FEDERAL COURT OF AUSTRALIA

Tax Practitioners Board v Lamede Group Proprietary Limited (No 2) [2016] FCA 656

File number: | QUD 125 of 2014 |

Judge: | DOWSETT J |

Date of judgment: | |

Legislation: | |

Date of last submissions: | 7 April 2016 |

Registry: | Queensland |

Division: | General Division |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Category: | No Catchwords |

Number of paragraphs: | |

Solicitor for the Applicant: | Australian Government Solicitor |

Counsel for the First Respondent: | The First Respondent did not appear |

Counsel for the Second Respondent: | The Second Respondent appeared in person |

Table of Corrections | |

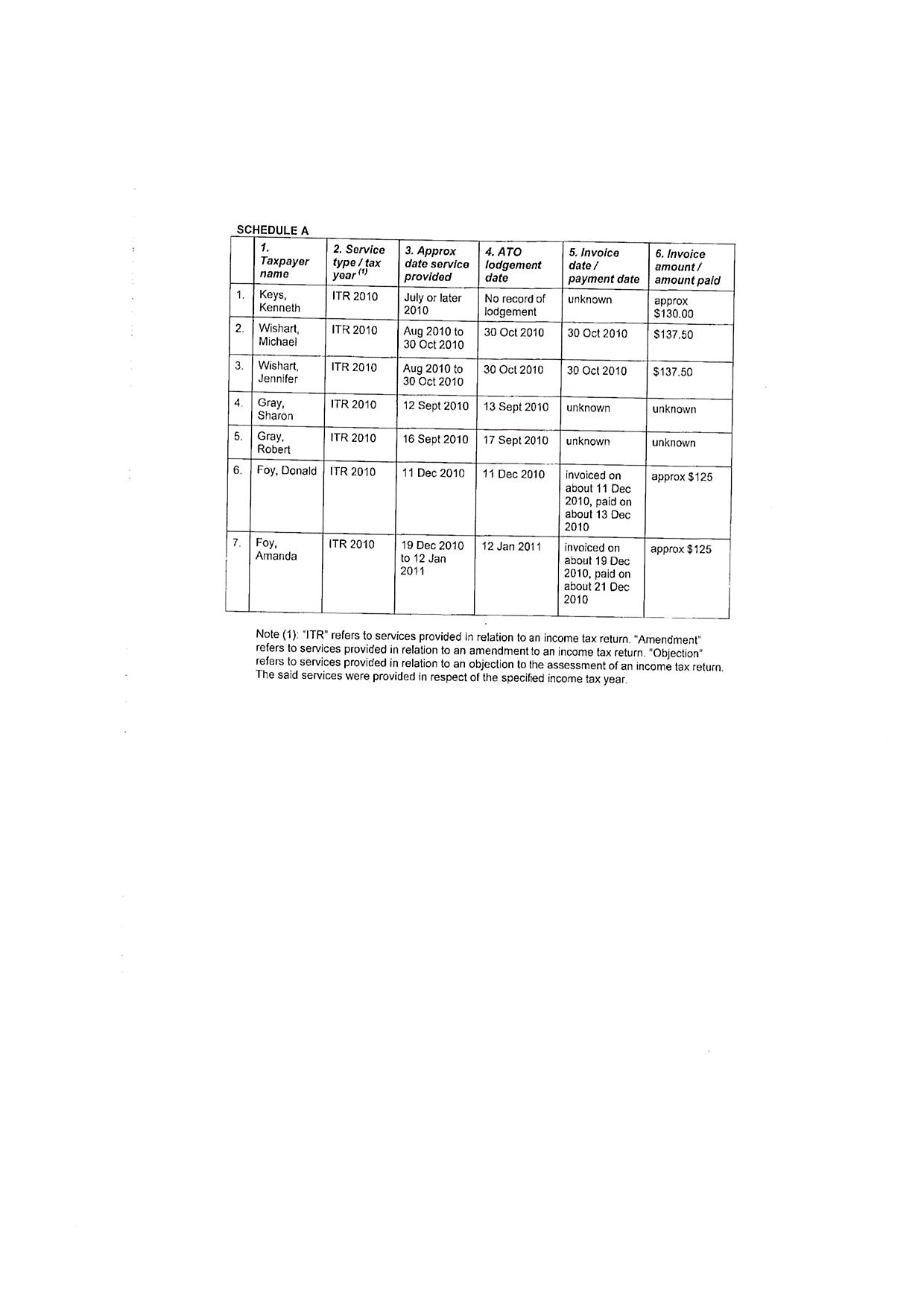

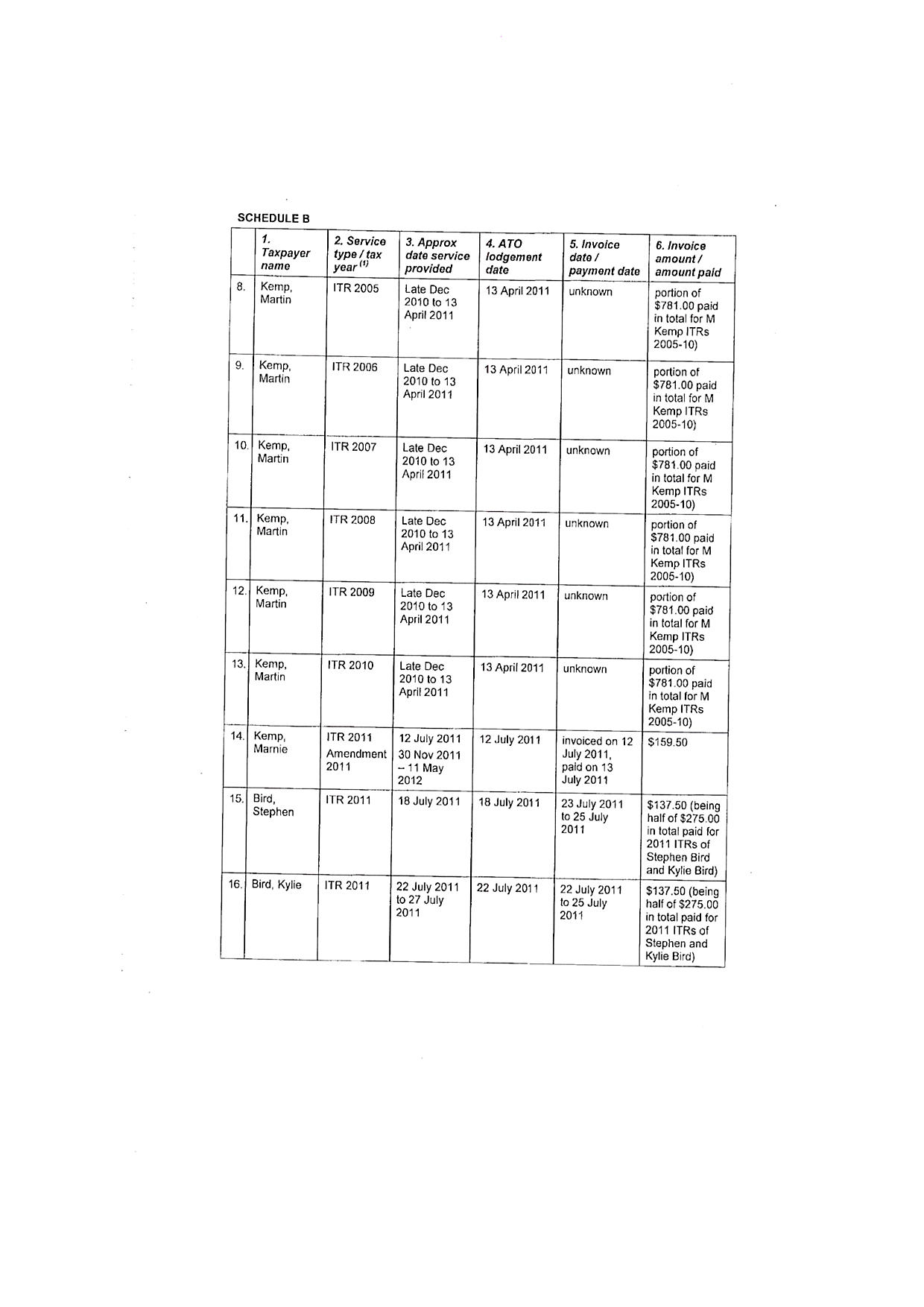

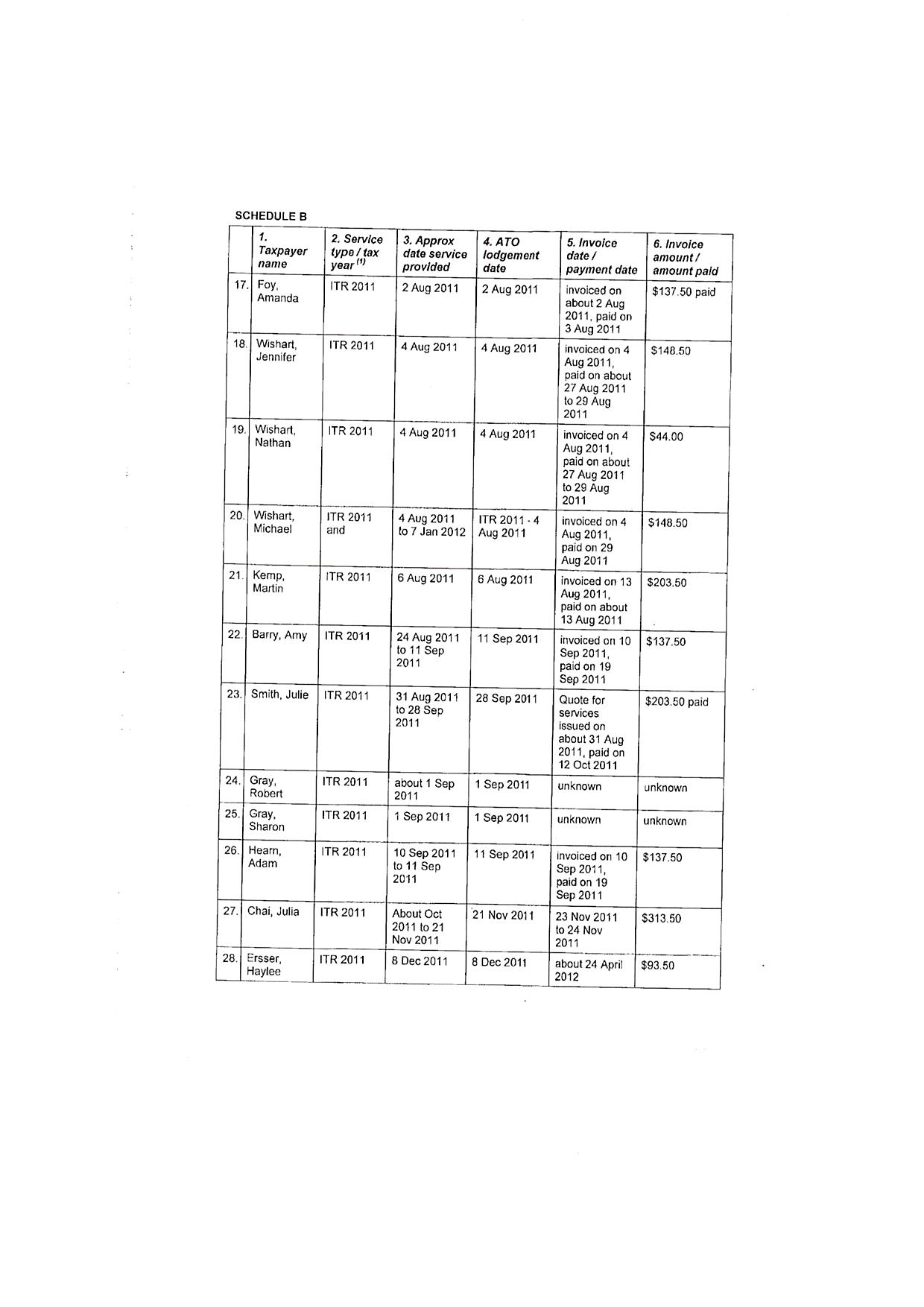

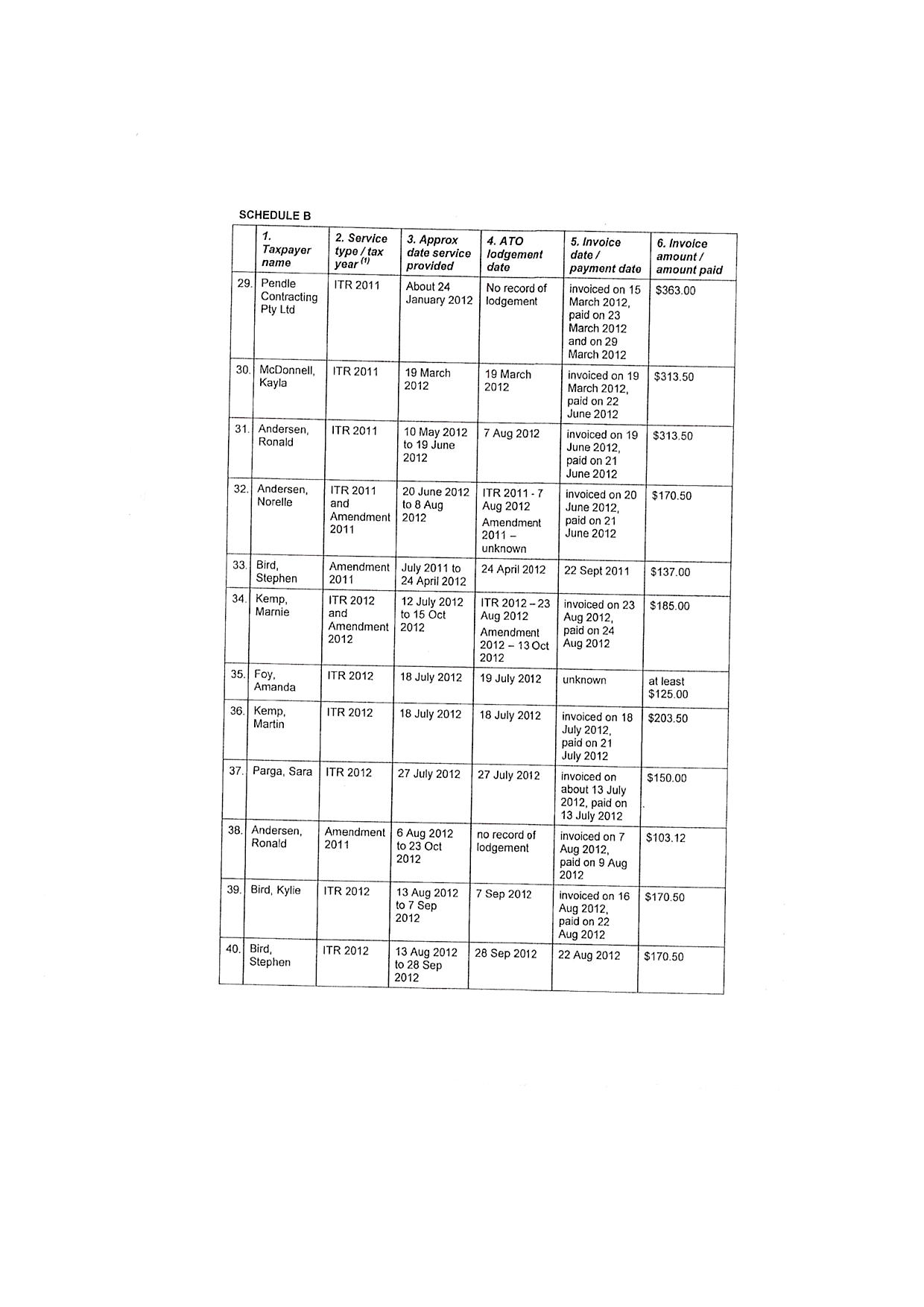

Schedules A and B have been added to the Orders |

ORDERS

Applicant | ||

AND: | LAMEDE GROUP PROPRIETARY LIMITED ACN 148 020 017 First Respondent LORRAINE GALE AMEDE Second Respondent | |

DATE OF ORDER: |

THE COURT DECLARES THAT:

1. the first respondent, between about January 2011 and about August 2013, by knowingly providing to each person, in relation to each income tax return (ITR), amendment of an ITR (amendment) and objection to an assessment of an ITR (objection) by the Commissioner of Taxation (Commissioner) itemised in Schedule B hereto in respect of that person, a service:

1.1 which involved the first respondent:

1.1.1 requesting from the person or his or her authorised representative information which was relevant or potentially relevant to the preparation of the person’s ITR, amendment and/or objection;

1.1.2 giving advice to the person or his or her authorised representative concerning his or her liabilities, obligations or entitlements which arise, or could arise, under a taxation law; and/or

1.1.3 completing for the person and lodging any forms or correspondence relevant to the matters in sub-paragraph 1.1.1. with the Commissioner; and

1.2 for which service the first respondent charged a fee;

1.3 which services the person could reasonably be expected to rely on to satisfy liabilities or obligations, or claim entitlements, which arise, or could arise, under a taxation law;

1.4 when the first respondent:

1.4.1 was not a registered tax agent pursuant to the Tax Agent Services Act 2009 (Cth) (TASA);

1.4.2 was not providing the service in relation to a business activity statement; and

1.4.3 was not providing the service as part of a legal service;

has, in respect of each said itemised service, provided a tax agent service in contravention of sub-section 50-5(1) of the TASA;

2. the second respondent, between about July 2010 and about December 2010, by knowingly providing to each person, in relation to each ITR, amendment and objection to an assessment by the Commissioner itemised in Schedule A hereto in respect of that person, a service:

2.1 which involved the second respondent:

2.1.1 requesting from the person or his or her authorised representative information which was relevant or potentially relevant to the preparation of the person's ITR, amendment and/or objection;

2.1.2 giving advice to the person or his or her authorised representative about his or her liabilities, obligations or entitlements which arise, or could arise, under a taxation law; and/or

2.1.3 completing for the person and lodging any forms or correspondence relevant to the matters in sub-paragraph 2.1.1 with the Commissioner; and

2.2 for which the second respondent charged a fee;

2.3 which the person could reasonably be expected to rely on to satisfy liabilities or obligations, or claim entitlements, which arise, or could arise, under a taxation law;

2.4 when the second respondent:

2.4.1 was not a registered tax agent pursuant to the TASA:

2.4.2 was not providing the service in relation to a business activity statement; and

2.4.3 was not providing the service as part of a legal service;

has, in respect of each said itemised service, provided a tax agent service in contravention of sub-section 50-5(1) of the TASA; and

3. the first respondent, by offering to provide services:

3.1 on the internet:

3.1.1 from about 4 January 2011 until about 13 September 2013, via the internet-based business directory "Service Seeking";

3.1.2 from about 1 July 2011, for about one month, via the internet-based community noticeboard "Nnub";

3.1.3 from about 10 August 2012, for about one month, via the internet-based community noticeboard "Nnub";

3.1.4 from about 26 September 2012 until about 6 September 2013, on the website "http://www.lamede.com.au";

3.1.5 from about 30 October 2012 until about 17 October 2013, via the internet-based business directory "Oneflare";

3.2 which related or could reasonably be understood to relate to a tax agent service within the meaning of the TASA;

3.3 which were not:

3.3.1 services relating to a business activity statement;

3.3.2 offered to be provided as part of a legal service;

3.3.3 offered free of charge or on a voluntary basis; and

3.4 which services were offered while the First Respondent was not registered as a tax agent pursuant to the TASA;

in each of the 5 instances referred to in 3.1 above, advertised that it would provide a tax agent service while not a registered tax agent, in contravention of subsection 50-10(1) of the TASA.

THE COURT ORDERS THAT:

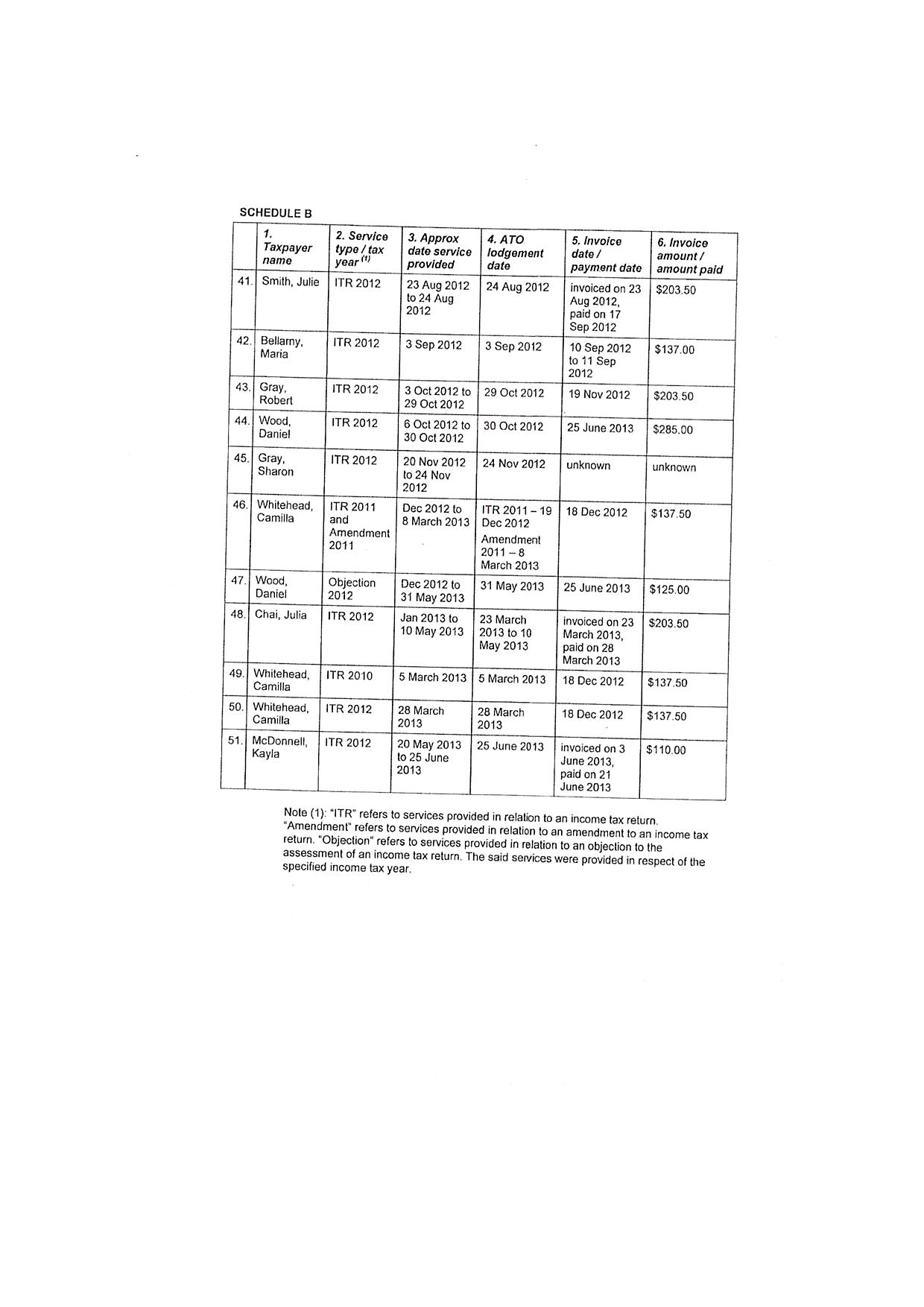

4. the first respondent pay to the Commissioner of Taxation on behalf of the Commonwealth of Australia pecuniary penalties in respect of the contraventions of subsection 50-5(1) of the TASA comprising the conduct referred to in paragraph 1 and with reference to the services itemised in the Schedule B hereto, in the amounts of:

4.1 for item 8, $1,500;

4.2 for items 9-13, $250 each;

4.3 for items 14- 28, $1,500 each;

4.4 for items 29- 32, $1,750 each;

4.5 for items 33-46, $2,000 each; and

4.6 for items 4751, $2,250 each;

5. the second respondent pay to the Commissioner of Taxation on behalf of the Commonwealth of Australia pecuniary penalties in respect of the contraventions of subsection 50-5(1) of the TASA comprising the conduct referred to in paragraph 2 and with reference to the services itemised in the Schedule A hereto, in the amounts of:

5.1 for item 1, $1,000; and

5.2 for items 2-7, $500 each;

6. the first respondent pay to the Commissioner of Taxation on behalf of the Commonwealth of Australia pecuniary penalties in respect of 5 contraventions of subsection 50-10(1) of the TASA comprising the conduct referred to in paragraph 3 above, in the amounts of:

6.1 $2,000, for the conduct referred to in sub-paragraph 3.1.1 above;

6.2 $500, for the conduct referred to in sub-paragraph 3.1.2 above;

6.3 $500, for the conduct referred to in sub-paragraph 3.1.3 above;

6.4 $1,500, for the conduct referred to in sub-paragraph 3.1.4 above; and

6.5 $1,500, for the conduct referred to in sub-paragraph 3.1.5 above;

7. the first respondent pay the pecuniary penalties totalling $77,500 referred to in paragraphs 4 and 6 above, to the Commissioner of Taxation on behalf of the Commonwealth of Australia, such payment to be made by instalments as follows:

7.1 $12,916 on or before 31 December 2016;

7.2 $12,916 on or before 31 December 2017;

7.3 $12,916 on or before 31 December 2018;

7.4 $12,916 on or before 31 December 2019;

7.5 $12,916 on or before 31 December 2020;

7.6 $12,920 on or before 31 December 2021;

8. the second respondent pay the pecuniary penalties totalling $4,000 referred to in paragraph 5 above, to the Commissioner of Taxation on behalf of the Commonwealth of Australia, such payment to be made by instalments as follows:

8.1 $665 on or before 31 December 2016;

8.2 $665 on or before 31 December 2017;

8.3 $665 on or before 31 December 2018;

8.4 $665 on or before 31 December 2019;

8.5 $665 on or before 31 December 2020;

8.6 $675 on or before 31 December 2021;

9. the first and second respondents have liberty to apply for the extension of any of the times provided for payment of the pecuniary penalties by paragraphs 7 and 8 herein; and

10. the parties have liberty to apply generally.

ENDORSEMENT UNDER RULE 41.06

TO: LAMEDE GROUP PROPRIETARY LIMITED

LORRAINE GALE AMEDE

You will be liable to imprisonment, sequestration of property or punishment for contempt if:

(a) where this order requires you to do an act of thing, you neglect or refuse to do the act or thing within the time specified in the order; or

(b) where this order requires you to abstain from doing an act or thing, you disobey the order.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

DOWSETT J:

1 On 10 February 2016, I handed down judgment in this matter, imposing pecuniary penalties for contraventions outlined in those reasons. At [78] of those reasons, the parties were asked to provide appropriate draft orders, including any timetable for payment of the penalties imposed.

2 On 12 February 2016, the legal representative of the applicant provided proposed orders. The second respondent, on behalf of herself and the first respondent, did not object to the proposed orders.

3 Subsequently, on 9 March 2016, the applicant requested that the proposed orders be amended to include an endorsement pursuant to r 41.06 of the Federal Court Rules 2011 (Cth). On 10 March 2016, in response to the applicant’s request, Ms Amede raised the following objection to the proposed orders:

I do not agree to point 3 3.1.1 regarding Service Seeking online. At no time did we ever advertise as tax agents or promote ourselves as tax agents. We solely sought book keeping business from this site.

I request that this be removed and any penalties associated with this item from the orders, as it is incorrect.

4 In light of the respondent’s objection, I sought to have the matter listed for hearing to enable Ms Amede to make submissions concerning the proposed orders. Ms Amede advised that she was unable to attend the hearing due to health problems and requested that the matter be dealt with on the papers. I proceeded on that basis. The parties were directed to exchange written submissions and provide them to the Court on or before 7 April 2016. The applicant provided submissions and proposed orders. The respondents did not do so.

5 The issues raised by Ms Amede in her email of 10 March 2016 were the subject of findings in the principal judgment. If Ms Amede wishes to challenge them, she should appeal. There is no basis upon which I could reconsider those issues at this stage.

6 The applicant’s proposed draft orders accurately reflect the reasons for judgment and provide a reasonable timetable for payment of the penalties.

7 I shall make orders in those terms.

I certify that the preceding seven (7) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Dowsett. |

Associate: