FEDERAL COURT OF AUSTRALIA

Phoenix Institute of Australia Pty Ltd v Commonwealth of Australia [2016] FCA 190

ORDERS

PHOENIX INSTITUTE OF AUSTRALIA PTY LTD Applicant | ||

AND: | First Respondent MINISTER FOR EDUCATION AND TRAINING Second Respondent SECRETARY TO THE DEPARTMENT OF EDUCATION AND TRAINING Third Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The proceeding be dismissed.

2. Subject to either party notifying the Court in writing by 4pm on 8 March 2016 that it wishes to be heard on costs, the applicant pay the respondents' costs of the proceeding, including any reserved costs, to be taxed if not agreed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MOSHINSKY J:

Introduction

1 The applicant (Phoenix) is a provider of vocational education and training (VET) courses. It is an approved VET provider under the Higher Education Support Act 2003 (Cth) (the Act) and eligible to receive funding from the first respondent (the Commonwealth) for the course fees of students who enrol with Phoenix to undertake accredited courses and borrow their tuition fees from the Commonwealth.

2 In July 2015, the third respondent, the Secretary to the Department of Education and Training (the Secretary) made a determination pursuant to the Act that an advance of $160,000,759 be made to Phoenix in respect of the 2015 calendar year. The effect of the determination, Phoenix contends, was that the Commonwealth was required to pay Phoenix:

(a) $13,333,277 on 15 October 2015;

(b) $13,333,277 on 15 November 2015; and

(c) $13,333,755 on 15 December 2015.

3 The Commonwealth has not paid these amounts to Phoenix. Rather, by a series of decisions (or purported decisions) which are impugned in this litigation, officers of the Department of Education and Training (the Department) purported to defer payment of these amounts, ultimately to 15 January 2016. Then, one day before that date, on 14 January 2016, the Secretary revoked the determination that an advance of $160,000,759 be made. The revocation decision is not challenged by Phoenix.

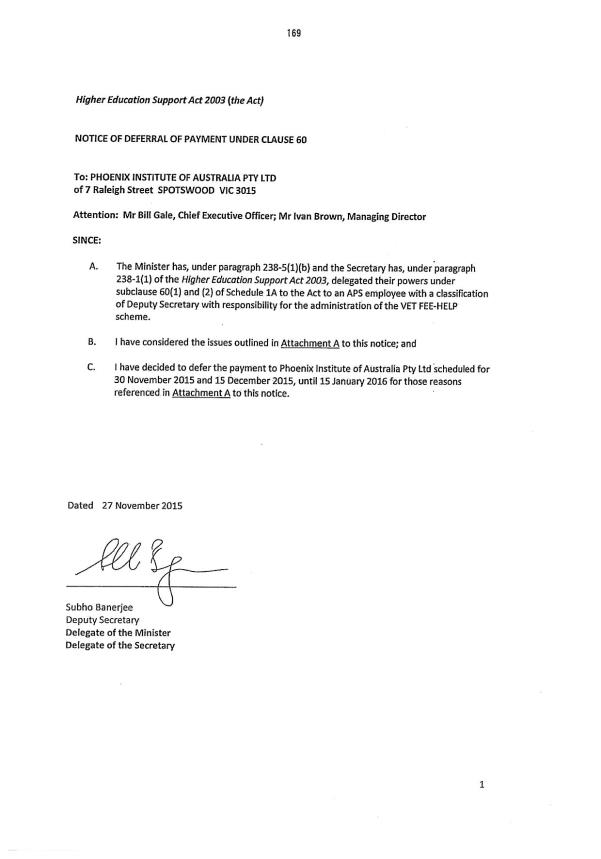

4 Phoenix contends that each of the decisions, or purported decisions, to defer payment was void, invalid and/or of no effect. It will be convenient to refer to the decisions or purported decisions as the 'deferral decisions', notwithstanding that their validity is challenged and, in one case, there is a question whether any decision was made. The four deferral decisions were notified to Phoenix by the following communications:

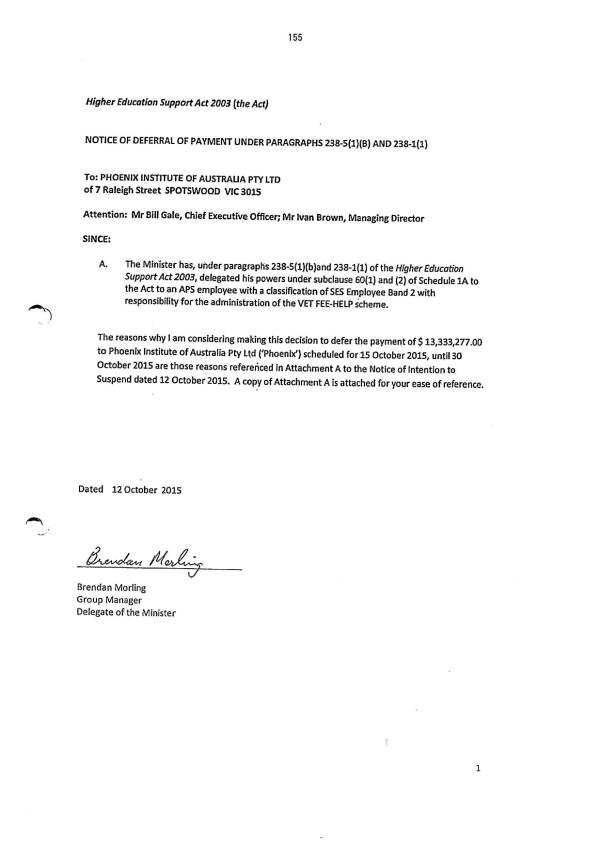

(a) a notice of deferral signed by Mr Brendan Morling dated 12 October 2015 (see Annexure 1);

(b) a letter signed by Mr Dean Woodgate dated 30 October 2015 (see Annexure 2);

(c) a letter signed by Dr Subho Banerjee dated 13 November 2015 (see Annexure 3); and

(d) a notice of deferral signed by Dr Banerjee dated 27 November 2015 (see Annexure 4).

5 Phoenix raises specific grounds of challenge in respect of each of the deferral decisions, based on the content and terms of the communications. Phoenix also raises a statutory construction issue applicable to all four deferral decisions: Phoenix contends that, properly construed, cl 60(2) of Sch 1A to the Act does not support a decision to defer a particular payment to a particular provider which is due to it pursuant to an extant determination to make an advance under cl 61(1); the power relates to the timing of payments generally.

6 Phoenix seeks relief under s 39B of the Judiciary Act 1903 (Cth) and judicial review and remedies under the Administrative Appeals (Judicial Review) Act 1977 (Cth) (the ADJR Act). Specifically, Phoenix seeks the following relief under s 39B of the Judiciary Act (and comparable relief under the ADJR Act):

(a) orders in the nature of certiorari quashing each of the deferral decisions;

(b) declarations to the effect that each of the deferral decisions is void, invalid and/or of no effect;

(c) an order in the nature of prohibition prohibiting the Commonwealth, the second respondent, the Minister for Education and Training (the Minister) and the Secretary from giving effect to the fourth deferral decision; and

(d) orders in the nature of mandamus to compel the Commonwealth to (alternatively, to compel the Minister and the Secretary to procure that the Commonwealth) pay to Phoenix the three amounts. The three amounts total approximately $40 million.

7 In response, the respondents contend that, on the true construction of the Act, a determination by the Secretary under cl 61(1) of Sch 1A to the Act that an advance is to be made does not create an obligation to pay the relevant amount; it is merely a facultative provision. Accordingly, there is no proper basis for an order in the nature of mandamus compelling payment of the three amounts (or a declaration that the amounts are payable). Further, the respondents contend that each of the deferral decisions validly deferred payment of the amounts, ultimately to 15 January 2016. Further or in the alternative, the respondents contend that, in the exercise of discretion, the Court should not grant the relief sought by Phoenix. The respondents contend that there is a live issue as to whether Phoenix has an underlying entitlement to be paid the relevant amounts by the Commonwealth (a matter to be determined at a later date, as part of a process of reconciliation); and that, in the event that Phoenix is required to repay the amounts as part of the reconciliation process, it may not be able to do so given its financial difficulties.

8 For the reasons that follow, my conclusions are:

(a) I do not accept Phoenix's contention that, properly construed, cl 60(2) of Sch 1A to the Act does not support a decision to defer a particular payment to a particular provider which is due to it pursuant to an extant determination to make an advance under cl 61(1). In my view, the power is able to support a decision to defer payment in such circumstances.

(b) I do not accept the respondents' contention that, properly construed, a determination by the Secretary under cl 61(1) of Sch 1A to the Act that an advance is to be made, does not create an obligation to pay the relevant amount. In my view, a determination does give rise to an obligation to pay (subject to determinations as to the manner and timing of payment under cl 60).

(c) In relation to the specific grounds of challenge in respect of each of the deferral decisions, none of these grounds is made out.

Background and context

9 Under the Act, eligible students may qualify for a loan known as 'VET FEE-HELP' (VFH); and under cl 55 of Sch 1A to the Act the amount of the loan is paid to a provider to discharge the student's fee liability. Under cl 61 of the schedule the Secretary may determine that an advance is to be made to a VET provider of an amount "expected to become payable to the provider".

10 On 8 December 2014, the Secretary determined under cl 61(1) that an advance be made to Phoenix of $2,410,292. Phoenix twice requested a variation of the advance payment determination, which was ultimately varied (on 13 July 2015) to $160,000,759. The Department published a document titled "VET Administrative Information for Providers" dated September 2015 (the AIP), which dealt, among other things, with payment arrangements. The AIP stated at page 65:

The Secretary may determine that an advance payment for VET FEE-HELP is to be made to a VET provider [HESA Schedule 1A subclause 61(1)]. The estimate is based on the amount of VET FEE-HELP that is expected to be provided to entitled students for VET units of study with census dates that occur between January and December. The amount of the advance payment is determined on a calendar year basis. Estimates are submitted through HITS. The VET provider must complete the estimate screen in HITS and submit the information to the department. Assessment of an estimate will not proceed without the relevant information being provided.

Once the Secretary has approved the advance, a payment schedule will be created in HITS. The payment schedule is available to be viewed by the VET provider in HITS and details the amount of payments that will be made in monthly instalments over the calendar year. If an adjustment or variation is made, a new payment schedule will be created to reflect the variation.

VET FEE-HELP payments are processed on the fifteenth day of each month. Funds are not immediately transferred, and may take up to five business days to appear in the VET provider's nominated bank account.

(emphasis added)

11 Phoenix relies on this passage in the AIP (in particular, the words emphasised in the above quotation) as constituting or evidencing a determination by the Minister under cl 60(1) that advances are to be paid in monthly instalments and a determination by the Secretary under cl 60(2) that payments are to be processed on the fifteenth day of each month. This is a necessary part of its case that it is entitled to each of the amounts set out in paragraph [2] above.

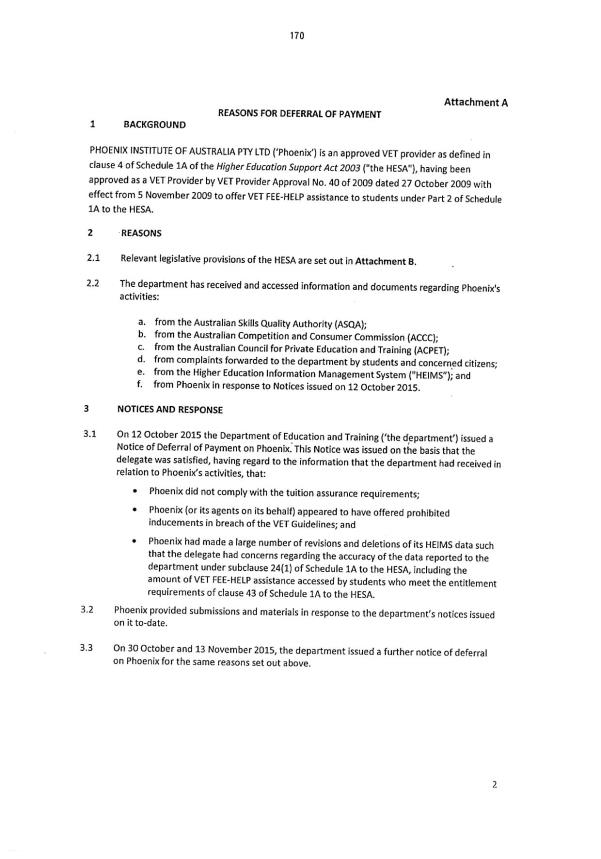

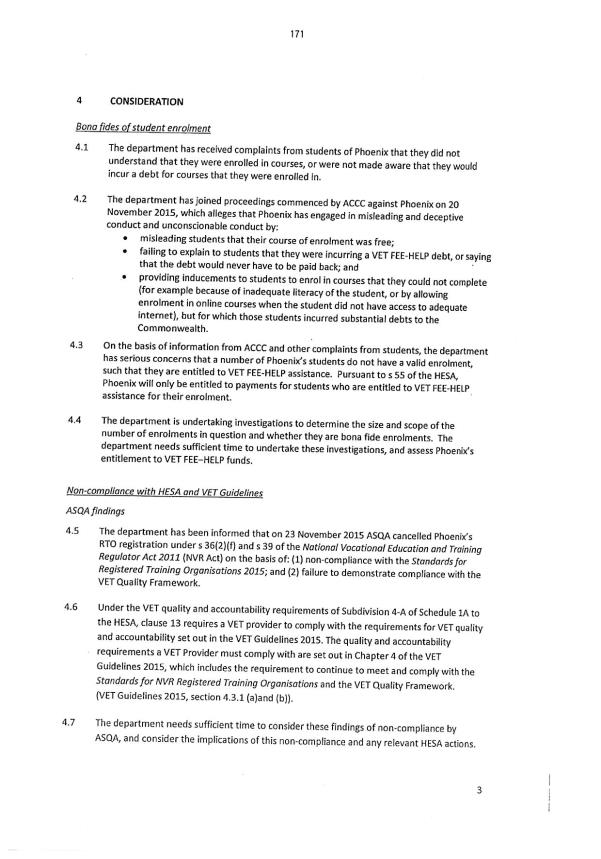

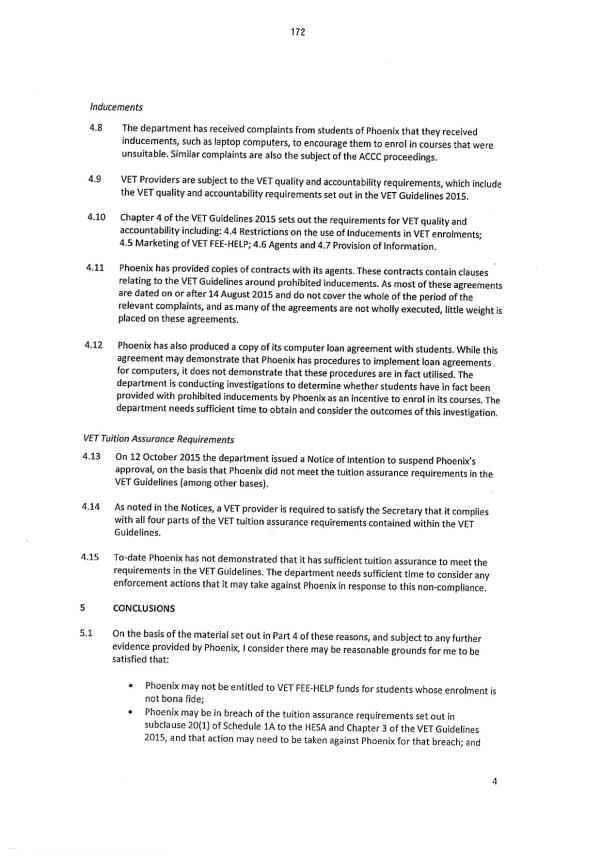

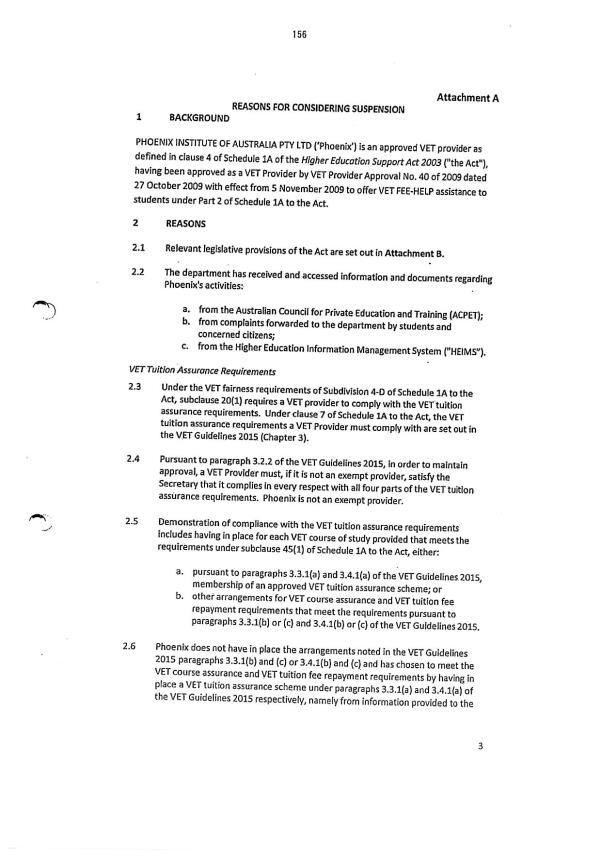

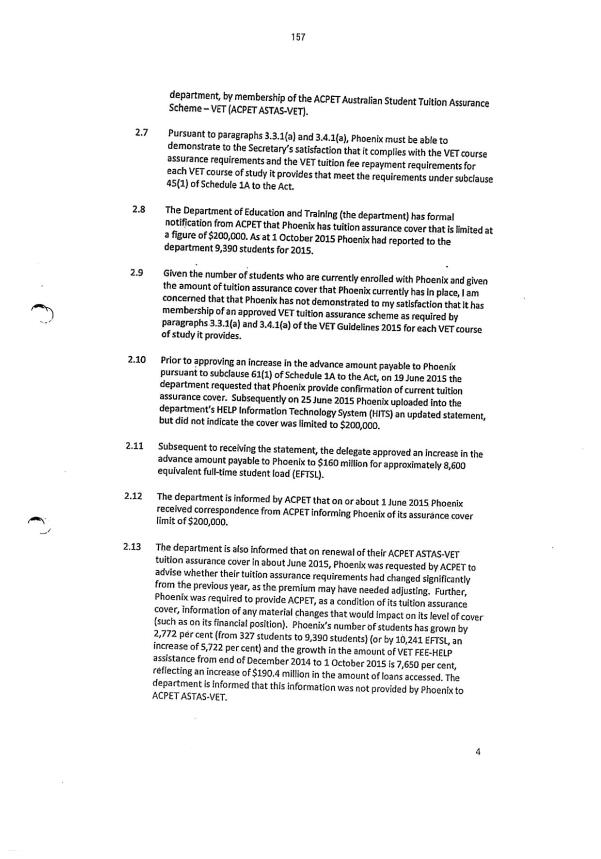

12 In the course of 2015, the Department received information raising concerns about Phoenix's compliance with various aspects of the regulatory regime for VET providers.

13 On 12 October 2015, Mr Morling, an officer of the Department, issued three notices to Phoenix:

(a) a notice of intention to make a decision to suspend Phoenix's approval as a VET provider;

(b) a notice of intention to make a decision to revoke the determination under cl 61(1) that an advance is to be made to Phoenix; and

(c) a notice of deferral of payment (that is, the communication relating to the first deferral decision).

14 The notices of intention to suspend Phoenix's approval as a VET provider and to revoke the advance payment determination provided Phoenix with an opportunity to respond to the matters raised by Mr Morling. Phoenix was invited to, and did, make submissions in relation to suspension and revocation, by provision of a submission and documents on 26 October 2015 and further documents on 10 and 12 November 2015. The Department also engaged in correspondence and face-to-face meetings with Phoenix.

15 Subsequently, on 30 October, 13 November and 27 November 2015, other officers of the Department made the second, third and fourth deferral decisions. These purported to defer payment of the advance amounts to 15 January 2016.

16 On 23 November 2015, the Australian Skills Quality Authority (ASQA) cancelled Phoenix's registration as a registered training organisation under the National Vocational Education and Training Regulator Act 2011 (Cth) and the Education Services for Overseas Students Act 2000 (Cth). Phoenix has sought merits review of this decision in the Administrative Appeals Tribunal. A stay of the decision has been granted pending the review, on condition that further students not be enrolled this year. Phoenix is, however, permitted to continue to teach existing students.

17 Also on 23 November 2015, the Australian Competition and Consumer Commission (ACCC) and the Commonwealth instituted proceedings against Phoenix in this Court alleging false or misleading representations and unconscionable conduct in contravention of the Australian Consumer Law. The remedies sought include cancellation of VET FEE-HELP loans.

18 On 14 January 2016, Mr Morling revoked the advance payment determination on the basis of non-compliance with tuition assurance requirements.

19 On 29 January 2016, Dr Bannerjee suspended Phoenix as a VET provider and issued a notice of intention to revoke its registration as a VET provider. On the same date, Mr Morling issued a letter to Phoenix informing it that it would be subject to an audit pursuant to cl 26 of Sch 1A to the Act to determine the veracity of its enrolments.

Legislative scheme

20 It was common ground that the relevant reprint of the Act is compilation number 57 (12 December 2015). Although there have been changes to the legislation since that date, for ease of expression reference will be made to the legislation as at that date as if presently in force.

21 The principal subordinate instrument of relevance is the VET Guidelines 2015 (Cth) (VET Guidelines). These guidelines were made under cl 99(1) of Sch 1A to the Act.

22 The Act's objects are set out in s 2-1 and relevantly include "to support students undertaking higher education and certain vocational education and training": s 2-1(d). That object is advanced by Sch 1A to the Act, which provides for financial assistance to students undertaking certain accredited VET courses by establishing the VET FEE-HELP scheme.

23 VET FEE-HELP is available in respect of accredited courses by approved VET providers. The requirements for approval as a VET provider are set out in Sub-div 3-B and in the VET Guidelines. Among other things, a VET provider must meet the VET tuition assurance requirements (which are set out in Ch 3 of the VET Guidelines) and the VET quality and accountability requirements (which are set out in Div 4 of Sch 1A).

24 There are six categories of VET quality and accountability requirements: (1) VET financial viability requirements; (2) VET quality requirements; (3) VET fairness requirements; (4) VET compliance requirements; (5) VET fee requirements; and (6) any other requirements set out in the VET Guidelines: cl 13. Content is given to each of the first to fifth requirements by a specific sub-division of Div 4.

25 The Minister may require a VET provider to be audited as to compliance with any of the VET quality and accountability requirements, save for the VET quality requirements: cl 26.

26 A body may cease to be an approved VET provider as a consequence of: (1) a revocation decision under Sub-div 5-AA, 5-B or 5-D; (2) a suspension decision under cl 36; or (3) if the notice of the provider's approval ceases to have effect under Part 5 of the Legislative Instruments Act 2003 (Cth): cl 29.

27 A student's entitlement to VET FEE-HELP assistance is determined by Part 2 of Sch 1A, together with Ch 6 of the VET Guidelines. A student is entitled to VET FEE-HELP assistance if he or she meets the requirements of cl 43 of Sch 1A, including that the student enrolled in the unit before the census date for the unit and remained enrolled at the census date, and that the student had, on or before the census date, completed, signed and given to an officer of the VET provider a request for Commonwealth assistance in relation to the unit or course of study.

28 Clause 55 provides that if a student is entitled to an amount of VET FEE-HELP assistance the Commonwealth must lend to the student the amount of that assistance and pay the amount lent to the student to the VET provider in discharge of the student's liability for the unit of study. It is in the following terms:

55 Payments

If a student is entitled to an amount of *VET FEE HELP assistance for a *VET unit of study with a *VET provider, the Commonwealth must:

(a) as a benefit to the student, lend to the student the amount of VET FEE HELP assistance; and

(b) pay the amount lent to the provider in discharge of the student's liability to pay his or her *VET tuition fee for the unit.

29 I was told during the hearing, and it appeared to be common ground, that a reconciliation process takes place after the end of a calendar year, to determine the ultimate entitlement of a provider under cl 55. I was told that this generally takes place in May or June of the following year, but it may be later.

30 The provision of VET FEE-HELP assistance to a student results in the student incurring a debt to the Commonwealth: s 137-18. The quantum of the debt is determined by s 137-18(2) and the time the debt is incurred is determined by s 137-18(3).

31 Div 11 of Part 3 of Sch 1A deals with payments by the Commonwealth. The two substantive clauses within that division (clauses 60 and 61) are central to the present dispute. They are in the following terms:

60 Time and manner of payments

(1) Amounts payable by the Commonwealth to a *VET provider under this Schedule are to be paid in such a way, including payment in instalments, as the Minister determines.

(2) Payments of amounts payable by the Commonwealth to a *VET provider under this Schedule are to be made at such times as the *Secretary determines.

61 Advances

(1) The *Secretary may determine that an advance is to be made to a *VET provider on account of an amount that is expected to become payable under a provision of this Schedule to the provider.

(1A) The *Secretary may vary or revoke a determination that an advance is to be made to a *VET provider if:

(a) the Secretary is satisfied that the provider has not complied with this Schedule and the regulations (if any) relating to this Schedule, and the *VET Guidelines that apply to the provider; or

(b) the Secretary is aware of information that suggests that the provider may not comply with this Schedule and the regulations (if any) relating to this Schedule, and the VET Guidelines that apply to the provider; or

(c) the Secretary is aware of information that suggests that the provider may not remain financially viable.

(1B) In deciding whether to take action under subclause (1A), the *Secretary may consider any or all of the following matters:

(a) in the case of non compliance or possible non compliance by the *VET provider:

(i) whether the non compliance or possible non compliance is of a minor or major nature; and

(ii) the period for which the provider has been approved as a VET provider; and

(iii) the provider's history of compliance with this Schedule and the regulations (if any) relating to this Schedule, and the *VET Guidelines that apply to the provider;

(b) in any case, the impact of the VET provider's non compliance, possible non compliance or possible lack of financial viability, and of the proposed variation or revocation of the determination, on:

(i) the VET provider's students; and

(ii) vocational education and training provided by the VET provider; and

(iii) the provision of vocational education and training generally;

(c) in any case, the public interest;

(d) in any case, any other matters specified in the VET Guidelines.

(2) If the advance exceeds the amount that becomes payable, an amount equal to the excess may be:

(a) deducted from any amount that is payable, or to be paid, to the provider under this Schedule; or

(b) recovered by the Commonwealth from the provider as a debt due to the Commonwealth.

(3) If the provider uses the advance for a purpose other than that for which it was given, an amount equal to the advance may be:

(a) deducted from any amount that is payable, or to be paid, to the provider under this Schedule; or

(b) recovered by the Commonwealth from the provider as a debt due to the Commonwealth.

(4) The conditions that would be applicable to a payment of the amount on account of which the advance is made are applicable to the advance.

(5) This clause does not affect determinations of advances under section 164-10.

32 It should be noted that cl 60 applies to payments under the schedule generally, not just to payments of an advance.

33 The Secretary may delegate all or any of his or her powers under the Act, the regulations or the VET Guidelines to an APS employee: s 238-1 of the Act and cl 98 of Sch 1A. Similarly, the Minister may delegate to the Secretary or an APS employee all or any of his powers under the Act (other than s 41-45 or 46-40): s 238-5 of the Act.

Evidence and objections

34 Phoenix relied on the following affidavits:

(a) Affidavit of Mr Michael Moffat dated 11 December 2015.

(b) Affidavit of Mr Moffat dated 5 February 2016.

(c) Affidavit of Mr Elliot Opolion dated 18 December 2015.

(d) Affidavit of Mr Opolion dated 9 February 2016.

35 There were no objections to those affidavits, and neither deponent was cross-examined.

36 The respondents relied on the following affidavits:

(a) Affidavit of Mr Richard Chadwick dated 29 January 2016.

(b) Affidavit of Mr Chadwick dated 1 February 2016.

(c) Affidavit of Mr Chadwick dated 8 February 2016.

(d) Affidavit of Mr Scott Gregson dated 29 January 2016.

(e) Affidavit of Mr Daniel Rudd dated 1 February 2016.

(f) Affidavit of Ms Adeline Ong dated 2 February 2016.

37 There was no cross-examination of these deponents. Phoenix raised a number of objections to these affidavits. Some of the objections were dealt with during the hearing. There were other objections (principally relying on the ground of relevance) which the parties were content for me to deal with in the judgment. Those objections were to the following parts of the affidavits:

(a) Affidavit of Mr Chadwick dated 29 January 2016:

(i) paragraphs 43-45 and annexures RJC18 to RJC20, to the extent not conceded by the respondents;

(ii) paragraphs 50-65 and annexures RJC27 to RJC39;

(iii) paragraph 80 and annexure RJC49;

(iv) paragraphs 85-87 and annexures RJC54 to RJC56;

(v) paragraphs 90-95 and annexures RJC58 to RJC61;

(vi) paragraph 93 and annexure RJC59;

(d) Affidavit of Mr Chadwick dated 1 February 2016: sub-paragraphs 3(a)-(b) and 4(a)-(h) and annexures RJC62 to RJC69;

(e) Affidavit of Mr Scott Gregson dated 29 January 2016.

38 These parts of the affidavits are relied on by the respondents to provide background and context for the deferral decisions, and to show that there is a live issue concerning Phoenix's underlying entitlement to the relevant amounts. In my view, these parts of the affidavits are relevant on this basis. In respect of some of the parts of the affidavits listed above, objection was also taken on the ground that the evidence was unfairly prejudicial or hearsay. Given the limited way in which the respondents seek to rely on this material, in my view the relevant parts are not unfairly prejudicial and do not constitute hearsay (being relied on for the fact that something was said rather than the truth of the contents of the statement).

39 I note that the respondents did not call the decision-maker in respect of any of the deferral decisions. In these circumstances, the four communications set out in paragraph [4] above provide the only direct evidence of the making and content of each of the deferral decisions.

Statutory construction issues

40 It is convenient to deal with the two main construction issues raised by the parties, before turning to the specific grounds of challenge in relation to each of the deferral decisions. The two construction issues are, first, Phoenix's contention that cl 60(2) does not support a decision to defer a particular payment to a particular provider which is due to it pursuant to an extant determination to make an advance under cl 61(1); and, second, the respondents' contention that a determination by the Secretary that an advance is to be made (under cl 61(1)) does not create an obligation or duty to make the payment but is merely facultative. Although the second issue arises most directly in connection with the matter of relief, it is also important more generally to the issues in dispute. It provides the framework within which to consider the specific grounds of challenge to the deferral decisions raised by Phoenix.

41 The principles applicable to statutory construction have been stated in a number of recent High Court authorities. The starting point in any task of statutory construction is the text of the provision which must be considered in its context including the statutory purpose: Alcan (NT) Alumina Pty Ltd v Commissioner of Territory Revenue (NT) (2009) 239 CLR 27 at [4] per French CJ, at [47] per Hayne, Heydon, Crennan and Kiefel JJ; Commissioner of Taxation v Consolidated Media Holdings Ltd (2012) 250 CLR 503 at [39] per French CJ, Hayne, Crennan, Bell and Gageler JJ; Thiess v Collector of Customs (2014) 250 CLR 664 at [22]-[23] per French CJ, Hayne, Kiefel, Gageler and Keane JJ. In relation to statutory purpose, in Thiess their Honours said (at [23]) that:

Objective discernment of statutory purpose is integral to contextual construction. The requirement of s 15AA of the Acts Interpretation Act 1901 (Cth) that "the interpretation that would best achieve the purpose or object of [an] Act (whether or not that purpose or object is expressly stated ...) is to be preferred to each other interpretation" is in that respect a particular statutory reflection of a general systemic principle. For:

"it is one of the surest indexes of a mature and developed jurisprudence not to make a fortress out of the dictionary; but to remember that statutes always have some purpose or object to accomplish, whose sympathetic and imaginative discovery is the surest guide to their meaning." [Cabell v Markham (1945) 148 F (2d) 737 at 739, quoted in Residual Assco Group Ltd v Spalvins (2000) 202 CLR 629 at [27]]

42 The first issue is whether cl 60(2) can support a decision to defer a particular payment to a particular provider which is due to it pursuant to an extant determination to make an advance under cl 61(1). Phoenix contends that the powers under clauses 60(1) and 60(2) relate to the manner and timing of payments generally and that this construction is supported by textual, contextual and purposive considerations:

(a) Phoenix contends that, by its language, cl 60(2), like cl 60(1), is directed to generic determinations, as appearing in the AIP. It contends that the usage of the plural in cl 60(2) indicates that the determinations contemplated are general, rather than specific in nature; had Parliament intended cl 60(2) to operate in respect of a particular payment, it would have read: "(2) Payment of an amount payable … is to be made at such time as the Secretary determines." Phoenix contrasts the singular language used in clauses 61(1) and 61(1A).

(b) Phoenix contends that the most significant indicator that cl 60(2) does not have the operation for which the respondents contend is the presence and content of cl 61. Clause 61(1) provides for the Secretary to make a determination that an advance is to be made to a particular VET provider on account of amounts that are expected to become payable to it. Such a determination may be varied or revoked under cl 61(1A), but the determination made is of an advance, and once given, the approval is in place unless and until varied or revoked under clause 61(1A). How and when an advance is paid is then governed by the matters determined by the Minister and Secretary under clauses 60(1) and 60(2).

(b) Phoenix contends that the Act makes express that the provision which arises for exercise upon the existence of compliance concerns is cl 61(1A), and not cl 60(2). The power under cl 61(1A), to revoke or vary a cl 61(1) determination to make an advance, is explicitly conditioned upon the Secretary being aware or satisfied of one or more of the compliance concerns set out in cl 61(1A) and further elaborated in cl 61(1B). This is to be contrasted, Phoenix contends, with the simple and general terms of cl 60(2).

(d) Phoenix contends that the structure of the Act points against the power in cl 60(2) being available. The key concepts relating to VFH in Sch 1A are an entitled student and an approved VET provider. Once the student is entitled to receive VFH under cl 43, and is enrolled with an approved VET provider, cl 55 commands payment of the tuition fee by the Commonwealth to the VET provider. A wide discretion to pay a particular fee as and when the Secretary sees fit does not sit well with the mandatory operation of clauses 55 ("must pay") and 61 ("an advance is to be made").

(e) Phoenix submits that the structure of the Act further conveys that cl 60(2) ought not be construed as a means by which the Secretary responds to specific compliance concerns. A procedural scheme for compliance is established under clauses 13 to 26A, with consequences for non-compliance set out in clauses 29 to 39. Those relevant powers in Part 1, Div 5 are vested in the Minister, not in the Secretary.

(f) Phoenix also relies on the Explanatory Memorandum for the enactment that inserted Sch 1A into the Act and contends that this identifies that the purpose of the schedule was to replicate the scheme available to higher education students under the Act, expanding the scope of that scheme to include certain VET qualifications. The Act facilitates enrolment in courses by students, paid for with Commonwealth loans. The purposes of the schedule are stated to be to provide for the approval and monitoring of VET providers, and to promote eligible students enrolling in courses with approved VET providers without needing to pay up-front for courses. Under the schedule, the circumstances in which a Commonwealth loan is payable require the existence of a liability owed by the student to the VET provider. A construction of cl 60(2) that allowed the Secretary to defer a particular scheduled payment to a particular VET provider tends to deny students the ability to discharge their contractual arrangements with VET providers and to undermine the viability of providers and the efficacy of the VFH system.

43 In my view, the construction advanced by Phoenix should not be accepted. First, while it is true that cl 60(2) can be used to make generic determinations as to the timing of payments (of which the AIP may be an example), the text does not suggest that the power conferred by cl 60(2) is limited to generic determinations. The use of the plural ("amounts") does not, to my mind, provide a sufficient textual foundation for the suggestion that the power is limited to generic determinations as to timing. The use of plural in this context is merely a convenient mode of expression. Second, while the power to vary or revoke a determination exists under cl 61(1A), and one of the situations in which this power can be used is where there are compliance concerns, this is not a sufficient basis to read down cl 60(2) as submitted by Phoenix. This is because the clauses are addressed to different matters: cl 61(1A) deals with variation or revocation of a determination, while cl 60(2) deals merely with the timing of payment. Depending on the circumstances, it may be that the Secretary, or his or her delegate, merely wishes to defer payment (for example, to enable investigation of compliance concerns) rather than taking the step of varying or revoking a determination. Third, the structure of Sch 1A does not indicate that the power in cl 60(2) is to be read down as submitted by Phoenix. Clause 55 of Sch 1A provides that, in certain circumstances, the Commonwealth "must … pay" the relevant amount to the provider in discharge of the student's liability to pay his or her tuition fee. Clause 60 provides that the manner and timing of payments are matters to be determined by the Minister and the Secretary respectively (under clauses 60(1) and 60(2)). The clause is applicable to payments under the schedule generally, not just to the payment of advances. There is no apparent reason, based on structure, for reading down those powers so that they can only be used generically and cannot be used in individual cases (including where there are compliance concerns).

44 I turn, then, to the second issue of construction, namely whether the making of a determination under cl 61(1) that an advance is to be made, creates an obligation to pay the amount, or whether the provision is merely facultative. The respondents submit as follows:

(a) The respondents submit that the Act imposes no duty on any of the respondents to pay any amounts by way of advance. The only duty to pay is that found in cl 55 of Sch 1A, and that duty arises only where an identified student is entitled to an amount of assistance. The respondents rely on the statements of principle and general approach taken in Barnes v Victoria [2015] VSCA 343 at [18], [21], [23]-[25], [30] per Santamaria, Ferguson and McLeish JJA.

(b) The respondents submit that neither cl 61 nor any other clause of Sch 1A imposes a duty on any of the respondents to make an advance payment. Even less so is there a duty to pay an amount subject to an advance payment determination on a particular date, determined pursuant to cl 60. An advance payment is in substance an ex gratia payment – under the terms of cl 61, a payment based on amounts expected to become payable, but not in fact payable − made without recognition of legal right or obligation. A decision to make an ex gratia payment does not give rise to any right to sue for the sum in question.

(c) The respondents submit that the Court should be reluctant to adopt a construction of cl 61 that would impose a duty on the Commonwealth or its officers to pay money to a person who has, at the relevant time, no legal entitlement to that money, and only an expectation of such entitlement. The respondents contrast cl 55, which in clear terms confers a duty.

45 In my view, the respondents' construction of cl 61(1) should not be accepted. In other words, in my view, if the Secretary makes a determination under that clause that an advance is to be made to a VET provider on account of an amount that is expected to become payable under a provision of the schedule to the provider, then the amount of the advance is payable by the Commonwealth to the provider, subject to determinations relating to the manner and timing of payment under cl 60. I have come to this view for the following reasons. First, I think this is the natural and ordinary meaning of the words "an advance is to be made". Although it is true that the language is different, and less emphatic, than cl 55 ("the Commonwealth must … pay the amount") the difference is explained by the subject-matter and context. Clause 61(1) is dealing with payment of an amount by way of advance in anticipation of an amount becoming payable in the future. It addresses the practical issue that providers are likely to need funds during the calendar year in order to provide courses, and may not be able to wait until the reconciliation process which usually takes place some months after the end of the year. The language of cl 61(1) reflects the situation it is dealing with. It is possible that the amount of an advance may need to be repaid, if it transpires during the reconciliation process that the provider has been overpaid; but that does not detract from the proposition that the amount of the advance is payable (subject to and in accordance with determinations under cl 60). Second, the formality and detail of the procedure established by cl 61 support the view that the amount of an advance is payable by the Commonwealth. The clause provides for the making of a determination by the Secretary, and for the variation and revocation of that determination in specified circumstances. This is a formal and detailed process, by a very senior decision-maker, consistent with the amount becoming payable (subject to determinations as to the manner and timing of payment under cl 60). Third, a construction to the effect that the amount of the advance is payable should not occasion practical difficulties, given the existence of the power to vary or revoke. If there are concerns about the provider's compliance with requirements, or about the financial viability of the provider, there is an express power, in cl 61(1A), to vary or revoke the determination. For these reasons, I conclude that where the Secretary determines under cl 61(1) that an advance is to be made, then the amount of the advance is payable, subject to determinations regarding the manner and timing of payment under cl 60.

46 I now turn to consider the specific grounds of challenge to the deferral decisions.

The first deferral decision

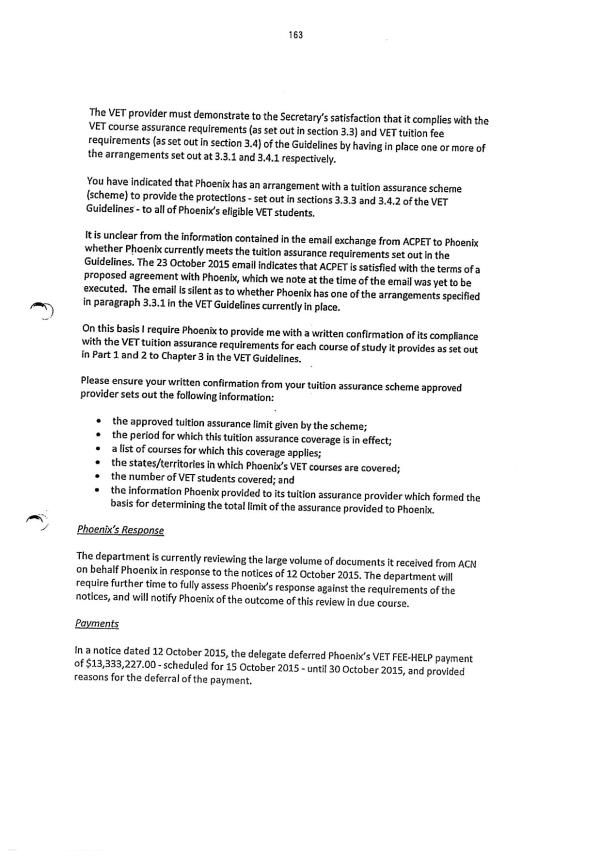

47 The relevant communication in relation to this decision is a one-page notice together with an attachment of five pages. A copy appears as Annexure 1 to these reasons. The notice is headed with the name of the Act followed by the words, "Notice of deferral of payment under paragraphs 238-5(1)(b) and 238-1(1)". It is dated 12 October 2015 and signed by Mr Morling. It was common ground that at all relevant times, Mr Morling was a delegate of both the Minister and the Secretary for the purposes of the exercise of their powers under clauses 60(1) and (2) of Sch 1A to the Act.

48 The notice is in the following terms:

SINCE:

A. The Minister has, under paragraphs 238-5(1)(b) and 238-1(1) of the Higher Education Support Act 2003, delegated his powers under subclause 60(1) and (2) of Schedule 1A to the Act to an APS employee with a classification of SES Employee Band 2 with responsibility for the administration of the VET FEE-HELP scheme.

The reasons why I am considering making this decision to defer the payment of $13,333,277.00 to Phoenix Institute of Australia Pty Ltd ('Phoenix') scheduled for 15 October 2015, until 30 October 2015 are those reasons referenced in Attachment A to the Notice of Intention to Suspend dated 12 October 2015. A copy of Attachment A is attached for your ease of reference.

49 Some initial observations may be made about the notice and attachment. First, the heading to the notice refers to ss 238-5(1)(b) and 238-1(1) of the Act. These are the provisions relating to delegation rather than to deferral of payment. I do not think anything turns on this. Second, the notice refers to the provisions dealing with delegation by the Minister and the Secretary (ss 238-5 and 238-1), and the powers under both cl 60(1) (which is a power of the Minister) and cl 60(2) (which is a power of the Secretary). Third, as indicated in the second paragraph quoted above, the attachment to the notice is a copy of the attachment to the notice of intention to suspend Phoenix's approval as a VET provider, which was issued on the same day.

50 Phoenix contends that the notice was flawed in at least three ways:

(a) it did not contain any decision;

(b) if it was a decision, it was by a delegate of the Minister, when no potentially applicable power was reposed in the Minister; and

(c) it was made in denial of procedural fairness to Phoenix.

51 In relation to the first ground, Phoenix submits that in the notice, Mr Morling used only the words "I am considering making this decision". The attached reasons also use the phrase "I am considering". Phoenix submits that the notice does not make or record any decision at all; and that the notice is no more than an advice to Phoenix of a contemplated decision, on which Phoenix is invited to comment. In my view, this argument should not be accepted. Although the language used in the body of the notice is inapt to cover a decision to defer, I think the heading to the notice sufficiently conveys that the document is giving notice of a decision to defer payment. Also, the inaptness of the language is at least partially explained by the fact that two other notices were given on the same day. It appears that some of the language of the other notices was inadvertently brought across to the second paragraph of this notice.

52 In relation to the second ground, Phoenix submits that the notice recorded and proceeded in reliance on the fact that Mr Morling was the Minister's delegate, and was expressly given and signed by him as "Delegate of the Minister". It was an act only of the Minister, and not of the Secretary. Accordingly, Phoenix submits, if it contained any decision at all, the notice could only have contained a decision under cl 60(1) and not cl 60(2). Phoenix submits that cl 60(1) does not authorise a deferral of the timing of a payment; that clause relates to the manner of payments, in contradistinction to clause 60(2), which deals with the timing of payments. Although I accept that a decision to defer payment, being a decision as to the time of payment, needs to be made by the Secretary under cl 60(2) (rather than the Minister under cl 60(1)), I think there is sufficient indication that the delegate sought to rely on both the delegation from the Secretary as well as the delegation from the Minister, and on cl 60(2) as well as cl 60(1). The heading and the first paragraph refer to s 238-1 (which deals with delegation by the Secretary) as well as s 238-5 (which deals with delegation by the Minister). The first paragraph refers to both clauses 60(1) and (2). In these circumstances, notwithstanding that paragraph A refers to the Minister and Mr Morling signed the notice above a statement that he was "Delegate of the Minister", I think the notice as a whole conveys that he was purporting to act both as the delegate of the Minister and the Secretary, and relying on both cl 60(1) and (2). In any event, for the reasons discussed in paragraph [65] to [71] below, in my view the first deferral decision is not vitiated on this basis.

53 In relation to the third ground, Phoenix submits that, even if the notice made or recorded a decision, the decision was invalid as having denied Phoenix procedural fairness, relying on Saeed v Minister for Immigration and Citizenship (2010) 241 CLR 252 at [25] and [58] per French CJ, Gummow, Hayne, Crennan and Kiefel JJ. Phoenix submits that it was not given any invitation or opportunity to comment and be heard on a proposed decision, which would have been a decision depriving it of its right to receive over $13 million on 15 October 2015. (There is no dispute about the fact that Phoenix was not given an opportunity to comment before the first deferral decision was made.) Phoenix submits that it is no answer to say that the deferral was interim, because the deferral itself was a serious adverse decision: see Dura (Australia) Construction Pty Ltd v Victorian Managed Insurance Authority (2009) 31 VAR 193 at [13] per Warren CJ, Nettle and Redlich JJ.

54 In my view, while there may be circumstances where it may be necessary to give a provider an opportunity to be heard before making a decision regarding the timing of a payment, in relation to the first deferral decision the content of the requirement of procedural fairness was reduced to zero. The deferral of payment of the instalment was for a short period of time (from 15 October to 30 October 2015). It did not affect Phoenix's entitlement to the advance or its ultimate entitlement to be paid under cl 55; it merely deferred payment of the instalment for a short period of time. Further, the purpose of the three notices issued on 12 October 2015 was to outline the Department's concerns and to provide Phoenix with an opportunity to respond to those concerns. While Phoenix was not given the opportunity to comment before the first deferral decision was made, that decision formed part of a broader process of providing procedural fairness to Phoenix: cf South Australia v O'Shea (1987) 163 CLR 378 at 389 per Mason CJ; Ainsworth v Criminal Justice Commission (1992) 175 CLR 564 at 578 per Mason CJ, Dawson, Toohey and Gaudron JJ.

55 Phoenix also relies on the construction argument discussed in paragraphs [42]-[43] above. For the reasons there given, I do not accept that construction.

56 For these reasons, in my view, the grounds of challenge to the first deferral decision are not made out.

The second deferral decision

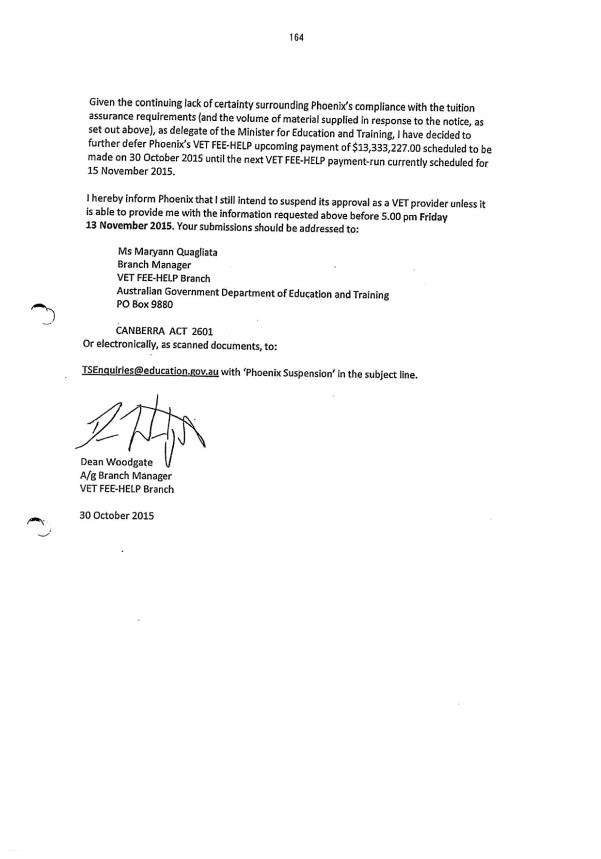

57 The relevant communication in relation to the second deferral decision is a three-page letter, a copy of which appears as Annexure 2 to these reasons. The letter is signed by Mr Woodgate and dated 30 October 2015. It was common ground that at all relevant times, Mr Woodgate was a delegate of both the Minister and the Secretary for the purposes of the exercise of their powers under clauses 60(1) and (2) of Sch 1A to the Act.

58 The letter starts by referring to the three notices dated 12 October 2015. The letter then sets out concerns regarding compliance with VET tuition assurance requirements and requires Phoenix to provide certain information. The letter contains the following paragraphs regarding payments:

In a notice dated 12 October 2015, the delegate deferred Phoenix's VET FEE-HELP payment of $13,333,227.00 - scheduled for 15 October 2015 - until 30 October 2015, and provided reasons for the deferral of the payment.

Given the continuing lack of certainty surrounding Phoenix's compliance with the tuition assurance requirements (and the volume of material supplied in response to the notice, as set out above), as delegate of the Minister for Education and Training, I have decided to further defer Phoenix's VET FEE-HELP upcoming payment of $13,333,227.00 scheduled to be made on 30 October 2015 until the next VET FEE-HELP payment-run currently scheduled for 15 November 2015.

59 Unlike the notice dated 12 October 2015, which relied on the delegations from both the Minister and the Secretary, the letter dated 30 October 2015 refers only to the delegation from the Minister.

60 Phoenix contends that the 30 October letter was ineffective or invalid because: it depended on the efficacy of the defective 12 October notice; and it was an act of the Minister, whereas the only potentially relevant power was that of the Secretary. As I have decided that the first deferral decision was effective, the first ground of challenge to the second deferral decision falls away.

61 In relation to the second ground of challenge, Phoenix contends that the letter contained a decision of the Minister, through his delegate, whereas the only even arguably applicable power to defer was a power of the Secretary, under cl 60(2). Phoenix reiterates its submissions on this issue referred to in paragraph [52] above.

62 The respondents submit that, assuming, for the sake of argument, the decision in question was one that was required to be made by the Secretary or her delegate, the evidence demonstrates that the Secretary had delegated her powers under Sch 1A to Mr Woodgate. The respondents submit that the fact that the document evidencing the decision did not refer to the delegation by the Secretary does not render the exercise of the delegated power invalid. They submit that a decision is not invalid merely because the decision-maker erroneously referred to the incorrect head of power: Eastman v Director of Public Prosecutions (ACT) (2003) 214 CLR 318 at [124] per Heydon J, and the authorities cited in fn 93 (in the CLR report); Mercantile Mutual Life Insurance v Australian Securities Commission (1993) 40 FCR 409 at 412-414 per Black CJ and 437, 441-442 per Gummow J. The respondents contend that it is sufficient in law that each decision-maker in fact held the necessary delegation.

63 Phoenix responds that there is a substantive difference between the present situation and a case where a decision-maker relies on an incorrect head of power (where an available head of power exists and the conditions for its exercise are satisfied). Here, Phoenix submits, the only person with the applicable power (the Secretary) did not purport to act.

64 As indicated in paragraph [52] above, I accept that a decision to defer payment, being a decision as to the time of payment, needs to be made by the Secretary under cl 60(2) rather than the Minister under cl 60(1). The question, then, is whether the second deferral decision is effective to defer payment in circumstances where the decision-maker purported to act as the delegate of the Minister rather than as the delegate of the Secretary.

65 In Brown v West (1990) 169 CLR 195, Mason CJ, Brennan, Deane, Dawson and Toohey JJ said (at 203) that "the validity of the Tribunal's determinations is unaffected by mistaking the source of the power to make them". In support of that proposition, their Honours cited Moore v Attorney-General (Irish Free State) [1935] AC 484 and R v Bevan; ex parte Elias and Gordon (1942) 66 CLR 452 at 487. In the latter case, Williams J explained (at 486-487) that the officer convening the court-martial was authorised both by the Admiralty and by the Governor-General, and that he convened the court-martial under his Australian authority. After pointing out that he could have convened the court under the authority conferred upon him by his commission from the Admiralty, Williams J said (at 487):

Even if he did err as to the source of an authority which he undoubtedly possessed his mistake in no way affected the personnel of the court or its proceedings, so that all the conditions on which the right of the court-martial to exercise jurisdiction depended were in fact fulfilled. His mistake under such circumstances would be in a non-essential matter which would not amount to want of jurisdiction (Moore v Attorney-General for the Irish Free State).

(footnote omitted)

66 In Mercantile Mutual Life Insurance Co Limited v Australian Securities Commission (1993) 40 FCR 409, the Australian Securities Commission (ASC) delegated certain powers to the second respondent. The second respondent authorised the third respondents to apply for a court order. The authorisation was expressed to be made pursuant to a particular provision of the Corporations Law. The Full Court of this Court held that the authorisation did not identify the correct source of power, but (applying Brown v West) that this did not affect its validity: see at 412-413 per Black CJ, at 424-425 per Lockhart J, at 435-437 per Gummow J. Black CJ said (at 412-413):

Although the instrument of authorisation reveals, in my view, that the ASC mistook the source of its power, in the sense that s 597 does not of itself confer the power sought to be exercised, it is clear that the ASC intended the discharge, in relation to BPTC, of the function of authorising persons to make an application for an order pursuant to provisions of s 597 of the Corporations Law. It was under no statutory obligation to specify the source of the power under which it was acting and no consequence attached to the specification of a source of power that did not in fact exist. The circumstances relevant to the proper exercise of the power were exactly the same whether the source of the power was s 597(1) of the Corporations Law, as it supposed, or whether the source was s 11(4) of the ASC Act operating in combination with s 597. The function for which s 11(4) provided the necessary power was the precise function to which the instrument of authorisation, which referred to both powers and functions, was directed and for purposes concerning the validity of the exercise of the power it was quite immaterial whether the source was s 597(1) or whether it was s 11(4) of the ASC Act in combination with s 597(2).

67 Gummow J said (at 437):

In my view, the truth of the matter can only be found by analysis of the particular statute or other written law said to authorise or empower the making of the decision in question. Having regard to any specification of manner and form and, on a more general level, to the subject matter, scope and purpose of the law, is it a requirement that the decision-maker specify in writing the source of the authority relied upon?

… If there be no such requirement, or if the requirement be directory in character, it must be very difficult to sustain a case that the propriety of the decision in question is to be judged by that head of power expressly relied upon (if any) to the exclusion of any other enabling authority.

Here, none of the heads of power suggested to support the authorisation specify any particular form, nor, indeed, that it be embodied in any written instrument. Nor does reliance upon one rather than another head of power lead to any difference in the consequences for third parties, such as the present applicants. The position was rather different with the legislation considered in Saatchi & Saatchi (supra).

68 Also, in the course of their reasons, both Black CJ and Gummow J referred to the possibility that the authorisation had referred to the wrong instrument of delegation. There had been two instruments of delegation and, on one view, the authorisation incorrectly referred to the first rather than the second instrument of delegation. Their Honours did not consider this to affect the efficacy of the authorisation. Black CJ said (at 414):

For reasons similar to those that lead to the conclusion that the incorrect assumption and statement of the source of the power in relation to the instrument of authorisation do not invalidate the exercise of the power to authorise, the reference to the first instrument of delegation in the recital to the instrument of authorisation does not preclude reliance upon the second instrument of delegation as a source of authority.

69 To like effect, Gummow J said (at 437):

In my view, the court should accept the submission for the respondents that the expressed reliance in the Instrument of Authorisation of 2 April 1992 upon s 597(1) is not fatal to the existence of the necessary authority in the Commissioner if it may be supported by another head of power. (For similar reasons, the recital in that instrument of the first delegation does not foreclose reliance upon the second delegation).

(emphasis added)

70 In Eastman v Director of Public Prosecutions (ACT) (2003) 214 CLR 318, Heydon J said (at [124]) that "[i]f the maker of an administrative decision purports to act under one head of power which does not exist, but there is another head of power available and all conditions antecedent to its valid exercise have been satisfied, the decision is valid despite purported reliance on the unavailable head of power".

71 The situation in the present case is not on all fours with the decisions considered above. Nevertheless, the situation is similar to that considered by Williams J in R v Bevan; ex parte Elias and Gordon (1942) 66 CLR 452 at 487. By parity of reasoning, in the present case, the decision-maker's mistaken reliance on the delegation from the Minister rather than the delegation from the Secretary (which he possessed) should not vitiate the decision. Further, although the case involves a mistaken reliance on the delegation from the Minister rather than the delegation from the Secretary, it is not substantively different from a mistaken reliance on an incorrect head of power. The reference to one delegation rather than the other implicitly involves reliance on cl 60(1) rather than cl 60(2), and thus reliance on an incorrect head of power. In these circumstances, the line of cases, discussed above, concerning reliance on an incorrect head of power provides further support for the conclusion that the mistaken reliance on the wrong delegation does not vitiate the decision.

72 Phoenix also relies on the construction argument discussed in paragraphs [42]-[43] above. For the reasons there given, I do not accept that construction.

73 For these reasons, in my view, the grounds of challenge to the second deferral decision are not made out.

The third deferral decision

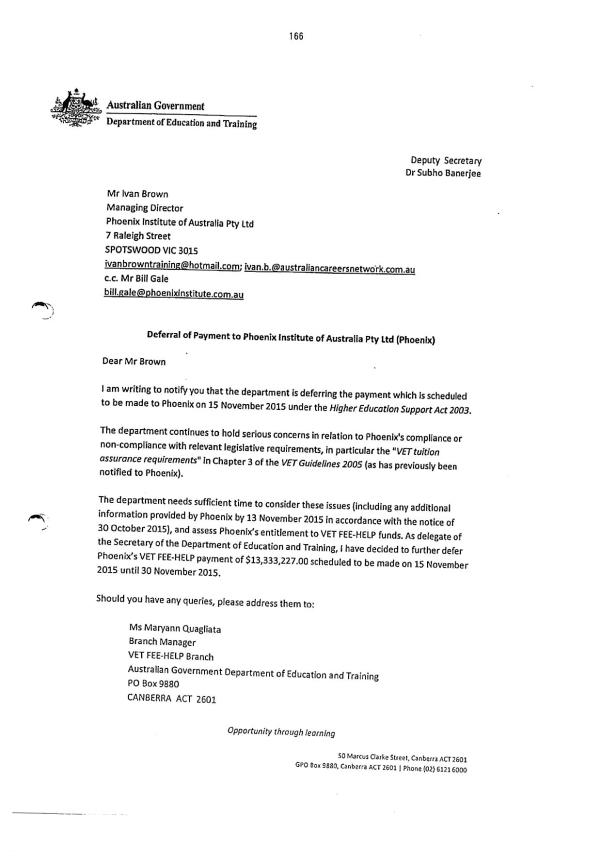

74 The relevant communication in relation to the third deferral decision is a two-page letter, a copy of which appears as Annexure 3 to these reasons. The letter is signed by Dr Banerjee and dated 13 November 2015. It was common ground that at all relevant times, Dr Banerjee was a delegate of both the Minister and the Secretary for the purposes of the exercise of their powers under clauses 60(1) and (2) of Sch 1A to the Act. The letter is headed "Deferral of Payment to Phoenix …" and states in part:

I am writing to notify you that the department is deferring the payment which is scheduled to be made to Phoenix on 15 November 2015 under [the Act]. …

The department needs sufficient time to consider these issues (including any additional information provided by Phoenix by 13 November 2015 in accordance with the notice of 30 October 2015), and assess Phoenix's entitlement to VET FEE-HELP funds. As delegate of the Secretary of the Department of Education and Training, I have decided to further defer Phoenix's VET FEE-HELP payment of $13,333.227.00 scheduled to be made on 15 November 2015 until 30 November 2015.

75 Phoenix contends that, properly understood, the 13 November letter purported to defer the October payment, not the November payment. That is apparent, Phoenix contends, from the fact that it records the delegate's decision to "further defer" the "payment of $13,333,227.00 scheduled to be made on 15 November 2015". Further deferral was a step only apposite and possible in respect of the allegedly previously deferred October payment, not the November payment, which had not previously been deferred. Phoenix submits that this is supported by the fact that the amount referred to in the 13 November letter matches the amount referred to in the 30 October letter, rather than the scheduled amount of the November payment.

76 In my view, reading the letter as a whole, and in context, it gives notice of a decision to defer the total amount which was now scheduled to be paid on 15 November 2015, that is, the amount that was originally due on 15 October (the payment of which had been deferred to 15 November) and the amount originally scheduled to be paid on 15 November. The context included the fact that the Department had raised serious concerns in relation to Phoenix in the three notices dated 12 October 2015, and that officers of the Department had deferred payment of the amount originally due on 15 October to 15 November. There is no suggestion that the matters concerning the Department had been resolved by 13 November. In these circumstances, it would be surprising if an officer of the Department decided to defer payment of one amount of approximately $13 million, but not the other. Read in this context, the first paragraph of the letter gives notice of a decision to defer payment of the total amount now scheduled to be paid on 15 November 2015. It is true that the third paragraph, particularly the words "further defer" and the reference to a single amount of approximately $13 million, taken in isolation, suggests that the deferral related only to the October payment. However, when the letter is read as a whole and in the context I have outlined, I think the better view is that it gives notice of a decision to defer the total amount now scheduled for payment on 15 November.

77 Phoenix also relies on the construction argument discussed in paragraphs [42]-[43] above. For the reasons there given, I do not accept that construction.

78 For these reasons, in my view, the grounds of challenge to the third deferral decision are not made out.

The fourth deferral decision

79 The relevant communication in relation to the fourth deferral decision is a notice of deferral together with two attachments. A copy of the notice and attachments appears as Annexure 4 to these reasons. The notice is signed by Dr Banerjee and dated 27 November 2015. The notice is headed with the name of the Act, followed by "Notice of deferral of payment under clause 60". The first paragraph refers to the delegations by the Minister and the Secretary of their powers under clauses 60(1) and 60(2) of Sch 1A to the Act. The second paragraph states that the decision-maker has considered the issues outlined in Attachment A to the notice. The third paragraph of the notice states:

I have decided to defer the payment to Phoenix Institute of Australia Pty Ltd scheduled for 30 November 2015 and 15 December 2015, until 15 January 2016 for those reasons referenced in Attachment A to this notice.

80 The notice is signed by Dr Banerjee as both delegate of the Minister and delegate of the Secretary.

81 Phoenix submits that the decision the subject of this notice was ineffective and invalid for two reasons. First, Phoenix submits that the decision purported to defer three payments to 15 January 2016: the payment for December, which was due on 15 December, and the payments for October and November, which had supposedly been deferred to 30 November. Phoenix submits that, for the reasons submitted in relation to the earlier deferral decisions, the October and November payments had not in fact been deferred, and liability to make those payments had already crystallised in the Commonwealth. In consequence, Phoenix submits, the notice dated 27 November was ineffective in respect of those payments, and at most could affect the 15 December payment. In light of the conclusions I have reached in relation to the earlier deferral decisions, this argument falls away.

82 Secondly, Phoenix submits that there was no power to make the decision. This argument has been dealt with in paragraphs [42]-[43] above.

83 For these reasons, in my view, the grounds of challenge to the fourth deferral decision are not made out.

Relief and discretionary considerations

84 In light of the conclusions I have reached, it is not necessary to consider the parties' submissions as to relief and discretionary considerations. However, given that detailed submissions were made about these matters, I make the following observations.

85 First, it was common ground that there is a discretionary element to the relief sought by Phoenix: see, eg, Commissioner of Taxation v Multiflex Pty Ltd (2011) 197 FCR 580 at [42] per Stone, Edmonds and Logan JJ; Fares Rural Meat and Livestock Co Pty Ltd v Australian Meat and Live-stock Corporation (1990) 96 ALR 153 at 170-171 per Gummow J. See also Aronson and Groves, Judicial Review of Administrative Action (5th ed, 2013), p 820 [13.200].

86 Second, if I had concluded that one or more of the deferral decisions was invalid, it would have been necessary to consider the impact, if any, of the revocation of the advance payment determination on 14 January 2016. In my view, assuming (without deciding) that the revocation did not have the effect that unpaid amounts ceased to be payable, the revocation may nevertheless have constituted a discretionary basis for refusing relief in the circumstances. While one can appreciate the practical importance to a provider of obtaining advance payments, in circumstances where the Secretary has revoked the advance payment determination (on one of the bases set out in cl 61(1A)), the Court may well have concluded that it would be inappropriate to order the Commonwealth to pay an unpaid instalment, and that it would be preferable to leave the matter to be resolved as part of the reconciliation process. I note that the bases for revocation of an advance payment determination under cl 61(1A) are: that the Secretary is satisfied that the provider has not complied with Sch 1A to the Act and any regulations relating to the schedule, and the VET Guidelines that apply to the provider; that the Secretary is aware of information that suggests that the provider may not comply with the schedule and any regulations relating to the schedule, and the VET Guidelines that apply to the provider; or that the Secretary is aware of information that suggests that the provider may not remain financially viable. In deciding whether to take action under cl 61(1A), the Secretary may consider the matters in cl 61(1B). It is also important to note that whether or not an instalment of an advance is paid does not affect the provider's ultimate entitlement to payment under cl 55.

87 Third, the evidence establishes, in my view, that there is a live issue as to Phoenix's ultimate entitlement to payment for the 2015 calendar year and that Phoenix is currently in difficult financial circumstances. In relation to there being a live issue as to Phoenix's ultimate entitlement, I refer to: the Ernst & Young report dated 24 December 2015; the second Ernst & Young report dated 25 January 2016; and the audit of the veracity of Phoenix's enrolments. In relation to Phoenix currently being in financial difficulties, I refer to: ASQA's cancellation of Phoenix's registration (although this is subject to a stay, that is conditional on Phoenix not enrolling new students this year); the suspension of, and notice of intention to revoke, Phoenix's approval as a VET provider; and the evidence of Mr Opolion. Phoenix contends that its financial difficulties are largely because the Commonwealth has not paid the three advance instalments. Be that as it may, if the Court were to order that the Commonwealth pay approximately $40 million to Phoenix, it is possible that Phoenix would not be able to repay that money in the event that, at the reconciliation for the 2015 calendar year, it was determined that some or all of it was repayable. In my view, these matters may well have constituted a discretionary basis for refusing relief if I had concluded that one or more of the deferral decisions was invalid.

Conclusion

88 For the reasons given above, the grounds of challenge in respect of the deferral decisions are not made out. It follows that the proceeding should be dismissed.

I certify that the preceding eighty-eight (88) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Moshinsky. |

Associate:

ANNEXURE 1

ANNEXURE 2

ANNEXURE 3

ANNEXURE 4