FEDERAL COURT OF AUSTRALIA

ABL Nominees Pty Ltd v Trinick (Trustee) [2016] FCA 996

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties be heard as to the appropriate orders in light of these reasons.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BESANKO J:

Introduction

1 This is an application by ABL Nominees Pty Ltd (“ABL Nominees”) and Bendigo and Adelaide Bank Limited (“Bendigo and Adelaide Bank”) for an order pursuant to s 222(1) of the Bankruptcy Act 1966 (Cth) (“the Act”) setting aside a Personal Insolvency Agreement (“PIA”) executed by Mr Glenn Trinick as Controlling Trustee and Mr David Irvin as the debtor on 9 October 2015. In the alternative to an order setting aside the PIA, the applicants seek an order that the PIA be terminated pursuant to s 222C of the Act. In the event that either of the aforementioned orders is made, the applicants seek a sequestration order against Mr Irvin’s estate (s 222(10) or s 222C(5)). In addition to these orders, the applicants seek an inquiry into Mr Trinick’s conduct as Controlling Trustee pursuant to s 179 of the Act. Before trial, I made an order which meant that the trial proceeded with respect to the orders sought pursuant to s 222 or s 222C of the Act. The application for an inquiry pursuant to s 179 of the Act remains to be determined.

2 The Controlling Trustee, Mr Trinick, is the first respondent. He appeared by counsel at the trial and he opposed the applicants’ application. He gave evidence. Sadly, he passed away recently. The debtor, Mr Irvin, is the second respondent. He appeared in person at the trial from the second day onwards.

3 The starting point for the procedure which may lead to a PIA under Part X of the Act is the authorisation of a Controlling Trustee pursuant to s 188. A debtor who wishes his or her estate to be dealt with under Part X rather than being sequestrated, may sign an authority for a Controlling Trustee to call a meeting of the debtor’s creditors and to take control of the debtor’s property. The decision whether the debtor be required to enter into a PIA is one for the creditors and must be made by special resolution.

4 A special resolution is a resolution passed by a majority of creditors in number and by at least three-fourths in value of the creditors present at a meeting of creditors and voting on the resolution. In this case, the special resolution requiring Mr Irvin to enter into a PIA was passed by a majority of two creditors to one creditor. The creditors in favour of the special resolution were a company called Wideview Holdings Pty Ltd (“Wideview Holdings”) which was admitted to vote for the value of $1, and a Mr Lou Vartesi who was admitted to vote for the value of $16,500. Among other activities, Mr Irvin worked as a photographer and he conducted his photography business through Wideview Holdings trading as “Group Portraits”. Wideview Holdings is a company related to Mr Irvin. Mr Vartesi was an accountant with TJ Edwards & Associates and he provided professional accountancy services to Mr Irvin. The applicants were the “creditor” which voted against the special resolution and collectively they were admitted for voting purposes as having one vote with a value of $1.

5 The applicants claim that they are creditors of Mr Irvin and they have standing to bring this application under s 222 and s 222C of the Act. ABL Nominees claims that it is a creditor of Mr Irvin in the amount of $781,587.36, and Bendigo and Adelaide Bank claims that it is a creditor of Mr Irvin in the amount of $1,000,801.68. The grounds of their application are as follows:

(1) They should have been allowed to vote on the special resolution for the full amount of their respective debts. They were opposed to the special resolution that Mr Irvin enter into a PIA and had they been admitted for the full amount of their respective debts, the special resolution would not have been passed. They point out, correctly, that even if they had been allowed to vote only for a small part of their debts (in the order of at least $5,500), the special resolution would have not been passed because there would not have been at least three-fourths in value of creditors in favour of the resolution. The applicants also point out, correctly, that in the alternative, had they each been allowed one vote instead of being admitted collectively with one vote, the special resolution would not have been passed because there would not have been a majority in number of creditors in favour of the special resolution.

(2) Wideview Holdings should not have been allowed to vote on the special resolution.

(3) Mr Vartesi should not have been allowed to vote on the special resolution.

(4) Mr Trinick as Controlling Trustee did not investigate matters properly or apply an appropriate degree of rigour to his investigation, including (but not limited to) as to the following:

(a) a property transferred by Mr Irvin to his mother in 2013 allegedly at an undervalue;

(b) certain superannuation contributions made by Mr Irvin and the potential to claim them back;

(c) various trusts in which Mr Irvin had an interest;

(d) the income and assets of the Mr Irvin; and

(e) the security position of the National Australia Bank.

(5) The PIA executed by the debtor and Mr Trinick as Controlling Trustee on 9 October 2015 differed in material respects from that put forward to the creditors.

(6) Mr Trinick as Controlling Trustee did not act with the required degree of impartiality.

6 For the following reasons, I have reached the conclusion that the PIA executed on 9 October 2015 should be set aside pursuant to s 222 of the Act.

The Key Events

7 On 10 June 2015, Mr Trinick was appointed the Controlling Trustee of Mr Irvin’s property. On the same day, Mr Irvin signed a Statement of Affairs in which he listed the Bendigo and Adelaide Bank as one of his unsecured creditors in the amount of $1.8 million, and he executed a proposed PIA by executing a pro forma document. At that point, the PIA provided that the antecedent transactions provisions of the Act (ss 120 – 125) applied to the agreement (s 188A(4)).

8 The Controlling Trustee was required by the Act to make such inquiries and investigations in connection with the debtor’s property and examinable affairs as the trustee considered necessary (ss 190(2)(b) and 190A(1)(f)). The Controlling Trustee was required to report to creditors, and must state whether he or she believes that the creditors’ interests would be better served by accepting the debtor’s proposal for dealing with his or her affairs under Part X or by the bankruptcy of the debtor (s 189A(1)).

9 It will be necessary for me to examine in some detail the events between the appointment of Mr Trinick as Controlling Trustee and the execution of the PIA. Before doing that, it is necessary for me to summarise Mr Irvin’s financial affairs and to consider events from 27 September 2013 to 10 June 2015.

10 I have already mentioned Wideview Holdings. Mr Irvin was the director and shareholder of that company. There were a number of other companies or entities in which he had or had had an interest which were operating or dormant or which had, in fact, been deregistered. There were two family trusts, a winery business, a restaurant business and the ownership of patents. There was a self-managed superannuation fund and a holiday timeshare. There was a property at Weaponess Road, Scarborough in the State of Western Australia, and a property previously mentioned as having been transferred to Mr Irvin’s mother in 2013 at Hidaway Drive, Bindoon in the State of Western Australia (“the Bindoon property”). The banker to Mr Irvin and his various companies was the National Australia Bank and it made various loans and took various security interests over assets owned or controlled by Mr Irvin. This is a sufficient description of Mr Irvin’s assets and liabilities at this stage.

11 In addition to these assets and liabilities, Mr Irvin had made investments in managed investment schemes involving Great Southern Finance Pty Ltd and companies associated with it and ABL Nominees Pty Ltd. Mr Irvin’s investments in what I will call the Great Southern investment schemes had given rise to very substantial liabilities. A number of investors were involved in the schemes and there was a class action in relation to the schemes in the Supreme Court of Victoria which, as far as I can see, was commenced in 2010 and settled in December 2014. I will refer to this as the Great Southern class action.

12 At all times relevant to this proceeding, Mr Trinick, Mr Ian Patterson and a Mr Shaun Boyle were directors of Frais Pty Ltd trading under the name of “Debt Crisis Solutions”. The business employed a number of staff, including Mr Thompson Goh and Ms Natasha Petrie. Debt Crisis Solutions provided, according to Mr Patterson’s evidence, “various debt related services to clients such as analysis of debts, debt restructuring, consolidation loans, creditor and summons negotiations, credit and debt management and budgeting, advice regarding late and overdue business activity statements, taxation due, debt agreements, Personal Insolvency Agreements and bankruptcy solutions under Parts IX & X of the Bankruptcy Act 1966”. In order to do that, it was necessary for the business to obtain as much detail as it could about a client’s financial affairs, including the client’s assets and liabilities.

13 Mr Irvin was a client of Debt Crisis Solutions from on or about 27 September 2013 to 10 June 2015. Plainly, a matter of importance during that period was Mr Irvin’s liabilities in relation to the Great Southern investment schemes and the outcome of the Great Southern class action.

14 For this period, Mr Patterson was the principal at Debt Crisis Solutions who was advising Mr Irvin about his financial affairs and his options. He met with Mr Irvin on a number of occasions and he or his staff collected information from Mr Irvin and third parties about Mr Irvin’s assets and liabilities.

15 Mr Patterson swore a lengthy affidavit in which he out set details of his meetings with Mr Irvin and the information he or his staff collected about Mr Irvin’s assets and liabilities. These details included company records, trust deeds and financial statements. He was assisted by Mr Goh, Ms Petrie and others. He annexed to his affidavit a number of the documents he or his staff obtained. Mr Patterson sets out the events in chronological order in his affidavit. It is not necessary for me to identify every meeting or event. It is sufficient if I set out the more important events. Some of the matters not mentioned in this section of these reasons will be identified later in these reasons when I deal with specific matters.

16 Mr Patterson met Mr Irvin on 27 September 2013 and the topics discussed included the loans in relation to the Great Southern investment schemes, the Great Southern class action, interests in Wideview Holdings and a family trust.

17 Mr Patterson met with Mr Irvin on 22 November 2013 and they discussed, among other things, what could occur under a bankruptcy or under a PIA.

18 Mr Patterson and Mr Trinick met Mr Irvin on 25 November 2013 and the topics discussed were Mr Irvin’s superannuation fund, the business of Wideview Holdings, the Bindoon property and companies including Howling Wolves Wine Group Pty Ltd, Bluezinnea Pty Ltd, Boxcella Pty Ltd, Wideview Holdings and a winery and restaurant at Yellingup. A “flowchart” showing various entities was prepared.

19 Mr Patterson met with Mr Irvin on 11 February 2014. Mr Patterson gave Mr Irvin an estimate of $300,000 “to fund a Part X offer to the creditors including the fees and disbursements of a trustee”.

20 Mr Patterson and Mr Trinick had a discussion on 22 September 2014. Mr Trinick said a minimum of $30,000 would be required “to start moving forward with a Personal Insolvency Proposal”.

