FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Mariner Corporation Limited [2015] FCA 589

Table of Corrections | |

2 July 2015 | In paragraph 141, “5 July 2014” has been replaced with “5 July 2012”. |

2 July 2015 | In paragraph 354, “before me” has been inserted after “At no stage”. |

IN THE FEDERAL COURT OF AUSTRALIA | |

IN THE MATTER OF AUSTOCK GROUP LIMITED

and

IN THE MATTER OF MARINER CORPORATION LIMITED

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The plaintiff’s originating application be dismissed.

2. Within 14 days of the date hereof, each party file and serve written submissions on the question of costs (limited to three pages each).

3. Within 14 days of receipt of any submissions referred to in paragraph 2 hereof, each party file and serve written submissions in response (limited to one and a half pages each).

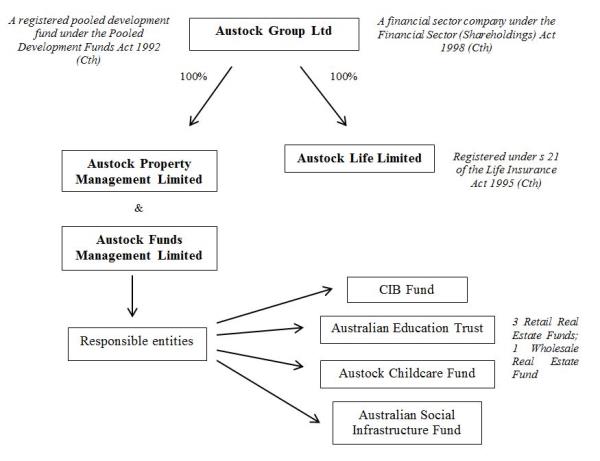

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 184 of 2014 |

IN THE MATTER OF AUSTOCK GROUP LIMITED

and

IN THE MATTER OF MARINER CORPORATION LIMITED

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff |

AND: | MARINER CORPORATION LIMITED (ACN 002 989 782) First Defendant DARREN OLNEY-FRASER Second Defendant DONALD JAMES CHRISTIE Third Defendant MATTHEW JAMES FLETCHER Fourth Defendant |

JUDGE: | BEACH J |

DATE: | 19 June 2015 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

1 This proceeding concerns the lawfulness of the defendants’ conduct relating to the announcement on 25 June 2012 of an off-market takeover bid by Mariner Corporation Limited (Mariner) for all of the issued capital of Austock Group Limited (Austock) at 10.5 cents per share. By way of an originating application filed on 2 April 2014, the Australian Securities and Investments Commissions (ASIC) brought this proceeding against Mariner and its three directors Mr Darren Olney-Fraser (Mr Olney-Fraser), Mr Donald Christie (Mr Christie) and Mr Matthew Fletcher (Mr Fletcher), alleging contraventions of ss 180, 631(2)(b) and 1041H of the Corporations Act 2001 (Cth) (the Act) with respect to that takeover announcement. ASIC has sought declarations against all defendants and pecuniary penalties and disqualification orders against the individual directors. At trial, only the three directors, Mr Olney-Fraser, Mr Christie and Mr Fletcher actively participated in defending the proceeding. Mariner was not represented at trial and filed what it termed to be a “submitting notice”. The trial proceeded on liability only, with questions of relief, penalties and ss 1317S and 1318 issues to be dealt with at a later hearing (if necessary).

2 In summary, ASIC has alleged that:

(a) Mariner failed to comply with s 631(2)(b) of the Act in that on 25 June 2012 it publicly proposed to make a takeover bid for Austock, reckless as to whether it would be able to perform its obligations relating to the takeover bid at 10.5 cents per share if a substantial proportion of the offers under the bid were accepted. ASIC has asserted that as at 25 June 2012 Mariner did not have the financial resources to fund the bid and had not received relevant assurances from and had no agreements with third parties concerning the provision of such funding.

(b) Mariner contravened s 1041H of the Act in that, on 25 June 2012, by making the announcement it engaged in conduct that was misleading or deceptive or likely to mislead or deceive because it was not permitted to make a takeover bid for shares in Austock at a price of less than 11 cents per share (the price representation); reliance was placed on s 621(3). Further, ASIC has alleged that Mariner misled the market as to Mariner’s ability to fund the bid at 10.5 cents per share or at the required 11 cents per share (the funding representation).

(c) Each of the directors breached his duty to act with due care and diligence in contravention of s 180(1) of the Act by making a decision that Mariner would announce a takeover bid for Austock and:

(i) causing Mariner to make a public proposal that contravened s 631(2)(b);

(ii) causing Mariner to make an announcement to the ASX which contravened s 1041H;

(iii) stating that Mariner would make a bid at 10.5 cents per share, which it could not lawfully do (see s 621(3)); and

(iv) failing to take into account regulatory constraints on the ability of Mariner to acquire more than various percentages of shares in Austock.

3 The defendants have denied that Mariner contravened ss 631(2)(b) or 1041H. Further, the directors argue that there is no foundation for any alleged breach of directors’ duties under s 180. Moreover, each director has submitted that they did not act in breach of their duties whether or not Mariner itself so engaged in contravening conduct; ASIC has asserted that the directors contravened s 180 irrespective of whether Mariner contravened ss 631(2)(b) or 1041H.

4 In my view, ASIC has not made out its claims against Mariner or the directors. Accordingly, its originating application will be dismissed.

5 In summary, I have reached the following views:

(a) The test for “reckless” under s 631(2)(b) is a subjective test. Applying that test, Mariner was not “reckless”.

(b) Alternatively, if the test for “reckless” under s 631(2)(b) is an objective test, Mariner was not “reckless”.

(c) Mariner did not engage in any conduct in contravention of s 1041H in relation to the price representation or the funding representation.

(d) Alternatively, if Mariner did engage in any misleading or deceptive conduct concerning the price representation, on no reasonable view would it be entitled to any relief. I express no view on whether relief would go if, alternatively, Mariner engaged in misleading or deceptive conduct concerning the funding representation.

(e) No director contravened s 180, whether or not Mariner contravened s 631(2)(b) or s 1041H.

(f) Alternatively, even if Mr Olney-Fraser contravened s 180, neither Mr Christie nor Mr Fletcher contravened s 180 given their reasonable reliance upon the information provided to them by Mr Olney-Fraser and their ability to invoke s 189.

6 For convenience, the relevant issues have been addressed in the following order:

[7] to [151] | |

II: Market value and funding mechanisms | [152] to [175] |

III: Credibility and other evidentiary issues | [176] to [216] |

(a) Mr Olney-Fraser – general | [176] to [189] |

(b) Mr Olney-Fraser – bridging finance | [190] to [197] |

(c) Mr Christie and Mr Fletcher | [198] to [201] |

(d) The rule in Browne v Dunn | [202] to [213] |

(e) ASIC’s witnesses | [214] to [216] |

IV: CONSTRUCTION OF SECTION 631(2) | [217] to [313] |

(a) Section 631(2) – general | [217] to [229] |

(b) Legislative history | [230] to [247] |

(c) Meaning of “reckless” | [248] to [279] |

(d) Meaning of “substantial proportion” of offers | [280] to [313] |

V: DID MARINER BREACH SECTION 631(2)? | [314] to [418] |

(a) Did Mariner publicly propose to make a takeover bid for Austock? | [315] to [317] |

(b) Was Mariner reckless as to whether it would be able to perform its obligations? | [318] to [387] |

(c) ASIC’s pleaded case | [388] to [392] |

(d) Takeovers Panel’s analysis | [393] to [414] |

(e) ASIC’s Regulatory Guides and Panel’s Guidance Notes | [415] to [418] |

VI: DID MARINER CONTRAVENE SECTION 1041H? | [419] to [438] |

(a) General | [419] to [422] |

(b) The price representation | [423] to [428] |

(c) The funding representation | [429] to [438] |

VII: DUTIES OF CARE AND DILIGENCE – SECTION 180 | [439] to [561] |

(a) Case against Mr Olney-Fraser | [453] to [524] |

(b) Case against Mr Christie | [525] to [551] |

(c) Case against Mr Fletcher | [552] to [561] |

VIII: CONCLUSION | [562] |

7 Mariner was a corporate investment company whose shares were listed for quotation on the Australian Stock Exchange (ASX). Its principal activity was to target and engage in mergers and acquisitions in the small cap sector (e.g. previously, Viento Group Limited, Tasmanian Pure Foods Limited and Capilano Honey Limited). As at July 2012, Mariner made strategic investments in other listed companies. Its strategy was to agitate for change at the board level in companies it took a strategic investment in and to otherwise work with the management of those companies to achieve improved results.

8 Mariner had 3 directors, being Mr Olney-Fraser, Mr Christie and Mr Fletcher. Mr Olney-Fraser and Mr Christie were appointed as directors on 4 November 2010; Mr Fletcher was appointed as a director on 11 April 2011. The directors worked together in a small office.

9 Mr Olney-Fraser was the Chief Executive Officer of Mariner. He had previously been a mergers and acquisitions lawyer, with over 10 years' experience. Mr Olney-Fraser practised as a solicitor with Baker & McKenzie and Blake Dawson, and had also been a partner at Andersen Legal. His commercial and legal experience was extensive.

10 Mr Olney-Fraser had authority from Mariner’s Board to trade (for example, to purchase shares in small cap companies) on behalf of Mariner up to $50,000 without obtaining approval from the other directors.

11 Mr Christie was the Executive Chairman of the Mariner board. He was a former corporate lawyer with significant experience in business and compliance matters. He had been the managing director of Equity Trustees Ltd and a former President of the Australian Trustee Corporations Association. He had held a number of non-executive directorships in unlisted companies. He had also worked in compliance and regulatory roles for predecessor regulators, namely, the Australian Securities Commission and the National Companies and Securities Commission.

12 Mr Fletcher was an investment banker who was experienced in corporate and commercial banking, specialising in structured property finance. He had been the chief executive officer of the “boutique” fund manager, Astrum Funds Management Ltd. He had also held senior management positions with Lloyds Banking Group Ltd, National Australia Bank Ltd and St George Bank Ltd.

13 Three observations should be made at the outset concerning ASIC’s case against the directors. First, the directors had extensive backgrounds and expertise in mergers, acquisitions and finance. Such backgrounds no doubt informed their judgment calls, assessments of risk and the strategies they pursued in relation to the transaction the subject of this proceeding. It is necessary to bear this in mind when assessing the case of a regulator second guessing such judgment calls with the benefit of hindsight, using a largely paper based analysis and viewing the events from a timeframe perspective divorced from the reality of the speed at which the events occurred in real time. Second, in looking at the transaction in question, it is important to adopt an ex ante perspective where one is not just looking at potential risks and downsides but also the potential benefits. That was the directors’ framework at the relevant time. And that is necessarily the framework within which s 180 must be analysed. A retrospective analysis of a transaction which did not proceed has the tendency to overlook that latter dimension. Third, ASIC made no attack on the credibility of the evidence given by Mr Christie or Mr Fletcher. Rightly so. Their evidence was measured, accorded with the probabilities and involved the making of appropriate concessions. I will deal with Mr Olney-Fraser later.

14 On 24 and 27 April 2012, Mr Olney-Fraser in accordance with his authority purchased 460,000 shares in Austock at 11 cents per share on behalf of Mariner (60,000 shares purchased on 24 April 2012 and 400,000 shares purchased on 27 April 2012). On 5 June 2012, Mariner sold 50,000 Austock shares thereby reducing its total holding to 410,000.

15 It is useful at this point to describe the business and corporate structure of Austock. Austock’s shares were listed for quotation on the ASX and 133,928,412 fully paid ordinary shares were quoted for trading. A wholly owned subsidiary of Austock, Austock Life Limited (Austock Life) was registered under s 21 of the Life Insurance Act 1995 (Cth); by reason of that fact, Austock was a financial sector company within the meaning of the Financial Sector (Shareholdings) Act 1998 (Cth) (FSSA), a characterisation that will become relevant later.

16 The life insurance business of Austock Life was a substantial segment of the operations of Austock and was the source of approximately 40 to 45% of the ongoing revenue of Austock. Austock was also a registered pooled development fund under the Pooled Development Funds Act 1992 (Cth) (PDFA). Wholly owned subsidiaries of Austock, Austock Property Management Limited and Austock Funds Management Limited were the responsible entities for three retail and one wholesale real estate funds, namely:

Australian Education Trust (AET);

Australian Social Infrastructure Fund (ASIF);

Austock Childcare Fund (ACF); and

The CIB Fund (CIBF).

17 Austock’s corporate structure at the relevant time can be simplistically illustrated as follows:

18 At the time of the 25 June 2012 announcement there were 708 non-Mariner shareholders in Austock, with the 10 largest non-Mariner shareholders holding just under 50% of the shares and the 50 largest non-Mariner shareholders holding approximately 87%.

19 Mr Bill Bessemer (Mr Bessemer) was the Chief Executive Officer of Austock and the controller of the largest block of shares. Austock had two key camps of shareholders: the Bessemer camp which held around 26% of the Austock shares; and the Whitelegg camp (associated with Mr Ryan Whitelegg) which held about 10% of the shares.

20 The financial report and accounts for Austock for the half year ending 31 December 2011 disclosed:

(a) that funds under management for the property business were around $555 million; revenue from the sector showed an increase of 14% over the relevant comparable period;

(b) that funds under management for the life business were around $263 million; revenue from that sector showed an increase of 27% over the relevant comparable period;

(c) net assets of $16.366 million;

(d) $9.940 million in cash as at 31 December 2011; and

(e) a net loss before tax and impairments of $3.4 million.

21 This material formed part of the Appendix 4D Report published on 29 February 2012. Further, what was anticipated, which then occurred, was the completion of the sale of Austock’s security business in mid-March 2012, which was to reduce overall employees of Austock from 130 to fewer than 30 staff; the sale to Intersuisse Holdings Pty Ltd had been made on 9 February 2012. This was expected to improve its P&L account position.

22 The published financial material of Austock prior to 25 June 2012 reasonably supported the valuations made by Mariner of Austock and its businesses.

23 The financial report and accounts for the year ending 30 June 2012 (Appendix 4E Report) had some changes, but they are not significant for present purposes. I have referred to the half year report and accounts as these were available to the directors of Mariner at and prior to 25 June 2012. The half year report and accounts were used by Mariner to prepare a Target Summary that I will discuss shortly.

24 The Target Summary also listed the top 10 shareholders of Austock as at 15 August 2011 (taken from the 30 June 2011 report and accounts).

25 For completeness, as at 30 June 2012, there were only 2 significant changes in such shareholdings. The holding of the Austock Employee Share Scheme was still shown as the largest shareholder but the holding had dropped from 24,004,553 shares (17.92%) to 12,861,775 shares (9.603%). Further, the tenth largest shareholder slipped to eleventh place, with M.F. Custodians Ltd taking tenth place at 3,844,721 shares (2.871%). As at 15 August 2011, the top 10 shareholders held 57.27%. As at 30 June 2012, the top 10 shareholders held just under 50%. The top 20 shareholders held about 68%. The largest 100 shareholders held about 94.8%.

(b) Arena’s approach to Mariner

26 As early as January 2012, an investment company, Arena Investment Management Limited (Arena), which was a part of the international real estate arm of Morgan Stanley Inc, had shown interest in acquiring Austock Property Management Limited and Austock Funds Management Limited and the associated property management business. Arena was a wholly owned subsidiary of Morgan Stanley Australia Ltd. Mr James Goodwin (Mr Goodwin), joint managing director of Arena, made an approach to Austock. A written “indicative non-binding” offer dated 28 May 2012 was forwarded to Austock. The written offer stated that Arena valued the Austock property management business in the range of $10 to $12 million in relation to the management rights plus the value of the other net assets associated with that business. It also said that “Arena currently holds more that $20 million in cash and has the ability to immediately fund the acquisition”. The approach was rebuffed by Austock and Arena was told that Austock had signed a confidentiality agreement with another party in relation to the potential sale of the Austock property management business.

27 Arena was one of the 5 largest unlisted fund and syndicate managers in Australia, with over 16,000 investors, 1,500 advisers and 321 dealer groups. Arena had experience in establishing and managing “social infrastructure funds”.

28 On 8 June 2012, Mr Goodwin telephoned Mr Olney-Fraser. This was an unsolicited approach by Arena. Mr Goodwin introduced himself as being from “Morgan Stanley” and said that together with Mr Bryce Mitchelson (Mr Mitchelson) he was the joint managing director of Arena. By that stage, media reports had made Arena aware of both Mariner and Folkestone Limited’s (Folkestone) interest in Austock.

29 The telephone call lasted approximately 10 minutes. Mr Goodwin said that he and Mr Mitchelson were keen for Arena to buy Austock's childcare fund and generally the Austock property management business. Mr Goodwin stated that the motivation for the purchase was to achieve economies of scale and synergies and to grow the Arena book.

30 Mr Goodwin said that Arena wanted to explore whether Mariner would be prepared to get control of Austock’s board. Specifically, Mr Goodwin stated that with Arena’s support, Mariner could buy a strategic stake in Austock, or make a full takeover bid, to get control of Austock and then sell the Austock property funds management business to Arena. Mr Goodwin stated that Morgan Stanley would not want Arena to be seen to be engaged in anything hostile towards Austock. Accordingly, meetings and conversations would need to be kept confidential.

31 Mr Olney-Fraser gave evidence that Mr Goodwin told him that he wanted to explore whether Mariner could be Arena’s “stalking horse” to get control of Austock’s board and make sure that Mariner acquired the business and that with Arena’s support, at least in terms of buying the Austock property management business, Mariner could buy a strategic stake in Austock or make a full takeover bid if necessary to get control of Austock. Mr Goodwin rejected this description of “stalking horse”, which I accept was not used by him. Nevertheless, in my view Mr Olney-Fraser’s account is largely accurate and accords with the probabilities. First, it was Arena that approached Mariner. Second, Arena thereafter continued to have discussions with Mariner representatives. Third, the steps, which Mr Olney-Fraser recounted that Mr Goodwin had said, were commercial and necessary steps if Mariner was to be in a position to control Austock so that it could then sell the Austock property management business to Arena.

32 Mr Olney-Fraser and Mr Goodwin then arranged to meet at Il Solito Posto to explore the details further.

(c) The Il Solito Posto meeting

33 On about 12 June 2012, Messrs Olney-Fraser and Goodwin met for coffee at Il Solito Posto, 113 Collins Street, Melbourne and continued the discussions about Austock. The meeting lasted about 30 to 45 minutes. Mr Mitchelson also attended the coffee meeting to add weight to Arena’s level of interest in buying the Austock property management business. Mr Goodwin told Mr Olney-Fraser about Arena's unsuccessful written offer to Austock to obtain the Austock property management business. Mr Goodwin made it clear to Mr Olney-Fraser during that meeting and subsequent telephone discussions that Arena wanted to acquire the Austock property management business.

34 As Mr Goodwin said in cross-examination, Arena:

[W]anted to make it clear to Mariner that if they got control, that we were very interested in buying in that business. And we - yes. We did hope that he would - that that would help him [Mr Olney-Fraser] to make the decision to proceed.

35 Mr Goodwin stated that Arena had put a valuation of $10 to $12 million on the Austock property funds management business and that it looked unlikely that a deal could be reached with Austock. Mr Goodwin was concerned that Austock might sell its property funds management business to Folkestone.

36 At the time, Mr Olney-Fraser assessed Austock's market capitalisation at approximately $12 million. Arena's assessment was that the break-up value of Austock was around $25 million. Mariner was also of the view that the break-up value of Austock was significantly higher than $12 million. Estimates made around this time revealed a break-up value of $20 million or more, the reasonableness of which were not seriously disputed by ASIC. The significance of that observation will become apparent later.

37 It was Mr Olney-Fraser's evidence that Mr Goodwin said to Mr Olney-Fraser that Arena could give Mariner the financial backing it needed to move forward and could help Mariner with financial assistance to assist Mariner to get over the line in acquiring Austock and to assist Mariner with any timing issues. Mr Goodwin rejected that version in cross-examination. I accept Mr Goodwin’s account for reasons that will become apparent later.

38 Mr Olney-Fraser further suggested that Mr Goodwin told him that Arena itself had considered making a bid for Austock, but that Morgan Stanley would not allow it. In cross-examination, Mr Goodwin said that he could not recall Arena seriously contemplating a bid in its own right. Arena had however discussed with Morgan Stanley whether an uninvited offer for the Austock property business should be made.

39 Mr Goodwin communicated to Mr Olney-Fraser that Morgan Stanley’s policy was to be invited into a deal and not to force itself onto a party and that Morgan Stanley would not approve of Arena becoming involved in a hostile takeover. However, if Mariner gained control of Austock, it would be in a position to invite Arena to make an offer, with the prospect of a mutually beneficial outcome.

40 In cross-examination, Mr Olney-Fraser described the discussions at the Il Solito Posto meeting as involving the exchange of mutual commitments by Arena to assist Mariner (including financially) to acquire control of Austock, by a takeover bid if necessary, and by Mariner causing Austock to sell the Austock property business to Arena when it obtained control, subject to Austock board and shareholder approval at the time. ASIC submitted that this characterisation was never put directly to Mr Goodwin (it was faintly hinted at in his cross-examination) and should not be accepted. As will become apparent later, I reject Mr Olney-Fraser’s evidence to the extent that it suggests that Arena indicated or offered any financing commitment for the takeover.

41 Messrs Christie and Fletcher were informed by Mr Olney-Fraser as to the nature of this discussion shortly after it took place.

(d) Preparation of first Target Summary

42 At or about this time Mr Olney-Fraser was developing his plans in relation to Austock and talking to other parties about them. There is very little evidence of the steps he took at this time and the conversations he had, but the following is revealed in the evidence:

(a) The evidence of Mr Justin Hoy (Mr Hoy), a broker at Macquarie, was that he had begun discussions with Mr Olney-Fraser about Austock in late May or early June. Those discussions related to the possibility of getting a level of control and board influence by acquiring 20 to 25% of Austock by aligning with the group of shareholders in disagreement with Mr Bessemer, the controller of the largest block of shares.

(b) On 13 June 2012, Mr Christie sent a spreadsheet to Mr Olney-Fraser listing the twenty largest shareholders of Austock, a calculation of the value of Austock at various share prices and an estimation that the cash and businesses of Austock might realise $20 million; his estimate was based upon $7 million in cash, $10 million value for the property business and $3 million value for the life business. Mr Christie stated that the “maximum offer looks like about 12-13c”. Mr Olney-Fraser appears to have requested Mr Christie to undertake this exercise.

(c) Mr Hoy said that Mr Olney-Fraser had provided him with a copy of the Austock share register. Mr Hoy had asked his assistant to summarise that register. On 13 June 2012, Mr Olney-Fraser asked Mr Hoy to approach one shareholder (Mr GK Goh of Singapore, who held approximately 8%) with an offer for his shares. Mr Goh ultimately declined that approach.

(d) Mr Olney-Fraser sent an email to a friend on 15 June 2012 in which he said “Getting good traction on an Austock bid next week. Macquarie, Morgan Stanley and Bruce Neill all in.” He agreed that it should be understood from this that he had had communications with these three entities and had some confidence about their involvement.

43 On 19 June 2012, Mr Olney-Fraser asked Mr Hoy to set up a meeting to be held at the offices of Macquarie Private Wealth on 21 June 2012, to be attended by Mr Bruce Neill (Mr Neill) and Mr Anthony Shadforth (Mr Shadforth). Mr Neill was a private investor and IOOF was a company in which he was a shareholder. He was not involved in its management. Mr Shadforth was a stockbroker at Equity Advisers Pty Ltd.

44 In preparation for the meeting, Mr Fletcher circulated an Austock Target Summary dated 19 June 2012 (19 June ATS) to Mr Olney-Fraser and Mr Christie. Mr Fletcher was asked to prepare the 19 June ATS and to contribute to some of its content by Mr Olney-Fraser. After some additions were made, by or on the instructions of Mr Olney-Fraser, this document was emailed by Mr Fletcher to Mr Hoy at Macquarie. Mr Olney-Fraser also emailed a copy to Mr Shadforth. Mr Olney-Fraser envisaged that Mr Shadforth would ultimately provide a copy to Mr Neill.

45 The 19 June ATS set out a 5 point strategy involving the acquisition of 20%, a spill of Austock’s board, the sale of the major assets (the “property funds” to Arena/Morgan Stanley for $10 million and the “life funds” to IOOF for $10 million), a capital return of 20 cents per share and the recapitalisation of the corporate shell with new management. The proposed action was to buy 3 key stakes amounting to 12% and to buy on-market at 12 cents per share about 8% to get to 20%. At this time, an off-market bid for all issued shares of Austock was not under consideration.

46 The 19 June ATS recorded that Mariner’s directors expected support for the board spill to be provided by the “Whitelegg camp” of shareholders, who as I have said held about 10% of Austock’s shares. The perceived opposing camp, the Bessemer camp, held about 26%; the employee share scheme also held at the time about 17.9%. The 19 June ATS referred to the fact that there were 133,928,412 shares on issue and that at 9.8 cents per share, Austock had a market capitalisation of $13.12 million.

47 Consistently with this proposed strategy, on 19 June 2012 Mr Hoy emailed one of the holders of those key stakes (Mr Goh) to initiate discussions about the possible purchase of his holding at 10.5 cents.

48 On Tuesday 19 June 2012, Mr Goodwin made a dinner booking at the then Stokehouse restaurant in St Kilda for 7.30 pm to meet with Mariner’s representatives. As Mr Goodwin said in cross-examination, “the purpose of the meeting was to make our intention that we wanted to buy the business very clear”.

49 The Stokehouse dinner was attended by Mr Olney-Fraser and Mr Fletcher for Mariner, and Mr Goodwin and Mr Mitchelson for Arena. Mr Christie did not attend. Mr Olney-Fraser had not previously met Mr Mitchelson. Mr Fletcher had not previously met either of the Arena joint managing directors.

50 Following an initial discussion about the Lloyds/HBOS debt, attention turned to Austock. Mr Goodwin and Mr Mitchelson conveyed to Mr Olney-Fraser and Mr Fletcher Arena’s position concerning Austock in the following terms. Arena had previously made a formal offer to Austock for its property funds management business on 28 May 2012 (the May Offer); the May Offer was a “full price offer” of between $10 and $12 million. That offer was rejected by Austock. Mr Goodwin subsequently learned that Austock was close to entering into an agreement with Folkestone. Arena was concerned that Austock was arranging a sale of the property funds management business to Folkestone and was seeking a partner who could promptly achieve a controlling interest and sell the property funds management business to Arena before it was sold to other interests.

51 Mr Goodwin handed Mr Olney-Fraser a copy of the May Offer. Mr Goodwin stated that Arena would resubmit the terms of the May Offer if Mariner obtained control of Austock. The parties discussed that time was of the essence in order to cut off any deal between Austock and Folkestone.

52 There was conflicting evidence given regarding the exact conversations that occurred during the Stokehouse meeting.

53 Mr Olney-Fraser's evidence was that during the dinner Messrs Goodwin and Mitchelson said that they:

(a) were resolute in their desire to purchase Austock's property funds management business for $10 to 12 million;

(b) would purchase Austock property funds management business for that amount from Mariner if it gained control of Austock; and

(c) would support Mariner’s attempt to gain control of Austock.

54 In particular, Mr Olney-Fraser asserted that he said that Mariner “did not have a balance sheet of any substance for an exercise like this” and was assured by Mr Goodwin that as joint managing directors he and Mr Mitchelson were able to provide any necessary financial support for Mariner. In cross-examination he went further and asserted that Mr Goodwin and Mr Mitchelson had made it clear to him that the $20 million of cash at their disposal was available to be used for a bridging finance facility to be put in place between the notice of intention to bid and the bid itself. Such a proposition was never put to Mr Goodwin or Mr Mitchelson in cross-examination and was not supported by Mr Fletcher’s account of the dinner. Again, I reject Mr Olney-Fraser’s evidence concerning the suggestion of an indication of financial support at this time, for reasons that I will later explain.

55 Mr Fletcher's evidence was that at the Stokehouse dinner, Arena's representatives said that:

(a) Arena was interested in engaging with Mariner as a “strategic partner” to promptly achieve a controlling interest in Austock and subsequently sell the property funds management business to Arena;

(b) Arena and/or Morgan Stanley was prepared to assist (in some undisclosed way) Mariner to enable Arena to acquire Austock's property funds management business; and

(c) Arena would be willing to acquire Austock's property funds management business from Mariner on the same terms as the written offer made to Austock and handed to Mr Olney-Fraser.

56 Mr Fletcher said that Mr Olney-Fraser explained that Mariner would most likely need to obtain third party funding to achieve an initial stake in Mariner but that Mariner had previously received good support for the right transactions in the past. Mr Olney-Fraser or Mr Fletcher discussed the acquisition of 20% of Austock. Nothing was said regarding an off-market full bid.

57 Mr Fletcher’s evidence of what occurred at the Stokehouse dinner made no reference to bridging finance being requested from or offered by Morgan Stanley. His evidence only made a vague reference to Arena/Morgan Stanley being “prepared to assist Mariner to enable Arena to acquire Austock’s property business”. That could simply have been a reference to taking a firmer position on acquiring the property business if Mariner took control. Mr Fletcher accepted in cross-examination that bridging finance had not been referred to at that dinner. All that Mr Fletcher advanced in his evidence was that it was “implied” that Arena/Morgan Stanley would provide funds. But he does not recall that the words “funds to assist” were used.

58 One must not lose sight of the fact that on 19 June 2012, what was in contemplation by Mariner was only the acquisition of a strategic stake to 20%. The full takeover bid concept evolved on 21 June 2012. That further confirms the view that bridging finance to the level required for a full bid simply was not on anyone’s radar on 19 June 2012, let alone being discussed at the Stokehouse dinner.

59 Mr Fletcher left the meeting thinking that Mariner was “arm in arm with Morgan Stanley and Arena”. To his mind, Arena/Morgan Stanley were “more than a counter-party to an acquisition”. He regarded “Mariner on the one hand and Arena and Morgan Stanley on the other hand as being partners or in a partnership”. He said that Arena/Morgan Stanley would “help [Mariner] achieve” the aim of Arena owning the property funds management business. As a result, Mr Fletcher told Mr Christie before 25 June 2012 that he was “firm in the fact that Morgan Stanley were going to back this deal” or words to that effect. It seems to me, though, that in context this is all referable to Arena/Morgan Stanley’s interest in and indication that they would purchase the Austock property management business after Mariner had completed its takeover of Austock.

60 Mr Goodwin deposed that “between the Stokehouse dinner on 19 June 2012 up to and including 25 June 2012 [he] could not recall Mr Olney-Fraser asking [him] to help Mariner with bridging finance of any kind for the acquisition of shares in Austock”. In cross-examination Mr Goodwin was unable to recall whether Mr Olney-Fraser raised the subject of funding and that Mariner would need some sort of underwriting or bridging finance for the purposes of the bid. But he gave evidence that:

(a) He did discuss with Mr Olney-Fraser at some stage how the bid “was going to be funded” and “funding” but he did not have a recollection of this occurring at the Stokehouse dinner specifically;

(b) Mr Olney-Fraser did raise with him the need for “some sort of underwriting or bridging finance” for the purpose of the bid “at some point”; but he did not recall Mr Olney-Fraser raising that subject prior to the bid announcement on 25 June 2012, but did not deny that this possibly occurred;

(c) He accepted that he never said to Mr Olney-Fraser before 25 June “don't look to Arena for any funding for any part of your proposed acquisition of Austock”; and

(d) He recalled “discussions about funding”, in particular a “bridge facility” “at some point”; but he could not recall whether this was before 25 June 2012.

61 Mr Mitchelson gave evidence that during the Stokehouse dinner:

(a) He and Mr Goodwin told Mr Olney-Fraser and Mr Fletcher that Arena could not be involved in a hostile approach to Austock, but that Arena would be interested in acquiring the Austock property funds business if Mariner obtained control of Austock subject to due diligence; and

(b) He did not tell Mr Olney-Fraser or Mr Fletcher that Arena or Morgan Stanley would provide funds to assist it in a proposed acquisition of Austock (or at any later time), and he did not hear Mr Goodwin do so.

62 In cross-examination it was put to Mr Goodwin that he or Mr Mitchelson told the Mariner directors that if Mariner were to make a bid or to try and acquire a large parcel of Austock shares and needed funding, that Morgan Stanley, or at least Arena, would “be there” for Mariner and assist them with financing. Mr Goodwin rejected this proposition; it was never put to Mr Mitchelson. In summary, neither Mr Goodwin nor Mr Mitchelson gave any indication that Arena/Morgan Stanley would assist in any bridging finance.

63 On Wednesday 20 June 2012, Mr Olney-Fraser and Mr Fletcher spoke to Mr Christie about what had occurred at the Stokehouse dinner. Mr Christie says that he was told of the following matters: Mr Goodwin and Mr Michelson had expressed Arena's keen interest in the Austock property funds management business; Mr Olney-Fraser had been shown the May Offer to buy the Austock property funds management business for $10 to 12 million; Mr Goodwin and Mr Mitchelson had said that Morgan Stanley would “support” Mariner to enable Mariner to take effective control, and that once Mariner could control the Austock Board, Arena would make a similar offer to the May Offer; Arena wanted to move quickly and did not want its involvement to be made public. Mr Christie’s reference to being told of “support” was nebulous and not a specific reference to bridging finance.

64 Mr Christie deposed that at this time he, Mr Olney-Fraser and Mr Fletcher were specifically discussing and focusing on the possibility of acquiring a 15 to 20% stake in Austock on-market, in the belief that if Mariner could acquire a 15 to 20% stake, then it would be able to gain effective control of the business with the support of other shareholders. The Mariner directors were aware (or at least they perceived) that there was an internal Board split within Austock, such that if Mariner could acquire a 15 to 20% stake it would be likely to be able to gain effective control of Austock. Whether such a perception was correct and such a strategy viable is not presently to the point. What is appropriate to note is that the strategy at this point in time was not centred on a full off-market bid requiring funding.

65 A board meeting of Mariner was convened later that day. Mr Olney-Fraser, Mr Christie, Mr Fletcher and Mr Adrian Olney (who was the company secretary of Mariner) were present. Austock was confirmed as a formal target and the Board consented to Mr Olney-Fraser's request to commence capital raising and to immediately seek to build a stake of up to 20% in Austock at a cost of $3 million. Mr Olney-Fraser and Mr Christie referred to the fact that contact had been made or would be made with large existing shareholders to determine their willingness to sell to Mariner. Macquarie, Morgan Stanley and Mr Neill were identified as potential sources of funds. It was noted that the future intention would be to spill the Board and sell the Austock property management business to Morgan Stanley and the life business to IOOF.

66 Later on 20 June 2012, Mr Hoy received a response from Mr Goh to the offer to purchase his shares at 10.5 cents per share. The offer was rejected. At this point, the directors of Mariner were aware that they were not able to purchase Mr Goh’s holding (approximately 8%) at 10.5 cents per share.

67 On Thursday 21 June 2012 at around 3.30 pm, a meeting was conducted at the offices of Macquarie at 101 Collins Street, Melbourne. The purpose of the meeting was to assess the level of support for the on-market acquisition of up to 20% of Austock's shares. The attendees were potential funders and interested parties being Messrs Olney-Fraser and Christie (Mariner), Mr Hoy and Stefan Whiting (brokers from Macquarie), Mr Shadforth and Chris McLoughlin (brokers from Equity Advisers), Mr Neill and Ian Urquhart (an observer). Mr Neill and Mr Shadforth's clients had had previous dealings with Mr Olney-Fraser. Mr Christie left the meeting early and had a limited recollection of what had occurred. Mr Fletcher did not attend the meeting.

68 Mr Hoy, Mr Whiting, Mr Shadforth, Mr McLoughlin, Mr Neill, Mr Olney-Fraser and Mr Christie have all given evidence about the meeting. There were conflicts in their recollections concerning both the commitments sought by Mariner and the commitments non-Mariner attendees gave to Mariner’s proposal. There was also imprecision as to whether an off-market bid had been raised by Mariner:

(a) Mr Hoy’s evidence was that no commitment was given at that meeting, beyond perhaps a commitment to have further discussions. Macquarie was not asked to “put a balance sheet behind any proposal”. Although he was asked for assistance in finding investors for convertible notes, Mr Hoy’s evidence is that he did not say to Mr Olney-Fraser that this was a possibility. His evidence was that this was not a possibility because of Macquarie’s rigorous deal assessment committee. Any proposal that involved new securities (including promissory or convertible notes) was not a possibility; Macquarie “couldn’t have been involved”. Subsequently, when Mr Olney-Fraser later on that day proposed “promissory notes”, Mr Hoy made clear that Macquarie could not assist with this either. Mr Hoy accepted that Mr Shadforth said words to the effect that his clients may be interested in supporting a takeover bid for Austock by Mariner, but would need to see the detail. Mr Hoy said that he recalled Mr Shadforth saying that “we will help you out”. It is likely that this was with respect to acquiring a 20% stake. Mr Hoy also recalled that Mr Neill may have said words to the effect that “he may be interested in purchasing Austock’s insurance business if Mariner obtained control”. Generally, according to Mr Hoy, Macquarie was never asked to put up money itself. But rather Mr Olney-Fraser asked for assistance in finding investors to either buy Austock shares or take convertible notes.

(b) Mr Shadforth said that no commitment was made by any person at the meeting. His evidence was that Mr Olney-Fraser did not ask for any commitment and there was no discussion to this effect. Mr Shadforth could not recall any discussion about whether Macquarie’s clients would be interested in being involved in the deal. Mr Shadforth could not say whether any of his clients would be interested in being involved in any deal because “it was never tested”; he “didn’t ever find out”. His evidence was that “people were going away to consider their positions, whether they were going to commit in one form or another” but that there was “quite a high level of comfort about the deal but it was early days”. Mr Shadforth did not recall any subsequent conversation with Mr Olney-Fraser before 25 June 2012 in which he was asked by Mr Olney-Fraser to “put down $500,000 in connection with the proposal”.

(c) Mr McLoughlin’s evidence was that he paid little attention to the individual attendees because he considered himself to be attending merely as an observer. He did not recall any discussion about how Mariner would fund a takeover bid and he did not recall any request for finance for a proposed takeover or any offer to provide finance. Nor did Mr McLoughlin offer to provide any finance or hear Mr Shadforth do so. Mr Urquhart was a client of Equity Advisers who had met with Mr McLoughlin and Mr Shadforth earlier in the day; Mr Shadforth had invited Mr Urquhart to the Macquarie meeting. Mr McLoughlin’s evidence was not challenged.

(d) Mr Neill had known Mr Shadforth in a personal and professional capacity for many years. Mr Neill was a substantial shareholder in IOOF. He knew the chief executive officer of IOOF, Mr Christopher Kelaher (Mr Kelaher), however he had no role in the management of IOOF and had no authority to act on its behalf. He knew Mr Olney-Fraser by early 2010 and had invested money with Stanfield Funds Management Ltd. The trustee of his family trust, Quality Life Pty Ltd was a substantial shareholder of Stanfield. He accepted that he knew at the time that Austock was an attractive investment at its then depressed share price. Mr Neill did accept that his understanding “from what was said during the meeting was that Morgan Stanley would be involved in partially funding the bid in some way because Morgan Stanley was interested in AET”. Mr Neill also accepted that he would have provided up to $500,000 to support Mariner’s bid “but probably only if Morgan Stanley and Macquarie, or an institution of similar standing, had also agreed”. He may have indicated this at the 21 June 2012 meeting, although he did not recall. Mr Neill recalled that there had been some discussion of a full bid at the 21 June 2012 meeting. According to Mr Neill, Macquarie indicated that they would assist in relation to acquiring a 20% stake by approaching Austock shareholders to sell and then placing such shares with their private clients; such private clients, presumably, may have then supported Mariner’s strategy. In terms of the $500,000 support, Equity Advisers may have taken shares to place and Mr Neill as a client may have taken such shares. Alternatively, he may have contributed by some form of convertible or promissory note, although the detail was unclear. At the meeting, Mr Neill said that he was very keen to be involved and that there was a need to move quickly before any decision on a sale of the property funds management business to another party was announced by Austock. Mr Neill also said that the Austock Life business would be very good buying at around $5 million and that IOOF would be interested at those levels. Mr Neill gave evidence that he had canvassed the Austock opportunity with Mr Kelaher about two or three years before. Mr Neill said that his presence at the 21 June meeting would be “an indicator” that he was there to “understand and support” the takeover bid.

(e) Mr Olney-Fraser said that he and Mr Christie spoke to the 19 June ATS which outlined the “value proposition”. He communicated that Austock was substantially undervalued at around 10 cents per share, and any buying at or around that level would be good value for Mariner, the other participants at the meeting and their investors. He said that the meeting discussed a price of 10.5 cents and that the plan discussed was to try to buy 20% off-market. However, if that could not be achieved by the following Monday, then a full off-market bid would be announced and there would also be purchasing on-market for 20% through Macquarie, Equity Advisers and Morgan Stanley Broking (if they agreed to participate).

(f) Mr Christie had a limited recollection of what had occurred as he had left the meeting early. Mr Christie says that he left with the impression that the participants were prepared to support Mariner financially in acquiring a substantial stake in Austock; again, this impression seemed nebulous and lacked content.

69 It seems that Mariner’s strategy relating to Austock had developed from the Board meeting the day before. It now included a full take-over bid for Austock. Mr Hoy recalls Mr Olney-Fraser saying that “We’re not having any luck in getting Austock shareholders over the line, so let’s just throw a bid [in] and see how we go.” Mr Olney-Fraser said he thought the words were more like “shake the tree”. The reference to not having any luck is likely to be a reference to the rejection by Mr Goh of the offer made for his shares.

70 Generally, it was accepted by the defendants that no conclusions were reached or commitments or assurances given at the meeting on 21 June 2012 by the non-Mariner participants.

71 Late in the afternoon of 21 June 2012, following the meeting at Macquarie, Mr Olney-Fraser returned to Mariner's office and informed Mr Fletcher of the meeting. Mr Olney-Fraser told Mr Fletcher that the meeting had gone well and that Mr Neill had agreed to assist with the takeover as he knew Austock's life insurance business was an attractive acquisition target. Mr Olney-Fraser also advised Mr Fletcher that he had received confirmation from Mr Goodwin that Arena might assist concerning funding.

72 At some time after the meeting and prior to 25 June 2012, Mr Christie was told by Mr Olney-Fraser that:

(a) Mr Hoy had said that Macquarie would have significant support from within their base; and

(b) Mr Shadforth said that he would be able to provide support, through his clients, for $500,000.

73 There is no direct evidence of any attempt on 21 June 2012 by Macquarie or anyone else to buy shares in Austock off-market after the 21 June board meeting. Mr Hoy gave no evidence about it in chief and was not asked about it in cross examination. Mr Olney-Fraser appeared to assume that calls were being made, but did not say how he knew or believed that. He said that Mr Hoy told him at the end of the day that he had had no interest from any of the unaligned top 20 shareholders. Mr Hoy was asked a couple of questions in cross-examination about a telephone call with Mr Olney-Fraser at the end of the day, but it was not suggested to him that it included this topic.

74 On the afternoon of Friday 22 June 2012, Mr-Olney-Fraser and Mr Goodwin exchanged text messages as follows:

(a) Mr Olney-Fraser asked Mr Goodwin at or about 1:51 pm to nominate someone at Morgan Stanley broking to whom he could speak;

(b) Mr Goodwin responded at or about 4:16 pm that he was “working on it”; and

(c) Mr Olney-Fraser then told Mr Goodwin that “Word's obviously out a bit as [Austock] this afternoon trading volume at 10c, not us. We have to move Monday morning first up.”

75 Mr Olney-Fraser and Mr Goodwin agreed that they needed to move quickly. Mr Goodwin told Mr Olney-Fraser that he wanted a public announcement on Monday to cut off Folkestone at the pass. If Folkestone acquired, effectively, the Austock property management business, that would stymie Arena’s own plans.

76 On Friday 22 June 2012, Mr Christie sent to Mr Olney-Fraser, Mr Hoy and Mr Shadforth a draft terms sheet for promissory notes to be issued to investors. This terms sheet was intended to relate only to the potential on-market acquisition of a 20% stake although its actual terms were arguably broader. These terms proposed that finance be provided for a period of 6 months from 1 July 2012 with investors to receive 50% of the profits (and bear all of the losses) from the purchase of shares in Austock. Repayment was proposed to be in cash or Austock shares, at the option of Mariner. I note that the promissory note concept was different from the convertible note concept referred to at the Macquarie meeting on 21 June 2012; the convertible note concept involved shares in Mariner rather than Austock.

77 Mr Hoy says that he took no notice of the draft terms sheet because he knew that the deal assessment committee within Macquarie would not approve it. Mr Shadforth did not respond to Mr Christie’s email and did not approach any of his clients to raise funds for Mariner’s bid through the issue of a promissory note. Mr Christie agreed that he heard no more about it after sending it.

78 A first draft of an ASX announcement was sent by Mr Fletcher to the other directors on the evening of Friday 22 June 2012. The draft included a paragraph in the following terms:

Mariner has spent time leading up to the takeover bid arranging a book build to secure funding support amongst various brokers and investors familiar with the success of Mariner’s recent acquisition activities. Mariner will provide information about funding, and the identity of persons who will provide cash consideration to meet the bid (and details of any underwriting) in our bidder statement.

79 At this point in time, Mr Olney-Fraser considered that the consensus from his discussions with Messrs Hoy and Shadforth included that Mariner would first try to buy up to 20% off-market over the next few days and that if Mariner could not get 20% off-market by Monday, it would (subject to a resolution of the directors) make a full takeover bid and put 20% buying “on the screen” upon the proposed takeover announcement being made. The draft paragraph referred to in the preceding paragraph came from the “Viento” ASX announcement; I will discuss the Viento documents shortly. It was later removed from the draft; it was inapposite in the present context.

80 At this time, Mr Olney-Fraser also said to Mr Christie that he was concerned that word was getting out into the market and that the price of Austock was moving. Accordingly, he said that it was important not to leave the market uninformed and that the possibility of the sale of the property funds management business to a third party meant that Mariner had to move quickly. Mr Christie and Mr Olney-Fraser discussed whether there was adequate funding support to make a takeover announcement at that stage and considered the past legal advice they had received on that issue from Don Clarke of Minter Ellison.

81 Further, in discussions at which Mr Fletcher was present, Mr Olney-Fraser stated that Arena had committed to the acquisition of the property funds management business in the amount of $10 million and to bridging finance and that Mr Neill “being on board” was significant as he had sufficient wealth to fund the entire acquisition. It is quite clear that Mr Olney-Fraser did not accurately state what the position was concerning bridging finance or Mr Neill’s position to either Mr Christie or Mr Fletcher.

82 In terms of Arena’s “commitment” at this point and how this may have impacted upon the mindset of Mariner and its directors, it is to be noted that Mr Goodwin conceded in cross-examination that:

(a) he would have known on 19 June 2012 that Mariner was not in a financial position to fund a large acquisition of Austock shares without some sort of external financing; Mr Goodwin was “fairly sure” he “would have known before the 25th” that Mariner could not “fund the full bid”;

(b) the purpose of the Stokehouse meeting was to “show Mariner how serious [Arena/Morgan Stanley was] about buying this childcare business”;

(c) Mr Goodwin wanted to “try and encourage … the Mariner people to make a bid for or otherwise acquire shares in Austock”;

(d) he could not deny that Mr Olney-Fraser raised the subject of “underwriting or bridging finance” during the Stokehouse dinner; he “definitely” had a discussion with Mr Olney-Fraser about a bridge facility at some point, but his position seemed to be that his “principal discussions” around funding came after the bid;

(e) Mr Olney-Fraser “may well have” raised the issue of underwriting or bridging finance in telephone discussions with Mr Goodwin before 25 June 2012;

(f) Mr Goodwin was trying to “play nice” with Mr Olney-Fraser “to give [Mr Olney-Fraser] the impression that [Arena/Morgan Stanley] were going to try and help ... and be cooperative to the extent [Arena/Morgan Stanley] could”;

(g) Messrs Goodwin and Olney-Fraser were speaking “every second day or thereabouts” in the two week period leading up to the announcement;

(h) Messrs Goodwin and Olney-Fraser definitely talked about “what Arena could do to assist” before the announcement; the issue in the case before me was, of course, the ambit of that “assistance”;

(i) Mr Goodwin “would have tried to make it clear” that he and Mr Mitchelson were “confident” they could get “the deal approved”; Mr Goodwin “would have said early on we were confident that we would be able to [get] the transaction approved”; again, the debate before me concerned the nature of the “deal” or “transaction” being referred to;

(j) Mr Goodwin said that “his memory” is that he offered Mariner $3 to $4 million of bridging finance but that this was an offer made after the announcement; and

(k) Mr Goodwin said that it is possible that he told Mr Olney-Fraser before 25 June 2012 that he “would ask Morgan Stanley for assistance”.

83 It is appropriate to observe that Mr Goodwin’s evidence evolved over the course of the proceeding from a brief account in his affidavit of his dealings with Mariner (and particularly Mr Olney-Fraser) to a more detailed account. Nevertheless, the theme of his evidence was consistent. He did not recall indicating to Mariner at or prior to 25 June 2012 the possibility of providing bridging finance.

84 At 7.56 pm on Friday evening, Mr Christie forwarded to Mr Olney-Fraser (via two emails) material that had been prepared and considered by Mariner concerning the takeover bid for Viento Group Ltd, including:

(a) a board paper dated 28 July 2011;

(b) a detailed schedule of a book build at that time;

(c) an ASX announcement dated 28 July 2011;

(d) a copy of an email dated 28 July 2011 from Mr Olney-Fraser to Mr Christie and Mr Fletcher; and

(e) a draft bidder’s statement used for Viento Group Ltd.

85 This material was circulated on Friday evening to be considered and appropriately modified for the Austock transaction.

86 The Viento board paper contained the following statement concerning s 631(2)(b):

Funding for Takeover Offer

The Corporations Act (s 631(2)(b)) and ASIC Reg Guide 59 impose requirements on an offeror before an intention to make a bid is announced to the market.

The Act says we cannot be “reckless” about whether a proposed bid is in fact made, and we cannot be reckless about whether we can fund a “substantial proportion of bids accepted”. The RG says that we must have “reasonable grounds for believing that we can fulfil the bid if accepted”. Neither the Act nor the RG require that funding is firm or underwritten when a bid is proposed.

Under s 636, the bidder statement (to be issued within 2 months) must set out the details of our funding, so that is the time when funding must be certain. The identity of the person(s) providing the bid cash consideration must be specified in that statement.

I have sought advice from Minter Ellison on this issue. In summary, their advice is that, at the time our announcement of a takeover bid, we should have a high level of confidence that we will be able to fund the bid if everyone accepts, however we do not need to be firm or have it underwritten until the bidder statement. In the bidder statement, we must identify where the funds will come from.

87 Further, Mr Olney-Fraser’s email of 28 July 2011 concerning Viento made reference to speaking with Don Clarke, a partner at Minter Ellison and a reference to his advice in terms:

[W]e need to have a reasonable basis for believing that we can fund the bid (i.e. not be reckless) but we don’t need to be firm or identify our source of funds in our ‘intention to make a bid’ announcement tomorrow; we do need to identify where the cash will come from in our formal bidder statement within 2 months.

88 I note that there was in evidence the unchallenged affidavit of Don Clarke deposing to the verbal legal advice that he had given to Mr Olney-Fraser in 2011 on s 631(2)(b). He confirmed that the advice that he had given was consistent with Mr Olney-Fraser’s recitation thereof in the 28 July 2011 email and the Viento board paper.

89 Clearly, as at late Friday evening and certainly as at the time of the board meeting on Monday morning 25 June 2012, the directors were aware of and had turned their minds to the legal requirements of s 631(2)(b). This is not a case where the directors were oblivious of or indifferent to the legal requirements of s 631(2)(b). I should note at this point, however, that the advice given by Minter Ellison differs from my own interpretation of “reckless”, but that is not material for the moment.

90 Before moving forward in the sequence of events, reference should also be made to the share price movements of Austock in the week ending 22 June 2012. One issue in the case, the relevance of which will become apparent later when discussing the credibility of Mr Olney-Fraser’s evidence, is when the share price started to “run”, if at all.

91 In the week ending 22 June 2012, Austock shares were only traded on 19 and 22 June 2012. On 19 June 2012, two trades occurred at 9.8 cents per share (31,000 shares); this was the same price that Austock shares last traded (14 June 2012). On 22 June 2012, the share price opened at 9 cents per share and closed at 10 cents per share. During the day there were 6 transactions with the total volume traded at 210,655 shares. On any view, during 22 June 2012 there was increased trading activity in Austock shares relative to prior periods. Moreover, on one view of the numbers, on 22 June 2012 the share price increased from 9 cents per share to 10 cents per share, which in terms of a relative change was significant. But ASIC takes a different view of the arithmetic. It says that at the start of the day there was a price fall (9.8 cents per share, the closing price from the previous day, to 9 cents per share) with a “recovery” to 10 cents per share, with a price change for the day of 0.2 cents per share; in other words a minimal change.

92 However you view the arithmetic, in my view there was some reasonable sense in which it could be said that there was unusual trading activity in Austock shares throughout 22 June 2012, but not prior. I will return to this issue later when discussing ASIC’s credit attacks on Mr Olney-Fraser.

93 Nothing of significance occurred on 23 June 2012.

94 On 24 June 2012, some documents were worked on. Late on 24 June 2012, Mr Olney-Fraser circulated to the other directors an amended version of what he described as the “cover” ASX Announcement. An amendment that was made in this version was to delete the paragraph referred to earlier from the draft prepared by Mr Fletcher. The amended version made no reference to the funding of the proposed bid. Mr Olney-Fraser’s email refers to this cover announcement being released with “Don’s document” (this appears to be a reference to Mr Christie) on the following day.

(i) The 25 June 2012 Mariner board meeting

95 Mr Olney-Fraser called a board meeting for 9.30 am on 25 June 2012.

96 At approximately 8.30 am on 25 June 2012, Mr Olney-Fraser says that he received a phone call from Mr Neill where Mr Neill stated that IOOF was still interested in the Austock Life business and would contribute $2 million if Morgan Stanley's broking division also injected $2 million. However, Mr Neill could not recall this phone call occurring or having any discussion with Mr Olney-Fraser about the level of support he was likely to provide prior to the bid on 25 June 2012. Mr Neill did not recall being specifically asked to commit to provide finance for Mariner’s takeover bid, or offering any such assistance to Mariner. He deposed that the maximum amount he would have provided in support would have been $500,000, if there was support from others. Equity Advisers may have taken shares to place and Mr Neill as a client may have taken such shares. I do not accept Mr Olney-Fraser’s evidence on the question of a reference to $2 million, although I am prepared to accept that at some stage Mr Neill indicated that he might support at a level up to $500,000.

97 At 9.14 am, Mr Christie circulated to the other directors a copy of a document titled “Mariner Board Paper” together with a draft fax and letter to the company secretary of Austock and the formal announcement of the proposed bid to the ASX. He had prepared the fax, letter and formal announcement over the weekend and on the Monday morning. In his affidavit, he denied having any role in the preparation of the Board Paper but later accepted that Mr Olney-Fraser’s recollection that it had been done by them jointly on his laptop was possible. I will discuss the Board Paper in more detail later.

98 At 9.16 am, Mr Goodwin sent to Mr Olney-Fraser a text message stating that he was “struggling to get support from M[organ] S[tanley] for anything hostile”. Mr Olney-Fraser did not understand Mr Goodwin’s message to mean that Arena was withdrawing from the proposal to acquire the property funds management business. By this stage Mariner had failed in its attempt to obtain off-market 20% of the shares in Austock. Mr Olney-Fraser said that he did not understand Mr Goodwin to have a problem with Arena being named in any bidder’s statement as the proposed purchaser of the property business. Mr Olney-Fraser replied to Mr Goodwin’s message that he would “discuss with my co-directors. We might do it this morning anyway”.

99 The following documents were prepared for the purposes of the Board meeting:

(a) A draft cover ASX announcement, a first draft of which was emailed by Mr Fletcher to Mr Olney-Fraser and Mr Christie at 6:40 pm on 22 June 2012. The draft cover announcement was subsequently amended by Mr Olney-Fraser.

(b) A more detailed ASX announcement, a draft of which was prepared by Mr Christie based largely on a previous ASX announcement that Mariner had made in relation to its proposed bid for shares in Viento.

(c) A draft letter to Austock – there is no specific evidence as to who prepared this document.

(d) A Board Paper and accompanying two page proposal recommending the proposed takeover offer, a Target Summary and spreadsheet.

100 The board meeting commenced at 9.30 am. At the board meeting the following occurred:

(a) Mr Olney-Fraser referred Mr Christie and Mr Fletcher to the spreadsheet and identified the committed funding parties for the initial $3 million on-market acquisition;

(b) Mr Olney-Fraser referred to the first paragraph under the heading “Funding for Takeover Offer” in the Board Paper and read it out aloud;

(c) The directors discussed the meaning of the term “reckless”. Mr Olney-Fraser explained that Mariner could not proceed with a takeover announcement without a reasonable basis for expecting that it could finance potentially up to 100% of shareholder acceptances even though a considerably lower level of acceptances was expected;

(d) Mr Fletcher asked Olney-Fraser if he had obtained any commitments in writing, and he and Mr Christie were told by Mr Olney-Fraser that:

(i) the first $3 million was committed by parties which had participated in previous Stanfield/Mariner capital raisings;

(ii) Arena remained committed to the acquisition of Austock's funds management business and had provided assurances to Mr Olney-Fraser that written confirmation of their offer would be made available in time for the bidder's statement;

(iii) Arena had also confirmed that Arena/Morgan Stanley would contribute bridging finance to ensure there was no timing issue in respect of the acquisition of Austock shares and subsequent sale of the Austock funds management business to Arena;

(iv) Mr Neill had confirmed that he was prepared to contribute to the funding not covered by Arena on the basis that the Austock Life business could readily be sold to IOOF; and

(v) Australian Unity was the other obvious buyer of the Austock Life business and that Mr Olney-Fraser was convinced that they would be interested.

101 Mr Christie has said that the Board discussed Arena's/Morgan Stanley's intention to buy the property business and the break-up value of Austock and that the Board then formed the view that Mariner would have no difficulty in arranging funding prior to the bidder's statement.

102 Neither Mr Christie nor Mr Fletcher were challenged in cross-examination as to their version of what occurred at the Board meeting. It is well apparent that Mr Olney-Fraser overstated the position concerning bridging finance coming from Arena/Morgan Stanley and also Mr Neill’s position. Their positions were not accurately represented by Mr Olney-Fraser to Mr Christie and Mr Fletcher.

(ii) The 25 June 2012 Mariner Board Paper

103 The issue of finance for the bid was discussed in the Board Paper. The Board Paper outlined a strategy for gaining control of Austock by making a takeover bid for all of the ordinary shares, although it was stated that it was believed that 25% was required to achieve the balance of power between the two factions on the Board. Mr Olney-Fraser’s evidence was that this should have said 20%. It is not material for present purposes whether such a strategy could have worked.

104 The Board Paper was unsigned. Its authorship is an issue in the proceeding. ASIC’s case is that it was written by Mr Olney-Fraser and based substantially on a board paper previously written by him for an earlier takeover attempt by Mariner of Viento. Mr Olney-Fraser’s evidence is that the Board Paper was “written in 10 minutes or so” and that he and Mr Christie “cut and paste[d]” from the board paper that Mr Olney-Fraser had written for an earlier takeover attempt by Mariner of Viento. Mr Olney-Fraser agreed with the proposition that the Board Paper contained errors and he sought to downplay its significance. But it was before the Board and considered by the Board. Moreover, the uncontested and unchallenged evidence of both Mr Christie and Mr Fletcher was that the Board Paper informed and played a role in their decision making process (see [34] and [35] of Mr Christie’s affidavit and [67] to [74] of Mr Fletcher’s affidavit).

105 One difference between the “Viento” board paper and the Board Paper was the absence of detail about funding support in the latter. Mr Olney-Fraser’s evidence was that he would “normally write a paper” with at least as much detail as the Viento board paper, but “that wasn’t done here because we really didn’t have the time. We were focusing on other matters”.

106 The section on funding for the takeover in the Board Paper commenced with reference to s 631. It was suggested that that section required Mariner to have “a reasonable level of confidence” that it would have sufficient funds for the bid. The author stated that:

In order to be in a position for Mariner to fund the takeover offer, I have done a book build today around our key brokers and investors. I attach a spreadsheet showing who I have spoken with, and what feedback and commitments I have secured.

Mr Olney-Fraser’s evidence was that the process that preceded the Viento proposal was an entirely different process. He said that this was an incorrect cut and paste from the Viento board paper. He said that he did not conduct any book build in order for Mariner to be in a position to fund the offer.

107 The spreadsheet attached to the Board Paper was prepared by Mr Olney-Fraser and dated 22 June 2012 (the Friday before). It identified four sources of what was said to be “on-market buying support” of $3 million. This $3 million figure is the funding or support that Mariner perceived that it required for the on-market acquisition of up to 20%. Accordingly, it was not directed to funding for the off-market bid. The spreadsheet then suggested that the realisation of Austock’s assets would produce $22 million, which was said to be “sufficient to fund 100% at 10.5 cents per share”. The use of the words “sufficient to fund” are notable. The spreadsheet in my view reveals the true position and state of mind of Mr Olney-Fraser. The assets of the target and their break-up value were seen as the foundation for obtaining funding. But, of course, the assets of the target could not literally fund the takeover in advance. But how the value of the assets of the target were relevant to funding was explained in the expert evidence that I discuss later.

108 For two of the sources identified for the on market acquisition up to 20%, namely Equity Advisers and Macquarie Bank, the support was to come from their clients. Of the other two named sources, as I have said Mr Neill was a private investor and IOOF was a company in which he was a shareholder, although not involved in its management.

109 Each of the persons named in the spreadsheet gave evidence that they made no commitment to Mariner to assist it with financing the takeover bid. Moreover, Mr Kelaher of IOOF, named as a source for potentially $1 million, never had any dealings with the directors of Mariner.

110 In any event, whatever may have been the position with these four sources, their potential contributions were to amount to $3 million, reflecting an acquisition of around 20%.

111 The second part of the spreadsheet demonstrated that the estimated realisable value of the assets was considerably in excess of Austock’s market capitalisation based upon a figure of 10.5 cents per share.

112 The Target Summary attached to the Board Paper was revised from the 19 June ATS (but undated). The 7 point strategy set out included the statement to “[d]irectly negotiate and acquire 20% from ‘Overhang’ shareholders”. It referred to a “[b]ook build pre formal takeover offer, by offering Mariner promissory notes secured by [Austock] shares to be acquired (limited, pro rata)” and the announcement of a formal takeover offer. The break-up values were set at $10 million for the property funds management business, $5 to 7 million for the life funds business, $5 million for cash held by Austock and $1 million for the shell, adding up to a range of $21 to 23 million.

113 The Board Paper stated that “We also should note that, in reality, we are only likely to require funding for up to 15% who would accept our bid. Nevertheless, we need to be in a position to…”. The narrative part of the paper abruptly stopped at this point. Mr Olney-Fraser’s evidence was that this paragraph “has no relevance and should not be there”.

114 The other possible sources of funding mentioned in the Board Paper were a capital raising by Mariner planned for July, “Stanfield”, “Nottingham” and “James Pearson/Cadence”.

115 No indication was given in the Board Paper as to the amount that might be generated from the proposed capital raising (in fact the share purchase plan was for $250,000). Stanfield Funds Management Ltd was a public company of which Mr Olney-Fraser and Mr Fletcher were directors. Nottingham Funds Management Pty Ltd was Mr Olney-Fraser’s family company. Both Stanfield and Nottingham were shareholders in Mariner.

116 In relation to Stanfield, there was little capacity for it to be a source of substantial funding. It had negative net assets or a deficiency in equity as at 30 June 2011 of $580,578. Moreover, its principal assets consisted of receivables, with the major receivable being a loan to Mariner of $913,786. Quality Life Pty Ltd, an entity associated with Mr Neill, was shown as holding 9.53% of shares in Stanfield as at 30 June 2011.

117 Mr Olney-Fraser gave evidence that this part of the Board Paper had “no relevance to the Austock context at all”. In terms of what was informing the directors as to potential funding sources, the possibility of Mariner obtaining funds from these sources has limited significance in determining whether the proposal made on 25 June 2012 was reckless.

118 The only reference to Morgan Stanley in the Board Paper was in the spreadsheet attachment to the Board Paper, where it was named as one of four prospective purchasers of the Austock Property Funds; there may be little doubt that Mr Olney-Fraser treated Arena and Morgan Stanley as one. It is notable that the reference was only to being a prospective purchaser of Austock’s property management business.

119 Mr Olney-Fraser gave evidence that he believed Arena would provide support for Mariner’s on-market bid that would come from the cash resources that Goodwin and Mitchelson could deploy in their capacity as joint managing directors without “too much up-line approval”. That proposition was not put to Mr Goodwin or Mr Mitchelson. It was not in Mr Olney-Fraser’s affidavit. ASIC submitted that it was contrary to the evidence that none of Morgan Stanley Broking, Morgan Stanley or Arena were included in the first part of the spreadsheet. ASIC submitted that any suggestion of Morgan Stanley or Arena providing support for Mariner’s “on-market” bid was “entirely reconstruction”. I agree with ASIC’s contention.

120 The minutes of the meeting of the directors of Mariner on 25 June 2012 record the formal consideration by the Board and the resolution passed in the following terms:

The Board considered a paper from Mr Olney-Fraser (attached) regarding a proposed take-over offer for Austock Group Limited (ACK)

The Board considered:

• the value of ACK as both an operating business and on a sum of parts valuation;

• the current shareholdings of ACK and the make-up of the Board;

• the company's available financial resources and the support from our network of brokers, funders and HNW supporters.

The Board resolved:

• In view of the information provided, the Board resolved to make an offer for ACK at 10.5 cents per share.

(iii) The 25 June 2012 ASX announcement

121 The release to the ASX occurred shortly after the board meeting at 10.03 am on 25 June 2012. It incorporated Mr Olney-Fraser’s draft from the previous evening, with minor amendments, and the drafts circulated by Mr Christie at 9.14 am that morning, which were unchanged. At 10:25 am, the announcement was published on the ASX Platform and stated inter alia:

Mariner will offer 10.5 cents per share, subject to 50% acceptance… Pending our off-market Bidder's Statement being sent to Austock shareholders, we intend to stand in the market from today to acquire up to 20% of the issued capital on-market at 10.5 cents per share to enable Austock shareholders to sell now, rather than wait for a bidder's statement...

122 The announcement included the text of a letter to Austock, which stated inter alia:

We expect to issue a Bidder’s Statement for shareholders, which will be issued to the Company and ASIC in accordance with the Corporations Act. Our intended offer will be made under Chapter 6 of the Corporations Act…

123 The proposed takeover bid was described as “an off-market offer” for all of the issued ordinary shares in Austock. The intended offer price was 10.5 cents. The intended offer was to be subject to eight conditions. Included among those conditions was a minimum acceptance condition of 50% of the subject shares as at the date the bid closed. Also included was a condition that after the date of the announcement neither Austock nor any subsidiary “sells, offers to sell or agrees to sell one or more companies, businesses or assets (or any interest therein) or makes an announcement in relation to such a disposal, offer or agreement”. No condition relating to the approval of any relevant regulatory authority was included in the announcement.

124 By virtue of the announcement, Mariner’s proposed takeover bid for Austock was “publicly proposed” within the meaning of s 631(2).