FEDERAL COURT OF AUSTRALIA

Colin R Price & Associates Pty Ltd v Four Oaks Pty Ltd [2016] FCA 764

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Within seven days, the parties provide agreed minutes of proposed orders to give effect to these reasons. If they cannot agree, each party provide minutes of proposed orders to give effect to these reasons, together with a short outline of submissions in support of those proposed orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MOSHINSKY J:

INTRODUCTION

1 In mid-2006, a syndicate of investors, through a trustee company, purchased a property at 33 Albion Road, Box Hill, Victoria for the purposes of renovating and building apartments and sale of those apartments (the Project). The syndicate comprised several of the respondents and the second applicant (Grovan). The trustee company was Twentieth Green Pty Ltd, the seventh respondent (Twentieth Green).

2 During the period November 2006 to November 2008, the first applicant (CRP) carried out the building work for the Project.

3 A dispute has arisen between the parties. In brief terms, CRP claims payment for the building works on a reasonable remuneration (or quantum meruit) basis calculated at cost plus a margin of 10 or 15%. It claims that a written “Australian Building Industry Contract ABIC SW-1 2002 Simple Works Contract”, which it entered into with Twentieth Green in November 2006 (the Simple Works Contract), does not govern the relationship between the parties, either on the basis that the parties agreed that it would only be used to obtain finance and would not record the terms under which CRP was to perform the works, or because it is void for uncertainty. CRP has alternative claims for misleading or deceptive conduct and unconscionable conduct.

4 Grovan claims that it has not been paid its share of the profits of the Project. One of the issues that arises in this regard concerns documents signed by Colin Price, the principal of CRP and a director of Grovan, on 3 September 2008 (the First Payment Authority) and 24 December 2008 (the Second Payment Authority). The first to seventh respondents rely on these documents as permitting approximately $100,000 of Grovan’s entitlements to be withheld from Grovan and paid to other persons. (The eighth respondent did not file an appearance and did not appear at trial.) Grovan contends that the Payment Authorities did not authorise Twentieth Green to apply the amount in this way. Grovan makes this contention on various grounds, including that the Payment Authorities were not validly executed by or on behalf of Grovan and that it is unconscionable for the respondents to rely on the documents. Grovan also contends that certain adjustments are required to the accounts of the unit trust for the Project.

5 The first to seventh respondents cross-claim against CRP. In brief, they contend that CRP repudiated the Simple Works Contract (by ceasing to work on the Project from about August 2008), which repudiation was ‘accepted’ by those respondents; that CRP breached the Simple Works Contract by not completing the works on time or to the required standard; and that Twentieth Green has suffered loss and damage as a result.

6 Orders were made for the separate determination of certain questions, namely:

(a) the basis upon which CRP was entitled to be remunerated for performing the works (or so much of them as it performed);

(b) all of the claims made by Grovan; and

(c) all of the claims made by the respondents in the cross-claim.

The effect of these orders was that the trial of the separate questions covered all aspects of CRP’s claims other than the quantum of any amounts payable to CRP, all aspects of Grovan’s claims and all aspects of the respondents’ cross-claim.

7 In summary, my conclusions are as follows:

(a) In relation to the basis upon which CRP was entitled to be remunerated, I conclude that the Simple Works Contract governed the relationship between the parties. The question whether the parties intended the Simple Works Contract to govern their relationship is to be determined objectively. The Simple Works Contract takes the form of a concluded legal agreement. It was signed both by Mr Price, on behalf of CRP, and Mr Stephen Power, on behalf of Twentieth Green. While it is true that the bank required a fixed price contract as a condition of funding the Project, and the contract was prepared to satisfy that requirement, the conduct of the parties in signing the Simple Works Contract evinced an intention to be bound by that document in relation to the building work for the Project. Further, it is not established that the parties agreed that the Simple Works Contract would not govern their relationship. In relation to the contention that the Simple Works Contract lacked certainty, I conclude that the document contained or incorporated sufficient detail about the works to be carried out to constitute a binding agreement notwithstanding that, at the date the document was signed, the engineering drawings and working drawings did not yet exist. I find that a ten-page scope of works document did exist at the time the contract was signed. The engineering and working drawings were produced in the months after the Simple Works Contract was signed. There was no issue between the parties about their content. The works were performed in accordance with those drawings without any issue about what they required. In relation to CRP’s alternative claims for misleading or deceptive conduct and unconscionable conduct, I conclude that the alleged representations underpinning these claims were not made, and consequently the claims are not made out.

(b) In relation to Grovan’s claims, I conclude that the First and Second Payment Authorities were not validly executed by or on behalf of Grovan. Neither document was signed by Faye Price, one of the two directors, despite the First Payment Authority expressly providing for her signature. Mr Price did not have actual or ostensible authority to sign the Payment Authorities on behalf of Grovan. It follows that Grovan is not bound by the Payment Authorities and that the amounts that were withheld from Grovan on the basis of the Payment Authorities should not have been withheld. Grovan is entitled to payment of those amounts. Further, in relation to the unit trust accounts, Grovan has established that an adjustment is required to be made.

(c) In relation to the cross-claim, I conclude that this is not made out. I find that Mr Price (or CRP) did continue to work on the Project in the period August to November 2008; that Twentieth Green did not comply with the procedure in the Simple Works Contract for making defect claims; and that Twentieth Green waived (in the sense of estoppel) its right to require CRP to complete the works by the date in the Simple Works Contract.

PROCEDURAL BACKGROUND

Parties

8 The applicants are CRP and Grovan. CRP was the builder for the Project. Grovan was one of the unit holders in a unit trust which carried out the Project, known as the Twentieth Green Unit Trust (the Unit Trust). The unit holders, and their respective interests, were:

(a) the first respondent (Four Oaks), a company associated with the fourth respondent, Noel Reynolds, and which had a 25% interest;

(b) the second respondent (NJC), a company associated with the fifth respondent, Stephen Power, and which had a 10% interest;

(c) the third respondent (ESA), a company associated with the sixth respondent, Geoffrey Rice, and which had a 25% interest;

(d) Retail Treasury Pty Ltd (in liq) (Retail Treasury), a company associated with the eighth respondent, Clestus Weerappah, and which had a 30% interest;

(e) Grovan, the directors of which were Mr and Mrs Price, and which had a 10% interest.

9 The trustee of the Unit Trust, Twentieth Green, is the seventh respondent to the proceeding.

10 The first to seventh respondents were jointly represented in the proceeding. As noted above, the eighth respondent, Mr Weerappah, did not file an appearance or appear at trial. He was, however, a witness called by the first to seventh respondents.

Pleadings

11 By their amended originating application (the Originating Application), the applicants seek declarations and make monetary claims. The declarations the applicants seek are that:

(a) the respondents have breached the agreements alleged in the amended fast track statement (the Fast Track Statement);

(b) the Simple Works Contract is void for uncertainty;

(c) the First Payment Authority and the Second Payment Authority provided no proper basis for the payment of any part of Grovan’s entitlement to the profits of the Project to any party other than Grovan;

(d) by making the representations alleged in the Fast Track Statement, the individual respondents engaged in conduct that was misleading or deceptive, or likely to mislead or deceive, contrary to s 9 of the Fair Trading Act 1999 (Vic) (the Fair Trading Act);

(e) the corporate respondents:

(i) made representations to CRP which were misleading or deceptive, or likely to mislead or deceive, contrary to s 52 of the Trade Practices Act 1974 (Cth) (the Trade Practices Act); and

(ii) engaged in unconscionable conduct within the meaning of s 51AC of the Trade Practices Act;

(f) the individual respondents aided, abetted, counselled or procured, or were directly or indirectly knowingly concerned in, or party to, the conduct of the corporate respondents which contravened ss 52 and 51AC of the Trade Practices Act.

12 In the Originating Application, CRP claims:

(a) as against Twentieth Green, the sum of $1,431,364;

(b) as against all of the respondents:

(i) damages for breach of the alleged agreements;

(ii) damages pursuant to s 82 of the Trade Practices Act of an amount to be determined;

(iii) damages pursuant to s 159 of the Fair Trading Act of an amount to be determined.

13 Grovan claims, in the Originating Application:

(a) orders requiring the respondents to repay such moneys they received from Twentieth Green as dividends or return of capital from the Project;

(b) as against all of the respondents:

(i) the sum of $156,563 as reimbursement for Grovan’s capital contribution less the sum of Grovan’s capital return;

(ii) an amount to be determined representing Grovan’s share of the profit derived by the Unit Trust from the Project;

(iii) damages pursuant to s 82 of the Trade Practices Act of an amount to be determined;

(iv) damages pursuant to s 159 of the Fair Trading Act of an amount to be determined.

14 I now summarise the applicants’ claims as set out in the Fast Track Statement, together with the first to seventh respondents’ responses to those claims:

(a) The applicants allege that an agreement (the First Agreement) was formed in or about early to mid-2006 between Mr Reynolds, Mr Rice, Mr Stephen Power, Mr Price and Mr Weerappah under which each agreed:

(i) to contribute such funds as were required (after financing part of the costs from a third party), to purchase the property and to complete the Project, in proportion to each unit holder’s unit holding in the Unit Trust;

(ii) on completion of the Project, to sell the units developed on the property and, after payment of all liabilities incurred in relation to the Project, to repay any moneys borrowed by Twentieth Green from financiers and then to distribute the balance of the moneys to each unit holder in the Unit Trust in proportion to its unit holding.

(b) In their fast track response, cross-claim and rejoinder (Fast Track Response), the first to seventh respondents admit the First Agreement save that they say that the terms of the agreement differed in the following respects:

(i) the First Agreement, while negotiated by the individual respondents and Mr Price, was made between the unit holders and Retail Treasury;

(ii) the unit holders and Retail Treasury were required to contribute equity before finance could be obtained;

(iii) the apartments developed on the property were not to be sold after completion, but were to be sold off the plan before construction commenced to obtain finance; and

(iv) each of the unit holders and Retail Treasury was entitled to elect to take title to a completed apartment in lieu of part of its right to profits from the Unit Trust.

(c) In the Fast Track Statement, the applicants alleged a second agreement (the Second Agreement) to the following effect: in or about November 2006, Mr Reynolds, Mr Stephen Power, Mr Weerappah and Mr Rice agreed with Mr Price that CRP would undertake the required building works on the property to renovate and build new units on the basis that CRP would be paid the cost of all materials and labour incurred in relation to the works plus a margin of 15%. However, at trial, the applicants said that they would not rely on the Second Agreement, in view of the provisions of the Domestic Building Contracts Act 1995 (Vic) (the Domestic Building Contracts Act). (See, in particular, ss 13 and 31 of that Act.)

(d) The applicants allege a third agreement (the Third Agreement) to the effect that, in or about November 2006, Mr Reynolds, Mr Stephen Power, Mr Weerappah and Mr Rice agreed with Mr Price that they would enter into the Simple Works Contract and that it would only be used to obtain finance for the Project and would not record the terms under which CRP was to perform the works. The particulars in relation to this allegation state that the agreement was negotiated at a meeting held at the offices of Holiday Concepts Corporation Pty Ltd (Holiday Concepts) (a company associated with Mr Reynolds and Mr Rice) in Richmond, Victoria in or about November 2006 at which Mr Reynolds, Mr Stephen Power, Mr Weerappah, Mr Rice and Mr Price were present. The first to seventh respondents deny the alleged agreement and make some positive allegations in their Fast Track Response, but it is not necessary to set them out.

(e) In a pleading introduced with leave at the beginning of the trial, the applicants allege that the Simple Works Contract is void for uncertainty. The particulars to that allegation state that the works to be carried out were not specified or agreed, nor was there any mechanism provided within the contract by which those matters would be determined. The allegation is denied.

(f) The applicants allege that Mr Reynolds, Mr Power, Mr Weerappah and Mr Rice made representations (the Contract Representations) to similar effect as the Third Agreement, namely that the Simple Works Contract would only be used to obtain finance for the Project and would not record the terms under which CRP was to perform the works. The allegation is denied.

(g) The applicants allege that CRP performed the works in reliance on (i) a representation to similar effect as the Second Agreement, namely that CRP would be paid the cost of all materials and labour incurred in relation to the works plus a margin of 15%; and (ii) the Contract Representations (together defined as the Works Payment Representations). The allegation is denied.

(h) In the Fast Track Statement, the applicants alleged a fourth agreement (the Fourth Agreement) to the following effect: in early 2008, Mr Reynolds, Mr Power, Mr Weerappah and Mr Rice agreed with Mr Price that if CRP continued to undertake the works still to be completed, and funded the costs to complete those works, they would ensure that CRP was paid the cost of all materials and labour plus a margin of 15%. However, the applicants indicated at trial that they would not rely on this alleged agreement, in view of the provisions of the Domestic Building Contracts Act.

(i) The applicants alleged that Mr Reynolds, Mr Stephen Power, Mr Weerappah and Mr Rice made representations (the Variation Representations) to similar effect, namely that if CRP continued to undertake the works still to be completed, and funded the costs to complete those works, they would ensure that CRP was paid the cost of all materials and labour plus a margin of 15%. The allegation is denied.

(j) CRP contends that the individual respondents, by making the Contract Representations, the Works Payment Representations and the Variation Representations, made representations to CRP which were misleading or deceptive, or likely to mislead or deceive, contrary to s 9 of the Fair Trading Act; further or alternatively, the corporate respondents made representations to CRP which were misleading or deceptive, or likely to mislead or deceive, contrary to s 52 of the Trade Practices Act, and engaged in unconscionable conduct within the meaning of s 51AC of the Trade Practices Act. CRP also contends that the individual respondents aided, abetted, counselled or procured, or were directly or indirectly knowingly concerned in, or party to, the conduct of the corporate respondents which was in contravention of ss 52 and 51AC. These allegations are denied.

(k) CRP contends, further or in the alternative, that on a quantum meruit basis it was entitled to be paid an amount of $678,634 (being the amount funded by CRP to complete the works); an amount of $453,123 (being 15% of the actual cost); and an amount of $299,605 (being interest paid by CRP to its financiers to fund the completion of the works after about April 2008), before any payments were made by Twentieth Green to any of the unit holders, and that Four Oaks, NJC and ESA should be ordered to repay such moneys as they received from Twentieth Green as dividends or return of capital. These allegations are denied.

(l) Grovan contends that in breach of the First Agreement and the terms of the trust deed for the Unit Trust, the respondents have failed to:

(i) account to Grovan for the profit or loss derived from the Project after payment of all liabilities incurred in relation to the Project and after repaying moneys borrowed by Twentieth Green from financiers;

(ii) account to Grovan for the returns of capital to the unit holders in the Unit Trust after payment of all liabilities incurred in relation to the Project and after repaying moneys borrowed by Twentieth Green from financiers;

(iii) provide to Grovan any accounting for the activities of the Unit Trust;

(iv) reimburse Grovan for its contribution of capital to the Project; and

(v) distribute to Grovan in accordance with its unit holding in the Unit Trust the profit derived by the Unit Trust from the Project after payment of all liabilities incurred in relation to the Project and after repaying moneys borrowed by Twentieth Green from financiers.

(m) The first to seventh respondents deny these allegations. They also allege in the Fast Track Response that:

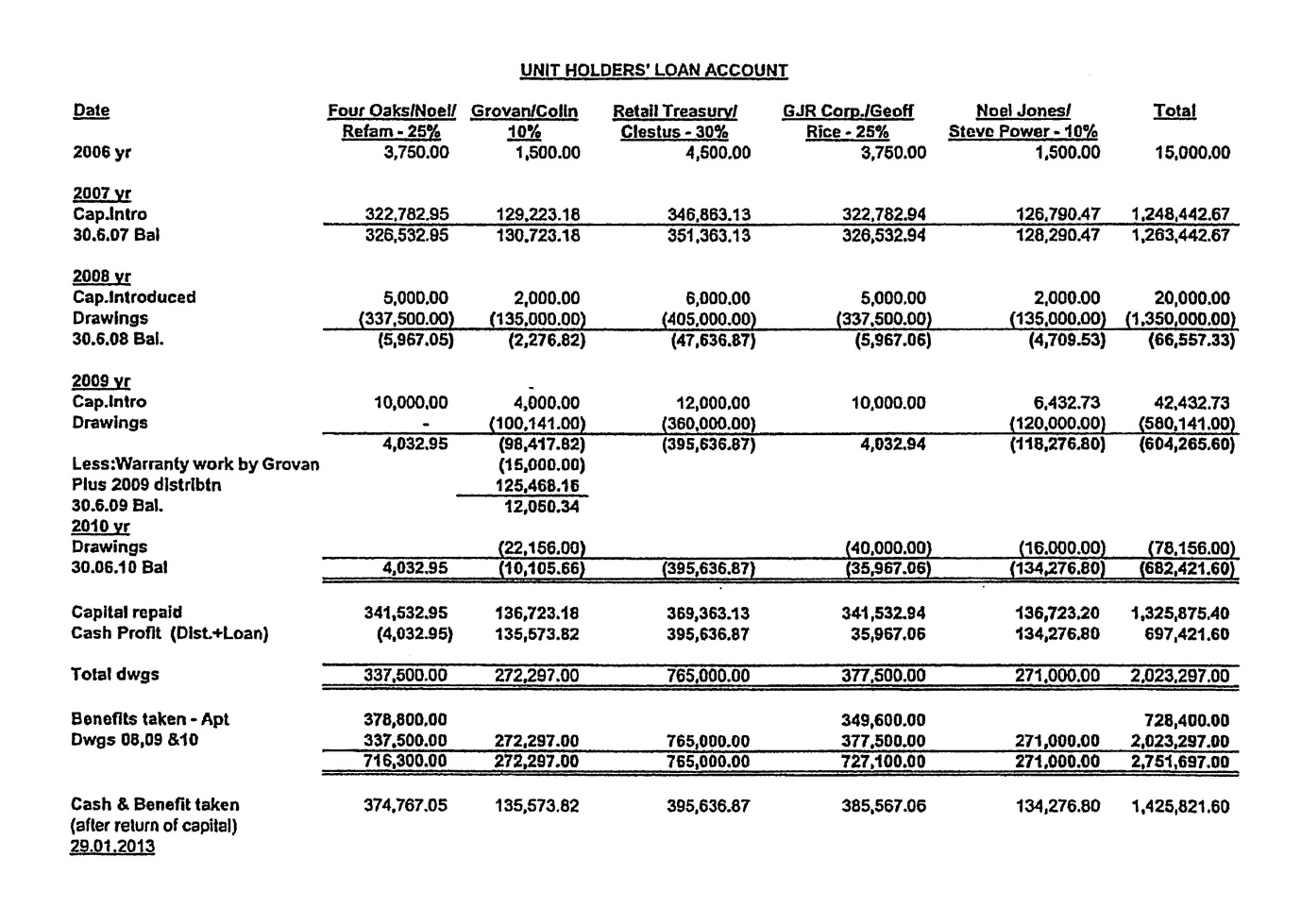

(i) at the conclusion of the Project, Grovan’s entitlement to a share of the proceeds of the Project was $272,297;

(ii) Twentieth Green distributed $157,156 directly to Grovan, as to $135,000 in the 2008 financial year and as to $22,156 in the 2009 financial year;

(iii) $10,105 was retained by Twentieth Green to pay for rectification of defects in the works for which CRP was responsible; and

(iv) $100,141 was paid by Twentieth Green, as instructed by Mr Price on behalf of Grovan, to Resort Systems Pty Ltd (Resort Systems) as repayment of moneys owed by CRP or Mr Price to Resort Systems, pursuant to the First Payment Authority and the Second Payment Authority.

(n) In response to the allegations regarding the First and Second Payment Authorities, the applicants contend in their amended fast track reply and defence to cross-claim:

(i) that the Payment Authorities were not signed by Mr Price (but this contention was not pressed at trial);

(ii) if they were signed by Mr Price, they were not signed by Mrs Price and therefore were not binding on Grovan;

(iii) if they were signed by Mr Price, Mr Price breached his fiduciary duties to Grovan by signing them as Grovan received no corporate benefit from signing the Payment Authorities; the directors of Twentieth Green were directors of Resort Systems (the beneficiary of the Payment Authorities) and were aware of Mr Price’s breach of fiduciary duties; Mr Reynolds, Mr Stephen Power and Mr Rice and through them the unit holders (excluding Grovan) knowingly assisted Mr Price in the breach of his fiduciary duties to Grovan; each of the unit holders (except Grovan) knowingly received the benefits of the payments made pursuant to the Payment Authorities; each of the respondents is obliged to repay the amount of $100,141 (referred to in sub-paragraph (m) above) to Grovan;

(iv) if the Payment Authorities were signed by Mr Price, it is unconscionable in all the circumstances for the respondents to seek to rely on them;

(v) the First Payment Authority only applied to present or past indebtedness as at the date of execution (namely, 3 September 2008); only applied to advances made by Resort Systems; and only applied to advances made to “C.R. Price and Associates”;

(vi) in fact, there was no such entity as “C.R. Price and Associates”; there was no indebtedness of $150,000 (as referred to in the First Payment Authority) owed by “C.R. Price and Associates” or any other entity to Resort Systems as at 3 September 2008; the payments relied on by the first to seventh respondents as ‘advances’ in their affidavit evidence were not all made by Resort Systems; in the premises, the First Payment Authority is void for uncertainty;

(vii) the First Payment Authority required Grovan to be answerable for alleged advances made to “C.R. Price and Associates” and, as such, was in the nature of a guarantee; in purporting to make Grovan answerable for the alleged advances made to “C.R. Price and Associates”, Grovan was a volunteer; if Mr Price did sign the First Payment Authority, he did so under a special disadvantage or disability (in that the effect of the document was not explained to him and he was given no opportunity to obtain legal or financial advice in relation to it; the effect of the document was confused and confusing; to the knowledge of the respondents, Mr Price was under significant financial and emotional distress and duress caused by the respondents’ failure to pay CRP for the work carried out on the Project and CRP and Mr and Mrs Price were facing financial ruin; Mr Price had enjoyed a trusting relationship with the respondents for a long time); the respondents took unconscientious advantage of Mr Price’s position of special disadvantage or disability in procuring his signature on the First Payment Authority; in the premises, Grovan is entitled to avoid the First Payment Authority and have it set aside, delivered up or cancelled;

(viii) the First Payment Authority, being in the nature of a guarantee, was not executed by Grovan, the party to be bound, in accordance with s 126 or 127 of the Corporations Act 2001 (Cth) (the Corporations Act) and is therefore void pursuant to s 126 of the Instruments Act 1958 (Vic) (the Instruments Act);

(ix) in the premises, the First Payment Authority provided no basis upon which Twentieth Green was entitled to apply Grovan’s entitlements to a share of the proceeds of the Project otherwise than by payment to Grovan;

(x) in respect of the Second Payment Authority: it identified the party undertaking to “repay principal and interest” as Mr Price; it made provision for execution by “Grovan Pty Ltd By Colin Price”; it did not identify to whom the “advances” the subject of the document were made; it referred to “various advances made by Resort Systems Pty Ltd and other associated Companies”; it provided for Mr Price to repay principal and interest out of “distributions from Twentieth Green Pty Ltd and Gruboc Pty Ltd [(Gruboc)] as and when they fell due”;

(xi) in fact, the Second Payment Authority fails to identify to whom the advances were made and in respect of what advances the undertaking to pay was made; it is unclear whether the party undertaking to be bound is Mr Price in his personal capacity or is Grovan; if the party undertaking to be bound is Mr Price personally, he did not sign the document in that capacity; the undertaking provided for Mr Price personally to repay principal and interest out of proceeds of distributions that were payable, not to him, but rather to Grovan; the payments relied upon by the respondents as ‘advances’ in their affidavit evidence were not all made by Resort Systems; and one of the ‘advances’ was paid by NJC, a company that was not associated with Resort Systems;

(xii) in the premises, the Second Payment Authority is void for uncertainty and provided no basis upon which Twentieth Green was entitled to apply Grovan’s entitlements to a share of the proceeds of the Project otherwise than by payment to Grovan;

(xiii) the Second Payment Authority purports to require Mr Price, or in the alternative Grovan, to be answerable for unspecified advances made to an unspecified party, but insofar as it may be found to have some meaning, it was in the nature of a guarantee; in purporting to make Mr Price, alternatively Grovan, answerable for the alleged advances, Mr Price or Grovan was a volunteer; if Mr Price did sign the Second Payment Authority, he did so under a special disadvantage or disability (for similar reasons to those set out in sub-paragraph (vii) above); the respondents took unconscientious advantage of Mr Price’s position of special disadvantage or disability in procuring his signature on the Second Payment Authority; in the premises, Grovan is entitled to avoid the Second Payment Authority and have it set aside, delivered up or cancelled;

(xiv) the Second Payment Authority, being in the nature of a guarantee, was not executed by the person to be charged, Mr Price personally, or in the alternative Grovan (pursuant to s 126 or 127 of the Corporations Act), and is therefore void pursuant to s 126 of the Instruments Act;

(xv) in the premises, the Second Payment Authority provided no basis upon which Twentieth Green was entitled to apply Grovan’s entitlements to a share of the proceeds of the Project otherwise than by payment to Grovan.

(o) In the Fast Track Response, the first to seventh respondents have a rejoinder (the Rejoinder) to the above allegations regarding the Payment Authorities. They deny the allegations and say, further or alternatively, that:

(i) on or about 3 September 2008, CRP informed Twentieth Green that CRP did not have the financial resources needed to complete the Project;

(ii) by an agreement made on 3 September 2008, Twentieth Green, CRP and Grovan agreed that Twentieth Green would procure that the moneys required to enable CRP to complete the Project were advanced to it (the Advance); and Grovan authorised Twentieth Green to withhold and apply an amount equal to the Advance from Grovan’s entitlement as unit holder to 10% of the proceeds of the Project, in satisfaction of the Advance; and

(iii) in performance of the agreement referred to in sub-paragraph (ii) above, Twentieth Green procured that the Advance was made to CRP and CRP was thereby able to complete the Project;

(iv) CRP and Grovan have accepted the Advance and the benefit thereof;

(v) by reason of the matters set out in sub-paragraphs (i) to (iv) above, it would be unconscionable for CRP and Grovan to deny the making of the said agreement;

(vi) accordingly, CRP and Grovan are estopped from denying the making of the said agreement and that Twentieth Green was duly authorised to withhold and apply an amount equal to the Advance, from Grovan’s entitlement as unit holder to 10% of the proceeds of the Project, in satisfaction of the Advance;

(vii) further, Twentieth Green is entitled to set off, alternatively it is just and equitable that Twentieth Green be entitled to set off, against any amount otherwise payable to Grovan by way of distribution from the Project as is necessary to satisfy the Advance and so to satisfy the Advance before the payment of any distribution to Grovan.

15 The first to seventh respondents’ cross-claim (and the pleadings in response) can be summarised as follows:

(a) It is alleged that there were terms of the Simple Works Contract as follows:

(i) CRP was to: complete the works to the standard set out in the contract documents; begin the works within 10 working days after receiving possession of the site; and carry out all necessary work diligently;

(ii) CRP was to direct the manner of performance of the necessary works and supervise the necessary works competently;

(iii) CRP warranted that its estimate of the number of working days needed to complete the works included a reasonable allowance for reasonable delays;

(iv) CRP was to bring the works to practical completion by 8 November 2007;

(v) CRP warranted that the contract price of $2,133,285 allowed for everything reasonably required to complete the works.

(b) The first to seventh respondents allege that, in or about August 2008, CRP repudiated the Simple Works Contract. The particulars under this allegation state that CRP ceased work on the Project and left the property without having completed the works. It is also pleaded that Twentieth Green accepted the repudiation.

(c) The first to seventh respondents allege that, in breach of the Simple Works Contract, CRP failed to bring the works to practical completion by 8 November 2007, and CRP failed to complete the works to the standard set out in the contract documents.

(d) It is alleged that CRP’s breach of contract, alternatively repudiation of contract, has caused Twentieth Green loss and damage. The particulars under this allegation state that: from the date of practical completion in the Simple Works Contract until actual practical completion, Twentieth Green paid $205,048 in interest to its financier, Bank of Western Australia Ltd (BankWest); and Twentieth Green caused defects to be rectified at a cost of $10,105 (which it claims if, contrary to its primary contention, it was not entitled to withhold that amount).

(e) The first to seventh respondents also contend that if CRP succeeds in its claim against Twentieth Green for all or part of its claim, then Twentieth Green claims from Grovan the amount that is equal to 10% of the amount of CRP’s successful claim, being Grovan’s contribution in proportion to its unit holding in the Unit Trust.

(f) In response to the cross-claim, the applicants in their amended fast track reply and defence to cross-claim admit that the terms of the Simple Works Contract are as alleged but say that the Simple Works Contract did not govern the terms upon which CRP agreed to undertake the works, and say that CRP and the respondents did not undertake the Project in accordance with the Simple Works Contract. Nine examples are provided to support these propositions; it is not necessary to set them out.

(g) CRP denies that it ceased work on the Project or that it left the property without completing all aspects of the works. CRP also says that, if the Simple Works Contract governed the terms upon which CRP undertook the works, CRP admits the works were not completed by 8 November 2007, but says that the respondents took no action when this occurred and allowed CRP to complete the works after 8 November 2007.

(h) In relation to the defects claim, CRP says that, if the Simple Works Contract governed the terms upon which CRP undertook the works, CRP denies that the alleged defects existed at handover, or that the Simple Works Contract required CRP to undertake such works.

(i) The applicants admit that Grovan’s claim in the proceeding is to be reduced by 10% of any sum awarded in favour of CRP, excluding any sum of costs or interest awarded in this proceeding against Twentieth Green in favour of CRP.

(j) Save as indicated above, the applicants deny the allegations in the cross-claim.

(k) The first to seventh respondents filed a fast track reply in response to cross-claim. Among other things, by this document the first to seventh respondents contend that to the extent, if at all, Twentieth Green did not enforce its rights under the Simple Works Contract, this did not constitute a waiver by virtue of a ‘no waiver’ clause in the contract.

Separate questions

16 On 6 December 2013, a judge of this Court made orders for the determination of separate questions in the following terms:

2. The issues set out in Orders 3 and 4 be determined before any other issues.

3. The Court determine on what basis the First Applicant (CRP) was entitled to be remunerated for performing the Works (or so much of them as it performed), in particular, whether:

(a) the terms of CRP’s engagement to undertake the Works for the Project is governed by the Contract;

(b) CRP and any or all the Respondents entered into agreements on the terms of the First Agreement, Second Agreement, Third Agreement and Fourth Agreement;

(c) the Second Agreement is void pursuant to the Domestic Building Contracts Act 1995 (Vic);

(d) the Third Agreement was capable of acceptance and accepted by the parties, was supported by consideration and was enforceable;

(e) the Fourth Agreement was supported by consideration;

(f) the Representations were:

(i) made;

(ii) misleading and deceptive;

(iii) relied upon by CRP;

(g) CRP is entitled to claim payment from the Respondents for goods and services supplied by it or contractors it engaged and paid to perform the Works for the Project on a quantum meruit basis and that the appropriate margin for the works was 15%;

(h) in all the circumstances concerning the course of dealings between the parties over many years, the circumstances surrounding the signing of the Contract and the making of the Representations, it would be unconscionable for:

(i) the First to Seventh Respondents to assert the Contract against CRP; and

(ii) for the First to Seventh Respondents not to pay the Claimed Amount or in the alternative an amount determined on a quantum meruit basis and that the appropriate margin for the works was 15%.

4. The Court determine all of the claims made by the Second Applicant (Grovan) in the Applicants’ Fast Track Application and all of the claims made by the First to Seventh Respondents in their Fast Track Cross-Claim.

17 As noted above, the effect of these orders was that the trial of the separate questions covered all aspects of CRP’s claims other than the quantum of any amounts payable to CRP, and all aspects of Grovan’s claims and the respondents’ cross-claim.

Trial

18 At trial, the applicants adduced evidence from the following witnesses:

(a) Mr Price, the sole director of CRP and a director of Grovan. Three affidavits of Mr Price were filed in the proceeding. Of these, only his first affidavit (dated 5 July 2013) and his third affidavit (dated 22 September 2015) were tendered in evidence by the applicants. His second affidavit, which related to a security for costs application, was not tendered by the applicants, but a paragraph from this affidavit was tendered by the first to seventh respondents.

(b) Faye Price, a director and the secretary of Grovan, and the wife of Mr Price.

(c) Jamie Vanderschoot, a builder engaged by Mr Price in relation to the Project.

(d) John Pimlott, a sub-contractor engaged by Mr Price in relation to the Project.

19 Mrs Price, Mr Vanderschoot and Mr Pimlott were not required for cross-examination. The evidence contained in their affidavits is therefore unchallenged and is accepted.

20 The first to seventh respondents adduced evidence from the following witnesses:

(a) Mr Reynolds.

(b) Mr Rice.

(c) Trevor Joyce, a forensic document examiner, who gave expert evidence in two affidavits about the signatures on the First Payment Authority and the Second Payment Authority. He was not required for cross-examination and his evidence is to be accepted.

(d) Mr Weerappah.

(e) Robert Power, who is the brother of Stephen Power. He was engaged by Twentieth Green to carry out some work on the Project from about mid to late 2008.

(f) Mr Stephen Power.

21 During the trial, the applicants served two notices to produce on the first to seventh respondents requiring production of documents relating to the accounting for the Project. This was in a context where there had been no orders for discovery by the first to seventh respondents. In response to the notices to produce, financial and other documents were produced during the course of the trial and then formed part of the cross-examination of the first to seventh respondents’ witnesses. This meant that some of the matters raised with those witnesses during cross-examination had not been the subject of prior particularisation or evidence adduced by the applicants.

ISSUES TO BE DETERMINED

22 In light of the pleadings and concessions set out above, the issues to be determined on the trial of the separate questions can be summarised as follows:

(a) In relation to CRP’s claims:

(i) Did the parties agree that the Simple Works Contract would only be used to obtain finance for the Project and would not record the terms under which CRP was to perform the Works?

(ii) Was the Simple Works Contract void for uncertainty?

(iii) Did the respondents make the Contract Representations?

(iv) Did the respondents make the Works Payment Representations?

(v) Did the respondents make the Variation Representations?

(vi) Have the respondents engaged in misleading or deceptive conduct which was relied on by CRP?

(vii) Is CRP entitled to be paid on a quantum meruit basis and, if so, at a margin of 15%?

(viii) Would it be unconscionable for the respondents to assert the Simple Works Contract against CRP, and for the respondents not to pay CRP the amount it claims or an amount determined on a quantum meruit basis?

(b) In relation to Grovan’s claims:

(i) Did the parties make the first agreement alleged in the Fast Track Statement?

(ii) Were the respondents entitled to rely on the First Payment Authority, the Second Payment Authority or the agreement pleaded in the Rejoinder to otherwise apply amounts due to Grovan?

(iii) Were Grovan’s entitlements wrongly withheld to pay for defects work?

(iv) Has Grovan been underpaid its entitlements?

(c) In relation to the cross-claim:

(i) Did CRP repudiate the Simple Works Contract in about August 2008 and was any repudiation accepted?

(ii) Did CRP breach the Simple Works Contract by failing to complete the works by 8 November 2007?

(iii) Did CRP breach the Simple Works Contract by failing to complete the works to the required standard?

(iv) Has Twentieth Green suffered loss and damage as a result of any repudiation or breach by CRP?

FACTUAL FINDINGS

23 I set out below my factual findings relevant to the issues to be determined, based on the affidavit and oral evidence and the documents in evidence. Where I do not refer to the evidentiary source of a factual finding, the matter was common ground or at least not controversial. I first make some observations about the witnesses.

24 The events with which this proceeding is concerned happened some time ago and none of the witnesses who were cross-examined had a good recollection of the relevant conversations or a precise recall of the detail or sequence of events. All of the witnesses who were cross-examined (with the exception of Mr Robert Power) had an interest in the outcome of the proceeding which may have affected their evidence.

25 In relation to Mr Price, while I consider his evidence to have been honestly given, he did not have a clear recollection of the events in question. There were significant inconsistencies between his first and third affidavits. There were also inconsistencies between his affidavit and oral evidence. I think these deficiencies were a product of insufficient familiarity with the process of preparation of affidavits and poor recollection of matters of detail, rather than any dishonesty. Mr Price made concessions during cross-examination, indicating that he was genuinely attempting to assist the Court to establish the relevant facts. Mr Price was a somewhat hesitant witness who, in his oral evidence, did not seek to exaggerate matters or advocate for the applicants’ case. If anything, on occasion, he understated matters that assisted the applicants’ case.

26 Mr Reynolds is a successful business man, now 80 years old. Prior to the Project, he was involved in the development of several time-share resorts. In his evidence at trial, he emphasised that both he and Mr Rice took a “back role” or “back seat” in relation to the Project, leaving the management of the project principally to others. Perhaps inconsistently with this, Mr Reynolds expressed himself in strong terms about many aspects of the Project and arrangements with Mr Price. Mr Reynolds did not appear to have a clear recollection of the relevant conversations.

27 Mr Rice played a limited role in relation to the Project. His evidence did not deal in detail with many of the matters in issue.

28 Mr Weerappah pleaded guilty and was convicted of three counts of using his position dishonestly with the intention of gaining an advantage contrary to s 184(2)(a) of the Corporations Act. He also pleaded guilty to making a false or misleading statement or admission in a document lodged with the Australian Securities and Investments Commission contrary to s 1308(2) of the Corporations Act and to an offence of falsifying books relating to the affairs of a company contrary to s 1307(1) of the Corporations Act. He was sentenced to imprisonment for these offences, with a total effective sentence of four years’ imprisonment, and with a non-parole period of two years. These offences, while not relating to the same subject matter as this proceeding, involved dishonesty. In these circumstances, I will generally place no weight on Mr Weerappah’s affidavit and oral evidence unless it was not challenged or was confirmed by objective evidence (such as unchallenged documents).

29 Mr Robert Power’s role in relation to the Project was limited to the period from mid to late 2008. His evidence was not material to many of the issues in dispute.

30 Mr Stephen Power’s background was in the sales and marketing side of the Holiday Concepts business. The Project was his first involvement in a property development project. He had the day-to-day responsibility for managing the Project and had general supervision of matters such as payments in and out in respect of the Project.

31 Taking into account the matters set out in paragraphs [24]-[27] and [29]-[30], I will generally place little weight on the affidavit and oral evidence of each of the witnesses discussed in those paragraphs unless it is unchallenged or supported by objective evidence (such as unchallenged documents). In relation to Mr Reynolds, Mr Rice and Mr Stephen Power, the applicants contend that each of them was involved in the preparation of false or misleading documents and this constitutes ‘tendency evidence’ which is relevant to the issues to be determined. I deal with this issue in paragraphs [230] to [235] below. For the reasons there given, I do not consider that the relevant evidence is admissible to prove that they had a tendency to act in a particular way. While the evidence referred to in those paragraphs is admissible in relation to credibility, in view of the general approach I will adopt to the affidavit and oral evidence of these witnesses, I do not consider any further allowance to be required.

The period before October 2005

32 Mr Price qualified as an architectural draftsman at Moorabbin TAFE. From about 1979, he worked for architectural firms. In about 1981, while he was working for a firm of architects, he met Mr Reynolds. Initially, Mr Price undertook drafting or design work for Mr Reynolds’s projects. Over time, the amount of work he carried out for Mr Reynolds increased.

33 In 1987, Mr Price incorporated CRP. From 1987 onwards, CRP provided drafting, design, building and construction services to clients.

34 From 1989, Holiday Concepts, which was involved in building time-share resorts, was the major client of CRP. In about 2000, Mr Price moved his business to the Richmond offices of Holiday Concepts.

35 CRP was commissioned by Holiday Concepts to work on numerous projects. In some cases, it carried out design work; in some cases, it acted as a project supervisor (or building supervisor); and in some cases from 1996 onwards it acted as the builder or principal contractor. Mr Price obtained registration with the Building Practitioners Board as a domestic builder in 1996; it was after he obtained this registration that he carried out work as builder or principal contractor.

36 When Mr Price (or CRP) undertook design work or project supervision work for Holiday Concepts, he charged on an hourly rate basis.

37 Where Mr Price (or CRP) was engaged as the builder, he charged on a ‘cost plus’ basis, that is, he charged the cost of labour and materials plus a percentage margin. This was accepted by Mr Reynolds and Mr Stephen Power during cross-examination.

38 There was dispute, however, as to the percentage of the margin in such cases. Mr Reynolds’s evidence was that it was always 10%. Indeed, he said during cross-examination: “I had an agreement with him for 10 per cent”. On the other hand, Mr Price’s evidence was that it was 10 or 15%, as he considered appropriate given the complexity of the job.

39 In paragraph 12 of his first affidavit, Mr Price said that when CRP was engaged as principal contractor, CRP charged and was paid on a costs plus percentage basis, being a margin of 15% which was added to the total labour and materials costs per progress claim of the project. He stated that CRP was never required to submit, and never submitted, quotes in advance of commencing the works. He also stated (in the last sentence of paragraph 12): “CRP always charged the 15% margin to the total labour and material costs, and that margin was never questioned or objected to by Holiday Concepts.” During cross-examination, Mr Price accepted that the last sentence of paragraph 12 was untrue and said that the amount charged varied, from 10 to 15%.

40 In his third affidavit, Mr Price stated that he determined whether CRP would charge Holiday Concepts a margin of either 10 or 15%, depending on the nature of the work involved in the project. He annexed to that affidavit some examples of invoices with a 10% margin and said that he had not been able to locate invoices where CRP charged a margin of 15% as these jobs were before 2006 and he had not kept the records. He said that whether CRP charged a margin of 10 or 15% for a particular project was not something he first discussed with Mr Reynolds, Mr Rice or anyone else at Holiday Concepts.

41 During cross-examination, Mr Price accepted that on most projects with Holiday Concepts where he was engaged as the builder, he charged a margin of 10%.

42 In light of the evidence discussed above, and in the absence of documentary evidence that Mr Price (or CRP) charged a margin higher than 10% when engaged as the builder by Holiday Concepts, I conclude that when Mr Price (or CRP) was engaged as the builder by Holiday Concepts this was on the basis of the cost of labour and materials plus a margin of 10%.

43 There was a conflict between the evidence of Mr Price and Mr Reynolds as to whether a ‘ballpark’ figure was provided in advance of work being carried out as the builder. Mr Price gave evidence that he was not required to, and did not, provide such a figure; Mr Reynolds said that this was provided. It is unnecessary to resolve this.

44 Mr Price stated in his third affidavit: “I had enjoyed a long relationship with Noel Reynolds, Geoff Rice and Holiday Concepts and I trusted them and I believed they trusted me to do the fair thing by them.” Mr Reynolds accepted during cross-examination that he had a trusting relationship with Mr Price. Their evidence to this effect is to be accepted.

October 2005 to October 2006

45 In late 2005, Mr Reynolds invited Mr Price to become an equity participant in some property development projects together with Mr Reynolds, Mr Rice, Mr Stephen Power and Mr Weerappah. Mr Price accepted. (Although in Mr Price’s first affidavit, he referred to this as occurring in early 2006, it is likely to have taken place in late 2005, as the trust deed for the Unit Trust (in which Grovan is named as a unit holder) is dated 14 October 2005.) In Mr Price’s first affidavit he gave evidence, which I accept, that it was explained to him by Mr Reynolds that:

(a) for each residential development project, the Syndicate set up a unit trust with each of the Syndicate member’s respective family trust companies holding units in the unit trust in proportion to their level of participation;

(b) CRP would project manage the residential development projects from feasibility through to completion, including design management, land acquisition, permit applications, negotiations with statutory authorities and project and construction management;

(c) CRP would be paid on hourly rates for work undertaken by me in relation to the services set out in paragraph … (b) above;

(d) Stephen Power’s role involved land acquisition, finance and sales; and

(e) Clestus Weerappah had a property investment background and had expertise in selecting properties for development, and for undertaking the feasibility studies for each project including build and construction costs.

46 On 14 October 2005, the Twentieth Green Unit Trust was formed. The corporate entities and percentage interest of each unit holder are set out in paragraph [8] above. The reason the company and trust were called Twentieth Green was because the syndicate members were initially interested in buying a golf course in Frankston. Ultimately, they did not acquire that property. They then looked for other opportunities.

47 In or about July 2006, the property in Box Hill was identified by Mr Weerappah. At this stage, town planning documents (Ex R10, tab 9) for the refurbishment of 15 apartments and the construction of eight new apartments were in existence, having been prepared in 2005, and a planning permit for this work had been obtained.

48 In July 2006, emails were exchanged between Mr Weerappah, Mr Rice and Mr Stephen Power in relation to the potential project in Box Hill. On Tuesday 25 July 2006, Mr Weerappah sent an email to Mr Rice and Mr Stephen Power with the subject line, “Update on Projects”. In the email, Mr Weerappah stated that he attached a feasibility for a set of apartments in 33 Albion Street, Box Hill; it had 15 apartments to be refurbished and plans for eight new apartments; he had sent the plans to Build Rite to finalise their costings for the work; and “I need to know if Colin [ie, Mr Price] is able to perform the work on the refurbished apartments himself and therefore the brief to Build Rite is only extending to the build of the new apartments”. Build Rite were a firm of builders carrying out a project in Oakleigh for Mr Reynolds. The email also stated:

I also know we are looking for Projects with a 30%+ return. Although this is around 20%, it is only a 9 month Project and would bring in $1,200,000 in profit. At around $56k per apartment profit, with little work and no risk, this is very reasonable and provides an alternative property to be offered to buyers instead of only having 1 standalone Project.

49 Mr Rice sent an email on the same day, in response to that email. His email stated in part: “Any chance of getting the plans ect (sic) for Box Hill so Pricey [ie, Mr Price] can determine the cost of refurb”.

50 Mr Weerappah then sent a further email to Mr Rice and Mr Stephen Power. This stated that Mr Weerappah would contact Mr Price and “try and get him past the site in Box Hill tomorrow in preparation for Thursday’s meeting”. This email attached an updated version of the feasibility document for the Box Hill project, indicating that Mr Weerappah had deleted an amount referable to marketing. The effect was to increase the projected profit per apartment to $70,000. I infer that the feasibility document attached to the email was an earlier version of the Feasibility Document in evidence, referred to in paragraph [58] below.

51 In late July or early August 2006, a site visit or site meeting took place, attended by all the syndicate members and two representatives of Build Rite. They were Bob Walpole and David Hanna. (Although Mr Reynolds during cross-examination referred to the first representative of Build Rite as Bob Newbold, most of the witnesses referred to him as Bob Walpole.) During the course of the site visit, the syndicate members and Build Rite representatives were walking around the site and talking in different groups; they did not stay together throughout the visit.

52 Mr Price gave evidence during cross-examination (and in his affidavits) that during the site visit he was discussing the cost of the project with the representatives of Build Rite and, in passing, Mr Hanna turned to him and said, “You won’t get much change out of three million, Col”. Mr Price said during cross-examination that he could not recall if Mr Reynolds or Mr Rice were present when this was said.

53 Mr Reynolds stated in his affidavit evidence that a representative of Build Rite at the site meeting said words to the effect, “You could build it for 2.2 million or 2.4 million if you used high quality finishes. But you don’t need high quality finishes on a place like this”. During cross-examination, Mr Reynolds said that Bob Newbold (it seems that this was Mr Walpole) told Mr Weerappah that “2.2 would do” to carry out the works, unless you want it “flashy”, in which case “you could probably spend 2.4”. Mr Reynolds said that Mr Rice and Mr Price were also present when this was said.

54 Mr Rice gave evidence in his affidavits and during cross-examination that during the site visit, Mr Walpole said in response to a question from Mr Reynolds that the cost of the development would be between $2.1 and $2.3 million, depending on the finishes. Mr Rice said during cross-examination that he could not recall whether Mr Price was present when this was said.

55 The evidence of Mr Reynolds and Mr Rice was put to Mr Price during cross-examination. He said that he could have been elsewhere on site and he did not know if he heard these statements or not.

56 Mr Reynolds also said during cross-examination that in the car on the way back (after the site visit), Mr Price said to him, “I believe there’s money to be made out of it” and that he replied, “Colin, if that’s what you feel, you do your numbers and you talk to the guys about it”. The reference to the “guys” was to the other syndicate members. Mr Reynolds did not refer to this conversation in his affidavits.

57 I express my findings in relation to the site visit below, after considering a meeting of syndicate member that took place soon after.

58 In or about early August 2006 (perhaps on the same day as the site visit or perhaps a few days later), there was a meeting of the members of the syndicate at the offices of Holiday Concepts in Richmond. Mr Weerappah tabled a one-page spreadsheet he had prepared assessing the feasibility of the Project (the Feasibility Document) (Ex R10, tab 3). The Feasibility Document included a box on the bottom left headed, “Project Summary”. This estimated revenue of $7,717,029, total cost (excluding land) of $2,807,145, land cost of $3,323,250, producing a profit of $1,586,634 which equated to a profit of 25.9% on costs and $68,984 profit per apartment. In the middle of the page was a section headed, “Construction Elemental Breakdown” with a total construction price of $2,105,000. That figure then appeared in the left-hand section of the spreadsheet. After adding GST, the figure for building costs was $2,315,300. Mr Stephen Power said during cross-examination (and I accept) that the Feasibility Document was a “a document brought to a table for people to consider as to whether it’s worth pursuing[;] so it’s a starting point”.

59 Mr Weerappah gave evidence that a written estimate of the constructions costs had been provided to him by Build Rite, but no such document was produced. Mr Stephen Power stated during cross-examination that at the time when the offer to purchase the property was made (15 August 2006), the only document he had relating to the Project costs was the Feasibility Document.

60 During cross-examination, it was put to Mr Price and he accepted that if the $3 million figure (referred to by Mr Hanna) was right, that would have a big impact on the profitability of the venture. It was put to Mr Price that if there had been a statement that the building cost was about $3 million, he would have raised this at the meeting at which the Feasibility Document was considered (that document containing a $2.1 million estimate). Mr Price accepted that he did not raise it at the meeting.

61 Mr Price stated in his third affidavit that during the August 2006 meeting, after it had been resolved to proceed with the purchase of the property, Mr Reynolds said to him, “You can build this one for us Col” and no-one at the meeting said anything to the contrary or expressed any disagreement or concern with Mr Price’s appointment as the builder.

62 Mr Stephen Power during cross-examination said that he agreed with Mr Price’s account of the meeting to the effect that, after the decision was made to proceed with the Project, Mr Reynolds suggested that Mr Price could be the builder and no-one disagreed.

63 Mr Reynolds’s evidence during cross-examination was that he did not recommend that Mr Price be engaged as the builder for the Project. Mr Reynolds said: “Mr Price told me that he believed there was money to be made in that job. After it was quoted by Build Rite at 2.2 million, he said there was money to be made.” Mr Reynolds said that he told Mr Price, “If the numbers are right, don’t see me, see the guys”, being a reference to the other syndicate members. Mr Reynolds denied that he said, “You can build this one for us, Col”. But he accepted that he did not have a clear recollection about how Mr Price was appointed the builder.

64 Mr Rice in his affidavit and during cross-examination said that a meeting of the syndicate members after the site visit, Mr Price said that he would like to build the Project.

65 Mr Robert Power may also have been present at the meeting in or about early August 2006. In his affidavit, he stated that at a meeting at which he was present Mr Price said words to the effect that he could be the builder for the development for the same price as Mr Weerappah had calculated, and asked if the others would agree to him being the builder. During cross-examination, Mr Robert Power said that he was surprised that Mr Price asked if he could carry out the work because he (Mr Robert Power) thought it was a fait accompli that Mr Price would build it.

66 In his first affidavit, Mr Price stated that he was not asked to quote or to undertake any costing of the Project; he had a set of town planning drawings, but had no working drawings or specifications that would enable him to cost the building works for the Project; he did not know what the structural, electrical or mechanical engineering specifications or the final materials would be, which he would have needed to price building costs to complete the Project.

67 In relation to the site visit and the meeting of syndicate members soon after, my conclusions are as follows. Given that the syndicate members and Build Rite representatives did not stay together during the site visit, but rather broke into various groups at different times, it is possible that Mr Price’s account of what Mr Hanna said, and Mr Reynolds’s and Mr Rice’s accounts of what Mr Walpole said, are both correct. In other words, it is possible that Mr Hanna said to Mr Price words to the effect that, “You won’t get much change out of three million, Col” and that Mr Walpole gave an estimate of $2.1 or $2.2 million, but that Mr Reynolds and Mr Rice were not present for the former and Mr Price was not present for the latter statement (and hence do not recall the statements being made). I think it is likely, and I find, that Mr Walpole did provide an estimate in the order of $2.1 or $2.2 million as the Feasibility Document discussed at the meeting is consistent with such an estimate. (Although Mr Walpole was not called by the first to seventh respondents, I do not regard him as being in their ‘camp’ and therefore do not consider that any Jones v Dunkel (1959) 101 CLR 298 inference arises from the failure to call him.) I am also prepared to accept that Mr Hanna made a statement to the effect described by Mr Price. Mr Price was clear in his recollection that such a statement was made. Given that the group did not stay together at all times, the other witnesses are not in a position to contradict that such a statement was made. Although it seems surprising that Mr Price did not raise this with the other members of the syndicate, there are a number of possible explanations for why he did not raise it. One is that, based on his experience, he considered that he could build it for less. Another is that he was unfamiliar with the feasibility process, being a new participant in such a project. In relation to the meeting of syndicate members, I accept Mr Price’s account, which is supported by Mr Stephen Power’s evidence, that after the decision was made to proceed with the Project, Mr Reynolds suggested that Mr Price be the builder for the Project and no-one disagreed. Mr Price had a clear recollection of this occurring. Mr Stephen Power’s recollection is more likely to be accurate than that of Mr Reynolds, given Mr Stephen Power’s closer involvement in the Project. I do not accept Mr Reynolds’s account of the conversation in the car on the way back from the site visit, given that it was not mentioned in his affidavits. I accept Mr Price’s evidence that he was not asked to provide, and did not provide, a quote or tender for the construction work before this meeting. I also find that Build Rite did not provide a written estimate, notwithstanding Mr Weerappah’s evidence to this effect. No such document has been produced, and Mr Stephen Power’s evidence, noted in paragraph [59] above, suggests the contrary.

68 On 15 August 2006, the syndicate made an offer to purchase the property for $3 million.

69 On 8 September 2006, a contract of sale was entered into for the purchase of the property for $3,150,000. The completion date was 8 December 2006.

70 Mr Price gave evidence in his third affidavit (and I accept) that once the syndicate agreed to undertake the Project and that CRP would build it, matters progressed relatively quickly; that no building works could commence until after settlement or before a building permit was obtained, but Mr Price engaged consultants, designers and engineers to prepare drawings and to undertake works in relation to the Project; and that the tasks he undertook included the following:

(a) Mr Price attended the property many times in the period September to November 2006 to meet consultants, obtained a preliminary existing condition survey, liaised with land subdivision consultants and building surveyors, commissioned the various consultants required, co-ordinated the design development with the architects.

(b) Mr Price obtained a soil test report.

(c) He commissioned the preparation of detailed working drawings including full elevations, roof plans and hydraulic drawings. On 2 October 2006, Stephen Quon of Archestral Designs Pty Ltd (Archestral Designs) provided a quotation (marked to the attention of Mr Price) to prepare working drawings for the Project. The quotation was accepted by Mr Price counter-signing the letter on 11 October 2006.

(d) Mr Price commissioned the preparation of detailed structural drawings, to be prepared by Macleod Consulting.

(e) Mr Price commissioned the preparation of mechanical and electrical drawings, to be prepared by Newton Engineering Services Pty Ltd. The quotation is dated 15 November 2006. This was accepted by Mr Price on behalf of Twentieth Green on 20 November 2006.

(f) Mr Price commissioned the preparation of detailed demolition plans, which were prepared and ready in November 2006.

71 On or about 18 September 2006, Mr Price measured each of the 15 apartments at the property and provided this information by fax to Mr Weerappah. Mr Weerappah had requested Mr Stephen Power to ask Mr Price to measure the internal areas.

72 On 19 September 2006, BankWest provided a financing proposal in relation to the Box Hill project. This was not an offer of finance but merely provided indicative terms. The document proposed a facility of $800,000 for construction of stage one and a facility of $1,400,000 for construction of stage two. The indicative terms included proposed conditions precedent, one of which was: “Agreement between you and a builder acceptable to us for the building works. This agreement must: (a) be a fixed price and time contract or on such other terms acceptable to us; …”. Another proposed condition precedent related to a quantity surveyor’s report and stated: “A quantity surveyor’s report satisfactory to us confirming the development costs, that the building contract is acceptable and other matters that we typically require a quantity surveyor to report on.”

73 In late September and early October 2006, emails were exchanged between Mr Stephen Power and BankWest in relation to finance for the Project. The person he was dealing with at BankWest was Andrew Samios. On 29 September 2006, Mr Stephen Power sent an email to Mr Samios which stated that the guarantors for the Project would be the five individuals associated with the five corporate entities, and identified the individuals by name. In the email, Mr Stephen Power stated that he would ask Mr Price to provide construction timelines which would determine cashflow drawings, but that it was their intention to have the required presales at a very early date which would facilitate the drawing down of funds required to refurbish and build the “super structure”. The email also stated that the building contract and the contract of sale would be forwarded to him early the following week.

74 On 3 October 2006, Mr Samios sent an email in response. This stated: “Received Colin’s [ie, Mr Price’s] information yesterday and also received a call from Clestus Weerappah re 20th Green.” The email stated that Mr Samios was yet to receive the development cashflow, résumé of the builder, building contract and contract of sale.

75 A two-page document headed, “Required Information” with handwritten annotations was in evidence. This was a standard document prepared by BankWest setting out the information it requested in order to consider the application for finance. The document stated: “Please ensure that all information that you provide to us is correct and is not misleading”. The document set out eleven items of information required and some of these were annotated by hand, “Col” or “Steve”, referring to Mr Price and Mr Stephen Power respectively. Mr Price accepted during cross-examination that the responsibility for provision of the material to BankWest was divided up between him and Mr Stephen Power. Item 9 (Documents) was annotated “Steve/Col” (indicating that they were jointly responsible) and requested provision of a copy of the following documents: land purchase or sale agreements (including pre-sales agreements); building or construction agreement; joint venture agreement; and partnership agreement. Item 10 dealt with licences and approvals and item 11 dealt with building approvals. Both of these were annotated “Col” and Mr Price had responsibility for provision of these documents to BankWest.

76 In early October 2006, Mr Price set about preparing the documents requested by BankWest in respect of which responsibility had been allocated to him.

77 On or about 5 October 2006, BMT & Associates (BMT), quantity surveyors, at the request of Mr Price, produced a document titled, “Preliminary Cost Plan” (Annexure CRP-39). This contained a cover letter addressed to Mr Price which stated:

Please find attached our Preliminary Cost Plan for the above-mentioned development.

Please refer to the attached indicative elemental trade breakup for an indication of the respective costs of the projects elements. Please note the following indicative elemental trade breakup has been derived from the total project costs, and only illustrates a very broad indication of the percentage of the total cost that can be allocated to the projects trade elements.

These figures have been derived from previous project of similar nature and do not necessarily reflect this project directly and as such can only be treated as a very broad indication.

We draw your attention to the lists of “Exclusions” and “Finishes” appended.

78 In the section headed, “Financial Summary” BMT estimated that the construction costs would be $2,442,210 (GST exclusive) or $2,686,431 (GST inclusive). A contingency of $122,111 (GST exclusive) or $134,322 (GST inclusive) was added, producing a total development cost of $2,564,321 (GST exclusive) or $2,820,753 (GST inclusive).

79 Underneath these figures, in a section headed “Descriptive Summary”, the document stated that the “development involves the construction of a Residential Development consisting of 23 units located at 33 Albion Road, BOX HILL”.

80 The Preliminary Cost Plan contained a schedule listing the information used in the preparation of the estimate. The information was: architectural drawings for the project (the numbers of the documents indicate that these were the town planning drawings); and written and verbal information provided by Mr Price. The Preliminary Cost Plan also included a one-page “Schedule of Finishes” which comprised a brief, high-level list of assumed finishes. The Preliminary Cost Plan included a page headed, “Indicative Trade Summary” which contained a one-page breakdown of costs which were used to derive the total cost estimate. Percentages for each item were included. The percentage for “Preliminaries & Margin” was 18.1%. Mr Reynolds accepted during cross-examination that this percentage was typical for these items. A note under these figures stated: “Please note the above trade costs have been derived from [a] previous project of similar nature and do not necessarily reflect this project directly and as such can only be treated as a very broad indication”.

81 Mr Stephen Power said during cross-examination that he could not recall the reason why the Preliminary Cost Estimate was sought. He rejected the proposition that it was obtained in order to check the figures used by Mr Weerappah in the Feasibility Document. He said that if the price for the building work had been $2.8 million, the syndicate would not have proceeded with the Project. He accepted that he saw the Preliminary Cost Estimate before the Project commenced.

82 In relation to the Preliminary Cost Estimate, CRP submits that this indicated that the price in the Simple Works Contract was not realistic. The first to seventh respondents submit that the document proceeded on the mistaken basis that the Project involved the construction of 23 apartments, rather than the refurbishment of 15 apartments and the construction of eight apartments. They rely on the statement quoted in paragraph [79] above and an item in the table under the heading “Financial Summary”, which stated that the construction cost per unit was $106,183. I do not think these matters demonstrate that this costing proceeded on a mistaken basis.

The Simple Works Contract (November 2006)

83 In November 2006, the Simple Works Contract was signed by Mr Stephen Power on behalf of Twentieth Green and Mr Price on behalf of CRP. The document utilised a standard form of contract prepared by the Master Builders Association Incorporated and the Royal Australian Institute of Architects. Mr Price purchased the document and inserted the required details by hand. The document is not dated but the evidence on both sides was that it was prepared and signed in November 2006. There were different contentions as to when during November 2006 it was most likely signed, but I do not think the evidence enables a conclusion to be drawn as to when during the month it was signed.

84 The document commenced with a section headed, “Introduction” which identified in item 1 (execution of the contract) the owner as Twentieth Green, the lending institution as BankWest, and the contractor as CRP. Although item 1 of the Introduction was the place provided for execution by the owner and the contractor, neither Twentieth Green nor CRP executed the contract in the places provided for execution in this part of the document. However, no point was taken in relation to this, given that the document was signed elsewhere.

85 Item 2 in the “Introduction” section dealt with the architect and was completed with details for Archestral Designs. However, as discussed below, Archestral Designs was not actually engaged; nor was any other architect engaged.

86 Item 3 of the “Introduction” was headed “Special conditions for houses and dwellings, the owner remaining in occupation, and other special conditions”. This item contained three questions, with “Yes” or “No” alongside each question, and the instruction to strike out the alternative which was not applicable. The first question had “No” struck through, but the other two questions did not have “Yes” or “No” struck through. Immediately after the third question, there was provision for signatures of the owner and the contractor. It is here that the document was signed, by Mr Stephen Power on behalf of the owner and by Mr Price on behalf of CRP.

87 Item 4 in the “Introduction” dealt with the contract price. The following figures were written in by Mr Price in the places provided:

(a) for the cost of the building work: $1,939,350;

(b) for GST: $193,935;

(c) for the contract price: $2,133,285.

88 This item was signed by Mr Stephen Power on behalf of the owner in the space provided. Immediately after those figures, the document set out a “warning” that the contract price could be subject to adjustment and then listed a number of relevant provisions of the contract.

89 Item 5 in the “Introduction” dealt with the works. The form stated that “this contract is for the *works set out in the *contract documents, as briefly described below”. (Words or expressions appearing in italics and preceded by an asterisk were defined in the definitions section, which was Section S.) The following description was written in by Mr Price:

REFURBISHMENT OF 15 no EXISTING APARTMENTS TOGETHER WITH THE CONSTRUCTION OF 8 no NEW APARTMENTS

90 The expressions “works” and “contract documents” were defined in Section S as follows. “Works” was defined as “the completed construction set out in the *contract documents (briefly described in item 5 of the Introduction)” and “contract documents” was defined as “any special conditions shown in schedule 2, the conditions in this contract, the specifications, the drawings and any other documents shown in schedule 3”.

91 Section A of the Simple Works Contract was headed, “Overview” and dealt with matters such as the obligations of the contractor and the obligations of the owner. Clause A6 was headed, “Architect to administer the contract” and provided as follows:

1. The architect for the purposes of this contract is shown in item 2 of the Introduction.

2. The architect is appointed to administer this contract on behalf of the owner. The architect is the owner’s agent for giving instructions to the contractor. However, in acting as assessor, valuer or certifier, the architect acts independently, not as the agent of the owner.

3. The owner must ensure that the architect, in acting as assessor, valuer or certifier, complies with this contract and acts fairly and impartially, having regard to the interests of both the owner and the contractor. The owner must not compromise the architect’s independence in acting as assessor, valuer or certifier.

4. The owner warrants that the architect has authority to administer this contract.

5. If the architect resigns, or becomes incapable of acting as architect, or if the owner terminates the engagement of the architect, the owner must immediately nominate another architect and give written notice of the name and address of the architect to the contractor.

6. If the contractor has no reasonable objection to the nominated architect, that person will be appointed as the architect for the purposes of this contract.

7. The newly appointed architect is bound by the written decisions of any previous architect.

92 Clause A10 provided that, where the contractor or the owner is entitled to compensation as determined under the contract, that compensation, when paid in full, was a sole and complete remedy for the contractor or the owner in those circumstances.

93 Section B was headed, “Documents”. Clause B1 provided that if either the contract or the owner discovered any discrepancy or omission in, or between, any of the contract documents, that party must promptly give written notice to the architect; and the architect must promptly resolve the discrepancy or omission by giving a written instruction to the contractor and a copy to the owner. Clause B2 dealt with the order of precedence of documents.

94 Section C dealt with security. Section D dealt with liability. Section E dealt with insurance. At the end of this section, there was a handwritten annotation (in Mr Price’s handwriting) to refer to the special conditions in schedule 2. Section F dealt with the site. Section G was headed, “Building the works”. Clause G2 within this section set out the contractor’s obligations.