FEDERAL COURT OF AUSTRALIA

Bradley v Voltex Group Holdings Pty Limited [2016] FCA 1230

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties confer and within 14 days of today’s date file agreed or competing proposed orders (including as to costs) reflecting the reasons for judgment.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

JAGOT J:

1 Matthew Bradley claims that the respondents are liable to him in damages for breach of contract and unconscionable conduct in contravention of the Australian Consumer Law (Schedule 2, s 21, of the Competition and Consumer Act 2010 (Cth)).

2 The determinant of liability for the contractual claim will be the terms of an agreement, styled a “Business Venture Agreement” (or BVA), into which the parties entered on 3 December 2013.

3 The determinant of liability for the unconscionable conduct claim will be the characterisation of the conduct of the respondents.

4 For the reasons set out below Mr Bradley succeeds in part on his contractual claims but fails in his unconscionable conduct claims.

5 Because the BVA was not executed until some five months after Mr Bradley began working with the respondents, it is convenient to start by identifying the relevant facts. Most of the disputes between the parties do not concern what happened or when but, rather, the characterisation of what happened.

Dealings between Mr Bradley and the respondents

6 In or around 2010, the fourth, fifth and sixth respondents, Michael Weston, Richard Ratcliffe and Raul Barrera established a business specialising in electrical power systems, trading under the group name of “Voltex”. Mr Ratcliffe and Mr Barrera are electrical engineers, and work hands on in the group’s business of providing electrical power systems to customers. Mr Weston is the business manager. The first respondent is Voltex Group Holdings Pty Ltd (VGH), a holding company established for the Voltex business, including Voltex Power Engineers Pty Ltd (VPE). Mr Weston, Mr Ratcliffe and Mr Barrera are all directors of VGH. I refer to them collectively as the directors.

7 By 2013, the directors recognised that Voltex’s business would be improved if they could offer a systems integration service, meaning a service automating the operation of the electrical power systems which they provided. In addition to the general opportunity presented by the capacity to offer these services as part of its business model, Voltex had two big projects on the go – a sludge treatment facility in Hong Kong and the Lihir Gold Project in Papua New Guinea (PNG) – and saw an opportunity to enter the automation market by providing automation services to these projects. As the projects were underway, the opportunity for Voltex to provide these services to these projects was subject to the pressure of time. Voltex wanted to take advantage of the opportunity the two projects presented but did not have the expertise in-house to provide such services.

8 This is where Mr Bradley enters the picture. Mr Bradley is an engineer specialising in the automation of plant.

9 Mr Bradley had been involved in a business venture known as PlantWeave Technologies Pty Ltd (PlantWeave), which provided automation services. The business relationship between Mr Bradley and his partner in the PlantWeave business was failing and Mr Bradley was in the process of exiting that venture subject, however, to a restraint of trade, the terms of which (as opposed to the parties’ understanding of the effect of the restraint) do not matter.

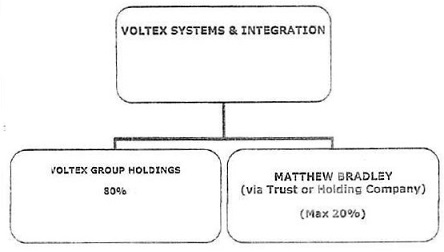

10 Mr Bradley knew Mr Barrera. In early 2013 he had sought Mr Barrera’s advice about his problems with PlantWeave and, in that context, discussed a possible investment in PlantWeave by Voltex. Mr Barrera thought this option was impossible and instead, no doubt with an eye to Voltex’s needs, raised with Mr Bradley the establishment of a new company offering automation services for electrical power systems. Mr Bradley was keen, given that his involvement with PlantWeave appeared to be going nowhere. By 17 April 2013, Mr Weston and Mr Ratcliffe were on board with the idea that a new company should be established to provide automation services involving Mr Bradley.

11 A first draft of a business venture agreement – or BVA – was provided to Mr Bradley on 23 April 2013 which included provisions by which Mr Bradley could gain equity in the new company of up to 20% of the shares, amongst other things, by sacrificing part of his salary. Discussions continued throughout April and much of May 2013. By 15 May 2013, Mr Weston was suggesting that they could “adjust the eventual new company name to Voltex Systems & Integration (VSI) which for the next six months will be run as a separate [b]usiness [u]nit within VPE, then once you are completely clear of Plant[W]eave, we will spin off into a separate company as discussed” and would “clarify the market rate for your position is estimated to be $200k pa, as the basis for current ‘Salary Sacrifice’ contributions to ownership”. In response, Mr Bradley recorded his understanding of the discussions saying that he was to be the CEO and a director of the new company, as well as a shareholder, with the “share breakdown” to be determined.

12 Mr Bradley’s position was that because he did not have any funds to contribute but wanted equity in the new company (by then being referred to as VSI although not yet incorporated) he would contribute financially by way of the sacrifice of salary. Gaining equity in the new company was essential from Mr Bradley’s perspective, and it was clear to Mr Weston (and, I infer, Mr Barrera and Mr Ratcliffe) that Mr Bradley would proceed with the proposal only if he could gain equity, despite his lack of funds to contribute. Versions of the BVA continued to circulate while the discussions continued.

13 Mr Bradley contends that in or about June 2013, he and VGH had orally agreed that a company would be established to conduct a new automation business and he would work in that business from July 2013. The oral agreement is relevant only to the unconscionable conduct claim because it is accepted for Mr Bradley that the BVA which was executed subsequently superseded the oral agreement. The respondents admit that there was an oral agreement but the terms are in dispute, the dispute largely reflecting that which exists in respect of the BVA. Mr Bradley contends that a term was that VGH would receive an 80% shareholding in the new business and he would receive a 20% shareholding six months later and could contribute by way of salary sacrifice, shareholder’s loan or by providing intellectual property. The respondents contend that the term was that Mr Bradley would receive a 20% shareholding six months after the establishment of the new business, “contingent upon Mr Bradley contributing 20% of the initial value of the new business”. This value was to be calculated in various ways including by reference to the value of salary sacrifice of part of an agreed base salary of $200,000, the value to the new business of any intellectual property provided by Mr Bradley, or the value of any shareholder’s loan he made.

14 At this point, it is appropriate to record that I have no doubt that the capacity to gain a 20% shareholding in the new business was essential to Mr Bradley and was understood to be such by the respondents. However, the contention that the oral agreement was that if Mr Bradley worked for VSI then, six months later, he would get a 20% shareholding even if he made no contribution to the new business apart from his labour, is inconsistent with Mr Bradley’s own evidence. The contemporaneous emails and discussions disclose that Mr Bradley knew that in order to get his shareholding he would need to make some contribution over and above working in the business. This is the reason there are references in the evidence of the negotiations to his capacity to salary sacrifice. Because he had no spare funds, salary sacrifice and the contribution of intellectual property (if he held any) were probably the only practical options he had to make a contribution over and above working for the new business, as necessary to secure his right to equity.

15 The evidence also shows that because the common focus was on his capacity to salary sacrifice, none of the parties were particularly bothered by the value of the contribution required and how the value of the contribution would be calculated. It seems to me that it was a common assumption at this time that Mr Bradley would be able to make a contribution considered to be satisfactory by way at least of salary sacrifice, and thus in six months would be issued his shareholding. Mr Bradley appears to have been happy to proceed on that assumption because he wanted to be involved in the new business and wanted the 20% equity. The directors appear to have been happy to proceed on that assumption because the two projects they had on the go in Hong Kong and PNG required the provision of automation services, and without the new business and Mr Bradley’s involvement Voltex was not equipped to take advantage of these opportunities.

16 This is consistent with the reason for the six months’ delay. It was common ground that the reason for the delay in the issue of shares to Mr Bradley was not related to assessment of or agreement about the value of his contributions, but resulted from a concern that Voltex not be complicit in any breach of the restraint to which Mr Bradley was subject in favour of PlantWeave.

17 It should be accepted, therefore, that when the time came for Mr Bradley to start working with Voltex, he and the directors shared an assumption that he could contribute satisfactorily to the new business by one of the three identified methods and, as a result, in six months he would be issued a 20% shareholding in VSI.

18 The second and third respondents, Voltex Systems Holdings Pty Ltd (VSH) and Voltex Systems & Integration Systems Pty Ltd (VSI), were incorporated on 11 June 2013. VGH owned all of the 80 shares issued in each of VSH and VSI on incorporation. Mr Weston was also the director of VSH and VSI, with Mr Ratcliffe becoming another director of VSH and VSI on 13 August 2013. It was intended that VSH would hold the relevant intellectual property rights to the new automation business and the business would be conducted through VSI. The fact that the 80 shares in VSI and VSH were issued to VGH is consistent with the common assumption which I have identified – everyone assumed that Mr Bradley would make a satisfactory contribution by one of the identified methods and, in six months’ time, would be issued 20 shares in VSH and VSI, equivalent to a 20% shareholding.

19 This context – pressure on Voltex to be able to take advantage of the opportunities in Hong Kong and PNG and Mr Bradley’s keenness to be involved in the new business on the basis that he would receive 20% equity – explains why the parties proceeded without a final BVA having been executed. The context also explains why, by 29 May 2013, Mr Bradley had executed a contract of employment with VPE. VSI had not yet been incorporated. Mr Weston sent Mr Bradley two contracts of employment, one with VPE and one with the (as yet non-existent) VSI. Mr Bradley executed the contract with VPE (unsurprisingly given that VSI did not exist). Under this contract of employment with VPE, Mr Bradley was to work as a “Systems & Integration Manger”, initially on a casual basis, on a base annual salary of $150,000, with no period of notice required for termination. By this time, Mr Bradley was gearing up to work in the new business, reviewing a business plan Mr Weston had sent and the projects Voltex had on the go. It is apparent that the terms of this agreement with VPE had been overtaken by events almost before it was executed. It had already been agreed that Mr Bradley’s base salary for managing VSI would be $200,000 per year, for example. It was also not the case that Mr Bradley would be working casually in VSI once it was incorporated. He was to be the full time Systems and Integration Manager of VSI, as reflected in the unexecuted contract of employment between VSI and Mr Bradley, and principally responsible for managing VSI’s business.

20 Again, it is appropriate to interpose some observations here. One unpleaded and unexplored issue in this case is the contract of employment under which Mr Bradley worked as the manager of VSI from July 2013 until January 2015. In closing submissions, the respondents referred to the contract with VPE which Mr Bradley executed as if this were the relevant contract of employment to support the proposition that termination of Mr Bradley without notice was authorised. But the contract with VPE could not have been the relevant contract of employment. Apart from the fact that it was with VPE not VSI, as noted, it provided for Mr Bradley to work casually at a rate of $150,000. This contract must have been understood by all involved to have been an interim measure and was overtaken by events when Mr Bradley started to work as the full-time manager of VSI on a salary of $200,000. Nor can the unexecuted contract between VSI and Mr Bradley be the relevant contract of employment for the simple reason that it was never executed. No doubt there was a contract of employment. The position, however, is this. No contract of employment was pleaded. No question was asked of any witness about the contract of employment. The interrelationship between the contract of employment and the BVA was neither pleaded nor explored. As such, it is not open to either party to suggest that the contract of employment is relevant to resolution of the issues.

21 By 3 June 2013, Mr Bradley wanted to let PlantWeave know that he was working for Voltex and had accepted a full-time position to do so as the general manager of the new business. By early July 2013 he was working full-time in the newly incorporated VSI, in effect as its manager and, as noted, at a salary of $200,000 per year. While there is a dispute about Mr Bradley’s contributions to VSI apart from working as its manager, it is apparent that Mr Bradley did not receive his full salary and this was understood at the time by Mr Bradley and the directors to constitute a “salary sacrifice” as provided for in the oral agreement. It is not in dispute that between July and December 2013 $18,062.50 of Mr Bradley’s salary was retained by VSI and that, on or around 14 January 2014, VSI repaid all but $9,000 of those funds to Bradley, the balance being held in VSI as a “shareholder’s loan” from Mr Bradley, with Mr Bradley thereafter contributing a further $1500 per month to VSI until July 2014, when Mr Weston (on behalf of VGH) agreed that Mr Bradley’s salary sacrifice could cease and all shareholder loans in VSI’s accounts were repaid in full.

22 Mr Bradley was sent VPE’s account categories on 12 July 2013 by Ms Schilpzand, Voltex’s in-house accountant and asked what he wanted to set up for VSI. He updated the directors about the work he was doing for VSI, including quotes for work related to the two existing VPE projects and other quotes being prepared for new projects, as well as the finalisation of a business plan for VSI. Mr Bradley also focused on employing people to work in VSI and developing new clients for VSI. By 5 September 2013, Nick Cuevas, Louis Tamburini and Wesley Hess had been employed by VSI. Another focus of Mr Bradley was VSI’s job management systems, as well as a draft budget for VSI. In other words, Mr Bradley was doing all the things that might be expected of a manager of a new business which had an advantage of tendering for work on two big projects on which its parent was already working and wanted to expand to attract new work.

23 Not everything was smooth sailing, however. For his part, Mr Bradley found it difficult to get time with Mr Weston to discuss and finalise matters relevant to VSI’s business. In this regard, it needs to be understood that Mr Barrera and Mr Ratcliffe are engineers and were very busy doing Voltex’s project engineering work and were often (perhaps mostly) out of Australia, so it was inevitable that most of the work involving the management of the new business would involve dealings between Mr Bradley and Mr Weston. Mr Bradley, however, had a pre-existing relationship with Mr Barrera and thus, if dissatisfied with his dealings with Mr Weston, seems to have tended to deal directly with Mr Barrera thus by-passing his problems with Mr Weston. For his part, over time, Mr Weston perceived Mr Bradley’s dealings with Mr Barrera as Mr Bradley trying to get his own way even if Mr Weston thought he had made the overall business position clear. Everyone was also concerned that a business plan for VSI had not been adopted. By 13 September 2013, Mr Barrera was asking Mr Bradley when the business plan would be finished and, in a response characteristic of Mr Bradley’s perception of his dealings with Mr Weston generally, Mr Bradley said he hoped to get some of Mr Weston’s time so the plan could be finalised the following week.

24 Mr Bradley sent Mr Weston a draft business plan on 17 September 2013. Mr Weston did not think much of the draft but seems to have kept his own counsel in this regard. While Mr Bradley wanted to meet to discuss the draft business plan Mr Weston saw it as nothing more than a “wish list” so, from his point of view, there was nothing to discuss in the draft. Mr Ratcliffe, whenever he came to look at it, also did not think much of the draft business plan.

25 Another major difference was surfacing between Mr Weston and Mr Bradley. Mr Bradley envisaged that it would be best if each business within the Voltex group operated independently according to its own requirements. He sought to resolve the relationship between VSI and the rest of the Voltex group on this basis. Mr Weston accepted that Mr Bradley repeatedly pressed him for clarification of VSI’s role within the group but, as far as Mr Weston was concerned, the position had been made clear in discussions from the outset that VSI was to be a Voltex group member and was to function as part of the group, and Mr Bradley’s repeated raising of the issue was a result of the fact that Mr Bradley did not accept this position.

26 If it is necessary to decide between the versions of Mr Weston and Mr Bradley, the contemporaneous emails support Mr Weston’s view. This is not to say that Mr Bradley was doing other than giving truthful evidence in this regard. It is to say that, having regard to all of the evidence (written and oral), it seems clear that Mr Bradley held strong views about the new business and, no matter how he couched his communications – whether as requests for clarification or direction or as a need to settle a business strategy – he wanted VSI to be autonomous and independent of the rest of the group and was prepared to repeatedly raise this issue despite Mr Weston considering it settled. So much is evident from an email Mr Weston sent in response to Mr Bradley on 23 October 2013, where he proposed a face to face meeting to thrash out the issue but stressed that “the vision is one for all Voltex Group”. The friction was increasing because, although presented by Mr Bradley as an issue that needed to be resolved, there seems to have been no issue apart from in Mr Bradley’s mind. Mr Weston was clear that VSI had to function as part of the Voltex group, and Mr Ratcliffe and Mr Barrera had never suggested to the contrary. Mr Bradley simply did not agree with or accept the vision of VSI being part of the group, and wanted to press his case for a different approach. Given these fundamentally different objectives, it was almost inevitable that the friction between Mr Weston and Mr Bradley would increase, and so it did, despite VSI gaining substantial work on the Hong Kong and PNG projects as the directors had wished.

27 One trigger for the deterioration of the relationship between Mr Bradley and Mr Weston was Mr Bradley’s work to create a document management system for VSI. Mr Weston, when he became aware of this work, pointed out that VPE “ALREADY” had a system and this system needed to be applied to “ALL Voltex group companies” (Mr Weston’s emphasis in his email to Mr Bradley of 7 October 2013). Mr Weston ended this email with the statement that:

As discussed, our branding is quite important, we have spent a lot of time and money on this, and it is equally important that we maintain a consistency of systems, even with the “look and feel”.

28 Mr Bradley, consistent with his overall approach, pushed back in a return email saying that the purpose of “commonality” needed to be considered, and that “[f]undamentally a business needs autonomy to be effective and successful”.

29 Another trigger was Mr Bradley’s desire for VSI representatives to attend a training session about some software known as “ETAP Realtime” in Malaysia which Mr Weston wanted VPE alone to control. On 30 October 2013, Mr Bradley notified Mr Weston of the fact that he and a VSI employee would be booking flights and accommodation in a few days. Mr Weston was irritated by the email, and expressed his irritation in an email to Mr Ratcliffe and Mr Barrera, which he copied (in all likelihood accidentally, despite his suggestion to the contrary) to Mr Bradley. While it is likely that there had been some discussion about this beforehand, it is apparent that Mr Weston felt that it had not been agreed that Mr Bradley and the other VSI employee would be attending or that Mr Bradley could take it upon himself to make arrangements to attend. The relevant point is that the email reflects what was already becoming obvious. Mr Weston thought it important for VSI and Mr Bradley to function as part of the overall Voltex group, whereas Mr Bradley wanted VSI to operate independently. Mr Weston was becoming exasperated by what he saw as Mr Bradley continually operating in this autonomous way, despite it being understood by Mr Weston to be clear that VSI was part of the overall Voltex group. Contrary to the submissions for Mr Bradley, there is no suggestion that the other directors thought Mr Weston was doing other than communicating to Mr Bradley a position common between them.

30 Having received the email in which Mr Weston expressed his exasperation, Mr Bradley suggested that a business orientated facilitator be appointed for a number of purposes including “identifying…our objectives” and “what our roles and responsibilities are”. From Mr Weston’s perspective, this was not a helpful suggestion. It was another way for Mr Bradley to put in issue the status of VSI and his own status as VSI’s manager when, so far as everyone else was concerned (Mr Weston expressly and the other directors by implication), VSI was part of the overall Voltex group. It is not difficult to sympathise with Mr Weston. Even if Mr Bradley was issued a 20% shareholding, the shareholding structure gave a majority interest to the Voltex parent, VGH. Despite Mr Bradley’s protestations, contemporaneous and otherwise to the contrary, it is apparent that to all bar Mr Bradley the role of VSI as a part of the group rather than an independent company had been clear from the outset. I do not accept that Mr Weston was of a “combative nature” and unwilling to talk to Mr Bradley. To the contrary, Mr Bradley continued to press for his preferred view of the role of VSI (and his own role as its manager) and his constant pressure for a changed position frustrated Mr Weston.

31 Accordingly, it would be wrong to characterise events as Mr Weston making issues about Mr Bradley’s conduct when there were no issues. It is not that Mr Bradley was doing something “wrong” or “improper”. It is that there was a fundamental difference between Mr Weston (and, by implication, the other directors) and Mr Bradley about the role of VSI and the degree of independence it should have from the Voltex group as a whole. There was real friction as a result and it was inevitable that the other VGH directors, Mr Barrera and Mr Ratcliffe, who were busy doing engineering work, would have to get more actively involved. A meeting of the directors of VGH and Mr Bradley was thus scheduled.

32 Mr Barrera emailed Mr Bradley on 19 November 2013 in anticipation of the meeting. He identified various “[s]ensitive topics” which he felt Mr Bradley should be prepared to discuss at the meeting, including Mr Bradley’s “directorship at group level” and identified this as a topic:

Issue of VSI shares to you (needs to happen now)

33 Mr Barrera confirmed in evidence that he thought Mr Bradley should be issued his shares then and there. Mr Barrera raised this with Mr Weston but Mr Weston disagreed because of continuing concern about Mr Bradley’s PlantWeave restraint. It is also evident that Mr Barrera and Mr Ratcliffe (and, no doubt, Mr Weston too) wanted VSI to succeed. They had no reason to wish otherwise. They saw that there was a real opportunity in the provision of these services and VSI was the way they could take advantage of the opportunity.

34 Mr Bradley made his position clear in an email to the directors of 29 November 2013. In that email he raised (again) the role of VSI within the group. While Mr Weston agreed there was nothing improper in Mr Bradley doing so, as noted, impropriety is not the point. The Voltex group was a small business dependent for its success on a high degree of co-operation and trust between its principals. Whether Mr Bradley liked it or not, VSI was structurally part of the Voltex group as a result of the VGH shareholding, and it was reasonable of Mr Weston to consider that it would be managed as such, at least unless and until the directors agreed otherwise. They had not agreed otherwise and did not so agree at the meeting which was held on 3 December 2013.

35 What did happen on 3 December 2013 was, despite any misgivings in the minds of Mr Bradley (who still wanted VSI to be independent) and Mr Weston (who must have recognised by this time that his working relationship with Mr Bradley was troublesome), the impetus towards continuation of the relationship was too great and the BVA was executed by VGH and Mr Bradley. Execution of the BVA, despite the misgivings, is not difficult to understand. The directors still had the Hong Kong and PNG projects on foot and needed VSI and Mr Bradley to take advantage of the opportunity for automation services those projects offered. Mr Bradley could see that VSI had real potential and was keen for the new venture to succeed, given the disappointment of his failed experience with PlantWeave.

36 It was put to Mr Weston that if the directors of VGH had any concerns about Mr Bradley’s competency, they would not have permitted VGH to enter into the BVA. This misses the point. VGH had projects on the go and needed VSI to work to take advantage of the position those projects offered, and needed Mr Bradley for that purpose. The directors made a pragmatic decision. However, that did not mean that they were unconcerned about, not so much Mr Bradley’s competency, but his fit within their business. Mr Weston said as much, describing the decision to proceed with the BVA as one based on an assessment that the business had the pressure of valuable projects, they wanted to make VSI work, and thus were willing to take the “risk” on Mr Bradley.

37 The construction of the BVA is in dispute but one thing that is clear is that in it, the date for the issue of shares to Mr Bradley had been moved backwards to September 2014. Mr Bradley asked about this and Mr Weston explained that it was done to ensure that Mr Bradley was not in breach of the PlantWeave restraint. Mr Bradley must be inferred to have accepted this because he entered into the BVA. Mr Weston’s concern was not unfounded. PlantWeave’s lawyers had written to Mr Bradley on 12 August 2013 raising the issue and possible breach by Mr Bradley of a deed with PlantWeave by reason of Mr Bradley’s involvement with Voltex.

38 The BVA also contained a definition of “Directors” that included Mr Bradley, but he was not appointed as a director of VSI or VSH then or subsequently.

39 Also on 3 December 2013, and reflecting concerns about Mr Bradley’s push for greater autonomy, Mr Bradley was asked to, and did, execute a document called a delegation of authority. Mr Weston said, and I accept, that the directors had not wanted to have such a document in place but felt it was necessary. The document required Mr Bradley to obtain approval from “the Voltex Group” and “VGH” for certain actions. Not unimportantly, this document disclosed that the delegation was for the purpose of ensuring adherence to “Voltex Group global policies and procedures”. It must be inferred that all three directors of VGH knew about and approved of the content of the delegation of authority, by which Mr Bradley’s authority as manager of VSI was subjected to authorisation from “the Voltex Group” and “VGH” for many matters.

