FEDERAL COURT OF AUSTRALIA

Woodings, in the matter of the Bell Group Limited [2016] FCA 369

ORDERS | |

IN THE MATTER OF THE BELL GROUP LIMITED (IN LIQUIDATION) ACN 008 666 993

DATE OF ORDER: |

THE COURT ORDERS THAT:

a. in the case of those Bell Group companies ordered to be wound up before 23 June 1993, namely:

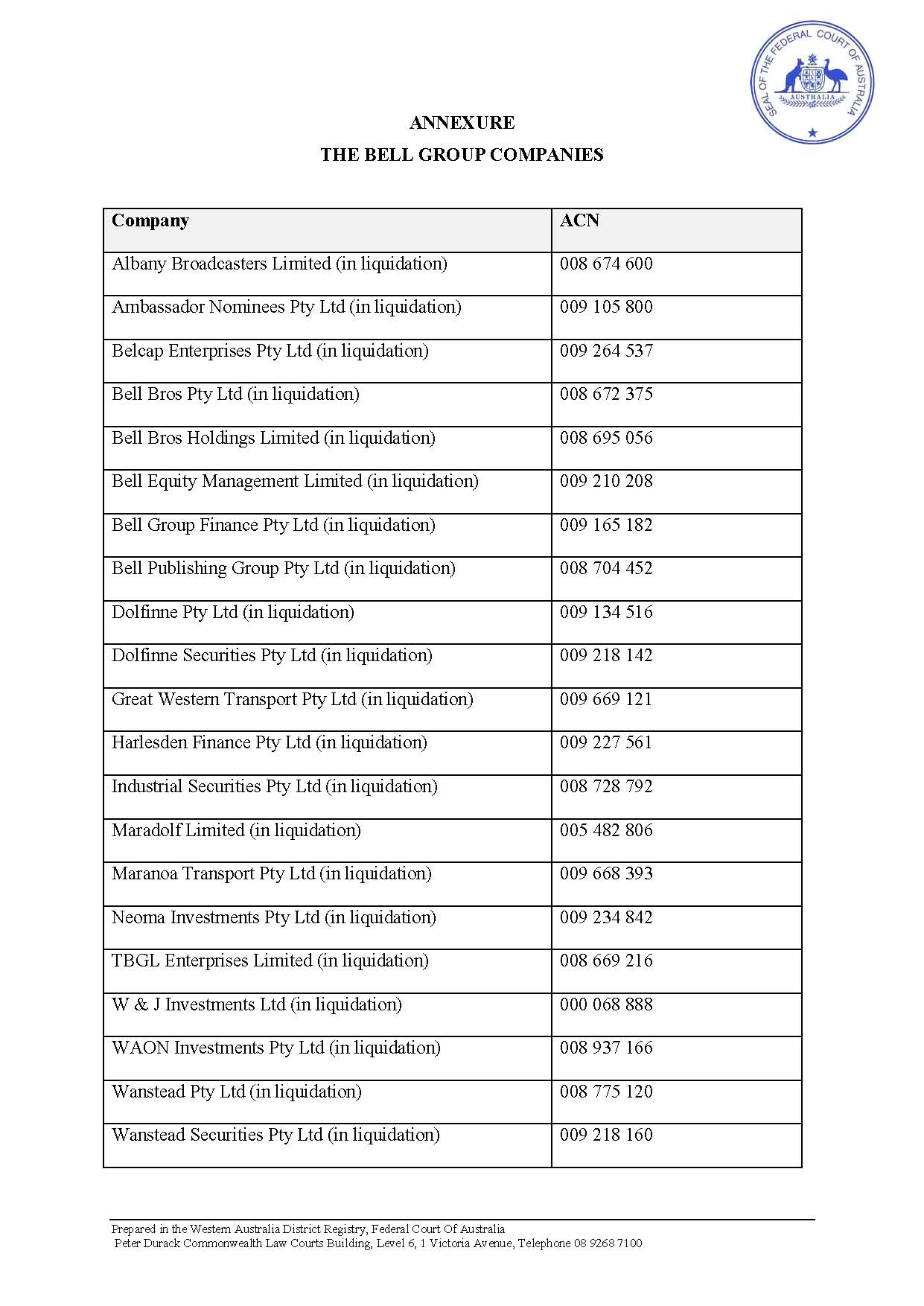

i. The Bell Group Limited (in liquidation) ACN 008 666 993;

ii. Albany Broadcasters Limited (in liquidation) ACN 008 674 600;

iii. Bell Bros Holdings Limited (in liquidation) ACN 008 695 056;

iv. Bell Group Finance Pty Ltd (in liquidation) ACN 009 165 182;

v. Bell Publishing Group Pty Ltd (in liquidation) ACN 008 704 452;

vi. W&J Investments Pty Ltd (in liquidation) ACN 000 068 888; and

vii. Wigmores Tractors Pty Ltd (in liquidation) ACN 008 679 221,

s 479(3) of the Corporations Law (as applied by s 1408(1) of the Corporations Act 2001 (Cth));

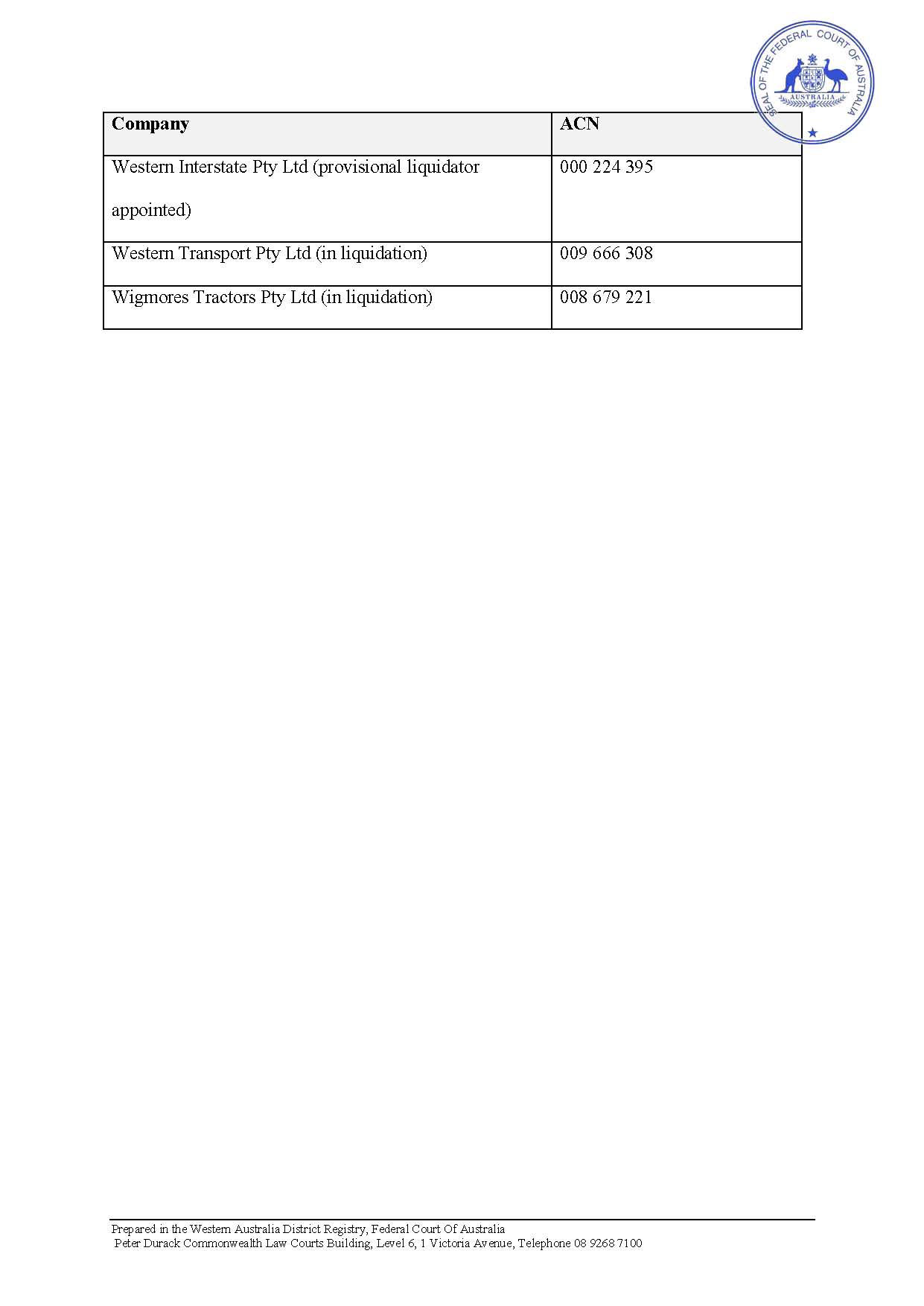

b. in the case of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395, the inherent or implied jurisdiction of the Court (and, if and to the extent required, s 479(3) of the Corporations Act 2001 (Cth)); and

c. in the case of the Bell Group companies other than those ordered to be wound up by the Court before 23 June 1993 and Western Interstate Pty Ltd (provisional liquidator appointed), s 479(3) of the Corporations Act 2001 (Cth),

it is directed that the plaintiff (as liquidator or provisional liquidator, as the case may be) will be acting properly and is justified in causing each of the companies as listed in the annexure to these orders (Bell Group companies) to enter into and perform a funding and indemnity agreement that is in or substantially in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

2. The plaintiff as liquidator of:

a. Ambassador Nominees Pty Ltd (in liquidation) ACN 009 105 800;

b. Belcap Enterprises Pty Ltd (in liquidation) ACN 009 264 537;

c. Bell Bros Pty Ltd (in liquidation) ACN 008 672 375;

d. Bell Equity Management Limited (in liquidation) ACN 009 210 208;

e. Dolfinne Pty Ltd (in liquidation) ACN 009 134 516;

f. Dolfinne Securities Pty Ltd (in liquidation) ACN 009 218 142;

g. Great Western Transport Pty Ltd (in liquidation) ACN 009 669 121;

h. Harlesden Finance Pty Ltd (in liquidation) ACN 009 227 561;

i. Industrial Securities Pty Ltd (in liquidation) ACN 008 728 792;

j. Maradolf Limited (in liquidation) ACN 005 482 806;

k. Maranoa Transport Pty Ltd (in liquidation) ACN 009 668 393;

l. Neoma Investments Pty Ltd (in liquidation) ACN 009 234 842;

m. TBGL Enterprises Limited (in liquidation) ACN 008 669 216;

n. WAON Investments Pty Ltd (in liquidation) ACN 008 937 166;

o. Wanstead Pty Ltd (in liquidation) ACN 008 775 120;

p. Wanstead Securities Pty Ltd (in liquidation) ACN 009 218 160; and

q. Western Transport Pty Ltd (in liquidation) ACN 009 666 308,

has approval under s 477(2B) of the Corporations Act 2001 (Cth) to enter into and cause those companies to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

3. The plaintiff as provisional liquidator of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395 has approval under s 477(2B) (as applied by s 472(5) of the Corporations Act 2001 (Cth)) to enter into and cause that company to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

4. The costs of the application are costs in the windings up of The Bell Group Limited (in liquidation) and Bell Group Finance Pty Ltd (in liquidation) in equal proportions.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MCKERRACHER J:

OVERVIEW

1 Orders were made late last year that the plaintiff as liquidator of The Bell Group Ltd (in liq) ACN 008 666 993 (TBGL) and as liquidator or provisional liquidator of certain subsidiaries will be acting properly and is justified in causing each of the relevant Bell Group companies to enter into and perform a funding and indemnity agreement (the proposed Agreement). The orders being somewhat unusual in nature, it is appropriate for my reasons to be recorded in relation to the facts as known at the time of the orders.

2 Two creditors most interested in the application, the Commonwealth and Bell Group NV (in liquidation) (BGNV), were joined. The latter made written submissions.

3 Under the proposed Agreement, one Bell Group company, Maranoa Transport Pty Ltd (in liquidation) ACN 009 668 393, will assume the funding of 50% of the costs of the winding up of the Bell Group companies generally. Previously, that 50% was met by the parent company of the Bell Group, Bell Group Limited.

4 The application was made when the Bell Group Companies (Finalisation of Matters and Distribution of Proceeds) Act 2015 (WA), which received royal assent on 26 November 2015, was a bill before the State Parliament of Western Australia (Bell legislation). The reasons that follow are based on the facts at the date of the final hearing and making of the orders.

5 Approval is required pursuant to s 477(2B) Corporations Act 2001 (Cth) as obligations under the funding and indemnity agreement will continue for more than three months. This provision is similarly applicable to the company in provisional liquidation by reason of s 472(5) of the Corporations Act.

6 There were two strands to the application:

(1) The first was a question of power: was there power for the liquidator to cause the Bell Group companies, and particularly Maranoa Transport, to enter into the proposed Agreement?

(2) The second was a question of propriety: was it proper for the liquidator to cause the Bell Group companies, and particularly Maranoa Transport, to enter into the proposed Agreement?

BACKGROUND

7 The plaintiff is the sole liquidator of the following companies:

TBGL;

Bell Group Finance Pty Ltd (in liquidation) ACN 009 165 182;

Albany Broadcasters Limited (in liquidation) ACN 008 674 600;

Ambassador Nominees Pty Ltd (in liquidation) ACN 009 105 800;

Belcap Enterprises Pty Ltd (in liquidation) ACN 009 264 537;

Bell Bros Pty Ltd (in liquidation) ACN 008 672 375;

Bell Bros Holdings Ltd (in liquidation) ACN 008 695 056;

Bell Equity Management Limited (in liquidation) ACN 009 210 208;

Bell Publishing Group Pty Ltd (in liquidation) ACN 008 704 452;

Dolfinne Pty Ltd (in liquidation) ACN 009 134 516;

Dolfinne Securities Pty Ltd (in liquidation) ACN 009 218 142;

Great Western Transport Pty Ltd (in liquidation) ACN 009 218 142;

Harlesden Finance Pty Ltd (in liquidation) ACN 009 227 561;

Industrial Securities Pty Ltd (in liquidation) ACN 008 728 792;

Maradolf Limited (in liquidation) ACN 005 482 806;

Maranoa Transport;

Neoma Investments Pty Ltd (in liquidation) ACN 009 234 842;

TBGL Enterprises Limited (in liquidation) ACN 008 669 216;

W & J Investments Limited (in liquidation) ACN 000 068 888;

WAON Investments Pty Limited (in liquidation) ACN 008 937 166;

Wanstead Pty Ltd (in liquidation) ACN 008 775 120;

Wanstead Securities Pty Ltd (in liquidation) ACN 009 218 160;

Western Transport Pty Ltd (in liquidation) ACN 009 666 308; and

Wigmores Tractors Pty Ltd (in liquidation) ACN 008 679 221.

8 The plaintiff is the provisional liquidator of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395 (Western Interstate).

9 Collectively, all the companies mentioned in [7] and [8] above are referred to as the Bell Group companies.

10 The plaintiff records by affidavit in support sworn on 1 October 2015:

• Geoffrey Frank Totterdell was the original sole liquidator of TBGL, having been appointed to that position on 24 July 1991 in matter COY 108 of 1991. Mr Totterdell was also the original sole liquidator of the following companies …:

(a) Ambassador Nominees;

(b) Belcap;

(c) Bell Bros;

(d) Bell Bros Holdings;

(e) Dolfinne;

(f) Maradolf;

(g) Maranoa;

(h) Neoma;

(i) TBGL Enterprises;

(j) WJI;

(k) WAON;

(l) Wanstead; and

(m) Wigmores Tractors.

• On 3 March 2000 I was appointed as additional liquidator to the TBGL Companies by orders of the Supreme Court of Western Australia. I held office jointly with Mr Totterdell from that time until 21 August 2014.

• On 21 August 2014 Mr Totterdell resigned as official liquidator of the TBGL Companies when he filed with the Principal Registrar of the Supreme Court and lodged with ASIC a memorandum of his resignation from the office of liquidator. ...

• By orders of the Supreme Court of Western Australia made on 21 August 2014 I was removed as additional liquidator upon Mr Totterdell's resignation taking effect and immediately re-appointed as sole official liquidator of the TBGL Companies. ...

11 Historically, the majority of the costs of the Bell Group companies' windings up have been divided equally between TBGL (the parent company) and BGF (the Bell Group treasury company). In the future, the plaintiff intends to seek directions as to the proper apportionment of those costs.

12 Any such application will await the outcome of the Bell legislation which was not at the time of the orders, but is now, the subject of legal proceedings in the High Court of Australia. At the time of the orders, the plaintiffs’ understanding of the Bell legislation upon proclamation was that:

(a) subject to certain tax-related exceptions, all property vested in or held on behalf of or on trust a WA Bell company (as defined in the Act) will be transferred to and vested in the WA Bell Companies Administrator Authority (Authority): sections 22(1)(a) and 22(1)(b);

(b) all property held by a person in the capacity of a liquidator of a WA Bell Company (as defined in the Act) on trust for any person other than a WA Bell Company will be transferred to and vested in Authority: section 22(1)(c);

(c) all liabilities of the WA Bell Companies immediately before the transfer of their property pursuant to s 22 may be proved against the Fund (as defined in the Act) in accordance with the regime provided for in the Act: section 25;

(d) certain agreements, including the agreements by which the Indemnifying Creditors agreed to fund Mr Totterdell and I to conduct the Bell Proceedings are taken to have always been void: section 26;

(e) from the beginning of the transfer day, all WA Bell Companies that were registered immediately before the transfer day are to be administered by the Authority - with the Authority having control of their property and affairs and being able to perform any function or exercise any power that the company or any officers could perform if the company were not under the control of the Authority - and with no person other than the Authority being able to exercise a function or power as an officer of the company save with the Authority's written approval or in the exercise of a power or duty under the Act: sections 26A, 26B and 26C;

(f) the Governor may, by proclamation, dissolve a WA Bell Company - which company ceases to exist upon its dissolution: section 27;

(g) the Authority must determine the property and liabilities of each of the WA Bell Companies and report to the Minister and make recommendations as to how the property ought to be distributed, after seeking submissions from affected creditors: sections 31 - 36;

(h) in making a recommendation to the Minister, the Authority must have regard to any agreement between any of the creditors as to the distribution of the proceeds of the Bell Proceedings entered into after 12:00 noon on the day before the day on which the Bill was introduced into the Legislative Assembly: section 36(3)(b);

(i) the final decision as to the distribution of the property will be made by the Governor (section 37) and administered by the Authority: section 38; and

(j) on the dissolution of a WA Bell Company, each person who is, or has at any time been, a liquidator of the company, and each person who has at any time acted for or on behalf of such a liquidator, is discharged from all liability out of anything done, or purportedly done, by them in performing their duties: section 39(1).

13 The plaintiff related that recent actions by the Commissioner of Taxation potentially exposed the plaintiff to substantial liability to the extent that the plaintiff caused TBGL to continue to fund the costs of the Bell Group companies' windings up in the way that has occurred in the past. Indeed, the Australian Taxation Office (ATO) has also suggested to the plaintiff that the plaintiff may be personally liable from the time income was derived or received by TBGL.

14 In particular:

On 10 August 2015 the Commissioner issued an assessment to TBGL. Shortly afterwards the assessment was amended and re-issued in an amount of some $298 million. An alternative assessment for the same amount was issued to the plaintiff in his capacity as liquidator of TBGL.

The Commissioner's position was that the assessment constitutes a post-liquidation liability that is a priority expense in TBGL's winding up under s 556(1)(a) of the Corporations Act.

The Commissioner contended the plaintiff is only entitled to pay other priority costs and expenses of the winding up pari passu with the assessment. To the extent that costs and expenses are paid out of TBGL's winding up other than on a pari passu basis with the Commissioner's $298 million, assessment the plaintiff will have a personal liability for the assessment under s 254(1)(e) of the Income Tax Assessment Act 1936 (Cth).

15 TBGL did not itself have sufficient funds to meet the $298 million assessment. But there was a tax sharing agreement between TBGL and other Bell Group companies that, in the usual course, would mean TBGL should have sufficient funds to meet the assessment. However, the Bell legislation may, depending on the circumstances, mean that TBGL was unable to secure contributions under the tax sharing agreement.

16 Costs and expenses in the winding up of the Bell Group companies were in the order of $650,000 per month. Such costs include significant costs in the general day-to-day conduct of the windings up of the Bell Group companies. As 50% of the costs were met by TBGL, each month the plaintiff has a potential exposure in the order of $325,000.

17 In the circumstances, the plaintiff considered alternate means of funding the ongoing conduct of the Bell Group companies' windings up.

PROPOSED AGREEMENT

18 The plaintiff proposed that Maranoa Transport, another Bell Group company, should provide the 50% funding of the costs and expenses of the Bell Group companies’ winding up that has until now been provided by TBGL.

19 At the time of the application, Maranoa Transport was in a position to fund 50% of the costs and expenses that have historically been paid by TBGL, as:

it held some $46 million;

it had not been issued with any assessment by the Commissioner; and

it was not registered in Western Australia and is not a ‘WA Bell Company’ as defined under s 3(1) of the Bell legislation. Accordingly, the $46 million Maranoa Transport holds will not be transferred by operation of s 22(1) of the Bell legislation if enacted in its form as at the time of the application.

20 Also, Maranoa Transport, which was being wound up as an insolvent company, had a small creditor base which is largely associated with TBGL. Relevantly, Maranoa Transport’s creditors comprise:

TBGL: as to 97.9% of the total creditor claims. (However, TBGL stands to receive the benefit of some 98.9% of the available assets in Maranoa Transport's winding up);

the Commissioner: as to 1.2% of creditor claims; and

Maradolf: as to 0.9% of creditor claims.

In respect of Maradolf, it is anticipated that there will be a surplus in the winding up process. That surplus will be payable to TBGL, which is the sole shareholder of Maradolf. Accordingly, indirectly, Maradolf's 0.9% creditor claim in Maranoa Transport will accrue for the benefit of TBGL.

21 Effectively, as Maradolf's creditor's claim will inevitably accrue to the benefit of TBGL, the only external creditor of Maranoa Transport is the Commissioner (for 1.2%). In summary, TBGL had the overwhelming economic interest in the funds in Maranoa Transport's winding up.

22 The plaintiff caused the proposed Agreement to be prepared. The key operative terms are:

the duration of the agreement is limited to 18 months unless extended by further Court directions and approvals;

effective from 10 August 2015 (the date the taxation assessment was issued to TBGL) Maranoa Transport agrees to pay the 50% share of the Bell Group companies' costs and expenses of winding up that have historically been paid by TBGL. Certain limitations apply. For example, the total so paid cannot exceed TBGL's proportionate entitlement to the net available assets in Maranoa Transport's winding up;

the amount paid by Maranoa Transport under the agreement is accounted for as a reduction against TBGL's entitlements to distributions by Maranoa Transport. This includes a notional interest component. The adjustment amount will be applied for the creditors of Maranoa Transport other than TBGL, i.e. Maradolf and the Commissioner. This adjustment process is designed to compensate the other creditors because by Maranoa Transport meeting obligations that would have otherwise been met by TBGL, TBGL obtains an immediate benefit that is unavailable to the other creditors of Maranoa Transport; and

existing rights between the Bell Group companies inter se are not affected by the agreement. This is to ensure that the agreement cannot affect any subsequent directions application as to the proper apportionment of costs and expenses as between the Bell Group companies' windings up.

POSITION OF THE VARIOUS CREDITORS

BGNV'S position

23 It is unnecessary to record the considerable affidavit detail as to the relationship and exchanges between the plaintiff, BGNV and its liquidator, Mr Trevor. Suffice it to say that all parties accept that BGNV may be heard on this application.

24 BGNV neither consents to, nor opposes, the plaintiff's application. Mr Trevor does, however, draw certain matters to the attention of the Court. In particular, Mr Trevor refers to the decision of the Full Federal Court in Fortress Credit Corporation (Australia) II Pty Ltd v Fletcher (2011) 281 ALR 38 on the question as to whether the plaintiff, as liquidator of Maranoa Transport, has power to cause that company to enter into the proposed funding agreement. The potential relevance and influence of Fortress Credit is dealt with in detail below.

The ATO's position

25 The only identified external creditor who might be adversely affected under the proposed Agreement is the Commissioner.

26 By way of letter dated 23 September 2015, the plaintiff sought the ATO's views about Maranoa Transport's funds being used to meet TBGL’s 50% share of the costs and expenses of the windings up of the Bell Group companies for so long as the current issues with the unavailability of TBGL's funds persist.

27 Significantly, the ATO supports the funding proposal described in the letter of 23 September 2015.

STATUTORY CONSIDERATIONS

28 As the plaintiff noted, two slightly different statutory regimes are relevant. This is because seven of the Bell Group companies were wound-up by orders made before 23 June 1993. The law in effect prior to 23 June 1993 relevant in the present case continues to apply for the purposes of a winding-up where the Court ordered the winding up of a company before 23 June 1993: Corporations Act, s 1408(1); Corporations Law, s 1383(2); Shaw v Goodsmith Industries Pty Ltd (2002) 41 ACSR 556 (at [6]-[8]). See further: Re Bell Group Ltd (in liq); Ex parte Woodings (2015) 293 FLR 215 (at [16]-[19]).

29 In summary:

(1) as to the application for directions, the application invokes s 479(3) of the Corporations Law of Western Australia as applied by s 1408(1) of Corporations Act (in relation to the pre-23 June 1993 windings up) and s 479(3) of the Corporations Act (in relation to the post-23 June 1993 windings up). There is no material difference in the two relevant statutory provisions. As to the company in provisional liquidation, Western Interstate, if s 479(3) does not apply, the Court has inherent jurisdiction to provide directions to an official liquidator appointed as provisional liquidator because an official liquidator is an officer of the Court: Re PR Clark Holdings Pty Ltd (1977) 2 ACLR 416 (at 416, 418-419); Re United Medical Protection Ltd (No 3) [2002] NSWSC 488 per Austin J (at [26]). Accordingly, I have the power to give directions to the plaintiff as provisional liquidators on his application, either under s 479(3) or in the exercise of the Court’s inherent jurisdiction; and

(2) as to the application for approval, the application invokes s 477(2B) of the Corporations Act (in relation to the post-23 June 1993 windings up). There is no equivalent statutory provision in the ‘old winding up law’ that applies to the pre-23 June 1993 windings up. Accordingly, no approval is required in relation to the seven Bell Group companies that were wound up by orders made pre-23 June 1993.

30 Relevantly, by s 479(3) of the Corporations Act, the liquidator may apply to the Court for directions in relation to any particular matter arising under the winding up. Further, by s 477(2B):

Except with the approval of the Court, of the committee of inspection or of a resolution of the creditors, a liquidator of a company must not enter into an agreement on the company’s behalf (for example, but without limitation, a lease or a an agreement under which a security interest arises or is created) if:

(a) without limiting paragraph (b), the term of the agreement may end; or

(b) obligations of a party to the agreement may, according to the terms of the agreement, be discharged by performance;

more than 3 months after the agreement is entered into, even if the term may end, or the obligations may be discharged, within those 3 months.

(emphasis added)

31 Section 477(2)(m) provides that, ‘[s]ubject to this section, a liquidator of a company may do all such other things as are necessary for winding up the affairs of the company and distributing its property.’

32 Finally, s 477(1) of the Corporations Act relevantly provides:

477 Powers of liquidator

(1) Subject to this section, a liquidator of a company may:

…

(c) make any compromise or arrangement with creditors or persons claiming to be creditors or having or alleging that they have any claim (present or future, certain or contingent, ascertained or sounding only in damages) against the company or whereby the company may be rendered liable; …

LEGAL PRINCIPLES

Directions under s 479(3)

33 The only binding effect of, or arising from, a direction given in pursuance of such an application (other than rendering the liquidator liable to appropriate sanctions if a direction in mandatory or prohibiting form is disobeyed) is the the liquidator, if he has made full and fair disclosure to the Court of the material facts, will be protected from liability for any alleged breach of duty as a liquidator to a creditor or contributory to the company in respect of anything done by him in accordance with the direction: Re GB Nathan & Co Pty Ltd (In Liq) (1991) 24 NSWLR 674 per McLelland J (at 679).

34 However, the power to give directions is not unfettered. As Goldberg J explained in Re Ansett Australia Ltd (No 3) (2002) 115 FCR 409 (at [65]):

There must be something more than the making of a business or commercial decision before a court will give directions in relation to, or approving of, the decision. It may be a legal issue of substance or procedure, it may be an issue of power, propriety or reasonableness, but some issue of this nature is required to be raised. It is insufficient to attract an order giving directions that the liquidator or administrator has a feeling of apprehension or unease about the business decision made and wants reassurance.

35 His Honour noted further (at [65]) that, in short, there must be ‘an issue calling for the exercise of legal judgment’.

36 In the present case, a direction is sought in terms that the plaintiff may ‘properly and justifiably’ take certain action.

37 The direction is sought in circumstances where there may be a perception that in making a decision to cause the relevant Bell Group companies to enter into the proposed agreement the plaintiff is in a position of potential or apparent conflict of interest or duty. The circumstance of conflict itself raises an issue of propriety making this an appropriate case for directions: see, for example, Australian Securities & Investments Commission in the Matter of Richstar Enterprises Pty Ltd ACN 099 071 968 v Carey (No 20) [2008] FCA 45 per French J, as his Honour then was (particularly at [20], [52]).

38 Accordingly, there is an issue of propriety or reasonableness. I am satisfied that directions are available and appropriate on that basis: cf Re Rewards Projects Ltd (In Liq); Ex parte Rewards Projects Ltd (In Liq) [2011] WASC 339 per Master Sanderson (at [22]).

Approval under s 477(2B)

39 Section 477(2B), sometimes referred to as the ‘long-term agreements’ provision, focuses particular attention on the need to ensure that the winding up will proceed in as expeditious a fashion as circumstances allow: Re HIH Insurance Ltd [2004] NSWSC 5 per Barrett J (at [15]). It is concerned to ensure that the Court exercises some oversight as to a liquidator's proposed action where that action falls within the purview of the provision. The Court will grant approval, which effectively authorises and permits the proposed action, where the case for the exercise of the power is sufficiently shown: Re HIH Insurance Ltd [2004] NSWSC 5 (at [15]).

40 The Court's usual approach was outlined by Giles J in Re Spedley Securities Ltd (1992) 9 ACSR 83 (at 85-86) (citations omitted):

... [T]he court pays regard to the commercial judgment of the liquidator. That is not to say that it rubber stamps whatever is put forward by the liquidator but ... the court is necessarily confined in attempting to second guess the liquidator in the exercise of his powers, and generally will not interfere unless there can be seen to be some lack of good faith, some error in law or principle, or real and substantial grounds for doubting the prudence of the liquidator's conduct.

The same restraint must apply when the question is whether the liquidator should be authorised to enter into a particular transaction the benefits and burdens of which required assessment on a commercial basis.

This passage has been approved in many subsequent authorities: see, for example, Re HIH Insurance Ltd [2004] NSWSC 5 (at [15]).

41 Relevant factors in determining whether to grant approval under s 477(2B) include:

(1) the interests of creditors: Re Spedley Securities Ltd (at 85);

(2) whether the agreement is for the proper realisation of the company's assets or whether it will assist the company's winding up: Re GA Listing & Maintenance Pty Ltd (1994) 15 ACSR 308 per Young J and

(3) the delay and uncertainty inherent in alternative courses of action: Cook v Scott William Law trading as E. R. Henry Wherrett & Benjamin [2003] FCA 966 per Heerey J (at [12]).

42 The function of the Court does not extend so far as to require the Court to review or be satisfied with the commercial desirability and terms of the agreement: Re HIH Overseas Holdings Ltd (In Liq) [2001] NSWSC 426 (at [5]); Re HIH Insurance Ltd [2004] NSWSC 5 (at [15]). This is because the approval of the Court is not an endorsement of the proposal, but rather permission for the exercise by the liquidator of his or her independent commercial judgment: Re GA Listing & Maintenance; Re United Medical Protection (2003) 46 ACSR 98 per Austin J (at [7]).

43 Accordingly, for approval under s 477(2B) of the Corporations Act, the Court will usually rely on the liquidator’s commercial judgment: Re Gate Gourmet Australia Pty Ltd (in liq) [2006] NSWSC 392 (at [7]). The Court will not second guess the liquidator’s judgment where the liquidator, in the exercise of his or her independent judgment, acting lawfully and in good faith and with appropriate advice, forms the commercial view that a transaction should be entered into, unless there are real and substantial grounds for doubting the prudence of it: Re United Medical Protection Ltd (2003) 46 ACSR 98 (at [6]). Although the liquidator must adduce a plausible evidentiary case before the Court in support of his or her commercial judgment: McLean v Elvapine Aberglasslyn Road Pty Ltd [2008] NSWSC 484 per Austin J (at [10]).

SOURCE OF POWER

Fortress Credit

44 It is necessary to give special consideration to the matters raised for BGNV concerning the Full Court decision of Emmett, Nicholas and Robertson JJ in Fortress Credit.

45 In Fortress Credit, the liquidators were liquidators of both Octaviar Ltd and its subsidiary, Octaviar Administration Pty Ltd. Administration was indebted to Octaviar and Octaviar was indebted to Fortress. Fortress claimed to be a secured creditor of Octaviar. Octaviar had various claims against Fortress (including a claim to impugn the validity of Fortress' security), but was without funds to pursue those claims. Administration, however, had assets consisting of a significant sum of cash. Administration and Octaviar entered into an ‘investigation agreement’ and later a ‘funding agreement’, whereby Administration agreed to lend funds to Octaviar (or provide it with other accommodation) to enable Octaviar to pursue its claims against Fortress. In consideration, which included indemnifying the liquidators and Octaviar in respect of any adverse costs orders and any undertaking as to damages given by the liquidators, for meeting the costs of pursuing those claims, Octaviar promised to repay the amount lent by Administration together with interest and a premium, if Octaviar's claims were successful. In the event that the funds obtained by Octaviar were insufficient to reimburse Administration for the amounts paid by it under the funding agreement, it was agreed that the liquidators of Administration could apply any dividend that was otherwise payable to Octaviar in the winding up of Administration to reimburse Administration and thereby reduce the debt owing by Administration to Octaviar.

46 At first instance, the Court approved entry into the funding agreement. Fortress, who had not been a party to the application for Court approval, obtained leave to appeal. The Full Court set aside the orders of the primary judge and remitted the matter for further consideration on the question of whether the entry into and performance of the obligations under the investigation agreement and funding agreement was ‘necessary’ for winding up the affairs of Administration and distributing its property within the meaning of s 477(2)(m) of the Corporations Act.

47 The liquidators in Fortress Credit unsuccessfully sought special leave to appeal to the High Court of Australia: Barnett v Fortress Credit Corporation (Australia) II Pty Limited; Fletcher v Fortress Credit Corporation (Australia) II Pty Limited [2012] HCA Trans 33.

48 There are parallels between the present case and Fortress Credit which BGNV draws to the Court’s attention. In particular, the position of TBGL (the claimant) corresponds with that of Octaviar, and the position of Maranoa Transport (the funder) corresponds with that of Administration. In addition, the proposed Agreement in this case adopts the same drafting technique as the funding agreement in Fortress Credit to set off and reduce the debt owing by Maranoa Transport to Octaviar. (Although, I note that in Fortress Credit the set off and reduction of debt between the claimant and the funder was only to occur if the funds obtained by the claimant from proceedings funded through the funding agreement were insufficient to reimburse the amounts paid under the funding agreement. Whereas, in this case, the sums paid under the proposed Agreement are (immediately) adjusted for as a reduction against the entitlements of TBGL (the claimant) to distributions by Maranoa Transport (the funder).)

49 Furthermore, BGNV notes differences of significance between this case and Fortress Credit. In particular:

in this case, Maranoa Transport, unlike Administration, does not stand to benefit financially should TBGL successfully challenge the Bell legislation or pursue any of its other claims, being the distribution and tax issues. Indeed, Maranoa Transport has no interest in challenging the Bell legislation as it was contemplated at the time of this hearing, as it is not a ‘WA Bell Company’ and is therefore unaffected by the Bell legislation. Put another way, both before and after the enactment of the Bell legislation, Maranoa Transport's financial position (absent the funding agreement) will be the same;

in Fortress Credit the liquidators deposed to their belief that it was in the interests of both the funder, Administration, and the claimant, Octaviar, to enter into the funding agreement. In contrast, in this case the plaintiff has only deposed to his belief that it is in the interest of TBGL to enter into the proposed Agreement. Nowhere in his affidavit does the plaintiff depose that he believes that it is in the interest of Maranoa Transport to enter into the funding agreement;

in forming the opinion that it was in the interests of the creditors of both Administration and Octaviar to enter into the funding agreement, the liquidators in Fortress Credit took into account the opinion of senior counsel concerning the prospects of success of Octaviar's proposed claims against Fortress. In contrast, in this case, there is no evidence before the Court on this issue. While the plaintiff has obtained legal advice on the constitutional validity of the Bell legislation, he has not disclosed to the Court the substance of that advice. Nor does the Court have before it any evidence as to the prospects of success of TBGL's other identified claims, such as its objections to the tax assessments; and

the liquidators in Fortress Credit had the benefit of an independent report as to the respective interests of Administration and Octaviar. The report demonstrated that ‘if the funding agreement were entered into and the proposed claims against Fortress were to succeed, there would be an improved return for creditors of both the funder and claimant’. There is no evidence of any such report in this case.

50 Broadly, BGNV contend that the appropriate question is whether the proposed Agreement is necessary (in the sense of expedient) for winding up the affairs of Maranoa Transport and distributing its property. Put another way: is the proposed agreement in the interests of the creditors of the funder (Maranoa Transport) as a whole (in their capacity as creditors of Maranoa Transport)? This is the question that falls to be assessed, as distinct from questions as to the interests of a particular group of creditors of Maranoa Transport, creditors of TBGL, or TBGL in a capacity other than as a creditor of Maranoa Transport.

51 The context of specific litigation funding, together with the primary loan structure of the funding agreement, led the Full Court in Fortress Credit to conclude that the arrangements ‘could only be authorised by s 477(2)(m)’: Fortress Credit (at [43]).

52 However, as the Full Court noted in Fortress Credit (at [41]):

... it does not necessarily follow from a conclusion that a proposed contract is in the best interests of creditors, or a group of creditors, of the company, that the contract is necessary for winding up the affairs of the company and distributing its property within the meaning of s 477(2)(m).

(emphasis added)

53 The Full Court in Fortress Credit concluded (at [44] and [47]) that s 477(2)(m) of the Corporations Act would not, for example, support the provision of litigation funding by a liquidator to an entirely unrelated litigant simply because such an arrangement offered the prospect of a commercial return. This was because such an arrangement could not be said to be ‘necessary’ for the winding up of the affairs of the company and distributing its property. In other words, there must be a benefit to the funding company beyond the return of a premium above the sum outlaid to fund the litigation.

54 BGNV submit that the Corporations Act does not afford to a liquidator an express power to lend money, much less an express power to enter into the proposed litigation funding Agreement. The proposed Agreement can only be authorised under s 477(2)(m) of the Corporations Act. This provision has been given a broad construction. ‘Necessary’ does not mean ‘essential’ or ‘indispensable’. Thus the section is not confined to matters without which the winding up of affairs and distribution of property cannot occur. Rather, s 477(2)(m) empowers a liquidator to do anything expedient, with reference to, or conducive to, the beneficial completion of the winding up of the affairs of the corporation and the distribution of its assets.

55 Accordingly, BGNV stress that before making an order under s 477(2B), or giving directions to the plaintiff under s 479(3), the Court must be satisfied and expressly find that there is a benefit to the creditors of Maranoa Transport as a whole from entering into the funding agreement, beyond the possible commercial return to be earned as consideration for lending money or granting accommodation to TBGL. In this context, Barrett J in Re HIH Insurance Ltd (2010) 266 ALR 642 (at Appendix 1 paras (25)-(26)) said:

... Before the court could conclude that the matter was within s 477(2)(m), it would have to see that there was some good and solid reason for concluding that the processes of winding up and distribution referred to in that provision would be enhanced by the particular outlay of funds envisaged in the particular circumstances prevailing, with the enhancement being demonstrable by comparison with the situation that would prevail if surplus funds were deployed in the ordinary way pursuant to s 543. The enhancement would have to be demonstrated by some informed and independent assessment of the separate and selfish interests of the funding company alone.

In the Bairnsdale Food case, Fullagar J emphasised that the existence of power must be distinguished from the propriety of its exercise. I do not lose sight of that distinction here. The point is that, when the question is whether a particular step is “necessary for” - in the s 477(2)(m) sense of “expedient with reference to” or “conducive to”- the progress and completion of the winding up process, the consequences or likely consequences of the step must be known (or, at least, reliably predicted, on the basis of known facts and informed assessment of their significance) as an essential ingredient of the formation of the opinion relevant to the existence of the power, quite separately from the wisdom of its exercise.

(emphasis added)

This passage was cited with approval by the New South Wales Court of Appeal in Fortress Credit Corporation (Australia) II Pty Ltd v Fletcher & Barnet (as liquidators of Octaviar Administration Pty Ltd (in Liq) (2015) 89 NSWLR 110 per Bathurst CJ, Beazley P, Macfarlan, Meagher and Barrett JJA agreeing (at [127]).

56 BGNV submit that the following question arises: can it be concluded that the process of winding up Maranoa Transport and distributing its assets will be enhanced by Maranoa Transport providing funding to TBGL? Having regard to the interests of Maranoa Transport alone, is Maranoa Transport better off with the proposed Agreement, compared to its position without the proposed Agreement?

57 In that regard, in Re HIH Insurance Ltd (2010) 266 ALR 692 (at Appendix 1 para (25)), Barrett J related the evidence of the liquidators and their expert that it was in the best interests of all participating companies, including the funding companies, to enter into the funding arrangements. However, Barrett J continued and relevantly said:

On the material before me, I do not see how I can safely conclude that it will be expedient with reference to, or conducive to, beneficial progress towards completion of the winding up of the affairs of any funding company and the distribution of its property for that funding company to provide financial assistance to the particular claimant company. A funding company could and, in the ordinary course, would deploy surplus funds in the normal types of investment entailing minimal risk: see s 543. For it to depart from that ordinary and expected course and to deploy its surplus funds in some other way would call for some analysis of pros and cons undertaken exclusively from the viewpoint of the funding company itself and having regard solely to its separate interests. That is what seems to me to be lacking here. It has not been suggested or shown that there has been any independent assessment, from the unilateral perspective of each funding company, of where the commercial and financial interests of that funding company lie, so far as the proposals are concerned. It is all very well to say, in the abstract, that by financially supporting the pursuit of particular litigation by a claimant company, a funding company may enhance its prospects of greater returns in its capacity as a creditor of the claimant company, in addition to recouping its funding outlay, plus interest and premium on a secured basis. That is no doubt supportable as a theoretical proposition. Also supportable in an abstract or theoretical sense is the proposition that the funding company faces the prospect of losing its total outlay without any return whatsoever.

(emphasis added)

58 Again, having regard solely to the interests of Maranoa Transport, BGNV question whether it can be safely concluded that it will be expedient with reference to, or conducive to, the beneficial progress towards completion of the winding up of the affairs of Maranoa Transport and the distribution of its property for it to provide financial assistance to TBGL. Would Maranoa Transport's commercial and financial interests be better served deploying its surplus funds, as now, in investments entailing minimal risk?

59 In answering these questions, regard must be had to the fact that the plaintiff is an experienced expert liquidator of both Maranoa Transport and TBGL. As Barrett J observed in Re HIH Insurance Ltd (2010) 266 ALR 642, after noting the position of conflict of the liquidators given that they were liquidators of both the funding companies and claimant companies (at Appendix 1 para (38)):

The court has not been given any separate assessment of where the funding companies' separate interests lie, so far as the proposed transactions are concerned. Opinions expressed by Mr McGrath (with whom Mr Honey concurs), Mr Hunter and Mr Lipman are opinions about the positions and interests of all the companies. To the extent that they speak of the interests of funding companies, the statements of those witnesses are necessarily coloured by the fact that they speak also of the interests of the assisting companies - indeed, the interests of all the companies affected by the proposals. As I have already said in the s 477(2)(m) context, someone qualified to do so needs to come to a fully informed and independent conclusion as to whether and, if so, how the separate interests of the funding companies (being, in the final analysis, the interests of the creditors who stand to receive distributions in the funding companies' windings up) will be promoted by having them commit their funds in the ways envisaged, when the alternative is for those funds to be husbanded in the normal way. Any application for fiduciary dispensation must necessarily proceed by reference to a comparison of that kind.

(emphasis added)

60 Those comments apply equally here.

Distinctions between Fortress Credit and the present case

61 While it was helpful to receive the observations of BGNV, I do not consider that the application of the principles which flow from Fortress Credit, nor Re HIH Insurance Ltd (2010) 266 ALR 642, prevents the making of the orders sought by the plaintiff.

62 The plaintiff points to the following matters concerning Fortress Credit:

The object and immediate context of the proposed funding agreement in Fortress Credit was the pursuit of specific litigation: Fortress Credit (at [12]-[13]).

The funding agreement in Fortress Credit was principally structured (and regarded by the Full Court) as providing for a loan. The funder was to lend money, or grant other accommodation, in return for a promise from the funded company to repay the amount of the money advanced or accommodation granted, with interest and a premium if success was achieved in the proposed litigation: Fortress Credit (at [43]).

While, as BGNV notes, there was provision in the Fortress Credit funding agreement for a ‘set off’ of any eventual dividend that might be payable to the funded company, that was only to be activated if the funding company could not be repaid in full from the primary loan arrangements, including from the proceeds of litigation: Fortress Credit (at [14]). The Full Court did not attach any significance to this ‘set off’ aspect of the agreement: Fortress Credit ([43]-[44]). Given that the predominant character of the agreement was one of loan and repayment, the Full Court was undoubtedly correct to approach the case before it in this manner.

63 In the present application, as it appears to me on the particular facts, all entities who could have reasonably been heard to oppose or support the orders sought have had the opportunity to do so and have done so where considered necessary. This is a central, probably essential, requirement.

64 In my view, there is a fundamental difference between Fortress Credit and this case: the proposed Agreement would not be correctly described as, nor appropriately confined to, a mere litigation funding agreement.

65 While the funding under the proposed Agreement might be used for litigation, its purpose is not so limited. There is no express restriction placed on use of the funds. Rather, the object of the proposed Agreement is to enable the windings up of all of the Bell Group companies to continue by ensuring that TBGL's 50% share of the costs and expenses of all group liquidations can continue to be met. The funds to be provided may be utilised to meet 50% of the costs and expenses incurred for any purpose properly in the interests of the windings up of any of the group companies which, hitherto, had been met by TBGL from its own funds.

66 This is an important distinction. It explains why certain queries or issues properly raised by BGNV about the proposed Agreement do not arise. In particular, BGNV queries why the plaintiff does not disclose his advice about the constitutional validity of the Bell legislation or evidence about prospects of success of objections to tax assessments and other claims. The answer is that the plaintiff is not seeking approval and directions to receive funding for specific matters such as these. Rather, the approval sought is simply to enable access to a source of funds other than the assets presently available in its liquidation.

Power under s 477(1)(c)

67 The proposed Agreement is not a ‘loan’ by Maranoa Transport to TBGL. Rather, where Maranoa Transport meets costs and expenses that otherwise would have been met by TBGL, the amount paid is adjusted for as a reduction against TBGL's proportionate entitlement to distributions from Maranoa Transport. This is similar to a prepayment of distributions that otherwise would be payable to TBGL in satisfaction of Maranoa Transport's existing liabilities to TBGL as its creditor.

68 In substance, the proposed Agreement thus provides a mechanism to ‘prepay’ part of the distribution that Maranoa Transport will in due course make to TBGL. TBGL receives at an earlier time the benefit of funds that would otherwise be distributed to it. Maranoa Transport reduces the claim of one of its creditors immediately.

69 Section 477(1)(c) empowers the liquidator of Maranoa Transport to make ‘any compromise or arrangement with creditors’: That is, some compromise or arrangement by which a particular creditor or particular creditors ‘agree to a particular regime with respect to their debts alone’: Re Dean-Willcocks; Alpha Telecom (Aust) Pty Ltd (2004) 208 ALR 414 per Barrett J (at [19]); Re Tayeh (2005) 53 ACSR 684 per Barrett J (at [8]).

70 The power under s 477(1)(c) will not authorise an abandonment or confiscation of rights without some corresponding advantage: Re Opes Prime Stockbroking Ltd (2009) 179 FCR 20 per Finkelstein J (at [31]).

71 The plaintiff argues, and I accept, that the proposed Agreement provides for an ‘arrangement’ under s 477(1)(c). It ‘touches and concerns’ the rights and obligations of Maranoa Transport and TBGL because, if executed, it will put in place a particular regime for Maranoa Transport to meet its liabilities to TBGL, as its principal creditor by a large margin. There is nothing illegal or contrary to law about the proposal. No rights are confiscated or abandoned.

72 The proposed Agreement is in TBGL's interests as the principal creditor of Maranoa Transport. The arrangement will not prejudice Maranoa Transport's remaining creditors, being Maradolf and the Commissioner, in respect of any later distributions in Maranoa Transport's winding up: see for example Re Wily (2003) 48 ACSR 86 per Barrett J (at [19]). Further, the only creditor of Maranoa Transport external to the Bell Group companies has been consulted about and supports the proposed Agreement as explained above.

73 These matters provide a sufficient basis for the Court to be satisfied that there are no real and substantial grounds for doubting the prudence or bona fides of the proposed agreement. Accordingly, the proposed Agreement is within power under s 477(1)(c) and it is appropriate in all the circumstances to grant the directions and authorisation sought by the plaintiff.

Power under s 477(2)(m)

74 The question for the Court under s 477(1)(c) is not the same as that which arises under s 477(2)(m). Subparagraph 477(2)(m) is directed to things done by the liquidator in and for the ordinary progression of the winding up.

75 In Re McGrath (at [22]), Barrett J summarised the general principles as to the power available to the liquidator under s 477(m) of the Corporations Act as follows:

The word “necessary”, as used in s 477(2)(m), has been given a broad meaning. It is not synonymous with “essential” or “indispensable”: see, for example, Re Wreck Recovery and Salvage Co (1880) 15 ChD 353 at p 362 per Thesiger LJ. The power is not confined to matters without which the winding up of affairs and distribution of property cannot occur. The test is, rather, one of what “may be thought expedient with reference to the assets of the company”: Re Cambrian Mining Co (1882) 48 LT 114 per Kay J. The later case of Re Bairnsdale Food Products Ltd [1948] VLR 264 provides an example of the scope of the power. That case concerned a company which had a right of first refusal in respect of land occupied by it as lessee. After commencement of the winding up, the lessor offered the company the opportunity to purchase. On the evidence, it would have been advantageous to the winding up for the liquidator to buy the land and re-sell it, thus realising the value of the right of first refusal. It was held that the purchase was justified as an incident of the subsequent sale and was therefore comprehended by the liquidator's power to sell. There was subsidiary reliance upon the equivalent of s 477(2)(m).

76 BGNV contends that Maranoa Transport does not stand to benefit financially if TBGL successfully challenges the Bell legislation or pursues its ‘other claims’ and that it has ‘no interest’ in such matters.

77 BGNV also question whether the proposed Agreement may not be conducive to or assist the beneficial winding up of the affairs of Maranoa Transport.

78 On the plaintiff’s evidence, particularly that adduced in the affidavits of the plaintiff, I consider both of these issues are addressed as:

Firstly, Maranoa Transport's winding up benefits from progression of the objections to the tax assessments. In short, the tax objections potentially enable Maranoa Transport to avoid a liability and thus potentially preserve more assets for its creditors.

Secondly, Maranoa Transport benefits from participating in or bringing any challenge to the Bell legislation. For example, the plaintiff says that a challenge to the Bell legislation, if enacted, may enable Maranoa Transport to protect its right to receive some $55 million presently held in trust by a company the subject of the Bell legislation, and thus preserve its assets for later distribution.

Thirdly, Maranoa Transport's winding up has benefited, and continues to benefit, from the prosecution of certain garnishee notice proceedings in NSD 1030 of 2015.

Fourthly, there is common utilisation of essential business services, utilities, third party service providers and staff of the liquidations of all Bell Group companies, including Maranoa Transport. Thus, Maranoa Transport's winding up benefits from the continued availability and provision of these services.

79 I am satisfied that these considerations are sufficient to demonstrate that the requirements of s 477(2)(m) are satisfied by the proposed Agreement.

PROPRIETY

80 In assessing the direction sought by the plaintiff, three of the observations made by Barrett J in Re McGrath (as liquidators of HIH Insurance Ltd) (2009) 77 ATR 775 (at [19]) are apposite:

It is essential to look separately at each company and the interests of that company alone.

Each company must be viewed as an embodiment of the interests of its own separate group of creditors.

The resources within each company in its winding up are applicable solely for the benefit of its own creditors.

81 There is little doubt that entry into the funding and indemnity agreement is in the interests of TBGL and its creditors. Costs and expenses that otherwise would have been met by TBGL will be met by Maranoa Transport. This will enable the windings up of the Bell Group companies to continue to be progressed, which is also in TBGL's interests. Further, TBGL benefits by effectively obtaining prior to declaration of dividend the use of funds held by Maranoa Transport which would otherwise only become available later in the windings up of TBGL and Maranoa Transport.

82 Insofar as Maranoa Transport is concerned, consistently with the approach in Re McGrath (at [19]), it should be viewed as the embodiment of the interests of its separate creditors, being TBGL, Maradolf and the Commissioner. But in the circumstances set out above, where the surplus in Maradolf’s winding up will accrue to the benefit of TBGL, the relevant interests are those of TBGL and the Commissioner.

83 Entry into the proposed Agreement will enable TBGL, holder of 97.9% of the creditors' claims, to immediately benefit from Maranoa Transport's winding up. In addition, the funding and indemnity agreement has been designed to provide for a countervailing benefit for the other creditors to appropriately compensate them for the immediate benefit that TBGL is to receive. TBGL's interests are served by entry into the funding and indemnity agreement.

84 The Commissioner supports the proposed Agreement. Importantly, the Commissioner is a sophisticated litigant with experienced and competent legal advisers, and is well able to determine his own interests.

85 In the circumstance of the potential or apparent conflict of interest or duty that arises, and particularly by reason of the plaintiff’s undertaking upon being appointed as sole liquidator of the Bell Group companies, I consider that the direction sought facilitates a proposed action which will be of benefit to the Bell Group companies individually and collectively where, absent the direction, a degree of personal risk attaches to the plaintiff liquidator. Indeed, it might otherwise be that the plaintiff liquidator would have to cease to incur costs and expenses in conducting the Bell Group companies' windings up. That would not be conducive to the effective and efficient conduct of the windings up.

86 As to approval under s 477(2B) of the Corporations Act:

the proposed funding and indemnity agreement has a life that is limited to 18 months unless extended following further directions and approval of the Court; accordingly, it will not needlessly protract the time for completion of the Bell Group windings up; it has no effect at all on the likely timeframe for finalisation of the windings up; and

the plaintiff contends that the funding and indemnity will assist the windings up: it will facilitate the continued effective and efficient conduct of the windings up, which will otherwise be at risk and (which I accept), there is no reason to believe that the proposed Agreement involves any lack of good faith, error of law or principle or lack of prudence on the part of the plaintiff.

An undertaking in the Supreme Court of Western Australia

87 The plaintiff was removed as an additional liquidator of the Bell Group companies and immediately re-appointed as the sole official liquidator of those companies, subject to an undertaking to the Supreme Court of Western Australia to raise any conflict of interest that might arise. BGNV raised the question of whether the present proceeding ‘complies with the terms of plaintiff’s undertaking’ given to the Supreme Court (in COR 122 of 2014).

88 The wording of the undertaking was to the effect that the plaintiff undertook to the Supreme Court (‘this Honourable Court’) that, if appointed as sole liquidator of TBGL and certain other companies, he would seek directions from ‘the Court’ in the event of a conflict emerging. The identity of ‘the Court’ was not specified in the text of the undertaking, but would normally be taken as being the court to which the undertaking was given.

89 The plaintiff argues that the policy of the undertaking favours a reading of ‘the Court’ that extends to any court having appropriate jurisdiction; this Court being such a court.

90 The object of the undertaking is to ensure that appropriate judicial oversight occurs when it comes to the plaintiff's actions in acting or failing to act in circumstances where an actual or potential conflict of interest emerges, bearing in mind the multiple liquidator appointments held. There is nothing about that policy which supports confining the giving of that oversight to the Supreme Court and no good reason for thinking the Supreme Court would have sought to confine the undertaking in the manner suggested. Any question as to this is a matter for the Supreme Court to determine, as the court to whom the undertaking was given.

91 The plaintiff explained on oath, in some detail, that for reasons of expediency only at the particular time, on this occasion, pursuit of the relief sought in this Court was the practical option pursued. The explanation is accepted. There is no evidence of avoiding the obligations of an undertaking by forum shopping or otherwise.

92 For these reasons I was satisfied that it was appropriate to make the following orders that:

(1) Pursuant to:

(a) in the case of those Bell Group companies ordered to be wound up before 23 June 1993, namely:

(i) The Bell Group Limited (in liquidation) ACN 008 666 993;

(ii) Albany Broadcasters Limited (in liquidation) ACN 008 674 600;

(iii) Bell Bros Holdings Limited (in liquidation) ACN 008 695 056;

(iv) Bell Group Finance Pty Ltd (in liquidation) ACN 009 165 182;

(v) Bell Publishing Group Pty Ltd (in liquidation) ACN 008 704 452;

(vi) W&J Investments Pty Ltd (in liquidation) ACN 000 068 888; and

(vii) Wigmores Tractors Pty Ltd (in liquidation) ACN 008 679 221,

s 479(3) of the Corporations Law (as applied by s 1408(1) of the Corporations Act 2001 (Cth));

(b) in the case of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395, the inherent or implied jurisdiction of the Court (and, if and to the extent required, s 479(3) of the Corporations Act 2001 (Cth)); and

(c) in the case of the Bell Group companies other than those ordered to be wound up by the Court before 23 June 1993 and Western Interstate Pty Ltd (provisional liquidator appointed), s 479(3) of the Corporations Act 2001 (Cth),

it is directed that the plaintiff (as liquidator or provisional liquidator, as the case may be) will be acting properly and is justified in causing each of the companies as listed in the annexure to these orders (Bell Group companies) to enter into and perform a funding and indemnity agreement that is in or substantially in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

(2) The plaintiff as liquidator of:

(a) Ambassador Nominees Pty Ltd (in liquidation) ACN 009 105 800;

(b) Belcap Enterprises Pty Ltd (in liquidation) ACN 009 264 537;

(c) Bell Bros Pty Ltd (in liquidation) ACN 008 672 375;

(d) Bell Equity Management Limited (in liquidation) ACN 009 210 208;

(e) Dolfinne Pty Ltd (in liquidation) ACN 009 134 516;

(f) Dolfinne Securities Pty Ltd (in liquidation) ACN 009 218 142;

(g) Great Western Transport Pty Ltd (in liquidation) ACN 009 669 121;

(h) Harlesden Finance Pty Ltd (in liquidation) ACN 009 227 561;

(i) Industrial Securities Pty Ltd (in liquidation) ACN 008 728 792;

(j) Maradolf Limited (in liquidation) ACN 005 482 806;

(k) Maranoa Transport Pty Ltd (in liquidation) ACN 009 668 393;

(l) Neoma Investments Pty Ltd (in liquidation) ACN 009 234 842;

(m) TBGL Enterprises Limited (in liquidation) ACN 008 669 216;

(n) WAON Investments Pty Ltd (in liquidation) ACN 008 937 166;

(o) Wanstead Pty Ltd (in liquidation) ACN 008 775 120;

(p) Wanstead Securities Pty Ltd (in liquidation) ACN 009 218 160; and

(q) Western Transport Pty Ltd (in liquidation) ACN 009 666 308,

has approval under s 477(2B) of the Corporations Act 2001 (Cth) to enter into and cause those companies to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

(3) The plaintiff as provisional liquidator of Western Interstate Pty Ltd (provisional liquidator appointed) ACN 000 224 395 has approval under s 477(2B) (as applied by s 472(5) of the Corporations Act 2001 (Cth)) to enter into and cause that company to enter into a funding and indemnity agreement that is in the form of the document that is attachment "ALJW-44" to the affidavit of the plaintiff sworn 1 October 2015 and filed herein.

(4) The costs of the application are costs in the windings up of The Bell Group Limited (in liquidation) and Bell Group Finance Pty Ltd (in liquidation) in equal proportions.

I certify that the preceding ninety-two (92) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice McKerracher. |

Associate: