FEDERAL COURT OF AUSTRALIA

Woodings, in the matter of the Bell Group Limited (No 2) [2016] FCA 1126

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

(a) in the case of those Bell Group companies ordered to be wound up before 23 June 1993, namely:

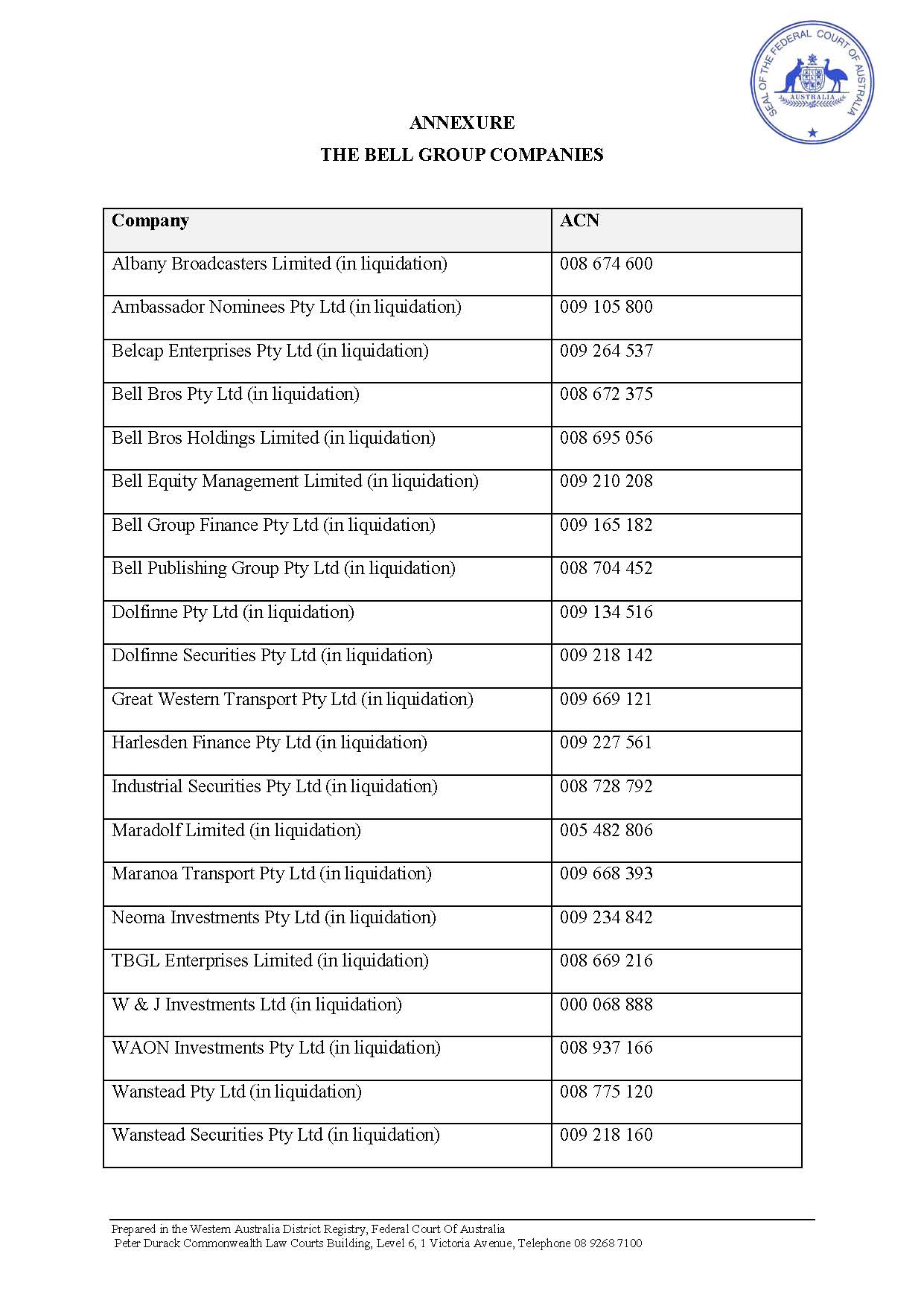

(i) The Bell Group Limited (in liquidation) ACN 008 666 993;