40 It was submitted for Mr Bradley that he was entitled to put his views about the role of VSI and it should not be assumed he had no entitlement (as a proposed director and shareholder of VSI) to challenge Mr Weston’s views. This too misses the point. The point is that VSI was part of the Voltex group. Mr Weston had made it repeatedly clear that this was fundamental. The delegation of authority confirmed this to be the position. The other directors must be inferred to have agreed with Mr Weston, because they ensured Mr Bradley signed the delegation of authority. At the same time the directors wanted VSI to work and, it is apparent, Mr Barrera and Mr Ratcliffe wanted the working relationship between Mr Weston and Mr Bradley to improve. But this does not mean that Mr Barrera and Mr Ratcliffe agreed with Mr Bradley that VSI should be managed as if it were not part of the Voltex group.

41 Unsurprisingly, given this dynamic, things did not go well between Mr Bradley and the Voltex group. Before execution of the BVA, Mr Bradley had inquired about the pay rate of Rommel Matheou. Mr Ratcliffe had hired Mr Matheou to work for VPE. He was employed on a casual basis and paid an hourly rate. Mr Matheou had particular expertise that was critical to the Hong Kong project. Mr Barrera emailed Mr Bradley saying “Please do not set any arrangements for Rommel as he is working for VPE. Talk to me first”. But Mr Bradley talked to Mr Matheou and emailed him suggesting a much higher rate of pay for Mr Matheou to work for VSI. Mr Bradley informed Mr Ratcliffe after doing so. Mr Ratcliffe expressed concern about the increase. Mr Barrera got involved. Mr Weston said that the directors thereafter approved the arrangement because they felt they had little choice as Mr Matheou was critical to the success of the Hong Kong project. I accept Mr Weston’s evidence. It is obvious that the directors would have had no reason to increase Mr Matheou’s pay to such an extent. He was due for a pay review by VPE three months after Mr Bradley’s intervention and the directors could have negotiated with him then. Mr Bradley said he began discussing Mr Matheou working for VSI instead of VPE because most of Mr Matheou’s work was done for VSI. This exposes Mr Bradley’s focus on VSI rather than the Voltex group. The effect of Mr Matheou working for VSI instead of VPE was that in future some $744,000 of revenue attributable to his work on the Hong Kong project was booked to VSI, and not to VPE.

42 It was put for Mr Bradley that any concern about Mr Bradley’s conduct with respect to Mr Matheou (or otherwise) were “inventions stubbornly clung to in the context of contested litigation to justify Mr. Bradley’s removal after the event”. This submission is divorced from reality. It may be accepted that the directors approved the transfer of Mr Matheou to VSI at the higher rate of pay. But they did so because they felt they had no choice given Mr Bradley’s discussions with Mr Matheou and the importance of retaining Mr Matheou’s services. It may be accepted further that VGH did not serve on Mr Bradley any notice of breach of the BVA about this or any other issue (if his conduct amounted to breach). But none of this means that the directors did not have genuine concerns about actions Mr Bradley had taken and their impact on the Voltex group. They plainly did, not only about what occurred with Mr Matheou, but about numerous issues all of which, in essence, come back to the point that Mr Bradley wanted VSI to function independently from the Voltex group.

43 In addition to the Hong Kong and PNG projects where VSI had obtained work off the back of the work VPE was doing on those projects, VSI obtained another, smaller, contract working for Horizon Power in Western Australia in late 2013. It was put for Mr Bradley that the work VSI obtained on these projects was a result of quotes Mr Bradley prepared. This is true. Nevertheless, the further suggestion that VSI obtained the work independently because no commercial entity would give VSI the work merely because of VPE’s prior involvement with the customer is unrealistic. It was VPE’s work on those projects which gave VSI the opportunity to quote for the work (and an advantage over competitors in quoting). The fact that VSI did not always succeed in obtaining work off the back of VPE contracts is immaterial and does not indicate to the contrary.

44 The work done by VSI for Horizon Power did not get off to a good start, with Mr Bradley acknowledging that VSI had engaged in “over promising”, and that other errors were made. Later, the work on this project would cause other difficulties for VSI and thus the Voltex group as a whole.

45 Apart from these problems, it must have been apparent to Mr Ratcliffe and Mr Barrera that things had not improved between Mr Bradley and Mr Weston. While Mr Bradley was in Hong Kong, where Mr Barrera and Mr Ratcliffe were working, they arranged a meeting to deal with various issues including “issues with communication”. At the meeting Mr Bradley described Mr Weston as having a “dictator” approach when he was only one of three directors of VGH. It was agreed that given what had been happening between Mr Weston and Mr Bradley there needed to be a clear understanding of the separate roles of each, and the joint roles. It is not entirely clear what this means but some other things are clear – the minutes of the meeting record that VSI was part of the Voltex group and there is no suggestion by Mr Ratcliffe or Mr Barrera that VSI should operate independently from the Voltex group.

46 It is revealing that in an email to Mr Barrera about VSI entering into an agreement to enable it to sell the ETAP Real Time software in Asia, not copied to Mr Weston or Mr Ratcliffe, Mr Bradley said to Mr Barrera that the delegation of authority he had signed did not require approval from the directors of VSI (Mr Weston and Mr Ratcliffe) but from VGH directors so “you [Mr Barrera] have full say and approval”. Again, it may be accepted that each of Mr Weston, Mr Ratcliffe and Mr Barrera were VGH directors and thus had an equal say in group affairs, but it is not difficult to see that having a manager of VSI who used a “divide and conquer” approach to his dealings with VGH directors was a problem and unlikely to be sustainable. In any event, and as to be expected, Mr Weston was unhappy when he found out that Mr Bradley had agreed with Mr Barrera and Mr Ratcliffe about VSI selling the ETAP Real Time software in Asia and made his view clear at a subsequent meeting with Mr Bradley.

47 Yet another autonomy issue arose about action Mr Bradley took in April 2014 to dismiss a VSI employee for changing a quote without approval. During an exit interview in which Mr Ratcliffe was involved, Mr Ratcliffe reached the view that the employee should not have been sacked. Mr Ratcliffe’s email to the employee of 12 April 2014 reinstating him is also revealing. Mr Ratcliffe described his role in the exit interview as representing the interests of Mr Weston, himself, “as well as the Group”. Again, it is not difficult to infer that Mr Ratcliffe thought Mr Bradley had overstepped the mark by peremptorily sacking the employee.

48 Yet another meeting on 4 April 2014 disclosed the problem between Mr Bradley and Mr Weston, which was so serious by this time that Mr Ratcliffe agreed to act as an intermediary. Mr Ratcliffe sent an email to Mr Bradley confirming this arrangement on 13 April 2014. It was put for Mr Bradley that this shows how difficult it was to work with Mr Weston. I disagree. What the email discloses, in my view, is that the directors wanted VSI to work given the ongoing projects in Hong Kong and PNG, and were willing to take action to ensure it could work, despite Mr Bradley’s management style being manifestly disruptive to the Voltex group as a whole.

49 At the same meeting, and in response to a request made by Mr Bradley, it was proposed that given VSI’s financial performance (which was strong given the work on the Hong Kong and PNG projects) Mr Bradley’s loan contributions by way of salary sacrifice to VSI should cease. This subsequently occurred in July 2014, after Mr Weston confirmed in an email of 12 June 2014 that “As VSI is becoming cash positive, it was agreed that Matt’s loan contributions should cease and be capped at the current amount of $16,500”.

50 Another document forwarded by Mr Ratcliffe on 17 May 2014 attaches an agenda of a meeting said to have occurred on 10 April 2014. Whether or not this is so, the relevant point is that the attachment discloses Mr Bradley’s view that treating VSI as an extension of VPE was not what he wanted as VSI would not then be a saleable proposition. He wanted a strategy for VSI adopted which would enable VSI to function as a stand-alone entity. I do not accept that this and similar documents mean that Mr Bradley was in the venture merely to make a “quick profit” and get out. But it is clear that he had a vision for VSI that was different from the directors. The willingness of Mr Barrera and Mr Ratcliffe to listen to Mr Bradley’s views and to explore the best strategy for VSI does not mean that they believed that Mr Bradley was right and Mr Weston wrong.

51 For example, it was put for Mr Bradley that an email dated 18 May 2014 from Mr Ratcliffe, encouraging discussion about VSI’s strategic direction proved that Mr Weston’s evidence, that Mr Bradley was repeatedly raising things that had already been decided, was wrong. The email does not have this effect. The email is directed toward enhanced efficiency between VPE’s business and VSI’s business. It is about what work VSI should focus on and how VSI and VPE could both function and grow without negatively impacting on each other. It does not suggest that Mr Weston was wrong to insist that VSI be managed as part of the overall Voltex group. All of the directors, including Mr Weston, had an interest in seeing VSI gain work and succeed. Mr Ratcliffe’s further communications thereafter about strategy are no different. They do not undermine Mr Weston’s view that VSI was part of the Voltex group and had to be managed as such. They were intended to identify the ways in which VSI could grow as part of the Voltex group, and thus support Mr Weston’s evidence.

52 The suggestion also made for Mr Bradley that Mr Weston just wanted to use VSI as a part of the group to offset losses, and Mr Bradley was right to insist to the contrary, is without foundation.

53 Mr Bradley returned to his theme in a draft business plan he prepared in June 2014. Again, this was presented as Mr Bradley doing no more than trying to get a business plan for VSI adopted and the incapacity of the directors to agree on a plan and strategy for VSI. The reality is Mr Bradley was again pressing his own case for VSI to be independent from the Voltex group. In these circumstances, the fact that a business plan for VSI was never adopted is merely another example of the fundamental difference between the directors and Mr Bradley about the role of VSI. It is not evidence of any dysfunction between the directors, apart from the dysfunction resulting from Mr Bradley’s attempts to have his vision for VSI prevail.

54 The other key fact is that by June 2014, VSI had no significant new confirmed projects in the pipeline. The position remained that VSI’s profit was predominantly driven by the Hong Kong and PNG projects, with the remaining profit resulting from work on only the relatively small Horizon Power project (and one even smaller project not mentioned during the hearing) otherwise obtained by VSI. It was put for Mr Bradley that VSI’s profitability was substantially due to Mr Bradley’s efforts but this is unfounded. VSI was quickly profitable because it had the benefit of VPE having already been involved in the Hong Kong and PNG projects. The transfer of Mr Matheou from VPE to VSI also increased VSI’s revenues. This context must be recognised when dealing with submissions for Mr Bradley to the effect that VSI was the most profitable business in the Voltex group for the 2013/2014 year. It was, but this was in large part because of the transfer of Mr Matheou and wholly because VSI had the benefit of obtaining work off the back of projects in which VPE was already involved.

55 At this point, another submission for Mr Bradley must be rejected. It was put that by this time, seeing how profitable VSI was, the VGH directors then had an incentive (on which they later acted) to ensure they had 100% control of VSI and exclude Mr Bradley. This had to be put squarely to the directors but was not, and is without foundation. It is also inconsistent with the fact that, despite the transfer of Mr Matheou contributing to VSI’s profitability, the directors did not hesitate to ensure Mr Bradley was given a 20% share of a dividend (dressed up as management fees) of $100,000 which was distributed by VSI in September 2014. This payment does not, however, prove that the directors had no problem with Mr Bradley’s management of VSI. As discussed above, they plainly did have a problem and it is not surprising they did. Mr Bradley’s management was incompatible with the status of VSI as a company within a group and created ongoing conflicts. While the conflicts were mainly with Mr Weston, this was not because Mr Weston was out on his own unsupported by the other directors. It was because the other directors were mainly overseas working on projects.

56 Another submission for Mr Bradley also must be rejected. It is that the directors refused to assist Mr Bradley in getting work for VSI. The submission is without substance. Mr Bradley was an experienced business person. He was expected to be able to generate work for VSI. VSI started with the advantage of the work VPE had on the two large projects in Hong Kong and PNG. Despite this, which assisted VSI to obtain work on the same projects, Mr Bradley never succeeded in attracting any substantial ongoing work to VSI. The argument that it must be inferred that the directors held no concerns about the lack of success in obtaining new work because no contemporaneous document discloses such a concern is unpersuasive. It was obvious that new work was not being obtained which, to a business like VSI, must have been of concern. Moreover, such concerns partly explain Mr Ratcliffe’s involvement in VSI strategy, as discussed above.

57 It was submitted for Mr Bradley that the directors did not respond to emails for contacts or business leads in July 2014, accompanied again by the unfounded suggestion that the explanation might be that they wanted him gone so they could gain 100% control of VSI because it had been so successful. A less dramatic explanation is apparent. By June 2014, Mr Bradley had been running VSI for a year. The year had been exemplified by one conflict after another, all basically a result of Mr Bradley’s objective of autonomy for VSI and himself. At the same time, there was no sign that Mr Bradley was succeeding in obtaining new work. It would be no surprise if the directors might have had enough of Mr Bradley by this time and were thinking it might be best if he left VSI, not because they wanted 100% control of VSI, but because the relationship between VSI as managed by Mr Bradley and the Voltex group was manifestly dysfunctional.

58 Consistent with this inference, the directors arranged a meeting with Mr Bradley on 15 July 2014 in Brisbane. Before the meeting the directors discussed and agreed that Mr Bradley should be asked to leave VSI. It was put to Mr Weston that he had made this decision before any discussion with the other directors, which he denied. I accept Mr Weston’s evidence. I accept that Mr Weston wanted Mr Bradley to go but felt he could only make his mind up in consultation with the other directors.

59 At this meeting, Mr Bradley was told that they considered it best if they and he went their separate ways. There is a dispute about the exact terms of the conversation but the relevant parts are that Mr Bradley agreed the relationship should end and, I accept based on Mr Ratcliffe’s evidence, raised the issue of payment out for his shares (which, in accordance with the BVA which provided for issue of the shares from September 2014, had not yet been issued to him). In any event, there is no doubt that payment out for the unissued shares was an issue to be resolved in the context of Mr Bradley exiting VSI because Mr Bradley sent an email on 18 July 2014 to the directors expressing both his disappointment about but understanding of their position, and asked for the directors’ preferences for his “shareholding exit” to be identified, on the basis that the “sale” would be to the VGH group.

60 I also consider it clear that in the minds of Mr Weston and Mr Ratcliffe at least, Mr Bradley was not entitled to any shares because they thought that he had not made contributions satisfying the requirement of the BVA. I do not accept that they were giving other than honest evidence when they said this, nor that it is inconsistent with their conduct. It is apparent that, rightly or wrongly, with Mr Bradley’s exit in mind, they formed a view that there was no entitlement on Mr Bradley’s part to 20% of the shares in VSI in the circumstances.

61 It was put for Mr Bradley that a subsequent conversation with Mr Ratcliffe disclosed that Mr Barrera and Mr Ratcliffe wanted Mr Bradley to stay, and only Mr Weston wanted Mr Bradley gone. I disagree. Mr Barrera had a relationship with Mr Bradley before VSI and, I accept, even after the July 2014 meeting wanted or hoped things could be worked out so Mr Bradley could stay. Mr Ratcliffe knew this to be Mr Barrera’s position. But this does not mean that Mr Weston had made the decision that Mr Bradley should leave VSI on his own. It means only that the other directors left open the possibility that the agreed position might change. Mr Ratcliffe’s view, which he expressed to Mr Bradley, was that if Mr Bradley wanted to stay then he had to win major work for VSI because all of VSI’s work had been derived from VPE’s work. What this conversation discloses is that, contrary to the submissions for Mr Bradley, concerns about Mr Bradley’s apparent inability to gain work for VSI were real and, if not the reason for the directors wanting Mr Bradley to leave (dysfunction being the operative reason), were a relevant background factor. Mr Ratcliffe’s willingness to have this conversation also shows that far from the directors wanting to have 100% of VSI to themselves, they wanted to see VSI succeed, and two of them might have been willing to reconsider Mr Bradley’s exit if Mr Bradley managed to win work for VSI. This does not show, however, that Mr Ratcliffe believed that Mr Bradley was entitled to 20% of the shares in VSI. It shows that Mr Ratcliffe’s interest was the success of VSI.

62 The submissions for Mr Bradley attacked the credit of Mr Ratcliffe (and Mr Weston), it being put that Mr Ratcliffe’s speculation in his affidavit that Mr Bradley might have been involved in directing work to an entity other than VPE in the PNG project was “outrageous”, an example of the “desperate” attempts by the respondents to “throw mud” at Mr Bradley to “justify their actions on 30 January, 2015” (when Mr Bradley’s services were purportedly terminated) and “transparently untrue”. I reject these submissions. Mr Ratcliffe never suggested that when the work was being carried out in 2014 it crossed his mind that Mr Bradley might have directed work away from VPE, in his own interests of currying favour with the other entity. His speculation was presented as the “only explanation” he could think of at the time of preparing his affidavit given that VPE could have done the work. The fact that there were communications from Mr Bradley to Mr Ratcliffe at the time saying that the client wanted the other entity to do the work does not mean that Mr Ratcliffe was engaging in “outrageous” and “untrue” allegations. Mr Ratcliffe accepted that, at the time, what Mr Bradley said seemed reasonable and that he did not then “question his capability or his motives”. It is only later, after the relationship breakdown, that Mr Ratcliffe had any reason to question Mr Bradley’s motives. His speculation, in terms, rose no higher than that. Mr Ratcliffe’s expression of the speculation did not undermine his credibility as a witness, which I accept.

63 In any event, despite Mr Ratcliffe’s encouragement, the fact is that Mr Bradley never won any other significant work for VSI, despite continuing to work at VSI for another six months.

64 Another thing that occurred later in July 2014 was that VSI repaid to Mr Bradley the balance of the money that he had salary sacrificed.

65 It was submitted for Mr Bradley that the lack of any communication from the respondents disputing his entitlement to the 20% shareholding, despite repeated efforts by Mr Bradley to resolve the issue, and the absence of any suggestion of breach by him of the BVA, puts their complaints about his management of VSI “in an extremely poor light”. I disagree. The complaints of the respondents about Mr Bradley reflect what was happening at the time and are not a recent invention to justify Mr Bradley’s termination. It did not take a notice of breach of the BVA, or even an allegation of breach, for it to be apparent that Mr Bradley’s management of VSI was incompatible with the harmony of the Voltex group as a whole. As noted, it would be one thing to put up with the problems if Mr Bradley was winning substantial work for VSI. It was obviously another when he was not.

66 The same conclusion applies to the payment to Mr Bradley of the 20% share of the $100,000 dividend from the profits of VSI which was paid in September 2014. The payment is not inconsistent with Mr Ratcliffe and Mr Weston considering that Mr Bradley had no entitlement under the BVA to a 20% shareholding. The payment had been proposed many months earlier when it appeared that VSI would post a healthy profit, with an 80/20% split in accordance with what Mr Weston described in an email of 12 June 2014 as “ownership plans”. The payment was in accordance with what had been proposed when it was assumed that Mr Bradley would remain at VSI.

67 This does not mean that there was no problem with the lack of response from the directors about the position in respect of Mr Bradley’s shares. But the evidence discloses why there was no response. Mr Weston and Mr Ratcliffe thought he had no entitlement. Mr Barrera still preferred Mr Bradley to stay with VSI, if a way forward could be worked out. In other words, the directors had not agreed a joint position about the shares, and thus did not respond to Mr Bradley about his shares or his exit date from VSI.

68 The lack of communication with Mr Bradley about the issue does not mean the directors were not thinking about it. On 22 September 2014, Mr Weston sent an email to Mr Ratcliffe and Mr Barrera, discussing the appropriate payment to be made. It was put for Mr Bradley that the email is inconsistent with Mr Weston believing Mr Bradley had no entitlement to shares. I disagree. Read as a whole, what emerges is that Mr Weston thought Mr Bradley had not contributed as required by the BVA and thus had no legal entitlement to the shares or a payment out for them, but that the BVA could be used to assess what might or might not be fair for an ex gratia pay out to Mr Bradley. Mr Weston thought using the formula in the BVA as the basis for any such payment would be unfair. He suggested a payment equivalent to 20% equity in VSI as calculated by the company’s accountant.

69 Mr Bradley repeatedly tried to get clarification over the next few months but it is apparent that the directors had still not resolved their agreed position. Again, it was put for Mr Bradley that their silence was inconsistent with any belief in the directors’ minds that he was not entitled to 20% of the shares under the BVA, and that Mr Weston and Mr Ratcliffe invented this after the event. I disagree, for the reasons already given. Throughout this period, the directors were trying to work out what should be paid to Mr Bradley but, in the minds of Mr Weston and Mr Ratcliffe at least, this was a payment outside the terms of the BVA. Mr Ratcliffe also said, and I accept, that the directors were extremely busy at this time given VPE’s ongoing work in Hong Kong, PNG and on other projects, and thus did not manage to agree about what should be done in respect of Mr Bradley’s exit between July and December 2014.

70 It is regrettable that the directors did not manage to agree a position and communicate it to Mr Bradley over this period. It should be appreciated, however, that Mr Bradley continued to work for VSI, being paid his salary equivalent to $200,000 per year. Further, while he did not know what the directors’ view about his shareholding was, despite the issue date in the BVA (September 2014) passing, he did know that he had not been issued shares and had not received any response to his requests for clarification. I consider that far from silence confirming that shares would be issued, the silence meant that Mr Bradley must have known there was an issue about his entitlement to shares from the directors’ (or VGH’s) perspective. So much would have been obvious from the lack of any response to his repeated requests for clarification.

71 The contemporaneous documents support this conclusion. In one of his emails, of 8 November 2014, Mr Bradley said that his preference was to work for VSI for a full two years (that is, until June 2015). This, of course, was the relevant period under the BVA to obtain protection from forfeiture of shares for an early (within two years) exit. In other words, it is clear that Mr Bradley believed that had he been issued shares and had he wished to exit as a shareholder within two years, his shares would have been forfeited. He wished to avoid this possibility, but to do so could not leave VSI before the two year period had expired.

72 As a result, submissions to the effect that Mr Bradley stayed on working at VSI after July 2014 in reliance upon some kind of representation that there was no issue about his entitlement to shares defy common sense. If it had been common ground that he had the entitlement he would not have felt the need to have clarification from the directors. Further, the directors would have had no reason not to clarify the position quickly. Their continued silence in the face of Mr Bradley’s repeated requests would have spoken volumes to him – he would have known that the directors (or some of them) did not necessarily agree that he was entitled to a shares (or payment out instead) under the BVA, but he chose to stay working for VSI because it suited him to do so, given his awareness of the terms of the BVA and the relevance of the two year period. The two year period was not relevant from the directors’ perspective, however, because Mr Weston and Mr Ratcliffe at least (the majority) believed that Mr Bradley had no entitlement to the shares in any event.

73 As I have said, I reject the submission that the directors’ intent in removing Mr Bradley was to gain control of 100% of the financial rewards offered by the VSI business. The relationship was not working. Mr Bradley’s objectives for VSI, and his management style were incompatible with the operation of the Voltex group as a whole. This incompatibility was a bona fide reason for the directors’ wish to terminate Mr Bradley’s management of VSI. Mr Bradley knew this as well as the directors did. Mr Bradley effectively accepted as much in his email of 8 November 2014 to Mr Barrera, in which he said:

As discussed:

What do I want to do? We need to continue what we started in July, get divorced. It just is not going to work. There is a fundamental misalignment on too many levels. Deep down I think it is the right thing to do, as disappointing as it is for me to lose the opportunity.

1. A good result for everyone.

1. For VGH an ongoing successful energy integration business.

2. For Matt a good payout and exit/ongoing employment/consulting

3. Future partners.

2 Exit the business as a shareholder, Reasons for exiting

1. Agreement was reached that it would be better for Matt to exit in July 2014, this is where my head is at. Agree that want to complete original 2 years and see VSI continue with success.

2. Original desire to do software business, moving towards this.

3. Conflict between individuals, Mick and Matt don’t play well together. Isolating Mick from the interface will just manifest further discontent. You need to remove me from the picture, so VHG Group can refocus on success.

4. Conflict of interests at shareholding and directors levels (What’s best for the group versus individual companies VSI).

5. Conflict at objectives, e.g. VGH grow for 10 years and sell, Matt move on in 2-3 years to do software business

6. Conflict at operational levels

7. I am seen as a necessary evil…this is not good business, you want someone you can trust and believe in running VSI.

8. I am not a good employee, have been too long doing my own thing

9. Misalignment/different paradigms/culture of operation – e.g. I cause to many problems doing the wrong thing. [sic] (emphasis removed)

74 In this email, Mr Bradley suggested a plan be created for a shareholder exit and sale using calculations as per the BVA, with a transition period operating until June 2015 (the end of the two year period under the BVA), when Mr Bradley would cease to manage VSI.

75 The submissions for Mr Bradley urged acceptance of contemporaneous records as the best evidence of what occurred, in preference to subsequent recollections. At least insofar as documents exist and do not show the signs of being self-serving at the time created, I agree with this approach. But there is a difference between accepting contemporaneous documents as good evidence about the matters to which they refer and drawing an inference that a lack of contemporaneous documents about an issue means the issue did not exist (the latter being approach put for Mr Bradley).

76 In any event, the email from Mr Bradley of 8 November 2014 is good evidence of what happened between the directors and Mr Bradley. It exposes exactly why the relationship had failed and why the directors were acting bona fides in deciding that Mr Bradley had to leave the business. The email is also inconsistent with the case theory for Mr Bradley that the directors were acting in bad faith (in order to gain 100% control of VSI) and that he was somehow duped into continuing to work for VSI after July 2014 on a promise that he would receive the 20% shareholding or the value equivalent to it calculated in accordance with the BVA. It is apparent that Mr Bradley was staying, not because he believed the relationship was successful and he wished to remain, but because he thought it was in his best interests, including securing his right to the 20% shares or what he believed was his entitlement to a buy out of the shares for value rather than forfeiture under the BVA.

77 Finally, on 30 January 2015 Mr Weston met Mr Bradley and said the directors had agreed that Mr Bradley’s role with VSI should be terminated immediately, he would be paid $40,000, the offer was open for 7 days, and was conditional on Mr Bradley signing a release.

78 Mr Bradley responded by email on the same day. Tellingly, the email does not express surprise at the offer. It says only that Mr Bradley wanted justification for the value of the offer and the “early” (that is, before his preference of June 2015) termination. This is consistent with the conclusions above. Mr Bradley believed he was entitled to the shares but decided to continue working for VSI to avoid forfeiture of his rights under the BVA, despite knowing that the directors did not necessarily share his view about his entitlement.

79 On 2 February 2015, Mr Bradley repeated his position that his 20 shares as per the BVA should be issued. There was no response but, again, this does not mean Mr Bradley believed the shares would be issued. To the contrary, by 4 February 2015, he had consulted a solicitor and advised the directors that he would not cease working at VSI “until an agreement is reached”. This must mean an agreement about the shares to which he believed he was entitled. The relevant point is that this position was also consistent with Mr Bradley’s earlier position – he was staying at VSI because he considered that the best way to achieve what he wanted (the issue of the shares or equivalent value calculated under the BVA rather than forfeiture by reason of an early exit) and it suited him to do so.

80 This prompted a letter from VSI to Mr Bradley, which each director signed on 4 February 2015, saying that formal notice of termination had been given to him on Friday, and:

Voltex is willing to pay to you an additional amount for services for the month of February, although we do not require those services to be provided. I request that you issue an invoice to us for payment in accordance with the prior monthly contractual payments. You are otherwise not entitled to any further payments from Voltex.

81 This discloses the lack of focus by all of the parties on the difference between the BVA and the contract of employment. It seems that this letter was seen by all to be, or to confirm, the termination of the BVA and the contract of employment between VSI and Mr Bradley. In any event, Mr Bradley did not work for VSI after 4 February 2015. He was not paid $40,000. Nor was he paid anything for February 2015, although it is unclear whether any such invoice was rendered, the most recent invoice in evidence referring to services in January 2015. While non-payment was said to show the high-handed approach of Mr Weston in particular, the lack of payment may not be unconnected to the fact that Mr Bradley commenced these proceedings in March 2015.

82 As noted, the directors also later paid themselves another $100,000 dividend from VSI for the 2014/2015 financial year but, by that time, were engaged in this litigation so, again, Mr Bradley got no part of this payment.

83 Much was made of the fact that VSI’s revenues collapsed after Mr Bradley left, in order to support the submission that he was responsible for VSI’s early success and that the directors undermined VSI’s value by not replacing Mr Bradley and trying to continue VSI’s work themselves when they had no handover from Mr Bradley and another VSI employee, Mr Hess, who also left. It is accurate to say that Mr Bradley was not replaced and VSI’s revenues collapsed but, otherwise, the submission is unfounded. As noted, VSI was successful because it had immediate access to a large volume of work off the back of the contracts VPE had in place. Otherwise, the only significant work Mr Bradley won was Horizon Power. Horizon Power was not well managed and after Mr Bradley left, VSI had to perform major rectification work at its own cost. Whether this is Mr Bradley’s fault or not is not the real point. The point is that the client was unhappy with VSI, and efforts were made in 2015 after Mr Bradley had left to ensure the client was satisfied. This was reasonable and appropriate. I thus accept the submissions put for the respondents about the problem which Mr Bradley left for them in terms of Horizon Power, as follows:

… the notion that the Horizon’s sign off on the project absolved VSI of responsibility for the system’s deficiencies might be contractually correct but is commercially unreal. The client’s infrastructure had not been properly assessed to determine whether the system could function. The program the client had paid for did not work. The client was dissatisfied. Bradley did not inform the VPE Principals of any of the difficulties despite the obvious risk of disputation.

Whether or not is was contractually obliged to do so, the reality is that VSI, for commercial and reputational reasons, had no option but to carry out the rectifications works that it did.

84 Further, the work in Hong Kong and PNG was always going to run out. As noted, one of the concerns the directors had with Mr Bradley was the lack of new work which he had obtained. Revenues were bound to drop catastrophically after the completion of the work in Hong Kong and PNG unless Mr Bradley managed to find substantial new work, which he did not. Thus, while VSI was still earning money in January 2015, this does not mean the business was not in decline at that time. It was in decline because it had no secured work in the pipeline. Contrary to the submissions for Mr Bradley, business development was his responsibility. It is referred to in the responsibilities of both VGH and Mr Bradley in Schedules 1 and 2 of the BVA, but Mr Bradley was the sole full time manager of VSI being paid a salary by that business. It was fundamental to his role that he obtain work for VSI. His conduct in preparing quotes and seeking new clients confirms that he understood this to be the case. The point is not that he did not try to do so; it is that despite his efforts for 18 months, he did not succeed other than in limited respect of the projects identified above.

85 Mr Bradley emphasised an observation by Mr Lytras, a valuer called by the respondents, that VSI was dependent on Mr Bradley’s specialist skills and “Mr Bradley’s departure would reasonably have significantly diminished VSI’s prospects”. There is no doubt VSI was dependent on Mr Bradley’s specialist skills. This was the reason VGH entered into the BVA. However, Mr Bradley’s specialist skills were of no material utility if he could not win ongoing work for VSI. There is no basis to infer that had Mr Bradley stayed until June 2015, as he wished, VSI’s financial performance would have been materially different from what it was. The fact that Mr Bradley and Mr Hess were not replaced is immaterial unless it can be inferred that there would have been new work for VSI to do in that period, but none of the tenders Mr Bradley submitted came to fruition, and there is no basis to think that a further 6 months would have resulted in any significant new project being secured by VSI.

86 Nor does the payment of $100,000 to VGH by VSI in the period between January and June 2015 indicate to the contrary. It is not in dispute that while the Hong Kong and PNG projects were continuing in 2014, VSI had a good revenue stream. The issue is that it did not have a viable future once that work was completed. The payment of a profit share of $100,000 for the 2014/215 financial year was a result of the early success of VSI off the back of contracts held by VPE.

87 After Mr Bradley left, it is no particular surprise that the directors decided to try to keep VSI going themselves in preference to finding a substitute for Mr Bradley; bringing Mr Bradley on board had failed. However, the directors had always been very busy with VPE work and, taking into account the work needed to rebuild the relationship with Horizon Power and thus protect the reputation of the Voltex group, it is also no surprise that they had no capacity to find new work for VSI. But this position was no different from that when Mr Bradley was in charge of VSI. VSI thus withered on the vine, but not due to any deliberate ploy by the directors to destroy the value of Mr Bradley’s asserted equity. Given their own investment in VSI, the directors had no reason to wish to do so and thereby destroy the value of their own majority equity in VSI.

88 Having explained the rocky course of the dealings between Mr Bradley and the respondents, consideration can now be given to the claims for damages for contractual breach and unconscionable conduct.

The contractual claims

Construction of the BVA

89 The relevant principles of construction are well-known, and have been expressed in many decisions.

90 It is convenient to refer to Electricity Generation Corporation v Woodside Energy Ltd [2014] HCA 7; (2014) 251 CLR 640 in which French CJ, Hayne, Crennan and Kiefel JJ said at [35] (citations excluded]:

…this Court has reaffirmed the objective approach to be adopted in determining the rights and liabilities of parties to a contract. The meaning of the terms of a commercial contract is to be determined by what a reasonable businessperson would have understood those terms to mean. That approach is not unfamiliar. As reaffirmed, it will require consideration of the language used by the parties, the surrounding circumstances known to them and the commercial purpose or objects to be secured by the contract. Appreciation of the commercial purpose or objects is facilitated by an understanding “of the genesis of the transaction, the background, the context [and] the market in which the parties are operating”. As Arden LJ observed in Re Golden Key Ltd [[2009] EWCA Civ 636 at [28]], unless a contrary intention is indicated, a court is entitled to approach the task of giving a commercial contract a businesslike interpretation on the assumption “that the parties … intended to produce a commercial result”. A commercial contract is to be construed so as to avoid it “making commercial nonsense or working commercial inconvenience”.

91 The submissions for Mr Bradley also referred to another principle which should be identified. It is that it is presumed that the parties to an agreement did not intend that one or other of them could take advantage of their own breach. The relevant principles were identified by Sackar J in Sydney Attractions Group Pty Ltd v Schulman [2013] NSWSC 858 as follows:

[188] The legal principles in this area are not controversial. In Alghussein Establishment v Eton College [1991] 1 All ER 267 the House of Lords was faced with a question of construction. A literal construction of the relevant provision of a lease would have led to an absurd result that a contractor who failed to complete a development without fault could not call for a lease, whereas a contractor who wilfully defaulted could do so. Lord Jauncey’s judgment (with which the other Law Lords agreed) was, as noted in the headnote to the report, to the effect that:

in the absence of clear express provisions in a contract to the contrary it was not to be presumed that the parties intended that a party should be entitled to take advantage of his own breach as against the other party was not limited to cases where a party was relying on his own wrong to avoid his obligations under the contract but applied also where a party sought to obtain a benefit under a continuing contract on account of his breach.

…

The principle that a party in default under a contract cannot take advantage of his own wrong is in general a rule of construction rather than an absolute rule of law and morality, although there may be situations, such as self-induced frustration, where an absolute rule exists.

[189] The principle was accepted, without much elaboration, in TCN Channel 9 Pty Ltd v Hayden Enterprises Pty Ltd (1989) 16 NSWLR 130 (at 147 per Hope JA, with whom Priestley and Meagher JJA agreed).

[190] In Brothers v Park (2004) 12 BPR 98,114, Giles JA (with whom Ipp JA [and] Wood CJ at CL agreed) said (at [82]):

[82] There was reference … to a … principle, described by Lord Diplock in Cheall v Association of Professional Executive Clerical and Computer Staff [1983] 2 AC 180 at 189 that “a man cannot be permitted to take advantage of his own wrong”. An application of the principle is that a party to a contract terminating upon an event or conferring a benefit upon an event can not rely on his own breach of contract bringing about the event; many of the cases are discussed in the speech of Lord Jauncey in Alghussein Establishment v Eton College [1988] 1 WLR 587, and a local illustration of this application is TCN Channel 9 Pty Ltd v Hayden Enterprises Pty Ltd (1989) 16 NSWLR 130 at 147–8,161. It is applied as a rule of construction (ibid), but has also been seen as an implied term: Thompson v ASDA-MFI Group Plc [1988] Ch 241; [1988] 2 All ER 722. The principle itself has a broader reach, for example in the interpretation of statutes (Grozier v Tate (1946) 16 LGR (NSW) 57 at 61; Allen v Bega Valley Council (NSWCA, Full Court, No CA 40500 of 1994, 22 December 1994, unreported, BC9403478)) and in the common law rules that an arsonist cannot recover under a fire insurance policy and murderer cannot claim in the estate of his victim.

[191] Giles JA, in the later case of Ruthol Pty Ltd v Tricon (Australia) Pty Ltd (2005) 12 BPR 98,225 gave further consideration to the principle and said (at selected passages from [19]–[24], Santow JA and Hunt AJA agreeing):

[19] … the principle is not concerned with arriving at compensatory damages for breach by the wrongdoer, but with whether the wrongdoer can enforce its contractual right.

[20] … in the absence of clear words, a contractual entitlement upon a particular event will not be enlivened if the event came about through breach of the party seeking to rely on it …

[21] … But … the operation of the principle is qualified … [citing Hooper v Lane (1859) 6 HL Cas 443 at 460–461 per Bramwell B]:

… that rule only applies to the extent of undoing the advantage gained, where that can be done, and not to the extent of taking away a right previously possessed. Thus, if A lends a horse to B, who uses it, and puts it in his stable, and A comes for it and B is away, and the stable locked, and A breaks it open, and takes his horse, he is liable to an action for the trespass to the stable, and yet the horse could not be got back, and so A would take advantage of his own wrong.

[22] Thus a party in breach of contract may be precluded from relying on a contractual entitlement arising from the breach, but will not be precluded from relying on a contractual entitlement which does not arise from the breach.

…

[24] … the maxim only applies to the extent of undoing the advantage gained by the wrongdoer and not the extent of taking away a right previously possessed.

[192] Ruthol involved a breach of a contract for the sale of land by the vendor. The vendor did not complete a contract for sale of land on the date fixed for completion. The purchaser was in possession as lessee. The vendor/lessor claimed arrears of rent from the date of contractual completion to the date of actual completion. The purchaser submitted that the vendor was prevented from relying upon its own wrong. The purchaser claimed damages for breach by the vendor. After discussing the principle that a party cannot take advantage of its own breach (see quoted passages above), Giles JA held that the principle had no application to the case (at [25]):

[25] In my opinion, the principle did not apply to preclude the appellant from recovering the rent claimed. The respondent was obliged from the beginning to pay the rent to the appellant for the term of the lease and while holding over as a monthly tenant, and to pay it without any set-off or deduction. The respondent remained in possession of the property, and its right to possession was referable only to its position as lessee and then as tenant holding over; it did not have a right to possession under the uncompleted contract for sale. The appellant’s breach of contract by failing to complete the contract for sale on 19 July 2001, or its breach of a contract found in the lease with its option to purchase rather than the contract for sale (which I doubt is correct), meant that the respondent was obliged to pay the rent for longer than would otherwise have been the case; but the obligation to pay the rent did not arise from the breach of contract.

92 Otherwise I accept the submissions for the respondents that:

(e) The contract should be construed as a whole and in a way which allows its various provision[s] to be read harmoniously: Australian Broadcasting Commission v Australasian Performing Right Association Ltd (1973) 129 CLR 99 at 109.

(f) As a corollary, a contract should be construed so as to give effect to each part of it on the basis of a presumption that each provision has been inserted intentionally: Chapmans Ltd v Australian Stock Exchange Ltd (1996) 67 FCR 402 at 411; Perpetual Custodians Ltd v IOOF Investment Management Ltd [2013] NSWCA 231; (2013) 278 FLR 49 at [80]–[82].

(g) Apparent internal inconsistency between provisions is to be resolved on the basis that one provision qualifies the other and, hence, that both have meaning and effect: Re Media Entertainment & Arts Alliance (No 1) (1993) 178 CLR 379 at 386-387.

93 For the present case, it is also worth emphasising the further statement in Australian Broadcasting Commission v Australasian Performing Right Association Ltd (1973) 129 CLR 99 at 109-110 that: