FEDERAL COURT OF AUSTRALIA

Tax Practitioners Board v Lamede Group Proprietary Limited [2016] FCA 63

QUD 125 of 2014 | ||

BETWEEN: | TAX PRACTITIONERS BOARD Applicant | |

AND: | LAMEDE GROUP PROPRIETARY LIMITED ACN 148 020 017 First Respondent LORRAINE GALE AMEDE Second Respondent | |

JUDGE: | DOWSETT J |

DATE: | 10 february 2016 |

These proceedings

1 The applicant (the “Board”), seeks declaratory, injunctive and other relief against the first and second respondents (“Lamede Group” and “Ms Amede” respectively) for admitted contraventions of ss 50-5(1) and 50-10(1) of the Tax Agent Services Act 2009 (Cth) (“TASA”). The contraventions involved the provision and advertising of tax agent services whilst each of the respondents was not a registered tax agent.

2 Ms Amede is the sole director of Lamede Group. Neither respondent was legally represented. Rule 4.01(2) of the Federal Court Rules 2011 (Cth) (the “Rules”) provides that “[a] corporation must not proceed in the Court other than by a lawyer”. At the commencement of the hearing, Ms Amede sought leave to appear on behalf of Lamede Group. This was not opposed. However she had no evidence of her authority so to appear. Counsel for the Board produced an historical company extract for Lamede Group (exhibit 1). It demonstrates that Ms Amede is, in fact, the sole director. The respondents’ previous solicitors had executed a statement of agreed facts. It was filed on 29 May 2014, pursuant to s 191 of the Evidence Act 1995 (Cth) (the “Evidence Act”). I am satisfied that the statement of agreed facts provides a proper basis upon which the Court may act. The hearing proceeded on the basis that Lamede Group had not appeared. However the Board accepted that submissions made by Ms Amede on her own behalf should be taken into account in the proceedings against Lamede Group. The statement of agreed facts is attached to these reasons. In the course of the hearing, counsel for the Board indicated that it did not press para 2 (to the extent that it dealt with an alleged contravention of s 50-15 of TASA) and para 56. At the hearing, Ms Amede sought to resile from some aspects of the statement.

3 I granted the Board leave to read and file an affidavit of Alexander John Gilmour Tate, sworn on 26 March 2015. The Board also read an affidavit by the same deponent, filed on 24 March 2014. It dealt with costs. Ms Amede sought to tender a letter dated 27 March 2014. It seems to have been written at an earlier date. Counsel for the Board objected to its receipt on the basis that it was evidentiary rather than by way of submission. Ms Amede was sworn as a witness in order to facilitate receipt of the letter into evidence. It became exhibit 2. Counsel for the Board cross-examined Ms Amede.

Legislative Framework

4 Subdiv 50-A of TASA prohibits certain conduct by a person or company who, or which is not registered. Registration is provided for in Pt 2. Relevantly, the Board submits that the respondents contravened ss 50-5(1) and 50-10(1). Section 50-5(1) provides:

You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a tax agent service; and

(b) the tax agent service is not a BAS service; and

(c) you charge or receive a fee or other reward for providing the tax agent service; and

(d) you are not a registered tax agent; and

(e) if you provide the tax agent service as a legal service—either:

(i) you are prohibited, under a State law or Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service consists of preparing, or lodging, a return or a statement in the nature of a return.

Civil penalty:

(a) for an individual—250 penalty units; and

(b) for a body corporate—1,250 penalty units.

5 Section 50-10(1) provides:

You contravene this subsection if:

(a) you advertise that you will provide a tax agent service; and

(b) the tax agent service is not a BAS service; and

(c) you are not a registered tax agent; and

(d) if the tax agent service would be provided as a legal service—either:

(i) you are prohibited, under a State law or Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service would consist of preparing, or lodging, a return or a statement in the nature of a return; and

(e) if the tax agent service would be provided on a voluntary basis—you would not provide the service under a scheme approved by the Commissioner by notice published in the Gazette.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

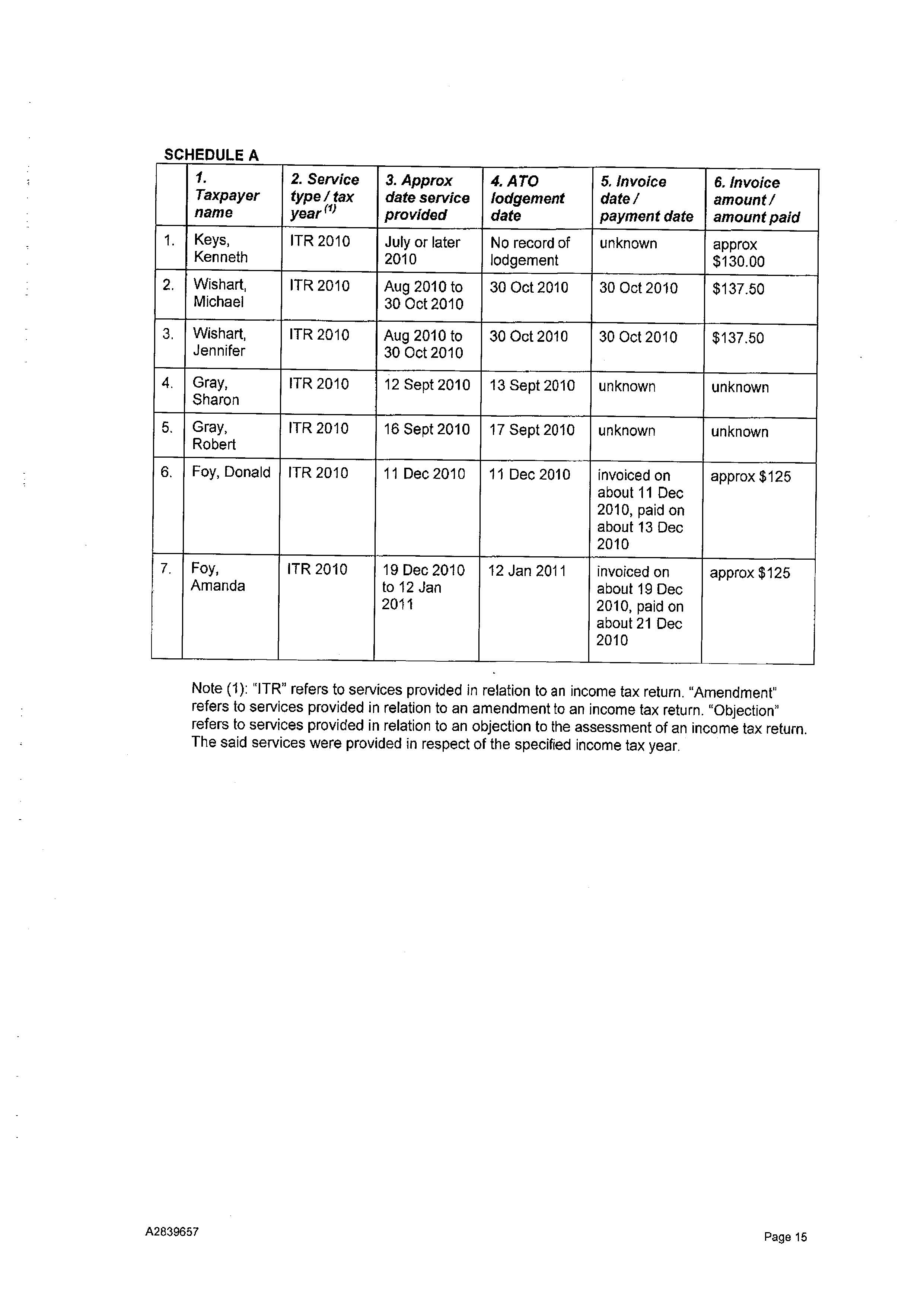

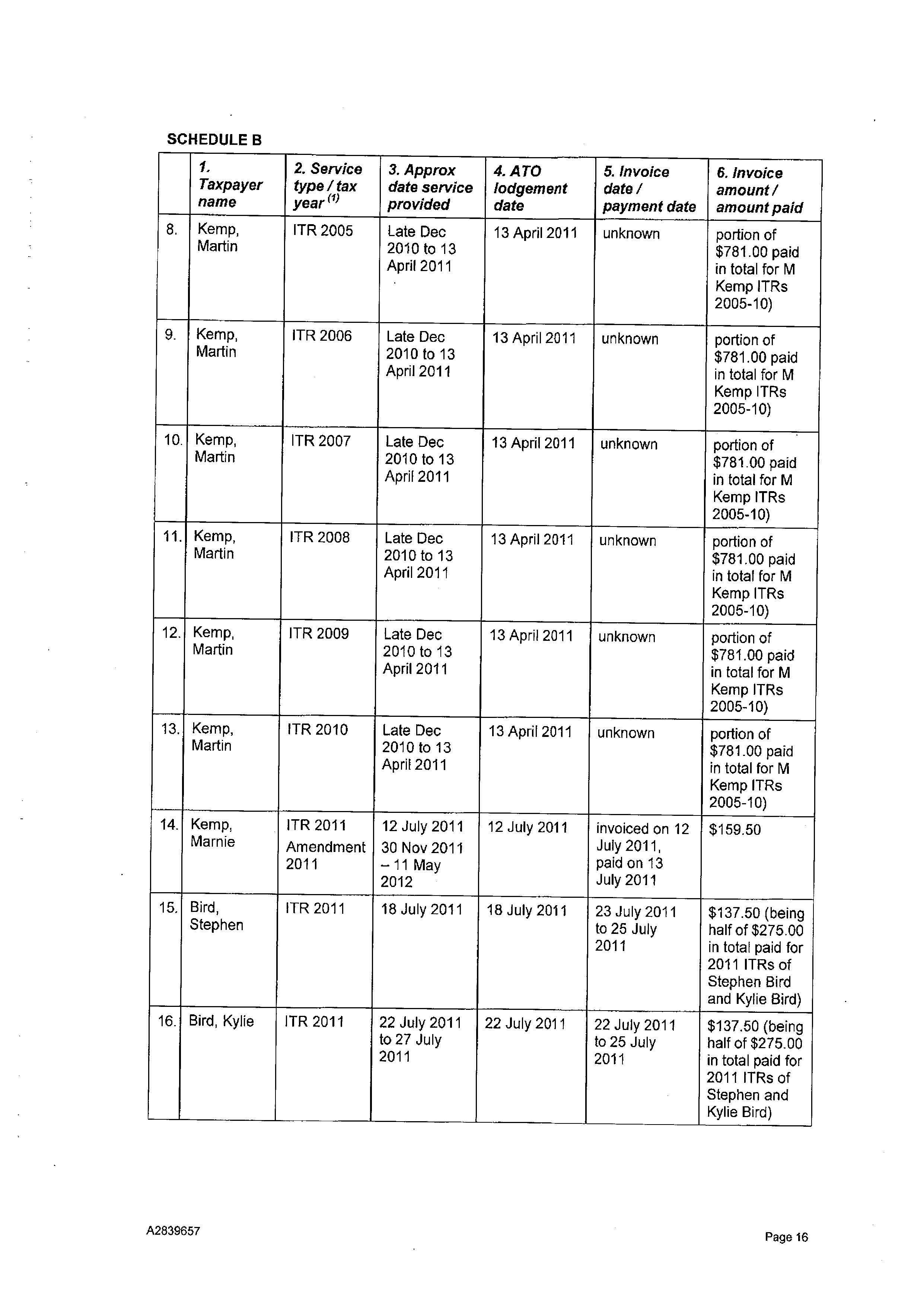

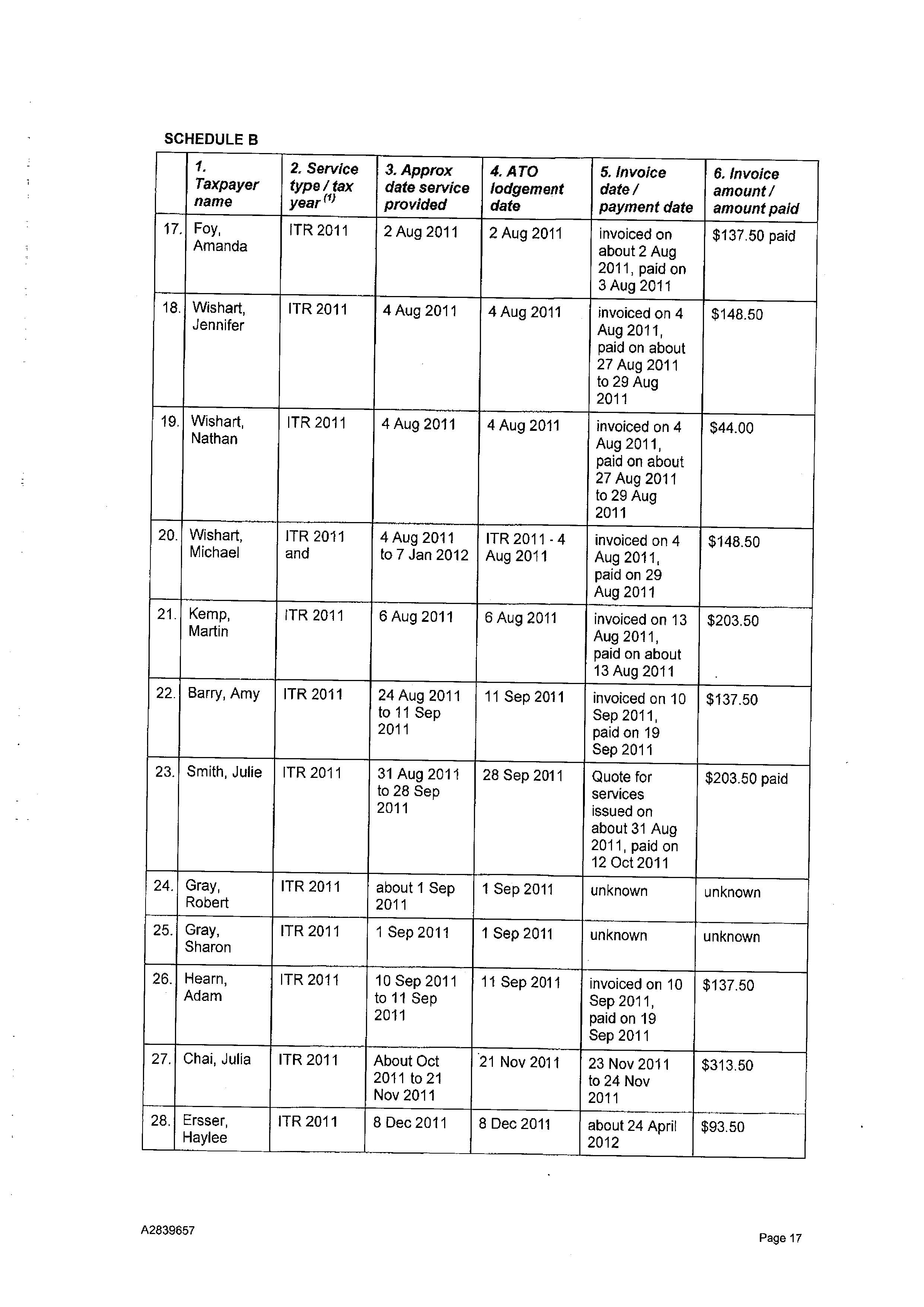

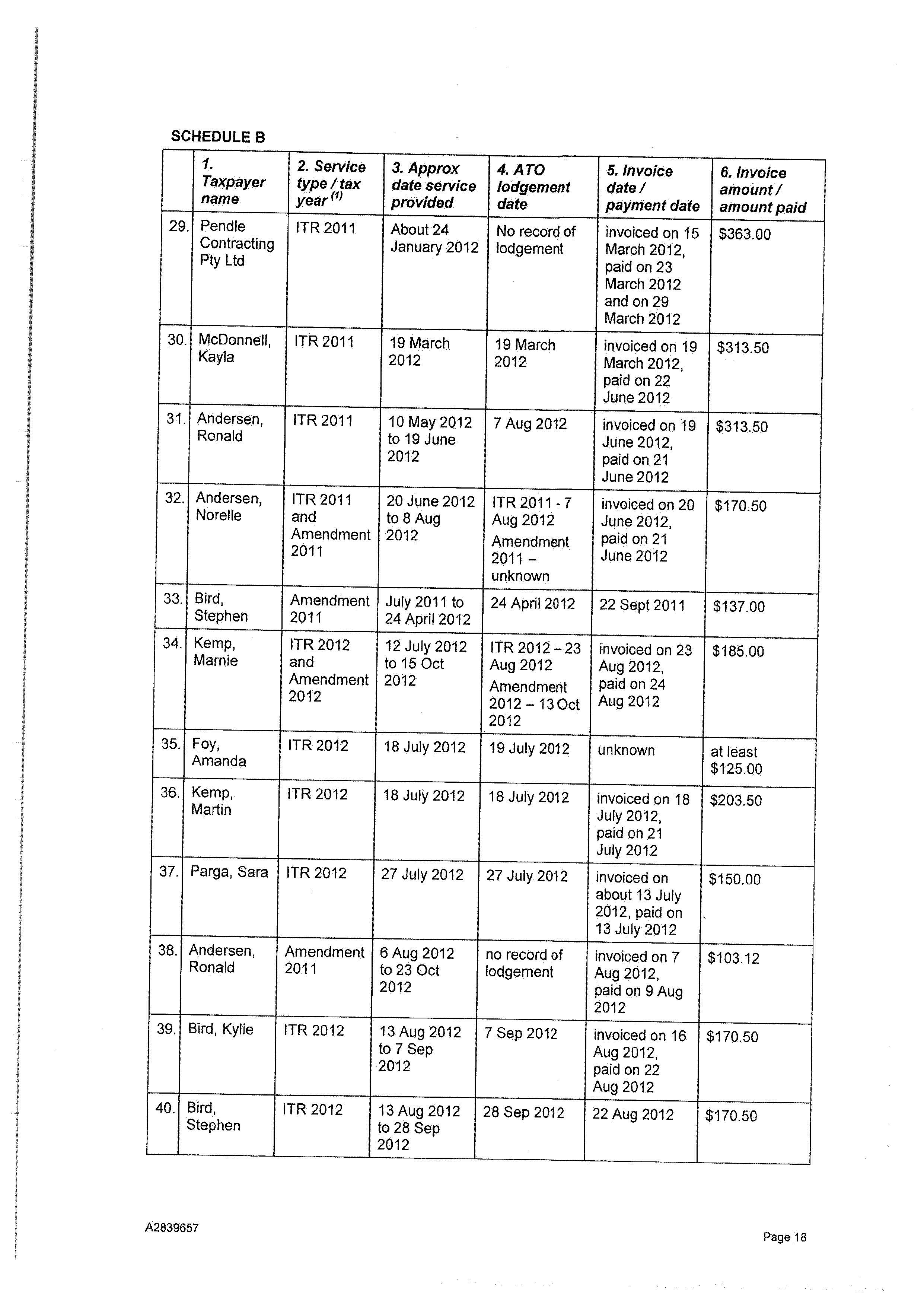

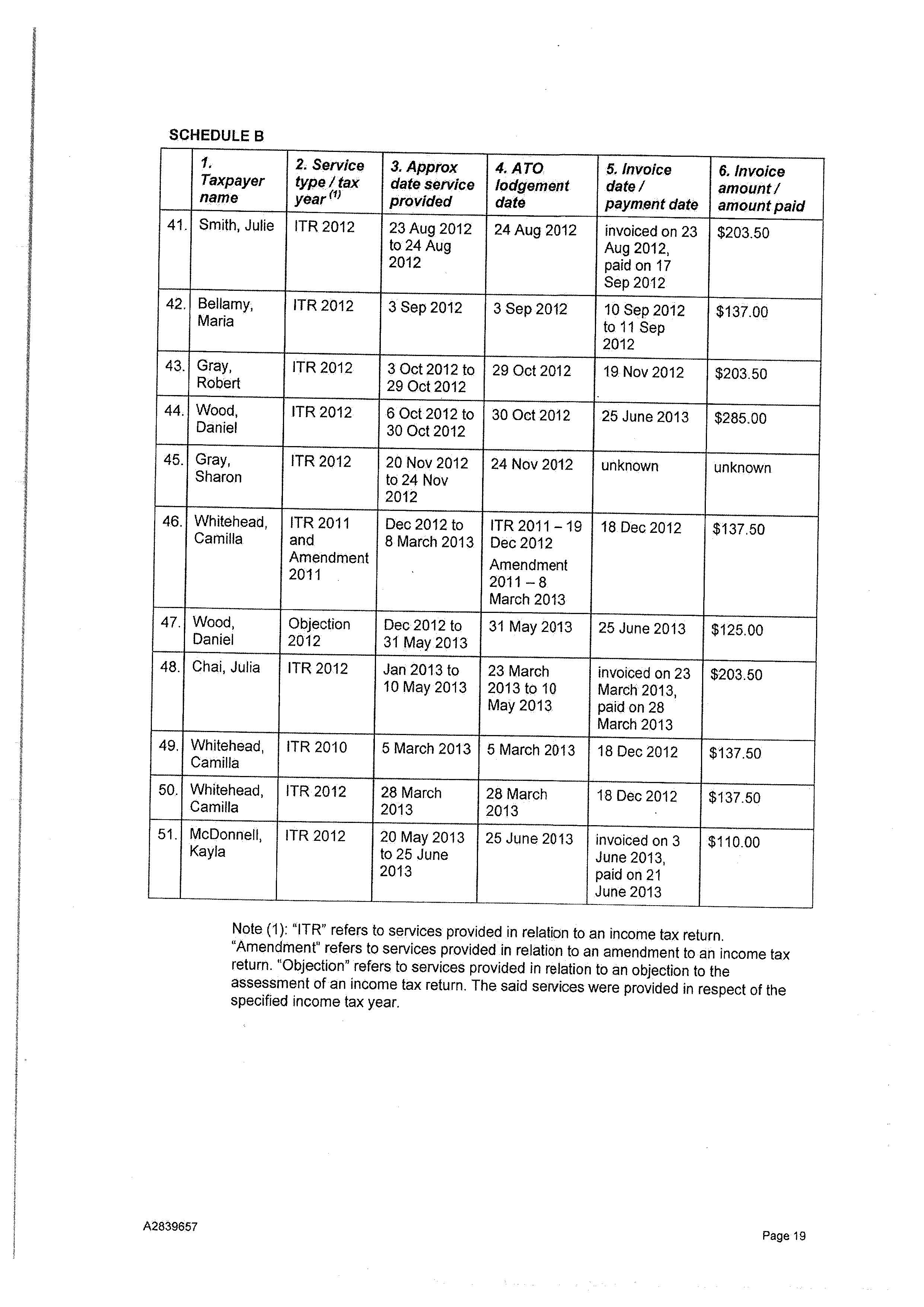

6 The terms “registered tax agent” and “registered BAS agent” mean respectively an entity registered under TASA as a tax or BAS agent. A “tax agent service” has the meaning given to it by s 90-5 which provides:

(1) A tax agent service is any service:

(a) that relates to:

(i) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise, under a taxation law; or

(ii) advising an entity about liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a taxation law; or

(iii) representing an entity in their dealings with the Commissioner; and

(b) that is provided in circumstances where the entity can reasonably be expected to rely on the service for either or both of the following purposes:

(i) to satisfy liabilities or obligations that arise, or could arise, under a taxation law;

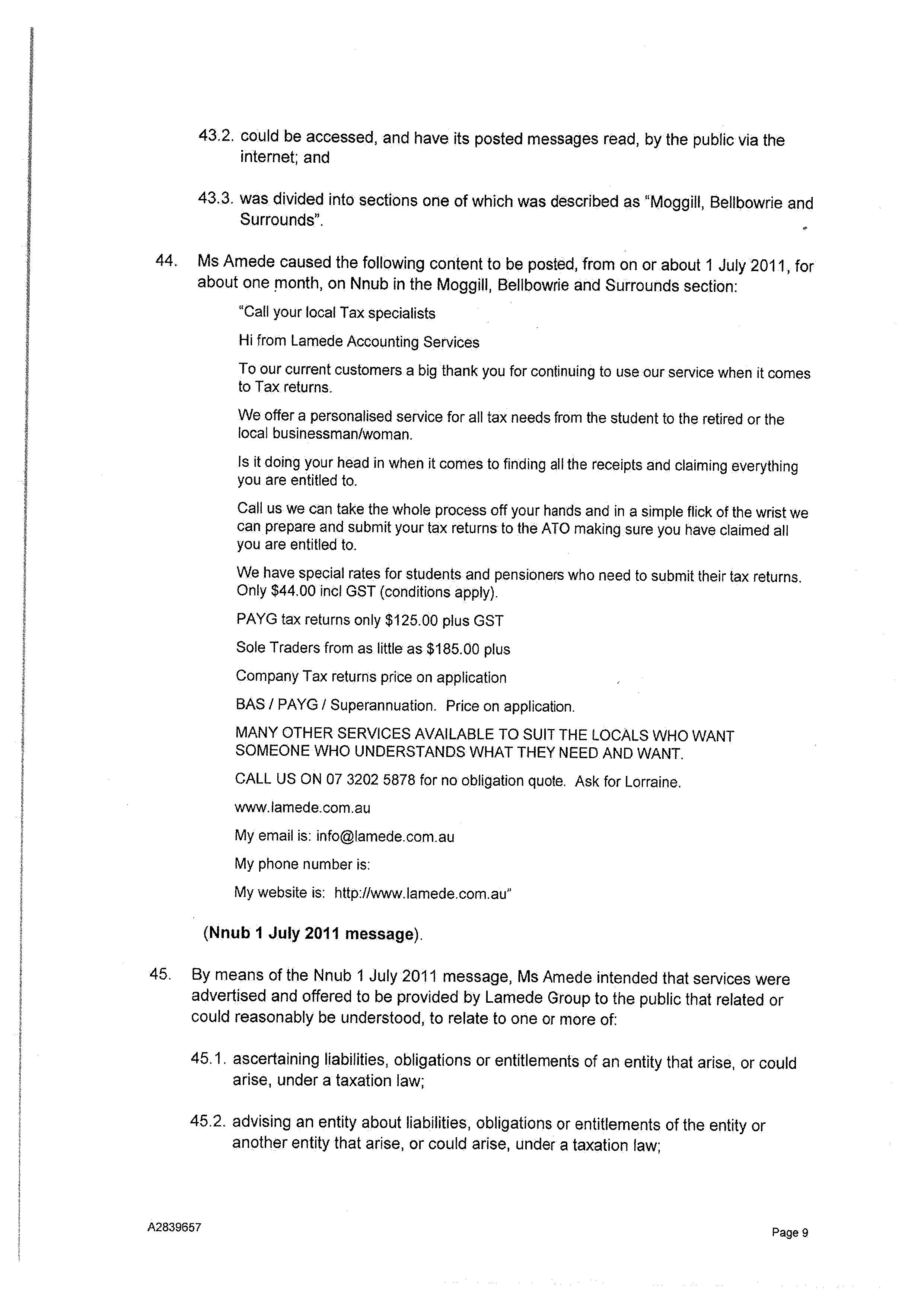

(ii) to claim entitlements that arise, or could arise, under a taxation law.

(2) A service specified in the regulations for the purposes of this subsection is not a tax agent service.

Statement of Agreed Facts

7 Section 191(2) of the Evidence Act provides:

In a proceeding:

(a) evidence is not required to prove the existence of an agreed fact; and

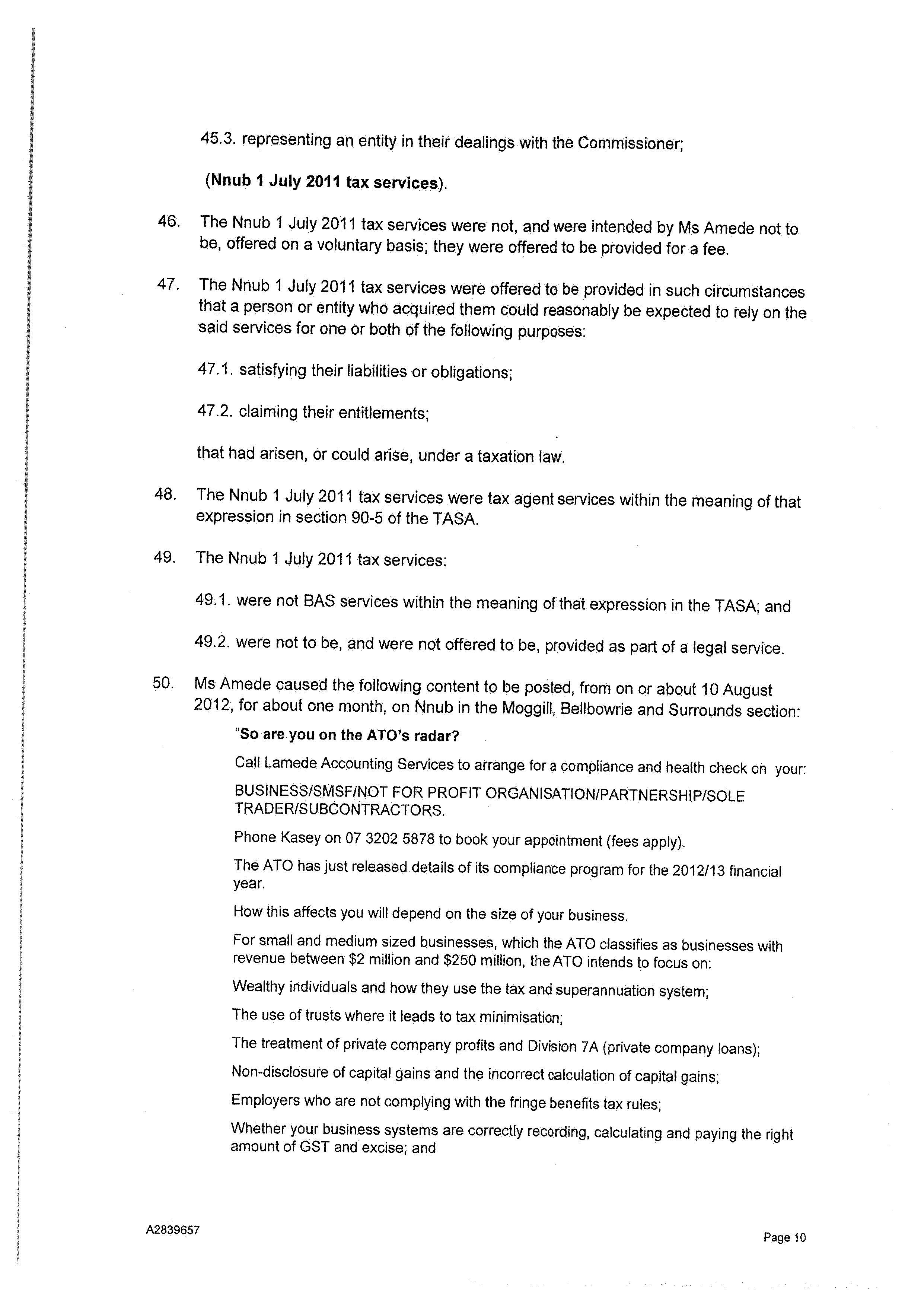

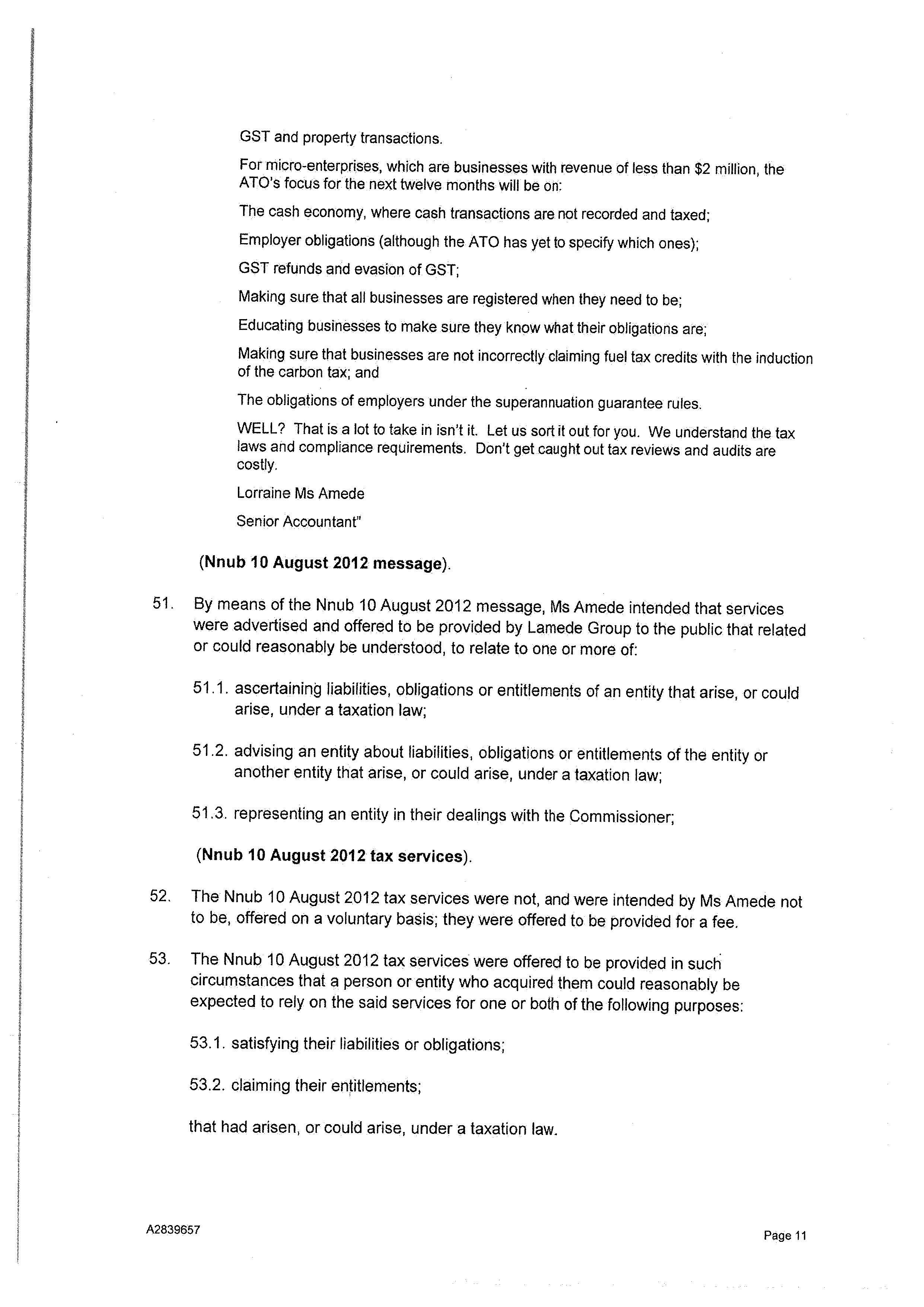

(b) evidence may not be adduced to contradict or qualify an agreed fact;

unless the court gives leave.

8 An “agreed fact” is defined in s 191(1) as “a fact that the parties to a proceeding have agreed is not, for the purposes of the proceeding, to be disputed”. In Australian Competition and Consumer Commission v Alvaton Holdings Pty Ltd [2010] FCA 760, Gilmour J said at [3]:

This does not mean that the Court must necessarily accept it as a fact: Minister for the Environment, Heritage and the Arts v PGP Developments Pty Limited [2010] FCA 58 at [35]. Ordinarily however, it seems to me, a Court will treat agreed facts as facts for the purposes of the proceeding.

9 Section 191 “does not prescribe the weight that is to be given to that evidence”. See Secretary, Department of Health & Ageing v Prime Nature Prize Pty Ltd (in liq) [2010] FCA 597 at [5] per Stone J. Furthermore, s 191 of the Evidence Act only applies to “facts”. Stone J said at [6]:

As it happened, the document tendered as a statement of agreed facts included not only statements of facts, but also statements of argument and conclusion. The distinction is important as s 191 only applies to facts. While I must accept those facts as evidence in the proceeding, I am not obliged to accept the parties’ submissions even if agreed between them and contained in the s 191 statement.

10 The statement of agreed facts contains a mixture of facts, arguments and conclusions. I am not obliged to accept statements that are not facts in the sense used in s 191 of the Evidence Act.

11 In FV v The Queen [2006] NSWCCA 237 at [42] - [44], Kirby J (with whom McClellan CJ and Hoeben J agreed) said that evidence which elaborated or supplemented an agreed statement did not “contradict or qualify” it. This observation must be kept in mind in considering Ms Amede’s evidence.

Ms Amede’s Evidence

12 Exhibit 2, the letter dated 27 March 2014, states that:

(1) both Lamede Group and its business, Lamede Accounting Services, have, “ceased to trade as at 1 December 2013”;

(2) Ms Amede is, “no longer active in the field of accounting as at 1 December 2013”;

(3) Ms Amede has suffered a loss of reputation and, “cannot continue to work in my profession”;

(4) Ms Amede regrets that she contravened the TASA but says her actions were not wilful;

(5) Ms Amede, at the time of the contraventions, ran, “a small accounting practice that provided jobs for eight local residents”; and

(6) Ms Amede is currently unemployed, has no income, and is supported by her family.

13 Concerning those paragraphs, the Board, in relation to:

paragraphs (1) and (2), did not seek to prove the contrary, but made submissions;

paragraph (3), did not seek to prove the contrary, but made submissions concerning its weight;

paragraph (4), submitted that, in relation to wilfulness, it was inconsistent with the statement of agreed facts such that Ms Amede required the Court’s leave to withdraw from such admissions; and

paragraph (6), submitted that it may seek to call evidence and to cross-examine.

14 The Board made no comments concerning para (5).

15 In cross-examination Ms Amede said that she was familiar with a website called “LinkedIn”, an internet-based system which allows professional persons to exchange information about work that they do. She has a LinkedIn profile. It was set up several years ago. She does not maintain it. It is not clear whether she has ever been involved in maintaining it, or whether such maintenance was performed for her by another person. She knows that her profile is still available on LinkedIn (ts 8, ll 20 - 34). Ms Amede was shown a copy of that profile (ts 8, ll 42). However it was not tendered in evidence. In it, Ms Amede is described as “the Principal at Australian R&D Funds and Grants Services Pty Ltd” (“Australian R&D”). She was directed to a paragraph in the middle of the first page, under the word “summary”. It states:

Lorraine has been involved with financial and contract management for 25 years and has run her own successful accounting practice for over 10 years. Having been the initiator and facilitator in obtaining R&D funds and grants for clients the accounting company has experienced exponential growth which in turn has lead expansion and to moving totally into the field of grants and funds. With a team of experts in R&D and other funds and grants acquisitions the new company is totally focussed on B2B with all levels of business.

16 Ms Amede agreed (ts 9, ll 4 - 29) that this paragraph describes the way in which her business moved from the area of accounting to that of grants and funds. She had a team of experts in research and development. The new business was focussed on “B2B with all levels of business”. “B2B” means “business to business”. It said that the company (Australian R&D), “can help you with”, a number of listed items namely:

capital injections;

funding for employment growth;

RTO & training investments; and

inventions, patents.

17 A 1300 telephone number is shown. Ms Amede said that the number was no longer connected (ts 9, ll 31 - 32). The profile states that Ms Amede has been the principal of the company (Australian R&D) from January 2014 to the present day. Ms Amede said that she is the principal by virtue of the fact that she is the sole director. She said (ts 9, ll 36 – 38 and ll 40-44):

What has happened is in October last year I went overseas to endeavour to bring back funds for Small – SMX. When I returned, the company had been totally decimated.

…

I had left it in the hands of people I thought were skilled enough to run it, however, due to some malicious intent, which is currently under investigation, and I’ve made my reports to the TPB, and to the police regarding the matters that concern that, that company no longer trades, or exists.

18 Australian R&D is, “still open, … but we have a number of issues, a number of liabilities that still need to be met, but we have no trading, and no clients. It has totally ceased” (ts 10, ll 11 - 13).

19 It was put to Ms Amede that she was, at least through her LinkedIn profile, continuing to advertise for business in the research and development field through Australian R&D Funds and Grants Services Pty Ltd. Ms Amede responded: “Currently – I didn’t advertise intentionally. I didn’t realise that it was still sitting there” (ts 10, ll 38 -39).

20 Ms Amede denied that she would provide tax/accounting services if someone approached her, seeking such services (ts 11, ll 6 - 11). She maintained that she had no intention of advertising for business, and that she had not realized that she was continuing to do so (ts 11, ll 19 - 22). Ms Amede was asked “why not?”. She replied (ts 11, ll 13 - 17):

There are a lot of complicated issues that are – surround this particular company, and to continue to trade in that company would be detrimental to myself, and my company, itself. So we have ceased trading as at the end of November, and I am only in the capacity of trying to continue to meet the requirements, or the expectations of my previous clients.

21 Ms Amede agreed that “notwithstanding” the above, she was unemployed and had no income (ts 11, ll 24 - 25).

22 It was put to Ms Amede that she knew that she was providing tax agent services beyond the scope of work involved in being a BAS agent. Ms Amede said (ts 11, ll 40 - 47):

The services came about … as a result of clients who had been with me for some time. The clients did not wish to be given to anyone else. They insisted that I continue to deal with them. As a result, I made it very clear to each and every client that I was not a tax agent, and that for me to continue they would have to give me authority. As a result of that I produced an authority letter that each client, having been informed, would either choose to go to another accounting practice for the service, or if they insisted that they stay with me, they had to sign that document, which is what I have produced evidence of that.

23 It was put to Ms Amede that she knew that she was providing tax agent services to the people whose names appear in the schedules to the statement of agreed facts. She replied (ts 12, ll 3 - 4):

Yes, but I made – I took all action to make sure that they were aware I was not a tax agent.

24 It was then put to her that in the statement of agreed facts, she had admitted that she knew that she was supplying tax agent services. She replied (ts 12, ll 6 - 10):

My solicitors last year were dismissed because I was not given the proper support. They didn’t tell me what they were submitting. I did not see it [para 56], and they also went out of – or they’ve changed – or they’ve closed their business.

25 It was put to Ms Amede that she had sought to arrange for a registered tax agent to file tax returns prepared by her. Ms Amede replied (ts 12, ll 15 - 19):

We did ask that – we tried to get a tax agent on board, and the first tax agent, who’s name I don’t have in front of me, advised us that it was common practice for accountants to have tax agents to submit it providing that they reviewed it. We took that as being acceptable, from a tax agent, who advised us of this, and we didn’t think to question it.

26 Ms Amede entered into such an agreement with a Mr Beeraka (ts 12, ll 21 - 22). The agreement lasted just over a month (ts 12, ll 24 - 28). Ms Amede said that she had previously made a similar arrangement with another tax agent (ts 12, ll 30 - 32).

27 Ms Amede said that at no time were any of her actions taken wilfully (ts 11, ll 27 - 28). It was put to Ms Amede that although she knew that the law required that she be registered, she continued to perform tax agent services, even during the period when she did not have an agreement in place with a registered tax agent. Ms Amede replied, “I’m not denying that” (ts 12, ll 34 - 39). It was put to her that, “to that extent”, she acted wilfully, in the sense that she knew that she was doing the wrong thing. Ms Amede replied, “I believed I was trying to do the right thing, but that doesn’t make a difference” (ts 12, ll 41 - 43).

DEPARTURE FROM THE STATEMENT OF AGREED FACTS

28 Counsel for the Board submitted that Ms Amede could only depart from the statement of agreed facts if I granted leave pursuant to s 191(2) of the Evidence Act. Paragraph 13 states:

13. Ms Amede knew and intended that the effect of providing the income tax services was to:

13.1. ascertain the taxpayer’s liabilities, obligations or entitlements that arise, or could arise, under a taxation law;

13.2. advise the taxpayer about liabilities, obligations or entitlements that arise, or could or arise, under a taxation law; and/or

13.3. represent the taxpayer in their dealings with the Commissioner.

29 Ms Amede agreed with the contents of that paragraph but said (ts 13, ll 38 - 40):

However, I did have written authority from my clients to prepare that. All my clients were fully informed that I was not a tax agent.

That statement does not “contradict or qualify” para 13. It rather offers an explanation which may go in mitigation. I doubt whether it is worthy of much weight. After all, the legislation is designed to protect clients.

30 Paragraphs 58-60 state:

58. At all material times, Ms Amede knew that persons and companies who wished to lawfully provide tax agent services for a fee or other reward were required to be registered with the Tax Practitioners Board.

59. At all material times, Ms Amede knew that the Tax Practitioners Board was also the agency responsible for assessing whether persons and companies were suitable to be registered as a tax agent, and that it would base that assessment on criteria relating to, amongst other things, qualifications, experience and fitness and propriety.

60. At all material times, Ms Amede knew that the Tax Practitioners Board had never assessed her or Lamede Group as suitable for registration as tax agents.

31 Ms Amede did not wish to depart from those paragraphs. However, she said (ts 14, ll 15 - 20):

… I applied – originally I did not wish to be a tax agent. I wasn’t – my model of business wasn’t going that way. However, due to the number of clients that kept coming to us, I felt that I had to do it. … We withdrew that tax application originally, because I didn’t – I still had second thoughts. At the time, I also had suffered a major diabetic event.

This statement does not “contradict or qualify” paras 58 - 60. In any event, it is again a plea in mitigation.

32 Paragraph 70 states:

Except in one case, Lamede Group did not inform its clients whose ITRs were lodged through Mr Beeraka’s firm that their ITRs were to be lodged by Mr Beeraka’s firm.

33 Ms Amede accepted that proposition but said (ts 14, ll 31 - 34):

Mr Beeraka actually came to my home office and had a look at what practices were in place, and he had offered to help guide us to bring it to the point where it would be acceptable to the Tax Practitioners Board. And that was the agreement that we had.

This statement does not “contradict or qualify” para 70. Again, Ms Amede’s statement goes only to mitigation.

LIABILITY FOR THE CONTRAVENTIONS

34 The statement of agreed facts provides the framework within which the Board’s case must be considered. I am presently concerned with two categories of alleged breach, namely:

fifty-one occasions between about July 2010 and August 2013, on which either Lamede Group or Ms Amede provided tax agent services for a fee; and

five occasions, between January 2011 and October 2013, on which Lamede Group advertised the availability of tax agent services.

35 There was a further allegation that Ms Amede had contravened s 50-15 of TASA. In the course of the hearing, the Board indicated that it would not press that count. I need not say any more about that alleged contravention, or about Ms Amede’s evidence concerning it.

36 Concerning the first category (the “tax agent contraventions”), Ms Amede has admitted seven contraventions in 2010 and 2011. See Sch A to the statement of agreed facts. Lamede Group has admitted 44 contraventions between 2011 and 2013. See Sch B to the statement of agreed facts. The second category, (the “advertising contraventions”) are particularized in paras 22 – 55 of the statement of agreed facts. The advertisements appeared on various websites namely, “Service Seeking”, “Oneflare”, “Lamede.com.au”, and the internet noticeboard “Nnub”. In the case of the “Service Seeking” website, the relevant material was displayed for (at least) the period from about 4 January 2011 until about 13 September 2013. On the “Oneflare” website the material was displayed from about 30 October 2012 until 17 October 2013. On the “Lamede.com.au” website the relevant material was displayed from about 26 September 2012 until about 6 September 2013. The internet noticeboard “Nnub” displayed material for a period of about one month from 1 July 2011 and different material for about one month from about 10 August 2012.

37 The facts alleged in the statement of claim are admitted in paras 1 and 2 of the statement of agreed facts. In paras 2 – 5 of the statement of claim the trading history of the respondents is set out. It seems that from 1 November 2004 until “at least about August 2013” Ms Amede traded under a registered business name, “Lamede Accounting Services”. From about May 2006 until at least August 2013 she was the registered holder of that name. From about 4 January 2011 until at least August 2013, Lamede Group also held that name, together with another business name. From 4 January 2011 until August 2013 Ms Amede was the sole director, manager and shareholder of Lamede Group. From 1 March 2010 until 23 December 2013 she was registered as an individual BAS agent.

38 The effect of the statement of agreed facts is that at para 1 Lamede Group admits the tax agent contraventions particularized in Sch B. They all occurred between April 2011 and June 2013. Lamede Group also admits the alleged advertising contraventions. At para 2 of the statement of agreed facts, Ms Amede admits the alleged tax agent contraventions particularized in Sch A, all of which occurred between July 2010 and January 2011. The reference to s 50-15 in para 2 may be ignored.

39 In the statement of claim, the Board does not consistently distinguish between Lamede Group and Ms Amede, partly because it pleads that Lamede Accounting Services took many of the steps involved in the alleged contraventions. “Lamede Accounting Services” is a “trading name”, not a legal entity. It seems that Ms Amede held the name from May 2006 until August 2013, and Lamede Group held it from January 2011 until August 2013. Perhaps both held the name during the overlap period. Alternatively, the register may not have been appropriately amended. The matter is further complicated by the fact that Lamede Group generally acted through Ms Amede. The Board pleads that she took many of the steps which constituted the contraventions, but the pleading is ambiguous as to whether she did so on her own behalf, on behalf of Lamede Group or both. At para 5 of the agreed statement of facts, it seems to be accepted that from 4 January 2011, Lamede Group and not Ms Amede, was carrying on the business.

40 There is nothing surprising or suspicious about these matters. Sole traders frequently identify the advantages of incorporating and decide to take advantage of them. Not infrequently, confusion and inconsistency follow, at least from a legal point of view. However, in these proceedings I must distinguish between Ms Amede’s conduct and consequential liability and the conduct of Lamede Group and the consequences thereof. There are, of course, circumstances in which both principal and agent may be liable for acts performed by the agent. For present purposes much may depend upon the definition of the proscribed conduct. Where a corporation incurs liability under a statute, the statute often imposes liability on the person whose conduct brought about such contravention. Liability is often extended to include persons who are “knowingly concerned” in the contravention. Other formulations are also used to achieve the same result. There is no such provision in TASA.

41 In the present case Lamede Group accepts responsibility for the tax agent contraventions which occurred after it acquired the “trading name”, and Ms Amede accepts responsibility for the tax agent contraventions which occurred prior to that time. Further, Lamede Group accepts responsibility for the advertising contraventions. The Board apparently accepts that this approach should be taken with respect to the imposition of pecuniary penalties and with respect to declaratory relief. It seeks pecuniary penalties against each of them for the contraventions which each has respectively admitted. Concerning Ms Amede, it seeks a declaration concerning the seven tax agent contraventions. As against Lamede Group, it seeks declarations concerning both the tax agent contraventions and the advertising contraventions. The advertising contraventions occurred between January 2011 and October 2013, after Ms Amede had ceased to carry on the business, and Lamede Group had commenced to do so.

42 However the Board also seeks injunctive relief against Lamede Group and Ms Amede concerning future conduct which may contravene either s 50-5(1) or s 50-10(1). In seeking injunctive relief against Ms Amede in connection with possible future advertising contraventions, the Board departs from the approach otherwise taken to those contraventions. Although Ms Amede has admitted the conduct upon which the Board relies in its case concerning the advertising contraventions against Lamede Group, she has not admitted that she contravened s 50-10(1).

43 Two other considerations cause further complications. Section 50-10(1) provides that “you” will contravene the section “if you advertise that you will provide a tax agent service”. Although the originating application and the statement of claim seem to raise alternative cases, namely that the advertised services were to be provided by both Lamede Group and Ms Amede, or Lamede Group or Ms Amede, the statement of agreed facts indicates that Ms Amede “intended that services were advertised and offered to be provided by Lamede Group …”. See paras 24, 32, 38, 45 and 51. Thus the case has been conducted on the basis that the advertisements related to the provision of tax agent services by Lamede Group, not by Ms Amede. Although Lamede Group may be liable for her placement of the advertisements, she did not place advertisements concerning the supply of such services by her. In the absence of any provision extending liability to persons “knowingly concerned” (or, otherwise involved in) contraventions, I cannot see that she has, herself, contravened s 50-10(1), although Lamede Group has done so. Whilst s 90-1(2) of TASA and s 4-5 of the Income Tax Assessment Act 1997 (Cth) extend the meaning of the word “you” to include a corporation, they do not dispense with the requirement in s 50-10(1) that the advertisement be inserted by the person whose services are being advertised.

44 The second difficulty is that injunctive relief is sought pursuant to s 70-5 of TASA. That section provides:

Injunction to restrain or require certain conduct

(1) If, on the application of the Board, the Federal Court is satisfied that you have engaged, or are proposing to engage, in conduct that would constitute a contravention of a civil penalty provision, the Federal Court may grant an injunction:

(a) restraining you from engaging in the conduct; or

(b) if in the Federal Court’s opinion it is desirable to do so, requiring you to do something.

(2) Before deciding the application, the Federal Court may grant an interim injunction:

(a) restraining you from engaging in conduct; or

(b) requiring you to do something.

45 For reasons which I have given, I am not satisfied that Ms Amede has contravened s 50-10(1), although she was apparently party to Lamede Group’s contraventions. No attempt has been made to attribute liability to her on any such basis. Further TASA seems not to provide for such imposition of liability.

46 Lamede Group is virtually defunct. Ms Amede controls it. She is diabetic and claims to have experienced at least one “major diabetic event”. She is presently unemployed and supported by her family. It seems most unlikely to me that either she or Lamede Group will in the future, engage in any business, so that the opportunities for further contraventions are likely to be minimal. I am not satisfied that either Lamede Group or Ms Amede proposes to engage in any future contravention of s 50-5(1) or s 50-10(1). It follows that injunctive relief may only be given against either respondent on the basis that it or she has previously contravened a pecuniary penalty provision of TASA. Any injunction should relate only to future conduct which is similar in kind to that constituting the relevant prior contravention.

Pecuniary Penalties

47 The maximum penalty for a breach of s 50-5(1) is 250 penalty units for an individual person and 1,250 penalty units for a corporation. The maximum penalty for each advertising offence is 50 penalty units for an individual person and 250 penalty units for a corporation. A “penalty unit” is defined in s 4AA of the Crimes Act 1914 (Cth). It has a dollar value which is varied from time to time. With effect from 28 December 2012 the value of the penalty unit increased from $110 to $170: see Crimes Legislation Amendment (Serious Drugs, Identity Crime and Other Measures) Act 2012 (Cth) Sch 3, Pt 2, item 9(1). Most of Lamede Group’s contraventions, and all of Ms Amede’s contraventions, occurred before 28 December 2012.

48 Regulatory systems of this kind are generally designed to protect persons who seek expert assistance. The purpose is to ensure that only properly qualified people offer the assistance in question. The penalty regime is designed to deter potential offenders. The imposition of a penalty also marks the community’s displeasure at a breach of its law.

49 These offences occurred over an extended period of time. There was always the risk of adverse consequences to clients. It seems that some clients suffered actual loss as the result of inadequacy in the services provided. The Board submits that, “[t]he penalty sufficient to serve as specific and general deterrence for conduct of this magnitude must significantly exceed these amounts, by some multiple”. See para 49 of the Board’s submissions.

50 The unlawful provision of tax agent’s services is punished much more heavily than is advertising the availability of such services. Opinions may differ as to which of those offences is the more serious. Concerning the advertising contraventions, Ms Amede suggests that she did not necessarily have control of such advertising. She also asserts a degree of inadvertence. However Ms Amede’s evidence is really too imprecise to weigh heavily in the balance. There can be no doubt that the advertising was designed to advance Lamede Group’s activities, or that it was aware of such advertising.

51 In fixing penalties, the starting point is generally the statutory maximum and any statutory minimum. However a dominant feature of this case is the large number of offences. The amounts received for the provision of tax agent’s services were relatively small, about $1,000 in Ms Amede’s case, and about $7,000 in the case of Lamede Group. Schedules A and B to the statement of agreed facts show that the amount received for each transaction was very small, in some cases less than $100, in some cases between $100 and $200 and in others, a little more. Where misconduct is for financial gain, the penalty must be sufficiently high that the risk of its incurrence will not be accepted as a mere cost of doing business. Ms Amede’s contraventions occurred in 2010 and early 2011. Lamede Group’s tax agent contraventions were committed between April 2011 and mid-2013, a period of a little over two years. In the case of a corporation, the relatively high maximum penalty of 1,250 penalty units (at $110 or $170 per unit) produces a maximum penalty which is well beyond any figure which might reasonably be imposed in this case. Each of the contraventions is at the lower end of any scale of seriousness. However the conduct extended over a period of more than two years. This is a significant circumstance of aggravation. There has, however, been a degree of cooperation which may, or may not reflect remorse. I find myself unpersuaded by Ms Amede’s expressions of regret. However I accord her and Lamede Group some consideration for cooperation.

COMPARABLE PENALTIES

52 In Tax Practitioners Board v Dedic [2014] FCA 511, Davies J imposed a pecuniary penalty of $43,000 in respect of 86 contraventions of s 50-5(1) of TASA. The contravention occurred between July 2010 and October 2012 and involved about 33 clients. The amount per penalty unit was, at the time, $110. Ms Dedic admitted that she had prepared and lodged the 86 tax returns but in 31 cases, denied that she had charged a fee. Davies J found that Ms Dedic charged a fee for all 86 contraventions. The overall financial benefit was approximately $17,370. Her Honour’s reasons as to liability may be found at [2014] FCA 307. The matter was resolved on the basis of a statement of agreed facts.

53 In Tax Practitioners Board v Hinckfuss [2013] FCA 1168, I imposed a total pecuniary penalty of $32,000 in respect of 25 contraventions of s 50-5(1) and seven contraventions of s 50-10 of TASA, comprising a penalty of $1,200 for each s 50-5(1) contravention and $1,000 for each contravention of s 50-10(1). At the time the amount per penalty unit was $110. The contraventions were admitted. A statement of agreed facts was filed. The conduct occurred between July 2010 and August 2012. Mr Hinckfuss received $12,475.31 in fees from the contraventions. He had distributed leaflets describing himself as a “tax guru”. Many of his clients were persons, “unsophisticated in financial and taxation matters”. Despite his apparently altruistic motives, there was a suggestion that he was “exploiting” the clients. Mr Hinckfuss had some accounting experience. He also had mental health issues. I summarized a number of early penalty outcomes and commented upon them. I have nothing further to say concerning those cases.

54 The following table compares the present case with the decisions in Hinckfuss and Dedic.

Matter | No. of s 50-5(1) offences | No. of s 50-10 offences | $ Amount derived | Period of time | $ Penalty s 50-5(1) | $ Penalty s 50-10 |

Hinckfuss | 25 | 2 | 12,475.31 | 2 years 1 month | 30,000 | 2,000 |

Dedic | 86 | - | 17,370 | 2 years 3 months | 43,000 | - |

Lamede | 44 | 5 | 7,000 | (s 50-5(1)) 2 years 6 months (s 50-10) 2 years 9 months | ||

Ms Amede | 7 | - | 1,000 | 6 months |

55 Dedic involved a much larger number of individual offences, whilst Hinckfuss involved fewer offences. Hinckfuss also included advertising offences. Dedic did not. Both Dedic and Hinckfuss involved substantially more in remuneration than was derived in the present case.

OTHER MATTERS

56 Ms Amede says that she is currently unemployed and has no income. She is supported by her family. She undoubtedly has limited capacity to meet any amount imposed by way of penalty. I do not fully accept the proposition that an offender’s capacity to pay any pecuniary penalty is of less importance than the need for a pecuniary penalty of appropriate deterrent value, if, by that proposition, it is meant that I should have no regard to the capacity of an offender to pay. Such an approach seems to assume that an unpaid penalty will nonetheless act as a deterrent. One suspects that if it became well-known that the courts were imposing penalties without any expectation that they would be paid, the deterrent effect of the penalty regime would be greatly undermined, as would be respect for court orders generally. Such an approach might also disadvantage an offender who genuinely seeks to pay the penalty as opposed to one who does not try, or intend to try. As I understand it, in imposing a fine in a criminal matter, the courts frequently take into account capacity to pay.

57 Paragraph 75.6 of the statement of agreed facts states that, probably due to the respondents’ conduct, some taxpayer’s affairs were audited and penalties imposed. Although this matter is relevant to penalty, the available information is not detailed. The Board also submits that I should give weight to the, “distress, embarrassment and loss of reputation”, suffered by those taxpayers. I shall do so.

58 Lamede Group’s contraventions were spread over numerous tax years and numerous clients, some of whom were provided with relevant services on more than one occasion. In some cases, services were provided to clients sharing common surnames. It is tempting to assume some sort of collective family engagement, and to treat those contraventions as comprising one course of conduct. However to proceed in that way would be to make assumptions without any evidentiary justification. In view of the repeated infringements over an extended period of time, I should consider imposing more severe penalties for the later offences than for the earlier offences.

59 With one exception, the Board submits that each tax agent contravention should be treated as a single course of conduct. The exception concerns the provision by Lamede Group, in April 2011, of tax agent services to Mr Kemp in connection with six tax years. These are items 8 - 13 in Sch B. I shall treat those contraventions as comprising one course of conduct.

60 I consider that Ms Amede’s contraventions should also be treated as one course of conduct. They occurred over a six month period, and all involved the 2010 tax year. As to the balance of the tax agent contraventions, I propose to deal with them as separate contraventions, but in groups as follows:

items 14 – 28, the contraventions having occurred between 1 July and 31 December 2011;

items 29 – 32, the contraventions having occurred between 1 January and 30 June 2012;

items 33 – 45, the contraventions having occurred between 1 July and 31 December 2012; and

items 46 – 51, the contraventions having occurred between December 2012 and 30 June 2013.

61 Such grouping will allow me to adjust the penalties to reflect the increasing seriousness of repeated contraventions. As to the advertising contraventions, for a short time, the “Service Seeking” advertisement was in place whilst the second “Nnub” advertisement was in place. This suggests that the two contraventions might appropriately be treated as part of one course of conduct. The similarities between the two “Nnub” advertisements might suggest that they also comprised one course of conduct. Although it may not be strictly correct in principle, I propose to deal with all three contraventions as comprising one course of conduct.

62 The Board submits that the Court should find that Lamede Group was “effectively the corporate alter ego of Ms Amede”. I am not sure where that approach might lead. The case has been resolved upon the basis of the admissions in the statement of agreed facts. In that statement, it is agreed that Ms Amede actually performed the acts relied upon in the case against Lamede Group, but there is no agreement that Ms Amede was, in the relevant sense, knowingly concerned in, or otherwise party to its contraventions. There is no suggestion that Ms Amede accepts legal liability for Lamede Group’s conduct, although such liability was asserted in the originating application. I cannot impose a penalty upon Ms Amede for any of Lamede Group’s contraventions. Nor may I increase the penalties imposed upon her for her own contraventions in order to take account of her involvement in Lamede Group’s conduct. I might, however, have taken account of any loss suffered by Ms Amede as the result of the penalties imposed on Lamede Group. This consideration is of no great importance, given that Lamede Group seems to have no money. In any event, Ms Amede has caused her own loss.

PENALTIES TO BE IMPOSED

63 Ms Amede’s contraventions were significantly fewer than was the case in each of Dedic or Hinckfuss, and were spread over a relatively short period of time. For each contravention, the maximum penalty is 250 penalty units at $110 per unit. Ms Amede derived very little benefit from her conduct. I have already indicated that I propose to treat these offences as comprising one course of conduct. With respect to item 1 in Sch A, I impose a penalty of $1,000. With respect to each of items 2 – 7, I impose a penalty of $500, a total of $4,000. I must consider the appropriateness of the total penalty, having regard to the overall extent of the misconduct, and make any adjustment necessary in order to ensure that the overall penalty is not too harsh. I see no reason for further adjustment.

64 In respect of all of these contraventions, the Board submitted that an appropriate penalty for Ms Amede was $9,100. It must be kept in mind that the total penalty relates to seven contraventions over about six months, yielding about $1,000. Her poor financial position must also be taken into consideration.

65 In the case of Lamede Group, the maximum penalty for items 8 – 46, is 1,250 penalty units at $110 per unit. For items 47 – 51 the maximum penalty is 1,250 penalty units at $170 per unit. Item 46 involves conduct which commenced prior to the increase in penalty and continued after such increase. I shall give Lamede Group the benefit of the doubt and impose a penalty based on the lower rate.

66 The purpose to be served by the distinction between the penalty for a natural person and that for a corporation is not entirely clear. One suspects that it has much to do with perceptions as to likely capacity to pay. However it may also be designed to deter the abuse of limited liability which generally attaches to commercial corporate undertakings. I propose to fix the penalties to be imposed on Lamede Group before making any adjustment to reflect the overall extent of the misconduct. Hence the following proposed penalties are, in that sense, provisional.

67 As I have said, I propose to treat items 8 – 13 as comprising one course of conduct. I would impose a penalty of $2,000 with respect to item 8 and $500 with respect to each of items 9 - 13. As to each of items 14 – 28, I would impose a penalty of $2,000. As to each of items 29 – 32, I would impose a penalty of $2,250. As to each of items 33 – 46, I would impose a penalty of $2,500. The increasing levels of penalty reflect the increasing seriousness of the misconduct as a result of its repetition. Items 47 – 51 all occurred after the increase in maximum penalty. In respect of each I would impose a penalty of $2,750.

68 As to the advertising contraventions, the maximum penalty for a body corporate is 250 penalty units. The “Service Seeking” advertisement was on display from 28 September 2012 until 6 September 2013. The first “Nnub” advertisement was on display from 1 July 2011, for about a month. The second “Nnub” advertisement was on display from 10 August 2012, for about one month. The “Oneflare” advertisement was displayed from about 30 October 2012 until 17 October 2013. The “Lamede” advertisement was displayed from about 26 September 2012 until about 6 September 2013. As can be seen, the “Service Seeking”, “Oneflare” and “Lamede” advertisements were on display before and after the increase in penalty. Had the conduct before and after the increase been treated separately in the application, I would have imposed higher penalties for the later contraventions in order to reflect the increase in the penalty rate. Given that such conduct has, in each case, been treated as one course of conduct, I propose to adopt the lower rate of $110.

69 The “Service Seeking” advertisement was on display for much longer than the other advertisements. However it was also the first of the contraventions. I would impose a penalty of $2,000. In light of the difference in maximum penalties provided for the two categories of misconduct, this may seem disproportionate as compared to the penalties imposed in connection with the tax agent contraventions. However, the length of time for which the advertisement was displayed is a seriously aggravating feature. With respect to each of the “Oneflare” and Lamede advertisements, I would impose a penalty of $1,500. As I have said, I propose to treat the two “Nnub” advertisements as comprising, with the “Service Seeking” advertisement, one course of conduct. I would impose, in respect of each, a penalty of $500.

70 For Lamede Group, the proposed penalties would be:

Items 8 – 13 | $4,500 |

Items 14 – 28 | $30,000 |

Items 29 – 32 | $9,000 |

Items 33 – 46 | $35,000 |

Items 47 – 51 | $13,750 |

Advertising contraventions | $6,000 |

Total | $98,250.00 |

71 I should again consider the appropriateness of the overall totality of the penalties as against the overall totality of misconduct. The total amount is substantially higher than the total imposed in both Dedic and Hinckfuss. It cannot be seriously suggested that the level of misconduct was as great as that in Dedic, although it was significantly more serious than that in Hinckfuss. There is also the smaller amounts derived by Lamede Group from the misconduct. Of course, the real reason for the disparity in penalty is the higher penalty for corporate offenders. Nonetheless, I consider that the disparity is such as to justify some reduction in the overall total. In the case of a small company, the difference between corporate and individual trading should not be taken too far. I shall reduce the proposed penalties to the following amounts:

for item 8, $1,500 and for each of items 9 – 13, $250, a total of $2,750;

for items 14 – 28, $1,500 for each item, a total of $22,500;

for items 29 – 32, $1,750 for each item, a total of $7,000;

for items 33 – 46, $2,000 for each item, a total of $28,000; and

for items 47 – 51, $2,250 for each item, a total of $11,250.

I do not intend to adjust the penalties for the advertising contraventions.

72 In summary, the penalties are:

Items 8 – 13 | $2,750 |

Items 14 – 28 | $22,500 |

Items 29 – 32 | $7,000 |

Items 33 – 46 | $28,000 |

Items 47 – 51 | $11,250 |

Advertising contraventions | $6,000 |

Total | $77,500.00 |

The Board submitted that an appropriate penalty for Lamede Group was $100,000. I suspect that the Board had not given enough weight to the overall extent of the relevant misconduct.

Other relief

73 The Board also seeks declarations concerning the respondents’ contraventions of TASA and injunctive relief. However the proposed declarations focus on the receipt of a fee. As I explained in the course of argument, this focus may confuse a casual reader. I am prepared to grant declaratory relief, but not in the form proposed by the Board.

74 As to injunctive relief, I have already discussed some of the relevant issues. I am satisfied that both respondents engaged in conduct in contravention of s 50-5(1) and that Lamede Group engaged in conduct in contravention of s 50-10(1). Section 70-5 gives little clear indication of the purpose to be served by an injunction granted pursuant to that section. Hence it is difficult to identify the considerations to be taken into account in deciding whether to grant injunctive relief. In general, injunctions are issued in order to compel or restrain conduct. See Meagher, Gummow & Lehane’s Equity Doctrines and Remedies (4th ed) at [21-005]. However statutes sometimes confer power to issue injunctions, apparently for the purpose of supplementing the Court’s power to grant that form of relief pursuant to the general law. See, for example, s 232(4) of the Australian Consumer Law and the discussion of statutory injunctions in JD Heydon, Competition and Consumer Law [140.2170] et seq. It is not infrequently submitted, and accepted, that the extended nature of statutory injunctive relief permits the use of that remedy for purposes other than to compel or restrain particular conduct, and that injunctive relief may be granted simply to mark the Court’s view of the gravity of the relevant misconduct. See Heydon at [140.2200]. I do not quite understand how an injunction can assist in achieving that purpose where the court also imposes a pecuniary penalty and/or makes a declaration.

75 In any event, although s 70-5 may create a distinct species of statutory injunction, Parliament has not extended the circumstances in which such relief may be available in the way that it has done in s 232(4) of the Australian Consumer Law. Section 70-5 offers the possibility of injunctive relief where there has been a previous contravention, even if the Court is not satisfied that the person is proposing to engage in any future contravention. Nonetheless, even in that case, the likelihood of future contraventions must be a significant consideration in the exercise of the discretion. As I have observed, an injunction is designed to compel or restrain conduct. Subparagraphs 70-5(1)(a) and (b) reflect that purpose. Nothing in TASA suggests that Parliament intended that injunctive relief, under the guise of restraining or compelling particular conduct, should be used to mark the Court’s views as to the seriousness of past or proposed conduct, or for any other purpose apart from restraining or compelling identified conduct. I consider that the likelihood of such conduct by either respondent is low. I decline to grant injunctive relief. I do not see that such relief would add anything to the effect of the declaration which I propose to make, and the pecuniary penalties which I propose to impose.

Costs

76 The Board seeks an order pursuant to r 40.02(b) of the Rules that it receive its costs of and incidental to these proceedings on a party and party basis, to be fixed in the sum of $2,000. In support, counsel for the Board read the affidavit of Alexander John Gilmour Tate filed on 24 March 2014. Mr Tate deposes that the Board’s taxable costs in this matter amount to about $16,145 and that the fixed sum sought:

…will result in savings of both costs and time by removing the need for taxation in this proceeding and that the proposed order is justified on the basis that it is substantially less than would be recovered by the [Board] if the matter proceeded to taxation.

77 I order that the respondents pay the applicant’s costs fixed in the amount of $2,000.

78 The parties are to bring in appropriate draft orders, including any timetable for payment of the penalties. I grant liberty to apply.

I certify that the preceding seventy-eight (78) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Dowsett. |

Associate:

Dated: 10 February 2016