FEDERAL COURT OF AUSTRALIA

Atlas Iron Limited, in the matter of Atlas Iron Limited [2016] FCA 366

Table of Corrections | |

In the first sentence of [53], the word “to” has been inserted before the word “express”. |

ORDERS

ATLAS IRON LIMITED (ACN 110 396 168) Plaintiff | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Plaintiff convene a meeting of the lenders under the Syndicated Facility Agreement dated 10 December 2012 between (among others) the Plaintiff and those lenders (TLB Lenders) for the purpose of considering and, if thought fit, agreeing (with or without modification) to a scheme of arrangement proposed to be made between the Plaintiff, the TLB Lenders and certain holders of subordinate claims against the Plaintiff (Scheme), being a scheme substantially in the form of that contained in Annexure A to the explanatory statement in relation to the Scheme which is Exhibit 1 in the proceeding.

2. The draft explanatory statement and notice of scheme meeting which is Exhibit 1 (Scheme Booklet) is approved for distribution to the TLB Lenders.

3. The Plaintiff dispatch to each TLB Lender a document substantially in the form of the Scheme Booklet by:

(a) in the case of any TLB Lender who is a party to the Restructuring Support Agreement dated 22 December 2015 (RSA), sending by courier one copy of the Scheme Booklet, marked to the attention of the relevant TLB Lender, to:

(i) the address stipulated in the column headed “Notice Details” in Schedule 6 of the RSA (in respect of each Original Participating Secured Lender under the RSA); and

(ii) the address stipulated in the Joinder Agreement executed by the TLB Lender (in respect of each Additional Participating Secured Creditor under the RSA);

(b) sending by courier one copy of the Scheme Booklet to Marathon Asset Management LP, One Bryant Park, 38th Floor, New York NY 10036, United States of America, marked to the attention of:

(i) Marathon Liquid Credit Long Short Fund;

(ii) Marathon Blue Grass Credit Fund LP; and

(iii) MV Credit Opportunity Fund LP; and

(c) sending by courier a copy of the Scheme Booklet to each of:

(i) Commonwealth Bank of Australia, at Ground Level 1, 201 Sussex Street, Sydney NSW, 2000; and

(ii) Caterpillar Financial Australia Limited, at 1 Caterpillar Drive, Tullamarine Victoria, 3043.

4. The scheme meeting be held at 10:30 am on 22 April 2016 at Level 11, 5 Martin Place, Sydney NSW.

5. Anthony Michael Walsh, or failing him, Bronwyn Rachel Kerr, be chair of the scheme meeting.

6. Except for procedural motions, all voting at the scheme meeting be by poll as declared by the chair.

7. The chair has the power to adjourn the scheme meeting in his or her absolute discretion.

8. The chair may, at his or her absolute discretion, determine that only proxy forms and proofs of debt in relation to the scheme meeting received by the chair no later than 4:00 pm on 18 April 2016 are valid.

9. The chair may rely on the information provided to the Plaintiff as at 18 April 2016 by Credit Suisse AG, Cayman Islands Branch, in its capacity as Administrative Agent for the TLB Lenders, for the purposes of admitting or rejecting a proof of debt for the purpose of voting.

10. The application of regulations 5.6.11 to 5.6.36A of the Corporations Regulations 2001 (Cth) to the scheme meeting pursuant to rule 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) be modified in the following respects:

(a) regulations 5.6.11 to 5.6.36A shall not apply to the scheme meeting, with the exception of the following regulations:

(i) regulation 5.6.14A(1);

(ii) regulation 5.6.16(1)(b),(c),(2),(3),(4);

(iii) regulation 5.6.26(1),(2); and

(iv) regulation 5.6.30,

(b) regulation 5.6.23(1) shall apply to the scheme meeting as modified to read: “A person is not entitled to vote as a creditor at a meeting of creditors unless his or her debt or claim has been admitted wholly or in part by the chairperson of the meeting and he or she has lodged, with the chairperson of the meeting a formal proof of debt”;

(c) regulation 5.6.26(3) shall apply to the scheme meeting as modified to read: “A decision by the chairperson to admit or reject a proof of debt or claim for the purpose of voting may be appealed against to this Court by an application filed with the Court within 48 hours of the decision, such appeal to be heard concurrently with the second court hearing”;

(d) regulations 5.6.28 and 5.6.31A shall apply to the scheme meeting as modified to remove the words: “(except in relation to the election of a chairperson)” where they appear in that regulation; and

(e) regulation 5.6.32(1) shall apply to the scheme meeting as modified to read: “A person may appoint the chairperson of a meeting by name or reference to his or her office, to act as his general or special proxy”.

