FEDERAL COURT OF AUSTRALIA

Lifeplan Australia Friendly Society Ltd v Woff [2016] FCA 248

Table of Corrections | |

29 March 2016 | In paragraph 2, third sentence, the word “the” has been deleted before the words “duties of confidence”. |

29 March 2016 | In paragraph 33, the word “not” has been deleted between the words “was” and “something”. |

29 March 2016 | In paragraph 40, the word “the” has been deleted between the words “of” and “Lifeplan’s”. |

29 March 2016 | In paragraph 79, the words “on line” has been replaced with “on-line”. |

29 March 2016 | In paragraph 85, the word “licence” has been replaced with “Licence”. |

29 March 2016 | In paragraph 236, the words “Mr Hughes” between the words “to” and “of” has been replaced with “him”. |

29 March 2016 | In paragraph 283, the word “the” has been inserted between the words “in” and “sales”. |

29 March 2016 | In paragraph 318, the word “the” has been deleted between the words “in” and “FPA’s”. |

29 March 2016 | In paragraph 405, the word “of” has been deleted between the words “and” and “his”. |

29 March 2016 | In paragraph 472, the word “the” has been inserted between the words “was” and “cost”. |

29 March 2016 | In paragraph 484, the word “to” has been deleted after the word “Annexure B”. |

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The applicants file and serve within seven days draft minutes of order reflecting the conclusions expressed in these reasons and containing any other orders they seek.

2. The proceeding be adjourned to a date to be fixed for the making of final orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[21] | |

[27] | |

[63] | |

[68] | |

[69] | |

[84] | |

[93] | |

[112] | |

[144] | |

[194] | |

[214] | |

[227] | |

Failure to disclose a business opportunity to the applicants | [229] |

[230] | |

Taking other confidential and/or valuable business intelligence | [247] |

Steps towards establishing a new business whilst still employed by Lifeplan | [250] |

[261] | |

Melbourne Mailing and the applicants’ list of funeral directors | [267] |

[282] | |

[283] | |

Involvement of Foresters in the conduct of Mr Woff and Mr Corby | [293] |

[327] | |

[327] | |

[377] | |

[382] | |

[386] | |

[390] | |

Failure to disclose a business opportunity to the applicants | [393] |

[396] | |

Taking other confidential and/or valuable business intelligence | [398] |

Steps towards establishing a new business whilst still employed by Lifeplan | [400] |

[403] | |

Melbourne Mailing and the applicants’ list of funeral directors | [405] |

[407] | |

[414] | |

[414] | |

[422] | |

[442] | |

The applicants’ claim for an account of profits against Mr Woff and Mr Corby | [446] |

[448] | |

The value of the Foresters Funeral Fund and the expert evidence | [449] |

[482] | |

Appendix A | |

Appendix B |

BESANKO J:

1 This proceeding involves claims made by Lifeplan Australia Friendly Society Ltd (“Lifeplan”) and Funeral Plan Management Pty Ltd (“FPM”) for declarations, an injunction, an order for delivery up of documents and an account of profits against Noel Geoffrey Woff, Richard Corby, Funeral Planning Australia Pty Ltd (in liquidation) (“FPA”) and the Ancient Order of Foresters in Victoria Friendly Society Limited (“Foresters”). The events which are said to give rise to the applicants’ claims took place in 2010 and 2011. In 2010, Mr Woff and Mr Corby were employees of Lifeplan. In late 2010, they left the employ of Lifeplan and became employees of Foresters. Shortly prior to the cessation of their employment with Lifeplan, they established FPA. They were the two directors and two shareholders of the company. On 31 December 2010, FPA entered into an agreement with Foresters whereby it agreed to provide promotional and marketing services to Foresters in return for the payment of a commission. The promotional and marketing services related to an investment product issued by Foresters known as funeral bonds. Lifeplan also issued funeral bonds.

2 The applicants’ case is that Mr Woff and Mr Corby acted in breach of the duties they owed to them and they identify those duties as fiduciary duties, duties of confidence and contractual duties. The applicants also allege that, in the case of Mr Woff, he contravened sections of the Corporations Act 2001 (Cth) dealing with the duties of officers and employees of a corporation. Foresters is a third party to the breaches and is said by the applicants to be liable for knowingly assisting the breaches by Mr Woff and Mr Corby of their fiduciary duties and duties of confidence, and for inducing them to breach their contracts of employment. Foresters is also said to have been involved in Mr Woff’s contraventions of the Corporations Act. The applicants also make a claim for passing off against Mr Woff, Mr Corby and Foresters. Finally, the applicants claim that Foresters is vicariously liable with respect to some of the equitable “wrongdoing” of Mr Woff and Mr Corby.

3 FPA traded for approximately two and-a-half years, commencing in early 2011. On 12 June 2013, it was wound up in insolvency by order of the Supreme Court of Victoria. I have granted the applicants leave to proceed against it under s 471B of the Corporations Act up to the entry of judgment (Lifeplan Australia Friendly Society Ltd v Woff [2013] FCA 1092). FPA has taken no effective part in the proceeding since I granted leave and it did not appear at the trial. The limited relief the applicants seek against FPA is described below.

4 During closing submissions, the applicants identified the orders they seek against the respondents. They seek declarations dealing with the alleged breaches by Mr Woff and Mr Corby, and the involvement of Foresters. The declarations they seek are as follows:

1. Noel Jeffrey Woff and Richard John Corby between July 2010 and the present date breached duties and obligations owed by each of them to Lifeplan Australia Friendly Society Ltd and to Funeral Plan Management Pty Ltd:

a. as a fiduciary of each of those companies;

b. pursuant to duties and obligations of confidence which each of them owed to each of those companies;

c. pursuant to each of their contracts of employment (employment contract) with Lifeplan Australia Friendly Society Ltd;

d. pursuant to Confidentiality and Intellectual Property Declarations which each of them signed with those companies; and

e. pursuant to the Information Technology Declaration which each of them signed with those companies.

2. Ancient Order of Foresters Friendly Society in Victoria Ltd:

a. induced Noel Jeffrey Woff and Richard John Corby to breach their employment contracts;

b. knowingly assisted Noel Jeffrey Woff and Richard John Corby to breach their fiduciary duties and obligations of confidentiality.

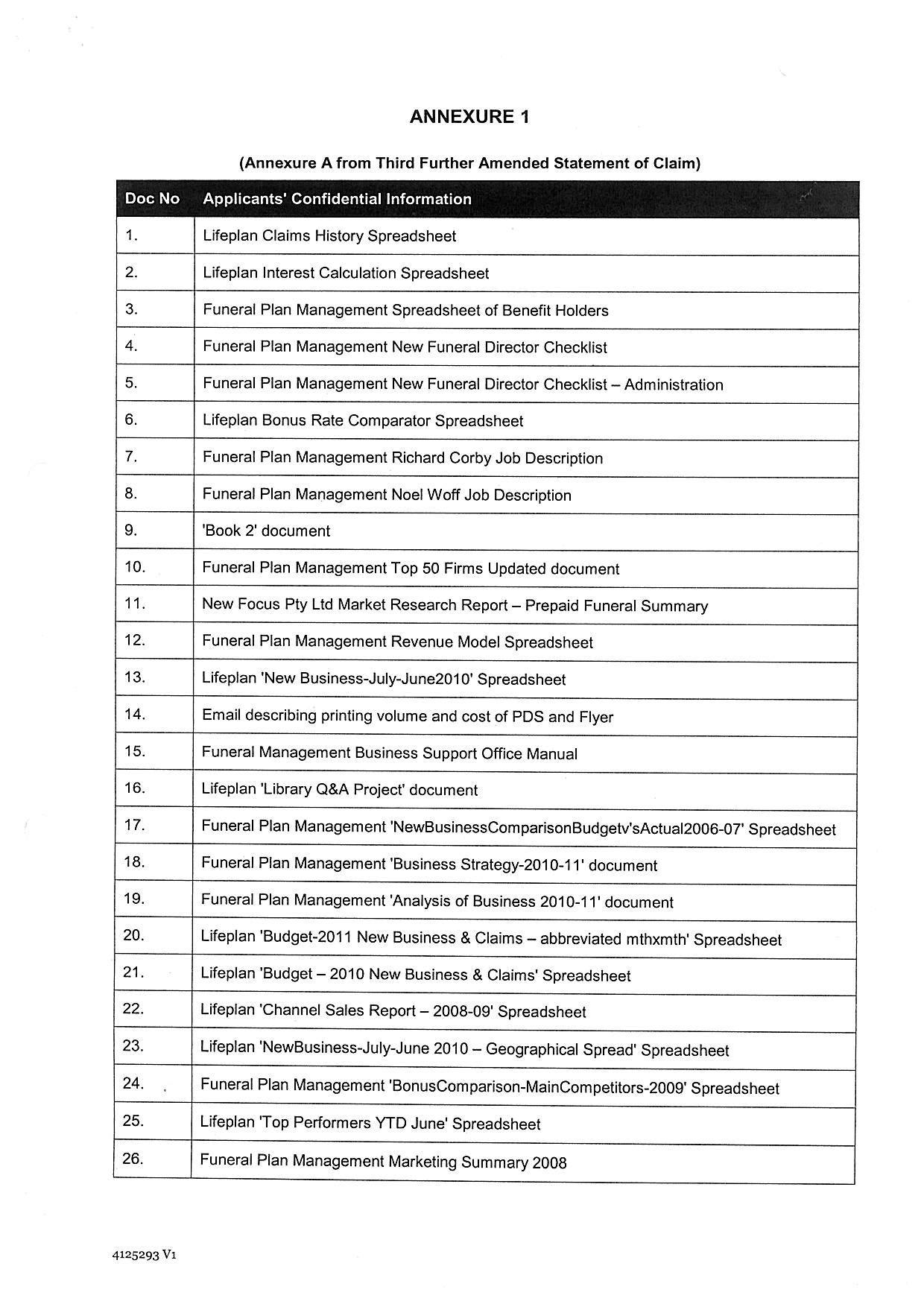

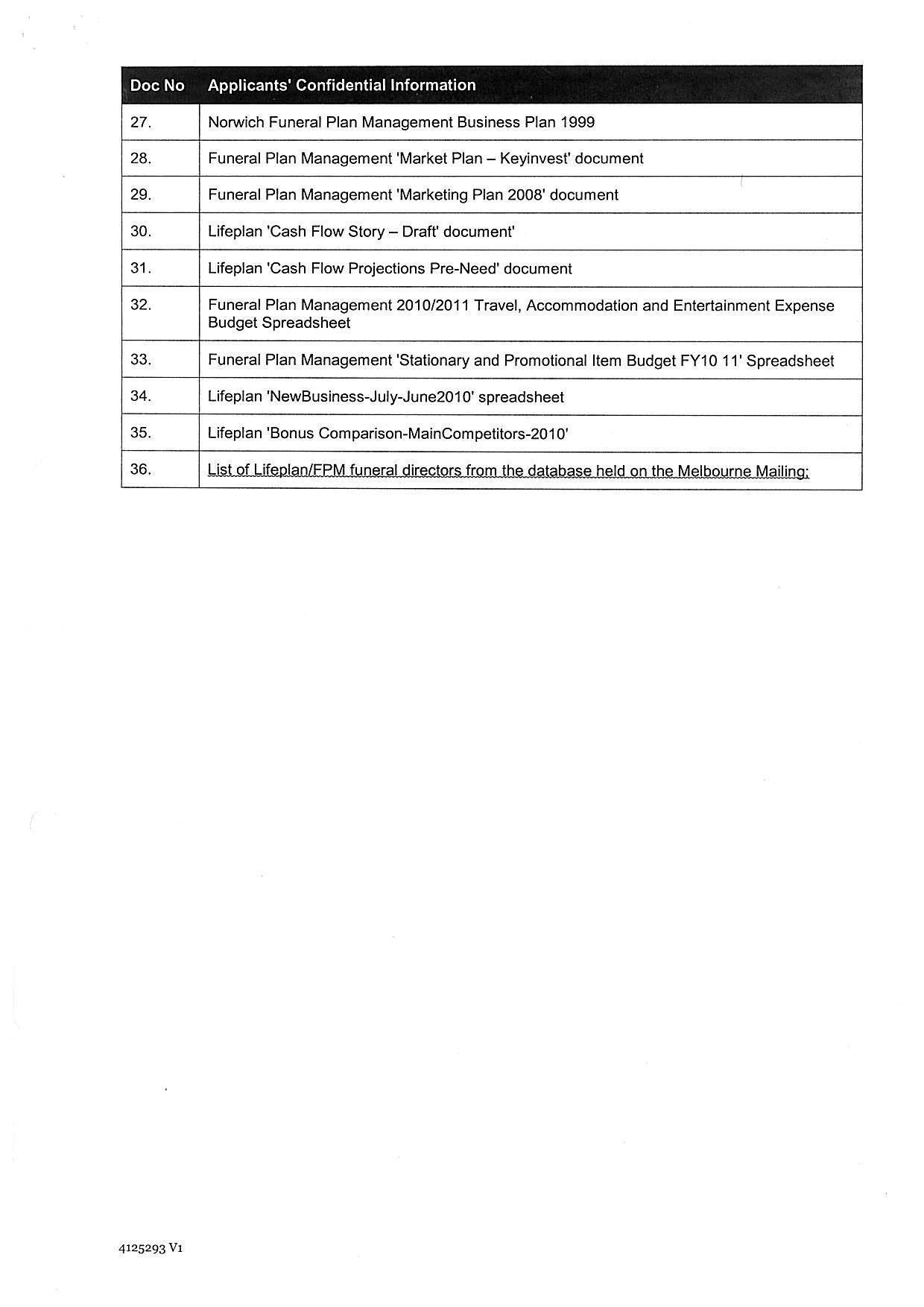

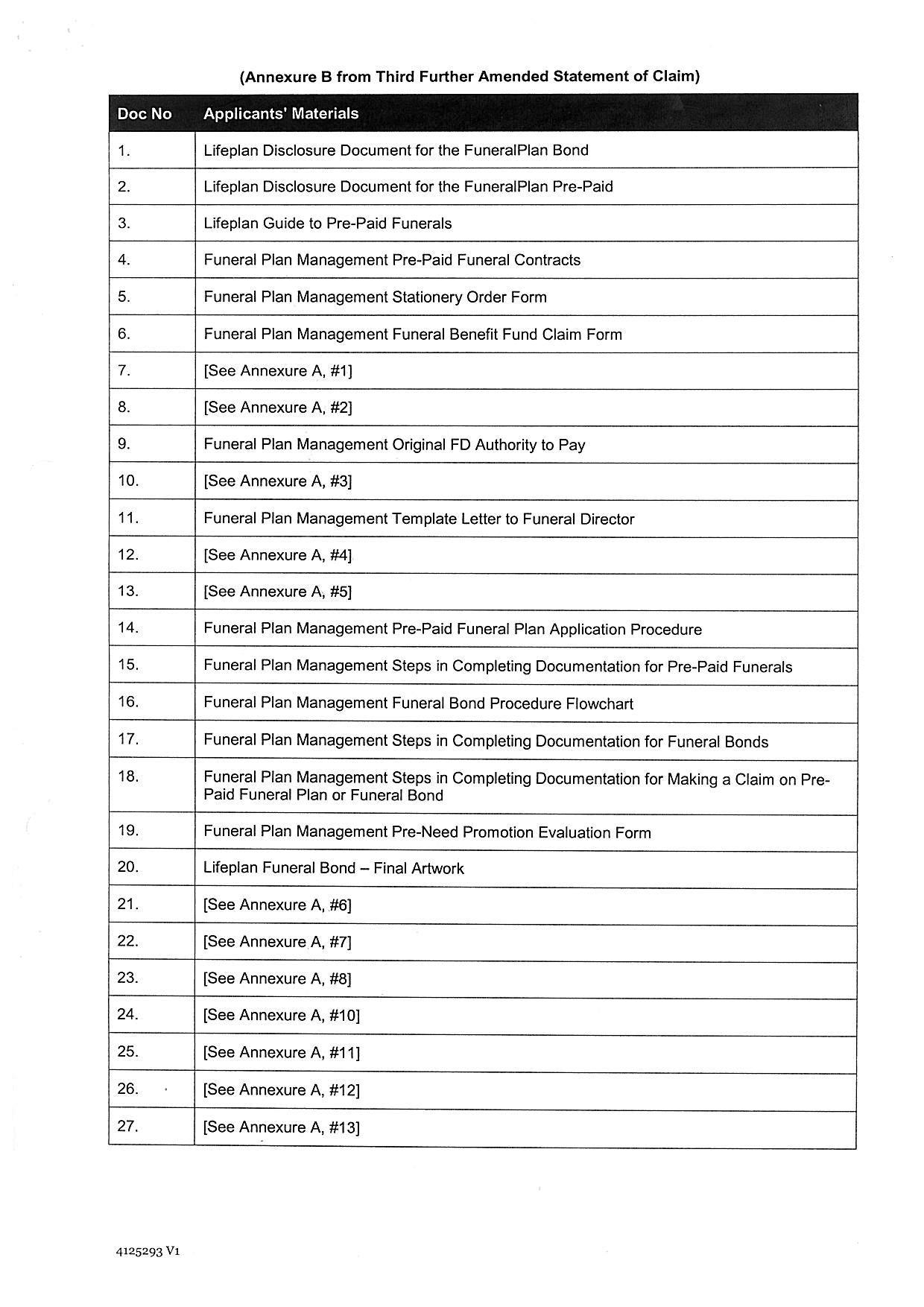

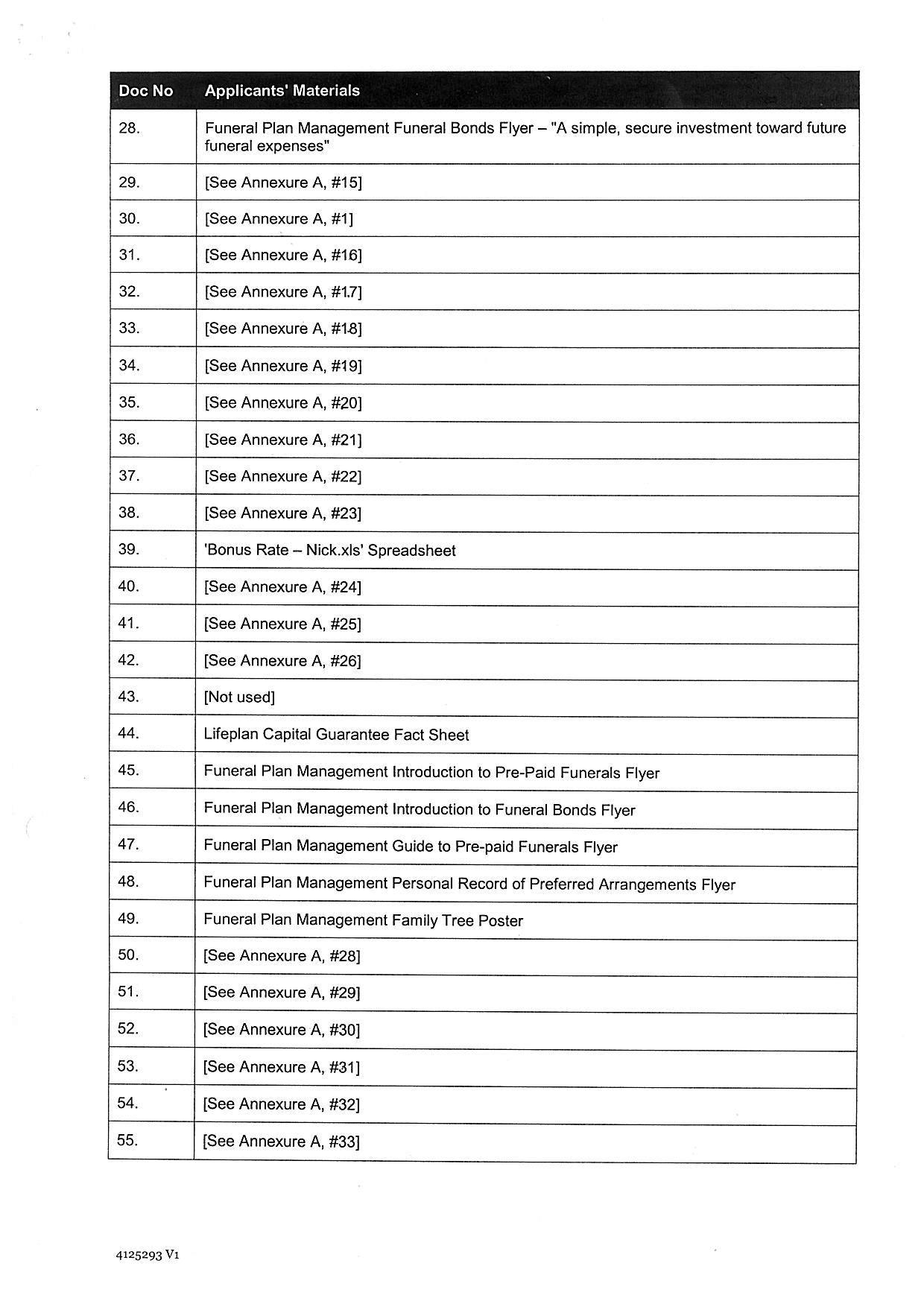

5 The applicants also seek an injunction and orders for delivery up against all four respondents in relation to 61 documents. There were two annexures to the Statement of Claim as it was until shortly prior to trial. In Annexure A, the applicants identified documents they contended contained confidential information taken and used by the respondents. In Annexure B, the applicants identified what they claimed were their copyright works and materials. Shortly prior to trial, the applicants abandoned their claim for infringement of copyright. They now contend that the documents identified in Annexures A and B contain their confidential or valuable information or both which has been taken and used by the respondents. I attach a modified version of Annexures A and B to these reasons. As will be seen, Annexure A identifies 36 documents and Annexure B 60 documents (number 43 not used). Thirty five of the documents identified in Annexure B are documents identified in Annexure A.

6 The orders sought by the applicants in relation to the documents in Annexures A and B are as follows:

3. Noel Jeffrey Woff, Richard John Corby, Funeral Planning Australia Pty Ltd (in liquidation) and the Ancient Order of Foresters Friendly Society in Victoria Ltd whether by themselves, their agents, employees or related entities (as defined by s 9 of the Corporations Act 2001 (Cth)) be permanently restrained from using or publishing the documents described in Annexure A and B of the Third Further Amended Statement of Claim and attached as Annexure 1 to this Order.

4. Noel Jeffrey Woff, Richard John Corby, Funeral Planning Australia Pty Ltd and the Ancient Order of Foresters Friendly Society in Victoria Ltd within 14 days:

a. deliver to the Applicants all hard copies of the documents described in Annexures A and B of the Third Further Amended Statement of Claim and attached as Annexure 1 to this Order in each of their possession, custody or control; and

b. permanently destroy all electronic copies of the documents described in Annexures A and B of the Third Further Amended Statement of Claim and attached as Annexure 1 to this Order in each of their possession, custody or control.

7 In terms of monetary relief, the applicants made an election well before trial for an account of profits rather than damages or equitable compensation. They did not seek to prove any specific loss or damage which they suffered as a result of the respondents’ conduct. As against Mr Woff and Mr Corby, the applicants seek the salaries they were paid by Foresters and some small amounts (relatively speaking) that Mr Woff and Mr Corby received through FPA. As against Foresters, the position is as follows. In 2010, Foresters had a relatively small funeral fund upon which it earnt a management fee. From the time Mr Woff and Mr Corby became employees of Foresters, the fund grew very substantially and Lifeplan’s funeral fund business has diminished. For bonds or plans written from 2011 onwards, Foresters earns a 2% management fee in relation to the fund. The 2% management fee is calculated by reference to the funds under management (“FUM”). This fund is predicted to grow as new bonds or plans are written. The applicants’ primary claim against Foresters is for an account of profits being the net present value of the profits earned and to be earned by Foresters with respect to the fund. The applicants’ case is that an account of profits against Foresters results in a figure in the order of $30 million.

8 In their pleadings and affidavits of evidence filed before trial, the applicants advanced a broad case concerning the scope of the respondents’ wrongdoing. They alleged that absent the wrongdoing, Foresters had neither the financial capacity nor the skills and systems to obtain and then operate the business it did from 2011 onwards. They alleged that FPM had a business system which they described as the “FPM Business System” and which comprised market facing documents, interfaces with funeral directors, support systems and business intelligence, and that the respondents took and used that system. I do not think that the applicants advanced a case in closing that Foresters did not have the financial capacity to establish and operate the business it did from 2011 onwards. In any event, I am satisfied on the evidence that Foresters did have that capacity. With respect to the allegation concerning the taking and use of a FPM Business System, whilst Mr Woff and Mr Corby took certain documents and reproduced them in documents used by Foresters, the evidence does not support a finding that the respondents took and used the applicants’ system of operating, or that all aspects of that system were unique.

9 As the applicants’ case was developed at trial, it concentrated on 11 acts or courses of conduct by Mr Woff and Mr Corby which were said to involve breaches of duty on their part. As my findings of fact are organised around these 11 matters, it is convenient that I identify them at the outset.

10 The business concept that Mr Woff and Mr Corby had in mind in the second half of 2010 involved them working together with Foresters to develop a successful funeral fund business. Mr Woff and Mr Corby were to leave their employment with Lifeplan and become employees of Foresters, and Foresters would engage their company FPA to promote and market the business in return for the payment of a commission. The proposal would involve substantial set-up costs to be borne by Foresters and there was a risk that the business would not succeed. The Board of Foresters had to approve the proposal and, it may be assumed, would only do so if satisfied the risks were worth taking. In order to persuade the Board of Foresters that the business concept was commercially viable, Mr Woff and Mr Corby, in the name of FPA, prepared a paper to present to the Board entitled “Funeral Fund Business Concept”. I will refer to this paper as the Business Concept Plan or BCP. The applicants’ case is that Mr Woff and Mr Corby used their confidential and valuable information in preparing the BCP and, indeed, included some of it in the BCP. The applicants’ case is that Foresters knew that the BCP contained the applicants’ confidential and valuable information.

11 Secondly, the applicants’ case is that between October and December 2010, Mr Woff, whilst still an employee of Lifeplan, and Mr Corby tried to solicit the business of one of the applicants’ major clients, Tobin Brothers Funerals (“Tobins”). In other words, they tried to persuade Tobins to transfer its business from the applicants to the proposed business with Foresters. Tobins was a major client which, unlike other funeral directors, entered into a contract (usually for three years) with the fund manager it selected.

12 Thirdly, the applicants’ case is that between October and December 2010, Mr Woff and Mr Corby, and in particular Mr Woff, whilst still employees of Lifeplan, approached other funeral directors with a view to soliciting the business of those funeral directors for the proposed business with Foresters.

13 Fourthly, the applicants’ case is that in July 2010, Mr Woff, whilst still an employee of Lifeplan, and with the knowledge and encouragement of Foresters, induced Mr Corby to leave his employment with Lifeplan.

14 Fifthly, the applicants’ case is that Mr Woff and Mr Corby, whilst still employees of Lifeplan, became aware of Foresters’ desire to increase its funeral products business and yet failed to disclose that “business opportunity” to the applicants.

15 Sixthly, the applicants’ case is that Mr Woff and Mr Corby took and used their FPM Business System. As developed, the primary documents which were the subject of this allegation were disclosure documents, stationery request forms, marketing flyers, claim forms and pre-paid contract forms.

16 Seventhly, the applicants’ case is that Mr Woff took other confidential and/or valuable business intelligence of the applicants. They point to the large number of their documents which Mr Woff sent to one or other of his private email addresses between July and December 2010.

17 Eighthly, the applicants’ case is that Mr Woff and Mr Corby took extensive steps whilst still employed by Lifeplan to establish FPA and to ensure that the proposed business with Foresters was in a position to commence immediately upon the cessation of their employment with Lifeplan. The applicants’ case is that the steps taken went well beyond what the law permits an existing employee to do.

18 Ninthly, the applicants’ case is that Mr Woff and Mr Corby prevailed upon a printing firm, Matgraphics and Marketing Pty Ltd (“Matgraphics”), which had been engaged by Lifeplan to print pre-paid funeral contract pads to provide to funeral directors, to use its electronic templates to print pre-paid funeral contract pads for Foresters to provide to its funeral directors. This was done without the applicants’ permission.

19 Tenthly, the applicants’ case is that Mr Woff and Mr Corby sent the applicants’ list of funeral directors to a mailing house, Melbourne Mailing, which then used it as Foresters’ mailing list of funeral directors.

20 Finally, the applicants’ case is that because of the similarity between the applicants’ key documents and those of Foresters, there was, at least for a time, confusion in the market between the applicants’ business and the business of FPA and Foresters. The applicants’ case is that FPA and Foresters were passing off their business as that of the applicants.

21 The applicants made an application to amend their Second Further Amended Statement of Claim shortly before the trial. The application was supported by an affidavit from their solicitor. Mr Woff swore an affidavit in opposition to the application. After hearing submissions, I granted leave to amend and a Third Further Amended Statement of Claim was filed. A brief description of the amendments and my reasons for allowing them is as follows.

22 The first class of amendments related to Annexure A to the Statement of Claim. Annexure A of the Second Further Amended Statement of Claim had identified 35 documents which were described as “confidential” or “commercially sensitive and/or proprietary”. Annexure A was amended to identify one additional document involving Melbourne Mailing and to refer to “confidential” or “commercially sensitive, confidential or valuable information”. There were corresponding minor changes in the body of the Statement of Claim. The addition of the reference to “valuable” information was designed, I think, to enable the applicants to argue that, in addition to misusing confidential and commercially sensitive information, Mr Woff and Mr Corby breached their duties to the applicants by copying documents containing valuable information during their employment with a view to using the documents after their employment had ended. “Valuable” was said by the applicants to mean no more than non-trivial (Spotless Group Ltd & Others v Blanco Catering Pty Ltd and Another [2011] FCA 979; (2011) 93 IPR 235 at 242-243 [27] per Mansfield J; Faccenda Chicken Ltd v Fowler and Others [1987] Ch 117 at 136; (1985) 6 IPR 155 at 164). It seemed to me that the amendment involved no more than a further characterisation of information already identified. I could not see any prejudice to the respondents in allowing this amendment.

23 The second class of amendments related to Annexure B. As I have already said, Annexure B of the Second Further Amended Statement of Claim had identified 60 documents which were said to be the subject of copyright in favour of the applicants and which the respondents were alleged to have infringed. There were also allegations of infringement of copyright in the body of the Statement of Claim. By this class of amendments, the applicants sought to add one additional document to Annexure B, add a reference alleging that the information in the documents was valuable (with corresponding minor changes in the body of the Statement of Claim), and delete all references to copyright in Annexure B and in the body of the Statement of Claim. In other words, the thrust of this amendment was the abandonment of the copyright claim and that was not seriously opposed by the respondents. The other amendments in this class were unlikely to cause any prejudice to the respondents. I granted leave to amend in relation to Annexure B and, insofar as it contained claims of copyright infringement (and inserted references to the information being valuable), the body of the Statement of Claim.

24 The third class of amendments involved the addition of a claim under s 1317H(2) of the Corporations Act for the profits made by Foresters as a result of Mr Woff’s contraventions of the Act. Section 1317H is in the following terms:

1317H Compensation orders—corporation/scheme civil penalty provisions

Compensation for damage suffered

(1) A Court may order a person to compensate a corporation or registered scheme for damage suffered by the corporation or scheme if:

(a) the person has contravened a corporation/scheme civil penalty provision in relation to the corporation or scheme; and

(b) the damage resulted from the contravention.

The order must specify the amount of the compensation.

Note: An order may be made under this subsection whether or not a declaration of contravention has been made under section 1317E.

Damage includes profits

(2) In determining the damage suffered by the corporation or scheme for the purposes of making a compensation order, include profits made by any person resulting from the contravention or the offence.

Damage includes diminution of value of scheme property

(3) In determining the damage suffered by the scheme for the purposes of making a compensation order, include any diminution in the value of the property of the scheme.

(4) If the responsible entity for a registered scheme is ordered to compensate the scheme, the responsible entity must transfer the amount of the compensation to scheme property. If anyone else is ordered to compensate the scheme, the responsible entity may recover the compensation on behalf of the scheme.

Recovery of damage

(5) A compensation order may be enforced as if it were a judgment of the Court.

25 The applicants alleged in their Second Further Amended Statement of Claim that Mr Woff had contravened ss 180, 181, 182 and 183 of the Corporations Act. Whilst it was never made clear why s 1317H(2) had not been pleaded earlier, I accepted the applicants’ submission that the “liability” plea (i.e., the plea of the contraventions of the Corporations Act) was already in the Second Further Amended Statement of Claim and that the parties had addressed the issue of the profits made in the evidence filed for use at trial in connection with the claim in equity for an account of profits. In those circumstances, I allowed the amendment.

26 Finally, the applicants sought to introduce a plea into their Statement of Claim that Foresters was vicariously liable for the conduct of Mr Woff and Mr Corby to the extent that such conduct occurred whilst each of them was employed by Foresters. This amendment was opposed by Foresters on the ground that it was not arguable that Foresters was liable for the equitable wrongdoing of Mr Woff and Mr Corby. I decided that the matter was arguable and that the amendment should be allowed. I have now had full argument on the issue and I have decided that Foresters is not vicariously liable for the equitable wrongdoing of Mr Woff and Mr Corby.

27 Mr Matthew Peter Walsh was the principal witness called by the applicants. He swore four affidavits which were read as his evidence-in-chief. The affidavits set out the applicants’ case, largely by reference to the documents which had been retrieved from Mr Woff’s computer, or discovered or produced on subpoena. At times, some of Mr Walsh’s statements were more in the nature of submissions rather than statements of fact.

28 Mr Walsh’s employment history and position at Lifeplan is as follows. He has been employed by Lifeplan since 1993 and he was the information services manager for Lifeplan from that date until 1998. In that position, he supervised the information technology functions of Lifeplan. In 1998, he became the general manager for strategic development and in that position, he was responsible for the business strategy functions, sales and marketing, product maintenance and development, customer services and information technology. His responsibilities also encompassed the business conducted by FPM and he had executive responsibility for that company and general oversight of its operations. After the merger of Lifeplan and Australian Unity Investments Ltd (“Australian Unity”) in August 2009, Mr Walsh held the position of Head of Lifeplan and General Manager of Specialised Products for Australian Unity and he also oversaw the management of FPM. Mr Walsh said that in his position as Head of Lifeplan and General Manager of Specialised Products for Australian Unity, he is responsible for the Lifeplan business as part of his role as head of the specialised products business of Australian Unity with a total of $2 billion funds under management, and over 100,000 clients in 2012.

29 Mr Walsh was cross-examined at length, principally by counsel for Foresters. An important aspect of the cross-examination was to suggest to Mr Walsh that the loss of business by Lifeplan and the securing of business by Foresters was not due to the alleged wrongdoing of Mr Woff and Mr Corby, but rather to other factors, including the poor performance in terms of investment returns of one of Lifeplan’s funeral benefit funds (i.e., Funeral Benefits Fund No. 2) and, to a lesser extent, cost cutting measures put in place after the merger of Australian Unity and Lifeplan. It seems that the performance of Funeral Benefits Fund No 2 was affected by the Global Financial Crisis and it may also have been affected by a depreciation in unlisted assets. There was a reference in the course of the evidence to collateralised debt obligations. There was a sale of equities before December 2008 and the fund was temporarily closed to new business. It has not to date been reopened to new business. It remains “open” for those making regular contributions into the fund (i.e., those paying by instalments). Lifeplan has established a new funeral benefit fund called the “Tax Minimiser Fund”. Those making regular contributions into the Funeral Benefits Fund No 2 number in the region of 100 to 150 of the 350 funeral directors who had an interest in the fund upon its closure. The fund paid returns of 0.25% in 2009, and 0.5% in 2010. During the same years, the Tax Minimiser Fund returned 4.30% in 2009, and 3.57% in 2010. Other funds returned in excess of 2.5% in these two years. The Consumer Price Index in 2009 was 1.46%, and in 2010 it was 3.05%.

30 Mr Walsh was quite defensive about the performance of the Funeral Benefits Fund No 2. At one point in his evidence, he described the return during the 2009 year as an excellent return in the circumstances. Although I accept the substance of Mr Walsh’s evidence, I think he took an unduly optimistic view of the performance of Funeral Benefits Fund No 2 in 2009 and 2010, and tended to downplay the likely reaction to the fund’s performance from the funeral directors who had invested in it. As I have said, another aspect of the cross-examination was to establish that cost cutting measures were put in place following the merger between Australian Unity and Lifeplan. I find that there were such measures and that they affected marketing (including sponsorships), travel and entertainment expenses. Mr Walsh was also cross-examined about the decline in staff numbers in the FPM sales team in the second half of 2010 and my findings in relation to that matter are set out below. Mr Walsh accepted in cross-examination that the financial documents suggested that Foresters had the capital to expand its business.

31 Counsel for Mr Woff and Mr Corby submitted that the applicants were not frank with their funeral director clients as to the reasons for the poor performance of Funeral Benefits Fund No 2. This was said to have two consequences. Mr Woff and Mr Corby were left to bear the brunt of the funeral directors’ annoyance as to the performance of the fund, and this is a reason they were prepared to leave Lifeplan. Furthermore, Lifeplan’s “misrepresentation” or “non-disclosure” as to reasons for the poor performance of the fund is a reason in equity why the applicants’ claim for an account of profits should be refused.

32 I think Funeral Benefits Fund No 2 performed poorly in terms of investment returns. I think funeral directors would have been angry or annoyed about that fact. I think that conclusion is supported by the evidence of the three funeral directors who gave evidence before me (see at [53] below). I will come back to the reasons for the poor performance of Funeral Benefits Fund No 2 and the alleged misrepresentations or non-disclosures to funeral directors when addressing Mr Woff’s evidence.

33 The other matter which Mr Walsh was cross-examined about at some length was the FPM Business System. There can be no doubt that FPM had a business system, but I am not persuaded that it was particularly unique or was something that was not, for the most part, the product of the nature of the business. In any event, as I will explain later in these reasons, I am not satisfied that other than in respects I identify, the respondents took and used the FPM Business System.

34 Subject to noting these matters, I consider that Mr Walsh was a satisfactory witness and that I can rely on his evidence.

35 The applicants tendered affidavits of the following persons as the evidence-in-chief of those persons:

(1) Ms Michelle Anne Rawe (employee of Lifeplan and executive assistant to Mr Walsh);

(2) Ms Sharon Patricia Ferguson (employee of Lifeplan and a service and support manager);

(3) Mr Christopher James Pullen (employee of Australian Unity and a senior infrastructure engineer);

(4) Mr Michael Francis Hutton-Squire (employee of Australian Unity and head of technical services/business technology); and

(5) Mr Jean-Pierre du Plessis (partner of Ferrier Hodgson specialising in computer forensics and data recovery, among other things).

36 Other than Ms Ferguson, these witnesses were involved in the investigation carried out by Lifeplan which I describe below. Ms Ferguson described events surrounding an information request made by Mr Woff in 2010. None of these witnesses were required for cross-examination and I accept their evidence.

37 The applicants called two experts, one an expert in accounting (Ms Dawna Wright), and the other an expert in actuarial calculations (Mr Michael Dermody). Both were credible and reliable. I discuss their evidence (and that of Foresters’ experts) below.

38 Mr Woff’s evidence-in-chief was contained in a number of affidavits which he had sworn and which were tendered. The affidavits were, in part, not in proper form because they were argumentative and expressed in terms of submissions rather than statements of fact. Some of the topics addressed were not relevant. For example, Mr Woff tried to explain his decision to leave Lifeplan by reference to a lack of opportunity for further career advancement and reference to his dissatisfaction with Lifeplan’s future intentions in respect of the expenses FPM might incur to increase its business, such as marketing rebates and discretionary spending. Mr Woff gave his opinion as to the reasons Lifeplan’s business declined and he suggested that it was, in part at least, the author of its own misfortune. He also gave his opinion as to the reasons Foresters was able to succeed in building up the Foresters Funeral Fund and in doing so he attributed a good deal of the success to the skills he and Mr Corby were able to bring to the Foresters’ business.

39 For reasons I will give, I do not accept Mr Woff’s evidence except where it is corroborated by evidence which I do accept. There were not many references to Mr Woff’s evidence-in-chief in his counsel’s closing submissions. Subject to one matter, I will refer to those aspects of Mr Woff’s evidence which were relied on by his counsel during his closing submissions in the context of particular topics.

40 The one matter which I deal with at this point is as follows. Mr Woff and Mr Corby submitted that the applicants were not entitled to the equitable remedy of an account of profits because they had not acted equitably. They submitted that the cause of the poor performance of Lifeplan’s Funeral Benefits Fund No 2 was poor investment decisions by Lifeplan and not, or not simply, the Global Financial Crisis. They submitted that the applicants misrepresented, or at least did not disclose, the true position to funeral directors. Mr Woff deposed to a conversation he had in June 2010 with a Mr Tony di Girolamo who was employed by one of the applicants as the Head of Specialised Products Lifeplan Funds Management. Mr di Girolamo allegedly told Mr Woff that in 2008, Lifeplan had made risky investment decisions resulting in a loss of $20 million which had been transferred to Funeral Benefits Fund No 2. In due course, an amount of $8 million was borrowed from the management fund to ensure the solvency of the fund. Mr di Girolamo allegedly said that Mr Walsh told him not to tell Mr Woff these things. I do not think this last matter, even if true, is sinister. Mr Walsh may have simply wished to keep control of the situation.

41 Counsel for Mr Woff pointed out that Mr Woff was not cross-examined about this conversation. Although that is correct, it does not mean that I have to accept the evidence in circumstances where there was a sustained attack on his credibility and reliability, and where I have found that I will not accept his evidence except where it is corroborated by evidence which I do accept. There are strands of evidence which bear on the poor performance of the Funeral Benefits Fund No 2, but I would hesitate to make a finding as to the cause or causes of that poor performance even if it was important that I do so because I think that the evidence was far from complete. However, I do not think that it is important that I do so because the evidence does not establish the alleged misrepresentations or non-disclosures to funeral directors. Furthermore, and in a sense this is the short answer to the submission, it was never explained and no authority was referred to which might assist in explaining how any conduct by Lifeplan in relation to Funeral Benefits Fund No 2 bars the applicants from making what is otherwise a proper claim against Mr Woff and Mr Corby.

42 A number of the matters which form the basis of my conclusion that I will not accept the evidence of Mr Woff except where it is corroborated by evidence which I do accept are set out in my discussion of particular facts. At a more general level, I base my conclusion on the following.

43 In the second half of 2010, Mr Woff sent a number of emails with the applicants’ documents attached from his Lifeplan email account to one or other of two private email addresses, ichbinnoddy@hotmail.com and noel.woff@hotmail.com. Except where it is necessary to refer to one of these private email addresses in particular, I will refer to them collectively as Mr Woff’s private email address. Mr Woff admitted in cross-examination that he “double-deleted” a number of emails from his Lifeplan account shortly before leaving the employment of Lifeplan and that, in hindsight, it was the wrong thing to do. He would not provide a direct answer to the question of whether he had doubled-deleted the emails in order to ensure that Lifeplan would not discover them. Mr Woff also admitted sending emails with attached information to his hotmail address and “that it was a mistake and in hindsight is something I shouldn’t have done”. He admitted referring to one or two of the emails for the purposes of preparing the BCP and that it was wrong.

44 In my opinion, Mr Woff’s explanation for not discovering emails and attachments sent to his ichbinnoddy@hotmail.com email address to the effect that a virus had attacked it and he shut the account, is completely implausible and a fabrication. The explanation is belated and I found his evidence on the topic entirely unconvincing.

45 In my opinion, Mr Woff’s evidence that he sent the emails through to his ichbinnoddy@hotmail.com email address for future reference and not to further the proposed business with Foresters was implausible and I reject it. The description of the subject of some of these emails, for example, “Recipe” and “New Food Conditions” was designed, I find, to avoid detection of what he was doing by the applicants.

46 I found Mr Woff’s evidence concerning the proposed role of FPA at the time of the BCP to be evasive, although he eventually acknowledged the position.

47 Mr Woff admitted that what he told Mr Walsh about where Mr Corby was going after he left Lifeplan was untrue and he said that he put his own personal interests above those of Lifeplan. A little later he said that he lied because he was negotiating his contracts with Foresters at the time. I think he also accepted that he was not entirely accurate in describing to Mr Walsh his proposed role at Foresters.

48 Mr Woff admitted on a number of occasions that the discovery given by Mr Corby and himself was inadequate. He was not able to provide an explanation for failure to give proper discovery. On a number of occasions during the course of his cross-examination when he was asked to explain the reason he had not discovered a document, he said that it was an oversight and he apologised to the Court.

49 There were occasions in cross-examination where Mr Woff’s logic was difficult to follow. For example, he asserted that it was irrelevant that he and Mr Corby had made statements in their proposal to Tobins in 2010 which reflected poorly on the applicants because Tobins was never going to award the new contract to the applicants. That is either a submission, or if intended to be evidence of a fact, it is illogical. It is illogical because if the statements were irrelevant, then they would not have been included. I reject his suggestion that they were included because Lifeplan is the benchmark.

50 Mr Corby did not give evidence. He is the second respondent to the proceeding and an employee of the fourth respondent, Foresters. As will become clear, there are events and circumstances in issue in this case about which Mr Corby could have given evidence. Mr Corby’s absence from the witness box in circumstances where there is nothing to suggest that he could not have given evidence means that I can infer that his evidence would not have assisted his case. Where there are competing inferences, Mr Corby’s absence from the witness box might enable me to be more confident in drawing one of the available inferences. These principles are well known (Jones v Dunkel and Another (1959) 101 CLR 298 at 308 per Kitto J; at 312 per Menzies J and 320-321 per Windeyer J; Australian Securities and Investments Commission v Hellicar [2012] HCA 17; (2012) 247 CLR 345 at 412-414 [164]-[170] per French CJ, Gummow, Hayne, Crennan, Kiefel and Bell JJ).

51 To the extent that Foresters disputes the applicants’ case relating to the events and circumstances about which Mr Corby could have given evidence, I think the same approach applies to it. Mr Corby was and remains an employee of Foresters and I think it was to be expected that Foresters would call him if it wished to challenge the applicants’ version of the relevant events and circumstances.

52 Foresters referred to the fact that Mr Corby was separately represented and that the whole of his affidavit evidence was subject to objection. Foresters submitted that it could not be expected to have arranged a new affidavit from Mr Corby. It submitted that no inference should be drawn against it. I reject that submission. If the submission is that in some way the pre-trial orders lead to the conclusion that the absence of Mr Corby from the witness box cannot give rise to the inferences I have identified, then I reject it. Foresters could have obtained affidavit evidence from Mr Corby or applied to lead oral evidence from him. If the submission is that nothing Mr Corby could have said was relevant to Foresters’ defence of the claim that it did not knowingly assist and was not involved within s 79 of the Corporations Act, then clearly if the premise is correct, the conclusion follows. The position with respect to Foresters and the absence of Mr Corby from the witness box might be different if there was clear evidence of a conflict between the two, but there is no such evidence. Mr Corby is still employed by Foresters.

53 Mr Woff and Mr Corby called three funeral directors to give evidence. They were Mr Craig Murphy of Murphy Family Funerals, Mr John Scott of TJ Scott and Son, and Mr Paul Graham of Graham Family Funerals. Each of these funeral directors was on friendly terms, to varying degrees, with either Mr Woff or Mr Corby or both. Nevertheless, there is no reason not to accept the substance of their evidence.

54 Mr Murphy owns Murphy Family Funerals and that business had investments with FPM. The returns on the investments were poor. Mr Murphy was contacted by Mr Corby in March 2011 and Mr Corby told him that he and Mr Woff had left FPM and commenced with Foresters. In November 2011, Mr Murphy started placing his investments with Foresters. He did not think that he had been told the truth about the reason for the poor performance of Lifeplan’s Funeral Benefits Fund No 2.

55 Mr Scott is the owner of TJ Scott and Son and that business had investments with FPM. He moved his investments from FPM to Foresters in March 2011 because he wanted to maintain a personal relationship with Mr Woff and Mr Corby. He said that neither Mr Woff nor Mr Corby solicited him for business for Foresters whilst they were employed by Lifeplan.

56 Mr Graham is the managing director of Graham Family Funerals and that business had investments with FPM. Mr Graham became dissatisfied with the low returns on the FPM pre-need funeral products and, in July 2011, he started placing his investments with Foresters. Mr Graham said that it was FPM’s poor rate of return that led him to move to Foresters.

57 The evidence of the funeral directors establishes, I think, that there was a perception amongst at least some funeral directors that Lifeplan’s Funeral Benefits Fund No 2 had performed poorly and that at least some funeral directors considered that they have suffered a loss where investment returns do not keep pace with the increase in funeral costs. It also establishes that the reasons a funeral director may transfer from one fund to another include the quality of the investment returns and the extent of the personal relationship with the salesmen representing the fund.

58 Foresters called four witnesses.

59 Mr Theodore Fleming is the non-executive Chairman of the Board of Foresters. He has held that position since 1995. Between December 1993 and 1995, he was a non-executive director of Foresters. Mr Fleming is a legal practitioner. He has practised law for nearly 40 years and he is the principal partner of the legal practice, Fleming & Rhoden Lawyers.

60 Mr Fleming swore an affidavit which was tendered as his evidence-in-chief. He was cross-examined at some length by counsel for the applicants. On occasions, Mr Fleming reformulated counsel’s question in a more extreme form and then denied it, or commented upon it. Nevertheless, I accept the substance of Mr Fleming’s evidence.

61 Mr Kerry Allan Hughes has been the chief executive officer of Foresters since October 2000. He swore seven affidavits which were tendered as his evidence-in-chief. He was cross-examined about a number of matters, including events in 2010, the adequacy of Foresters’ discovery and the decision to put FPA into liquidation in 2013. I accept much of what Mr Hughes said, although there are a couple of areas, which I will identify, where I do not accept his evidence.

62 Foresters also called two experts, one an expert in accounting (Mr Campbell Jackson), and the other an expert in actuarial calculations (Ms Caroline Bennet). Like the applicants’ experts, both were credible and reliable. Their evidence is discussed below.

63 The applicants allege that the respondents have not made proper discovery. They refer to orders for discovery made in the proceeding and, in particular, orders made on 22 October 2013 and 3 June 2014 respectively. They have put before the Court correspondence which has passed between the respective solicitors for the parties and affidavits about discovery filed by Mr Woff, Mr Corby and Mr Hughes respectively.

64 The applicants contend that the failure to make proper discovery means that I can and should infer that the applicants have been disadvantaged in their ability to prosecute the proceeding, and that the documents would have assisted the applicants in proving the breaches by Mr Woff and Mr Corby, and in proving the knowing assistance of Foresters.

65 It is trite that issues of discovery and, in particular, whether there has been adequate discovery are ordinarily dealt with before trial. Nevertheless, the failure to produce a document where there is an obligation to do so may lead to an adverse inference in certain circumstances (Microsoft Corporation and Another v Atifo Pty Ltd and Others (1997) 38 IPR 643). It would be necessary to show that the document exists, that there was an obligation to produce it, and that there has been an intentional withholding of the document. There would then need to be a precise identification of the inference to be drawn from the failure to produce the document. For example, the party seeking the inference would need to identify the precise process of reasoning from the absence of, say, document X, or a class of documents to the particular conclusion. The applicants have not done that. For example, in the case of Mr Woff and Mr Corby, it is said (among other allegations) that they have failed to discover documents concerning Foresters’ purported loans to FPA, Mr Woff and Mr Corby, and have failed to discover documents regarding the hybrid trust arrangement, but it is not made clear how it is said that these documents would have assisted the applicants to prove the breach of duties alleged. If it is said that these documents are relevant not to breach but to the account of profits, one may ask rhetorically, what are the competing inferences to which these documents relate. The applicants’ written submissions tended to focus almost entirely on the deficiencies in the discovery and not also on these issues.

66 Having said that, there is no doubt that the discovery of Mr Woff and Mr Corby has been deficient in a number of respects. Mr Woff admitted as much on a number of occasions in the course of his cross-examination. I do not think I need to pursue this any further because I think I can make clear findings about the conduct of Mr Woff and Mr Corby from the evidence which has been put before me.

67 The position with Foresters is somewhat different. Except for the fact that Mr Hughes has not searched for the FPA proposal to Tobins or caused any person at Foresters to carry out a search for this document, there appears to be a dispute about whether the orders for discovery have been complied with. In their closing written submissions, the applicants identified the deficiencies in Foresters’ discovery in similar terms to a letter from their solicitors dated 30 January 2014. I note that Foresters denied any deficiencies in the letter from their solicitors dated 12 February 2014. I am not prepared to find that Foresters deliberately failed to make proper discovery.

68 I now set out my findings of fact. Many of the background facts are not in dispute as they are clearly established by the evidence of Mr Walsh or the documents put in evidence. Where there is a dispute, I will identify the dispute and the way in which I resolve it.

69 Lifeplan described itself and FPM in its 2009 Disclosure Documents in the following terms. Lifeplan is a leading Australian specialist fund manager and provider of investment products. It is a provider of Funeral Bonds, tax effective investment products and Education Savings Plans. It holds an Australian Financial Services Licence. FPM is a wholly-owned subsidiary of Lifeplan and it is a specialist business dedicated to providing funeral benefits, investment management and customised administration services for funeral directors and their clients. Lifeplan and its funeral products are regulated by its constitution, the Corporations Act and the Life Insurance Act 1995 (Cth). Its funeral bond product is regulated by the Australian Prudential Regulation Authority (“APRA”) under the Life Insurance Act.

70 Mr Walsh expanded on this description with particular emphasis on Lifeplan’s funeral bond business as follows. Lifeplan is in the business of funds management and the provision of investment products. In conjunction with FPM, Lifeplan provides professional administration, investment products and information on aspects of planning for a funeral in advance of a customer’s death. Lifeplan has been involved in the funeral products business since 1984. FPM promotes, markets and distributes Lifeplan’s funeral products. As at 2012, these products were sold through 250 Australian funeral directors. FPM both recruits and maintains relationships with funeral directors for this purpose. FPM has the capacity and had prior to 2012, promoted the products of entities other than Lifeplan. It previously promoted and distributed funeral bond products of another friendly society, KeyInvest Limited. FPM no longer promotes and distributes KeyInvest funeral bond products but does administer them on behalf of KeyInvest Limited. FPM’s business planning includes a strategy of seeking out and securing other friendly society funeral product providers.

71 A funeral bond is a funeral investment product offered by a friendly society through a benefit fund. In the usual course, there is a requirement that the monies which have been invested be paid out only on the death of the client and used for the purpose of their funeral. The idea of a funeral bond is that it allows individuals to set aside funds to meet the costs of future funeral expenses.

72 Mr Walsh said, and I accept, that the ways in which funeral bonds can be used relate to the type of sale and the mechanism by which the benefit is paid to the funeral director. Funeral directors use funeral bonds in two principal ways. First, the most common way is to use the funeral bond in association with a pre-paid funeral contract that sets out the desired funeral arrangements and stipulates a fixed price for the funeral services. This type of funeral bond is called a Funeral Plan Pre-Paid Bond. The maximum amount of the bond is the cost of the funeral service under the pre-paid funeral contract. The pre-paid funeral plan can be paid out to the funeral director on the death of the client and following confirmation from the funeral director that the funeral has been conducted in accordance with the pre-paid funeral contract. The second way in which a funeral bond can be used is through a transaction referred to as a Funeral Plan Bond. The client executes a document containing specified funeral services, but without a contractual commitment as to the pricing of those services. In the case of this type of funeral bond, when the client dies the funeral director would requote the funeral based on the pre-arranged details and any further modifications based on the prices current as at the date of death. The funeral bond is used to contribute to the cost. There is a maximum amount allowed for the bond. In Lifeplan’s 2009 Disclosure Document, it is stated to be $10,750. Under both types of bond, payments may be made by instalments.

73 The largest sales channel for funeral bonds is through funeral directors. Funeral directors introduce funeral bonds to customers on behalf of friendly societies because it enables them to promote and sell their own services prior to the death of the individual in what is known as the “pre-need” market. In 2010, the applicants had a large share of the market in the order of 70%.

74 Funeral bonds can also be sold through financial planners and there is no contact with funeral directors at this time. Such funeral bonds can be converted at a later time to one of the bonds referred to above. Funeral bonds can also be bought directly from a friendly society.

75 Mr Walsh explained the relationship between the client and a particular funeral director in relation to the bonds. I accept his explanation. The first and most common mechanism is that the funeral bond is “assigned” by the client to the funeral director when it is taken out, making the funeral director the owner of the bond, with the client being the “life assured”. The effect of such an arrangement is that the client has assigned all the rights and benefits of the bond, and monies can only be paid to the funeral director upon the death of the life assured. The second mechanism is one whereby the funeral director is nominated as the beneficiary of the bond and on the death of the client, the bond is paid to the funeral director. The client remains the owner of the bond and is able, during their lifetime, to change the nominated beneficiary if they see fit. The third mechanism is for the client to hold the bond as the legal and beneficial owner thereof and, in that case, the funeral director relies on the executor acting for the deceased estate, to honour any pre-arrangement that may be in place.

76 Mr Walsh said, and I accept, that in the case of each method of sale and mechanism through which the benefit is paid to the funeral director, the essential element of a funeral bond is that it can only be claimed following the death of the client and for the purposes of contributing to their funeral expenses.

77 In 2010, Lifeplan and FPM had two main funeral investment products, being a funeral bond, known as the FuneralPlan Bond, and a pre-paid funeral plan known as the FuneralPlan Pre-Paid. Lifeplan manages investment funds for funeral bonds and pre-paid funeral plans and it receives a management fee for those services. FPM markets, distributes and administers the funeral bonds and pre-paid funeral plans through funeral directors. Mr Walsh said, and I accept, that FPM has a commercial relationship with those funeral directors who utilise Lifeplan funeral products in order to support their funeral planning business. FPM provides marketing materials, standard contractual documents and other stationery to those funeral directors and it may also provide specialist sales and marketing advice. FPM may also provide a marketing budget to certain funeral directors to use in promoting Lifeplan’s funeral products. FPM administers the payment of claims out of the Lifeplan Benefit Fund. Mr Walsh said, and I accept, that FPM’s commercial relationships and arrangements with funeral directors provide the key distribution channel for Lifeplan funeral products.

78 Lifeplan owns and has created and developed a suite of documents in relation to the promotion and administration of its funeral bonds and pre-paid funeral plans. Mr Walsh identified these documents as being marketing materials and administrative documentation. The marketing materials include a marketing brochure entitled “The Guide to Pre-Paid Funerals”, a disclosure document entitled “Funeral Plan Pre-Paid”, and a disclosure document entitled “Funeral Plan Bond”. The administrative documents include a pre-paid funeral plan contract, including terms of agreement, a funeral benefit fund claim form, and a stationery request form.

79 Lifeplan maintains template funeral contracts and terms of agreement. They are provided to funeral directors so that they can use them in entering into pre-paid funeral contracts with customers. The contracts comprise a coversheet to be filled in recording the client details, the services agreed upon, and details of the document’s execution and a page of standard terms of agreement. Lifeplan provides the funeral contracts to their funeral directors by way of a contract pad. Lifeplan arranges for funeral directors to include their name, trade mark and contact details on the upper left hand side of the contract. The contracts contain a branding of FPM and references to FPM on the front page and in the terms and conditions. Lifeplan also provides funeral directors with access to the contracts on-line, and if that facility is used, the contracts may be printed and executed in hard copy form.

80 FPM prepares a stationery order form for funeral directors to order supplies of the contracts and Lifeplan promotional materials. It also provides a funeral benefit fund claim form which is completed by the funeral director when the beneficiary of the funeral product dies, and there is either a pre-paid funeral contract in place or a funeral bond which has been assigned or where the funeral director has been nominated as the beneficiary of the funeral bond.

81 In 2001, Lifeplan merged with Norwich Union Friendly Society Ltd (“NUFS”) and as part of that merger, Lifeplan purchased the share capital in Norwich Union Funeral Plan Management Pty Ltd (“NUFPM”) from Norwich Union Holdings Australia Ltd. Before the acquisition, NUFPM promoted and distributed funeral products on behalf of NUFS, and after the acquisition, NUFPM promoted and distributed Lifeplan funeral products through the use of the Norwich Union Funeral Fund Customer Information Brochure. On 25 June 2001, NUFPM changed its name to Funeral Plan Management Pty Ltd (“FPM”). Mr Woff was part of the NUFPM business and after the acquisition, he reported to Mr Walsh in the latter’s executive capacity as general manager, strategic development.

82 Lifeplan merged with Australian Unity in August 2009. Lifeplan is a subsidiary of the Australian Unity Group, and its parent company is Australian Unity Limited.

83 Australian Unity is based in Melbourne. Lifeplan is based in Adelaide. Until shortly prior to May 2012, there was an FPM office in Melbourne which dealt with marketing and distribution.

84 Foresters described itself and FPA in its 2011 Disclosure Documents in the following terms. Foresters is a public company registered under the Corporations Act and a traditional friendly society. It manages the Foresters funeral bond Fund under rules of the Fund and is subject to the Corporations Act and the Life Insurance Act. It administers the Fund and it stated in its disclosure documents in 2011 that FPA promotes and markets the Fund. It describes FPA in those documents as a specialised funeral planning company providing customised administration and marketing services for funeral directors and their clients Australia wide.

85 Mr Hughes expanded on this description in his evidence as follows. Foresters is a public company limited by shares and guarantee. It is registered under s 21 of the Life Insurance Act and has been determined by the APRA to be a friendly society under s 16C of that Act. Its principal activities are the marketing and management of investment and insurance products, including friendly society bonds, funeral bonds, and death and distress benefit funds under an Australian Financial Services Licence. It is regulated by the Australian Securities and Investments Commission under the Corporations Act and prudentially regulated by the APRA under the Life Insurance Act. Foresters currently operates five funeral funds, the two largest being the STL Funeral Benefit Fund established in 1997 and with assets worth $33 million (as at March 2013), and the Funeral Benefit Fund established in 1990 with assets worth $40 million (as at March 2013).

86 There was very significant growth in the business of Foresters between 1997 and 2011. Benefit fund assets comprising funeral benefit fund increased from $19.1 million as at 30 June 1997 to $220.1 million as at 30 June 2011. Management fund assets increased from $3 million as at 30 June 1997 to $14.6 million as at 30 June 2011.

87 The increase in size of the business of Foresters between 2000 and 2010 resulted from the acquisition of various smaller friendly societies, or the transfer of funds operated by them. In October 2000, Foresters had two funeral bond products. In the years that followed, it acquired the businesses of a number of other friendly societies. Until 2008, the State Trustees which in the 2007/2008 financial year had an operating revenue of almost $60 million, invested in the Foresters funeral bond. Tobins invested in Foresters pre-need funeral bond product until 2008.

88 Mr Fleming said, and I accept, that by 2010, the Board of Foresters had concluded that there was limited scope for further growth through the acquisition of other friendly societies or the transfer of other friendly society funds and it directed the chief executive officer, “to identify opportunities for organic growth in our existing funds”.

89 The funeral funds which Foresters had under management increased significantly from 2011 when Mr Woff and Mr Corby were engaged as employees of Foresters. The funeral fund of Foresters which is the subject of the proceeding was established on 3 December 1990 and is known as the “Foresters Funeral Benefit Fund – Exempt and Taxable” (“Foresters Funeral Fund”). Foresters manages other funeral funds, including STL (or State Trustees), Funeral Benefit Fund and MUA Bluechip Funeral Fund. As at 30 June 2010, the balance of the Foresters Funeral Fund was $13,238,399, and as at 30 June 2013, the balance of the Foresters Funeral Fund was $62,940,608. The Foresters Funeral Fund is an “approval benefit fund” for the purposes of the Life Insurance Act.

90 Mr Hughes described the features of a funeral bond and his description does not differ in any material way from that given by Mr Walsh. In general terms, funeral bonds involve an investment by an individual so as to provide for the payment in due course of their funeral expenses, and the benefit of the investment may or may not be assigned to a funeral director. Pre-paid funeral plans involve an investment by an individual in conjunction with the execution of a fixed price funeral contract between the individual and a funeral director. Under the plan, the individual assigns the benefit of their investment, but not their membership of the fund, to the funeral director.

91 In the case of Foresters Funeral Fund, the individual and not the funeral director is always the member of the Fund and even if the individual assigns the benefit of the investment to a particular funeral director, the individual and not the funeral director remains the member of the Fund. The Foresters Funeral Fund is and always has been capital guaranteed and this means that the “guarantee” is supported by the solvency reserves maintained by Foresters in accordance with APRA regulatory requirements.

92 In 2010, Foresters had a disclosure document in relation to each of its funds.

Lifeplan and Mr Woff and Mr Corby

93 Mr Woff commenced employment with NUFPM as a funeral fund manager on 2 April 1990. His employment was transferred to Lifeplan following the acquisition of NUFPM and the terms of his employment are recorded in a letter dated 27 March 2001.

94 Mr Woff operated the FPM office in Melbourne where he supervised on average four to five staff members. He reported to Mr Walsh. The FPM office in Melbourne was engaged in the promotion and distribution activities of FPM and the administration of the funeral products was carried out in Lifeplan’s offices in Adelaide. Mr Woff’s position was described as “Manager, Funeral Plan Management”. Mr Walsh described that position as a senior management position and I accept that that was the case. Mr Woff was responsible for the oversight of the marketing and distribution arm of FPM and Lifeplan’s funeral director based funeral product business. Mr Woff’s remuneration in 2010, including salary and bonuses, was $333,000 per annum.

95 Mr Walsh said, and I accept, that Mr Woff had overall responsibility for maintaining and protecting Lifeplan’s distribution network of funeral directors. He, together with other staff, helped deliver Lifeplan’s package of products and services to funeral directors. He exercised a fair degree of autonomy in managing the day-to-day activities of the operation.

96 On 13 July 2006, Mr Woff executed a Confidentiality Declaration and an Intellectual Property Rights Declaration. In the Confidentiality Declaration he acknowledged that he would use all confidential information received in connection with his employment only for that employment and that, except in the proper performance of his duties, he would not copy or disclose to any person, any information with respect to the affairs of Lifeplan whilst an employee or after he had ceased to be an employee. In the Intellectual Property Rights Declaration he acknowledged that Lifeplan owned all intellectual property rights arising as a direct or indirect result of the performance of his employment. On 13 July 2006, Mr Woff executed an acknowledgement that he would abide by a Technology Usage Guide and Agreement which imposed restrictions on the usage of Lifeplan’s computer system, including in relation to confidential and sensitive information.

97 Mr Woff was an employee of Lifeplan and, therefore, subject to the duties in s 182 (not to use his position improperly), and s 183 (not to use information improperly) of the Corporations Act. The applicants also allege that he was an “officer” of both applicants and, therefore, subject to the duties in s 180 (to exercise reasonable care and diligence), and s 181 (to act in good faith in the best interests of the corporation and for a proper purpose) of the Corporations Act. The term “officer” is defined in s 9 of the Corporations Act to mean a person who makes, or participates in making, decisions that affect the whole, or a substantial part, of the business of the corporation; or who has the capacity to affect significantly the corporation’s financial standing; or in accordance with whose instructions or wishes the directors of the corporation are accustomed to act. In addition to the matters referred to in paragraphs 94 and 95, Mr Walsh said that Mr Woff made and participated in making decisions that affected the whole of the business of FPM and a substantial part of the business of Lifeplan. That evidence of Mr Walsh is a conclusion expressed in terms of paragraph (b)(i) of the definition of officer in s 9 of the Corporations Act. I do not think I should accept it without examining whether it is supported by specific evidence. Mr Walsh said, and I accept, that Mr Woff attended strategic business planning events for Lifeplan and, at least, one off-site strategic meeting of senior executives of Australian Unity Executives and presented on the strategic approach he would be implementing at FPM. Mr Woff’s job description included the following responsibilities:

… manage business unit with particular emphasis on relationship management to protect existing client bases, driving sales to increase market share and develop and implement specific business strategies to secure business units continued future success …

Maintain strong relationships with existing funeral firms and in particular the top ten accounts.

98 Mr Woff denied that he was an officer of either applicant. He gave evidence that in his 10 years at Lifeplan, he had attended only one, possibly two, meetings of the Board of Lifeplan. He gave evidence that the Australian Unity/Lifeplan group was a large organisation, that he reported to Mr Walsh, and that at the end of his employment he was the only person in the FPM office in Melbourne.

99 Notwithstanding those matters, Mr Woff was the senior manager of FPM charged with, among other responsibilities, the responsibility of creating and maintaining relationships with funeral directors. I think he made and participated in the making of decisions that affected the whole, or a substantial part, of the business of FPM and I hold that he was an officer of FPM within s 9 of the Corporations Act. Although I am prepared to accept that the funeral fund business was an important aspect of Lifeplan’s business and FPM was a wholly-owned subsidiary of Lifeplan, I do not think the conclusion that Mr Woff was an officer of FPM means that he was also an officer of Lifeplan. In order to address that issue, I would need evidence of Lifeplan’s overall business and the place of FPM’s business in that business. I do not have specific evidence on that matter and, in those circumstances, I am not prepared to hold that Mr Woff was an officer of Lifeplan.

100 Mr Woff resigned on 1 December 2010. His resignation was effective on 29 December 2010. At the time of his resignation, Mr Woff spoke to Mr Walsh on the telephone and told him that he was joining Foresters.

101 Mr Corby commenced employment as National Sales Manager for FPM on 16 December 2002. He signed a letter of employment dated 11 November 2002. Mr Corby was based in FPM’s office in Melbourne and he reported to Mr Woff. Mr Corby’s maximum annual remuneration in 2010, including salary and bonuses was $163,338. Mr Corby’s position required him to oversee the sales performance of the business unit and that required him to service existing clients and recruit new ones.

102 Mr Corby also signed a Confidentiality Declaration and an Intellectual Property Rights Declaration and a Technology Usage Guide and Agreement in July 2006. Mr Corby had, in fact, executed an earlier Confidentiality Declaration in November 2002.

103 On 28 October 2010, Mr Woff advised Mr Walsh that Mr Corby had handed in his resignation effective on 25 November 2010.

104 In June 2010, the FPM sales team consisted of Mr Woff, Mr Corby, Ms Alisha Nee and Ms Keira Anderson. Ms Anderson’s role was principally to provide administrative support for the FPM sales team of Mr Woff, Mr Corby and Ms Nee. For example, she prepared the paperwork for invoice payment, travel bookings, credit card statement reconciliations, and she organised the dispatch of documents to funeral directors.

105 Ms Nee’s role was principally to provide sales services to funeral directors and that included attending to the customisation of contract pads, stock control, organising the dispatch of documents to funeral directors, following up on inquiries, assisting with the training of funeral directors in the use of what was described as the FPM Business System, and general relationship management of Lifeplan and FPM’s funeral director client base. Ms Nee focussed on sales to smaller funeral directors.

106 On 23 July 2010, Ms Anderson handed in her notice of resignation. Mr Woff advised Mr Walsh that Ms Anderson’s role did not require a replacement, explaining that his remaining team members could absorb her workload. Ms Anderson’s last day at Lifeplan was 6 August 2010. On 7 October 2010, Ms Nee handed in her notice of resignation.

107 In October 2010, the work performed by Ms Anderson and Ms Nee was taken over by staff in the Adelaide office. In the same month, there was correspondence between Mr Woff and Mr Walsh concerning Ms Nee’s replacement. Mr Woff suggested that Lifeplan and FPM replace Ms Nee by employing another administrative person in Adelaide not Melbourne.

108 Ms Nee’s last day at Lifeplan was 28 October 2010. On the same day, Mr Corby handed in his notice of resignation. Mr Woff advised Mr Walsh that Mr Corby had indicated to him that he wanted to take a break and “then that he has a couple of business opportunities to pursue with friends in January”. Mr Woff later advised Mr Walsh:

From what I can gather he has an opportunity to either buy into or join a couple of mates in the recruitment field.

109 On 1 November 2010, Mr Woff wrote to Mr Walsh suggesting that there was no need to replace Mr Corby immediately, although he again suggested that there was a need for someone in Adelaide to perform administrative tasks. As previously noted, Mr Corby’s last day at Lifeplan was 25 November 2010.

110 On 1 December 2010, Mr Woff handed in his notice of resignation. Mr Woff spoke to Mr Walsh on the telephone and Mr Woff advised Mr Walsh that he had received an offer to move into a “general manager” role at Foresters with the potential to move into a CEO role when Mr Hughes retired. Mr Walsh contacted his superior and it was decided that Mr George Takianos would take over Mr Woff’s sales management role at FPM. On 3 December 2010, Mr Takianos recommended to Mr Walsh that Mr Trevor Holst replace Mr Corby. On 15 December 2010, Mr Takianos appointed Mr Holst as the business development manager for FPM. FPM advised funeral directors of the staff changes. On 15 January 2011, Ms Maria Messineo commenced as business development assistant/sales team coordinator for the sales team. She was based in Adelaide.

111 FPA was incorporated on 11 November 2010 and it signed a Marketing & Service Agreement with Foresters on 31 December 2010. Mr Corby commenced employment with Foresters on 6 December 2010, and Mr Woff commenced employment with Foresters on 4 January 2011.

112 Shortly after 21 February 2011, Mr Walsh’s executive assistant, Ms Michelle Rawe, noticed an email on Mr Woff’s Lifeplan email account which caused Mr Walsh to investigate further. He took steps to search Mr Woff’s Lifeplan email account, but not much was revealed by those searches. He did search FPA and discovered that Mr Woff and Mr Corby were directors of that company.

113 Mr Walsh was concerned about the activities of Mr Woff, Mr Corby, FPA and Foresters, and in May 2011, he became aware that a funeral director seeking to order FPA stationery forms had contacted Lifeplan to place an order. In early June 2011, the administration team at Lifeplan received a pre-paid contract that was meant for Foresters but was sent to Lifeplan. The pre-paid contract had an FPA logo on it. In late June 2011, Mr Walsh discovered from an article in the Journal of the Funeral Directors Association of New South Wales that FPA formed and operated by Mr Woff and Mr Corby had entered the pre-paid funeral plan market. On 10 August 2011, Lifeplan received a second “lot” of pre-paid contracts intended for Foresters and containing an FPA logo.

114 Mr Walsh obtained brochures and disclosure documents of FPA and arranged for them to be compared with those of FPM. He noted a number of similarities. He also obtained claim forms, stationery request forms and pre-paid contracts of FPA.

115 In August 2011, Mr Walsh commenced a process which led to the restoration of a number of emails in Mr Woff’s Lifeplan email account. These emails had been deleted from his inbox and sent items, and then deleted from his deleted items file. There were 10,000 emails restored, 5,000 of which needed to be reviewed one by one. A large number of emails had been sent to Mr Woff’s private email address.

116 It became apparent from Mr Walsh’s investigations that Mr Woff and Mr Corby whilst employed by Lifeplan were taking steps preparatory to the establishment of another business. For example, they were drafting flyers. Mr Woff emailed from his Lifeplan email address to ichbinnoddy@hotmail.com on 7 September 2010 a document entitled “Recipe”. This document is referred to in more detail below (at [171]). The steps Mr Woff and Mr Corby were taking included considering registration of a funeral contribution fund, and contact with MGR Accountants concerning a proposed venture.

117 Mr Woff sent a number of documents to his private email address principally between July and December 2010. In this section, I will concentrate largely on those documents which are identified in Annexure A and Annexure B.

118 On 6 October 2010, Mr Woff sent an email with an attachment from his Lifeplan email address to his private email address. The subject of the email was “Claims History” and the attachment was a Claims History Spreadsheet containing Lifeplan’s claims history since 1990 (A1, B7). This document contained information on the behaviour of Lifeplan’s funds and was plainly a confidential document.

119 On 18 October 2010, Mr Woff sent an email with attachments from his Lifeplan email address to his private email address. The subject of the email was “FW: Info. For future reference” and the attachments were as follows:

(1) Lifeplan Interest Calculation Spreadsheet being a spreadsheet of bonus rates paid in relation to investment products dating from 1988 to 2004 (A2, B8).

(2) Funeral Plan Management Spreadsheet of Benefit Holders being a document containing personal information of benefit holders with a range of funeral directors (A3, B10).

(3) Funeral Plan Management New Funeral Director Checklist being a document showing processes and tasks required to be completed for the establishment of a new commercial relationship with a new funeral director (A4, B12).

(4) Funeral Plan Management New Funeral Director Checklist – Administration being a document showing a list of questions to be posed to a new funeral director in order to establish a file for that funeral director (A5, B13).

(5) Funeral Plan Management Original FD Authority to Pay being a form used by FPM for the authorisation of payments of benefits to funeral directors (B9).

(6) Funeral Plan Management Template Letter to Funeral Director (B11).

(7) Funeral Plan Management Pre-Paid Funeral Plan Application Procedure being a flow chart showing the process whereby a funeral director completes an application for a new client’s funeral plan in conjunction with FPM (B14).

(8) Funeral Plan Management Steps in Completing Documentation for Pre-Paid Funerals being a step-by-step description of what is required in order for a funeral director to complete documentation for pre-paid funerals (B15).

(9) Funeral Plan Management Funeral Bond Procedure Flowchart being a flow chart showing the process for a funeral director to assist a client with an application for a new funeral bond in conjunction with FPM (B16).

(10) Funeral Plan Management Steps in Completing Documentation for Funeral Bonds being a document showing a step-by-step guide to completing documentation for funeral bonds (B17).

(11) Funeral Plan Management Steps in Completing Documentation for Making a Claim on Pre-Paid Funeral Plan or Funeral Bond being a step-by-step guide to the same (B18).

(12) Funeral Plan Management Pre-Need Promotion Evaluation Form being a form providing for funeral directors to give feedback to FPM on a promotion of pre-need funeral products (B19).

120 Mr Walsh said, and I accept, that the documents described in paragraphs (2), (3) and (4) contain confidential information of the applicants and that the document described in paragraph (11) is intellectual property of the applicants. These documents and the other documents are important administrative documents of FPM used in the administration of funeral products.

121 Later on the same day, Mr Woff sent an email with an attachment from his Lifeplan email address to his private email address. The subject of the email was “Cash Flow Story - Update” and the attachment was entitled “Cash Flow Story - Draft” which Mr Walsh described as marketing material connected to cash flow projections for pre-need funeral products (A30, B59). The document includes a table containing data which is almost identical to data in the Claims History Spreadsheet (A1, B7).