FEDERAL COURT OF AUSTRALIA

Mentha, in the matter of Arrium Limited (administrators appointed) [2016] FCA 1300

File number: | VID 1260 of 2016 |

Judge: | DAVIES J |

Date of judgment: | |

Catchwords: | BANKRUPTCY AND INSOLVENCY – administration – orders pursuant to s 447A of the Corporations Act 2001 (Cth) – whether appropriate to make orders modifying the operation of Part 5.3A in respect of concurrent meetings of creditors – whether appropriate to make orders modifying the operation of Part 5.3A in respect of report to creditors – whether appropriate to make direction that administrators are justified in providing an aggregated report to creditors |

Legislation: | Corporations Act 2001 (Cth), ss 439A, 447A, 447D |

Cases cited: | Australian Workers’ Union v Arrium Limited (Administrators Appointed), in the matter of Arrium Limited (Administrators Appointed) [2016] FCA 381 Re Green (as voluntary administrators of Bevillesta Pty Ltd) [2011] NSWSC 417; (2011) 84 ALR 215 |

Date of hearing: | 25 October 2016 |

Registry: | Victoria |

Division: | General Division |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Category: | Catchwords |

Number of paragraphs: | |

Solicitor for the Plaintiffs: | Arnold Bloch Leibler |

Counsel for the Australian Securities and Investments Commission: | J P Moore QC with O Bigos |

Solicitor for the Australian Securities and Investments Commission: | Australian Securities and Investments Commission |

Counsel for the Australian Workers’ Union: | K Farouque of Maurice Blackburn |

ORDERS

JUDGE: | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to section 447A(1) of the Corporations Act 2001 (Cth) (the Act), Part 5.3A of the Act is to operate in relation to each of the Second Plaintiffs (the Arrium Administration Group Companies) as if it provided that at the concurrent meetings of creditors of the Arrium Administration Group held pursuant to section 439A of the Act or at any subsequent meetings of the creditors of the Arrium Administration Group Companies, each employee of any of the Arrium Administration Group Companies who is a member of one of the following Unions:

(a) Australian Workers’ Union (AWU);

(b) Australian Manufacturing Workers’ Union (AMWU);

(c) Communications Electrical Electric Electronic Energy Information Postal Plumbing and Allied Services Union of Australia (CEPU);

(d) National Union of Workers (NUW);

(e) Construction Forestry Mining and Energy Union (CFMEU); or

(f) Professionals Australia,

had duly appointed:

(g) in the case of the AWU, Mr Scott McDine or Mr Daniel Walton;

(h) in the case of the AMWU, Mr Glenn Thompson;

(i) in the case of the CEPU, Mr Matthew Murphy or Mr John Adley;

(j) in the case of the NUW, Ms Monique Segan or Mr Paul Richardson;

(k) in the case of the CFMEU, Mr David Noonan; and

(l) in the case of Professionals Australia, Ms Sarah Andrews,

to be her or his attorney pursuant to Regulation 5.6.31A for the purpose of those meetings save for:

(m) any employee who attends any meeting in person; and

(n) any employee who signs a proxy appointing some other person to attend any meeting on his or her behalf.

2. Pursuant to section 447A of the Act, Part 5.3A of the Act is to operate in relation to each of the Arrium Administration Group Companies as if section 439A(4) of the Act is modified to read as follows:

“(4) [Form of notice to creditor] The notice given to a creditor under paragraph 3(a), as modified by the Orders of the Federal Court of Australia made on 10 May 2016, must be accompanied by a copy of:

(a) a single report prepared on an aggregated basis by the Administrators about the Arrium Administration Group’s businesses, property, affairs and financial circumstances; and

(b) a statement setting out the administrators’ opinion about each of the following matters:

(i) whether it would be in the creditors' interests for the Arrium Administration Group Companies to execute cross-conditioned deeds of company arrangement;

(ii) whether it would be in the creditors' interests for the Arrium Administration Group Companies’ administrations to end;

(iii) whether it would be in the creditors' interests for the Arrium Administration Group Companies to be wound up;

and also setting out:

(iv) his or her reasons for those opinions; and

(v) such other information known to the administrators as will enable the creditors to make an informed decision about each matter covered by subparagraph (i), (ii) or (iii); and

(c) if deeds of company arrangement are proposed- a statement setting out details of the proposed deeds.”

3. The Plaintiffs and any creditor of the Arrium Administration Group Companies affected by these orders shall have liberty to apply upon five business days’ written notice to the parties to the proceeding.

4. Pursuant to rules 1.39 of the Rules and 1.3(2) of the Corporations Rules, service of this originating process on the Australian Securities & Investments Commission, the Australian Workers Union and the Australian Council of Trade Unions in accordance with rule 2.7(1) of the Corporations Rules is abridged as required.

5. The Plaintiffs’ and the Australian Workers Union’s costs of this application be costs in the administrations of the Arrium Administration Group Companies.

6. Within 1 business day of completing the report to be given to creditors of the Arrium Administration Group Companies in accordance with section 439A(4) of the Act (as modified by paragraph 2 of these orders), the Plaintiffs file with the Court an affidavit exhibiting a copy of that completed report and post a copy of the completed report on the websites of KordaMentha and the Plaintiffs’ lawyers Arnold Bloch Leibler.

THE COURT DIRECTS THAT:

7. Pursuant to section 447D of the Act, the First Plaintiffs may properly and justifiably send an aggregated report to creditors of the Arrium Administration Group Companies in accordance with section 439A(4) of the Act (as modified by paragraph 2 of these orders) in substantially the same form as the Arrium 439A Report produced at Tab 24 to Exhibit BW-1 to the Affidavit of Brian Webster affirmed 21 October 2016 (Webster Affidavit) and filed in this proceeding.

8. Pursuant to section 447D of the Act, the First Plaintiffs may properly and justifiably cause the Arrium Administration Group Companies in their capacities as creditors of any other Arrium Administration Group Companies to vote in favour of the entry into proposed Deeds of Company Arrangement, as summarised in Tab 22 to Exhibit BW-1 to the Webster Affidavit, at the meetings of creditors of the Arrium Administration Group Companies convened pursuant to section 439A of the Act.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

DAVIES J:

Introduction

1 The administrators intend to hold the second creditors’ meetings of the Arrium Group Companies listed in Schedule 1 (“collectively the Arrium Administration Group Companies”) on 4 November 2016. On 21 October 2016, the administrators filed an application for orders and directions in relation to the conduct of those meetings and the report which they intend to give creditors pursuant to s 439A(4) of the Corporations Act 2001 (Cth) (“the Act”). In summary, the administrators applied for:

(a) an order pursuant to s 447A of the Act that Part 5.3A of the Act is to operate in relation to each of the Arrium Administration Group Companies as if it provided that, at the second creditors’ meetings, or at any of the subsequent meetings of the creditors of the Arrium Administration Group Companies, each employee of any of the Arrium Administration Group Companies who is a member of AWU, AMWU, CEPU, NUW, CFMEU or Professionals Australia had duly appointed representatives of those unions to be her or his attorney pursuant to reg 5.6.31A of the Corporations Regulations for the purpose of the second creditors’ meetings and any subsequent meetings save for:

(i) any employee who attends any meeting in person; and

(ii) any employee who signs a proxy appointing some other person to attend any meeting on his or her behalf;

(b) an order under section 447A of the Act modifying section 439A(4) of the Act so that the administrators may provide creditors of the Arrium Administration Group Companies with a single aggregated report about the Arrium Administration Group’s businesses, property, affairs and financial circumstances (“the s 439A report”);

(c) a direction under section 447D of the Act that the administrators may properly and justifiably send an aggregated s 439A report to creditors of the Arrium Administration Group Companies; and

(d) a direction that the administrators are justified in causing the Arrium Administration Group Companies which are creditors of other Arrium Administration Group Companies to vote in favour of the entry into proposed deeds of company arrangement.

2 The application was heard on 25 October 2016. ASIC appeared at the hearing and did not oppose the orders and directions sought, but did bring to the attention of the Court certain matters bearing upon the Court’s consideration as to whether those orders and directions should be made.

3 Due to the timing of the second creditors’ meeting, I gave my decision on the application on 26 October 2016 and pronounced the orders and directions sought, stating that I would publish written reasons at a later point in time. These are my reasons for making the orders and directions sought.

in respect of Order 1

4 On 11 April 2016, this Court made an order under s 447A of the Act modifying the operation of Part 5.3A by appointing a union representative to be the attorney for union members who are employees of the Arrium Administration Group Companies in relation to the first meetings of creditors convened under s 436E of the Act: Australian Workers’ Union v Arrium Limited (Administrators Appointed), in the matter of Arrium Limited (Administrators Appointed) [2016] FCA 381. Order 1 makes similar orders for the purposes of the second creditors’ meetings and any subsequent meetings of the creditors of the Arrium Administration Group Companies in respect of additional unions whose members are employees of those companies. The order is justified and appropriate because of the large numbers of employees involved, being around some 6,000 employees. Those employees are employed by various entities in the Arrium Administration Group and located across some 160 sites across Australia. The location and number of employees poses both practical and timing difficulties in obtaining proxies from individual employees and the making of the order facilitates the representation of each employee at future meetings whilst preserving their right to attend personally or to provide a proxy appointing some other person to attend the meeting on the employee’s behalf.

in respect of Order 2 and order 7

5 These orders relate to the s 439A(4) report to creditors.

6 Order 2 has modified the operation of Part 5.3A of the Act to enable the administrators to provide a single aggregated s 439A report to creditors covering the businesses, property, affairs and financial circumstances of all the Arrium Administration Group Companies. The proposed report in question was put before the Court in an exhibit to the affidavit of Bryan Webster affirmed on 21 October 2016 and, by Order 7, the Court has directed that the administrators are justified in sending a report to creditors in substantially those terms. The administrators sought that direction from the Court because the proposed report does not strictly comply with the provisions of the ARITA Code of Professional Practice (“ARITA Code”), and also because the proposed deeds of company arrangement, which the administrators are recommending to creditors that the Arrium Administration Group Companies execute, contain several unusual features.

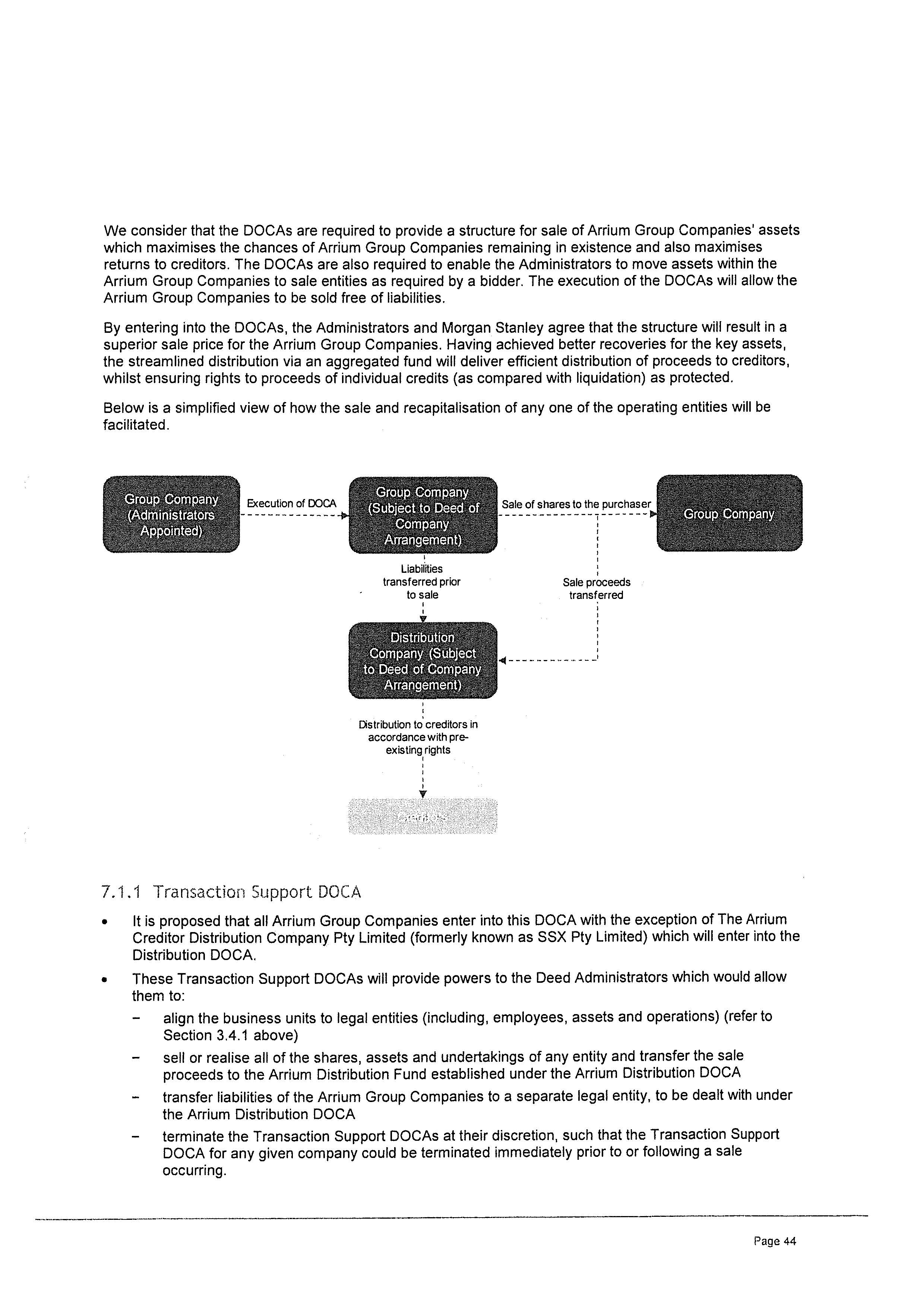

7 Mr Webster, who is one the administrators, in his supporting affidavit explained several of the difficulties and issues that the administrators have faced in establishing a sale and realisation process for the Arrium Administration Group Companies due to the size, complexity and financial and operational integration of the businesses conducted by the Arrium Group. Some of those difficulties and issues arise from the fact that the Arrium Group historically has carried on business without regard to the corporate entity structure and conducted its operations under six separate business divisions, namely Mining & Port, Whyalla Steelworks, Manufacturing, Distribution, Recycling and Head office/shared services. These businesses are not operated on an entity by entity basis but are intermingled as between various corporate entities within the Arrium Group, with a number of entities holding the assets, and conducting the operations, of more than one division, and with a number of the 6,000 employees (each employed by one of nine companies within the Arrium Group) working across multiple business divisions. The Arrium Group also has complex inter-company financing arrangements, which include two Deeds of Cross Guarantee creating two separate cross guarantor groups within the Arrium Group. Mr Webster stated that the financial and operational integration of the Arrium Group’s affairs has presented insuperable difficulties for the administrators in developing a sale and realisation strategy that maximises the chances of the Arrium Administration Group Companies continuing in existence and maximises returns to creditors. Another issue is that the Arrium Group has approximately 30,000 customers and 10,000 suppliers which, in the administrators’ view, makes it impractical to sell businesses operated or assets owned by the Arrium Group as the transfer of those customer and supplier agreements may take in excess of 6 months to complete and may create uncertainty which is unattractive to a potential bidder.

8 Mr Webster stated that in view of the complexities and difficulties faced in selling or realising the assets of those companies in administration holding property or carrying on the Arrium businesses (of which there are 25 companies), the administrators have proposed deeds of company arrangement to facilitate the realisation, sale or recapitalisation of those entities and distribution to creditors of the Arrium Administration Group on an aggregated basis. The administrators have developed 94 cross-conditioned deeds of company arrangement that they will recommend to creditors to vote upon at the second creditors’ meetings. Ninety three of those proposed deeds of company arrangement are identical. It is proposed that all Arrium Administration Group Companies enter into these deeds of company arrangement (the “Transaction Support Deeds of Company Arrangement”), with the exception of SSX Pty Ltd (to be renamed the Arrium Creditor Distribution Company Pty Ltd), which it is proposed, will enter into a deed of company arrangement, under which the proceeds of all the sales/realisations will be aggregated into a fund and distributed to creditors (called the “Arrium Distribution Deed of Company Arrangement”). The Transaction Support Deeds of Company Arrangement are said by the administrators to provide a structure for the sale of Arrium Administration Group Companies’ assets which maximises the chances of Arrium Group Administration Companies remaining in existence and also maximises returns to creditors. It is the administrators’ opinion that this structure will result in a superior sale price for the Arrium Administration Group Companies than would be available in a liquidation scenario. It is further proposed that a single Arrium distribution fund will be established by the Arrium Distribution Deed of Company Arrangement and that the proceeds of all of the sales and realisations will be aggregated into that fund for distribution to creditors. Distributions will only be paid to creditors from that aggregated fund.

9 On 29 July 2016, the administrators mandated Morgan Stanley to conduct a sale and realisation process of the 25 companies in administration holding property or carrying on the Arrium businesses (“the Arrium Sales Entities”), but if that is not possible a sale of different Arrium Sales Entities or parts of the Arrium businesses to different bidders.

10 The key features of the proposed deeds of company arrangement are set out in the proposed s 439A report exhibited to Mr Webster’s affidavit at Part 1.6.1 and Part 7 of that report (which are extracted in Annexure A to these reasons). Revisions to the proposed report have been made since Mr Webster prepared his affidavit but there have been no material changes to the key parts. The latest version of the report is an exhibit to an affidavit of Mr Zwier filed 27 October 2016.

11 Mr Webster’s affidavit contains the following summary of the key features of the proposed deeds of company arrangement:

The DOCAs do not identify a particular sale or recapitalisation transaction but will operate interdependently to facilitate any eventual sale or recapitalisation transaction(s) that may arise from the process being undertaken by Morgan Stanley. The DOCA structure is designed to provide the flexibility to bidders to acquire particular Arrium Group businesses, including by allowing assets, employees and liabilities to be moved between the Arrium Administration Group companies and empowering the Administrators to extinguish creditors’ debts and claims or novate them.

Some of the key features of the DOCAs are as follows:

(a) the Administrators will be appointed Deed Administrators under the DOCAs;

(b) the DOCAs provide for the appointment of an Arrium creditors’ committee which will comprise the members of the Arrium Committee of Creditors appointed at the First Creditors’ Meetings (DOCA Creditors’ Committee). Save for a limited exception that I explain below, the DOCA Creditors’ Committee will vote on resolutions in which a poll is called in precisely the same manner as creditors voting in a meeting of creditors under Part 5.3A of the Act, namely, on poll the members will vote on the basis of those creditors they represent in number and value. The number and value of the creditors’ votes will be determined by the number and value of their votes at the Second Creditors’ Meeting. The Deed Administrators will have a casting vote in the event of a deadlock between number and value, except in the circumstances where there is a deadlock between number and value in relation to a resolution:

(i) to make payments to priority creditors following a liquidation of an Arrium Group company; and

(ii) to liquidate an Arrium Group company.

In the event of a deadlock between the number and value of votes of members of DOCA Creditors’ Committee in these circumstances, the Deed Administrators will apply to the Court for directions, rather than exercising the casting vote;

(c) the DOCAs will be cross-conditioned in the sense that each DOCA will be conditional upon the execution of each of the other DOCAs;

(d) the Deed Administrators will have broad powers to implement the sale and restructure transactions in the best interests of creditors and stakeholders subject always to the consent of the DOCA Creditors’ Committee for transactions in excess of $20 million;

(e) the Arrium Distribution DOCA provides that the Deed Administrators must transfer all proceeds of sale or realisation assets to the Arrium Distribution Company as part of the Arrium Distribution Fund;

(f) the proceeds of sale from the Moly-Cop Entities will be assigned to an Arrium Group company and will not form part of the Arrium Distribution Fund due to the fact that the value of the Moly-Copy Entities’ and their assets is less than value of their indebtedness to the Arrium Lenders; and

(g) the Arrium Distribution DOCA will provide a ‘waterfall’ for payment of creditors' claims as against the Arrium Distribution Fund that broadly reflects the priority regime in Division 6 of Part 5.6 of the Act subject to a discretion of the Deed Administrators to apply the Arrium Distribution Fund in a way that ensures that unsecured creditors of the Arrium Administration Group companies are not unfairly prejudiced when compared to the position they would be in if they were proving their claims in a liquidation of any individual Arrium Administration Group company.

12 Mr Webster deposed as follows:

We have recommended all creditors to vote in favour of the DOCAs because we are of the unanimous view that they will achieve a better return under the DOCAs than from a liquidation of the Arrium Administration Group, even though we have not included in the Arrium 439A Report a comparative of estimated returns to creditors for each as recommended by ARITA and as we would usually provide. Let me explain why. First, the DOCAs provide the most flexible, speedy and certain process to transact a sale of the Arrium Sales Entities or their assets. Morgan Stanley agrees with us. A liquidator appointed to the Arrium Administration Group would not be able to replicate that process. So without quantifying the precise benefit of the superior sale process, we are confident the process will result in a superior outcome to that which would arise in a liquidation. Second, the DOCA process increases the likelihood of a sale of the Arrium Sales entities as going concerns. If we are able to achieve a sale of all the Arrium Sales Entities as going concerns we will avoid crystallising the priority claims of the employees. In a liquidation of the Arrium Administration Group those employee claims will crystallise and rank to a priority over ordinary unsecured creditors. Third, if we are able to maintain the Arrium Sales Entities as going concerns the ordinary trade creditors will have a greater prospect of continuing to do future business with them. Fourth, by conducting the Arrium administrations on an aggregated basis we will be able to avoid costly intra-creditor disputes and circumvent the need to conduct 94 separate administrations. In a liquidation of the Arrium Administration Group, each company will be administered separately. Fifth, under the DOC As we have sought to bind creditors to mediate all disputes that may arise prior to litigation. This may reduce legal costs. A liquidator cannot impose a requirement on creditors to mediate. Sixth, because the Administrators may subsequently recommend that any one or more of the Arrium Administration Group be placed into liquidation if there are specific reasons to do so, say for example the pursuit of legal claims only available to a liquidator of that company, then the Administrators will be able to achieve that outcome but only with the support of the DOCA Creditors' Committee. The DOCAs are so flexible that liquidators claims are currently preserved. A liquidation of the Arrium Administration Group provides no equivalent flexibility.

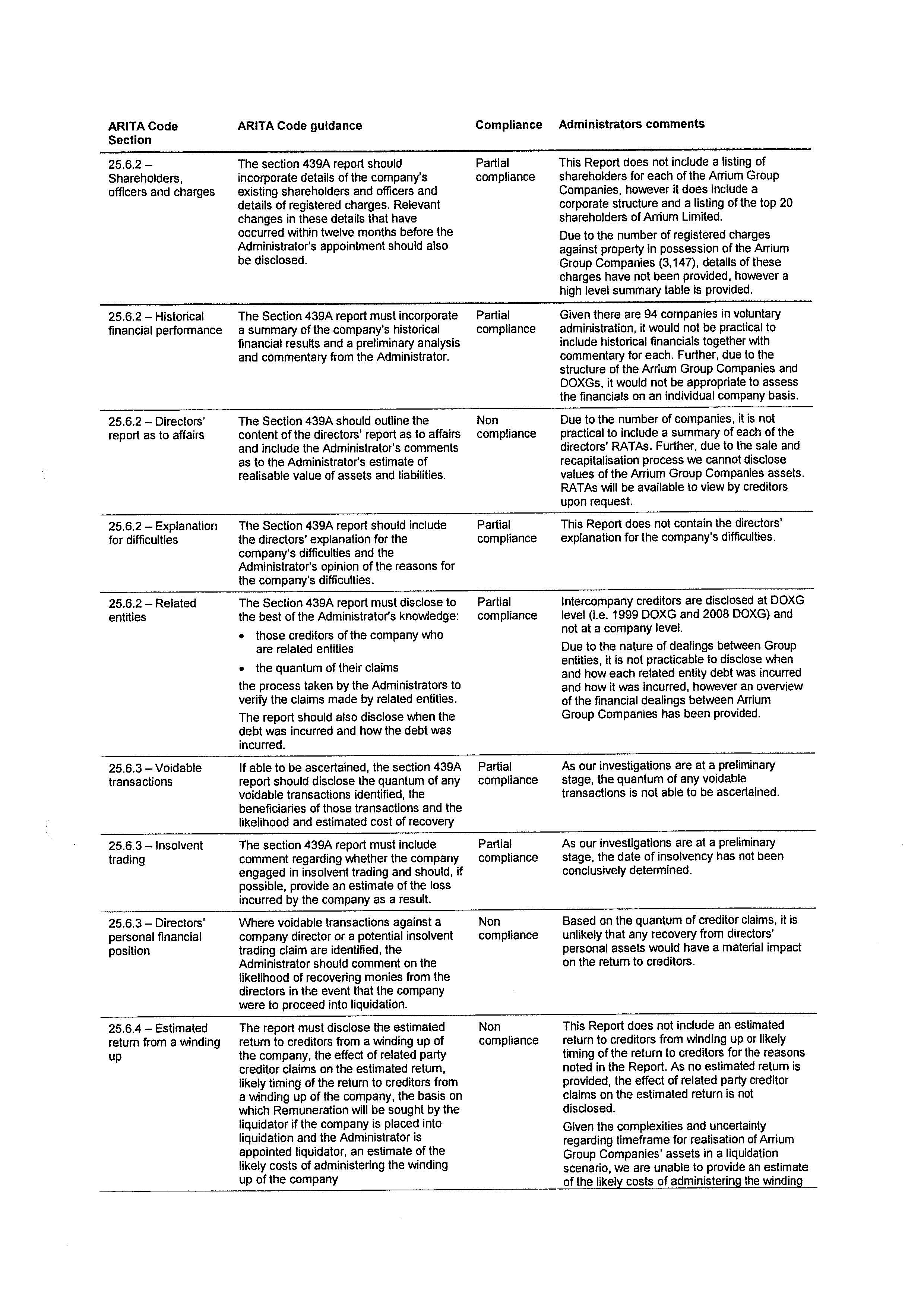

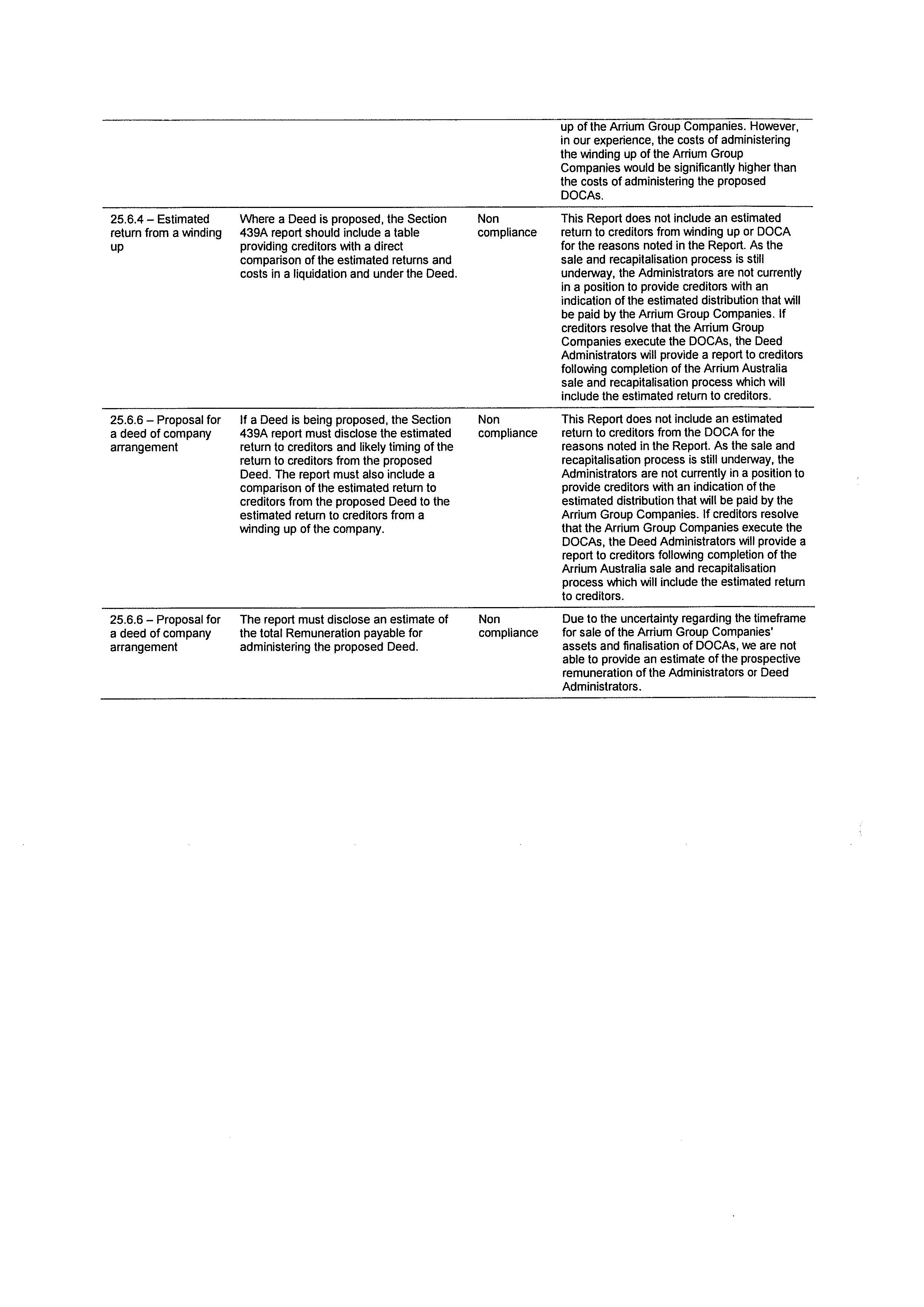

13 Mr Webster’s affidavit also identified in table form the aspects of the proposed single aggregated s 439A report that do not comply (at least to an extent) with the guidelines and requirements of the ARITA Code. The table is reproduced in Annexure B to these reasons. Mr Webster deposed that:

Pursuant to section 439A(4) of the Act, we would be required to provide creditors of each Arrium Administration Group company with a report about each Arrium Administration Group company's business, property, affairs and financial circumstances. This would involve the preparation and distribution to creditors of 94 separate reports as prescribed by section 439A(4) of the Act. This would be a costly, time-consuming and complex task.

…

Due to the complexities of the Arrium Administration Group that I have outlined above, we are not able to prepare an aggregated section 439A report that provides to creditors all of the information recommended in the guidelines set out in the ARITA Code of Professional Practice (ARITA Code) in relation to the preparation of section 439A reports.

…

We have recommended all creditors to vote in favour of the DOCAs because we are of the unanimous view that they will achieve a better return under the DOCAs than from a liquidation of the Arrium Administration Group, even though we have not included in the Arrium 439A Report a comparative of estimated returns to creditors for each as recommended by ARITA and as we would usually provide. Let me explain why. First, the DOCAs provide the most flexible, speedy and certain process to transact a sale of the Arrium Sales Entities or their assets. Morgan Stanley agrees with us. A liquidator appointed to the Arrium Administration Group would not be able to replicate that process. So without quantifying the precise benefit of the superior sale process, we are confident the process will result in a superior outcome to that which would arise in a liquidation. Second, the DOCA process increases the likelihood of a sale of the Arrium Sales entities as going concerns. If we are able to achieve a sale of all the Arrium Sales Entities as going concerns we will avoid crystallising the priority claims of the employees. In a liquidation of the Arrium Administration Group those employee claims will crystallise and rank to a priority over ordinary unsecured creditors. Third, if we are able to maintain the Arrium Sales Entities as going concerns the ordinary trade creditors will have a greater prospect of continuing to do future business with them. Fourth, by conducting the Arrium administrations on an aggregated basis we will be able to avoid costly intra-creditor disputes and circumvent the need to conduct 94 separate administrations. In a liquidation of the Arrium Administration Group, each company will be administered separately. Fifth, under the DOC As we have sought to bind creditors to mediate all disputes that may arise prior to litigation. This may reduce legal costs. A liquidator cannot impose a requirement on creditors to mediate. Sixth, because the Administrators may subsequently recommend that any one or more of the Arrium Administration Group be placed into liquidation if there are specific reasons to do so, say for example the pursuit of legal claims only available to a liquidator of that company, then the Administrators will be able to achieve that outcome but only with the support of the DOCA Creditors' Committee. The DOCAs are so flexible that liquidators claims are currently preserved. A liquidation of the Arrium Administration Group provides no equivalent flexibility.

Even if we could provide a general guide as to estimated comparative returns we are loath to do so because those estimates will reveal to the parties interested in acquiring the Arrium Administration Group businesses our estimate of a low and high value of the businesses we are selling. This may severely prejudice the outcome of the sale particularly if a bidder has estimated the synergies of an acquisition or other benefits far more generously than we may have done (in our capacity as insolvency practitioners). In most other administrations, when estimated comparative returns are provided by the Administrators to creditors, it is in the context of a sale for which approval of creditors is being sought. The Arrium Administration Group issues are bespoke in that respect.

In all these circumstances, we also seek a direction under section 447D of the Act that we may properly and justifiably provide creditors of the Arrium Administration Group companies with the Arrium 439A Report in substantially the same form as the Report at [Tab 24] referred to above.

14 Mr Zwier for the administrators submitted that the proposed deeds of company arrangement provide a bespoke solution to bespoke problems arising in the administrations of the Arrium Administration Group Companies because of the complexity and intermingling of the financial and operational affairs of those companies. He submitted that there are compelling special circumstances that justify the making of order 2 and the direction in order 7 for the following reasons.

15 First, the proposed deeds of company arrangement as outlined in the draft s 439A report are, in the administrators’ opinion, in the best interests of creditors as a whole and promote the policy and objects of Part 5.3A. The administrators and their advisors are currently pursuing a going concern sale/realisation process consistent with the objects of Part 5.3A of the Act to preserve the going concern value of the businesses and maximise the chances of the Arrium Administration Group Companies and/or businesses remaining in existence, and avoid the crystallisation of liabilities, including substantial employee liabilities, on a liquidation or cessation of operation. The administrators are of the opinion that the Transaction Support Deeds of Company Arrangement are required to provide a structure for the sale of the Arrium Administration Group Companies’ assets and consider that the structure and flexibility of the deeds of company arrangement will result in a superior sale for the Arrium Administration Group Companies than would be available in a liquidation scenario.

16 Secondly, the deeds of company arrangement contain appropriate safeguards to protect the interests of creditors against any perceived prejudice or disadvantage that might be said to arise from the deeds of company arrangement and the aggregation mechanism provided for by them. The safeguards and protections for creditors in relation to the deeds of company arrangement include that the statutory regime in Part 5.3A is not supplanted by the deeds of company arrangement and creditors’ rights, such as the right of appeal against a decision by a deed administrator under s 1321 of the Act and the right under Division 11 of Part 5.3A to seek a variation or the termination of the deeds or to apply to the Court for an order declaring the deeds or a provision of the deeds to be void remain in force, as well as the curial supervision regime in Division 13 of Part 5.3A. There is also a discretion within the Arrium Distribution Deed of Company Arrangement for the deed administrators to apply the proceeds to creditor claims in such a way that creditors are not unfairly prejudiced when compared with the position they would occupy in the winding up of any particular Arrium Administration Group company. Additionally, the deeds of company arrangement also preserve the ability to pursue voidable transaction or insolvent trading claims that would be available in the liquidation of any particular entity in the Arrium Administration Group should the administrators’ investigations identify such transactions that are in the interests of creditors to pursue.

17 Mr Zwier pointed out that the deed administrators’ discretionary powers under the deeds of company arrangement are also subject to safeguards, which include the appointment of a deed creditors’ committee comprised of members who represent a cross section of the major creditor groups of the Arrium Administration Group including the Arrium lenders, the US noteholders, the State Government of South Australia, the Commonwealth Government of Australia, trade creditors, non-union employees, the AWU and the ACTU. The creditors represented on the proposed deed creditors’ committee will represent more than 50% by number and value of all Arrium Administration Group creditors and the deed administrators will be required to obtain the approval of the deed creditors’ committee for any transactions above a $20 million threshold.

18 Thirdly, the administrators are of the view that to maximise the chances of the companies remaining in existence and the return to creditors, the administrators will need to be able to move assets and transfer employees into and out of those entities and be able to extinguish, novate or release pre-administration debt in order to attract, and then meet, the particular requirements of a successful bidder. Powers will be conferred on the deed administrators under the deeds of company arrangements for that purpose.

19 Fourthly, the sheer size and complexity of the Arrium Group and its businesses and operations, which include the mining and steel operations in Whyalla, South Australia which is heavily dependant upon the Arrium Group’s survival. The administrators have developed the deeds of company arrangement so as to provide a structure that is as flexible as possible to enable a going concern transaction to be undertaken in order to preserve the Arrium Administration Group’s businesses and operations in Whyalla. The South Australian Government and the Commonwealth Government are both represented on the Arrium Committee of Creditors and have been kept informed of the deed of company arrangement proposals and the application.

20 Fifthly, the complexity of the financial affairs of the Arrium Administration Group.

21 It was also submitted that the s 439A report fulfils its substantial function as provided for in s 439A(4) of the Act. It was submitted that whilst the report does not comply with all the guidelines in the ARITA Code, it nevertheless provides creditors with sufficient information to inform them to decide which course to adopt under s 439C of the Act at the second creditors’ meetings and the material details of the proposed deeds of company arrangement.

22 The s 439A report primarily departs from the ARITA Code in that it does not provide an estimate of returns to creditors in the windings up of the Arrium Administration Group Companies or a comparison between the estimated returns under the deeds of company arrangement and under a liquidation. The Court was informed that the reason why this information was not included is that the deeds of company arrangement are not predicated upon a particular transaction, but rather they are facilitative of any transaction that may arise from the current sale process. As the sales process is still underway the administrators are not currently in a position to provide an estimated return to creditors under the deeds of company arrangement. Further, it was submitted, if the administrators provided an estimated return based upon valuations of the Arrium Administration Group’s businesses and assets, this may impair the current sales process given the complexities and sensitivities of the current sale/recapitalisation process. It was submitted that the materiality of the comparison between the estimated returns to creditors under the deeds of company arrangement compared with the liquidation is of less importance in the particular circumstances of these deeds of company arrangement where the possibility of liquidating a particular Arrium Administration Group company is preserved along with the ability to pursue claims if that resulted.

23 Finally, it was submitted that the administrators have made prompt and transparent disclosure of the relevant matters in respect of which the direction is sought and have communicated extensively with ASIC in relation to the deeds of company arrangement, the s 439A report and the application since August 2016, have kept the Arrium Creditors Committee informed of the proposed deeds of company arrangement and the application, and have also served the application and the affidavit in support on the AWU and the ACTU.

24 Mr Moore QC appearing for ASIC did not oppose the order and directions sought, but did raise with the Court that there are two aspects of the proposed deeds of company arrangement that he described as “very unusual”, namely:

(a) the discretion given to the deed administrators to apply the proceeds generated from the sales or realisations in a manner that the administrators consider would not disadvantage creditors; and

(b) the creditors granting the deed administrators a power of attorney in relation to their claims.

25 Whilst Mr Moore QC did not submit that the Court should refuse to give the direction sought because of these “unusual” features, he did emphasize that ASIC should not be taken to have given its approval to the proposal.

26 Having regard to the detailed evidence of Mr Webster and the submissions of Mr Zwier on behalf of the administrators I was satisfied that the administrators are justified in putting the proposal they have developed to creditors in a single aggregated s 439(4) report.

27 First, I have accepted Mr Zwier’s submission that there are special circumstances with respect to these administrations that justify the approach taken by the administrators and I am satisfied that what is being proposed is both consistent with, and in furtherance of, the objects of Part 5.3A of the Act. As well, the protections and advantages provided to creditors under that Part are to be preserved under the proposal to be put to creditors: Re Green (as voluntary administrators of Bevillesta Pty Ltd) [2011] NSWSC 417; (2011) 84 ALR 215 at [65].

28 Secondly, it does not appear to be the case that creditors’ rights will be impaired, nor does it appear that it is likely that creditors will be significantly disadvantaged, by the structure to be adopted if the creditors vote in favour of the entry into the deeds of company arrangement. Critically in this regard, the statutory order of priority in s 556 of the Act is to be preserved under the deeds of company arrangement and the discretion to be given to the deed administrators to apply the proceeds generated from the sales or realisations is part of the mechanism by which to ensure that creditors are not disadvantaged by the aggregation of the Arrium Administration Group Companies in the sale/realisation process when compared to the position they would be in if they were proving in a liquidation of any of those companies. The discretion is an unusual feature, as ASIC stated, but it is there to ensure that unsecured creditors are not unfairly prejudiced by sale/realisation on an aggregated basis and, in the exercise of that discretion, the deed administrators will have fiduciary and statutory duties to creditors and will remain subject to the Court’s supervision in relation to the exercise of the discretion, as they will also with respect to the authority granted to them under the powers of attorney in aid of the administrators’ powers under the deeds of company arrangement. Further, the powers of attorney are only given to the deed administrators in relation to the debt and do not empower them to release third parties.

29 Thirdly, for the reasons given by Mr Webster in his affidavit, which are elaborated on in the table contained in Annexure B, I am satisfied that the administrators have sufficiently justified the departure from the requirements and guidelines of the ARITA Code. I am also satisfied that the report contains sufficient information for the report to achieve its statutory purpose.

30 Fourthly, without order 2, the administrators otherwise would have been required to prepare 94 separate reports in relation to each of the Arrium Administration Group Companies. I accept the submission that this would be needlessly time consuming, costly, complicated and inappropriate in the particular circumstances of the Arrium Administration Group Companies, due to the cross-conditionality of the deeds of company arrangement that are proposed.

Order 8

31 A number of the Arrium Administration Group Companies are dormant entities and non-operating and only have Arrium inter-company liabilities and no external creditors. The administrators propose to vote the inter-company debt in favour of the deeds of company arrangement and have also sought a direction under s 447D of the Act that they may properly and justifiably vote the Arrium Administration Group inter-company debt in favour of the proposed deeds of company arrangement. The administrators expressed concern that by voting the intercompany debt in favour of the deeds of company arrangement proposal they may be exposed to criticism if their vote has the effect of carrying the vote in opposition to external creditors by value and number in a dormant entity or of being in a position of conflict as they will later become the deed administrators under the deeds of company arrangement.

32 Although the administrators’ vote of the inter-company debt is necessary to enable the passage of the deeds of company arrangement in relation to the dormant entities with no external creditors, because of the cross conditionality of the deeds of company arrangement, regardless of the administrators’ vote in relation to the inter-company debt in the dormant Arrium Administration Group Companies, the deeds of company arrangement will only become effective if the external creditors pass the requisite resolutions at the second creditors’ meetings in favour of the execution of those deeds. Accordingly I accept that it is appropriate for the Court to grant this direction.

orders 3, 4, 5 and 6

33 These orders are not controversial and are appropriate in the circumstances.

I certify that the preceding thirty-three (33) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Davies. |

Associate:

ANNEXURE A

ANNEXURE B

Schedule 1 |

1 A.C.N. 006 769 035 Pty Limited (ACN 006 769 035) | |

2 Akkord Pty Limited (ACN 060 486 991) | |

3 ANI Construction (W.A.) Pty. Limited (ACN 008 670 871) | |

4 Arrium Finance Pty Limited (ACN 093 954 940) | |

5 Arrium Iron Ore Holdings Pty Limited (ACN 152 752 844) | |

6 Arrium Limited (ACN 004 410 833) 7 Atlas Group Employees Superannuation Fund Pty. Limited. (ACN 060 568 998) | |

8 Atlas Group Staff Superannuation Fund Pty. Limited. (ACN 059 654 241) | |

9 Atlas Group Superannuation Plan Pty Limited (ACN 065 649 050) | |

10 Australian National Industries Pty Limited (ACN 000 066 071) | |

11 Australian Wire Industries Pty Limited (ACN 064 267 456) | |

12 Austube Mills Holdings Pty Limited (ACN 123 160 172) | |

13 Austube Mills Pty Limited (ACN 123 666 679) | |

14 AWI Holdings Pty Limited (ACN 004 157 475) | |

15 B.G.J. Holdings Proprietary Limited (ACN 004 859 536) | |

16 Bradken Consolidated Pty Limited (ACN 000 011 932) | |

17 Central Iron Pty Limited (ACN 143 503 397) | |

18 Cockatoo Dockyard Pty Limited (ACN 000 025 918) | |

19 Comsteel Pty. Limited (ACN 006 218 524) | |

20 Coober Pedy Resources Pty Limited (ACN 151 599 905) | |

21 Eagle & Globe Pty Limited (ACN 000 122 305) | |

22 Email Accumulation Superannuation Pty Limited (ACN 065 263 658) | |

23 Email Executive Superannuation Pty Limited (ACN 065 263 818) | |

24 Email Holdings Pty Limited (ACN 092 348 555) | |

25 Email Management Superannuation Pty Limited (ACN 065 263 710) | |

26 Email Metals Pty. Limited. (ACN 004 574 681) | |

27 Email Pty Limited (ACN 000 029 407) | |

28 Email Superannuation Pty Limited (ACN 065 263 603) | |

29 Emwest Holdings Pty. Limited. (ACN 001 992 123) | |

30 Emwest Properties Pty Limited (ACN 003 146 334) | |

31 GSF Management Pty Limited (ACN 064 116 874) | |

32 J. Murray-More (Holdings) Pty Limited (ACN 000 158 412) | |

33 John McGrath Pty Limited (ACN 000 004 937) | |

34 Kelvinator Australia Pty Limited (ACN 007 873 734) | |

35 Litesteel Products Pty Limited (ACN 109 854 677) | |

36 Litesteel Technologies Pty Limited (ACN 113 101 054) | |

37 Metals Properties Pty. Limited. (ACN 000 040 040) | |

39 Metpol Pty Limited (ACN 000 927 373) | |

40 N.K.S. (Holdings) Proprietary Limited (ACN 004 321 313) | |

41 O Dee Gee Co. Pty. Limited. (ACN 004 208 191) | |

42 Onesteel Americas Holdings Pty Limited (ACN 147 067 016) | |

44 Onesteel Coil Coaters Pty Limited (ACN 123 138 732) | |

45 OneSteel Manufacturing Pty Limited (ACN 004 651 325) | |

46 Onesteel MBS Pty Limited (ACN 096 273 979) | |

47 Onesteel NSW Pty Limited (ACN 003 312 892) | |

48 Onesteel Queensland Pty Limited (ACN 010 558 871) | |

49 Onesteel Recycling Holdings Pty Limited (ACN 059 240 952) | |

50 Onesteel Recycling Overseas Pty Limited (ACN 105 479 356) | |

51 Onesteel Recycling Pty Limited (ACN 002 707 262) | |

52 Onesteel Reinforcing Pty Limited (ACN 004 148 289) | |

53 Onesteel Stainless Australia Pty Limited (ACN 004 610 851) | |

54 Onesteel Stainless Pty Limited (ACN 006 362 652) | |

55 Onesteel Technologies Pty Limited (ACN 096 380 219) | |

56 Onesteel Trading Pty Limited (ACN 007 519 646) | |

57 Onesteel US Investments 1 Pty Limited (ACN 131 211 606) | |

58 Onesteel US Investments 2 Pty Limited (ACN 131 211 571) | |

59 Onesteel Wire Pty Limited (ACN 000 010 873) | |

60 Overseas Corporation (Australia) Pty Limited (ACN 004 242 086) | |

61 P & T Tube Mills Pty Limited (ACN 010 469 977) | |

62 Palmer Tube Mills Pty Limited (ACN 010 469 879) | |

63 Pipeline Supplies of Australia Pty Limited (ACN 008 573 475) | |

64 Reosteel Pty Limited (ACN 000 142 094) | |

65 Roentgen Ray Pty Limited (ACN 000 028 106) | |

66 Southern Iron Pty Limited (ACN 119 611 068) | |

67 SSG Investments Pty Limited (ACN 085 490 526) | |

68 SSG No.2 Pty Limited (ACN 087 840 720) | |

69 SSG No.3 Pty Limited (ACN 087 840 515) | |

70 SSGL Share Plan Nominees Pty Limited (ACN 085 943 540) | |

71 SSX Acquisitions Pty Limited (ACN 090 574 520) | |

72 SSX Employees Superannuation Fund Pty Limited (ACN 064 431 116) | |

73 SSX Holdings Pty Limited (ACN 087 813 116) | |

74 SSX International Pty Limited (ACN 084 990 947) | |

75 SSX Pty Limited (ACN 082 181 726) | |

76 SSX Retirement Fund Pty Limited (ACN 064 431 303) | |

77 SSX Services Pty Limited (ACN 083 090 831) | |

78 SSX Staff Superannuation Fund Pty Limited (ACN 064 431 072) | |

79 Tasco Superannuation Management Pty Limited (ACN 071 901 712) | |

80 The ANI Corporation Pty Limited (ACN 000 421 358) | |

81 The Australian Steel Company (Operations) Pty Limited (ACN 069 426 955) | |

82 Tube Estates Pty. Limited. (ACN 010 449 939) | |

83 Tube Street Pty Limited (ACN 004 785 157) | |

84 Tube Technology Pty. Limited. (ACN 010 469 986) | |

85 Tubemakers of Australia Pty Limited (ACN 000 005 498) | |

86 Tubemakers Somerton Pty Limited (ACN 004 595 546) | |

87 Western Consolidated Industries Pty Limited (ACN 001 185 913) | |

88 Whyalla Ports Pty Limited (ACN 153 225 364) | |

89 X.C.E. Pty Limited (ACN 004 081 903) | |

90 XEM (Aust) Pty Limited (ACN 004 158 025) | |

91 XLA Pty Limited (ACN 004 239 392) | |

92 XLL Pty Limited (ACN 006 301 266) | |

93 XMS Holdings Pty Limited (ACN 008 742 014) | |

94 Zinctek Pty limited (ACN 010 474 790) |