Diab Pty Ltd v YUM! Restaurants Australia Pty Ltd [2016] FCA 43

ORDERS

DIAB PTY LTD (ACN 003 168 812) Applicant | ||

AND: | YUM! RESTAURANTS AUSTRALIA PTY LTD (ACN 000 674 993) Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Proposed orders, by consent or as proposed by each party, be sent to chambers by 19 February 2016.

2. Any proposed redactions to the reasons, said to be confidential, be sent to chambers by 19 February 2016.

3. The matter be stood over to 23 February 2016 at 9.30am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

TABLE OF CONTENTS

[3] | |

[3] | |

[6] | |

[11] | |

[15] | |

[20] | |

[23] | |

[23] | |

[25] | |

[28] | |

[29] | |

[31] | |

[35] | |

[39] | |

[39] | |

[40] | |

[42] | |

[43] | |

[46] | |

[49] | |

[50] | |

[51] | |

[52] | |

[55] | |

[59] | |

5.3.3.3 DPL’s conclusion on the presentation of the ACT Test during the Franchisee Update presentation | [60] |

[61] | |

[64] | |

[67] | |

[71] | |

[72] | |

[75] | |

[78] | |

[81] | |

[84] | |

[94] | |

[97] | |

[100] | |

5.4.6 Was $4.95 was an unprofitable price for the Classics range? | [103] |

[109] | |

[110] | |

[113] | |

[119] | |

[122] | |

[125] | |

[125] | |

[136] | |

[139] | |

5.8 The reasons of Jagot J in the interlocutory application for injunctive relief | [140] |

[149] | |

[149] | |

[153] | |

[159] | |

[160] | |

[162] | |

[165] | |

[168] | |

[171] | |

[173] | |

[177] | |

[178] | |

[185] | |

[190] | |

[196] | |

[203] | |

[203] | |

[206] | |

[210] | |

[217] | |

[220] | |

[220] | |

[232] | |

[250] | |

[266] | |

[279] | |

[283] | |

[284] | |

[286] | |

[306] | |

[318] | |

[334] | |

[347] | |

[353] | |

[353] | |

[362] | |

9.3 The ACT Test, the Yum Model and the first mover advantage | [371] |

[402] | |

9.5 The intervention of the interlocutory proceedings and Domino’s pre-emptive launch of a $4.95 every day pizza | [403] |

[427] | |

[436] | |

[439] | |

[440] | |

[440] | |

[440] | |

[441] | |

[443] | |

[448] | |

[448] | |

[451] | |

[453] | |

[458] | |

[461] | |

[462] | |

[465] | |

[465] | |

[468] | |

[470] | |

[470] | |

[474] | |

[478] | |

[481] | |

[482] |

BENNETT J:

1 These proceedings, brought by Diab Pty Limited (DPL), a franchisee of Pizza Hut outlets, concern a decision made by Yum! Restaurants Australia Pty Limited (Yum), the franchisor. That decision, which was announced to Pizza Hut franchisees on 10 June 2014 and implemented on 1 July 2014, was to reduce the ranges of Pizza Hut pizzas from four to two and reduce the prices in the available ranges to two price points: $4.95 for “Classics” pizzas (from $9.95) and $8.50 for “Favourites” pizzas, formerly called “Legends” pizzas (from $11.95). Yum’s strategy was known as the Value Strategy (VS) and the reduced price points were predicated on various iterations of a model prepared by Yum personnel (the Yum Model). DPL brings its claim against Yum as the representative applicant of all persons who were franchisees under an International Franchise Agreement (IFA) with Yum to operate Pizza Hut outlets as at 1 July 2014 (Franchisees; singular: Franchisee).

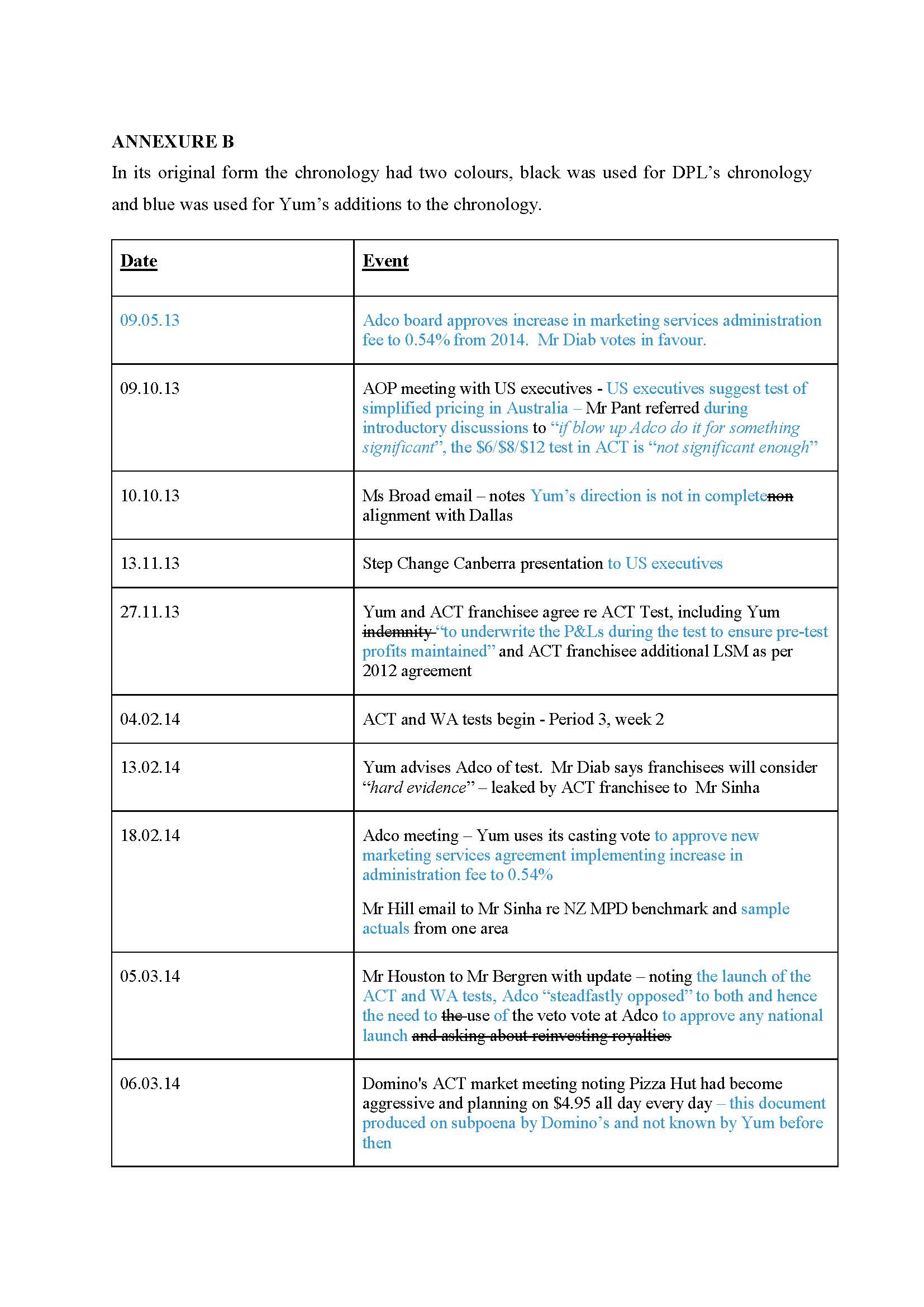

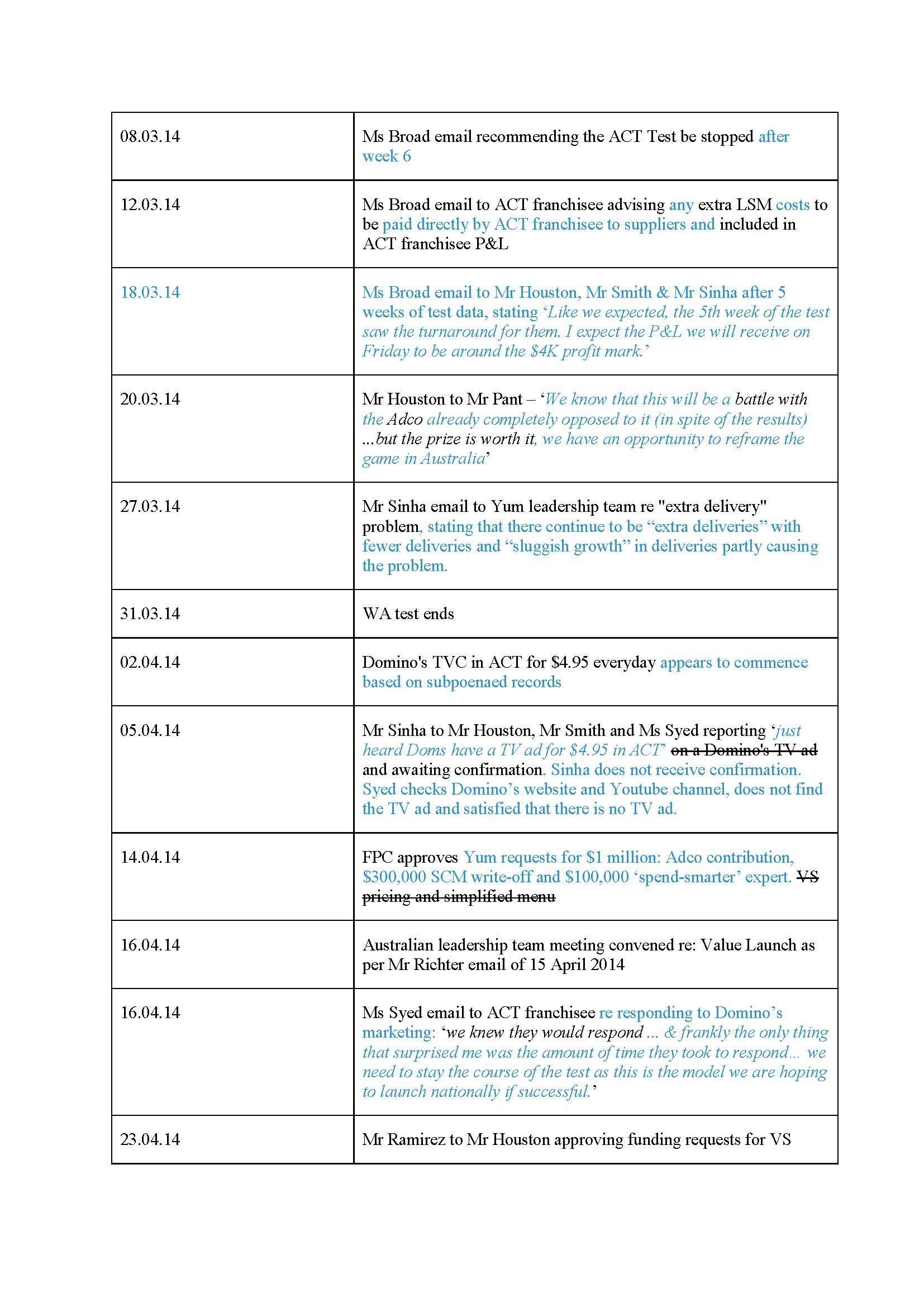

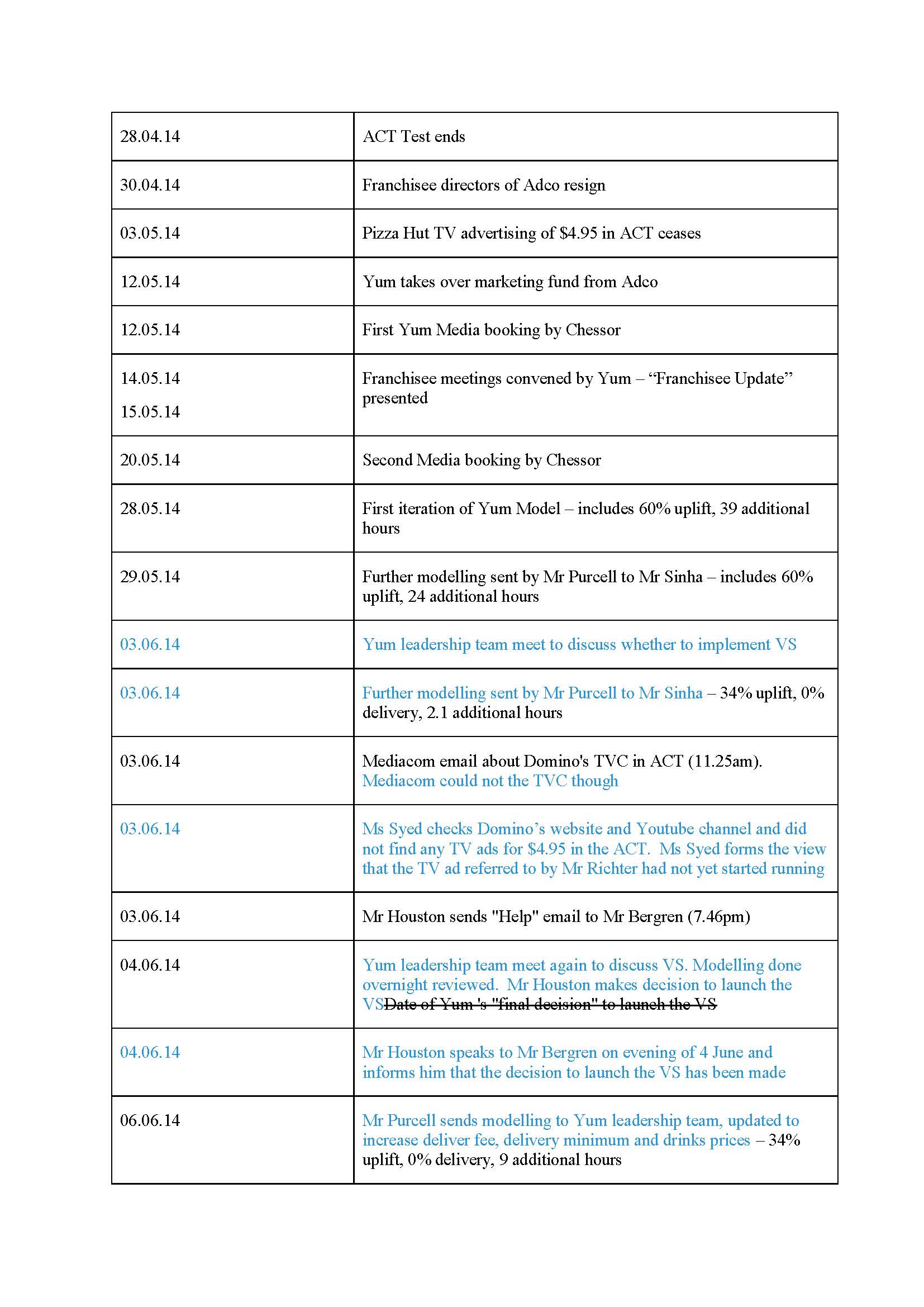

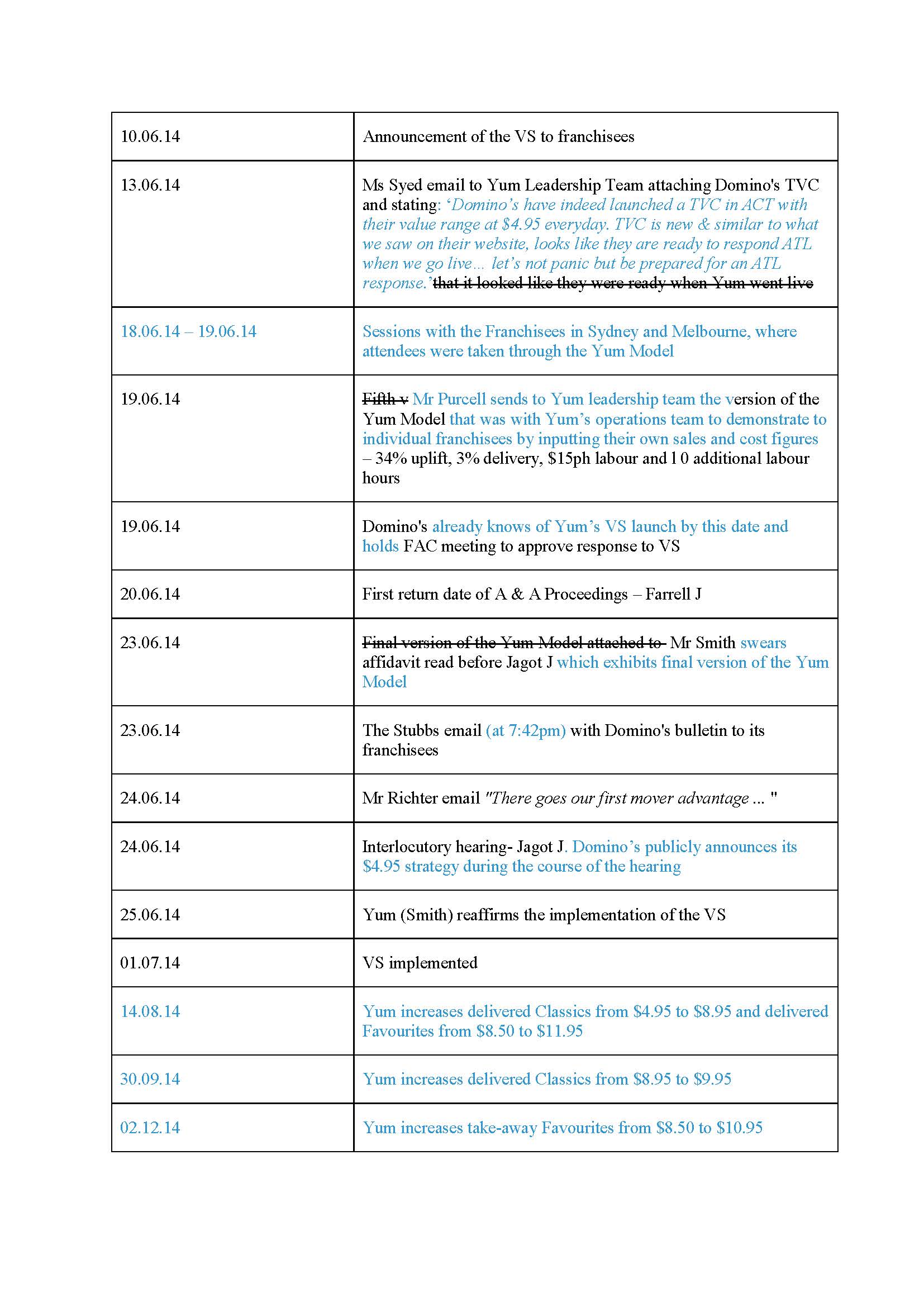

2 A range of terminology and definitions are used in these reasons. Accordingly, a glossary of terms is attached in Annexure A. Further, the parties provided a series of chronologies, following the hearing, and a summary chronology of the events relevant to this matter is attached in Annexure B. That chronology, submitted by the parties, is not agreed as to all of the facts as provided but serves only to provide a convenient reference of the relevant date. DPL provided the original chronology, which is represented in black in Annexure B, and Yum made changes to DPL’s chronology and those changes are represented in blue in Annexure B.

3 DPL is a Pizza Hut franchisee which owns and operates six Pizza Hut outlets in the Greater Macarthur region of south-western Sydney, pursuant to a separate IFA for each outlet.

4 DPL was formed in 1986. Mr Danny Diab is the majority shareholder and managing director of DPL. Since 1995, Mr Diab has had an extensive involvement in all aspects of the Pizza Hut business in Australia, including as a franchisee director of Pizza Hut Adco Limited (Adco), a body that, in conjunction with Yum, is responsible for marketing and promotional activities and promoting the Pizza Hut business, brands and products in Australia. Mr Diab was a director of Adco until April 2014 and was a representative on many of Yum’s joint councils with Franchisees. Mr Diab is also a director of Restaurant Brands New Zealand Limited (RBNZ), the New Zealand Pizza Hut master franchisee.

5 When compared to the national average, all of the current DPL outlets are high volume stores. Mr Diab gave evidence that DPL outlets have a 2-to-1 advantage over the Domino’s stores in the Greater Macarthur region. This is not the case with other Pizza Hut outlets. The importance of this numerical advantage and scale was recognised within Yum as seen in an email of 11 August 2013 from the senior planner of Yum in the USA. In the period February to June 2014 DPL outlets were experiencing increasing sales with a “run rate” of approximately 3.55% increase in sales growth. Mr Diab gave evidence that he advised Yum of the positive progress that DPL was making. DPL states that since the implementation of the VS, it has experienced a significant decline in its sales and profitability.

6 Yum is an Australian subsidiary of Yum! Brands, Inc. (Yum US), which is a publicly listed company on the New York Stock Exchange and is among the world’s top 250 companies on the Fortune 500 list. Yum operates the Pizza Hut business in Australia. Yum called key personnel involved in the launch of the VS to give evidence. The personnel included:

Mr Graeme Houston, the General Manager of Pizza Hut South Pacific (SOPAC);

Ms Lynne Broad, employed by Yum as the Head of Finance and Supply Chain, Pizza Hut;

Mr Kurtis Smith, employed by Yum in July 2013 as the Head of Operations of Pizza Hut SOPAC and in January 2014, he became the Market Director for Pizza Hut in Australia until January 2015;

Ms Fatima Kamali-Syed, employed by Yum as the Head of Marketing; and

Mr Devesh Sinha, employed by Yum as the National Operations Manager from January 2014 until 15 July 2015.

7 Mr Houston has been a director of Yum since 21 December 2011. Ms Broad became a director in December 2014. Mr Smith and Mr Sinha no longer work for Yum; however, both have roles in Yum US’ Dallas headquarters. Mr Smith is the Senior Director of Development of the USA Pizza Hut business and Mr Sinha is now the Senior Manager of Operations for what has been described as Pizza Hut Global.

8 Mr Houston gave evidence that, as at 27 November 2014, there were approximately 210 Pizza Hut franchisees in Australia, of which approximately 45 were franchisees which operated more than two outlets and approximately 4 were franchises which operated more than 5 outlets.

9 In terms of its own financial reporting cycle, Yum provides quarterly reports to the Chief Financial Officer (CFO) of Pizza Hut Global, Mr Enrique Ramirez, commencing each year with a forecast known as Q0F, which is then updated in subsequent periods by forecasts known as Q1F, Q2F and Q3F. According to Ms Broad, these forecasts are then built into a consolidated forecast for the Pizza Hut business as a whole.

10 In terms of business and financial planning, Yum commences this process in about July of each year when Yum, with every other business unit which is a subsidiary or related entity around the world, submits a market growth plan which outlines store build and profit targets, which are agreed with the Pizza Hut Global CFO. In about October of each year, there is a conference between Yum’s leadership team and the Yum US senior leadership team. During this conference, Yum presents its business strategy known as the Annual Operating Plan (AOP) to the Yum US senior leadership team. The AOP meeting for the 2014 Yum year took place on 9 October 2013.

1.3 Representative proceedings and group members

11 These representative proceedings were commenced by DPL under Part IVA of the Federal Court of Australia Act 1976 (Cth) (the FCA Act). The group members are defined as the Franchisees who suffered loss as a result of the introduction of the VS. Opt-out notices were sent to all potential group members on 10 October 2014, as a result of which only 11 of the Franchisees opted out. It follows that approximately 190 of 200 of the Franchisees are group members for the purposes of the proceedings.

12 In accordance with s 33H(1)(c) of the FCA Act, DPL has specified the questions of law and fact common to the claims of all group members in the Amended Originating Application dated 2 April 2015 (the application): (Merck Sharp & Dohme (Australia) Pty Ltd v Peterson [2009] FCAFC 26 at [6]).

13 DPL submits that, other than questions relating to the quantification of damages, there is a very high level of commonality between the claims of DPL and each of the group members – essentially because Yum’s conduct involved the introduction of a single, national strategy and Yum’s legal relationship with the Franchisees was and is conducted pursuant to a standard form IFA. However, other group members may have separate claims that they may wish to advance against Yum pursuant to s 33R of the FCA Act. These separate claims would be in addition to the claims made in the Amended Statement of Claim dated 2 April 2015 (ASC). Also, it is probable that each group member would have to establish his, her or its damages if liability is established.

14 It should be noted that, in [26] of the ASC, DPL has clearly specified that it claims damages on its own behalf as an individual claim, which includes the quantification of its loss as to which it has led evidence from both Mr Diab and Mr Potter. DPL particularised, in [27] of the ASC, that ‘[p]articulars of the loss and damage suffered by the [Franchisees] will be provided after the determination of the common issues relating to liability and the determination of the individual damages claim of [DPL]’. That is, if the Court finds in favour of DPL and awards damages to DPL, the judgment will enure for the benefit of all group members as findings on the common questions, other than in respect of the quantification of damages. The Court’s power to award damages to DPL only at this time is established by s 33Z(1)(e) of the FCA Act. The Court may then take submissions as to the appropriate orders or directions to be made in respect of the damages claims or assessments to be made in respect of all other group members under s 33Z(1)(g) or s 33ZF of the FCA Act.

15 Mr Diab, and each Franchisee, executed the IFA for a term of 10 years with a right of renewal for a further 10 years, subject to certain conditions of compliance (clause 18). The IFA provides in clause 14 that the Franchisee cannot sell or transfer any interest in the IFA without Yum’s prior written approval of the proposed transferee.

16 Clause 1.1 provides that Yum grants to the Franchisee the right to use a comprehensive restaurant system (the System). The Franchisee agrees to use its best endeavours to develop the Business (defined as the business of preparing, marketing and selling the products) and to increase the Revenues (defined as gross receipts received by the franchisee as payment for the products and for other goods and services) (clause 1.2). By clause 2.3, the initial and annual payments made by the Franchisees are in consideration of the rights granted in clause 1.1 and not for Yum’s performance of any specific obligations or services.

17 Also relevant are clauses:

5.2 Franchisor may, by notice to Franchisee, at any time change or withdraw any Approved Product or add new Approved Products. Franchisee will implement such changes, withdrawals and additions within the period specified in the notice.

…

6.1 Franchisee will not execute or conduct any advertising or promotional activity in relation to the Business or the System without Franchisor’s prior written approval.

6.2 Franchisee will participate in such national and regional advertising, promotions, research and tests as Franchisor from time to time requires and Franchisee will not have any claim or action against Franchisor in connection with the level of success of any such advertising, promotion, research or test.

…

23.1 This Agreement constitutes the entire agreement between the parties with respect to its subject matter and supersedes all prior negotiations, agreements or understandings.

18 “Approved Products” are defined, in schedule A of the IFA, as ‘the products from time to time approved by Franchisor for sale in the Business.’ Yum also points to the “franchisee’s representation” which forms part of the IFA:

(a) Franchisee has reviewed this Agreement with the assistance and advice of independent legal counsel and understands and accepts the terms and conditions of this Agreement;

(b) Franchisee has relied upon its own investigations and judgment in entering this Agreement, after receiving legal and financial advice, and no inducements, representations or warranties other than those expressly set forth in this Agreement, have been given in respect of the System, the Business or this Agreement; and

(c) Franchisee acknowledges that establishment and operation of the Business will involve significant financial risks and that the success of the Business will depend upon the skills and financial capacity of Franchisee and also upon changing economic and market conditions and that such risks, skills and conditions are not in any way guaranteed or underwritten by Franchisor.

19 The key clause with respect to the exercise by Yum of its power to fix the prices pursuant to the VS is clause C1 the IFA. This clause provides:

MAXIMUM RETAIL PRICE

Franchisee will not permit any Approved Product to be sold at the Outlet at any price exceeding the maximum retail prices advised by Franchisor to Franchisee from time to time.

3. THE STATEMENT OF CLAIM/THE ASC

20 There are certain matters as to the IFA that are not in dispute on the pleadings:

The IFA provided the structure for the System.

The Franchisees agreed to comply with specifications concerning the operation of the System, which provided for uniform operation of all restaurants within it.

The matters set out in clause 1.1 of the IFA.

The Franchisee is an independent contractor and no fiduciary relationship exists between the franchisor and the Franchisee.

The Franchisees will not permit any Approved Products to be sold at any price exceeding the maximum retail prices advised by the franchisor to the Franchisees from time to time.

The franchisor may, by notice to the Franchisees, change, withdraw or add new Approved Products.

The Franchisees will participate in advertising and promotions as the franchisor requests, with no claim in connection with the level of success.

The Franchisees will spend an amount on advertising as directed by the franchisor, being 6% of revenues, as defined, payable to the Adco or as directed by Yum and 0.5% of revenues on local advertising and promotions approved by the franchisor.

21 DPL’s pleaded case in contract has two related components:

(1) DPL pleads that on the proper construction of clause C1, Yum was obliged to set profitable prices – being prices that would enable a Franchisee to make, maintain or increase its profits;

(2) DPL pleads that Yum was subject, in any event, to the following implied duties owed by Yum under the IFA to DPL and to each Franchisee:

(a) A duty to cooperate with the Franchisees to achieve the objects of the IFA; and

(b) A duty to comply with standards of conduct that are reasonable having regard to the interests of the parties to the IFA.

22 Diab also pleads that ‘for the purpose of the Implied Duties and/or for the purpose of construing Yum’s powers under the IFA’ the following, in summary, applies:

The object of the IFA is to generate profits for DPL and for each Franchisee performing in accordance with the IFA.

The benefit of the IFA for DPL and each Franchisee, and their interest under the IFA includes:

the ability to make and increase profits after covering operating costs, overheads and cost of capital, from developing the business and by investment of capital, time, skill and labour using a proven business system and brand developed by Yum, without having to share those profits with Yum except by way of fixed royalty percentage;

the ability to market, sell and transfer the business and reap a capital gain; and

the collective marketing of the Pizza Hut brand to consumers in Australia, in relation to which all Franchisees contribute.

23 Mr Diab is the managing director and the majority shareholder of DPL. Mr Diab has been involved in the pizza business since 1987 and has been involved with Pizza Hut since 1989. His involvement with Pizza Hut includes:

Over the last 25 years, he has overseen the development and operation of DPL’s Pizza Hut outlets.

From 1998 to 2011 and from 2012 to May 2014, Mr Diab was a franchisee director of Adco.

He was a franchisee representative of a number of other Yum bodies including the Pizza Hut Purchasing Council, the Pizza Hut Operations Council, the Pizza Hut Development Council and the Customer Service Centres Council.

Between 2009 and 2012, Mr Diab was President of the Australasian Pizza Association Inc, which is a representative body for approximately 150 of the Pizza Hut franchisees. Further, between 2000 and 2008, Mr Diab was the President of the National Pizza Association, which was the predecessor of the Australasian Pizza Association Inc.

Since 2013, Mr Diab has been a director of RBNZ. Prior to 2013, he worked as a consultant to RBNZ and advised it in relation to its acquisition of the Eagle Boys chain in New Zealand during 1999-2000 and in relation to its acquisition of 51 Pizza Hut Outlets in Victoria in 2002, which it subsequently sold in the 2007/2008 financial year.

24 Mr Diab also holds a Diploma in Company Directorship from the University of New England and the Australian Institute of Company Directors (AICD), and a Graduate Diploma in Corporate Management from the Institute of Corporate Managers, Secretaries and Administrators (ICMSA). Further, Mr Diab is a Foundation Fellow of the AICD, since 1991, and a Fellow of ICMSA, since 1995.

25 Mr Houston is employed by Yum as the General Manager Pizza Hut South Pacific (SOPAC) and has held this position since 2011.

26 Mr Houston was awarded a Bachelor of Commerce from Canterbury University in New Zealand in 1986. He has been employed by Yum, or its related entities, since 1990. His various roles have included:

From 1990 to 1994, he held various Area Manager Positions in Auckland and Dunedin in New Zealand and Wollongong, New South Wales in KFC Operations (which is a division of Yum). At that time KFC was part of Pepsi Co International.

In 1994, he was promoted to the position of Operations Manager New South Wales KFC.

In 1995, he was promoted to market manager for Pizza Hut New Zealand and this was the most senior position in Yum that was based in New Zealand.

In 1997, Mr Houston was promoted to Market Manager KFC Victoria, Tasmania and South Australia where he was responsible for 90 company owned restaurants and 48 franchised outlets.

In 2002, he was promoted to Chief Supply Chain Officer for both KFC and Pizza Hut, based in Sydney. In that role he reported to the Managing Director Yum SOPAC.

In 2003, Mr Houston became the General Manager Pizza Hut Operations SOPAC, in which he led the Operations team for Pizza Hut in Australia and New Zealand.

In 2006, Mr Houston became the Vice President of Pizza Hut Delivery Operations of Yum! Restaurants International (which is a division of Yum US). Mr Houston was responsible for developing the Pizza Hut delivery business for all countries in which Pizza Hut did business except the USA and China. He held this job until 2011. During this period, Mr Houston also participated in the Global Pizza Hut Brand Council, which is an annual meeting of “key thought leaders” from the global Pizza Hut brand to help develop and refine the Pizza Hut brand strategy.

27 From 2013, Mr Houston has also assumed responsibility for establishing and developing the Pizza Hut brand in Russia. This role was expanded from 2014 as Pizza Hut Africa was added to his portfolio.

28 Mr Broad is employed by Yum as the Head of Finance & Supply Chain, Pizza Hut and has held this position since the middle of 2013 and reports to Mr Houston. Ms Broad has held the position of Head of Finance since January 2011. Ms Broad commenced employment with Yum in April 2007 and has held the following roles: Group Taxation & Treasury Manager, Finance Manager and Commercial Planning Manager. Ms Broad was awarded a Bachelor of Commerce from the University of Sydney and Graduate Diploma from the Institute of Chartered Accountants in Australia. Ms Broad is currently a director of Yum and was appointed in December 2014.

29 Ms Syed is the Head of Marketing of Yum and a member of the Leadership Team. Ms Syed has held these positions since January 2013. She has seven employees in her team, five in the Marketing Team and two in the Research and Development Team. Mr Richter is the Marketing Manager and the most senior person reporting to Ms Syed. Ms Syed began working for Yum in November 2010 as the Group Marketing Manager.

30 Ms Syed was awarded a Bachelor of Business Degree by the University of Technology, Sydney, in 2000 and was awarded a Masters of International Business Degree from the University of Sydney in 2001. She has worked as a marketing professional in Australia for 12 years, in the following roles:

Assistant Brand Manager at Nestlé Australia Ltd from 2002 to 2004.

Brand Manager at Reckitt Benckiser Healthcare Australia Pty Limited from 2004 to 2006.

Brand Manager at PepsiCo Australia and New Zealand from 2006 to 2008 and Senior Brand Manager from 2008 to 2010.

Group Marketing Manager at Yum from 2010 to 2012.

31 Mr Sinha was the National Operations Manager of Yum from January 2014 until 15 July 2015.

32 Mr Sinha had extensive work experience before joining the Yum system, including:

From 1994 to 1995, he was a Hotel Operations Management Trainee at the Taj Mahal Hotel in Mumbai, India.

From 1995 to 1996, he was the Managing Partner of Zodiac – Multicuisine Restaurant in India.

From 1996 to 1998, he was the Executive of Hotel Services at Eurest Radhakrishna Hospitality Services Pvt. Ltd in India.

From 1998 to 2000, Mr Sinha was a District Manager of Domino’s Pizza India.

33 Mr Sinha first worked in the Pizza Hut system in India in 2000 as the Restaurant General Manager for Favorite Food India (which was a subsidiary of Wybridge, the Master Franchisor for Pizza Hut in Indonesia), where he opened and managed Pizza Hut stores in Mumbai. In that capacity, Mr Sinha had personal experience in making, and supervising the making, of pizzas in a Pizza Hut store. Since 2000, Mr Sinha has had many roles associated with the Pizza Hut business. These include:

In 2002, Mr Sinha was the Area Coach in Wellington for RBNZ, in which he managed the operation of the Pizza Hut Stores. He stayed at RBNZ until 2006.

From 2006 to 2009, he had the position of Franchise Business Coach and EDI Operations Leader for Yum Restaurants International in India.

From 2009-2011, Mr Sinha was the Area Manager of Southern Restaurants Pty Ltd in Melbourne, Victoria.

In 2011, Mr Sinha became the Pizza Hut State Operations manager for New South Wales with Yum.

34 In January 2014, Mr Sinha was promoted to National Operations Manager. Each State Operations Managers reported directly to Mr Sinha and the operations team was responsible for maintaining operational standards across all Pizza Hut stores in Australia. Mr Sinha reported directly to Mr Smith. Mr Sinha had the overall responsibility for all operational matters that impacted customers, including such matters as food preparation, food and operational safety and customer service.

35 Mr Smith is the Senior Director of Development in the Pizza Hut USA business and has held that position since January 2015. At the time of the hearing before Jagot J, Mr Smith was employed as a Market Director by Yum and held this position since January 2014. The role required him to oversee day-to-day operations at Pizza Hut Australia and he reported to Mr Houston.

36 Mr Smith was awarded a Bachelor of Science in Business Administration, majoring in Accounting, from the University of Richmond, in Virginia in the USA, in 2002. Further, in 2007, he was awarded a Masters of Business Administration from the University of Chicago – Booth School of Business.

37 Mr Smith’s professional background is, as follows:

From 2002 until 2005, Mr Smith worked as an Associate at Deloitte.

From 2006 to 2009, he was a consultant at Bain & Company.

From December 2009 until October 2010, he was the Senior Manager, Strategy, at Hewlett Packard.

Between October 2010 and July 2013, Mr Smith was employed by Yum! Restaurants International in which he held a range of positions including Manager, Strategic Planning (from October 2010 to June 2011), Senior Manager, Strategic Planning (from June 2011 to December 2011) and Director Financial and Capital Planning (from January 2012 to July 2013).

38 Mr Smith joined Yum in July 2013 as the Head of Operations, Pizza Hut SOPAC.

39 Mr Potter qualified as a Chartered Accountant in 1990. He is now the principal of Axiom Forensics Pty Limited. Mr Potter’s relevant experience to this matter is, as follows:

He was a trainee accountant in Perth for two years, before obtaining a Bachelor of Commerce at the University of Western Australia.

He was a graduate accountant in Perth for three years and worked as a Chartered Accountant in Perth and Sydney for 24 years. Mr Potter’s experience in that time included 13 years in insolvency and reconstruction accountancy specialisation and 16 years in forensic accounting, which has included investigations for regulators on issues including valuation, valuation disputes and competition related disputes, pricing decisions and/or valuation matters, damages assessments and consulting assignments.

40 Mr Gower is a Chartered Accountant and has been a director of GoweJones & Co Pty Limited since 2009. Mr Gower’s professional background is, as follows:

Between 1977 and 1982, Mr Gower was employed by Arthur Young in South Africa and Australia.

In 1982, Mr Gower joined Duesbury’s (a predecessor firm of Deloitte Touche Tohmatsu).

From 1987 to 1993, Mr Gower was a Partner off Duesbury’s and from 1993 to 1998 he was a Partner of Deloitte Touche Tohmatsu.

Between 1998 and 2003, Mr Gower was a sole practitioner at GCA Gower & Co and he became a director of GCA Gower & Co from 2003 until 2009.

41 Mr Gower has provided accounting support across a range of areas, including:

Analysis of the fairness of the acquisition considerations to be paid.

Valuation of businesses.

Due diligence investigations.

General financial analysis and advice in respect of the preparation of forecasts, feasibility studies and evaluation of the benefits of transactions.

Litigation engagements, involving providing evidence in respect of accounting matters generally and quantification of economic loss.

5. FACTUAL BACKGROUND AND SUBMISSIONS ON THE FACTS

42 DPL has analysed Yum’s closing submissions by subsequently providing a comprehensive table of responses to various of those submissions, and Yum has responded to these comments. Nonetheless, this section will summarise facts asserted and, where appropriate, the parties’ submissions as to the facts as presented prior to the table being provided by DPL. I will then turn to my consideration of the facts asserted and submissions advanced by the parties, taking the table, with Yum’s responses, into account as relevant.

43 DPL provided a useful table that compared headline prices for Pizza Hut and Domino’s before the VS and at 1 July 2014 when the VS was implemented. Relevantly to the calculation of loss and damage, the analysis is of the prices of Pizza Hut pizzas before the VS, the prices due to the implementation of the VS and the prices of pizzas during the period of loss. Accordingly, the prices of the ranges of Pizza Hut pizzas, with a delivery fee of $8.00, before the VS were:

DELIVERY | PICK UP | ||

Range of pizza | Price | Range of pizza | Price |

Mia (6 pizzas in range) | $5.00 | Mia (6 pizzas in range) | $5.00 |

Classics (6 pizzas in range) | $9.95 | Classics (6 pizzas in range) | $9.95 |

Legends (8 pizzas in range) | $11.95 | Legends (8 pizzas in range) | $11.95 |

Signature (7 pizzas in range) | $14.95 | Signature (7 pizzas in range) | $14.95 |

44 As at 1 July 2014, the date of the implementation of the VS, the delivery price was increased to $8.95, the Legends range was changed to Favourites (with the number of pizzas increasing from 8 to 11 in the range) and the Mia and Signature ranges were removed. The prices of the ranges of Pizza Hut pizzas as at 1 July 2014 were:

DELIVERY | PICK UP | ||

Range of pizza | Price | Range of pizza | Price |

Mia (6 pizzas in range) | Deleted | Mia (6 pizzas in range) | Deleted |

Classics (6 pizzas in range) | $4.95 | Classics (6 pizzas in range) | $4.95 |

Favourites (11 pizzas in range) | $8.50 | Favourites (11 pizzas in range) | $8.50 |

Signature (7 pizzas in range) | Deleted | Signature (7 pizzas in range) | Deleted |

45 Yum says that major price adjustments were made to the ranges of pizzas following the implementation of the VS. Yum relies on Ms Syed’s affidavit dated 13 July 2015, which is relevantly summarised as follows:

On 14 August 2014, Yum increased the delivered price for the Classics range from $4.95 to $8.95, increased the delivered price for the Favourites range from $8.50 to $11.95 and the delivery fee was decreased from $8.95 to $4.95.

On 30 September 2014, Yum increased the delivered price for the Classics range from $8.95 to $9.95.

On 2 December 2014, Yum increased the pick up price for the Favourites range from $8.50 to $10.95. A new tier of pizza range was also introduced, which was called the Loaded Classics range. The price for this range was $7.95 and the delivered price was $10.95.

On 22 December 2014, Yum increased the fixed delivery fee from $4.95 to $7.95.

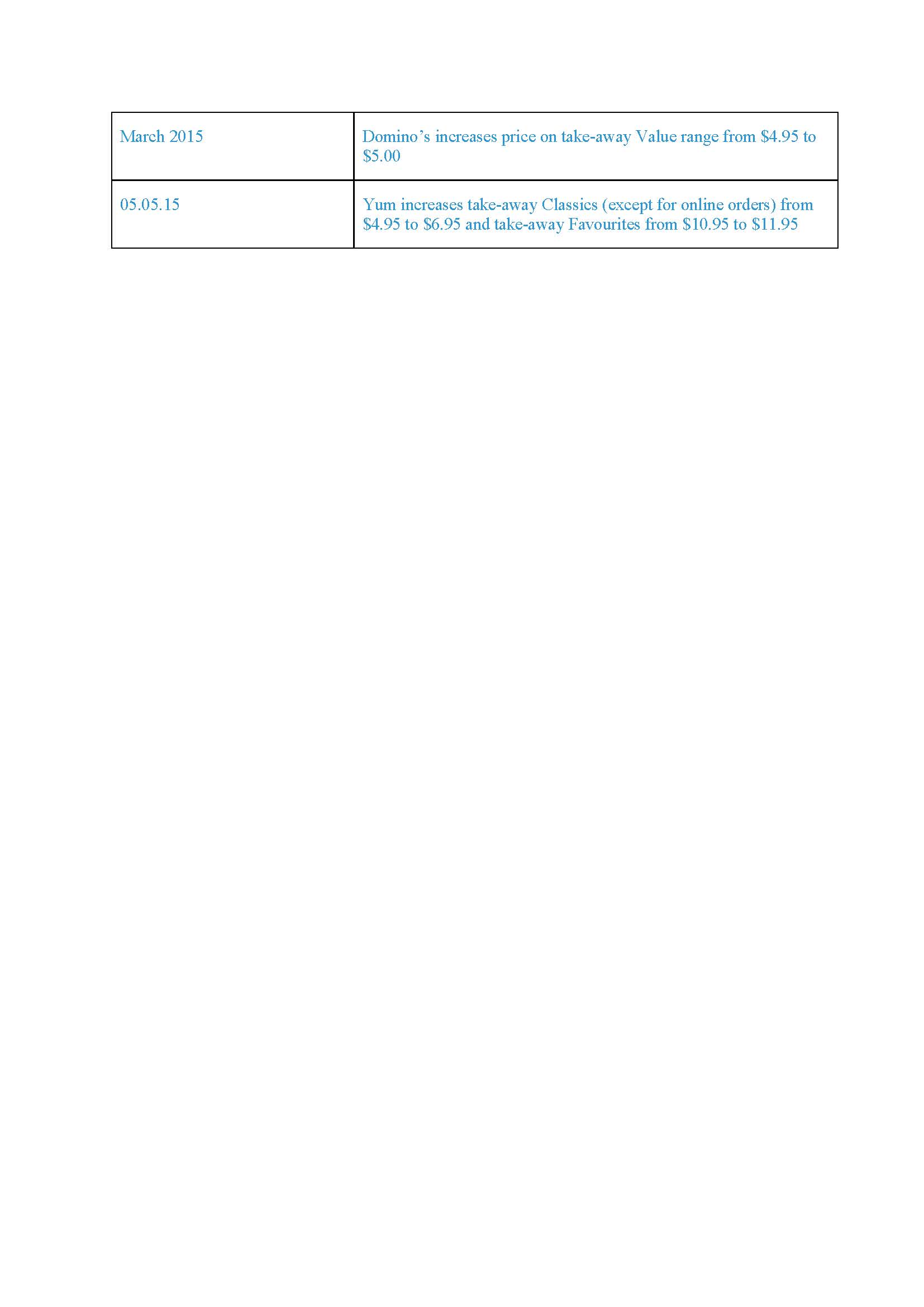

On 5 May 2015, Yum increased the pick up price for the Classics range from $4.95 to $6.95 (except on its website), increased the pick up price for the Loaded Classics range from $7.95 to $9.95 and increased the pick up price the Favourites range from $10.95 to $11.95.

5.2 Characterisation of the VS

46 DPL describes its characterisation of the VS in [13] of the ASC, which is as follows:

On 10 June 2014, Yum advised the Applicant and the other Franchisees (Advice), that:

(a) On an from 1 July 2014, it was reducing the maximum prices that could be charged for pizzas sold at Pizza Hut Outlets for takeaway and delivery to two price points (Reduced Prices):

(i) “Classics” pizzas at $4.95 (including GST) – being a reduction of approximately 50% from the preceding price of $9.95; and

(ii) “Legends” pizzas at $8.50 (including GST) – being a reduction of approximately 29% from the preceding price of $11.95.

(b) On and from 1 July 2014, Yum was reducing the range of Approved Products to be sold at Pizza Huts to the “Classics” and “Legends” ranges of pizzas (removing the “Signature” and “Pizza MIA” ranges of pizzas);

(c) Yum had made its decision to implement the Reduced Prices in (a), the change in the range of Approved Products in (b) and certain other changes, including changes to delivery prices (Reduced Price Strategy) on the basis of trials of a reduced price strategy at Pizza Hut Outlets in the ACT and experience in New Zealand, which it asserted had provided evidence of a significant increase in sales revenue in those markets in response to those trials;

(d) On an from 1 July 2014, Yum would initiate a public marketing campaign of the new Pizza Hut prices as being for a limited time only, for the purpose of achieving a spike in sales, when it was not Yum’s intention that the prices be for a limited time only;

(e) The introduction of the Reduced Price Strategy would be accompanied by an advertising program lasting 1 month only with financial support from Yum’s US parent company;

(f) Yum would provide $1,000 per Outlet to each Pizza Hut franchisee in Australia by way of assistance to cover stock write offs arising from the deletion of the “Signature” pizza range;

(g) Yum would not otherwise provide any compensation to franchisees for any loss of profits they may incur in implementing the Reduced Price Strategy.

47 Paragraph 13 of the ASC refers to ‘Reduced Prices’ as providing the foundation of the VS. As described by DPL, the VS comprised four main elements:

the “Reduced Prices” – being the new price points for pizzas, which in fact became $4.95 for “Classics” and $8.50 for “Favourites” (previously called “Legends”);

a menu reduction to two ranges of pizzas, by eliminating the “Signature” range and the “Mia” range;

an advertising campaign to support the launch of the VS. A media booking authorisation form from Mediacom dated 20 May 2014 indicated approval for media spending of XXXX XXXXXXX; and

a provision of assistance to the Franchisees of $1,000 including GST per outlet in relation to the launch.

48 Yum criticises DPL’s characterisation of the VS as it contends that DPL seeks to confine the VS to only the elements enumerated in the ASC. Yum submits that it has always said that the VS was an integrated market strategy that contained many elements, ranging from menu design, to an aggressive and attention catching marketing campaign, to reducing and simplifying the price points at which products could be purchased. In particular, it was always intended by Yum, as part of the VS, that Yum would be first into the market with an everyday value proposition of full sized pizzas at $4.95 all day every day. Yum says that these elements are not acknowledged by DPL, as DPL has isolated one aspect of the strategy by naming it the ‘Reduced Price Strategy’ in [13] of the ASC. Accordingly, Yum submits that this terminology diminishes the significance of the remaining elements of the VS, in particular, being first to market with an all-day every day value proposition.

49 Yum used a test in the ACT to trial the VS before its implementation (the ACT Test). It was commenced on 4 February 2014 and concluded on 28 April 2014. The ACT franchisee, who owned all 8 outlets in the ACT market, implemented the VS during this period with the assistance of Yum. Yum agreed to underwrite any losses suffered by the ACT franchisee during the test period. As a result of the ACT Test, Yum paid the ACT franchisee the sum of $143,000 to make good his losses. The ACT franchisee continued to implement the VS after 28 April 2014 and Yum also paid him $51,000 to make good the losses in this period after the completion of the test.

50 The parties are not in dispute that Yum’s decision to test the VS in the ACT was appropriate. The test was appropriate for the following reasons:

Yum believed that there was a “value” problem in Australia and it wished to see whether adopting the New Zealand $4.90 strategy would increase sales, transactions and Franchisee profitability.

Conducting a trial of a strategy, such as the VS, was an appropriate action by a franchisor acting responsibly towards its franchisees, particularly where it had the cooperation and support of the participating franchisee and had agreed to indemnify him.

The ACT was an appropriate place to conduct such a test because it was a distinct media market with its own signal, there was a single franchisee who owned all 8 outlets in the market, the franchisee was one of the better performing franchisees and the low average current level of per store average (PSA) sales meant that there was significant room for improvement.

5.3.2 Mr Diab’s response to being informed of the ACT Test

51 DPL submits that Mr Diab’s response on being informed of the Act Test at the Adco meeting on 12 February 2014 was measured and appropriate, as he advised his franchisee colleagues in an email on 13 February 2014:

These tests are quite radical and have strong long term implications on our business, however we will assess the results carefully and decide whether this is the right thing for our businesses – if these tests are unsuccessful then we would have put the discount strategy fight to bed once and for all. I reiterate the Adco directors are currently opposed to these strategies, however have agreed to examine and scrutinise any results, at the end of the day it will require significant hard evidence to determine the viability or failure of either of these tests.

5.3.3 Profitability of the ACT franchisee

52 DPL contends that Yum asserted that profitability of the ACT franchisee improved during the ACT Test and that this was presented to the Franchisees on 14 and 15 May 2014 and repeated without qualification in the evidence presented before Jagot J during the Franchisees’ interlocutory application to prevent Yum from implementing the VS. Yum represented to the Franchisees, in a presentation on 14 May 2014 entitled “Franchisee Update May 2014” (the Franchisee Update), that there had been a $425 per week per store improvement ($425 improvement) in comparable profit in weeks 5 – 10 of the ACT Test. Yum submits that weeks 1 – 4 were not included in the presentation to the Franchisees on 14 May 2014 because the results in that period were not in a “steady state” and this issue was not challenged by DPL. Yum also submits that weeks 11 and 12 were not included because of the impact of the Easter and ANZAC Day holidays. At the time of the presentation, Ms Broad did not have profit and loss statements from the ACT franchisee; however, Ms Broad agreed that she did have sales information for that period but could not recall why same store sales growth (SSSG) was not presented. DPL contended that this calculation of the $425 improvement was ‘simply a product of financial engineering by Ms Broad that does not withstand reasonable scrutiny’. However, DPL did not establish that Ms Broad engaged in deliberate “engineering” of the results but did establish that the presentation to the Franchisees did not include relevant data, which may have affected the conclusions that could be drawn.

53 DPL submits that the true position, which was neither revealed to the Franchisees nor to Jagot J, was that the ACT franchisee incurred a loss during the test of approximately $140,000, for which it was compensated by Yum pursuant to the indemnity or “backstop” arrangement. Furthermore Yum had also agreed to pay the additional $51,000 to the ACT franchisee for its post-test losses on the basis that it maintained the VS prices following the conclusion of the test.

54 DPL submits, relying on the Franchisee Update, that there were two elements that comprised the calculation of the alleged $425 improvement:

(1) An alleged post-launch profit for weeks 5 – 10 of $155 per week per store; and

(2) A prior year loss of $270 per week per store.

5.3.3.1 Alleged post-launch profit

55 Ms Broad concedes that the $155 per week per store figure was taken from the adjusted profit and loss figures for weeks 5 – 9 (in Exhibit AO) not weeks 5 – 10 as stated in the above presentation document. In cross-examination, Ms Broad, stated that the calculation of $155 was only until week 9 and then Yum ‘double-checked to see if week 10 made a difference to that number’. DPL contends that Ms Broad invented this answer in the witness box to ‘attempt to cover up this relatively trivial slip’.

56 Nonetheless, the figure of $155 per week per store was calculated using 1.5% of sales for local store marketing (LSM) costs. DPL argues that Ms Broad arrived at this figure by “stripping out” LSM costs in excess of 1.5% and that this approach was not according to normal accounting practices of “matching” expenses and revenues. DPL analysed the full 12 week profit and loss for the ACT franchisee who incurred a 1.8% charge for ‘Local Store Marketing – Leaflet’ costs and a 4% charge for ‘Additional LSM’. On this basis, the ACT franchisee incurred costs equating to 5.8% of sales during the ACT test which were as a result of LSM.

57 Ms Broad explained that the 4% additional LSM was not actually spent by the ACT franchisee on LSM but was paid by it to Yum as a contribution to the overall marketing budget for the ACT Test. Nonetheless, DPL contends that Yum failed to account for all marketing expenses when determining net profit and arbitrarily cut off the expenses at 1.5% of sales rather than accounting for the 5.8% in total marketing expenses. It follows, DPL says, that if Yum had taken the full cost into account, the amount of extra cost would have been at least three times the amount calculated for LSM expenses in the Franchise Update, and an overall loss would have been calculated. Ms Broad did not object to this proposition if DPL’s calculation was correct and if it was appropriate to take the additional LSM into account.

58 Yum acknowledges that the ACT franchisee did provide 4% additional LSM. However, it contests the argument that the 4% should have been taken into account when analysing whether the ACT Test was profitable. Ms Broad said that she was ‘trying to get an understanding of what would happen to the [profit and loss] of a store if we launched the pricing strategy nationally’ and that the 4% additional LSM was required to replicate the marketing budget that would be used nationally. Yum submits that the “matching principle” was not appropriate in the circumstances because Ms Broad was analysing the impact on profitability that the VS would have upon a national rollout and the 4% Additional LSM would not be replicated on a national level. That is, the expense would not be incurred by the Franchisees on a national level, as the Franchisees’ contribution to the overall marketing budget would be what they currently paid.

59 Ms Broad acknowledged that the prior year loss of $270 per week per store presented to the Franchisees in the Franchisee Update did not reflect her own estimate for period 3 of 2013 which she calculated as a loss of $257 per week per store. DPL suggests that the most likely explanation for the $270 per week per store figure is that it was based upon an average of the ACT franchisee data from period 5 to period 11 in 2013, which showed an average weekly loss per store of $273. DPL contends that this figure included a deduction for head office costs which, if removed, would have resulted in a profit of $239 per week per store for the ACT franchisee in 2013. That is, if this profit figure were used, there would have been a loss of approximately $980 per week per store, comparing 2013 and weeks 5 – 9 of the ACT Test.

5.3.3.3 DPL’s conclusion on the presentation of the ACT Test during the Franchisee Update presentation

60 DPL concludes that Yum actively engaged in a “public relations exercise” by presenting manipulated data to the Franchisees, which presented a false picture of the profitability of the ACT Test. Further, DPL contends that even if Yum did not have the full 12 weeks of data at the date of the presentations to the Franchisees on 14 and 15 May 2014, it certainly did have data at the time of the interlocutory hearing before Jagot J and it failed to make any qualification or explanation to the Franchisees or to the Court. It follows, DPL says, that Yum was in breach of its implied obligations to act reasonably and cooperatively in relation to the exercise of its power to set maximum prices under clause C1 of the IFA, because the true result of the ACT Test was that the VS prices caused the ACT franchisee to make a loss and thus Yum had no justification for reducing the price points for the Franchisees by application of the VS.

61 DPL contends that Yum presented misleading sales results in the Franchisee Update, as it compared an SSSG of -5%, from the 12 weeks before the ACT Test to a range of increases in sales during the ACT Test, ranging from 14% to 48%. DPL argues that the presentation of SSSG in the Franchisee Update was misleading for the following reasons, as put to Ms Broad:

The prior 12 week period was never a valid comparison, as it included Christmas and the January holidays, which as times when Canberra sales are traditionally low due to Parliament not sitting, school holidays and the public service shuts down. The trend is clear when one assesses the decline in PSA sales in the past two years over this period.

The 48% increase in Week 6 reflected an abnormal dip in the prior year, which was associated with the transition period prior to the ACT franchisee taking over control of all the ACT outlets.

Weeks 7 and 8 in 2014 were inflated due to the misalignment of Easter dates between the two years. That is, in 2014 Parliament was sitting in both of those weeks, whereas in the prior year Parliament sat for only one of those weeks as the other was during Easter.

62 Yum challenges DPL’s criticism that the prior 12 week period was never a valid comparator. Yum relies on Ms Broad’s explanation that the 12 week period before the ACT Test was used because:

Ms Broad had the profit and loss statements for that period and the data were better, relying on assumed data.

Ms Broad did not regard a failure to adjust for Christmas as a serious failure.

Mr Houston believed that it was the only rational period to use and did not see anything that was not representative of the business, even though Christmas fell in the period.

63 Following the ACT Test, the ACT franchisee continued to implement the VS with Yum’s consent. The ACT franchisee experienced poor sales results after week 12 of the ACT Test. Yum attributed this to Yum ceasing advertising and the fact that Domino’s was not advertising on television. DPL contends that this assertion cannot be sustained in light of the Nielsen reports, which show that there was continued advertising by Yum and Domino’s following week 12 of the ACT Test.

5.3.5 Replication of the ACT Test

64 DPL contends that to the extent that there were any positive results generated by the ACT Test, they were not replicable because of the amount of money that was spent by Yum on advertising to generate those profits. DPL argues that, as Yum knew as at 14 May 2014 when the Franchisees briefings commenced, the only conclusion to be drawn from the sales results in the ACT was that extensive advertising could increase sales significantly in the absence of any response by Domino’s. Pizza Hut outspent Domino’s by 2:1 on media spending during the ACT Test, which contrasted the usual spending ratio, where Domino’s outspent Pizza Hut by 2:1. DPL says that there was simply no basis for Yum to have formed the conclusion as at that date, with all of the data which were then available, that the ACT test had been a success in terms of sales. By 10 June 2014, when the VS was announced to the Franchisees, the situation in the ACT was worse, and the negative trend was continuing as at 24 June 2014 when an interlocutory hearing took place before Jagot J.

65 Yum strongly denies DPL’s assertion that Yum’s large advertising budget during the ACT Test meant that the results were not replicable. Yum relies on Ms Syed’s evidence. Ms Syed stated that she believed that ‘[t]he plan could be replicated nationally’ even though additional funds may be required ‘to support the launch’.

66 DPL’s theory was that the expenditure on marketing for the ACT stores must be calculated and then that figure multiplied by stores nationally. Ms Syed rejected this theory as she said that media is replicated based on ‘reach and frequency as opposed to looking at a dollar amount and working from there’ and Yum contends that there is no evidence to support the theory that Yum did not believe that the strategy could be replicable nationally. Further, Yum submits, Mr Houston stated that “replicate” meant achieve the media outcome achieved in the ACT, not the dollars actually spent. That is, focusing on the actual dollars spent was not the correct approach in assessing whether the ACT Test could be replicated. The VS as formulated included provision for an increased national marketing budget. This was not available upon implementation as planned, as it required not only Adco approval but also extra contribution from the Franchisees, which were not forthcoming.

67 On 8 March 2014, during week 5 of the ACT Test, Ms Broad sent an email to Mr Smith, Mr Houston and Mr Sinha providing her opinion as to the success of the ACT Test. Ms Broad stated the following opinion, based on three weeks profit and loss data:

My opinion at this stage is that the test was well worth doing and the marketing team should be congratulated – the sales growth and transaction growth we have achieved in this test have proven beyond doubt that velocity pricing is the path we need to head down. … Having said that, from a profitability stand point, I believe it’s marginal – this is one of our best Franchisee groups and I don’t believe they are making the same amount of money they were previously – it’s borderline at best at this stage.

…

From my perspective, looking at these numbers, our underlying business model doesn’t support velocity pricing… and I believe we should stop the test at the end of week 6…

68 DPL concludes that Ms Broad’s statement was vindicated by the national rollout of the VS, as the sales data after its inception show a negative downward trend, which is very similar to the negative downward trend in PSA sales for the ACT from the time of Domino’s intervention in the ACT. It follows, DPL says, that Ms Broad’s conclusion ‘was and ought to have been obvious to any reasonable and fair minded observer conscious of Yum’s duties to act reasonably and cooperatively under the [IFAs]’.

69 Yum argues that DPL’s reliance on Ms Broad’s email is misplaced for the following reasons:

Ms Broad’s view was based only on three weeks’ profit and loss. Profitability did not improve until the fifth week of the ACT Test.

Data for the first four weeks of the ACT Test were not representative, as a steady state had not been reached. Yum argues that a steady state was reached in weeks 5 – 10 of the ACT Test.

Ms Broad made it clear in her affidavit evidence that subsequent results of the ACT Test allayed her concerns about the VS.

Ms Broad acknowledged that after 3 weeks it was only a profitability point that prevented her from supporting the implementation of the VS.

70 DPL submits that Yum cannot escape a finding of breach of the implied duties of reasonableness and cooperation, on the basis of selective information and manipulated data, by turning a clear and catastrophic loss result produced under otherwise ideal conditions in the ACT into evidence which was sufficient to justify the imposition of the VS upon DPL and all other Franchisees.

71 Prior to 10 June 2014 and after the ACT Test, Yum prepared a model for deciding whether to implement the VS (Yum Model). Mr Houston stated that Ms Broad was responsible for the Yum Model and that Mr Smith’s role was to ‘validate and refine it’.

5.4.1 Operation of the Yum Model

72 In its written submissions, Yum describes the Yum Model’s operation, as to which Yum’s witnesses gave evidence:

242. Firstly, the Yum Model is an Excel model. The model itself is an electronic Excel document, not a paper document. It is comprised of various pieces of data and assumptions contained in different cells on different worksheets. Various cells are linked to other cells (often on different worksheets) by means of formulas which also form part of the model. It is the data, assumptions and formulas, as embodied in the electronic document, which constitute the Yum Model.

243. The Yum model contains numerous input cells, into which different inputs could be placed. In some cases, if an input is changed in one input cell it automatically changes the inputs in certain other cells. For example, upon selecting a particular store in the store selector drop-down box, the “Store Profile” inputs (such as the average value of sales, number of transactions, and so on) automatically update. In other cases, each input cell needs to be altered manually. The input cells which require manual alteration are shaded yellow in the Yum Model.

244. The Yum model operates by applying the chosen inputs to the existing data, assumptions and formulas to produce certain outputs. Every time that an input or multiple inputs are changed, the outputs are recalculated by the model.

245. Once the Yum Model was created, it was used in an iterative process. That is, over the period in late May and early June 2014, on numerous occasions Mr Sinha and Mr Purcell altered various inputs in order to see what outputs would result. Their ultimate goal was to determine what level of transaction uplift or increase would be required, following the introduction of the Value Strategy, in order for the National Average store to maintain the same EBITDA level as it had before the introduction of the Value Strategy.

246. Every time a “version” of the Yum Model was saved, emailed or printed out, what was saved, emailed or printed included the particular set of inputs and the resultant outputs in the model at that particular time. The model itself, however, continued to exist in electronic form.

73 Yum also commented in its submissions on different versions of the Yum Model in evidence:

247. [DPL] has put into evidence 5 emails from Mr Purcell, at different points in time, which attach a particular “version” of the model – i.e. containing particular inputs and outputs. This is only evidence that Mr Purcell had placed particular inputs into the model, resulting in particular outputs, at a particular point in time and had reason to email the results, either to Mr Sinha (Ex[hibits] V, W and X) or to Yum’s LT (Ex[hibits] G and H).

74 DPL contends that it put into evidence every version of the model that was discovered by Yum, so that Yum’s statement that there were “only” 5 emails is an unfair characterisation.

5.4.2 Purpose of the Yum Model

75 DPL describes the purpose of the Yum Model and its contents in [13C] – [13F] of the ASC, as follows:

13C. The Yum Model:

(a) Was constructed by Yum as a model of the profitability at a store EBITDA level for each Pizza Hut Outlet in Australia;

(b) Included 52 weeks of data available to Yum from its Micros system in relation to sale and transactions at each Pizza Hut Outlet in Australia;

(c) Calculated sales and transactions for a “National Average” Outlet in relation to sales and transactions at all Pizza Hut Outlets in Australia from its Micros system;

(d) Included a calculation of the weekly “National Average” store level EBITDA for the 52 week period covered by the data referred to in (b) above;

(e) Included a model for calculating the cost of labour by reference to the different types of labour used in an Outlet, including the number of hours and pay rates for management and crew members (Labour Model);

(f) Included a provision for comparing current levels of Outlet performance with future levels of Outlet performance and for the “National Average”, based on different assumptions, designated as “Now” and “Future”, including in relation:

(i) The elements used to determine the sales revenue, and in particular sale price, transaction composition in terms of pizzas per order and sides per order, transaction mix and delivery mix;

(ii) The elements comprising the Labour Model, and in particular the number of hours and pay rates for management and crew members, and a rate for driver costs per day of the week.

13D. On the basis of the Yum Model, and prior to providing the Advice to the Applicant and the other Franchisees on 10 June 2014, Yum determined that the “break even” increase in transactions for the “National Average” Outlet upon the assumptions made in the Yum Model was 34.5% (Break Even Transaction Level).

…

13F. The Break Even Transaction Level for the “National Average” in the Yum Model was based on the following assumptions in relation to the effect of the Reduced Prices and/or Reduced Price Strategy:

(a) There would be an increase of 218 transactions per week;

(b) Thirteen (13) additional labour hours for crew members would be required to produce the additional 218 transactions per week;

76 Yum characterises the Yum Model somewhat differently. Yum’s characterisation of the purpose of the Yum Model is that ‘it was in essence a “break even” model’. That is, Yum used the Yum Model to ascertain the level of increase in transactions required for the national average store to retain the same EBITDA level of profitability after the introduction of the VS as it had before the VS. Yum says that the Yum Model relied on data derived from Yum’s records about the operation of the notional national average store for the 12 months from May 2013 to May 2014 and assumptions about the likely impact of the VS derived largely from the experience during the ACT Test.

77 Through an iterative process of entering various inputs, Yum relied on the conclusion based on the Yum Model that transactions would need to increase by approximately 34.5% for the national average store to “break even”. This was an increase of 218 transactions per week (from 635 transactions to 853 transactions per week). Yum submits that this result was one of the factors which it considered in deciding whether to proceed with the VS. Yum points out what the Yum Model was not used for, including:

Yum did not attempt to predict what would happen if the VS was implemented. For example, the Yum Model did not predict what increase in transactions or profits would result from implementing the VS. Its purpose was to predict what increase in transactions would be required for profit levels to remain the same and to assist in evaluating the likelihood of whether there would be an increase in transactions sufficient to maintain or increase profits by reference to other matters.

The Yum Model was not a pricing model. Yum contends that the Yum Model did not attempt to calculate what prices should be charged for pizzas (or any other products) under the VS and that the decision concerning prices was determined independently of the Yum Model. That is, the Yum Model simply applied the prices which were provided as input into the model in order to do the “break even” calculations.

5.4.3 Usefulness of the Yum Model

78 DPL does not criticise all aspects of the Yum Model, as DPL states that it was ‘a very useful EBITDA model for Australian Pizza Hut outlets, and was capable of being [sic] to evaluate the impact of the VS upon those outlets through the consideration of the “national average” outlet’. To this extent, DPL says, it accepts Ms Broad’s evidence that ‘[m]odelling a store on a national average basis is a standard financial average technique used in the business’.

79 DPL accepts all of Yum’s inputs into the 34.5% Yum Model other than the input for “variable labour”. Yum made an assumption in the Yum Model that an additional 13 hours of variable labour would be required to process the additional 218 transactions that would occur if there was a 34.5% increase in transactions. That is, the 34.5% was the “output” of the Yum Model designed to identify the break-even point of the Franchisees’ profitability.

80 DPL and Yum have used different rates to determine variable labour: DPL relies on “dockets per hour”, whereas Yum relies on “minutes per docket” (MPD). Mr Sinha’s described MPD as follows:

The MPD value is derived by dividing the total amount of variable labour employed (expressed in minutes) by the number of transactions. The higher the MPD figure, the less efficient the labour is.

(emphasis added)

5.4.4 Assumption of 13 additional labour hours

81 Mr Sinha placed the additional 13 hours of variable labour assumption into the Yum Model. Yum summarised how Mr Sinha derived his assumption as follows:

Mr Sinha first calculated the minimum number of weekly labour hours which would be required to staff a Pizza Hut outlet, given Yum’s rules about minimum staffing levels. This was 97 hours of management, 70 hours of team member time and 40 hours of delivery drivers who also assist in the store. That is, the total was 207 hours. Mr Sinha formed the view that these hours were more than sufficient to service the pre-VS transaction level of 635 transactions per week. Mr Sinha gave evidence that 70 team member hours when divided by 635 transactions, gives an MPD of 6.6 and his reasoning was that it was less efficient than the New Zealand benchmark of 5.6 and the results achieved during the ACT Test. That is, Mr Sinha concluded that an MPD of 6.6 was reasonable and, therefore, that his estimates of 70 team member hours was also reasonable.

Mr Sinha then allocated the 218 additional transactions on a day-by-day basis during the week, maintaining the same relativities on a day-by-day basis as before the VS. This resulted in a different number of additional transactions for each day, ranging from 20 additional transactions on a Monday to 41 additional transactions on a Friday.

On the basis of Mr Sinha’s own experience of utilising labour in Pizza Hut outlets, he formed the view that the existing minimum labour hours would not be fully utilised before the VS. In other words, in Mr Sinha’s opinion the minimum 207 labour hours used before the VS was capable of producing more than 635 transactions per week.

Mr Sinha then assessed the quantity of additional transactions on each day. He formed the view that the existing level of labour was sufficient to cover the additional number of transactions on Mondays, Wednesdays, Thursdays and Sundays (which ranged from 20 to 28 additional transactions per day). He also formed the view that the additional number of transactions on Tuesdays, Fridays and Saturdays (which ranged from 37 to 41 additional transactions per day) would require additional labour and allocated additional hours on those days, totalling 13 additional hours for the week.

82 Mr Sinha calculated that an additional 13 team member hours resulted in an overall MPD of 5.84. Mr Sinha noted that MPD rates for the ACT stores during the ACT Test from week 4 of the ACT Test onwards were below 5.6. As the MPD of 5.84 was higher (and therefore less efficient) than both the New Zealand benchmark and the results in the ACT Test (from week 4 onwards), Mr Sinha was satisfied that his calculations of 13 additional labour hours was a reasonable one.

83 Mr Sinha was the internal Yum expert responsible for modelling labour hours and allocating the correct labour hours and Mr Houston and Ms Broad relied on his expertise in this area. Mr Sinha’s evidence is that Mr Travis Purcell had primary responsibility for the structure of the Yum Model and for entering data into the model and that Mr Sinha assisted in preparing some parts of the Yum Model, including preparing the labour cost figures.

5.4.5 Variable labour as a balancing item

84 DPL argues that Yum’s “break-even” position is that if ‘more than 13 hours of labour were required, [the F]ranchisees would lose money if there was a transaction uplift of 34.5%’. That is, if more than 13 hours of additional labour were required, the break-even transaction uplift would be greater than 34.5%.

85 DPL contends that Mr Sinha’s evidence in support of the 13 additional labour hours ought to be rejected for the following reasons:

Mr Sinha regarded an MPD of 5.6 as an appropriate “benchmark” for measuring labour efficiency during the ACT Test. This decision was based on an email that Mr Sinha received from Mr David Hill, the sole New Zealand franchisee, (dated 16 February 2014) about the New Zealand experience. DPL submits that the benchmark figure of 5.6 MPD was an ‘aspirational target’ and was a forecast rather than an actual result achieved by the various New Zealand outlets in question.

The actual MPD rate for those outlets, contained in the material sent to Mr Sinha, was 6.69. When Mr Sinha was asked why he relied on the benchmark rather than the underlying data, his response was: ‘[w]hen I got 5.6, I had an opportunity of testing it in ACT and that’s how I got confirmed that yes, that’s a reasonable benchmark… And when we started achieving [the benchmark], I didn’t really have any reason to go back to the New Zealand data because we were achieving better results in ACT’. DPL contends that ignoring the actual data was ‘an inexcusable misuse of the data’ and that Mr Sinha’s attempts to explain why the data were not used were unacceptable and should be rejected.

Even though the New Zealand data represented a limited sample of high volume stores in 2 weeks in Christchurch, Yum has not explained why it did not seek full data directly from RBNZ so that it had a comparable data set for the NZ outlets for the purpose of analysing the ACT Test or for use in the Yum Model. Yum argues that Mr Sinha did not assess whether particular stores in New Zealand met the benchmark as this was irrelevant to him; rather, he concentrated on the benchmark figure.

Extra deliveries were being made by drivers but were not being converted into labour hours and were ignored in determining the MPD rate from the ACT Test, which included only the actual team member hours. DPL contends that this produced MPD rates for all ACT outlets other than Erindale of less than 5.6, which resulted in Mr Sinha concluding that the ACT outlets had been more efficient in their labour usage than New Zealand.

The Court is entitled to find that the true position is that the ACT franchisee was using delivery drivers as proxy crew members, and paying them on the basis of $14 per hour, being the rate of 2 deliveries at a contract rate of $7 per delivery. If the extra deliveries in the ACT Test were accounted for on the basis of 2 extra deliveries being equivalent to 1 hour of team member labour, and additional team member labour were added to existing team member labour, the average MPD of the ACT Test was 8.70.

Mr Sinha said that the ACT franchisee was guaranteeing two deliveries to a driver per hour as a bare minimum and if the driver did not get the two deliveries, then the ACT franchisee would guarantee the money. DPL submits that the effect of this explanation is that the ACT franchisee was prepared to pay drivers to do nothing in its stores and, to the extent that they substituted for team members, Mr Sinha was not prepared to account for it in his calculations.

86 Yum argues that DPL’s proposition advanced in submissions that the labour records produced to the Court did not accurately reflect these extra hours, is false. (In the table of asserted inaccuracies served after the conclusion of the hearing, DPL says that it did not mean to state that the labour sheets were inaccurate but rather that there was an inconsistency in the hours recorded for the ACT franchisee stores in the labour sheets, in terms of how total labour was comprised or allocated. Yum says that this is irrelevant and (see [94]) that Mr Potter selected Erindale to the exclusion of other ACT stores for a specific reason and that this was not due to the extra delivery issue). DPL did not call any evidence to prove that the records were inaccurate; rather, it relied on Mr Potter’s assumption of inaccuracy based on an exhibit, Exhibit Y, where Mr Sinha said: ‘Most stores have drivers who can help out so it makes sense to put extra of those when either the Kitchenhand is new or is not available’. Mr Potter’s criticism relies on the view that the ACT labour records understate labour hours and Yum argues that Mr Potter has no expertise which would enable him to form any judgment on the appropriateness of the labour rate. Yum argues that the statement at its most ‘suggests that on limited occasions drivers were asked to help out. It says nothing about the accuracy of the labour records. It does not say that any entry in the records for the extra deliveries was a payment for work done as a kitchen hand’. Further, Mr Sinha gave evidence that Mr Singh (who worked for the ACT franchisee) confirmed that it was an exceptional occasion where ACT outlets were using additional driver hours as crew hours and if these drivers were working in stores, then they should have been converted to drivers who work in the store and are paid an hourly rate.

87 Yum rejects DPL’s criticism of Mr Sinha and DPL’s submission that Mr Sinha’s evidence was in effect developed only in cross-examination.

88 Yum criticises Mr Potter’s reliance on Exhibit Y as the foundation for his criticisms of the Yum Model. Exhibit Y is an email exchange between Mr Sinha and the ACT franchisee about the use of delivery drivers in the kitchen. As a result, Yum provided a lengthy explanation in its submissions of the email correspondence. The explanation is as follows:

(i) The cause of the email correspondence is Mr Sinha’s concern about the high number of extra deliveries (i.e. deliveries being paid for but not done) in the ACT stores – see email of 27.3.14, 8.04 pm.

(ii) Mr Sinha was concerned to know whether new leaflets would help increase delivery sales and thus reduce the extra delivery numbers – email of 28.3.14, 12.06 am. This directly corroborates Mr Sinha’s evidence of his understanding of extra deliveries as a minimum payment guarantee for delivery drivers. If it was a minimum payment guarantee, then increasing the number of delivery transactions would reduce the number of extra deliveries paid. If, however, extra deliveries constituted payment for drivers working as kitchen hands, then increasing the number of delivery transactions would not decrease the number of extra deliveries (and could well increase them if those extra delivery transactions had to be processed by drivers working as kitchen hands).

(iii) Mr Singh told Mr Sinha that the number of actual deliveries during the ACT Test was decreasing during non-peak times, which partly explains the increase in extra deliveries compared to before the ACT Test.

(iv) Mr Singh explained that, with respect to the Kingston store, he needed to have two delivery drivers engaged even though there were only three deliveries to be done, as one driver could not do those deliveries in the required time, but that also meant he ended up paying for extra deliveries – email of 28.3.14, 11:52 am. This is again consistent with extra deliveries being a minimum payment guarantee to drivers.

(v) Mr Singh stated to Mr Sinha that, when stores had drivers available to help out (i.e. when they were not doing deliveries) it made sense to utilise them as kitchen hands if a kitchen hand was new or not available – email of 28.3.14, 9:19am. Mr Sinha responded by asking Mr Singh to identify where the under-utilised drivers were working so that Mr Sinha could see if there was an opportunity to utilise them more effectively – email of 28.3.14, 11:29am. This was a request by Mr Singh to be allowed to use delivery drivers as a form of kitchen hand labour in certain limited circumstances, given the pressures he was under. It is not evidence that this was in fact a common practice.

(vi) Under cross-examination, Mr Sinha accepted that the use of drivers as kitchen hand labour may have been occurring occasionally in the ACT, but he was not aware of it being a regular practice, he instructed Mr Singh to make sure it was not happening and he was told by Mr Singh “That’s taken care of”.

89 DPL criticises Yum’s submission in (iii) above. It submits that Mr Sinha’s evidence that he was told delivery transactions were decreasing in the ACT as part of his “guaranteed delivery” explanation, is false. DPL contends that there is no evidence to corroborate Mr Sinha’s attempt to corroborate this hearsay evidence from Mr Singh. Yum disagrees with DPL’s analysis. It argues that Mr Singh’s response in various emails makes it clear that the reason for the increase in “extra deliveries” was the requirement to have sufficient drivers on hand always and to pay them, even when there were no deliveries. Further, Yum submits that it is incorrect that there is no other evidence to corroborate Mr Sinha’s evidence to the effect that decreasing deliveries were a reason for the increase in extra deliveries, as Yum says that Mr Sinha sent an email to the Yum leadership team stating that Mr Sinha would work with Mr Singh to minimise extra deliveries but that delivery sales had been sluggish in comparison to takeaway sales.

90 DPL contends that the “true position” is that variable labour was used as a balancing item in the Yum Model. DPL states that this is an explanation for variable labour being allocated across a range of values between 2.1 hours to 39 hours in the six versions of the Yum Model and why all other models, other than the final Yum Model, made no allocation of the variable labour across the different days of the week.

91 On 5 May 2014, Mr Russell Creedy of RBNZ sent Mr Houston an email that stated that the “secret” to the strategy is to maintain the labour hours despite the higher volumes and that in New Zealand they were able to prevent an increase in labour costs to meet the additional transactions. DPL noted that Mr Smith acknowledged the need to control labour costs and it argued that this reflected Mr Smith’s mindset about additional labour. DPL argues that this mindset would explain why variable labour was treated as a balancing item, as it would make the Yum Model look “reasonably credible”, rather than providing a genuine and reasonable estimate of the additional labour costs required to implement the VS.

92 On 28 May 2014, Mr Purcell sent an email to Mr Sinha stating that the ‘model is completed just to finish entering some semis and fixed costs but overall it is working’. Attached to this email was an Excel document containing the model and at that point the transaction growth percentage was at 60%. DPL submits that the Court is entitled to infer from this email that Yum knew that the true breakeven point for the VS was 60%, as Mr Purcell modelled, and that Yum’s own model showed that the failure of the VS was inevitable, irrespective of a reaction by Domino’s.

93 Yum relies on Mr Sinha’s labour calculations and his fundamental assumption that the minimum weekly labour hours to operate a Pizza Hut were capable of processing more than the 635 transactions of the national average store before the VS. That is, the existing labour hours had significant capacity to process some (but not all) of the additional transactions which would result from a 34.5% transaction increase, which means that as transactions increased, the labour efficiency (measured as the number of transactions processed for every hour of labour) would also increase. Yum contends that Mr Potter has effectively assumed that there is no spare capacity, meaning that labour efficiency rates would essentially stay the same, regardless of the level of transactions. Yum says that this is contrary to the ACT data that clearly show that as the overall number of transactions increased during the ACT Test, labour efficiency also increased.

5.4.5.1 Mr Potter’s calculation of variable labour

94 Mr Potter concluded, in his calculations, that the additional labour required by the Yum Model ought to be 52 hours rather than the 13 hours stipulated by Yum. DPL contends that Mr Potter’s calculation should be accepted over that of Yum’s because of the following evidence:

Labour data from the ACT Test from the store at Erindale in the ACT, which was the outlet least affected by the “extra delivery” issue. Mr Sinha conceded that the labour hour statistics for Erindale were more reflective of what should actually happen in a well-run store.

An analysis done by Mr Potter in relation to the actual New Zealand labour data, which showed that the actual New Zealand rate of MPD was substantially higher than the benchmark rate assumed by Mr Sinha (see [85] above).

A sensitivity and regression analysis done by Mr Potter in relation to ACT data, including the “extra deliveries”, that indicated that the labour costs experienced in the ACT test were substantially higher than those used in Mr Sinha’s assessment of an appropriate cost.

95 Mr Gower disagrees with Mr Potter’s calculations of the additional labour hours. DPL comments on Mr Gower’s basis of disagreement as follows, in summary:

Mr Gower argues that “extra deliveries” should be counted for the purpose of determining actual team member hours in the ACT Test. DPL contends that this is a false premise, as Mr Gower converted “extra deliveries” into team member hours when he should not have done so.

Mr Gower treats Erindale as an “outlier” because it has a different labour cost profile to the other ACT stores in terms of team member hours. DPL agrees that Erindale is different from other ACT outlets; however, DPL argues that it is only different because it has a more conventional approach to labour than the other ACT outlets in the ACT Test, and includes the least amount of “extra deliveries”. DPL concludes that Erindale is a good proxy for the national average outlet used in the Yum Model because the PSA sales for Erindale during the ACT Test fell within the “Now” and “Future” sales range of the national average outlet, and the average ticket price also fell within the ranges in the Yum Model.