(ii) Albany Broadcasters Limited (in liquidation) ACN 008 674 600;

(iii) Bell Bros Holdings Limited (in liquidation) ACN 008 695 056;

(iv) Bell Group Finance Pty Ltd (in liquidation) ACN 009 165 182;

(v) Bell Publishing Group Pty Ltd (in liquidation) ACN 008 704 452;

(vi) W&J Investments Pty Ltd (in liquidation) ACN 000 068 888; and

(vii) Wigmores Tractors Pty Ltd (in liquidation) ACN 008 679 221,

s 479(3) of the Corporations Law (as applied by s 1408(1) of the Corporations Act 2001 (Cth));

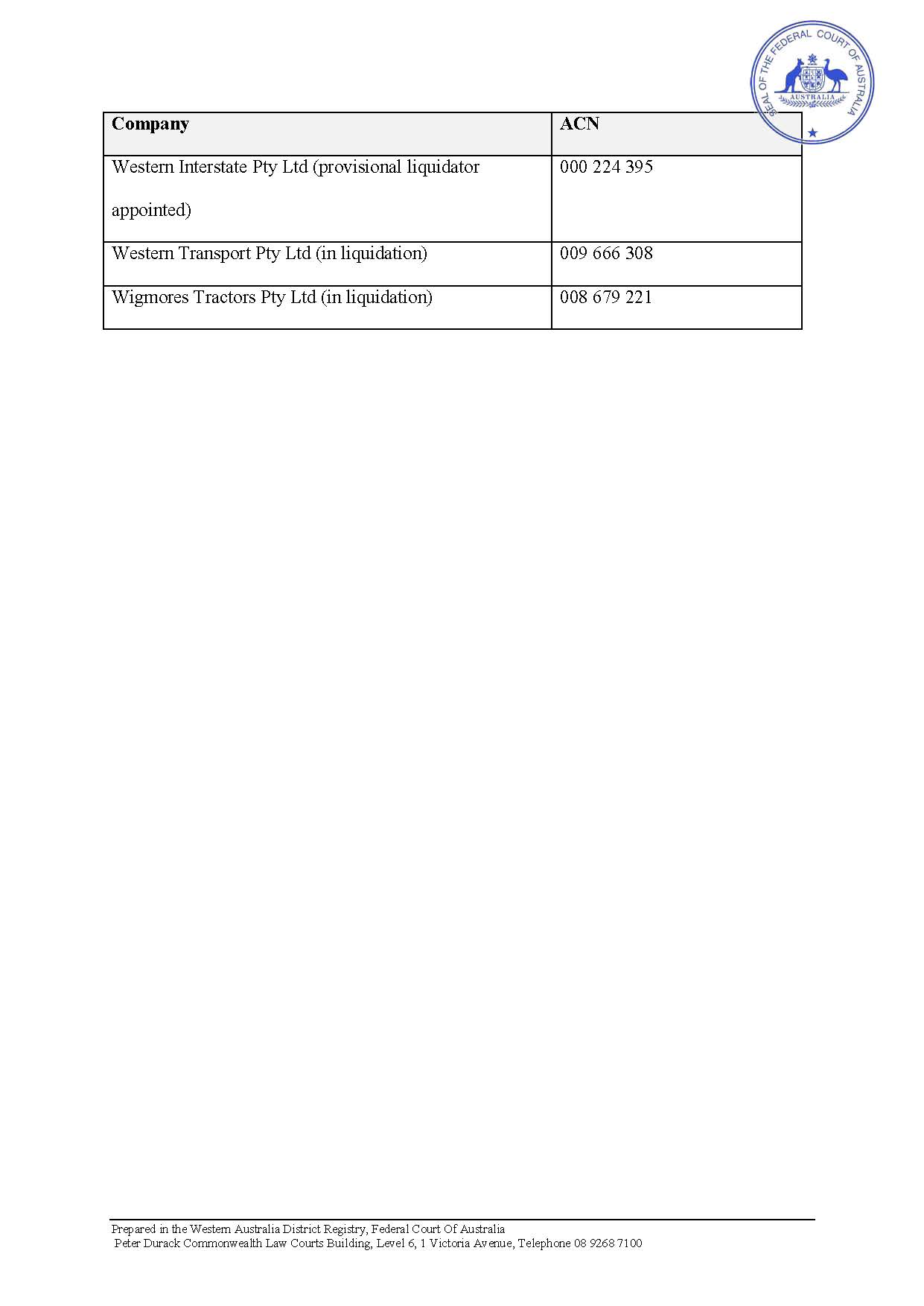

(b) in the case of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395, the inherent or implied jurisdiction of the Court (and, if and to the extent required, s 479(3) of the Corporations Act 2001 (Cth)); and

(c) in the case of the Bell Group companies other than those ordered to be wound up by the Court before 23 June 1993 and Western Interstate Pty Ltd (provisional liquidator appointed), s 479(3) of the Corporations Act 2001 (Cth),

it is directed that the plaintiff (as liquidator or provisional liquidator, as the case may be) will be acting properly and is justified in causing each of the companies as listed in the annexure to these orders (Bell Group companies) to enter into and perform a funding and indemnity agreement that is in or substantially in the form of the document that is attachment "ALJW-72" to the affidavit of the plaintiff sworn 20 July 2016 and filed herein.

2. The plaintiff as liquidator of:

(a) Ambassador Nominees Pty Ltd (in liquidation) ACN 009 105 800;

(b) Belcap Enterprises Pty Ltd (in liquidation) ACN 009 264 537;

(c) Bell Bros Pty Ltd (in liquidation) ACN 008 672 375;

(d) Bell Equity Management Limited (in liquidation) ACN 009 210 208;

(e) Dolfinne Pty Ltd (in liquidation) ACN 009 134 516;

(f) Dolfinne Securities Pty Ltd (in liquidation) ACN 009 218 142;

(g) Great Western Transport Pty Ltd (in liquidation) ACN 009 669 121;

(h) Harlesden Finance Pty Ltd (in liquidation) ACN 009 227 561;

(i) Industrial Securities Pty Ltd (in liquidation) ACN 008 728 792;

(j) Maradolf Limited (in liquidation) ACN 005 482 806;

(k) Maranoa Transport Pty Ltd (in liquidation) ACN 009 668 393;

(l) Neoma Investments Pty Ltd (in liquidation) ACN 009 234 842;

(m) TBGL Enterprises Limited (in liquidation) ACN 008 669 216;

(n) WAON Investments Pty Ltd (in liquidation) ACN 008 937 166;

(o) Wanstead Pty Ltd (in liquidation) ACN 008 775 120;

(p) Wanstead Securities Pty Ltd (in liquidation) ACN 009 218 160; and

(q) Western Transport Pty Ltd (in liquidation) ACN 009 666 308,

has approval under s 477(2B) of the Corporations Act 2001 (Cth) to enter into and cause those companies to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-72" to the affidavit of the plaintiff sworn 20 July 2016 and filed herein.

3. The plaintiff as provisional liquidator of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395 has approval under s 477(2B) (as applied by s 472(5) of the Corporations Act 2001 (Cth)) to enter into and cause that company to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-72" to the affidavit of the plaintiff sworn 20 July 2016 and filed herein.

4. The costs of the application are costs in the windings up of The Bell Group Limited (in liquidation) and Bell Group Finance Pty Ltd (in liquidation) in equal proportions.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MCKERRACHER J:

INTRODUCTION

1 The plaintiff, as liquidator or provisional liquidator of various Bell Group companies, applied for directions and approval to enter into a funding and indemnity agreement, together with various ancillary orders. I made the orders sought on 11 August 2016 for the following reasons.

2 The plaintiff applied for similar orders in October 2015, in support of which he relied upon his affidavit sworn 1 October 2015 (First Affidavit), as supplemented by a further affidavit sworn 26 October 2015. The Court made those orders on 28 October 2015 and the plaintiff entered into the relevant funding and indemnity agreement (original funding and indemnity agreement) shortly thereafter. On 14 April 2016, the Court published reasons for making the orders: Woodings, in the matter of the Bell Group Limited [2016] FCA 369 (Bell No 1).

3 The original funding and indemnity agreement was short-lived. Its funding mechanism ceased operation in respect of costs or liabilities incurred after the point at which the ‘transfer day’ arose under the Bell Group Companies (Finalisation of Matter and Distribution of Proceeds) Act 2015 (WA) (Bell Act), being 27 November 2015.

4 The High Court of Australia determined the Bell Act to be invalid in its entirety on 16 May 2016. Shortly after, in view of the expiry of the funding mechanism under the original agreement and the prevailing circumstances, the plaintiff applied to the Court on 20 July 2016 (supported by an affidavit sworn 20 July 2016) (Third Affidavit) for, essentially, an expansion of the relief he sought in October 2015.

5 In substance, the plaintiff sought:

a direction that he will be acting properly and is justified in causing the relevant Bell Group companies to enter into a new funding and indemnity agreement, which is substantially the same terms as the original agreement (the Further MT Funding Agreement); and

an order for approval to enter into the Further MT Funding Agreement.

6 Under the Further MT Funding Agreement, one Bell Group company, Maranoa Transport Pty Ltd (in liquidation), will assume the funding of 50% of the costs of the windings up of the Bell Group companies from the date that the original funding and indemnity agreement ceased to operate. Previously that 50% was met by the Bell Group’s treasury company, Bell Group Finance Pty Ltd (BGF).

7 The directions were sought, as on the previous occasion, because the plaintiff apprehends there may be a perception that in making the decision to cause the relevant Bell Group companies to enter into the Further MT Funding Agreement he is in a position of potential or apparent conflict of interest or duty.

8 Approval is required as obligations under the Further MT Funding Agreement will continue for more than 3 months: see s 477(2B) of the Corporations Act 2001 (Cth) (and, as to the company in provisional liquidation, s 472(5), which in turn applies s 477(2B).)

RELEVANT STATUTORY PROVISIONS

9 As set out in Bell No 1 (at [28]-[29]), two slightly different statutory regimes apply. This is because six of the Bell Group companies were ordered to be wound up before 23 June 1993.

10 In summary, and as was the case in Bell No 1:

As to the application for directions, the application invokes s 479(3) of the Corporations Law of Western Australia as applied by s 1408(1) of Corporations Act (in relation to the pre-23 June 1993 windings up) and s 479(3) of the Corporations Act (in relation to the post-23 June 1993 windings up). There is no material difference in the two relevant statutory provisions.

As to the application for approval, the application invokes s 477(2B) of the Corporations Act (in relation to the post-23 June 1993 windings up). There is no equivalent statutory provision in the ‘old winding up law’ that applies to the pre-23 June 1993 windings up. Accordingly, no approval is required in relation to the six Bell Group companies that were wound up by orders made before 23 June 1993.

Directions under s 479(3)

11 Consistent with the relevant principles outline in Bell No 1 at [33]-[38]), the directions sought in the present context:

(1) are in terms that the plaintiff may ‘properly and justifiably’ take certain action. Accordingly, there is an issue of propriety or reasonableness, such that directions are available and appropriate; and

(2) arise in a circumstance where there may be a perception that in making a decision to cause the relevant Bell Group companies to enter into the Further MT Funding Agreement the plaintiff is in a position of potential or apparent conflict of interest or duty. The circumstance of conflict itself raises an issue of propriety making this an appropriate case for directions.

Approval under s 477(2B) of the Corporations Act

12 The relevant principles concerning the application of s 477(2B) set out in Bell No 1 (at [39]-[43]).

THE ORDERS AS SOUGHT

Power to make the orders

13 As with the application and approval obtained in October 2015, and for the reasons set out in Bell No 1 (at [67]-[71]), the Further MT Funding Agreement is authorised by s 477(1)(c) of the Corporations Act as an arrangement between Maranoa Transport and The Bell Group Ltd (in liquidation) (TBGL).

