FEDERAL COURT OF AUSTRALIA

Donaldson v Natural Springs Australia Limited [2015] FCA 498

Table of Corrections | |

26 May 2015 | In paragraph 206, “(and in fact)” has been added to the fourth sentence. |

IN THE FEDERAL COURT OF AUSTRALIA | |

Plaintiff | |

AND: | NATURAL SPRINGS AUSTRALIA LIMITED First Defendant JURGEN CHRISTIAN KURT SCHLOTZER Second Defendant WOLFGANG ZINK Third Defendant PETER ROSE Fourth Defendant PRIME LOG BROKERS LTD Fifth Defendant |

DATE OF ORDER: | 22 May 2015 |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The plaintiff’s originating application be dismissed.

2. The plaintiff pay the defendants’ costs of and incidental to the proceeding including any reserved costs.

3. The defendants have liberty to apply for an additional order for costs against David Graer and Hakel Investments Pty Ltd.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 1178 of 2011 |

BETWEEN: | GORDON BRUCE DONALDSON Plaintiff |

AND: | NATURAL SPRINGS AUSTRALIA LIMITED First Defendant JURGEN CHRISTIAN KURT SCHLOTZER Second Defendant WOLFGANG ZINK Third Defendant PETER ROSE Fourth Defendant PRIME LOG BROKERS LTD Fifth Defendant |

JUDGE: | BEACH J |

DATE: | 22 May 2015 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

1 This proceeding concerns claims made by Gordon Bruce Donaldson (Donaldson) against the five defendants for:

(a) breach of contract;

(b) tortious conduct said to amount, in its various dimensions, to an interference with contractual relations; and

(c) oppression under s 232 of the Corporations Act 2001 (Cth) (the Act).

2 Donaldson, previously a director of the first defendant Natural Springs Australia Pty Ltd (Natural Springs), has alleged that each of the defendants intentionally interfered with the transfer of his shares in Natural Springs to a second company Hakel Investments Pty Ltd (Hakel Investments) and the registration thereof, causing him a loss of $300,000. Donaldson seeks damages of $300,000, alternatively an order that the defendants purchase his shares in Natural Springs for that amount.

3 For the reasons that follow, in my view Donaldson’s originating application should be dismissed.

Factual background

4 The background to this matter is protracted.

5 Natural Springs was a company that exported spring water to Asian markets including Singapore. Natural Springs initially operated by sourcing Australian spring water and bulk shipping it to Albatross International Pty Ltd (Albatross) in Singapore, its agent for a time, for bottling.

6 On 21 May 2001, Donaldson acquired the issued capital of Natural Springs (then called “Your Team Pty Ltd” and later “Liquid Bulk Solutions Pty Ltd” until its name change to Natural Springs as part of the 22 March 2005 restructure). Until 22 March 2005, Donaldson was the sole director and shareholder.

7 From 2002, the second defendant Jurgen Schlotzer (Schlotzer) was an employee of Natural Springs. Schlotzer was also a director of Albatross from 1 June 2004.

8 On 22 March 2005, Natural Springs was restructured. Schlotzer and the third defendant Wolfgang Zink (Zink) were appointed as directors, with Donaldson continuing as a director. Schlotzer was also made the manager of finance and logistics; Schlotzer was also an alternate director for Zink. At that time, each of Donaldson, Schlotzer and Zink effectively acquired 11.96 million shares in Natural Springs. Schlotzer's shares were held by the fifth defendant, Prime Log Brokers Pty Ltd (Prime Log), a company of which he was the majority shareholder and managing director. Zink was based in British Columbia, Canada and at all relevant times was absent from Australia. Zink’s shares were held on trust. The fourth defendant Peter Rose (Rose) was an investor who, along with his wife Leisa Rose, acquired a shareholding of 3.12 million shares held on trust for the Rose Family Trust.

9 The 11,959,900 shares issued to Donaldson on 22 March 2005 were issued to him in his capacity as trustee of the Donaldson Family Trust. At that time, Donaldson already personally held 100 shares in Natural Springs, which shareholding pre-dated the restructure. The fact that Donaldson’s shares were held in two different parcels and in two different capacities is relevant to an issue which I will later address concerning the forms of share transfers that he later proffered for registration under cl 51 of Natural Springs’ Constitution.

10 On 19 May 2005, Natural Springs was converted to an unlisted public company and adopted a new Constitution. Relevantly, cll 2, 6, 11(a), 18, 20, 23, 24, 45, 46 and 51 to 53 of the Constitution provided:

Effect as a Contract

2. This Constitution is as a contract between:

(a) the Company and each Member, and

(b) the Company and each Director and each Secretary, and

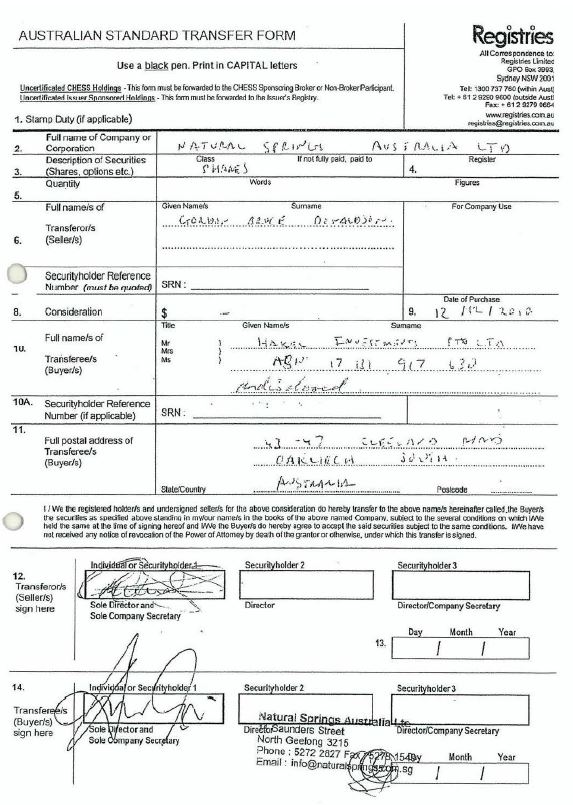

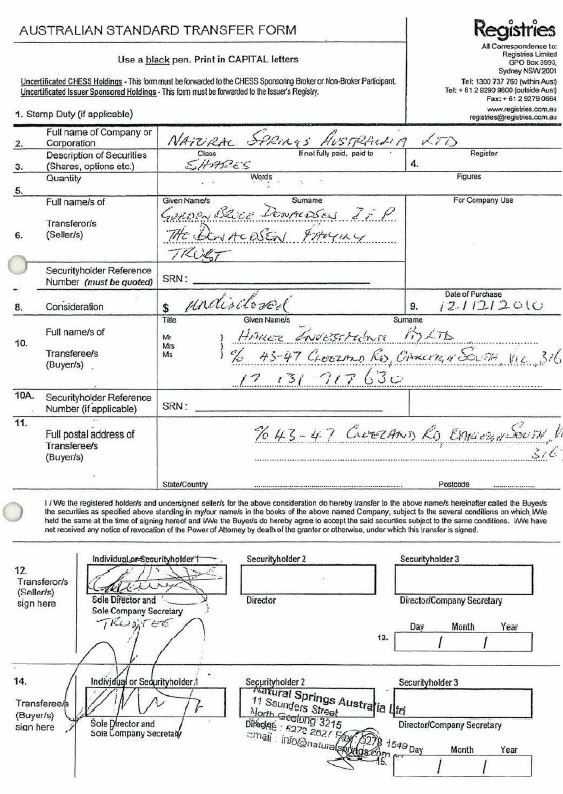

(c) a Member and each other Member; and each person agrees to observe perform and be bound this Constitution.

…

Management of Company

6. The Company is managed by its Directors, who may delegate their powers.

…

Powers & Entitlements

11. The Directors may do anything permitted by law, including each of the following:

(a) exercise all of the powers of the Company which are not required to be exercised by the Members in General Meeting;

…

Calling of Meetings

18. A Director may call a Directors' Meeting at any time, and the Secretary will call a meeting of Directors if asked to do so by a Director.

…

Quorum

20. At least 2 Directors must be present before business can be transacted at a Directors’ Meeting.

…

Voting at Directors’ Meetings

23. A question that arises at a Directors' Meeting will be decided by a vote. The Chairperson of the meeting may not cast a second vote. A decision reached by vote is treated as the decision of all the Directors. In the event of equal votes, the question will be deemed to have been decided in the negative.

Method of Meeting

24. The Directors may hold a meeting in person, or by telephone, video conference or any other means of communication, provided everyone can hear and be heard throughout the meeting. If the meeting is not held in person, each of the following conditions are to be met for the meeting to be valid:

(a) each of the Directors has received notice of the fact that the meeting is to be held; and

(b) each Director who is present must announce, at the beginning of the meeting, that he or she is present.

…

Share Certificates

45. The Company will give each Member, free of charge, a Share Certificate. In the event that Company maintains a Seal, the Directors may determine if it is to be affixed to a certificate issued. If the Company does not maintain a Seal, or if the Directors have not determined that the Seal be affixed, then a Share Certificate will be signed by a Director or Secretary of the Company. If the shares are jointly owned, it is sufficient to give a Share Certificate to one of the joint Members.

Recognition of Interests in Shares

46. Except where required at law, the only interest in shares that the Company recognises is the registered Member's absolute right to the whole of the share.

…

Transfer Of Shares

51. A Member may transfer shares to another person by completing a written transfer document in a common form or a form approved by the Directors, signed by or on behalf of the Member and the purchaser. To have the transfer registered by the Company, the transferor or transferee must give the written transfer document and the relevant share certificates to the Company. The Directors may require additional evidence of the transferee's entitlement to be registered before registering the transfer. The transferee becomes the holder of the shares when the transfer is registered and his or her name is entered in the Register of Members. The Company retains the transfer document.

Suspension Of Registration

52. The Directors may suspend registration of shares at any time for any reason, however the total period of suspension must not exceed 30 days in any year.

No Right To Refuse To Register Transfer

53. Except as permitted by the Act or at law, the Directors may not refuse to register any transfer.

11 Donaldson has asserted that in or about April 2006 the relationship between himself and each of Schlotzer, Zink and Rose broke down. He gave the following examples:

In April 2006 he prepared a discussion paper outlining his concerns in relation to Natural Springs. He was concerned at this time that Schlotzer was “still drawing a salary of $60,000 per annum from Natural Springs… [while] also receiving money via Albatross out of Singapore” whereas Donaldson was receiving around $300 per week for his work. As Donaldson saw it, he was angry that the profits of Natural Springs were effectively being “diverted” to Schlotzer through Albatross’ failure to remit the contract price of various invoices and that Natural Springs was paying for Albatross’ expenses.

Donaldson said that he was under considerable pressure from Schlotzer and the other shareholders/directors who he said effectively “acted as a block” and “ganged up”.

Donaldson emailed his discussion paper to Zink. Donaldson asserted that at a Natural Springs’ board meeting held on 21 April 2006, Schlotzer was angry that Donaldson had communicated with Zink.

Donaldson asserted that Schlotzer told him that if he did not resign, he would be removed as a director and sacked as an employee.

12 Donaldson also had other issues with Schlotzer. Donaldson was unhappy that Schlotzer had travelled to Hong Kong and China to perform work for another company around November 2005, leaving Donaldson to run Natural Springs without assistance and retaining the benefits of being on the payroll. Donaldson also perceived that Schlotzer was not properly contributing to Natural Springs, except for bookkeeping. Further, Donaldson was unhappy that Schlotzer required approval for Donaldson's expenditure but did not seek approval for his own expenditure.

13 There is little doubt that Schlotzer was dissatisfied with Donaldson’s conduct. For example:

In October 2005, Donaldson volunteered to provide technical assistance to Albatross in Singapore, to assist with the installation of a new bottling plant. Apparently Donaldson wanted to assist because, in part, the travel fitted with his interest to do a motorcycle trip from Singapore to Phuket, Thailand with some friends. Donaldson travelled to Singapore but left the Albatross project unfinished to attend to his holiday. Ms Sheila Wee, an employee of Albatross, telephoned Schlotzer to complain about that conduct.

Schlotzer spoke to Donaldson several times in early 2006, after Donaldson returned from his trip, about that conduct and that he was unhappy with Donaldson’s behaviour.

Schlotzer subsequently asked Donaldson to take 3 weeks leave to consider his position in Natural Springs.

At the board meeting on 21 April 2006, there was discussion (in Donaldson’s presence) of his excessive expenditure, his conduct in Singapore and other causes of dissatisfaction with his conduct. Schlotzer accepted that Donaldson was requested to resign.

14 Donaldson himself had some awareness of his level of under-performance. For example, the opening three paragraphs of his “discussion paper” said the following:

Just over three weeks ago, Jurgen has accused me of not doing my job properly, citing that over the past 9 months or so that I have not been putting in a full effort and that he feels he has to oversee my work. In making this accusation he has said that while the issues he speaks of are individually small, the total runs up to be a larger problem to him. He has therefore questioned my role in the company as Managing Director and hence what my future with the company is. Stating that he has Wolf’s proxy on the matter I was to take three weeks off and think about my role and future with the company.

Having taken the request, I have spent this time to consider my past and future in respect to these matters and make the following comments.

Whilst I do not think for a moment that I have lost site [sic] of what is best for the company I will certainly concede that I have been somewhat untidy in my activity, an area in which I intend to concentrate on improving. The fact that I chose to discuss most things with Jurgen rather than just doing it without his involvement, then I am guilty. My desk is a mess as well as the workshop area I use. These areas are problems that I intend to change for the better.

[emphasis added]

15 Rose also gave evidence, not cross-examined on, concerning Donaldson’s work practices. So he said in his affidavit at [10] to [11]:

10. Throughout 2005 I began to observe Mr Donaldson in the workshop more and I began to become personally concerned about how he was performing and going about things. I believed Mr Donaldson's methods were very inefficient, for example he preferred to buy equipment in parts and put it together himself rather than looking to see whether the same equipment could be bought at a lower price off the shelf. I also began to see that Mr Donaldson would spend money for the business regardless of whether there was money in funds to spend.

11. In January 2006 Mr Donaldson went over to Singapore to set up the bottling plant. Mr Schlotzer told me that Mr Donaldson had not finished this job properly and had left to go on a holiday in Thailand, leaving the bottling plant in a mess. I was concerned about this and thought the Mr Donaldson was not showing proper responsibility in what he was doing and was not doing what was best for NSA's interests.

16 On 24 April 2006, Donaldson resigned as a director of Natural Springs and was replaced by Rose. From about that time, Donaldson alleged that he was effectively “shut out” from management of Natural Springs. I will deal with this assertion later.

17 Soon after his resignation, Donaldson attended the offices of Natural Springs with his sons Christopher Donaldson and David Donaldson to collect his belongings. Schlotzer alleged that at this time Donaldson removed his share certificates from the premises; Donaldson denied this.

18 Donaldson remains a shareholder of Natural Springs, holding a total of 11.96 million shares personally (as to 100 shares) and as trustee (as to 11,959,900 shares).

19 On 8 January 2007, Schlotzer resigned as a director of Natural Springs. He had earlier sent a letter dated 12 December 2006 to Natural Springs in the following terms:

I herewith would like to tender my resignation as Managing Director of Natural Springs Australia Ltd at the earliest possible date.

As discussed with Peter and Wolfgang I am looking to take up a leading role in Natural Springs Australia (HK) Ltd and to avoid any conflict I am voluntarily stepping down from my position in NSA.

I am prepared however to continue with the current operation in Geelong for NSA as Chief Executive Officer and my remuneration shall be unchanged. I will report to the board of Directors on a regular basis.

20 Donaldson alleged that following this time, Schlotzer nonetheless continued to act as a director in a de facto sense. Schlotzer has denied this but in my view and given the nature of Schlotzer’s activities, I accept Donaldson’s contentions in this respect. On that day, Schlotzer was appointed as the Chief Executive Officer of Natural Springs, a position he continued to hold until 26 November 2010. Angela De Lucio Huerta (Huerta) was appointed as a director of Natural Springs in Schlotzer’s place. Huerta is the wife of Schlotzer. Since 5 December 2006, Huerta has been the company secretary for Natural Springs. Donaldson alleged, however, that Schlotzer also acted as the de facto company secretary. Huerta was also a shareholder in Prime Log, as well as a director of Albatross (as was Schlotzer and others) and its majority shareholder. As I have said earlier, Schlotzer has acted as an alternate director for Zink. Huerta has also alternated for Zink. After Schlotzer’s resignation as a director, thereafter the directors of Natural Springs at all relevant times were Zink, Rose and Huerta, with Huerta as company secretary.

21 Before proceeding further, I should make several observations. The events in 2006 were remote from the real issues in the case which turned on the events dealing with the share transfers in late 2010 and early 2011 and the alleged sale to Hakel Investments. Donaldson sought to use these historic events as an important foundation to the oppression case and a significant setting for the events 4 to 5 years later. I must say that I found the 2006 events remote and ephemeral to the real issues that I had to decide. True it was that there had been a breakdown of the relationship between Schlotzer and Donaldson leading to Donaldson’s resignation in 2006. No doubt this was in part due to the differing personalities involved. Donaldson had a style which did not put a premium on attention to detail. Schlotzer was highly intelligent and had an exactitude which Donaldson lacked. Such differences also manifested themselves in the way each dealt with the events of 2010 and 2011. Each sought to give their honest recollections in evidence, albeit from their different perspectives of the key events. No doubt their breakdown in 2006 was due to the events that I have recited and each parties’ differing perspective thereon. But so far as I am concerned, I do not need to definitively determine each asserted “right and wrong” associated with the 2006 events. The fact is that in 2006, Donaldson resigned as a director and then remained a largely passive investor in Natural Springs for many years thereafter. There were no acts of “oppression” then or thereafter. Indeed, there is little evidence demonstrating any complaint after 2006 by Donaldson as to how Natural Springs’ affairs were being conducted apart from the conversion of Natural Springs’ status which I refer to at [61]. He remained a passive investor. He continued to receive all notices, reports and financial accounts as a shareholder as he was entitled to do. He was given the opportunity to attend every annual general meeting. Over the intervening period, Schlotzer and Donaldson were not on the best of terms, but had little to do with each other. Donaldson’s “oppression” case in my view is contrived, at least in so far as it sought to be founded on these historic events. They only have relevance in the most general of ways in setting the scene for the 2010/2011 events.

(a) Attempted sale of Donaldson’s shares to Natural Springs

22 In 2006, Paul Madden (Madden) of Advance Business Centres (ABC) Accountants, company accountant for Natural Springs, offered on behalf of Natural Springs to buy back all of Donaldson's shares for $5,000. Donaldson declined on the basis that he believed this to be an undervaluation.

23 On 6 December 2007, an annual general meeting of Natural Springs was held. Donaldson was in attendance. At that meeting a motion was passed by Natural Springs to purchase back 100,000 shares from a shareholder, Mr Gero von Aderkas McFarlane, for the original purchase price of $5,000 (being 5 cents per share). McFarlane had provided a loan to Natural Springs and in return had been issued shares. When the loan was repaid, the shares were repurchased. As Schlotzer explained, the shares were collateral for the loan; the price set was a nominal price and was not intended to represent the true value of shares in the company at the time they were issued; they were not based on a valuation. At that time, Donaldson asked Schlotzer to buy back his shares at this rate of 5 cents per share (which transposes into just under $600,000 altogether). Schlotzer declined and said that Natural Springs would purchase Donaldson’s shares for $100 in total; Donaldson rejected that offer.

24 In early 2008, Madden offered on behalf of Natural Springs to buy back the totality of Donaldson's shares for $10,000. No sale occurred.

25 On 11 June 2008, an annual general meeting of Natural Springs was held. Donaldson, Huerta and Schlotzer attended. Donaldson again offered to sell his shares back to the company at the rate of 5 cents per share. Schlotzer again rejected this offer on behalf of Natural Springs. The option for Donaldson to sell his shares back to Natural Springs was not taken further.

26 There are several further matters of context that should also be noted at this point. Donaldson had little to do with Natural Springs after 2006, apart from such discussions dealing with the transfer of his shares. Moreover, after 2008, the question of the sale of Donaldson’s shares was not raised again until 2010. There was otherwise little interaction between Donaldson and the defendants after 2006 until the end of 2010. However, Donaldson attended several annual general meetings, received copies of various accounts but advanced little opposition as to how the affairs of Natural Springs were being conducted.

(b) Attempted sale of Donaldson’s shares to Hakel Investments

27 In early 2010, Donaldson engaged Advisory Business Solutions Pty Ltd (ABS), a corporate advisory company related to Hakel Investments, to negotiate the sale of his shares. Mr David Graer (Graer) is a partner at ABS. Graer deposed that Donaldson asked him to investigate whether he could find other purchasers, whereby Donaldson and the new purchasers could take over the business of Natural Springs by buying out the other shareholders. However, in cross-examination, Donaldson denied that his intention was to buy out the other shareholders, although his position on this fluctuated and was not entirely clear.

28 Graer subsequently “completed due diligence of the water industry” including approaching a number of people in the “Australian investment industry” who might be interested in so purchasing. Apparently, Graer himself then became interested in purchasing all of the shares in Natural Springs through his own company ABS. Graer telephoned Schlotzer and enquired whether Schlotzer was interested in selling Natural Springs. Schlotzer was apparently initially receptive, but according to Graer became hostile when Graer said that he represented Donaldson. Further, Schlotzer allegedly said that if Donaldson was looking to sell his shares, the other shareholders would not be the buyers.

29 In mid-May 2010, Graer arranged to meet with Schlotzer to have an informal meeting with him in relation to the water business; Graer wanted to discuss the possibility of ABS buying into Natural Springs. Graer and Schlotzer met at a café in the city in Melbourne along with two other persons. This was the first time they had met in person. Schlotzer and Graer also discussed the sale of Donaldson’s shares, but Graer was primarily interested in discussing the purchase of Natural Springs. Allegedly, Schlotzer became angry when Donaldson was mentioned. Schlotzer said that “he and his partners” would not sell their shares and that Natural Springs was an “offset business for other water businesses overseas”. Schlotzer apparently made two offers – of $10,000, and then $5,000, to purchase Donaldson’s shares. Graer apparently offered to purchase the entirety of the shares in Natural Springs for $10,000.

30 A few days after this meeting, Graer apparently had a follow-up telephone conversation with Schlotzer. Schlotzer said that Natural Springs was not for sale to Graer. Schlotzer again offered to purchase Donaldson’s shares for $5,000. Graer offered to purchase the entirety of the shares in Natural Springs for $5,000. Schlotzer apparently rejected this offer.

31 Nothing further was then heard by Schlotzer about Graer’s interest in Natural Springs until late 2010 (see [44] below).

32 On 25 November 2010, a board meeting of Natural Springs was held to discuss the future of the company. Rose, Huerta and Schlotzer were in attendance. Schlotzer acted as an alternate director for Zink on that occasion. The board discussed its concern that Natural Springs’ relationship with Albatross had ended on 1 September 2010 and that as a result Natural Springs had “lost the majority of its income”. It is important to set out the minutes and resolutions made at that meeting as it provides the setting for later events. Moreover, and contrary to what Donaldson now asserts, it shows that Natural Springs and Schlotzer acted quite appropriately in seeking to wind down the affairs of Natural Springs. No evidence was advanced by Donaldson (other than his bare assertions mostly raised after the event) challenging the appropriateness of the steps to be advanced. The minutes recorded:

The directors of the company have met to assess the situation of the company. It has been an ongoing concern that the business relationship with Albatross International Pte Ltd. Singapore had come to an end effectively on 1. September 2010.

For that reason the company has lost the majority of its income. The financial situation is becoming difficult. Therefore it has been decided to close the warehouse and sell off the remaining assets.

It was decided that it will be brought to the shareholders during the next shareholders meeting that the company has ceased operation with effect of 27.11.2010. It will be recommended to the shareholders that the company been [sic] voluntarily closed.

The company has no 3rd party liabilities. It will need to be put to the shareholders that the cost for dissolving the company will have to be raised by the shareholders, as the company has no further assets, because:

1) It was decided that all remaining assets will be taken over by Prime Log Brokers Pty Ltd at book value and that this purchase price shall be reconciled at value against the outstanding liability the company has towards Prime Log Brokers.

2) It was decided to terminate the lease of the company vehicle WAC 190 with effect of 30.11.2010.

3) It was decided the Prime Log Brokers will take over the remaining outstanding from Albatross International in Singapore and will reconcile the proceed [sic] against the outstanding liability the company had towards Prime Log Brokers.

4) Upon dissolving the company Prime Log Brokers has agreed to waive all remaining outstandings which will then put the company in a neutral position – free of any liabilities (other than current tax and accounting fees).

The company will require a further $10,000 for outstanding tax liabilities, accounting and auditing fees. The company is not expecting any income and the directors are requesting the shareholders for additional contribution.

This issue shall be discussed during the next AGM. As an alternative the directors propose to issue shares and offer these to the shareholders for purchase. The directors propose to offer an additional 10,000,000 shares for consideration of $10,000.00.

It was decided that the Annual General Meeting for the financial year 2009/2010 and all the above issues to be held on 21.12.2010 at 11 am at the office 11 Saunders Street, North Geelong. Mr Schlotzer will send the invitation to the members together with the financial statements 2009/2010.

It was decided that Mr. Jurgen Schlotzer will be relieved from his duty as CEO on 26.11.2010. and his last salary payment shall be on 29.11.2010. Notice was given to Mr. Schlotzer already in October 2010. Mr Schlotzer agrees to this decision.

[emphasis added]

33 On 26 November 2010, Schlotzer emailed Donaldson stating that the directors of Natural Springs had resolved to:

(a) relieve Schlotzer from his position as CEO with effect from 26 November 2010;

(b) cease Natural Spring’s operations with effect from 27 November 2010; and

(c) recommend to the members of Natural Springs that the company be voluntarily wound up.

34 It is appropriate to set out its text, which was:

Hello Bruce

I am pleased to advise that we have scheduled our next AGM for Natural Springs Australia Ltd for Tuesday 21. December 2010 at 11 Saunders Street, North Geelong at 10am.

Attached please find the financial report for the year ending 20.06.2010 as well as a directors resolution.

Topics of the AGM are outlined in this resolution.

In particular the following issues will need to be resolved by the shareholders of the company:

1) the closure of Natural Springs Australia Ltd at 31.12.2010

2) call for additional funds to pay for forthcoming company administrative liabilities (tax, accountant, auditor etc.)

Please confirm receipt of this mail and your attendance.

Best regards

for and on behalf of

Natural Springs Australia Ltd

Jurgen Schlotzer

35 The text and attachments (the financial report and the minutes referred to above) demonstrate to my mind appropriate and commercial behaviour on the part of Schlotzer and Natural Springs. There are several observations to make. First, Donaldson was sent the directors’ resolution I have just referred to. At the time, there was no objection by Donaldson to the course proposed. Donaldson now says in his evidence that he didn’t receive this because at the time he was away (T33). But he did not say this in his first affidavit of 29 January 2013 (see at [73]). In any event, he responded to this email on 15 December 2010. He has now also complained that he did not receive notice of that directors’ meeting. But that complaint goes nowhere as he was not a director. Second, the way Schlotzer expressed himself to Donaldson in the invitation did not suggest to me any deep seated animosity on the part of Schlotzer. The communication was in appropriate and informative terms. Third, Donaldson was sent the financial report for the year ending 30 June 2010. That disclosed an excess of liabilities over assets (liabilities totalled $226,265 and assets $144,269 as at 30 June 2010) and a net deficiency of $81,996. For the year ending 30 June 2010, profit before income tax was $60,113. Donaldson at the time took no issue with these figures, this financial position or how Natural Springs had reached this point. And as I say, from 1 September 2010, Natural Springs had lost the majority of its income. A further notable feature is that after this time, on Donaldson’s case, Hakel Investments offered to purchase his 30.66% interest for $300,000, and notwithstanding that Graer made no financial investigation of Natural Springs’ affairs at this time; Graer’s “due diligence”, if it could be so described, pre-dated May 2010. I will deal with this apparent paradox later.

36 On 2 December 2010, Schlotzer sent the following letter to Donaldson:

Hello Bruce,

[S]ince I have not received your confirmation that you have received my e-mail invitation I herewith would like to inform you that we have scheduled our next AGM for Natural Springs Australia Ltd for:

Tuesday 21. December 2010 at

11 Saunders Street, North Geelong

at 10am.

The financial report for the year ending 20.06.2010 [sic] as well as a directors resolution has been sent to you by email on 26.11.2010. If you have not received it kindly advise your new e-mail address.

Topics of the AGM are outlined in the resolution.

Please confirm receipt of e-mail and your attendance.

Best regards

for and on behalf of

Natural Springs Australia Ltd

Jurgen Schlotzer

37 On or about 11 December 2010, Donaldson had a telephone conversation with Graer about the sale of his shares to Hakel Investments. On 12 December 2010, Graer and Donaldson agreed that Donaldson would sell his shares in Natural Springs to Hakel Investments for $300,000. Graer asserted that this agreement was subject to conditions; I will deal with the detail of this later. There was no written agreement.

38 Graer was not a director of Hakel Investments. Rather, Ms Merryn Young (Young), Graer’s wife, was the sole director and sole beneficial shareholder of Hakel Investments. Graer asserted that he “owned” Hakel Investments, but the evidence indicated that Young did. In his second affidavit sworn on 3 March 2014, Graer asserted that he had the power to bind Hakel Investments to legally enforceable agreements, and that at all times after agreeing to purchase the entirety of Donaldson’s shares, Hakel Investments was “ready, willing and able” to pay the agreed purchase price of $300,000 (at [7]).

39 Donaldson alleged that he subsequently acted to give effect to the sale of his shares to Hakel Investments, but due to the actions or omissions of the defendants the share transfer was frustrated or “stonewalled”. I reject Donaldson’s assertions that the defendants frustrated or stonewalled the transaction. Rather, Donaldson neglected to comply with cl 51 of the Constitution, notwithstanding that this was pointed out to him. It is appropriate to elaborate on the relevant chronology of events in this respect.

40 On 12 December 2010, Donaldson attended Graer's office. With the assistance of Alan Munt (apparently previously a lawyer and a consultant to ABS), Donaldson and Graer completed and signed two share transfer forms. Munt was the person who initially introduced Donaldson to Graer. It was asserted that he was present at various critical times, including when the share transfer forms were apparently signed on 12 December 2010. He was not called to give any evidence. Graer apparently found the blank share transfer forms online, and printed them for this use. There were errors and inconsistencies in Graer's evidence. In one of his affidavits, Graer stated on three separate occasions that he prepared the two share transfer forms on 12 December 2010. But during cross examination, Graer stated that he believed his wife or Munt prepared the share transfer forms. Donaldson gave evidence that Munt filled out one form and Donaldson filled out the other (cf Donaldson’s affidavit sworn 11 March 2014 at [46] where he originally said that Graer printed and filled out the forms). Donaldson and Graer then signed them. The detail of these inconsistencies is not material for present purposes. On those forms, the following information was completed: the name of the company, the description of the securities, the names of the transferor and transferee, the date of purchase, the postal address of the transferee and the signatures of the parties. The quantity of shares, consideration, security holder reference number and date of signing fields were left blank. It appears that two forms were used to purportedly effect the transfer of shares held by Donaldson both personally and in his capacity as trustee. Donaldson signed one form in his personal capacity, and one form in his capacity as trustee. Both forms were incomplete in various ways, the detail and significance of which I will return to shortly.

41 Donaldson said that he and Graer agreed that Donaldson would deliver the forms to Natural Springs for the purpose of Natural Springs processing and registering the transfers including entering Hakel Investments’ name in the share register.

42 On the same day, Donaldson posted under cover letter to LBW Accountants (being the appointed auditors of Natural Springs) the share transfer forms executed by himself and Hakel Investments. This was an erroneous step. The transfers should have been sent to Natural Springs’ address or the company secretary. At all events, the transfers were not sent to the correct address. Donaldson in his affidavit of 29 January 2013 at [86] gave an explanation as to why he sent the transfers to the auditors. Whatever the explanation, he did not send them to the correct address. The cover letter, which in the top right hand corner made reference to “The Donaldson Family Trust”, provided inter alia:

Re: Shares held by this trust and those of Gordon Bruce Donaldson…

This is to advise that all shares held by the above are hereby sold to Hakel Investments …

Noting that while documentation exists for 11,959,900 shares, in the name of Bruce Gordon Donaldson (incorrectly stated for order of name in the Minutes of the Annual meeting 06.12.2007) the numbers of shares held by the two parties (The Donaldson Family Trust & Gordon Bruce Donaldson individual) are not distinguished apart.

As contact with the company is hostile, hence this letter serves to clarify my believe [sic] that the split of ownership is possible and there are possibly another 100 or so shares held separately in my name from the original changing of structure to the unlisted company.

The sale of these shares is done in consideration to the payment of funds negotiated.

43 I have set out in a schedule to these reasons the 2 incomplete transfer forms in the form that they were hand delivered by Donaldson to Schlotzer on 5 February 2011 who then stamped a receipt thereon (see at [53]).

44 On 15 December 2010, Donaldson emailed Schlotzer informing him of the sale of all his shares to Hakel Investments. This email responded to Schlotzer’s email of 26 November 2010 which I have referred to at [34] above. This of course demonstrates that Donaldson received the 26 November 2010 email and attachments. This was the first occasion that Natural Springs itself received, albeit informally, notice of the proposed transfer (putting to one side for present purposes the letter and attachments sent to the auditors). Donaldson’s email set out the following:

Good morning Jurgen

Please note that I have sold the shares in Natural Springs Australia Ltd held by the Donaldson Family Trust and myself to Hakel Investments Pty Ltd as such [sic] I will not be attending the AGM.

Regards

Bruce Donaldson

45 Further, on 15 December 2010, Graer also emailed Schlotzer informing him of the purchase by Hakel Investments of the shares held by Donaldson both personally and as trustee. That email provided as follows:

Following our discussions and subsequent meeting, please be informed that Hakel Investments pty ltd has purchased the shares held by The Donaldson Family Trust and Bruce Donaldson in his own right.

Therefore any notices and correspondence should be directed to the attached address.

Further your letter to Mr Donaldson outlines the Financial report and Directors Resolution, could be so kind now to send same to the attached email.

As discussed sometime ago we would like to attend the AGM, the topics from my position will be the value of the shares held and actual value of the operating entity.

This will have to be quantified as the offer for our shares were such that the whole business was worth $17,670.00 [sic], I feel this will have to be a question to the Auditors amongst others.

Please call at any time should you have any queries and look forward to meeting with the shareholders on the 21/12/2010 with my advisors.

46 On 20 December 2010, Schlotzer replied to Graer stating that the procedures for a transfer of shares had not been followed, as Natural Springs had not been provided with any share transfer documentation to date, and accordingly that the transfer had not been effected. That email provided as follows:

[Y]our mail noted.

Following paragraph 51 of the constitution of Natural Springs Australia Ltd certain procedures for a transfer of shares will need to be followed. The company has not been notified and provided with any documentation to date. Accordingly the company records do not reflect any changes in shareholders.

As such the company does not recognise Hakel Investments or its representatives as a member and an invitation to the forthcoming Annual General Meeting is not issued.

47 At this point, it should be noted that the transfer forms were incomplete, the transfer forms were not accompanied by the share certificates, and the incomplete transfer forms had been sent to the auditor’s address, rather than Natural Springs’ registered office address or its company secretary at least. Graer originally stated in his evidence that he did not receive a reply to his email of 15 December 2010. That assertion was inaccurate. Graer conceded in cross-examination that he did receive a reply; this is but one example of the general unreliability of Graer’s evidence; I will deal in more detail later with Graer’s lack of credibility.

48 On 21 December 2010, an annual general meeting of Natural Springs was held. Donaldson attended briefly before the meeting commenced and informed the attendees that he had sold his shares to Hakel Investments and did not intend to attend the 2010 AGM as he was no longer a shareholder. Donaldson alleged that Schlotzer said that he would not accept Hakel Investments as a member of Natural Springs and would not register the transfer. Schlotzer denied this, claiming that he said that Hakel Investments was not welcome at the 2010 AGM as it was not presently a shareholder. Schlotzer gave evidence that he tried to tell Donaldson that Natural Springs could not recognise his sale of shares as the requirements of the Constitution had not been met. I accept Schlotzer’s version. His evidence better fitted the contemporaneous documents. They reveal to my assessment that provided that Donaldson complied with cl 51 of the Constitution, the transfers would have been registered. At the 2010 AGM, the resolutions set out at [33] above were given effect. Schlotzer prepared a contemporaneous note of what occurred at least as he saw it from his perspective. It provided:

Office Memo by Jurgen Schlotzer 21.12.2010 10.30hrs

At 9.50 Mr. Bruce Donaldson appeared at the office in 11 Saunders Street. As the AGM was scheduled to start at 10.00hrs I have offered Mr. Donaldson a seat. He declined and stated that he was here for Mr. David Graer to inform me that he has sold his shares to Hakel Investments and that he did not want to attend the AGM as he was no longer a shareholder.

He interrupted 3 attempts to explain to him that the company cannot recognise this sale/transfer of shares unless the requirements of the company's constitution are met.

He acknowledged however that I said that Hakel Investments or Its representatives are not welcome at the AGM and that I have sent them an e-mail saying so.

He got agitated and left the office at 09.55hrs claiming that he is not attending and that it is about time that they buy me out (or throw me out) – where I am not sure what he meant.

Hence the AGM has started as scheduled at 10.00hrs without Mr. Donaldson.

It needs to be noted that neither Mr. David Graer nor any other representative of Hakel Investments appeared at any time of that day either.

At the time of that incident I was still alone in the office, but Mr. Donaldson's appearance was noticed by Mr. Peter Rose.

I accept in one sense that the preparation of a note such as this may be attended with a certain degree of artificiality. But given Schlotzer’s precise personality and Donaldson’s imprecise behaviour, it is understandable that Schlotzer wanted to create a record of what had occurred. He gave evidence in accordance with this note, which I accept. Schlotzer’s evidence is also confirmed by Rose’s evidence.

49 Minutes of the AGM were also taken by Huerta which provided as follows:

Present:

Jurgen Schlotzer for Wolfgang Zink (11,960,000 shares - 30.66%)

Peter Rose for the Rose Family Trust (3,120,000 shares - 8.02%)

Jurgen Schlotzer for Prime Log Brokers (11,960,000 shares - 30.66%)

Absent:

Bruce Donaldson for the Donaldson Family Trust (11,960,000 shares - 30.66%)

(Mr Donaldson left at 09.55 hrs proclaiming that he will not attend the meeting)

Mr Jurgen Schlotzer took the chair of the meeting. He gave a brief of the company’s activities during the financial year 2009/2010.

It was voted and unanimously resolved that:

- the accounts prepared by Advance Business Centres and audited by LBW to be accepted.

- Advanced Business Centre and LBW (if needed) to be reappointed as accountant/auditor

- the directors resolution dated 25.11.2010 to be executed

…

50 On 27 December 2010, Schlotzer emailed Donaldson the minutes of the 21 December 2010 AGM.

51 On 5 January 2011, Donaldson sent a letter to the auditors in the following terms:

In your capacity as Auditors for Natural Springs Australia Ltd of 11 Saunders Street, North Geelong.

Subject: Minutes of the AGM meeting held Tuesday 21st December 2010 at 10.am - (Copy attached)

I have been sent the minutes, which in my view, have a blatant misrepresentation, which I wish to clarify.

The statement: “Mr Donaldson left at 9.55am proclaim he would not attend the meeting" does not provide an accurate account of what has transpired and hence misrepresents the facts.

I wish to state as a matter of record that:

I arrived at 9.55am that day to advise Mr Schlotzer that I had sold our shares in the company to Hakel Investments Pty Ltd and that he should therefore talk to their representative Mr David Graer. I also added that as I was no longer representing the shares I would not have voting rights, and hence had moved on.

I advised Mr Schlotzer that Mr Graer had requested I attend to provide this confirmation of sale as Mr Schlotzer had spoke to Mr Graer prior and request he not attend as the sale of these shares had not yet been advised to him formally.

Mr Schlotzer stated that he would “not entertain Mr Graer at all”.

Given the shareholding thus represented, surprising the meeting was not adjourned.

On one view, Donaldson’s reference that Schlotzer would “not entertain Mr Graer at all” is a reference simply to the fact that Graer (or Hakel Investments) was not a shareholder and so could not attend or participate in the AGM at any level. And this is the evidence Schlotzer gave, which I accept.

52 Between 10 January and 4 February 2011, emails and correspondence was sent between Donaldson, Schlotzer, Madden and LBW as follows:

(a) On 10 January 2011, Ben Kelly (Kelly) of LBW Accountants emailed Schlotzer copies of two letters from Donaldson to LBW dated 12 December 2010, as well as the incomplete share transfer forms. On the same day, Schlotzer replied stating that this was the first time he had seen the share transfer applications, and that they were invalid because they did not indicate the number of shares to be transferred. He sent 2 emails to Kelly in the following terms:

Hello Ben

[T]hanks for that. I am a bit puzzled by Mr. Donaldson’s approach. We have been contacted by e-mail by Hakel Investments on 15.12. advising us that they have purchased the shares of Mr. Donaldson and those of the Donaldson Family Trust.

I have sent this e-mail to Paul Madden for information and Paul concurred with my opinion that the share transfer has not been executed properly at that stage.

I have replied on 20.12. to Hakel investment that according to paragraph 51 of our constitution certain procedures needed to be followed before the company can/will recognize such a transfer. Nothing further was heard from Hakel Investments to date.

Until today we have not received any share transfer application from neither party other than your e-mail.

Mr. Donaldson appeared on the day of the AGM and verbally advised that he has sold his shares. He did not let me explain that he needs to submit documents to the company before such a transfer can be registered. I have explained though that the company can not entertain Hakel Investment at the AGM - as they are not a registered shareholder.

I have offered to Mr. Donaldson to attend the AGM, but he declined and left at 9.55hrs as stated in the minutes.

Attached please find my office memo about this discussion for your reference.

The remaining members did not see any necessity to adjourn the AGM neither did Mr. Donaldson request any adjournment. The AGM was held as scheduled with the majority of the members present.

The issue with the proper share description on Mr. Donaldson's family trust has not been an issue since the company has been formed. In all our previous AGM the shareholdership was described exactly the same and no objection had ever been raised by him.

The issue of a 'hostile' relationship is only Mr. Donaldson's opinion and I believe it originated when the majority of the members requested his resignation as director and asked him to leave the company in April 2006.

Please also note that Natural Springs Australia Ltd does not wish to entertain such a mediator role of LBW on our account. If Mr. Donaldson is asking for your intervention kindly act on his behalf and charge him accordingly.

Hello Ben

I also just noticed that the transfer documents you have attached do not indicate any number of shares transferred. As such, the document is not complete and has to be considered invalid.

To me this transfer form might represent an intention to sell the shares - but the sale has not been taken place, yet.

(b) On 21 January 2011, Schlotzer sent letters to Donaldson by registered mail stating that the share transfer forms he provided did not comply with the requirements of the Constitution and advising him that Natural Springs was issuing new shares and that he was invited to purchase them. The relevant letter dealing with the share transfers did not contain any refusal to accept Hakel Investments as a shareholder. One letter enclosed extracts of the Constitution being cll 51, 52 and 53. The two letters were in the following terms:

Dear Bruce,

[A]s advised in the Director's Resolution dd 25.11.2010 and discussed during the AGM 21.12.2010 the company will issue 10,000,000 additional unrestricted shares. The Directors have set the purchase price of $ 10,000.00 for these shares.

Article 31 of our constitution requires these shares to be offered to members first.

We herewith offer you the above shares for the sum of $ 10,000.00 in cash to be paid into the company's bank account.

Please state in writing to the company until 14. February 2011 whether you intend to buy these shares. Should you prefer not to reply, we herewith inform you that a non reply will be considered a 'no intention to buy' and the directors will proceed with the sale of these shares as they see fit.

For any further information please do not hesitate to contact me.

Dear Bruce,

[R]eference is made to your information sent to LBW, e-mail exchange with you and Hakel Investments Pty Ltd as well as conversation with you on 21.12.2010 at our office concerning a transfer of your shares.

Attached please find an extract of our constitution for your reference. I kindly ask you to follow these requirements.

Until these requirements are met, the share transfer be approved by the Directors, the transfer be registered with the company secretary and ASIC been notified - you are still considered being the sole owner of these shares.

Therefore you are kindly requested to continue to act as a member of the company until the share transfer has been completed.

(c) On 24 January 2011, Donaldson sent Schlotzer an email acknowledging receipt of his letters dated 21 January 2011 and requesting a copy of Natural Springs’ Constitution, which Schlotzer provided by reply email. Donaldson expressed himself in terms of “Hi Jurgen” and “Cheers Bruce”. Clearly such language does not suggest major antipathy.

(d) On 4 February 2011, Donaldson sent Schlotzer a letter stating that Donaldson had no intention of buying any new shares and foreshadowing an action under s 232 of the Act. The reference to oppression had no substance. Moreover, it was a non-response in relation to what Schlotzer had advised him concerning non-compliance by Donaldson with relevant provisions of the Constitution dealing with the share transfers. The letter was in the following terms:

Thank you for your letter dated 21st January 2011.

I have no intention of buying shares at this stage.

Further, I have no clear value or valuation of this business and have no understanding of the raising capital requirements that you are writing about.

My colleague wants my shares and you have refused to acknowledge same. Therefore we can only take action under the provisions of the Corporations Act 2001 Section 232 and following, not withstanding action as a minority shareholder.

Further you have offered a sales price for my shares that was insulting, however, now set the basis of value of the business.

We shall commence proceedings against the directors and the company forthwith.

(e) Further, on 4 February 2011, Donaldson also emailed Schlotzer to arrange a time to deliver the share transfer forms in person to Huerta or Schlotzer. Schlotzer replied on the same day and a meeting time the following day was organised. This hardly establishes procrastination on the part of Schlotzer. It demonstrates cooperation on the part of Schlotzer. The email chain was in the following terms:

Hello Jurgen

I dropped by your office today but you were not in.

Can you please advise me a date, time and place that I can deliver the share transfer forms to Angela in her capacity as Company Secretary, or to you if she is not available.

Bruce

Hello Bruce,

You must have missed me by a couple of minutes only.

How about tomorrow, Saturday 5.2 at 10am at Saunders Street?

Please advise.

Jurgen

Yes that will be fine, see you then

Bruce

53 Donaldson collected the original share transfer forms (still incomplete) from Kelly of LBW Accountants. On 5 February 2011, Donaldson met with Schlotzer at the Natural Springs’ offices and hand delivered the share transfer forms (still incomplete) to him. Again, no share certificates were delivered with these incomplete forms. Schlotzer stamped a date of receipt on the accompanying letter and transfer forms.

54 Schlotzer subsequently showed the share transfer forms to Rose. They agreed that they were incomplete, although it is apparent that Rose was following Schlotzer’s advice. Donaldson alleged that at this time Schlotzer and Rose refused to give effect to the transfer of Donaldson’s shares to Hakel Investments by refusing to enter Hakel Investments’ name on Natural Spring’s register of members in the place of Donaldson, present the share transfer forms to the other directors, secretary or office of Natural Springs or do any other thing for the purpose of giving effect to the transfer. I will deal with this assertion later.

55 Donaldson also alleged that Zink was also responsible for this refusal, despite being absent from Australia. It was said that Schlotzer and Rose carried out such tasks on behalf of Zink in his absence and were exercising Zink’s delegated powers at the time of the refusal. Donaldson also alleged that Prime Log was responsible for the refusal as Schlotzer was acting as an authorised agent of Prime Log at the time of the refusal. Donaldson alleged that by reason of the participation of Schlotzer, Rose and Zink in the refusal, Natural Springs also was responsible for the decision and the failure to register (see at [33] to [36] of the second amended statement of claim). I will deal in more detail with these allegations later.

56 On 16 February 2011, Schlotzer sent an email to Madden in the following terms:

Hi Paul,

[A]ttached letter from Bruce turning down the offer to purchase additional shares. Hence I think the path is clear to issue additional shares so we can raise the money needed to pay our bills.

Can you please send the necessary form to ASIC for the issuing of 10,000,000 new shares in consideration of $ 10,000.00 paid by Prime Log.

The Original of Bruce' [sic] letter received by registered mail last week.

He also dropped off the share transfer form 2 weeks ago. I am having a problem accepting those as there is no number of shares mentioned. I am tempted to turn the application down.

Bruce does not seem willing to speak to me. However, may be we can convince him to have a joint discussion together with you and me.

I know I can drag this matter for an almost indefinite time, but I would like to close the company down asap.

Please advise. If you agree, then please send Bruce an invitation for a meeting in your office with or without me.

Please advise.

In relation to the reference “drag this matter”, there is some indication here that Schlotzer had an appreciation that he could have dragged the matter out. But the fact is, first, he indicated to Madden that he did not want to and, second, he did not so drag it out. Schlotzer gave evidence that he was trying to speed the process up by getting Madden to speak with Donaldson.

57 On 21 February 2011, Schlotzer emailed Donaldson stating that the transfers still could not be completed as the relevant requirements had not been met insofar as the documents did not stipulate the number of shares being transferred, nor were they dated and Donaldson had not surrendered his share certificates. Schlotzer also sought a declaration of intention from Hakel Investments given that Natural Springs had ceased trading. The full text of the email is as follows:

Hello Bruce,

[T]hanks for your letter 4.2. advising that you do not wish to buy the shares offered. The shares have been taken up by another shareholder now.

As for paragraph 2 of your letter we advise that the complete financial set has been submitted to you together with the invitation to the AGM. This set of documentation has given you a very exact understanding of the value of the shares. The directors resolution (dd 25.11.2010) that was sent to you with the same invitation explained why additional capital is required. It also stated that the company is in the process of closing down and the actions the directors have put in motion.

Contrary to your statement in paragraph 3 of your letter we have never refused any transfer of shares, but objected the method of notification you have chosen.

Our company constitution has set out very simple transfer procedures, which you fail to follow. You mention in the same para that Hakel Investments is your ‘colleague’? Please elaborate so we can understand the relationship between you and Hakel Investments.

Also following your paragraph 4 – can you please advise at what date we have offered an ‘insulting’ price for your shares? As far as I remember, our last offer was 4 years ago and was reasonably reflecting the value of the company.

We also acknowledge the receipt of share transfer documents you have dropped off at the office on 5.2.2011

We have studied the same and need to inform you that the company can still not proceed with a share transfer because:

- the share transfer form does not stipulate the number of shares transferred

- the share transfer form is not dated

- the share certificates have not been surrendered (as required by our constitution)

Furthermore the directors seek a declaration of the intention of Hakel Investment as the company has ceased operation on 27.11.2010.

A sale of your shares to Hakel Investments on 12.12.2010 (2 weeks after the company ceased operation) bares [sic] any commercial foundation and can only be considered a ‘threat’ to the company. As such, the directors might refuse to acknowledge the transfer if no proper explanation is provided.

We have therefore requested Paul Madden of ABC Accountants to contact you so you may seek independent advice.

58 Schlotzer gave evidence that when he made the request seeking a declaration of intention, he and some of the directors (not Rose apparently) felt threatened. They could not understand its commercial foundation, given that Natural Springs had negative net tangible assets and it had, effectively, ceased substantive operations. They wanted to understand what Graer or Hakel Investments intended. In my view, Schlotzer and the directors were entitled to request that information. However, they were not entitled to refuse to register the transfers if such information was not forthcoming. It made good commercial sense for management to request what an incoming shareholder was intending. The request was not answered. In any event, the registration was not refused because of the failure to answer that query. The reference in the email to “might refuse” was just that. The email did not say that the directors would refuse to register Hakel Investments because they were unsure of its intentions or that Hakel Investments was somehow undesirable. Rather, the actual refusal was due to the other three deficiencies mentioned.

59 Nothing further was then heard from Donaldson on the share transfer question until April 2011. On 5 April 2011, Graer called Donaldson to inform him that he did not want to go ahead with the share purchase. Donaldson alleged that this was due to the refusal of Natural Springs to register the transfers to Hakel Investments. Donaldson subsequently emailed Schlotzer stating:

I am informed by Hakel Investments that they have not received the transfer of shares that we had instigated in December 2010.

As such they have withdrawn their purchase agreement with me based on your failure to accept the terms of the sale.

Please therefore return these original documents to me…

60 On the same day, Schlotzer replied to Donaldson stating that Natural Springs was prepared to register the transfer of shares to Hakel Investments as soon as the necessary requirements had been fulfilled. Schlotzer wrote as follows:

[R]eference is made to my mail to you 21.02 in which I have outlined why the shares where not transferred and what you have to do to have them transferred. [sic] Apart from having had the proposed meeting with Paul Madden I have not heard from you nor have you complied with any of the requirements outlined in that mail. Hence, the share transfer did not proceed any further so far.

This hold up has absolutely nothing to do with the company’s failure to accept the terms of sale and your allegation is denied. The company is still prepared to transfer those shares as soon as the necessary requirements are fulfilled…

Donaldson alleged that by this time, however, Hakel Investments did not wish to proceed with the share purchase.

61 On 4 May 2011, a Natural Springs’ board meeting was held and Natural Springs was converted to a proprietary limited company. An amendment to Natural Springs’ name, as named in the originating application, has not been sought by Donaldson. However, I accept that Natural Springs has been a proprietary limited company from 4 May 2011.

62 On 19 May 2011, Prime Log acquired 10 million extra shares in Natural Springs issued pursuant to the directors’ resolution of 25 November 2010. The shares were issued to raise additional capital, being $10,000, to pay for Natural Springs’ outstanding tax liabilities, accounting and auditing fees (see the explanation for the need for this amount in the minutes set out at [32]).

63 Pursuant to a notice to admit, the defendants have admitted that Natural Springs (at the time of trial) had no assets and that Donaldson's shares were presently of nominal value only.

The trial

64 The allegations originally pleaded by Donaldson were wide-ranging and included claims relating to his alleged forced resignation as a director, the refusal by Natural Springs to purchase his shares, the dilution of his shareholding, failure to give proper notice of shareholder resolutions and misleading or deceptive conduct by Schlotzer and Prime Log.

65 Subsequently, the allegations were narrowed. A second amended statement of claim was filed on 26 June 2014. The key oppression allegation persisted with was the failure of Natural Springs to permit or effect the transfer of Donaldson’s shares to Hakel Investments (at [20] to [37] and [40]) causing him a loss of $300,000. Donaldson also claimed that the refusal to register the transfer of shares was a breach of cl 53 of Natural Springs’ Constitution, which provided that the directors were not permitted to refuse to register a share transfer except as permitted by law (at [38] to [39], [41] and [61] to [63]). Donaldson further pleaded that as the Constitution operated as a contract, cll 51 and 53 of the Constitution or its implied terms required Natural Springs upon production of the share transfer forms to give effect to the transfer and this requirement was breached (at [43] to [55]). Donaldson further pleaded tort claims against Schlotzer, Zink, Rose and Prime Log, being that they intentionally interfered, both directly and indirectly, with contractual relations under the Constitution and between himself and Hakel Investments (at [56] to [60]) including, in relation to the indirect interference claim, the use of unlawful means being their breaches of duties of care and good faith and the like (ss 180, 181, 182 of the Act) (at [64] to [68]).

66 The defendants denied that they obstructed the transfer of shares to Hakel Investments or that their conduct was oppressive. They pleaded that the share transfer forms provided by Donaldson did not comply with the Constitution as no date was recorded for the transfer, nor the number of shares to be transferred, and nor the consideration provided. Further, Donaldson had not surrendered his share certificates. Accordingly, they submitted that no obligation was triggered under the Constitution requiring registration.

67 Donaldson admitted that the share transfer forms did not specify on their face the quantity of shares to be transferred or the date of transfer, but said that the defendants knew that he had sold and intended to transfer to Hakel Investments the entirety of his shares (11.96 million), alternatively that this information was available to Natural Springs or could have been calculated by Natural Springs. Further, it was asserted that Natural Springs could have inserted the missing information into the forms. Donaldson also alleged that his share certificates had always been in the possession of Natural Springs and remained on their premises. Donaldson further conceded in evidence that he and Graer omitted the consideration from the transfer forms as they considered such information commercially sensitive and wanted to keep it confidential, particularly from the directors and shareholders of Natural Springs.

68 The trial was heard on 9, 10, 11 and 16 December 2014.

69 Donaldson relied upon his affidavits affirmed on 29 January and 21 February 2013, 11 March (incorrectly dated on first page as 6 March) and 4 September 2014, three affidavits of Graer, an affidavit of Young and affidavits of his sons, David Nicholas Donaldson and Christopher Jeremy Donaldson.

70 The defendants relied on two affidavits of Schlotzer sworn on 6 February and 6 June 2013 and an affidavit of Rose sworn on 6 February 2013.

71 Donaldson, Graer, Schlotzer, Rose and Young were cross-examined at trial.

72 During the cross-examination of Graer on 10 December, it became apparent that there was no probative evidence showing that at the relevant time Hakel Investments had the funds to pay the agreed $300,000 purchase price for Donaldson’s shares. Graer deposed that there were bank statements for a third bank account, the detail of which he conceded was “missing” from his affidavit sworn on 3 March 2014, which he asserted evidenced the ability of Hakel Investments to complete that transaction. Counsel for the defendants called for those bank statements.

73 On 11 December 2014, further bank statements for Hakel Investments were produced, along with bank statements and corporate information for a different company, Brahman Pastoral Pty Ltd. To formalise the admission of this material, which Donaldson’s counsel sought to tender on the call, I directed that Donaldson should file and serve a further affidavit of Graer on the question of Hakel Investments’ means or availability of funds. I adjourned the hearing until 16 December 2014 to allow this to occur.

74 Subsequently, Donaldson filed a third affidavit of Graer, who deposed that his affidavit sworn on 3 March 2014 was inaccurate with respect to Hakel Investments’ ability to finance the purchase directly, and that Mr Kim Jennings of Brahman Pastoral Pty Ltd was an investor willing, through that entity, to provide $300,000 for the purchase of Donaldson’s shares on the advice of Graer. Jennings was never called.

75 On 16 December 2014, the hearing resumed and I accepted the further Graer affidavit into evidence over the defendants’ objection. But some of Graer’s evidence was ruled inadmissible as to form or as being hearsay. No further cross-examination of Graer took place. On that day, Young was cross-examined.

76 I will elaborate on key factual issues shortly. But I must say that I found the evidence concerning Hakel Investments’ asserted capacity to pay the relevant $300,000 and to meet its obligations under any agreement with Donaldson quite unsatisfactory. Despite initial assertion, the evidence evolved in a way which demonstrated that Hakel Investments itself did not have its own resources to meet its purchase obligations under any such agreement. The suggestion that some other person could have been called upon by Graer to put up the funds remained shadowy. Graer’s change of position in terms of Hakel Investments’ resources gave me little confidence in his unsatisfactory evidence on that question, and, as a consequence, more generally on the detail of what he asserted to be the agreement with Donaldson on the share purchase. I will deal with Graer and his evidence later.

77 It is appropriate to focus more closely on the share transfer registration question and Donaldson’s attempts on that aspect and Natural Springs’ and Schlotzer’s response. If the share transfers were deficient and the correct documents were not provided, and otherwise the defendants’ conduct was in accordance with the Constitution, then the key factual foundation for all of Donaldson’s asserted causes of action fails. Of course, causes of action such as the s 232 claim can be viewed more broadly in theory. But the only key event in context put forward by Donaldson (and pleaded as such in [40] and [41] of the second further amended statement of claim) to justify the proposition that there had been “oppressive”, “unfairly prejudicial” or “unfairly discriminatory” against Donaldson within the meaning of s 232(e) of the Act was the circumstances surrounding Natural Springs’ and Schlotzer’s dealings with the share transfers. I do accept, however, that although the oppression case focused around this event rather than a pattern of behaviour over time, nevertheless the powers in s 233 can be triggered by a single act or omission (see s 232(b)).

78 But even if Donaldson’s factual foundation was made good, the question is whether any loss was sustained. In my view, Donaldson suffered no substantive loss. The evidence of Graer and Hakel Investments concerning the agreement, its conditions and Hakel Investments’ ability (or otherwise) to meet its obligations thereunder will be assessed later. But I am not satisfied that the agreement became unconditional and, further, that Hakel Investments could meet its obligations thereunder in any event. In my view, no valuable opportunity was lost. Further, there was no probative evidence adduced, independently of this so called Hakel Investments opportunity, to the effect that these shares had any value at the end of 2010; indeed quite the converse.

Share transfers – key events

79 The key sequence of events relevant to the share transfers that can be distilled from the earlier chronology is the following.

80 On or about 12 December 2010, Donaldson and Graer signed two share transfer forms, which were subsequently sent by post to Natural Springs auditors, LBW Accountants; to be clear, Natural Springs’ registered address and place of business were different; further, Natural Springs had different accountants acting for it (Madden of ABC accountants). Nothing was sent to Natural Springs as such. Copies of these share transfer forms were not received by Natural Springs until 10 January 2011. The originals were not received until 5 February 2011.

81 On 15 December 2010, Donaldson sent an email to Schlotzer:

Please note that I have sold the shares in Natural Springs Australia Ltd held by the Donaldson Family Trust and myself to Hakel Investments Pty Ltd as such I will not be attending the AGM

82 This was the first time that Natural Springs received any notice of the proposed transfer of shares from Donaldson to Hakel Investments. There was no reference to any share transfer forms. This email did not constitute any formal notification which might trigger Natural Springs or its directors to take any steps to facilitate the transfer of shares.

83 On that same day, Graer sent an email to Schlotzer stating that:

Hakel Investments pty ltd has purchased the shares held by The Donaldson Family Trust and Bruce Donaldson in his own right.

84 Schlotzer replied to Graer's email on 20 December 2010:

Following paragraph 51 of the constitution of Natural Springs Australia Ltd certain procedures for a transfer of shares will need to be followed. The company has not been notified and provided with any documentation to date. Accordingly the company records do not reflect any changes in shareholders.

As such the company does not recognize Hakel Investments or its representatives as a member and an invitation to the forthcoming Annual General Meeting is not issued.

85 On 21 December 2010, Donaldson attended the office of Natural Springs, and had a conversation with Schlotzer. But Donaldson did not produce any documentation in relation to the proposed transfer of shares from Donaldson to Hakel Investments. Donaldson's evidence is that during that conversation Schlotzer said that he would not entertain Graer as a shareholder at all, and that he would not transfer the shares. Schlotzer's evidence is that he said he would not entertain Graer attending the meeting as he was not a shareholder at that stage. In my view, Schlotzer's evidence on this issue should be preferred as it is consistent with all prior and subsequent written communications (see an elaboration earlier at [48]). It was not disputed that Donaldson left the office before the commencement of the AGM, notwithstanding that he was specifically invited to remain in attendance.

86 On 10 January 2011, Kelly of LBW Accountants sent an email to Schlotzer and forwarded electronic copies of the share transfer forms. This is the first time that a copy of any written transfer document came into the possession of Natural Springs; in any event they were only copies. One of the share transfer forms listed “Gordon Bruce Donaldson” as the transferor. The other form listed “Gordon Bruce Donaldson IFP The Donaldson Family Trust” as the transferor. The documents were incomplete insofar as they did not specify the number of shares to be transferred, the consideration to be paid and they were not dated. The original share transfer forms were sent under cover of a letter dated 12 December 2010 written by Donaldson which I have set out earlier at [42]. Donaldson's covering letter was ambiguous and confusing. It did not provide any clarity to the question of how many shares were to be transferred pursuant to either of the signed share transfer forms.

87 On 21 January 2011, Schlotzer sent a letter to Donaldson, which I have referred to earlier, stating:

Attached please find an extract of our constitution for your reference. I kindly ask you to follow these requirements.

Until these requirements are met, the share transfer be approved by the Directors, the transfer be registered with the company secretary and ASIC been notified - you are still considered being the sole owner of these shares.

Therefore you are kindly requested to continue to act as a member of the company until the share transfer has been completed.

[emphasis added]

88 Schlotzer's letter did not contain any refusal to register the transfer of shares from Donaldson to Hakel Investments. The letter simply identified the need to comply with the requirements set out in the Constitution. The letter and the request were unremarkable.

89 On 24 January 2011, Donaldson sent an email to Schlotzer, asking for a copy of the Constitution. Donaldson did not otherwise respond to any of the matters raised by Schlotzer in his email of 21 January 2011. Schlotzer provided a copy of the Constitution as requested. Schlotzer’s conduct was quite appropriate and did not manifest any strategy on his part to prevent the transfer.

90 On 4 February 2011, Donaldson sent a letter in reply to Schlotzer which I have set out at [52(d)]. This letter illustrated Donaldson's failure to engage in any meaningful discussion with Natural Springs to progress the proposed transfer of his shares. He said nothing in relation to the requirements set out in the Constitution, nor did he propose what steps he thought that Natural Springs ought take in relation to the share transfer forms to deal with his own omissions (which were still with LBW Accountants at this time).

91 Donaldson retrieved the original signed share transfer forms from LBW Accountants. On 5 February 2011, Donaldson attended the offices of Natural Springs and delivered those original documents to Schlotzer. This is the first time that the original written transfer documents came into the possession of Natural Springs. Significantly, Donaldson did not take this opportunity to specify the number of shares to be transferred or date the transfer forms. No share certificates were delivered.

92 Schlotzer gave evidence that in the absence of any express instructions from Donaldson and/or Graer, he did not consider himself authorised to make any additions or alterations to the original share transfer forms. Schlotzer's view in this regard was completely reasonable and proper in the circumstances. Donaldson's failure to engage in any meaningful dialogue with Schlotzer thus resulted in an impasse with regard to the share transfer forms. This is apparent from the email Schlotzer sent to Madden on 16 February 2011 (see at [56] above).

93 There is no basis for Donaldson to assert that Natural Springs or its directors somehow assumed a duty to initiate a solution to the apparent deficiencies associated with the share transfer forms, beyond the information that they had already provided to Donaldson. Donaldson was repeatedly provided with the relevant information and Natural Springs’ preliminary views about the status of the purported transfers. Yet he did nothing to address the deficiencies.