FEDERAL COURT OF AUSTRALIA

Bamboo Direct Pty Limited (in liq), in the matter of Bamboo Direct Pty Limited (in liq) [2016] FCA 264

ORDERS

DATE OF ORDER: |

THE COURT DIRECTS THAT:

1. The second plaintiff would be justified in deciding that the first plaintiff holds the proceeds from the sale of Small-scale Technology Certificates (“STCs”) referred to as “Category 1 STCs” in the affidavit of the liquidator filed with the originating process in its own right and that the proceeds comprise part of the “property of the company” within the meaning of s 501 of the Corporations Act 2001 (Cth).

2. The second plaintiff, in his capacity as liquidator of the first plaintiff, would be justified in distributing the proceeds as “property of the company” within the meaning of s 501 in the winding up of the first plaintiff.

THE COURT ORDERS THAT:

3. The second plaintiff is entitled to recover his costs and expenses of this proceeding in the winding up of the first plaintiff.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GLEESON J:

Background

1 The first plaintiff (“Bamboo Direct”) is a company that, with related entities, was engaged in the business of purchasing and importing solar hot water heaters and solar panels in New South Wales. Bamboo Direct is the registered holder of the business name “RECS Direct”. As part of its business, Bamboo Direct was involved in the creation, sale and monitoring of “Small-Scale Technology Certificates (“STCs”).

2 STCs are created under and regulated by the Renewable Energy (Electricity) Act 2000 (Cth) (“Renewable Energy Act”).

3 On 23 December 2011, the second plaintiff (“Mr Morgan” or “liquidator”) was appointed as the administrator of Bamboo Direct pursuant to s 436A of the Corporations Act 2001 (Cth) (“Corporations Act”). On the same day, he was also appointed as the liquidator of three related entities, being Solar Installations (NSW) Pty Limited (“Solar Installations”), Solar & Bamboo Direct Tamworth Pty Limited (“Solar Tamworth”) and Solar & Bamboo Direct Coffs Harbour Pty Limited (“Solar Coffs Harbour”).

4 On 1 March 2012, Bamboo Direct executed a deed of company arrangement, of which Mr Morgan was the deed administrator. The deed of company arrangement was terminated pursuant to s 445C(c) of the Corporations Act and, through the operation of s 446B of that Act and reg 5.3A.07 of the Corporations Regulations 2001 (Cth), Bamboo Direct was taken to have passed a special resolution under s 491 of the Corporations Act that it be wound up.

5 On 11 July 2012, Mr Morgan was appointed as liquidator of Bamboo Direct.

Relief sought by the liquidator

6 This proceeding has been brought to determine how the liquidator of should deal with an amount of $739,428.73 held by Bamboo Direct, being the proceeds of sale of STCs.

7 The proceeding was commenced under s 511 of the Corporations Act and, to the extent necessary and appropriate, s 479(3) of that Act.

8 Section 511 provides relevantly:

(1) The liquidator … may apply to the Court:

(a) to determine any question arising in the winding up of a company; or

(b) to exercise all or any of the powers that the Court might exercise if the company were being wound up by the Court.

…

(2) The Court, if satisfied that the determination of the question or the exercise of power will be just and beneficial, may accede wholly or partially to any such application on such terms and conditions as it thinks fit or may make such other order on the application as it thinks just.

9 Section 479(3) provides that the liquidator may apply to the Court for directions in relation to any particular matter arising under the winding up.

10 In his originating process, the liquidator sought the following final relief:

(1) A declaration that Bamboo Direct holds the proceeds from the sale of STCs referred to as “Category 1 STCs” in the affidavit of the liquidator filed with the originating process in its own right and that the proceeds comprise part of the “property of the company” within the meaning of s 501 of the Corporations Act.

(2) A direction that Mr Morgan, in his capacity as liquidator of Bamboo Direct, would be justified in distributing the proceeds as “property of the company” within the meaning of s 501 in the winding up of Bamboo Direct.

(3) In the alternative to (1) above, a declaration that Bamboo Direct holds the proceeds on trust for the persons named in the schedule to the originating process.

(4) In the alternative to (2) above, a direction that the liquidator would be justified in distributing the proceeds to those persons named in the schedule to the originating process.

(5) An order that the liquidator is entitled to recover his costs and expenses in making the application in the winding up of Bamboo Direct.

(6) Such further or other orders as the Court deems appropriate.

11 Concerning the proposed alternative orders (3) and (4), the persons named in the schedule to the original process comprise 359 customers of Solar Installations, Solar Tamworth and Solar Coffs Harbour whom the liquidator has identified, from the books and records of Bamboo Direct, as persons who may not have been paid the proceeds from the sale of STCs that they had assigned to Bamboo Direct. Accordingly, they are persons who may have a claim over part of the proceeds of sale of the STCs (“potential claimant customers”).

12 At the hearing, the liquidator submitted that the Court should make orders and directions that:

(1) Bamboo Direct holds the proceeds from the sale of the STCs referred to as “Category 1 STCs” in the affidavit of Mr Morgan sworn on 27 July 2015 in its own right and that the proceeds comprise part of the “property of the company” within the meaning of s 501 of the Corporations Act .

(2) Mr Morgan in his capacity as liquidator of Bamboo Direct is justified in distributing the proceeds as “property of the company” within the meaning of s 501 of the Corporations Act in the winding up of Bamboo Direct.

(3) The liquidator is entitled to recover his costs and expenses in making this application in the winding up of Bamboo Direct.

Notification of Interested Parties

13 On 19 August 2015, I made orders for the purpose of giving notice of the proceeding to the 359 potential claimant customers, to give them an opportunity to be heard in the proceeding. In summary, the orders required the liquidator to send a copy of a notice explaining the proceeding to those customers for whom the liquidator had a postal or email address, and also required him to publish the notice in The Daily Telegraph and The Coffs Harbour Advocate newspapers. I am satisfied that the liquidator complied with the 19 August 2015 orders, and that all reasonable steps have been taken to bring the proceeding to the attention of the relevant customers of Solar Installations, Solar Tamworth and Solar Coffs Harbour.

14 When the matter was listed for case management on 22 September 2015, four potential claimant customers (including Mr Carroll) were represented at the bar table by two separate practitioners, and a further six were in attendance at the Court. A solicitor from Legal Aid NSW represented Mr Carroll informed the Court that Legal Aid wished to take steps to contact the remainder of the 359 possible participants, with a view to determining their interest in the proceeding. The proceedings were stood over for two months to allow Legal Aid to do this.

15 When the matter was listed for case management on 26 November 2015, four potential claimant customers were represented (including, again, Mr Carroll). There was no suggestion from Legal Aid that more time was required to contact further potential claimant customers. The matter was set down for hearing in February 2016.

Parties granted leave to appear

16 Two parties were granted leave to be heard in the proceeding, without becoming a party to the proceeding, pursuant to r 2.13 of the Federal Court (Corporations) Rules 2000 (Cth). They were the ANZ Banking Group Ltd (“ANZ”), a secured creditor of Bamboo Direct and Mr Carroll, the potential claimant customer mentioned above. Each of ANZ and Mr Carroll were represented by counsel who made oral and written submissions.

17 As at 11 November 2014, ANZ claimed that it was owed $537,234.34 by Bamboo Direct. ANZ submitted that the Court should make the orders proposed by the liquidator.

18 On behalf of Mr Carroll, Mr Brender of counsel submitted that his STCs would be worth about $5,738.17, and that the liquidator holds this amount on Mr Carroll’s behalf. On behalf of Mr Carroll, it was submitted that the Court should make proposed orders (3) and (4) in the originating process.

Australian Commonwealth Government’s Small-scale Renewable Energy Scheme

19 The Small-scale Renewable Energy Scheme is managed by the Clean Energy Regulator pursuant to the Renewable Energy Act. Prior to April 2012, the functions of the Clean Energy Regulator were managed by the Office of the Renewable Energy Regulator (“ORER”).

20 Under the scheme, customers who engaged Solar Installations, Solar Tamworth or Solar Coffs Harbour to install certain hot water heaters and solar panels were eligible to create STCs. This eligibility arose from Pt 2 Div 4 of the Renewable Energy Act. Subdivision B of Div 4 concerns STCs for solar water heaters. Subdivision BA of Pt 2 Div 4 concerns STCs for small generation units. A small generation unit means a device that generates electricity that is specified by the regulations to be a small generation unit.

21 Section 20B provides that certificates created under Subdiv B of Pt 2 Div 4 of the Renewable Energy Act are STCs. Section 23AB provides that certificates created under Subdiv BA of Pt 2 Div 4 are STCs.

22 Sections 21 and 23A concern when an STC may be created. Section 21 provides:

(1) If a solar water heater is installed on or after 1 April 2001, certificates may be created after the heater is installed.

Note: For offences and civil penalties related to the creation of certificates, see Subdivision C.

(1A) The regulations:

(a) may provide that certificates cannot be created in relation to a solar water heater unless particular conditions are satisfied in relation to the solar water heater or its installation; and

(b) without limiting paragraph (a), may:

(i) require information or documents to be given to the Regulator in relation to a solar water heater or its installation; and

(ii) provide that information or documents required to be given to the Regulator must be verified by statutory declaration.

(2) The certificates may only be created within 12 months after the installation of the solar water heater.

(3) The regulations may make provision in relation to the time at which a solar water heater is taken to have been installed.

(4) If a solar water heater is an air source heat pump water heater, certificates may only be created for the installation of such an air source heat pump water heater if it has a volumetric capacity of not more than 425 litres.

23 Section 23A provides:

(1) If a small generation unit is installed on or after 1 April 2001, certificates may be created after the small generation unit is installed.

Note: For offences and civil penalties related to the creation of certificates, see Subdivision C.

(1A) The regulations:

(a) may provide that certificates cannot be created in relation to a small generation unit unless particular conditions are satisfied in relation to the small generation unit or its installation; and

(b) without limiting paragraph (a), may:

(i) require information or documents to be given to the Regulator in relation to a small generation unit or its installation; and

(ii) provide that information or documents required to be given to the Regulator must be verified by statutory declaration.

(1B) To avoid doubt, regulations under subsection (1A) may impose conditions to be complied with in relation to a small generation unit after its installation.

Note: For example, conditions may be imposed so that certificates cannot be created in relation to a small generation unit unless the unit remains functional.

(2) The regulations may make provision in relation to the time at which a small generation unit is taken to have been installed.

(3) The regulations may make provision in relation to:

(a) the time when a right to create certificates in relation to a small generation unit arises; and

(b) the period within which certificates may be created in relation to a small generation unit.

24 Sections 23 and 23C concern who may create an STC. Section 23 provides:

(1) The owner of the solar water heater at the time that it is installed is entitled to create the certificate or certificates that relate to the solar water heater.

(2) However, the owner may, by written notice, assign the right to create the certificate or certificates to another person. If the owner does this, the owner is not entitled to create the certificate or certificates but the person to whom the right was assigned is entitled to create the certificate or certificates.

(3) Despite subsections (1) and (2), a person who is not registered may not create a certificate that relates to the solar water heater.

25 Section 23C provides:

(1) The owner of the small generation unit at the time that a right to create a certificate or certificates arises in relation to the small generation unit is entitled to create the certificate or certificates.

(2) However, the owner may, by written notice and in accordance with the regulations, assign the right to create the certificate or certificates to another person. If the owner does this, the owner is not entitled to create the certificate or certificates but the person to whom the right was assigned is entitled to create the certificate or certificates.

(3) Despite subsections (1) and (2), a person who is not registered may not create a certificate that relates to the small generation unit.

(4) Regulations made for the purposes of subsection (2) may make provision:

(a) in relation to when the right may be assigned; and

(b) in relation to the kind of persons to whom the right may be assigned.

(5) Subsection (4) does not limit the regulations that may be made for the purposes of subsection (2).

26 Bamboo Direct was registered pursuant to Div 2 of Pt 2 of the Renewable Energy Act. None of Solar Installations, Solar Tamworth and Solar Coffs Harbour was registered.

27 Regulation 19 of the Renewable Energy (Electricity) Regulations 2001 (Cth) (“Renewable Energy Regulations”) provides, relevantly:

(1) For subsection 21(3) of the Act, the time at which a solar water heater is taken to have been installed is the day the heater is first able to produce and deliver hot water heated by solar energy, if this happens no more than 60 days from the start of installation of any component of the heater.

(2) To avoid doubt, a solar water heater is taken to have been installed once only during the life of the unit.

Note: Subsection 2(2) of the Act provides that certificates may be created only within 12 months after the installation of the solar water heater.

28 Regulation 19D provides:

(1) For subsection 23A(2) of the Act, the time at which a small generation unit is taken to have been installed is the day the unit is first able to produce and deliver electricity.

(2) For subsection 23A(3) of the Act, a right to create certificates for a small generation unit arises:

…

(d) if:

(i) the unit is a solar (photovoltaic) system; and

(ii) no certificate has been created for the unit under paragraph (a), (b) or (c);

for a unit installed during a year mentioned in column 1 of the following table within 12 months of installation and for the period mentioned in column 2 for the item.

…

(3) Where a right to create certificates has been exercised under the period specified for the unit in paragraph (2)(d), no additional right to create certificates arises.

29 Regulation 20A of the Renewable Energy Regulations provides:

Assignment of small generation unit certificates (Act s 23C)

For subsection 23C(2) of the Act, a right to create a certificate for a small generation unit under regulation 19D may be assigned for a 1-, 5- or 15-year period.

30 STCs are registered in the Australian Government’s Renewable Energy Certificate Registry (“REC Registry”). The REC Registry is an online system that allows for the creation, registration, transfer and surrender of STCs.

Liquidator’s examination of Bamboo Direct’s books and records

31 The liquidator has deposed that Bamboo Direct’s books and records that relate to the creation and assignment of STCs are not well maintained and are, in many cases, incomplete. Having reviewed the books and records and from his investigations into its affairs, the liquidator came to understand that Bamboo Direct adopted the following procedures in relation to STCs:

(a) in the process of contracting with Solar Installations, Solar Tamworth or Solar Coffs Harbour for the sale and installation of solar hot water heaters and solar panels, customers executed documents that assigned the customer’s right to create STCs to Bamboo Direct (“assignment forms”) pursuant to s 23(2) and s 23C(2) of the Renewable Energy Act. The assignment forms were based upon a template assignment form distributed by the ORER;

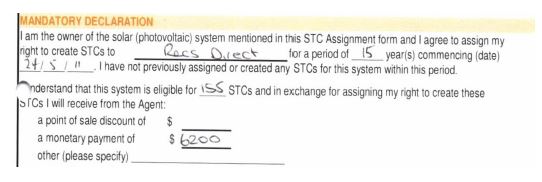

(b) Bamboo Direct (trading as RECS Direct) also provided certain customers with a document headed “STC Assignment Form for Solar Photovoltaic Systems” for the purpose of assigning a customer’s right to create STCs to Bamboo Direct (“Solar Electricity System assignment form”), following the installation of solar panels provided by Bamboo Direct;

(c) Bamboo Direct (trading as RECS Direct) also provided certain customers with a document headed “Renewable Energy Certificate Assignment Form for Solar Hot Water” for the purpose of assigning a customer’s right to create STCs to Bamboo Direct (“Solar Hot Water System Assignment Form”), following the installation of a solar hot water system provided by Bamboo Direct;

(d) Bamboo Direct would either provide a point of sale discount off the price of the relevant solar panel or hot water system, or alternatively agree to subsequently pay the customer an amount of money;

(e) in its customer information and documentation files, Bamboo Direct used the term “Renewable Energy Certificates” (or “RECs”) interchangeably with “Small-Scale Technology Certificates” (or “STCs”), consistent with industry practice at that time.

32 The liquidator has identified certain common errors and omissions that were made in the documentation executed by Bamboo Direct’s customers:

(a) the right to create STCs was assigned by the customer to one of Bamboo Direct’s related entities, rather than Bamboo Direct;

(b) where the customer was more than one individual person (usually a married or de facto couple), only one customer had signed the relevant assignment form; and

(c) assignment forms had not been completed correctly, or insufficient information was provided in the forms.

ORER audit and sale of “Category 1 STCs”

33 In early to mid-2012, the ORER conducted an audit of the documents held by Bamboo Direct concerning the STCs that had been registered in Bamboo Direct’s REC Registry account. As part of the audit, officers of the ORER attended at the offices of Bamboo Direct.

34 The outcome of the ORER’s audit was set out in a table supplied by the ORER to the liquidator. The ORER audit determined in particular that several thousand STCs had been improperly created or assigned. This appears to have arisen as a result of a number of assignment forms having been incorrectly completed or having been signed prior to the systems being eligible for STCs (i.e. prior to the systems being installed).

35 Following the ORER’s audit, the liquidator undertook to transfer certain STCs to customers, and in doing so surrendered a significant portion of the STCs previously held by Bamboo Direct.

36 In relation to 25,838 of the STCs, the ORER audit determined that these STCs had been both correctly created under the Renewable Energy Act and correctly assigned to Bamboo Direct. In his affidavit of 27 July 2015, the liquidator has described these STCs as “Category 1 STCs”. Following the ORER’s determination in relation to the Category 1 STCs, the liquidator sought to sell the STCs throughout the course of 2013. The sale process resulted in sale proceeds of $956,534.50.

37 There is currently $739,428.73 that is held by the liquidator as a result of the realisation process, being the net proceeds from the sale of the Category 1 STCs. In the ordinary course, the liquidator would make priority payments pursuant to s 556 of the Corporations Act and would pay ANZ (being the secured creditor) in part or in full. Assuming that the $739,428.73 is the property of Bamboo Direct, the liquidator’s view is that it is unlikely that any funds will be available to pay a distribution to Bamboo Direct’s unsecured creditors.

38 The potential claimant customers are the persons whom the liquidator identified as persons who may have an interest in proceeds from the sale of the Category 1 STCs that they had assigned to Bamboo Direct. The liquidator deposes in relation to these persons that:

Bamboo’s books and records record details of the realised STCs together with the corresponding customer that the STC relates to. However, the books and records do not sufficiently record whether sale proceeds have previously been remitted to the customer. Consequently, some of the Potential Claimant Customers may in fact have already been paid by Bamboo.

39 To the extent that the potential claimant customers have not been paid by Bamboo Direct, if there is a trust (or trusts) over the proceeds of sale of the STCs, then the customers have equitable rights as beneficiaries of the trust (or trusts) which can be asserted against the trust fund. On the other hand, if there is no trust, then the customers are unsecured creditors of the company to the extent that they have not been paid for the assignment of the STCs to Bamboo Direct.

Power to make substantive orders affecting third parties

40 In Meadow Springs Fairway Resort Ltd (in liq) v Balanced Securities Ltd [2007] FCA 1443; (2007) 25 ACLC 1433, French J held that it was a matter of discretion whether the Court should determine competing claims in an application brought by a liquidator under s 511(1). His Honour referred to Australian Securities Commission v Melbourne Asset Management Nominees (1994) 49 FCR 334 where Northrop J said in relation to s 479(3):

It has been accepted that Courts have power to make final orders in preference claims on an application by a liquidator under sections similar to s 479(3) of the Corporations Law. There is no logical reason why final orders binding on other persons cannot be made on applications under s 479(3) with respect to other subject matters. The second passage from the judgment of McLelland J cited above [Re G B Nathan & Co Pty Ltd (in liq) (1991) 24 NSWLR 674] refers to consent of parties or to cases where a party “will not suffer injustice in consequence of the alteration to the status of the proceedings”. This is the crucial matter. In proceedings brought by a liquidator under s 479(3), I can see no reason why binding orders cannot be made where the parties affected have been given the opportunity to be heard … The parties affected by the directions and orders sought on the motion in the winding up proceedings are before the Court and have been heard.

In my opinion it is open to the Court, in a suitable case, to entertain an application for the determination of questions under s 511 by joining affected parties with competing interests as defendants and permitting them to file cross-claims for declaratory relief as between themselves and any other interested parties and the liquidator so that there can be a res judicata between all of them. Such a course may be appropriate where the evidence necessary to determine the questions and the competing claims is largely documentary and amenable to expeditious hearing and determination. Otherwise the parties can simply commence their own substantive proceedings.

42 In Re Willmott Forests (No 2) [2012] VSC 125; (2012) 88 ASCR 18, Davies J noted (at [46]) that the limitation on the power under s 511(1) is that, by s 511(2), the court is only to accede to the liquidator’s application if the determination of the question or exercise of power “will be just and beneficial”.

43 In Re Enviro Friendly Products Pty Ltd (in liq) [2013] FCA 852, Foster J made a direction to the effect that the liquidators would be justified in deciding that the company held certain STCs on trust for certain named persons and that the company held other STCs in its own right.

44 In Bastion v Gideon Investments Pty Ltd [2000] NSWSC 939; (2000) ACSR 466, the Court held that it was appropriate, on the evidence, to direct that a trust be recognised by the liquidator on terms of the draft trust deed and that certain persons be recognised as beneficiaries.

45 These cases support a conclusion that how a liquidator should treat particular property held (whether as trust property or otherwise) is an issue that is appropriate for directions under these provisions. Without joinder of affected parties, however, I am not convinced that it is appropriate to grant declaratory relief.

Company property or trust property

46 Pursuant to s 501 of the Corporations Act, the property of a company must, on its winding up, be applied in satisfaction of its liabilities equally. “Property” is defined in s 9 to comprise “any legal or equitable estate or interest (whether present or future and whether vested or contingent) in real or personal property of any description and includes a thing in action”. Property will accordingly embrace all kinds of choses in action.

47 The Corporations Act does not specify what assets held by the company being wound up are exempt from the liquidator’s control, however, under general law, property held in trust by the company for another is exempt, including property of the company in which another person has an equitable interest, as the company is not the beneficial owner of the property: Michael Murray and Jason Harris, Keay’s Insolvency (Thomson Reuters, 8th ed, 2014) 402.

48 On behalf of the liquidator, the following submissions were made in support of a conclusion that the proceeds from their sale of the STCs is property of Bamboo Direct:

(1) while the books and records of Bamboo Direct are in some disarray and the relevant assignment documents are inelegantly drafted, it is sufficiently clear that what occurred was a valid assignment of the various STCs to Bamboo Direct;

(2) sections 23(2) and 23C(2) of the Renewable Energy Act provide that an owner may “by written notice” assign the right to create the certificate to another person;

(3) ORER, through its audit, satisfied itself that the “Category 1 STCs” had been validly assigned to Bamboo Direct;

(4) the assignment documents used by Bamboo Direct appear to have been based upon the template or pro-forma document issued by the Clean Energy Regulator;

(5) taking the assignment document used by Mr Carroll:

(a) the document is headed on each page “STC Assignment Form for Solar Photovoltaic System”;

(b) the document has been completed and signed by Mr Carroll (being the assignor);

(c) the document provided under the heading “Mandatory Declaration”:

(6) the reference to “Recs Direct” is a reference to the trading name of Bamboo Direct;

(7) no particular form of words need be used for an assignment provided that they express a final and settled intention to transfer the property: Re Williams [1971] 1 Ch 1. There must also be an intention to assign, that is, to transfer the property in the chose in action from the assignor to the assignee: Evans v National Provincial Bank of England (1897) 13 TLR 429. The intention must be manifested and will be construed objectively: Shah v Shah [2010] EWCA Civ 1408;

(8) in terms of formal requirements for a legal assignment in New South Wales, s 12 of the Conveyancing Act 1919 (NSW) requires that for an absolute assignment to occur, it must be done in writing by the assignor and with notice;

(9) the assignment document (including the declaration) evidences an unequivocal expression of intention to immediately assign, and the document must be taken to be an effective absolute legal assignment within the meaning of s 12;

(10) the declaration’s reference to Mr Carroll’s understanding that he will receive certain consideration “in exchange for assigning” can have no impact or bearing upon the assignment that is otherwise effected by the document. This approach is consistent with an ordinary and common sense reading of the document. The first sentence of the declaration must be taken to have effected the assignment;

(11) if it is the case that Mr Carroll (or any other potential claimant customer) did not receive what was understood to be the “point of sale discount” or “monetary payment”, such a circumstance can only give rise to a personal breach of contract claim against Bamboo Direct sounding in damages, which in Mr Carroll’s case would amount to $6,200 (being what was understood to be the monetary payment to be received). Having arisen before the relevant date for the purpose of the winding up of Bamboo Direct, the claim would be one that is “admissible to proof against the company” within the meaning of s 553 of the Corporations Act;

(12) it would not be correct to characterise the proceeds realised from the sold STCs and held by the liquidator as being somehow trust property over which certain potential claimant customers have some kind of proprietary interest. The fact is that the potential claimant customers, by the assignment documents, validly assigned their “right to create STCs” to Bamboo Direct and accordingly, no proprietary interest can be said to have arisen.

Submissions on Behalf of Mr Carroll

Trust as a matter of objective intention

49 Mr Brender’s starting proposition was that an express trust may be created by any language which shows a sufficiently clear intention: Lord v Australian Elizabethan Theatre Trust (1991) 30 FCR 491 at 502; 102 ALR 681; Associated Alloys Pty Limited v ACN 001 452 106 [2000] HCA 25; 202 CLR 588. On Mr Carroll’s behalf, it was submitted that the documents, considered in the statutory context, demonstrate that:

…the “rebate” was objectively part of a single transaction and the contract was entered with the apparent intention that the right to create the STCs would be assigned, the STCs sold and the proceeds remitted to the customer, not mixed with the general funds of the company.

50 Mr Brender submitted that, because he was not registered under the Renewable Energy Act, the assignment of the right to create the relevant STCs was a necessary intermediate step to give Mr Carroll the benefit of the bargain. I accept this submission.

51 Next, it was submitted that the tax invoice issued to Mr Carroll demonstrates that the contract was entered with the (objective or imputed) mutual intention that a fundamental part of it was that the right to create the certificates arising from the installation would be assigned, the certificates created, sold and the proceeds “paid to customer”. This submission was based on the following words in the invoice, which is dated 11 May 2011, under the heading “description”:

155 [STCs] assigned to Solar Systems as at 1/1/2011 [sic]. STCs at $40 inc GST = value of $6200.00 SUBJECT TO CHANGE WITH MARKET VALUE. Paid to customer approx. 90+ days after install.

52 Mr Brender submitted that the assignment of the right to create the STCs was “for an express purpose – to create, sell and pay the…proceeds of the sale”. This conclusion was said to be reinforced by the consideration that the “rebate” constituted by the proceeds of the sale of the certificates almost equalled 60% of the purchase price, including installation. It was argued that the liquidator held the STCs for a purpose and only because the company had agreed with Mr Carroll to create them, sell them and remit the proceeds to Mr Carroll.

53 In Coolbrew Pty Ltd v Westpac Banking Corporation [2014] NSWSC 1108, Darke J said, concerning the question whether there is an intention to create a trust:

[52] It is now clear that in deciding whether there is an intention to create a trust, the court ascertains that intention by inference from the outward manifestations of intention. The task of ascertaining an intention to create a trust and, if so, on what terms, is similar to the task of ascertaining the intention of parties to a contract: (see Raulfs v Fishy Bite Pty Ltd; Fishy Bite Pty Ltd v Raulfs (supra) at [48] per Campbell JA where his Honour cited the decision of the High Court in Byrnes v Kendle (supra) at [53]-[59] per Gummow and Hayne JJ and [102]-[115] per Hayden and Crennan JJ). The focus of the enquiry is upon objective indications of intention, not subjective intentions which may have existed but are not apparent from what was said and done (see Byrnes v Kendle (supra) at [113]-[115] per Heydon and Crennan JJ).

[53] As stated by Campbell JA in Raulfs v Fishy Bite Pty Ltd; Fishy Bite Pty Ltd v Raulfs (supra) at [51], it is necessary to analyse the particular factual situation presented for the purpose of deciding whether there is an intention to create a trust, and, if so, on what terms.

54 At [57], Darke J found that the mere fact that money was provided to a company for a specific purpose is not sufficient to establish a resultant trust; what is also required is evidence that the parties intended that the beneficial interest in the relevant property would at all times remain the property of the transferor and not become the property of the transferee. Darke J’s decision was affirmed on appeal: Coolbrew Pty Ltd v Westpac Banking Corporation [2015] NSWCA 135.

55 I do not accept Mr Brender’s submissions for the following reasons:

(1) Contrary to what was submitted, the assignment is expressed in language to the effect that it was made for the express purpose of obtaining a right to $6,200. There is no language to the effect that the assignment was made for the purpose of obtaining a right to the proceeds of the sale of the STCs (which might be more or less than $6,200);

(2) The documents do not refer to the payment or remittal of the “proceeds” of the sale of the STCs to Mr Carroll. The declaration refers to receipt of a “monetary payment” of $6,200. The tax invoice does not clearly specify what amount would be paid to Mr Carroll in respect of the STCs, but to the extent that it specifies a value of $6,200 (being 155 STCs at $40 each), that is not consistent with the remittal of the proceeds of sale where the invoice also says that the value of the STCs is “subject to change with market value”;

(3) There is no evidence to suggest an agreement that the proceeds of sale of the STCs would not be mixed with the general funds of the company;

(4) There is nothing in the documents which refers to the parties’ relationship as one of trustee and beneficiary.

Trust arising as a result of invalid assignment.

56 The premise for this contention, which is inconsistent with the submission referred to in para 50 above, is that there was no valid assignment of the right to create STCs. If this premise is correct, then the rights continue to be held by Mr Carroll and he has no basis to argue for any interest in the proceeds of sale received by Bamboo Direct.

57 On behalf of Mr Carroll, it was suggested that his rights to create STCs were converted by Bamboo Direct. The remedy for conversion of the proceeds of property said to have been paid for (and beneficially owned by) Mr Carroll, namely the right to create STCs, is the imposition of a resulting or constructive trust.

58 Mr Carroll’s counsel did not point to authority in support of the proposition that the right to create an STC is capable of being the subject matter of the tort of conversion: cf R v Hansford (1974) 8 SASR 164.

59 In any event, as stated above, I am satisfied that there was a valid assignment by Mr Carroll of his right to create STCs.

60 Mr Brender put two arguments to the contrary.

61 The first argument was that the assignment was not an “absolute” assignment but only a limited assignment for a period of 15 years. When asked to identify what interest in the relevant rights was not assigned, Mr Brender referred to the possibility that Mr Carroll actually assigned a right to generate the certificates for a period of 15 years, allowing the assignee to get “15 years’ worth of benefit from the certificates”, after which time any residual right would revert if they had not been sold. In my view, this response confirms the true position which is that there was an absolute assignment of Mr Carroll’s rights to create STCs, except to the extent that he might have some rights to create STCs which might arise after a period of 15 years.

62 As it turns out, when the statutory framework is considered, it is plain that there is no possibility of rights that might arise after 15 years because, by reg 19D of the Renewable Energy Regulations, the right to create the relevant STCs arose “within” 12 months of installation.

63 It is unnecessary to address Mr Brender’s second argument, which depends upon the assumption that the assignment is only valid, if at all, in equity.

Conclusion

64 I am satisfied that the proceeds of sale of the “Category 1 STCs” are the property of the company. I will make directions accordingly.

I certify that the preceding sixty-four (64) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: