FEDERAL COURT OF AUSTRALIA

Addenbrooke Pty Limited v Duncan (No 6) [2015] FCA 793

IN THE FEDERAL COURT OF AUSTRALIA | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. Leave to amend the Amended Originating Application and the Second Amended Statement of Claim in accordance with the amendments set out in MFI-11 be refused.

2. The whole of this proceeding be dismissed.

3. The First and Second Cross-Claims be dismissed.

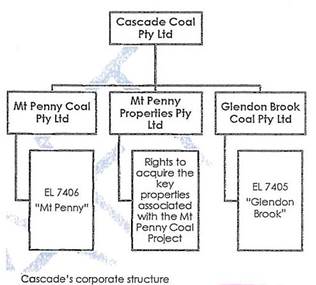

4. The plaintiff pay the costs of the first defendant (Travers William Duncan), the second defendant (Peter Gray) and the third defendant (Southern Cross Equities Pty Ltd) of and incidental to this proceeding (including the costs which those parties are ordered to pay to the cross-defendants pursuant to Order 5 and Order 6 below).

5. The cross-claimant in the First Cross-Claim (Southern Cross Equities Pty Ltd) pay the cross-defendants’ costs of and incidental to that Cross-Claim.

6. The cross-claimant in the Second Cross-Claim (Peter Gray) pay the cross-defendant’s costs of and incidental to that Cross-Claim.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 2243 of 2012 |

BETWEEN: | ADDENBROOKE PTY LIMITED (ACN 055 973 576) Plaintiff |

AND: | TRAVERS WILLIAM DUNCAN First Defendant PETER GRAY Second Defendant SOUTHERN CROSS EQUITIES PTY LTD (ACN 071 935 441) Third Defendant |

and between: | SOUTHERN CROSS EQUITIES PTY LTD (ACN 071 935 441) Cross-Claimant on the First Cross-Claim |

AND: | CASCADE COAL PTY LTD (ACN 119 180 620) First Cross-Defendant on the First Cross-Claim ARTHUR PHILLIP PTY LTD (ACN 100 908 101) Second Cross-Defendant on the First Cross-Claim RICHARD JONATHON POOLE Third Cross-Defendant on the First Cross-Claim |

AND BETWEEN: | PETER GRAY Cross-Claimant on the Second Cross-Claim |

AND: | CASCADE COAL PTY LTD (ACN 119 180 620) Cross-Defendant on the Second Cross-Claim |

JUDGE: | FOSTER J |

DATE: | 5 AUGUST 2015 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 Addenbrooke Pty Limited (Addenbrooke), which is the plaintiff in this proceeding, is the family company of the well-known Sydney businessman and entrepreneur, Denis James O’Neil. Denis O’Neil is accustomed to making investments through Addenbrooke. Denis O’Neil has been a director of Addenbrooke since 1993. He is the Chairman of Directors. He owns all of the issued capital of Addenbrooke, and always has.

2 Denis O’Neil has a son, Ned Arthur O’Neil. In mid-2014, Ned O’Neil was 29 years of age. He finished school in 2002 and then attended the University of Sydney where he gained the degree of Bachelor of Commerce. Before commencing work in the family businesses, Ned O’Neil worked for a short time for Multiplex Constructions as a junior project manager. He has had no other external post-graduation work experience. Ned O’Neil became a director of Addenbrooke in 2009 or 2010 when he was 24 or 25. At all times thereafter, Denis O’Neil and Ned O’Neil have been the only directors of Addenbrooke.

3 Gregory Alexander Smith (Smith) has been the Company Secretary and Financial Controller of Addenbrooke since 2006. Before 2006, he was the Company Secretary of Addenbrooke and a financial accountant employed by it. He commenced employment with Addenbrooke on 23 August 1999. He is not and never has been a director of Addenbrooke.

4 In September or October 2010, Gregory Keith Jones (Jones) mentioned to Denis O’Neil that he (Jones) was involved in a coal deal and that the company involved (Cascade Coal Pty Ltd) (Cascade Coal) was about to undertake a capital raising with the assistance of Southern Cross Equities Pty Ltd (SCE). He told Denis O’Neil that the operative at SCE who would have the carriage of the raising was Peter Gray (Gray). At that time, Gray was SCE’s Director Corporate. Gray was well known to Denis O’Neil. He had been Addenbrooke’s stockbroker for some years.

5 On 17 November 2010, Gray sent an Information Memorandum to Denis O’Neil, Ned O’Neil and Smith. Gray called that memorandum a “deal sheet” and described it as “… a summary of what we will be discussing on Friday”.

6 The essence of the transaction as described in the deal sheet was that Cascade Coal was going to place up to 601,307 new fully paid ordinary shares at $46.57 per share in order to raise a total of $28 million of new capital. In the deal sheet, the following appeared:

Application of Funds

Placement proceeds will be applied to reduce third party debt and creditors

7 The two projects which Cascade Coal then had in mind were the Mt Penny and Glendon Brook projects. In the deal sheet, the authors said:

Cascade Coal Pty Ltd, incorporated in 2006, is focused on the identification and development of Australian coal mining projects. Cascade holds Exploration Licence 7406 (“EL7406” or “Mt Penny”) through its subsidiary Mt Penny Coal Pty Ltd and Exploration Licence 7405 (“EL7405” or “Glendon Brook”) through its subsidiary Glendon Brook Coal Pty Ltd, both located in NSW.

8 In these Reasons for Judgment, I shall refer to the two Exploration Licences mentioned in the deal sheet as “EL7405” and “EL7406” respectively. I shall refer to Mt Penny Coal Pty Ltd as “MPC” and to its sister subsidiary of Cascade Coal, Mt Penny Properties Pty Ltd as “MPP”.

9 On p 1 of the deal sheet, next to a map of NSW and immediately after the text which I have extracted at [7] above, the following corporate chart appeared:

10 At 11.00 am on 19 November 2010, a meeting took place in the board room at the offices of SCE at Level 32, Aurora Place, 88 Phillip Street, Sydney, NSW. The following persons attended that meeting:

Denis O’Neil (Addenbrooke)

Ned O’Neil (Addenbrooke)

Smith (Addenbrooke)

Travers William Duncan (Duncan)

Gray

Rex William Adams (Adams) (SCE)

John Atkinson (Atkinson) (or John Vern McGuigan) (John McGuigan ) (Cascade Coal)

11 There is no dispute that a meeting took place at the offices of SCE at 11.00 am on 19 November 2010 (the 19 November meeting). There is no dispute that the O’Neils, Smith, Duncan, Gray and Adams were present at that meeting. There is a dispute as to whether it was Atkinson or John McGuigan who also attended. Those attendees who gave evidence before me all agreed that the person who attended was either Atkinson or McGuigan. No-one suggested that both of those men attended. Gray and Adams said that the person who attended was John McGuigan while Ned O’Neil sand Smith said it was Atkinson.

12 The 19 November meeting is critical to Addenbrooke’s case. Addenbrooke contends that it was misled at this meeting by Duncan and by Gray.

13 Addenbrooke argues that it was induced to invest in Cascade Coal by representations made at the 19 November meeting and by representations made in the deal sheet. Addenbrooke also complains that it was not told certain matters which, had they been communicated to it, would have caused it not to invest in Cascade Coal. The matters of which they were not told concerned the involvement of the Obeid family in the project.

14 In particular, it is Addenbrooke’s case that, as at November 2010:

(a) Family members of the Obeid family, of which the patriarch was Edward Moses Obeid MLC (Eddie Obeid) and/or corporate or individual nominees of family members of the Obeid family, owned or had a legal entitlement to acquire at their election three rural properties which comprised all or most of the land area over which EL7406 had been granted;

(b) In mid-2009, a company which was the nominee of members of the Obeid family, Buffalo Resources Pty Ltd (Buffalo Resources), had entered into an unincorporated joint venture with Cascade Coal pursuant to which Buffalo Resources was to receive 25% of the proceeds of the development or sale of the Mt Penny coal reserves;

(c) From about the middle of 2010, the directors of Cascade Coal had embarked upon a course of action designed to take out the Obeid family and its nominees as landowners in respect of EL7406 and as joint venturer with Cascade Coal in respect of the Mt Penny coal reserves;

(d) The capital raising in which Addenbrooke was invited to participate was devised and implemented in order to raise sufficient funds for Cascade Coal to enable it to pay out the Obeid family and its nominees and to sever all ties with the Obeid family and its nominees; and

(e) Both Duncan and Gray knew of the matters to which I have referred at subpars (a) to (d) above but did not disclose any of those matters to any of Denis O’Neil, Ned O’Neil or Smith at the 19 November meeting or at any other time. Addenbrooke argues that all of those matters should have been disclosed to it and that, if any one or more of them had been disclosed, it would not have invested in Cascade Coal.

15 I am comfortably satisfied that the evidence tendered before me established the facts and matters summarised in subpars (a) to (d) of [14] above. In truth, in the end, there was no serious contest as to whether those matters had been proven.

16 There was, however, a real and substantial dispute about the matters referred to in subpar (e) of [14]. In particular, the remaining defendants (Duncan, Gray and SCE) and all of the cross-defendants (Cascade Coal, Arthur Phillip Pty Ltd (Arthur Phillip) and Richard Jonathan Poole (Poole)) submitted that Addenbrooke’s case has been heavily influenced by hindsight. Those parties argued that the Court should be wary of allowing its judgment to be influenced by matters which have, since 2010, become matters of considerable notoriety in the public domain in respect of Eddie Obeid and his family and should confine its attention to the facts proven in evidence in this proceeding and nothing else. These cautionary remarks are well made. I am very conscious that I must be careful to ensure that my judgment is based upon only those facts actually proven in evidence before me and not to allow myself to travel beyond those facts. Of course, there is nothing unusual or out of the ordinary about such an approach—it is always the correct approach in every case. But, in this particular case, extra care must be taken to avoid the pitfalls that may be created by the distorting effect of hindsight.

17 The defendants and cross-defendants argued that, despite the evidence to the contrary led by Addenbrooke, in 2010, Denis O’Neil was still the real decision-maker on behalf of Addenbrooke in relation to its investments and that he had been the real decision-maker in respect of Addenbrooke’s investment in Cascade Coal. They then submitted that, even if the Court accepts that he was not told any of the matters referred to in subpars (a) to (d) of [14] above, had he been told all of those matters, he still would have caused Addenbrooke to proceed with its investment in Cascade Coal. This was so because, in 2010, the Obeid name did not carry the kind or level of negative connotations it had come to bear in subsequent years. Those parties submitted that, at the time, Eddie Obeid was known as a power-broker in the Australian Labor Party in NSW but was not then generally seen by the public in NSW as corrupt or dishonest. The defendants and cross-defendants said that, given the short-term nature of Addenbrooke’s investment in Cascade Coal and the real potential for Cascade Coal to unlock the value of the Mt Penny coal reserves by onselling its interests at Mt Penny to a public company, Denis O’Neil and thus Addenbrooke would not have been phased or discouraged by the full disclosure of the Obeids’ interests in the venture and may have even regarded the Obeids’ involvement as a positive factor. After all, Addenbrooke stood to make $2 million on an investment of $8 million in a three to six month timeframe. It was submitted that greed and the love of money were very powerful drivers for Denis O’Neil in 2010 when he was considering this investment. It seemed to him to be a no-brainer. The defendants and cross-defendants also submitted that, in any event, Denis O’Neil had made up his mind to cause Addenbrooke to invest in Cascade Coal before he attended the 19 November meeting. He had done so, it was submitted, because of the influence of Jones with whom he had a close business relationship at the time and because he had made his own assessment of the deal.

18 In order to decide whether Addenbrooke would still have gone ahead had it known all there was to know about the Obeids’ involvement in the venture and in order to explain my conclusion that Addenbrooke has established the facts and matters summarised in subpars (a) to (d) of [14] above, it will be necessary to traverse the facts in some detail.

19 Of the main players in this story, only Denis O’Neil, Ned O’Neil, Smith and Gray gave evidence at the hearing. Adams was also called. But Duncan, John Alan Kinghorn (Kinghorn), John McGuigan, James McGuigan (John McGuigan’s son), Atkinson and Poole did not testify at all. In addition, many other potential witnesses were not called. Neither Eddie Obeid nor any member of his family was called to give evidence. In particular, none of Eddie Obeid’s sons Paul Edward Obeid, Moses Edward Obeid, Edward Joseph Obeid, Damien Edward Obeid or Gerard Obeid testified before me.

20 The absence of so many witnesses has meant that, in many cases, the documents, email communications, correspondence, notes and memoranda tendered in the case fall to be interpreted as part of the documentary jigsaw puzzle placed before the Court by the parties without the assistance of the authors and without explanation from those who theoretically may have been able to explain or qualify them. For the most part, no great difficulty was caused by these circumstances as the documents generally spoke for themselves.

21 On 26 November 2010, Addenbrooke invested a few dollars less than $8 million in Cascade Coal. As matters presently stand, that investment is worthless.

22 Addenbrooke claims declaratory relief and damages equating to its lost $8 million plus interest against Duncan, Gray and SCE. It had originally sued others—Arthur Phillip, Arthur Phillip Nominees Pty Ltd (APN), Cascade Coal, Poole, John McGuigan, Atkinson, Kinghorn, Coal and Minerals Group Pty Ltd (CMG) and Amanda Poole, Poole’s wife—but subsequently settled with all of those parties. It relies upon ss 12DA, 12GF, 12GB and 12GM of the Australian Securities and Investments Commission Act 2001 (Cth). It also relies upon a common law action in negligence as against SCE and Gray.

23 Gray and SCE have brought Cross-Claims against Cascade Coal, Arthur Phillip and Poole by which they seek to offload to those parties some or all of any liability which they are found to have to Addenbrooke.

24 Thus, at the end of the hearing, the active parties in this proceeding were:

Addenbrooke (plaintiff);

Duncan (first defendant);

SCE (third defendant and cross-claimant in the First Cross-Claim);

Gray (second defendant and cross-claimant in the Second Cross-Claim);

Cascade Coal (the first cross-defendant in both Cross-Claims);

Arthur Phillip and Poole (the second and third cross-defendants in the First Cross-Claim)

The Obeids, Cascade Coal and Mt Penny—The Early Period (September 2007–September 2010)

25 The narrative set out in this section of these Reasons for Judgment and the findings made therein are based entirely upon the documents ultimately admitted into evidence as Exhibit E and inferences drawn from those documents. No witness who might have spoken to this period and addressed the relevant documents was called by any party.

26 By Contract for Sale of Land made on 27 September 2007, Locaway Pty Ltd (Locaway), as trustee for the Moona Plains Family Trust, agreed to purchase for $3,650,000 the rural property at Bylong known as “Cherrydale Park”. Bylong is in the centre of the area over which EL7406 was granted. The vendor was John Howard Cherry. Under the contract, settlement was to take place on 15 November 2007. The vendor agreed to finance part of the purchase price. The contract contained a confidentiality clause. The two directors of Locaway who executed the contract on its behalf were Damian Obeid and Paul Obeid. The guarantors named in the contract were Paul Obeid, Edward Joseph Obeid, Damian Obeid and Moses Obeid—four of Eddie Obeid’s sons. I infer that Locaway was a company owned and controlled by the four Obeid sons named in the contract or which acted as their nominee in the transactions.

27 On 22 July 2008, Warwick Grigor, in his capacity as Chairman of Monaro Mining NL (MMNL) wrote to Mr Gardner Brook (Brook), who was at the time a senior executive at Lehman Brothers, confirming that MMNL was seeking to bid for coal exploration licences in New South Wales. Grigor said that MMNL was seeking the support of Lehman Brothers to tender for certain thermal and coking coal tenements which were expected to be promoted via a closed tender process within 30 days after the date of the letter. He said that while Monaro RO (MRO) was a listed company with the ability to raise equity capital through the issue of shares, he believed that Lehman Brothers’ participation as a principal with MRO in tendering would better distinguish the bid application. He said:

In return for Lehman Brothers participation with MRO through the tender process, we propose that Lehman Brothers would be issued an option for 60% of the issued shares in the bid company Special Purpose Vehicle (SPV). The option would be issued to Lehman Brothers for $1 and would only be exercisable upon a bid being successful. Lehman Brothers would have the right to transfer all or part of its option or shares post conversion.

The option could also be exercisable over a direct equity in the licence as opposed to shares in the subsidiary company, at your election.

At all times, including once a bid is won, Lehman Brothers would maintain the right of first refusal to provide or arrange capital for the purpose of developing a mine asset. Lehman Brothers would be under no obligation or capital or advice at any time.

28 In an internal document prepared at Lehman Brothers on 23 July 2008 and sent by Pryor, an employee of Lehman Brothers, to Brook, Pryor recorded:

Monaro has become aware of certain tenements that are expected to come up for closed government tender in the next few days, and is seeking our financial support as per their written offer (attached) to make bids for Exploration Licences. Monaro has also (unofficially) identified a party whom is currently the holder of land parcels which are anticipated to be crucial to the successful development of coal tenements. The “land related” party is seeking to participate in the ownership of a mine and accordingly provide favourable to terms to any land reclamation in the event a mining license [sic] is awarded. To this end, it is proposed that Lehman Brothers would receive a 20% option over the shares in a successful JV bid SPV with Monaro, and a further option for 40% of the SPV shares would be issued to the land related party.

29 In the document in question, Pryor depicted this scenario in a table following immediately after the paragraph which I have quoted. Obviously, the “‘land-related’ party” referred to by Pryor was Locaway. I infer from the contents of the document referred to at [28] above that both Pryor and Brook knew that members of the Obeid family were ultimately in control of the land referred to and that the Obeids wanted a stake (40%) in the mining venture.

30 Pryor continued:

In return for Lehman Brothers participation with Monaro through the tender process, Lehman Brothers would be issued an option for 20% of the issued shares in the bid company Special Purpose Vehicle (SPV). The option would be issued to Lehman Brothers for $1 and would only be exercisable upon a bid being successful. An option on similar terms will be issued to the Land Related Entity.

Should an exploration license [sic] be granted it is anticipated that Lehman have the option to fund exploration and feasibility study expenditure in order to increase its ownership in Monaro Coal. The terms of such an agreement are still to be negotiated.

31 In the document, Monaro Coal is identified as the bid SPV.

32 On 25 July 2008, Chris Rumore, a partner at Colin Biggers & Paisley, lawyers, met with Gerard Obeid and possibly Moses Obeid and Paul Obeid.

33 On Monday 28 July 2008, Rumore reported to Gerard Obeid, Moses Obeid and Paul Obeid informing them that:

(a) Colin Biggers & Paisley had ordered two companies, in respect of one of which Greg Skehan would be the sole director and shareholder (which company will enter into the option for the shares in Monaro Coal (Aust) Pty Ltd) and the other in respect of which Rumore would be the sole director and shareholder and which entity would acquire the properties as trustee for Equitexx Pty Ltd as trustee for the Obeid Family Trust No 2.

(b) Rumore had sent faxes that day to the solicitors for the “various vendors” requesting amendments to the contract and two options.

(c) Rumore noted that the recipients of the email were to check the schedule of improvements and inclusions annexed to the largest contract being the contract for the purchase from TE O’Brien (Merriwa) Pty Ltd. Rumore requested any suggestions for amendments.

(d) Rumore confirmed that the cheques for the option fees for the two O’Brien options and the deposit cheque for the purchase from the estate of Stanmore needed to be drawn on the bank account of the relevant company. He undertook to provide the necessary details.

34 On 30 July 2008, Rumore reported to Gerard Obeid, Moses Obeid and Paul Obeid that the company which would acquire the properties at Bylong (in respect of which Rumore would be the shareholder and director) was Geble Pty Ltd (ACN 132 441 877) (Geble) and that the company which was to take the option in respect of the shares in Monaro Coal (Aust) Pty Ltd (in respect of which Greg Skehan will be the director and shareholder) was Voope Pty Ltd (ACN 132 441 868) (Voope). As at 30 July 2008, there were three transactions in prospect: a purchase of a rural property from the estate of the late KJ Stanmore, an option to purchase a rural property from TE O’Brien and an option to purchase an additional rural property from TE O’Brien (Merriwa) Pty Ltd.

35 Each of Geble and Voope was registered on 28 July 2008.

36 In its monthly Exploration Status Report (Group Projects) of August 2008, MMNL recorded the following:

4. NSW Coal

Activities

A new company Monaro Coal Pty Ltd (MCP) was registered to deal with a potential coal opportunity in NSW. Monaro was recently approached by Middle East interests via Leahman [sic] Brothers Australia Pty Ltd with the view to acting as the public face of a consortium wishing to tender for large coal deposits in NSW. To facilitate this process, an option deed was executed between Monaro Mining NL and Voope Pty Ltd (VPL), which will enable the latter to exercise an option to purchase shares in MCP in the event that MCP secures coal mining rights in NSW. MCP would end up with a minority interest in one or more potentially large coal deposits.

At the same time, advice from the Department of Primary Industries (DPI) regarding the Company’s direct approach to them regarding coal areas in the Western Coal Fields of NSW, suggests that it will be another month or 2 before the Company is advised about its request to secure ground in this area.

Schedule

Awaiting futher [sic] developments regarding MCP and a response from the DPI.

37 By contract for sale of land dated 6 August 2008, Geble agreed to purchase from the estate of the late KJ Stanmore the property at Bylong known as “Donola” for $600,000.

38 On the same day (6 August 2008), Geble entered into a Call Option Agreement dated that day with Terence Edward O’Brien. By that Agreement, Geble was granted the right to call for the transfer of a rural property owned by O’Brien for the total consideration of $73,678 (including the call option fee). The Call Option Agreement contained a confidentiality clause.

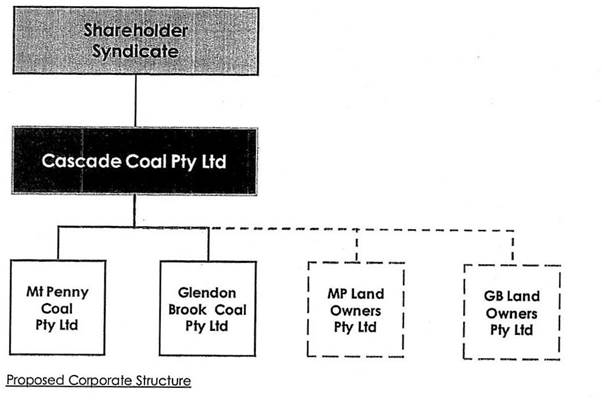

39 By a second Call Option Agreement made on 6 August 2008, Geble required the right from TE O’Brien (Merriwa) Pty Ltd to secure the transfer of a second property at Bylong being “Coggan Creek”. The acquisition price was $3,481,218.30 (including the call option fee).

40 By a Deed made on 20 August 2008 between MMNL and Voope, MMNL agreed to grant to Voope an option to acquire 80% of the fully paid ordinary shares in MCP upon the terms and conditions more fully set out in that Deed. The recitals in the agreement recorded that Voope was assisting MCP in relation to an application in respect of a tenement described as:

… the mining lease, exploration licence or any other mining interest applied for pursuant to the invitation to tender issued by the Department [of Primary Industries] at any time after the date of this document but prior to 1 January 2009 and granted pursuant to the [Mining Act 1992 (NSW) and any regulations or ordinances made pursuant to it] in [NSW] for the exploration or mining of coal.

41 No money was to change hands for this benefit granted to Voope. The consideration was described as “the provision of consultancy, general assistance and advisory services by or on behalf of [Voope] or at the direction of [Voope] for the benefit of [MMNL] and [MCP]”. The option granted by this document was to be kept open for a period of three years.

42 Thus, by the end of August 2008, companies controlled by members of the Obeid family had acquired or had the right to acquire Cherrydale Park at Bylong, Donola at Bylong and Coggan Creek at Bylong. The total cost to those companies of those acquisitions was a little over $7.8 million. In addition, Voope had placed itself in the position to control the mining venture then contemplated by MMNL.

43 By letter dated 9 September 2008, the Department of Primary Industries (DPI) invited MMNL “to participate in Expressions of Interest for coal Exploration Licences, in accordance with the Mining Act 1992, in one or more exploration areas, in the Sydney and Gunnedah Basins as follows”. [There followed a list of 11 coalfields of which one was the Mt Penny coalfield.]

44 The letter from DPI went on to say that only companies who had been invited to lodge an expression of interest may respond to its letter. Invited parties who decided to respond were required to submit their expression of interest to the DPI with details of an exploration and development program. The closing time and date for expressions of interest was said to be 12 noon on 24 November 2008.

45 By notice dated 6 November 2008, Geble, through its nominee Coopers World Pty Limited (ACN 133 940 388), exercised the call option granted to it pursuant to the Call Option Agreement dated 6 August 2008 between it and TE O’Brien. On 7 November 2008, a contract for the sale of part of the property known as Coggan Creek at Bylong was entered into between TE O’Brien (Merriwa) Pty Limited and Coopers World Pty Limited for the purchase price of $3,427,359.

46 By a Deed of Variation of Option over Shares entered into between MMNL and Voope on 22 December 2008, MMNL and Voope agreed to vary the definition of “Tenement” in the principal deed dated 20 August 2008 by removing all reference to the date “1 January 2009” in that definition.

47 The effect of that change was to leave open the arrangements between the parties indefinitely.

48 On 14 January 2009, James McGuigan, who is the son of John McGuigan, sent an email to Poole, John McGuigan and Atkinson. The email said that attached to it was the “NSW Coal Allocation – 9 January.pdf”. The email was in the following terms:

John, John and Richard

Yesterday we received the Expression of Interest Information Pack from the NSW Department of Primary Industry. It is attached, but the key points are:

– The 4 medium and 7 small allocations from our previous meeting are on the table.

– This includes the Mt Penny and Spur Hill areas that we were previously of the view that there had been a deal done for them.

– This does not include the other major coal allocation (Bennalbri) in the Gunnedah Coalfield

– The expression of interests are to be submitted by 16 February

As discussed before the Director General (Dr Richard Sheldrake) will make his recommendation to the Minister (Ian McDonald) in relation to rewarding the licence. The evaluation criteria is quite detailed, and we will most likely have to engage the services of a mine/exploration consultancy firm to assist us with the exploration program, mine development proposal, infrastructure plan etc…I have arranged a meeting with Behre Dolbear for early next week, however if you guys have other consultants that you think may assist please let me know.

Each submission will cost approx $11,000 to submit, further if are awarded the licence a one off payment for the area is required to the DPI’s Coal Development Fund:

– Spur Hill $1.5

– Mt Penny $1m

– Glendenbrook $300k

Additional financial contributions may be included as part of an applicant’s Expression of Interest.

Moving forward, John M is arranging a meeting with Greg Jones for this Saturday to figure out if the Mt Penny and Spur Hill areas have effectively already been allocated. If this is the case, from our meeting in November we were thinking:

– Glendenbrook for Redman Mining

– Spur Hill for Cascade Coal

Both of those are Hunter Coalfield areas. We may want to revisit the WEC/Cessnock leverage point here. Further, both areas are close to Coal and Allied mines.

I have attached the information package (Atko I sent one to North Sydney attention to John M). Below is also the article from December 30 referring to Ian McDonald’s allegations of buying personnel items on ministerial credit cards.

I propose we arrange a meeting on Monday, after Saturday’s meeting to set a plan for the following 3 weeks.

Please give me a call if there is anything else.

James McGuigan

Arthur Phillip Pty Ltd

Level 33 Colonial Centre

52 Martin Place

Sydney NSW 2000

Accused minister Ian Macdonald likely to be cleared by inquiry

NSW Primary Industry Minister Ian Macdonald is set to be cleared of an accusation that he bought a $1299 LCD television for himself using taxpayers’ money.

The Australian learned last night an internal inquiry by the Department of NSW Premier Nathan Rees had determined that key aspects of the allegations – first aired in a Sunday newspaper earlier this month – were unsubstantiated.

The newspaper reported that Mr Macdonald used a departmental credit card in 2005 to pay for the TV with built-in DVD player, despite ministerial use of corporate cards having been banned in 1995. It said the TV had been in Mr Macdonald’s home but was subsequently moved to his office.

Mr Macdonald’s name and private mobile number were included on a purchase order from Bing Lee, Burwood, that was leaked to The Sunday Telegraph. However, a spokeswoman for Mr Rees said that, while the inquiry was yet to be finalised, “so far it’s found that the statement he bought the TV on a credit card is false”.

The spokeswoman also said the TV was never in Mr Macdonald’s home. She said the inquiry would be concluded soon but that the findings so far were “pretty conclusive”.

The finding marks a reprieve for Mr Rees, who has had to sack two ministers for misbehaviour. Former police minister Matt Brown was dismissed in September after it was revealed he had danced at a party in Parliament House in his underpants. Former medical research minister Tony Stewart was sacked last month for verbally intimidating a female staff member at a public function.

49 In the email, James McGuigan referred to a newspaper article involving the NSW Primary Industry Minister, Ian Macdonald. The allegations referred to in the newspaper article concern the misuse of a departmental credit card. It also appears that, from at least January 2009, James McGuigan was employed by Arthur Phillip.

50 On 3 February 2009, Michael Johnstone (Johnstone), a mining engineer with whom Duncan had had dealings from time to time, sent an email to Duncan with a copy to James McGuigan. The subject matter of that email was said to be “Coal area release”. The email was in the following terms:

Travers

I had a telecon this afternoon with James, John and Richard.

My preferences are Vickery South, Mount Penny and Glendon Brook. The latter is very tough but would like to keep it in at this stage.

Vickery south presents a small OC <30mt inferred at grass, but coal quality is very good 5-9% ash raw. Whitehaven will be looking at this after they got access to Vickery ML consent late last year.

Mount Penny, presents a larger resource say 50-150Mt of OC and UG coal. Ulan seam is target, with upper half of seam better quality 17-25% ash raw. Rail runs through northern part of EL Tenement bounds Anglo area, which DPI believe has not been tested and may have significant low ash resource in lower seam. Anglo will come under pressure to renew this EL.

DPI advise that a property called “Cortina” owned by Bruce Reid, was the target for regional coal exploration program sponsored by Macgen in Mt Penny area. Ive asked James to check this property location.

Glendon Brook is former HWE EL, on its own not much opportunity. Too much road to get to rail. However, Mitchells flat has resources next door, I think Xstrata have this now, and may bail out. If this is the case there may be opportunity for a mini power plant. Im thinking in terms of cost of rail contruction [sic] (12km), versus installed cost per MW of power generation, a 25 to 50 MW plant may stand up.

Intention is to have broad outline for three areas by Monday and discuss PM. I suggested some financial “engineering” say a multiplier for 1, 2 or 3 properties with a Macgen incentive. You all should look at this, and CSIRO collaboration.

John will [sic] to do some research on Spur Hill. From geological point there are mineable resources, though Arrowfield winery may be an issue!!

Mining technology [sic], should include a heavy tilt at local content and job creation.

Post discussion with Cascade I have arranged through A Wells, some words on local environment issues etc. I am aware that Alan was on Singleton Local government, when Peter Murray tried to get Mitchells Flat going. He has some documents which may be usefull [sic].

Alans time has been capped to four days, and Ive asked him to bill this. Would it be easier for him to invoice me or Cascade? Can you give me some direction in this regards?

Mike

51 On 4 February 2009, James McGuigan passed on to Poole, John McGuigan and Atkinson the email which he had received the day before from Johnstone. In his covering email, after referring to Glendon Brook and Vickery South coalfields, James McGuigan said that he would not begin work on Mt Penny “until after the discussion with Greg Jones”.

52 The reference to a discussion with Jones in that email appears to be a reference to the planned meeting between John McGuigan and Jones to which reference had been made in earlier emails.

53 On 16 February 2009, by letter dated that day, on the letterhead of Cascade Coal, John McGuigan wrote to the Executive Director, Mineral Resources of the DPI, submitting an expression of interest for the Mt Penny Exploration Area in response to the request published by the DPI on 9 January 2009. That letter was in the following terms, omitting formal parts:

Re: Expression of Interest – Mt Penny Exploration Area

Cascade Coal Pty Limited (“Cascade Coal”) is pleased to submit an Expression of Interest for the Mt Penny Exploration Area in response to the request published by the Department of Primary Industries on 9 January 2009.

Cascade Coal has been specifically established to engage in greenfields exploration and developments within the coal sector preferably in New South Wales. You will note from the materials attached that the shareholders of Cascade Coal have significant experience in the coal sector and have been associated with large scale developments of coal properties in Australia and overseas. Cascade also currently has an active exploration program and holds a number of highly speculative tenements in Victoria referable to Brown Coal deposits.

The shareholders of Cascade are committed to developing a coal project and have committed to inject sufficient capital to meet the up front fees and initial Program of Works as required in the event that Cascade is successful with its application. In this regard the shareholders have secured an underwriting from the investment bank Arthur Phillip Pty Ltd to underpin their commitment.

In addition having regard to both the experience and expertise of the shareholders in raising substantial development capital in the coal sector the shareholders are confident that the necessary capital to enable the development of the above areas will be raised on a timely basis. Our submission for the area addresses in some detail the relevant exploration program, the proposed mine development methodology, the relevant infrastructure, the required mitigation of greenhouse gasses, other environ-mental concerns and the benefits to local and regional communities.

We look forward to the opportunity of discussing the attached expressions of interest with you. Our nominated contact person is Michael Johnstone who may be contacted on [phone numbers omitted].

54 The Expression of Interest document is a document of 31 pages in which Cascade Coal set out its plans for the Mt Penny tenement as well as details of the shareholders of Cascade Coal. These shareholders were identified in the Expression of Interest document as Messrs Kinghorn, John McGuigan, Atkinson, Poole and Duncan. The document also contained details of Cascade Coal’s work program and mining methods intended for the site.

55 Messrs Duncan, Kinghorn, John McGuigan and Atkinson were appointed directors of Cascade Coal on 19 February 2009.

56 In May 2009, the DPI prepared a confidential evaluation of the expressions of interest received in respect of a number of NSW coal areas. In that document, in respect of Mt Penny, the author of the document recorded that it (the DPI) had received expressions of interest from four entities including MMNL and Cascade Coal. The author said that the submission made by MMNL was considered to be far superior in terms of its proposed technical program and additional financial contributions of $25,000,000 upon the grant of an exploration licence. The author went on to make favourable comments about MMNL’s program of exploration and conceptual mine development proposals. The evaluation team considered that the MMNL expression of interest was superior to other expressions of interest.

57 By email sent on 20 May 2009, Moses Obeid provided some preliminary information on Go Radar to John McGuigan and Jones.

58 At the meeting of its directors held on 22 May 2009, MMNL decided to abandon its “NSW Coal Project”. The meeting was attended by Messrs Malone, Rampe and Barns. The Minutes recorded the following matters:

Opening address

The Chairman referred to the discussion between the Directors and Gardner Brook held immediately prior to the Board Meeting in reference to the NSW Coal Project and the Expressions of Interest submitted by the Company. In summary, the Chairman indicated that the NSW Government’s requirement to have all fees and contributions paid within 30 days of offer placed the Company at too great a risk, should the Company fail to source the funds required. It was considered that the possibility of raising the funds nominated in the Expressions of Interest within the time frame suggested would be extremely difficult if not impossible. Given this very significant change to the anticipated strategy, the Chairman suggested that the Coal project was no longer viable.

The Chairman noted the request from Gardner Brook representing Voope Ltd, who had expressed the desire to attempt a salvage of the coal project (in particular Mt Penny), given their significant exposure to the project.

A discussion was then held between the directors during which time, various views were expressed.

Resolution

Resolved: to abandon the project, contingent upon the following:

Voope to provide a new agreement outling [sic] a satisfactory mechanism for transferring any licences that may be awarded away from Monaro Mining and holding Monaro Mining harmless in all aspects;

Voope to reimburse Monaro expenses, should it be successful in securing a coal licence

The Chairman advised that he would report the result of the meeting to Mr M Duncan. The Chairman felt that Mr Duncan would be sympathetic to the above resolution. A circular resolution would be distributed to all directors giving effect to the above resolution.

Next meeting

To be advised

Closure

There being no further business the Chairman declared the meeting closed at 10.45 am.

59 It appears that Brook had attended at the offices of MMNL immediately prior to the directors’ meeting in an endeavour to ensure that Voope did not lose its interest in the Mt Penny project. I infer that, by 22 May 2009 at the latest, Brook was acting as the agent of and in the interests of the Obeid family, in particular, the four sons who had been involved in the land acquisitions at Bylong.

60 It appears that, by late May 2009, Johnstone began to wonder whether there were links or associations between Cascade Coal and MMNL. He raised this with James McGuigan in an email sent at 6.47 pm on 25 May 2009. In response to that email, James McGuigan said that there were no links or associations between Cascade Coal and MMNL. He went on to say:

There was the proposal of a deal to be brokered last week, where we would take 90% of Mt Penny and a Monaro associate would take 10%.

What’s going on behind the scenes is that we are trying to raise the question on Monaro’s ability to raise finances, especially after they have committed on each EOI.

That’s just between you and me.

I think our stance is that we’re not going to negotiate anymore.

Let’s see how it plays out.

61 Johnstone reverted to James McGuigan by saying that his email had “clarified some of the mixed spiel that he had been getting”.

62 At 10.18 am on 1 June 2009, John McGuigan sent an email to his son James McGuigan to which was attached a document headed “Key Principles – 31-05-2009”. That document is in the following terms:

Key Principles

l. Acquire land from landowners at a consideration equal to the assessed value of the land for agricultural purpose together with a premium that reflects the marketplace assessment for a sale of agricultural land to the holder of Mining Rights.

2. The contract to purchase and the determination of the consideration to be formally entered into within 90 days of the award of the Exploration License for Mount Penny to Cascade Coal Pty Ltd (“Cascade”).

3. Title and ownership in the properties owned by the landowners will remain with the land owners until completion.

4. Completion will take place within 90 days of the grant to Cascade of its application for a mining lease over Mount Penny and any additional contiguous areas.

5. The landowners and in particular UPG Pty Ltd (“UPG”) will fully cooperate with Cascade in its pursuit of the grant of a Mining Lease.

6. In recognition of UPG’s position as the key land holder Cascade will grant UPG or its Nominee a 25% interest in the Joint Venture Company formed to hold the Exploration License over Mount Penny and to pursue the grant of a mining lease and subsequent mining operations.

7. UPG or its Nominee will not be required to make any contribution to the costs of the Joint Venture up to the time of the grant of a Mining Lease. For the avoidance of doubt the costs will include the exploration costs, the costs associated with the development application for the Mining Lease and the costs in purchasing the land.

8. Once the Mining Lease is granted, UPG or its Nominee will be required to make its proportionate contribution to all costs of the development of Mount Penny or be diluted in accordance with the provisions of the Joint Venture governing the development of Mount Penny.

9. Cascade agrees to seek the grant of an Exploration License or other rights over areas contiguous to Mount Penny should they become available. To the extent that either Cascade or the Joint Venture Company acquires the rights over the contiguous areas, UPG or its nominee will be entered to a 25% interest.

10. In the principles outlined in paragraphs 7 and 8 with respect to Mount Penny will apply equally to any contiguous areas.

11. UPG or its nominee will be entitled to participation on the board of the Joint Venture Company to an extent to commensurate with its equity interest.

63 The essence of the deal embodied in this email was:

(a) Cascade Coal or its nominee would acquire all of the Bylong land owned by the Obeid nominee companies;

(b) The Obeid interests would be awarded a 25% interest in a joint venture company to be formed to hold the exploration licence over Mt Penny and to pursue the grant of a mining lease and subsequent mining operations;

(c) The Obeid interests would not be required to contribute to the initial costs being the exploration costs, the costs associated with the development application for the mining lease and the costs of purchasing the land. Once the mining lease is granted, the Obeid interests would have to pay 25% of the costs of development incurred thereafter.

64 The reference to “UPG” in the email is a reference to United Pastoral Group Pty Limited (UPG), an Obeid-controlled company.

65 By an email sent from Brook to James McGuigan at 5.18 pm on 1 June 2009, Brook passed on to James McGuigan his email address for him to send the first draft. He did not identify the subject matter of that draft. He then said:

Monaro completed all that I indicated today, and the share transfer will occur tomorrow.

I’ll send the relevant letters and agreement showing that we now have control of the bids.

66 At 6.43 pm on 1 June 2009, James McGuigan sent an email to Jones, John McGuigan and Poole. Attached to that email were documents described in the following terms: “Cascade Coal Letter – Land Owners.docx (31.54 kB); Cascade Coal Letter – Equity.docx (32.48 kB)”. The email was in the following terms:

Greg, John and Richard

Please find attached two Letters of agreement:

1) Letter of Agreement between Cascade Coal Pty Ltd (“Cascade”) and United Pastoral Group Pty Ltd, Geble Pty Ltd, Coopers World Pty Ltd [collectively “the Landowners”].

2) Letter of Agreement between Cascade Coal Pty Ltd (“Cascade”) and the (“Nominee”], collectively (“the Parties).

I have had a discussion with Mo, but am yet to receive what Nominee company they want to do it with, as well as any of the Land Agreements as promised from Paul.

Key changes made to these agreements include:

1) We have agreed to form a Joint Venture instead of a Joint Venture Company with the Mount Penny asset to sit in Cascade

2) With regards to Gardner’s comment about whether money in – will be treated as debt or equity, the following was inserted

“The Nominee acknowledges it has received consideration for the relevant land and that any contributions up to the grant of the Mining Lease shall be treated as shareholder loans and repaid out of profits in due course.”

Of immediate importance is the issue regarding as to what the multiplier which will be applied to the agricultural land – let’s discuss this.

Greg, we will discuss this tomorrow @ 11:30 at Arthur Phillip’s offices which are: Level 33, 52 Martin Place (Colonial Centre)

John, although documents are attached here I will resend as emails so that you can read on Blackberry. Please call me when you can.

In other news, Monaro completed all that they indicated yesterday – today, and the share transfer will occur tomorrow.

It will be a 100% entity owned by Gardner known as Royal Coal.

Cheers

67 The reference to “Mo” in that email is clearly a reference to Moses Obeid. I say this because earlier references to “Mo” in emails from Mr Rumore were sent to Streetscape, a business operated by Moses Obeid. In addition, in the same breath as referring to “Mo”, James McGuigan also referred to “Paul”. I infer that that reference was a reference to Paul Obeid.

68 The letter agreements attached to this email were agreements whereby Cascade Coal agreed to acquire the three properties referred to in the letters. These were the properties owned by UPG, Geble and Coopers World Pty Ltd which had previously been acquired from the estate of KJ Stanmore, TE O’Brien and TE O’Brien (Merriwa) Pty Ltd. The second draft attached to James McGuigan’s email dealt with a proposed joint venture between Cascade Coal and a corporation to be nominated by Moses and Paul Obeid. This joint venture letter was in the following terms:

Dear Sir DRAFT

Re: Letter of Agreement between Cascade Coal Pty Ltd (“Cascade”) and the [“Nominee”], collectively (“the Parties”)

I refer to our recent discussions in relation to Cascade’s intention to acquire a land interest in the Bylong region and to be granted an exploration licence (“the Exploration Licence”) and mining lease (“the Mining Lease”) over the Mount Penny area, and the letter of agreement between Cascade and the Landowners, dated 2 June 2009. Cascade has submitted an expression of interest requesting to be granted an Exploration Licence over the Mount Penny area.

Subject to the grant of the Exploration Licence, the Parties have agreed to form a Joint Venture (“JV”) to explore and develop the Exploration Licence and pursue the granting of the Mining Lease, in addition the JV will pursue the grant and issue of all relevant exploration licences and mining leases for any additional contiguous areas to Mount Penny.

Obligations of the Party’s

In recognition of the Nominee’s position as the key owner of land in the Mount Penny area and in consideration of the Nominee:

• and its associates or related parties undertaking not to pursue the grant of any mining rights to the area or any contiguous area;

• agreeing to assist Cascade to explore and develop the Exploration Licence and Mining Lease;

• agreeing to make available and provide their expert knowledge of the area to assist with further exploration and review of the contiguous areas:

Cascade will agree to grant to the Nominee a 25% interest in the JV on the basis that the Nominee does not have to make any contribution to costs up to the grant of the Mining Lease.

Obligations of the Nominee

For the avoidance of doubt, prior to the granting of the Mining Lease the Nominee will not be liable to contribute to the exploration costs, the costs associated with the development application for the Mining Lease and the costs in purchasing the relevant land situated at Mount Penny. The Nominee acknowledges it has received consideration for the relevant land and that any contributions up to the grant of the Mining Lease shall be treated as shareholder loans and repaid out of profits in due course.

Once the Mining Lease is granted, the Nominee will be required to make a contribution to all costs of the development of the commercial mining operations in Mount Penny proportionate to the Nominee’s equity interest in the JV. Failure to contribute costs proportionate to the Nominee’s equity percentage will result in the Nominee’s interest in the JV being diluted pro rata in accordance with the provisions of the JV agreement governing the development of commercial mining operations in Mount Penny.

Contiguous Areas

If from time to time, the NSW Department of Primary Industries seeks expressions of interest from parties for the granting of a [sic] exploration licence, mining lease or any other mining interest for land that is contiguous to or adjoining or relevant to the future development of Mount Penny (“Contiguous Area”), Cascade on behalf of JV must use its best endeavors to become the successful applicant in any such exploration licence, mining lease or mining interest. To the extent that Cascade acquires the rights to pursue a mining interest over the contiguous areas, such areas shall be added to the JV.

The principles outlined above under the section “Obligations of the Nominee” with respect to contribution of costs relating to the development of a commercial mine at Mount Penny, will apply equally to the Contiguous Area.

Management of the Joint Venture

The Nominee will be entitled to participate on the board of JV to the extent to commensurate with the Nominee’s equity interest in JV.

The Nominee will be entitled to participate in the management of JV to an extent to [sic] commensurate with the Nominee’s equity interest in JV

Confidentiality

Except as expressly permitted by this Letter of Agreement, Cascade and the Nominee undertake and agree to hold each of the terms in this Letter of Agreement in strict confidence and not to disclose or discuss any Confidential Information to or with any person except, in accordance with this Letter of Agreement or as otherwise permitted by Cascade or the Nominee.

Cascade and the Nominee will ensure that no Confidential Information is photocopied, reproduced or recorded in any manner except to the extent that is necessary to provide such number of copies as are reasonably required by either Cascade or the Nominee.

Cascade and the Nominee will not use or disclose the Confidential Information or any part of it to gain any commercial, financial or other advantage for itself or any other person or to the competitive disadvantage or otherwise to the detriment of either Cascade or the Nominee.

Executed as an Agreement

Signed for and on behalf of

Cascade Coal Pty Ltd

ACN 119 180 620

Director Director

Name of Director Name of Director

(BLOCK LETTERS) (BLOCK LETTERS)

Signed for and on behalf of

[“Landowners”]

ACN [ ]

Director Director

Name of Director Name of Director

(BLOCK LETTERS) (BLOCK LETTERS)

69 By letter dated 1 June 2009 sent to the DPI, MMNL requested that all exploration licences which are granted to it pursuant to the expressions of interest currently lodged with the DPI be issued to its nominee company “Royal Coal Pty Ltd” (Royal Coal). MMNL then said that the ownership of Royal Coal would be transferred to Voope which was described as the financial partner in MMNL’s consortium. The author of the letter went on to say that it was intended that MMNL would provide consultancy services to Royal Coal via a management agreement should Royal Coal be awarded any exploration licences.

70 A later version of that letter was tendered in evidence. That version is dated 2 June 2009. It appears to be in the same terms as the earlier letter dated 1 June 2009 with the exception that the reference to “Royal Coal Pty Ltd” was altered to “Loyal Coal Pty Ltd” (Loyal Coal).

71 At 2.37 pm on 2 June 2009, Moses Obeid sent an email to James McGuigan which was in the following terms:

James

As discussed I have included a copy of the Landowners agreement.

The multiple falls under 1.1 definitions clause ‘Criteria’.

The name of the entity being used by Gardner for the JV is BUFFALO RESOURCES PTY LTD.

I await you [sic] draft agreement.

Cheers

72 By an email sent at 3.09 pm on 2 June 2009 by James McGuigan to Moses Obeid and Brook (copied to John McGuigan and Poole), James McGuigan sent the final form of the two Cascade Coal letters which had been the subject of consideration as drafts the day before. It would appear that Moses Obeid had received a revised draft of the landowners’ letter earlier that day.

73 Later in the day on 2 June 2009, a meeting was arranged at the offices of James McGuigan for 10.00 am on 3 June 2009. It was expected that that meeting would be attended by Brook, Moses Obeid, Poole and James McGuigan.

74 On 2 June 2009, Voope entered into a deed with MMNL. The recitals to that deed recorded the fact that Voope and MMNL had entered into an option deed in respect of certain shares in MCP (as controlled by MMNL) and that the parties agreed to release each other from their obligations under that option agreement. The deed recorded that MCP was to be renamed Loyal Coal Pty Ltd and that MMNL was to ensure that any exploration licences were granted in the name of Loyal Coal Pty Ltd. The commercial deal recorded in the document seemed to be that, in consideration for MMNL transferring all of its shares in Loyal Coal Pty Ltd to Voope, Voope would pay MMNL the sum of $1 and keep MMNL indemnified against all claims, liabilities or causes of action arising from Loyal Coal becoming the successful bidder in respect of the relevant exploration licences. This deed formalised the transfer of control and ownership of Loyal Coal Pty Ltd from MMNL and possibly others to Voope alone.

75 By an email sent by John McGuigan to James McGuigan at a time when John McGuigan was overseas at a resort called Tabang in Indonesia apparently sent at 8.46 pm on 2 June 2009 and headed “CC – update”, John McGuigan said to his son:

Call me after your meeting.

I had a detailed discussion with Travers and we are on the same page.

Once you have the land owners agreement we need to verify title etc.

It is important we don’t give up on clause we inserted today re trigger of land purchase.

I am around now if you pick this up.

Tabang unbelievable.

76 I infer that John McGuigan brought Duncan up-to-date with Cascade Coal’s dealings with the Obeids. No doubt they discussed the form of the two letters in play at that time and the commercial arrangements embodied therein.

77 That email from John McGuigan was sent in response to an email from James McGuigan sent an hour or so earlier in which James McGuigan reported that there was to be a meeting at 10.00 am on 3 June 2009 in Sydney. He makes reference to “they” in his email to his father. It is perfectly plain that the “they” to which reference is made in that email are Moses and Paul Obeid. This much was made clear in an email sent by James McGuigan to Jones at 4.52 pm on 2 June 2009 where he said that he had sent the Letters of Agreement “to the boys”. In an email, he said to Mr Jones:

Not sure if you want to come to the meeting – just letting you know so you are up to date with the events.

78 At 5.57 pm on 3 June 2009, James McGuigan sent updated Letters of Agreement to Moses Obeid and Brook with copies to his father, Jones and Poole. In that email, James McGuigan said:

… Let’s aim to sign at Kent St on Friday at 12:00.

79 In the email, he continued as follows:

Before that happens we are going to need to gain comfort on the following issues:

- the formal definitions of the land parcels that are referred to in the opening paragraph of the Landowners Agreement (highlighted in the attachment)

- the addresses of the land holdings of the three Landowners properties, so that I can conduct a Title Search;

- to confirm the existing mortgage agreements;

- John McGuigan and Travers Duncan want to understand why we changed from “Mining Lease” to “Mine Approval”;

- And to approve the withdrawal letters regarding Mount Penny and Glendon Brook Coal Release Areas from Loyal Coal Pty Ltd (formerly Monaro)

- And the Buffalo Resource ACN

Also please note I added in the equity letter under Obligations of the Parties the following comment regarding Glendon Brook

• “and its associates or related parties undertaking not to pursue the grant of any mining rights to the Mount Penny area or any contiguous area, or the Glendon Brook EOI Coal Release Area;”

Please call or email me if there are any other matters to discuss.

Cheers

80 I infer from the reference to “Travers Duncan” in James McGuigan’s email that Duncan had carefully reviewed the letters as at 3 June 2009.

81 As I have mentioned, attached to that email were updated drafts of the Letter Agreements which had been under discussion over the preceding few days.

82 After the meeting held on 3 June 2009, Brook met with Moses Obeid and requested an alteration to the joint venture letter agreement. The amendment was intended to protect the Obeid interests against early dilution of their interest. A copy of that email was sent to Moses Obeid.

83 By email sent at 2.04 pm on 3 June 2009 to Brook and Moses Obeid, James McGuigan asked whether they had received their ACN for Buffalo Resources.

84 On 4 June 2009, Brook sought legal advice from a solicitor in respect of the landowners’ letter and the joint venture letter which had been under discussion and which was intended to be signed the next day (5 June 2009). In his covering email, Brook said that the land agreement was with a related party.

85 Later the same day, Moses Obeid provided the lot numbers for the relevant land to James McGuigan and to Brook. Brook passed on that information to the solicitor whom he was consulting at that time.

86 On 4 June 2009, MMNL submitted a share transfer in respect of all of its shares in Loyal Coal for stamping by the Chief Commissioner of State Revenue. As anticipated, a Joint Venture Letter Agreement was signed between Cascade Coal and Buffalo Resources on 5 June 2009. That agreement was in the following terms:

5 June 2009

Gardner Brook

Buffalo Resources Pty Ltd

GPO Box 1810, Sydney

NSW 2001

Dear Sir,

Re: Letter of Agreement between Cascade Coal Pty Ltd (“Cascade”) and Buffalo Resources Pty Ltd (“Buffalo”), collectively (“the Parties”).

Further to our recent discussions this agreement is intended to outline the commercial terms for which both Buffalo and Cascade intend to establish a joint venture with the specific purpose of exploring and developing the Mount Penny Coal Release Area (“The Area”).

Subject to the grant of the Exploration Licence (for the purposes of this agreement (“Exploration Licence”) means an exploration licence granted to Cascade (or an affiliate) as a result of the current tender process and includes any extension renewal or replacement of that licence), the Parties have agreed to form either a Joint Venture Company or an unincorporated Joint Venture (“JV”) to explore and develop the Exploration Licence and pursue the grant of Mining Approval over the Area. For the purposes of this agreement (“Mining Approval”) shall mean the obtaining of all necessary permits and approvals including without limitation the grant of an appropriate mining tenement or tenements and environmental and native title approvals necessary for the development of a 100 million tonne resource.

In addition the JV will pursue the grant and issue of relevant Exploration Licences and Mining Approvals over the area contiguous to the Area and detailed on the attachment hereto currently known as EL 6676 or any portion thereof (“Contiguous Area”).

Obligations of the Parties

In recognition of Buffalo’s intellectual property contribution and in consideration of Buffalo:

• and its associates or related parties including Gardner Brook and Loyal Coal Pty Ltd withdrawing any existing applications in relation to the Mount Penny and Glendon Brook Coal Release Areas and undertaking not to pursue the grant of any mining rights to the Area or any Contiguous Area, or the Glendon Brook EOI Coal Release Area;

• agreeing to assist Cascade to explore and develop the Exploration Licence and obtain the Mining Approvals;

• agreeing to make available and provide their expert knowledge of the Area to assist with further exploration and review of the Contiguous Area.

Cascade agrees to:

• vest 100% of its interest in the Exploration Licence in the JV; and

• grant to Buffalo a 25% interest in the JV.

Buffalo does not have to make any contribution to costs of the JV until the earlier of either:

• Mining Approval for a 100 million tonne resource; or

• minimum exploration expenditure of A$10m.

Contributions up to this milestone by Cascade to the JV shall be treated as equity.

For the avoidance of doubt, prior to the earlier of the, granting of the Mining Approval or minimum exploration expenditure of A$10m, Buffalo will not be liable to contribute to the costs of the JV including exploration costs.

Upon the earlier of the grant of the Mining Approval or minimum exploration expenditure of A$10m Buffalo will be required to contribute its proportionate share of equity to fund costs should third party debt finance be unavailable or insufficient to fund such costs, including proportionate costs of any land acquisition. Failure to meet required equity contributions proportionate to Buffalo’s equity percentage will result in Buffalo’s interest in the JV being diluted pro rata in accordance with the provisions of the JV agreement governing the development of the Area.

Contiguous Area

If from time to time, the NSW Department of Primary Industries seeks expressions of interest from parties for the granting of a Exploration Licence, Mining Approval or any other mining interest in relation to the Contiguous Area, Cascade on behalf of the JV must use its best endeavors to become the successful applicant in any such Exploration Licence, Mining Approval or mining interest. To the extent that Cascade and its associates and related parties acquire the rights to pursue a mining interest over the Contiguous Area, such areas and rights shall be assigned to the JV.

Management of the Joint Venture

Buffalo will be entitled to participate on the board and management of the JV to the extent commensurate with Buffalo’s equity interest in the JV.

Buffalo will be entitled to review the books and records of the JV to ensure Cascade has complied with its obligation under this agreement and to inspect and obtain copies of all exploration records and data.

No transfer or encumbrance

No party may transfer or encumber its interest in the EL, any underlying mining rights or the JV without obtaining the consent of the other party.

Confidentiality

Except as expressly permitted by this Letter of Agreement, Cascade and Buffalo undertake and agree to hold each of the terms in this Letter of Agreement in strict confidence and not to disclose or discuss any Confidential Information to or with any person except, in accordance with this Letter of Agreement or as otherwise permitted by Cascade or Buffalo.

Cascade and Buffalo will ensure that no Confidential Information is photocopied, reproduced or recorded in any manner except to the extent that is necessary to provide such number of copies as are reasonably required by either Cascade or Buffalo.

Cascade and Buffalo will not use or disclose the Confidential Information or any part of it to gain any commercial, financial or other advantage for itself or any other person or to the competitive disadvantage or otherwise to the detriment of either Cascade or Buffalo.

87 The Agreement was signed by John McGuigan on behalf of Cascade Coal and by Brook on behalf of Buffalo Resources.

88 On the same day (5 June 2009), Buffalo Resources executed a Deed Poll. That document was signed by Andrew Kaidbay and Mario Sindone as directors of Buffalo Resources. By that Deed Poll, Buffalo Resources declared that it held all of its interest in the joint venture documented in the letter between it and Cascade Coal dated 5 June 2009 on behalf of Warbie Pty Limited (ACN 137 486 018) (Warbie) and Equitexx Pty Limited (ACN 100 544 483) (Equitexx). The beneficial interest of Equitexx in those companies’ share of the joint venture was stated as 88%.

89 On 6 June 2009, Cascade Coal and Buffalo Resources entered into a further letter agreement varying the agreement which they had entered into the day before. This later letter agreement was in the following terms:

Dear Sirs

Letter of Agreement between Cascade Coal Pty Limited and Buffalo Resources Pty Limited

We refer to the letter agreement between Cascade Coal Pty Limited and Buffalo Resources Pty Limited dated 5 June 2009 (JV Agreement). We would like to clarify a few points in the JV Agreement (by way of variation to the JV Agreement) by:

1. deleting the words “or an unincorporated Joint Venture” in line 5 of paragraph 2 on page 1 of the JV Agreement; and

2. deleting the first two (2) paragraphs on page 2 of the JV Agreement and replacing them with the following:

“In recognition of Buffalo’s Intellectual property and for Buffalo and its associates or related parties including Gardner Brook and Loyal Coal Pty Limited withdrawing any existing applications in relation to the Mount Penny and Glendon Brook Coal Release Areas and undertaking not to pursue the grant of any mining rights to the Area or any Contiguous Area, or the Glendon Brook EOI Coal Release Area, Cascade agrees to:

• vest 100% of its interest in the Exploration Licence in the JV; and

• on and from the date of this agreement grant to Buffalo the right to acquire at anytime a 25% interest in the JV for $1.00.

Buffalo’s contribution to the JV will be to:

• Assist cascade to explore and develop the Exploration Licence and assist Cascade to obtain the Mining Approvals

• Make available and provide its expert knowledge of the Area to assist with further exploration and review of the Contiguous Area.”

Could you please confirm your acceptance of this variation and clarification by signing a copy of this letter.

Dated: 6/6/09

90 On 9 June 2009, MMNL and Loyal Coal withdrew their interest in (amongst others) the Mt Penny coal release area.

91 On 10 June 2009, James McGuigan sent an email to his father and to Poole. In that email, James McGuigan said:

The property Cherrydale Park is owned by Locaway Pty Ltd

Directors of Locaway Pty Ltd

- Paul Obeid

- Edward Obeid

- Damien Obeid

- Moses Obeid

Shareholding of Locaway Pty Ltd

Paul Obeid 50%

Obeid Corporation 50%

So, there are some issues here.

92 On 11 June 2009, in response to an inquiry from Poole, James McGuigan sent an email in which he said:

I spoke to Dad last night and set that we thought the logical progression was for Locaway to transfer the Cherrydale Park Asset to UPG.

He’s having a meeting with Moses today.

Will let you know as soon as there is news

Cheers

93 Poole followed up James McGuigan at 1.50 pm. James McGuigan reported to him that there was no news as at that time and said:

Hopefully we will sit down with Moses by end of today and then I guess find out then.

94 By letter dated 19 June 2009 and signed by the Director General of the DPI, the DPI informed Cascade Coal that it had been selected as the successful EOI applicant for the exploration licence over the Mt Penny coal release area. The author of the letter invited Cascade Coal to apply for the exploration licence over that area. The letter went on to specify certain financial terms and conditions.

95 In June and July 2009, the shareholders of Cascade Coal actively considered how they would fund the exploration licences which they had been granted including over the Mt Penny coal release area.

96 By late August 2009, James McGuigan (and possibly Poole) had prepared a document entitled “Cascade Coal: Shareholder Update (August 2009)”.

97 On 22 August 2009, James McGuigan sent a draft of that Shareholder Update document to Poole for his consideration. Poole made some suggestions for improvement.

98 In an email sent by him to Poole on 23 August 2009, James McGuigan said:

Richard –

I’ve put your changes through as well reformatted it.

I won’t resend until we discuss whether we go into more detail with the Mt Penny agreements.

I understand the sensitivities of putting who the parties are – however I think we have to disclose who Buffalo is (i.e entities associated with the land owners) – and remove the Monaro comment – but allude to it.

I am saying this because if we don’t include the background information – the comments don’t mean anything.

Also – as I have been writing this email – Mike Johnstone has emailed the GB ELA.

What are your thoughts on including it as an attachment or referring to it?

Give me a call when you can to discuss – at the office

Cheers

99 On Monday 24 August 2009, the updated version of that document was sent to John McGuigan, Atkinson, Kinghorn and Poole. In that email, James McGuigan said that the update outlined that Cascade was proceeding to achieve the grant of exploration licences over the Mt Penny and Glendon Brook coal release areas and that an initial capital call of $2.1 million would be made ie $300,000 for each shareholder group. He said that it was imperative that those funds be received before the end of that week (Friday 28 August 2009). This email and its attachment (the revised Cascade Coal Shareholder Update) was also sent to an email address used by Duncan. I infer that it reached Duncan.

100 The revised Shareholder Update document circulated on 24 August 2009 was in landscape format. On pages 10 and 11 of that document, the authors addressed the Mt Penny agreements involving the landowners and Buffalo Resources in the following terms:

3. MT PENNY AGREEMENTS

In preparation for the development of Mt Penny Cascade has entered into two agreements with:

- the Landowners of the Mt Penny Area as well as;

- Buffalo Resources Pty Ltd (“Buffalo”).

The key points are summarised below.

The Landowners Agreement

To ensure Cascade can secure the land necessary for the development of Mt Penny and to reduce the risk in the project (given recent land owner issues in NSW) Cascade has entered into a conditional agreement to acquire three rural interests in the Bylong region specifically Cherrydale Park, Donola and Coggon Creek (“the Properties”) that are situated on the Mt Penny Area in the event that Cascade determines that it will proceed to mine This contract should ensure Cascade’s access for exploration and potential mine development at Mt Penny over a substantial portion of the Exploration License.

The key terms of the agreement are:

- Cascade to acquire 100% of each property. The purchase price shall be an amount equal to four times the total sum of the Properties. The value of each property shall be agreed as the improved value as at 1 June 2009 of each property and agreed between the parties or in the event of a failure to agree as determined by an independent valuer. Cascade’s obligation to acquire the properties is conditional upon Cascade being satisfied that it will undertake a mine development at Mt Penny and a Mining Lease be granted for that purpose.

- Cascade will provide within 60 days if the grant of the Exploration License a facility enabling the Landowners to replace the existing mortgagee with Cascade, or its nominee, on standard commercial terms other than that Cascade will essentially assume responsibility for the interest payments or at its option Cascade shall commence paying all interest attached to the existing mortgages.

Buffalo Resources Pty Ltd Agreement

An arrangement has been entered into with Buffalo Resources Pty Ltd (“Buffalo”) whereby:

- Cascade to vest 100% of the Mt Penny EL into a special purpose entity and to subsequently grant Buffalo a 25% interest in the entity;

- Buffalo agreeing to assist Cascade to explore and develop the Exploration License and obtain the Mining Approvals;

- Buffalo agreeing to make available and provide their expert knowledge of the Area to assist with further exploration and review of the Contiguous Area.

- Buffalo does not have to make any contribution to costs of the JV until the earlier of either: Mining Approval for a 100 million tonne resource; or minimum exploration expenditure of A$10m.

This above arrangement was entered into in recognition of Buffalo undertaking not to pursue the grant of any mining rights to Mt Penny or any contiguous areas and agreeing to facilitate the provision of unimpeded access to the Area.

101 At pages 18 and 19 of that document, the authors addressed the corporate structure of Cascade Coal in the following way:

6. CORPORATE STRUCTURE OF CASCADE COAL

Shares in Cascade Coal will be held equally by the seven shareholder groups. Please advise as a matter of priority.

Relevant to the award of the exploration licence was the fact that it could be demonstrated that Cascade had an existing interest in the coal sector. In this regard we were able to point to the fact that Cascade had an existing exploration program and that it was engaged in the “coal business”. This was relevant to the successful application. In this regard Cascade currently holds several highly speculative exploration licences in Victoria, Australia. Now that Cascade has been successful in the Mt Penny and Glendon Brook applications these will be transferred out with all related loans and expenses so Cascade has a clean balance sheet.

It is envisaged that a Shareholders Agreement will be entered into covering the normal matters namely:

- Appointment of Directors;

- Management of the company and decision making;

- Capital Raising;

- Transfer of shares and Pre Emptive Provisions;

- Tag along and Drag along rights.

Two wholly owned subsidiaries have been established, Mt Penny Coal Pty Lt [sic] and Glendon Brook Coal Pty Ltd. The applications for the relevant Exploration Licences will be made in the names of the wholly owned subsidiaries.

Additionally, two other wholly owned subsidiaries will be incorporated:

- MP Landowners Pty Ltd;

- GB Landowners Pty Ltd;

The chart on the following page illustrates the intended corporate structure:

102 The evidence was that the email address “bsweeney@blest.com.au” was the email address of Bill Sweeney who generally acted as the accountant for Jones and was participating in this particular venture as the nominee or trustee of Jones’ interests.