FEDERAL COURT OF AUSTRALIA

Crescent Capital Partners Management Pty Limited v Crescent Funds Management (Aust) Limited [2016] FCA 229

File number: | NSD 448 of 2014 |

Judge: | BENNETT J |

Date of judgment: | 9 March 2016 |

Catchwords: | TRADE PRACTICES – misleading and deceptive conduct claims brought under Australian Consumer Law and Australian Securities and Investments Commission Act 2001 (Cth) – companies engaged in financial services industry – whether contravening conduct established – whether business names, domain names and business activities sufficiently similar to be confusing and causative of contravening conduct – whether financial services market susceptible to division on basis of asset classes – whether financial services market susceptible to division on basis of investor characteristics – whether distinction between sophisticated investors and other investors relevant – whether distinction between retail and wholesale investors relevant TRADE PRACTICES – claims of accessorial liability for misleading and deceptive conduct of others – whether respondents could be said to have participated with requisite knowledge in contravening conduct |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) ss 5(2)(b), 12DA, 12DB, 12GD, 12GF Competition and Consumer Act 2010 (Cth), Sch 2 ss 2, 18, 29 Corporations Act 2001 (Cth) ss 79, 761G Corporations Regulations 2001 (Cth) regs 7.1.18(2), 7.1.19(2), 7.1.28 |

Cases cited: | Anchorage Capital Partners Pty Ltd v ACPA Pty Ltd (2015) 115 IPR 67 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd (2014) 317 ALR 73 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640 Bridge Stockbrokers Ltd v Bridge (1984) 4 FCR 460 Campomar Sociedad Limitada v Nike International Ltd (2000) 202 CLR 45 Cassidy v NRMA Health Pty Ltd [2002] FCA 1228 Chase Manhattan Overseas Corporation v Chase Corporation Ltd (1986) 12 FCR 375 Roumanus v Orchard Holdings (NSW) Pty Limited (in Liq) (2012) 90 ACSR 677 Yorke v Lucas (1985) 158 CLR 661 |

Date of hearing: | 31 August, 1, 2, 3, 4 September 2015 |

Registry: | New South Wales |

Division: | General Division |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Category: | Catchwords |

Number of Paragraphs: | 93 |

Counsel for the Applicants: | Mr R Cobden SC with Ms E Whitby |

Solicitor for the Applicants: | Gilbert + Tobin |

Counsel for the Respondents: | Mr MJ Darke SC with Ms C Bembrick |

Solicitor for the Respondents: | Corrs Chambers Westgarth |

ORDERS

JUDGE: | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties confer and submit agreed or, if there is no agreement, competing orders to give effect to these reasons by Friday 11 March 2016 at 12 noon.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BENNETT J:

1 This proceeding concerns a number of corporations and businesses operating in the financial services industry which possess somewhat similar names. Relevantly, both the applicants and many of the respondents have names which feature the word “Crescent”. Moreover, the unchallenged evidence is that both the applicants and the respondents refer to themselves, for example on their websites, and are referred to by others, for example by the media as, simply, Crescent.

2 The applicants, Crescent Capital Partners Management Pty Ltd and Crescent Capital Partners Ltd (together, Crescent Capital), contend that various of the respondent entities’ names (Crescent Funds Management (Aust) Ltd, Crescent Investments Australasia Pty Ltd, Crescent Consolidated Group Holdings Pty Ltd, Crescent Financial Services Pty Ltd, Crescent Foundation Fund Pty Ltd, Crescent Holdings Australia Pty Ltd and Crescent Super Pty Ltd (together, Crescent Wealth)) are misleadingly or deceptively similar to its own name, such that those respondents have falsely or misleadingly made representations in trade or commerce that their services and products are in some way connected to Crescent Capital. Crescent Capital abandoned the passing off case which had been initially pleaded at the hearing, as well as its claim against the eighth respondent (the Crescent Institute).

3 Crescent Capital seeks relief, relevantly, under ss 18 and 29 of the Australian Consumer Law (the ACL), contained in Sch 2 to the Competition and Consumer Act 2010 (Cth) and ss 12DA and 12DB of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act). Further, it claims that all of the respondents and in particular the ninth and tenth respondents (Yassine Corporation and Mr Yassine) are liable as accessories to the other respondents’ contraventions.

4 Crescent Wealth, for its part, sought to resist Crescent Capital’s claims, by distinguishing the nature of its activities from those in which Crescent Capital engages, so as to demonstrate the unlikelihood of anyone being led into error by the similarity of the names Crescent Wealth and Crescent Capital.

5 For the reasons which follow, I have decided that Crescent Capital should have certain of the the relief which it seeks. I will first consider Crescent Capital’s case concerning the activities of Crescent Wealth and then turn to the liability of each of the respondents.

FACTUAL BACKGROUND

6 The evidence as to the history of the parties and the use of the “Crescent” name was not in dispute, but is relevant to an understanding of the nature of the businesses operated by the parties, the persons to whom their activities are directed, and the manner in which those persons would understand the parties’ activities.

(i) Crescent Capital

7 The first applicant has held a licence to provide financial advice, products and services since on or about 24 November 2000 and the second applicant has, since 27 July 2004, been an authorised representative under that licence. Crescent Capital operates a business managing private equity funds. It has done so since around November 2000. The evidence is that Crescent Capital selected “Crescent” because it comes from the Latin word ‘cresco’, meaning grow, expand or increase, no doubt both an apt and aspirational name for an investment business. There is evidence that Crescent Capital, until about September 2010, utilised a logo which featured a crescent shape, together with the words ‘Crescent Capital Partners’. The logo no longer features a crescent shape, but does feature an emboldened “Crescent” (see [30] below). There was further evidence that this logo is used by Crescent Capital, including on invoices, stationery, and promotional and marketing materials. I accept that Crescent Capital has made such use of the logo and the name.

8 Further, since at least 28 November 2000, Crescent Capital has operated a website with the domain name crescentcap.com.au.

9 Crescent Capital has established, and there is no real dispute, that as at and since the commencement of Crescent Wealth’s activities in 2010, it had and has a reputation and goodwill in the financial services and financial management industry in the name Crescent Capital, and is often referred to as Crescent. That reputation derives from its own activities, from its approaches to investors and financial advisors, as the recipient of awards and from its activities in raising money for investment in its funds (which include the use of promotional and marketing materials), as well as from media reports.

