FEDERAL COURT OF AUSTRALIA

Tax Practitioners Board v HP Kolya Pty Ltd [2015] FCA 472

IN THE FEDERAL COURT OF AUSTRALIA | |

Applicant | |

AND: | HP KOLYA PTY LTD (ACN 150 479 315) First Respondent PETER KOLYA Second Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT DECLARES THAT:

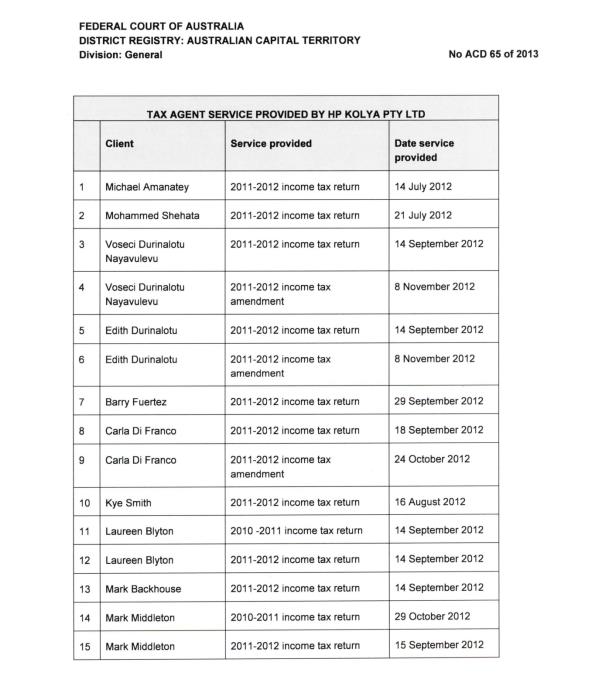

1. On the thirty-one (31) occasions more particularly described in Annexure A to these Orders, between 29 August 2011 and 8 November 2012, the first respondent, HP Kolya Pty Ltd (HP Kolya) supplied and charged for a tax agent service, namely the preparation and lodgment of an income tax return or amendment to an income tax return, in each case in contravention of subs 50-5(1) of the Tax Agent Services Act 2009 (Cth) (the Act).

2. On 23 August 2013, HP Kolya supplied and charged for a tax agent service, namely the preparation of an income tax return for Alecia Buckthorpe:

(a) In contravention of subs 50-5(1) of the Act; and

(b) Contrary to Order 1 of the orders made by the Federal Court of Australia on 26 July 2013 (the Interim Injunctions).

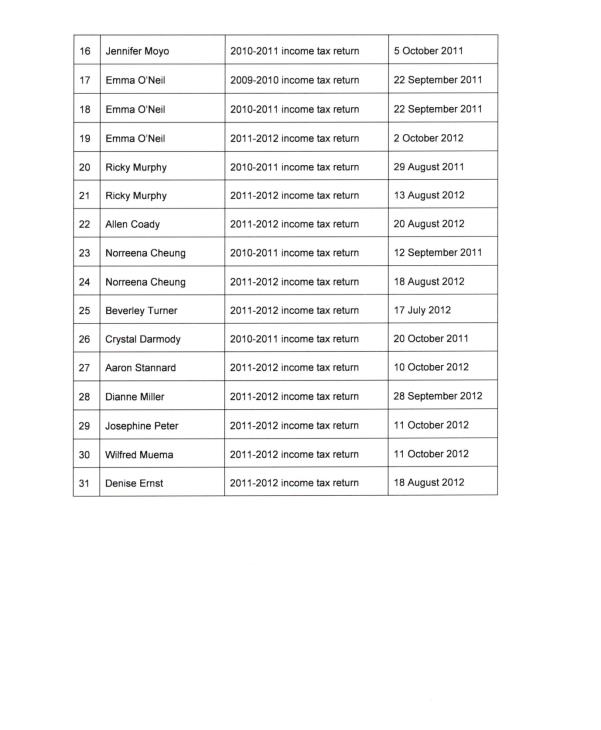

3. On the seven (7) occasions more particularly described in Annexure B to these Orders, between 23 August 2012 and 24 October 2012, the second respondent, Peter Kolya (Mr Kolya), supplied and charged for a tax agent service, namely the preparation and lodgment of an income tax return, in contravention of subs 50-5(1) of the Act.

4. On or about 23 August 2013, Mr Kolya performed a tax agent service on behalf of HP Kolya, namely the preparation of an income tax return for Alecia Buckthorpe, contrary to Order 2 of the Interim Injunctions.

5. On or about 8 August 2012, HP Kolya supplied and charged for a BAS service, namely the preparation of a business activity statement for Premier Housing Projects Pty Limited, in contravention of subs 50-5(2) of the Act.

6. On or about 24 October 2012, Mr Kolya supplied and charged for a BAS service, namely the preparation of a business activity statement for Premier Housing Projects Pty Limited, in contravention of subs 50-5(2) of the Act.

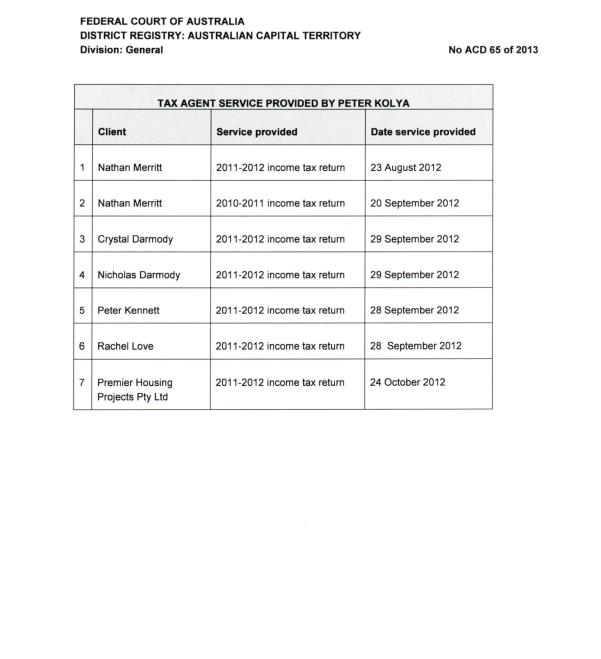

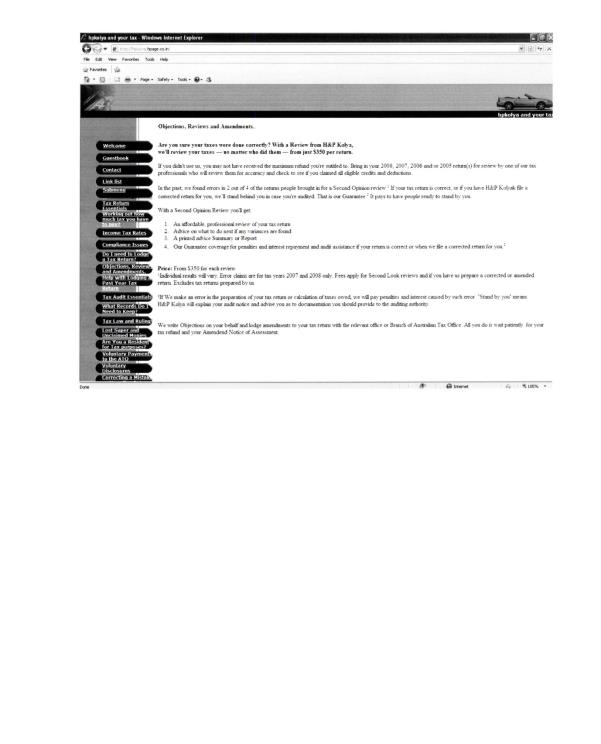

7. By placing and maintaining a listing for HP Kolya in the online version of the White Pages with a link to the webpage hpkolya.hpage.co.in (a copy of which is included at Annexure C to these Orders), HP Kolya advertised a tax agent service while unregistered in contravention of subs 50-10(1) of the Act.

8. By maintaining the webpage “hpkolya.hpage.co.in” after 26 July 2013, HP Kolya offered to perform tax agent services contrary to Order 1 of the Interim Injunctions.

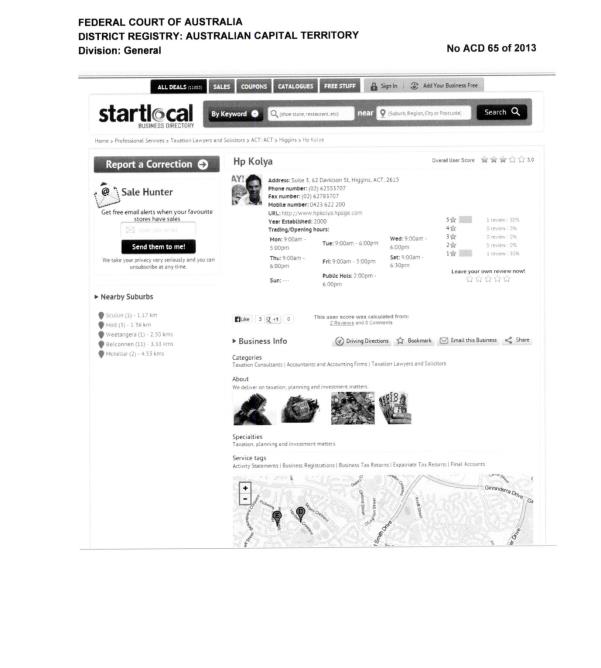

9. By placing a listing for HP Kolya in the online Start Local business directory on 10 February 2010 and by maintaining that listing (a copy of which is included at Annexure D to these Orders), Mr Kolya advertised a tax agent service while unregistered in contravention of subs 50-10(1) of the Act.

10. By maintaining the listing for HP Kolya in the online Start Local business directory after 26 July 2013, Mr Kolya offered to perform tax agent services contrary to Order 2 of the Interim Injunctions.

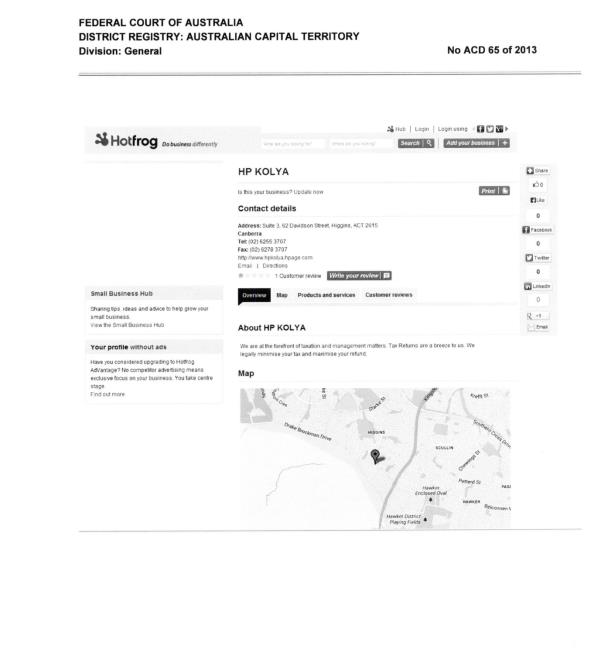

11. By placing a listing for HP Kolya in the online Hotfrog business directory on 14 June 2009 and maintaining that listing (a copy of which is included at Annexure E to these Orders), Mr Kolya advertised a tax agent service while unregistered in contravention of subs 50-10(1) of the Act.

12. By maintaining the listing for HP Kolya in the online Hotfrog business directory after 26 July 2013, Mr Kolya offered to perform tax agent services contrary to Order 2 of the Interim Injunctions.

THE COURT ORDERS THAT:

13. Pursuant to subs 70-5 of the Act, HP Kolya is restrained from providing or offering to provide any tax agent services (as defined in the Act) and any BAS service (as defined in the Act) for a period of ten (10) years unless:

(a) HP Kolya is at the time of providing or offering to provide the tax agent service, a registered tax agent or, at the time of providing or offering to provide the BAS service, a registered tax agent or BAS agent; or

(b) The tax agent service or BAS service is provided free of charge, fee or reward.

14. Pursuant to subs 70-5 of the Act, Mr Kolya is restrained from providing or offering to provide any tax agent service (as defined in the Act) and any BAS service (as defined in the Act) for a period of ten (10) years unless:

(a) Mr Kolya is at the time of providing or offering to provide the tax agent service, a registered tax agent or, at the time of providing or offering to provide the BAS service, a registered tax agent or BAS agent; or

(b) The tax agent service or BAS service is provided free of charge, fee or reward.

15. Pursuant to subs 70-5 of the Act, HP Kolya is restrained for a period of ten (10) years from advertising in any form or by any medium that it will or might provide, or a person associated with it (including Mr Kolya) will or might provide, a tax agent service (as defined in the Act) or a BAS service (as defined in the Act) unless the conditions outlined above at paragraph 13, as they apply to any such advertisement, are satisfied.

16. Pursuant to subs 70-5 of the Act, Mr Kolya is restrained for a period of ten (10) years from advertising in any form or by any medium that he will or might provide, or a person associated with him (including HP Kolya) will or might provide, a tax agent service (as defined in the Act) or a BAS Service (as defined in the Act) unless the conditions outlined above at paragraph 14, as they apply to any such advertisement, are satisfied.

17. Pursuant to subs 50-35 of the Act, HP Kolya pay pecuniary penalties to the Commonwealth totalling $750,000 for the contraventions described in paragraphs 1, 2, 5 and 7 above.

18. Pursuant to subs 50-35 of the Act, Mr Kolya pay pecuniary penalties to the Commonwealth totalling $150,000 for the contraventions described in paragraphs 3, 6, 9 and 11 above.

19. The respondents pay the applicant’s costs of and incidental to this proceeding.

THE COURT NOTES THAT:

20. The applicant will not bring proceedings for contempt against HP Kolya or against Mr Kolya for any of the breaches of the Interim Injunctions described in declarations 2, 4, 8, 10 and 12 above.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

ANNEXURE B

ANNEXURE C

ANNEXURE D

ANNEXURE E

AUSTRALIAN CAPITAL TERRITORY DISTRICT REGISTRY | |

GENERAL DIVISION | ACD 65 of 2013 |

BETWEEN: | TAX PRACTITIONERS BOARD Applicant |

AND: | HP KOLYA PTY LTD (ACN 150 479 315) First Respondent PETER KOLYA Second Respondent |

JUDGE: | FOSTER J |

DATE: | 14 MAY 2015 |

PLACE: | SYDNEY (HEARD IN CANBERRA) |

REASONS FOR JUDGMENT

1 By the Tax Agent Services Act 2009 (Cth) (TAS Act), the Tax Practitioners Board (Board) is (inter alia) charged with the responsibility of regulating the activities of tax agents and BAS agents and of enforcing the provisions of the TAS Act in respect of such agents.

2 In the present proceeding, the Board seeks civil penalties against both respondents. It also seeks declaratory and injunctive relief. The second respondent (Mr Kolya) is the sole director of and one of only two shareholders in the first respondent (HP Kolya). Mr Kolya controls HP Kolya.

3 The Board contends that, in the period from late August 2011 to late August 2013, the respondents systematically supplied tax agent services to members of the public in contravention of subs 50-5(1) of the TAS Act. The Board contends that neither respondent was permitted to supply such services in that period because neither respondent was a registered tax agent at any time in that period. Neither respondent was a registered tax agent or a BAS agent at any time in that period. There is no dispute about these facts in the present proceeding. However, from March 2010 until March 2012, Mr Kolya was entitled to provide BAS services under statutory transitional arrangements which allowed him to do so and as a result of a temporary stay first granted by the Administrative Appeals Tribunal (AAT) and continued by the Court.

4 In addition, the Board contends that, on or about 8 August 2012, HP Kolya supplied a BAS service to a member of the public in contravention of subs 50-5(2) of the TAS Act and that, on or about 24 October 2012, Mr Kolya supplied a BAS service in contravention of subs 50-5(2) of the TAS Act. Again, in respect of these two contraventions, it is the Board’s case that neither respondent was permitted to provide a BAS service on the occasions referred to because neither was a registered tax agent or a BAS agent at the time the services were provided.

5 The Board also contends that, in June 2009 and again in February 2010, Mr Kolya advertised a tax agent service while unregistered in contravention of subs 50-10(10) of the TAS Act.

6 At the commencement of the hearing before me, the Board abandoned an additional case based upon contraventions of subs 50-15 of the TAS Act and also did not press certain claims for injunctive relief. It had become unnecessary for the Board to press these latter claims in light of the terms of certain interlocutory injunctions granted by me on 26 July 2013. I granted those injunctions on that occasion in the absence of Mr Kolya who was well aware of the listing of the Board’s application on 26 July 2013 although he chose not to appear. He was informed of the precise terms of those injunctions soon after 26 July 2013.

7 By its Amended Statement of Claim filed in Court on 17 March 2014 (ASC), the Board pleaded in considerable detail the facts, matters and circumstances relied upon by it in support of its case. With the exception of the matters pleaded in subpars 427.1–427.14 and an argument based upon subs 50-5(1)(e) of the TAS Act and its equivalents, the respondents admitted the essential matters pleaded by the Board in the ASC as the foundation for its case.

8 Paragraphs 427.1–427.14 contain allegations made against both respondents in respect of a former client named Alecia Buckthorpe. These paragraphs were added to the Board’s Statement of Claim at the commencement of the hearing.

9 The conduct of the respondents relied upon by the Board in respect of Ms Buckthorpe occurred on and shortly after 23 August 2013. 23 August 2013 was about one month after I had granted interlocutory relief against both respondents. The Board argues that, in providing tax agent services to Ms Buckthorpe, not only did the respondents contravene the TAS Act, but they also breached the interlocutory injunctions granted by me on 26 July 2013. The Board did not bring an application against the respondents for orders punishing them for contempt of Court and expressly disavowed any intention of ever doing so. The introduction of the material concerning Ms Buckthorpe was said by the Board to be for the purpose of demonstrating the respondents’ steadfast refusal to comply with the law, even when also restrained by Court-imposed injunctions.

10 The respondents denied ever having done any work for Ms Buckthorpe. This gave rise to a dispute in relation to the Board’s allegations concerning her. I shall return to those allegations later in these Reasons.

11 Apart from circumstances relied upon by the Board in respect of Ms Buckthorpe, the only substantive defence raised by the respondents to the case brought by the Board is found at pars 134 and 135 of the Defence filed by them on 20 September 2013. With the exception of several allegations in pars 17–21 of the ASC, all other allegations pleaded in the ASC were admitted. In pars 134 and 135 of their Defence, the respondents plead that:

(a) Mr Kolya holds “a permit” pursuant to s 16 and s 17 of the Legal Profession Act 2006 (ACT);

(b) Mr Kolya is registered throughout Australia as a migration agent under the Migration Act 1958 (Cth) and is also the “legal personal representative” of the taxpayers for whom he did work; and

(c) In light of the circumstances referred to in subpars (a) and (b) above, both of the respondents were permitted to provide tax agent services and BAS services to members of the public because those services were provided as a “legal service” within the meaning of subs 50-5(1)(e) of the TAS Act and its equivalents.

12 This defence requires the Court to consider four questions, namely:

(a) Whether, as a matter of fact, Mr Kolya was qualified as a legal practitioner under the Legal Profession Act 2006 (ACT);

(b) Whether, at all relevant times, Mr Kolya was a registered migration agent;

(c) Whether Mr Kolya was the “legal personal representative” of any of his clients within the meaning of subs 50-5(3) and its equivalents; and

(d) In light of the findings required to be made in respect of the questions raised in subpars (a), (b) and (c) above, whether the respondents or either of them can avail themselves of the exception to the general registration requirements specified in the TAS Act permitted by subs 50-5(1)(e) of the TAS Act and its equivalents. This question, in turn, requires the Court to interpret that subsection.

13 Notwithstanding that, in their Defence, the respondents admitted all of the important elements of the Board’s case, the respondents nonetheless adopted stances and made arguments during the run of the hearing which caused the hearing to take longer than it ought to have. In these Reasons for Judgment, I intend only to address those evidentiary matters and legal arguments which bear upon the Board’s case involving Ms Buckthorpe, the issues summarised at [11] and [12] above and the issues which are relevant to the Court’s determination of the Board’s claims for relief.

14 There was no agreement between the parties in relation to any of the claims for relief made by the Board. As has been the practice for many years in matters such as this, the Board made detailed submissions in relation to the relief claimed by it, including submissions directed to the quantum of the appropriate civil penalties sought by it.

The Regulatory Framework

15 The object of the TAS Act is expressed in subs 2-5 of that Act in the following terms:

2-5 Object

The object of this Act is to ensure that *tax agent services are provided to the public in accordance with appropriate standards of professional and ethical conduct. This is to be achieved by (among other things):

(a) establishing a national Board to register tax agents, BAS agents and tax (financial) advisers; and

(b) introducing a *Code of Professional Conduct for *registered tax agents, BAS agents and tax (financial) advisers; and

(c) providing for sanctions to discipline registered tax agents, BAS agents and tax (financial) advisers.

16 At the time of the respondents’ contraventions in the period from late August 2011 to late August 2013, subs 2-5 did not include any reference to “tax (financial) advisers”. This circumstance is of no significance in the present case.

17 Subsection 2-10 provides a general guide to each part. That section is in the following terms:

2-10 General guide to each Part

(1) You need to be registered to provide *tax agent services for a fee or to engage in other conduct connected with providing such services. Part 2 sets out the requirements for registration.

(2) Once registered, you must comply with several requirements, in particular, the *Code of Professional Conduct. The Code is set out in Part 3.

(3) Part 4 sets out the circumstances in which your registration can be terminated.

(4) Part 5 provides for civil penalties aimed at ensuring your compliance with this Act.

(5) Part 6 establishes the Tax Practitioners Board and sets out the Board’s functions and powers. The Board may investigate breaches of this Act and has certain reporting obligations.

(6) Part 7 contains miscellaneous provisions, mainly administrative and machinery provisions relating to the operation of this Act.

(7) Part 8 contains the Dictionary, which sets out a list of most of the terms that are defined in this Act. It also sets out the meanings of some important concepts and rules on how to interpret this Act.

18 Subsections 3-5 and 3-10 provide:

3-5 When defined terms are identified

(1) Many of the terms used in this Act are defined in the Dictionary, starting at section 995-1, to the Income Tax Assessment Act 1997. However, some terms used in this Act are only defined in this Act.

Note: Expressions in the Income Tax Assessment Act 1997 (other than the expression “this Act”) have the same meaning in this Act as well, see subsection 90-1(2).

(2) Most defined terms in this Act and the Income Tax Assessment Act 1997 are identified by an asterisk at the start of the term: as in “*BAS service”.

3-10 When defined terms are not identified

(1) Once a defined term has been identified by an asterisk, later occurrences of the term in the same subsection are not usually asterisked.

(2) Terms are not asterisked in the *Guides, headings or notes contained in this Act.

(3) The term “Board” is not identified with an asterisk.

(4) If a term used in the Income Tax Assessment Act 1997 is used in this Act and the term is not identified with an asterisk in that Act, the term is not identified with an asterisk in this Act.

Note: For expressions in the Income Tax Assessment Act 1997 that are not identified with an asterisk, see subsection 2-15(3) of that Act.

19 The Board was established by subs 60-5 of the TAS Act. Under Pt 6 Div 60, the Board has responsibility for registering tax agents and BAS agents, ensuring that agents maintain appropriate skills and knowledge, investigating complaints against agents and ensuring that unregistered entities do not hold themselves out to be agents.

20 Part 5 of the TAS Act provides that tax agent services and BAS services can only be provided by persons who are registered in the appropriate category. To be registered, a person must satisfy the Board that (inter alia) that person is a “fit and proper person” (see subs 20-5). Once registered, agents must comply with a Code of Professional Conduct requiring them to act honestly, independently, competently and in other appropriate ways (subs 30-10). Failure to comply with these requirements may lead to the agent’s registration being suspended or terminated (subs 30-15).

21 Prior to the introduction of the TAS Act, tax agents were regulated under a regime established by Pt VIIA of the Income Tax Assessment Act 1936 (Cth) which involved registration with State boards. That regime had originally been introduced in 1943. The TAS Act was passed by the Parliament in order to give effect to the Parliament’s view that the tax environment had changed significantly since 1943 with a much higher proportion of the population using tax agents (74% of individuals and over 95% of businesses).

22 The Commonwealth Parliament has reposed in the Board the power to seek civil penalties, declarations and injunctions from this Court. According to the relevant Explanatory Memorandum (Explanatory Memorandum to the Tax Agents Services Bill 2008, House of Representatives, at par 1.17) these powers are intended to secure compliance through deterrence and prevention. In the Explanatory Memorandum, the government emphasised the need for more significant monetary penalties to be available to the Court in order to deter tax agents and BAS agents from contravening the civil penalty provisions in the TAS Act.

23 Subsection 50-5 of the TAS Act provides:

50-5 Providing tax agent services if unregistered

(1) You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a *tax agent service; and

(b) the tax agent service is not a *BAS service or a *tax (financial) advice service; and

(c) you charge or receive a fee or other reward for providing the tax agent service; and

(d) you are not a *registered tax agent; and

(e) if you provide the tax agent service as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service consists of preparing, or lodging, a return or a statement in the nature of a return.

Civil penalty:

(a) for an individual—250 penalty units; and

(b) for a body corporate—1,250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B of Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(2) You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a *BAS service; and

(b) you charge or receive a fee or other reward for providing the BAS service; and

(c) you are not a *registered tax agent or BAS agent; and

(d) if you provide the BAS service as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that BAS service; or

(ii) subject to subsection (4), the service consists of preparing, or lodging, a return or a statement in the nature of a return; and

(e) if the BAS service relates to imports or exports to which an *indirect tax law applies—you are not a customs broker licensed under Part XI of the Customs Act 1901.

Civil penalty:

(a) for an individual—250 penalty units; and

(b) for a body corporate—1,250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B of Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(2A) You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a *tax (financial) advice service; and

(b) the tax (financial) advice service is not a *BAS service; and

(c) you charge or receive a fee or other reward for providing the tax (financial) advice service; and

(d) you are not a *registered tax agent or a *registered tax (financial) adviser; and

(e) in the case of you providing the tax (financial) advice service as a legal service—you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax (financial) advice service.

Civil penalty:

(a) for an individual—250 penalty units; and

(b) for a body corporate—1,250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B in Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(3) Subparagraph (1)(e)(ii) does not apply if you provide the *tax agent service as a legal service in the course of acting for a trust or deceased estate as trustee or *legal personal representative.

(4) Subparagraph (2)(d)(ii) does not apply if you provide the *BAS service as a legal service in the course of acting for a trust or deceased estate as trustee or *legal personal representative.

(5) If you wish to rely on subsection (3) or (4) in civil penalty proceedings, you bear an *evidential burden in relation to that matter.

24 Subsection 50-10 is in the following terms:

50-10 Advertising tax agent services if unregistered

(1) You contravene this subsection if:

(a) you advertise that you will provide a *tax agent service; and

(b) the tax agent service is not a *BAS service or a *tax (financial) advice service; and

(c) you are not a *registered tax agent; and

(d) if the tax agent service would be provided as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service would consist of preparing, or lodging, a return or a statement in the nature of a return; and

(e) if the tax agent service would be provided on a voluntary basis—you would not provide the service under a scheme approved by the Commissioner by notice published in the Gazette.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B of Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(2) You contravene this subsection if:

(a) you advertise that you will provide a *BAS service; and

(b) you are not a *registered tax agent or BAS agent; and

(c) if the BAS service would be provided as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that BAS service; or

(ii) subject to subsection (4), the service would consist of preparing, or lodging, a return or a statement in the nature of a return; and

(d) if the BAS service relates to imports or exports to which an *indirect tax law applies—you are not a customs broker licensed under Part XI of the Customs Act 1901; and

(e) if the BAS service would be provided on a voluntary basis—you would not provide the service under a scheme approved by the Commissioner by notice published in the Gazette.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B of Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(2A) You contravene this subsection if:

(a) you advertise that you will provide a *tax (financial) advice service; and

(b) the tax (financial) advice service is not a *BAS service; and

(c) you are not a *registered tax agent or a *registered tax (financial) adviser; and

(d) where the tax (financial) advice service would be provided as a legal service—you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax (financial) advice service.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

Note: Subdivision 50–C of this Act and Subdivision 298–B in Schedule 1 to the Taxation Administration Act 1953 determine the procedure for obtaining a civil penalty order against you.

(3) Subparagraph (1)(d)(ii) does not apply if you would provide the *tax agent service as a legal service in the course of acting for a trust or deceased estate as trustee or *legal personal representative.

(4) Subparagraph (2)(c)(ii) does not apply if you would provide the *BAS service as a legal service in the course of acting for a trust or deceased estate as trustee or *legal personal representative.

(4A) If you wish to rely on subsection (3) or (4) in civil penalty proceedings, you bear an *evidential burden in relation to that matter.

(5) A notice under paragraph (1)(e) or (2)(e) is not a legislative instrument.

25 Subsections 50-5(1)(e), 50-5(2)(d), 50-10(1)(d), 50-10(2)(c), 50-5(3), 50-5(4), 50-5(5), 50-10(3) and 50-10(4) are the provisions in the TAS Act relied upon by the respondents as the statutory foundation for their Defence to which I have referred at [11] and [12] above.

Some Important Matters of History

26 At [7] above, I noted that the scope of the dispute between the Board and the respondents insofar as liability for the alleged contraventions is concerned was very limited. Notwithstanding that circumstance, the Board chose to flesh out by evidence the substance of the interactions between fifteen of the respondents’ clients and Mr Kolya and his staff. This material is found in Exhibit A which is a Notice of Intention to Adduce Evidence of Previous Representations given pursuant to s 67 of the Evidence Act 1995 (Cth) to which no objection was taken within time by the respondents. In addition, the Board also chose to prove a number of other matters which it argued should be taken into account when the question of relief was being determined by the Court. This evidence was not tendered in order to expand the number of contraventions relied upon by the Board but rather to place those contraventions and the attitude of the respondents to their obligations under the law in an appropriate context. In particular, the Board submitted (and I agree) that these additional matters which it established in the evidence supported the following conclusions:

(a) The pleaded contraventions formed part of a significant overall business which Mr Kolya had been conducting for many years;

(b) Mr Kolya knew that the pleaded conduct was in breach of the TAS Act;

(c) Mr Kolya knew that he was engaging in conduct which he had been prohibited from undertaking by various decisions of courts and tribunals;

(d) Mr Kolya was well aware of the likely harm that his continued conduct of his business was likely to cause;

(e) Mr Kolya has never shown any contrition whatsoever for the pleaded conduct and appears to have no appreciation of its seriousness; and

(f) Heavy penalties should be imposed upon the respondents as well as other appropriate relief in order to ensure that the conduct complained of ceases.

27 I will now turn to make a number of findings which are amply supported by the evidence. Indeed, in large part, they are not matters which the respondents disputed.

28 In the period from 1 July 2001 to March 2010, Mr Kolya prepared and lodged tax returns and provided other tax advice to members of the public. In 2010, he described himself as “self-employed” and stated that, throughout the period 2005–2009, he spent 95% of his working time providing tax agent services. During that period, he prepared over 1,800 tax returns for individuals, partnerships and companies.

29 Throughout the period 2001–2010, Mr Kolya operated his business by claiming that H&R Block Ltd was his supervising agent and that he was entitled to use tax agent No 66837074 which was one of H&R Block Ltd’s tax agent numbers. Mr Kolya was not entitled to use that tax agent number and his claim to have been operating under the auspices of H&R Block Ltd was completely false. I find that Mr Kolya knew that this claim was false and also appreciated that these activities were unlawful.

30 In 2008, H&R Block Ltd became aware of Mr Kolya’s activities. As a result, through its solicitors, it immediately took steps to require Mr Kolya to cease representing that he had an appropriate connection with H&R Block Ltd.

31 “HP Kolya” was registered by Mr Kolya as a business name on 1 July 2003. In the period thereafter, up to 2010, he traded under that business name. On 18 April 2011, Mr Kolya brought into existence HP Kolya, the first respondent. Mr Kolya is and always has been the sole director of HP Kolya. He holds all ten of the company’s issued ordinary shares although an associate of his holds some shares in a different class. He controls HP Kolya. It carries on business for Mr Kolya’s benefit.

32 Since 2011, HP Kolya and Mr Kolya have continued to provide tax agent services to members of the public. In that period, they prepared and lodged on behalf of clients more than 650 tax returns. On 26 July 2013, as I have already mentioned, I granted interlocutory injunctions against both respondents preventing them from providing any further tax agent services and from carrying on other unlawful activities.

33 Neither Mr Kolya nor HP Kolya has ever been registered under the TAS Act as a tax agent. Since 2011, Mr Kolya and HP Kolya made a number of attempts to secure an appropriate registration under the TAS Act. All of those attempts were unsuccessful.

34 After the TAS Act became law, on 3 March 2010, Mr Kolya submitted an application to the Board for transitional registration as a tax agent. In that application, he claimed to have been registered as a tax agent under the name H&R Block Ltd, citing its tax agent number. He also claimed not to have been convicted of a serious taxation offence. On 29 September 2010, the Board rejected Mr Kolya’s application finding (inter alia) that:

(a) In claiming to have been registered as a tax agent with H&R Block Ltd, Mr Kolya had knowingly provided false information in his application;

(b) Contrary to his assertions, he had in fact been convicted of serious taxation offences and had knowingly claimed otherwise;

(c) Mr Kolya lacked a proper understanding of the regulatory regime and had been operating as an unregistered provider;

(d) Mr Kolya had failed to demonstrate that he had provided taxation services to a competent standard for a reasonable period; and

(e) Mr Kolya was not a person of good fame, integrity and character.

35 By virtue of certain transitional arrangements, Mr Kolya was, from 1 March 2010, taken to have been registered as a BAS agent. His continued registration as a BAS agent was reviewed by the Board at the same time as the Board considered his tax agent application. On 24 November 2010, the Board made a decision to terminate Mr Kolya’s registration as a BAS agent for the same reasons as it had declined to grant his application to be registered as a tax agent.

36 Mr Kolya then challenged both decisions of the Board in the AAT. As part of this process, he obtained a temporary stay of the Board’s decision to terminate his BAS agent registration (Kolya v Tax Practitioners Board (2011) 81 ATR 912). On 15 November 2011, the AAT upheld the Board’s decision (Kolya v Tax Practitioners Board (2011) 85 ATR 635). At [54]–[55] of its Decision, the AAT held that Mr Kolya’s registration as a migration agent did not permit him to describe himself as an Australian legal practitioner. In addition, at [93], the AAT observed:

There is powerful evidence that [Mr Kolya] has misled clients about his tax agent registration. He has provided incorrect information to the Board about his previous tax agent registration, and about his previous relevant experience and his qualifications. And I am satisfied that he knew, or had good reason to know, that this information was incorrect at the time he provided it to the Board.

37 On 30 November 2011, Mr Kolya appealed from the AAT decision. On 13 March 2012, Flick J dismissed Mr Kolya’s appeal and ordered that he pay the costs of the Board (Kolya v Tax Practitioners Board (2012) 87 ATR 474).

38 I pause to note that, as a consequence of the statutory transitional arrangements and the temporary stay which Mr Kolya secured from the AAT, he should be taken as having been registered as a BAS agent throughout the period 1 March 2010 to 13 March 2012.

39 On 3 April 2012, Mr Kolya appealed to the Full Court from the decision of Flick J. At that time, he also filed an Interlocutory Application seeking to prevent the AAT’s decision from coming into effect. On 11 May 2012, I dismissed his Interlocutory Application (Kolya v Tax Practitioners Board (2012) 88 ATR 471). On 12 July 2012, Mr Kolya discontinued his appeal to the Full Court.

40 In late 2011, Mr Kolya submitted further applications to the Board for registration as a BAS agent and as a tax agent. These applications were again refused by the Board.

41 On 23 November 2011, following the Board’s refusal of Mr Kolya’s application to become a registered tax agent, HP Kolya applied for registration as a tax agent. The Board rejected this application on 3 May 2012 upon the basis that its sole director, Mr Kolya, was not a person of good fame, integrity and character (noting its earlier decisions and findings about Mr Kolya).

42 The following conclusions may be drawn from the above narrative:

(a) Throughout the period 2001–2013, Mr Kolya either on his own account or through HP Kolya carried on a substantial business of providing tax agent services and BAS agent services at a time when he must be taken to have been fully aware that he was not permitted to do so. He made false representations about his association with H&R Block Ltd, made false representations as to whether he had been convicted of serious taxation offences, displayed a keen and detailed understanding of the TAS Act by taking advantage of certain transitional arrangements provided for under that Act in respect of his status as a BAS agent and persisted with his argument that his registration as a migration agent under the Migration Act was sufficient to allow him to avail himself of the exception to the requirement for registration as a tax agent specified in various subsections of subs 50-5 and subs 50-10 of the TAS Act.

(b) Mr Kolya pursued unmeritorious appeals in order to retain the benefit of the temporary stay which he had originally secured from the AAT in respect of the termination of his status as a BAS agent and systematically and persistently exploited that state of affairs for his own commercial benefit; and

(c) By all of the conduct to which I have referred, Mr Kolya displayed a flagrant disregard for the relevant registration requirements under the TAS Act.

Liability for the Pleaded Contraventions

43 I shall deal with Mr Kolya’s defence of the case put against him and against HP Kolya in respect of Ms Buckthorpe in the next section of these Reasons.

44 I now turn to deal with the only substantive defence raised by the respondents to the case put against them being that, by reason of Mr Kolya’s registration as a migration agent under the Migration Act, the tax agent services and BAS services provided by him and by HP Kolya over the years were within the statutory exceptions to registration provided for in subss 50-5(1)(e), 50-5(2)(d), 50-10(1)(d) and 50-10(2)(c) of the TAS Act. Mr Kolya also argued that he could rely upon subss 50-5(3), 50-5(4), 50-5(5), 50-10(3) and 50-10(4).

45 In their Defence, the respondents admit that Mr Kolya is not an Australian lawyer as defined in the Legal Profession Act 2006 (ACT). On the other hand, they put in issue the matters pleaded by the Board in pars 17–21 of the ASC. Those paragraphs are in the following terms:

17. Mr Kolya is not an Australian legal practitioner as defined in the Legal Profession Act 2006 (ACT).

18. HP Kolya Pty Ltd has not given the law society council written notice of its intention to engage in legal practice in accordance with section 104 of the Legal Profession Act 2006 (ACT).

19. HP Kolya Pty Ltd does not have a legal practitioner director and therefore does not meet the requirements of section 107 of the Legal Profession Act 2006 (ACT).

20. By reason of each and both of the matters pleaded in paragraphs 18 and 19 it is unlawful for HP Kolya Pty Ltd to engage in legal practice in the ACT.

21. By reason of the matters pleaded in paragraphs 16 and 17 it is unlawful for Mr Kolya to engage in legal practice in the ACT.

46 There is no doubt that, when appropriate regard is had to the admissions made by the respondents in their Defence and to other evidence tendered before me, the respondents have provided tax agent services and BAS agent services as alleged by the Board at a time when neither of them was registered as a tax agent under the TAS Act or as a BAS agent under that Act.

47 Taking subs 50-5(1) as an example of the way in which subs 50-5 and subs 50-10 operate, a person contravenes that subsection if that person is not a registered tax agent and provides a tax agent service which is not a BAS service or tax (financial) advice service in circumstances where that person knows, or ought reasonably to know, that the service is a tax agent service and that person charges or receives a fee or other reward for providing a tax agent service.

48 In addition to the requirements which I have spelt out at [47] above, the final element of the contravention is that which is found in subs 50-5(1)(e) which provides that, if you satisfy the conditions specified at [47] above, and:

if you provide the tax agent service as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service consists of preparing, or lodging, a return or a statement in the nature of a return.

you will contravene the subsection.

49 Subsection 50-5(3) of the TAS Act provides that the element specified in subs 50-5(1)(e)(ii) will not be satisfied if the tax agent service is provided as a legal service in the course of acting for a trust or deceased estate as trustee or legal personal representative.

50 Mr Kolya argued that the tax agent services provided by the respondents were provided as a legal service in the course of acting for a trust or deceased estate as trustee or legal personal representative. He then submitted that subs 50-5(1)(e)(ii) did not apply to the tax agent services provided by the respondents.

51 None of the services provided by the respondents to clients were provided in the course of acting as a trustee of a trust or as a trustee or legal representative of a deceased estate.

52 In respect of many clients, Mr Kolya procured a signed document authorising one or other of the respondents as the “legal personal representative” of the client in question. But this is just a device. The term “legal personal representative”, when used in subs 50-5(3) is a term of art which refers to an executor or administrator appointed as the legal personal representative of a deceased person in accordance with the law of succession. In my judgment, subs 50-5(3) does not encompass the giving of a general power of attorney from one living person to another. The purpose of subs 50-5(3) is to except from the requirement to be registered persons who provide a tax agent service consisting of preparing, or lodging a return or a statement in the nature of a return as part of a legal service in the course of acting as the trustee of a trust or the trustee or legal personal representative of a deceased estate. The present case does not engage subs 50-5(3) at all. I do not think that s 995-1 of the Income Tax Assessment Act 1997 (Cth) requires a different conclusion.

53 Mr Kolya submitted that the tax agent services and BAS agent services provided by the respondents were provided to their clients “… as a legal service” and that neither of the respondents was prohibited in the manner specified in subs 50-5(1)(e)(i) and its equivalents from providing those services. In addition, as I have already mentioned, he also argued that subs 50-5(1)(e)(ii) and its equivalents did not apply by reason of the operation of subs 50-5(3) and its equivalents. I have already rejected this latter argument.

54 The linchpin of the respondents’ Defence is the proposition that the tax agent services and the BAS agent services provided by them were provided “… as a legal service” within the meaning of subs 50-5(1)(e) and its equivalents.

55 “Legal service” in those subsections is not defined for the purposes of the TAS Act. When used in the TAS Act, it should be interpreted having regard to its ordinary meaning, the statutory context, the statutory purpose and any relevant extrinsic materials (see Project Blue Sky Inc v Australian Broadcasting Authority (1998) 194 CLR 355).

56 In the Legal Profession Act 2006 (ACT), “Australian lawyer” and “Australian legal practitioner” are terms which are defined in s 7 and s 8.

57 Section 16(1) provides that a person commits an offence if the person “engages in legal practice in the ACT” and the person is not an Australian legal practitioner. The section goes on to give examples of what is meant by “engaging in legal practice”. Those examples indicate that the legislature had in mind that the concept of “engaging in legal practice” involves doing work or transacting business which, according to convention and the relevant case law, is generally accepted at the relevant time as work which is done by a practising lawyer qualified to practise as such. Section 16 is typical of statutory provisions governing the practice of law in Australia which require that work ordinarily regarded as part of carrying on legal practice should only be done by qualified persons who, by dint of their qualification, have satisfied appropriate academic and training requirements and who are susceptible to supervision and regulation by the relevant supervising authorities. In the dictionary at the end of the Act, “engage in legal practice” is defined as including “practise law”. In the same dictionary, “legal services” is defined as meaning “work done, or business transacted, in the ordinary course of legal practice”. These provisions and concepts are also found in other State and Territory laws which regulate the legal profession.

58 Thus, it seems to me that the ordinary meaning of a “legal service” or “legal services” is a service or services ordinarily provided by qualified lawyers entitled to practise as such and which unqualified persons are prohibited from supplying.

59 In my judgment, when used in subs 50-5(1)(e) and its equivalents in the TAS Act, the expression “legal service” is used in this sense. For this reason, the activities of a person registered as a migration agent under the Migration Act who is not a person who is also entitled to practise as a lawyer are not apt to be described as “legal services”. That is not to say that such activities may not fall within that concept if performed by lawyers entitled to practise as such but that is not the present question.

60 As submitted by Counsel for the Board, the ordinary meaning which I have attributed to the expression “legal service” is supported by the statutory context in which that expression is found in the TAS Act. Immediately following the reference to “legal service” in subs 50-5(1)(e) and its equivalents, there is specific reference to State laws or Territory laws which regulate legal practice and the provision of legal services. The juxtaposition of that reference to the expression “legal service” suggests that the Parliament had in mind that only persons qualified as practising lawyers were entitled to provide legal services. In addition, the Explanatory Memorandum at pars 4.39 and 4.40 makes clear that a legal service is one provided by persons such as legal practitioners who are permitted to provide legal services under a State or Territory law regulating legal practice and the provision of legal services.

61 Neither HP Kolya nor Mr Kolya is entitled to provide legal services under any State or Territory law. In those circumstances, neither of them can bring themselves within the exception to registration provided for in subs 50-5(1)(e) and its equivalents.

62 For all of the above reasons, I am of the view that the Board has established the contraventions pleaded against each of the respondents.

The Alecia Buckthorpe Matter

63 The Board read and relied upon an affidavit sworn by Alecia Sabalo Buckthorpe sworn on 11 February 2014.

64 In that affidavit, Ms Buckthorpe swore that Mr Kolya had prepared an Income Tax Return for her in late August 2013 and that she had paid him $250 in cash for that service. She later became aware that her Income Tax Return had not been lodged and that Mr Kolya was not a registered tax agent. She then went to H&R Block Ltd who prepared a substitute Tax Return for her which was subsequently lodged.

65 Mr Kolya gave oral evidence to the effect that he had never met Ms Buckthorpe. He admitted that it was possible that someone employed by him may have carried out the work which she described in her affidavit. But he could not assist with any evidence as to who that might be. Mr Kolya said that he had never dealt with Ms Buckthorpe in any capacity.

66 The evidence given by Mr Kolya was in direct conflict with that given by Ms Buckthorpe. She testified that she met a man who introduced himself as Peter Kolya when she attended at his residential address on 23 August 2013.

67 Mr Kolya was cross-examined about the evidence of Ms Buckthorpe. It was suggested to him that he was not telling the truth when he said that he had never met her. In particular, Mr Kolya was cross-examined about the provenance of the Invoice which Ms Buckthorpe testified that he had given to her for work done by him in preparing her 2013 Income Tax Return. Mr Kolya could not satisfactorily explain the existence or provenance of the Invoice in question and resorted to claiming that the Invoice was a forgery.

68 I do not accept Mr Kolya’s evidence concerning Ms Buckthorpe. I am satisfied that Ms Buckthorpe’s recollections as to her dealings with Mr Kolya are accurate. I reject Mr Kolya’s contention that he had no dealings with Ms Buckthorpe. For these reasons, I find that the Board has made out its case in respect of Mr Kolya’s dealings with Ms Buckthorpe.

69 That finding necessarily means that I am also satisfied that Mr Kolya breached the injunctions which I granted on 26 July 2013 by providing a tax agent service to Ms Buckthorpe. The evidence established that the terms of the injunctions which I granted on 26 July 2013 were brought to Mr Kolya’s attention soon after that date. He had been well aware of the fixture prior to 26 July 2013 but had decided not to attend in Court on that day. The matter had then proceeded in his absence.

70 I also find, therefore, that Mr Kolya knowingly breached the injunctions which I granted on 26 July 2013. I consider this to be a most serious matter. I propose to take it into account when fixing the pecuniary penalties to be imposed upon each of the respondents.

The Appropriate Penalties

71 At [67]–[72] of Clean Energy Regulator v MT Solar Pty Ltd [2013] FCA 205, I summarised the general principles to be adopted when this Court comes to impose civil penalties in a regulatory context. At those paragraphs, I said:

67 The relevance of maximum penalties when consideration is being given by the Court to the imposition of a pecuniary penalty in a criminal case has been authoritatively determined by the High Court in Markarian v The Queen (2005) 228 CLR 357 (Markarian). At 372 [31] in Markarian, Gleeson CJ, Gummow, Hayne and Callinan JJ said:

It follows that careful attention to maximum penalties will almost always be required, first because the legislature has legislated for them; secondly, because they invite comparison between the worst possible case and the case before the court at the time; and thirdly, because in that regard they do provide, taken and balanced with all of the other relevant factors, a yardstick. That having been said, in our opinion, it will rarely be, and was not appropriate for Hulme J here to look first to a maximum penalty (The maximum selected by his Honour was not, as will appear, the maximum available in respect of the principal offence.), and to proceed by making a proportional deduction from it. That was to use a prescribed maximum erroneously, as neither a yardstick, nor as a basis for comparison of this case with the worst possible case. That he used the maximum penalty impermissibly appears from his Honour’s particular deference to it in this passage ((2003) 137 A Crim R 497 at 506 [37]):

“Parliament cannot have intended that, other things being equal, the penalty for supplying more than 250 g should be less than for supplying that quantity.”

The form of the statement is explained by the fact that his Honour did not start with the maximum penalty for an offence involving the quantity in question, but used another maximum penalty as his starting point, that is, the maximum for an offence in the category of seriousness immediately below that of the principal offence.

68 In this Court, these remarks by the High Court in Markarian have been held to apply to the imposition of civil penalties (see Australian Ophthalmic Supplies Pty Ltd v McAlary-Smith (2008) 165 FCR 560 (Australian Ophthalmic Supplies) at 584 [108] (per Buchanan J); Minister for Sustainability, Environment, Water, Population and Communities v Woodley [2012] FCA 957 (Woodley) at [40]–[41] (per Foster J); Australian Communications and Media Authority v Bytecard Pty Ltd [2013] FCA 38 (Bytecard) at [38]–[39] (per Foster J); and Secretary, Department of Health and Ageing v Export Corp (Australia) Pty Ltd (2012) 288 ALR 702 at 714 [49]–[50] and at 718 [67] (per Perram J)).

69 It is plain that the legislature has given the clearest possible indication that contraventions of s 24B and s 154N of the REE Act are to be considered as serious matters when a court comes to determine an appropriate civil penalty.

70 The principal object of civil penalty provisions is to ensure deterrence. In Trade Practices Commission v CSR Limited (1991) ATPR 41-076, which was a case dealing with s 76 of the Trade Practices Act 1974 (Cth), French J (as he then was) said (at p 52,152):

The principal, and I think the only, object of the penalties imposed by s 76 is to attempt to put a price on contravention that is sufficiently high to deter repetition by the contravenor and by others who might be tempted to contravene the Act.

71 The dictum of French J in Trade Practices Commission v CSR Limited which I have extracted at [70] above has been applied not only in the trade practices context but in a wide variety of regulatory regimes. In particular, the need for a penalty to have a proper deterrent effect has been emphasised in the context of laws passed by the Parliament to protect the environment (eg Woodley [2012] FCA 957, esp at [53]–[67]).

72 In both Woodley and in Bytecard, I approached the determination of civil penalties by applying the process commonly called “instinctive synthesis”. As I said in both of those cases, that process, as I understand it, has the following attributes:

(a) There must be a weighing of all relevant factors, rather than starting from a predetermined figure and making incremental additions or subtractions for each separate factor (Markarian, at 373–375 [36]–[39] (per Gleeson CJ, Gummow, Hayne and Callinan JJ) and at 385–387 [69]–[73] (per McHugh J); and

(b) It is critical that the reasoning process involved in synthesising the penalty be transparent (Markarian at 373–375 [36]–[39] (per the plurality) and at 390 [84] (per McHugh J).

72 In the same case, I considered the course of conduct principle which allows the Court to impose a sentence or punishment which fairly reflects the substance of the offending conduct, rather than a purely mathematical accumulation of sentences for each offence which may be able to be technically identified. In addition, I also discussed the totality principle. At [81]–[83], I said:

81 The totality principle operates as a “final check” to ensure that the penalties to be imposed on a wrongdoer, considered as a whole, are “just and appropriate” (Mill v The Queen (1988) 166 CLR 59 (Mill) at 62–63 and Johnson at 347–348 [3]–[5] (per Gleeson CJ) and at 354–358 [18]–[35] (per Gummow, Callinan and Heydon JJ). The totality principle has been adopted and applied in the civil penalty context (Mornington Inn at 386–387 [5]–[7] (per Gyles J) and at 396–398 [41]–[46] and 408 [90]–[92] (per Stone and Buchanan JJ)).

82 Consideration of the totality principle will not necessarily result in a reduction from the penalty considered appropriate prior to the application of that principle. However, in cases where the Court considers that the total penalties to be imposed are inappropriate, the Court should alter the final penalties to ensure that they are “just and appropriate”. It is now recognised in the civil penalty context that the proper approach when applying the totality principle is to start by ascertaining the penalty which would be appropriate for each individual contravention and then to reduce the total of the amounts derived in this fashion for reasons of totality. It is undesirable to start with a single global total penalty and then to divide it among the individual contraventions in order to derive separate penalties.

83 Counsel for the regulator advocated that the Court should not apply the course of conduct principle but rather deal with any lack of proportionality in the penalties to be imposed in the present case through the application of the totality principle.

73 The Board submitted that, in this case, there was no occasion to apply the course of conduct principle since none of the contraventions pleaded arise from the same conduct but should rather be regarded as separate wrongful acts attracting separate penalties. I think that this submission is correct and I propose to consider the question of penalties upon the basis that each contravention is a separate wrongful act.

74 I do think, however, that I should apply the totality principle which I explained at [81]–[83] in Clean Energy Regulator v MT Solar Pty Ltd.

75 The statutory maximum penalty applicable to each contravention is as follows:

(a) Providing tax agent and BAS services contrary to subs 50-5(1) and (2): $27,500 for an individual and $137,500 for a body corporate.

(b) Advertising tax agent services contrary to subs 50-10(1): $8,500 for an individual and $42,500 for a body corporate.

76 The relevance of maximum penalties when consideration is being given by the Court to the imposition of a pecuniary penalty in a criminal case has been authoritatively determined by the High Court in Markarian v The Queen (2005) 228 CLR 357 (Markarian). I cited [31] in Markarian at [67] in Clean Energy Regulator v MT Solar Pty Ltd. I have extracted that paragraph at [71] above.

77 As I noted in Clean Energy Regulator v MT Solar Pty Ltd (at [68]), these remarks by the High Court in Markarian have been held to apply to the imposition of civil penalties.

78 In the present case, upon the assumption that each contravention should be treated as a separate matter requiring the imposition of a separate penalty, the maximum penalty that can be imposed upon HP Kolya for all of the contraventions which have been proven against it is $4,442,500 and the maximum penalty that can be imposed upon Mr Kolya for all of the contraventions proven against him is $237,500.

79 There are no criteria expressed in the TAS Act itself for the imposition of pecuniary penalties against persons who contravene the civil penalty provisions of that Act. Nonetheless, I propose to apply the principle articulated by French J (as he then was) in Trade Practices Commission v CSR Limited [1991] ATPR 41-076 where his Honour stated unequivocally that the main object of civil pecuniary penalties [in that case under the Trade Practices Act 1974 (Cth)] is to attempt to put a price on contraventions that is sufficiently high to deter repetition by the contravenor and by others who might be tempted to contravene the relevant statute.

80 In the present case, there is an urgent and strong imperative to impose penalties which will, once and for all, bring home to Mr Kolya that he can no longer flout the regulatory requirements embodied in the TAS Act for his own commercial benefit. He is the principal perpetrator of the contravening conduct. He is the person who has caused HP Kolya to contravene the TAS Act. To date, he has been a recalcitrant contravenor who has repeatedly and persistently ignored the prohibition on providing tax agent services and BAS services and advertising the same on persons who are not registered tax agents or BAS agents. Not only has he shut his eyes to the obvious over a lengthy period, but he has taken steps of an artificial kind designed to prolong his opportunities for commercial gain while contesting the legitimate and valid concerns of the Board. He has actively engaged in conduct which is diametrically opposed to the object of the TAS Act. In so doing, he has caused significant harm to ordinary members of the public who were entitled to assume when dealing with him that he had the necessary qualifications and competence to perform the tasks which he undertook to perform for them. In addition, he has shown no contrition for his conduct and has failed to cooperate with the Board. He does not accept that he has done the wrong thing. He shows no remorse or contrition. Rather, he has persisted, even to the end of the case, in his argument that his registration as a migration agent is sufficient for him to justify his providing tax agent services and BAS services.

81 This case requires a strong response from the Court both in order to specifically deter Mr Kolya and also to make clear to others who may be minded to replicate his conduct that they should think very carefully before doing so because the penalties which will be imposed if caught will be significant.

82 In the present case, Counsel for the Board made very detailed written submissions and oral submissions directed to the relevant principles governing the imposition of pecuniary penalties in the present context. These submissions were also directed to persuading the Court to impose substantial penalties. After providing an appropriate analysis, the Board suggested that the penalties which should be imposed should be in the following range:

(a) For HP Kolya: $800,000–$900,000; and

(b) For Mr Kolya: $110,000–$125,000.

83 Those suggested ranges were arrived at after a substantial discount was allowed on account of the totality principle.

84 At the trial, I received both the written and oral submissions made by Counsel for the Board, including submissions directed to the imposition of civil penalties in the present case. Indeed, in addition, Mr Kolya was given an opportunity to address those matters. It must be remembered, of course, that this is not a case where the parties have agreed upon all of the material facts and also agreed upon the appropriate penalties. Although there was little real dispute as to the facts, Mr Kolya never admitted liability nor did he engage with the Board in relation to the appropriate penalties upon the assumption that liability was admitted.

85 On 1 May 2015, the Full Court delivered judgment in Director, Fair Work Building Industry Inspectorate v Construction, Forestry, Mining and Energy Union [2015] FCAFC 59 (Inspectorate v CFMEU). In that judgment, the Court considered a number of issues relevant to the case before it arising out of the decision of the High Court in Barbaro v The Queen (2014) 305 ALR 323 (Barbaro).

86 In a subsequent written submission forwarded to me after the hearing, the Board addressed the question of whether Barbaro had any relevance to the present case. It submitted that Barbaro had no relevance to the present case for a number of reasons. Mr Kolya did not engage with the Board on the Barbaro questions.

87 I shall briefly refer to Barbaro and Inspectorate v CFMEU in the next section of these Reasons.

88 At the moment, all I need say is that, while I have received and considered both the written and oral submissions made by the Board in relation to the imposition of civil penalties in this case, I have made up my own mind as to the appropriate penalties to be imposed.

The Relevance of Barbaro v The Queen

89 In Barbaro, the appellants, Messrs Barbaro and Zirilli, pleaded guilty to serious drug offences in the Supreme Court of Victoria. Before they pleaded guilty, there were discussions between the lawyers on both sides as to the range of sentences to which the offenders might be sentenced. The offenders were then sentenced. At the sentencing hearing, the trial judge refused to accept any submission from the prosecution or the defence as to the range of sentences that could be imposed upon the appellants. Leave to appeal was refused to Mr Barbaro. Mr Zirilli’s appeal was dismissed. In the High Court, the appellants argued that the sentencing hearing before the trial judge was procedurally unfair because she had failed to take into account a relevant consideration, namely, the views of the parties as to the appropriate sentence.

90 In the High Court, the majority (French CJ, Hayne, Kiefel and Bell JJ) held that the appellants’ arguments depended upon two flawed premises. The first was that the prosecution is permitted (or required) to submit to a sentencing judge its view of what are the bounds of the range of sentences which may be imposed on an offender. The second was that that premise is a submission of law (see the remarks of the majority at 325 [6]).

91 At 325 [7]–[8], the majority said:

7. The prosecution's statement of what are the bounds of the available range of sentences is a statement of opinion. Its expression advances no proposition of law or fact which a sentencing judge may properly take into account in finding the relevant facts, deciding the applicable principles of law or applying those principles to the facts to yield the sentence to be imposed. That being so, the prosecution is not required, and should not be permitted, to make such a statement of bounds to a sentencing judge.

8 Because the premises for the applicants’ arguments are wrong, the appeals must fail. Before examining the premises further, however, it is necessary to say something about the facts.

92 At 327–328 [20]–[23], the majority explained that, in Victoria, in criminal matters, as a result of the decision in R v MacNeil-Brown (2008) 20 VR 677 (MacNeil-Brown), a practice had developed in that State of a sentencing judge asking Counsel for the prosecution to make a submission as to the “available range” of sentences. The majority in the High Court considered this practice to be wrong in principle. They held that MacNeil-Brown should be overruled. The majority specifically held that that practice should cease.

93 At 328–332 [24]–[43], the majority gave their reasons for the conclusions to which they had come. In those paragraphs, the majority explained that the use of the expression “an available range” in respect of a sentence for a criminal offence is apt to mislead. At 329 [28] in particular, the Court said that a conclusion that an error has (or has not) been made in a sentence neither permits nor requires setting the bounds of the range of sentences within which the sentence should (or could) have fallen. The correct principle is that a sentence may be set aside if it is manifestly excessive or manifestly inadequate. In that event, the discretion to sentence must be re-exercised.

94 At 329 [29], the majority said:

The practice countenanced by MacNeil-Brown assumes that the prosecution's proffering a statement of the bounds of the available range of sentences will assist the sentencing judge to come to a fair and proper result. That assumption depends upon the prosecution determining the supposed range dispassionately. It depends upon the prosecution acting not only fairly (as it must) but in the role which Buchanan JA rightly described (MacNeil-Brown at [128]) as that of “a surrogate judge”. That is not the role of the prosecution.

95 The majority went on to emphasise the need for sentences to be imposed dispassionately. They emphasised that the role of the prosecution and the role of the judge in the sentencing process is not the same. At 330 [33], the majority said:

… If a judge sentences within the range which has been suggested by the prosecution, the statement of that range may well be seen as suggesting that the sentencing judge has been swayed by the prosecution's view of what punishment should be imposed. By contrast, if the sentencing judge fixes a sentence outside the suggested range, appeal against sentence seems well nigh inevitable.

96 The focus of the majority judgment at 330–331 [34]–[40] was on the actual sentence itself. In my view, the majority held that it was permissible for the parties to address the Court on the relevant sentencing principles and on comparable sentences. The prohibition articulated by the majority is confined to the prosecution’s suggesting a particular sentence. In particular, at 331 [38] and [40], the majority said:

38. If a sentencing judge is properly informed about the parties' submissions about what facts should be found, the relevant sentencing principles and comparable sentences, the judge will have all the information which is necessary to decide what sentence should be passed without any need for the prosecution to proffer its view about available range. If the judge is not sufficiently informed about what facts may or should be found, about the relevant principles or about comparable sentences, the prosecution's proffering a range may help the sentencing judge avoid imposing a sentence which the prosecution can later say was manifestly inadequate. But it will not do anything to help the judge avoid specific error; it will not necessarily help the judge avoid imposing a sentence which the offender will later allege to be manifestly excessive. Most importantly, it will not assist the judge in carrying out the sentencing task in accordance with proper principle (cf Wong (2001) 207 CLR 584 at 611 [75]; Markarian v The Queen (2005) 228 CLR 357 at 373 375 [37]; [2005] HCA 25; Muldrock v The Queen (2011) 244 CLR 120 at 128 [18]; [2011] HCA 39; Munda v Western Australia (2013) 87 ALJR 1035 at 1046 [59]; 302 ALR 207 at 219; [2013] HCA 38).

…

40 The setting of bounds to the available range of sentences in a particular case must, however, be distinguished from the proper and ordinary use of sentencing statistics and other material indicating what sentences have been imposed in other (more or less) comparable cases. Consistency of sentencing is important. But the consistency that is sought is consistency in the application of relevant legal principles, not numerical equivalence (Hili (2010) 242 CLR 520 at 535 [48] [49]).

97 At 332 [42]–[43], the majority held that the proffering of a sentencing range by the prosecution was a statement of opinion not a submission of law.

98 At 332–333 [44]–[49], the majority held that there was no want of procedural fairness and no other unfairness in the sentencing judge’s refusal to receive submissions as to the range of appropriate sentences.

99 Justice Gageler joined in the orders which the majority held should be made. However, his Honour took a different view as to the status of a submission proffered by the prosecution in relation to sentence. His Honour held that such a submission is a submission of law and not merely a statement of opinion. His Honour went on to hold that the prosecution had a duty to assist the Court to avoid appealable error by making a submission as to the range of appropriate sentences if the sentencing court requests such assistance or if the prosecution thinks that there is a significant risk that the Court will impose an appealable sentence in the absence of such a submission. His Honour also held that the Court is not obliged to accept the submission and is required to give effect to its own conclusion as to the appropriate sentence.

100 In Inspectorate v CFMEU, the ratio of the Full Court was that the reasoning in Barbaro applies to proceedings for the imposition of a civil pecuniary penalty where the parties have agreed upon the penalties and, pursuant to that agreement, where the parties make joint submissions to the Court as to the appropriate penalties or range of possible penalties.

101 However, in Inspectorate v CFMEU, the Full Court went further and expressed the view that the reasoning of the majority of the High Court in Barbaro inevitably leads to the conclusion that it is not permissible for the regulatory authority in civil pecuniary penalty cases to make a submission to the Court identifying a range of penalties, nominating specific penalties or urging the adoption of agreed penalties. At [239]–[243], the Full Court said:

239 We accept that in the short term, there may be inconvenience and perhaps increased expense to regulators and respondents in cases where agreed penalties, or agreed ranges have already been identified. We do not expect that such additional cost will be significant. We have already said much about why we consider that the decision in Barbaro should inform our approach to the agreed statement. Primarily, we consider that the sentencing process, and that in which a pecuniary penalty is imposed are very similar in nature. In particular, both address punishment by the State, and both require an assessment of a wide range of considerations which interact in complex ways. Hence each involves the instinctive synthesis to which we have referred. We consider that the concerns identified in Barbaro are relevant to the pecuniary penalty process. The impermissible expression of an opinion as to the amount of the penalty reflects a well-established limitation upon the ambit of a party’s right to make submissions. Further, the difficulty in understanding the method by which any such opinion is formed is as real in pecuniary penalty cases as it is in criminal sentencing, as is the risk that such opinions may compromise the sentencing process and/or create a public perception of such compromise.

240 Insofar as concerns submissions as to the range within which the penalty should fall, it is equally as inappropriate in pecuniary penalty cases as in criminal sentencing. The High Court has made it clear that statutory discretions are not to be limited other than by reference to the relevant statute. It is difficult to identify any other statutory discretion conferred upon a court which has been limited in the way in which the decisions in NW Frozen Foods and Mobil have limited the discretion to fix a pecuniary penalty. When examined, the historical basis for that limitation is not grounded in principle.

241 As to an agreed penalty, we have previously indicated that any admission of liability may be a relevant consideration in sentencing or imposing a pecuniary penalty. Willingness to submit to the imposition of a substantial penalty may also be relevant in that way. However, even if the offender nominates a substantial figure as the penalty to which it will submit, the Court must still fix the appropriate penalty, taking into account such contrition as well as all other relevant considerations. As we have said, any such agreement is no more than an expression of a shared opinion, and therefore inadmissible. As we have also said, the amount of the agreed penalty may simply reflect the point at which each party considers that it is in its interest to agree. In either case, the agreed amount offers no assistance in fixing the amount of the appropriate penalty.

242 Finally, we do not dismiss the concerns of the regulators as to the importance of negotiations and agreements in the enforcement of the various statutes pursuant to which pecuniary penalties may be imposed. However we do not accept that the problem is as great as the regulators suggest. The adversarial system depends upon the capacity of professional advocates to explain the most complicated of legal and factual situations by reference to the evidence and the law. The issues to be ventilated in pecuniary penalty cases may be complex, but they are not amongst the most complex matters which this Court regularly considers. We expect that regulators and offenders will continue to seek to reach agreement as to factual matters and as to the application of the law. As to uncertainty of outcome, we consider it to be the inevitable consequence of entrusting the pecuniary penalty process to the judiciary. NW Frozen Foods and Mobil establish that it is for the Court to fix the penalty. That proposition has been constantly repeated in subsequent cases. In these proceedings, no party has suggested otherwise. Once that proposition is accepted, the only remaining question is as to the relevance, to the Court’s consideration, of submissions as to ultimate penalty or range of penalties, or the fact of any agreement as to penalty. In Barbaro, the High Court held that statements as to ultimate outcome or range were merely expressions of opinion and therefore could not properly be advanced in submissions. There can be no justification for taking a different view in pecuniary penalty proceedings.

243 We appreciate that the views which we have expressed are inconsistent with the long established, although perhaps imprecise practice described in NW Frozen Foods and Mobil. We depart from that practice only because the decision in Barbaro, in our view, requires that we do so.

102 In Inspectorate v CFMEU, the Full Court sat in the original jurisdiction of the Court pursuant to a direction made by the Chief Justice under s 20(1A) of the Federal Court of Australia Act 1976 (Cth).

103 It may be thought that the Full Court’s decision in Inspectorate v CFMEU is not binding upon single judges of this Court because the Full Court was exercising the original jurisdiction of the Court and not the appellate jurisdiction of the Court. I do not agree with that notion. I do not think that the status of the decision as a precedent is diminished or put into question at all by the circumstance that the Full Court was exercising the original jurisdiction of the Court. Quite clearly, the Full Court was appropriately constituted as a Full Court pursuant to s 20(1A) of the Federal Court Act and proceeded to deal with the matter accordingly. I see no reason why the decision should not be regarded as binding upon single judges of the Court.

104 That said, it is well to remember that, in Barbaro, the majority did not hold that parties were not permitted to make submissions directed to what facts should be found, to the relevant sentencing principles or to comparable sentences. The only matter which is subject to the prohibition articulated by the majority in Barbaro is the nomination of a specific penalty or sentence.

105 In the present case, as I have already indicated, I have read and considered the submissions made by both parties in respect of the relevant principles to be applied in respect of the imposition of the civil penalties called for in the present case as well as taken into account the material facts proven in evidence and the subject of submissions. I have also received submissions as to the appropriate penalties to be imposed. I wish to make it very clear that, in relation to all of these matters, I have made up my own mind and come to my own conclusions. In particular, in imposing the penalties which I have decided to impose, I have weighed the various relevant factors to which I have referred for myself. I have not been constrained in any way by the specific penalties nominated by the Board or the responsive submissions to the Board’s nomination made by the respondents.