FEDERAL COURT OF AUSTRALIA

Hannover Life Re of Australasia Ltd v Wright [2014] FCA 1163

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

HANNOVER LIFE RE OF AUSTRALASIA LTD (ABN 37 062 395 484) Applicant | |

|

AND: |

First Respondent UNISUPER LIMITED (ABN 54 006 027 121) Second Respondent |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

2. The decision of the Superannuation Complaints Tribunal recorded in paragraphs 7 and 57 of its Review Determination and Reasons dated 26 September 2013 (Determination No D13–14\057 in File No 11–1851) be set aside.

3. In lieu of the determination set aside by Order 2 above, the decisions made by the applicant and the second respondent to include and thereafter to refuse to remove a total spine exclusion clause in the terms and conditions of the Total and Permanent Disablement cover provided to the first respondent under the second respondent’s insurance arrangements with the applicant be affirmed.

4. There be no order as to the costs of the appeal.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 2199 of 2013 |

|

ON APPEAL FROM THE SUPERANNUATION COMPLAINTS TRIBUNAL |

|

BETWEEN: |

HANNOVER LIFE RE OF AUSTRALASIA LTD (ABN 37 062 395 484) Applicant |

|

AND: |

PAULA IRENE WRIGHT First Respondent UNISUPER LIMITED (ABN 54 006 027 121) Second Respondent |

|

JUDGE: |

FOSTER J |

|

DATE: |

31 OCTOBER 2014 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

1 In the period from 1 January 2007 to late 2011, Paula Irene Wright, who is the first respondent in this proceeding, was employed as a Teaching Associate by various universities in Victoria (La Trobe University, Swinburne University of Technology and Monash University).

2 In May 2007, Ms Wright joined UniSuper, a superannuation fund which provides superannuation benefits to employees of Australian universities. UniSuper Limited (USL) is the trustee of UniSuper. UniSuper Management Pty Ltd (USM) is the administrator of UniSuper.

3 On 10 February 2011, Ms Wright informed USL that she was interested in increasing the death and disablement cover provided to her as part of the benefits for which she had contracted when she joined UniSuper. At that time, she had one unit of such cover. That level of cover was the basic level of cover or default cover. The default cover was provided automatically without the member having to undergo a medical examination.

4 On the same day, a consultant employed by USM sent the 1 July 2010 version of UniSuper’s Optional Insurance Guide (guide) to Ms Wright.

5 On 19 July 2011, Ms Wright completed and lodged with USL a UniSuper Death and Disablement Insurance Application Form (DDI form) whereby she sought to increase her total death and disablement cover to ten units overall.

6 As at 30 June 2011, Ms Wright was entitled to a death benefit of $227,626.60 and optional death and disablement cover of $196,000. Both the form which Ms Wright completed and lodged on 19 July 2011 and the guide made clear that USL had taken out group life policies with Hannover Life Re of Australasia Ltd (Hannover Life) to provide the optional insurance cover described in the guide. In the guide, USL said that all optional insurance cover was subject to the conditions set out in the insurance policy documents.

7 The death and disablement cover provided to USL in respect of Ms Wright was provided under group life policy number VGL3753 which commenced on 1 July 1993 (policy). That policy is a contract of insurance between USL, in its capacity as trustee of the UniSuper Division D Accumulation 1 plan (referred to in the policy as “the Plan”), as proposer, and Hannover Life, as insurer. By the policy, USL reinsures the insurance obligations which it has undertaken vis-À-vis its members.

8 Increased death and disablement cover was ultimately provided to Ms Wright. However, the provision of additional units of cover was provided on terms that the additional five units of disablement cover were to be subject to a total spine exclusion because of Ms Wright’s medical history. That exclusion was in the following terms:

Total and Permanent Disablement benefits shall not be payable for any disability caused by any disease or disorder of or injury to the spine, its intervertebral discs, nerve roots or supporting musculature and ligaments. This exclusion will apply above current acceptance levels.

9 Initially, Ms Wright did not accept the total spine exclusion sought to be imposed in respect of her increased disablement cover. However, on 27 October 2011, she did accept the cover on terms which included the total spine exclusion. She did so, in effect, on a “without prejudice” basis.

10 In the meantime, on 20 September 2011, Ms Wright lodged a complaint with the Superannuation Complaints Tribunal (Tribunal). In her complaint, Ms Wright said that there were two issues: First, she complained about the inclusion of the total spine exclusion in her disablement cover. Second, she complained that she had not been given the level of cover which she had sought. She had requested nine extra units of cover but had been offered only five extra units.

11 In January 2012, Hannover Life was joined as an additional party to Ms Wright’s review proceeding in the Tribunal.

12 Conciliation of Ms Wright’s complaint was unsuccessful.

13 In a decision given on 26 September 2013, the Tribunal:

(a) Affirmed the decision of USL in respect of the level of cover provided as a result of Ms Wright’s application dated 19 July 2011; and

(b) Varied the decision of USL to include the total spine exclusion in the terms of cover provided to Ms Wright by redrafting the total spine exclusion so as to exclude any claim (with respect to the units above the automatically accepted level of cover) in relation to Ms Wright’s back that is related to, associated with or aggravated or exacerbated by her pre-existing muscle tightness and/or back soreness. The Tribunal noted that, for the avoidance of doubt, the one unit of cover automatically allocated to Ms Wright when she joined UniSuper in 2007 was not to be affected by that redrafted exclusion.

14 Hannover Life was dissatisfied with the Tribunal’s decision.

15 On 24 October 2013, Hannover Life filed in this Court a Notice of Appeal from the Tribunal’s decision. It named Ms Wright and USL as the respondents to that Appeal.

16 On 12 November 2013, Hannover Life filed an Amended Notice of Appeal.

17 Ms Wright has taken no part in this proceeding although I am satisfied that she was duly served with and is well aware of all documents filed from time to time in this proceeding. I am also satisfied that she was informed of the date of the hearing before me. USL filed a Written Submission on 7 March 2014 in which it informed the Court that it would submit to any order of the Court save as to costs. In that Submission, it also emphasised that its decision to include the total spine exclusion was the result of having to comply with the requirements of Hannover Life under its contractual arrangements with that corporation. USL submitted that it had no choice in the matter.

18 The Tribunal took the view that it need not be made a party to this proceeding presumably upon the basis that it would also submit to any order of the Court had it been made a party. The Tribunal probably should have been made a party although I do not propose to require that it be joined at this stage. The Tribunal is also well aware of the existence of the proceeding and has chosen not to participate. As is normal in cases of this type, it has forwarded to the Court its entire file in respect of Ms Wright’s complaint.

The Appeal Framework

19 Section 45 and s 46 of the Superannuation (Resolution of Complaints) Act 1993 (Cth) (Complaints Act) provide:

45 Notification of appeal rights

If the Tribunal determines a review, the Tribunal must give each party a written notice that includes a statement to the effect that, if the party is dissatisfied with the decision of the Tribunal on a question of law, the party may appeal to the Federal Court under section 46.

46 Appeals to Federal Court of Australia from determinations of the Tribunal

(1) A party may appeal to the Federal Court, on a question of law, from the determination of the Tribunal.

(2) An appeal by a person under subsection (1) is to be instituted:

(a) not later than the 28th day after the day on which a copy of the determination of the Tribunal is given to the person or within such further period as the Federal Court (whether before or after the end of that day) allows; and

(b) in accordance with rules of court made under the Federal Court of Australia Act 1976.

(3) The Federal Court is to hear and determine the appeal and may make such order as it thinks appropriate.

(4) Without limiting by implication the generality of subsection (3), the orders that may be made by the Federal Court on an appeal include an order affirming or setting aside the determination of the Tribunal and an order remitting the matter to be determined again by the Tribunal in accordance with the directions of the Court.

(5) The Federal Court must not make an order awarding costs against a complainant if the complainant does not defend an appeal instituted by another party to the complaint.

20 Section 46(1) gives a right of “appeal” which is of the same character as the right of “appeal” provided to a party to a proceeding before the Administrative Appeals Tribunal pursuant to s 44(1) of the Administrative Appeals Tribunal Act 1975 (Cth) (AAT Act). Such an appeal is not an appeal in the strict sense but is a matter which must be heard in the original jurisdiction of this Court.

21 As is the case with appeals pursuant to s 44(1) of the AAT Act, the Court’s jurisdiction in respect of an appeal pursuant to s 46 of the Complaints Act is enlivened only by the existence of a question of law. For that reason, the question or questions of law posed by an applicant who seeks to engage that section must be articulated with precision (see Federal Commissioner of Taxation v Crown Insurance Services Ltd (2012) 207 FCR 247 at 250 [13], and the cases cited therein, per Lander and Foster JJ; and Soames v Secretary, Department of Families, Housing, Community Services and Indigenous Affairs (2013) 59 AAR 500 at 510 [58] per Katzmann J). Similarly, in my judgment, the principles explained by Branson and Stone JJ in Birdseye v Australian Securities and Investments Commission (2003) 38 AAR 55 at 59–60 [13]–[16] and by the Full Court in Repatriation Commission v Bawden (2012) 206 FCR 296 at 307–308 [51] also apply with equal force to appeals pursuant to s 46 of the Complaints Act. That is, in such appeals, it is not legitimate to call in aid the grounds specified in the Notice of Appeal in order to read down the questions of law relied upon in that Notice of Appeal. There is a clear distinction between expressing the questions of law sought to be raised by the appeal and stating the grounds relied upon in support of the appeal. Further, this Court has repeatedly held that merely to assert that a tribunal has erred in law in making a particular finding is not to state a question of law. Where a choice falls to be made between two conclusions open on a consideration of the facts, the question is one of fact.

The Issues

22 Hannover Life contends that the Tribunal had no power to interfere with the contract of insurance between USL and Hannover Life or with the terms upon which death and disablement cover would be offered by USL and Hannover Life to members of UniSuper. In the alternative, Hannover Life contends that the decision of the Tribunal to vary the total spine exclusion clause was unfair and unreasonable.

23 The precise questions of law raised by Hannover Life are:

1. By the Respondent's letter dated 27 October 2011, did a contract of insurance come into existence as between the Insurer and the Respondent that was subject to the Exclusion (“Contract”)?

2. Did the Superannuation Complaints Tribunal have the power to vary the terms of the Contract?

3. Was the decision of the Insurer to impose the Exclusion unfair and unreasonable?

4. Did the Superannuation Complaints Tribunal act outside its jurisdiction in its variation of the Exclusion?

24 The references to the Respondent in question 1 are references to Ms Wright.

25 The grounds relied upon by Hannover Life are:

1. In respect of the orders concerning the variation of the Contract, there was an error of law in that the Tribunal:

a. erred in finding that the Respondent’s acceptance of the offer only provided cover pending the outcome of the Respondent’s complaint;

b. erred in finding that the Respondent’s acceptance of the offer allowed the Tribunal to vary the decision of the Insurer in relation to the Exclusion;

c. did not take into account evidence before it that the Exclusion was a term of the Contract; and

d. acting [sic] outside its power by varying the terms of the Contract.

2. In respect of the finding that the Exclusion operated unfairly and unreasonably, there was an error of law in that the Tribunal:

a. erred by failing to find that the Exclusion operated fairly and reasonably;

b. erred in finding that an insurer acting fairly and reasonably, would consider a claim in the event that the First Respondent suffered an injury to her back that is unrelated and not connected to her muscle tightness and/or back soreness;

c. acted outside its power by finding that the Exclusion operated unfairly and unreasonably;

d. erred in finding that the Exclusion should be limited to events that are unrelated to the medical condition from which the First Respondent already suffers; and

e. acted outside its jurisdiction by amending the Exclusion.

26 Hannover Life seeks an order setting aside par 7 and par 57 of the Tribunal’s decision and, in lieu thereof, an order affirming the decisions of USL and Hannover Life to include the total spine exclusion clause in the terms and conditions of the cover provided to Ms Wright under UniSuper’s insurance arrangements in respect of death and disablement cover.

The Relevant Facts

27 As I mentioned at [5] above, on 19 July 2011, Ms Wright lodged a DDI Form with UniSuper dated that day. A blank version of that form was furnished to Ms Wright as part of the guide sent to her earlier in 2011.

28 In the introductory text on p 1 of that form, persons who were interested in applying for optional insurance cover were counselled to read the guide for detailed information on eligibility criteria and special conditions for optional death and disablement cover. On the same page of that form, a summary of the relevant eligibility criteria for that cover was set out. In addition, the form included a clear statement that the optional death and disablement cover being offered by UniSuper was provided by Hannover Life.

29 Prima facie, Ms Wright was eligible to take out optional death and disablement cover. On the form, Ms Wright specified that she wished to take out ten units overall of death and disablement cover at $1.40 per unit per week. As I have said, that request involved the purchase of nine additional units of cover.

30 USL and Hannover Life required an applicant for optional death and disablement cover to answer a number of questions set out on the DDI form concerning that person’s medical history. Ms Wright answered those questions. In doing so, she disclosed that she suffered from a number of medical conditions. In particular, she said that she suffered from occasional back pain the onset of which had commenced in 1998. She said that she had never lost time off work because of the back pain which she suffered from time to time. She stated that her back pain was managed with manipulative therapies and that she had consulted an osteopath for treatment in respect of her back pain.

31 Ms Wright signed the declaration required of her at the end of the form. One matter which she acknowledged by that declaration was that she understood that all optional insurance cover would be subject to the terms and conditions of the policy between USL and Hannover Life.

32 By letter dated 5 August 2011, USM requested Ms Wright to complete two further questionnaires. One was a financial questionnaire and the other a Back/Neck Disorder Questionnaire. In addition, she was required to undergo a medical examination in connection with which she completed a Standard Medical Exam Form.

33 In the Standard Medical Exam Form, Ms Wright disclosed that, from time to time, she suffered from back and shoulder pain which she treated with rest, stretching and OTC pain medicine. On that form, she said that she had fully recovered from such pain. In the Back/Neck Disorder Questionnaire, Ms Wright said that she suffered intermittently from pain in the back/neck, the onset of which had commenced in 2000 and was continuing. She said that the symptoms comprised muscle tightness which she treated with stretching, massage and manipulative therapies. She disclosed in that document that her last visit to the osteopath had occurred in July 2011. This was only a matter of weeks before she made her application for additional cover.

34 Based upon internal underwriting advice given in late August 2011 and formally confirmed on 8 November 2011, Hannover Life decided to offer additional death and disablement cover to Ms Wright upon the following terms:

(a) The additional cover offered was to be subject to Ms Wright’s acceptance of the total spine exclusion clause within 60 days of the new cover being offered; and

(b) Overall cover was to be reduced to six units (in lieu of the requested ten units) in view of the financial details provided by Ms Wright in the Financial Questionnaire completed by her.

35 In the formal internal notification of the underwriting advice, the author noted that the total spine exclusion wording was standard industry wording and that Hannover Life was unable to modify it.

36 By letter dated 31 August 2011 sent by USM to Ms Wright, USM said:

Your application for Death and Disablement Insurance

Member number: 13783872

Your application has been assessed and we are able to offer you this insurance with an exclusion/s.

To accept this offer, please sign the enclosed letter and return it to us in the envelope provided within the next 28 days [emphasis in original].

The attached exclusion, once accepted, will only apply to this application. Your existing Death and Disablement insurance cover of 1 units, will remain unchanged.

Please note that whilst your cover has been accepted with an exclusion/s, you have a duty under the Insurance Contracts Act 1984 to disclose to your insurer every matter that may be relevant to the acceptance of this insurance.

Your acceptance of this offer is required within the next 28 days. If we do not hear from you, we will assume you do not wish to proceed and this application for insurance will be cancelled. [emphasis in original]

If you have any questions please contact us to talk to one of our Claims Consultants on 1800 331 685.

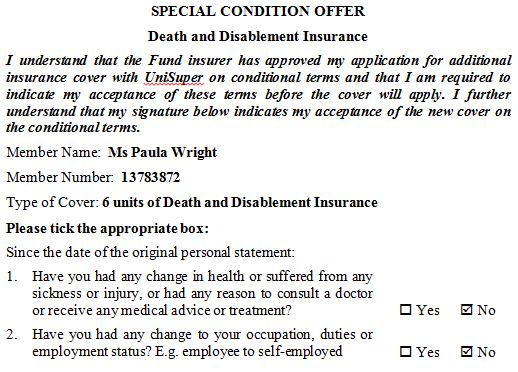

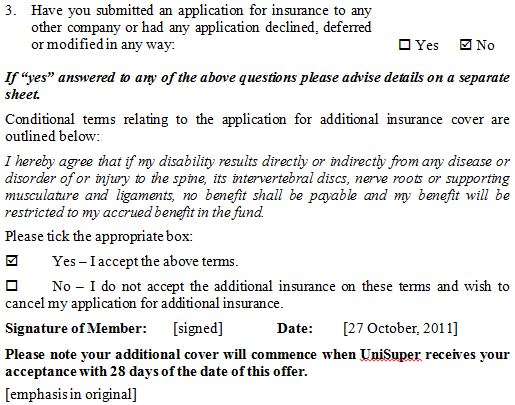

37 Enclosed with that letter was a formal document entitled Special Condition Offer.

38 By letter dated 7 September 2011 to USL, Ms Wright queried the fact that USL and Hannover Life had imposed the total spine exclusion as a condition of the offer made to her. In that letter, she said:

RE: SPECIAL CONDITION OFFER

PAULA WRIGHT Member number 13783872

Dear Sir or Madam,

I received your letter dated 31 August regarding my application for death and disablement insurance. I write to you to let you know I am considering the offer but may not accept within 28 days because of my concern with the special condition, and to ask you to resolve the issue with the special condition.

I am asked to accept that:

“if my disability results directly or indirectly from any disease or disorder of or injury to the spine, its intervertebral discs, nerve roots or supporting musculature and ligaments, no benefit shall be payable and my benefit will be restricted to my accrued benefit in the fund.”

I assume that this special condition is a response to my declaration that I suffer occasional back soreness (that is relieved with stretching and massage).

However, this special condition would seem to exclude every single muscle or spine injury which could conceivably occur. If I were to suffer paralysis because a meteor landed on my head, for example, I would not be covered. Any soreness I currently experience does not make me any more prone to accident and I do not accept that I am not entitled to coverage.

I accept that UniSuper should not cover a disability which is pre-existing, but there is no evidence there is an existing disability, and if there were, this clause goes much further than this. I ask that you give further and prompt consideration to my offer of insurance.

39 By letter dated 16 September 2011 to Ms Wright, USL informed Ms Wright that Hannover Life had reviewed the terms of the total spine exclusion. The author of the letter said that, since the exclusion wording was standard industry wording, the decision had been made that the exclusion would remain.

40 On 20 September 2011, Ms Wright lodged her formal complaint with the Tribunal.

41 On 27 September 2011, Ms Wright forwarded to the Tribunal a copy of:

(a) USM’s letter to her dated 31 August 2011;

(b) USM’s letter to her dated 16 September 2011; and

(c) The Special Condition Offer.

42 By letter dated 19 October 2011 from Ms Wright to USL, Ms Wright said:

RE: DEATH AND DISABLEMENT INSURANCE

PAULA WRIGHT Member number 13783872

Dear Sir or Madam,

On 16 September I received your letter declining to review the attachment of an exclusion to my policy and other matters. I disagree with this, and I have referred my concerns to the Superannuation Complaints Tribunal. I hoped to have this matter resolved quickly, but as of today my complaint has not been resolved by the Tribunal.

These concerns with the exclusion have delayed my acceptance but I would like you to provide cover while the matter is resolved. I accept the offer of insurance pending the resolution of my concerns. I understand that you would not provide cover for the excluded conditions pending the resolution of these issues.

43 By email sent by USM to Ms Wright on 26 October 2011, a further copy of the Special Condition Offer was forwarded to Ms Wright. In the covering email, the following was said:

If you would like to accept the cover and current exclusion, please sign the document and return as soon as you are able.

We understand you have pursued the exclusion with the Superannuation Complaints Tribunal/Ombudsman. If you require any assistance regarding this matter, or your account, please contact me directly on (03) 9910 6152. I would be happy to assist.

44 On 27 October 2011, Ms Wright signed and returned to USL the Special Condition Offer. The signed acceptance of that offer was received by USL on 2 November 2011. That document is in the following terms:

45 On 8 November 2011, Hannover Life approved Ms Wright’s application for additional death and disablement cover.

46 By letter dated 9 November 2011, USM informed Ms Wright that her application for six units of optional death and disablement insurance cover had been approved. In that letter, USM said:

However, a full spine exclusion will apply to 5 units of your Disablement cover.

As a result, you now have 6 units of Death and Disablement insurance cover in total.

Cost of Cover

The costs of the insurance cover are deducted from your account/accumulation component monthly in arrears based on the number of Fridays in the month.

Commencement of insurance cover

Death cover will commence on 26 August 2011.

Disablement cover will commence on 2 November 2011.

For the full terms and conditions which apply to UniSuper’s optional insurance cover, including eligibility criteria, please refer to the Optional insurance cover for members booklet, which is available on our website www.unisuper.com.au.

Details of the Death and Disablement insurance cover will appear on your next Benefit Statement.

Please note the exclusion only applies to the additional units of cover your [sic] have purchased.

If you have any queries, please call the UniSuper Helpline on 1800 331 685 or email your query to enquiry@unisuper.com.au.

47 After it was joined as a party to the review proceeding in the Tribunal in early 2012, by letter dated 9 February 2012, Hannover Life forwarded to the Tribunal a number of documents. Included within those documents was a document styled Underwriting Guidelines (ASCENT) relating to Back and Neck Disorders. Those guidelines provided that, if an applicant for total and permanent disablement cover had suffered mild back or neck pain within 12 months of the date of his or her application, the standard total spine exclusion clause should be included in the cover provided.

48 In that letter, Hannover Life explained its position in relation to the imposition of the total spine exclusion and the reduction of the level of cover sought by Ms Wright. In respect of the back exclusion, Hannover Life said the following:

1. Back exclusion. Based on the medical history that has been provided the underwriting guidelines clearly confirm that exclusion needs to apply to the TPD cover.

In brief, the documents obtained indicate that the member has had a back pain since 1998 (See Death and Disablement insurance application form signed 19 July 2011). The member’s latest episode or treatment was less that [sic] 12 month from the date of application. (See Back/Neck Disorder Questionnaire signed 14 August 2011). The member had treatment in July 2011 by Richard Todd (Osteopath). The member reports experiencing symptoms of pain in the back/neck and that these symptoms commenced in 2000 and are continuing.

The exclusion wording that has been applied is an industry standard.

49 By letter dated 27 February 2012, USL made a detailed submission to the Tribunal.

50 By letter dated 8 March 2013, Hannover Life made a further detailed submission to the Tribunal. In that submission, the author emphasised the fact that Ms Wright had accepted the conditions upon which the additional death and disablement cover was offered and was, for that reason, bound contractually by those conditions. In addition, the author emphasised that the total spine exclusion imposed on Ms Wright was in the form of standard industry wording.

51 USL then made further submissions to the Tribunal.

52 Ms Wright declined to lodge any submissions, being content to rest with the information originally supplied to the Tribunal in September 2011.

53 At the hearing before me, Hannover Life read and relied upon an affidavit affirmed by Roel Roozendaal on 10 March 2014. Mr Roozendaal was the underwriter employed by Hannover Life who assessed Ms Wright’s application for additional death and disablement cover and who advised that the total spine exclusion should be included as a term and condition of that cover.

54 At pars 13–26 of his affidavit, Mr Roozendaal described the actions which he took, as underwriter, in order to deal with Ms Wright’s application. He said that the processes which he adopted were standard practice in the underwriting department at Hannover Life in the period July–September 2011 and were based upon Hannover Life’s underwriting guidelines.

55 At pars 17–26 of his affidavit, Mr Roozendaal said:

17 Once Ms Wright returned the documents referred to above [referring to the questionnaire], I went into Hannover’s underwriting workflow system called MAZ and entered a summary of what she had disclosed. This information is then saved.

18 I then proceeded to the underwriting advice screen which requires me to elect whether the [sic] request further information, or whether to make a decision with respect to the coverage to be offered and on what terms.

19 I elected to make a decision in this case and as a result I was directed to the “application administration system”. This is a computer system that has a series of pop up boxes which require me to make a number of elections. The first election I was required to make was whether to:

(a) apply a limit (an exclusion); or

(b) or not apply a limit.

20 In this case, and in compliance with Hannover’s underwriting guidelines contained in a manual called “Ascent”, I elected to apply an exclusion to Ms Wright’s increased cover. At tab 46, page 254 of Appeal Book B is a copy of the relevant pages of Ascent relating to back and neck disorders.

21 I was then required to elect the type of exclusion. In this instance I elected the TPD exclusion.

22 I was then required to elect what body part the exclusion related to. I selected the “back” option.

23 I was then required to select what part of the back the exclusion would relate to. I selected the “spine” option.

24 At this point the Workflow/MAZ system generates the applicable exclusion that must be applied to the member’s increased cover. Annexed hereto and marked RR1 is a copy of a screen shot displaying the various exclusion wording options that must be selected if a member has disclosed a back disorder or ongoing symptoms in accordance with Hannover’s underwriting manual. Based upon my review of RR7 and my training, knowledge and experience I am able to say that the wording “...benefits shall not be payable for any disease or disorder of or injury to the spine, its intervertebral discs, nerve roots or supporting musculature and ligament” does not vary from exclusion to exclusion.

25 Given the unpredictability of back conditions, the exclusion wording is expressed in broad terms.

26 Based upon my qualifications, skills and experience as an underwriter at Hannover, I am able to say that:

(a) Hannover does not, and cannot customise exclusion wording for particular Members;

(b) Hannover uses is [sic] standardised and system generated and consistent with the wording used by the insurance industry in general; and

(c) if Hannover was able to customise the exclusion wording for individual members (which it is not) this would impact upon the pricing of the units of insurance coverage. If the exclusion was narrowed this would increase the risk to Hannover and therefore increase the cost of the insurance cover. The amount by which the Policy premium would be increased would require complex calculations and I cannot be precise as to the quantum of any increase without very substantial analytical work being undertaken.

UniSuper’s Relevant Insurance Arrangements

56 When Ms Wright joined UniSuper in 2007, she was provided with one unit of death and disablement cover.

57 In addition to that basic cover, USL entered into the policy so that it could provide additional optional insurance cover to its members, at their election.

58 From time to time, USL prepared and made available to its members versions of the guide. In early 2011, Ms Wright was given the 1 July 2010 version of the guide.

59 On the inside cover of that version of the guide, under the heading Important Information, the following was said:

The Trustee [referring to USL] can only pay an insured benefit once the Insurer [referring to Hannover Life] has accepted the claim, the insurance proceeds have been received from the Insurer and a condition of release has been met by the member. The Trustee does not guarantee payment of any insured benefit.

…

Full terms and conditions relating to the optional insurance cover are contained in the insurance policy documents. To the extent that this booklet contains any information about optional insurance cover which is inconsistent with the insurance policy documents, the insurance policy documents will prevail.

The terms and conditions regarding the provision of optional insurance cover are subject to change from time to time. Where required you will be notified of any changes.

60 On p 2 of the guide, the following appeared:

UniSuper provides optional Death and Disablement insurance (including cover for terminal illness) and optional Income Protection insurance cover to members who meet the eligibility criteria. The Trustee [referring to USL] has taken out group life policies with [Hannover Life] (the Insurer), to provide the optional insurance cover. All optional insurance cover is subject to the conditions set out in the insurance policy documents (you may request a copy of the policy documents free of charge by calling the UniSuper Help Line on 1800 331 685).

61 On p 4 of the guide, under the heading Overview of optional insurance cover, the following was said:

The provision of optional insurance cover and the payment of insured benefits are subject to the satisfaction of eligibility criteria, as set out in this booklet. The type, level and cost of cover available to you will depend on such factors as your membership category, your age, what cover you choose to purchase and, if your cover is subject to underwriting, your state of health.

62 On p 9 of the guide, under the heading How to purchase additional optional Death and Disablement cover, it was stated that a member will generally be eligible to take out such cover provided that (inter alia) the member provides health evidence to Hannover Life in the relevant application form and provides any additional information requested by Hannover Life (including medical and financial details). Under the same heading, the following text appeared:

The cover for any additional optional Death and Disablement insurance will start from the date your application is approved, or where applicable, from the date you have agreed to accept any offer of cover which is provided on the basis of an exclusion or premium loading.

63 There then followed an explanation of the fundamental features of fixed cover and unitised cover.

64 On p 14 of the guide, certain general exclusions and special conditions were described.

65 There then followed an explanation of the definition of disablement for the purpose of the relevant insurance arrangements.

66 At the back of the guide, there was a blank DDI Form and a blank Income Protection Application Form.

67 Under Reg 9 of the UniSuper Regulations made under the UniSuper Trust Deed, in order to be eligible to purchase death and disablement cover under Pt B of Div D of those Regulations, a member was obliged to satisfy the relevant requirements of the insurer (Hannover Life).

The Policy

68 Clause 9.1 of the policy provides that the policy is evidence of a contract of insurance between the Plan (the trustee of which is USL) and Hannover Life for the payment of benefits upon the terms and conditions set out in the policy.

69 Under cl 7.6 of the policy, Hannover Life promises to pay any benefit to USL or to the person to whom USL instructs it to pay the benefit.

70 The categories of benefit provided to USL under the policy are death, total and permanent disablement and terminal illness.

71 Item 7 of the schedule to the policy sets out the criteria for eligibility to be insured under the policy. There is no doubt that Ms Wright met those eligibility criteria.

72 At Item 11 of the schedule to the policy there is set out the way in which the agreed benefit to be paid under the policy is to be determined. Appendix 1 to the policy specifies the per unit of agreed benefit for unitised cover.

73 Clause 1.2 of the policy provides that Hannover Life is the insurer under the policy and that it provides group life insurance cover in relation to members of the group eligible for that cover. Clause 1.3 provides that the insurance cover provided under the policy is governed by the conditions in the policy. It also provides that all of Hannover Life’s obligations under the policy are subject to USL, and any person for whom cover is provided under the policy, abiding by all of the policy conditions which apply to them.

74 Clause 2 of the policy sets out the definitions of death, disablement and terminal illness as well as the definition of total and permanent disablement.

75 Clause 4.1 of the policy provides:

4.1 Eligibility

A person can only become covered under this policy if they are an Eligible Person. An Eligible Person is someone who:

(a) is a member or Deemed Member of the Plan; and

(b) is an Australian Resident; and

(c) meets the requirements that have been listed in Item 7 of the Schedule; or

(d) we have agreed in writing that we will insure under this policy.

76 Clause 4.2 deals with default cover.

77 Clause 4.4 and cl 4.5 of the policy provide:

4.4 Applying to Increase Cover or Joining When Not First Eligible

To obtain increased cover or cover when joining the Plan when not First Eligible, the Plan must provide us with any information about an Eligible Person, which we consider necessary for our underwriting purposes.

We may specify that this information must be given in a form of our choosing.

We may, after considering any information that we have received in relation to the Eligible Person in our absolute discretion, either:

(a) request further information; or

(b) accept the Eligible Person for cover under this policy, or

(c) refuse to cover the Eligible Person under this policy for the portion of cover being underwritten; or

(d) offer to accept the Eligible Person subject to such terms as we consider appropriate including premium loadings, restrictions or exclusions.

Should an Insured Person elect to increase their existing Agreed Benefit or should an Eligible Person join the Plan when not First Eligible, their cover will be subject to a Personal Statement & Declaration of Health being completed in the first instance.

We reserve the right to ask for additional information based on the contents of their Personal Statement & Declaration of Health.

All Personal Statement & Declaration of Health forms must be received by the Plan for assessment within 31 days of being signed by the Insured Person. Where this requirement is not met an Eligible Person will be asked to complete a new Personal Statement & Declaration of Health before their application will be considered.

Cover will commence on the date that we notify the Plan, in writing, that we have agreed to accept cover or the date that the Plan has agreed to accept cover on our behalf under the terms agreed between the Plan and us from time to time.

4.5 Limitations to Cover

Unless agreed otherwise, the maximum Agreed Benefit that an Insured Person may have under The Policy is determined by reference to Item 12 of the Schedule.

An Insured Person may elect different amounts of death and Total and Permanent Disablement cover, however their Agreed Benefit for Total and Permanent Disablement cover cannot exceed their Agreed Benefit for death cover.

78 Clause 9.3 of the policy provides:

9.3 What Documents Make up this Policy?

The documents that constitute this policy are:

(a) the document in which the Proposer applied for this policy;

(b) this printed document including the Schedule;

(c) all documents which record an authorised variation of this policy;

(d) any statement relevant to their cover under this policy completed by or on behalf of any Insured Person;

(e) all documents that set out a condition, restriction or increase in premium that applies to an Insured Person.

79 That clause appears under a general heading: The Policy.

The Decision of the Tribunal

80 After dealing with procedural matters, the substance of Ms Wright’s complaint, the factual background to the complaint, the terms of the Trust Deed and Regulations governing UniSuper and the terms of the relevant policy, the Tribunal turned its attention to the submissions made on behalf of each of the parties.

81 The Tribunal recorded that Ms Wright had argued that the imposition of the total spine exclusion clause into the terms of death and disablement cover offered to her was an “over reaction” to her disclosure that she suffered from mild back pain.

82 The Tribunal then noted (at [27]–[29] of its Decision) that USL had submitted that it acted in accordance with the Trust Deed and policy and that any loadings, exclusions or reductions applied by Hannover Life were not matters over which USL had any discretion. For these reasons, USL submitted that it had acted fairly and reasonably with respect to the arrangement of additional cover for Ms Wright.

83 At [30]–[36], the Tribunal recorded the submissions made on behalf of Hannover Life.

84 At [35], the Tribunal noted that Hannover Life relied upon the circumstance that Ms Wright had signed an acceptance of the exclusion and of her reduced cover and relied upon that fact as a matter of contract law. It was said that the Tribunal ought to uphold the contract thereby constituted. Hannover Life went on to state that the only alternative to upholding that contract was to void all cover over the automatic acceptance limit (one unit). Hannover Life also submitted that the inclusion of the total spine exclusion in Ms Wright’s cover was within its own underwriting guidelines. For this reason, it claimed that it had not acted unreasonably.

85 At [37]–[53], the Tribunal explained its reasons for the decision to which it ultimately came.

86 At [37], the Tribunal said:

The Tribunal’s role is to determine whether the decisions of the Insurer and the Trustee to reduce the level of cover offered to the Complainant and impose an exclusion in relation to any injuries to her spine were fair and reasonable in their operation in relation to the Complainant in the circumstances. The issue is not what decision the Tribunal would have made on the evidence before it. In reaching its determination, the Tribunal took the whole of the evidence and submissions into account.

87 At [42], the Tribunal also said:

The Trustee

It is convenient to first deal with the decisions of the Trustee. The Tribunal agrees with the Trustee that the effect of Regulation 9 of the Trust Deed is that a member must satisfy the requirements of the Insurer in relation to the purchase of death and disablement cover and the Trustee has no capacity to provide cover on different terms. The Trustee has acted in accordance with the Trust Deed and the Tribunal can find no unfairness or unreasonableness in the Trustee’s decisions in relation to this complaint.

88 At [43], the Tribunal accepted that it had been reasonable for Hannover Life to reduce the level of cover given Ms Wright’s financial circumstances.

89 At [44]–[53], the Tribunal then addressed the question of whether the imposition of the total spine exclusion clause was fair and reasonable in all the circumstances.

90 At [44]–[53], the Tribunal said:

44 The second issue for consideration by the Tribunal is the exclusion imposed by the Insurer in relation to any disease or disorder of or injury to the spine, its intervertebral discs, nerve roots or supporting musculature and ligaments, whether incurred directly or indirectly.

45 In the Tribunal’s view, it was fair and reasonable in the circumstances for the Insurer to impose an exclusion in accordance with its underwriting guidelines in relation to the Complainant’s pre-existing condition. The guidelines indicate an exclusion rather than a loading and in the Tribunal’s view, the Insurer has followed its procedures and it was fair and reasonable for the Insurer to follow these guidelines.

46 However, in the Tribunal’s view, the effect of the exclusion as drafted could be as described by the Complainant, i.e. she could be involved in an event and suffer injuries to her back which are unrelated to her current back conditions, and she would be excluded from receiving a benefit. The view of the Tribunal is that the exclusion should be limited to events that are related to the medical condition from which the Complainant already suffers, and further, that it should not apply to the 1 unit of cover already held by the Complainant without restriction, as at the date of application for additional cover.

47 The Insurer submitted that it has used standard wording in relation to the exclusion, however, the use of the standard wording is not of itself a sufficient reason to render the Insurer’s decision fair and reasonable in the circumstances.

48 In the Tribunal’s view, an insurer, acting fairly and reasonably, would consider a claim in the event that the Complainant suffers an injury to her back that is unrelated and not connected to her muscle tightness and/or back soreness.

49 The Tribunal is of the view that it is unlikely that the Insurer would be attempting to exclude cover for events unrelated to the Complainant’s muscle tightness in her back and/or back soreness. Accordingly, the Tribunal is of the view that it is fair and reasonable to vary the Insurer’s decision to state that the exclusion does not apply in this event.

50 For the avoidance of doubt, the Tribunal is also of the view that it is clear that the Complainant signed the Special Condition Offer to secure additional cover pending the outcome of her complaint, and that her signing the offer does not mean that she is no longer seeking a decision from the Tribunal in relation to her complaint.

51 She has not withdrawn her complaint and has sought a determination from the Tribunal in relation to both the amount of cover approved, and the imposition of the full back exclusion.

52 Further, in the Tribunal’s opinion, the Complainant signing the offer does not prevent the Tribunal varying the decision of the Insurer in relation to the exclusion.

53 For the reasons set out above, the Tribunal considers that the decision of the Insurer to impose an exclusion in relation to the Complainant’s back condition, to the extent that it excludes cover in the event that the Complainant suffers an injury or illness to her back that is unrelated to her pre-existing muscle tightness and/or back soreness, operates unfairly and unreasonably in relation to the Complainant in the circumstances.

91 The Tribunal then made the determination which I have summarised at [13] above.

Consideration

92 As I have already mentioned, Ms Wright did not participate at all in this proceeding. She took no action whatsoever to oppose the making of the orders claimed by Hannover Life. USL adopted a position of neutrality, although it did provide a Written Submission to the Court by which it sought to defend the decisions which it took in relation to Ms Wright’s application for additional cover.

93 Hannover Life filed two sets of Written Submissions and made available Senior Counsel’s speaking notes (MFI-1).

94 Effectively, the orders sought by Hannover Life were not opposed by any interested party.

95 In those circumstances, I do not intend to recount in detail the submissions made on behalf of Hannover Life. I propose to grant the relief sought by it. I will shortly state my reasons for doing so. To a large extent those reasons are based upon or influenced by submissions made on behalf of Hannover Life.

96 The Tribunal held that USL had acted in accordance with the Trust Deed with the consequence that its decision to impose the total spine exclusion as a condition of Ms Wright’s cover was not unfair or unreasonable (par 42 of the Tribunal’s Decision).

97 In addition, the Tribunal considered the fairness and reasonableness of the terms of the total spine exclusion when looking at the position of Hannover Life. Essentially, the Tribunal took the view that the scope of the exclusion went much further than was reasonably necessary.

98 The Tribunal did not consider whether s 37(5) of the Complaints Act prevented it from approaching the matter in the way that it did.

99 Section 37 of the Complaints Act provides:

37 Tribunal powers—complaints under section 14

(1) For the purpose of reviewing a decision of the trustee of a fund that is the subject of a complaint under section 14:

(a) the Tribunal has all the powers, obligations and discretions that are conferred on the trustee; and

(b) subject to subsection (6), must make a determination in accordance with subsection (3).

(2) If an insurer or other decision maker has been joined as a party to a complaint under section 14:

(a) the Tribunal must, when reviewing the trustee’s decision, also review any decision of the insurer or other decision maker that is relevant to the complaint; and

(b) for that purpose, has all the powers, obligations and discretions that are conferred on the insurer or other decision maker; and

(c) subject to subsection (6), must make a determination in accordance with subsection (3).

(3) On reviewing the decision of a trustee, insurer or other decision maker that is the subject of, or relevant to, a complaint under section 14, the Tribunal must make a determination in writing:

(a) affirming the decision; or

(b) remitting the matter to which the decision relates to the trustee, insurer or other decision maker for reconsideration in accordance with the directions of the Tribunal; or

(c) varying the decision; or

(d) setting aside the decision and substituting a decision for the decision so set aside.

(4) The Tribunal may only exercise its determination making power under subsection (3) for the purpose of placing the complainant as nearly as practicable in such a position that the unfairness, unreasonableness, or both, that the Tribunal has determined to exist in relation to the trustee’s decision that is the subject of the complaint no longer exists.

(5) The Tribunal must not do anything under subsection (3) that would be contrary to law, to the governing rules of the fund concerned and, if a contract of insurance between an insurer and trustee is involved, to the terms of the contract.

(6) The Tribunal must affirm a decision referred to under subsection (3) if it is satisfied that the decision, in its operation in relation to:

(a) the complainant; and

(b) so far as concerns a complaint regarding the payment of a death benefit—any person (other than the complainant, a trustee, insurer or decision maker) who:

(i) has become a party to the complaint; and

(ii) has an interest in the death benefit or claims to be, or to be entitled to benefits through, a person having an interest in the death benefit;

was fair and reasonable in the circumstances.

100 The decisions about which Ms Wright complained to the Tribunal were the decision by USL to include in the additional death and disablement cover offered to Ms Wright a total spine exclusion clause and the decision to reduce the level of cover which she sought from nine additional units to five additional units. Both of those decisions were decisions made by USL, not by Hannover Life although, of course, they necessarily followed Hannover Life’s underwriting decisions.

101 In those circumstances, Ms Wright’s complaint, properly understood, was a complaint made under s 14 of the Complaints Act. Her complaint was made within time as required by s 14(3) and s 14(4). Section 14(2) provides that a person may make a complaint (other than an excluded complaint) to the Tribunal that the decision is or was unfair or unreasonable.

102 Ms Wright may also have been entitled to complain about Hannover Life’s corresponding decisions under s 15J of the Complaints Act. However, she did not make a direct complaint about Hannover Life’s decisions. Because Hannover Life was joined as a party to the review proceeding initiated by Ms Wright’s complaint, nothing turns on the fact that her complaint was made about decisions of USL rather than decisions of Hannover Life.

103 Hannover Life placed considerable emphasis upon s 37(5) of the Complaints Act. It submitted that the variation to the total spine exclusion clause which the Tribunal ordered in the present case was contrary to law, contrary to the governing rules of UniSuper and contrary to the terms of the policy.

104 It relied upon two decisions of single Judges of this Court: Retail Employees Superannuation Pty Ltd v Crocker (2001) 48 ATR 359 (Crocker), a decision of Allsop J (as his Honour then was); and Colonial Mutual Life Assurance Society Limited v Brayley [2002] FCA 1333 (Brayley), a decision of Branson J and observations made by Kirby J in Attorney-General v Breckler (1999) 197 CLR 83 (Breckler).

105 At 363 [15]–[16] in Crocker, Allsop J said:

15 In the context of a trustee acting as the trustee of a superannuation fund pursuant to a trust deed and an insurer issuing a policy to the trustee on behalf of the members of a fund, allegations of the kind just mentioned might throw up for consideration a number of matters if one were concerned with analysing or determining all the legal rights and obligations of the three parties (member, trustee and insurer) inter se: questions as to whether the member was entitled under the terms of the trust or the terms of the insurance policy to disability cover; questions as to whether, irrespective of the terms of the policy, the trustee had bound itself in some fashion to the member to provide disability cover; questions as to whether any such obligation had been created in contract, by estoppel or in some other legal or equitable framework; and questions as to whether, if the trustee had so bound itself and was not entitled to have the insurer pay the claim, it was entitled to indemnify itself out of the trust fund to meet such obligation.

16 However, the Tribunal’s task was not to determine all such rights and obligations of the parties. To do so would, in all likelihood, see it purport to engage in the exercise of judicial power. Rather, the Tribunal’s task was confined to the role given to it by the Superannuation (Resolution of Complaints) Act 1993 (Cth). At this point I gratefully adopt the description of the legislative scheme set out by the Full Court in National Mutual Life Association of Australia Limited v Campbell (2000) 99 FCR 562 at 565-68 [10] to [20]. This relieves me of refering to the Superannuation (Resolution of Complaints) Act 1993 (Cth), other than to the provisions essential to these reasons.

106 His Honour then described the functions of the Tribunal by reference to s 12 and s 14 of the Complaints Act and then set out s 37. At 364–367 [21]–[32], his Honour said:

21 The central task of the Tribunal was to review the decision of the Trustee and, since the Insurer had been joined under s 17A and s 18, to review any decision of the Insurer: para 37(2)(a). In carrying out this task the Tribunal had all the powers, obligations and discretions conferred on the Trustee and the Insurer: paras 37(1)(a) and 37(2)(b). In carrying out this task the Tribunal was required to make a determination in accordance with subs 37(3). The Tribunal’s task was to decide for itself whether the Trustee’s decision and any decision of the Insurer was and is unfair or unreasonable. This flows from, first, the nature of the subject matter of review – a complaint under subs 14(2) as to the unfairness or unreasonableness of the Trustee’s decision, secondly, the exhaustive universe of possible determinations in subs 37(3), thirdly, the nature of the limitations on the exercise of the powers in subs 37(3) set out in subs 37(4) and, fourthly, the requirement under subs 37(6) to affirm the decision under subs 37(3) if the Tribunal is satisfied that the decision in its operation in relation to the complainant was fair and reasonable in the circumstances.

22 While the determination of the Tribunal was required to be predicated upon its view as to whether the relevant decision was unfair or unreasonable, the Tribunal was enjoined by subs 37(5) from doing anything under subs 37(3) that would be contrary to law, or to the governing rules of the fund or to the terms of the relevant insurance policy, here the Prudential policy.

23 The phrase “governing rules of the fund” means the terms governing the conduct of the superannuation fund, which was a regulated superannuation fund under the Superannuation Industry (Supervision) Act 1993 (Cth) (the SIS Act). It is not limited to the schedule to the trust deed which set out the “rules for the management” of the fund. It means the terms of the trust under which the fund is carried on, which includes the “rules for the management” of the fund: cl 1.2 of the annexure to the deed of amendment dated 13 December 1988.

24 In short, the task of the Tribunal was to review the decisions of the Trustee and Insurer as to whether they were (or either was) unfair or unreasonable and to make a determination under subs 37(3) in the light of that consideration. This task was one to be undertaken, to use the language of Merkel J in Briffa v Hay (1997) 75 FCR 428 at 443-4 and Seafarers’ Retirement Fund Pty Ltd v Oppenhuis (1999) 94 FCR 594 at 598-99 [19] to [23], “in the shoes of” the Trustee and the Insurer: see also paras 37(1)(a) and 37(2)(b). The directions for reconsideration of the decision (under para 37(3)(b)) or the variation of the decision (under para 37(3)(c)) or the substituted decision (under para 37(3)(c)) either affect or become the original decision of the Trustee and the Insurer. Thus the strictures of subs 37(5) can be seen not only to prevent, at the point of remedy, something unlawful being ordered to be done, but as an essential reflection of the task being undertaken: a consideration of a decision of the Trustee, qua trustee, that is of the Trustee acting in accordance with law and the terms of its governing trust and making a determination, as if the Tribunal were the Trustee, to affect, vary or substitute a decision. The same applies to the task in relation to the Insurer and its decision.

25 It is important to appreciate what I have just said, because in my view it affects the meaning of “unfair or unreasonable”. The words “fair” and “reasonable” have been discussed in this Court by Nicholson J in Pope v Lawler (1996) 41 ALD 127 at 135 where his Honour had recourse to the New Shorter Oxford Dictionary (4th Ed) 1993 in ascribing, for the purposes of s 14 and s 37 of the Superannuation Industry (Supervision) Act 1993 (Cth), to the word “fair” the meaning “just, unbiased, equitable, impartial” and to the word “reasonable” the meaning “within the limits of reason; not greatly less or more than might be thought likely or appropriate”; by Sundberg J in National Mutual Life Association v Jevtovic (unreported, Federal Court, Sundberg J, No VG656 of 1996) at pp 9-10; and by Merkel J in Briffa v Hay, supra at 436 and in Collins v AMP Superannuation (1997) 75 FCR 565 at 578 (referring, without disapproval, to Pope and Jevtovic).

26 While I do not disagree with these expressions of view as to the meaning of these words, it must be the case (and I do not read anything said by their Honours to be to the contrary) that the words must take their meaning from the place and context which they occupy in the statute. Further, I note the comments of the Full Court in National Mutual v Campbell, supra at 571, concerning the dangers of paraphrasing, even through the use of a dictionary.

27 The task of the Tribunal and the meaning of the phrase “unfair or unreasonable” are inextricably intertwined and both are governed by the Superannuation Industry (Supervision) Act 1993 (Cth), and, especially, by s 37. It is the decision of the Trustee, recognising its obligation to act in conformity with the governing rules of the fund, and the decision of the Insurer, recognising its obligation (and entitlement) to act in conformity with the terms of the relevant policy, which must be reviewed for unfairness or unreasonableness. The unfairness or unreasonableness must be of the decision (as expanded by s 4) under, and in conformity with, the governing rules or the terms of the policy. It is not some other perceived (rightly or wrongly) unfairness or unreasonableness in and about the conduct of the fund.

28 The question as to whether a decision was unfair or unreasonable cannot be judged otherwise than by having regard to the conformity of the decision with the governing rules of the fund and the terms of the policy. The conformity of the decision with those matters is therefore a relevant consideration in the sense discussed in Minister for Aboriginal Affairs v Peko-Wallsend (1986) 162 CLR 24 at 39-40 and see Telstra Corporation Ltd v Seven Cable Television Pty Ltd (2000) 102 FCR 517 (special leave refused on 20 August 2001). If conformity with the governing rules or the terms of the policy required the very decision, which was made, to be made, the strictures of subs 37(5), the universe of possible conduct under subs 37(3) and the balance of the Superannuation Industry (Supervision) Act 1993 (Cth), including subs 37(6), would require a conclusion of the Tribunal that the decision was not unfair or unreasonable. It could not be otherwise, as it would, on this hypothesis, be the only decision capable of being reached by the Trustee or the Insurer in the light of the governing rules or terms of the policy; or, put another way, any determination under paras 37(3)(b),(c) or (d) would involve the Tribunal doing an act contrary to the governing rules or the terms of the policy.

29 It may be that a decision of a trustee or an insurer is in conformity with, but not required by, the governing rules of the fund or the terms of the policy. This may be because the decision could be described as one of a discretionary character: see s 14AA of the Superannuation Industry (Supervision) Act 1993 (Cth) and Merkel J in Collins v AMP, supra at 578-79. For myself, I would prefer not to use any dichotomy between discretionary and non-discretionary decisions as a tool in this analysis. I do not think that the presence of s 14AA mandates it. The presence of s 14AA is to be understood for reasons other than any which make the terminology used within it a compulsory tool for analysis of the understanding by the Tribunal of its task: see National Mutual v Campbell, supra at 568-70 [21] to [30] and Seafarers’ Retirement Fund v Oppenhuis, supra at 596-98. It may be that the decision of a trustee or an insurer is in conformity with, but not required by, the governing rules or policy terms not because there was involved any exercise of discretion, properly so-called, but because the decision was one which so involves elements of fact, degree, opinion or value judgment that different minds can legitimately differ in reaching a decision or because one aspect of the rules or policy terms, but not another, has been the foundation of the decision. A decision of a trustee or an insurer about a matter of judgment, for instance one involving weighing competing expert or lay opinion about a state of affairs, might be lawful and in conformity with the governing rules and policy terms. It might be described as “correct” in that it was the product of an inquiry directed to the right question and in that there was material available to support it. In this, perhaps limited, sense the decision was correct and was open to be made. However, the Tribunal is not engaged in a form of judicial review. It reviews the decision (as expanded by s4) complained of from the position of the trustee or insurer (paras 37(1)(a) and 37(2)(b)). The Tribunal may find, in its opinion, in some degree (see subs 37(4)), the decision to be unfair or unreasonable and may act under subs 37(3) to give effect to its view of the merits as long as subs 37(5) is not infringed. It seems to me that this analysis accords with the approach described by the Full Court in National Mutual v Campbell, supra at 570-71 [32] and [33] and see also Kirby J in Attorney-General v Breckler (1999) 197 CLR 83 at 129 [88]. It seems to me that the very use of the words “unfair” and “unreasonable” in their breadth, individually and in the composite phrase “unfair or unreasonable”, supports this view: see, in other contexts, George Mitchell (Chesterhall) Ltd v Finney Lock Seeds Ltd [1983] 2 AC 803 at 815-16, and Samuels JA in Antonovic v Volker (1986) 7 NSWLR 150 at 154-55.

30 It may be that what I have said does not differ in substance from the views of Merkel J in Collins v AMP at 578 and Sundberg J in Wilkinson v Clerical Administrative and Related Employees Superannuation Pty Ltd (1997) 77 FCR 469 at 491 about “non-discretionary” decisions if they are “correct” or if they “conform to” or are “made in accordance with” the governing rules of the fund or terms of the policy. In many cases, for non-discretionary questions, the governing rules or policy terms will only yield a single result.

31 The Tribunal’s task is not to engage in ascertaining generally the rights of the parties, nor is it to engage in some form of judicial review of the decision of the trustee or insurer. Rather it is to form a view, from the perspective of the trustee or insurer, as to whether the decision of either was (recognising the overriding framework given by the governing rules and policy terms, respectively) unfair or unreasonable.

32 Thus, essential to the task before the Tribunal, as a consideration mandated by the terms of s 37, is an inquiry as to whether the decision by the trustee or insurer was in conformity with the governing rules or the terms of the policy. If the Tribunal finds that the decision is contrary to the governing rules or the terms of the policy it may well be an easy step to conclude that it is unfair or unreasonable. I do not need to decide whether a finding by the Tribunal that the trustee’s or insurer’s decision was contrary to the governing rules or policy terms required a finding of unfairness or unreasonableness: cf Merkel J in Collins v AMP at 578–79 and Sundberg J in Wilkinson, supra at 492. If the Tribunal finds that the decision of the trustee or the insurer is in conformity, with and required, by the governing rules or policy terms, in the sense which I have discussed above, it cannot other than find or be satisfied that the decision is fair and reasonable. If the Tribunal finds that the decision of the trustee or the insurer is in conformity with, but not required by, the governing rules on policy terms, in the sense which I have discussed above, it may proceed, in effect, to supplant the decision of the trustee or insurer with its view of the merits, bearing in mind the limitations of subs 37(4) and 37(5).

107 In Crocker, Allsop J held that the Tribunal was not entitled to make a determination reflecting its view of the rights of the parties inter se, if that determination was contrary to the terms of the governing rules or policy terms.

108 In Brayley at [28]–[34], Branson J said:

28 The Tribunal is expressly empowered by s 14AA(1) of the Act to review a decision concerning which a complaint is made under s 14 of the Act whether or not the decision involved the exercise of a discretion (see [16] above). The Act does not define the expression ‘the exercise of a discretion’. In some contexts the exercise of a discretion may be distinguished from the making of a judgment (see, for example, National Mutual Life Association of Australia Ltd v Campbell [2000] FCA 852; 99 FCR 562 at [30]-[31]; Employment Advocate v Williamson [2001] FCA 1164; 111 FCR 20 per Branson J at [78]; J Edelman, ‘Judicial Discretion in Australia’, Australian Bar Review, vol. 19, no. 3, June 2001, p. 285). However, it seems relatively plain that in the context of s 14AA of the Act the reference to a decision which did not involve ‘the exercise of a discretion’ is intended to be a reference to a decision where the law, the rules of the relevant fund or the terms of any relevant contract of insurance mandated a particular result (see Attorney General v Breckler, per Kirby J at [88]). That is, that s 14AA(1) is intended to make it clear that a complaint may be made under Part 4 of the Act that a decision is or was unfair or unreasonable even where the decision was one which did not call for a judgment to be made as to fairness or reasonableness or otherwise.

29 I note incidentally that it is likely that the expression ‘contrary to law’ is intended to bear a wider meaning in s 14AA(2) than the same expression bears in s 37(5) of the Act. In s 37(5) ‘contrary to law’ is used in contradistinction to contrary to the governing rules of the fund concerned and contrary to the terms of a contract of insurance. In the context of s 37(5) it would appear that “contrary to law” is intended to mean contrary to the general law. However, the expression ‘contrary to law’ when used in s 14AA(2), which was only inserted into the Act by s 8 of the Superannuation Legislation Amendment (Resolution of Complaints) Act 1998 (Cth), seems intended to have a broader meaning so as to encompass not only contrary to the general law but also contrary to the governing rules of the fund concerned and contrary to the terms of a contract of insurance. It appears plain that s 14AA(1) was enacted to make it clear that the Tribunal’s jurisdiction was not confined to reviewing the exercise of discretionary powers on the part of a trustee (see Wilkinson v Clerical Administrative and Related Employees Superannuation Pty Ltd [1998] FCA 51; 79 FCR 469). Section 14AA(2) is concerned with how the Tribunal should deal with a complaint concerning a decision that did not involve the exercise of a discretion. The subsection will have a narrow field of operation, and thus leave the Tribunal without guidance to a significant degree, unless the subsection reaches not only to non discretionary decisions that are contrary to the general law but also to non discretionary decisions that are contrary to the governing rules of the fund concerned or contrary to the terms of a contract of insurance.

30 Where the Tribunal reviews a decision that did not involve the exercise of a discretion within the meaning of s 14AA its options are limited. If it forms the view that the decision was contrary to law (see [29]), it must proceed on the basis that the decision was unfair and unreasonable (s 14AA(2)). As the Tribunal may not itself make a determination on a complaint under s 14 of the Act that would be contrary to law (s 37(5)), the determination of the Tribunal under s 37(3) will in a case of this kind of necessity reflect the Tribunal’s view of the decision that was required by the law. If the Tribunal forms the view that the decision was not contrary law, for the same reason the Tribunal will be obliged to affirm the decision.

31 Where the Tribunal reviews a decision that did involve the exercise of a discretion within the meaning of s 14AA, the appropriate course, in my view, is for it to consider first whether the actual decision, as opposed to the process by which the decision was reached, was fair and reasonable in the circumstances (National Mutual Life Association of Australia Ltd v Jevtovic, unreported, Sundberg J, 8 May 1997). The words “unfair” and “unreasonable” are used in the Act as words of broad content so that difficulty attends any attempt to define them precisely (National Mutual Life Association of Australia Ltd v Campbell at [36]). If the Tribunal forms the view that the decision was fair and reasonable in the circumstances it must affirm the decision (s 37(6)). It must do so even though the Tribunal might not itself have made the same decision (National Mutual Life Association of Australia Limited v Scollary [2002] FCA 695 at [37]).

32 If the Tribunal is not satisfied that the decision was fair and reasonable in the circumstances, ss 37(1) and (2) require the Tribunal put itself in the position of the trustee and, in an appropriate case, the insurer and other relevant decision maker (National Mutual Life Association of Australia Ltd v Campbell at [32]; Briffa v Hay (1997) 75 FCR 428 at 443–445). From that position or positions the Tribunal must determine whether, consistently with:

(a) the general law;

(b) the governing rules of the fund concerned; and

(c) if a contract of insurance between the insurer and a trustee is involved, the terms of the contract,

the unfairness or unreasonableness that the Tribunal has identified in respect of the trustee’s decision can be addressed in whole or in part.

33 If the Tribunal concludes that it cannot address, in whole or in part, the unfairness or unreasonableness identified by it without acting in a manner that is contrary to the general law, the governing rules of the fund concerned or the terms of a relevant contract of insurance between an insurer and the trustee, the Tribunal is required to leave the perceived unfairness or unreasonableness unaddressed (s 37(5)). If the Tribunal concludes that the unfairness or unreasonableness identified by it can be addressed consistently with the general law, the governing rules of the fund concerned and the terms of any relevant contract of insurance between an insurer and the trustee, it must exercise its determination-making power for the purpose of placing the complainant as near as practicable in such a position that the unfairness or unreasonableness, or both, that the Tribunal has identified no longer exists (s 37(4)).

34 The above analysis reveals that although all complaints made to the Tribunal under s 14 of the Act are, in a formal sense, complaints that a decision is unfair or unreasonable (s 14(2)), the Tribunal is not empowered to remedy all unfairness or unreasonableness that it may perceive. In particular, the Tribunal lacks power to remedy any perceived unfairness or unreasonableness that is a necessary consequence of the application in the particular case of the governing rules of the fund concerned or the terms of a contract of insurance between an insurer and the trustee.

109 Branson J adhered to the views which she had expressed in Brayley in a subsequent case: Employers First v Tolhurst Capital Ltd (2005) 143 FCR 356 at [77]–[84].

110 These views are consistent with the views of Kirby J in Breckler (at 128–129 [87]–[88]) where his Honour said:

87 Nature of the Tribunal’s functions: As the reasons of the judges of the Full Court demonstrate (Compare Briffa v Hay (1997) 75 FCR 428 with the views of all of the judges on this point in Wilkinson (1998) 79 FCR 469), there are strong arguments for both sides as to the reconciliation of ss 14 and 37 of the Complaints Act. In the end, it may not help much, for constitutional purposes, to classify some of the Trustees’ decisions as “discretionary” and others as “non-discretionary”, as the judges of the Full Court did. A safer course is to recognise that, in terms, s 14(2) of the Complaints Act is not restricted to a “decision” of a particular character whether described as “discretionary” or otherwise. The subsection affords a person the entitlement to make a complaint to the Tribunal about any decision of a trustee. But then, by s 37, the Tribunal is restricted in the response which it may give to such a complaint. Specifically, it must not do anything “that would be contrary to law, to the governing rules of the fund concerned” and, if relevant, to the terms of a contract of insurance. In effect, these restrictions require the Tribunal to form a view (necessarily not conclusive) about the requirements of the applicable law, including the meaning of the rules of the fund and of any relevant contract of insurance. But it is not unusual for statutory tribunals to be obliged, in the performance of their functions, to make findings of fact and to apply rules of law (cf Re Boulton; Ex parte Construction, Forestry, Mining and Engineering Union (1998) 73 ALJR 129). Doing so involves no inherent invasion of the judicial power. It amounts to nothing more than the tribunal’s complying, like every other individual and legal entity, with the law of the land.

88 Where an applicable legal rule imposes a duty on a trustee, or confers a right or privilege on a beneficiary, compliance with s 37(5) of the Complaints Act obliges the Tribunal to give effect to its understanding of that law. This is not because it deems a decision in accordance with the applicable law to be “fair” or “reasonable” as the Attorney-General suggested. Nor is it because the decision, which is otherwise within the trustee’s jurisdiction, is somehow placed outside that jurisdiction by the limited powers which the Tribunal enjoys to disturb the decision. It is simply because, although the decision is reviewed pursuant to the complaint, the Tribunal is forbidden to do anything that would be contrary to law, to the governing rules of the fund concerned and to any contract of insurance that is relevant. Obviously, the occasions for the intervention of the Tribunal on the grounds of “unfairness, unreasonableness, or both” (Complaints Act, s 37(4)) may, as a practical matter, be confined to cases where the law, the rules of a fund or the terms of the contract of insurance do not yield a single result. The “unfairness” or “unreasonableness” which the Tribunal may address will thus arise where the exercise by a trustee of its powers involves an element of discretion, opinion or judgment. That alone will enliven the “determination-making power” of the Tribunal in a way that can be effective. The restriction of the grounds of complaint to present or past unfairness or unreasonableness matches the restrictions in s 37(4) and (6) of the Complaints Act on the Tribunal’s powers to interfere with a decision of a trustee.

111 I propose to apply the reasoning of Kirby J, Branson J and Allsop J to which I have referred.

112 In the present case, Reg 9 of the UniSuper Regulations obliged a member who wished to be eligible to purchase additional death and disablement cover to satisfy the relevant requirements of Hannover Life.

113 The insurance cover provided under the policy is governed by the conditions in the policy (cl 1.3). Cover is subject to USL, and any person for whom cover is provided under the policy, abiding by all of the policy conditions which apply to them (cl 1.3).

114 Under cl 4.1 of the policy, cover is only put into place when Hannover Life has agreed in writing that it will insure the particular member under the policy.