FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Fast Access Finance Pty Ltd [2015] FCA 1055

IN THE FEDERAL COURT OF AUSTRALIA | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. the parties exchange submissions as to the proposed forms of order and file such submissions within 21 days; and

2. there be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 489 of 2013 |

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant |

AND: | FAST ACCESS FINANCE PTY LTD ACN 078 233 084 First Respondent FAST ACCESS FINANCE (BEENLEIGH) PTY LTD ACN 095 585 292 Second Respondent FAST ACCESS FINANCE (BURLEIGH HEADS) PTY LTD ACN 104 904 225 Third Respondent |

JUDGE: | DOWSETT J |

DATE: | 30 SEPTEMBER 2015 |

PLACE: | BRISBANE |

REASONS FOR JUDGMENT

THESE PROCEEDINGS

1 The applicant (“ASIC”) seeks declaratory and other relief pursuant to the National Consumer Credit Protection Act 2009 (Cth) (the “Credit Protection Act”) and the National Consumer Credit Protection (Transitional and Consequential Provisions) Act 2009 (Cth) (the “Transitional Act”). It seeks such relief against the first, second and third respondents (respectively “Fast Access Finance”, “FAF Beenleigh” and “FAF Burleigh Heads”). In its amended statement of claim ASIC refers to FAF Beenleigh and FAF Burleigh Heads as “FAF Licensees”. The precise relationship between Fast Access Finance on the one hand, and each of FAF Beenleigh and FAF Burleigh Heads on the other, is far from clear. Where appropriate I shall describe each of those companies as an “FAF entity”. I may also, from time to time, use the expression in referring to other identified or unidentified companies which are similarly connected to Fast Access Finance. Of the other FAF entities only FAF Beaudesert Pty Ltd (“FAF Beaudesert”) has any present relevance.

2 The factual allegations which lie at the heart of ASIC’s case appear at paras 6 – 10 of its amended statement of claim as follows:

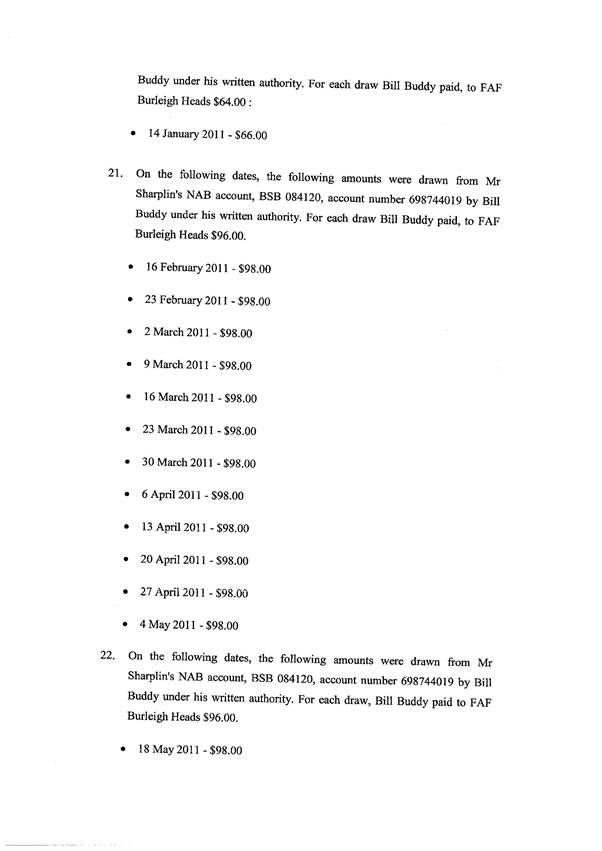

6. At all material times, [Fast Access Finance], with FAF Beenleigh and FAF Burleigh Heads … carried on business in accordance with a business model, key features of which were as follows (FAF Business Model):

a. prospective customers contacted [the relevant FAF entity] with a view to obtaining a small value loan;

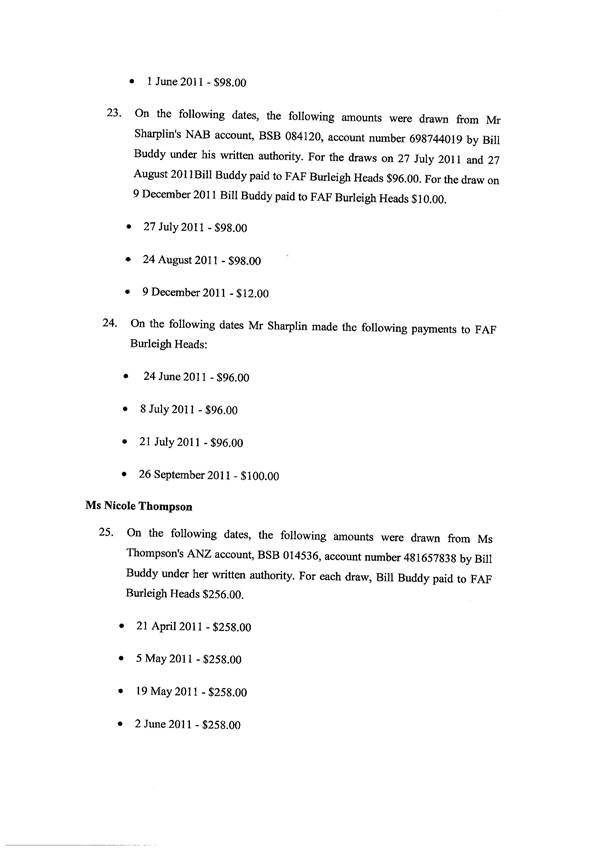

b. the [relevant FAF entity] arranged for the prospective customer to sign a purported contract with it, pursuant to which the customer purportedly purchased a number of diamonds from the [relevant FAF entity] for a fixed price of $250 per diamond (Sale Agreement);

c. the Sale Agreement included a term to the effect that the customer repay the amount of the total purported sale price of the diamonds by instalments to the [relevant FAF entity];

d. concurrently with the signing of the Sale Agreement, the [relevant FAF entity] arranged for the customer to sign a second purported contract, with DCH, pursuant to which the customer purportedly sold the same number of diamonds it had purchased from the [relevant FAF entity], to DCH for a fixed price of $125 per diamond (Purchase Agreement);

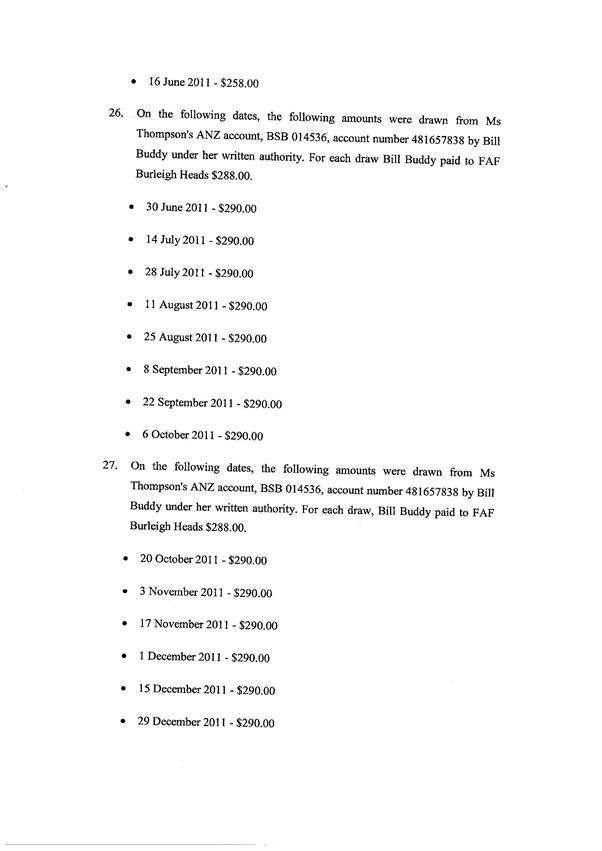

e. the customer then received, by payment into a bank account nominated by the customer, money equivalent to the total sale price of the diamonds purportedly sold to DCH pursuant to the Purchase Agreement;

f. there were never any diamonds the subject of the Sale Agreement and the Purchase Agreement, but rather the Sale Agreement and the Purchase Agreement were mere pretences to obfuscate an underlying loan transaction, and of no effect respectively as sale and purchase contracts for diamonds.

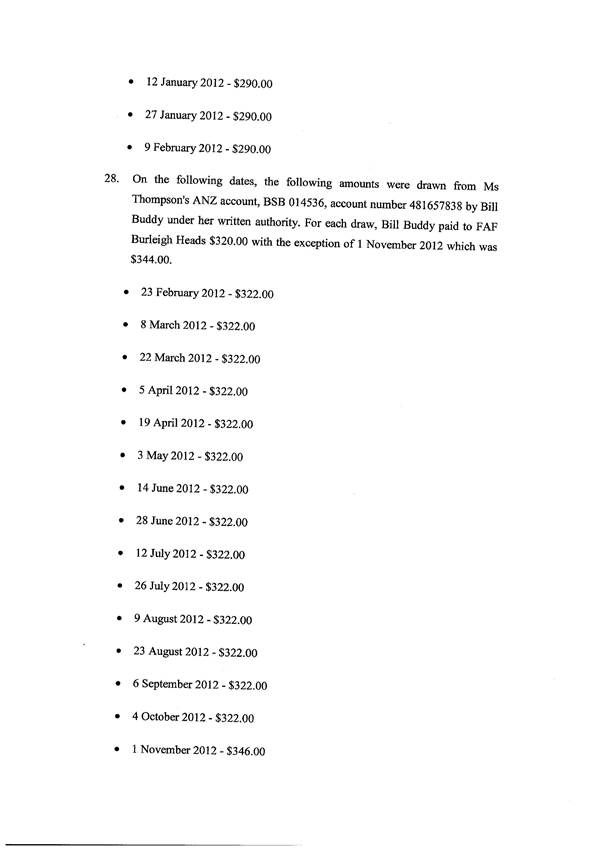

7. The practical effect for customers who entered into transactions in accordance with the Business Model was that:

a. the money received by them referred to at subparagraph 6.e above was the amount of the loan customers had sought from the [relevant FAF entity];

b. customers assumed an obligation to repay to the [relevant FAF entity] an amount equal to twice the amount received by them pursuant to the transaction.

8. [Fast Access Finance]:

a. devised the FAF Business Model;

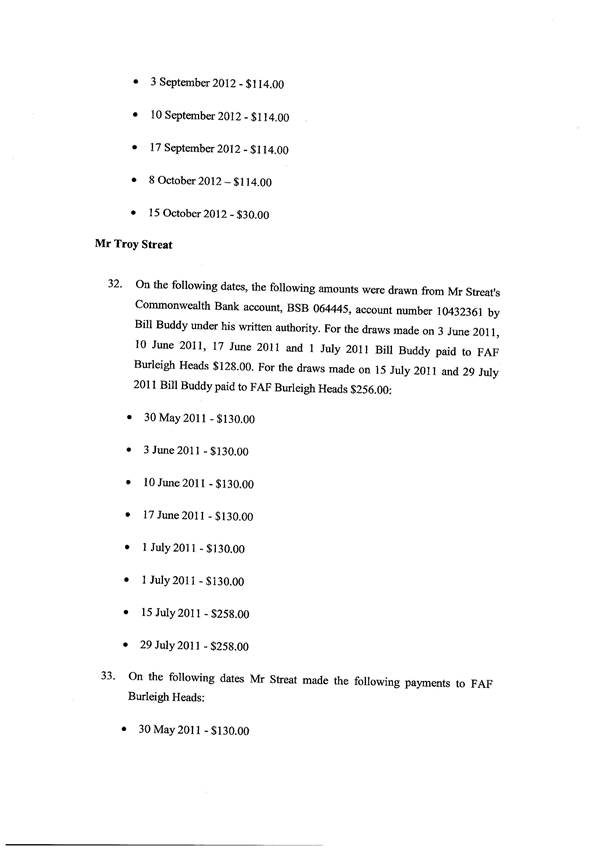

b. implemented the FAF Business Model;

c. maintained the FAF Business Model.

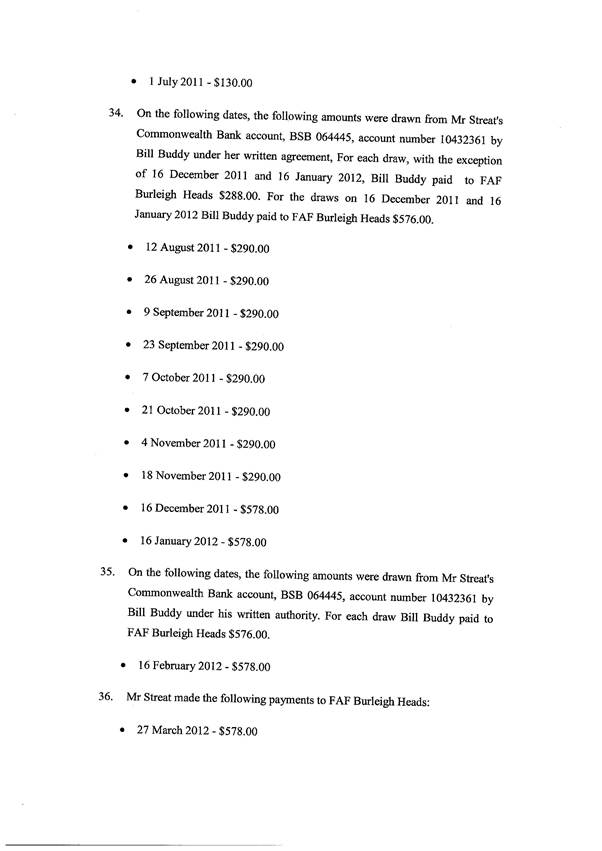

9. [Fast Access Finance] devised, implemented and maintained the FAF Business Model to circumvent:

a. the 48% annual percentage rate cap applicable to consumer credit contracts, instituted first by the Queensland government pursuant to s 3(1) of the Consumer Credit (Queensland) Special Provisions Regulation 2008, and subsequently maintained by s 32 of the Credit (Commonwealth Powers) Act 2010… ; and, or alternatively,

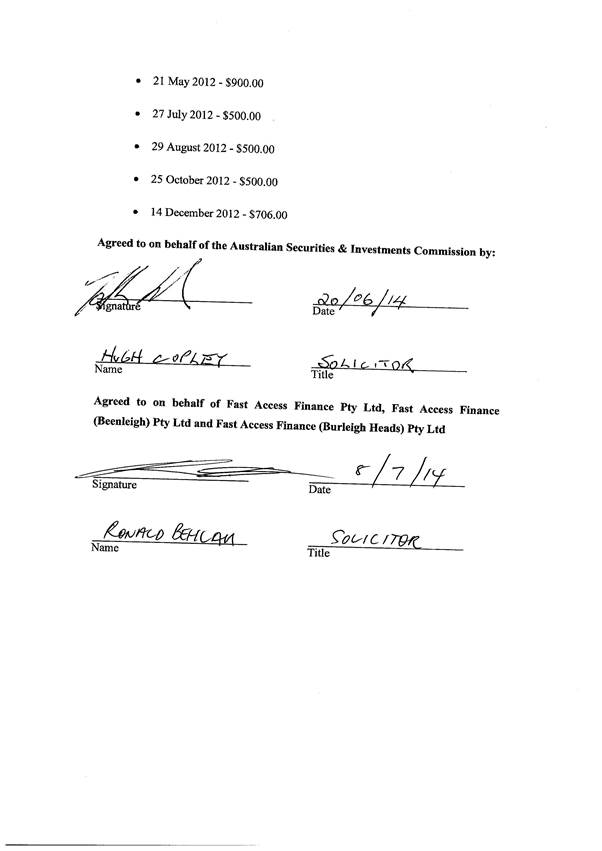

b. the provisions of the Consumer Credit (Queensland) Act 1994, the Transitional Act and the [Credit Protection Act].

10. At no time did [Fast Access Finance] direct, request or otherwise require either FAF Beenleigh or FAF Burleigh Heads to:

a. register to engage in a credit activity for the purposes of the Transitional Act;

b. apply for an ACL authorising FAF Beenleigh or FAF Burleigh Heads to engage in credit activity;

c. hold an ACL for the purposes of the [Credit Protection Act].

The document referred to as a “Sale Agreement” is actually headed “Sales Agreement”. I shall so refer to it. I shall use the term “Purchase Agreement” in the same way as it is used in the pleading. It may not be convenient to use the term “FAF Business Model”. I shall describe the relevant transactions as having being carried out pursuant to the “diamond model”. Those transactions involved other standard documentation to which I shall refer. The reference to “DCH” is to Diamond Clearing House Pty Ltd, which acronym I shall also adopt. In para 6 of the pleading ASIC pleads that the FAF Business Model (the diamond model) purportedly involved the sale and purchase of diamonds. In para 12 ASIC alleges that:

DCH was established at the instigation of Mr James Legat, a director of Fast Access Finance; and

DCH purported to purchase diamonds from customers of FAF entities and to sell diamonds to FAF entities.

3 The reference in the pleadings (and in these reasons) to “ACL” is to an Australian Credit Licence.

4 In para 11 of the pleading ASIC sets out the circumstances upon which it relies in order to demonstrate the relevant relationship between Fast Access Finance and each of FAF Beenleigh and FAF Burleigh Heads. At paras 12 – 13, ASIC pleads facts said to demonstrate that, as pleaded at para 14, “DCH acted as a mere conduit”, for the transfer of money between each of those entities and its customers. At paras 15 – 211, ASIC pleads that FAF Beenleigh entered into one relevant transaction with Mr Eadie and two with Ms Jones, and that FAF Burleigh Heads entered into:

four such transactions with Mr Sharplin;

four such transactions with Ms Thompson;

three such transactions with Ms Thorne; and

three such transactions with Mr Streat.

5 I shall refer to each of these persons as a “customer”. In the end, none of the parties suggests that any of the impugned transactions is materially different, for present purposes, from any of the others. For this reason, I shall, in these reasons, use Mr Eadie’s transaction as a typical example of the transaction in question.

STATUTORY PROVISIONS

6 Sections 35 – 37 of the Credit Protection Act provide for the issue of ACLs. Section 35 provides:

(1) An Australian credit licence is a licence that authorises the licensee to engage in particular credit activities.

(2) The credit activities that the licensee is authorised to engage in are those credit activities specified in a condition of the licence as the credit activities that the licensee is authorised to engage in.

7 Section 29(1) of the Credit Protection Act provides:

Prohibition on engaging in credit activities without a licence

(1) A person must not engage in a credit activity if the person does not hold a licence authorising the person to engage in the credit activity.

Civil penalty: 2,000 penalty units.

8 The term “credit activity” is defined in s 6 of the Credit Protection Act. Section 6(1) contains a table which provides (inter alia) that a person engages in a credit activity if, “the person is a credit provider under a credit contract”. ASIC’s case is that in each of the relevant transactions, either FAF Beenleigh or FAF Burleigh Heads engaged in a credit activity by providing credit under a credit contract.

9 Section 5 of the Credit Protection Act provides that the term “credit provider” “has the same meaning as in s 204 of the National Credit Code, and includes a person who is a credit provider because of section 10”. Section 10 is not presently relevant. The National Credit Code (“the Code”) is contained in Sch 1 to the Credit Protection Act. Section 204 of the Code provides:

Credit provider means a person that provides credit, and includes a prospective credit provider.

10 The terms “credit” and “credit contract” have the meanings attributed to them by ss 3, 4 and 5 of the Code which provide:

3 Meaning of credit and amount of credit

(1) For the purposes of this Code, credit is provided if under a contract:

(a) payment of a debt owed by one person (the debtor) to another (the credit provider) is deferred; or

(b) one person (the debtor) incurs a deferred debt to another (the credit provider).

(2) For the purposes of this Code, the amount of credit is the amount of the debt actually deferred. The amount of credit does not include:

(a) any interest charge under the contract; or

(b) any fee or charge:

(i) that is to be or may be debited after credit is first provided under the contract; and

(ii) that is not payable in connection with the making of the contract or the making of a mortgage or guarantee related to the contract.

4 Meaning of credit contract

For the purposes of this Code, a credit contract is a contract under which credit is or may be provided, being the provision of credit to which this Code applies.

5 Provision of credit to which this Code applies

(1) This Code applies to the provision of credit (and to the credit contract and related matters) if when the credit contract is entered into or (in the case of precontractual obligations) is proposed to be entered into:

(a) the debtor is a natural person or a strata corporation; and

(b) the credit is provided or intended to be provided wholly or predominantly:

(i) for personal, domestic or household purposes; or

(ii) to purchase, renovate or improve residential property for investment purposes; or

(iii) to refinance credit that has been provided wholly or predominantly to purchase, renovate or improve residential property for investment purposes; and

(c) a charge is or may be made for providing the credit; and

(d) the credit provider provides the credit in the course of a business of providing credit carried on in this jurisdiction or as part of or incidentally to any other business of the credit provider carried on in this jurisdiction.

(2) If this Code applies to the provision of credit (and to the credit contract and related matters):

(a) this Code applies in relation to all transactions or acts under the contract whether or not they take place in this jurisdiction; and

(b) this Code continues to apply even though the credit provider ceases to carry on a business in this jurisdiction.

(3) For the purposes of this section, investment by the debtor is not a personal, domestic or household purpose.

(4) For the purposes of this section, the predominant purpose for which credit is provided is:

(a) the purpose for which more than half of the credit is intended to be used; or

(b) if the credit is intended to be used to obtain goods or services for use for different purposes, the purpose for which the goods or services are intended to be most used.

Pursuant to s 3(1) the provision of credit is the deferment of payment of a debt or incurrence of a deferred debt. The term “deferred” is not defined, but I infer that the meaning is that payment of the relevant debt has been deferred. Pursuant to s 204 of the Code the term “contract” “includes a series or combination of contracts, or contracts and arrangements”.

11 In paras 30 and 31 of the amended statement of claim ASIC pleads, with respect to the Eadie transaction, that either:

the Eadie Credit was provided under a contract, as that word is defined in section 204 of the Code … terms of which were that:

i. FAF Beenleigh agreed to provide credit of $4000 to Eadie;

ii. FAF Beenleigh charged Eadie a fee or charge of $2000 in connection with the making of the contract … which fee or charge formed part of the credit;

iii. Eadie agreed to repay the credit to FAF Beenleigh in 31 weekly payments of $128 and 1 final payment of the balance owing.

or

the Eadie Credit was provided under a contract, as that word is defined in section 204 of the Code … terms of which were that:

i. FAF Beenleigh agreed to provide credit of $2000 to Eadie;

ii. FAF Beenleigh charged $2000, in the nature of an interest charge, for the provision of credit to Eadie ($2000 Eadie Charge);

iii. Eadie agreed to repay the credit and the $2000 Eadie Charge to FAF Beenleigh in 31 weekly payments of $128 and 1 final payment of the balance owing.

12 In its final submissions, ASIC put the case in a somewhat different way. In paras 95 and 96, of its submissions, ASIC submits:

95. The agreement between the consumer and the [relevant FAF entity] comprises the application for finance (written or oral), the Sales Agreement and the Purchase Agreement. As will be explored further below, that trinity of (a) application, (b) Sales Agreement and (c) Purchase Agreement, satisfies the statutory definition of “contract” for the purposes of identifying a credit contract under the National Credit Code.

96. In as much as those documents refer to diamonds, however, those references are a pretence which do not reflect the reality of the transactions.

13 The respondents concede that credit was provided pursuant to each Sales Agreement but deny that any credit was provided pursuant to any of the Purchase Agreements. They submit that whether those agreements are construed as one transaction or as separate transactions, the only provision of credit is that provided by one or other of the FAF entities. The respondents seem not to address the possibility that the relevant contract may be wider than the combination of the two agreements, as ASIC effectively submits.

EFFECT OF THE TRANSITIONAL ACT

14 Engagement in a credit activity without the relevant licence contravenes s 29 of the Credit Protection Act. However, the statutory scheme is a little more complicated than I have so far disclosed. The Transitional Act regulated the transition from the pre-existing legislative regime (pursuant to State legislation) to the regulatory regime prescribed by the Credit Protection Act and the Code. The impugned transactions occurred between August 2010 and February 2012. Over that period, the effect of the Transitional Act is that:

from 1 July 2010 until 31 December 2010 a person was prohibited from engaging in credit activity unless that person was registered to engage in such activity, or held a licence authorising such engagement;

from 1 January 2011 until 30 June 2011, a person was prohibited from engaging in credit activity unless that person was registered to engage in such activity and had applied for a licence authorizing such engagement, or held such a licence; and

since 1 July 2011 a person has been prohibited from engaging in credit activity unless that person holds a licence authorising such engagement.

15 The relevant transactions may be categorized as follows:

Transactions entered into between 1 July 2010 and 31 December 2010

the Eadie transaction;

the first Sharplin transaction; and

the first Thorne transaction.

(Item 4 of Sch 2 to the Transitional Act)

Transactions entered into between 1 January 2011 and 30 June 2011

the first Jones transaction;

the second Sharplin transaction;

the third Sharplin transaction;

the fourth Sharplin transaction;

the first Thompson transaction;

the second Thompson transaction;

the second Thorne transaction; and

the first Streat transaction.

(Item 6 of Sch 2 to the Transitional Act)

Transactions entered into since 1 July 2011

the second Jones transaction;

the third Thompson transaction;

the fourth Thompson transaction;

the third Thorne transaction;

the second Streat transaction; and

the third Streat transaction.

(Section 29 of the Credit Protection Act.)

It is common ground that neither FAF Beenleigh nor FAF Burleigh Heads has ever been registered or licensed. Hence the changes in the statutory regime do not have any real effect on these proceedings.

STATEMENT OF AGREED FACTS, AFFIDAVIT EVIDENCE AND OTHER DOCUMENTARY EVIDENCE

16 The parties have filed a statement of agreed facts. I attach it to these reasons. ASIC has read two affidavits, one by David Leslie Lonton, and the other by Robyn Gay Lyons. Neither deponent was required for cross-examination. Mr Lonton is employed as a senior investigator by ASIC. His evidence includes corporate history details of a number of companies, including the respondents, and the results of searches of the Australian Credit Licensees Register, the Australian Credit Representatives Register and the Credit Registered Persons Register. Ms Lyons is Senior Legal Counsel for the National Australia Bank. Her evidence concerns bank records. ASIC also relies upon expert evidence from an accountant, Mr David Hockley of the firm Grant Thornton. Mr Hockley says in his report (exhibit 2) at para 2 that his instructions were to:

(a) [c]alculate the annual percentage rate of interest for each of the sets of data provided by ASIC, … in accordance with s 34 of the Credit (Commercial Powers) Act 2010 (Qld) … ;

(b) [c]alculate whether the annual percentage rate of interest calculated for each of the sets of data would be different if it were calculated using the formula contained in either s 4 of the Consumer Credit (Queensland) Special Provisions Regulations 2008 (Qld) or s 32B of the [Code]; and

(c) [c]alculate the simple interest rate for each of the sets of data.

(Quote varied for style.)

17 His report deals with those matters. The “sets of data” are the details of the various transactions between the relevant FAF entities and the customers, including the amounts of credit, total repayments, and repayment terms.

18 All of this evidence is virtually undisputed. Other evidence comes from the customers and from persons who were in control of, or associated with Fast Access Finance and/or either or both of the relevant FAF entities, or were otherwise involved in the affairs of one or more of those companies. One witness, Ms Lange, was relevantly involved only to the extent that she was involved in the affairs of DCH.

EVIDENCE CONCERNING FAST ACCESS FINANCE AND DCH

Robert Andrew Corwin Legat

19 Mr Robert Legat is in-house counsel for Fast Access Finance. He is also a director and the secretary of that company. He has been secretary since 1997, a director since 2011, and in-house counsel since 2002. He holds a solicitor’s practising certificate. FAF Beenleigh was the first “franchise operation” set up by Fast Access Finance. In about 2001, Fast Access Finance gave FAF Beenleigh a licence to use its intellectual property. It permitted use of the name “Fast Access Finance”, associated procedures, “know-how”, software and documents. FAF Burleigh Heads was incorporated in about 2005. It had a “shareholders’ agreement” which regulated its activities. It did not hold an intellectual property licence. Fast Access Finance provided assistance to FAF Beenleigh and FAF Burleigh Heads in connection with diamond transactions in that it provided the, “connections to other business entities that enabled them to partake”. It made suggestions concerning their operations and identified the documentation which they were required to use if they were to participate in the diamond model. They were to use a particular software programme which kept track of diamond stock numbers and associated matters. They were required to make sure that they did not sell the diamonds for too high a price for, “legal reasons”. They were given directions as to their dealings with DCH. They could only depart from those directions if Fast Access Finance had given its approval.

20 Mr Legat described the business model used by the FAF entities. It provided, “a means for the companies to carry on business”. The entities had a product to sell, namely diamonds. They used documents which had been created by Fast Access Finance. They used its software to record transactions in accordance with procedures prescribed by it. He said that the, “mechanics of the model”, involved a company, FAF Beenleigh, FAF Burleigh Heads or another company, selling a quantity of diamonds to a consumer. Diamonds could be sold on a cash basis or on an instalment basis. If it sold on an instalment basis, payments were made over time. The relevant FAF entity would “manage” the payments.

21 The FAF entity was able, “to act on behalf of the mother entity on instruction called [DCH], and [DCH] had instructed that it would agree to purchase particular specifications of diamonds from customers of the company for a set price, and that it would pay for them at point of sale or immediately thereafter”. This seems to mean that DCH would buy diamonds from customers of the FAF entities at a fixed price, payable at the time of sale, or shortly thereafter.

22 Mr Legat understood that DCH is now deregistered and no longer trades. The sole director of DCH was Joylene Lange. He had known her for a number of years. She was approached in early 2008 to see if she was interested in assisting with the “diamond model” and whether she was prepared to form a business arrangement. She was introduced to Mr Legat by his brother, James. At a meeting early in 2008, they discussed the proposed model. Ms Lange indicated that she was prepared to participate and registered DCH. In the early 2000s Fast Access Finance had engaged a programmer to create proprietary software for use in its consumer credit and business lending activities. The software was a web-based platform, accessible on the internet. In it were recorded details of borrowers and loan transactions. It could calculate interest, keep loan ledgers, and “that type of thing”. When the diamond model was developed, the same programmer was engaged to modify the software so that it could record the sale of diamonds, track stock, sales figures and history, keep ledgers of instalment sales and balances, record payments “and so on”. The software was known as LMS, standing for “Loan Management System”. The programmer was Mr Shidong Yu.

23 A set of documents had been designed for use in consumer credit lending and/or business lending. Such documents included a credit contract, a continuing credit contract, a Collateral Security Agreement in the form of a bill of sale, an acknowledgment document and, “other legislative requirements”. Mr Legat was shown various of the transactional documents and said that he was the author of most of them, with some input from others. The diamond model started operation on 4 August 2008. The acquisition of diamonds was primarily handled by either James Legat or Graeme Bray. Mr Robert Legat saw diamonds on a number of occasions. On one occasion he saw all of the diamonds at the Fast Access Finance office. He used the words, “various companies in one place at once”. I took this to mean that the diamonds were identified as belonging to particular FAF entities. They were in display cases or in zip-lock bags. On one occasion he took photographs of the diamonds. The diamond model ceased operation in April 2012, the last transaction occurring on Friday, 13 April 2012. That model had been adopted because of the imposition in 2008, by Queensland legislation, of an interest rate cap on consumer credit lending. The commencement of trading using the diamond model coincided with the commencement of that legislation.

24 In cross-examination Mr Legat agreed that prior to the adoption of the diamond model, Fast Access Finance and associated companies had been engaged in “micro-lending”. FAF Beenleigh and Burleigh Heads had been primarily involved in consumer lending. Mr Legat’s evidence in this respect was somewhat vague. However he knew that the FAF entities lent money, and that Fast Access Finance itself earned money from transactions involving those entities. He agreed that prior to 2008, the FAF entities were primarily concerned with consumer credit and business lending, and that consumer lending was by far the greater part of their business. He agreed that the new legislation undermined the profitability of their businesses.

25 He agreed that the effect of the documentation (which he had prepared) was that persons who came in, “to obtain a certain amount of money”, were provided with, “a model by which they could obtain that amount of money”. He agreed that in the majority of cases, the effect of the documents was that the customer had to pay back double the amount borrowed. Each transaction involved the sale by the FAF entity to the customer of a number of diamonds at $250 each, and purchase by DCH of the diamonds at $125 each. Hence the customer would be required to pay to the FAF entity twice the amount which he or she had received from DCH. A customer would not take physical possession of any diamonds unless he or she asked for them. If he or she did so then, presumably, the Purchase Agreement would not be executed, and DCH would not pay the customer anything.

26 Although there is some suggestion in the evidence that on rare occasions, customers had asked to take the diamonds, the case has been conducted on the basis that whilst it may have been theoretically possible for the customer to do so, they did not. Certainly, there is no suggestion that diamonds were ever delivered to a customer by FAF Beenleigh or FAF Burleigh Heads. Mr Legat was not surprised to be told that diamonds were not kept at either the FAF Beenleigh premises or the FAF Burleigh Heads premises. He was asked if he knew that customers were not, in reality, coming to the FAF entities to buy diamonds. He said that he would not agree or disagree with that proposition. He was asked if he asserted that a consumer who required money to pay for a bond loan was intending to buy diamonds. He said that he had no direct involvement with any of the customers, and that any answers to the questions would be hearsay. He agreed that it would not be advantageous to use the diamond model for a loan obtained for business purposes, as the relevant expenses would not be tax deductible.

27 Mr Legat was then taken to a document which is now exhibit 135. It is headed “Finance Application”. He agreed that it was part of a suite of documents used in connection with the diamond model. He said that the document was also designed for use in other models. He agreed that a customer would initially fill out such a document and other documents. The application could be completed and submitted online. He was referred to the part of the document on p 3, which is headed “Funding Request”. He agreed that this part of the document suggested that the customer was seeking funds and not diamonds. However he said again that the form was designed for use in various business models. Mr Legat denied that he understood that the diamond model was merely a pretence, and that, in reality, there was no sale or purchase of diamonds.

28 Mr Legat was referred to a decision of the Queensland Civil & Administrative Tribunal (QCAT) in 2011 (exhibit 7). See Carter v Fast Access Finance (Beaudesert) Pty Ltd [2011] QCAT 525. The decision concerned FAF Beaudesert. Mr Legat acted as solicitor for that company in those proceedings. He gave evidence and was otherwise present at the hearing. He distributed the written decision to Mr James Legat and Mr Bray. The Tribunal concluded that the diamond model was, “highly unlikely, improbable and implausible”, so as to constitute a, “complete fiction”. See [27]. Mr Legat said that he communicated this view to the other directors of Fast Access Finance. The model continued to be used until April 2012. The decision was under appeal. Mr Legat did not consider that the model was a “complete fiction”. He agreed that there were no diamonds at the Beenleigh or Miami premises, and that it was no part of the model that specific diamonds be identified in relation to any transaction. He said that a customer could request that the diamonds be provided for identification and for sale. There were no secure storage facilities at the FAF Beenleigh or FAF Burleigh Heads premises. Mr Legat agreed that if the full suite of documents were executed, no diamonds would physically change hands. The diamonds were kept at James Legat’s home.

29 He was then taken to exhibit 131, a Sales Agreement. Item I2 on the front page is headed “Delivery”. That part of the document deals with delivery to a customer of diamonds purchased from an FAF entity. Mr Legat was then taken to exhibit 136, a Purchase Agreement used in the sale of diamonds to DCH by a customer. He agreed that the Purchase Agreement did not identify the diamonds in question as those obtained by the customer from the relevant FAF entity. He agreed that he was not aware of any delivery of diamonds by a customer to DCH. Clause 2 of the Purchase Agreement required such delivery by the customer.

30 Mr Legat was then questioned concerning the recording of transactions in the computer system. He agreed that it was, “nearly an accurate description”, to say that on a given day, the number of funding transactions which had occurred would be entered into the computer and that, as a result, a communication would be sent to a DCH account, directing payment of moneys owing to customers pursuant to transactions on that day. He agreed that usually on the same day, equivalent amounts would be paid into the DCH bank account, either from a Fast Access Finance account or another account controlled by Fast Access Finance. It was put to him that the funds paid out to customers by DCH were derived from, or reimbursed by Fast Access Finance, and that the diamonds supplied by the FAF entity to the customer, and by the customer to DCH, were sold back by DCH to Fast Access Finance. Mr Legat seemed to suggest that Fast Access Finance would only pay for diamonds acquired from DCH, so that DCH was not always reimbursed for moneys paid out to FAF entity customers. He also said that diamonds sold to FAF by DCH may not have been the diamonds sold to FAF entity customers.

31 Mr Legat said that although DCH did not make money on individual transactions, it was paid a fixed fee of $500 per month. He agreed that Ms Lange was the sister of James Legat’s wife. He said that in addition to the $500 monthly payment, she obtained some free accountancy work from Mr James Legat. At some stage Mr Legat was authorized to operate on the DCH account. Mr James Legat and Mr Graeme Bray also had authority to operate on the account.

32 Mr Legat had previously been President of the National Financial Services Federation (Queensland) Incorporated. That organisation was concerned with, “micro-lending and the pay-day lending industry”. That industry was involved in small loans. He was familiar with the legislative changes which occurred, and with the Credit Protection Act and the Transitional Act. He was aware of the registration and licensing systems, with pecuniary penalties for non-compliance. He agreed that neither FAF Beenleigh nor FAF Burleigh Heads was registered or licensed, although FAF Beenleigh was on the “Register of Carried Over Instruments”. This register related to loan contracts entered into before the legislation came into effect. He said that he did not appreciate that the various companies ought to have been licensed or registered under the legislation. He did not realize this, even after the QCAT decision.

33 It is difficult to know what to make of Mr Legat’s evidence. In effect, he asserts that the transactions were genuinely by way of sale and purchase rather than lending and borrowing. It is possible that he honestly holds that view. For the moment, I do not assume to the contrary. However, he was clearly aware that the diamond model was set up to avoid the statutory interest cap. It is also difficult to avoid the conclusion that DCH was not independent of Fast Access Finance, and that he was aware of that fact. As he did not deal with customers, it may be that he did not appreciate the artificiality of any attempt by FAF entity staff to explain the transactions to customers. However with even a small amount of imagination, he would have realized that the typical customer would be looking for cash, not diamonds, and that such a customer would be unlikely to care much about the apparent structure of the documentation.

James George Robert Legat

34 Mr James Legat is the accountant for Fast Access Finance and was previously a director. He is also the accountant for FAF Burleigh Heads and was previously a director of that company. He is the accountant for FAF Beenleigh but has never held any other office in that company. As a director his role with Fast Access Finance was to give accounting and financial support. Typically he would attend at the office once a week and give any direction that was required. He has practised as an accountant since 1986. He currently practises at Clear Island Waters on the Gold Coast under the firm name, SB Partners. Previously, it was called Swan & Baker Pty Ltd. He is familiar with the diamond model adopted by Fast Access Finance. He said:

Basically, it was a purchase and sale arrangement whereby the offices would sell particular diamonds to a consumer, and there was a relationship with a third party where the consumer could on-sell those diamonds.

(ts 358 ll 12-15.)

35 The third party was DCH. The sole director and shareholder of that company was his sister-in-law, Ms Lange. He was also the accountant for that company and for Ms Lange. He had no day-to-day involvement in the affairs of DCH. The diamond model was introduced in mid-2008. Its introduction was brought about by Queensland legislation, introducing an interest cap. It made the existing lending model unviable. He was involved in the implementation of the diamond model to the extent that he was a director at the time. The legal functions were left to his brother, Robert. Mr James Legat dealt with any financial aspects to do with GST reporting. Previously, the “entities” were not subject to GST because of the nature of their lending, but the change to the diamond model involved trading, purchase and sale, raising GST questions.

36 In 2008 Mr Legat had discussions with Ms Lange about the incorporation of DCH. A meeting at Mr Legat’s residence was attended by himself, Ms Lange, Mr Bray and Mr Robert Legat. They discussed the concept of the diamond model and Ms Lange’s involvement in it, whether she would be comfortable with it and whether she was prepared to accept the relevant responsibility. She was prepared to do so and asked that they form the company. Once the model came into effect, Mr Legat did not have any day-to-day involvement in dealings between Fast Access Finance and DCH. He has seen the diamonds associated with the diamond model. They were obtained from one of Swan & Baker’s clients, Diamonds on Broadbeach Pty Ltd, and stored at Mr Legat’s home. However two other suppliers seem to have been involved, Teracast Diamonds and ADTC. In the early stages, Mr Legat dealt with Diamonds on Broadbeach, telling them his requirements. Thereafter, Mr Bray usually dealt with them. Mr Legat did not recall being directly involved in payment for diamonds. He thought that Mr Bray had attended to that matter.

37 The diamonds were kept in a safe at his home. It had initially been acquired to store off-site backup for his accounting practice. When the diamonds were received, they were in bulk. They would typically come in a packet, wrapped in paper, within a plastic bag, or loose in a plastic bag. He separated them into the respective “offices” (presumably the FAF entities) in the quantities required by each of them. Initially, they were put into plastic containers. In the end Mr Legat ran out of containers and stored the diamonds, “separately per office”, in plastic bags. The expression “per office”, presumably meant that the diamonds belonging to each FAF entity were stored in a bag reserved for that entity’s diamonds. There were a couple of occasions on which he gave diamonds to Mr Bray, because people had purchased them. Otherwise, he did not have any further dealings with the diamonds on a day-to-day or weekly basis. The relevant interest cap became effective on 31 July 2008. Trading in diamonds commenced on 4 August 2008. In 2010 he ceased to be a director of Fast Access Finance. He ceased to be a director of FAF Burleigh Heads in 2005 or thereabouts.

38 In cross-examination Mr Legat said that he was a director of Legat Holdings Pty Ltd, a shareholder in Fast Access Finance. He is also a director of Legat Investments Pty Ltd which is, in turn, a shareholder in Legat Holdings Pty Ltd. Legat Investments Pty Ltd is the trustee of a family discretionary trust. Mr Robert Legat is not associated with either Legat Holdings Pty Ltd or Legat Investments Pty Ltd. Mr James Legat and his wife control Legat Investments Pty Ltd. In this indirect way, he and his wife have an interest in Fast Access Finance.

39 Mr Legat agreed that he spoke to Ms Lange about DCH after the diamond model had been more or less designed. At a meeting involving Ms Lange, Mr Robert Legat, Mr James Legat and Mr Bray, the proposal was discussed. It seems that its operation was largely automated, using the Bill Buddy payment system. Ms Lange was initially paid a fee based on volume of activity. Subsequently it was fixed at $500 per month. Some of the cross-examination proceeded on the basis that when there was a sale by a customer to DCH, there would be a payment by that company to the customer of $250 per diamond, and a corresponding payment of a similar amount (from companies associated with Fast Access Finance), presumably to DCH. My understanding of other evidence is that such sales were for $125 per diamond. At the end of each day, the transactions were consolidated, and Fast Access Finance repurchased the stock in bulk from DCH. In summary the cash flow would involve (say) $1,000 going out to the consumer and an equivalent amount coming into a DCH account. In that sense DCH made no money on the transaction, save for the $500 per month fee. There was no written agreement between Fast Access Finance and DCH.

40 Mr Legat asked Ms Lange to be the director of DCH because she had experience as a book-keeper, was a family member and was looking for more income. In other words he was trying to help her. It was suggested to Mr Legat that in fact, DCH was being used as a cipher whereby Fast Access Finance was lending money to individual customers. He said that he did not believe so. It was suggested that there were, in truth, no diamond sales. He disagreed. He said that the diamonds were all consistent in size, cut and clarity. However they were not separately identified in any way. He would transfer diamonds into bags for the various branches, and then return them to the safe. He did not move diamonds on a daily basis. He understood that diamonds were not kept at the FAF Beenleigh or FAF Burleigh Heads premises.

41 Mr Legat agreed that prior to adoption of the diamond model, Fast Access Finance and the FAF entities had been lending into the consumer market, making small loans for personal use, as opposed to business use. In excess of 90% of the business involved personal loans. Something less than 10% involved business loans. Advertising was aimed at the “smaller” end of the market. He agreed that there were instances of desperate people seeking loans, but said that there was an obligation on, “ourselves and the customers to make sure that [any loan] was affordable”. He believed that nobody was lent money, which loan he or she could not afford to repay.

42 He agreed that he was charging interest at an annualised rate of 240%. However he said that a loan was not generally for a year, so that the figure of 240% was a little misleading. He agreed that he looked for repeat business from customers, but not by use of any improper means. He understood that promotional letters were posted, presumably to customers or potential customers. He had heard that one such letter was described as a “star” letter. He agreed that the 48% interest cap made the lending business unviable. He agreed that he took security from customers where it was available, particularly over motor vehicles. He agreed that people might initially approach an FAF entity to borrow money. He also said that he did not know why they came into the office. He was not familiar with advertising placed after the diamond model was introduced.

43 He assumed that when a person came into an office looking for money, he or she would fill out a financial application. He was not familiar with the standard documents that were used, although he had seen them. He said that a particular application form shown to him had been used prior to the diamond model being introduced. He did not know whether there was ever any change in the form. He agreed that the application form seemed to contemplate that a person was seeking funds. He knew that FAF Beenleigh and FAF Burleigh Heads were catering to customers who were seeking advances of money, that at those places, there were no diamonds on the site, and that all of the diamonds in his safe were the same. It was put to him that the he was not running a jewellery business. He said that he was selling diamonds. He was not aware that after customers came in seeking funds, they would be told whether they had been approved for the funds. He agreed that if they were approved, they would be presented with the relevant documents, and that diamonds would not be physically delivered. However if a customer wanted the diamonds, he or she could have them. The loans were funded from internal cash. About $1.5 m was tied up in diamonds, involving a severe capital cost.

44 Mr Legat agreed that in 2010, he ceased to be a director of Fast Access Finance, and that the Code had come into effect in July 2010. The agreed statement of fact states that he ceased to be a director on 1 August 2010. He said that the commencement of the Code was not the reason for his ceasing to be a director. He had been spending more time at his accounting practice and did not have the time which he needed to dedicate to Fast Access Finance. He understood that credit providers who were engaged in credit activities under the Code needed to be registered and licensed. He knew this prior to his resignation as a director. His brother may have told him of these requirements.

45 He agreed that Fast Access Finance used an automated system which included a software system known as LMS, standing for Loan Management System. It was a proprietary system, owned by Fast Access Finance. The company also maintained a server which operated the programme. FAF Beenleigh and FAF Burleigh Heads were able to access the software from computers located in their offices. They did so with the permission of Fast Access Finance. He was taken to a version of the Sales Agreement which had been developed by Fast Access Finance. On the third page, the statement, “Copyright 2008, Fast Access Finance Pty Ltd” appears. He agreed that other documents in the bundle were also developed by Fast Access Finance and related to the diamond model. Fast Access Finance had intellectual property in these documents and allowed FAF Beenleigh and FAF Burleigh Heads to use them. He said that after he ceased to be a director of Fast Access Finance, he did not participate in decision-making in connection with that company.

46 He believed that whilst the diamond model was in operation, the diamonds were delivered to customers pursuant to the Sales Agreements by way of “legal delivery”. He seems to have used this term in contradistinction to physical delivery. He considered that customers passed title to DCH by the Sales Agreements. He said that the diamonds were to him, “like buying tennis balls – they are all the same”. He agreed that consumers did not take physical possession but said that they took what he described as “legal possession”. He agreed that the diamonds were at his home in a safe, but said that they were available to whomsoever wanted to see them. They were not ordinarily shown to customers. He denied that each transaction was a pretence, or that the documents merely purported to be for the sale and purchase of diamonds when, in reality, an amount of money was being lent.

47 He said that he broadly knew that under the Code, credit providers who engaged in credit activity would have to be licensed or registered. However he left all legal matters to his brother. The matter was discussed broadly before the relevant legislation came into effect, but they did not believe that it applied to “us”. He agreed that he had “set up” DCH, but did not recall who paid for it. He could not recall whether money was injected into DCH by Fast Access Finance. He agreed that the diamond model did not commence operations until about August 2008. Having looked at bank records, he agreed that significant moneys had been injected into DCH between April and July. He said that the deposits appeared to have come from entities such as FAF Beenleigh and FAF Burleigh Heads. He understood that the money so injected was by way of float capital. He agreed that Ms Lange did not put any money into DCH.

48 Mr Legat was asked about a company, Legat Brothers Pty Ltd, another shareholder in Fast Access Finance. It is Mr Robert Legat’s company. It is not a trustee company, but a corporate trading entity in its own right. Mr Legat was also familiar with the entity, Bill Buddy Pty Ltd which was used for effecting repayments. Each repayment attracted a $2 fee. Mr Legat did not recall how much Bill Buddy had earned from that business. When asked about the overall turnover of the diamond business, he said that FAF Beenleigh, for example, might have a, “typical loan book that might exist for vendor sales of diamonds”, in the region of $200,000. Over the whole of the Fast Access Finance operation, $2 m or $3 m might be involved.

Graeme John Bray

49 Mr Bray is a director of Fast Access Finance, FAF Beenleigh and FAF Burleigh Heads. His duties concerning the diamond model were minimal. He was predominantly responsible for organizing signage, advertising and liaising with staff. He had no day-to-day dealings with either FAF Beenleigh or FAF Burleigh Heads. However he had dealings with the other directors of those companies. The other director of FAF Beenleigh was Michael Maloney. The other director of FAF Burleigh Heads was Graeme Beattie. His communications with them concerned their business operations, including the sale and purchase of diamonds.

50 Mr Bray gave evidence of instructions given to FAF Beenleigh and FAF Burleigh Heads. Pursuant to those instructions, if a customer sought a sum of money, the FAF entity would identify whether it was for a consumer or business purpose. If it was for a consumer purpose, the FAF entity was to inform the customer that it could not offer a loan but had a facility which could provide the required sum. This facility was introduced in August 2008. He knew of DCH, but was not involved in its affairs. He has had no involvement with Ms Lange concerning the affairs of DCH, or its interaction with Fast Access Finance.

51 Concerning the acquisition of diamonds, he said that James Legat had a client who had a diamond business in Broadbeach. Mr Legat arranged the purchase of diamonds from that source. From time to time, he asked Mr Bray to collect such diamonds from the Broadbeach outlet. Mr Bray would organize a cheque in payment, deliver the cheque, pick up the diamonds and deliver them to James Legat. He did this on many occasions. He did not retain any diamonds for himself. He acquired diamonds for both FAF Beenleigh and FAF Burleigh Heads. He would organize payment by the relevant FAF entity to Fast Access Finance. The diamonds would be uploaded into the Fast Access Finance computer system so that the relevant FAF entity could sell them. Each of FAF Beenleigh and FAF Burleigh Heads would have held between 20 and 50 diamonds at any one time. None of the diamonds was returned to him. He received valuation documents from the diamond supplier. They appear at exhibit 140. Diamond sales at both FAF Beenleigh and FAF Burleigh Heads continued until 2012. Neither is now trading. Mr Bray said that the funds for acquiring the diamonds came from a company called Tri Star which is not related to the Fast Access Finance companies.

52 In cross examination Mr Bray said that he did not recall being a signatory on the DCH account. He denied knowing that DCH was being used as a “cipher” to move funds to customers in lending transactions. He was aware that each day, there were electronic transfers of funds from the National Australia Bank to DCH for payments to customers. He said that the money paid to DCH from the Fast Access Finance accounts was, “because the office was restocking on the diamonds that had been sold for that day”. He said that DCH received a facility fee, but made no specific profit on individual transactions. He understood that DCH was owned by Ms Lange, and that she was James Legat’s sister-in-law. He agreed that effectively, DCH did nothing. Fast Access Finance did all of the necessary work. He did not agree that DCH was simply a cipher, that the “construct of diamond sales and diamond purchase” was just a pretence or that the transactions were really by way of loan.

53 He said that prior to the end of June 2008 the predominant business of Fast Access Finance and the FAF entities had been lending money to consumers. At the end of June 2008 a statutory cap was placed on interest for loans to consumers. He agreed that business loans were a very small part of the Fast Access Finance business. He agreed that prior to the imposition of the cap, advertising had focussed upon borrowings for bonds, car registration, “fast money” and “quick cash”. The advertisements were designed to attract consumers who were in urgent need of personal finance. He agreed that many of these people were desperate. The cap, if observed, would have deprived Fast Access Finance of virtually all of its profit. It was important that it continue to operate. Even after the diamond model was introduced, the advertising focussed on borrowing for the purpose of paying residential lease bonds. Mr Bray agreed that the advertising was, even after the commencement of the diamond model, designed to attract customers who were “consumer borrowers”, particularly those looking for money to post residential bonds. It would be fair to say that none of those people came into the office for the purpose of buying diamonds.

54 He agreed that the finance application form asked the customer to identify the purpose for which funds were required. When asked if he agreed that the model did not provide for the delivery of diamonds to the customer, he said that if a customer wanted the diamonds he or she could have them. Notwithstanding the fact that a customer had not come into the office to obtain diamonds, he or she was invariably given a finance application form. If approved, the customer would receive two documents, one purporting to be an agreement for the sale of diamonds to him or her and the other, an agreement for the sale of diamonds by the customer to DCH. The customer was expected to sign both. It was put to Mr Bray that he knew that the customer was not going to receive diamonds. He said that if the customer did not want the diamonds, he or she would not receive them. He knew that no diamonds were kept on the FAF Beenleigh or FAF Burleigh Heads premises, and that specific diamonds were not allocated to particular transactions. He agreed that the customer would receive an amount which he or she would have to repay, together with an equivalent amount which, Mr Bray said, was for the purchase of the diamonds. It was put to him that he knew that the additional amount represented interest or a credit charge. He insisted that it was the cost of the diamonds.

55 Mr Bray said that Mr Robert Legat kept him informed of legislative changes. He knew that under Commonwealth legislation, the Code was to commence on 1 July 2010. He was also aware of the Transitional Act. He knew that such legislation provided that credit providers who were “providing credit activity” had to be registered and, ultimately, licensed. He denied knowing that FAF Beenleigh and FAF Burleigh Heads were providing credit. He knew that they were not registered or licensed under the proposed legislative scheme. He did not know that DCH was neither registered nor licensed. He was aware of the hearing in QCAT involving Fast Access Finance Beaudesert. He was a director of that company. He did not attend the hearings but was informed about them. DCH was also a party. He instructed Mr Robert Legat to appear on behalf of FAF Beaudesert. He did not recall being provided with a copy of QCAT’s reasons (exhibit 7).

56 Mr Bray was advised that QCAT had found that the characterization of the transactions was so highly unlikely, improbable and implausible as to be a complete fiction. He disagreed with the proposition that the sale and purchase of goods comprised a mere pretence to conceal a lending transaction, although he understood that QCAT had so found. He said that “we” did not believe that the FAF entities were providing consumer credit. Mr Bray gave the impression that he wanted to distance himself from operation of the diamond model. My comments concerning Mr Robert Legat’s evidence otherwise apply to his evidence.

Joylene Melissa Rae Lange

57 Ms Lange is Mr James Legat’s sister-in-law. She has known him for over 25 years. He has been her accountant since some time before 2007. At the beginning of 2008 Mr Legat approached her, suggesting that she start a company called Diamond Clearing House. The company would sell diamonds to Fast Access Finance. That company would find customers from whom DCH would buy diamonds. In about March 2008, she had a meeting with Mr James Legat, Mr Robert Legat and Mr Graeme Beattie in which more detail was provided concerning the proposed operation. They wanted a company separate from Fast Access Finance. As she knew all three of them, they would have a relationship of trust as well as a business relationship. DCH was to be responsible for selling diamonds to Fast Access Finance offices. Fast Access Finance would work as an agent for DCH, finding customers who wanted to sell diamonds back to it. DCH was to operate under a second-hand dealer’s licence. Fast Access Finance would deal with day-to-day operations, “paperwork” and documentation. It would organize the purchase by DCH of diamonds and the purchase of diamonds from DCH.

58 DCH was to be the entity which controlled the set up and how it worked and operated, with Ms Lange as director. She was to be responsible for checking that everything was done in accordance with their agreement. For the privilege of its acting as agent for DCH, Fast Access Finance was to pay an agency fee to DCH. At first the fee was calculated on a per diamond basis. That system only operated for a couple of months. It was found to be too cumbersome. A flat fee of $500 per month was negotiated.

59 The proposal was acceptable to Ms Lange, and so DCH was incorporated, with Mr James Legat as its accountant. He also assisted in incorporating it. They set up a business bank account with National Australia Bank. Mr Robert Legat did the paperwork for the second-hand dealer’s licence and explained to Ms Lange the process of applying for such licence. She was the only director of DCH. Its share capital was $2. She was the only shareholder. It has now been deregistered. When the bank account was established with the National Australia Bank, Ms Lange and Mr James Legat were the signatories. Computer access was granted to Fast Access Finance. It could view the account but not operate on it. Not long after the account was established Mr James Legat was removed as a signatory. Ms Lange was then the only signatory.

60 Ms Lange was shown various documents which related to the establishment of the bank account. She was also shown Excel documents, showing the money paid out of the DCH account to customers on a daily basis. Ms Lange received these documents by email from the Fast Access Finance head office in Nerang. She described a form of agreement by which DCH purchased diamonds. It identified the customer selling the diamonds, the number of diamonds, the relevant amount and bank details. I infer that this was in the form of the Purchase Agreements to which I have referred. The document was drafted by Ms Lange in conjunction with Mr Robert Legat, Mr James Legat and Mr Graeme Beattie.

61 On a day-to-day basis DCH did not really do anything. Ms Lange would check the reports and the bank account, making sure that everything was running smoothly. DCH purchased the first quantity of diamonds to which Mr Bray referred. Ms Lange said that Mr James Legat had sourced a number of diamonds of a specific carat, clarity and size. She received a bank cheque which was delivered to the diamond seller, but Mr James Legat actually attended to the transaction. Ms Lange authorized the payment. The diamonds were stored in a safe. Thereafter, Fast Access Finance, on a day-to-day basis, attended to the purchasing and selling of diamonds. She believed that, save for subsequent purchases from customers, there was only one purchase of diamonds, at the very beginning of the project. Ms Lange did not remember providing another bank cheque. She said that there were two sides to the business. One was selling diamonds to Fast Access Finance. The other was finding clients from whom to buy diamonds, which task was undertaken by Fast Access Finance. Ms Lange was asked whether she sold diamonds to Fast Access Finance, or to the individual FAF entities. She said that payments came from the entities but, “it was all done through the main office at Nerang, so they would actually put in their orders to the main office, and then they organised … the purchase of them”.

62 In cross-examination Ms Lange agreed that Mr Bray and Mr Robert Legat were also signatories on the DCH account. Mr James Legat decided who were to be signatories. She did not recall Mr Robert Legat or Mr Bray being removed as signatories. Although she had said that Fast Access Finance could not operate on the DCH account, in fact there was a software programme which enabled it to do so. Every day, funds were transferred in accordance with directions from Fast Access Finance. She said that there was an agreement that Fast Access Finance would operate the Fast Access Finance software system so that every day, electronic information relating to consumer transactions would be sent to the bank. The bank would act on that information by paying the customers who had entered into diamond model transactions. Ms Lange said that Fast Access Finance would not necessarily buy all diamonds which DCH had acquired from clients. They would only acquire the number that they needed, or at least that was her understanding. It was suggested to her that DCH was being used as a cipher, to give the appearance that there were diamond sales. She denied this, saying that there were diamond sales. She agreed that DCH did not make money on the sale of diamonds, apart from the fee. It was put to her that the fee of $500 was a payment to her for acting as director and shareholder. She denied this.

63 DCH did not sell diamonds to anybody other than Fast Access Finance. It did not carry on such a business. She did not remember if she had added anything to the drafting of the Purchase Agreement. She said that the information she received on a daily basis was in the form of an attachment to an email.

64 She agreed that the diamond model ceased to operate in 2012, and that a document dated 5 December 2013 (which was shown to her) did not relate to operations for that year. She said that when the company was set up, funds were provided by Fast Access Finance which, “were put in as a bond”. She, herself, did not invest any money in the company. The funds were used to purchase diamonds. She had no prior experience in the diamond industry. There was no written agreement in relation to the arrangement. She did not seek to identify the actual diamonds which were the subject of any particular purchase agreement. She had never previously been a company director.

65 I very much doubt that Ms Lange believed that she was running DCH. I am inclined to infer that she was happy to take a moderate fee in return for the use of her name as a director. I do not accept that she exercised any real control over the company’s affairs or had any real understanding of the diamond model.

Shidong Yu

66 Mr Yu is a software architect, designer and programmer. He is presently a director of Bill Buddy Pty Ltd. That company provides online payment services. Since 2003, he has been designing and programming software for Fast Access Finance. He has designed loan management systems, diamond sales systems and some other customer-related management systems. In providing these services, he was instructed by Messrs Bray and Robert and James Legat. The loan management system kept a record of loan transactions, posting interest and performing other services in connection with the repayments and recording of repayments. The software was owned by Fast Access Finance. It could be accessed from a web browser. Each Fast Access Finance "office" could go to the portal of the system where they would see, "a user name and a password verification screen". A person who sought to enter had to provide the relevant information in order to obtain access. The offices could also enter data into, and obtain reports from the system. Data to be entered might include loans which had been created and other transactions, such as posting fees or entering cash receipts. It also contained data with respect to customers, each of whom had a customer identification. When Fast Access Finance adopted the business model involving diamonds, Mr Yu modified the existing system in order to accommodate the diamond model.

67 He said that:

…when every single sale is being generated by the time when the office – the office user is keying in the data, the real time the diamond stock is being checked, and is the number of diamonds available for sale is on the screen, so they can see that.

(ts 332 ll 8-11.)

68 Each diamond had a unique identifier so that sales could be linked to such identifiers. He said:

So when the sales are being created there is a link that's being established between the sales and these unique identifiers, so we can keep a track of that by the diamond level. And then by checking the history of the time stamp when the sales were created, we can determine that whether the status of the diamond is available for sale or is still in the “on hold” status.

(ts 332 ll 18-23.)

69 By "on hold" Mr Yu meant that a diamond was not available for sale because it had been sold and could not be resold for 10 days after such sale. This evidence may suggest that if necessary, particular diamonds could be identified as having been appropriated to a particular sale. However, in cross-examination, Mr Yu said otherwise. The system interacted with Bill Buddy's online payment system, directly debiting customers' accounts with repayment amounts. It generated a "payment due" report which resulted in a withdrawal from the customer's bank account and, presumably, a corresponding credit to the account of the relevant FAF entity.

70 Bill Buddy allowed small businesses and individuals to utilize a direct debit facility, a BPAY facility or a credit card facility. Bill Buddy required Fast Access Finance to obtain from customers two forms, one called a "Direct Debit Authorization Form" and the other, a "Facility Agreement Form". The first form provided the customer's authorization for the direct debit of instalment amounts against his or her bank account. The second form informed the customer that he or she had agreed to pay the fees involved in such transactions, presumably to Bill Buddy. Mr Yu was then taken through some of the screens available in the system. He had not seen all of the diamonds, although he had seen some.

71 Under cross examination, he agreed that although his system gave a unique number to a theoretical diamond, such numbers were not assigned to specific diamonds held by Fast Access Finance. He agreed that the system contained a facility for directing the National Australia Bank to pay money to customers. At ts 338 ll 20 - 33, this passage appears:

MR SULLIVAN: Did Bill Buddy organise for payments to be made to Diamond Clearing House? --- I understand that, because despite of the question you ask before, I did not know the nature of these transactions. Generally, despite of these transactions, Bill Buddy was in the middle of Fast Access Finance, the customer, and Diamond Clearing House. So literally almost all the money going into the Diamond Clearing House was coming from Bill Buddy at that moment, and all the money coming back from the customer, going back to Fast Access Finance, goes to Bill Buddy and then goes to Fast Access Finance. So I'm not sure which part of the transaction it is, because at the end of the day is if Fast Access - that's what I was aware of - is if Fast Access, sorry, if Diamond Clearing House is selling the diamond back to Fast Access Finance, and Bill Buddy is in charge of direct debiting the money from Fast Access Finance and give it to Diamond Clearing House. This could be the transaction you are referring to, but I - I can't really confirm that because this is first time I see this one and I have to verify with the system.

72 To the extent that it is relevant, I accept Mr Yu's evidence. There is no reason for doing otherwise.

EVIDENCE CONCERNING THE FAF BEENLEIGH TRANSACTIONS

Steven James Eadie

73 Mr Eadie dealt with FAF Beenleigh in August 2010. Immediately before that time, he and his wife were seeking to rent residential premises and needed to raise sufficient money to cover the amount of the rental bond. They had enough money to pay the rent but not quite enough for the bond. Mr Eadie was seeking about $1,000 for that purpose. He and his wife searched online and found that FAF Beenleigh was conveniently located. His wife telephoned the FAF Beenleigh office to, “find out what paperwork was required”. Once the paperwork had been assembled they went to that office. The “paperwork” included payslips, bank details, bank statements and a vehicle registration document. Some of the relevant documents are in evidence. Mr Eadie was asked to describe the premises at Beenleigh. He said that, “[t]he only thing I can recall is when I went there was a sign saying, ‘Fast Access Finance’, and then as I walked towards the building, it was just – I opened the door and we walked in”.

74 When they entered the premises they found a receptionist’s desk to the rear of the right-hand wall, and four or five chairs to the left. A corridor led to the back of the building. They remained in the front room. Mr Eadie did not remember whether there was any signage in the room. There were no goods on display. They went to the receptionist’s desk and spoke to a woman who was sitting behind the desk. Her name was something like Loretta or Leanne. He told her that they had a meeting with Michael concerning a rental loan or a bond loan. I infer that “Michael” was Mr Maloney, another witness, and that Loretta was his then wife. Mr Eadie did not remember any discussion concerning the amount to be obtained. They were provided with further “paperwork” to complete. They sat down and did so. One document was exhibit 29, a finance application. It shows the applicant for the loan as being Mr Eadie. The amount requested by way of “funding” is $2,000. He identified most of the handwriting on the second and third pages as being that of his wife. However the figure of $130 in brackets (which appears on the third page, opposite the question: “How much can you afford to pay?”) is not hers. It seems that in answer to that question, Mr Eadie’s wife had inserted the figure of $110 weekly. Somebody else subsequently inserted the figure of $130. They had sought only to obtain $1,000. Mr Eadie did not remember how the substitution of $2,000 for $1,000 had occurred, but understood that somebody had told them that the amount of $2,000 was the minimum amount permitted.

75 After they had completed the application, they waited for a couple of minutes. Michael then entered the room and introduced himself. They were still in the front room. They discussed the purpose for which funds were being sought. At some stage Michael said something, “about diamonds”. Mr Eadie asked, “What’s diamonds got to do with it?” Michael said something like, “It’s just how we put it through. It’s just a way to get around things”. Mr Eadie’s wife said that she was not going to hand over her engagement ring. Michael said that he was not going to take her engagement ring. Michael then went into the back room with the documents. In his absence Mr Eadie and his wife spoke about diamonds, although they were not sure about Michael’s comments. After a couple of minutes Michael returned and asked for paperwork concerning Mr Eadie’s motor vehicle. As a result of that conversation Mr Eadie and his wife went to a nearby Queensland Transport Office where they obtained the relevant paperwork, and then returned to the FAF Beenleigh office. They handed the paperwork to Michael. The document obtained from Queensland Transport appears to have been a vehicle registration renewal notice (exhibit 30). At some stage somebody other than Mr Eadie completed a document described as a Privacy Act consent form. He signed it. That document is exhibit 34.

76 Michael went away and returned with documentation concerning, “the loan of the money or the purchase of the money that we wanted to borrow”. He turned the documents so that they could read them and explained them. Mr Eadie made sure that the personal details were correct. He recalled that on some pages there were references to diamonds. He did not understand those references. He was only seeking a loan. Michael said, “Don’t worry if you see diamonds on the paperwork. It’s just how we put it through to get around things”. Mr Eadie, “shrugged it off”, as they needed the money. When he went to FAF Beenleigh he had not intended to buy or sell diamonds. He was seeking a loan, “of money for rental”. He did not recall seeing any signage about diamonds, nor were any diamonds shown to them. There were no display cabinets. No diamonds were ever provided to them. He did not provide any diamonds to the “Fast Access Finance people” with whom he was dealing.

77 Concerning the documents, he was told to make sure that the personal details were correct. He skipped over the rest of the pages and signed the back page. He was then referred to a document headed “Direct Debit Request” (exhibit 35). He identified his signature on that document. There was no discussion concerning it. He did not recognize the other writing on the document. He was shown exhibit 36, the Sales Agreement. He said that this was the document of which he said that he read the front page but skipped over the balance. Whilst he was reading it, the discussion about diamonds occurred. Mr Eadie said that he had a, “quick glimpse over it”, but did not read it in detail.

78 He was then taken to a document entitled “Purchase Agreement” (exhibit 38). He recognized his signature on it. He was asked to check the details of his address and bank details. He said that he was again told not to worry if he saw references to diamonds in the document. He said that the company, “Diamond Clearing House Pty Ltd”, had not been mentioned to him. He understood that he was dealing with “Fast Access Finance at Beenleigh”. He signed the Purchase Agreement. He was then taken to a document entitled “Tax Invoice”, dated 27 August 2010 (exhibit 39). He remembered seeing that document. He understood it to indicate the amount which he had to pay on a weekly basis. He noted that the amount of the loan was $4,000. He said, “I knew I was going to have to pay some sort of interest back, but didn’t realise it was going to be to this extent”. He was then taken to a document headed “Diamond Sales Forecast Report” dated 27 August 2010 (exhibit 40). He recalled that he had been shown this document. It was explained to him. He said that the dates for payment and the amounts were explained. He was then taken to a document headed, “Westpac Choice eAccount” (exhibit 41). It appears to be a bank statement. Mr Eadie said that the figure of $2,000, shown as a credit on p 7, represented the amount obtained from FAF Beenleigh. He spent it on a bond for a rental property and used some of it to hire a truck to move furniture to the new residence. Exhibit 37 is entitled, “Collateral Security Agreement”. By it Mr Eadie transferred his motor vehicle to FAF Beenleigh to secure performance of his obligations under the Sales Agreement.

79 At some stage during the period over which he was repaying the loan, his employment circumstances changed, so that instead of being paid weekly, he was being paid fortnightly. This caused some temporary difficulty in making repayments. He approached FAF Beenleigh. It agreed to postpone payments until he had reorganized his finances. This accommodation came at a cost. FAF Beenleigh generated a “Sales Agreement” dated 22 October 2010 (exhibit 42), a document headed “Collateral Security Agreement” dated 22 October 2010 (exhibit 43), and a third document headed “Purchase Agreement” dated 22 October 2010 (exhibit 44). These documents evidence the basis upon which such further financial accommodation was extended. He was referred to a document which appears not to be amongst the exhibits. It bore the words, “Instalments will vary to $260.00 … each fortnight commencing 9 November 2010”. He said that at about that time his employer’s payment cycle had changed. He had no intention of dealing in diamonds when he signed these documents. He was then taken to documents described as “Westpac Choice eAccount” (exhibit 45), a series of bank statements. On p 14 of 16 a deposit of $250 appears.

80 At some stage he obtained a bank loan and contacted FAF Beenleigh to obtain a payout figure. The payout figure was $2,900. He paid it. He was taken to a letter headed “Re: Account Finalisation”, dated 29 November 2010 (exhibit 46). It is on the letterhead of FAF Beenleigh and reads:

Thank you for choosing Fast Access Finance. We would welcome the opportunity to provide further assistance to you in the future.

We can confirm that at the date of this letter, your account has been paid in full and the amount currently owing to us is nil. Security held by Fast Access Finance ahs [sic] been released.

…

81 Before turning to the cross-examination of Mr Eadie I should say a little about the documents to which he was taken in the course of his evidence. They are more or less common to all relevant transactions. Mr Eadie’s Finance Application is exhibit 29. I shall say a little more about it at a later stage. The Sales Agreement (exhibit 36) describes the “Goods” as, “16 x loose modern brilliant cut diamond, 0.10cts, colour “H”, clarity P1”. The “Price of Goods” is shown as “Deposit: $0” and “Balance: $4,000 including GST”. The delivery date is blank. It is followed by the words in brackets, “If blank, 3 business days from the date of this Agreement”. Against the words “Type of Sale” a cross appears in the box opposite the words “Instalment Sale”. The alternative box is “Cash Sale”. Terms of payment are said to be “Cash Sale: In full on Delivery Date” and “Instalment Sale: 31.00 payments of $128.00 each and 1 payment of the balance owing, commencing 08/09/2010 and payable WEEKLY”.

82 There are then two columns. One is headed “Instalment Sale Conditions”. In the document the spelling “Installment” is used. I shall use the spelling “Instalment” as it seems to be more common. The other column is headed “Cash Sale Conditions”. Both deal with the purchase and delivery of the “Goods”, payment, passing of title, ability to deal with goods, payment default, effect of default and consent to the future supply of marketing materials. In the Instalment Sale Conditions column there are also provisions relating to prepayment, security and the circumstances in which the “Seller” is to be entitled to take immediate action to recover the balance owing. Under the heading “Security” at I9, it is said that:

In consideration for entering into this Agreement and agreeing to accept instalments for payment of the Goods, the Buyer agrees to grant the Seller security against the promise to pay by instalments by entering into a Collateral Security Agreement with the Seller. The terms of the Collateral Security Agreement are to be read in conjunction with this Agreement, and default under the Collateral Security Agreement shall be a default under this Agreement.

83 By the Collateral Security Agreement (exhibit 37), Mr Eadie, as grantor, warranted that he was the beneficial owner of the motor vehicle in question and agreed to transfer and assign it to FAF Beenleigh, upon the proviso that the charge would be released, at Mr Eadie’s expense, in the event that he satisfied his obligations pursuant to the Collateral Security Agreement and under the Sales Agreement. It is not, at this stage, necessary to say any more about that document.

84 The Purchase Agreement dated 27 August 2010 (exhibit 38) provided for the purchase from Mr Eadie by DCH of, “16 x loose modern brilliant cut diamond, point 10cts, colour “H”, clarity P1” for $2,000. The conditions of sale are short and are as follows:

1. Purchase

The Purchaser agrees to purchase the Diamonds from the Vendor and to pay the full Price of Diamonds on the Date in exchange for the Diamonds.