PTY LTD (ABN 82 147 481 758) | 22 November 2010 | |

Third Respondent | TELCO SERVICE HOLDINGS PTY LTD (FORMERLY SURE TELECOM PTY LTD) (IN LIQ) (ABN 79 150 231 155) | 4 April 2011 | 26 November 2014 |

Fourth Respondent: | SURE TELECOM PTY LTD (FORMERLY BP TECH CORP PTY LTD) (RECEIVERS AND MANAGERS APPOINTED) (IN LIQ) (ABN 40 166 698 415) | 11 November 2013 | 4 March 2015 |

Fifth Respondent: | COMMS SERVICE OPS PTY LTD (FORMERLY SOLENET PTY LTD) (ABN 22 601 833 925) | 15 September 2014 | |

Sixth Respondent: | SN OPERATIONS PTY LTD (ABN 74 606 419 121) | 15 June 2015 | |

Seventh Respondent: | SOLENET GROUP PTY LTD (ABN 68 607 137 628) | 17 July 2015 | |

Eighth Respondent: | TECH GROUP NSW PTY LTD (ABN 31 607 173 491) | 20 July 2015 | |

Ninth Respondent: | TECH GROUP QLD PTY LTD (ABN 22 607 173 893) | 20 July 2015 | |

Tenth Respondent: | TECH GROUP AUS PTY LTD (ABN 29 607 173 919) | 20 July 2015 | |

Eleventh Respondent: | TECH GROUP VIC PTY LTD (ABN 44 607 173 544) | 20 July 2015 |

30 The second respondent is a billing and management company; it received all payments on behalf of the other companies and paid all expenses on their behalf. The third to sixth and eighth to eleventh respondents carried on, or carry on, the business of supply of telecommunications services to residential customers and small businesses. The seventh respondent was created for the purpose of investment in private and publicly listed telecommunications businesses. As at July 2016, this company owned the trading name “SoleNet”. The eighth, ninth, tenth and eleventh respondents were at times referred to by the parties in their submissions as the Tech Group companies. The eighth, ninth and eleventh respondents supply services in the geographical areas indicated in their names, and the tenth respondent supplies services in the rest of Australia.

31 Initially, in about 2010, Mr Harrison obtained customers by door-knocking in the Parramatta area in Sydney. He did this himself. Subsequently, he engaged companies with staff in India to conduct telemarketing activities (also referred to as cold calling) on behalf of his companies. From about 2012 to November 2015, the Harrison Companies used Vishnu Solutions to carry out telemarketing. The Harrison Companies engaged a company in the Philippines to carry out some administrative tasks and a company in Sydney (Servcorp Ltd) to dispatch the Welcome Packs and contracts to new customers.

32 The Harrison Companies used four wholesalers from 2011 to 2016:

(a) ispONE Pty Ltd (ispONE), from about 2012 to 19 August 2013;

(b) iTelecom Wholesale Pty Ltd (iTelecom), from about 19 August 2013 to 29 August 2014;

(c) Wireline Pty Ltd (Wireline), from about 29 August 2014 to 4 June 2015;

(d) Telco in a Box, since about 4 June 2015.

33 At all material times, eCollect, a debt collection agency, acted on behalf of the Harrison Companies. eCollect maintained a database to manage its debt collection activities for each client. This was accessible by staff of the Harrison Companies through a login in Mr Harrison’s name. The policy of the Harrison Companies was to send files to eCollect after the account was 60 days in arrears. eCollect was contacted directly by the Philippines administration staff, who would enter the customer and debt details into the eCollect portal. The decision to send a file to eCollect was made either by the Philippines staff, following company practice, or by the accounts manager for the Harrison Companies. Harrison Company staff had authority to compromise debts up to 50% of their value without speaking with Mr Harrison. Mr Harrison accepted during cross-examination that he set up the debt collection policy for the Harrison Companies and that he engaged and gave the authority to eCollect to collect debts.

34 During the same period, EC Legal, a firm of solicitors, acted on behalf of the Harrison Companies.

35 It is admitted in the Concise Response, and I find, that there was no provision in the customer contracts to transfer customers to another entity.

36 The TIO was established by the Telecommunications (Consumer Protection and Service Standards) Act 1999 (Cth) to investigate, make determinations and give directions relating to complaints about telephone or internet services by end-users of those services. As an industry-funded ombudsman, the TIO imposes complaint charges on industry participants for consumer complaints it investigates.

37 ACMA is the independent statutory authority established by the Australian Communications and Media Authority Act 2005 (Cth) to regulate, among other things, telecommunications in accordance with the Telecommunications Act 1997 (Cth) and the Telecommunications (Consumer Protection and Service Standards) Act 1999 (Cth) and the TCP Code.

38 The TCP Code (as published in May 2012) contained a number of provisions of present relevance. The TCP Code was published by Communications Alliance Ltd, described in the document as a company formed in 1997 to provide a unified voice for the Australian communications industry. The introductory statement to the document noted that the code is a code of conduct designed to ensure good service and fair outcomes for all consumers of telecommunications products in Australia and that carriage service providers who supply telecommunications products to customers in Australia are required to observe and comply with the code. As noted in the introductory statement, the code was registered with ACMA which had powers of enforcement of the code. The parties proceeded on the basis that this version of the code was in place at all material times.

39 Clause 2.1 of the TCP Code contained the following definitions of present relevance:

Corporate Reorganisation

means a reorganisation of the corporate group of which the Supplier is a part with the result that a Customer will be provided with Telecommunications Services by another supplier after that reorganisation is complete.

…

Transfer

means the transfer of all or part of a Consumer’s Telecommunications Service from one Supplier to the Gaining Supplier.

40 Clause 6.10 of the TCP Code (headed “Debt collection”) provided in part:

Suppliers must ensure that their arrangements with debt collection agents include provisions which comply with the requirements of legislation, and debt collection codes and guidelines as determined from time to time by recognised bodies such as the ACCC and ASIC.

6.10.1 A supplier must take the following actions to enable this outcome:

…

(b) Collection activities: while ever it is in force, adopt best practice as set out in the ACCC guideline “Debt collection guideline for collectors and creditors: joint publication by ACCC and ASIC” issued in October 2005 when collecting amounts due;

41 Chapter 7 of the TCP Code dealt with changing suppliers. The summary at the commencement of the chapter stated:

Summary

This chapter sets out Consumer rights and Supplier obligations when Consumers seek to change their current Supplier of a Telecommunications Service to an alternative Supplier. It also sets out Suppliers’ obligations to Customers when a transfer of a Customer’s Telecommunications Service arises as a result of the sale of a Supplier’s business or a corporate reorganisation of the Supplier.

42 Clause 7.2 of the TCP Code provided:

Obtaining Consent

A Gaining Supplier must use reasonable endeavours to ensure that a Consumer is only the subject of a Transfer by a Gaining Supplier if the Consumer has provided their consent to such Transfer.

7.2.1 A Gaining Supplier must take the following steps to enable this outcome:

(a) Consent: the Gaining Supplier must ensure that the Consumer provides consent to the Transfer; and

(b) Authorisation: the Gaining Supplier must use its reasonable endeavours to ensure that person requesting the Transfer is the Rights Of Use Holder of the Telecommunications Service to be transferred, or is authorised to do so.

43 Clause 7.3 dealt with what constitutes consent. Clause 7.4 dealt with information to be provided regarding a transfer. Clause 7.6 dealt with keeping consumers informed of certain matters regarding a transfer. Clause 7.7 dealt with notification of completion of a transfer. Clause 7.9 dealt with access to records regarding a transfer.

44 Clause 7.11 of the TCP Code provided as follows:

Sale of Supplier’s Business or Supplier Reorganisation

If a Supplier proposes to Transfer a Customer’s Telecommunications Service as the result of a sale of the Supplier’s business or a Corporate Reorganisation, the Supplier must notify the Customer in writing prior to that Transfer being initiated. The Supplier must ensure that that Customer may terminate its Customer Contract for that Telecommunications Service within the period specified in this clause 7.11.

7.11.1 A Supplier must take the following actions to enable this outcome:

(a) Notification of Transfer: before the Transfer is initiated, notify the Customer in the manner in which the Supplier normally communicates with the Customer:

(i) that the Customer’s Telecommunications Service will be Transferred to the Gaining Supplier as a result of a sale of the Supplier’s business or a Corporation Reorganisation;

(ii) of any details then known to the Supplier regarding how the Customer’s Telecommunications Service may be the subject of a materially adverse effect regarding its features, characteristics or pricing as a result of the Transfer;

(iii) of any impact this change has on the Customer’s use of existing equipment;

(iv) of the contact details of the Gaining Supplier;

(v) of the proposed date by which the Transfer will be completed;

(vi) that the Supplier will use reasonable efforts to notify the Customer of the completion of the Transfer on the day it occurs;

(vii) of the appropriate contact details for lodging an inquiry or a Complaint about any aspect of the Transfer; and

(viii) of the applicable termination rights for that Customer that may result from the Transfer, including the applicable notice period and contract termination charges for that Customer.

(b) Termination by a Customer: ensure that, if so notified by the Customer who is exercising the applicable termination right, if any, as a result of a Transfer, the Supplier terminates the relevant Customer Contract relating to the Telecommunications Service within 5 Working Days of receiving the Customer’s notice.

7.11.2 Provided that a Supplier complies with the terms of this clause 7.11 in circumstances where a Transfer of a Customer’s Telecommunications Service arises as a result of a sale of the Supplier’s business or a Corporate Reorganisation, the Supplier is not required to comply with the other provisions of this Chapter in relation to such a Transfer except for clauses 7.6, 7.7 and 7.9.

45 It is convenient to note at this point that the TCP Code is not an “applicable industry code” for the purposes of s 22(1)(g) of the Australian Consumer Law, but is an “industry code” for the purposes of s 22(1)(h). The expression “industry code” is defined in s 2(1) of the Australian Consumer Law by reference to s 51ACA of the Competition and Consumer Act. It is there defined as a code regulating the conduct of participants in an industry towards other participants in the industry or towards consumers in the industry. The TCP Code falls within this definition.

December 2012

46 On 17 December 2012, Simon Holmes from the TIO sent an email to Mr Harrison attaching a copy of a letter which had been sent to him by registered post on 14 December 2012 from the TIO’s Industry Engagement Manager, Simon McKenzie. Mr Harrison sent an email in reply on 17 December 2012. The email was in the following terms:

Mr McKenzie must realise that if court action proceeds, then we do have a large case for losses caused by TIO and it will take 3 years to go through court as we will file a large defence and maybe a claim against the TIO for over $100,000 which we mean there will need to be a date set for the higher courts of which there are 18 month waiting lists to even hear a case and by that time Sure Telecom would have become a shell company and a different company would have taken the customers or the customer would have died off, you have no personal Guarantee from me.

Anyway this the above is hyperthetical as per Simons hyperthetical TIO Ltd may take us to court.

It doesn’t seem as though the TIO are willing to let me have a little time to look at the cases surrounding the alleged debt and to put my case across.

(Errors in original.)

August 2013 to December 2013 (including the first transfer)

47 On 19 August 2013, ispONE was placed into voluntary administration. On the same day, the third respondent switched wholesalers, to iTelecom. Between August 2013 and December 2013, there was a dispute between the third respondent and the administrator of ispONE about the amount owed by the third respondent. On Mr Harrison’s calculations, about $40,000 was owed. But the administrator was claiming in excess of $200,000. It seems that the administrator was relying on provisions in the contract to contend that the amount was owed, notwithstanding Mr Harrison’s contention that he had changed providers due to a breach of contract by ispONE.

48 On 4 October 2013, a default judgment was entered against the third respondent in the Magistrates’ Court of Victoria in a proceeding commenced by the TIO. The judgment amount was $50,649.

49 On 11 November 2013, Mr Harrison incorporated the fourth respondent. On the same day, Mr Harrison sent an email to eCollect asking for all payments to go into a new bank account, and providing the details.

50 On 22 November 2013, ACMA issued the third respondent with a preliminary investigation report relating to breaches of the TCP Code by the company.

51 During December 2013, the third respondent (trading as Sure Telecom) transferred its customer contracts to the fourth respondent (also trading as Sure Telecom).

52 Mr Harrison stated in his affidavit that the transfer of customers had nothing to do with the TIO or ACMA, and that it was entirely due to what he considered was the erratic, and wrong, position of ispONE and its administrators. Mr Harrison did not explain in his affidavit why the amount claimed by the TIO was not paid or why the third defendant allowed judgment in default to be entered against it. I do not accept that the actions of the TIO and ACMA formed no part of the reason for the transfer. The timing suggests that this is likely to have been, at least, a factor in the decision to transfer the contracts.

August 2014 to March 2015 (including the second transfer)

53 On 26 August 2014, the fourth respondent received a demand from the TIO for $3,974.

54 By about August 2014, the fourth respondent’s relationship with the wholesaler, iTelecom, had broken down. On 29 August 2014, Mr Harrison caused the fourth respondent to switch wholesalers from iTelecom to Wireline.

55 On 4 September 2014, Mr Harrison sent an email to iTelecom setting out his complaints, including about $200,000 in disputed charges.

56 On 10 September 2014, ACMA issued the fourth respondent with a direction to comply with the TCP Code after ACMA found that it had breached 19 separate clauses of the code.

57 On the same day, iTelecom responded to Mr Harrison’s email and demanded payment of $146,946. They also appointed receivers and managers to the fourth respondent. Mr Harrison considered these to be invalid appointments, because the dispute had not first been referred to arbitration.

58 On 15 September 2014, Mr Harrison incorporated the fifth respondent. On the same day, Mr Harrison provided new bank account details to eCollect.

59 During September 2014, the fourth respondent (trading as Sure Telecom) transferred its customer contracts to the fifth respondent (which commenced trading as SoleNet). 1,895 customers were transferred. The invoice documentation before and after the transfer was similar. The format was the same, but the trading names were different and the colours (at least of the logos, but possibly of the invoices generally) were different (Sure Telecom was orange and black and SoleNet is bright purple and black). (The copies of the invoices in evidence were black and white, but Mr Harrison gave evidence, which I accept, about the colours.)

60 Mr Harrison stated in his affidavit that his reason for the transfer was that he was concerned that any Sure Telecom customers would be caught up in the dispute with iTelecom; and that it had nothing to do with the TIO or ACMA. I do not accept that the actions of the TIO and ACMA formed no part of the reason for the transfer. Again, the timing suggests that the actions of the TIO and ACMA are likely to have been, at least, a factor in the decision to transfer the contracts.

61 On 26 September 2014, Mr Harrison sent a letter to eCollect. It is to be inferred that eCollect had received a request from the receivers and managers of the fourth respondent to pay moneys received to them. The gist of Mr Harrison’s letter was to insist that all moneys collected be paid to the second respondent (being the billing company) rather than to the receivers and managers of the fourth respondent.

62 On 14 November 2014, a default judgment was entered in the Magistrates’ Court of Victoria against the fourth respondent in a claim brought by the TIO. The amount was $4,990.

63 On 21 January 2015, the TIO brought an application to wind up the fourth respondent in the Supreme Court of Victoria, on the basis of failure to comply with a statutory demand dated 2 December 2014.

64 On 4 March 2015, the fourth respondent was wound up.

April 2015 to June 2015 (including the third transfer)

65 In about April-May 2015, Mr Harrison was becoming increasingly concerned with the levels of service provided by the wholesaler, Wireline, and complained in writing about billing errors. Wireline did not accept his position in relation to these complaints.

66 On 9 April 2015, ACMA gave the fifth respondent a direction to comply with the TCP Code. ACMA found that the company had contravened several clauses of the code.

67 On 4 June 2015, Mr Harrison received an email from Wireline, demanding payment of $50,000. On the same day, Mr Harrison signed a contract with a new wholesaler, Telco in a Box. That evening, Wireline disconnected about 150 SoleNet customers due to its dispute with the fifth respondent. These customers were lost to SoleNet.

68 On 10 June 2015, a default judgment was entered against the fifth respondent in the Magistrates’ Court of Victoria. The proceeding had been brought by the TIO. The amount of the judgment was $11,917.

69 On 15 June 2015, Mr Harrison registered the sixth respondent.

70 In June 2015, the fifth respondent transferred its customer contracts to the sixth respondent. Both traded as SoleNet. The invoice documentation was in substantially the same form before and after the transfer.

71 Mr Harrison stated in his affidavit that the transfer was due to the actions of Wireline; and that he was concerned that Wireline might take some other action (cancelling the customer connections or speculative court action to try to recover the clients). However, the further actions of the TIO and ACMA (see [66] and [68] above) are likely to have been, at least, a factor in the decision to transfer the contracts.

July 2015 (including the fourth transfer)

72 In July 2015, the sixth respondent purported to transfer its customer contracts to State-based companies, namely the eighth, ninth, tenth and eleventh respondents. All of these companies traded as SoleNet. The invoice documentation was in substantially the same form before and after the transfer.

73 Mr Harrison stated in his affidavit that the “initial reason” for these transfers was the “extreme behaviour of Wireline”. However, the further actions by the TIO and ACMA suggest that these actions are likely to have been, at least, a factor in the decision to transfer the contracts.

74 Mr Harrison also stated in his affidavit that these customers were transferred on a geographical basis, as he had decided that it might be possible in the future to sell the client base on a State-by-State basis; and he considered there were potential tax, sale and accounting benefits in having the companies structured like this, which was primarily why the structure was adopted. I do not take this evidence to be an explanation of why the fourth transfer occurred, but merely why it involved transferring the assets and customer contracts to four companies rather than one.

December 2015 to June 2016

75 On 29 December 2015, Mr Harrison incorporated a company called JRD Investments Ltd, which has a registered address in the Cook Islands. On 14 January 2016, he applied on behalf of this company to open a bank account with Bank of Saint Lucia International Limited.

76 In February 2016, the TIO commenced proceedings in the Magistrates’ Court of Victoria against each of the fifth, eighth, ninth, tenth and eleventh respondents for unpaid complaint charges.

77 On 29 February 2016, Mr Harrison sent an email to eCollect requesting them to “please pay the larger account payment to the following business account” and providing details of an account in the name of JRD Investment Ltd with Bank of Saint Lucia. Shortly after this, the ACCC applied in proceeding VID 220/2016 for ‘freezing orders’ and the Court made such orders. Mr Harrison stated in his affidavit that the payment to Bank of Saint Lucia was a “one-off” payment to fund a proposed new venture. It is unnecessary to make a finding about this.

78 As at 16 March 2016, there were approximately 1,400 retail customers with the Harrison Companies. In his affidavit dated 25 July 2016, Mr Harrison stated that at that time his companies had about 1,600 active services for customers.

79 As at 27 June 2016, the status of TIO recovery actions in relation to the Harrison Companies for unpaid complaint charges was as follows:

(a) In relation to the fifth respondent, the TIO commenced a proceeding in the Magistrates’ Court of Victoria on 12 February 2016 seeking payment of $7,552 plus interest and costs. Judgment was entered by consent in the sum of $8,000 on about 29 April 2016. The TIO sought compliance with the judgment on 6 June 2016 but the company did not comply. As at 27 June 2016, the TIO intended to enforce the judgment including by taking winding up action.

(b) In relation to the eighth respondent, proceedings were commenced in the Magistrates’ Court of Victoria on 8 February 2016 seeking payment of $7,719 plus interest and costs. Judgment was obtained in default of a defence in the sum of $9,070. The TIO sought payment of the judgment amount by 16 March 2016. No payment was received. As at 27 June 2016, the TIO intended to enforce the judgment, including by taking winding up action. In addition, a solicitor’s demand had been sent for $1,929 owing pursuant to the TIO’s January invoice. No reply or payment had been received and recovery action was being considered. A further solicitor’s demand was sent on 10 March 2016 for $1,776 owing pursuant to the TIO’s February invoice and recovery action was being considered.

(c) In relation to the ninth respondent, proceedings were commenced in the Magistrates’ Court of Victoria on 8 February 2016 seeking payment of $1,872 plus interest and costs. Judgment was obtained in default of a defence in the sum of $2,902. The TIO sought payment of the judgment amount by 16 March 2016. No payment was received. As at 27 June 2016, the TIO intended to enforce the judgment, including by taking winding up action. In addition, a solicitor’s demand had been issued in respect of $143 owing pursuant to the TIO’s January invoice. No reply or payment had been received and recovery action was being considered.

(d) In relation to the tenth respondent, proceedings were commenced in the Magistrates’ Court of Victoria on 9 February 2016 seeking payment of $3,190 plus interest and costs. Those proceedings were initially defended. Subsequently, the Court made orders striking out the company’s defence and entering judgment in default of appearance. The TIO sought compliance with the judgment by 25 May 2016. No payment was received. As at 27 June 2016, the TIO intended to enforce the judgment, including by taking winding up action. In addition, a solicitor’s demand had been sent in respect of $2,330 owing pursuant to the TIO’s January invoice. No reply or payment had been received and recovery action was being considered. Also, $285 was overdue pursuant to the TIO’s February invoice.

(e) In relation to the eleventh respondent, proceedings were commenced in the Magistrates’ Court of Victoria by the TIO on 8 February 2016 seeking payment of $3,102 plus interest and costs. Judgment was obtained in default of a defence in the sum of $4,051. The TIO sought payment of the judgment amount by 16 March 2016. No payment was received. As at 27 June 2016, the TIO intended to enforce the judgment, including by taking winding up action. In addition, a solicitor’s demand had been sent in respect of $718 owing pursuant to the TIO’s January invoice; no reply or payment had been received and recovery action was being considered. A further solicitor’s demand had been sent in respect of $2,205 owing and unpaid pursuant to the TIO’s February invoice and recovery action was being considered.

The entire period

80 One of the factual issues in dispute is whether or not the Harrison Companies sent notifications of the transfers to customers. The ACCC in its Concise Statement alleged that Mr Harrison purported to transfer the customers’ contracts from one Harrison Company to another without the customer’s knowledge. In the Concise Response, the respondents contended that all customers were given notice of the transfers. The ACCC, in its Concise Reply, stated that that contention was “not admitted”.

81 Of the six customers who gave evidence, five gave evidence to the effect that they did not recall being notified of the transfer. There was no cross-examination on this issue. Mr Harrison’s affidavit evidence in relation to the notification issue was as follows:

(a) In the part of Mr Harrison’s affidavit dealing with the first transfer (December 2013), Mr Harrison did not refer to customers being notified.

(b) In relation to the second transfer (September 2014), Mr Harrison stated: “All customers were notified of the transfer from Sure Telecom to SoleNet”. He stated that annexure “JH-10” was a copy of the notification. That annexure is a standard form letter on Sure Telecom letterhead in the following terms:

13th September 2014

FIRST NAME LAST NAME

STREET ADDRESS

SUBURB

STATE POSTCODE

Dear FIRST NAME

RE: Transfer of your account

Thank you for your custom, we appreciate the opportunity that we have had to support your services. Please be advised that your service will now be transferred to SoleNet Pty Ltd due to an agreement with SoleNet to continue the supply your contract. Your service and pricing will remain as agreed and there will be no service disruption or equipment change required.

If you wish to speak with SoleNet regarding the move, please contact them on 1300 660 196 or email support@solenet.com.au. The transfer will be completed with the next 10 Business Days and we will notify you if we are unable to transfer your service for any reason. You may terminate your contract in accordance with the terms and conditions of your agreements by notifying SoleNet.

James Harrison

Director

Sure Telecom

(c) In relation to the third transfer (June 2015), Mr Harrison stated that he “did notify the customers of this transfer”.

(d) After dealing with the fourth transfer (July 2015), Mr Harrison made some general comments regarding notifications to customers. These appear under the heading “Notifications to customers” and appear to relate to all four transfers. He stated:

92. … At the time of the transfers all customers were advised in writing and a notice was placed on the website. Copies of these notices are attached and marked “JH17. Attached is a copy of the letters sent to customers for the transfer from Sure Telecom to Solenet and the transfer from Solenet to the various Techgroup companies. I cannot locate the notice for the transfer from Sure Telecom to BP Tech Corp as data in Sure Telecom was lost when the administrators were appointed. To the best of my recollection the notice from Sure Telecom Pty Ltd to BP Tech Corp Pty Ltd was in a similar format to the attached notices.

93. In addition, where contact details existed, an email and SMS message about the transfers was sent. I no longer have access to the Sure Telecom SMS system.

(e) Annexure “JH17” comprises a standard form letter and a notice. The letter is the same as “JH10” (set out above). The notice is as follows:

SoleNet Pty Ltd assets were purchased by SN Operations Pty Ltd at which time SN Operations Pty Ltd began a Corporate Restructure.

Tech Group NSW Pty Ltd t/a SoleNet now own and operate customer contracts in the state of New South Wales and Australian Capital Territory.

Tech Group VIC Pty Ltd t/a SoleNet now own and operate customer contracts in the state of Victoria.

Tech Group QLD Pty Ltd t/a Sole Net now own and operate customer contracts in the state of Queensland.

Tech Group AUS t/a SoleNet now own and operate customer contracts in the state and territory of Western Australia, South Australia, Northern Territory and Tasmania.

All customer services and plan pricing and terms will remain as per the agreed contract terms of service and there will be no disruption to your services or required equipment.

All Contract Details and Payment Methods will remain the same, there will be no change in the way you communicate with SoleNet.

OUR Contact Details

PH. 1300 660 196

FAX 02 8458 6105

EMAIL support@solenet.com.au

ADDRESS: Level 32, 1 Market Street, Sydney, NSW 2000

We thank you for your continued support and we will continually produce innovative products and services and seek more ways to communicate with customers better and provide a more proactive customer service approach.

James Harrison

CEO

SoleNet

82 Mr Harrison’s affidavit does not provide any details of the process by which a letter or notice was sent to customers in relation to any of the transfers. The only transfer in respect of which a form of letter has been produced is the second transfer. But even in respect of this transfer, there is no detailed evidence about the process by which the letter was sent out, and no documentary evidence to verify that such letters were sent. As for the statement that, where contact details existed, an email and SMS message were also sent, no detailed evidence has been provided as to the process by which this occurred, and no documentary evidence has been provided to verify that this occurred. Mr Harrison was cross-examined on the topic of whether notifications were sent to customers in respect of the transfers. It was put to him several times that no notifications were sent. He maintained that notifications were sent. However, he did not (whether in cross-examination or re-examination) explain the process by which letters were sent to customers or produce any documentary evidence to support his evidence that this occurred. One would ordinarily expect there to be at least some documents verifying that this occurred, particularly as the Harrison Companies outsourced many administrative functions (for example, Servcorp in Sydney mailed out the Welcome Packs). But, apart from “JH10” and “JH17”, no documents have been produced. In relation to emails, no copy has been produced of emails sent to customers. In relation to SMS messages, no copy has been produced of SMS messages sent to customers. Mr Harrison stated in his affidavit that he no longer has access to the Sure Telecom SMS system, but did not refer to the SoleNet SMS message system. Mr Harrison said during cross-examination that the emails were on the server of a staff member in the Philippines who used to work for him, but did not explain why he could not obtain copies from other sources (for example, customers).

83 In closing submissions, the respondents submitted that: it was never put to Mr Harrison during his section 155 examination that the notifications were a fiction; at no time before Mr Harrison’s cross-examination had the ACCC alleged that Mr Harrison’s evidence during that examination was a fiction; despite the notifications being squarely raised in the Concise Response, the ACCC did not allege that the notification documents were a fraud in its Concise Reply – it was required to do so; and none of the ACCC’s witnesses gave evidence to the effect that his or her recollection supported the ACCC’s contentions.

84 Insofar as the respondents submit that the ACCC did not put to Mr Harrison during the section 155 examination that notifications were not sent, I do not accept that this precludes the ACCC from so contending during the proceeding (provided proper notice is given). The section 155 examination forms part of the investigatory phase. The fact that a certain matter was not put to a witness during the examination does not in itself preclude the ACCC putting the matter to the witness at trial. I do not think it was incumbent on the ACCC to allege fraud in its Concise Statement or Concise Reply because that is not the submission it makes in closing submissions. The ACCC’s submission is that notifications were not sent to customers. Acceptance of that proposition does not necessarily carry with it that the documents at “JH10” and “JH17” are fraudulent. The standard form letter at “JH10” may be a genuine document, prepared at the time, but not sent. The notice forming the second part of “JH17” may be a genuine document that was placed on the website but not mailed to customers. Thus it was not incumbent on the ACCC to allege fraud in order to contend that notifications were not sent. I do not accept the contention that the recollections of the customers who gave evidence did not support the contention that notifications were not sent to customers. Five out of six gave evidence to the effect that they did not recall being notified of the transfer (see [94](g), [96](g), [98](o), [102](k), [104](m)). And the other customer’s evidence was silent on the matter. Further, the issue of whether notifications were sent to customers in relation to the transfers was squarely raised. The Concise Statement included the allegation that Mr Harrison purported to transfer customer contracts from one Harrison Company to another without the customer’s knowledge; the respondents themselves contended in the Concise Response that notifications were sent; and that contention was “not admitted” in the Concise Reply.

85 In light of the matters referred to above, I do not accept Mr Harrison’s evidence that letters or notices were sent by mail to customers in respect of the transfers. Although Mr Harrison stated in his affidavit that this occurred, and maintained this position during cross-examination, I do not accept this in light of: the evidence of five of the customer witnesses to the effect that they did not recall being notified of the transfer (and the absence of any cross-examination on this matter); the general lack of reliability of Mr Harrison’s evidence; the absence of documentary evidence other than “JH10” and “JH17” which supports that letters or notices were sent by mail to customers in circumstances where one would ordinarily expect such evidence to exist; and the absence of detailed evidence as to the process by which such letters/notices were sent.

86 Further, I do not accept Mr Harrison’s evidence that, in addition, where contact details existed, an email and an SMS message were sent to customers in respect of the transfers. Although Mr Harrison stated in his affidavit that this occurred, and maintained this position during cross-examination, I do not accept this in light of: the evidence of five of the customer witnesses to the effect that they did not recall being notified of the transfer (and the absence of any cross-examination on this matter); the general lack of reliability of Mr Harrison’s evidence; the absence of copies of any such email or SMS message (with only a partial explanation for the failure to adduce such evidence); and the absence of detailed evidence as to the process by which such emails and messages were sent.

87 I acknowledge that, in other circumstances, it might be thought to be improbable that a company would transfer contracts with its customers to another company and not even send a notification to customers that it was doing so. However, in circumstances where, as the evidence generally establishes, the Harrison Companies often failed to conduct themselves in accordance with normal standards of commercial behaviour (for example, repeatedly failing to pay debts due to the TIO), it does not strike me as implausible that they did not send notifications of the transfers to customers.

88 Accordingly, I am satisfied that the Harrison Companies did not send notifications of any of the transfers to customers.

89 Turning to the question of consent, the evidence is clear that the Harrison Companies did not seek or obtain the express consent of customers to the transfer of the customer’s contract.

90 A further issue, which it is convenient to deal with at this stage, is Mr Harrison’s belief as to the validity and propriety of the transfers. (Later in these reasons I consider the validity of the transfers and their compliance with the TCP Code and conclude that they were not valid and that they did not comply with the Code.) Mr Harrison stated in his affidavit that it was his belief at the time that the transfers were legitimate and valid and complied with the TCP Code. He stated that he does not have a legal background and was relying on his interpretation of the Code. He did not, however, set out in any detail his reasoning process for coming to these views. Mr Harrison’s evidence during cross-examination was to the same effect.

91 I do not accept that evidence. I think it likely that Mr Harrison knew that notifications had not been sent to customers and therefore that the transfers were not valid. (Mr Harrison’s evidence that he believed that the transfers were valid was premised on notifications having been sent.) Given Mr Harrison’s close control of each of the Harrison Companies, it is likely that he knew whether or not notifications were sent. Further, given that (as is admitted) there was no provision in the customer contracts to transfer customers to another entity, and the likelihood that Mr Harrison was aware of this, it is likely that he knew that customer consent was required in order to transfer the contracts. Yet, as Mr Harrison well knew, customer consent was not sought or obtained. In light of these matters, I am satisfied that Mr Harrison knew that the transfers were not valid and effective.

92 Further, I think it likely that Mr Harrison knew that the transfers did not comply with the TCP Code. Mr Harrison did not produce any contemporaneous documentation to support his evidence that he believed at the time that the transfers complied with the TCP Code. Nor did he explain in any detail the reasoning process by which he formed this view at the time. Mr Harrison gave evidence (which I accept) that he was familiar with the TCP Code. The straightforward way to read ch 7 of the Code is that a Gaining Supplier must use reasonable endeavours to ensure that a consumer is only the subject of a transfer if the consumer has provided his or her consent to the transfer (clause 7.2, set out in [42] above). Mr Harrison was well aware that no steps had been taken to seek or obtain the consent of customers to the transfers. During cross-examination Mr Harrison made a number of references to corporate reorganisation and in closing submissions counsel for the respondents presented an argument that the transfers constituted a “corporate reorganisation” within the meaning of the TCP Code and therefore it was sufficient to comply with clause 7.11 of the Code (set out in [44] above). That clause requires that the customer be notified of a series of matters before the transfer is initiated. There is no contemporaneous documentation to show an attempt to comply with the notification requirements of clause 7.11. Nor is there any contemporaneous documentation to support the proposition that Mr Harrison believed at the time that the transfers complied with the TCP Code on the basis that they constituted a “corporate reorganisation”. In light of these matters, I am satisfied that Mr Harrison knew that the transfers did not comply with the TCP Code.

93 Information in the eCollect database for the Harrison Companies indicates that between June 2011 and March 2016:

(a) eCollect sought to recover debts on behalf of the Harrison Companies from approximately 2,400 customers;

(b) the total value of debts pursued was approximately $2.4 million;

(c) approximately 540 customers paid the debt in full or paid an agreed lesser amount in satisfaction of the debt;

(d) over $400,000 was recovered from customers by eCollect;

(e) at least 100 of the customers pursued were customers who had been subjected to transfers the value of whose debts amounted to more than $100,000.

Ms Adams and Sure Telecom/SoleNet (March 2014 to April 2015)

94 Ms Adams gave evidence by way of an affidavit and was not cross-examined. I accept her evidence. On the basis of her affidavit, I make the following findings:

(a) Ms Adams is a pensioner. Before turning 65 years old, and commencing to receive the aged pension, she received a disability pension for several years. Her physical disability requires her to permanently use a wheelchair and it is essential for her to have a reliable and affordable landline telephone service to access healthcare and support services.

(b) In late March 2014, Ms Adams received a telephone call from a man with an Indian accent. The man said words to the following effect: “You’re a long term Telstra customer and a pensioner; we’re offering you a special, cheaper deal of just $29 per month. Your bill will be so much cheaper with us.” The man told her that she would also have to pay 20 cents for each local call she made. Because of the statements made by the man (that Ms Adams was a long term Telstra customer and a pensioner), Ms Adams believed that the company the man was phoning from was affiliated with, or a subsidiary of, Telstra. Based on what the man said, Ms Adams thought the $29 a month plan was cheaper than her existing plan for her home landline phone and so she agreed to transfer her landline phone service to the company. She also agreed to the company direct debiting her bank account for payment of monthly invoices.

(c) In early April 2014, Ms Adams received in the post at her home address a Sure Telecom Welcome Pack. The Welcome Pack included a covering letter thanking Ms Adams for becoming a customer of Sure Telecom, a receipt for $69.00, comprising a $20.00 connection fee, a $20.00 security deposit and a $29.00 product plan fee, and a contract with Sure Telecom. The company details on the Welcome Pack (ABN ending 415) indicate that it was issued by the fourth respondent.

(d) Ms Adams received invoices from Sure Telecom for the months of May 2014, June 2014 and July 2014. She has been unable to locate these. They were paid by direct debit.

(e) In early August 2014, Ms Adams received an invoice from Sure Telecom. This was dated 4 August 2014 and was for the amount of $91.33. Ms Adams was surprised and annoyed at the very high amount of this invoice. She had made relatively few landline phone calls during July 2014 and thought her bill from Sure Telecom should not have been much over the standard monthly plan amount of $29. After she received the August 2014 invoice she phoned Sure Telecom on the phone number stated near the bottom of the invoice under “Contact Details” and spoke to a man. They had a conversation to the following effect. Ms Adams introduced herself and said: “I’m phoning to complain about the very high bill I’ve just received from your company for $91.33. I don’t make many landline calls so how possibly could I receive a bill as high as this?” The man said: “Oh yes, we’ve had some complaints about doubling-up on this month’s bills. Sorry, there’s been a glitch and they have been doubled-up.” Ms Adams said: “They haven’t been doubled-up, they’ve been tripled-up.” He said: “Oh, oh, don’t worry, we’ll make sure that it’s fixed up for next month.”

(f) In early September 2014, Ms Adams received an invoice from Sure Telecom. This was dated 4 September 2014 and was for the amount of $18.36. The low amount of the invoice reflected the adjustment promised to Ms Adams by the Sure Telecom representative when she phoned Sure Telecom in early August 2014 to complain about the high amount of the August 2014 invoice.

(g) In early October 2014, Ms Adams received an invoice from SoleNet. This was dated 4 October 2014 and was for the amount of $47.95. The company details (ABN ending 925) indicate that it was issued by the fifth respondent. Ms Adams was confused and worried because she did not know who SoleNet was. She got other bills out that she had received from Sure Telecom and saw that the address details on the SoleNet invoice were the same. Shortly after receiving the October 2014 invoice, she phoned SoleNet and complained about receiving a bill from them. She had a conversation to the following effect with a man from SoleNet. Ms Adams introduced herself and said: “I was a customer of Sure Telecom. I’ve just got a bill from another company called SoleNet. What’s going on? Why am I getting a bill from this company when I am a customer of Sure Telecom?” The man said: “It’s the same company, it has just changed name.” Ms Adams said: “You just can’t do this without telling your customers. You have to let people know. It’s not good practice, it’s not on.” Ms Adams stated in her affidavit that she did not remember Sure Telecom or SoleNet asking for her permission to change provider; and she did not agree to it.

(h) In early November 2014, Ms Adams received a bill from SoleNet. This was dated 4 November 2014 and for the amount of $66.11. The company details (ABN ending 925) indicate that it was issued by the fifth respondent. Given that she was on a $29 monthly plan and did not make many landline calls, Ms Adams was again concerned at the high amount she was being charged on her monthly bill and phoned SoleNet to complain about it. She said to a man at SoleNet, words to the effect: “Why are you doing these things to me? I just don’t understand. You haven’t kept any of your promises”, referring to the statements made in late March 2014 that if she changed to Sure Telecom she would only have to pay Sure Telecom $29 a month plus 20 cents for each of the landline calls she made, and that Sure Telecom would be cheaper than what she was being charged at the time by Telstra. Ms Adams did not receive a satisfactory explanation. Ms Adams considered the representative to be very condescending. He talked over her and said that the charges were in line with the contract and monthly plan.

(i) In early December 2014, Ms Adams received an invoice from SoleNet. This was dated 4 December 2014 and was for the amount of $73.49. The company details (ABN ending 925) indicate that it was issued by the fifth respondent. Shortly after she received the December 2014 invoice, Ms Adams phoned SoleNet again to complain about the high amount she was being charged on her monthly bill. As with the previous month, Ms Adams did not receive a satisfactory explanation, other than that the charges were in line with the contract and the plan she was on with SoleNet. Ms Adams said to the man at SoleNet, words to the effect: “For heaven’s sakes, this is ridiculous. I’m sick and tired of these issues”, referring to Sure Telecom/SoleNet continually breaking their promises to her and charging her far more than the promised $29 a month for her landline service plus 20 cents for each local call that she made. After receiving the December 2014 invoice, Ms Adams started to seriously think about cancelling her contract, as she was fed up with continually receiving high bills from Sure Telecom/SoleNet, and their broken promise that she would save money if she transferred from Telstra. She was also very dissatisfied with the poor service that she received from Sure Telecom/SoleNet when she phoned them to complain about the high bills.

(j) In early January 2015, Ms Adams received an invoice from SoleNet. This was dated 4 January 2015 and was for the amount of $60.86. The company details (ABN ending 925) indicate that it was issued by the fifth respondent.

(k) In early February 2015, Ms Adams received another invoice from SoleNet. This was dated 4 February 2015 and was for the amount of $60.79. The company details (ABN ending 925) indicate that it was issued by the fifth respondent. After receiving this invoice, Ms Adams decided to cancel her contract.

(l) On or about 11 February 2015, Ms Adams phoned Bankwest about cancelling her authority for SoleNet to direct debit her account. Bankwest suggested that she visit their nearby local branch to arrange this. On or about the same day, she visited her local branch and instructed Bankwest to immediately cancel her authority for Sure Telecom/SoleNet to direct debit her account. The final date for the direct debit for Sure Telecom/SoleNet was 11 February 2015.

(m) On or about 11 February 2015, Ms Adams also phoned Telstra about transferring her landline phone service back to Telstra. Telstra transferred her landline phone service back to them on 12 February 2015.

(n) On 26 February 2015, Ms Adams paid the amount owed on the February 2015 invoice at an Australia Post office.

(o) In mid to late February 2015, after Ms Adams had transferred her landline phone service back to Telstra, she received a phone call from a man at SoleNet regarding having transferred from SoleNet. They had a conversation to the following effect. The man said: “You’ve broken your 24 month contract with us. Under your contract you are now liable to pay SoleNet early termination fees. If you don’t, we’ll refer it to our debt collector.” Ms Adams said: “Me, broke my contract, you must be kidding me, you’ve broken every promise to me. I’m a pensioner mate. I won’t be paying it. You can do whatever you want. You can’t get blood out of a stone. I don’t owe your company anything because you haven’t kept your side of the contract. I was promised savings if I transferred to Sure Telecom and only having to pay a monthly plan of $29 plus the cost of 20 cents for each local call. I never made many landline calls and yet you’ve continually charged me a lot more than what I paid Telstra and broken all your promises to me.” The man said: “You’ve broken your contract and you have to pay early termination fees.”

(p) In early March 2015, Ms Adams received an invoice from SoleNet. This was dated 4 March 2015 and for the amount of $473.49 and stated that the due date for payment was 18 March 2015. The amount claimed was $473.49. The company details (ABN ending 925) indicate that it was issued by the fifth respondent.

(q) As Ms Adams had transferred her landline phone service back to Telstra on 12 February 2015 and had paid the February 2015 SoleNet invoice, and based on what the man had said, she assumed that the $473.49 was an early termination fee. She did not pay the March 2015 invoice.

(r) In mid-March 2015, Ms Adams received a letter dated 12 March 2015 from SoleNet headed “SoleNet Collection Referral Notice”. This notice referred to “Overdue Amount - $859.90”. The company details (ABN ending 925) indicate that it was issued by the fifth respondent. Ms Adams stated in her affidavit (and I accept) that, as she is a disability pensioner with very limited income, she felt threatened, nervous and scared about SoleNet’s demand that she pay them $859.90, which she could not afford to pay. Shortly after receiving the March 2015 SoleNet Collection Referral Notice, she phoned SoleNet and spoke to a man. They had a conversation to the following effect. Ms Adams introduced herself and said: “I received your letter demanding that I pay SoleNet $859.90. I’m not paying this. I owe you nothing. You’ve broken every promise to me.” The man said: “You owe this. You’ve broken your 24 month contract, and we’ll pursue you if you don’t pay.” Ms Adams said: “No, you broke the contract, you’ve never kept the contract, you’ve never given me the promised service.” The man said: “We’ll be pursuing it.” Ms Adams said: “Go for it. Go for it.” Mr Harrison accepted during cross-examination that the $859.90 amount was incorrect and was not due. He said that the Philippines staff had used the wrong template and had entered the wrong amount (being the amount for another customer) and that this was an administrative error. He did not explain, however, why the correct information was not available to the representative with whom Ms Adams spoke and therefore why that representative maintained, incorrectly, that $859.90 was due.