FEDERAL COURT OF AUSTRALIA

Smith, in the matter of Oceanic Asset Management Pty Ltd [2016] FCA 644

ORDERS

THE COURT ORDERS THAT:

Australian Global Capital Pty Ltd

1. For the period from 24 August 2015 up to and including 12 November 2015, the applicant is entitled to remuneration of $69,548.60 (plus GST) for work undertaken by him in his capacity as provisional liquidator of Australian Global Capital Pty Ltd ACN 130 826 470 (in liquidation) (AGC).

2. The applicant be indemnified from, and is entitled to an equitable lien over, the assets of AGC for the amount of the remuneration, costs and expenses incurred by the applicant in his capacity as provisional liquidator of AGC.

Mulato Nominees Pty Ltd

3. For the period from 24 August 2015 up to and including 12 November 2015, the applicant is entitled to remuneration of $85,997 (plus GST) for work undertaken by him in his capacity as provisional liquidator of Mulato Nominees Pty Ltd ACN 008 980 309 (in liquidation).

4. The applicant be indemnified from, and is entitled to an equitable lien over, the assets of Mulato for the amount of the remuneration, costs and expenses incurred by the applicant in his capacity as provisional liquidator of Mulato.

Costs

5. The applicant’s costs of the interlocutory process filed 4 May 2016 be paid from the assets of AGC and Mulato in equal proportions.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

BARKER J:

1 On 24 August 2015, the Court made orders appointing Mr Vincent Smith as provisional liquidator of the following companies:

(1) Oceanic Asset Management Pty Ltd ACN 110 278 110 (in liquidation);

(2) Oceanic Equities Pty Ltd ACN 122 561 522 (in liquidation);

(3) Australian Global Capital Pty Ltd ACN 130 826 470 (in liquidation) (AGC);

(4) Mulato Management Services Pty Ltd ACN 140 307 526 (in liquidation);

(5) Mulato Nominees Pty Ltd ACN 008 980 309 (in liquidation); and

(6) Ridgeway House Pty Ltd ACN 125 133 806 (in liquidation).

(together, the Companies).

2 On 12 November 2015, the Court made further orders that each of the Companies be wound up and that Mr Smith be appointed liquidator of each of the Companies.

3 By interlocutory process filed 4 May 2016, Mr Smith now applies for remuneration for work undertaken by him in his capacity as provisional liquidator of AGC and Mulato during the period of 24 August 2015 and 12 November 2015 (inclusive), in the amounts of $69,548.60 (plus GST) and $85,997.00 (plus GST) respectively. He further seeks to be indemnified from, and to be entitled to an equitable lien over, the assets of AGC and Mulato for the amount of remuneration, costs and expenses incurred in his capacity as provisional liquidator of those companies. In this regard, Mr Smith claims that he and his staff incurred disbursements of $2,758.18 and $2,760.69 in relation to AGC and Mulato respectively.

4 Mr Smith does not seek remuneration for work undertaken by him in his capacity as provisional liquidator of the other Companies as, based on his investigations, those companies do not presently hold any assets: [4] of the affidavit of Mr Smith sworn 24 March 2016 (first affidavit).

power to determine provisional liquidator’s remuneration

5 The Court has power to determine the remuneration of a provisional liquidator pursuant to s 473 of the Corporations Act 2001 (Cth). Section 473(2) relevantly provides:

A provisional liquidator is entitled to receive such remuneration by way of percentage or otherwise as is determined by the Court.

6 Rule 9.3 of the Federal Court (Corporations) Rules 2000 (Cth) provides that an application under subs (2) must be made by interlocutory process, as has occurred here. Prior to filing the interlocutory process, R 9.3 requires observation of the following procedure:

(3) At least 21 days before filing the interlocutory process seeking the order, the provisional liquidator must serve a notice in accordance with Form 16 of the provisional liquidator’s intention to apply for the order, and a copy of any affidavit on which the provisional liquidator intends to rely, on the following persons:

(a) any liquidator (except the provisional liquidator) of the company;

(b) each member of any committee of inspection or, if there is no committee of inspection, each of the 5 largest (measured by amount of debt) creditors of the company;

(c) each member of the company whose shareholding represents at least 10 per cent of the issued capital of the company.

(4) Within 21 days after the last service of the documents mentioned in subrule (3), the liquidator, or any creditor or contributory, may give to the provisional liquidator a notice of objection to the remuneration claimed, stating the grounds of objection.

(5) If the provisional liquidator does not receive a notice of objection within the period mentioned in subrule (4):

(a) the provisional liquidator may file an affidavit, made after the end of that period, in support of the interlocutory process seeking the order stating:

(i) the date, or dates, when the notice and affidavit required to be served under subrule (3) were served; and

(ii) that the provisional liquidator has not received any notice of objection to the remuneration claimed within the period mentioned in subrule (4); and

(b) the provisional liquidator may endorse the interlocutory process with a request that the application be dealt with in the absence of the public and without any attendance by, or on behalf of, the provisional liquidator; and

(c) the application may be so dealt with.

(6) If the provisional liquidator receives a notice of objection within the period mentioned in subrule (4), the provisional liquidator must serve a copy of the interlocutory process seeking the order:

(a) on each creditor or contributory who has given a notice of objection; and

(b) on the liquidator (if any).

7 Mr Smith did not receive, either personally or by his solicitors, any notice of objection to the remuneration claimed from any creditor or member of either AGC or Mulato: affidavit of Mr Smith sworn 2 May 2016 (second affidavit). Consequently, pursuant to subr (5), the Court now deals with the interlocutory process in the absence of the public and without Mr Smith’s attendance.

whether remuneration claimed is fair and reasonable

8 The onus is on Mr Smith to establish that the remuneration claimed is fair and reasonable. The Court must consider whether, prima facie, Mr Smith has made out a case for the determination of the amounts claimed. The absence of objections to the claim does not detract from the Court’s duty in this respect, but is relevant if a prima facie case is established. See ACN 104 635 369 Pty Ltd (in liq) (formerly Total Plant Services Pty Ltd) v Hamilton [2015] FCA 1219 at [21], citing Deputy Commissioner of Taxation v Starpicket Pty Ltd (No 2) [2013] FCA 699 at [22], and Venetian Nominees Pty Ltd and Others v Conlan (1998) 20 WAD 96 at 102-103; (1998) 16 ACLC 1653.

9 Mr Smith must provide the Court with sufficient information to enable an assessment to be made as to whether the total costs charged are reasonable. In Re Korda; in the matter of Stockford Ltd (2004) 149 FCR 424 at [48]; [2004] FCA 1682, by reference to Re Medforce Healthcare Services (in liq) [2001] 3 NZLR 145 at 155, Finkelstein J provided the following guidance in this regard:

As a minimum it seems to us that what is required is a statement of the work undertaken during the course of the liquidation, together with an expenditure account sufficiently itemised to enable the charges to be made related to the work done. The detail would have to be sufficient to enable the judicial officer to determine whether the personnel involved in the liquidation and their respective charge-out rates were appropriate to the nature of the work undertaken. This information may in some cases raise concerns as to whether there has been overservicing and overcharging. If there are suggestions of this in the information provided, the Court can request further information.

10 In total, Mr Smith claims $155,545.60 (plus GST) for his remuneration. The basis for that claim is set out in his first affidavit, which annexes the remuneration reports of both AGC and Mulato, said to be prepared in accordance with the procedures detailed by the Australian Restructuring Insolvency and Turnaround Association.

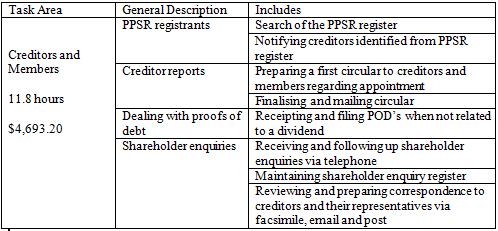

11 The remuneration reports identify, in table form, the total number of hours devoted to, and costs incurred in respect of, seven particular “task areas”. The particular tasks involved in each “task area” are also provided. For example, information concerning the task area “Creditors and Members” is presented as follows:

12 The remuneration reports include detailed narrations of the work undertaken by Mr Smith and his staff during the period of 24 August 2015 and 12 November 2015 (inclusive). Those narrations are in the standard form of an itemised bill, with each line item detailing the particular task undertaken, the date and by whom it was performed, their hourly rate, the time spent on the task and the total cost of the work.

13 The reports further identify, separately for Mr Smith and each member of his staff, the total hours of work performed by each individual in each task area, their charge out rate, and the amount of fees attributable to each individual in each task area.

14 From 24 August 2015 to 12 November 2015 (inclusive), Mr Smith and his staff recorded 167.9 hours in connection with the liquidation of AGC at an average hourly rate of $414.23 (excluding GST). The majority of the work was performed by a Mr Wilson, with the title “Executive 1”, who performed 73.2 hours at an hourly charge out rate of $375.00 (excluding GST). Mr Smith himself performed a total of 8.2 hours at an hourly rate of $650.00 (excluding GST).

15 For the same period, Mr Smith and his staff recorded 219.7 hours in connection with the liquidation of Mulato at an average hourly rate of $391.43 (excluding GST). The majority of the work was again performed by Mr Wilson, with the title “Executive 1”, who performed 122.7 hours at an hourly charge out rate of $375.00 (excluding GST). Mr Smith himself performed a total of 4.1 hours at an hourly rate of $650.00 (excluding GST).

16 The detailed narrations in the remuneration reports enable the Court to sufficiently identify the work to which the claimed remuneration relates. Further, the work performed by Mr Smith and his staff from 24 August 2015 to 12 November 2015 (inclusive) involved tasks ordinarily performed by a provisional liquidator, and appears to have been reasonably necessary. The Court has no reason to doubt that the work was in fact performed, or that Mr Smith and his staff acted reasonably in performing that work.

17 Mr Smith calculated his fees using a time-based method that is common in such matters. The hourly rates charged are the same as those set out in his notice of consent to act dated 14 August 2015. The Court has no reason to doubt the reasonableness of these rates.

18 In all the circumstances, the Court is satisfied that Mr Smith has established a prima facie case that the amount of remuneration claimed is fair and reasonable.

Power to approve disbursements

19 Mr Smith also seeks to assert an equitable lien over the assets of AGC and Mulato for the amount of “remuneration, costs and expenses” incurred by him in his capacity as provisional liquidator of the two companies. It is clear that the Court is only able to determine what “remuneration” a provisional liquidator is entitled to under s 473(2). The concept of remuneration does not include disbursements. See Venetian Nominees at 100, as applied in Korda at [50], Re Timeshare Resort Club Ltd (in liq) (2010) 187 FCR 13 at [36]-[37]; [2010] FCA 673, and Starpicket at [15].

20 In his capacity as a provisional liquidator, Mr Smith has a right to reimbursement from the company of all his expenses. Accordingly, in the absence of a challenge to the disbursements claimed under s 536 or s 1321 of the Act, Mr Smith appears not to need any specific order determining the amount of disbursements he incurred in his capacity as provisional liquidator of AGC and Mulato. See Venetian Nominees at 101, and Starpicket at [14]-[21].

21 To the extent they affirm Mr Smith’s right to reimbursement out of the assets of AGC and Mulato for his disbursements, but do not require the Court to fix an amount in this regard, the orders sought are fitting and no further observations concerning the disbursements incurred are necessary.

orders

Australian Global Capital Pty Ltd

(1) For the period from 24 August 2015 up to and including 12 November 2015, the applicant is entitled to remuneration of $69,548.60 (plus GST) for work undertaken by him in his capacity as provisional liquidator of AGC.

(2) The applicant be indemnified from, and is entitled to an equitable lien over, the assets of AGC for the amount of the remuneration, costs and expenses incurred by the applicant in his capacity as provisional liquidator of AGC.

Mulato Nominees Pty Ltd

(3) For the period from 24 August 2015 up to and including 12 November 2015, the applicant is entitled to remuneration of $85,997 (plus GST) for work undertaken by him in his capacity as provisional liquidator of Mulato.

(4) The applicant be indemnified from, and is entitled to an equitable lien over, the assets of Mulato for the amount of the remuneration, costs and expenses incurred by the applicant in his capacity as provisional liquidator of Mulato.

Costs

(5) The applicant’s costs of the interlocutory process filed 4 May 2016 be paid from the assets of AGC and Mulato in equal proportions.

I certify that the preceding twenty-one (21) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Barker. |