10 Crescent Capital has won a number of awards from the Australian Private Equity & Venture Capital Association Limited for investments in which it has been involved, including for ‘management buyouts’ of a window business known as Trend/Breezway in 2003 and a travel insurance business known as Cover-More in 2014. In addition, Crescent Capital’s investment activities have garnered media coverage in such publications as the Australian Financial Review and the Sydney Morning Herald.

11 I accept that Crescent Capital has developed a reputation among the financial community as a successful private equity fund manager.

12 Crescent Capital describes its business as follows:

Crescent Capital operates a private equity funds management business. It raises money from investors and uses these funds either to invest directly into a business or to acquire the business and typically holds its investment for three to six years with the aim of improving and growing the underlying business, before selling it and returning the proceeds to investors (after Crescent Capital’s fees are paid). Crescent Capital raises money in a series of pools, called “funds”, and approaches new and existing investors and offers the opportunity to invest in (also called “subscribe to”) the new fund.

13 Crescent Capital has raised money for a series of funds. The investments into Crescent Capital’s first fund came from both “retail clients” and “wholesale clients”. These expressions have some significance, as Crescent Wealth relies upon this distinction between investors as a key basis for differentiating itself from Crescent Capital. It says that this differentiation removes any possible confusion between the parties and answers Crescent Capital’s claims of misleading and deceptive conduct.

14 It is convenient to consider the expression “wholesale” client first. Section 761G(7) of the Corporations Act 2001 (Cth) and Pt 6D.5, Div 2 of the Corporations Regulations 2001 (Cth) relevantly provides when a person will be a wholesale client. Where, inter alia, the price of the financial product, or the value of the financial product to which a financial service relates, is greater than or equal to $500,000 (see regs 7.1.18(2) and 7.1.19(2)), or the financial product or service is being acquired by a person who has previously provided a copy of a certificate from a qualified accountant, which states that the acquirer has net assets of at least $2.5 million or a gross income for each of the last two financial years of at least $250,000 (see reg 7.1.28), or the person is a professional investor, then the person is a wholesale client. A retail client is simply one who is not a wholesale client (s 761G(1)).

15 The parties commonly referred to these concepts, using the language of “investors” rather than clients. The references in these reasons to retail and wholesale investors should be understood as incorporating this distinction.

16 Other matters relevant to the description of Crescent Capital’s business are, put shortly:

A fund is closed once the monetary target is reached or when some pre-determined period of time elapses.

There is then a call on committed funds from investors, as Crescent Capital identifies suitable investments over a ten year life of the fund, being a business identified as capable of generating the required rate of return on investment.

Crescent Capital specialises in acquiring or investing in small to medium sized, privately owned businesses.

The businesses which Crescent Capital targets are usually located in Australia and New Zealand, with enterprise values between AUD$50 and $300 million.

Crescent Capital has also acquired smaller Australian and New Zealand based businesses to integrate into an existing larger business. Sometimes smaller businesses are acquired as part of a ‘roll-up’ or aggregation strategy; for example, there was evidence that Crescent Capital had engaged in such activity in respect of dental practices with individual values of as little as $1 million.

The businesses are operated with a view to sale or listing on the stock exchange.

The business model requires Crescent Capital to take control of a company or group in which it invests and to offer value-added services to companies in which it invests, such as providing strategic advice and introducing alliance networks.

The first fund (Crescent I) raised $25 million in 2001, the second (Crescent II) $100 million in 2004, the third (Crescent III) $400 million in 2007 and the fourth (Crescent IV) $490 million in 2012. There is a further fund, Crescent V, the amount raised is confidential, but it is substantial.

Since 2004, funds have been raised exclusively from wholesale investors.

Returns are through long term capital appreciation rather than through immediate and regular payments of principal and interest. Investors’ money, once committed, is tied up for the life of the fund, viz. ten years.

It engages in fund raising every three to four years, approaching both new and existing investors.

Crescent Capital does not advertise to the general public. It does operate a website, of which only part is publicly accessible.

Crescent Capital is frequently referred to in the financial media by reference to its name, Crescent Capital Partners, or simply as Crescent.

17 Only Crescent I raised money from retail investors although Crescent Capital, through Crescent Capital Partners Management Pty Ltd’s financial services licence, retains the ability to approach retail investors. Superannuation funds and large institutions represent the majority of investors in the funds. The minimum amount for investing in the most recent fund is confidential but is substantially higher than the $250,000 that was the minimum for the second fund, Crescent II. The average amount invested by each investor for Crescent IV was extremely high. Participation in funds after Crescent I has, in effect, been by invitation.

18 Investment in Crescent Capital’s funds can be characterised as high risk, high return investment and requires long term commitment of funds with no certainty of returns. Investors, including prospective investors, can be characterised as highly sophisticated investors who consider investments carefully before proceeding. Many of those investors use expert advisers and many are large institutions or high net worth individuals.

(ii) Crescent Wealth

19 Crescent Wealth’s business is concerned with the making of investments. It offers Sharia compliant superannuation, via the Crescent Wealth Superannuation Fund, and additional managed investment products to the public.

20 It could be said to operate a wealth management business. Crescent Wealth has taken steps to ensure that its Sharia compliant products accord with the highest international standards of Sharia compliance.

21 Although Crescent Wealth invests, and promotes itself as investing, in Sharia compliant services, its Australian Financial Services Licence is not so limited. It is authorised to provide financial services to retail and wholesale clients of any, or no, faith, including high net worth individuals and financial planners. Crescent Wealth’s marketing is directed toward the public at large, with a particular emphasis on retail investors of the Islamic faith. It does have a significant institutional investment, of $1.5 million, from Aon Hewitt, an Australian superannuation fund.

22 At the end of 2014, Crescent Wealth had funds under management of approximately $70 million and about 3,000 members. It predicted that by the end of 2015 it would have funds under management of approximately $150 million to $200 million.

23 The managed investments which Crescent Wealth offers (the Crescent Australia Equity Fund, the Crescent Wealth International Equity Fund, the Crescent Diversified Property Fund and the Crescent Islamic Cash Fund) are not managed by Crescent Wealth; rather it engages a range of third party investment managers, such as the Bank of London and Middle East and HSBC Amanah. The proportion of an investor’s superannuation contributions invested in each Crescent Wealth product depends on the investor’s choice between “growth”, “balanced” and “conservative” investment options. The products are designed for, and available to, retail investors. They are low risk and low return, especially when compared to the returns expected from Crescent Capital’s funds. Returns are distributed regularly and the superannuation product has no minimum investment requirement; the other managed investment products each have a minimum requirement for direct investment of $5000, subject to a discretion to accept lower investment amounts. Funds can be withdrawn by an investor at any time.

24 It is convenient at this point to say something about the Sharia compliant financial products which Crescent Wealth offers. Essentially, Crescent Wealth’s funds avoid making investments which would offend against principles that have been derived from the Islamic faith. In this regard, the ‘Crescent Wealth Superannuation – Investment Choice Guide’ states:

Permissible Investments are investments which do not derive their income or gains from Non-Permissible Activities. Non-Permissible Activities include gambling, sale or manufacture of weaponry, sale or manufacture of alcohol, tobacco, sale or production of adult material, conventional financial services and other activities that Crescent Wealth, on advice of the SSB [Shariah Supervisory Board] may deem to be Non-Permissible.

Depending on the type of asset or asset class, certain assets may be considered Permissible Investments even where a small proportion of their income is derived from Non-Permissible Activities, provided that they meet the limits of Non-Permissible Activities as set out below. These limits are set by the AAOIFI [Accounting and Auditing Organisation for Islamic Financial Institutions, the global not-for-profit organisation that maintains and promotes Islamic investment standards for Islamic financial institutions, participants and the overall industry].

25 Any prohibited income generated, such as income derived by the payment of interest, is ‘cleansed’ by distributing it to the fifth respondent (the Foundation) which, in turn, makes donations to Australian registered charities of corresponding amounts. The Foundation does not offer goods or services to the public, but plays an integral role in ensuring that Crescent Wealth remains Sharia compliant.

26 Crescent Wealth’s efforts to ensure that its products remain Sharia compliant are, indeed, extensive. As the above extract from the ‘Crescent Wealth Superannuation – Investment Choice Guide’, together with the evidence of one of Crescent Wealth’s directors, Professor Yerbury, demonstrates, Crescent Wealth has adopted a number of distinctive procedures to ensure the ongoing compliance with Islamic financial principles. These include:

ensuring that investments comply with Accounting and Auditing Organisation for Islamic Financial Institutions standards, viz. the global standards for Islamic investment principles. The effort involved in this regard is considerable, as the standards mean, for example, that investments can only be made in companies with certain debt to equity ratios;

implementing the review of investments by the Shariah Supervisory Board (the SSB), which is comprised of Islamic experts and scholars;

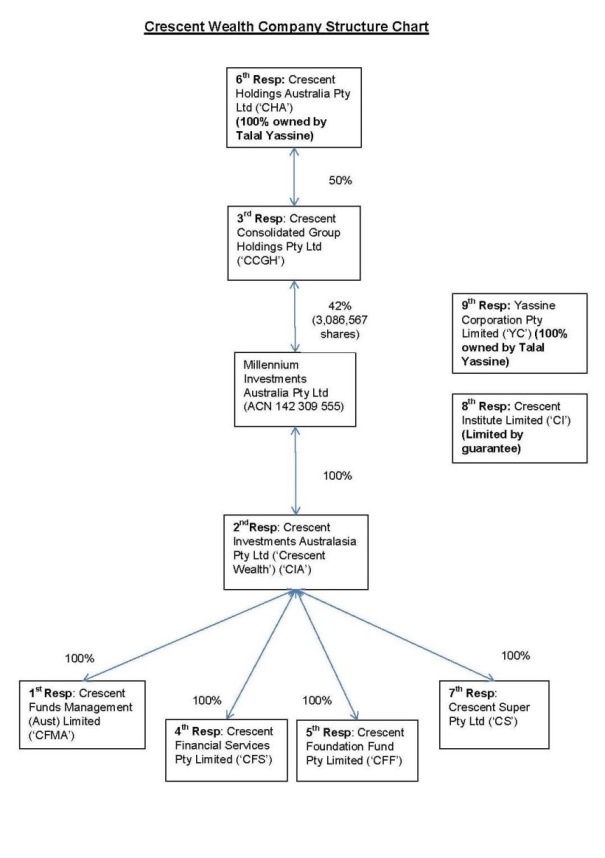

ensuring that investments comply with the various Fatwas (rulings) issued by the SSB;

engaging an Islamic investment firm, Ideal Ratings, to analyse each investment; and

ensuring that profits from prohibited sources are ‘cleansed’ by the Foundation, as already explained.

27 I accept that adherence to Islamic investment principles is a core component of Crescent Wealth’s business and investment strategy. Moreover, it is apparent, and I accept, that Crescent Wealth has established a reputation in relation to Sharia compliant financial products.

28 Crescent Wealth’s superannuation offering is its primary product, with 80% to 90% of the funds under management by Crescent Wealth attributable to superannuation. Nevertheless, Crescent Wealth also accepts investments into the managed investment products directly. Such investment accounts for the remaining 10% to 20% of the funds it manages.

29 Crescent Wealth is the registered owner of several domain names. These domain names, and the relevant dates from which Crescent Wealth has been their registered owner, are as follows:

crescentinvestments.com.au (from around 25 June 2014);

crescentwealth.com.au (from around 16 April 2014);

crescentfunds.com.au (from around 25 June 2014);

crescentfunds.net (from around 25 June 2014); and

crescentinstitute.com.au (from around 16 April 2014).

Further, since about 29 March 2012 it has operated a Facebook page and since around 17 December 2012 it has operated a YouTube channel.

(iii) The parties’ logos

30 The respective logos of the parties are quite different:

RELEVANT STATUTORY PROVISIONS

31 As noted above at [3], Crescent Capital’s claims against Crescent Wealth are made under the ACL and the ASIC Act.

32 Sections 18 and 29 of the ACL provide, relevantly, as follows:

18 Misleading or deceptive conduct

(1) A person must not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive.

…

29 False or misleading representations about goods or services

(1) A person must not, in trade or commerce, in connection with the supply or possible supply of goods or services or in connection with the promotion by any means of the supply or use of goods or services:

…

(b) make a false or misleading representation that services are of a particular standard, quality, value or grade; or

…

(g) make a false or misleading representation that goods or services have sponsorship, approval, performance characteristics, accessories, uses or benefits; or

(h) make a false or misleading representation that the person making the representation has a sponsorship, approval or affiliation; or

…

33 Sections 12DA and 12DB of the ASIC Act provide, relevantly, as follows:

12DA Misleading or deceptive conduct

(1) A person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive.

…

12DB False or misleading representations

(1) A person must not, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion by any means of the supply or use of financial services:

(a) make a false or misleading representation that services are of a particular standard, quality, value or grade; or

…

(e) make a false or misleading representation that services have sponsorship, approval, performance characteristics, uses or benefits; or

(f) make a false or misleading representation that the person making the representation has a sponsorship, approval or affiliation; or

…

34 Crescent Capital also claims that each respondent was ‘involved’ in each other respondent’s contraventions within the meaning of the definition of that term in s 2 of the ACL, or otherwise liable under ss 12GD and 12GF of the ASIC Act.

35 The definition in s 2 of the ACL is as follows:

involved: a person is involved, in a contravention of a provision of this Schedule or in conduct that constitutes such a contravention, if the person:

(a) has aided, abetted, counselled or procured the contravention; or

(b) has induced, whether by threats or promises or otherwise, the contravention; or

(c) has been in any way, directly or indirectly, knowingly concerned in, or party to, the contravention; or

(d) has conspired with others to effect the contravention.

36 Section 12GD of the ASIC Act is relied on by Crescent Capital as a basis for enjoining the respondents from continuing to engage in, or otherwise be involved in, contraventions of ss 12DA and 12DB.

37 Crescent Capital claims under s 12GF of the ASIC Act for loss or damage said to have been occasioned by it as a result of the respondents alleged contraventions of ss 12DA and 12DB. However, the trial was confined to the issue of liability only.

LEGAL PRINCIPLES

38 The legal principles relevant to a consideration of ss 18 and 29 of the ACL, which are mirrored in ss 12 DA and 12 DB of the ASIC Act and apply to conduct in relation to ‘financial services’, are not in contention. Relevantly, and drawing from, inter alia, the discussion in Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd (2014) 317 ALR 73 and Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640:

It is necessary to view the conduct as a whole and in its proper context, taking account of the type of market, the manner in which goods are sold and the characteristics of purchasers.

The conduct is judged by the effect on the “ordinary” or “reasonable” member of the class of prospective purchasers of that product or service.

The relevant language is “likely” to mislead or deceive, not “liable” to mislead or deceive.

For a representation to be misleading or deceptive, a not insignificant number of investors must be drawn into negotiation on the basis of an erroneous belief engendered by the message conveyed by the person in question.

The conduct to be examined is the actual or threatened conduct, as directed to the class of persons.

A distinction is to be drawn between the standard of misleading or deceptive conduct and conduct that gives “cause to wonder”.

The question is whether ordinary or reasonable members of the class of consumers will, or are likely to, mistakenly infer from the use of a business name that one business is connected with another business.

In looking to future changes in the activity of parties, there must be at least a real prospect based on the evidence of those changes occurring.

39 In Chase Manhattan Overseas Corporation v Chase Corporation Ltd (1986) 12 FCR 375, a case that bears some factual similarity with this case, the Full Court observed that considerations for the purposes of a contravention of s 52 of the Trade Practices Act (the predecessor to s 18 of the ACL) include existing common fields of business activity as a relevant but not necessary factor, and whether there are business activities in which the parties intend to engage which will overlap, where the intended activities are natural extensions of the relevant businesses.

40 As to the application of accessorial liability notions, captured by the expression ‘involved’ in the ACL, it is well-settled that an accessory must have had actual knowledge of the facts giving rise to a contravention, where those facts correspond with the essential elements of the offence (Yorke v Lucas (1985) 158 CLR 661 at 666-670; Cassidy v NRMA Health Pty Ltd [2002] FCA 1228 at [72]-[73]). Further, the accessory must have intentionally participated in or assented to, the contravention committed by the primary wrongdoer.

41 The contest between the parties concerns the application of these principles. Crescent Capital’s pleaded case is that it had acquired a reputation in the use of “Crescent” in respect of financial services and products, specifically in the context of managed investments, such that, when Crescent Wealth commenced operating in the same financial services and products market, the use of “Crescent” by Crescent Wealth involved the making of representations that Crescent Wealth’s products and services were:

(1) those of Crescent Capital;

(2) marketed, offered or promoted by Crescent Capital or a company associated with them or otherwise licenced, sponsored or approved by them; and/or

(3) of the same standard, quality, value and grade as Crescent Capital’s products and services.

42 The dispute primarily centred on the extent to which it could be said that the parties operated in the same market and whether the participants in that market, if there be a single common market in which they operate, would be likely to be misled or deceived by Crescent Wealth’s conduct.

SUBMISSIONS

43 Crescent Capital submits that there is nothing inherently Islamic about CRESCENT or a crescent symbol and points out that Crescent Wealth’s logos did not and do not project an Islamic image. It submits that the ordinary consumer would not make such an association. Crescent Capital points out that the Crescent Wealth name and the names of its funds are put before the public in many non-Islamic contexts, such as in the media and in the receipt of awards.

44 Crescent Capital’s submissions focus on what it terms “likely markets”, while accepting that such an analysis must be realistic on the evidence. Its submissions recite the fact that Crescent I did target retail investors, that Crescent Wealth’s subscribers include persons with ‘considerable amounts’ to invest and that Crescent Wealth’s marketing plan of late 2014 includes high net worth individuals and financial advisors, with its growth trend suggesting $1 billion under management by August 2017. Thus, Crescent Capital says, Crescent Wealth is in no way limited to “mum and dad investors”. In addition, Mr Yassine accepted that Crescent Wealth intends to attract large resources of potential Islamic investors worldwide. This, Crescent Capital says, could overlap with likely investors into its funds. Crescent IV and V have one such investor.

45 Crescent Capital relies on the reasoning in Bridge Stockbrokers Ltd v Bridge (1984) 4 FCR 460 to make the following submissions:

The relevant public includes members who are not familiar with the financial services industry

The financial services market cannot be easily divided into separate fields of activity.

At first instance, Sheppard J (upheld on appeal on this aspect) found that the names ‘Bridges, Son & Shepherd’ and ‘Bridge Stockbrokers Limited’ were likely to mislead, despite the fact that the two parties operated to a large extent in different sections of the market, with some degree of overlap. His Honour also looked to the fact that future changes, in that case the proposed deregulation of activities of stock exchanges, may cause the nature of the businesses to undergo some change.

46 Crescent Capital also submits that the hypothetical individual, as the relevant member of the class, is not an institutional investor or perhaps not even a sophisticated investor and that such a person might see Crescent Wealth as being connected to, or a branch of, Crescent Capital, or see Crescent Wealth’s products as emanating in some way from Crescent Capital. In that regard, Crescent Capital points to the fact that mainstream financial institutions may form Islamic, Sharia compliant subsidiaries. This has been done by HSBC with the HSBC Amanah Islamic Bank of Malaysia.

47 Accepting that evidence of confusion is neither required nor determinative, Crescent Capital points to some evidence of confusion, namely:

Mr Yassine clarifying, in an email to Mr Mortimer of Crescent Capital, a reference to ‘the Crescent Team’ using “(your Crescent Team :))”.

Conversations such as one in which a person involved in the sale of dental and child-care businesses asking an employee of Crescent Capital ‘are you the Islamic Equity Fund?’.

A telephone enquiry to Crescent Capital asking to speak to Mr Yassine.

A comment of the then Federal Treasurer to Mr Mortimer at a dinner indicating that he had met someone from “Crescent”, being Mr Yassine.

Other comments to Mr Mortimer from business associates connecting Mr Yassine to Crescent Capital.

An email addressed to employees of Crescent Capital from the Unlisted Unit Trust team at BNP Paribas seeking information about a Crescent Wealth fund as well as about Crescent Capital’s funds.

48 Crescent Capital submits, in summary, that Crescent Wealth has engaged in misleading and deceptive conduct because:

The names are very similar and confusingly similar.

The names become identical where Crescent Capital is frequently shortened to Crescent in the market and both parties offer financial services by reference to the name CRESCENT.

Both companies operate in the financial services industry.

Many of the funds of Crescent Capital and Crescent Wealth use the word CRESCENT in their names.

Both offer fund management services to a target audience that overlaps.

The words “wealth” and “capital” are descriptive and, in at least one sense, synonyms.

There are actual examples of confusion.

There is a likelihood of confusion in the future as the parties’ respective businesses continue to expand in the financial services market.

Crescent Wealth’s financial services licence is not limited to Sharia compliant investments, nor to retail customers.

Crescent Wealth does not limit its offerings to Islamic investing. It manages funds which have no Islamic focus. For example, the media release for the Crescent International Equity Fund dated 19 September 2014, marketed to retail and wholesale investors, contains no mention of any Islamic focus.

Both parties receive investment from superannuation funds.

That is, both parties have an overlapping present target audience and future activity by both will increase the overlap.

Consumers who are aware of the Islamic focus of Crescent Wealth may think that it is the Islamic finance arm of Crescent Capital.

Crescent Wealth was aware of Crescent Capital, its name and its business, yet took no steps to provide disclaimers or explanations on its website or in investment product statements or to take steps otherwise to avoid confusion.

49 Crescent Wealth submits that:

Crescent Capital’s reputation is limited to persons in the financial services industry who are familiar with private equity or venture capital and it has no reputation in the word “Crescent”, or at all, among the relevant class of consumers who are the target of Crescent Wealth’s conduct.

Nevertheless, if Crescent Capital does have a reputation among some members of the relevant class of consumers then, in all the circumstances, and particularly given the lack of any common field of activity between Crescent Capital and Crescent Wealth, Crescent Wealth’s conduct is not likely to cause those consumers to be misled or deceived.

There is no evidence sufficient to establish future diversification by either party into common fields of activity.

Any conduct by Crescent Wealth will only be capable of misleading or deceiving the relevant class of consumers if the name “Crescent” used by Crescent Capital has acquired a reputation among them, as at the date of the impugned conduct, namely 2011.

Accepting that such evidence is not necessary, it is a factor to be weighed that there is no evidence of members of the relevant class being misled or deceived.

Any transitory association between the parties’ businesses, or of the financial products that they offer, would be immediately dispelled upon comparison.

Venture capital and private equity are clearly distinguished in the financial services industry from traditional asset classes such as shares, bonds and property. However, Crescent Wealth accepts that a sophisticated investor desiring a diversified portfolio might have investments in venture capital and in other asset classes.

Crescent Wealth’s products remain open to investors through the life of the product and are liquid, enabling withdrawals at any time subject to minimum withdrawal limits. The investment products aim to make half yearly distributions of income and annual distributions of capital.

50 Crescent Wealth submits that its investors are “mum and dad” investors looking for safety and security with a modest return. It advertises to the general public, in particular in areas with large Muslim populations. It says that the investment by Aon Hewitt was a “one-off”, though the evidence of Mr Yassine was that such investments would be welcomed in the future.

51 Basically, Crescent Wealth submits that Crescent Capital has no reputation among the class of consumers who ‘make up the universe of prospective purchasers’ relevant to Crescent Wealth and to whom its conduct is directed. It says that the parties are not engaged in any common field of activity, offering different products in different asset classes to very different types of investors.

52 It also submits that post-2011 evidence is of no assistance and cannot be taken into account to establish a reputation for Crescent Capital among the relevant class. On the other hand, it points out, there is no evidence of an investor actually being misled or deceived by reason of the similarity of names; rather, the evidence goes no higher than a “cause to wonder”.

53 It also points to evidence that 75% of businesses and potential investor companies approached by Mr Scrine, for Crescent Capital, have not heard of it, let alone refer to it by “Crescent” alone.

54 It emphasises that members of the class of persons for whom the assessment of the conduct said to be misleading or deceptive is relevant are not those in the financial services industry, who are familiar with venture capital or private equity and who see media reports which refer to Crescent Capital Partners or by the short form of Crescent. Alternatively, it argues, to the extent that Crescent Capital does have a reputation among the relevant class of customers, that it will be confined to those who have dealt with it in the course of its business activities, such as professional advisers or owners and employees of businesses that it has acquired or in which it has invested, and that there is no likelihood of such persons being misled or deceived by Crescent Wealth’s conduct.

CONSIDERATION

55 It is not determinative or necessary but I note that there is no evidence to support an intention on Mr Yassine’s part to deceive or mislead anyone to believe that Crescent Wealth was associated with Crescent Capital. His use of “Crescent” in naming the Crescent Institute predated the commencement of Crescent Wealth and his explanation of the choice of name, as the symbol of Islam in the context of Sharia compliant investing, was cogent. The word “Crescent” is a common English word which can mean “increasing” or “growing”, (Macquarie Dictionary), which is why it was chosen by Crescent Capital. It is also a symbol of Islam. I accept that the crescent would be seen as a symbol of Islam by many of that faith and by people of other faiths. I note too that I found Mr Yassine to be an impressive witness.

56 As at the present, there are a number of matters that differentiate the two parties, including:

The products provided.

The logos associated with the respective businesses.

The class of consumers to whom the products are provided.

The nature of the investments offered.

The persons or institutions to which the products are marketed.

The emphasis by Crescent Wealth on Sharia compliant products.

57 There are also a number of similarities, including:

The use of “Crescent” with respect to offerings.

Domain names.

58 The concern raised by Crescent Capital is largely directed to the future conduct of Crescent Wealth in the light of its rapid growth and likely expansion beyond its existing consumer base, which already includes institutional investors. In that regard, Crescent Capital points out that Crescent Wealth also operates through fund managers and diversification into the higher risk category of property investment. The fund managers must make investments in accordance with Sharia principles but that does not of itself prevent diversification into private equity.

59 Crescent Wealth says that there is no evidence of any realistic prospect that it will enter the private equity field, or operate as a private equity business in any way and that Mr Yassine’s evidence was to the contrary. It also submits that there is no evidence that Crescent Capital has any intention to commence Sharia compliant investing. That submission focuses on the steps taken to ensure the highest levels of Sharia compliance that Crescent Wealth has taken.

60 However, Crescent Capital has already agreed, in side letters with specific investors, to limit the nature of investments in accordance with what it terms “ethical investing”, including some limitations that accord with aspects of Sharia law and other limitations desired by an investor that might not be said to come within Sharia law or ethical investing. It is apparent that Crescent Capital has readily agreed to limitations requested by investors without regard to the reason for such limitations. Nevertheless, while to date Crescent Capital has engaged in what it terms ethical investing but has not engaged in fully Sharia compliant investing and not to the level of compliance adopted by Crescent Wealth, it cannot be said that Crescent Capital has decided to remove itself from offering Sharia compliant investments. However, there is no evidence to suggest that Crescent Capital intends to offer superannuation products or any products other than private equity investments. Retention of the possibility of offerings to retail investors does not evidence such an intention, particularly when one takes account of the nature and amounts of investment progressively in the Crescent Funds since Crescent I.

61 There is no evidence that Crescent Capital, as a private equity firm, will offer superannuation products or that Crescent Wealth will set up a private equity business. However, Crescent Wealth recognises that, as it grows, it may attract wholesale investors. It submits that such growth would not be sufficient to give rise to a likelihood of misleading or deceptive conduct, as the differences in the businesses would remain. Indeed, it submits that any likelihood of confusion would diminish with the growth of the businesses. Nevertheless, it is likely that any separation that can be said presently to exist in the class of investors in the respective funds will diminish.

62 Crescent Wealth recognises that both parties use the word “Crescent” on a stand-alone basis. Its response is, in summary:

The businesses operate primarily through written communications, in the context of the full name of each company and their differing logos.

Reference to “Crescent” in media reports is inevitably preceded by the use of the full name.

Reference to Crescent Wealth as “Crescent” in the media is accompanied by reference to the fact that it is an Islamic or Sharia compliant wealth manager of a superannuation fund.

Communications with investors of either party are usually documentary and accompanied by documentary material that makes clear the business referred to.

The relevant investment decisions are important and carefully considered such that an oral reference to “Crescent” would lead, at most, to transitory confusion, not “commercially relevant” confusion.

63 Crescent Wealth’s case is beguiling. It depends on a neat division between classes of consumers within the financial services industry and in the fields of funds or investment management into retail and wholesale investors, between unsophisticated and sophisticated investors and between those who invest in private equity and those who do not. This distinction is, however, artificial and not in accordance with commercial realities, including the fact that fund managers and investors may make investments across many different asset classes in order to balance their portfolios and to maximise returns. Crescent Wealth already operates across four of the five asset classes identified (cash, fixed interest, property, shares but not yet ‘alternative’). As Crescent Capital puts it, funds or investment management involves taking a person’s money, investing it in an asset class with the sole purpose of providing a return to that person, whether it be by income, capital gain or both over a period of time. Investors, as consumers in this industry, do not necessarily or practically restrict themselves to one class of investment, or to one offeror of investment opportunities, whether within an asset class or across asset classes.

64 Furthermore, as the High Court emphasised in Campomar Sociedad Limitada v Nike International Ltd (2000) 202 CLR 45, the occupation of a common field of activity is not essential for a successful misleading and deceptive conduct claim.

65 The names of funds operated by and connected with the parties, which use only the “Crescent” part of their respective names, demonstrate the difficulty of obvious separation in the minds of consumers/investors:

Crescent Growth Fund (or Crescent I)

Crescent II, III, IV and V

(for Crescent Capital)

Crescent Wealth Superannuation Fund

Crescent Australia Equity Fund

Crescent Wealth International Equity Fund

Crescent Diversified Property Fund

Crescent Islamic Cash Fund

(for Crescent Wealth)

66 By 2011 Crescent Capital had already established a reputation in the use of Crescent in relation to funds, having raised both Crescent I and Crescent II by this time.

67 Similarly, the domain names are not conducive to separate identification:

crescentcap.com.au

(for Crescent Capital)

crescentinvestments.com.au

crescentwealth.com.au

crescentfunds.com.au

crescentfunds.net

crescentinstitute.com.au

(for Crescent Wealth)

68 Further, Crescent Wealth’s AFS licensee is named Crescent Funds Management (Aust) Limited.

69 “Funds management” is a term that is not confined so far as investors are concerned. Both parties operate funds by reference to “Crescent”. I accept that persons making investments, in particular investments of the quantum invested in Crescent Capital’s funds, would take care in the object of that investment and, at present, there is a difference in the nature of the investments that parties offer. However, as noted above, investors do not necessarily restrict themselves to a single asset class. Crescent Wealth is diversifying within and across asset classes and expanding the amounts of funds under its management. That, in turn, attracts investors beyond the ‘mum and dad’ category that presently provides much of its superannuation investment. Each operates under the name “Crescent” in circumstances where the distinguishing logos are not present. There is sufficient likelihood of investors and those advising them being misled or deceived or confused by Crescent Wealth’s offerings into believing that Crescent Wealth’s funds are those of Crescent Capital or are part of, or associated with, or managed by, or connected to Crescent Capital.

70 This case is distinguishable from Anchorage Capital Partners Pty Ltd v ACPA Pty Ltd (2015) 115 IPR 67. In that case, Perram J concluded that the relevant consumers of each parties’ products were large institutional investors who invest money in the respective funds, which had ‘a correspondingly high degree of sophistication’. His Honour said (at [19])that ‘The idea that these kinds of finance houses would have invested tens of millions of dollars into the wrong fund because of the similarity in names is implausible … In the context of the markets in which the applicant moved it was not misleading that two firms had the same name’. The distinction here is that Crescent Wealth is not aiming its activities at highly sophisticated investors, such that less sophisticated consumers might well be misled. As Crescent Capital submitted, the relevant consumer is not, in the circumstances, necessarily a sophisticated one.

71 It follows that Crescent Wealth’s business activities have involved conduct which is likely to mislead or deceive.

72 The position of each individual respondent must now be considered.

THE INDIVIDUAL RESPONDENTS

73 The Crescent Wealth company structure, setting out the relationship between the respondents is as follows:

74 It is agreed that there is no relevant distinction, for present purposes, between the first and second respondents. The parties were agreed that the first and second respondents could be treated as a single entity. The second respondent is the operating company of the Crescent Wealth business, while the first respondent is the responsible entity for that business. The business of Crescent Wealth was established in about 2010 by Mr Yassine, together with Mr Dandan and Mr Eid, although it only began trading under that name in around August 2011.

75 Crescent Capital pleads that each of the first to eighth respondents carry on business supplying investment services, including in relation to wholesale and retail asset and fund investment management services, and products and that all have been registered and traded under company names incorporating the word “Crescent”. Crescent Capital also pleads that from at least 2010 the respondents have advertised, marketed, offered and provided investment services and products under and by reference to the name “Crescent”. Reference is also made in the statement of claim to the ownership of domain names: crescentinvestments.com.au, crescentwealth.com.au, crescentinstitute.com.au, crescentfunds.com.au and crescentfunds.net, as well as applications for trade marks and the establishment of a Facebook page. Particulars are also given of the role as issuer or promoter of funds containing the word “Crescent” (without reference to the added word “Wealth”).

76 Crescent Capital alleges that each of the respondents engaged in conduct that was relevantly false or misleading or likely to mislead or deceive for the purposes of ASIC Act and ACL. Crescent Capital alleges that, to the extent the impugned conduct was engaged in by one or more (but not all) of the respondents, each respondent:

(a) aided, abetted, counselled and procured;

(b) was directly or indirectly, knowingly concerned in; or

(c) was a party to,

that conduct, within the meaning of s 2 of the ACL or ss 12GD and 12GF of the ASIC Act.

77 The following facts seem to be agreed:

The first respondent (CFMA) is the responsible entity that makes offers in Crescent Wealth funds to investors.

The second respondent (CIA) is the operating company.

The third and sixth respondents are holding companies and are, in effect, dormant. They do not engage in offers or supplies to investors. They are non-operating holding entities through which the founders of Crescent Wealth invested in Crescent Wealth. The third respondent has not been used to make any subsequent investments; does not offer, and has not offered, investment products or services to the public; and has not marketed itself to investors or potential investors. Accordingly, the third respondent has not engaged in any conduct directed at relevant members of the class of consumers, nor has it made any representations that could mislead or deceive such consumers.

The fourth and seventh respondents are wholly owned by CIA. They are dormant and do not engage in any conduct, let alone the relevant conduct. They do not undertake any activities or hold any assets.

The fifth respondent is a wholly owned, not-for-profit entity which makes charitable donations that serve to “cleanse” investments made through CFMA and CIA that do not comply with Sharia law, so as to ensure ongoing Sharia compliance; moneys are given through the Foundation to charity. The Foundation does not offer investment products or services to the public and plays no role in determining which funds are provided to it, nor does it have any control over the amount of funds distributed to it.

The eighth respondent, the Crescent Institute, is, in effect, a networking group. It is the corporate incarnation of a networking group founded in the 1990s by Mr Yassine under the name “The Crescent Club”, while he was at University. It holds thought leadership and networking events on topics of interest to those of the Muslim faith and others in business and the wider community. Crescent Capital does not now seek any orders in respect of this party.

The ninth respondent is a corporate vehicle for investments by the Yassine family.

Mr Yassine is the tenth respondent. He is the co-founder and managing director of Crescent Wealth and the founder and now patron of the Crescent Institute.

78 A person who suffers loss or damage may recover that loss or damage by action against the primary contravenor or against “any person involved in the contravention”: s 12GF of the ASIC Act. The phrase “involved in the contravention” has the same meaning as in s 79 of the Corporations Act 2001 (Cth): s 5(2)(b) of the ASIC Act.

79 In considering whether a party is “involved” in a contravention, such as to be accessorily liable for that contravention, the jurisprudence relating to similar provisions in the Competition and Consumer Act 2010 (Cth) is apposite (Roumanus v Orchard Holdings (NSW) Pty Limited (in Liq) (2012) 90 ACSR 677 at [178]; Cassidy v NRMA Health Pty Ltd at [71]). That jurisprudence provides that the alleged accessory must have had actual knowledge of the facts that gave rise to the contravention, with such knowledge extending to the essential elements of the offence (even if the accused does not know that those elements comprise a contravention) (Yorke v Lucas at 666-670; Cassidy v NRMA Health Pty Ltd at [72]-[73]). Further, the alleged accessory must have intentionally participated in (or assented to) the contravention by the primary contravener: (Yorke v Lucas at 667, 670).

80 Crescent Capital submits that orders should be made as against all of the respondents (other than Crescent Institute) to remove the name “Crescent” in order to remove ‘the tools that might tempt’ in the future, in the case of the fourth and seventh respondents because they are part of the ‘operating armoury’ of CIA and, in the case of the Foundation, because it is ‘squarely part of the business’ of CFMA and CIA and is mentioned on the Crescent Wealth website. It presses orders against the ninth respondent, seemingly because Mr Yassine has ‘collected them together’ and it was the owner of two domain names which have now been transferred to other respondents.

81 The case that Crescent Capital makes against the third to seventh respondents is that they have company names that include “Crescent” and have a direct or indirect “involvement” in the business of Crescent Wealth, including ‘as shareholders, associated charities, investment vehicles or associated networking companies’.

82 There is no dispute that Mr Yassine was instrumental in the choice of the Crescent Wealth name and that he was involved in, but not necessarily the decision maker in, the decision to persist with the use of that name after concerns were raised by Crescent Capital. He had checked that the name Crescent Investments Australasia Pty Limited (the second respondent) was available to be registered as a company name before doing so. He has, therefore, participated in contraventions with the requisite knowledge and is liable as an accessory to the contraventions of the first and second respondents.

83 The evidence of relevant contravening conduct as against the third, fourth, sixth and seventh respondents is either non-existent or insufficient. None of these entities were (or are) involved in the activities of Crescent Wealth in any way in offering superannuation products or managed investment products to the public, or in marketing such products as set out above. There is no evidence of existing or likely future conduct or that they will be used as “tools” of CIA. The most that seems to be said against them is that they have the word “Crescent” in their name and that Mr Yassine has some involvement with them. “Crescent” is an ordinary English word. Crescent Capital cannot monopolise or preclude its use unless it is used in a way to mislead or deceive, or be likely to mislead or deceive investors. The third to eighth respondents were not involved in Crescent Wealth’s conduct, nor did those respondents engage in conduct which facilitated or procured the alleged contraventions. They also played no role in the making of the statements or representations alleged to have been made by Crescent Wealth. These entities cannot be said to have participated in any alleged contraventions.

84 It is quite extraordinary for Crescent Capital, which has deliberately removed the sign of the crescent from its logo (which it previously included), to seek to prevent a charitable foundation associated with Sharia compliance from using the symbol of Islam, especially, in the absence of evidence of contravening conduct by that foundation. To the extent that the Foundation is “involved” in any activity of Crescent Wealth by serving to “cleanse” investments in order to make them Sharia compliant, this involvement commences after any relevant conduct has occurred. It therefore does not participate in any alleged contravention.

85 In respect of the ninth respondent, Yassine Corporation, this company is an investment vehicle for Mr Yassine’s family. Crescent Capital limits the claim to one of accessorial liability for the alleged misleading or deceptive conduct claim alleged against the other respondents and says that Yassine Corporation is accessorily liable for the conduct of Crescent Wealth in circumstances where it held, but no longer holds, two domain names which the applicant claims are relevantly misleading: crescentwealth.com.au (now held by CIA) and crescentinstitute.com.au (now held by the eighth respondent, against which no claims are now pressed). I reject these claims. The Yassine Corporation has not been shown to have participated with knowledge in any of the alleged contraventions of the other respondents. To have held the domain names for a period of time is insufficient to constitute ‘participation’ in the requisite sense.

86 Therefore, Crescent Capital has failed to make out its case against any of the third to ninth respondents. Other than with respect to Mr Yassine, there is simply no evidence to make out the accessorial liability case.

ORDERS

87 Apart from declarations, Crescent Capital seeks orders that the respondents be restrained from, broadly, dealing in or marketing investment services or products by reference to the word “Crescent” or a word “deceptively similar” to the word Crescent. It also seeks orders that the respondents change their names to remove any references to “Crescent”, as well as orders deregistering domain names and the business name.

88 In my view, the orders sought are too wide, even as against the first and second respondents. I do not propose to make any orders as against the third to ninth respondents.

89 The conclusion that the first and second respondents have engaged in conduct which was misleading or likely to mislead or deceive follows from the use of “Crescent Wealth” and the names of the funds and domain names which use the name “crescent” together with generic words such as “investments”, “funds” and the like. It is this use that is likely to lead investors to believe that the funds, products or services are those of, or associated with, or affiliated with, Crescent Capital. However, this does not mean that all use of the word “Crescent”, alone or in association with other words, or in conjunction with a disclaimer, would result in the misleading of investors/consumers.

90 Crescent Capital is entitled to a declaration and orders concerning the conduct of the first and second respondents and of the tenth respondent. It is also entitled to orders that within a reasonable time, which would be of the order of 28 days, the first and second respondents, or, if appropriate, another of the respondents, take steps in respect of the deregistration of the offending domain names and the names of the funds.

91 I will give the parties the opportunity to propose consent or, if there is no consent, competing orders to give effect to these reasons.

92 Although this proceeding concerned liability and not damages, it is presently apparent that Crescent Capital has suffered little if any damage from the existing conduct of the first, second or tenth respondents in circumstances where there is no evidence of actual misleading or confusion on the part of investors, or of investors actually having been misled or deceived into investing in the wrong fund or other investment class.

93 Crescent Capital has succeeded as against the first and second respondents and, accordingly, against the tenth respondent. It has not succeeded against the remaining respondents. It is appropriate to make a costs order which takes into account that lack of success.

I certify that the preceding ninety-three (93) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Bennett. |

Associate:

NSD 448 of 2014 | ||

Respondents | ||

Fourth Respondent: | CRESCENT FINANCIAL SERVICES PTY LIMITED (ACN 155 740 631) | |

Fifth Respondent: | CRESCENT FOUNDATION FUND PTY LIMITED (ACN 149 971 577) | |

Sixth Respondent: | CRESCENT HOLDINGS AUSTRALIA PTY LTD (ACN 150 960 731) | |

Seventh Respondent: | CRESCENT SUPER PTY LTD (ACN 138 223 686) | |

Eighth Respondent: | CRESCENT INSTITUTE LIMITED (ACN 155 826 467) | |

Ninth Respondent: | YASSINE CORPORATION PTY LIMITED (ACN 077 199 654) | |

Tenth Respondent: | TALAL YASSINE | |