21 Mr Patterson met Mr Irvin on 5 January 2015. Mr Patterson told Mr Irvin that he could not be a director if he went bankrupt or whilst a PIA was on foot.

22 In January 2015, the applicants had an action against Mr Irvin pending in the District Court of South Australia and, on 13 January 2015, the action was listed for hearing on 21 May 2015. The applicants consented to an order vacating the trial dates fixed by the District Court of South Australia.

23 Mr Patterson met Mr Irvin on 11 March 2015. Mr Irvin told Mr Patterson that he proposed to have the photographic business sold to his partner, Ms Carol Bull. Mr Patterson told Mr Irvin that if he wished to appoint Debt Crisis Solutions to progress the PIA, then Debt Crisis Solutions required funds to be deposited “up front”.

24 A search of the records held by the Australian Securities and Investments Commission reveals that Ms Carol Bull became the owner of the shares in Wideview Holdings previously held by Mr Irvin effective on 31 March 2015.

25 On 24 April 2015, Mr Irvin executed a Section 188 (Controlling Trustee) Authority in Mr Trinick’s favour.

26 Mr Patterson met Mr Irvin on 30 April 2015 and they discussed the information required for the completion of Mr Irvin’s Statement of Affairs.

27 On 5 May 2015, Mr Chris Milne (of Jarrett Business Assessments) provided a valuation of the business of Wideview Holdings.

28 On 12 May 2015, Debt Crisis Solutions received indemnity monies from Mr Irvin in the sum of $53,000.

29 With this background in mind, I turn to the period after Mr Trinick had been appointed Controlling Trustee on 10 June 2015.

30 On 12 June 2015, Mr Trinick signed a report to creditors which he had prepared (“the First Report to Creditors”). On 18 June 2015, the applicants received that report, together with a letter from Mr Trinick. In his declaration of relationships in the First Report to Creditors, Mr Trinick said that Mr Patterson first met Mr Irvin on 27 October 2013 and had since met with Mr Irvin and his adviser sporadically to discuss Mr Irvin’s financial position. The first meeting and subsequent discussions did not exceed 50 hours and were made for the purpose of gathering sufficient information to enable a determination to be made as to the solvency of Mr Irvin, the likelihood of recovery action in respect of sundry debtors and related party transactions, the commerciality and quantum of assessment recovery, and the various options available to Mr Irvin, taking into consideration the interests of creditors.

31 The First Report to Creditors disclosed the fact that Mr Irvin had signed a draft PIA. It referred to Mr Irvin as director, secretary and shareholder of Wideview Holdings. It referred to Lowline Holdings Pty Ltd as trustee of Lowline Holdings Superannuation Fund as a related entity. It enclosed a Form 8, proof of debt and requested the lodgement of a proof of debt with supporting documentation, in particular, invoices, statements and other documents. It referred to Projected Unsecured Creditors’ Claims drawn from the Statement of Affairs, being Bendigo and Adelaide Bank ($1.8 million), National Australia Bank ($1.13 million), TJ Edwards & Associates (Mr Vartesi) ($20,000). In total, seven entities were listed totalling about $3.335 million. Wideview Holdings was not named as a projected unsecured creditor.

32 On 3 July 2015, Mr Trinick signed a second report to creditors which he had prepared (“the Second Report to Creditors”). The creditors were advised that there would be a meeting of creditors on 15 July 2015. The creditors were given a copy of the proposed PIA executed by Mr Irvin and dated 10 June 2015. The Second Report to Creditors disclosed the following matters to the creditors. First, Mr Irvin considered the main cause of his insolvency to be his investment in the Great Southern investment schemes which was financed by Great Southern Finance and the Bendigo Bank. He said that he did not receive any return on his investment and there was a significant shortfall resulting from the debts. Secondly, Mr Trinick said that, based on his preliminary investigations, he agreed with Mr Irvin’s views as to the reasons for his financial circumstances. Thirdly, Mr Trinick said that Mr Irvin disclosed in his Statement of Affairs that he started having difficulties in paying his debts in 2009. The available documents indicated that Mr Irvin was unable to meet his financial commitments in early 2010 when he failed to make payments to the Bendigo Bank and the latter issued written notices of demand for the debt owing. Mr Trinick said that it was fair to conclude that Mr Irvin was possibly insolvent from January 2010. Fourthly, Mr Trinick advised the creditors that his agent had provided a valuation of Group Portraits and the business had a market value of between $370,000 and $390,000, and Group Portraits had a net worth of $599,080. Mr Trinick went on to say that the business was heavily dependent on Mr Irvin’s experience, technical skills and personal relationship with the existing client base and that without Mr Irvin’s cooperation with the handover process in the event of the sale of the business, the likely value of the business was nil. Fifthly, in addressing transfers to defeat creditors, Mr Trinick referred to the fact that Mr Irvin’s bank accounts revealed a transaction whereby an amount of $100,000 was transferred by Group Portraits on 29 October 2013, and then between 11 November 2013 and 14 November 2013, a total amount of $80,000 was transferred to Ms Bull, the “Debtor’s business partner”. Mr Trinick advised the creditors that Mr Irvin had later clarified that it was their intention to transfer the monies directly from Group Portraits to Rivendeel Wines. Ms Bull is a director and shareholder of Rivendeel Wines. Sixthly, Mr Trinick advised the creditors that the proposed PIA provided a greater, more certain and timely return to creditors than a likely nil return in bankruptcy, and he expressed the opinion that the creditors’ interest would be better served by resolving that Mr Irvin be required to execute the proposed PIA. Seventhly, Mr Trinick advised the creditors that the primary purpose of the meeting was to consider the proposed PIA, and the agenda for the meeting included the tabling of that document. Eighthly, Mr Trinick advised the creditors of the need to provide a written statement setting out (a) the amount the creditor claims the debtor is indebted to the creditor; (b) if a creditor has been assigned a debt, the value of the consideration the creditor gave for the assignment; (ab) whether the creditor is a related entity; (b) as it is the first meeting of creditors, whether the creditor holds security, and, if so, the value of the security and the amount of the debt after deducting that value, and brief particulars of the transaction and circumstances that gave rise to the debt. Ninthly, the creditors are advised that completing the Form 7 – Statement of Claim and Proxy Form enclosed will comply with the above requirements. Finally, the creditors are advised that they may vote by proxy and that if they wished to do so, the form of appointment of proxy enclosed should be submitted with the s 64D statement.

33 On the day before the first meeting of creditors, the applicants sent information to the Controlling Trustee’s firm in support of their claims to be creditors of Mr Irvin. The details of the claims are set out in the following table which is taken from paragraph 26 of the first affidavit of Mr Stephen James Flamer-Smith:

Loan No | Annexure | Loan date | Original Lender | Loan amount | Current creditor | Claimed amount |

1 | “SFS11” “SFS12” | 01/07/2003 | GSF | $485,050 | Bendigo & Adelaide Bank Limited (BABL) | $256,201.71 |

2 | “SFS13” “SFS14” | 01/07/2003 | GSF | $303,250 | ABL Nominees Pty Ltd (ABL) | $160,285.50 |

3 | “SFS15” | 15/06/2006 | ABL | $240,960 | ABL | $280,642.84 |

4 | “SFS16” | 15/06/2007 | ABL | $222,450 | ABL | $340,659.02 |

5 | “SFS17” “SFS18” | 01/07/2005 | GSF | $305,017.50 | BABL | $345,342.40 |

Guaranteed | “SFS19” “SFS20” | 01/07/2004 | GSF | $354,760 | BABL | $399,257.57 |

34 The documents sent by the applicants to Mr Trinick at that point were four statements of claim and proxy forms and, in addition, as to each loan, the loan application form, the Loan Deed, and the current account statement for the loans.

35 The first statement of claim and proxy form relates to Loans 1 and 5. The correspondence from the applicants enclosing this document stated the following:

These loans are held by Bendigo & Adelaide Bank Ltd. The loans were purchased by the Bank at full face value under a securitisation arrangement with Great Southern Finance.

The Bank paid 100 cents in the dollar for the loan and should therefore be entitled to vote for the full value of the debt as at 10 June 2015.

The first statement of claim indicates that the debts had been assigned to the Bendigo and Adelaide Bank Ltd and the consideration paid for the assignments was “100c/$ (full face value)”.

36 The second statement of claim and proxy form relates to Loan 6 (i.e., “Guaranteed”). The correspondence from the applicants enclosing this document stated the following:

This loans [sic] is held by Bendigo & Adelaide Bank Ltd and was issued in the name of Lowline Holdings Pty Ltd – Mr Irvin is the guarantor of the loan. The loan was purchased by the bank at full face value under a securitisation arrangement with Great Southern Finance. The bank paid 100 cents in the dollar for the loan and should therefore be entitled to vote for the full value of the debt as at 10 June 2015.

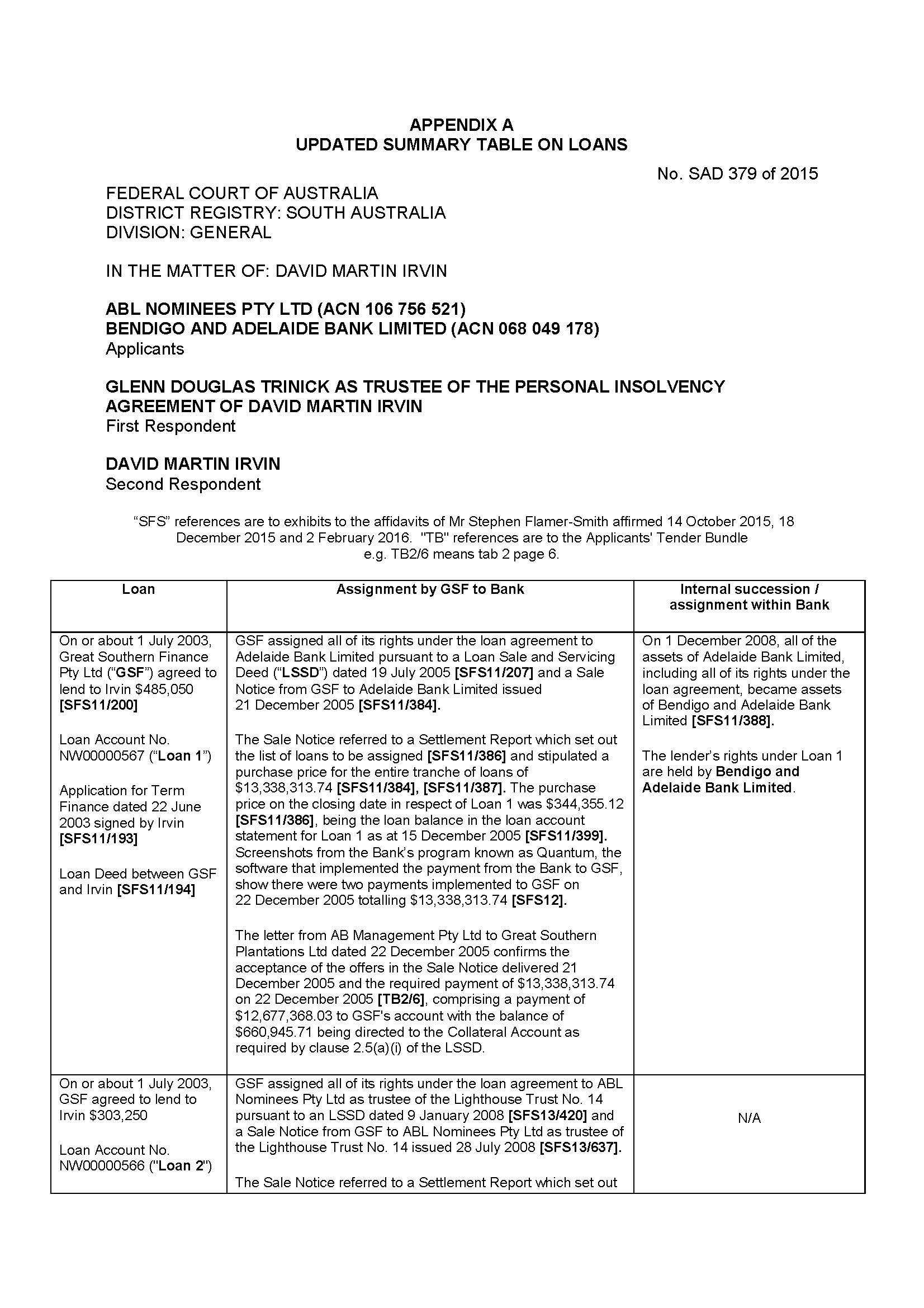

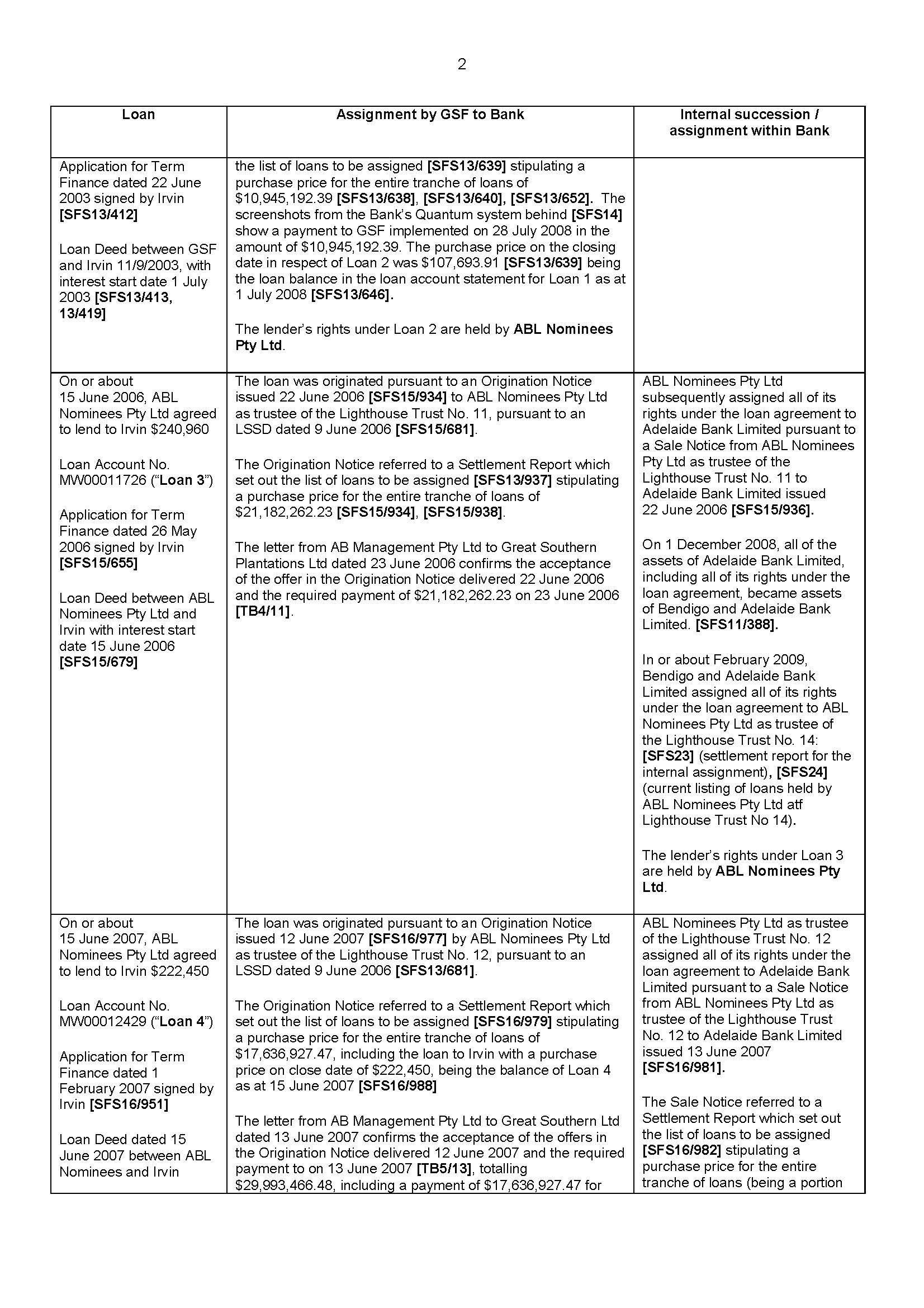

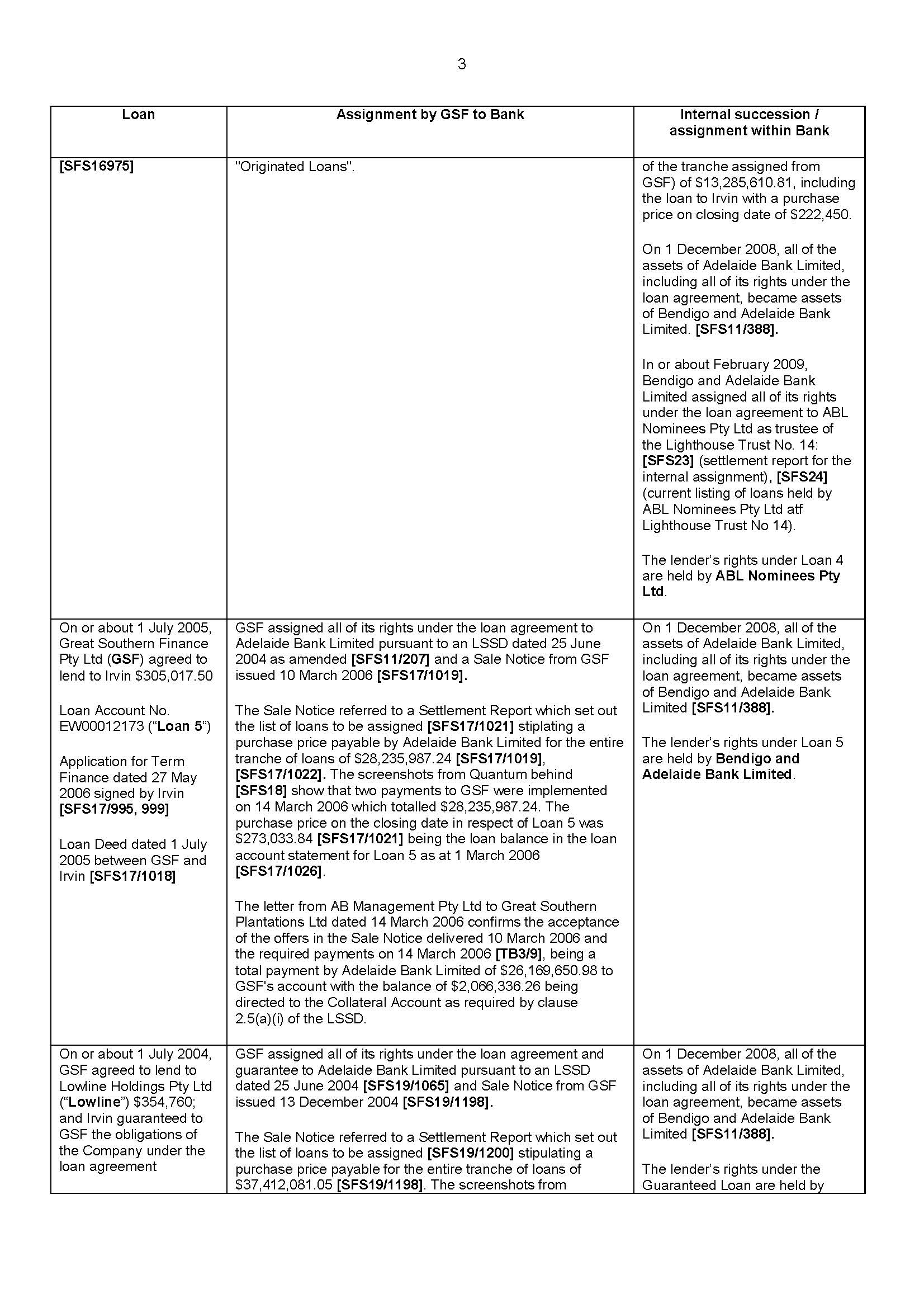

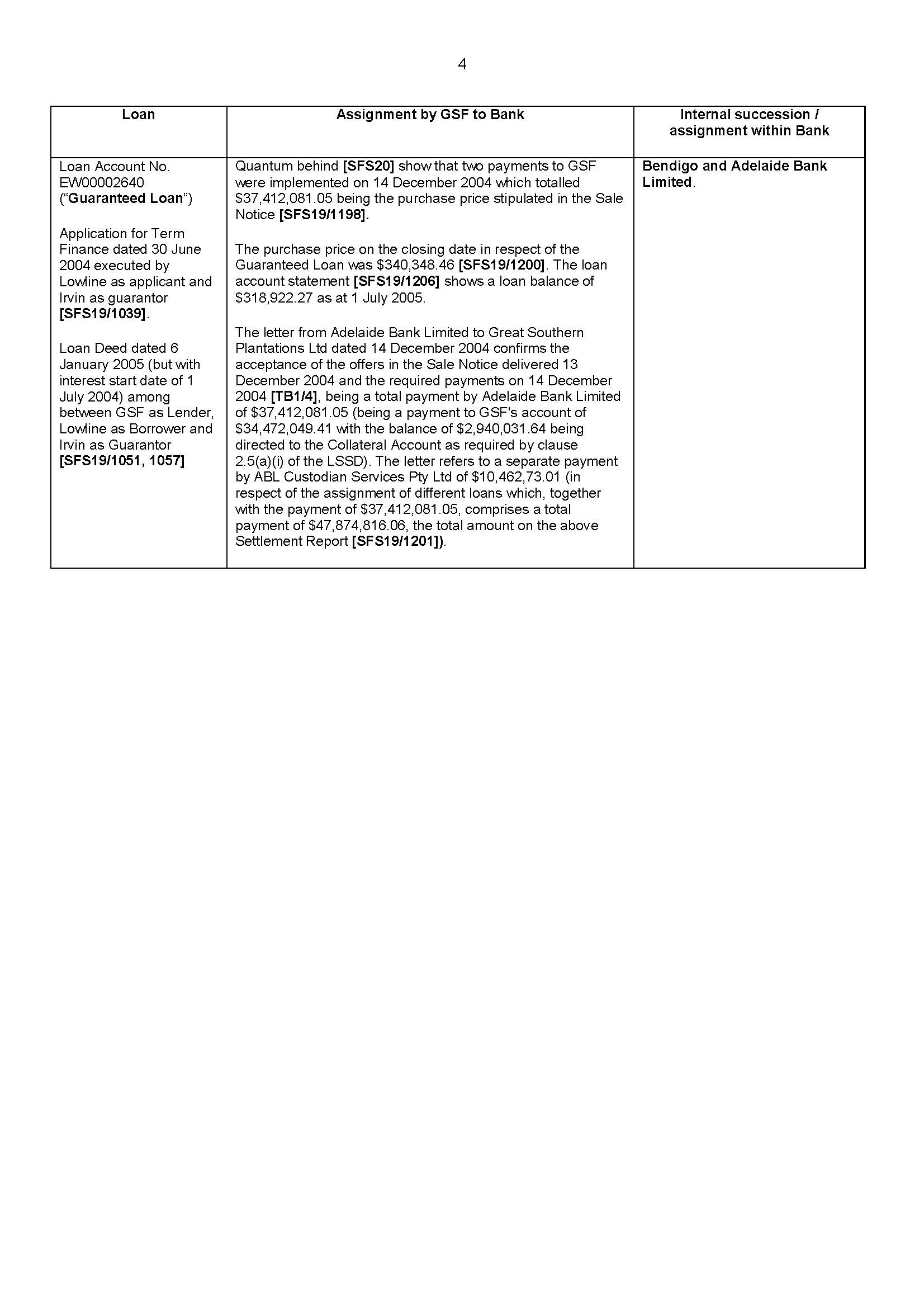

The second statement of claim indicates that the debt was assigned to the Bendigo and Adelaide Bank and contains a similar statement as to the consideration paid for the assignment as the statement in the case of Loans 1 and 5.

37 The third statement of claim and proxy form relates to Loans 3 and 4. The correspondence from the applicants enclosing this document stated the following:

These loans are held by ABL Nominees Pty Ltd a wholly owned subsidiary (but separate legal entity) of Bendigo & Adelaide Bank Ltd. These loans were issued by ABL Nominees Pty Ltd directly to Mr Irvin.

The third statement of claim contains a statement that the debts were not assigned to ABL Nominees.

38 The fourth and final statement of claim and proxy form relates to Loan 2. The correspondence from the applicants enclosing this document stated the following:

This loan is held by ABL Nominees Pty Ltd a wholly owned subsidiary (but separate legal entity). The loan was provided to David Irvin in his capacity as trustee of the David Irvin trust. The loan was purchased by the Bank under securitisation arrangement with Great Southern Finance. The Bank paid 100 cents in the dollar for the loan and should therefore be entitled to vote for the full value of the debt as at 10 June 2015.

The fourth statement of claim indicates that the debt was assigned and contains a similar statement as to the consideration provided for the assignment as is the case with Loans 1, 5 and 6.

39 The applicants gave proxies to the chairperson in relation to the first meeting of creditors held on 15 July 2015. Mr Irvin, through his accountant, advised Mr Trinick approximately 30 minutes before the meeting that he sought to amend the PIA so that the antecedent transactions provisions of the Act did not apply to him.

40 Mr Trinick, Mr Patterson, Mr Irvin (by telephone), Mr Vartesi, Mr Goh and Ms Petrie attended the first meeting of creditors. Mr Trinick ruled on the statements of claim. The applicants and Mr Vartesi were each admitted for voting as to the full amount of their claims. In the case of ABL Nominees that was for $781,587.36, and in the case of the Bendigo and Adelaide Bank, that was for $1,000,801.68. In the case of Mr Vartesi, that was for $16,500. It is relevant to note that Wideview Holdings were not identified as a creditor at that stage. Mr Trinick was appointed the President of the meeting. He outlined Mr Irvin’s proposed PIA and the proposed change to it. He confirmed that there was no material change to the status, remuneration or recommendation contained in his Second Report to Creditors. However, he recommended that the meeting be adjourned because of the proposed change and the need for him to review the legitimacy of creditors’ claims in the estate and to conduct further investigations to resolve outstanding issues. A resolution was passed that the meeting of creditors be adjourned to a date not later than 10 October 2015.

41 It seems that it was around this time that relations between the applicants and Mr Trinick began to sour. Mr Stephen Flamer-Smith, on behalf of the applicants, had asked for details of Mr Trinick’s work-in-progress and those details had been provided. On 15 July 2015, Mr Flamer-Smith advised Mr Goh that the Bendigo and Adelaide Bank did not intend to submit a proof of debt at that stage. Mr Trinick sent an email to Mr Flamer-Smith asking for a proof of debt if Bendigo and Adelaide Bank wish to be considered a creditor and advising him that he should make a complaint against him, “rather than being blunt, rude and arrogant to my staff”.

42 On 16 July 2015, the Bendigo and Adelaide Bank lodged a complaint against Mr Trinick with the Australian Financial Security Authority (“AFSA”) in which it raised concerns over a lack of independence.

43 In August 2015, Mr Irvin approached Bennett and Co, solicitors, to provide assistance “to investigate and liaise with Bendigo and Adelaide Bank”. On 18 September 2015, Mr Thaw Thaw Htin of Bennett and Co sent an email to Mr Irvin and Mr Patterson (copy to Mr Martin Bennett) in the following terms:

I have reviewed the documents provided by both of you and attach a draft letter for the Controlling Trustee to send to Stephen Flamer-Smith of Bendigo & Adelaide Bank.

In summary, we recommend that the Controlling Trustee should request all supporting documentation about the assignments of the debts from Great Southern. Under section 64ZB(8) of the Bankruptcy Act, the bank can only vote for the amount of the consideration paid for the debts assigned by Great Southern Finance. The Trustee must value the vote having regard to section 64ZB(8) and is not limited by what the bank estimates was the consideration paid in the statement of claim form. This is an objective determination and the Trustee can ascribe a nominal value of $1 to the value of the vote if there is insufficient or no information about the consideration paid for the assignment (Bechrose Pty Ltd v Jefferson (Trustee) [1999] FCA 1153).

Attached to the email was a letter Mr Htin had drafted for Mr Trinick to send to the applicants.

44 On 24 September 2015, Mr Trinick signed a third report to creditors (“the Third Report to Creditors”) in which he addressed a number of matters. First, he expressed the opinion that the likely dividend under the proposed PIA was $0.05 to $0.06 in the dollar compared to a nil return in bankruptcy. He recommended that the creditors accept the proposed PIA. Secondly, he provided advice to the creditors about the possibility of recovering the Bindoon property under s 120 of the Act. His advice was that the property was not recoverable because, even if Mr Irvin did not hold the property on trust for his mother when he bought the property in 2002, he did after she repaid the purchase price in 2005. Mr Trinick advised the creditors that, in those circumstances, it may be considered that the transfer for the purposes of the section took place in 2005 and Mr Irvin was not insolvent at that time and this occurred outside the relation back period of four years specified in s 120(3)(a) of the Act. Thirdly, Mr Trinick advised the creditors that Mr Irvin had an entitlement in a joint self-managed superannuation fund and they are told that the value of that entitlement as at 30 June 2014 is $1,198,235. The creditors are advised that there might be recoverable transactions in the sum of $43,000, but that there would be the difficulty of establishing an intention to defeat creditors. There was a lack of evidence of an intention to defeat creditors and, in addition, in light of the ongoing Great Southern class action, Mr Irvin may argue that he was not insolvent until December 2014 when the action was concluded. Fourthly, Mr Trinick identified Wideview Holdings as a creditor of Mr Irvin in the amount of $334,986. Mr Trinick said that he had spoken to Mr Irvin’s accountant and that he was satisfied that the debt was legitimate. He referred to the fact that, in the event of a PIA, Wideview Holdings had agreed not to rank for a dividend. Fifthly, Mr Trinick summarised the effect of the proposed PIA. He advised the creditors that in his opinion, “in the event of bankruptcy there is a high degree of certainty that there would be no return to creditors”. Sixthly, Mr Trinick advised the creditors that there was the potential of a shortfall to the National Australia Bank. Seventhly, Mr Trinick advised the creditors that the Bendigo and Adelaide Bank had provided particulars of their debt, but they were yet to lodge a proof of debt form. The creditors were advised that the bank may have security. Finally, Mr Trinick expressed the view that the creditors’ interests would be better served by resolving that Mr Irvin be required to execute the proposed PIA and he advised that there was a “high probability” that bankruptcy would yield no return to creditors.

45 On 25 September 2015, Mr Goh emailed to Mr Flamer-Smith a letter from Mr Trinick dated 24 September 2015. His letter is largely based on the draft letter Mr Htin of Bennett and Co sent with his email dated 18 September 2015. In his letter, Mr Trinick pointed out to the applicants that they had not provided any supporting documentation concerning the assignment of the loans. He advised the applicants that he was in the process of reviewing the voting entitlements of each of them, and he asked that they provide information confirming that the loans which were allegedly assigned were in fact assigned and were purchased for 100 cents in the dollar. He also raised a query as to the applicants’ security over Mr Irvin’s property. He asked the applicants to advise as to the form of consideration used to purchase the book debts and the conditions which were attached. He asked for the information by close of business on 29 September 2015. In concluding his letter, he said:

If I do not receive the information requested, I will have no alternative but to ascribe a nominal value of $1 to the votes of ABL and BAB at the reconvened creditors meeting on 7 October 2015. In this regard, I refer you to section 64ZB(8) of the Bankruptcy Act 1966 which permits a creditor by assignment to vote only for the value of the consideration it gave for the assigned debt owed by the debtor. In determining the value of the debt said to be assigned, I am not confined to the value that ABL and BAB chooses to ascribe to that consideration in the statement of claim form (Bechrose Pty Ltd v Jefferson (Trustee) [1999] FCA 1153).

46 On 28 September 2015, the applicants’ solicitors wrote to Mr Trinick enclosing a draft creditors’ petition and details of the debts with all supporting information. As I understand it, the supporting information included, where appropriate, a document called a Loan Sale and Servicing Deed, a Sale Notice, a document called a Settlement Report (as at a certain date), documents detailing the restructuring arrangement between Adelaide Bank Limited and Bendigo and Adelaide Bank and correspondence to Mr Irvin. A document identified later in these reasons which was not provided to Mr Trinick at that time was the document recording the payments of the consideration for the assignments.

47 On 5 October 2015, Mr Htin of Bennett and Co sent an email to Mr Irvin and Mr Patterson attaching another draft letter for Mr Trinick to send to the applicants’ solicitors. The draft letter contained the following two paragraphs:

In my letter to your client dated 24 September 2015, I explained that section 64ZB(8) of the Bankruptcy Act 1966 permits a creditor by assignment to vote only for the value of the consideration it gave for the assigned debt owed by the debtor. In determining the value of the debts said to be assigned, I am not confined to the value that your clients choose to ascribe to that consideration in the statement of claim form and I can have recourse to all of the information provided to me by your client. I have already referred your client to the case of Bechrose Pty Ltd v Jefferson (Trustee) [1999] FCA 1153 in relation to my discretion to admit your clients’ debts in the amount of $1 if I consider this is necessary. Your assertion that there is no proper basis to admit your clients’ debts in the amount of $1 and that it is only appropriate where a debt is contingent is misconceived in the circumstances.

Please provide me with evidence of the actual payments made by your clients for the assignment of the loans under the Sales Notices so that I can determine the value of your clients’ votes. Javelin Asset Management v Byrne [2015] VSC 491 only deals with Javelin’s right to sue for the loan and not whether sufficient information has been provided in relation to section 64ZB(8).

48 Mr Trinick did send a letter to the applicants’ solicitors on 6 October 2015. The comparable paragraphs in Mr Trinick’s letter to the applicants’ solicitors are as follows:

In my letter to your client dated 24 September 2015, I explained that section 64ZB(8) of the Bankruptcy Act 1966 permits a creditor by assignment to vote only for the value of the consideration it gave for the assigned debt owed by the debtor. In determining the value of the debts said to be assigned, I am not confined to the value that your clients choose to ascribe to that consideration in the statement of claim form and I can have recourse to all of the information provided to me by your client. I have already referred your client to the case of Bechrose Pty Ltd v Jefferson (Trustee) [1999] FCA 1153 in relation to my discretion to admit your clients’ debts in the amount of $1 if I consider this is necessary. Your assertion that there is no proper basis to admit your clients’ debts in the amount of $1 and that it is only appropriate where a debt is contingent is misconceived in the circumstances.

I require a dollar value on the assignment of each debt and evidence of how the amount was derived.

In relation to the proxies submitted by your client for the debts owing to Bendigo and Adelaide Bank Ltd and ABL Nominees Pty Ltd, I have given your client one (1) vote as the information provided by yourselves and your client shows that all of the rights attributable to ABL Nominees Pty Ltd were transferred to Bendigo and Adelaide Bank Ltd.

49 The differences between Mr Htin’s draft letter to the applicants’ solicitors and the letter Mr Trinick actually sent to the applicants’ solicitors is explained by the fact that after receiving Mr Htin’s letter dated 5 October 2015, Mr Trinick sought and obtained his own legal advice from Carles Solicitors. On 5 October 2015, Mr Goh wrote to Mr Carles enclosing the documentation relevant to the applicants and asking for advice as follows:

Please provide your opinion as to whether the Controlling Trustee would be able to reduce Bendigo Bank’s vote to $1. In addition, if the debt was assigned with no cash paid, then would the debt be valued as of the date of the assignment or the face value?

50 A redacted copy of a letter of advice from Mr Carles to Mr Trinick dated 6 October 2015 was tendered by the applicants. In the section entitled “Summary of Advice”, the following appears:

1. A statement of claim form for voting purposes should specify the actual dollar amount paid for an assignment of debt. It is not sufficient in my view for such a form to simply state that “100 cents in the dollar (full face value)” was paid as this is insufficient to enable a bankruptcy trustee to determine the dollar amount at which the vote should be allowed i.e. the current amount claimed for the debt is likely to include accrued interest etc and may well be different to the amount which was paid for the assignment.

2. If the creditor rectifies the above issue then the voting statement will comply with s64D (and in particular s64D(aa)) and the creditor should be entitled to vote for the amount paid for the amount paid for [sic] the assignment without further evidence being required.

The letter goes on to identify the difficulties caused by different figures appearing in relation to Loan 6.

51 The applicants’ solicitors responded to Mr Trinick’s letter dated 6 October 2015 by letter dated 7 October 2015. In addition, on the same day, they sent to Mr Trinick a statutory declaration made by Mr Flamer-Smith dealing with the debts. In that statutory declaration, Mr Flamer-Smith identifies the purchase price in relation to each of the loans.

52 The second meeting of creditors was held on 7 October 2015. Mr Flamer-Smith, on behalf of the applicants, attended the meeting by telephone. Mr Flamer-Smith said that Mr Trinick told the meeting that he had legal advice about the legitimacy of the applicants’ claim. That advice was that the form received pursuant to s 64D of the Act did not stipulate a specific amount for the consideration of any assignment and, therefore, could not be accepted. His legal advice was that the expression “100c/$ full face value” was not permitted, and because the form did not have the completed details, it could not be accepted. Mr Trinick told the meeting that he was bound to follow the legal advice. The applicants would be allowed one vote collectively for the value of $1. Wideview Holdings, a related party creditor, was admitted as a creditor for $1 on the basis of discussions Mr Trinick had with Mr Irvin’s accountant to satisfy himself that a debt existed and Mr Vartesi of TJ Edwards & Associates (Mr Irvin’s accountants) was admitted as a creditor to vote for $16,500 based on an invoice dated 15 June 2015. The creditors by a majority passed a special resolution which, according to Mr Flamer-Smith’s account, required Mr Irvin to execute a PIA which, by its terms, appoints the trustee as trustee.

53 On 9 October 2015, Mr Trinick, as Controlling Trustee, and Mr Irvin signed a PIA. The key features of the PIA as executed are as follows:

(1) The Deed defines “Creditors” as “creditors of Mr Irvin as at 10 June 2015”.

(2) The property available to pay the creditors’ claims is described as follows:

(a) the sum of $53,000 paid to the trustee prior to the date of the Deed;

(b) Ms Carol Bull will pay to the trustee the sum of $200,000 for the purchase of Mr Irvin’s shares (100%) held in the company, Wideview Holdings trading as Group Portraits, payable on the following terms: upfront payment of $100,000 upon execution of the Deed, and four payments of $25,000 each with the first payment to be made within 90 days after the execution of the Deed and each subsequent payment to be made within 90 days thereafter (total payments within 12 months from the date of execution of the Deed).

(3) There is no income or future income of Mr Irvin which is to be made available to pay the creditors’ claims.

(4) The property of Mr Irvin received under the PIA is to be distributed in the manner set out in cl 7.

(5) The void (antecedent) provisions in ss 118 and 120 to 125 of the Act are not applicable.

(6) Mr Irvin is released and discharged from all provable debts, save and except that Wideview Holdings is an excluded party. The Deed provides that Wideview Holdings is not entitled to make a claim against the debtor during the term of the Deed, whether under the deed or otherwise, for the payment of a dividend, but it also provides that the debt of Wideview Holdings is not extinguished as a result of the Deed.

Witnesses and Evidence

54 The applicants called Mr Flamer-Smith as a witness and tendered a number of documents. Mr Flamer-Smith is a manager, Legal and Resolutions, employed by the Bendigo and Adelaide Bank. ABL Nominees is a wholly owned subsidiary of the Bendigo and Adelaide Bank. Mr Flamer-Smith swore three affidavits which were tendered in evidence and which comprised his evidence-in-chief. Mr Flamer-Smith was cross-examined about the following topics. First, he was cross-examined about each of the loans and the fact that there was no bank statement or bank cheque or electronic funds transfer evidencing the payment of the consideration for the assignments of the loans. Mr Flamer-Smith was also cross-examined about the screenshots generated by the bank’s program called Quantum which showed (according to the applicants), the payment for loans in batches, that is to say, the payment for the assignment of a number of loans at the one time. Secondly, Mr Flamer-Smith was cross-examined about certain internal assignments which had apparently taken place in relation to Loans 3 and 4, and the paucity of documents in relation to those assignments. Thirdly, Mr Flamer-Smith was cross-examined about “claw back” provisions in favour of the assignees and the establishment of a collateral account (see, by way of example, cl 11 of the Loan Sale and Servicing Deed in relation to Loan 1). Finally, Mr Flamer-Smith was cross-examined about the notes he made of the meeting of creditors on 7 October 2015. Mr Flamer-Smith had produced handwritten notes he took at the time of the meeting and typed notes which he prepared two days after the meeting. One of Mr Trinick’s witnesses, Mr Patterson, produced Mr Trinick’s minutes of the meeting of creditors held on 7 October 2015. The two versions were not the same and that is of significance in considering the precise terms of the special resolution.

55 I will deal with the effect of Mr Flamer-Smith’s evidence as I deal with particular topics. At this stage, I record the fact that I found Mr Flamer-Smith to be a straightforward witness and I accept his evidence.

56 Mr Trinick gave evidence and he called evidence from Ms Petrie and Mr Patterson.

57 Mr Trinick swore three affidavits which were tendered and comprised his evidence-in-chief. He was cross-examined at length by counsel for the applicants. Unfortunately, he was not a satisfactory witness. He displayed considerable frustration with, and anger towards, the applicants throughout his evidence. His frustration and anger was at times directed towards the applicants’ counsel who he referred to as a liar and time-waster. More than once he described the applicants’ claims as fraudulent. At times, he gave long-winded and rambling answers containing what appeared to be internal inconsistencies and which were, at the very least, difficult to follow. He appeared to date the deterioration of his relationship with the applicants to the first meeting of creditors on 15 July 2015 and the applicants’ complaint about him to the AFSA. I will refer to aspects of Mr Trinick’s evidence later in these reasons when I deal with specific topics. At this stage, I record the fact that I found him an unsatisfactory witness and I do not think that I can rely on his evidence.

58 An affidavit of Ms Natasha Margaret Petrie was tendered and she was not required for cross-examination. Ms Petrie has worked as a manager at Debt Crisis Solutions since 12 January 2015. Ms Petrie gave evidence about a meeting she had with Mr Trinick, Mr Paresh Rathod, and Mr Goh of Debt Crisis Solutions on 22 September 2015. The meeting was called to discuss a draft of the third report to creditors and two major issues which remained to be finalised. Those two issues were the superannuation payments made by Mr Irvin to his superannuation fund, and whether any of those payments could be recovered as superannuation contributions made to defeat creditors pursuant to ss 128B, 128C or 121 of the Act. The second major issue concerned the transfer of the Bindoon property by Mr Irvin to his mother on 12 February 2014. Ms Petrie deposed to the consideration which was given to the question of whether that transfer might constitute an undervalued transaction within s 120 of the Act. Ms Petrie also gave evidence of the recording of pre-appointment time charges in relation to work performed by Debt Crisis Solutions before Mr Trinick was appointed as Controlling Trustee.

59 Mr Patterson swore a lengthy affidavit which was tendered in evidence as his evidence-in-chief. He was cross-examined about his contact with Mr Irvin in 2013 and whether he was monitoring developments in the Great Southern class action. He was cross-examined about his discussions with Mr Irvin about the ramifications of entering into a PIA as against being made bankrupt. He was also cross-examined about the minutes of the second meeting of creditors and, in particular, the resolution which is recorded in the minutes to have been passed in relation to the PIA.

60 It is not necessary to say a great deal about Mr Patterson’s evidence. I did not find him to be particularly helpful as he seemed to have a relatively poor recollection of a number of events.

61 Mr Irvin appeared on the second day of the trial. He had sat in the body of the Court on the first day of trial. When he appeared, he sought to make a statement. I pointed out to him that he had not appeared earlier and that he had not complied with orders of the Court made before trial concerning the filing and serving of any affidavit material on which the respondents intend to rely at the hearing of the application. I told Mr Irvin that if he wished to, he could file an application supported by the information or affidavit he sought to rely on. Mr Irvin sat at the bar table for the rest of the trial, but he did not file an application.

62 On the third day of trial, Mr Irvin applied to ask Mr Trinick some questions. I decided not to allow him to do so and my reasons are set out in the transcript (p 241).

63 On the final day of trial, I received, subject to relevance, a five page handwritten statement of Mr Irvin and four pages of a Discharge Summary dated 10 May 2015. Counsel for the applicants did not seek to cross-examine Mr Irvin.

64 Mr Irvin’s statement dealt with the following matters. First, he said that he had recently suffered a stroke. Secondly, he set out the reasons he did not want to be made bankrupt. Thirdly, he said that the decline of his school photography business was due to market competition. Fourthly, he referred to the support he had received from his partner and love, Carol Bull. Fifthly, he said that he received $53,000 as a result of the class action and that he paid that to the Controlling Trustee. Finally, he addressed briefly the Bindoon property, his daughter’s motor vehicle, and the superannuation contributions which he had made.

Are the Applicants Creditors of Mr Irvin?

65 In order to bring an application under s 222 or s 222C of the Act, each applicant must show (relevant to this case) that it is a creditor. Section 222 provides, relevantly, as follows:

222 Court may set aside personal insolvency agreement

Setting aside on grounds of unreasonableness etc.

(1) If a personal insolvency agreement is in force, the Court may, on application by:

(a) the Inspector General; or

(b) the trustee; or

(c) a creditor;

make an order setting the agreement aside if the Court is satisfied that:

(d) the terms of the agreement are unreasonable or are not calculated to benefit the creditors generally; or

(e) for any other reason, the agreement ought to be set aside.

Setting aside on grounds of non compliance with this Part etc.

(2) If a personal insolvency agreement is in force, the Court may, on application by:

(a) the Inspector General; or

(b) the trustee; or

(c) a creditor; or

(d) the debtor;

make an order setting the agreement aside if the Court is satisfied that:

(e) the agreement was not entered into in accordance with this Part; or

(f) the agreement does not comply with the requirements of this Part.

(3) The Court must not make an order setting aside a personal insolvency agreement on the ground that it does not comply with the requirements of this Part if the agreement complies substantially with those requirements.

…

(10) The trustee or a creditor may include in an application under subsection (1), (2) or (5) an application for a sequestration order against the estate of the debtor. If the Court, on the first mentioned application, makes an order under this section setting the personal insolvency agreement aside, it may, if it thinks fit, immediately make the sequestration order sought.

…

66 Each of the applicants in this case claims to be a creditor of Mr Irvin.

67 Mr Trinick’s first submission in response to the applicants’ claims that each is a creditor of Mr Irvin is that neither is a creditor of Mr Irvin because neither applicant had lodged a proof of debt. Mr Trinick relied on ss 83 and 84 of the Act in support of the proposition that a person is not a creditor unless and until he or she had lodged a proof of debt. I reject this submission. There is no warrant for reading the word “creditor” in ss 222 and 222C as subject to compliance with ss 83 and 84. If s 83 qualified ss 222 and 222C in this way, then not only would a proof of debt have to be lodged, but it would also have to be admitted. As far as s 84 is concerned, that section identifies the procedure to be followed in lodging a proof of debt. Mr Trinick’s submission seems to be inconsistent with the fact that far from claiming under the PIA, the applicants are applying to have it set aside and with the notion that the authorities say in relation to an earlier form of the section that the term “creditor” has been used in a wide sense and includes any person who could prove in bankruptcy (Beard v Prestige Baking Industries Pty Ltd and Another (1981) 52 FLR 384 at 404 per Fox J).

68 The applicants handed up as an aide mémoire a document which summarised their case to the effect that they are creditors of Mr Irvin. I am satisfied that this table accurately reflects the evidence and I attach it to these reasons as Appendix A. The reference to “SFS” followed by a number is a reference to an annexure to one of Mr Flamer-Smith’s affidavits, and the reference to “TB” followed by a number is a reference to one of the documents in the Tender book which became Exhibit A1. In the left hand column of Appendix 1, the details and documents relating to each loan are identified. I do not understand any of that material or indeed the loans themselves to be in dispute. As I understand it, these documents were provided to Mr Trinick with the applicants’ statements of claim. In the middle column of Appendix 1, the documents relating to the assignment of the loans are identified. Documents such as Loan Sale and Servicing Deeds, Sale Notices, Origination Notices and Settlement Reports were provided to Mr Trinick by the applicants’ solicitors on 28 September 2015 and certainly before the second meeting of creditors on 7 October 2015. The documents in the middle column described as screenshots from the bank’s program known as Quantum and as letters from AB Management Pty Ltd and Adelaide Bank Limited were not provided to Mr Trinick, but have been tendered as exhibits in this proceeding. As far as the right hand column is concerned, there is no issue concerning the fact that on 1 December 2008, all of the assets of Adelaide Bank Limited, including all of its rights under the loan agreement, became assets of Bendigo and Adelaide Bank. As I understand it, apart from the documents described as SFS23 and SFS24 which were tendered in evidence, but not provided to Mr Trinick, the other documents referred to were provided to Mr Trinick on 28 September 2015 by the applicants’ solicitors.

69 Mr Trinick’s principal submission was that neither applicant has proved that it was or is a creditor of Mr Irvin because neither has proved that it paid the consideration for the assignment of the loans. He points out that the payment of consideration has not been proved by the production of a bank statement or a bank cheque or an electronic funds transfer.

70 I have read the documents carefully and I reject the submission. The following general points should be noted at the outset. First, as I have said, I do not think there is any dispute about the fact that the loans were made and the outstanding balances. Secondly, the Loan Sale and Servicing Deeds have a definition of purchase price which means the aggregate principal amount outstanding at a particular date (cl 1.2). Thirdly, the seller of the loans, being loans identified in a Settlement Report can give a Sale Notice to the purchaser which the purchaser may accept by payment (cl 2.5). Fourthly, there is provision for the seller to establish a collateral account to which the purchaser has certain rights in relation to unpaid amounts (cl 11). I refer to this because Mr Trinick referred to these “claw back” provisions as affecting the consideration the applicants provided for the assignments. The Schedules to the Deed contain forms for various notices referred to in the Deed and they include the format for a Settlement Report. Fifthly, the Sale Notices had attached to them the Settlement Reports which related to the relevant sale. The loans were sold in batches and the total amounts involved were very large. The Settlement Reports tendered have been redacted to exclude references to other debtors. Finally, Mr Flamer-Smith explained that his understanding was that the payment for a “batch” of loans was made using the bank’s program known as Quantum and he produced what he called “screen dumps” from the Quantum system.

71 I will take the evidence produced in relation to Loan 1 as an example for the purposes of Loans 1, 2, 5 and 6, and the evidence produced in relation to Loan 3, as an example for the purposes of Loans 3 and 4.

72 The making of Loan 1 is established. The Loan Sale and Servicing Deed relevant in the case of Loan 1 is dated 25 June 2004, and Great Southern Finance Pty Ltd, ABL Nominees, Adelaide Bank Limited and Great Southern Managers Australia Limited were parties to the Deed. A Sale Notice under the Deed was given to Adelaide Bank Limited by Great Southern Finance Pty Ltd on 21 December 2005 and the accompanying Settlement Report identified the purchase price on closing date of Loan 1 ($344,355.12) and an overall consideration for the relevant batch of loans of $13,338,313.74. The loan account statement, although not having an exactly matching date, supports the figure in the Settlement Report. A letter from Adelaide Bank Limited to Great Southern Plantations Limited dated 22 December 2005 states that the offer in the Sale Notice dated 21 December 2005 is accepted and that Adelaide Bank Limited had paid a total of $13,338,313.74. The screenshots confirm the payments. The statutory declaration made by Mr Flamer-Smith identifies the purchase price on closing date of $344,355.12. The pattern of documents in relation to Loans 2, 5 and 6 is similar.

73 I am satisfied that Loans 1, 2, 5 and 6 were assigned for their full value on the dates alleged.

74 As I have said, I will take the evidence produced in relation to Loan 3 as an example for the purposes of Loans 3 and 4.

75 The original loan by ABL Nominees to Mr Irvin is not in dispute. An Origination Notice dated 22 June 2006 was issued pursuant to cl 2.1 of the Loan Sale and Servicing Deed as amended on 9 June 2006. The loan was assigned by ABL Nominees to Adelaide Bank Limited pursuant to a Sale Notice from ABL Nominees as trustee of the Lighthouse Trust No. 11 to Adelaide Bank Limited issued on 22 June 2006. I am prepared to accept that the loan was transferred from ABL Nominees to Adelaide Bank Limited. The second internal assignment was from Bendigo and Adelaide Bank to ABL Nominees. This is said to have taken place in or about February 2009. A Settlement Report, including Loan 3 and a listing of loans, including Loan 3 presently owned by ABL Nominees in its capacity as trustee of the Lighthouse Trust No. 14, have been tendered. Mr Flamer-Smith explains that he has been unable to locate any other documents concerning the second internal assignment. He explains that, given the assignment was between non-arm’s length companies who were wholly owned subsidiaries of the Bendigo and Adelaide Bank, there would not have been a payment by way of cheque, cash or electronic funds transfer via the electronic banking system. It is likely the payment would have been recorded by book entries, leading to adjustments to each entity’s general ledger to reflect on the movement of money and the change of ownership of the loan, although Mr Flamer-Smith has not been able to locate the specific entry for the movement of money. Mr Flamer-Smith said that the fact that Loan 3 appears on the listing of loans owned by ABL Nominees means that ABL Nominees and the Bendigo and Adelaide Bank regard the payment as having been made. Mr Flamer-Smith said that such internal assignments were always affected at the full face value of the loan balance at the time, not at a discount. Any internal sales of loan assets at a discount would have required a detailed process of writing down each of the assets.

76 In my opinion, the second internal assignment of Loan 3 took place. If for some reason the assignment was ineffective, that would mean no more than that the Bendigo and Adelaide Bank was the creditor in relation to the loan.

77 I reject the suggestion that the applicants have not established that they are not creditors because of what were referred to as “claw back” provisions. There is no suggestion, having regard to the substantial documentation produced in this case that those provisions are relevant to the outstanding amounts due to the applicants.

78 The applicants are each creditors of Mr Irvin in the amounts claimed and have standing to bring this application under s 222 and s 222C of the Act.

Should each of the Applicants have been admitted to vote for the value of their debts as set out in their respective statements of claim?

79 At the second meeting of creditors held on 7 October 2015, the applicants were admitted to voting collectively as a creditor with a value of one dollar ($1).

80 The applicants’ case is that each of them should have been admitted to vote as a creditor and, in the case of ABL Nominees, with a value of $781,587.36 and, in the case of Bendigo and Adelaide Bank, with a value of $1,000,801.68.

81 There are two aspects to Mr Trinick’s case. First, the applicants were not admitted for the value of their respective loans because they did not specify in their respective statements of claim a dollar amount as the actual amount paid for each assignment. This approach is reflected in the minutes of the second meeting of creditors which were produced by Mr Patterson. Although, as I have said, I found parts of Mr Trinick’s evidence confusing, the approach is also reflected in answers he gave in cross-examination suggesting that there would not have been a problem had the applicants specified a dollar amount as the actual amount paid for each assignment. The second aspect is seen most clearly in Mr Trinick’s closing submissions and is to the effect that he was entitled to take the position he did in the absence of proof from the applicants of the amount actually paid for each assignment. This aspect of Mr Trinick’s approach is also reflected in Mr Flamer-Smith’s recollection confirmed in his notes, and which I accept is accurate, that at the second meeting of creditors Mr Trinick said that there was no evidence of cash changing hands and, therefore, there was no evidence of the assignment.

82 In Re Dingle; Westpac Banking Corporation v Worrell and Another (1993) 47 FCR 478 at 486, the Full Court of this Court made it clear that in determining whether a person is entitled to vote as a creditor, the Court must act on the material before it and is not limited to the material before the trustee.

83 Mr Trinick called the meeting of creditors under s 188 of the Act, and Division 5 of Part IV of the Act which deals with meetings of creditors of a bankrupt applies to the meetings as if the debtor was bankrupt and the Controlling Trustee was the trustee in the bankruptcy (s 196).

84 Section 64D deals with notices of meetings and relevantly provides:

64D Statement by creditor as to amount of debt

The notice must state that each creditor must give to the trustee at or before the meeting a written statement setting out:

(a) the amount in respect of which the creditor claims that the bankrupt is indebted to the creditor; and

(aa) if the creditor has been assigned a debt that the bankrupt owes to the creditor—the value of the consideration that the creditor gave for the assignment of the debt; and

(b) if the meeting is the first meeting of the bankrupt’s creditors:

(i) whether the creditor holds a security in respect of the debt and, if so, the value of the security as estimated by the creditor and the amount of the creditor’s debt after deducting that value; and

(ii) brief particulars of the transaction and circumstances that gave rise to the debt.

85 Section 64ZA deals with entitlement to vote and relevantly provides:

64ZA Entitlement to vote

(1) This section applies to voting:

(a) at an election under section 64P of a person to preside at a meeting; and

(b) on any motion proposed at a meeting or an amendment proposed to such a motion.

(2) In this section:

“creditor” means a creditor who, or whose proxy or attorney, participates in the meeting in person or by telephone.

(3) A person other than a creditor is not entitled to vote.

(4) Subject to subsections (5) and (6), each creditor is entitled to vote and has one vote.

(5) If a creditor is a secured creditor, the creditor is not entitled to vote unless the debt, or the total amount of the debts, owed to the creditor exceeds the amount estimated by the creditor in the statement given to the trustee under section 64D to be the value of the security.

(6) A creditor who has failed to give to the trustee a statement in accordance with section 64D is not entitled to vote.

(7) A creditor is not disqualified from voting merely because the creditor is the President or the minutes secretary.

(8) The trustee may determine any question that arises as to the entitlement of a person to vote.

…

86 Section 64ZB deals with the manner of voting and in that context s 64ZB(8) deals with the value of a creditor who has been assigned a debt, is present at the meeting and is voting on the motion. The subsection provides as follows:

(8) For the purposes of determining whether a motion proposed at the meeting is resolved, the value of a creditor who:

(a) has been assigned a debt; and

(b) is present at the meeting personally, by telephone, by attorney or by proxy; and

(c) is voting on the motion;

is to be worked out by taking the value of the assigned debt to be equal to the value of the consideration that the creditor gave for the assignment of the debt.

87 These provisions were considered by Drummond J in Bechrose Pty Ltd v Jefferson and Another (1999) 94 FCR 494 (“Bechrose”), a case relied on by Mr Trinick both at the time of the relevant events and at the trial before me. I should note at this point that the first reference to Bechrose at the time of the relevant events was in Mr Htin’s email dated 18 September 2015. I am not prepared to find, based on Mr Trinick’s evidence, that he had any real appreciation of the case before it was raised by Mr Htin. Before considering Bechrose, I note the following.

88 French J (as his Honour then was) considered the obligations of a trustee in bankruptcy in determining whether a person who claimed to be a creditor (in that case not a creditor by way of an assignment of a debt) should be permitted to vote in Starkey v Rondo Building Services Pty Ltd [2005] FCA 1081 (“Starkey”). His Honour said that the admission by the trustee of a person to vote does not involve a final determination of that person’s proof of debt. The trustee may decide from the particulars provided that a claim is frivolous or without a proper basis or involves a debt not provable in bankruptcy and refuse to admit it for voting purposes. To that extent, the particulars provide “a procedural protection against frivolous or baseless claims” (at [46]). On the other hand, the section contemplates that the trustee will act in a summary way, having regard to the information available to him or her (at [46]).

89 The information the trustee may require in the context of a proof of debt is set out in s 84(2) and (3) of the Act.

90 Section 64D(aa) and 64ZB(8) use the word, “gave”. The definitions of “give” in the Macquarie Dictionary (3rd ed, Macquarie, 1997) are as follows:

1. to deliver freely; bestow; hand over: to give someone a present. 2. to deliver to another in exchange for something; pay. 3. to grant permission or opportunity to; enable; assign; award. 4. To set forth or show; present; offer …

91 Mr Trinick emphasised the reference in the second definition to the word “pay”.

92 The Explanatory Memorandum for the amendment which introduced s 64D(aa) and s 64ZA(8) identified the mischief to which those provisions were directed in the following way.

93 Creditors with significant debts in a bankruptcy analyse the bankrupt’s financial circumstances. They may conclude that they are unlikely to receive any substantial return and decide to assign their debts to get what they can. The assignees who purchase the debts then vote in favour of proposals that are beneficial to or favour the bankrupt. In this process, the wishes of smaller creditors who are not in a position to bargain for the assignment of their debts are overruled. This mischief is overcome, it is considered, if the assignee is entitled to vote only for the value he or she actually gave for the debt. The Explanatory Memorandum states:

59.2 In some cases, a creditor will determine not to continue to pursue his or her rights against a debtor, but will assign a debt to another person for some consideration which the assigning creditor considers to be reasonable in the circumstances. The assignee is able to vote at a meeting of creditors for the full amount of the debt owed to the original creditor, even though the assignee may have paid only a fraction of the amount of the original value of the debt. It has occurred that a bankrupt or debtor arranges for friends or relatives or persons favourably disposed toward the bankrupt to acquire from independent creditors an assignment of a debt, and be in a position, at a creditor’s meeting, to control the outcome of resolutions and special resolutions which can determine the future course of the debtor’s or bankrupt’s affairs. Frequently, it is institutional creditors who are owed large sums who assign debts. That a person favourably disposed towards a debtor or bankrupt can by this device acquire control over voting at a meeting can appear to work, if not actually work, an injustice to smaller creditors. This is because the assigning creditor has made a commercial judgment that in reality, his or her debt is only worth the value that the assignee is prepared to pay for it. Smaller creditors may not be in the position to assign debts, and their small entitlement to vote may be insufficiently attractive to a person wishing to purchase the creditor’s debt to make any offer worthwhile. However, the commercial judgment of the assigning creditor may have placed the voting power at a meeting in the hands of a person whose interest is not in actually collecting dividends in respect of the debt, but rather, in assisting the debtor or bankrupt to achieve his or her objectives, of for example getting an annulment of bankruptcy.

59.3 Accordingly, the Bill proposes to amend the Act so that an assignee of a debt can vote at a meeting only for the amount of consideration that he or she gave to the assigning creditor. Thus if ABC Bank was owed $lm. by Peter, the bankrupt, and Richard acquired the debt for $500, Richard would be able to vote to a value of $500, and not $lm, the $500 being the amount for which Richard acquired the debt.

59.4 Item 166 proposes the insertion into subsection 64D a new paragraph (aa) which provides that if a creditor has been assigned a debt that the bankrupt owes to the creditor, the creditor should state in the notice to the trustee setting out the amount which the creditor claims the bankrupt owes the value of the consideration the creditor gave for the assignment of the debt.

94 In Bechrose the property assigned by the bank (Westpac Banking Corporation) to Bechrose were two mortgages granted by a company called Chelmscliff Pty Ltd over a farming property, a floating charge over the company’s undertaking and a guarantee given by the bankrupt that the company would repay loan monies to Westpac. There was also the benefit of a costs order in favour of Westpac. The issue before the Court was the value of the consideration which Bechrose had given for the guarantee. Bechrose had chosen for its own purposes not to apportion any part of the price it paid for the assignment of the guarantee, the mortgages and the costs order to the guarantee. Drummond J said that the inference was strong that Bechrose was not at arm’s length from the bankrupt. The trustee admitted Bechrose as a creditor for voting purposes at the meeting of creditors and had estimated that the value of the proof was the sum of $1. Importantly in terms of the ratio of the case, Drummond J accepted that the evidence showed that the monetary consideration paid by Bechrose to Westpac for the assignments was paid solely as consideration for the transfer of the two mortgages (at [56] et seq.)

95 Drummond J said that the value of the consideration given was a matter for objective determination and that a creditor cannot control the value of the vote it is entitled to cast at a meeting of creditors by what it claims to be the consideration for the assigned debt when the true position is that it in fact gave consideration of lesser value. It seems to me that Bechrose is something of a special case. Drummond J was confronted with a case where the consideration was provided for the assignment of a debt and other assets and the assignee refused to place a value on the debt. Bechrose failed to comply with s 64D(aa) and that meant, having regard to s 64ZA(6), it was not entitled to vote at the meeting. Drummond J said that strictly, the trustee should have ruled that Bechrose was not entitled to vote at the meeting. In the alternative, having regard to the evidence, the trustee was entitled to conclude that Bechrose “can only fairly be regarded as having given nominal consideration for the assignment to it of debt on the guarantee” (at [72]).

96 The following passages from his Honour’s reasons illustrate these points (at [69], [70] and [71]):

69. The applicant contends that it gave a single undivided consideration for the assignment to it of the debts secured by the mortgages and the mortgage debenture, the debt under the guarantee and the benefit of the costs order obtained by Westpac against the Sherrys. For the reasons given, there are good grounds for thinking that it adopted that position to ensure that the application of s 64ZB(8) to the valuation by the trustees of the applicant's right to vote at the meeting would require that vote to be valued at the very large figure contended for by the applicant.

70. But s 64ZB(8) does not require the trustees to stand impotent in the face of the applicant's refusal to ascribe a value to the consideration it gave for the debt on the guarantee, as distinct from the consideration it gave for the debts under the mortgages and the benefit of the costs order. It obliges the trustees to value the applicant’s vote by reference to the consideration it gave for the assignment to it of the debt on the guarantee, and that alone.

71. The applicant was required by s 64D(aa) to provide that information in writing to the trustees at or prior to the creditor’s meeting. It failed to do that. Section 64ZA(6) accordingly disentitles the applicant, though undoubtedly a creditor of the bankrupt, to vote at the meeting of creditors in question. Strictly, the trustees should have ruled that the applicant was not entitled to vote at the meeting. Instead, they ascribed to the applicant’s entitlement to vote, which they accepted, a nominal value only.

97 There is clearly a difference between stating the value of the consideration given for the assignment of a debt and proving the value of the consideration given for the assignment of the debt. The first must be done. It was not done in Bechrose. I do not think the second must be done. It seems to me that it depends on the circumstances. There is the type of case identified by French J in Starkey where the claim appears frivolous or without a proper basis. The trustee would be entitled in those circumstances to ask for more information. There is the type of case that arose in Bechrose where one consideration was paid for a number of assets of which the assignment of debt was but one. I think a trustee in those circumstances would be entitled to ask for evidence which provides a rational basis for the valuation of the consideration given for the assignment of the debt.

98 Subject to these types of cases, one must go back to the words of s 64D to determine the obligation of a person who claims to be a creditor by reason of the assignment of a debt. That person must give the trustee a statement which includes the value of the consideration that he or she gave for the assignment of the debt and brief particulars of the transaction and circumstances that gave rise to the debt. That is the extent of the obligation. Again, subject to the type of cases I have mentioned, I do not think that the later section, s 64ZB(8), dealing with the working out of the value of the creditor, enlarges the obligation of the person who claims to be a creditor as a result of the assignment of a debt. That subsection merely provides that the value of the creditor is to be determined by reference to the value of the consideration given for the assignment of the debt.

99 The other point to be made is that I do not think that the value stated in the statement of claim lodged by the creditor is necessarily decisive if the appropriate figure is clear from all the documents lodged by the person claiming to be a creditor. If the person provides information showing the value of the consideration given for the assignment of the debt and another figure for the debt as at the date of the statement of claim, I do not think the trustee is entitled simply to reject all the figures. There may be different figures which result from the fact that the debt has increased because interest has accrued since the assignment or from the fact that the debt has been reduced because the debtor has made repayments since the assignment. At the very least, the trustee should take the lowest figure in those circumstances. This means I reject the approach taken by Mr Trinick at the second meeting of creditors as revealed in the minutes of that meeting produced by Mr Patterson. Mr Trinick said that there were three different figures for Loan 6 and that that justified or at least supported his approach. The documents provided to him by the applicants in relation to Loan 6 clearly identified the value given by the assignee for the debt ($340,348.46) and the amount owing with respect to the debt as at 10 June 2015 ($399,257.57). If he was in any doubt, it was open to him to accept the lower of these two figures.

100 In my opinion, Mr Trinick should have proceeded on the basis that the value of ABL Nominees as a creditor and the value of the Bendigo and Adelaide Bank as a creditor was as asserted in their respective statements of claim. Even if he was justified in taking the lower figure (in those cases where it was a lower figure) of the amount at the time of the assignment, both applicants were substantial creditors of Mr Irvin. On either view, the special resolution would not have been passed.

101 I should say before leaving this topic that, even if the law was that in the case of an assignment of debt the amount actually paid for the assignment had to be shown (as Mr Trinick asserted), I do not accept the assertion that that could only be done by the production of a bank statement, bank cheque or electronic funds transfer. In fact, as to at least some of the loans (and acceptance of only one of the loans and the assignment thereof would have meant that the special resolution was not passed), the transactional documents provided, including the Deeds, led to the inference that payment for the assignment had in fact taken place.

Should Wideview Holdings and Mr Vartesi been admitted to Vote?

Wideview Holdings

102 As I have said, in his Third Report to Creditors, Mr Trinick said that a balance sheet of Wideview Holdings as at 30 June 2014 showed that Mr Irvin owed the company an amount of $334,986. He said that he had had discussions with the company’s accountant and was satisfied that the debt was legitimate. At the second meeting of creditors, Wideview Holdings was admitted to vote with a value of $1. There is a dispute as to Mr Trinick’s explanation for not admitting Wideview Holdings for the full amount of its claimed debt. Mr Flamer-Smith’s account of the meeting was that Mr Trinick said it was because Wideview Holdings was a related party, whereas the minutes of the meeting produced by Mr Patterson record Mr Trinick as saying that it was because “full detailed transactions” were not yet available. Although nothing appears to turn on the resolution of that dispute, Mr Flamer-Smith was a reliable witness and I would be disposed to accept his version of events.

103 The applicants submitted that, having regard to a number of matters which they identified, Wideview Holdings should not have been permitted to vote because it was not a creditor of Mr Irvin. The onus is on the applicants to prove this allegation (Re McLean and Another; Ex parte Friends’ Provident Life Office (1992) 36 FCR 502; George v Deputy Commissioner of Taxation and Another (2004) 57 ATR 450; [2004] FCA 1433).