FEDERAL COURT OF AUSTRALIA

Atkinson v Commissioner of Taxation [2014] FCA 1217

IN THE FEDERAL COURT OF AUSTRALIA | |

| First Applicant PETER PAALVAST AS ASSIGNEE BY THE TRUST'S NOMINATED TRUSTEE FOR THE CORRECT PARTY NAMELY THE BANGARRA TRUST Second Applicant | |

AND: | Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The originating application be dismissed.

2. The applicants pay the respondent’s costs as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 653 of 2014 |

BETWEEN: | PHILLIP GORDON ATKINSON First Applicant PETER PAALVAST AS ASSIGNEE BY THE TRUST'S NOMINATED TRUSTEE FOR THE CORRECT PARTY NAMELY THE BANGARRA TRUST Second Applicant

|

AND: | COMMISSIONER OF TAXATION Respondent

|

JUDGE: | JAGOT J |

DATE: | 14 NOVEMBER 2014 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 By an originating application filed on 27 June 2014 the applicants sought orders against the respondent, the Commissioner of Taxation (the Commissioner), as follows:

1. A Declaration that any and all indebtedness of Phillip Gordon Atkinson for monies previously asserted by the Respondents to be owing to the Respondent in relation to an amount of taxation of $112,500 allegedly being due and payable, has been discharged in Law by operation of the Bills of Exchange Act 1909 (Cth.) (and inter alia Section 50(1) thereof).

2. An Order that the Respondent do pay to the Applicant the sum certain of four hundred and fifty thousand dollars ($450,000) along with costs, interest and disbursements as provided for and contained within the Default and Liability Clauses associated with the relevant Bill of Exchange number 13070903.

3. All other Costs as the Court considers reasonable by the abusive statutory process undertaken by the Respondent.

2 The facts said to support this claim are not in dispute.

3 The Commissioner commenced proceedings in the Local Court against the first applicant seeking payment of tax owing in the amount of $99,608.46.

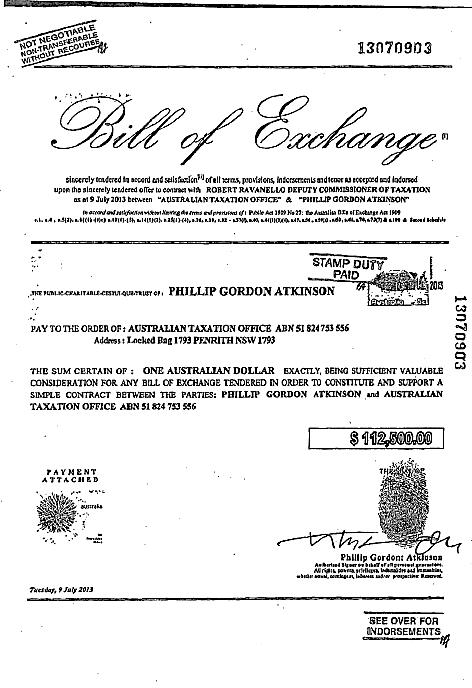

4 On 4 July 2013 the Australian Taxation Office (the ATO) sent to the first applicant a statement of account in respect of his income tax debt. This statement specified the amount of $96,592.55 as the “overdue amount as at 1 July 2013” and stated, amongst other things, that:

You are required to pay this amount immediately

Interest Charge (GIC) may be accruing

5 The statement of account contained a payment slip at the bottom and, on the notes on the back, specified methods of payment, being BPay, direct credit, mail payments of cheque or money order, and post office payment by cash, cheque or EFTPOS.

6 On or about 7 July 2013 the ATO received a document from the first applicant. The document was the statement of account which the ATO had sent to the first applicant, on which stamps had been affixed and handwriting had been marked.

7 One stamp said:

NOT NEGOTIABLE

NON-TRANSFERABLE WITHOUT RECOURSE

8 Another stamp said:

INCHOATE INSTRUMENT ACCEPTED FOR VALUE

RETURNED COMPLETE BY SUPRA PROTEST

PAY the sum certain of ONE AUSTRALIAN DOLLAR EXACTLY

9 The handwriting said, amongst other things:

NOTICE: This is an acknowledged offer/inducement to contract between all the parties named below and is a statement of a transaction giving rise to payments required to be executed between them all.

10 Against this statement are initials noted to be the “acknowledged simple signature of payee” initialled by a third party.

11 Beneath the transactions list on the statement of account there is written in handwriting:

+ General interest charges, disbursements & incidentals - $15,907.45

Equals a sum payable of $112,500.00 being a sum certain of one dollar exactly.

12 Various names on the statement of account have been placed in brackets and identified as, for example, “party 6” (the Deputy Commissioner of Taxation) and “party 2 (the ATO).

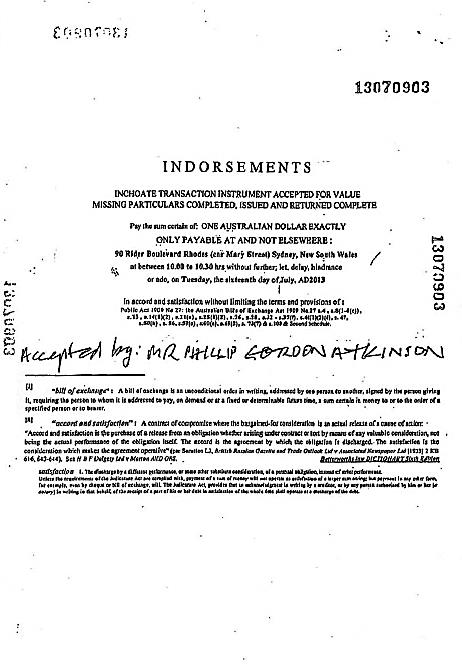

13 Other stamps on the statement of account appear as follows:

ACCEPTED AS INDORSED

SEE OVER FOR INDORSEMENTS

14 Against the words “amount paid” on the payment slip part of the statement of account is written:

$112,500.00

Being a sum certain of one dollar exactly

15 The notes on the back of the statement of account have been struck through and written beneath them are the words:

*NOTICE: CHEQUE MEANS a bill of exchange payable on demand, drawn on a banker. A banker includes a body of persons, whether incorporated or not, who carry on the business of banking.

16 Other documents are attached to the statement of account. One such document is a letter from the first applicant to the Deputy Commissioner of Taxation. The letter is in these terms:

_____________________________________________________________________________________________________________

Re: ‘Overdue amount’ as at 01 July 2013 for $96,592.55 as shown on ‘ATO statement number 29’ dated 04 July 2013 – received 8 July 2013

_____________________________________________________________________________________________________________

** NOTICE TO THE PRINCIPAL IS NOTICE TO THE AGENT **

** NOTICE TO THE AGENT IS NOTICE TO THE PRINCIPAL **

Dear Robert Ravanello (or agents, assigns or nominees),

Please accept my humble and sincere apologies for any belated correspondence and dishonours that may have previously occurred regarding this matter.

I am in receipt of the above captioned statement along with several earlier statements all received 8 July 2013 and I shall rely upon your most recent one dated 04 July 2013.

All other debts having been settled on previous accounts please find coupled hereto the statement of transaction and the payment of the outstanding sum certain owing, as negotiated for and assented to, enclosed for the sum payable of $112,500.00 being the sum certain as per the indorsements, terms, provisions and tenor of the true debt owing tendered in accord and satisfaction with the Bills of Exchange Act 1909, and I trust this will satisfy all outstanding claims.

At no additional expense to you/r office, a notary public will be in attendance to facilitate, notarise and record these events and will provide your office sufficient evidence of any additional resolution if required.

With all due respect afforded I stress the importance of the [fiduciary] responsibilities of your office upon your receipt of the stamp duty, which as you know will note has been paid.

In anticipation of every honourable equitable co-operation afforded, I most sincerely thank you.

Yours sincerely, ……………###……………

Phillip Gordon Atkinson

All rights, powers, privileges, indemnities and immunities whether actual, contingent, inherent or prospective: Reserved

17 Another such document is a page entitled “Default and Liability Clause and Notice”. This is a page of fine print said to embody a legal agreement between the first applicant, the ATO, the Deputy Commissioner of Taxation, and the Commissioner of Taxation.

18 Two more documents follows. Copies of those documents appear below.

19 This sequence of events is the foundation of the claims made in the originating application.

20 Claims to similar effect have been made in other proceedings.

21 In Deputy Commissioner of Taxation v Sproule [2012] FMCA 1188 (Sproule) the respondent owed a tax debt. He purported to serve on the ATO two bills of exchange as payment for his liability. In common with the present case, the bills of exchange included a copy of a statement of account the ATO had sent to the respondent, filled up with details to the same general effect as those noted above. The Federal Magistrate said this:

[22]… Without embarking on a detailed historical and legislative review of the Bills of Exchange Act 1909 (Cth), a bill of exchange, most simply put, is a financial document that requires an individual or business that is addressed in the document to pay a specific amount of money on the date that it cites within the text of the document. Considered to be a negotiable instrument the date for the demand to pay generally ranged from the current date to some date in the future. A bill of exchange will also require the authorising signature of the drawee, if accepted then the acceptor (debtor) in order to be considered legal and binding. There is no evidence that the DCT [Deputy Commissioner of Taxation] has accepted the bill of exchange. Without explanation, Mr Sproule has embarked on this very novel and misguided use of this negotiable instrument.

[23] On the structure of the documentation before the court, Mr Sproule has prepared a bill of exchange with a face value of $1 AUD and forwarded that to the ATO seeking acceptance as settlement for an outstanding debt of $436,472.14. Logic as to why the DCT would accept that document is completely unexplained by either Mr Sproule or Mr Andrews…

[24] The nature of the material contained in the various documents tendered by Mr Sproule indicates that there has been considerable attention focused on the various sections of the Bills of Exchange Act, however, the basic concept and mechanism of this financial instrument appears to be totally misunderstood or misconceived. In the normal course a bill of exchange is prepared by a party who is advancing a line of credit to another with the expectation that the indebtedness of the party to whom it has been given will settle that amount either when some event occurs, such as supply of goods, or at some specified date which is mutually agreed between the parties and accepted by the party that is incurring the liability. The use of the bill of exchange proposed by Mr Sproule is either a complete misunderstanding of the use of the instrument or some cynical ploy to avoid the debt. In the absence of any logical explanation of how Mr Sproule intends to resolve his indebtedness to the ATO this whole approach for this form of settlement is misconceived and should be dismissed.

22 In Bertola v Australian and New Zealand Banking Group Ltd [2014] FCA 609 (Bertola) Barker J dealt with a debt owed to the ANZ bank which had led to the making of orders by the Supreme Court of Western Australia to facilitate assets over which the debt was secured. The applicant sought an interlocutory injunction from Barker J to prevent the sale based on an originating application and statement of claim which challenged the validity of the security instruments.

23 Mr Paalvast, the second applicant in the present proceeding, was granted leave to speak on behalf of the applicant. Barker J noted the following:

[11] It then became apparent that Mr and Mrs Bertola sought to attract the operation of the Bills of Exchange Act by the following process. First, they had made a copy of the relevant judgment of the Master of the Supreme Court of Western Australia facilitating the sale of assets. Secondly, they had made various annotations to that copied document and attached to it other documents exhibiting various stamps and seals and a fingerprint of Mr Bertola. Thirdly, they had recently delivered this new document, comprising some four pages, to the Bank [Australia and New Zealand Banking Corporation].

[12] The apparent expectation of Mr and Mrs Bertola, which I infer was created by Mr Paalvast, was that upon receipt of this new document the Bank would be obliged to respond and, if it did not, would be taken as having accepted the document in “accord and satisfaction“ of all monies due to the Bank under the securities that underpinned the Supreme Court order facilitating the sale of assets. I may not have fully represented the complete scope of the argument outlined by Mr Paalvast before me, but this was how I understood its substance.

[13] Mr Paalvast made a particular submission concerning the operation of s 25 of the Bills of Exchange Act in relation to the documents served on the Bank. He also made suggestions that there was some contract, as a result of the delivery of this new document to the Bank, between the Bank and Mr and Mrs Bertola, and presumably the company too (albeit a company to which receivers had been appointed by the Bank and which was also in liquidation).

[14] The arguments put on behalf of Mr and Mrs Bertola relying on s 25 of the Bills of Exchange Act and other provisions of that Act made little sense to me at the time Mr Paalvast sought to articulate them, as I then sought to convey to him and to Mr Bertola.

[15] After hearing briefly from counsel for the Bank, I not only dismissed the application for interlocutory injunction, but also invited and entertained an application made on behalf of the Bank that there should be summary dismissal of the proceeding, and ordered that the proceeding be dismissed.

[16] I incorporate in this judgment the transcript of the hearing at which I made these orders. I do so for a number of reasons. First, it is, in my judgment, the most convenient way to attempt to outline the apparent cause of action advanced by Mr Paalvast on behalf of Mr and Mrs Bertola at the hearing, and to demonstrate that it was not only hopeless but nonsense, and should not be allowed to take up any further time of the court or indeed the parties.

24 In Wilmink as Trustee for the Bangarra Trust v Westpac Banking Corporation [2014] FCA 872 (Wilmink) Bennett J dealt with a debt owed to Westpac bank (via a wholly owned subsidiary, RAMS). The debtor claimed that he had paid the debt of $313,563.55 by way of a bill of exchange. Bennett J recorded that:

[4] Mr Waden, at the hearing in the District Court, explained that he had paid the $325,000 by way of a “bill of exchange“ (the Bill). On the front page of the Bill, Mr Waden appeared to direct himself (both in his own right and as trustee for the Trust) to pay RAMS the amount of one Australian dollar. The Bill further provided that the sum of $1 could only be accepted at the corner of Cuthbert Drive and Darlington Drive, Yatala, Queensland at 1430 hours on Friday, 24 May 2013, or “by prior mutual agreement at another agreed alternate address”. Annexed to the Bill was a home loan statement issued by RAMS to Mr Waden for the period 1 March 2012–31 May 2012 (the Loan Statement).

[5] Relevantly for the present case, the Bill also contained a “Default and Liability Clause and Notice” (the Default Clause), which provided that, in the event of default, the amount of $1,300,000 would become payable by Westpac within seven days of the default.

[6] On 13 December 2013, Westpac was awarded summary judgment in the District Court proceedings in the amount of $345,748.08, possession of the Property and costs. An application for a stay of the judgment was dismissed on 24 January 2014. Westpac says, and it does not appear to be in dispute, that there is no evidence of any appeal having been lodged.

[7] The applicants have now commenced proceedings in this Court alleging default by Westpac and seeking damages in the amount of [$1,300,000] , plus interest and costs, or, in the alternative, orders that Westpac pay the applicants $975,000, discharge the mortgage over the Property and indemnify the defendants in the District Court proceedings against any further claim.

25 Bennett J explained that:

[30] The above arguments appear to have been previously considered in Bertola v Australian and New Zealand Banking Corporation [2014] FCA 609 (Bertola) and Deputy Commissioner of Taxation v Sproule [2012] FMCA 1188 (Sproule), each of which dealt with facts and issues significantly similar to the present case. The applicants submit that these cases were wrongly decided.

[31] In Sproule, a debtor (Mr Sproule) attempted to use a bill of exchange to satisfy a debt to the Australian Taxation Office (ATO). Judge Lloyd-Jones rejected Mr Sproule’s argument that a bill of exchange with a face value of $1 could be used to satisfy his debt to the ATO, noting (at [23]) that:

… logic as to why the [Deputy Commissioner of Taxation] would accept that document is completely unexplained …

[32] Judge Lloyd-Jones concluded (at [24]) that:

The basic concept and mechanism of this financial instrument appears to be totally misunderstood or misconceived … The use of a bill of exchange proposed by Mr Sproule is either a complete misunderstanding of the use of the instrument or some cynical ploy to avoid the debt. In the absence of any logical explanation of how Mr Sproule intends to resolve his indebtedness to the ATO this whole approach for this form of settlement is misconceived and should be dismissed.

(emphasis added)

[33] Similarly in Bertola, Barker J considered the question on submissions advanced by Mr Paalvast, one of the applicants in this proceeding. His Honour rejected the submissions as “not only hopeless but nonsense” and dismissed the application. The same observations could well apply to this case.

26 I made an order in the present proceeding on 12 August 2014 as follows:

Pursuant to s 20A of the Federal Court of Australia Act 1976 (Cth), the proceeding be dealt with, without an oral hearing.

27 The applicants were not present at the directions hearing when I made this and other orders to facilitate the determination of the proceeding.

28 Section 20A of the Federal Court of Australia Act 1976 (Cth) (the FCA Act) provides as follows:

(1) This section applies in relation to any civil matter coming before the Court in the original jurisdiction of the Court.

(2) The Court or a Judge may deal with the matter without an oral hearing (either with or without the consent of the parties) if satisfied that:

(a) the matter is frivolous or vexatious; or

(b) the issue or issues on which determination of the matter depends have been decided authoritatively in the case law; or

(c) determination of the matter would not be significantly aided by an oral hearing because:

(i) there is no real issue of fact relevant to determination of the matter; and

(ii) the legal arguments in relation to the matter can be dealt with adequately by written submissions.

29 By written submissions filed on 30 September 2014 the second applicant, Mr Paalvast, said that he did not consent to the matter being dealt with without an oral hearing. He denied that s 20A of the FCA Act applied and contended that he was being robbed of his inalienable right to a hearing.

30 Section 20A of the FCA Act is available whether or not a party consents. I was (and remain) satisfied that, despite the lengthy submissions in writing of Mr Paalvast to the contrary, this matter is frivolous and vexatious. Despite the attempts by Mr Paalvast to distinguish the reasoning in Sproule, Bertola and Wilmink the submissions in the present case remain the obscure, impenetrable, hopeless nonsense that led to the dismissal of each of those three proceedings.

31 In his submission dated 6 August 2014 Mr Paalvast submitted that:

Section 50(1) of the Bills of Exchange Act 1909 (Cth.) is completely unequivocal in its terms. That Statute, without more, totally answers what the proper outcome of today’s proceedings must be, provided only that the proper Law, under the prevailing rules of equity is duly applied. The parties were duly notified and the Court is without lawful excuse for ignoring the undisputed facts of this and the previous cases.

32 The matters said to support this proposition were detailed as follows:

1. The AUSTRALIAN TAXATION OFFICE as potential Payee delivers some form of a written Demand for Payment hereinafter referred to as the “Statement of the Transaction” addressed from the payee to MR PHILLIP G ATKINSON as a prospective Drawee.

…

3. In this case the Drawee who was addressed as a representation of their proper self was the Receiver of the Demand for Payment, this being Phillip Gordon Atkinson as Drawer in fact, without representation, in his proper persona being the principal of the natural and equitable interest in the natural persona. This Receiver, Phillip Gordon Atkinson received the inchoate Statement of the Transaction instrument. This was accepted as correctly expressed by the Payee, as being a representative of the Crown’s estate namely the cestui que trust. An original trust arrangement being created by delivery between the Payee to the named Drawee.

4. Thereof, the Drawer as the recipient of the AUSTRALIAN TAXATION OFFICE’S Demand for Payment, being expressed in a representative capacity, he had an unalienable right, pursuant to both Section 21 (a) and Section 36 (5) of the Bills of Exchange Act 1909 (“the Act”) to “negative or limit his personal liability”.

5. Any such instrument as originally present, if inchoate, is permitted to be filled up and completed by indorsement pursuant to Section 25(1) if the one in possession of the instrument sees fit to do so. This subsection referring to any instrument or writing as it does in several other specific places within the Act. Section 25(2), refers specifically to any incomplete (inchoate) bill of exchange, whereas Subsection (1) more broadly refers to any legal or formal document in writing.

6. Therefore, pursuant to the respective sections of the Act, Phillip Gordon Atkinson was able to “negative or limit his personal liability as he saw fit” by his electing to as he saw fit to bargain or negotiate the ‘negotiable inchoate instrument (not expressed as being not negotiable)’ to a lesser value. Upon payment, valuable consideration now having been tendered, becomes the ‘sum certain’ as expressed on the face of the Bill of Exchange.

7. Section 14(2) of the Act stipulates that where a conflict as to quantum arises within an instrument, the lesser or the least (lowest) amount prevails. This capacity entrenches anyone’s right (given Consideration as defined in Section 32(1) of the Act) to bargain or negotiate quantum, with any instrument not previously expressed to be “Not Negotiable”. See Section 41(1) and (2).

8. The Statement of the Transaction giving rise to the Bill of Exchange [See section 8(3)(b)], (in this case, the AUSTRALIAN TAXATION OFFICE’s Demand for Payment) was inchoate. On its face, it appeared not to be an equitable instrument, being of a unilateral nature. As it was incomplete, Section 25(1) permitted the Receiver (the person legitimately in possession of the inchoate instrument from what remains a public servant/service provider) to include a Default and Liability Clause and Notice to be fairly and equally binding on all parties subject to the transaction. The Default and Liability Notice by its nature, is what it states, default provisions for commercial dishonour, with an instrument operating under the doctrine of uberrimae fidei and therefore is and cannot be a penalty provision.

9. With regards to Section 8 of the Act, before the completed Statement of the Transaction was coupled to the unconditional order in writing to pay (the bill of exchange), it was transferred from Drawer to Drawee said document was indorsed as being: “Not Negotiable”, “Non Transferable”, “Without Recourse to Drawer or Drawee”.

Subsequently, when Phillip Gordon Atkinson as Drawer drew up the unconditional order to pay a sum certain in money, paid the impress stamp duty and coupled the Statement of the Transaction to the Bill of Exchange, ordering the MR PHILLIP G ATKINSON as Drawee to pay in accord and satisfaction of the tenor of his acceptance and indorsements, the sum certain of One Australian Dollar (expressed in words) and $112,500 (expressed in figures) as differentiated; pursuant to Section 14(2) of the Act, as notified to all the Parties.

The Drawer was thus instructing the Drawee to issue and tender an unconditional order in writing to the Payee for the tenor of the sum certain [see section 25(2) and section 14], and the Drawee indorsed the Bill of Exchange [see section 8 of the Act] as it saw fit with the requisite valuable Consideration affixed to the instrument. This thereby constituted valuable Consideration sufficient to support a simple contract [See Section 32(1)].

10. This now ‘more complex instrument’ complete with issued Bill of Exchange coupled thereto as the Consideration, was then perfected and issued to the first transferee [see section 36(1)].

11. The originating debt has in Law thus been bargained for or renegotiated in accord and satisfaction, obviating the need for strict performance [see Section 32(1)] as is indorsed on the instruments.

12. The character of the Bill of Exchange in issue in these proceedings, is one of a 'Bill' requiring presentment at a specific future time and location [see Section 50(2)(a) and Section 44]. And whilst Section 51 makes provision for compliance with such requirement to be excused or dispensed with, the AUSTRALIAN TAXATION OFFICE failed to communicate in a timely manner and none of the circumstances Section 51 refers to arose.

13. At the appointed time and neutral venue for presentment, the AUSTRALIAN TAXATION OFFICE having under the prevailing notified rules of equity a legal duty to appear, made no appearance and failed in a timely manner, or at all to provide excuse or apology. The legal effect of these circumstances is incontrovertibly mandatory and Evidence of the default involved is now what is before the Court. A particularly apposite case on this point is: Duncan Properties Pty Ltd v Donald Alan Keith Neal and Colin John Taylor [1993] FCA 373 (10 August 1993)… [See also Sections 56, 100 and the Second Schedule to the Act].

14. The fact that the AUSTRALIAN TAXATION OFFICE have initiated proceedings in the Local Court whilst being estopped by virtue of any earlier accepted negotiated debt having already been discharged by the mandatory effect of Section 50(1) of the Act prior to their application for judgment, enlivened the Default and Liability provisions previously notified (accepted) as coupled with the Bill of Exchange. Quality legal advice has it that the notarial act in the form of a Certificate of Protest having been issued, has sufficiently confirmed that the debt is now settled and discharged. That advice is also that said notarial act provides sufficient evidence as set out in Section 100(2) to create the equivalent of a judgment awarded by a Justice of the Supreme Court of a State, or of the Federal Court of Australia.

15. The clear consequence of the above is that any debt allegedly owed to the AUSTRALIAN TAXATION OFFICE is, by operation of statute law "discharged". These facts also necessarily invoke or enliven the abovementioned Default and Liability provisions, the terms of which direct the award of Damages of a quantum fourfold that of the amount originally sued for, plus certain costs and disbursements in circumstances where the bargained for Consideration had been provided. That fact discharged any debt and rendered nugatory any standing for the AUSTRALIAN TAXATION OFFICE to legitimately pursue a Cause of Action in the Local Court, as it has.

16. In accord with the clear powers and provisions of the relevant Default and Liability Clauses, Phillip Gordon Atkinson has legitimately elected to assign his rights pursuant to these clauses to the Bangarra Trust, which now appears as Assignee and Receiver of the sum certain default amount in these proceedings. Those amounts are clearly notified within the Default and Liability Clause and Notice known to have been in the Payee's possession.

33 Submissions to the same effect were made in Mr Paalvast’s reply, as well as in various affidavits filed in support of the originating application.

34 On behalf of the Commissioner, an officer of the ATO filed an affidavit which, amongst other things, said:

The ATO debt collection policy is only to accept cash, bank cheque, electronic funds transfer or personal cheque to pay debts and not to accept bills of exchange generally.

Only I and Michelle Coble, another ATO officer, worked on this file between 4 July 2013 and 4 August 2013. No one within the ATO accepted the ‘Bill of Exchange’ by signing it for the purposes of section 22 of the Bills of Exchange Act 1909 (Cth) or for any other purposes. None of the handwriting on the document headed “Bill of Exchange” is mine.

35 The Commissioner filed written submissions on 14 October 2014 which included the following:

This is the third time this year that this Court has been called upon to decide a case in which Mr Peter Paalvast (the second respondent) has been involved: see Bertola v Australia and New Zealand Banking Group Ltd [2014] FCA 609; and Wilmink as trustee for the Bangarra Trust v Westpac Banking Corporation [2014] FCA 872.

In each case, the party associated or advised by Mr Paalvast has owed significant amounts to a creditor.

In each case, the debtor (with Mr Paalvast’s assistance) has “filled up” a statement received from the creditor recording the debtor’s liability so that it resembles a “bill of exchange”. In this case, the document “filled up” by the applicants was a computer generated “Statement of Account” issued by the respondent to the first applicant in relation to the first applicant’s outstanding tax debt.

In each case, the debtor has been delivered the “filled up” statement to the creditor and asserted that delivery, and the creditor’s failure to negotiate the debt, has effected discharge of the debt pursuant to s 50 of the Bills of Exchange Act 1909 (Cth).

…

In conclusion, the arguments that the applicants have cynically deployed in this proceeding to obtain a stay of the Local Court proceeding have been characterised as hopeless nonsense in previous proceedings, and hopeless nonsense they remain.

In light of the above, the respondent submits that the Court should deal with this matter on the papers pursuant to s 20A of the Federal Court of Australia Act 1976 (Cth) by reason that the applicant’s claim is frivolous, vexatious, and the argument has been decided authoritatively in the case law: s 20A(2)(a) and (b). It remains the case that there is no real issue of fact and the matter can be dealt with adequately by reference to the written submissions: s 20A(c).

The respondent submits that the proceeding should be dismissed with costs.

36 The Commissioner’s submissions should be accepted.

37 Under s 4 of the Bills of Exchange Act 1909 (Cth) (the Act) a “bill” is a bill of exchange.

38 Section 8(1) of the Act provides that:

A bill of exchange is an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand, or at a fixed or determinable future time, a sum certain in money to or to the order of a specified person, or to bearer.

39 The other provisions of the Act, on which Mr Paalvast relies, depend on there being a bill of exchange as defined in s 8.

40 Accordingly, s 21 of the Act is in these terms:

The drawer of a bill, and any indorser, may insert therein an express stipulation:

(a) negativing or limiting his or her own liability to the holder; or

(b) waiving as regards himself or herself some or all of the holder's duties.

41 Section 22(1) of the Act provides that:

The acceptance of a bill is the signification by the drawee of his or her assent to the order of the drawer.

42 Section 25 of the Act states that:

(1) Where a simple signature on a blank stamped paper stamped with an impress duty stamp is delivered by the signer in order that it may be converted into a bill, it operates as a prima facie authority to fill it up as a complete bill for any amount the stamp will cover, using the signature for that of the drawer or the acceptor or an indorser.

(2) And in like manner when a bill is wanting in any material particular, the person in possession of it has a prima facie authority to fill up the omission in any way he or she thinks fit.

(3) In order that any such instrument when completed may be enforceable against any person who became a party thereto prior to its completion, it must be filled up within a reasonable time, and strictly in accordance with the authority given. Reasonable time for this purpose is a question of fact:

Provided that, if any such instrument after completion is negotiated to a holder in due course, it shall be valid and effectual for all purposes in his or her hands, and he or she may enforce it as if it had been filled up within a reasonable time and strictly in accordance with the authority given.

(4) For the purposes of subsection (1) of this section, duty stamp includes a duty stamp, required, by the law of the State in which the instrument is issued, to be impressed on a bill.

43 Section 32(1) of the Act is as follows:

(1) Valuable consideration for a bill may be constituted by:

(a) any consideration sufficient to support a simple contract; or

(b) an antecedent debt or liability. Such a debt or liability is deemed valuable consideration whether the bill is payable on demand or at a future time.

44 Section 50 deals with the rules as to presentment for payment of a bill of exchange.

45 It is apparent that Mr Paalvast’s case depends on the proposition that the ATO, by sending a statement of account to the first applicant, engaged s 50(1) of the Act. The first applicant then, it is said, had authority under that section to “fill up” the statement of account so that it became a complete bill of exchange. As the drawer of the bill of exchange, the first applicant then limited (or negatived) his own liability in accordance with s 21. The first applicant then delivered the filled up bill of exchange to the ATO. By some mechanism not apparent, by filling up the statement of account and purportedly making it a bill of exchange which ordered the recipient to pay the original amount owed to the ATO plus interest and other charges (totalling $112,500), delivering it to the ATO and the ATO not objecting thereto, the ATO defaulted in respect of some obligation said to arise and thereby became liable to the first applicant (or, properly, to Mr Paalvast as an assignee from the first applicant) in that amount.

46 None of the propositions make sense.

47 The statement of account is not a bill of exchange as defined in s 8(1) of the Act. The first applicant was not authorised to do anything with the statement of account under the Act. Writing and putting various stamps on the statement of account had no legal effect under the Act. Nor did delivering that statement of account back to the ATO. The Act is simply not engaged at all by the facts of this case. The notion that a person who owes the ATO money for non-payment of tax can transform the ATO’s statement of account into a bill of exchange and then deliver the statement of account back to the ATO and, in so doing, discharge the person’s own indebtedness for some nominal amount ($1) and render the ATO liable to pay the original amount owed to the ATO plus interest and other charges is some form of fantasy, unconnected to the operation of the Act.

48 The proceeding must be dismissed with costs. If Mr Paalvast persists with applications of this character consideration should be given to whether a vexatious proceedings order should be made under s 37AO of the FCA Act.

I certify that the preceding forty-eight (48) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Jagot. |

Associate:

Dated: 12 November 2014