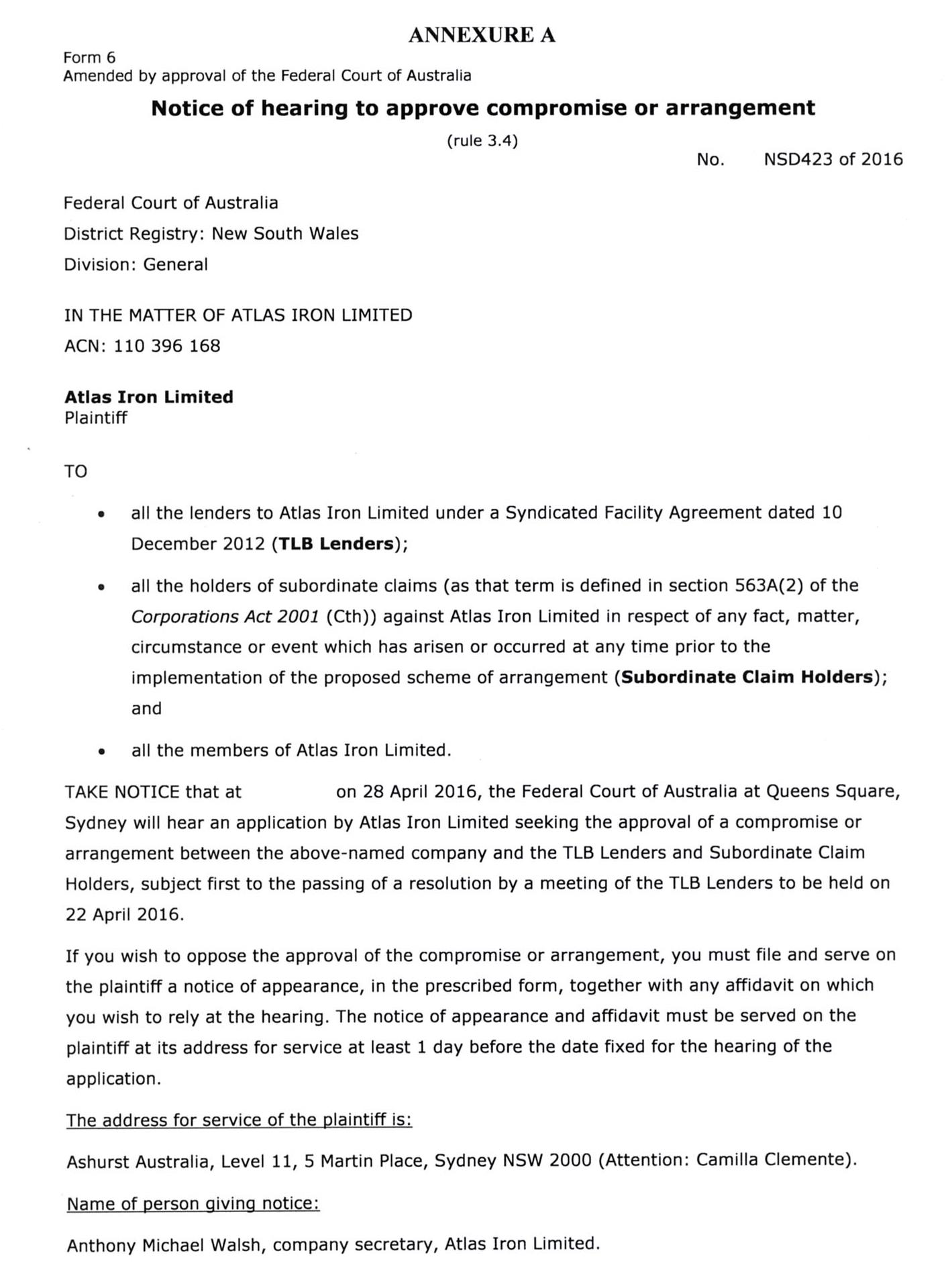

11. Notice of the hearing of an application pursuant to section 411(4)(b) of the Corporations Act 2001 (Cth) for orders approving the Scheme be published once in The Australian newspaper, by advertisement substantially in the form of Annexure A to these orders, such advertisement to be published on or before 21 April 2016 and the Plaintiff otherwise be exempted from compliance with r 3.4 of the Federal Court (Corporations) Rules 2000 (Cth).

12. The proceeding be adjourned to 10:15 am on 28 April 2016.

13. Liberty to apply on 2 days’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

NSD 423 of 2016 | ||

IN THE MATTER OF ATLAS IRON LIMITED (ACN 110 396 168) | ||

BETWEEN: | ATLAS IRON LIMITED (ACN 110 396 168) Plaintiff | |

JUDGE: | GLEESON J |

DATE: | 6 APRIL 2016 |

THE COURT ORDERS THAT:

1. Order 11 of the orders made 31 March 2016 be varied as follows:

Notice of the hearing of an application pursuant to section 411(4)(b) of the Corporations Act 2001 (Cth) for orders approving the Scheme be published once in The Australian newspaper, by advertisement substantially in the form of Annexure A to these orders, such advertisement to be published on or before 21 April 2016 and the Plaintiff otherwise be exempted from compliance with r 3.4 of the Federal Court (Corporations) Rules 2000 (Cth).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GLEESON J:

1 On 24 March 2016, the plaintiff (“Atlas”) filed an originating process seeking orders pursuant to s 411(1) of the Corporations Act 2001 (Cth) (“Act”) for the convening of a meeting of certain creditors of Atlas, being lenders pursuant to a Syndicated Facility Agreement dated 10 December 2012 (“TLB lenders”), to consider a scheme of arrangement (“scheme”) and, if the Court thinks fit, approving the scheme.

2 On 31 March 2016, I heard Atlas’s initial application, being for orders that Atlas convene a meeting of the TLB creditors and approving for distribution the explanatory statement for the scheme (“first court hearing”). With leave, Ms Wong of counsel appeared for the TLB lenders. The Australian Securities and Investments Commission (“ASIC”) wrote a lengthy letter to the directors of Atlas dated 30 March 2016, commenting on and expressing concerns about the scheme, and instructing the directors to draw the letter to the Court’s attention. ASIC did not attend Court to oppose the initial application or to propose any variation to the orders sought by Atlas. I will address ASIC’s letter in more detail below.

3 After the hearing, I made the orders sought by Atlas. These are my reasons for making those orders, and for the order, varying the orders in one respect, made today.

Background

4 Atlas is an Australian iron ore mining company listed on the Australian Stock Exchange (“ASX”).

5 As at 21 March 2016, Atlas has 2,669,787,052 ordinary shares on issue to a large number of institutional and retail investors. Twenty shareholders hold approximately 44% of the total issued shares.

6 As at the close of trade on 22 March 2016, the price of each share as quoted on the ASX was $0.03.

Financial position of Atlas

7 Atlas mines and ships iron ore from Port Hedland in the Pilbara region of Western Australia. It has three key production projects (in addition to other projects in varying stages of development in the Pilbara region), being Abydos Mine, Mt Webber Mine and Wodgina Mine.

8 The evidence of David Nathan Flanagan, Atlas’ managing director, was that Atlas engages mining contractors to extract iron ore from the mines and process it through processing plants. The processed iron ore is hauled from the mines to Port Hedland by contractors, before port and handling contractors then ship it. Consequently, Atlas is heavily reliant on its contractors for the operation of its business.

9 Mr Flanagan stated that Atlas derives almost all of its revenue from the sale of iron ore, so that its business is affected by fluctuations in the iron ore prices from time to time. According to Mr Flanagan, iron ore prices have been volatile for a significant period.

10 Atlas’ income from its business operations is also affected by fluctuations in the exchange rates for US and Australian dollars.

Syndicated Facility Agreement

11 Pursuant to the Syndicated Facility Agreement, Atlas obtained a “Term Loan B” facility in the sum of US$275,000,000 secured by a general security deed and featherweight floating charge. The principal obligations under the facility are guaranteed by certain subsidiary companies of Atlas.

12 The debt, which now stands at approximately $259,300,000, is due for repayment in December 2017 (“TLB debt”).

Proposed scheme

13 The proposed scheme was summarised by counsel for Atlas as follows:

(a) Atlas will make a cash payment to the TLB lenders equal to all accrued and unpaid interest owing to them as at the implementation date together with a further cash payment of US$2,500,000 (scheme, cl 7.5(d));

(b) Atlas will issue to the TLB lenders:

(i) ordinary shares so that, following the share issue, the TLB lenders will hold 70% of the total ordinary shares in Atlas; and

(ii) options to acquire ordinary shares such that, following the option issue, the TLB lenders will hold 70% of all quoted options to acquire ordinary shares in Atlas (scheme, cl 7.5(f));

(c) in consideration for the payments referred to in (a) above and the issue of equity referred to in (b) above, the TLB lenders will release Atlas and its guarantors from the obligation to pay so much of the principal amount owing under the Term Loan B Facility as exceeds US$135,000,000 (scheme, cl 7.5(h));

(d) the remaining TLB debt will be held on the terms of an amended Syndicated Facility Agreement, pursuant to which the TLB debt will become due for repayment five years from the implementation date and certain financial covenants will be varied (scheme, cl 7.5(j) and Sch 2);

(e) the TLB lenders will appoint three directors to the board of Atlas and two of the four existing directors (excluding the managing director, Mr Flanagan) will resign (scheme, cll 7.5(e) and (k));

(f) there will be mutual releases as between the TLB lenders and past and present directors, officers and employees of Atlas and its subsidiaries which have guaranteed Atlas’ debt (scheme, cl 7.5(g)); and

(g) any existing subordinate claims within the meaning of s 563A of the Act will be released, except to the extent of the net proceeds of any policy of insurance that responds to any subordinate claim (scheme, cl 7.5(1)).

14 The scheme will have no effect on unsecured trade creditors or on secured or unsecured creditors of Atlas other than the TLB Lenders and subordinate claim holders.

15 It is a condition precedent to the scheme being implemented that the shareholders of Atlas approve the issue of shares and options to the TLB lenders at a meeting in accordance with ASX Listing Rule 7.1 (“shareholders meeting”). Due to the requirement for shareholders to receive 28 clear days’ notice of a shareholder meeting under the ASX Listing Rules, Atlas despatched notices of the meeting on 24 March 2016 (“notice of general meeting”).

16 The debt restructure to be effected by the scheme is supported by 93% of the TLB lenders, holding 86.2% of the TLB debt, who have signed a Restructuring Support Agreement with Atlas dated 22 December 2015. There are five lenders who have not yet consented to the debt restructure, being the Commonwealth Bank of Australia, Caterpillar Finance Australia Limited and three foreign lenders (Marathon Liquid Credit Long Short Fund, Marathon Blue Grass Credit Fund LP and MV Credit Opportunity Fund LP).

Reasons scheme is being propounded

17 Atlas identified the following two reasons for the scheme:

(1) There is a requirement in cl 7.13 of the Syndicated Facility Agreement to the effect that Atlas will not permit the Total Assets to Total Secured Debt Ratio, as determined as of the last day of each semi-annual period, to be less than 2:1 (“Asset Coverage Ratio”). This covenant is tested as at 30 June and 31 December of each year. Atlas is concerned that there is a high risk that it will fail to satisfy the Asset Coverage Ratio when it is next tested as at 30 June 2016.

Failure to satisfy the Asset Coverage Ratio constitutes an Event of Default under cl 8.l(c) of the Syndicated Facility Agreement, which in turn entitles the TLB lenders to demand immediate repayment of the TLB debt and appoint a receiver. Atlas is concerned that if that were to occur, it is unlikely it or its subsidiaries would have sufficient liquidity or be able to raise sufficient capital or external finance to repay the TLB debt immediately. Mr Flanagan’s evidence was that, in those circumstances the directors would have no choice but to appoint a voluntary administrator. The scheme avoids these consequences by providing for an amended Syndicated Facility Agreement which removes the covenant to comply with the Asset Coverage Ratio;

(2) As matters stand, Atlas must repay the TLB debt in December 2017. Based on present cash flow forecasts (and assuming the scheme is not implemented), Atlas will be unable to repay the TLB debt on maturity from its forecast available cash flows. The TLB debt will become a current liability in December 2016. Despite extensive efforts to explore other debt and equity financing options, the Atlas board has no current basis for forming a view that any of these options or the company’s future anticipated operating performance will permit the full repayment or refinance of the TLB debt in December 2017. The scheme avoids this scenario by extending the maturity date of the TLB debt.

EVIDENCE

18 The plaintiff read the following affidavits in support of the application:

(1) affidavit of Marcus William Ayres, chartered accountant and partner of PPB Advisory (“PPB Advisory”), sworn 30 March 2016;

(2) affidavit of Philip Patrick Carter, chartered accountant and partner of PPB Advisory, sworn 30 March 2016;

(3) affidavit of Camilla Clemente, solicitor employed by Ashurst Australia, Atlas’ Australian lawyers (“Ashurst”), sworn 24 March 2016;

(4) affidavit of Ms Clemente sworn 31 March 2016;

(5) affidavit of Mr Flanagan sworn 24 March 2016;

(6) affidavit of Mr Flanagan sworn 30 March 2016;

(7) affidavit of Campbell Jaski, valuer and partner of PPB Advisory, sworn 31 March 2016;

(8) affidavit of Bronwyn Rachel Kerr, legal manager of Atlas, sworn 23 March 2016;

(9) affidavit of Ms Kerr sworn 30 March 2016;

(10) affidavit of Simon Theobold, chartered accountant and managing partner, Western Australia of PPB Advisory, sworn 30 March 2016;

(11) affidavit of Anthony Michael Walsh, company secretary of Atlas, sworn 24 March 2016; and

(12) affidavit of Mr Walsh sworn 30 March 2016.

19 In addition, the plaintiff tendered the following documents:

(1) a copy of the draft explanatory statement to be sent to the scheme members (“scheme booklet”) (exhibit 1);

(2) an exhibit to the affidavit of Mr Carter sworn 30 March 2016 (exhibit PC-1);

(3) an exhibit to the affidavit of Ms Clemente sworn 24 March 2016 (exhibit CC-1);

(4) an exhibit to the affidavit of Ms Clemente sworn 31 March 2016 (exhibit CC-2);

(5) an exhibit to the affidavit of Mr Flanagan sworn 23 March 2016 (exhibit DF-1);

(6) an exhibit to the affidavit of Mr Walsh sworn 30 March 2016 (exhibit “AMW-1”).

Opinions

Directors

20 Mr Flanagan’s opinion is that the scheme represents by far the best alternative available to TLB lenders (as well as Atlas’s other creditors and shareholders) to permit the preservation of Atlas’s business as a going concern.

21 In the notice of general meeting, the directors of Atlas expressed their belief that the resolution for approval to issue new shares and new options under the financial restructuring is in the best interests of the company and its shareholders, and unanimously recommend that shareholders vote in favour of the resolution

Independent expert

22 PPB prepared an independent expert report dated 24 February 2016. After Atlas received comments from ASIC, PPB prepared a supplementary report dated 30 March 2016. The supplementary report expresses the view that:

(1) there is a high degree of risk that Atlas will breach the Asset Coverage Ratio test as at 30 June 2016 in the event that the scheme is not implemented; and

(2) in the event that the scheme is not implemented and that Atlas passes the Asset Coverage Ratio test at 30 June 2016, it is likely that Atlas will breach the covenant at 31 December 2016 unless there is a significant uplift in the AUD/USD exchange rate and/or the iron ore price or an equity injection;

(3) if the ratio is breached, the TLB lenders will be entitled to demand immediate repayment of the TLB debt and, if that occurs, Atlas and its subsidiaries are unlikely to have sufficient liquidity or be able to raise sufficient capital or external finance to repay the TLB debt in such a short timeframe. If this were to occur, it would likely result in Atlas and its subsidiaries becoming insolvent and administrators or receivers and managers being appointed;

(4) as the maturity date of the TLB debt is 31 December 2017, it is likely the debt will be reclassified from non-current to current in the 31 December 2016 halfyearly accounts. If that occurs, the directors would need to consider whether the debt could be repaid or refinanced in the next 12 months. Without a substantial improvement in the iron ore price, PPB considers that Atlas and its subsidiaries would be unable to refinance the debt and would need to consider appointing an external administrator;

(5) if Atlas were to be wound up on either 30 June 2016 or 31 December 2016, the TLB lenders are highly unlikely to be repaid in full and there will be no funds available to pay subordinate claimholders;

(6) there is a forecast deterioration in the TLB lenders’ recovery position between 30 June 2016 and 31 December 2016. This would be a factor in the TLB lenders’ decision as to whether to enforce their security if a breach of the Asset Coverage Ratio were to occur as at 30 June 2016;

(7) if the scheme is implemented, Atlas and its subsidiaries will be solvent, with positive month end cash balances for the next 12 months and a positive net asset/current asset position. The solvency of the group remains dependent on a forecast improvement in the Benchmark iron ore price and compliance with the minimum cash covenant agreed between Atlas and the TLB lenders.

ASIC

23 ASIC’s 11 page letter commences by identifying the rationale for the scheme (in a manner consistent with the rationale set out above) and by noting that it “is not clear that it is inevitable that Atlas will breach the Asset Coverage Ratio or not be able to pay all outstanding capital and interest at the maturity date”. The letter does not say that any of the scheme documentation states or implies any such inevitability. As I read the letter, the purpose of these introductory observations was to emphasise that the proposed scheme is intended to address the risk of adverse future events (which the directors assess to be a high risk) rather than certain future events.

24 ASIC’s letter contends that the creditors voting on the scheme and the shareholders voting at the shareholders meeting need further information to enable them to make fully informed decisions. Initially, the letter identifies the further information as additional sensitivity analysis assessment of the risk of a breach of the Asset Coverage Ratio, and an opinion from directors about the extent of improvement in iron ore prices that would allow Atlas to refinance or repay the TLB lenders. As appears below, later in the letter ASIC contended that shareholders also require an independent expert report.

25 ASIC observes that the scheme documentation does not provide “clear current evidence of any stated intention of any creditors to appoint a receiver on 30 June 2016, 31 December 2016 or December 2017”. This is correct: the directors express their opinion as to the likelihood that the TLB lenders would demand immediate repayment of the secured debt and appoint a receiver and manager if the Asset Coverage Ratio is breached and, at ASIC’s request, added further information about the basis for that opinion. ASIC does not suggest that the directors’ opinion is unreasonable or imprudent. In the absence of such a suggestion, I did not understand the relevance of this observation.

26 Next ASIC argued that, by reason of the ongoing economic interest of Atlas’s shareholders, they should be able to vote on the scheme “in an appropriate manner on the basis of complete information so that they can make a fully informed decision”. ASIC set out legal principles which it contended were relevant to the Court’s exercise of its discretion at the first court hearing. It set out contentions concerning the need for an independent expert report addressing the fairness and reasonableness of the scheme for members, and expressed the view that the scheme should have been structured differently, so that it was conditional on the implementation of a member’s scheme. These are very substantial issues but I did not understand ASIC to be contending that the Court should refuse to make the orders sought by Atlas by reason of the matters that it raised. If that was its contention, I would have expected ASIC to appear at the first court hearing.

27 Finally, ASIC proposed steps that might be taken by Atlas to ensure that shareholders are treated fairly. These were:

(1) no Atlas board or management members or scheme creditors (if they own any Atlas shares) vote at the shareholders meeting;

(2) the scheme documentation and PPB reports and enclosures be included in the notice of general meeting as they contain material information relevant to shareholders;

(3) the notice of general meeting disclosure be improved with respect to how Atlas believes the scheme and thereby the shareholder dilution is in the best interests of shareholders; and

(4) there be an independent expert report which opines on whether the scheme is in the best interests of shareholders.

28 Atlas has agreed to take step (1), but has chosen not to take the other steps, although the scheme notice of general meeting contains the following statement:

1.5.3 Further information about the Financial Restructuring and Creditors’ Scheme

Further details regarding the Financial Restructuring, the Creditors’ Scheme and the implications for the Company are set out in Section 2, as well as the Schedules to this Notice. Further details are also included in the announcement released on ASX on 23 December 2015.

Shareholders are also encouraged to monitor the ASX company announcements platform and Atlas’ website for any announcements that are relevant to the Financial Restructuring made by the Company between the Last Practicable Date and the date of the Meeting. For example, the independent expert’s report being prepared by PPB Advisory for the purposes of the Creditors’ Scheme is expected to be made available on the ASX company announcements platform and Atlas’ website; however, Shareholders are reminded that such a report has been commissioned to consider only the interests of TLB Lenders and Subordinate Claim Holders.

These further announcements can be found on ASX’s website at www.asx.com.au (under ASX Code: AGO) and on the Company’s website at www.atlasiron.com.au. Shareholders may also request hard copies of any announcements made during this time and will be provided with such hard copies by the Company free of charge.

Relevant legal framework

Jurisdictional requirements

29 There are three stages to an application under s 411. First, the Court approves the convening of a scheme meeting and approves the scheme booklet. Secondly, members vote on the proposed scheme at the scheme meeting. Thirdly, the Court approves the proposed scheme: Re CSR Ltd [2010] FCAFC 34; (2010) 183 FCR 358 (“Re CSR”) at [7] per Keane CJ and Jacobson J; Re Amcom Telecommunications Ltd [2015] FCA 341 at [8] per McKerracher J; Re Central Pacific Minerals NL [2002] FCA 239 at [6] per Emmett J.

30 The following matters are required to be proved at the first court hearing (cf. Re Orion Telecommunications Ltd [2007] FCA 1389 at [5]):

(1) the plaintiff is a “Part 5.1 body”;

(2) the proposed scheme is an “arrangement” within the meaning of s 411 of the Act;

(3) the scheme booklet will provide proper disclosure to its addressees, in this case, the TLB lenders;

(4) the scheme is bona fide and properly proposed;

(5) ASIC has had reasonable opportunity to examine the proposed scheme and explanatory statement, to make submissions and has had 14 days’ notice of the proposed hearing date of the first court hearing; and

(6) any other procedural requirements have been met, such as rule 3.2 of the Federal Court (Corporations) Rules 2000 (Cth) as to the nomination of a chairperson for the scheme meeting.

Standard of review

31 The approach of the Court at the first court hearing is that “the court will not ordinarily summon a meeting unless the scheme is of such a nature and cast in such terms that, if it receives the statutory majority at the...meeting the court would be likely to approve it on the hearing of a petition which is unopposed”: per Street CJ (with whom Hutley and Samuels JJA agreed) in FT Eastment & Sons Pty Ltd v Metal Roof Decking Supplies Pty Ltd (1977) 3 ACLR 69 at 72 (“FT Eastment”). The High Court approved this observation in Australian Securities Commission v Marlborough Gold Mines Ltd [1993] HCA 15; (1993) 177 CLR 485 at 504. The FT Eastment approach has been consistently followed.

32 In Re Foundation Healthcare Ltd [2002] FCA 742; (2002) 42 ACSR 252 (“Foundation Healthcare”), French J (as he then was), said relevantly at [36] and [44]:

... Owen J has observed that the practice has developed that the Court, on a first stage application, closely scrutinises the scheme documents. If it be of the view that the scheme would be unlikely to receive approval, then the Court should not give leave to convene the meeting – Re Bond Corporation Holdings Ltd (1991) 5 ACSR 304 at 316 and see Re Stockbridge Ltd (1993) 11 ACLC 201 (Murray J). It is however important to bear in mind that, by granting leave to convene the meeting, the Court does not give its imprimatur to the proposed scheme. If the arrangement is one that seems fit for consideration by the meeting of members or creditors and is a commercial proposition likely to gain the Court’s approval if passed by the necessary majorities, then leave should be given – Re ACM Gold Ltd [1992] FCA 89; (1992) 10 ACLC 573 (O’Loughlin J). The Court is not required to give close consideration to the effects of the scheme upon individual members of the classes of members or creditors affected. So to do would be to “introduce burdensome and to a large extent ineffectual consideration at this interlocutory stage” – Re Jax Marine Pty Ltd (1967) 1 NSWR 145 at 148 (Street J).

…

The Court at the stage of ordering a meeting to approve a scheme does not ordinarily go very far into the question of whether the arrangement is one which warrants the approval of the Court – Re NRMA [Insurance Ltd (No 1) [2000] NSWSC 82; (2000) 156 FLR 349] at 605. That question is to be answered when the scheme returns to the Court for final approval. That is not to exclude the possibility that a scheme may appear on its face so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further. The Court is not required to be satisfied either at the convening or approval stage that no better scheme could have been devised...

33 In Re CSR at [58], Keane CJ and Jacobson J referred to the observations of French J in the passages set out above with apparent approval. See also Re Centro Properties Limited (2011) 87 ACSR 131 at [63]-[66] per Barrett J.

34 At the first court hearing, the Court exercises its supervisory jurisdiction to review the scheme and the explanatory statement and raise any queries with the plaintiff. In Re Crusader Ltd [1996] 1 Qd R 117; Thomas J said at 125 that “[t]he courts are concerned with the notion of a fair picture being presented” and went on to embrace the observations of the Full Federal Court in Fraser v NRMA Holdings Ltd (1995) 55 FCR 452 at 468:

If every possible formulation of the commercial objective of the proposal, and arguments for and against every theoretical possibility, were set forth the total package of information to members would be likely to confuse rather than illuminate the issue for decision, even for people having a familiarity with corporate law and commerce. The need to make full and fair disclosure must be tempered by the need to present a document that is intelligible to reasonable members of the class to whom it is directed, and is likely to assist rather than confuse.

35 The second court hearing is where the court makes its “final determination”, and is the most important hearing if the matter becomes contested, but in practice the first court hearing is where the court intervenes if it has any concerns. One reason for this is that (per Santow J in Re Archaean Gold NL (1997) 23 ACSR 143 at 147):

[C]ourt approval to convene the scheme meetings is viewed by the market as giving assurance that the scheme is at least in form and substance such as warranted receiving such preliminary court clearance. It must not be forgotten that trading thereafter takes place on that basis.

36 At both court hearings there is a duty of disclosure which falls on the plaintiff and its counsel, as set out in the dictum of Barrett J in Re Permanent Trustee Company Ltd [2002] NSWSC 1177; (2002) 43 ACSR 601 at [7]:

The fact that the application is ex parte is not without some significance. The absence of any defendant or contradictor sharpens the duty of the applicant. While a case such as the present is distinguishable from one where an interlocutory injunction is sought in the absence of a defendant (in that there is here no defendant as such) I think it is fair to say that an applicant in this kind of situation, like an applicant ex parte for an injunction, carries the responsibility of bringing to the court’s attention all matters that could be considered relevant to the exercise of discretion.

Part 5.1 body

37 The term “Part 5.1 body” is defined in s 9 of the Act to mean, relevantly, a company.

“Arrangement”

38 The term “arrangement” is of wide import. In Re NRMA Insurance Ltd (No 1) [2000] NSWSC 82; (2000) 156 FLR 349, Santow J said (at [20]):

Generally speaking, unless the arrangement is ultra vires the company or seeks to deal with a matter for which a special procedure is laid down by the Corporations Law or to evade a restriction imposed by the Corporations Law, almost any arrangement otherwise legal which touches or concerns the rights and obligations of the company or its members or creditors, and which is properly proposed, may come under s 411; compare Re International Harvester Co of Australia Pty Ltd [1953] VicLawRp 90; [1953] VLR 669 at 672 per Lowe ACJ.

39 An arrangement to which s 411(1) applies includes one between a company and its creditors or any class of them.

Subordinate claims

40 The scheme releases the claims of subordinate claimants within the meaning of s 563A(2) of the Act, except to the extent of the net proceeds of any policy of insurance that would respond to the subordinate claim. The effect of s 411(5A) is that, if the scheme is approved by the Court, those claimants are bound by the scheme despite the fact that they have not voted on it at a meeting convened under s 411(1).

41 Section 411(5A) was introduced into the Act by the Corporations Amendment (Sons of Gwalia) Act 2010 (Cth). The same legislation also introduced s 600H, which provides, relevantly, that a subordinate claimant within the meaning of s 563A is entitled to vote in their capacity as a creditor of the company at a meeting ordered under s 411(1) or during the external administration of the company only if the Court so orders. The term “external administration” is defined to include a compromise or arrangement under Part 5.1.

42 A November 2010 report of the Legal and Constitutional Affairs Legislation Committee of the Senate (“Senate Report”) records the following concerns expressed by the Law Council of Australia (“LCA”) at [3.57] and [3.58]:

The LCA also noted that the postponement of claims by proposed new section 563A “is confined to the context of winding up” a company meaning that the Bill does not adequately address situations where there is an attempt to formally reconstruct an insolvent company through a scheme of arrangement process. In particular, an insolvent company will be unable to use the scheme of arrangement to achieve an effective compromise with creditors and shareholders with “subordinate claims” as these claims will survive any reconstruction of the company.

[The LCA] explained further:

With this legislation clause 600H)(b) deprives [subordinated creditors] of their right to vote... The problem with a scheme of company arrangement, however, is that a scheme will only bind a class of creditor who has voted in relation to the scheme...the legislation as it is proposed effects a postponement of the subordinate claim; it does not extinguish them... that is the reason for the problem. You cannot reconstruct a company and come out clean on the other end if these subordinate claims survive the reconstruction, so there needs to be some mechanism to binding these claimants to the reconstruction...

43 The Senate Report continues at [3.63] and [3.64]:

… the Treasury clarified its view on the effect of the Bill with respect to schemes of arrangement, outlining two possible scenarios. In the first, the court grants subordinated shareholder compensation claimants leave to vote (for example where the court determines it is appropriate they should vote, in light of factors such as whether they have a financial interest in the company) and they are bound if the class of creditors collectively votes “yes”. In the second, the court does not grant subordinated shareholder compensation claimants leave to vote and consequently the scheme cannot bind them. The Treasury noted this second scenario will mean subordinated shareholder claimants “will effectively remain free to frustrate deals in relation to matters in which they have no demonstrated interest (or to use their ability to frustrate deals to extract from other stake holders a financial interest which they would not otherwise be entitled to)”.

44 At [3.65], the Senate Report records that the Treasury later provided the following additional information to the committee, noting that it had undertaken further discussions with the LCA regarding its concerns:

It is Treasury’s understanding that the LCA’s concerns may be addressed by amendments that would have the effect of providing that a Part 5.1 compromise or arrangement would be binding on creditors with subordinated claims who had not been given leave to vote, despite the fact that a meeting of that class of creditors had not been ordered by the Court under s 411(1).

45 It seems that the LCA’s concerns were addressed by the inclusion of s 411(5A) in Corporations Amendment (Sons of Gwalia) Bill 2010. The Supplementary Explanatory Memorandum to the Bill states, relevantly:

[1.13] In relation to compromises or arrangements under Pt 5.1 of the Corporations Act, section 411 provides that a creditors' scheme of arrangement is binding on a class of creditors only if a majority by number and more than 75 per cent by value of creditors in that class vote for the scheme. The Bill provides that in relation to a meeting convened under section 411(1) in relation to a compromise or arrangement under Part 5.1 of the Corporations Act, creditors subordinated under section 563A are only entitled to vote as creditors if they obtain leave of the Court. The Bill provides that creditors who are subordinated under section 563A are bound by the compromise or arrangement under Pt 5.1 of the Corporations Act, even if they do not obtain the leave of the Court under section 600H (as inserted by this Act) to vote at the creditors meeting convened by the Court under subsections 411 and 411(1A) of the Corporations Act. [Schedule 1, item 1A, section 411(5A)]

46 The significance of subordinate claimants’ financial interest in the company is highlighted in the Supplementary Explanatory Memorandum by clause [1.15] which states that, in determining whether to exercise its discretion under s 600H, a court might be expected to have regard to whether the person might reasonably be considered to possess “a real financial interest in the external administration”.

Consideration

Part 5.1 body

47 The evidence proves that Atlas, being a registered Australian public company, is a Part 5.1 body.

Proposed scheme is an “arrangement”

48 The text of the scheme (annexed to the scheme booklet) provides prima facie evidence that the proposed scheme is an “arrangement”.

49 The text of the scheme identifies the parties to the scheme as Atlas, the TLB lenders and the subordinate claim holders. The shareholders of Atlas are not parties to the proposed scheme.

50 As to the subordinate claim holders, the independent expert report states that they would receive a nil return on an external administration winding up. On that basis, at this stage of the application, there appears to be no objection to Atlas’ proposed use of s 411(5A) to propound a scheme that has the effect of releasing subordinate claimants’ claims against the company (except to the extent of any net insurance proceeds which might be available).

51 Further, as Atlas observed, there is a risk for the TLB lenders if they are not able to take the benefit of s 411(5A) because, if subordinate claims could be brought after the scheme is implemented in respect of matters which occurred before the implementation date, such claim holders would achieve a degree of priority over the TLB lenders (to the extent that secured debt is swapped for equity).

52 ASIC did not address the position of the subordinate claim holders in its 30 March 2016 letter.

53 In the absence of any appearance from ASIC to explain the submissions contained in its 30 March 2016 letter, I am not satisfied that the Court has power to assess for itself, at the first court hearing, whether shareholders should be permitted to express their view on the scheme to which they are not party because, for example, they are so materially and adversely prejudiced by the scheme that there should be a separate members’ scheme: cf Damian A and Rich A, Andrew, Schemes, Takeovers and Himalayan Peaks (3rd ed., University of Sydney Faculty of Law, 2013) [9.11.1]. If ASIC were of the view that the proposed scheme is so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further (to use the language of French J in Foundation Healthcare), then I would have expected ASIC to attend Court to say so. I infer that ASIC is not presently of this view.

54 I should record that, on the materials presented to me, and bearing in mind that the Court’s task did not require me to give close consideration to the effects of the scheme upon the shareholders, I did not form the view that shareholders would be prejudiced by the scheme. However, as Mr Sheahan SC for Atlas acknowledged, that is a matter which may be agitated at the second court hearing (after the shareholders meeting) as a matter relevant to the discretion whether to approve the scheme. ASIC also has other options which it may choose to pursue if it continues to be of the view that shareholders have not been provided with sufficient information for the shareholders meeting.

Scheme booklet will provide proper disclosure to TLB lenders

55 The factual information in the scheme booklet was verified by Mr Walsh’s 30 March 2016 affidavit. I am satisfied that there is prima facie evidence that the scheme booklet will provide proper disclosure to the TLB lenders.

56 I am not persuaded that the TLB lenders require either additional sensitivity analysis of the risk of a breach of the Asset Coverage Ratio, or an opinion from directors about the extent of improvement in iron ore prices that would allow Atlas to refinance or repay the TLB lenders. Both matters go to the inherently difficult question of evaluating the extent of the risk against which the scheme is proposed. There is no particular reason to think that this additional information would assist the TLB lenders to make a more reliable judgment about that risk.

Scheme is bona fide and properly proposed

57 The Restructuring Support Agreement provides prima facie evidence that Atlas has committed itself to propounding the scheme and that, accordingly, the scheme is bona fide and has been properly proposed.

58 In its submissions, Atlas noted that although the release of subordinate claims is not expressly mentioned in the Restructuring Support Agreement. It believes that the Restructuring Support Agreement was entered into on the basis of the company’s net asset position not being diminished by the need to meet any such claims and that, unless subordinate claims are released, the TLB lenders may require changes to the amended Syndicated Facility Agreement to protect them against any such claims, or may not agree to the scheme.

Notice to ASIC

59 There is evidence that ASIC has had a reasonable opportunity to examine the proposed scheme and explanatory statement, and to make submissions and it has had 14 days’ notice of the proposed hearing date of the first court hearing.

Other procedural requirements have been met

60 Consents to act as chairman and alternate chairman at the scheme meeting has been obtained.

61 The proposed scheme administrators are Messrs Ayres, Carter and Theobold, partners of PPB Advisory. I accept Atlas’ submission that this is a relatively minor future engagement which does not materially compromise the independence of the expert reports. The focus for this purpose is on independence from the company and the creditors affected by the scheme. The proposal to use PPB partners as scheme administrators is efficient for Atlas and has been fully disclosed in the scheme booklet. Atlas’ counsel noted that the same sequence of appointments seems to have occurred in the Nine/PBL scheme: Re Nine Entertainment Group Ltd (No 1) [2012] FCA 1464; (2012) 211 FCR 439 at [30].

Conclusion

62 I am satisfied that the jurisdictional requirements for the orders sought were met. The appropriate course is to make the orders sought on the basis that the proposed scheme is of such a nature and is cast in such terms that, if it were to receive the expected requisite statutory majority, the Court would be likely to approve the scheme on the hearing of an unopposed application.

Variation to form of notice of hearing to approve compromise or arrangement

63 The form of the notice, required to be published in The Australian newspaper, was originally addressed only to the TLB lenders and the subordinate claim holders. Having regard to the matters raised by ASIC, and acknowledging the disclosure obligations of Atlas to its shareholders, I consider that it is prudent to address the notice to the members of Atlas. Atlas consented to an order varying order 11 made on 31 March 2016 accordingly.

I certify that the preceding sixty-three (63) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: