FEDERAL COURT OF AUSTRALIA

GE Commercial Australasia Pty Ltd v Tinkler, in the matter of Nathan Tinkler [2016] FCA 55

Table of Corrections | |

In the Appearances on the cover page in the field Solicitor for a supporting creditor the words “of Merewether & Co as agents for SR Law” have been added. |

ORDERS

IN THE MATTER OF NATHAN TINKLER

GE COMMERCIAL AUSTRALASIA PTY LTD ACN 096 876 292 Applicant | |

AND: | Respondent |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. A sequestration order be made against the estate of Nathan Tinkler.

2. All proceedings under the sequestration order be stayed for a period of 21 days.

3. The applicant’s costs be paid from the estate of the respondent in accordance with the Bankruptcy Act 1966 (Cth).

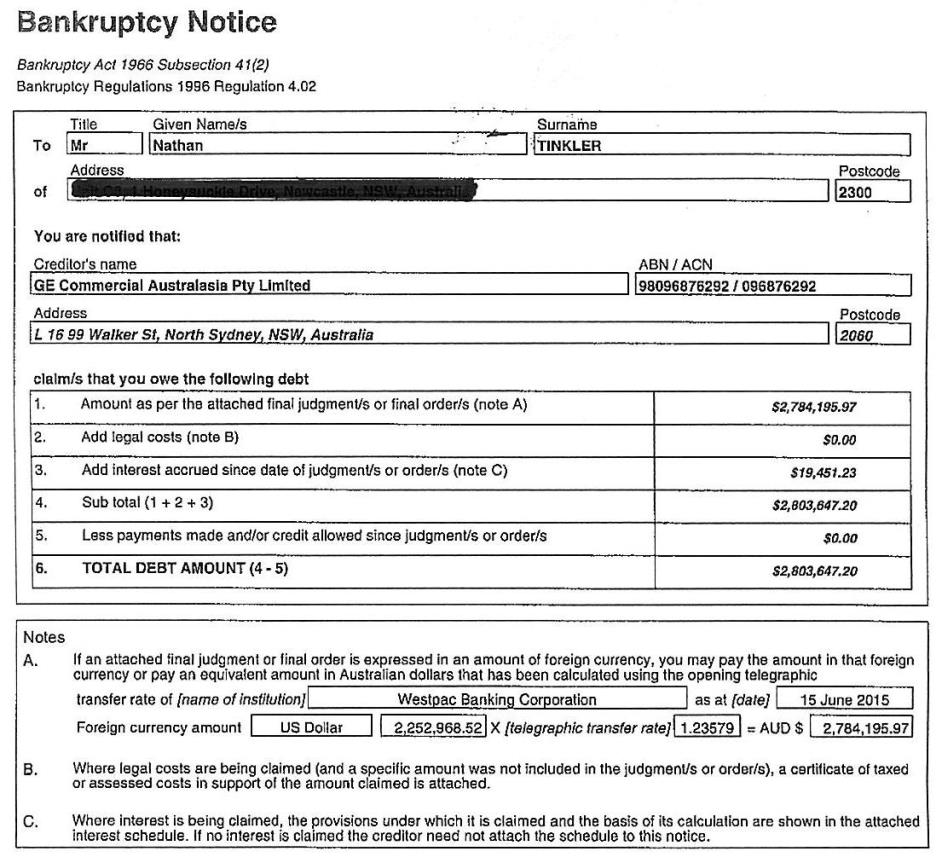

THE COURT NOTES THAT:

4. The date of act of bankruptcy is 16 July 2015.

5. A consent to act as trustee has been signed by John Melluish.

6. A copy of this order must be provided to the Official Receiver in Sydney within 2 days pursuant to reg 4.05 of the Bankruptcy Regulations 1996 (Cth).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GLEESON J:

1 The applicant (“creditor” or “GE”) petitions for a sequestration order under s 43 of the Bankruptcy Act 1996 (“Act”) against the estate of the respondent debtor (“Mr Tinkler”).

2 The creditor’s petition is dated 21 July 2015.

3 By amended notice stating grounds of opposition to the creditor’s petition, dated 11 November 2015, Mr Tinkler raised the following two grounds of opposition to the petition:

(1) he is solvent;

(2) he did not commit an act of bankruptcy, as the creditor’s bankruptcy notice did not comply with the requirements set out in reg 4.04 of the Bankruptcy Regulations 1966 (Cth) (“Regulations”) and was invalid.

4 An act of bankruptcy by the debtor is a precondition to the Court’s power to make a sequestration order against the estate of the debtor: s 43(1)(a) of the Act.

5 A bankruptcy notice is a nullity if it fails to meet a requirement made essential by the Act: Kleinwort Benson Australia Ltd v Crowl [1988] HCA 34; (1988) 165 CLR 71 at 79; see also The Australian Steel Company (Operations) Pty Ltd v Lewis [2000] FCA 1915; (2000) 109 FCR 33 at [22] to [25]. A debtor may dispute the validity of the bankruptcy notice on the hearing of the creditor’s petition: Re Pollard; ex parte Lensing Management Co Pty Limited (1991) 33 FCR 284 (“Re Pollard”). Where the defect in the bankruptcy notice is other than a formal one, the notice itself is defective and failure to comply with it does not constitute an act of bankruptcy: Re Pollard at 286.

6 Regulation 4.04 provides:

Judgment or order in foreign currency

(1) This regulation applies to a bankruptcy notice if the judgment or order lodged under subregulation 4.01(1) in relation to the notice is expressed in an amount of foreign currency (whether or not the judgment or order is also expressed in an amount of Australian currency).

(2) A bankruptcy notice to which this regulation applies must:

(a) contain a statement to the effect that payment of the amount of foreign currency expressed in the judgment or order may be paid in that foreign currency or by means of a specified amount of Australian currency that is stated to be equivalent to the amount of foreign currency; and

(b) set out:

(i) the applicable rate of exchange, being the rate worked out in accordance with subregulation (3); and

(ii) the conversion calculation; and

(iii) a statement that the conversion of the amount of foreign currency into Australian currency has been made in accordance with this regulation.

(3) For paragraph (2)(b), the conversion of an amount of foreign currency into an equivalent amount of Australian currency must be done in accordance with the telegraphic rate of exchange prevailing on the second day before the day when the application to which the conversion applies is lodged under subregulation 4.01(1).

7 Mr Tinkler’s case was that GE has not demonstrated that the rate in the bankruptcy notice is the “applicable rate of exchange, being the rate worked out in accordance with subregulation (3)” as required by subreg 4.04(2)(b)(i). In particular, Mr McDonald, counsel for Mr Tinkler, argued that GE has not demonstrated that the rate is the “telegraphic rate of exchange prevailing” on the relevant date because it has not demonstrated that the rate was the best rate available on that date for a telegraphic transfer of the amount of the judgment debt upon which the bankruptcy notice is founded, being US$2,252,968.52. Mr McDonald also argued that the rate in the bankruptcy notice was not the applicable rate because it is a rate that was available on 15 June 2015 and that date is not the second day before the day on which the application for the bankruptcy notice was lodged.

8 No evidence was adduced on behalf of Mr Tinkler that the rate in the bankruptcy notice is not the “telegraphic rate of exchange prevailing” on the relevant date.

9 It is not disputed that reg 4.04 applies to the bankruptcy notice in this case. The creditor accepted that, if the bankruptcy notice does not comply with reg 4.04, then the bankruptcy notice is defective and the creditor’s petition must be dismissed: cf Parianos v Lymlind Pty Ltd [1999] FCA 684; (1999) 93 FCR 191 (“Parianos”) at [19] and [31].

Solvency

10 By s 52(2)(a) of the Act, if the Court is satisfied by the debtor that he or she is able to pay his or her debts, it may dismiss the petition.

11 The evidence relied upon by Mr Tinkler did not support his contention as to solvency and Mr McDonald did not direct any submissions to that issue.

12 Accordingly, this ground of opposition fails.

Form of bankruptcy notice

13 The relevant portion of the bankruptcy notice is in the following form:

14 The form of the bankruptcy notice follows the form prescribed by reg 4.02 of the Regulations. I note that Note A requires the insertion of a rate by which the relevant foreign currency amount is multiplied to calculate an equivalent Australian dollar sum.

15 The judgment upon which the bankruptcy notice is based is a judgment of the Supreme Court of New South Wales dated 19 May 2015, and made by consent.

16 Mr McDonald did not dispute that the bankruptcy notice sets out both the conversion calculation required by subreg 4.04(2)(b)(ii) and the statement required by subreg 4.04.(2)(b)(iii). The conversion calculation is set out in the portion of the bankruptcy notice above. The required statement is set out in a letter attached to the bankruptcy notice.

17 There is no evidence to suggest that there is a readily ascertainable “telegraphic rate of exchange prevailing” (the language of subreg 4.04(3)) on any given date, in the sense that there is a rate published under this description.

18 Nor is there evidence to suggest that there is a readily ascertainable “opening telegraphic transfer rate” (the language of the prescribed form of the bankruptcy notice) of any institution by which a foreign currency amount may be multiplied to calculate an equivalent Australian dollar amount. That is, there is no evidence that any Australian institution publishes such rates (or any rates) under the description “opening telegraphic transfer rate”.

19 The evidence of Mr Tinkler’s solicitor, Mr Kam, might suggest that his attempts, in November 2015, to verify the rate in the bankruptcy notice as a rate complying with reg 4.04 were unsuccessful. According to the evidence, Mr Kam made inquiries of four major banking institutions (National Australia Bank (“NAB”), Westpac Banking Corporation (“Westpac”), Commonwealth Bank of Australia (“CBA”) and Australia and New Zealand Banking Group Ltd (“ANZ”)). When he asked for a “foreign exchange rate in respect of a telegraphic transfer” on 15 June 2015, to convert United States (“US”) dollars to Australian dollars, Mr Kam was told that:

(a) NAB could not provide the rate for 15 June 2015;

(b) Westpac did not have a record of the rate for a transfer of US$2,252,968.52 on that date;

(c) CBA could not provide the rate “because that rate would have been calculated at that specific point in time for that specific amount” (being the amount of US$2,252,968.52);

(d) ANZ was “unable” to provide the historical version of the rate published on its website.

20 However, Mr Kam did not give evidence that he could not verify the rate in the bankruptcy notice as the inverse of a foreign exchange rate published by Westpac on 15 June 2015 as the rate generally available in respect of a telegraphic transfer involving a conversion from US dollars to Australian dollars.

Evidence that the rate in the bankruptcy notice is the “applicable rate of exchange”

21 Mr Clark, a solicitor acting for GE, gave evidence, which I accept, of the following facts:

(a) On 15 June 2015, Mr Clark accessed the “foreign exchange rates” feature on the website of Westpac and observed the rate displayed for the sale of United States (“US”) dollars to Westpac.

(b) On 17 June 2015, Mr Clark accessed the “FX historical rates search” feature on the website of Westpac to search for the foreign exchange rates applicable to US dollars on 15 June 2015. From the results of his search, Mr Clark understood that the telegraphic transfer rate at which Westpac was willing to buy US dollars in exchange for Australian dollars on 15 June 2015 was 0.8092 (“Rate”). Mr Clark recalled that the Rate was the same as the rate that he had observed on the “foreign exchange rates” feature of the website on 15 June 2015.

(c) Mr Clark calculated the inverse of the Rate. He rounded the inverse of the Rate to five decimal places, being 1.23579, because that was the maximum number of decimal places the “online form” (provided on the website of the Australian Financial Security Authority (“AFSA”)) allowed him to enter.

(d) Prior to making the application for the bankruptcy notice, Mr Clark did not contact Westpac to confirm the Rate or make any other enquiries about the historical rates. Nor did he make any enquiries of any other financial institution.

(e) On 17 June 2015, Mr Clark made an online application to AFSA for a bankruptcy notice. As part of that application, Mr Clark was required to supply the “telegraphic transfer rate”, which Mr Clark noted in the application to be 1.23579.

22 Mr Clark’s evidence included images of the webpages that he visited for the purposes of ascertaining the relevant rate.

23 The webpage that Mr Clark accessed on 15 June 2015 shows that Westpac provides a “Currency converter” which states that rates are “current” as at a specified date and time. To use the currency converter, it is necessary to identify that currency “I have”, the currency “I want” and the amount “I have” or the amount “I want”. It is also possible to check a box under the heading “I have it as” next to the words “Telegraphic transfer”.

24 On the same webpage, there is also a table headed “Foreign exchange rates”. Under the heading is a note that “All rates on this page are current as at” a date and time. The table is then divided into two sections under the headings “I want to buy” and “I want to sell”. Each section is divided into a further three columns headed “Global Currency Card”, Cash of Travellers Cheques” and “Telegraphic Transfers or Drafts”.

25 On the right hand side of the web page are the words “Transfers over $100,000? Call us for a rate”.

26 The webpage that Mr Clark accessed on 17 June 2015 is titled “Services Foreign exchange historical rates. FX historical rates search”. Under the heading “Important instructions” is the following note “Please note that rates displayed are for Westpac to Buy and Sell the specified currencies”.

27 When Mr Clark conducted his search on 17 June 2015, the Rate (of 0.8092) was described by Westpac as a “TT buy rate”. From the search, Mr Clark understood that it was the only “TT buy” rate published by Westpac on 15 June 2015.

28 From Mr Clark’s 7 December 2015 affidavit, it is apparent that the 17 June 2015 search produced other rates, particularly a “sell” rate. Mr Clark has regard to the note set out at paragraph 26 above to form the conclusion that the Rate, being a “TT buy rate” was the relevant rate.

Use of inverted rate

29 On Mr Tinkler’s behalf, it was not disputed that, if a “telegraphic rate of exchange” or a “telegraphic transfer” rate was published as a rate at which the relevant financial institution would buy or sell foreign currency in exchange for Australian dollars, it would be necessary to invert such a rate in order to obtain a rate by which a foreign currency amount could be multiplied to produce an equivalent Australian dollar amount.

Grounds on which Mr Tinkler disputes that GE complied with reg 4.04

30 The written submissions filed on behalf of Mr Tinkler identified the following alleged defects in the way in which the judgment was converted from US to Australian dollars:

(1) GE has not explained the use of the “buy” rate in determining the telegraphic rate of exchange, as opposed to the “sell” rate. The difference between the two rates is significant;

(2) GE has not explained why the inverted exchange rate was rounded to four decimal points or rounded up at all;

(3) GE did not obtain a quote for the telegraphic rate of exchange from any bank other than Westpac, with Mr Tinkler’s evidence being that the other prime banks offer to exchange US dollars to Australian dollars and, on any day, the rates offered by each will materially differ;

(4) GE used Westpac’s rate for the telegraphic rate of exchange which was expressed to be for amounts of less than $100,000, when the amount in the bankruptcy notice was over US$2,250,000, with Mr Tinkler’s evidence being that, as an example, Westpac would offer a materially different exchange rate on such an amount;

(5) As the application for the issue of the bankruptcy notice was not properly made until 18 or 19 June 2015, GE did not use the “telegraphic rate of exchange prevailing on the second day before the day” on which the creditor applied for the bankruptcy notice.

31 As to proposition (1), the conflicting evidence was not identified in the written submissions, or in the oral submissions made on behalf of Mr Tinkler. The allegedly significant difference between relevant buy and sell rates was not identified. In his affidavit evidence, Mr Clark explained that he used a rate published by Westpac on 15 June 2015 in a table headed “Foreign exchange rates” on a row labelled “USA Dollars “USD”, under the column “I want to sell” and the sub-column “Telegraphic Transfers” (subsequently described by Westpac as a “TT buy” rate as at 15 June 2015), rather than a “sell” rate, because he thought that the rate he selected was the rate at which Westpac would buy US dollars in exchange for Australian dollars. There is no evidence of the “sell” rate on 15 June 2015 or whether it was significantly different from the rate in the bankruptcy notice.

32 As to proposition (2), the exchange rate in the bankruptcy notice is a figure rounded to five decimal points. As noted at para 20(c) above, Mr Clark did give an explanation (in his 7 December 2015 affidavit sworn after Mr Shannon’s written submissions were filed) for why the inverted exchange rate used was rounded to five decimal points.

33 As to proposition (3), it is correct that GE did not obtain a quote for the telegraphic rate of exchange from any bank other than Westpac. There was evidence that Westpac, CBA and ANZ offer to exchange US dollars to Australian dollars. However, I do not accept that the evidence supports a conclusion that, on any given day, the rates offered by each will materially differ. Nor does it support a conclusion that the rates offered on 15 June 2015 materially differed from the rate in the bankruptcy notice. Mr Kam’s evidence demonstrates that the different banks published the following different rates on 19 and 20 November 2015 for a telegraphic transfer involving a conversion of US dollars to Australian dollars:

Published rates | ||

Date | Bank | Rate |

19.11.2015 | NAB | 0.7423 |

20.11.2015 | NAB | 0.7472 |

20.11.2016 | Westpac | 0.7472 |

20.11.2015 | CBA | 0.7523 |

20.11.2015 | ANZ | 0.7473 |

34 Further, on 19 and 20 November 2015, Mr Kam also obtained different (and more favourable rates) from two banks (Westpac and CBA) to exchange the amount of US$2,252,968.52 to Australian dollars. The other two banks declined to provide a rate apart from their respective published rates.

35 As to proposition (4), I accept that the evidence supports an inference that, as at June 2015, Westpac offered to provide a rate for transfers of currency amounts over $100,000 and that such a rate was likely to be more favourable than its published rate, being 0.8092.

36 The factual elements of proposition (5) are considered below.

Interpretation of reg 4.04

Legislative history and case law

37 The early legislative history of reg 4.04 is set out by Sackville J in Parianos at [24] and following. In brief, prior to 1985, the Act made no specific provision for the issue of bankruptcy notices founded on foreign currency judgments. The absence of such provisions caused difficulties for parties seeking to issue bankruptcy notices based on foreign currency judgments. These difficulties led to legislation dealing specifically with bankruptcy notices founded on such judgments: see House of Representatives Explanatory Memorandum, Statute Law (Miscellaneous Provisions) Bill (No.2) 1985 (Cth), p 8. In 1985, the Statute Law (Miscellaneous Provisions) Act (No. 2) 1985 (Cth) introduced ss (2A), (2B) and (2C) into s 41 of the Act:

(2A) Where the judgment debt or sum ordered to be paid in accordance with the judgment or order is expressed by the judgment or order as an amount in the currency of a foreign country (in this sub-section referred to as the ‘amount of foreign currency’), the bankruptcy notice shall state that payment is to be made in either -

(a) the amount of foreign currency; or

(b) a specified amount of Australian dollars, being an amount that is the equivalent in Australian dollars of the amount of foreign currency on the second business day before the day on which application was made for the issue of the bankruptcy notice.

(2B) The rate for ascertaining on a particular day for the purposes of paragraph (2A)(b) the equivalent in Australian dollars of an amount of foreign currency is the average of the rates at which Australian dollars may be bought in that foreign currency at -

(a) 11 o’clock in the morning; or

(b) if another time is prescribed for the purposes of this sub-section - that other time, on that day from 3 authorised foreign exchange dealers selected by the creditor who applied for the issue of the bankruptcy notice.

(2C) In this section:

‘authorised foreign exchange dealer’ means a person authorised by a general authority issued by the Reserve Bank of Australia under regulation 38A of the Banking (Foreign Exchange) Regulations to buy and sell foreign currency;

‘business day’, in relation to an application for the issue of a bankruptcy notice, means a day that is not a Saturday, a Sunday or a public holiday or bank holiday in the place where the application is made.

38 In Re Bond; Ex parte HongKongBank of Australia Limited (1992) 34 FCR 447 (“Re Bond”), Morling J stated at 450 to 451:

It is reasonably plain that the legislature’s intention in enacting s 41 (2A) and (2B) was to provide a simple and precise method of calculating an amount that is the equivalent in Australian dollars of an amount of foreign currency.

39 In Re Bond, the judgment debtor argued that the creditor “did not obtain the average of the rates which three authorised foreign exchange dealers would have provided for a dealing in a parcel of US$194,644,443.97 [being the judgment debt] and that the failure to obtain and use the average of such rates resulted in non-compliance with the requirements of s 41(2A) of the Act”: at 450. In dismissing the argument, Morling J said at 450:

In my opinion the reference in subs (2B) to “rates at which Australian dollars may be bought in that foreign currency” at the time and on the date specified in the subsection is a reference to rates which can be ascertained and identified as historical facts, ie rates at which Australian dollars could have been bought at the relevant time. It is not a reference to rates which might have been quoted had a hypothetical transaction taken place in the market.

40 His Honour further stated at 451:

The ascertainment of [the rates in s 41(2A) and (2B)] involves no more than the making of inquiries of authorised foreign exchange dealers as to exchange rates at a particular point in time. Dealers can answer such inquiries by reference to their records. But if Mr Coles’ argument is correct, much more would be required of them. They would be required to apply their minds to the question whether a historical exchange rate may have differed and, if so, to what extent, had it been influenced by a transaction which did not in fact take place. It might be expected that many dealers would decline to express an opinion upon such a matter or would do so only upon payment of a fee. It is unlikely that the legislature could have intended that judgment creditors would be faced with the task of obtaining such opinions from dealers.

41 In Bond v HongKongBank of Australia Limited (1992) 34 FCR 453 (“Bond v HongKongBank”), the Full Court dismissed an appeal from the decision in Re Bond.

42 The Full Court (Lockhart, Gummow and Foster JJ) noted at 459:

Subsection (2B) postulates that the equivalent in Australian dollars of any amount of foreign currency for which an equal value is required for the formulation of a bankruptcy notice to comply with subs (2A) will be ascertained by use of a “rate”, that is to say, by adopting a particular basis for calculation so as to express one currency in terms of another. This rate is not expressed as any one rate in actual use in any particular transaction, nor as the rate which would or might have obtained in a hypothetical transaction. As counsel for the respondent rightly emphasised, the subsection directs attention to the general, rather than to the particular, by speaking of “the average of the rates at which Australian dollars may be bought in that foreign currency ...”

43 The Full Court accepted the submissions of the respondent creditor that speculation by dealers as to what the rate might have been for a hypothetical transaction two business days before the application for issue of the bankruptcy notice was not a statement of the rate at which Australian dollars might be bought at that time on that day. Their Honours agreed with the conclusion of Morling J that it was unlikely that the legislature would have intended that creditors would be presented by the 1985 amendments with the task of obtaining from dealers such opinions.

44 In 1996, ss 41(2A), (2B) and (2C) were repealed: Bankruptcy Legislation Amendment Act 1996 (Cth). The repeal took effect on the same day as the commencement of the Regulations. The view was taken that the provisions governing bankruptcy notices founded on foreign currency judgments should be placed in the Regulations, rather than in the Act itself: see Senate Explanatory Memorandum, Bankruptcy Legislation Amendment Bill 1996 (Cth), par 41.2.

45 Subsequent to the amendments in 1996, reg 4.04 provided:

(1) This regulation applies to a bankruptcy notice if the judgment or order lodged under subregulation 4.01 (1) in relation to the notice is expressed in an amount of foreign currency (whether or not the judgment or order is also expressed in an amount of Australian currency).

(2) A bankruptcy notice to which this regulation applies must:

(a) contain a statement to the effect that payment of the amount of foreign currency expressed in the judgment or order may be paid in that foreign currency or by means of a specified amount of Australian currency that is stated to be equivalent to the amount of foreign currency; and

(b) set out:

(i) the applicable rate of exchange, being the rate worked out in accordance with subregulation (3); and

(ii) the conversion calculation; and

(iii) a statement that the conversion of the amount of foreign currency into Australian currency has been made in accordance with this regulation.

(3) For the purposes of paragraph (2)(b), the conversion of an amount of foreign currency into an equivalent amount of Australian currency must be done in accordance with the exchange rate that, on the second working day before the day on which the relevant application is lodged under subregulation 4.01 (1), is the relevant opening telegraphic transfer rate of the Commonwealth Bank of Australia.

46 In Parianos at [17] and [18], Sackville J said, concerning this form of reg 4.04:

Regulation 4.04(3) itself specifies the manner in which the conversion must be done. In particular, it requires the conversion to be done in accordance with the opening telegraphic transfer rate of the CBA on the second working day before the day on which the application for a bankruptcy notice is lodged under reg 4.01. Thus reg 4.04(3) identifies a particular exchange rate prevailing at a particular time in a particular institution.

Regulation 4.04 is clearly intended to establish a specific scheme for bankruptcy notices issued in relation to foreign currency judgments. The scheme has two principal objects. The first is to inform the judgment debtor that, in order to comply with the bankruptcy notice, he or she has an option. The debtor may pay the judgment debt in the foreign currency in which the judgment is expressed. Alternatively, he or she may choose to pay “by means of a specified amount of Australian currency that is stated to be the equivalent to the amount of foreign currency”. The second and related object is to identify the precise means by which the “specified amount of Australian currency” must be calculated and therefore to notify the debtor of the precise amount of Australian currency that must be paid, if he or she exercises the option to pay in local currency. The means chosen to identify the exchange rate recognises the obvious fact that exchange rates may vary, not merely from day to day, but from hour to hour or even by the minute or second. For this reason, a clearly identified and readily ascertainable rate of exchange is nominated for the purpose of undertaking the calculation required by reg 4.04.

47 It is interesting to note the use by Sackville J of the word “prevailing”.

48 At [30], Sackville J stated that “the Bankruptcy Regulations retained the essentials of the approach previously embodied in the legislation while establishing a simpler and more specific means of determining the appropriate rate of exchange for the necessary currency conversion”. His Honour also noted at [31], “[g]iven the similarities between reg. 4.04 and subss 41(2A), (2B) and (2C), it seems to me that the drafter intended that the regulation should have much the same effect, except for the changes necessarily flowing from the differences in language”.

49 In 2010, reg 4.04 was amended to its current form.

50 The Explanatory Statement for Bankruptcy Amendment Regulations 2010 (No. 1), item 5 provides:

Item 5 removes reference in subregulation 4.04(3) to any particular bank in converting into Australian currency where a judgment or order lodged in relation to a bankruptcy notice is expressed in an amount of foreign currency.

51 Prior to the amendment, the prescribed form contained the following section in relation to foreign currency:

Note 3: Foreign currency amount conversion (see Bankruptcy Regulations, reg. 4.04.) Total debt owing, expressed in foreign currency (amount) Commonwealth Bank of Australia opening telegraphic transfer rate on _/_/_ (date) x (rate) ___________ Australian dollar equivalent = $ (amount) |

52 In 2010, this note was replaced by note A which appears in the extract from the bankruptcy notice set out at paragraph 13 above.

Principles of statutory interpretation

53 The general principles of statutory interpretation apply to delegated legislation: Collector of Customs v Agfa-Gevaert Ltd [1996] HCA 36; (1996) 186 CLR 389 at 398.

54 However, in Australian Tea Tree Oil Research Institute v Industry Research and Development Board [2002] FCA 1227; (2002) 124 FCR 316 at [37], Stone J referred to comments of Lord Reid in Gill v Donald Humberstone & Co Ltd. [1963] 1 WLR 929; [1963] 3 All ER 180 in support of construing delegated legislation “in the light of practical considerations”, saying:

Lord Reid, in the course of considering regulations made under the Factories Act 1937 (UK) concerning the use of scaffolding etc, commented that such regulations were addressed to practical people and were directed to preventing accidents. His Lordship observed (at 934; 183) that such regulations:

“…ought to be construed in the light of practical considerations, rather than by a meticulous comparison of the language of their various provisions, such as might be appropriate in construing sections of an Act of Parliament ... difficulties cannot always be foreseen, and it may happen that in a particular case the requirements of a regulation are unreasonable or impracticable; but, if the language is capable of more than one interpretation, we ought to disregard the more natural meaning if it leads to an unreasonable result, and adopt that interpretation which leads to a reasonably practicable result.”

Meaning of “prevailing”

55 On behalf of Mr Tinkler, it was submitted that the “prevailing” rate is the most favourable rate to the judgment debtor. Mr McDonald argued that the Court should adopt the following reasoning of Judge Manousaridis in Jagatramka v Coeclerici Asia (Pte) Limited (No 2) [2015] FCCA 2743:

142. Reg.4.04(3) of the Regulations does not only require that the Foreign Currency Judgment Amount be converted by use of the telegraphic transfer rate; the Foreign Currency Judgment Amount must be converted by use of a rate that is the “prevailing” telegraphic transfer rate as at the relevant date. The word “prevailing” in the context in which it appears, therefore, presupposes there is more than one institution that makes available to the public documents or other records or sources of information that set out the rates at which on a given day or at a given time on a given day the institution or institutions is or are willing and able to exchange Australian dollars for foreign currencies; and in those documents or information there will be a prevailing rate for the currency in which the Foreign Currency Judgment Amount is denominated. In that context, prevailing means the best rate for converting the currency in which the Foreign Currency Judgment Amount is denominated into Australian currency. That would be the rate that would result in the conversion of the lowest amount of Australian dollars for the Foreign Currency Judgment Amount in question.

…

159. There is another matter I wish to address. If I am correct about the meaning of “the telegraphic rate of exchange prevailing on” the relevant day, there is no simple or certain way of ascertaining that rate. It may be that the difficulty arises from the fact that the rate reg.4.04 of the Regulation requires be used – the “telegraphic rate of exchange” – is a rate that was used and which was well understood in foreign exchange markets which operated under technological and regulatory conditions that were very different from those which apply to contemporary foreign exchange markets. In my opinion, the “telegraphic rate of exchange” should be replaced with a simpler method for identifying the exchange rate with which to convert Foreign Currency Judgment Amounts. One method may be to require the creditor to apply the exchange rates published daily by the Reserve Bank of Australia. The method by which those rates are prepared [is] explained by the Reserve Bank as follows:

Since 1 July 2008, the rate shown for the US dollar is the WM/Reuters Australian Dollar Fix at 4.00 pm (Sydney) on the day concerned, sourced from page AUDFIX on Thomson Reuters and rounded to four decimals. . . . Rates shown for most other currencies are calculated by crossing the rate for the US dollar with the Reserve Bank’s observations of mid-points of buying and selling rates quoted around the same time. These rates are indications of market value only and may differ from those quoted by foreign exchange dealers and other market sources.

160. In the meantime, a creditor who wishes to ascertain “the telegraphic rate of exchange prevailing on” the relevant day for the purposes of converting a Foreign Currency Judgment Amount into Australian dollars may consider adopting a procedure along the following lines:

a) On a day that is two days before the day on which the creditor intends to apply for a bankruptcy notice, the creditor should enquire of the major banking institutions whether they have publicly available rates which they are willing and able to apply for the purpose of exchanging Australian dollars for the currency in which the Foreign Currency Judgment Amount is denominated.

b) If (a) is answered in the affirmative, the creditor should ensure the rates apply to the amount of the Foreign Currency Judgment Amount that is to be converted into Australian dollars.

c) The creditor should then identify from these rates the most favourable rate; that is, the rate that, when applied to convert the Foreign Currency Judgment Amount, will produce the smallest amount of Australian dollars. That is the rate the creditor should apply when converting the Foreign Currency Judgment Amount into Australian dollars.

d) If (a) is answered in the negative, the creditor will need to approach the major institutions to obtain quotes for the rate at which each institution is willing and able to exchange Australian dollars for the Foreign Currency Judgment Amount. The creditor should then apply the most favourable rate to convert the Foreign Currency Judgment Amount; that is, the creditor should choose the rate that results in the least amount of Australian dollars.

56 On behalf of GE, it was argued that the “prevailing” rate was the “current” or “generally current” rate.

57 The Macquarie Dictionary Online defines “prevailing” to mean:

adjective 1. predominant.

2. generally current.

3. having superior power or influence.

4. effectual.

58 The Oxford Dictionary provides the following definition:

Prevailing

…

That prevails; spec. (d) superior, victorious, effective;

(b) predominant in extent or amount; generally current or accepted.

Japan Times At prevailing prices the mines are inclufrring sbustantial losses, prevailing wind the wind that most frequently occurs at a place (as regards direction).

Prevaillingly adverb l18. prevaillingness noun (rare) 19.

59 In my view, the following factors support a conclusion that the word “prevailing” is intended to describe the rate that is generally current, in contrast with a rate that is available to exchange a particular amount (such as the amount of a judgment debt):

(1) The need to identify a rate arises in a context in which there is, potentially, a multiplicity of rates on offer from various institutions. That context is apparent from the explanatory statement to the 2010 amendment, which refers to removing the reference to a particular bank in converting a judgment or order to Australian currency. In that context, the word “prevailing” can meaningfully signify the rate currently or generally available, as opposed to the most favourable rate;

(2) The legislative history of the regulation reveals an intention to specify a rate that is generally available, as opposed to a rate that applies to the particular amount that will be the subject of the exchange calculation. As originally formulated, the applicable rate was an average and, therefore, not necessarily available as an actual rate. As modified, it was expressed to refer to a particular rate and not to a rate that would or might have been available for a particular transaction. The current language does not reveal a clear intention to move away from the previous policy in favour of selecting a rate applicable to a particular hypothetical transaction;

(3) As Sackville J’s reasoning in Parianos makes clear, an ordinary and natural meaning of the word “prevailing” in relation to exchange rates is a rate that is generally available. To describe the opening telegraphic transfer rate of the CBA on a given day, as a particular exchange rate prevailing at a particular time in a particular institution recognises that the rate is the rate initially quoted, but subject to variation (at least in the case of transfers of large amounts);

(4) The requirement to identify a rate prevailing on the second working day before the day on which the relevant application is lodged under subreg 4.01(1) is designed to promote certainty rather than to require the judgment creditor to identify a rate favourable to the judgment debtor. As Sackville J noted in Parianos, and as appears from the reference in the prescribed form to an “opening” rate, the context in which the rate is identified includes the possibility of rates which may vary within a short space of time. The reference to an “opening” rate in the form also indicates that the regulation is concerned to promote certainty, rather than to promote the interests of the judgment debtor by performing a calculation based on the rate most favourable to him or her;

(5) The judgment creditor’s capacity to obtain a generally current rate is obvious, because (as the evidence reveals) generally current rates are published. On the other hand, the evidence also shows that the capacity to obtain a rate applicable to a particular judgment sum may depend upon the judgment creditor’s relationship with one or more banks. The potential impracticalities of requiring the judgment creditor to obtain an actual rate were identified in Re Bond and Bond v HongKongBank and the legislature does not appear to have amended the regulation to clarify that an actual rate must be obtained, contrary to the courts’ earlier interpretation;

(6) The need to identify a rate is not for the purpose of conducting an actual transaction. Rather, it is to provide an option to the debtor to comply with the notice by a payment in Australian currency. Whether that option will be attractive to the debtor will depend upon exchange rate movements between the date of the bankruptcy notice and the date of any payment of the debt.

60 The factors set out above, particularly (2), (3), (4), (5) and (6) tend against Mr Tinkler’s interpretation. I also accept the argument made on behalf of GE that the word “prevailing” rate does not signify the best rate available, or the best rate available for transfer of the judgment debt, because that meaning is likely to impose an impractical burden on the person wishing to issue a bankruptcy notice. It is not obvious that enquiries of the major banking institutions about publicly available rates would be sufficient to identify the best rate. Better rates might be available from other banking institutions, or might be available on request but not publicly available. In order to obtain the best rate, the judgment creditor might be required to seek quotes from every institution which provides for telegraphic transfer of currency. The judgment creditor might be put to considerable expense to obtain quotes and institutions might be put to the inconvenience of providing quotes for a hypothetical transaction.

61 There is no reason to believe that the best rate would be the most widely available rate. To the contrary, the evidence suggests that better rates are available for particularly large transfers and less favourable rates are offer for more typical, smaller transfers. Accordingly, I respectfully disagree with Judge Manousaridis’ interpretation of reg 4.04. I note that his Honour does not refer to the decisions in Bond.

Is the rate in the bankruptcy notice the telegraphic rate of exchange prevailing on 15 June 2015?

62 On behalf of Mr Tinkler, it was not disputed that the rate in the bankruptcy notice is correctly described as a “telegraphic rate of exchange” or a “telegraphic transfer rate”. Nor was it suggested that these expressions do not refer to the same rate.

63 I accept, on the evidence of Mr Clark, that the rate in the bankruptcy notice is the inverse of a telegraphic rate of exchange published by Westpac and available from Westpac for telegraphic transfers from US dollars to Australian dollars on 15 June 2015.

64 I also accept that the rate in the bankruptcy notice is the rate prevailing, in the sense of being generally current, for exchanges by telegraphic transfer of US to Australian dollars through Westpac on 15 June 2015.

65 Was GE required to provide evidence about other rates of exchange available on 15 June 2015 to demonstrate that the Westpac rate as the prevailing rate within the meaning of reg 4.04? In my view, the form of the bankruptcy notice shows that the regulation will be satisfied by the inclusion of a rate that is published by a banking institution as generally available for the relevant date, or is published as having been generally available on that date, being a rate that answers the description “telegraphic rate of exchange”.

66 Such a rate is sufficient to achieve the apparent purpose of the regulation, being to calculate an Australian dollar amount equivalent to the amount of a judgment expressed in foreign currency. If the regulation were intended to require more, then the form of the bankruptcy notice would probably have been drafted to require the inclusion of that information or, alternatively, the regulation would have stipulated some other means by which the creditor would be required to demonstrate, to AFSA and the creditor, that the required steps were taken to ascertain the “applicable rate of exchange”.

67 For these reasons, I am satisfied on the balance of probabilities, that the rate in the bankruptcy notice is the applicable rate of exchange. I am fortified in that conclusion by the absence of evidence from Mr Tinkler that there was a rate different from the rate in the notice that was the “prevailing” rate on 15 June 2015.

Is 15 June 2015 the second day before the day when the application for the bankruptcy notice was lodged under subreg 4.01(1)?

68 Subregulation 4.01(1) provides:

(1) Subject to subregulation (2), to apply for the issue of a bankruptcy notice, a person must lodge with the Official Receiver:

(a) an application in the approved form; and

(b) 1 of the following documents in relation to the final judgment or final order specified by the person on the approved form:

(i) a copy of the sealed or certified judgment or order;

(ii) a certificate of the judgment or order sealed by the court or signed by an officer of the court;

(iii) a copy of the entry of the judgment or order certified as a true copy of that entry and sealed by the court or signed by an officer of the court.

69 Subregulation 4.01(2) does not apply to this case.

70 The creditor’s case depended upon the Court finding that the application for the bankruptcy notice was lodged on 17 June 2015.

71 The relevant facts are:

(1) On 17 June 2015, Mr Clark submitted an application to AFSA for a bankruptcy notice. He made the application using an online form provided on AFSA’s website. Mr Clark completed the form by entering various details and uploading a copy of the judgment on which the bankruptcy notice was to be based. As the judgment debt was expressed in US dollars, Mr Clark also provided details concerning conversion of the amount of the judgment into Australian dollars. He entered the following details:

(a) Name of institution: Westpac Banking Corporation;

(b) Date: 15 June 2015;

(d) Foreign currency amount: 2,252,968.52; and

(e) Telegraphic transfer rate: 1.23579.

(2) At 15:06, AFSA sent Mr Clark a letter, by email, stating that the application was assigned application number 182116, that it was currently awaiting assessment and that, once assessed, Mr Clark would receive an advice on the outcome of his application;

(3) At 15:38, AFSA sent Mr Clark a second email, attaching a letter in the following terms:

The Bankruptcy Notice for Nathan TINKLER that you have submitted (Application Number: 182116) could not be processed due to the following reason:

Other – 1) The judgment number entered in the judgment number field and on the post judgment interest schedule is incorrect. The judgment number refers to the case number on the attached judgment. Please amend the judgment number field and post judgment interest claim. 2) The converted AUD dollar amount is to be entered in the judgment amount field as the calculations are made in AUD for the post judgment interest claim and debt total. 3) The currency conversion statement under general details “The conversion of the amount of foreign currency into Australian currency has been made in accordance with Regulation 4.04(2)” must be entered on a separate sheet of paper and uploaded with the judgment as this must be served on the debtor along with the judgment.

Available options

1. Resubmitting your application

You may resubmit your appropriately revised application without incurring additional costs if you do so within 28 days.

If you have submitted a paper application you will receive a replacement application form in the next few days.

2. Submitting a new application

If you do not resubmit a revised application within 28 days, you will be required to submit a new application and pay the appropriate fee.

(4) Sometime before 17:18 on 17 June 2015, Mr Clark submitted a revised application which sought to address the matters set out in AFSA’s letter. At 17:18, he received a second letter from AFSA stating that the application was currently awaiting assessment and that, once assessed, Mr Clark would receive an advice on the outcome of his application;

(5) On 18 June 2015 at 10:56, AFSA wrote to Mr Clark in the following terms:

The bankruptcy Notice for Nathan TINKLER that you have submitted (Application Number: 182116) could not be processed due to the following reason:

Other – Kindly include the statement regarding the currency conversion with the judgement instead of a separate supporting document as AFSA is required to issue the Bankruptcy Notice with the judgement and said statement attached.

Available options

1. Resubmitting your application

You may resubmit your appropriately revised application without incurring additional costs if you do so within 28 days.

If you have submitted a paper application you will receive a replacement application form in the next few days.

2. Submitting a new application

If you do not resubmit a revised application within 28 days, you will be required to submit a new application and pay the appropriate fee.

(6) Sometime before 11:04am on 18 June 2015, Mr Clark submitted a .pdf document which included the judgment and the statement regarding the currency conversion. At 11:04, he received a third letter from AFSA stating that the application was currently awaiting assessment and that, once assessed, Mr Clark would receive an advice on the outcome of his application;

(7) On 19 June 2015, AFSA wrote to Mr Clark to inform him that his application for the issue of a bankruptcy notice in respect of Mr Tinkler had been accepted. The bankruptcy notice was issued on 19 June 2015.

72 Neither party identified an approved form of application within the meaning of subreg 4.04(1)(a). I infer that the online form completed by Mr Clark is the approved form.

73 On the basis of the evidence set out above, I am satisfied that the application for the bankruptcy notice was lodged on 17 June 2015, when Mr Clark submitted the application that was assigned the number 182116. I infer that the application was lodged in the approved form when it was first lodged because:

(a) it was assigned an application number;

(b) the first two matters raised in AFSA’s 15:38 letter concern the content of the application rather than the form of the application;

(c) although the third matter could be regarded as a matter of the form of the application (in that it requires the relevant statement to be entered on a separate sheet of paper and uploaded with the judgment as this must be served on the debtor along with the judgment), I am not satisfied that this requirement was part of the “approved form” within the meaning of subreg 4.04(1)(a) because there was no evidence to support such a conclusion;

(d) there is no other evidence that the application was not in the approved form and the bankruptcy notice was issued in due course.

74 Accordingly, the applicable rate of exchange was the telegraphic rate of exchange prevailing on 15 June 2015.

Compliance with requirements for a sequestration order

75 Section 52 provides, relevantly:

(1) At the hearing of a creditor’s petition, the Court shall require proof of:

(a) the matters stated in the petition (for which purpose the Court may accept the affidavit verifying the petition as sufficient);

(b) service of the petition; and

(c) the fact that the debt or debts on which the petitioning creditor relies is or are still owing;

and, if it is satisfied with the proof of those matters, may make a sequestration order against the estate of the debtor.

…

(2) If the Court is not satisfied with the proof of any of those matters, or is satisfied by the debtor:

(a) he or she is able to pay his or her debts; or

(b) for other sufficient cause a sequestration order ought not to be made;

it may dismiss the petition

(3) The Court may, if it thinks fit, upon such terms and conditions as it thinks proper, stay all proceedings under a sequestration order for a period not exceeding 21 days.

76 On behalf of Mr Tinkler, Mr McDonald raised only one issue concerning the creditor’s compliance with the requirements for a sequestration order. He argued that the creditor’s petition misstated the amount owed by Mr Tinkler because it stated that he owed GE $2,803,647.20 being the total debt (in Australian dollars) in the bankruptcy notice. The amount in the creditor’s petition could not be the same amount as in the bankruptcy notice, which was issued about one month earlier, because there would be interest accruing between the issue of the bankruptcy notice and the date of the creditor’s petition.

77 Mr McDonald did not identify any authorities in support of this argument, which I reject. By s 44(1) of the Act:

(1) A creditor’s petition shall not be presented against a debtor unless:

(a) there is owing by the debtor to the petitioning creditor a debt that amounts to $5,000 or 2 or more debts that amount in the aggregate to $5,000, or, where 2 or more creditors join in the petition, there is owing by the debtor to the several petitioning creditors debts that amount in the aggregate to $5,000;

(b) that debt, or each of those debts, as the case may be:

(i) is a liquidated sum due at law or in equity or partly at law and partly in equity; and

(ii) is payable either immediately or at a certain future time; and

…

(d) the act of bankruptcy on which the petition is founded was committed within 6 months before the presentation of the petition.

78 There is no requirement that the creditor’s petition state the precise amount of the debt owing as at the date of the petition.

79 Mr McDonald did not submit that s 44(1) was not satisfied, except by reference to the arguments addressed above.

80 The creditor’s petition states:

1. The respondent debtor owes the applicant creditor the amount of $2,803,647.20, being the amount payable under the judgment of the Supreme Court of New South Wales in proceedings 2014/00146886 (Proceedings) in relation to the respondent debtor’s obligations under an agreement entitled ‘US$ Aircraft Loan Facility Agreement’ dated 17 September 2010 (Facility) as guarantor of a loan provided by the applicant creditor.

2. The applicant creditor does not hold security over the property of the respondent debtor.

3. At the time when the act of bankruptcy was committed, the respondent debtor:

(a) had a dwelling house or place of business in Australia; and

(b) was carrying on business in Australia either personally or by an agent or manager.

4. The following act of bankruptcy was committed by the respondent debtor within 6 months before presentation of this petition:

(a) In the Proceedings, the applicant creditor brought a claim against the respondent debtor for payment of money owed under the Facility.

(b) Judgment was entered in the Proceedings on 19 May 2015 in favour of the applicant creditor in the amount of US$2,252,968.52 (Judgment Debt).

(c) On 19 June 2015, the Official Receiver issued a bankruptcy notice to the respondent debtor in relation to the Judgment Debt. The bankruptcy notice was served on him on 25 June 2015.

(d) The respondent debtor failed to comply on or before 16 July 2015 with the requirements of the bankruptcy notice served on him on 25 June 2015 or to satisfy the Court that he had a counter-claim, set off or cross demand equal to or more than the sum claimed in the bankruptcy notice, being a counter-claim, set-off or cross demand that he could not have set up in the action in which the judgment referred to in the bankruptcy notice was obtained.

81 Paragraphs 1 to 3 of the creditor’s petition were verified by an affidavit of Simon Davies, a portfolio manager of GE, affirmed 22 July 2015.

82 The matters in paragraph 4 of the creditor’s petition were verified by the affidavit of Mr Clark sworn 13 November 2015 as to paragraphs 4(b) and (c), except for proof of service of the bankruptcy notice which is proved by the affidavit of Mark Stephenson sworn 21 July 2015 and annexed to Mr Clark’s affidavit sworn 25 August 2015. Paragraph 4(d) is verified by Mr Davies’ 22 July 2015 affidavit.

83 Service of the petition was effected by substituted service, and was proved by affidavits of Mr Stephenson sworn 24 September 2015 and Mr Clark sworn 25 September 2015.

84 The fact that the debt on which GE relies is still owing was proved by an affidavit of debt affirmed by Mr Davies on 11 December 2015 by which Mr Davies affirmed that the debt on which GE relies was still owing as at 11 December 2015.

85 There is an affidavit of Mr Clark sworn 13 December 2015 showing that, on that date, he caused a search to be made of the National Personal Insolvency Index which revealed no details of a debt agreement about the debt on which GE relies.

86 Accordingly, I am satisfied that GE has proved the matters required by s 52(1).

87 For the reasons given above, I am not satisfied of either of the matters set out in s 52(2). I am not satisfied that there is any other matter which would warrant the exercise of the Court’s residual discretion not to make a sequestration order.

I certify that the preceding eighty-seven (87) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: