Hua Wang Bank Berhad v Commissioner of Taxation [2014] FCA 1392

FEDERAL COURT OF AUSTRALIA

Hua Wang Bank Berhad v Commissioner of Taxation [2014] FCA 1392

CORRIGENDUM

1 The last two sentences in paragraph [116] should be removed and the paragraph read as follows:

‘116 It is more than passing strange that Mr Gould should be looking after Mr Borgas' travel arrangements. The inference I draw is that the litigation was being conducted by Mr Gould for Mr Gould and Mr Borgas' role was to turn up when requested. Although Mr Borgas claimed that he was the ultimate source of instructions for the taxpayer there is no prospect that this could be true.’

I certify that the preceding one (1) numbered paragraph is a true copy of the Corrigendum to the Reasons for Judgment herein of the Honourable Justice Perram. |

Associate:

Dated: 10 March 2015

IN THE FEDERAL COURT OF AUSTRALIA | |

Applicant | |

AND: | Respondent |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

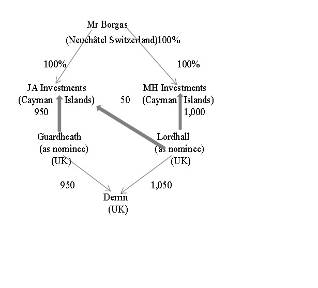

GENERAL DIVISION | NSD 652 of 2011 |

BETWEEN: | BYWATER INVESTMENTS LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 654 of 2011 |

BETWEEN: | CHEMICAL TRUSTEE LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 655 of 2011 |

BETWEEN: | SOUTHGATE INVESTMENT FUNDS LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 656 of 2011 |

BETWEEN: | DERRIN BROTHERS PROPERTIES LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | VID 672 of 2010 |

BETWEEN: | DEPUTY COMMISSIONER OF TAXATION Applicant |

AND: | HUA WANG BANK BERHAD Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | VID 887 of 2010 |

BETWEEN: | DEPUTY COMMISSIONER OF TAXATION Applicant |

AND: | CHEMICAL TRUSTEE LIMITED First Respondent DERRIN BROTHERS PROPERTIES LIMITED Second Respondent BYWATER INVESTMENTS LIMITED Third Respondent |

JUDGE: | PERRAM J |

DATE OF ORDER: | 19 december 2014 |

WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The parties provide, by way of email to chambers, proposed short minutes of order to give effect to these reasons on or before 7 January 2015.

2. The matter be listed for directions on 2 February 2015 at 9:30 am.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 653 of 2011 |

BETWEEN: | HUA WANG BANK BERHAD Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 652 of 2011 |

BETWEEN: | BYWATER INVESTMENTS LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 654 of 2011 |

BETWEEN: | CHEMICAL TRUSTEE LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 655 of 2011 |

BETWEEN: | SOUTHGATE INVESTMENT FUNDS LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 656 of 2011 |

BETWEEN: | DERRIN BROTHERS PROPERTIES LIMITED Applicant |

AND: | COMMISSIONER OF TAXATION Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | VID 672 of 2010 |

BETWEEN: | DEPUTY COMMISSIONER OF TAXATION Applicant |

AND: | HUA WANG BANK BERHAD Respondent |

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | VID 887 of 2010 |

BETWEEN: | DEPUTY COMMISSIONER OF TAXATION Applicant |

AND: | CHEMICAL TRUSTEE LIMITED First Respondent DERRIN BROTHERS PROPERTIES LIMITED Second Respondent BYWATER INVESTMENTS LIMITED Third Respondent |

JUDGE: | PERRAM J |

DATE: | 19 december 2014 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1. Introduction | [1] |

2. Central Provisions and the Facts about the Location of the Taxpayers’ Businesses | [5] |

(a) The relevant provisions | [5] |

(b) Basic facts about each taxpayer | [9] |

Chemical Trustee Limited | [9] |

Derrin Brothers Properties Limited | [19] |

Bywater Investments Limited | [27] |

Southgate Investment Funds Limited | [35] |

Hua Wang Bank Berhad | [45] |

3. The Boundaries of the Location Debate | [56] |

(a) Chemical Trustee, Derrin and Bywater – common issues | [61] |

The corroborative witnesses | [118] |

Global effect of the corroborative evidence | [143] |

(b) Chemical Trustee Limited | [144] |

The Commissioner’s 18 matters | [145] |

(i) Mr Gould’s beneficial ownership of Chemical Trustee | [145] |

(ii) The loans were all to entities associated with Mr Gould | [153] |

(iii) Loans to Gould/Leaver related entities via Normandy UK | [162] |

(iv) Loans via Indo-Suez/JA Investments | [191] |

(v) Outright Transfers to Indo-Suez | [200] |

(vi) Transfers from Chemical Trustee to City and Westminster | [207] |

(vii) Chemical Trustee’s investments in Vita Life Sciences Ltd via Lloyds & Casanove | [212] |

(viii) Chemical Trustee’s investment in Mitre Focus through Lloyds & Casanove | [217] |

(ix) Transfers from Mr Gould to his charitable interests | [220] |

(x) Chemical Trustee’s share investments for the benefit of Mr Gould | [226] |

(xi) Explicit investment instructions from Mr Gould about Chemical Trustee | [238] |

(xii) Mr Gould micromanaged Chemical Trustee’s reporting and banking | [276] |

(xiii) Anglore’s invoicing of Chemical Trustee | [285] |

(xiv) Mr Gould’s involvement in ASX compliance by Chemical Trustee | [290] |

(xv) Chemical Trustee’s investments through Perkasa Normandy Malaysia | [294] |

(xvi) Chemical Trustee’s borrowings from the Bank of Commerce (Micronesia) | [295] |

(xvii) Funds transfers between Chemical Trustee and the Hua Wang Bank | [307] |

(xviii) Meetings of directors and shareholders of Chemical Trustee | [308] |

Conclusions on Chemical Trustee | [310] |

(c) The position of Derrin Brothers Properties Ltd | [315] |

(i) Mr Gould’s beneficial ownership of Derrin Brothers | [318] |

(ii) Loans made by Derrin were for the benefit of entities associated with Mr Gould | [321] |

(iii) Other transactions associated with Mr Gould | [323] |

Hua Wang Bank | [323] |

Tifu Pty Ltd | [324] |

Indo-Suez | [326] |

(iv) The Dubai Property | [327] |

(v) Mr Gould’s checking of financial statements and involvement in the banking of Derrin Brothers | [333] |

(vi) Directors’ and shareholders’ meetings | [338] |

(vii) Conclusion | [339] |

(d) Bywater Investments Limited | [340] |

(e) Hua Wang Bank Berhad | [344] |

(f) Southgate Investment Funds Limited | [366] |

4. Central Management and Control | [386] |

5. Double Taxation Issues | [421] |

(a) United Kingdom after 2004 | [421] |

(b) United Kingdom prior to and including the 2004 year | [431] |

(c) Switzerland | [433] |

6. The Capital/Revenue Distinction | [441] |

7. Capital or Revenue Account? | [445] |

8. Trading Stock Issue | [457] |

9. Nominee Transactions | [464] |

(a) Hua Wang Bank – Sunland shares | [465] |

(b) Hua Wang Bank – Cyclopharm shares | [469] |

(c) Bywater – Russell Associates | [475] |

10. Chemical Trustee – Penalties | [478] |

11. The Charging Orders | [481] |

12. Miscellaneous Matters | [483] |

13. Conclusions | [484] |

1 This case concerns taxation appeals from decisions of the Commissioner of Taxation disallowing five taxpayers’ objections to a number of assessments issued by him. The taxpayers, the relevant income years in dispute and the combined amount of tax in dispute in this Court are as follows:

Taxpayer | Financial Year | Amount |

Chemical Trustee Ltd | 2001, 2003-2004, 2006-2007 | $1,750,439.82 |

Derrin Brothers Properties Ltd | 2003-2005 | $3,500,294.10 |

Bywater Investments Ltd | 2002-2007 | $5,239,294.00 |

Hua Wang Bank Berhad | 2004, 2006-2007 | $2,629,907.92 |

Southgate Investment Funds Ltd | 2000-2002, 2006-2007 | $1,144,982.69 $14,264,918.53 |

2 In addition to these primary tax liabilities each of the taxpayers has been levied a substantial amount in penalties and the general interest charge. Part of the case in this Court concerns a penalty of $21,794.30 imposed on Chemical Trustee. All of the penalties imposed on the other taxpayers are not in dispute in this Court although appeals from them are pending in the Administrative Appeals Tribunal (‘the Tribunal’).

3 Each of the taxpayers made profits on the acquisition and sale of securities in entities listed on the Australian Stock Exchange (‘the ASX’) which the Commissioner has treated as income and exigible to income tax. There are eight sets of issues between the parties:

(a) The central management and control issue. The Commissioner contends that each of the taxpayers had its place of central management and control in Australia from where he alleges that they were completely controlled by Mr Vanda Gould, an accountant. If this contention be made good, the Commissioner submits that this will entail that each of the taxpayers was an Australian resident: Income Tax Assessment Act 1936 (Cth) (‘ITAA 1936’), s 6(1). In turn, this will render each of the taxpayers liable to income tax on all sources of income whether inside Australia or outside it: Income Tax Assessment Act 1997 (Cth) (‘ITAA 1997’), ss 6-5(2), 995-1(1). Each of the taxpayers says that its place of central management and control was in various overseas locations (Apia in Samoa, London or Neuchâtel in Switzerland) because, summarising it somewhat loosely, this is where their directors met or where the actual decisions about the share transactions in question were made. The Commissioner, by contrast, submits these structures are entirely formal and that, in truth, it was Mr Gould who was pulling all of the strings from Sydney. The taxpayers deny this but say, in any event, that it does not matter because the issue is to be decided by reference to where the decisions of the taxpayers, as a matter of formality, were made. They deny nevertheless Mr Gould’s role as a decision-maker, instead characterising him as an advisor to the taxpayers.

(b) The double taxation issue. In the event that the taxpayers were found to be Australian residents for the purposes of Australian law then each taxpayer, apart from Hua Wang Bank, submitted that they were also resident in the United Kingdom or Switzerland. If this were accepted this then raised an issue as to whether they were entitled to invoke any of three double taxation treaties between Australia and those nations. Under the terms of those treaties they will be entitled to relief from Australian taxation if, in the case of two of the treaties, they had their ‘place of effective management’ in either jurisdiction. In the case of the third, the test is where they are ‘managed and controlled’. In effect, a similar, although not identical, debate would then ensue as had occurred under the rubric of the central management and control issue.

(c) The capital/revenue issue. The Commissioner submitted that the share trading which had taken place was on the taxpayers’ revenue accounts. The taxpayers submitted that the shares in question were purchased as ‘growth’ stocks, that is to say, with the view to making profits from growth in the value of the underlying company rather than through gains from cyclical fluctuations in the price of the shares. This then formed the foundation for an argument that the profits had been made on capital account. Ordinarily, this issue might have been academic given the existence of a capital gains tax. The taxpayers involved, however, claimed that they were foreign residents and entitled to an exemption unless the shares in question had a connexion with Australia. The Commissioner denied the former and asserted the latter.

(d) The trading stock issue. If the previous issue were decided against them and it was held that the gains made on the sale of the shares were on revenue account, the taxpayers then submitted that the shares should be treated as trading stock, being assets held for purposes of ‘manufacture, sale or exchange in the ordinary course of a business’: ITAA 1997, s 70-10(a). If so they were entitled to make trading stock elections.

(e) The penalties issue. The Commissioner imposed a 75% penalty on Chemical Trustee on the basis that it had failed to lodge a return by the due date and that the return had been necessary for the accurate determination of its tax position: Taxation Administration Act 1953 (Cth) (‘TAA 1953’) Sch 1 s 284-75(3). Chemical Trustee denied that this provision applied where it had taken the position of not filing its return on the basis of a reasonable belief that it was not an Australian resident for tax purposes. It also submitted that the Commissioner could have assessed its income from other sources apart from its returns and that this also made the provision inapplicable. Although the Commissioner applied other penalties to each of the taxpayers these penalties are not the subject of the current proceedings (although, as already noted, appeals are pending in relation to them before the Tribunal).

(f) The nominee issues. Hua Wang Bank and Bywater denied that they were beneficially entitled to the shares the subject of the trading activity in question and submitted that any profits which had been made were not theirs and hence not exigible to income tax in their hands.

(g) The charging orders. Early in the proceedings, the Deputy Commissioner obtained summary judgment against the taxpayers on the basis of the uncontestable nature of the notices of assessment he had issued. He then sought to enforce these judgments against Hua Wang Bank and Bywater, and, in particular, certain of their shareholdings. These two taxpayers then contended that they did not beneficially own these shares and that the Court should not make charging orders against the shares. This raised essentially the same as question (f).

(h) Miscellaneous issues. There were a number of miscellaneous matters about which the parties made no submissions but which seem to be open on the parties’ statements of issues.

4 I deal with these issues in turn.

2. Central Provisions and the Facts about the Location of the Taxpayers’ Businesses

5 The basic statutory issues are generated by ITAA 1997, s 6-5(2) which provides:

‘6‑5 Income according to ordinary concepts (ordinary income)

…

(2) If you are an Australian resident, your assessable income includes the *ordinary income you *derived directly or indirectly from all sources, whether in or out of Australia, during the income year.

…’

6 An ‘Australian resident’ is defined in ITAA 1997 s 995-1(1) to have the same meaning it bears in the ITAA 1936. Section 6(1) of the ITAA 1936 provides relevantly:

…

(1) In this Act, unless the contrary intention appears:

resident or resident of Australia means:

…

(b) a company which is incorporated in Australia, or which, not being incorporated in Australia, carries on business in Australia, and has either its central management and control in Australia, or its voting power controlled by shareholders who are residents of Australia.’

(emphasis added)

7 Before turning to what this requires it is necessary to find some facts. The facts in this case are, unfortunately, quite complex. In a global sense there are two levels. The first consists of the facts which the taxpayers allege represent the true position. The second consists of additional matters which the Commissioner submits justify the conclusion that the structures are an elaborate façade to conceal the nature of Mr Gould’s dominion over them. Largely, it is easier to approach the second level only once the first has been mastered. I therefore propose to examine, in the first instance, the taxpayers’ version of events. In doing so, I will leave out of account – in the main – the Commissioner’s criticisms of this material. In short, I give first an account of the outer surface of what the Commissioner alleges is a façade, postponing for now an assessment of whether that is its true nature.

8 The positions of the taxpayers are not identical and they each require separate treatment.

(b) Basic facts about each taxpayer

9 Chemical Trustee was incorporated in the United Kingdom originally under the name Raybell Properties Limited. It was renamed Susally Properties Limited in 1962. It acquired its present name in 1996. As at 28 March 1996, Chemical Trustee had on issue 4,152 shares which were held in the name of Guardheath Securities Ltd (‘Guardheath’). Guardheath is a company owned by the partners of a London firm of accountants, Lubbock Fine. There is no evidence of any subsequent change in this capital structure and I find that in the relevant income years (being 2001-2007) Guardheath was the owner of the whole of the share capital of Chemical Trustee.

10 Guardheath holds the shares in Chemical Trustee as nominee for JA Investments Ltd (‘JA Investments’). JA Investments is incorporated in the Cayman Islands. Chemical Trustee’s abbreviated accounts for the income years 1999 to 2005 record that its ultimate parent is JA Investments. I return to the topic of JA Investments in more detail below. It will suffice for present purposes to say that the records for JA Investments show that it has only one shareholder, Mr Peter Martin Borgas.

11 Consistently with Mr Borgas’ shareholding, the directors of Chemical Trustee have at all times relevant to this litigation been Mr Borgas, his wife Mrs Winny Borgas and their son, Mr Timothy Borgas. The minutes of the meetings of the board of Chemical Trustee record that all of its meetings during the relevant years were held in Neuchâtel, a town in Switzerland in the French speaking canton of the same name, and were attended by Mr Borgas and his wife.

12 In the income years 2001-2007 Chemical Trustee bought and sold a large number of shares on the ASX. In all but the 2005 year it made substantial profits by doing so. The details of the share transactions involved appear at Appendix A to the Commissioner’s appeal statement. The detail of the particular transactions is of little moment for present purposes. All that matters is that substantial profits were made. At issue is the tax treatment of those profits.

13 Mr Borgas gave evidence before me. He testified that he made all the commercial judgments on behalf of Chemical Trustee and that he exercised his powers as an appointed director to decide upon all of its transactions and that he did this in Neuchâtel. This evidence forms the mainspring for Chemical Trustee’s primary argument that its place of central management and control was Neuchâtel.

14 The Commissioner’s submission is that this evidence was false and that Mr Borgas did nothing but act as Mr Gould’s cipher making no decisions about any of the taxpayer’s affairs and taking his instructions entirely from Mr Gould. Chemical Trustee’s somewhat convoluted ownership structure (involving as it did apparently unnecessary layers of complexity in London and the Cayman Islands) was, on this view, to be seen as material designed to obscure Mr Gould’s role.

15 The assessment of that submission requires the traversing of a large amount of material mostly of a documentary nature but also involving corroborative testimony called by the taxpayers from a number of witnesses.

16 Chemical Trustee’s position has always been that it was not an Australian resident for tax purposes and on that basis it did not file any income tax returns for the financial years 2001-2007. On 12 August 2010, the Commissioner issued assessments (and in one case, subsequently, an amended assessment) in which he assessed Chemical Trustee as having taxable income over those years of $6,186,526 on which was due $1,859,376.52 in income tax. On top of this he levied in each year a 75% administrative penalty pursuant to s 284-75(3) of Schedule 1 to the TAA 1953 for failing to lodge a return and thus requiring the Commissioner to assess its income himself. In every year except the first, i.e., 2001, he levied a further administrative penalty of 20% on the basis that it had been liable to pay a penalty in the preceding year.

17 The assessments were as follows:

Year ended 30 June | Taxable income | Tax Payable | Penalty |

2001 | $85,468 | $29,059.12 | $21,794.30 |

2002 | $435,770 | $130,731.00 | $117,657.90 |

2003 | $553,912 | $166,173.60 | $149,556.20 |

2004 | $287,488 | $86,246.40 | $77,621.75 |

2006 | $1,044,884 | $313,465.20 | $282,118.65 |

2007 | $3,779,004 | $1,133,701.20 | $1,020,331.05 |

Total | $6,186,526 | $1,859,376.52 | $1,669,074.85 |

18 Chemical Trustee has paid all of these assessments. It objected to them on 13 September 2010 and the Commissioner disallowed those objections on 30 March 2011. It is from those objection decisions that Chemical Trustee now appeals to this Court, apart from the decisions relating to the primary tax liability for the year ended 2002, and the penalties for all years apart from 2001, which are all subject to review in the Tribunal.

Derrin Brothers Properties Limited

19 I turn then to the position of Derrin Brothers. It was incorporated in the United Kingdom on 19 May 1959 under the name Garrett Properties Limited. It changed its name to Derrin Brothers Properties Limited on 27 October 1992.

20 The shareholders of Derrin are two United Kingdom companies Guardheath (mentioned above as the shareholder in Chemical Trustee) and another Lubbock Fine entity, Lordhall Securities Limited (‘Lordhall’). At all times, Guardheath has held its shares as nominee for JA Investments, the same Cayman Islands company which holds all of the shares in Chemical Trustee and which, according to the taxpayers, is controlled by Mr Borgas.

21 Lordhall holds 50 of its 1,050 shares in Derrin as nominee for JA Investments. It holds the remaining 1,000 for another Cayman Islands entity, MH Investments Limited (‘MH Investments’). MH Investments was incorporated in the Cayman Islands on 5 January 1994. The sole shareholder in MH Investments was previously Offshore Nominees Limited, another company incorporated in the Cayman Islands. Since 2012 the sole shareholder of MH Investments has also been Mr Borgas. The present structure of Derrin Brothers is, therefore, as follows:

22 This is an example of what will be many exotic shareholding arrangements in this litigation.

23 The directors of Derrin were, once again, Mr Borgas and his wife although, on this occasion, not their son. The secretary was a company called M & N Secretaries Limited. United Kingdom law permitted, until 2008, a company to have directors who were other companies. From 1 October 2008, that law was changed to require there to be at least one natural person as a director. The minutes of the meetings of directors for Derrin show that, as with Chemical Trustee, all of its meetings took place in Neuchâtel, Switzerland and were attended by Mr and Mrs Borgas.

24 As in the case of Chemical Trustee, Derrin made profits on the purchase and sale of shares listed on the ASX in the 2003, 2004 and 2005 years. The share trades relied upon by the Commissioner appear in Appendix A to his appeal statement. It was not substantially in dispute that the trades had occurred.

25 Derrin, like Chemical Trustee, took the view that it was not an Australian resident for tax purposes and did not, in consequence, file any returns for the years 2003-2005. On the same day that he issued notices of assessment to Chemical Trustee, 12 August 2010, the Commissioner also served notices of assessment on Derrin.

26 These Derrin objected to on 13 September 2010. The Commissioner disallowed these objections on 30 March 2011. Subsequently, he issued amended notices of assessment on 15 June 2011. It is these amended assessments which are in issue in the appeal. They are as follows:

Year ended 30 June | Taxable income | Tax Payable |

2003 | $95,879 | $28,763.40 |

2004 | $6,480,096 | $1,944,028.80 |

2005 | $5,091,673 | $1,527,501.90 |

Total | $11,667,647 | $3,500,294.10 |

27 Bywater was incorporated in the Bahamas on 20 June 1994. It has two shares on issue both of which are held by a company called Anglore S.A.R.L. (‘Anglore’) (‘société à responsibilité limitée’). It is not clear to me where Anglore was incorporated, however, this does not matter. Anglore is an important actor in this case and more will need to be said of it in due course. For present purposes the following will suffice: Anglore is said to be a ‘corporate services business’ based in Neuchâtel. It is the principal vehicle through which Mr Borgas provides, so the parties agree, ‘corporate services’. What are these corporate services? It markets itself as a ‘discrete, low profile fiduciary and administration company’. It offers to provide the service of ‘the incorporation of companies located in many jurisdictions throughout the western world’ and, additionally, the service of ‘the provision of directors and other corporate officers for such companies’. The office holders of Anglore are Mr and Mrs Borgas and a Mr Lonsdale.

28 For reasons which will be presently unclear, but will begin to make sense later in these reasons, Anglore does not hold its shares in Bywater for itself but instead for MH Investments (the same Cayman Islands company referred to above).

29 Returning then to Bywater, it appears to have had three directors, Mr Borgas and his wife and a company known as NTW Directors Inc which has an address in Nassau in the Bahamas. The corporate records for Bywater appear to include only a cashbook which records payments from and receipts into its bank account. Under the law of the Bahamas it was not required to have directors’ meetings or annual general meetings and it has not done so. The cashbook is maintained at the offices of Lubbock Fine in London.

30 In the years 2002-2007, Bywater made profits on the acquisition and sale of shares listed on the ASX. The details of the trading activity alleged by the Commissioner appear at Appendix A to his appeal statement in Bywater’s appeal. As a result of that trading activity the Commissioner came to the view that Bywater had made assessable income in the years 2002-2007. On 12 August 2010 (as in the case of the other taxpayers) the Commissioner issued assessments to Bywater to which it objected on 13 September 2010. The Commissioner upheld Bywater’s objection in part in relation to the 2005 year but otherwise dismissed the objection. As a result Bywater has been assessed to income tax as follows:

Year ended 30 June | Taxable income | Tax Payable |

2002 | $908,615 | $272,585 |

2003 | $653,104 | $195,931 |

2004 | $2,448,560 | $734,568 |

2005 | $7,390,395 | $2,217,119 |

2006 | $3,675,337 | $1,102,601 |

2007 | $2,388,301 | $716,490 |

Total | $17,464,312 | $5,239,294 |

31 It is from the objection decisions resulting in these determinations that Bywater now appeals.

32 For completeness, it should be noted that Bywater has also had imposed upon it administrative penalties. It has sought a separate review of those before the Tribunal. They are not relevant to the present case.

33 For the three taxpayers considered above it is clear that the taxpayers’ case is that they were located for tax purposes (to use a neutral expression intended to encompass all of the relevant tests) either where Mr Borgas and his wife conducted board meetings or Mr Borgas otherwise made decisions or at the offices of Lubbock Fine in London where employees of that firm gave effect to instructions apparently given by Mr Borgas. In all events, it is relatively easy to follow that the basic debate between the parties is as to the respective roles of Mr Borgas and Mr Gould with some additional consideration of the role of Lubbock Fine.

34 In the case of the remaining two taxpayers – Hua Wang Bank Berhad and Southgate Investment Funds Limited – the facts are more complex. Both taxpayers had identifiable directors who were situated outside Australia but their ultimate ownership was not something the taxpayers sought very much to explore. The Commissioner contended in the case of these two taxpayers that the ultimate control was vested in Mr Gould. Another difference between these two taxpayers and the initial three is that these seem to have had a connexion with the South Pacific lacking in the case of Mr Borgas’ companies which, in general, have a Euro-Caribbean flavour. Yet, as events will show, Mr Borgas is not without involvement either. With those introductory words I move then to the position of Southgate Investment Funds Ltd (‘Southgate’).

Southgate Investment Funds Limited

35 Southgate was incorporated under the law of the United Kingdom on 4 August 1998. In the period 2000-2007 it filed tax returns in the United Kingdom reflecting income of a modest nature (i.e. £396.00 in 2007) earned as a nominee company.

36 The shareholders in Southgate are Guardheath and Lordhall which are United Kingdom entities through which the London accountants Lubbock Fine control companies on behalf of their clients and in respect of which mention has already been made. The directors and shareholders of these two entities have at all times been either partners or staff of Lubbock Fine.

37 For whom did the Lubbock Fine entities hold their shares in Southgate? The immediate answer is that they were held on trust for IRSS Nominees (4) Limited. IRSS Nominees (4) Ltd was a Samoan company incorporated as an ‘international company’ under the provisions of the International Companies Act 1987 (Samoa) on 7 April 1994. IRSS Nominees (4) Ltd appears, in turn, to have held its beneficial interest in the shares in Southgate as the trustee of the LJK Nominees Superannuation Fund (Samoa). This fund is an ‘international trust’ registered under the provisions of the International Trusts Act 1987 (Samoa). The members of this fund are the Sydney anaesthetist and investor, Dr Joseph David Ross, and his wife Lucille June Ross.

38 There is no doubt that Southgate’s directors (who were Lubbock Fine entities or personnel) had a written instruction from IRSS Nominees (4) Limited to do as Mr Gould told them. It also instructed them to open an account in Southgate’s name upon which Mr Gould was to be an authorized signatory.

39 Some confusion arose about who the ultimate owners were. For reasons I later give, the situation was this: Mr Gould was providing to some of his clients an arrangement designed to minimise tax using international superannuation funds. Dr Ross was one of the clients who took part. The day-to-day administration of these structures was under the control of Mr Gould.

40 The debate between the parties was not really concerned with the issues of ownership but rather with where Southgate had its place of central management and control. Its directors’ meetings appear to have been held in London at the office of Lubbock Fine. It was not suggested that Mr Borgas had a role in that process. The Commissioner’s contention is that the share trading decisions were made by Mr Gould in Sydney and that Lubbock Fine’s role was ornamental.

41 Under the terms of the trust deed for the LJK Nominees Superannuation Fund, the ‘principal employer’ was said to be LJK Nominees Pty Ltd. The shareholders in LJK Nominees Pty Ltd are Dr Ross and his wife Lucille. The company is also the trustee of the JD Ross Family Trust.

42 During the period 2000-2007 Southgate derived substantial gains and losses by the purchase and sale of shares listed on the ASX. The details of those transactions are set out in Appendix A to the Commissioner’s appeal statement. There is presently no debate about the fact of these trades.

43 On 12 August 2010 the Commissioner issued assessments to Southgate for the years 2000-2002 and 2006-2007 on the basis that the gains made on the share transactions were assessable income. Southgate objected to these on 13 September 2010. The Commissioner disallowed the objections on 30 March 2011 and made adjustments to a number of the assessments by issuing amended assessments on 15 and 16 June 2011. The tax now in dispute is as follows.

Year ended 30 June | Taxable income | Tax Payable |

2000 | $1,567,944 | $564,459.84 |

2001 | $16,800 | $5,712.00 |

2002 | $761,866 | $229,559.80 |

2006 | $602,532 | $180,759.57 |

2007 | $551,639 | $165,491.48 |

Total | $3,500,781 | $1,144,982.69 |

44 Penalties were also imposed and an appeal in respect of them is pending in the Tribunal.

45 I turn then to the Hua Wang Bank Berhad.

46 In the interests of brevity I will call this taxpayer ‘the Bank’. However, as will appear in due course, it is neither a bank in any ordinary sense of the word nor, despite the name ‘Hua Wang’ does it have the slightest connexion to China or Hong Kong. In fact, it is Samoan. It was incorporated on 17 January 1994 in that nation under the terms of its International Companies Act 1987.

47 Since 20 June 1994 there have been 250,000 shares in the Bank on issue. These have been held by Pacific Securities Inc, another international company incorporated in Samoa under the provisions of the International Companies Act 1987. Prior to Pacific Securities becoming the shareholder in the Bank it issued a bearer debenture. The terms of this debenture provided that whilst it was unredeemed the rights of the members of the company to vote or demand a poll were suspended. The ability of the debenture so to provide was sustained by the terms of its articles and by ss 15 and 57 of the International Companies Act 1987. The effect of those rules and such a debenture structure is to place control of a company in the hands of persons other than its members.

48 On 4 March 1998 Pacific Securities resolved to convert the original secured debenture to a registered secured debenture in the following name:

‘J.A. Investments Ltd

c/- Moore Stephens’

“Cayside”

Shedden Road, George Town

PO box 1782, GT

GRAND CAYMAN, CAYMAN ISLANDS’

49 This, of course, was one of Mr Borgas’ companies in the Cayman Islands.

50 Although no direct issue about this arises, it appears that at an earlier time the debenture holder had been a Malaysian company, Perkasa Normandy Holdings which was based in Kuala Lumpur. It was the holding company for the Normandy Malaysia Group whose managing director was Mr Daud Bin Yunus. Mr Yunus testified before me.

51 The register of directors and secretaries for the Bank reveals several individuals over the period 2000 to 2007 and two companies, Westco Directors Ltd and Westco Secretaries Ltd. All the individuals, save one, were persons employed by another entity, Asiaciti Trust Samoa Ltd in Samoa. Asiaciti Trust Samoa Ltd in turn is based in Apia and one of its beneficial owners is Mr Graeme Briggs. Mr Briggs is the group managing director of Asiaciti and, apparently its ‘founder’ as well. Asiaciti is an international trustee and service provider and its services apparently include the provision of international companies, trusts, trustee services and international tax planning. Mr Briggs was the other person named as a director of the Bank. Westco Directors Ltd was a member of the Asiaciti Group. All of the persons authorized to act on its behalf were or had been employees of Asiaciti Trust’s Samoan office.

52 By and large the directors of the Bank met in Apia in Samoa. As I have said, the Bank was not a bank in usual parlance. Instead it was an ‘offshore bank’ under the terms of the Off-Shore Banking Act 1987 (Samoa). It was granted a ‘B’ class licence as such on 20 June 1994 by the then Finance Minister of Western Samoa. At all relevant times it has maintained that licence. Although I will return to this in more detail later, the basic feature of an offshore bank under Samoan law is that none of its customers may be resident in Samoa. As will appear, in due course, the ‘customers’ of the Bank were all clients of Mr Gould.

53 During the income years 2004 and 2006-2007 the Bank made profits on the purchase and sale of shares listed on the ASX. The fact of these transactions is not in dispute. What is in dispute is the issue of whose transactions they actually were and the issue of where the Bank had its place of central management and control. The Bank contends that some of the profits on which the Commissioner sought to impose tax were generated on the sale of shares which it was holding on trust for others. Consequently, those profits were not liable to income tax in its hand. For his part the Commissioner submitted that the Bank had failed to prove this. On the question of central management and control a number of the Bank’s directors were called. I will not attempt to summarise their evidence at this stage other than to observe, neutrally, that none purported to suggest that it was they who were the original authors of the Bank’s management decisions, which it was accepted came from Mr Gould. The Bank submitted that they nevertheless each discharged the office of director in Apia. The Commissioner submitted that they were window dressing.

54 On 12 August 2010 the Commissioner issued assessments to the Bank. Following objections these assessments were varied as follows:

Year ended 30 June | Taxable income | Tax Payable |

2004 | $4,115,073 | $1,234,522.02 |

2006 | $3,621,547 | $1,086,464.10 |

2007 | $1,029,739 | $308,921.80 |

Total | $8,766,359 | $2,629,907.92 |

55 It is from these determinations that the Bank now appeals. The Commissioner has also imposed administrative penalties and an appeal from those is pending before the Tribunal.

3. The Boundaries of the Location Debate

56 It was the Commissioner’s contention that all five taxpayers were conducted by Mr Gould. Whilst considerable effort had been expended in trying to make Chemical Trustee, Derrin and Bywater look as if they were conducted from Neuchâtel or London this was a deception serving only to mask the true role of Mr Gould as the owner and controller of these entities. Evidence given by Mr Borgas and members or employees of Lubbock Fine that it was Mr Borgas who was the owner and who made the relevant decisions was to be rejected.

57 A similar situation obtained in relation to the affairs of the Bank and Southgate. The Commissioner contended that regardless of who owned Southgate, it was Mr Gould who was running it. The interposition of the Lubbock Fine entities was, once again, window dressing to conceal the control of Mr Gould. Insofar as the Bank was concerned the same result applied. The directors provided by Asiaciti in Asia were puppets who did as Mr Gould told them.

58 The Commissioner submitted that the question of central management and control was a factual one and the facts would show overwhelmingly that it was Mr Gould who was running these taxpayers and doing so from Sydney.

59 The taxpayers, for their part, whilst not admitting Mr Gould was the ultimate owner and in control of the taxpayers, did not address any submissions as to why the Commissioner’s submissions on this issue ought not to be accepted. Their principal focus was instead on the idea that the directors of all of the taxpayers, whilst perhaps heavily influenced by Mr Gould, nevertheless still applied their minds to the discharge of their respective offices. This fact, together with a number of other factors such as the place of each taxpayers’ incorporation, meant that the Court should not conclude that they had their place of central management and control in Australia. Support for this view was said to be discernible in, inter alia, the reasons of Gibbs J in Esquire Nominees Limited v Commissioner of Taxation (1973) 129 CLR 177.

60 The question of central management and control is a factual one. For the reasons which follow I am satisfied that the directors of the taxpayers exercised no independent judgment in the discharge of their offices but instead merely carried into effect Mr Gould’s wishes in a mechanical fashion. The taxpayers’ places of central management and control were in Sydney. I turn first to the common issues arising with Chemical Trustee, Bywater and Derrin.

(a) Chemical Trustee, Derrin and Bywater – common issues

61 These taxpayers submitted that no disposition of money or other assets of theirs ever took place without the express authorization of Mr Borgas or some act by him that purported to be on their behalf. They gestured, by way of example, to three sets of activities to make good this general point. These were:

(a) the placing of orders with the stockbroker Bell Potter;

(b) the transmission of signed letters on their letterheads; and

(c) oral instructions given to staff at Lubbock Fine.

62 The testimony of Mr Borgas given in chief provided support for this view. At T1009 he gave this evidence about his role:

‘MS SEIDEN: And where did the idea come for the beneficiary? The idea came from discussions that I have had with – or that I had with Mr Vanda Gould.

Now, you’ve mentioned that Chemical also has some stock market activities? Yes.

All right. Could you explain to the court what your investment criteria is? Yes. Very simply, it is capital growth through long-term investment in the stock in a particular company.

And who makes the decisions for Chemical Trustee about buying and selling shares? I do.

How do you go about making the decision? The – the decision is based on advice that I receive from people such as Mr John Leaver, Mr Vanda Gould, stockbrokers, for example, the late – one – one person in particular who was always very helpful is the late Jamie Saba of Wilson HTM, Ted Cod [sic] of Bell Potter. So I have a – and – and even sometimes suggestions are passed to me by Hasmukh Vara of Lubbock Fine in London, I mean, because they are quite close to the goings on in the stock market, and – but, having – having assembled the basic information – all right, so John Leaver has made a suggestion to Vanda – a recommendation to Vanda which is passed on to me, then I might – I might go back and check, for example, with Jamie Saba, “Have you got any input on this possible investment?” So it’s – the – all right. The recommendations come from those people – people such as those, but the final decision about making the investment is mine.

All right. Once you’ve made a decision about a particular stock, what are the mechanics for executing the transaction? I send a – just imagine – all right. We’re talking about a buy order. I send a fax or email to the broker confirming that we wish to purchase x number of stocks in that company, and – or at your discretion, or – anyway, if prices are mentioned, that will be mentioned. So I send a complete set of instructions to the broker. The broker – and I also send a copy of those instructions to Hasmukh Vara at Lubbock Fine in London. Once the order is completed, and it may not necessarily be completed in one fell swoop, it may be done in different stages, because the price that we’ve indicated may be fluctuating a little bit. Anyway. Once the order has been completed, the broker then sends a contract note to both Hasmukh Vara in London and to me in Neuchâtel. Hasmukh Vara is then responsible for ensuring that the funds that are due for settlement on that particular contract note are paid within the time stipulated on the contract note.

And how does he effect the payment? What’s the mechanics for that? Well, let’s take a company like Chemical Trustee as an example. All right. Chemical Trustee has his bank account, and the authorised signatories on the bank account are myself, plus any two of the equity partners in Lubbock Fine in London. That’s just a purely practical measure. So when the time comes for him to settle, or to – to pay for the shares that have been purchased, he will then prepare the bank account – the bank pages, and, in normal circumstances, will have those signed by two of the equity partners within Lubbock Fine, rather than the papers being transmitted to me in Neuchâtel.

All right? But I – I do stress that I – I do have the power to sign on the account.’

63 Further, the taxpayers submitted that Mr Borgas' testimony was corroborated by the testimony of the following individuals:

(a) Mr Codd, a stockbroker with Bell Potter;

(b) Mr Yunus, an investment portfolio advisor, who also had dealings with Mr Borgas;

(c) Mr Vara, an accountant at Lubbock Fine;

(d) Mr Gibbs, a client advisor at Bell Potter;

(e) Mr Paul Watson, the regional director of a Christian group called Ellel Ministries; and

(f) Mr Lee Facey, the auditor of Chemical Trustee.

64 They also submitted that Mr Borgas’ testimony was corroborated by statements which were made by a deceased man, Mr Jamie Saba, who had been a stockbroker at Wilson HTM. I assess this evidence below at [118] and following. As will be seen, I either do not accept the evidence given by these witnesses or I find that they were deceived by Mr Borgas.

65 The taxpayers also submitted that Mr Borgas’ version was corroborated by a large volume of documentation. There are literally hundreds of these documents but a letter of 23 July 2003 from Chemical Trustee to Lubbock Fine will serve well enough as a general example:

‘Mr. Hasmukh Vara

Messrs. Lubbock Fine

Russel Bedford House

City Forum

250 City Road

London EC1V 2QQ

England

By fax

(original by post)

23rd July 2003

PB/Angl.

Dear Hasmukh,

Re: Chemical Trustee Limited

[instruction already given from fax [initialled] 28/7/03]

Please accept this letter as your authority to advance AUD 1,000,000. – to Lloyds & Casanove Investment Partners Limited for the purposes of acquiring a further AUD 1,000,000. – worth of convertible notes in Vita Life Sciences Limited.

I look forward to hearing from you in the usual way.

Kind Regards

Yours sincerely

[signed]

Peter Borgas, Director

Lubbock doc.5 Word’

66 In general, almost every transaction in which these three taxpayers appear to have engaged is supported by a letter signed by Mr Borgas. Viewed in isolation this material certainly makes it appear that Mr Borgas was making the decisions for them.

67 I am satisfied that Mr Borgas’ evidence about this was false and that the document trail generated by Mr Borgas is false too. All of these taxpayers’ decisions were made by Mr Gould and Mr Borgas’ role was to make it appear that he had transacted the business on their behalf. The documents which have been generated to corroborate Mr Borgas’ evidence are designed to give the impression that Mr Borgas was the decision-maker and that impression is false.

68 But if that be so, why it might be asked would Mr Borgas obey Mr Gould’s instructions when it was Mr Borgas who owned these taxpayers through JA Investments and MH Investments in the Cayman Islands? The answer to this question came early in the trial when documents were tendered which showed that it was Mr Gould who owned JA Investments and MH Investments and that Mr Borgas’ ownership of them was a front.

69 This point, therefore, provides a convenient juncture at which to consider the role of JA Investments more closely. It was incorporated on 28 January 1994 in the Cayman Islands. Initially, it had two members, a Mr Douglas and a Mr Bowring. In May 1997 they ceased to be members and were replaced by Mr Parker. On 11 April 2003 Mr Parker, as the sole member, resolved to replace the existing memorandum and articles of association with a new set.

70 Article 3 then provided:

‘3. The subscribers to the Memorandum of Association and such other persons as are admitted to membership in accordance with these Regulations shall be the members of the Company. No person shall be admitted as a member of the Company unless he is nominated in writing by the Appointor or after the death of the Appointor, his legal personal representatives (and the survivors and survivor of them) at the date of his death but the Appointor shall not be entitled to nominate himself. Every person who wishes to become a member of the company shall deliver to the Company an application for membership in such form as the Directors may require signed by the applicant and accompanied by the requisite nomination, and on receipt of same by the Company the applicant shall be admitted to membership.’

71 And Article 1(b) defined ‘the Appointor’ to be:

‘the person or persons nominated as such by instrument in writing signed by the members and deposited at the Registered Office of the Company’

72 There is no evidence that such a document was ever lodged and there is some evidence that it was not. I will return to this topic below. Three days later on 14 April 2003 Offshore Nominees applied to become a member of JA Investments. Article 3, of course, required a written nomination by ‘the Appointor’. On 14 April 2003, Mr Gould executed a nomination document in these terms:

‘J.A. INVESTMENTS LTD.

(the “Company”)

NOMINATION OF MEMBER

I, MR, VANDA RUSSELL GOULD OF 2 DARLING STREET, CHATSWOOD, NSW, AUSTRALIA being the Appointor under the amended and restated Articles of Association of J.A. INVESTMENTS LTD., HEREBY NOMINATE the undermentioned as a Member of J.A. Investments Ltd. pursuant to Article 3 of the amended and restated Articles of Association of J.A. Investments Ltd.:

Offshore Nominees Ltd.

P.O. Box 1982GT

Grand Cayman

Cayman Islands

Dated this 14th day of April, 2003

[Signed]

Vanda Russell Gould’

73 This suggested that Mr Gould regarded himself as the appointor. Mr Borgas appears to have had the same view. On 21 April 2003 he executed the following document:

‘J. A. INVESTMENTS LTD.

(the “Company”)

Written Resolutions of the Sole Director of the Company adopted

in accordance with the Articles of Association of the Company

APPOINTMENT OF NEW MEMBER

IT WAS RESOLVED that the application for membership duly signed by the authorised signatory of Offshore Nominees Ltd. accompanied by the requisite nomination by the Appointor, pursuant to Article 3 of the Company’s Articles of Association, be accepted and that Offshore Nominees Ltd. be and is hereby appointed as a Member of the Company with immediate effect until such time as he may resign or be removed or otherwise disqualified in accordance with the Articles of Association.

RESIGNATION OF MEMBER

IT WAS RESOLVED that a Letter of Resignation from Jeffrey M. Parker as a Member of the Company dated 14 April 2003 be accepted, such resignation to take immediate effect.

[signed]

Peter Martin Borgas

Dated: 21st April 2003’

74 Mr Borgas signed this as ‘director’. It appears he became the sole director of JA Investments in May 1997. Mr Borgas gave evidence that Mr Gould had been the appointor since 1997. This exchange occurred during his cross-examination by Mr Fagan SC for the Commissioner:

‘MR FAGAN: Well, now going back to article 3 then, which was page 118. Certainly from when you became a director on 22 May 1997, Mr Gould was the appointer for the company, wasn’t he? Yes.

And as long as you have known anything about the company, which is up until to date from whenever you started to have any connection with it, he has always been the appointer, you’ve never known of any other? No.’

75 The Commissioner submitted that I should conclude that Mr Gould had been the appointor since 1997 and that it should be inferred that the articles had earlier contained some provision similar to the version which was put in place in April 2003. The taxpayers submission about this so far as it concerned JA Investments was in these terms:

‘50. It is a matter for this court how many discrete factual findings the court proposes to make about the numerous collateral matters that the Respondent has raised, such as: the ownership of JA Investments and MH Investments, the significance (if any) that Peter Borgas was in the habit of describing inter-company payments as ‘management fees’, and Peter Borgas’s level of knowledge of the internal operations of the Hua Wang Bank. The court may wish to refrain from making findings on these collateral points given that:

(a) Many of the matters canvassed by the Respondent in cross-examination were not particularized by the Respondent prior to the hearing and related to other entities that were connected to the Applicants only tangentially;

(b) Many of these matters have only scant relevance to Central Management and Control, which has always been assessed on an entity-by-entity basis rather than globally; and

(c) Each of Vanda Gould, John Leaver and Peter Borgas are facing criminal charges.’

76 I regret that I must reject the proposition that the question of Mr Borgas’ ownership of JA Investments is a collateral matter. It is central. Turning to the points raised by paragraph 50(a)-(c) as to why the Court ought not to consider these issues, I confess some confusion. I can well understand that a want of particularization, for example, could provide a basis for submitting that a case was not open to be pursued but I did not apprehend that this was what was contemplated in (a). If it was, however, it was clear from the moment the Commissioner sought to tender this material where the case was going. The most extensive objections were advanced as to why the material should not be received. Thereafter, the taxpayer did not contend – nor could they have contended – that it was not open to the Commissioner to seek to prove that Mr Borgas was a puppet. Accordingly, if (a) is an argument that the case is not open, I reject it.

77 As to (b), I do not accept that Mr Borgas’ ownership of JA Investments is of ‘scant’ relevance to the question of central management and control. If Mr Borgas was lying about his ownership of JA Investments this must cast doubt upon the veracity of his evidence that he was making the decisions for Chemical Trustee. Why would he be making decisions in respect of a company which was not his? And why, if he was making these decisions, did he lie about the ownership structure? Observations of that kind well-show that the proposition that this material was of ‘scant relevance’ is, with respect, misconceived and symptomatic of a total divorce from reality which suffused much of the taxpayers’ case.

78 As to (c), the charges have since been dropped. No application was made to me to stay these proceedings whilst the criminal proceedings were on foot. I am not prepared to read (c) as a subtle suggestion that I should do so now. Even if that were wrong, the dropping of the charges would mean that there remained no reason not to proceed.

79 In those circumstances, I conclude that there was a position of Appointor under the articles of JA Investments from 1997 onwards and that person was Mr Gould. Further, I conclude that there was a provision in the form of Article 3 before the new articles were adopted since the existence of the position would make no sense without such an article.

80 The effect of Article 3 was that it was Mr Gould who could control the affairs of JA Investments by appointing additional members. Further, Article 43 provided that the members could remove any director and Article 24 made clear that the members could appoint directors. This structure delivered complete control of JA Investments to Mr Gould, at least as a matter of legal theory.

81 That theoretical capacity was reflected in indisputable reality in the terms of a deed executed by Mr Gould dated 31 August 2005 with Offshore Nominees. Recital A provided that:

‘The Appointer [Mr Gould] has a Company with the name of J.A. Investments Ltd. (hereinafter called “the Company”) to be registered in the name of one or more of the Nominees [Offshore Nominees].’

82 And Recital B provided:

‘[Offshore Nominees] are acting solely as Nominee for [Mr Gould] with respect to the said shares.’

83 These recitals suggested a complete subordination of Offshore Nominees to the will of Mr Gould. Clause 2 conveyed the situation with respect to ownership:

‘[Offshore Nominees] hereby declare[s] that [it] hold[s] the said shares in the Company together with all dividends, bonuses and interests therein of behalf of [Mr Gould] and will deal with the said shares as [Mr Gould] may from time to time direct.’

84 It could not be plainer what the effect of these clauses was. In truth, they merely reflected the inevitable working through of what the powers of Mr Gould were, and always had been since 1997, under the articles.

85 Mr Borgas gave evidence that he was the beneficial owner of JA Investments at T1013:

‘Q: … Just taking JA Investments Ltd for the moment, who is the beneficial owner of JA Investments?

A: I am.’

86 This testimony left Mr Borgas with the challenge of explaining the role of Mr Gould as ‘appointor’ under the articles and, of course, the terms of the deed, which appeared to recognize Mr Gould’s beneficial ownership. His first attempt to do so involved an assertion that it was all to be explained as a question of estate planning. At T1013-1014 he gave this evidence in chief when questioned by Ms Seiden SC, appearing for the taxpayers:

‘Could you explain to the court why there is an appointer? Yes. Because there are companies within – I – I will continue to call them the group companies unless you – you consider that inappropriate – but there are group companies such as Chemical Trustee which hold money for third parties. Now, the appointer: his role is to step in in the event of my death so as to ensure that the parties who are owed money, or have other assets that are held on a nominee basis, receive those assets back in the administration of my estate, and the appointer is responsible for ensuring that nominee assets don’t go with my estate but go back to the party for whom they’re held on a nominee basis.

All right. And who is the appointer? Mr Gould. Vanda Gould.’

87 As the Commissioner pointed out in his written submissions there are at least four reasons why this cannot be correct.

88 First, Article 3 cannot operate this way. It does not deal with the situation of Mr Borgas’ death. If Mr Borgas were to die nothing in the articles of JA Investments imposes any obligation on Mr Gould to ensure that assets held by Mr Borgas on a nominee basis do not pass to his estate.

89 Secondly, Article 3 achieves a dominion over Mr Borgas’ position during his life which is unnecessary for the suggested purpose.

90 Thirdly, if the stated purpose were to be achieved by Mr Borgas under the articles it would make more sense for him to have been the appointor himself under Article 3.

91 Fourthly, Mr Borgas’ version of events is inconsistent with the terms of the deed of 31 August 2005. That deed makes Mr Gould the beneficial owner which is inconsistent with Mr Borgas’ contention that he was the owner.

92 After Mr Borgas gave his evidence on 10 October 2013 he returned the following day to continue his cross-examination. At that time he gave an entirely different account of why he was the beneficial owner. This time he contended that Article 1(b) required the appointor to be appointed in writing and that there was no written instrument appointing Mr Gould as such. Consequently, so Mr Borgas testified, Mr Gould was not the appointor. The cross-examination proceeded this way:

‘MR FAGAN: Well, what is it that you want to say, Sir, about 1[b]? I want to say that I – I know that you have received a whole series of documents from the Cayman Islands. In those documents, was there a document nominating an appointor pursuant to 1[b] for both JA Investments and MH Investments?

Well, I’m not going to answer your question, Sir. I’m just asking you questions and getting answers from you. Now, if all you have to say with respect to 1[b] is to ask me a question, well, that’s the end of it. But you have – you agree that you told us yesterday that from – throughout your involvement with JA and MH, Mr Gould has been the appointor, didn’t you? No. No.

Well, you did tell us that yesterday, didn’t you? In the sense – in one sense that we were talking about within a certain interpretation. There – to the best of my knowledge, recollection, there is no document in existence that complies with the provision of 1[b].

Well, whether there’s a document or not, you did tell the court yesterday on your oath that Mr Gould had been the appointor in respect of both companies throughout the period of your involvement with the knowledge of them, didn’t you? For the purpose of dealing with the reimbursement of people to whom group companies owed moneys in the event of my death. But I did not – and if I did imply – say I withdraw what I said about Mr Gould being the appointor having read clause 1[b].

You would like to escape from those answers that you gave yesterday now, would you, on the basis that you would resort to the requirement in the articles that there would be an instrument of appointment and that you think the Commissioner doesn’t have one? Yes.

Is that what you would like to do? Well, that’s – that’s right.

Yes. And the problem with that, Sir, is that what you said yesterday was that Mr Gould was chosen as the appointor because of years and years of trust that you had with him? In relation, Sir, to acting as a form of protector, if I can use that expression, in relation to the repayment of parties to whom assets or moneys were owed from the group companies.

Well, you introduced there the word “protector” but the questions you–? Yes, because I think – I think to describe the role that I was trying to get – the role of Mr Gould that I was trying to get across to you yesterday is better described as a protector than as an appointor having regard to the very specific provision of clause 1[b] of the articles of association.’

93 This evidence followed from an invitation of the cross-examiner, Mr Fagan SC, at the end of the previous day to Mr Borgas to have a look overnight at the articles of, inter alia, JA Investments.

94 This explanation required Mr Borgas to say that his evidence that Mr Gould was the appointor given the previous day was wrong. His evidence then became that Mr Gould was a ‘protector’; a position having no existence under the articles and to which I can ascribe no rational content.

95 This new evidence was again directly contradicted by the terms of the deed of 31 August 2005 which was signed by Mr Gould and which recited in terms permitting of no uncertainty that Mr Gould was the appointor. It was also contradicted by Offshore Nominees’ application for membership of JA Investments which attached a form signed by Mr Gould ‘as Appointor’ consenting to Offshore Nominees becoming a member and which application said ‘Attachment to this application is the requisite nomination form signed by the Appointor’. Mr Borgas signed the resolution approving Offshore Nominees’application, as extracted above at [73].

96 Mr Borgas was taxed by the cross-examiner about three of these four documents. All that Mr Borgas could say was that Mr Gould had not been appointed in writing.

97 I am unable to accept Mr Borgas’ evidence about his beneficial ownership of JA Investments. It was directly contradicted by the documents and was incoherent. Mr Borgas was not the beneficial owner of JA Investments and did not control it.

98 Mr Borgas’ evidence about this persuaded me that he was a witness who was willing to lie on oath in a most discreditable way.

99 The dishonesty of Mr Borgas is borne out by another matter. On 29 January 2009 and 3 February 2009 the ATO began the process of information gathering in relation to entities connected to Mr Gould and Mr Borgas. On 6 February 2009 Mr Gould executed an extraordinary document in these terms:

‘WRITTEN RESOLUTION of the sole Member/Appointer/Beneficiary of the Company passed as at the 6th day of February 2009 and made pursuant to the Articles of Association of the Company, which resolution shall be as valid and effective as if the same had been passed at a meeting of the sole Director of the Company duly convened and held at Neuchatel, Switzerland on the 6th February 2009 THAT, I, Mr Vanda Russell Gould hereby acknowledge being the sole appointer of the Nominee Agreement held between the Company and Offshore Nominees Ltd, sole Member of the Company dated the 31st August 2005 THAT it is hereby authorized to cancel such Nominee Agreement with immediate effect, AND THAT Mr Peter Borgas be accepted and appointed as the Sole Member of the Company with immediate effect as in the herein attached Director resolution, hereby being made part of the corporate minutes of the Company.’

100 On the same day Mr Borgas resolved on behalf of JA Investments to transfer Offshore Nominee’s share to himself. Before doing so he wrote to the firm who handled the paperwork for JA Investments in these terms:

‘I have your fax of yesterday about outstanding fees for JA. I shall deal with this in the very near future.

In the meantime, I need your urgent assistance in relation to the transfer of the issued share in JA. I attach a copy of the share register and would be grateful if you would arrange for the share now held by Offshore Nominees Ltd. to be transferred to me. Mr. Gould knows about this and has agreed to the transfer.

As I say, the share should be transferred to me i.e. Peter Martin Borgas, Port Roulant 30, 2000 Neuchatel, Switzerland.

The matter is important and I hope that you will be able to deal with this before the end of the week. Once the transfer has taken place, please let me have (by fax or email) a certified copy of the share certificate in my name together with a certified copy of the up-dated share register.

…’

(emphasis in original)

101 The broker who conducted trading on behalf of the taxpayers was Bell Potter and it received one of the notices sent on 29 January 2009. I infer that this was reported by Bell Potter to Mr Borgas. This flurry of activity by Mr Borgas and Mr Gould was an attempt to hide the truth.

102 My rejection of Mr Borgas’ evidence that he was the beneficial owner of JA Investments is supported by some matters showing its use by Mr Gould as his own vehicle. These related to donations made to religious organizations apparently organized by Mr Gould. On 19 January 2007 Austrac records show that JA Investments transferred $150,000 to the ‘Church Army in Australia’. On 24 January 2007 the Church Army issued a receipt to Mr Gould and his wife for that amount. The receipt formed part of a letter from the Church Army’s national director. It read:

‘Dear Vanda & Debbie,

Thank you for your gift to Church Army Australia. Your ongoing support is vital to ensure we can continue and grow our ministries in 2007, reaching the least, the last and the lost.

We truly appreciate your support of our mission to reach the darkest places in Australia for Christ – a dream we cannot even begin to realise without the generosity of donors such as you.

I hope you feel part of this mission, as you certainly are, and will continue to pray with us on this journey.

Gods richest blessings.’

103 Mr Borgas gave some evidence trying to explain other donations apparently made by companies alleged to be controlled by Mr Borgas to religious bodies associated with Mr Gould. This he did on the basis of what he said was their shared common faith and as a token of appreciation for all of the ‘help and assistance’ he had received from Mr Gould. I have no doubt Mr Borgas was making this up.

104 Nor was this the first time that Mr Gould had made such a donation. A receipt was in evidence issued by the Church Army for $106,000 on 1 January 2006 to Mr and Mrs Gould. In May 2006 Mr Gould subsequently corresponded with the Church Army in these terms:

‘Dear Tim

I confirm that the substantial donation arranged by me in December 2005 of $106,000 was for the purpose of funding projects in 2006 as set out in your funding request letter. You will no doubt recall the concerns I expressed about some of the proposed applications of those funds in 2006.

May God bless you in all you are seeking to do.’

105 This shows that Mr Gould was certainly expressing sentiments consistent with control in respect of the donation of $106,000. There is no evidence that that donation came from JA Investments so this letter does not show, directly in any event, that the donation of $150,000 which was made by JA Investments was as a result of Mr Gould’s control. But it does show that Mr Gould was a donor to the Church Army. The receipt for the $150,000 donated on 19 January 2007 is evidence of a fairly direct kind that Mr Gould caused that donation. His history of donating to the Church Army, the receipt, the fact that Mr Gould was the true owner of JA Investments and my conclusion that Mr Borgas was lying about his role in relation to it lead me to conclude that it was Mr Gould who arranged that the donation of $150,000. This merely reflected the fact that JA Investments and its assets belonged to him.

106 There is further evidence of Mr Gould’s use of JA Investments as his own. On 22 January 2007 JA Investments transferred to the Mary Andrews College $100,000. It issued a receipt dated 22 January 2007 to ‘Vanda & Debbie Gould’.

107 On the 16th day of the trial the Commissioner read the affidavit of Archdeacon Arline Jarrett. Between 1985 and 2008 Archdeacon Jarrett was the principal of Mary Andrews College which is an evangelical training college for women. She gave evidence that Mrs Debbie Gould had been a student at the college and had become a member of the college’s committee. She said that whilst a student of the college she had discussed with Mrs Gould the college’s financial needs. Mrs Gould had offered to ask her husband, Mr Gould, to assist the college with funding. Following these discussions, Mr Gould started to donate money to the College and the amounts involved were significantly higher than those to which the College was accustomed. In Archdeacon Jarrett’s view, Mr Gould was the College’s most significant financial supporter and his efforts made a substantial difference to it. She was able to recall that the largest donation he made was $100,000 which I infer was the payment made on 22 January 2007 by JA Investments.

108 No objection was taken to the affidavit of Ms Jarrett being read and she was not cross-examined. I emphasise that this occurred on the 16th day of the trial (11 October 2013). Although Mr Gould was subsequently arrested during the course of the trial this had not occurred by this stage.

109 What can one make of this evidence? Only this: it shows on the balance of probabilities that Mr Gould used JA Investments to donate $100,000 to the College as his own money. In turn, this provides powerful corroboration that what the corporate records of JA Investment show – viz Mr Gould’s actual total control – accords with the reality.

110 The finding I make is that the true owner of JA Investments and the person in actual control of it was Mr Gould. I further find that Mr Borgas did nothing in relation to the affairs of JA Investments other than give effect to Mr Gould’s will.

111 So much for JA Investments. As already noted, JA Investments owned Chemical Trustee through the nominee structure involving Guardheath. One puzzling aspect of the case is why this double layered, multinational structure existed at all. At T1035-1036 Mr Borgas was asked this precise question. He gave the following evidence:

‘Why did you want the shares in Chemical Trustee to be held beneficially for, or in [sic] trust for, JA, rather than just on trust for you or for Anglore, or for some other entity in Switzerland that you could control? Why did you want them held for a company in the Cayman Islands? Because that company in the Cayman Islands is a company which I owned beneficially.

Yes. Well, you own other companies beneficially? Indeed.

So why did you want it – why did you want that one? Why? Without wanting to be facetious, it sounded – it seemed like a good idea at the time, and a sensible way of putting the position, or dealing with the position, as it should – it should have been dealt with.

A good idea for what purpose, to have – ? Well –

shares, ultimately, held by a company in the Cayman Islands, administered by FCM? For what purpose? I really, really don’t recall. We’re going back to ’98. And I cannot give you any explanation of the thinking that occurred at the time that this ’98 nominee deed was put into place.

And the answer would be the same in relation to Bywater, would it, in relation to which we’re going back to 1994, that you just can’t recall why it was a good idea? No.

Well, although it does go back to those dates, it’s not as if nothing has happened in the meantime, Mr Borgas. These entities have been there ever since. And you say that ever since, over a period of about 15 years, you’ve owned them and controlled them, and they’ve been yours. Now, having regard to that 15 year history, can’t you tell me why you ever set it up in the first place? No, I cannot recall.’

112 If Mr Borgas truly beneficially owned JA Investments he would have the answer to this. In my opinion, the reason he could not remember is because he never knew the purpose of the structure since it was Mr Gould’s.

113 Mr Borgas’ evidence about his control of JA Investments is also quite inconsistent with the manner in which the trial before me was conducted. At stake in the case of these three taxpayers was around $14 million in tax and the general interest charge. Mr Borgas did not arrive from Switzerland until the end of the applicants’ cases. Three hearing days had to be vacated whilst the Court anxiously awaited his arrival from Switzerland. Up until his arrival, he was not present to give instructions during the applicants’ case. Of course, there is the telephone. But if Mr Borgas had been giving instructions for the running of these appeals by such or other equivalent means, he displayed a remarkable ignorance of what had been going on in the case prior to his arrival. I return below to deal with the position of the Bank. As something of a prelude it may be noted that whilst Mr Borgas claimed to own that bank through JA Investments’ ownership of the bearer debenture he was completely unaware of who its directors were. The director of the Bank was Westco Directors Ltd and its directors were Mr Carran, Ms Nicolson and Mr Hanning. Each was called by the applicants in the case. This remarkable exchange occurred at T1057.1 – 1057.17: