FEDERAL COURT OF AUSTRALIA

National Australia Bank Limited, in the matter of San Esteban (former Bankrupt) v State of New South Wales [2015] FCA 289

IN THE FEDERAL COURT OF AUSTRALIA | |

NATIONAL AUSTRALIA BANK LIMITED (ABN 12 004 044 937) Applicant | |

AND: | First Respondent GLOBAL FINANCIAL GROUP (GFG) PTY LTD (ACN 073 220 747) Second Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. Pursuant to s 133(9) of the Bankruptcy Act 1966 (Cth), the whole of the land comprised in Certificate of Title, Folio Identifier 307/808666 and known as 22 Ashwick Circuit, St Clair in the State of New South Wales (the Property), vest in the Applicant, subject to the conditions in Order 2 below.

2. Pursuant to s 133(9) of the Bankruptcy Act 1966 (Cth), upon the vesting of the Property in the Applicant:

(a) the Applicant may only deal with the Property pursuant to its powers as mortgagee under the Real Property Act 1900 (NSW) and under its mortgage over the Property dated 31 January 2005, bearing registered number AB331115 (the Mortgage);

(b) the Applicant be entitled to calculate the amount secured by the Mortgage as including all moneys that would have been secured by the Mortgage had the trustee of the former bankrupt estate of Ariel San Esteban not disclaimed the Property, and to deduct and retain for its own absolute use and property such amount from any proceeds of sale of the Property as if it were money secured by the Mortgage (including all costs properly incurred in selling, and incidental to the sale of, the Property);

(c) the Applicant must, within 14 days after settlement of any sale of the Property, provide an account of its payments and receipts to:

(1) David James Hambleton as trustee of the former bankrupt estate of Ariel San Esteban (the Trustee);

(2) the Registrar of the Court;

(3) Global Financial Group (GFG) Pty Ltd (ACN 073 220 747); and

(4) the State of New South Wales.

(d) the Applicant must pay into Court any surplus arising from the sale of the Property (if any).

1. In the absence of any interlocutory application being filed in the proceedings within 28 days after the account provided for in Order 2(c) is provided, the Originating Application is otherwise dismissed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 1375 of 2014 |

BETWEEN: | NATIONAL AUSTRALIA BANK LIMITED (ABN 12 004 044 937) Applicant |

AND: | THE STATE OF NEW SOUTH WALES First Respondent GLOBAL FINANCIAL GROUP (GFG) PTY LTD (ACN 073 220 747) Second Respondent |

JUDGE: | FLICK J |

DATE: | 1 APRIL 2015 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 Presently before the Court is an Application made by National Australia Bank Limited (“the Bank”) pursuant to s 133(9) of the Bankruptcy Act 1966 (Cth) (the “Bankruptcy Act”). The application seeks an order that a parcel of land in respect to which the Bank is a mortgagee be sold and thereafter an account be given of the proceeds of the sale and that any surplus of monies be paid into Court.

2 The land in question is a parcel of land at St Clair, a suburb of Sydney. The Bank was granted a mortgage over that land in 2005 by Mr San Esteban. In 2007 a caveat was lodged on the property by Global Financial Group Pty Ltd. Curiously enough, that entity apparently claimed an interest in the land which arose under a personal loan agreement. But nothing turns on that. Mr San Esteban was made bankrupt in March 2008. He was discharged from his bankruptcy in March 2011 pursuant to s 149 of the Bankruptcy Act.

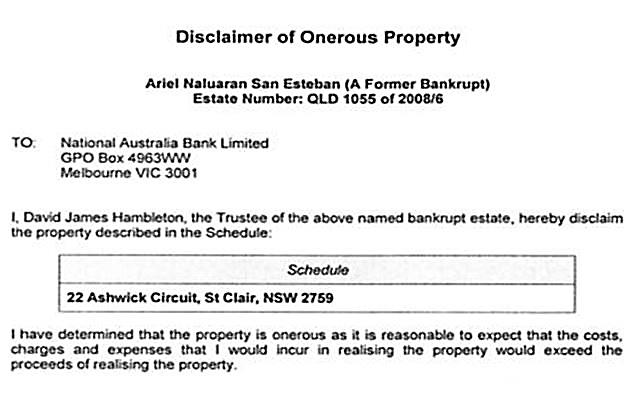

3 In January 2014 the trustee gave the Bank notice of its disclaimer of the land as “onerous property” pursuant to s 133(1) of the Bankruptcy Act. The form of notice was relevantly as follows:

4 As at December 2014 the total indebtedness to the Bank was about $350,000; the land was valued at $440,000. A more recent statement of the indebtedness to the Bank indicates a total indebtedness of about $340,000. Although the quantum of the claim made by Global Financial Group Pty Ltd remains unspecified, the trustee as at February 2014 was of the view that the amount owing “extinguished any prospect of equity on the property…”. If that be correct, the prospect of any surplus monies being paid into Court remains remote.

5 The Respondents to the Application are the State of New South Wales and Global Financial Group Pty Ltd, the State being a party upon the basis that the disclaimer operates to vest the title in the land in it. Both Respondents have filed a submitting notice. Mr San Esteban has also been notified of the hearing of the Application but has indicated that he did not wish to attend.

6 Subject to some minor revisions, the orders as sought by the Bank should be made.

Section 133

7 Section 133 provides in relevant part as follows:

Disclaimer of onerous property

(1AA) Where any part of the property of the bankrupt consists of:

(a) land of any tenure burdened with onerous covenants; or

(b) property (including land) that is unsaleable or is not readily saleable;

subsection (1) applies.

…

(1) Subject to this section, the trustee may, notwithstanding that he or she has endeavoured to sell or has taken possession of the property or exercised any act of ownership in relation to it and notwithstanding, in the case of property the transfer of which is required by a law of the Commonwealth or of a State or Territory of the Commonwealth to be registered, that he or she has not become the registered owner of that property, by writing signed by him or her, at any time disclaim the property.

…

(2) A disclaimer under subsection (1) or (1A) operates to determine forthwith the rights, interests and liabilities of the bankrupt and his or her property in or in respect of the property disclaimed, and discharges the trustee from all personal liability in respect of the property disclaimed as from the date when the property vested in him or her, but does not, except so far as is necessary for the purpose of releasing the bankrupt and his or her property and the trustee from liability, affect the rights or liabilities of any other person.

…

(9) The Court may, on application by a person either claiming an interest in, or being under a liability not discharged by this Act in respect of, disclaimed property, and after hearing such persons as it thinks fit, make an order, on such terms as the Court considers just and equitable, for the vesting of the property in, or delivery of the property to, a person entitled to it or a person in whom, or to whom, it seems to the Court to be just and equitable that it should be vested or delivered, or a trustee for that person.

(10) Subject to subsection (11), where an order vesting property in a person is made under subsection (9), the property to which it relates vests forthwith in the person named in the order for that purpose without any conveyance, transfer or assignment.

(11) Where:

(a) the property to which such an order relates is property the transfer of which is required by a law of the Commonwealth or of a State or Territory of the Commonwealth to be registered; and

(b) that law enables the registration of such an order;

the property, notwithstanding that it vests in equity in the person named in the order, does not vest in that person at law until the requirements of that law have been complied with.

The phrase “the property of the bankrupt” is defined in s 5.

8 Section 133(1), it will be noticed, was the power invoked by the trustee to “disclaim” the land. Section 133(9) is the power now sought to be invoked by the Bank. The section has its origins in s 23 of the Bankruptcy Act 1869 (UK): Hunter M, Graham D, and Crystal M, The Law and Practice in Bankruptcy (19th ed, Stevens & Sons, 1979) p 385.

The effect of a disclaimer of land

9 Section 133, however, is not a section without difficulty. It presents at least two difficulties.

10 First, there is an uneasy tension apparent in s 133(2). That subsection provides on the one hand that:

a disclaimer will operate “to determine forthwith the rights, interests and liabilities of the bankrupt”

and, on the other hand provides that:

a disclaimer will not “affect the rights or liabilities of any other person”.

The Courts, however, “have not been troubled by this anomaly”: National Australia Bank Ltd v New South Wales [2014] FCA 298 at [8] per Perram J.

11 When considering the comparable terms of s 296(2) of the Companies Act 1961 (NSW) Needham J in Re Tulloch Ltd (in liquidation) (1978) 3 ACLR 808 at 813 observed that it was “not easy to give an entirely satisfactory meaning to s 296(2)”. His Honour nevertheless concluded that the rights of a mortgagee continued notwithstanding the disclaimer of property. In so concluding, his Honour observed:

The next question is what remains to the mortgagee. It was submitted on behalf of AGC that, upon disclaimer, contractual and statutory rights vested in the mortgagee disappeared. This submission was supported by counsel for the Crown. It is not easy to give an entirely satisfactory meaning to s 296(2). In order to release “the company and the property of the company from liability” it is certainly necessary to hold that the contractual provisions of the mortgage cease to apply. The words “property of the company” in that phrase, I think, refer to the property of the company other than that disclaimed. There can remain no personal covenant and, as the Crown would take not as a successor to the company but by operation of law, the various provisions of the mortgage would not apply to it. There being no obligation on the company to comply with the contractual covenants, there could be, it would seem, no default in complying with them which would permit the mortgagee to exercise its powers, eg, of sale. Where, however, the default already exists, it would follow, in my opinion, that the right to sell vested in the mortgagee is one of the rights not affected by the disclaimer by virtue of s 296(2).

The same conclusion has been reached in respect to s 133(2) of the Bankruptcy Act: Rams Mortgage Corporation Ltd v Skipworth (No 2) [2007] WASC 75, (2007) 210 FLR 11 at 15. Heenan J there similarly concluded:

[11] … Nevertheless, it is clear from the language of the relevant statutory provisions (eg s 133(2) of the Bankruptcy Act) that certain rights and liabilities of other persons continue to subsist following the disclaimer of land. Despite this apparent theoretical anomaly, the continuation of interests in the land by persons other than the bankrupt has been recognised both by statute and in the cases cited.

There was an appeal from the decision of Heenan J but, by the time of the appeal, “the issues raised in the appeal [were] moot and the appeals [were] without utility”: Rams Mortgage Corporation Ltd v Skipworth [2008] WASCA 148 at [15] per Buss JA (Pullin JA and Murray AJA agreeing).

12 The second difficulty emerging from s 133 in respect to the disclaimer of realty is that upon a disclaimer the land escheats to the Crown. One consequence is that afterwards there remains no personal covenant upon which a mortgagee can take action against the Crown.

13 Notwithstanding the manner in which land reverted to the Crown pursuant to the ancient doctrine of escheat, and notwithstanding some question as to whether land should be regarded as falling to the Crown in the right of the Commonwealth and not the State of New South Wales, it has been concluded that the operation of s 139(9) is such that Torrens title land which has been disclaimed may be vested in a mortgagee: National Australia Bank Ltd v New South Wales [2009] FCA 1066, (2009) 182 FCR 52. Rares J there also exhaustively reviewed the authorities, including the authorities on the doctrine of escheat, and concluded:

[29] … I am of opinion that the land should be vested under s 133(9) in the bank for the purpose for which it originally was mortgaged, namely to secure payment to the bank of all principal, interest and other moneys due to it notwithstanding the effect of the disclaimer. If, after a sale, there is a shortfall the bank will be able to prove for it as an unsecured creditor in the bankrupts’ estate.

Heenan J made similar observations in Rams Mortgage Corporation Ltd v Skipworth (No 2) [2007] WASC 75, (2007) 210 FLR 11 at 15. Observations as to whether Torrens title land in New South Wales could revert to anyone other than the grantor of the land, namely the State, may presently be left to one side. See also: Re Woo; National Australian Bank Ltd v Leroy [2003] FCA 862 at [5] to [7] per Madgwick J; Westpac Banking Corporation v State of New South Wales [2014] FCA 1368 at [19] to [20] per Robertson J. In National Australia Bank Ltd v Victoria [2010] FCA 1230 at [12], (2010) 118 ALD 527 at 530 Bennett J also concluded that “there is no restriction to the meaning of ‘a person claiming an interest’ within s 133(9) to preclude its application to a mortgagee of land held under the Torrens system”. Her Honour there further observed that land “does not escheat absolutely to the Crown such as to preclude the court’s ability to make an order vesting the title in someone else pursuant to s 133(9)”: [2010] FCA 1230 at [15], (2010) 118 ALD 527 at 531.

14 Further to the reasoning of both Heenan J in Rams Mortgage and Rares J in National Australia Bank, it may be noted that s 133 applies to both realty and personal property. Although it may reasonably be expected that realty will in many cases be the “property” that is sought to be “disclaimed”, the section applies to both forms of property. A statutory licence may, accordingly, be the “property” which is sought to be disclaimed: cf. In re Celtic Extraction Ltd (in liquidation) [2001] 1 Ch 475. It would be a curious result if the interests of a security holder in “property” were to have a different “interest” for the purposes of s 133(9) depending upon the form of “property” being “disclaimed” simply by reasons of a doctrine almost having no continuing significance in Australian law. But it may be that personal property which is “disclaimed” also “vests in the Crown … as bona vacantia”: cf. Menzies v Paccar Financial Pty Ltd (No 4) [2014] NSWCA 210 at [101], (2014) 101 ACSR 25 at 44 per Emmett and Leeming JJA and Sackville AJA.

CONCLUSIONS

15 Real estate formerly held by Mr San Esteban was mortgaged in the Bank in 2005. Following the bankruptcy of Mr San Esteban, that property became vested in his trustee. There it remained, notwithstanding the fact that Mr San Esteban was discharged from his bankruptcy in March 2011.

16 The trustee has disclaimed his interest in that property pursuant to s 133(1) of the Bankruptcy Act. The manner in which the trustee did so was by a notice which complied with r 6.10 of the Bankruptcy Regulations 1996 (Cth). The trustee formed the view that the land was “burdened with onerous covenants” for the purposes of s 133(1AA)(a). The rather cumbersome way in which this was expressed in the Disclaimer of Onerous Property as a determination “that the property is onerous” assumes no significance: cf. National Australia Bank Ltd v State of South Australia (No 2) [2015] FCA 240 at [20] per Griffiths J. The land was in fact “burdened with onerous covenants” for the purposes of s 133(1AA)(a), namely the Bank’s mortgage and the caveat lodged by Global Financial Group Pty Ltd.

17 There is no reason to question the analysis by Rares J as to the operation of s 133 in National Australia Bank or the appropriateness of the orders there made.

18 For the purposes of s 133(9), it is concluded that:

an “application has been made by a person … claiming an interest in [the] disclaimed property”, namely the Bank;

all other persons who may wish to have been heard in respect to the Bank’s Application – namely Global Financial Group Pty Ltd, the trustee, the State of New South Wales and Mr San Esteban – have been notified of the hearing and have indicated that they do not wish to be heard; and

upon the imposition of the “terms” substantially as proposed by the Bank, it is “just and equitable” for an order to be made vesting the property in the Bank.

The form of orders sought by the Bank were understood to have been modelled upon those made by Rares J in National Australia Bank and followed in subsequent decisions of this Court. That form of orders has only been varied in the present proceeding such that:

the Bank should also provide an account of the proceeds of payments and receipts upon the sale of the property to the State of New South Wales – in the event of there being any surplus of monies available, all persons having a potential interest in their distribution will accordingly be placed on notice; and

the Application made by the Bank should be otherwise dismissed – but only after an account has been provided and an opportunity extended to interested persons to make any such application to the Court as they may see fit.

It is not considered necessary to:

vary the form of Order 1 to ensure that any secured creditor having an interest in the land (and having priority to the Bank) was in fact paid in priority to the Bank being paid. The form of the mortgage itself expressly provides, not surprisingly, for the payment of monies “to anyone with a prior claim”. Any outstanding rates payable upon the property, it was thus accepted by way of example, were to be paid in priority to any payment to the Bank; or

include any express order as to the costs of the present proceeding – the form of mortgage being expressed in sufficiently broad terms to ensure that the Bank’s legal fees were otherwise recoverable under the mortgage itself.

An order should be made upon terms pursuant to s 133(9) of the Bankruptcy Act vesting the legal title in the Bank so that it may sell the property and receive payment of the monies secured by the mortgage.

THE ORDERS OF THE COURT ARE:

1. Pursuant to s 133(9) of the Bankruptcy Act 1966 (Cth), the whole of the land comprised in Certificate of Title, Folio Identifier 307/808666 and known as 22 Ashwick Circuit, St Clair in the State of New South Wales (the Property), vest in the Applicant, subject to the conditions in Order 2 below.

2. Pursuant to s 133(9) of the Bankruptcy Act 1966 (Cth), upon the vesting of the Property in the Applicant:

(e) the Applicant may only deal with the Property pursuant to its powers as mortgagee under the Real Property Act 1900 (NSW) and under its mortgage over the Property dated 31 January 2005, bearing registered number AB331115 (the Mortgage);

(f) the Applicant be entitled to calculate the amount secured by the Mortgage as including all moneys that would have been secured by the Mortgage had the trustee of the former bankrupt estate of Ariel San Esteban not disclaimed the Property, and to deduct and retain for its own absolute use and property such amount from any proceeds of sale of the Property as if it were money secured by the Mortgage (including all costs properly incurred in selling, and incidental to the sale of, the Property);

(g) the Applicant must, within 14 days after settlement of any sale of the Property, provide an account of its payments and receipts to:

(1) David James Hambleton as trustee of the former bankrupt estate of Ariel San Esteban (the Trustee);

(2) the Registrar of the Court;

(3) Global Financial Group (GFG) Pty Ltd (ACN 073 220 747); and

(4) the State of New South Wales.

(h) the Applicant must pay into Court any surplus arising from the sale of the Property (if any).

1. In the absence of any interlocutory application being filed in the proceedings within 28 days after the account provided for in Order 2(c) is provided, the Originating Application is otherwise dismissed.

I certify that the preceding eighteen (18) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Flick. |