14 The Further MT Funding Agreement, if executed, will put in place a particular regime for Maranoa Transport to meet its liabilities to TBGL, as its principal creditor by a large margin. It does this through a mechanism whereby, to the extent that Maranoa Transport meets costs and expenses that otherwise would have been met by TBGL, the amount paid is adjusted as a reduction against TBGL's proportionate entitlement to distributions from Maranoa Transport. This is within the scope of s 477(1)(c), which merely requires that a particular arrangement touches and concerns the rights and obligations of the company (Maranoa Transport) and its creditor (TBGL).

15 The Agreement being within the scope of s 477(1)(c), the question for the Court (given that directions and orders under s 477(2B) are sought as to the proposed exercise of power under that provision by the liquidator) is whether there is good reason for doubting the bona fides or prudence of the proposed compromise or arrangement: see Bell No 1 (at [72]-[73]).

16 Separately, and to the extent necessary, the plaintiff also relied on s 477(2)(m) of the Corporations Act as providing an alternative source of power for the entry into the Further MT Funding Agreement. To the extent it needs to be considered, the question for the Court in this respect (again, given that directions and orders under s 477(2B) are sought as to the proposed exercise of power under that provision by the liquidator) is whether there is reason to think the Further MT Funding Agreement may ‘enhance’ the winding up of Maranoa Transport: see Re HIH Insurance Ltd [2010] NSWSC 404 (at Appendix 1, (25)-(26), see also Bell No 1 (at [74]-[75]).

Appropriateness of the orders

17 The First Affidavit explained how, prior to the entry into of the original funding and indemnity agreement, the bulk of the costs of the Bell Group companies' windings up were split 50/50 between TBGL (the parent company) and BGF (the Bell Group's ‘treasury company’). Mr Woodings also deposed in the First Affidavit that he intends to seek directions as to the proper apportionment of those costs at a suitable time. This remains the position in the context of the proposed Further MT Funding Agreement and is reiterated by the Third Affidavit.

18 Mr Woodings was, at the time of the application in October 2015, at the very least arguably, exposed to substantial liability to the extent that he caused TBGL to continue to fund the costs of the Bell Group companies' windings up in the way that had occurred in the past. This arose from:

(1) the Commissioner of Taxation's issue of a post-liquidation assessment to TBGL and to Mr Woodings in his capacity as its liquidator which (as amended) was for approximately $298 million;

(2) the Commissioner’s view to the effect that the assessment constitutes a post-liquidation liability which is a priority expense under s 556(1)(a) in TBGL's winding up and the plaintiff is only entitled to pay other priority costs and expenses of the winding up pari passu with the assessment (to the extent that costs and expenses are paid out of TBGL's winding up other than on a pari passu basis with the Commissioner's $298 million assessment, the plaintiff will have a personal liability for the assessment); and

(3) the fact that TBGL lacked sufficient funds to meet the $298 million assessment and that, while the tax sharing agreement could enable TBGL to obtain access to sufficient additional funds to meet the assessment, the Bell Act then before the Western Australian State Parliament might, depending on circumstances, mean that TBGL would be unable to secure such contribution under the tax sharing agreement.

19 Further, Mr Woodings also became exposed to liability as a result of the Commissioner giving PAYG instalment notifications in August 2015 and again in late September 2015 requiring (subject to deferral) payment by TBGL of monthly PAYG instalments. There is a question, or at least a challenge, as to the validity of these notifications but the plaintiff deposes that, on their face, they purport to impose an ongoing liability for instalments of some $32 million per month.

20 The original funding and indemnity agreement enabled Maranoa Transport, another Bell Group company, to provide the 50% funding that until that time had been provided by TBGL to meet the funding needs of the group windings up. It was designed to remove Mr Woodings' exposure to substantial personal liability in the circumstances set out above for the period of its operation.

21 The original funding and indemnity agreement was, however, prepared and entered into in circumstances where the enactment of the Bell Act was imminent. In view of the terms of that Bill, in particular the provisions purportedly giving control of TBGL and most other Bell Group companies to a new body known as the WA Bell Companies Administrator Authority, the original funding and indemnity agreement was constructed to cut off funding for Bell Group costs and liabilities incurred on and after the ‘transfer day’ as defined in the Act that arose out of the Bill. That day was 27 November 2015, the day after the Bell Act received Royal Assent.

22 In view of the terms of the Bell Act as just described, Mr Woodings was unable for a time after the enactment of the Bell Act to progress the windings up of the Bell Group companies of which control was intended to be given to the Authority. This included TBGL and BGF. Mr Woodings sought and obtained directions to bring a High Court challenge to the Bell Act in his capacity, amongst other things, as liquidator of Maranoa Transport (which company was not, at the time, within the scope of the Bell Act). As part of seeking and obtaining those directions, Mr Woodings obtained approval to enter into a separate funding agreement, under which Maranoa Transport met the costs of the High Court challenge. The High Court funding agreement is still in effect, but is limited in the manner described.

23 Mr Woodings brought his challenge, and the High Court determined on 16 May 2016 that the Bell Act was invalid in its entirety: see Bell Group NV (in liq) v Western Australia [2016] HCA 21. By reason of that determination, the plaintiff has resumed the conduct of the windings up of TBGL and the majority of the other Bell Group companies.

24 The original funding problem has, however, effectively arisen again due to the fact that:

(1) the post-liquidation assessment of $298 million issued to TBGL and to the plaintiff is and remains unpaid;

(2) separately and additionally, TBGL prima facie has a distinct liability to pay PAYG instalments on an indefinite, monthly basis on and from August 2015;

(3) the Commissioner refused a further request to defer the outstanding tax liabilities (ie, both the assessment amount and the PAYG instalments);

(4) there are ongoing costs and expenses to be met related to the windings up of all of the Bell Group companies on and from 27 November 2015 and there is no reason to believe that there has been a change in the Commissioner's position as to the plaintiff’s personal exposure if he pays such costs out of TBGL's assets other than on a pari passu basis with the tax liabilities;

(5) Maranoa Transport's obligation under the original funding and indemnity agreement entered into pursuant to the orders of 28 October 2015 to fund TBGL's 50% share of the Bell Group companies' costs and expenses of winding up has ceased to apply to liabilities incurred on and from 27 November 2015; and

(6) the High Court funding agreement continues to provide a source of funding, but it only requires Maranoa Transport to meet the costs of and associated with proceedings involving a challenge to the constitutional validity of the Bell Act (see cl 2.1).

25 One fundamental distinction between the present situation and the situation prevailing in October 2015 at the time of Bell No 1 is that the Bell Act as it was passed (or the Bill in similar terms) has ceased to have legal effect. Thus, it may be supposed that TBGL could seek to rely on the tax sharing agreement in order to pay the tax liabilities in full and thereby eliminate the risk of the plaintiff incurring personal exposure to pay costs and expenses out of TBGL's assets.

26 The plaintiff explains in his affidavit why he does not consider the tax sharing agreement eliminates the funding problem or his personal exposure:

(1) First, the question of whether (and how) to pay the tax liabilities is complex because of the decision in Commissioner of Taxation v 4 Doonan Street Collinsville Pty Ltd (In Liq) [2016] NSWCA 69. This decision, on one view, may have the consequence that if the tax liabilities are paid but are later shown to be (in effect) incorrect, then TBGL and the other Bell Group companies may not be entitled to recover any refund from the Commissioner because the tax refund might (in effect) be set off against pre-liquidation tax debts and interest owing by the Bell Group companies. This may well be a matter of substantial concern to a liquidator and thus the plaintiff may require directions as to what steps he should take concerning payment of the tax. It will take time for directions to be obtained and for the appropriate course to become clear.

(2) Secondly, calling on the tax sharing agreement and calculating, as part of that process, contribution amounts from other members of the consolidated tax group in order to pay the tax liabilities may itself require directions. This is because calculating the contributions may require a number of value judgments to be made, resulting in a range of possible calculations, some of which may be more or less favourable for certain companies in the Group vis-à-vis others. This may possibly give rise to an actual or potential conflict of interest in view of the plaintiff’s position as liquidator of all of the relevant Bell Group companies. Again, it will take time for directions to be obtained and for the appropriate course to become clear.

(3) Thirdly, even if the $298 million assessment and liability for monthly PAYG instalments were ultimately to be paid, there is a real risk that further tax liabilities will arise in the medium term and the funding problem would again resurface. For example, the plaintiff anticipates that assessments for post-liquidation income tax may be raised for income years later than the 2014 financial year. TBGL would ultimately be liable for such assessments given its position as ‘head of the consolidated tax group’. While the plaintiff might apply if further tax liabilities were to arise for orders to put in place a further funding solution, such uncertainty around the availability of continued funding is (as the plaintiff deposes) undesirable. It leaves the liquidations of the Bell Group companies open to ongoing disruption and impedes their efficient progression, which is not in the interests of the conduct of the windings up.

27 In all these circumstances, the plaintiff has formed the view, which I accept, that given TBGL's limited available assets and its position as ‘head of the tax consolidated group’, it should not solely fund the liquidations of the Bell Group on an ongoing basis from its own assets for the foreseeable future. Rather, a stable, alternative funding solution for the needs of the Group is required in the medium to long-term. The proposed solution is essentially a restated and updated version of the original funding and indemnity agreement with Maranoa Transport.

28 Maranoa Transport remains in a position to fund 50% of the costs and expenses that have historically been paid by TBGL. Its creditor base remains the same as in October 2015: see Bell No 1 at [20]-[21]. That is, as Maradolf's creditor's claim will inevitably accrue to the benefit of TBGL, the only external creditor of Maranoa Transport is the Commissioner (for 1.2%). TBGL has the overwhelming economic interest in the funds in Maranoa Transport's winding up.

29 The plaintiff caused the proposed Further MT Funding Agreement to be prepared. The operative terms are the same as those set out in the original funding and indemnity agreement and summarised in Bell No 1 (at [22]), save that:

(1) the duration of the agreement is limited to 5 years (rather than 18 months) unless extended by further court directions and approvals: cl 2 (consistent with the plaintiff’s view that in these most unusual historical circumstances a stable, alternative funding solution for the needs of the group needs to be obtained for the medium to long-term); and

(2) the funding mechanism is proposed to be effective from 27 November 2015 (the date the funding mechanism under the original funding and indemnity agreement ceased operating): cl 3.1.

30 An important post-script as in the case of the original funding and indemnity agreement approved in October 2015, amounts paid for by Maranoa Transport under the agreement are adjusted for as a reduction against TBGL's entitlements to distributions by Maranoa Transport. This includes a notional interest component. The adjustment amount will be applied for the creditors of Maranoa Transport other than TBGL, for example, Maradolf and the Commissioner: cl 3.3 and cl 3.4. This provides a countervailing benefit for the other creditors to appropriately compensate them for the immediate benefit that TBGL is to receive under the agreement.

31 Significantly, the only external creditor who might be adversely affected is the Commissioner, and following consultation about the funding proposal, the Commissioner has made clear that he supports the funding proposal.

CONCLUSION

32 As in this case, the original funding and indemnity agreement approved in Bell No 1, there is little doubt that entry into the funding and indemnity agreement is in the interests of TBGL and Maranoa Transport. The observations made in Bell No 1 (at [81]-[84]) apply equally now.

33 I considered it appropriate at the time of making the orders herein, to grant the direction that the plaintiff will be acting properly and is justified in causing the relevant Bell Group companies to enter into the Further MT Funding Agreement and to make an order for approval to enter into the Agreement for the following reasons:

(1) there is no good reason for doubting the bona fides or prudence of the proposed compromise and arrangement embodied in the Further MT Funding Agreement;

(2) to the extent necessary, there is reason to reach the view that the Further MT Funding Agreement may ‘enhance’ the winding up of Maranoa Transport;

(3) the direction sought under s 479 of the Corporations Act facilitates a proposed action which will be of benefit to the Bell Group companies individually and collectively where, absent the direction, a degree of personal risk attaches to the plaintiff: see Bell No 1 (at [85]); and

(4) for the purposes of approval under s 477(2B) of the Corporations Act, the Further MT Funding Agreement has no effect on the likely timeframe for finalisation of the windings up and there are no real or substantial grounds for doubting the legality, bona fides or prudence of the plaintiff’s opinion that the Agreement will facilitate the continued effective and efficient conduct of the windings up.

I certify that the preceding thirty-three (33) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice McKerracher. |

Associate: